estate administration - law society of … · estate administration ... then it should be done by...

TRANSCRIPT

ESTATE ADMINISTRATION

Brenda R. Hildebrandt Brenda R. Hildebrandt Law Office

Box 526 Moosomin, SK S0G 3N0

Not to be used or reproduced without permission - Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

ACKNOWLEDGMENT

A portion of this material was prepared by Pamela J. Haidenger-Bains, Q.C. and is used with her permission

Revised August 2004 Not to be used or reproduced without permission - Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program i Wills and Estates – Estate Administration

TABLE OF CONTENTS

I. INTRODUCTION .......................................................................................................... 1

II. PRELIMINARY MATTERS ......................................................................................... 1

A. THE INITIAL INTERVIEW ................................................................................ 1 1. Informing the Beneficiaries ............................................................................. 2 2. Duties and Compensation ................................................................................ 2 3. Income Tax and GST Requirements ................................................................ 5 4. Authority to Invest ........................................................................................... 7 5. Securing the Assets .......................................................................................... 7

B. INVENTORY AND VALUE OF THE ASSETS................................................. 8 C. OTHER PRELIMINARY MATTERS .................................................................10 1. Canada Pension Plan Benefits..........................................................................10 2. Life Insurance, RRSP’s, Superannuation, Private Pensions ............................11 3. Assets Owned Jointly with Right of Survivorship...........................................11 4. Cheques Made Payable to the Deceased..........................................................11 5. Canadian Wheat Board ....................................................................................11 III. APPLICATION FOR A GRANT...................................................................................12

A. TYPES OF GRANTS ...........................................................................................12 1. Letters Probate .................................................................................................12 2. Letters of Administration .................................................................................12 3. Letters of Administration with Will Annexed .................................................12 4. Resealed Letters Probate or of Administration ................................................12 5. Ancillary Grants ...............................................................................................13 6. Letters of Administration de bonis non............................................................14 7. Letters of Administration Granted Pursuant to a Power of Attorney ..............14

B. THE APPLICATION FOR A GRANT ................................................................14 1. Rules of General Application...........................................................................14 2. Application for Grants of Probate....................................................................18 3. Grants of Administration .................................................................................21 4. Letters of Administration with Will Annexed .................................................23 5. Resealed Letters Probate or Letters of Administration....................................24 6. Ancillary Grants ...............................................................................................27 7. Letters of Administration de bonis non............................................................27 8. Letters of Administration by Power of Attorney .............................................28

C. MATTERS CONCURRENT WITH THE APPLICATION.................................29 1. Notify the Beneficiaries ...................................................................................29 2. Advertising for Creditors .................................................................................29

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program ii Wills and Estates – Estate Administration III. CALLING IN THE ASSETS AND THE PAYMENTS OF DEBTS.............................31

A. TRANSMISSION OF THE ASSETS...................................................................31 B. INVESTMENT OF ESTATE FUNDS .................................................................32 C. PAYMENT OF DEBTS........................................................................................32 IV. PRE-DISTRIBUTION CONSIDERATIONS ................................................................34

A. TAX CLEARANCE CERTIFICATES.................................................................34 B. ADEMPTION OF ASSETS..................................................................................35 C. SIX MONTH WAITING PERIOD.......................................................................35 D. COMPARATIVE TAX RATES ...........................................................................36 V. PASSING OF ACCOUNTS ...........................................................................................37 VI. THE OFFICE OF THE PUBLIC GUARDIAN AND TRUSTEE .................................39 VII. COURT APPLICATIONS AND CONTENTIOUS BUSINESS...................................44

A. PROOF IN SOLEMN FORM...............................................................................44 B. COMPELLING PRODUCTION OF THE WILL ................................................46 C. ISSUES ARISING DURING THE ADMINISTRATION ...................................47 D. THE FILING AND PASSING OF ACCOUNTS.................................................48 E. REVOCATION OF A GRANT ............................................................................48 F. REMOVAL OF AN EXECUTOR OR ADMINISTRATOR ...............................48 APPENDICES APPENDIX A – Estates Checklist ........................................................................................A – 1 APPENDIX B – Documents To Be Filed Checklist..............................................................B - 1 APPENDIX C – Estate Information Sheet ............................................................................C – 1 APPENDIX D – GST INFORMATION ...............................................................................D – 1

