excellence in leadership - july 2013

DESCRIPTION

ÂTRANSCRIPT

Issue 2 | 2013 | £12

THE

Humphrey Singer, group finance director at Dixons Retail, on introducing

a brand-new business model

Trevor Dighton, former CFO at G4S, on implementing a crisis management plan

Sir Charlie Mayfield, chairman of the John Lewis Partnership, on the success of

the employee-ownership model

Jacek Levernes, VP of Hewlett-Packard’s business services in EMEA, on how

finance drives strategy in his organisation

Andrew Newman, CFO at Huawei, on growing a multi-billion-dollar business

Excellence in Leadership

S T R A T E G Y A N D I M P L E M E N T A T I O N

ISSUE

Strate

gy a

nd

imp

lem

en

tation

Ex

celle

nce

in L

ea

de

rship

ISS

UE

2 2

013

Tips from global business leaders on plotting and driving successful strategies

model that accurately reflects the changing realities faced by the organisation.

In the retail sector Humphrey Singer, group FD at Dixons Retail, talks to us about how its strategy has succeeded where other high-street retailers have failed (page 32). Meanwhile, Trevor Dighton, former FD of G4S explains how the company’s finance team helped to restore shareholder confidence after the company’s much-publicised failure to provide sufficient security cover at last year’s Olympic Games (page 18).

The popularity of the well-established business model of employee ownership is on the rise. In this issue I interview Sir Charlie Mayfield, chairman of the John Lewis Partnership – a highly successful employee-owned business that has stuck to its principles while also moving with the times (page 14). He explains how the organisation’s finance professionals are essential business

partners in helping to develop strategy, drive growth, support decision-making and open the company’s eyes to potential risks and opportunities.

At a recent CIMA event in London I was joined by HSBC’s group chief accounting officer,

Russell Picot, and Unilever’s CFO, Jean Marc Huët, to mark the start of the IIRC’s consultation for its draft integrated reporting framework. On page 44 we outline the discussions that took place and why integrated reporting is the next step in the development of reporting.

I very much hope that this issue of Excellence in Leadership will stimulate debate on how organisations can develop winning formulas for business models and their strategic implementation in an environment where change is the new normal.

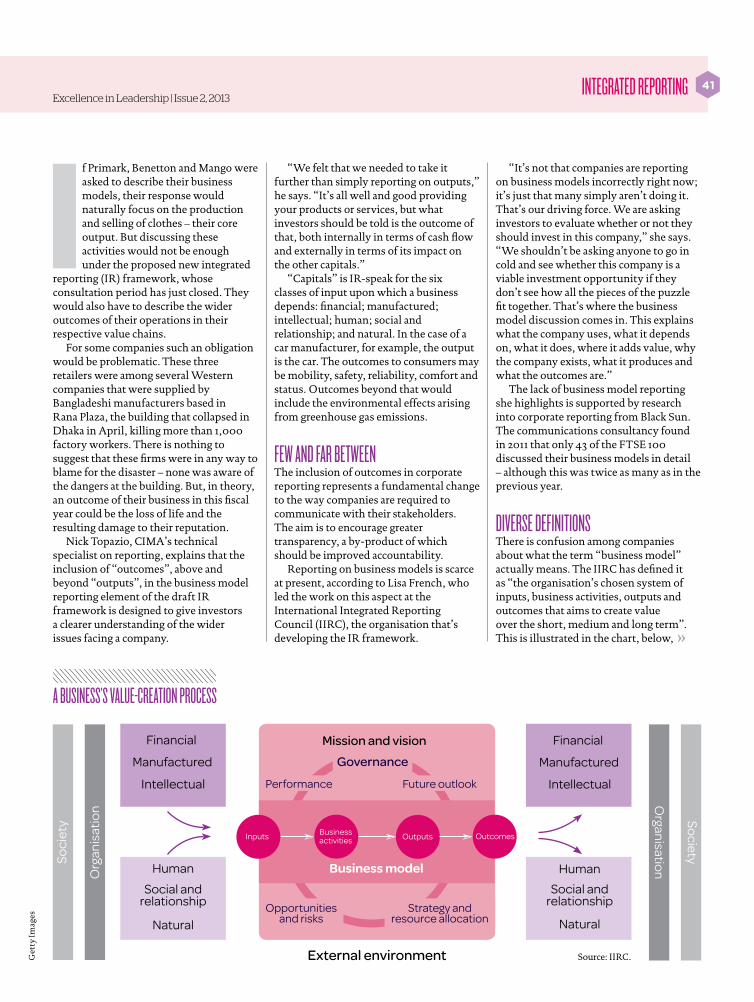

It goes without saying that a robust and flexible business model lies at the heart of an organisation’s success. But it is surprising how many different definitions there are of business models when companies come to report on them. CIMA recently joined forces with PwC and the International Federation of Accountants to support greater reporting consistency by providing a universally

acceptable definition. This work was done as part of an initiative by the International Integrated Reporting Council (IIRC) to create an integrated reporting framework – a subject I outlined in the previous issue.

Early on in the IIRC’s discussion about the framework, it was agreed that the business model should be one of three central themes (the others being value creation and capitals) that will affect the future direction of reporting. The emphasis on the business model as a reportable element reflects the IIRC’s view that one of the main starting points for an investor’s analysis should be the business model and how it relates to the organisation’s strategy, governance, performance and prospects.

In this issue we look at how business models are developing in the fast-moving and volatile environment of the global economic arena. We also analyse the ways in which both new and established enterprises have weathered economic storms to plan and implement their strategies successfully.

What’s clear from the many business leaders we have interviewed is that the finance function is playing an increasingly influential role in shaping, implementing and validating corporate strategy. To chart this development, we start by talking to three senior finance professionals from very different sectors – advertising, cloud storage and business consulting – to find out what key strategic challenges they are helping to overcome (page 8). Andy Blackstone, FD at M&C Saatchi, discusses the constant tension between how much is allocated to growing the business and how much is booked as profit. Graeme Mackenzie, FD at Pulsant, explains his quest to generate clearer, more concise forecasts. And Kevin Booth, partner at Alexander Sloan, describes how his team is concentrating on pulling data into a business

Charles Tilley,chief executive, CIMA

FOREWORD

Strategy and implementation

‘The �nance function is playing an increasingly in�uential role in shaping, implementing and validating corporate strategy’

Excellence in Leadership is the official publication of CIMAplus. For more information visit: www.cimaglobal.com/cimaplus

Cov

er im

age:

Mat

t Mu

rph

y/H

and

som

e Fr

ank

. Th

is p

age,

illu

stra

tion

: Mas

ao Y

amaz

aki/

Du

tch

Un

cle

Excellence in Leadership | Issue 2, 20133

Editorial advisory boardMalinga Arsakularatnechief financial officer, Hemas Holdings

David Blackwoodgroup finance director, Yule Catto & Co

George Ridingchief financial officer, Middle East and north Africa, SAP

Arul Sivagananathanmanaging director, Hayleys BSI

Bogi Nils Bogasonchief financial officer, Icelandair Group

Kai Peterschief executive, Ashridge Business School

Jeff van der Eemschief financial officer, United Biscuits

Jennice Zhufinance director, Unilever China

CONTENTS

3 Foreword6 Vital statistics 8 The new strategy owners Andy Blackstone, FD, M&C Saatchi; Graeme Mackenzie, FD, Pulsant; and Kevin Booth, partner, Alexander Sloan, on the finance function’s role in shaping, implementing and checking the soundness of business strategy.

14 The big interview Charles Tilley, CEO of CIMA, asks Sir Charlie Mayfield, chairman of the John Lewis Partnership, how he has steered the retailer through tough trading conditions.

