everything nonprofits need to know about employee benefits

TRANSCRIPT

Everything Nonprofits Need to Know About

Employee Benefits

12/1/16 1pm Eastern

The presentation will begin shortly.

3

This presentation is being recorded! The recording and slides will be emailed to you.

Please chat in any questions for our guest. We will answer them in the formal Q&A session

at the end of the presentation.

Follow along on Twitter with #Bloomerang @BloomerangTech.

For best audio quality, dial in by phone. (check your email for dial-in info from ReadyTalk)

Before we get started »

3

Our guest presenter »Danielle Mason

• VP, Client Strategy at Benefit Innovations, LLP • specializes in group benefits for medium to

large employers, with focus on cost-containment, employee communication, and ACA compliance

• consults with employers to assist in navigating the nuances of the Affordable Care Act and has spoken about the bill and it's implications to a range of audiences

Not-for-Profit

Benefit StrategyDanielle Mason, HCRS

Benefit Innovations, LLP

2016

Benefit Concerns for NFP’s Comply with the ACA Employer Mandate

All businesses with 50 or more full-time equivalent employees (FTE) provide health insurance to at least 95% of their full-time employees and dependents up to age 26, or pay a fee

Attract & retain good employees

Create employee loyalty Nearly 40 percent of employees say a wide selection of

benefits would make them feel more loyal to their employer

Keep administration simple

Include cost-containment

Why offer benefits?

Attract & Retain talent

Reduce costs through group coverage vs.

individual market

Increase employee loyalty

Make options available: medical, life

insurance, dental, vision, disability,

cancer, hospital policies, telemedicine,

student loan consolidation, etc.

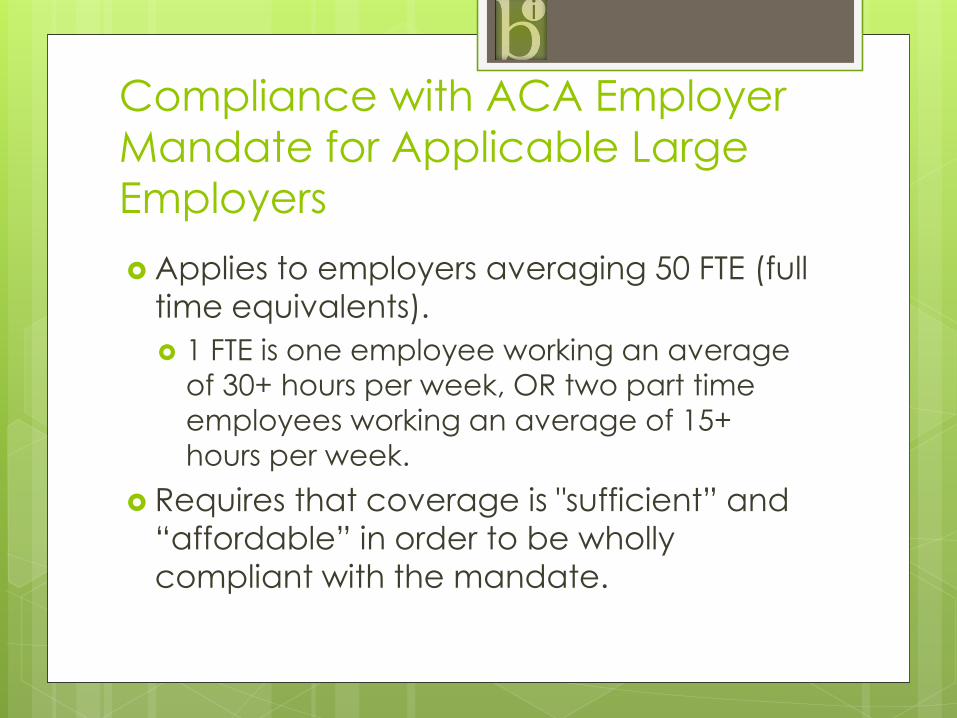

Compliance with ACA Employer

Mandate for Applicable Large

Employers

Applies to employers averaging 50 FTE (full

time equivalents).

1 FTE is one employee working an average

of 30+ hours per week, OR two part time

employees working an average of 15+

hours per week.

Requires that coverage is "sufficient” and

“affordable” in order to be wholly

compliant with the mandate.

“Sufficient” and “Affordable”

Sufficient: requires that medical insurance

covers at least 60% actuarial value of the

costs of healthcare

Affordable: requires that the cost of

coverage offered by an employer does

not exceed 9.5% of employee’s

household income

W-2 Safe Harbor: Use of the employee’s W-2

wages to determine compliant expense

What does non-compliance

cost? Sledge hammer tax: the tax that an employer is

exposed when nothing is offered and any employee attains a PTC on the FFM ~$2K* per employee per year, less the first 30

employees.