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program iii Wills and Estates – Estate Administration PRECEDENTS

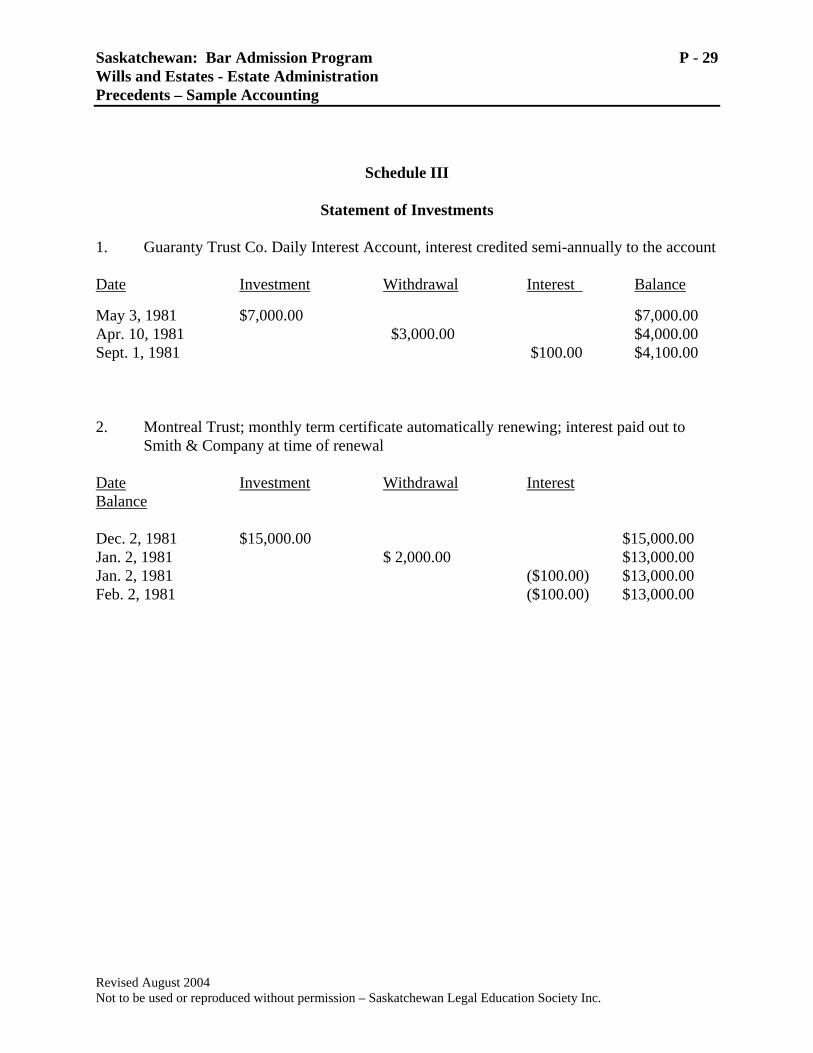

PRELIMINARY MATTERS: Authority to Invest Trust Funds.............................................................................................P – 1 Notice of Appointment of Attorney.......................................................................................P - 2 Suggested Procedure for Dealing with Motor Vehicles ........................................................P - 3 Form Letters...........................................................................................................................P - 4 TIPS ON DRAFTING APPLICATIONS FOR A GRANT...................................................P - 19 THE PUBLIC GUARDIAN AND TRUSTEE’S INVOLVEMENT IN THE TRANSFER OF ASSETS........................................................................................P - 25 SAMPLE ACCOUNTING: Preliminary Distribution - Simple Estate...............................................................................P - 27 Final Distribution - Simple Estate .........................................................................................P - 31

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 1 Wills and Estates – Estate Administration

I. INTRODUCTION

The Administration of Estates Act, S.S. 1998, c. A-4.1 was proclaimed in force July 1, 1999.