18 Crisis response Trevor Dighton was CFO of security giant G4S when the business was thrust into the spotlight for failing to meet its

Effective IRHow to produce a clear and informative integrated report p40

Where the buck stops How the finance function’s new role includes checking the soundness of strategy p8

Leading the chargeHow �nance drove Dixons Retail’s new business strategy p32

obligations to provide security staff for the 2012 Olympic Games. He recalls how finance helped to steady the ship.

22 Shared success How the performance of finance shared services is managed and improved at energy giant Shell.

28 Brave new worldNeil Hodge identifies a number of businesses that have successfully adopted online business models – and the challenges they’ve faced.

32 High-street success Group FD Humphrey Singer explains how Dixons Retail overhauled its business plan in the wake of the digital revolution – and saw off its rivals in the process.

36 Growing influence VP Jacek Levernes on how finance drives strategy and implementation in Hewlett-Packard’s global business services across EMEA.

40 How to report it right In light of the publication of the IIRC’s consultation draft of the international IR framework, what are the key ingredients for a successful integrated report?

44 Why IR is important Key messages from a group of senior finance professionals on the value of integrated reporting to businesses around the world.

46 Rapid rise Andrew Newman, CFO of Chinese telecoms giant

Huawei, explains how the business grew from a $6,000 start-up to a multi-billion-dollar concern.

50 Stating its case Huawei defends its security record amid a political row.

52 Employee ownership Why the employee-owned business model is proving so successful – and what global companies can learn from it.

58 Tools of our trade CIMA and the AICPA have produced a resource entitled Essential Tools for Management Accountants. CIMA’s Rebecca McCaffry explains why.

66 CIMA directory

63 CIMA events 65 Next issue

Excellence in Leadership | Issue 2, 20135

61 Get involved with CIMA

Excellence in Leadership | Issue 2, 2013

CIMA is the Chartered Institute of Management Accountants 26 Chapter Street, London SW1P 4NP 020 7663 5441 www.cimaglobal.com

CIMA contact: Learning and development specialist Gillian ButlerEmail: gillian.butler @cimaglobal.com

Excellence in Leadership is published for CIMA by Seven, 3-7 Herbal Hill, London EC1R 5EJ Tel: 020 7775 7775

Group editor Jon WatkinsGroup art director Simon CampbellJunior designer Josh FarleyManaging editorDarren BarrettTechnical editorNeil ColeChief sub editor Steve McCubbin Deputy chief subChristina Ryder Deputy picture editor Louise Fenerci Picture researcher Alex Ridley Editorial director Peter Dean Managing directorJessica Gibson Creative director Michael Booth Production manager Mike Doukanaris Group publishing director Rachael StilwellCommercial directorHilton YoungAdvertising manager Lisa GovierEmail: lisa.govier @seven.co.ukTel: 020 7775 5578

Chief executive Sean King Chairman Tim Trotter

© Seven © CIMA

Cover artwork Matt Murphy

The contents of this publication are subject to worldwide copyright protection and reproduction in whole or in part, whether mechanical or electronic, is expressly forbidden without the prior written consent of CIMA/Seven. All rights reserved.

Origination by Rhapsody. Printed in the UK by Wyndeham Press Group.

The products and services advertised in Excellence in Leadership are not necessarily endorsed by or connected in any way with CIMA. The editorial opinions expressed in the publication are those of the individual authors and not necessarily those of CIMA or Seven. While every e�ort has been made to ensure the accuracy of the information in this publication, neither Seven nor CIMA accepts responsibility for any errors or omissions.

VITAL STATISTICS

Adopting new business models

6

The proportion of �rms that say they make it regular practice to go back and compare their results against the performance forecasts produced for each of their business units in their three- to-�ve-year strategic plans.

Measuring success

Source: The Build Network, 2013.

When was the last time that your organisation had to adopt an entirely new business model?

54%26%

11%9%

It’s happening right now

Never

Longer than 5 years

1 to 5 years ago

37%

E�ective implementation?Strategic planning is crucial to pro�table business growth, but companies typically realise only about 63 per cent of their business strategy’s potential �nancial value because of defects and breakdowns in strategic planning and implementation.

of potential value lost

Source: Mondaq, 2013.

Source: Mondaq, 2013.

15%

Source: CIMA, IFAC, PwC, 2013.

Research conducted by CIMA, the International Federation of Accountants (IFAC) and PwC at the request of the International Integrated Reporting Council shows that very few big companies clearly articulate their business models — ie, what they do, what they rely on and what sets them apart from the competition.

Integrated reporting

77% of the FTSE 350 mention their business models in their accounts

20% 40% 60% 80% 100%

40% provide insightful detail about those models

8% integrate business-model reporting with strategy and business risks

The proportion of chief executives who agree that sustainability is an important factor in strategy and operations for their businesses.Source: “Drivers of long-term business value”, Deloitte, 2012.

81%

8

Get

ty Im

ages

The �nance function is playing an increasingly in�uential part in shaping, implementing and checking the

soundness of corporate strategy in a range of industries. Anthony Harrington asks senior �nance professionals at an advertising agency, a cloud storage provider and a business

consultancy to explain how they approach the task

9

ROLE

An

10

»

ANDY BLACKSTONE

The key to the success of a business whose value depends almost entirely on the skills of its people lies in the fundamental philosophy articulated by the board, according to Andy Blackstone. This guides the strategies and policies of his organisation and can be summed up as the belief that individual entrepreneurs are fully motivated only when they can control their own destiny. This means that, when the company acquires a creative team, the policy is to empower that group of creatives to do what they are good at – namely: creating a good business, producing great work and making a profit.

M&C Saatchi is unique in that it operates as a federation of agency businesses, ranging from start-ups to long-established teams. The company has 29 offices spread across 22 countries. So what metrics can an FD use to monitor progress – particularly since one of the maxims of the company is that it is “designed to be allergic to bureaucracy”?

“The key is to use feedback from clients, as well as measurements such as the win or loss rate of a particular team,” Blackstone says. “For local reasons some companies are going to do very well in a given year and some are not.”

The firm’s Japanese offices, for instance, saw a decline in business after the earthquake of March 2011, but less drastic cyclical changes also take effect from region to region. All these factors must be accounted for when evaluating the group’s performance.

How does M&C Saatchi seek out new acquisition opportunities and, having found them, how does it model a new team of creatives?

“We find our opportunities in two ways. First, you stay in close touch with the market and with your network of contacts, so you have a good understanding of who’s out there. Second, there are plenty of good consultants whom you can ask to do the research and identify good prospects,” says Blackstone, who adds that, once a new office has been lined up, the actual modelling of costs and revenues is relatively straightforward. The executives in the new

team are best placed to make projections of expected revenues, while the office costs incurred by a team of creatives are well understood.

“At the group level you know that a new office is going to cost a certain amount and you check that your expenditure forecasts will cover this. There is always a tension between how much money you opt to spend on growing the business and how much you book as profit. That is a difficult strategy decision and a constant challenge for a board to resolve – not only for our firm, but for any growth business,” Blackstone says. “You are trying to work out where the best place to invest is and which people you are going to invest in, because it’s the people who achieve your growth for you.”

FDs often get closely involved in determining a reasonable bid for an acquisition target. When the target is a business that depends greatly on the skills of its people, this process is rather different from what it would be with a manufacturing firm, for instance.

“Ideally, you are trying to spot people who have been overlooked for reward by the market but who are fantastic. Here you are often looking at the next generation of creative people – those who have yet to make their mark,” he says. “Another part of the process is to monitor the kinds of clients that an office is winning. There is no point in having a great creative team that’s getting bogged down in doing non-creative work for them.”

M&C Saatchi does much of its business in the digital space. One whole floor of the group’s seven-storey London office is full of programmers, rather than people who dream up advertising and branding ideas. Getting the right mix of people doing the right jobs is an operational responsibility, Blackstone says, but it will show up in the numbers if it is not being pursued properly and is one of the factors that an FD working with creative teams must bear in mind.