Tack hammer tax: the tax that an employer is exposed to if offering coverage that does NOT meet the requirements of “sufficient and affordable”: ~$3K* per employee per year that receives a PTC

on the FFM, to a maximum of (the sledge hammer tax) ~$2K* per employee per year less the first 30 employees.

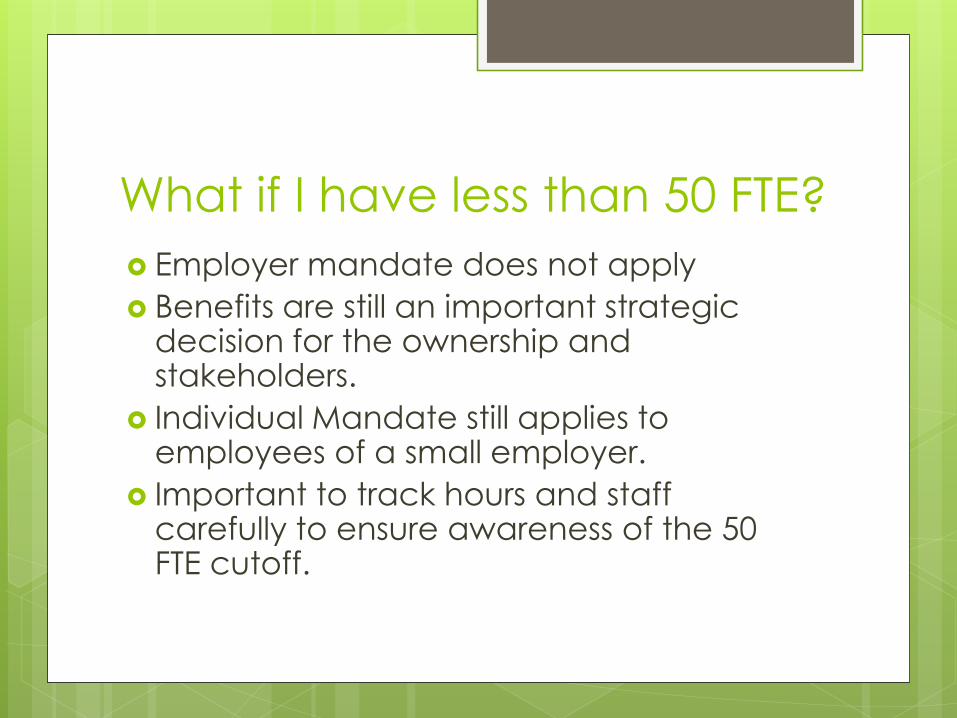

What if I have less than 50 FTE?

Employer mandate does not apply

Benefits are still an important strategic decision for the ownership and stakeholders.

Individual Mandate still applies to employees of a small employer.

Important to track hours and staff carefully to ensure awareness of the 50 FTE cutoff.

Medical Plan Options Comprehensive/major medical/”sufficient

and affordable” coverage.

Fully insured through a carrier like Anthem, United Healthcare, etc.

Partially self-insured, level premium plan (looks and acts like a fully-insured policy); comes with potential savings from a refunding provision.

Self-insured with a TPA and a reinsurance carrier; exempt from state mandates but still exposed to all federal mandates. Overseen by DOL instead of the DOI