This separate piece of legislation replaced former sections 100 to 141 of the Queen’s Bench Act

dealing with the administration of estates, which had previously been located in the Surrogate

Court Act prior to 1992. While the principles of estate administration have remained the same

over the years, and much of the wording in the new legislation is similar to the previous, the

organization of the legislation has been altered significantly. Additionally, some matters of

substantive law have been moved from the Queen’s Bench Rules to the Act.

II. PRELIMINARY MATTERS

A. THE INITIAL INTERVIEW

Your first contact with the estate client generally arises shortly following the death when you

meet with the proposed executor or administrator of the estate. This will often be a difficult time

for your client as he/she may still be grieving the loss of a loved one. Good communication

skills are essential to provide reassurance to your clients and to properly acquaint them with the

anticipated procedures.

At this stage you should obtain as much information as possible, to simplify and streamline the

estate administration process. Most law firms will have some form of estate questionnaire which

assists in the gathering of this information. These questionnaires are designed to address the

matters which must be included in later estate documentation and help to ensure that potential

complications are identified early in the process.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

2 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

1. Informing the Beneficiaries

There is no legal requirement that a formal reading of the Will be held. However, some solicitors

find this to be a useful practice in that it provides an opportunity to meet with those persons with

whom they will be dealing on a regular basis. It can help to instill the sense of trust that is required

for smooth dealings in an estate. It can also be used as an opportunity to outline to those persons

present some realistic expectations about the administration of the estate. Beneficiaries in particular

should be prepared for delays which will inevitably occur before they receive their shares. If the

solicitor cannot convey the information in person, then it should be done by letter.

Although this contact with the beneficiaries is useful, one must always bear in mind that the

client is the estate and instructions are taken from the executor or administrator and not the

beneficiaries. The solicitor’s first duty, therefore, is to the executor or administrator. The

purpose in keeping the beneficiaries informed is to try and prevent complaints from arising

during the course of administration, which complaints make the executor’s/administrator’s job

and the solicitor’s job more difficult.

2. Duties and Compensation

The solicitor and the executor/administrator should have a clear understanding of the terms of

engagement and the respective duties of each party. The legal fees chargeable in connection

with estate administration are set forth in Rule 745 which reads as follows: “745(1) Subject to subrule (3), the lawyer retained by the personal representative shall not accept payment for services to the personal representative or to the estate in excess of that provided in tariff Schedule I “C”. (2) The lawyer shall provide the personal representative with a copy of this rule and tariff. (3) Where a lawyer and a personal representative agree that the lawyer should be paid a fee greater than the fee provided for in the tariff, the lawyer shall be entitled to that fee if the beneficiaries, after being provided with a copy of this rule and tariff Schedule I “C”, approve the agreement.”

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 3 Wills and Estates – Estate Administration

Pursuant to Schedule I “C”, the lawyer is entitled to charge a percentage fee “for all necessary

services rendered preparing all papers leading to grant; for preparing and filing any estate tax

and succession duty or like return and the settling of any tax or duty assessed (not including

attendance in court or chambers in proceedings with respect thereto); for transmitting title to all

estate assets to the personal representative and the transfer thereof to a beneficiary; for

publishing Notice to Creditors; for obtaining the Public Guardian and Trustee’s Certificate; for

ordinary attendances and correspondences.” However, under Paragraph 3 of Schedule I “C”, if

the executor/administrator performs the bulk of the duties of the executorship or administration,

then the legal fees shall be reduced by 40%.

Presumably, Schedule I “C” delineates the scope of the services rendered by a solicitor in an

ordinary estate. This leaves to the executor/administrator the tasks of securing the assets,

performing inventory of the assets, ascertaining the creditors, preparing and filing income tax

returns and obtaining Tax Clearance Certificates, selling assets (if required), paying out all

creditors, investing and managing the estate assets, assembling an accounting and obtaining

releases. Often the lawyer will perform many of these services for the same fee as allowable

under Schedule I “C”; however, it should be recognized that these are in fact services over and

above those required.

The issue may become important when determining the amount of any compensation payable to

the executor or administrator. A personal representative cannot charge for services which have

been rendered by the solicitor for the estate, nor is a solicitor entitled to receive compensation for

services performed by the executor which would otherwise have been performed by the solicitor.