“We run a decentralised finance operation, with monthly reporting into the centre and regular face-to-face conversations with our offices around the world,” he says. “Spreadsheets are fine, but the key is meeting people and keeping in touch. Spreadsheets alone are dangerous, because the assumptions that underpin them may well change in the real world.”

Andy BlackstoneFinance director, M&C Saatchi

Excellence in Leadership | Issue 2, 2013

12

GRAEME MACKENZIE

Excellence in Leadership | Issue 2, 2013

Graeme MackenzieFinance director, Pulsant

Any FD lucky (or astute) enough to find themselves in an industry segment that’s growing at between 15 and 20 per cent a year, while the rest of the market grows at 0.05 per cent, will undoubtedly be content with their business strategy. But Graeme Mackenzie, of managed hosting provider Pulsant, stresses that his job still provides plenty of challenges.

“Each year we have a large capital expenditure on expanding and fitting out our data centre estate, plus a significant amount of spending on the computer infrastructure that will allow us to increase our capacity and deliver the next generation of cloud services,” he says. “Last year we spent £8m fitting out our data centre estate and £4m on cloud computing infrastructure and customer equipment. This year we are budgeting for a total outlay on data centres and computer equipment of about £8m. All this has to be spent before we generate additional revenues from the extra capacity, so that is a delicate balancing act.”

It was a lot more delicate two years ago, when Pulsant’s annual income was £20m. Now that the firm turns over more than twice that amount, such big capex projects are relatively more comfortable. There is some irony in the fact that the operational flexibility that makes cloud computing so attractive to companies – because it allows them to switch from a capex model to an operational expenditure model, which is far more tax efficient – is not available to the owner of the assets. By way of contrast, the FD of an IT services company that rents infrastructure and data centre space from Pulsant to provide cloud-based applications could claim the outlay against tax as an operational expense.

When it comes to staffing, Mackenzie’s job is easier. About two-thirds of Pulsant’s employees are the responsibility of the operations director, whose task is to specify how many people he thinks he is going to need when a cloud computing service or a new data centre is under consideration.

“It’s not for me to forecast and budget for that side of things, but it is my task to incorporate it into the overall company forecast and ensure that it hangs together with the revenues anticipated from the new service,” Mackenzie says. “The point is that our whole operation flows from the strategy generated by the board down to the individual directors, who turn that into a forecast of revenue and expenditure. We are one of the larger data centre players in the UK – with ten

data centres, including three in Scotland – so it is not a simple exercise to model the business.”

Pulsant secured private-equity backing in 2010 and has since taken over three companies. FDs always play a key role in such deals, but Mackenzie stresses that the whole senior team at his company has become skilled at integrating a newly acquired business.

“We have our own formalised approach and we pretty much stick to our checklist when we acquire and integrate a company. We bring in an external project manager and all the directors have calls with the project manager to ensure that the whole exercise is carried through with a good deal of rigour,” he says. “We are very much a unitary business – a single operation across multiple data centres – which is one of our core strengths.”

The system focuses on forecasts, giving Mackenzie and the board a view 12 months out of what is likely to happen to expenditure and income. “About 95 per cent of our revenues are recurring by the very nature of the service we provide, so I have a very good view of future revenue streams, while our business gears very well indeed,” he says. “A new data centre will take a long time to become profitable, but after that it will generate a good deal of revenue, much of which goes straight to the bottom line. The challenge for the company is to develop new business from the latest data centre investment and to get that operation to where it’s increasing our profitability.”

To do this means selling Pulsant’s services on a sufficient scale to generate significant extra revenue. Mackenzie’s team produces monthly management reports for directors and senior managers, showing all the KPIs. But he emphasises that most of the effort in the monthly management reports goes on providing a view of the future.

“Part of my team is involved with historic numbers and, of course, you want to be completely rigorous and accurate with those – you don’t want any surprises. But the past is the past, so we put a great deal of our effort into getting the forecasting right.”

Mackenzie points out that, when it comes to reporting on the monthly results, how the story is told is almost as important as the story itself. If you bury the directors in detail, they will struggle to see the picture that most concerns them, so highlighting the key figures in a plain and simple way in an executive summary at the start of the report is always important.

“When you’ve run your forecast, you want to show the key things that are likely to affect management,” he says. “That’s why I spend a lot of my time thinking about what is going to make things clearer for my readers.”

Excellence in Leadership | Issue 2, 201313

Kevin BoothPartner, Alexander Sloan

For Kevin Booth, financial models tend to be about helping a client of his eight-partner firm of consultants to evaluate the implementation of their general business strategy or a particular project.

“There are good tools out there that can help you to do this, such as Sage WinForecast, which is an excellent modelling tool for basic forecasts. But, because it runs off a database, it can be a bit inflexible with regard to how you structure some of the what-if analysis. So I tend to prefer to work with Microsoft Excel for more complicated scenarios,” says Booth, although he concedes that setting up a complex model in Excel can take time and, with time being chargeable, this option wouldn’t be cost-effective for a client in many cases.

A good financial model should include a cash flow projection, a P&L projection and a balance sheet. “These interact, of course, but they are very different things and you need all three. I often see clients treating a profit forecast as if it were a cash flow statement,” Booth says. “This is a crucial mistake and can be fatal for the business. I have seen firms with a good profit forecast, based on sound assumptions, that still failed because the cash side of the business was not managed closely enough.”

The problem with cash, obviously, is that you are at the mercy of your creditors the moment it runs out. But having a grasp of profit is equally important in the medium term, since unless a business is either generating a profit or can see its way to a sustainable profit, it will be going out of business anyway. So any evaluation of business strategy has to consider both

dimensions – cash and profit – while the balance sheet shows at a glance what the business has by way of assets and liabilities.

“If you are going to have a comprehensive plan for your business, you need it to cover all of these factors,” Booth says. “The make and break issues are critical, but it is also vital to present a credible model to a potential funder. They want to see sufficient detail to show them that the owner, director or the board has a real grasp of things and has thought through the challenges. The funder will take comfort from seeing that management has a proper view of the issues involved.”

He adds that, because costs are often very much easier to predict than sales, managers need to achieve

a level of confidence that the sales projections are robust and not too optimistic.

“Communication inside the business is key. Any business of any scale has many moving parts, from sales teams to production, all feeding data into the model. The way the finance department pulls everything together and reflects it in the model is vital. If there are surprises and critical changes to assumptions, you need to see that these feed through into the model in a timely fashion. One of the biggest dangers with models is that they fail to reflect the changing realities faced by the business.”

KEVIN BOOTH

‘I o�en see clients treating a pro�t forecast as if it were a cash �ow statement. This is a crucial mistake and can be fatal for a business’

14

The UK has few medium-sized �rms compared with nations such as Germany, whose substantial Mittelstand drives the economy. It’s widely thought that

one way to expand Britain’s mid-market is for more companies to adopt an employee-ownership model. CIMA’s chief executive, Charles Tilley, asks Sir Charlie Mayfield, chairman of the John Lewis Partnership – a thriving employee-owned business – to share his recipe for success

THE IN-DEPTH INTERVIEW

The

BUSINESSPEOPLE

14

Get

ty Im

ages

, Reu

ters

15

people

At last year’s Talk Power conference one of our customer’s presented fascinating insight into how energy strategy played such a big role in developing their fruit production business.

But what are the risks and opportunities for your business in the new energy landscape? And how are UK businesses investing in energy HMEQ@RSQTBSTQDÄSNÄADMDÆSÄSGDHQÄBTRSNLDQR�

Reserve yourself a free seat for this years premier DMDQFXÄBNMEDQDMBDÄ@MCÄÆMCÄNTSÄVG@SÄSGDÄOHBJÄNEÄthe crop are taking about.