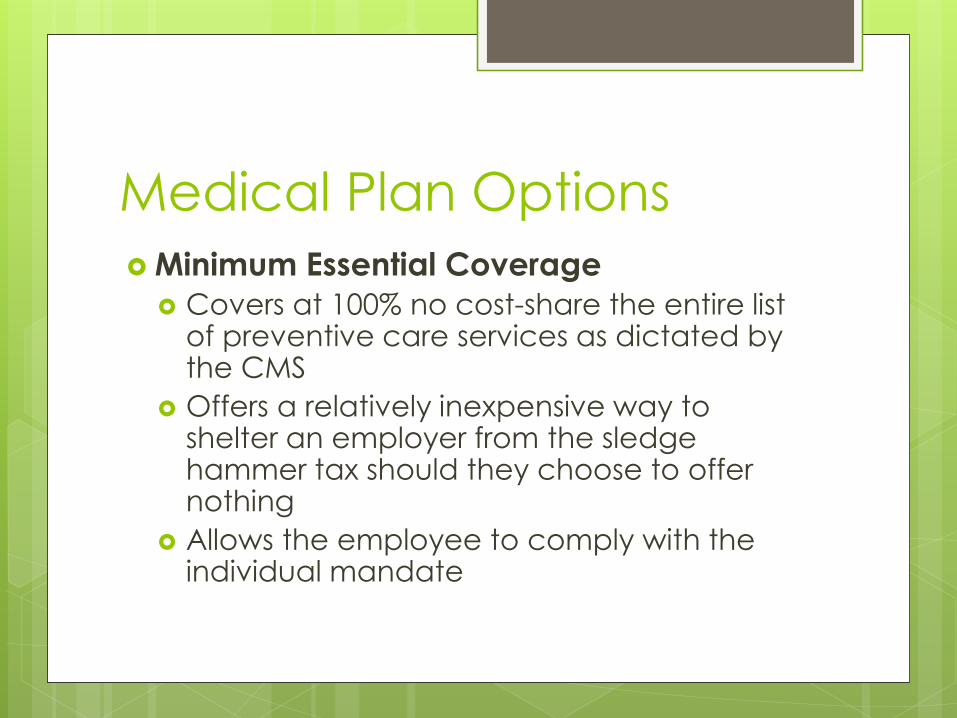

Medical Plan Options

Minimum Essential Coverage

Covers at 100% no cost-share the entire list of preventive care services as dictated by the CMS

Offers a relatively inexpensive way to shelter an employer from the sledge hammer tax should they choose to offer nothing

Allows the employee to comply with the individual mandate

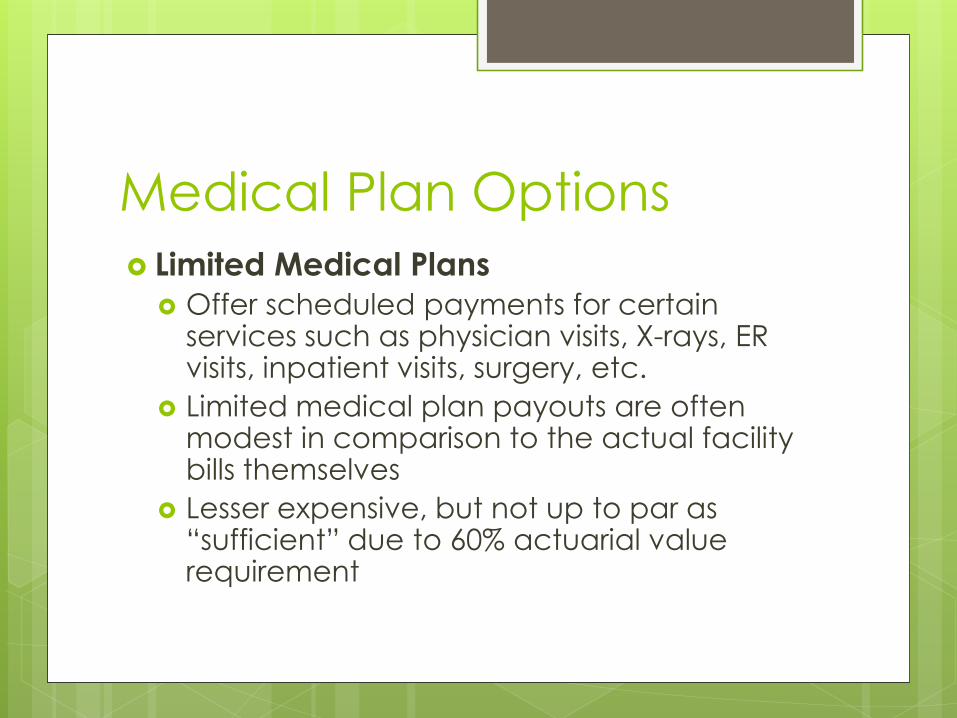

Medical Plan Options

Limited Medical Plans

Offer scheduled payments for certain services such as physician visits, X-rays, ER visits, inpatient visits, surgery, etc.

Limited medical plan payouts are often modest in comparison to the actual facility bills themselves

Lesser expensive, but not up to par as “sufficient” due to 60% actuarial value requirement

Medical Plan Options

Cost-plus pricing strategy

Claims from facilities are re-priced

according to CMS reported costs

Facilities receive a check and agreement

to terms upon cashing

Allows for significant claims savings in the

ballpark of 60-70% on facilities claims as

opposed to PPO discounting of 25-40%

Cost Containment Strategies Telemedicine

Lowers costs to plan of PCP visits, ER visits, urgent care, etc.