Re Nash Estate (1955), 17 W.W.R. 246 (B.C.S.C.)

Re Lloyd Estate (1954), 12 W.W.R. 445 (Man. C.A.)

An excessive charge by an executor or administrator for compensation could therefore result in

either the proposed compensation or the solicitor’s bill being reduced for the areas of overlap.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

4 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

Paragraph 3 of Schedule I “C” implies that a lawyer does in fact carry out administrative duties

thereby reducing the effectiveness of the argument that the services under Paragraph 2 of

Schedule I “C” relate only to legal documentation.

The executor or administrator should be advised from the outset to keep track of his time spent,

services performed and disbursements incurred if it is anticipated that a claim for compensation

may later be made.

With respect to compensation payable to an executor, the Saskatchewan Queen’s Bench case of

Re Verbonac (1984), 31 Sask. R. 161 reiterated the considerations previously expounded by our

Court of Appeal. These were:

(a) the magnitude of the trust; (b) the care and responsibility springing therefrom; (c) the time occupied in performing the requisite duties; (d) the skill and ability displayed; and (e) the success which attended its administration. In Verbonac, the accounts were approved based on percentages in the range of 1% to 5% for

each phase of the estate. Commenting on this in the case of Re Preboy Estate (1989), 72 Sask.

R. 33, affirmed (1989) 74 Sask. R. 223 (C.A.), Mr. Justice McLellan noted that, while courts

have often resorted to the use of percentage figure on the value of the asset involved in each

specific phase of the administration, such a method is only a guide to which the court can refer,

and along with the five considerations, determine a reasonable allowance.

In the more recent case of Gerrand et al v. Safian (1995), 134 Sask R. 229 (C.A.), the Court of

Appeal referred to Preboy Estate and Re Verbonac with approval. The Court of Appeal further

made it clear that in determining a fair and reasonable allowance it is difficult to consider an

appropriate amount of compensation where sufficient information of time expended is not

provided. Therefore, all executors seeking compensation should keep records of the time

expended in pursuit of their duties. The Gerrand decision has been relied upon in such recent

decisions as Re Dimmock Estate, [2002] S. J. No. 606.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 5 Wills and Estates – Estate Administration

If the beneficiaries perceive that any delay in the administration of the estate is attributable to the

executor, the quantum of the executor’s compensation may well become a contentious issue

when the time comes for execution of the final Releases.

Pursuant to Rule 745(1) the lawyer cannot accept a fee greater than that set forth in Schedule I

“C” unless there is compliance with Rule 745(3). The lawyer must also provide the executor or

administrator with a copy of Rule 745 and Schedule I “C”, which together outline the fees

chargeable by the lawyer. It is best to provide a copy of this information at the outset so that it is

not overlooked at the time of billing. This practice also helps to ensure that the client knows the

basis upon which legal fees are charged.

3. Income Tax and GST Requirements

The executor/administrator and the beneficiaries should be advised of certain income tax and

GST requirements which will impact on the administration of the estate.

Under section 159 of the Income Tax Act, an executor or administrator cannot distribute any

part of the estate without first having obtained a Tax Clearance Certificate from the Canada

Revenue Agency. If distribution of the estate proceeds without a Tax Clearance Certificate and

taxes are later found to be owing, then the executor or administrator can be held personally

liable to pay the outstanding taxes. The process of obtaining the Tax Clearance Certificate,

however, will be the major source of delay in distribution of the estate. A Clearance Certificate

cannot be obtained until all relevant tax returns have been filed and processed. Therefore, it

can take from six months to a year to obtain the necessary clearances, although Canada

Revenue Agency has been endeavouring to speed this process. The executor/administrator

must therefore be forewarned of this potential delay.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

6 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

Section 270 of the Excise Tax Act similarly requires that a personal representative obtain a

Clearance Certificate in connection with remittance of GST. Failure to obtain a Clearance

Certificate will leave the personal representative liable under section 270(2) for unpaid past or

future GST, which would include any GST collectible by the estate on supplies of property from

the estate to the beneficiary.