Get stuck in at Talk Power - 8 October 2013

Visit letstalkpower.com

"NMÆQLDCÄROD@JDQR�

McKinsey & Company Ä&KNA@KÄL@M@FDLDMSÄBNMRTKSHMFÄÆQL

Ä,DQUXMÄ!NVCDM Ex-energy manager of Marks & Spencer

HM Treasury

Government Procurement Service

Network Rail

EDF Energy

&QD@SÄHCD@RÄto sink your teeth into

8 October l The Mermaid Conference Centre l London

REGISTER

TODAY

Talk Power l 8 O

ctober 2013

visit letstalkpower.com

EDFE_TP_AD_CIMA_ART.indd 1 25/06/2013 12:45

Excellence in Leadership | Issue 2, 201317

THE IN-DEPTH INTERVIEW

The John Lewis Partnership (JLP) is a visionary organisation. It is a great example of how to do business successfully, boldly putting the happiness of employees at the centre of everything it does. All 84,700 workers at the retail powerhouse are partners, jointly

owning 39 John Lewis stores, an online and catalogue business, 290 Waitrose supermarkets and even a production unit and farm.

JLP, which was named multi-channel retailer of the year at the Oracle Retail Week Awards in March, is arguably the most successful case of an employee- owned partnership – and the employees certainly do share the rewards in a business that posted sales of £9.54bn last year. Customer trust underpins this success. John Lewis’s famous slogan is “never knowingly undersold”, which highlights its commitment to price matching.

JLP offers an apprenticeship programme that creates jobs, sustainable career paths and a genuine alternative to university for young people – increasingly important as the costs of higher education continue to spiral. The programme guarantees that all who enter it will secure a job once their training is complete.

Sir Charlie Mayfield became JLP’s fifth chairman in the spring of 2007. He’d joined the organisation in 2000 as head of business development and was appointed to the board as development director only a year later, winning plaudits for developing the partnership’s online strategy before becoming managing director of John Lewis stores in January 2005. Mayfield also chairs the UK Commission for Employment and Skills and in June 2011 he became president of the Employee Ownership Association, a body that represents more than 150 employee-owned companies in the UK.

FOUR TO FOLLOWMayfield’s tips for long-term success in business include the following:• Value and reward your people. “Employees are the last great source of competitive advantage, so they must be at the centre of everything a business does,” he says. “We at JLP never underestimate the value of relationships, advice and service. That is at the heart of our employee-ownership model. It enables us to build stronger links with high-quality suppliers, such as Heston Blumenthal, as they know that it will be a long-term association benefiting all involved. The employee-ownership model fosters long-term planning and accountability. We believe that the responsibility of ownership is to nurture your resources, rather than to look to sell your assets. Our model ensures that we have committed, motivated people who strive for continuous improvement, and

we ensure they are well rewarded. While the fortunes of plcs may fluctuate, JLP’s growth has been steady.” • Understand and take advantage of new technology. “The growth of the web has changed people’s lives and it’s had a massive impact on business models. Like the industrial revolution before it, the IT revolution has dramatically altered how business is done. Traditionally, retailers were constrained by the size of their premises, but now they have more options and can offer consumers an unlimited choice. We have recognised how service is transforming and have put the appropriate emphasis on our online platforms.”• Innovation is the best route to success. “What can you offer that others can’t? This is the key question that all business leaders should ask. Innovation that supports the customer experience is what really adds value. We’re proud of the range of products we bring to market and we consistently review our research and development to keep us ahead of the game.”• Make full use of your finance function. “The best companies will have the most involved finance teams. We’ve seen a steady shift from a department concerned with simply adding up the numbers towards a more engaged finance function that’s helping to develop strategy. Our finance people are essential business partners, driving growth and supporting decision-making. A key part of the role is opening people’s eyes to potential risks and opportunities.”

Mayfield’s comments are very much in tune with CGMA Magazine’s findings relating to risk and innovation (bit.ly/CGMAriskInnovation), which are two sides of the same coin. The key challenge is for companies to promote a culture of innovation and renewals while bringing ideas to market efficiently and managing the risks associated with innovation.

The real impact of technology is rooted in where it disrupts business models. Companies must understand how their models are being affected and what this means for the competition they will face. JLP is a prime example of an organisation that has successfully adapted its business model in order to stay ahead and ensure its success in the long term.

When people talk about what influences property values, the adage is that the most important factors are “location, location, location”. When it comes to business, it should be “people, people, people”.CGMA Magazine’s survey on the talent pipeline has shown that, while most companies understand the importance of human capital, they do not have the right systems, processes and information in place to manage talent effectively. This needs to change. Management accountants can support the change by analysing both financial and non-financial data and then putting it to good use – for instance, by looking ahead to identify the skills that will be needed in years to come and ensuring that current recruitment and development programmes are fit for purpose.

Having served as a captain in the Scots Guards, May�eld joined SmithKline Beecham in 1992 as a marketing manager for Lucozade. A�er a four-year stint at the McKinsey consultancy, he joined JLP in 2000 as head of business development. He became managing director of John Lewis stores in 2005 and was appointed chairman of JLP two years later.

CHARLIE MAYFIELD

18

Olympic -sized How to survive an

Get

ty Im

ages

corporate crisis

19

Last July G4S, the world’s biggest security company, failed to supply enough guards for London 2012 –

plunging the �rm into the worst crisis in its history. Its CFO at the time, Trevor Dighton,

tells Nick Huber how he handled the situation

Olympic -sized

and the role he played in helping to calm employees, clients and investors.

Dighton was in the US on business with Buckles when they were told in a series of phone calls that the company would be unable to fulfil its contract.

“In the space of about a week we went from ‘we might have a problem’ to ‘we will definitely have a problem’,” he recalls.

Putting aside his initial feelings of puzzlement, anger and disappointment, Dighton put the contingency plan in motion. First he phoned the company’s main investors to reassure them that G4S had the contract problem under control and that this would not affect the wider business.

“We contacted the top 20 investors in the first three days,” says Dighton, who has a calm, affable manner.

20Excellence in Leadership | Issue 2, 2013

In the reception area of G4S’s headquarters near Gatwick airport, symbols of the company’s association with the 2012 Olympics are emblazoned across the walls. In one frame, Lord Coe, chairman of the organising committee for the games, thanks the firm for its contribution in helping to run the world’s greatest sporting event.

Given that G4S’s most notable contribution was its failure to provide enough security guards – forcing the government to call in military and police personnel to meet the shortfall – it seems safe to assume that some of Coe’s private comments about G4S weren’t anything that the company would want to shout about. Its £284m contract, which turned into a loss of £70m, should have been a marketing dream. Instead, it was a public relations disaster that shook the FTSE-100 company to its core.

IN THE EYE OF THE STORMThe story surfaced last July, only two weeks before the start of the 16-day extravaganza. G4S admitted to the organisers that it would be unable to supply the 10,500 or so private security guards agreed under its contract. In the end the company, which employs 657,000 people and operates in more than 125 countries, was able to provide only about 8,500 security personnel. The news of its failure soon went global. Some politicians said that the problematic contract was proof that the government could not always rely on the private sector.

G4S’s share price fell by about 20 per cent that month. The company’s chief executive, Nick Buckles, faced calls to quit. But he held on in 2012, although in September two directors did resign.

By early this year, G4S’s share price recovered to more than it was before the announcement about its Olympic problems. The longer-term damage to its reputation is harder to gauge, although fears that the London 2012 fiasco would mean that G4S would not win future government contracts don’t seem to have materialised.

Trevor Dighton was the company’s CFO at the time of the crisis. In his last major interview before stepping down from the job at the end of April, he explains how it felt to be in the eye of the storm

A career in financeTrevor Dighton’s working life has probably been more varied than those of most of his counterparts working in multinational companies. He le� school at 16 and his early jobs included construction work and grave digging.

Dighton then took a diploma in business studies at college and began studying for the CIMA quali�cation. A�er a stint at an electronic components factory he found a job as an internal auditor with Anglo American in Zambia, where he worked at a copper mine.

“You weren’t even told what the job was until you got there,” he recalls.