70% or better of all office visits can be handled by phone or by video

24/7 access helps redirect out of emergency or urgent care situations

Medical Advocacy Programs Helps employees navigate the “system”

Helps to direct care in-network

Employees are able to get assistance finding the least expensive or highest efficiency care

Billing Advocacy Programs Scours bills for mistakes or replications

Negotiates discounts on behalf of the employee

Cost Containment Strategies RX Funding Programs

Allows for those with expensive medication to seek assistance in affording said medication

Connects those with interest in giving financial donations with those in need of RX assistance.

Wellness Initiatives Keeps plan members healthier in the long-term an in

doing so, pushes medical claims down over time and consistent application

On-site/Near-site/Shared Clinics Creates access to care near the employees themselves

and lowers cost of using standing PCP offices, clinics, urgent care, etc.

Creating responsible consumerism of healthcare and the employer plan.

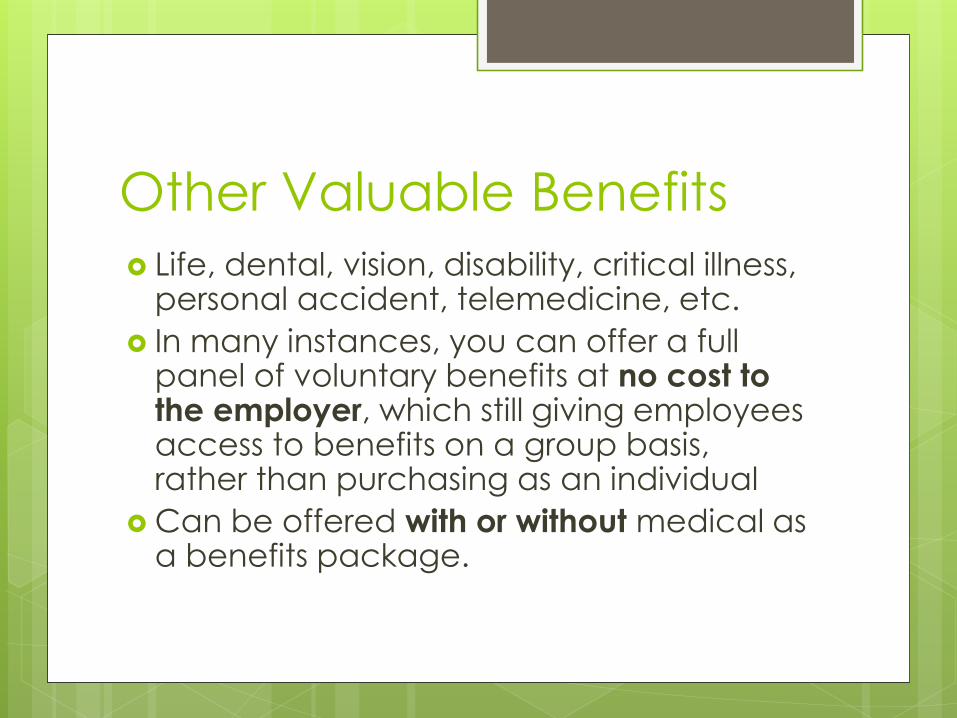

Other Valuable Benefits

Life, dental, vision, disability, critical illness, personal accident, telemedicine, etc.

In many instances, you can offer a full panel of voluntary benefits at no cost to the employer, which still giving employees access to benefits on a group basis, rather than purchasing as an individual

Can be offered with or without medical as a benefits package.