In the period shortly following the implementation of the Goods and Services Tax, some offices

of Revenue Canada Customs and Excise were unwilling to issue Clearance Certificates in estates

where the deceased was not registered for GST purposes. From the perspective of the personal

representative, this type of response was not satisfactory. Depending upon the nature of the

property, there can be liability for GST on the transfer of assets to beneficiaries. Also, it is

possible, particularly if the death occurred in the so-called transition period following the

implementation of the GST legislation, that the deceased should have been registered for GST

purposes or the estate should have been registered for GST purposes but was not. As a result,

there could be GST liability even though neither the deceased nor the estate was registered. The

prudent course of action would be to insist upon obtaining an actual Clearance Certificate,

however, this may become more difficult to do given amendments to the Excise Tax Act in recent

years.

If the executor/administrator is also the sole beneficiary of the estate, then the decision might be

made to distribute without waiting for the Clearance Certificate. As the executor/administrator

in such circumstances is also the person who receives the assets, it makes little difference

whether any outstanding taxes are paid by the estate or by the personal representative/beneficiary

after distribution.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 7 Wills and Estates – Estate Administration

4. Authority to Invest

If it is anticipated that the lawyer will be handling funds on behalf of the estate it is common

practice to have the executor (or administrator, when appointed) execute an Authority to Invest

Trust Funds, a sample of which is found in the precedent materials. The purpose of such a form

is twofold.

First, there are those practitioners who feel that the form is necessary and required in all

situations where funds are to be invested on behalf of a client because of the provisions found in

the Legal Professions Act and the Rules of The Law Society of Saskatchewan regarding payment

of interest to the Law Foundation and the handling of trust funds.

Secondly, the investment of estate monies is a discretionary power of the executor/administrator

which cannot be usurped by the solicitor. It is therefore in the best interests of both the

executor/administrator and the solicitor that written instructions as to the investment of funds

appear on the file in the event that such investment is required of the solicitor. In this regard, it

should be noted that both the Trustee Act and Part 13 of The Law Society Rules limit the type of

investment which the solicitor can make.

5. Securing the Assets

The executor or administrator may find it necessary to protect the assets of the estate prior to

even obtaining the grant of probate/administration. Some suggestions as to the types of actions

which might be necessary are found in the Checklist in these materials. The executor or

proposed administrator should, however, resist intermeddling in the estate to the greatest extent

possible so as to avoid incurring liability should there be a problem with the grant.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

8 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

B. INVENTORY AND VALUE OF THE ASSETS

Prior to applying for a grant, it is necessary to prepare an accurate inventory of the estate assets.

This inventory will serve more than one purpose so it necessary to spend some time and effort in

ensuring that it is as accurate as possible.

An accurate inventory is first required for filing with the petition documents, as Rule 701

requires an inventory which is verified under oath. Form 104, referred to in Rule 701, indicates

that the statement of assets is divided into Parts One and Two. Part One lists all of the assets

which will pass through the estate and which are within the jurisdiction of the Saskatchewan

grant. Part Two lists all of the assets which do not pass through the estate (for example, jointly

owned assets) or which are not within the jurisdiction of the Saskatchewan courts (for example,

real property in another province). The values shown are the fair market value as of the date of

death.

In a case relating to former Surrogate Court Rule 23, Mr. Justice Baynton provided clarification

of exactly what is meant by the term “at the time or date of death”. He indicated that Rule 23

(which in large part is reproduced in Rule 701 and Form 104) only makes sense if the words

“property of the deceased at the time of death” or “at the date of death” are interpreted to mean

“the property that this deceased owned just before he died”.

See Re Brown Estate, [1993] 2 W.W.R. 513 (Sask. Q.B.)

This analysis, which appears correct in law, is not, however, being followed in relation to

Canada Pension Plan death benefits. In the fall of 1997, The Law Society of Saskatchewan

published a notice indicating that the Judges of the Court of Queen’s Bench had recently agreed

that the estimated Canada Pension Plan death benefit should be included in Part One of the

Statement of Assets.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 9 Wills and Estates – Estate Administration

More recently, section 8 of the Administration of Estates Regulations was made effective.