A�er �ve years in Papua New Guinea working for KPMG, he returned to the UK to join BET, an industrial group that is now part of Rentokil.

Two years a�er joining Securicor’s vehicle services division in 1995, Dighton was appointed �nance director of its security division. He became its deputy group FD in 2001 and was appointed Securicor’s group FD in 2002.

In 2004 Securicor merged with Group 4 Falck’s security businesses to form Group 4 Securicor. Dighton was appointed CFO in July of that year.

STATS

the cost G4S put on its doomed Olympics contract.

Source: Ernst & Young.

£70M

Excellence in Leadership | Issue 2, 201321

G4S one year on

Twelve months a�er the Olympics, G4S is undergoing a series of changes. CEO Nick Buckles stepped down on 31 May to be replaced by the CFO, Ashley Almanza.

Almanza had only been appointed CFO on 1 May. G4S said it had sought someone with the skills to step up to the role of CEO when appointing him.

“We told them that we were on the case, the contract was a one-off and [its value] was small compared with that of the total group.

“We also took them through our crisis management plan.”

During the crisis Buckles and most of the other directors on the executive board were based at Canary Wharf – the main site for the Olympics – but Dighton spent the next few weeks flying around the world, talking to employees and clients, particularly in Europe and America.

They needed reassurance that their services would not be affected by G4S’s problems in covering London 2012. Dighton’s main message was that, although the company was extremely disappointed by its failure to fulfil its obligations under the Olympic contract, this one was very different from other security contracts. Clients were understanding and supportive, he recalls.

The visits also gave Dighton the chance to correct what he says were “massive amounts of inaccuracies” in the media’s coverage. He was responsible for ensuring that the rest of the business continued as normal, too.

As the situation progressed, did he have any sleepless nights? Was he worried about losing his job?

“I don’t usually suffer from stress,” he says, but admits that there was a time when he thought the Olympics contract was going to have more of an adverse impact on the brand than it did.

Part of the reason why the Olympics went so wrong for G4S was the sheer scale of the project. Organisational challenges included recruiting and training thousands of guards to work shifts at about 100 sites across the country.

“We had to make such difficult assumptions about the number of people and timing of people to put in place for an eight-week period,” Dighton says. “We had to create a massive £200m-turnover company that started exactly at the right time and lasted for eight weeks and then finished. It’s just very difficult to get your head round.”

People would tell G4S that they wanted to work on the contract and then not turn up, he adds.

G4S’s contracts for other sporting events, such as Wimbledon (it supplies security staff for the tennis tournament), are small compared with the Olympics.

If the contract was clearly going to be such a logistical challenge, why did the firm accept it?

“We were really the only company that was capable of fulfilling the contract. I’m not saying that we were obliged to do it – we could have said no,” Dighton says. “We should have been able to do it.”

LESSONS LEARNTDighton says that before the Olympics the company believed that its risk-assessment procedures were “pretty robust”. After the games G4S commissioned PwC to review the project in an effort to learn from the experience.

G4S is recruiting a chief operating officer who will be responsible for ensuring that large contracts go through a “more forensic review”, he says.

Life goes on – Dighton and G4S are understandably keen to put London 2012 behind them. Was it at least satisfying to know that he helped to steer a global business through an Olympian crisis?

“The self-fulfilment element of work is all about dealing with difficult issues and not sailing along,” says Dighton – before adding with a rueful laugh: “I’m not saying that we ever want to go through that experience again.”

STATS

the fall in �rst-half pro�ts experienced by the �rm in 2012.

Source: G4S.

60%

Drivingperformance

22

Drivingperformance

In the latest in a series of articles exploring the role of �nance at Shell, the shared-service centre (SSC)

research team at Loughborough University ask George Connell, vice-president of strategy, �nance

operations, at Shell, how the performance of �nance shared services is managed and improved

Excellence in Leadership | Issue 2, 201323

How does the company’s finance operation manage its performance?The answer has five perspectives. First, from a conventional, hierarchical perspective, there’s a process that operates throughout Shell. From top to bottom, everyone has financial and non-financial objectives that they agree with their line manager at the start of the fiscal year. These follow through into specific targets and individual development plans (IDPs). These enable staff to identify development needs and training opportunities for the year.

Taking myself as an example, I set my deliverables and agree with my line manager how they will be measured. If it’s a new relationship, it’s probably going to mean more of a frequent discussion – maybe monthly. In my case, I’ve been working with my line manager for many years, so regular phone calls and meetings take place to discuss performance. But we also have formal, face-to-face mid-year and year-end reviews. Overall, there’s a very established process for performance reviews.

Based on my targets and achievements I’m given an individual performance rating, which is then assessed

as a relative performance factor across a pool of managers with similar grades and skills. The big challenge for Shell is to ensure that the evaluation process discriminates sufficiently – we don’t want to get too many ratings in the middle and hence a bell curve that’s too steep.

As with any such scheme, we have to be vigilant against becoming too cosy and ensure that we really challenge the performance measures and targets. On the other hand, if objectives have been set realistically and there is proper support through the IDPs featuring regular discussions of progress (and problems), one wouldn’t expect too many surprises at the end of the year. Again, it’s about challenge and change, but also about good planning and performance. This gives us a level of predictability that’s helpful. It’s about balance.

Is there a sense of evolution in both the overall SSC journey and day-to-day operations?Yes, the whole process is intended to be dynamic and we can add to that as we go along. The world doesn’t stand still and neither can the work of Shell »C

orbi

s

24Excellence in Leadership | Issue 2, 2013

finance. Some of my objectives will be consistent from year to year, but some new initiatives will occur. These will need new success criteria to be established – and thus new performance measures.

You seem to be describing a mix of management by objectives and the balanced scorecard.Yes, we have taken the best bits from what tend to be presented as two distinct approaches and fused them into a method that works for us.

Tell us about the second perspective.We have a framework of behavioural expectations embodied across a number of codes that everyone at the company is expected to follow. First and foremost of these is safety, which is non-negotiable. Then there are the Shell business principles and a code of conduct, which covers aspects of personal behaviour, including business integrity, ethics and general compliance.

Next are the five behaviours that SSC staff are expected to show from day to day – namely: external focus, commercial mindset, delivery, speed and simplicity. When everyone is demonstrating these behaviours daily, it allows Shell to drive its business forward in an ethical and sustainable way. We evaluate personal performance on how successfully our employees have enacted these behaviours throughout the year.

What about the third perspective?Shell’s ambition is to develop the best leaders. This is enabled by our leadership attributes framework, which includes elements of authenticity, growth, collaboration and performance.

And the fourth perspective?We continually benchmark our performance against our competitors and the wider industry peer group. We do this in a number of ways. First, we are benchmarked by external consultants who can come in and assess where we stand. This gives us a helpful

guide to what we need to achieve. Also, the CIMA-Loughborough Shared Service Centre Forum events have provided a fantastic platform for us to listen in depth to what others in the SSC space are doing and how they have driven their own businesses towards success. The opportunity to ask questions – and thereby get a real insight – has been invaluable.

And the fifth?We measure individual processes and component activities at an operational level in lots of different ways – for example, through key performance indicators, targets, project milestones and so on.

The first perspective, concerning line management control, sounds straightforward, but then you have these other four perspectives. Although these look rational in themselves, taken all together they seem to create scope for confusion. How do you explain this complex-looking picture to employees?The delivery of hard targets is important – ie, the “what”. But it is also important that we understand how we deliver our performance and that this is done in a safe, sustainable, resilient environment that’s underpinned by our core values, including professional and social behaviours.

OK, but do these feed into the strategic key performance indicators?Well, they should and they do, but it’s often difficult to identify a definitive cause-and-effect relationship between activities at the bottom of the organisation and the results at the top of it.