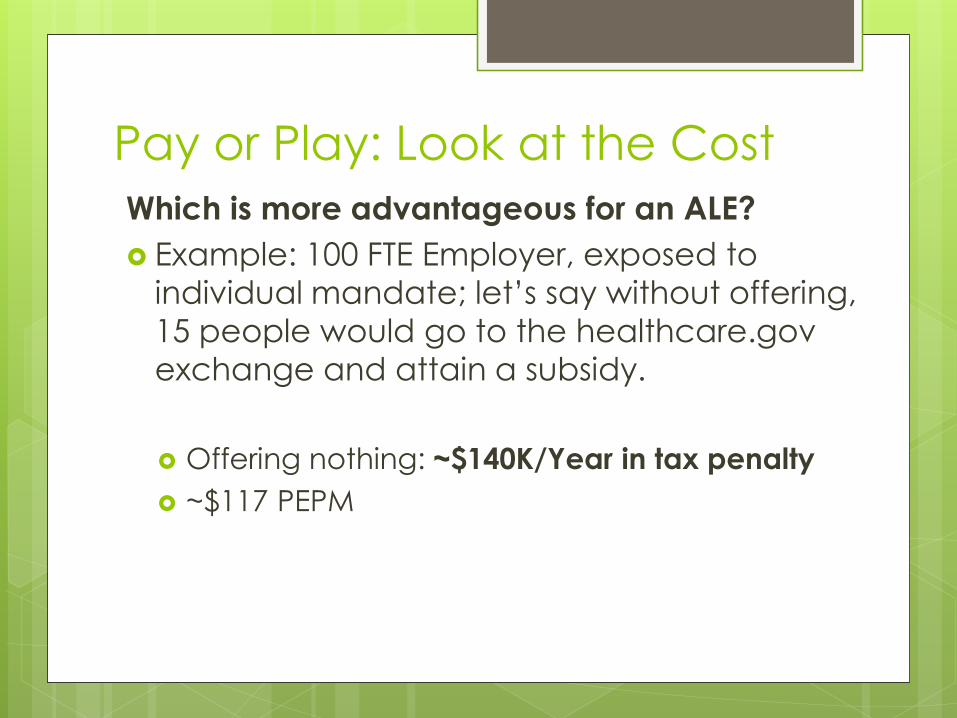

Pay or Play: Look at the Cost

Which is more advantageous for an ALE?

Example: 100 FTE Employer, exposed to

individual mandate; let’s say without offering,

15 people would go to the healthcare.gov

exchange and attain a subsidy.

Offering nothing: ~$140K/Year in tax penalty

~$117 PEPM

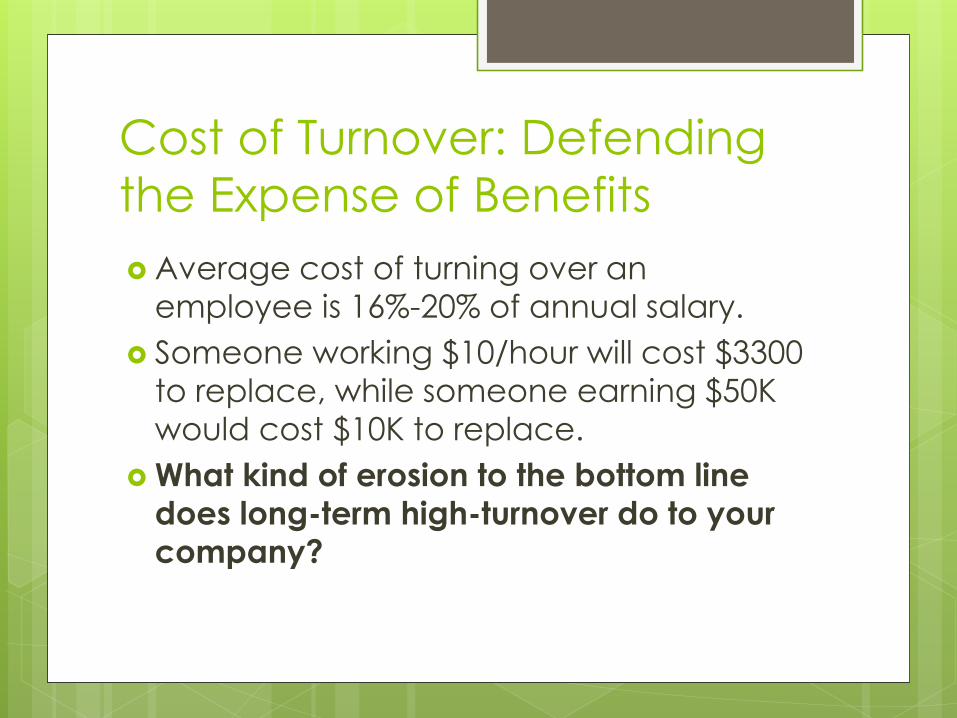

Cost of Turnover: Defending

the Expense of Benefits

Average cost of turning over an

employee is 16%-20% of annual salary.

Someone working $10/hour will cost $3300

to replace, while someone earning $50K

would cost $10K to replace.

What kind of erosion to the bottom line

does long-term high-turnover do to your

company?

Questions?

Danielle Mason, HRCS

Vice President, Client Strategy

Benefit Innovations, LLP

317-663-4044

https://bloomerang.co/resources

•Nonprofit Wrap-Up •Bloomerang TV •Bloomies •eBooks

•Daily blog post •Weekly webinars •Templates •Guides

Our next free webinar »

How to Maintain and Upgrade Your New End of Year Donors

Friday, Dec. 9th – 1:00pm Eastern

Rachel Muir

https://bloomerang.co/resources/webinars