Section 8(3) lists those assets which are not to be considered as property of the deceased person.

Of these, item (c), concerning Canada Pension Plan payments, delineates only payments to a

surviving spouse or child.

The estate inventory will also be examined by Canada Revenue Agency prior to its issuing a Tax

Clearance Certificate. It is therefore necessary to be as accurate as possible so that the statement

reflects the taxable status of the deceased. A well-prepared Statement of Assets is very useful to

the accountant in preparing the income tax returns.

Additionally, the probate fees charged by the court and the legal fees are both based upon the

gross value of the assets as shown in the inventory.

The form letters which appear in the precedents relate to the collection of the information

required to prepare an accurate inventory of the assets. Examination of the sample Statement of

Assets provided indicates that it is usual to include items such as the accrued but unpaid interest

on such assets as bank accounts, term deposits and Canada Savings Bonds. This information

also becomes very useful at the time of preparing the income tax returns for the estate. The

Checklist found in the materials indicates the different methods of valuation for the different

types of assets.

While it would appear that the job of assembling the inventory of assets belongs to the executor

or proposed administrator, this service is most often actually performed by the solicitor because

of his or her greater familiarity with the information required.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

10 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

C. OTHER PRELIMINARY MATTERS

It may take a month to six weeks to receive back all of the information required to prepare a

complete Statement of Assets. In the meantime, there are often preliminary matters which can

be undertaken. In particular, assets which can be transferred without receiving a grant can be

collected in at this time.

1. Canada Pension Plan Benefits

Where the deceased had contributed to the Canada Pension Plan for any three years after 1996,

the estate will be entitled to certain benefits from the Plan. Forms can be obtained from the

federal Department respecting the various applications for benefits.

The estate is entitled to receive a Death Benefit, the amount of which is based on past

contributions. Its purpose is to assist in defraying the funeral expenses. It is therefore paid to

the estate, and not to the surviving spouse. It must therefore be applied for by the

executor/administrator. It will be reported as income earned by the estate, on the T-3 Trust

Return.

The surviving spouse is entitled to receive a monthly payment which continues for life or until

remarriage occurs. The surviving spouse, therefore, applies for this benefit, not the

executor/adminstrator.

Monthly payments are also available for children under the age of 18 years, and for children over

18 who are attending school or university. Again, these applications are made by the surviving

spouse or the adult child, and are not the responsibility of the executor/administrator.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 11 Wills and Estates – Estate Administration

2. Life Insurance, RRSP’s, Superannuation, Private Pensions

Where assets such as life insurance, retirement savings plans, superannuation or private pension

plans have a designated beneficiary for the policy or plan, the proceeds of the policy or plan can

be applied for immediately. Each company will have to be contacted for its requirements for

payment out.

3. Assets Owned Jointly with Right of Survivorship

Assets which are owned jointly with a right of survivorship can be transferred immediately to the

surviving joint tenant. However, it is the responsibility of the surviving joint tenant to arrange

for or give instructions for the transfer and pay for the costs of the same.

4. Cheques Made Payable to the Deceased

The banks may refuse to deposit cheques which are made payable to the deceased, after he or she

has died. It is therefore a common practice to return cheques made payable to the deceased to

the issuer, and request that they be made payable to the estate.

Additionally, this serves as a useful safeguard to ensure that the deceased is still entitled to

receive the cheque. For example, the estate is entitled to keep the Canada Pension cheque

received in the month of death, but must return all other Canada Pension cheques of the deceased

which are thereafter received.

5. Canadian Wheat Board

The Canadian Wheat Board will not permit grain to be hauled in on a deceased person’s permit

book. It is therefore important to have the plastic plate re-issued in the name of the estate so that

grain can be hauled if a quota opens.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

12 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

III. APPLICATION FOR A GRANT

A. TYPES OF GRANTS

Prior to preparing the documents which are required for the grant, it must first be determined

what kind of grant is to be sought. The following are some of the more common types of grants:

1. Letters Probate

Where the person dies leaving a Will which names an executor, and the executor is willing to

act, the grant applied for is that of Letters Probate.