But we thought you said that everything flowed from top to bottom.In one sense it does. But that can, at best, deliver a level of performance against only one plan at a certain time – and don’t forget that the budget is already out of date when the company’s fiscal year starts. Our business is changing; new technology

‘We have taken the best bits from what tends to be presented as two approaches and fused them into a method that works for us’

»

Excellence in Leadership | Issue 2, 201327

and working practices are evolving; and we continuously need to challenge everything to keep up with our competition.

In other words, the performance measures that you’re working to are dynamic. Yes. But, to clarify this: it’s the way that we interpret and react to performance measures that’s dynamic. (That doesn’t mean to say that we don’t create new measures and retire old measures.)

Will they necessarily relate to the organisation’s top-down strategic targets?I think the best way to answer this question is to say that, given all the challenges of change and continuous improvement, we use an array of measures in a flexible manner to deliver a coherent strategic response. Remember that a lot of change is conceived and enacted from the bottom – hence our empowered approach.

How do you measure the performance of finance processes in the SSC?The first stage is to benchmark our performance externally from perspectives including effectiveness, efficiency, compliance and strategic measures. We then establish our metrics for the processes and functions that we operate. We also have to make conscious choices on where we want to focus – arguably there is no organisation that operates at world-class performance levels in all that it does. So we need to focus selectively, which may include some conscious practical trade-offs.

We believe in empowerment and work to make this a part of our people’s working lives. Giving people the power to make decisions creates a strong sense that they have a stake in what the company is trying to do. As a result they are driven to perform better. Again, we encourage the teams not only to focus on the “what” but also to openly discuss the “how”.

is Shell’s vice-president of strategy, �nance operations, and its Glasgow SSC lead. Connell has been with the energy giant for 15 years. He has an MBA in accounting and �nance from the University of Glasgow and holds the CGMA designation.

GEORGE CONNELL

‘Giving people the power to make decisions creates a strong sense that they have a stake in what the company is trying to do’

Ian Herbert, FCMA, is deputy director of the Centre for Global Sourcing and Services at the School of Business and Economics, Loughborough University, where Lin Fitzgerald, ACMA, is professor of management accounting. This series of articles is supported by CIMA’s general charitable trust.

This includes conversations about health and safety, resilience and sustainability – all with an element of fun and social interaction.

We encourage our colleagues to speak their minds freely – this is one of the key measures for team leaders in our annual people survey. We really do care for our people and I think this will continue to be a strong differentiator in our ambition to attract and retain the best talent.

To what extent do you believe that shared services can be applied in Shell?When one evolves to the mature state that we are now in, it’s a question not only of which activities we can transfer to the centres but also of what we should transfer, based on having a sustainable model that incorporates an SSC network and retained finance population in our global environment.

Shell uses the phrase “performance management in a dynamic environment”. What exactly do you mean by this?It’s a recognition that we operate in a globally connected and dynamic environment that is substantially different from what it was a few years back. The physical footprint of the finance function has changed and technology has enabled this. I would expect this pace of change to continue, so we need to constantly challenge how we perform and develop as individuals and teams.

Brave new world

28

Gal

lery

Sto

ck, G

etty

Imag

es

Excellence in Leadership | Issue 2, 2013

Running a pro�table internet enterprise is easier said than done for content providers in an arena where

users aren’t used to paying for what they consume. Neil Hodge examines a number of �rms that are developing successful online business models – and considers how �nance is playing a key role

29

Many industries have complained that it’s virtually impossible for them to make money on the internet, because consumers expect web-based content

and services to be free. Yet a number of new-tech companies in particular have made providing a free online service a selling point. They have attracted millions of users as a result and have lured some of these into buying extra products.

Dylan Smith, co-founder and CFO of Box.com, which launched a web-based data-sharing service in 2006 and is planning a $1bn-plus flotation next year, says that the company uses a “freemium” model, whereby the basic service it provides is free, but users have to pay to use the extra functions or services on offer. It has 15 million users in total, including 140,000 businesses and more than 450 companies in the Fortune 500.

“Our view was that we needed to look at what we did uniquely well, while ensuring that as many people as possible realised that we offered the best service and that they would become regular adopters,” Smith explains. “We have a situation now where 97 per cent of our customers are using our services for free. In effect, the other 3 per cent of users that pay for premium services are funding the business. This has its risks, but the point is that, if you focus on delivering your product the best way you can and make it easy for customers to use, then you’ll retain them and bring in more people who will use it and pay for services.”

THE SHARING ECONOMYSeveral organisations have hit on the idea of tying consumers into short-term subscriptions for premium content and services as a way of retaining their custom and increasing the certainty of cash flow. The so-called subscription (or sharing)

economy has spawned a generation of firms that are trying to keep up with a huge influx of new customers and different operating models. Subs-based businesses such as Netflix, WhipCar and Spotify have been leading the charge. Also, a resurgence in the media, led by publishers such as News International and the Financial Times, has been driven by a growing acceptance among consumers of the subscription model.

Tien Tzuo, founder and CEO of Zuora – a software-as-a-service company that was set up as an online handler of customer orders and payments for firms that have a subs-based revenue model – says that it should not come as a surprise that more and more media groups are moving much of their content behind a pay-wall after the Wall Street Journal led the way back in 1997.

“Good journalism requires money and the advertisement model is not working any more. Advertising revenue from print publishing has not been this low »

30

since the 1950s, so publishers need other sources of income to fill the gap,” Tzuo says. “Readers have proved they’ll always pay for quality writing. Newspapers must realise that readers are their real customers, not advertisers, and that the only long-term way to dig themselves out of their failing business model is to build and monetise relationships with their readers. Different readers have different needs, which means that the papers need to design bundles that give readers choice.”

Tzuo believes that the newspaper industry needs to move beyond simple pay-walls and enter the “pay-wall 2.0” era, which is all about building relationships with customers, encouraging their loyalty and offering them product options, both free and chargeable, that make sense. This entails using flexible, tiered and targeted pricing, while using the right metrics to optimise customer relationships.

“The days of filing financial reports describing turnover, assets and debts are over – this is no longer descriptive enough,” he says. “Now we need to know about retention levels and innovation. In the old world you thought of yourself as a product company and the goal was to ship as many units as you could at the lowest cost. In the

new world it really doesn’t matter how many units you ship. It’s about how many customers you have and the average revenue per customer. It’s fundamentally a completely different business model.”

FINANCE IS KINGNaturally, as the company’s business model is a strategic issue, the CFO is going to be involved – whether signing off the project or getting more hands-on in the change process. Perry Offer, CEO and formerly CFO at Dialogue.net, an SMS aggregator that conducts marketing campaigns via mobile phone networks, believes that the role of the CFO is crucial in determining whether an organisation has chosen the right business model.

“There can be a lot of noise in our industry about what the next new big thing is, but we feel that the best way to move forward is to keep things simple,” Offer says. “For example, we don’t think there is any point in developing new products or services when there is still plenty of opportunity for further market penetration using our existing block messaging service. We have limited resources, so it’s the job of the CFO to

Alan Burns is CFO at PhotoBox Group, which owns two distinct online brands. One of them, PhotoBox, is a digital photo service with more than 22 million users. This allows customers to upload pictures to its website to produce a real photo album that’s then posted back to them. The other is Moonpig, the UK’s leading online card and event gi� retailer, which the group acquired in 2011.

Both brands were launched despite the continuing popularity of the traditional method of buying both cards and photo albums from high-street retailers – and they have since transformed the market. Both businesses are growing, while their bricks-and-mortar counterparts are �nding the high street an increasingly tough trading environment.

Burns attributes the success of both brands to their ability to embrace new technology. For example, Moonpig has developed a mobile application enabling users to make their own cards and buy gi�s. More than one million people have downloaded the app since it was released.

“There has been a clear indication from customers that they want to transact online,” he says. “Those businesses that respond to this demand are the ones that are going to be successful.”

Yet, despite the success of the brands online, Burns believes that the domestic markets they are based in can be exploited further – and that their business models do not need to be altered with an overseas expansion. (With the exception of a small operation it recently launched in Australia, Moonpig operates exclusively in the UK.) He estimates that the single card market in the UK is worth at least £1.2bn a year and that only about 4 per cent of this is generated online.

“It is all about knowing your business and justifying the case for targeting foreign markets,” he says. “At the moment, the �gures do not stand up for us to try to launch in countries such as the US. We can more e�ectively expand here than we could anywhere else.”

Excellence in Leadership | Issue 2, 2013

CASE STUDY: PHOTOBOX GROUP

make the management team aware of the costs involved in developing new offerings and question the return on investment that might be achieved compared with that of marketing an existing product to a larger number of potential customers.”

Steve O’Neill, regional CFO for strategic operations at global technology company EMC, says that the CFO’s role here is to “be the voice of reason. You always need to ask questions and challenge the company’s strategic thinking to find out whether it is on a firm financial footing or not. You need to find out what the return on investment will be if the company develops another product or service, or if it changes its business model; what kind of due diligence has been done; how the figures have been derived; what the expected benefits and risks are; what the competition is up to; and whether or not there is sufficient customer demand. CFOs might not lead the strategy, but they certainly have a hand in steering it.”

Alan Burns, CFO at PhotoBox Group, agrees that the finance chief has a crucial role in determining whether the business model is sound. “We have a responsibility

Excellence in Leadership | Issue 2, 201331

Many online content providers have struggled to make signi�cant revenue quickly, despite the popularity and cutting-edge capabilities of the services they provide. But there are always exceptions – even when the business recognises that its users will not pay.

Helen Biggart, CFO at Switzerland-based Viewster, a global provider of on-demand internet streaming media, says that in the beginning the company was a content aggregator that syndicated movies and clips to other services and device manufacturers. She says the �rm learnt its �rst big lesson when it launched its apps for web-enabled televisions.

“Although our apps were installed on all key manufacturers’ sets in 2011, usage didn’t take o�. There is practically no way to market your app on a connected TV; you can only hope to be discovered,” Biggart says. “Many people have not connected their TVs to the web yet and many others struggle to �nd the apps they want. But we still invest signi�cant resources in these apps because we see a strong strategic position in being there. We believe this will eventually be a meaningful channel for our services.”

Viewster sees a clear preference from its audience for free content over the pay-per-view rental model, especially among younger consumers who are used to watching free channels. “Our business model is driven by the huge demand for targeted online video advertising in a brand-safe, premium environment. With our website we’re able to meet this demand. We’re experiencing healthy growth and margins, and we expect that trend to continue. We also invest heavily in making Viewster as engaging for our visitors as possible. We invest in a wide range of content aimed at younger

people. The depth of our library is expanding week by week and we’re working hard to give users a strong social entertainment experience that makes them want to come back again and again.”

Viewster’s users watched more than one billion videos last year and more than 90 per cent of those views were ad-based and free – on all devices, on web, mobile and connected TVs. As a result, the bulk of its revenue comes from advertising. This income, Biggart says, is “shared with the content owners, who are more than happy to participate in our distribution model, since it gives them exposure to markets and target groups that they would normally �nd di�cult to commercialise. As a business we are focusing on audio-video on demand, because that is what our users prefer and it allows us to di�erentiate ourselves from, and compete with, pay-per-view or subscription-based services.”

Biggart has four tips for other companies that are considering a new – and potentially risky – business model: “First, if you have an idea that you are convinced makes commercial sense, try it out, but ensure that you’ve done your homework and you have a good sense about the industry in which you are active,” she says.

“Second, be �exible and brave enough to change focus dramatically. Most companies hit bumps in the road and it is important to learn from those experiences and persevere. Third, keep an eye on your spending. Money is a very precious commodity when you are a young company, so it’s important that you spend it wisely. Lastly, listen to the right people: the customers, the competition and the big players in whose back yard you want to trample – and do it better than them.”

HOW VIEWSTER WILL PROFIT FROM PROVIDING ‘FREE’ CONTENT

to challenge the senior management team about their thinking behind any important project and to question the financial impact of such a fundamental change. For instance, they need to ask what the reasons are for change and

whether the proposed new business model will capitalise on it,” he says. “At the end of the day, CFOs will be funding the strategy, so it is up to them to ensure that the business case stands up to scrutiny.”

Leading the charge32

Excellence in Leadership | Issue 2, 2013

UK electricals giant Dixons Retail has transformed its business to adapt to technological and market

shi�s that have proved fatal to several other big high-street players. Humphrey Singer, the group’s FD,

tells Rima Evans about his department’s key role in plotting and executing a timely change of strategy

33

B ritish retail chains have taken a battering over the past few years, as harsh trading conditions have transformed the look and feel of the high street. Household

names such as Woolworths, Borders, JJB Sports, MFI and HMV have either disappeared altogether or been rescued as online-only operations.

Yet one of the most familiar and recognisable names among consumers – electricals giant Dixons Retail, which owns the Currys and PC World brands and has had a presence on the high street since the 1930s – has weathered the storm. More than that, it has even seen off its arch-rival Comet, which went bust at the end of last year.

Dixons Retail, which formerly operated a chain of stores badged with the Dixons name, may now be benefiting from being the only specialist electrical retailer left on the high street. But its prime position has been hard-earned. A wide-ranging turnaround plan has helped the business to swing from net debts of £477.5m in 2009 to a position of £42.1m net cash, announced this June.

The strategy at the heart of this shift – known internally as the renewal and transformation plan – was put in place in May 2008, only months after chief executive John Browett (who has since left, to be replaced by Sebastian James)

took the reins of the parent company, which was then called DSG international.

But it’s not only the detailed content of that programme, which puts customers at its heart, that’s of great significance. It signalled a new collaborative approach among business functions – one in which the finance team became a more integral part of the organisation, central to both strategy creation and implementation.

FINANCE TO THE FOREHumphrey Singer, the group’s finance director, explains: “There was a culture shift in which finance became much more commercial. We are now involved in high-level debates and discussions about the direction we are going in and we’re seen as crucial to any of the decisions that are made. Finance directors have a seat at the top table of each of the executive teams of our various business units and it’s important that they are seen as business partners.”

Singer was part of the team that created that new vision. Although he took up his present job in 2011, he’d joined the company four years before that as FD of Currys and had held other influential positions, including FD of the UK and Ireland division, before being appointed to the group’s board. He has been a key player in the transformation that Dixons Retail has undergone over the past five years.

The first shift in thinking came in 2006, when its UK stores ceased trading under

the Dixons name and were rebranded as Currys.digital. Dixons became an online-only offering (although that too was subsumed by the Currys brand last year) in response to consumers’ increasing preference for shopping on the web.

Yet this move didn’t formally mark the start of the turnaround plan. That came two years later when the new management team arrived, and it focused on the company’s customers.

“A combination of realising that customers were changing and living through a deep recession prompted a lot of the change,” Singer recalls. “At the heart of it all is the customer. That can be a cliché but it’s genuinely the starting point for everything we do here. In the pre-internet world, Dixons was all about new technology or product trends and its buying relationships with suppliers. That suited the company back then, but it’s not what works these days, when customers are much more in command.”

This switch underpinned the five-point renewal and transformation plan, launched in a bid to revive the company’s flagging performance. Its key aims include improving choice, value and service for customers; fulfilling the potential of the firm’s position in the UK market; improving the buying experience in stores; cutting costs by simplifying processes; and offering multi-channel retailing.

“Customers want to shop partly online, so we are responding to that,” Singer says. “We’re much less worried about whether »G

alle

ryst

ock,

Get

ty Im

ages

34

customers shop specifically with us online or in stores. It’s about ensuring that they shop with us full stop and that those two bits of our business interact seamlessly. Our research shows that customers will typically make four shopping journeys for larger products such as TVs. In the old days these journeys would have always involved going to a store. Today probably one of those trips – usually the first, to conduct research – is online.”