2. Letters of Administration

Where the person has died without a Will, the person applying is seeking a grant of Letters of

Administration.

3. Letters of Administration with Will Annexed

Where the person died leaving a Will, and the Will fails to name an executor, or the executor and

any alternate executor is unable or unwilling to act, an application is made for Letters of

Administration with Will Annexed.

4. Resealed Letters Probate or of Administration

If a grant of probate or of administration has been received in any other province or territory, in

the United Kingdom, in any other country of the British Commonwealth or in any state of the

United States of America, then the executor or administrator so named can apply in

Saskatchewan to have the original grant “resealed”. Once the original grant has been resealed,

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 13 Wills and Estates – Estate Administration

then it is as effective in the new jurisdiction as if it had originally been granted here. Only the

person named in the original grant can apply for a resealing.

The reason for resealing, or applying for an ancillary grant which will be discussed later, is to

deal with property located outside the original jurisdiction. Under the English law of conflicts, a

grant made within any particular jurisdiction is effective with respect to all assets located in that

jurisdiction. It does not extend to any immoveables (real property) located outside the

jurisdiction. There is some dicta to the effect that where the deceased died domiciled in, for

example, Saskatchewan, then a Saskatchewan grant extends to all of his movables (personal

property), wherever located. There is some dispute as to the correctness of this position. [See

Dicey & Morris, The Conflicts of Laws, 11th edition, Rule 129, Comment (1)]; however, a grant

from one Canadian province is generally recognized elsewhere in Canada as being effective for

dealing with Canadian movables. The most common reason, therefore, for applying for a

resealing or ancillary grant is to deal with real property in another jurisdiction.

5. Ancillary Grants

Where a grant has been received in some jurisdiction other than a Canadian province, territory,

the United Kingdom, a British Commonwealth country or one of the states of the United States

of America, an application for resealing cannot be made. Additionally, if the grant was

originally from one of the above jurisdictions but the executor or administrator cannot for some

reason (such as death) apply, then a resealing cannot be sought. Instead, application is made for

an ancillary grant. It recognizes, however, that there is already a primary grant in existence to

which it is merely ancillary or secondary.

See Re Dunning Estate (1984), 28 Sask. R. 204.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

14 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

6. Letters of Administration de bonis non

Where an administrator fails to complete the administration of an estate before his or her own

death, then another grant must be obtained in order to complete the administration of the estate.

This grant is known as Letters of Administration de bonis non.

Where an executor dies before completing his or her administration of the estate, the rights of

executorship will pass on down to his or her executor, assuming that the first executor left a Will

naming an executor, and that second executor has taken out Letters Probate. If the chain of

executorship is broken, then application is made for Letters of Administration de bonis non with

Will Annexed.

7. Letters of Administration Granted Pursuant to a Power of Attorney

In some circumstances the person or persons entitled to apply for Letters of Administration (with

or without Will Annexed) will not wish to act for the time being, but also do not wish to

renounce. Such person(s) may give power of attorney to someone else to apply for Letters of

Administration by means of a power of attorney. An executor cannot give a power of attorney to

someone else to apply for Letters Probate.

B. THE APPLICATION FOR A GRANT

The basic rules of practice regarding the application for grants are found in sections 4 through 19

of the Administration of Estates Act and Rules 690 through 723.

1. Rules of General Application

Some of the Rules and sections in the Administration of Estates Act must be considered in every

application. These provisions are discussed in the following.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 15 Wills and Estates – Estate Administration

(a) Section 4(1) of the Administration of Estates Act;

“4(1) Letters probate or letters of administration may be granted under the seal of the court on proof: (a) that the deceased:

(i) resided in Saskatchewan at the time of death; (ii) resided outside of Saskatchewan at the time of death and left real or personal property within

Saskatchewan; or (iii) resided outside of Saskatchewan at the time of death but the executor or administrator will be

a party to an action within Saskatchewan; and (b) of the will or of the fact that the deceased died intestate.”

(b) Rules 698 though 703.

These Rules set out the basic information that must appear in every application for a grant.