The past five years have seen the refitting of stores; the launch of PC World and Currys megastores; and the creation of a new type of superstore that brings both brands under one roof. This was first trialled in late 2008.

In 2010 DSG international also changed its name to Dixons Retail. “The most noticeable changes to customers were in stores, particularly in the UK, because of our programme of refitting,” Singer says. “About 80 per cent of our turnover is now through the refitted stores. We will finish that in the next couple of years.”

The revamp has gone hand in hand with a plan for a steady reduction in the number of outlets – the target for the UK is about 400. There are currently just under 500, excluding Dixons Travel shops, which are based in airports.

Singer admits that there had initially been an intense debate about creating the combined PC World and Currys stores, because some people felt that there was a risk that two well-recognised and powerful brands serving distinct markets – computing and electrical/white goods – would be diluted in the process. But the performance of the new two-in-one format exceeded expectations. The trial store in Surrey generated an uplift to gross profit of 65 per cent compared with the results it achieved before the refit.

“In the end, even the advocates were surprised by how well the trial store did,”

Singer says. “It made a very strong offer, providing the best of both worlds. It also attracted a broader range of customers who then shopped in both parts of the store.”

The roll-out programme for two-in-one stores has been accelerated as a result – there are now more than 100 such outlets and further ones are planned.

CONTROL AND STEWARDSHIPFor Singer, there are several aspects to the finance function’s involvement in the turnaround plan. He believes it’s about contributing to the strategic debate as it continues to develop; adding value through the business partnering model; and delivering the core tasks of effective control and stewardship, thereby improving the efficiency of the business.

On the business partnering side, a key project has been to build more collaborative relationships with suppliers, moving away from what was quite an adversarial approach focused mainly on buyer negotiations. This shift was critical in improving the company’s ability to deliver product ranges that it felt were more in line with the new approach.

“The changes we have been through mean that our relationship with Apple, for example, has gone from strength to strength. We’re now the biggest reseller of Apple products in Europe, probably second only to their own stores. Apple are picky about who they partner, so we had to demonstrate to them that we had the right kind of attitude towards how we served our customers and that we were the sort of people they might want to do business with,” Singer says. “A range of suppliers, including other big names such as Samsung, have been very important to us and a critical part of our turnaround. This has enabled us to offer the right kinds of products to our customers.”

Unusually, the finance team itself interacts with key suppliers, forging relationships separate from those established by the procurement function.

“We have a finance-to-finance dialogue about how we are doing financially, lines of credit and so forth,” Singer says. “In my experience there hasn’t been as much of that kind of finance-supplier relationship building elsewhere, but it is pretty well developed here at Dixons Retail. Such relationships mean that finance is playing its part in helping other stakeholders, such as suppliers, to get involved in the company’s transformation journey.”

Elsewhere, the function has been working collaboratively on a project to evaluate the economics and profitability of its different product categories. Although that work began back in 2008, it has intensified in the past two years.

“We wanted to really understand where we make money. That sounds like it should be a straightforward question to answer, but it never is. For example, white goods such as fridges and washing machines occupy a lot of space, so when we think about the profitability of white goods we need to reflect the fact that a lot of the shops’ rentable space is there because we need to display these large bits of kit,” Singer explains. “When a laptop is sold, it’s not only the computer; it’s also the bag and all the accessories that go with it or even the service we offer to set up the computer. So it’s about really understanding the bottom-line contribution that each of those categories make, which is critical. As our analysis has become more sophisticated we have gained more insight.”

The findings then link in with commercial buying teams’ decisions about the range of products they get in and the price they pay, Singer adds. “It helps us

Excellence in Leadership | Issue 2, 2013

‘Apple are picky about who they partner, so we had to demonstrate to them that we had the right kind of attitude towards how we served our customers’

Excellence in Leadership | Issue 2, 201335

and our suppliers to work out how to maximise the value from this business.”

MORE THAN MERE NUMBERSDixons Retail’s adoption of a more customer-focused strategy has had a profound effect on the way the finance function sees its purpose. It’s about more than saving money; it’s also about reinforcing the importance of the company’s commitment to customers.

“We have to be balanced, commercial finance people. So we’re not simply taking the black-and-white view that ‘this will cost a lot of money, so let’s not do it’ and somehow being the blocking agency. Instead, for us it’s about understanding the commercial value of a project and then trying to ensure that it’s also a profitable opportunity that adds value for our shareholders.”

This approach is exemplified by the company’s pay policy. Singer explains that an important change was made a couple of years ago in the way in which the company rewards staff to reflect the new focus on consumers. It was agreed that, providing that stores delivered excellent customer-satisfaction scores, partial bonuses would still be paid, even if they failed to hit financial targets.

“As a finance person you inevitably start twitching when something like that is suggested,” Singer admits. “You do worry that somehow you will lose some financial edge. But it was brave that we could see beyond the potential shorter-term financial impact.”

Finance gave the idea the go-ahead and the investment has been worthwhile. The scores from exit surveys (feedback given by customers as they leave stores to monitor levels of service) and mystery shoppers have rocketed, which Singer credits partly to the change in bonus

Dixons Retail, a FTSE-250 company, is one of Europe’s largest specialist electrical retailers.

The company employs 36,500 people, operating in 16 countries.

Dixons Retail runs the consumer electronics section in Harrods although there is no Currys or PC World branding.

Its airport stores still bear the Dixons name because the brand is so well recognised among overseas customers. Dixons Travel is present in all key British airports, as well as those in Dublin, Copenhagen, Rome and Milan.

DIXONS FACT FILE

structure. Last summer it was reported that 95 per cent of customers were leaving stores satisfied – an increase of 32 percentage points on the previous year.

Innovatively, employees in the stores are also rewarded for online sales on their patch to underline the importance of the company’s multi-channel approach and prevent the online channel from competing with the stores. “We genuinely want colleagues to be agnostic about whether the customer they are talking to buys in their shop or goes home and buys online. It’s about promoting a genuine and seamless multi-channel strategy,” Singer says.

These sorts of initiatives are undoubtedly reinforcing finance’s role as a business partner and enabling it to add more value. “That’s the journey we are on and collaborative relationships are important,” Singer says, but he adds that this still has to be balanced with the function’s “heartland” responsibilities, which include applying controls, ensuring compliance and improving efficiency in order to maintain profitability.

The group is in a two-year programme targeting £90m in cost savings, for example, and is on target to achieve that through measures such as reducing store numbers, increasing energy efficiency and making the head office’s operations leaner.

“The classic finance areas also include protecting our assets, by controlling stock properly, and strengthening the balance sheet,” he says.

But the finance function’s wider strategic role is undoubtedly a requisite in any high-performing business. “There’s a strong correlation between having a very commercially focused, involved finance team at the centre of things and having a successful business. That’s what we are aspiring to,” Singer says.

Despite this, he is clear that the turnaround is far from complete. Challenges remain for its southern European operations, for example, where the group posted an 8 per cent drop in like-for-like sales this year compared with 2011-12. The group maintains that its performance is “robust”, given the difficult markets.

The UK and Ireland, meanwhile, saw a 7 per cent rise in year-on-year sales figures and profits increase by 39 per cent to £113.3m.

“While profitability is improving substantially in the UK, it still needs to go further. That’s the plan,” he says. “So we are not done yet.”

Excellence in Leadership | Issue 2, 201336

Sharing the value

Get

ty Im

ages

Excellence in Leadership | Issue 2, 201337

STATS Poland accounted for 40 per cent of the total head count in eastern European outsourcing centres in 2012.

Source: Association of Business Service Leaders in Poland.

40%

Jacek Levernes, vice-president of Hewlett-Packard’s business services across EMEA, explains how �nance is helping to devise and implement strategy at the technology giant – and how this can drive growth Jacek Levernes is the