Rule 698 provides that the various Queen’s Bench forms, appropriate to a request for the various

types of grants, must be followed. The application must be signed and verified by an affidavit of

the applicant [Rule 700]. Specific forms for these affidavits are also provided in the Rules.

Every application for a grant must set out the following information as required by Rule 699(1):

i. the name and address and relationship to deceased of every person entitled to share in the deceased’s estate;

ii. the age and marital status of the deceased at death; and

iii. that the applicant is of the full age of 18 years, or is a trust company.

By Rule 699(2) the application for a grant must state whether or not the deceased is survived by

a child or dependent adult. Where a child or dependent adult is interested in the estate, or may

have a claim under the Dependants’ Relief Act, 1996 or the Family Property Act, this

information must be included in the application and a notice to the Public Guardian and Trustee

or the Property Guardian, as the case may be, in Form 101, must be filed, in duplicate, with the

application.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

16 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

To obtain a certificate that no infants are interested in the estate, a request is made to the local

registrar in accordance with subsections (2) and (3) of section 4 of the Administration of Estates Act: “4(2) On the request of the applicant, where the local registrar is satisfied that no infants are interested in the estate of the deceased, the local registrar shall provide the applicant with a certificate to that effect, together with the letters probate or letters of administration. (3) An executor or administrator may apply to the public guardian and trustee for a certificate that no minors are interested in the estate of the deceased: (a) where the local registrar does not issue a certificate stating that no minors were interested in the estate at the time when the letters probate or letters of administration were granted; or (b) where letters probate or letters of administration were granted by the Surrogate Court for Saskatchewan before November 15, 1992.”

It is important to remember to request the certificate that no infants are interested at the time the

documents in connection with the application for the grant are submitted to the Court House.

With respect to section 3(a) of the Act, an example of the situation where the Public Guardian

and Trustee will become involved in the issuance of the certificate is where a certificate cannot

be obtained right away. For instance, an infant may be interested in the estate, but the estate is

awaiting passage of the six-month period in connection with a potential claim under the

Dependants’ Relief Act, 1996.

An application for grant must also contain a statement in Form 104 showing all the real and

personal property of the deceased at the time of death. This statement is to be verified by an

exhibited to the applicant’s affidavit [Rule 701(1)]. This statement is divided into two parts, the

first of which sets out all the assets which will pass through the estate and be subject to the

jurisdiction of the Saskatchewan court. Part Two sets out the assets which either fall outside the

estate or are not within the Saskatchewan jurisdiction.

As noted earlier, the value of the assets must be set out in the statement. The value which is

given is the current or fair market value as of the date of death. It is important to try and

ascertain the values as closely as possible to this date as it will have certain income tax

consequences.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 17 Wills and Estates – Estate Administration

Additionally, if it is a very old estate which is now being probated, the value as of the date of

death may well be significantly lower than the current value.

The value of the assets to be shown is the gross value. No deduction is made for the debts of the

deceased unless the debt is a loan, mortgage or agreement for sale relating to the real property in

excess of any insurance proceeds which will be used to discharge that debt. The deduction of the

mortgage or loan is shown in relation to the particular piece of property involved and is not

shown as a general deduction from all of the assets. It is also not necessary to include a

statement of debts with the application, although it is useful to get information concerning the

debts of the estate at the time of your initial interview. Such information may be required in

connection with preparation of the income tax returns as well as in connection with dealings with

the Public Guardian and Trustee.

Where a second grant is being sought (that is, a grant de bonis non, a resealing, or an ancillary

grant), then only the value of the unadministered property or the property to be administered in

Saskatchewan is to be listed in the statement [Rule 701(2)].

If the death occurred before January 1, 1977, then, pursuant to Rule 702, the application must

also include a succession duty or estate tax return, or the waiver of the Government that it does

not require the filing of the return. Whether it is a succession duty or estate tax return which is

required will depend upon the time period involved. The collection of death taxes rotated

between the federal and provincial governments during different time periods. These time

periods are as follows:

(a) Death before April 1, 1947 - the province collected succession duty tax.

(b) Death between April 1, 1947, and December 31, 1958 - the federal government collected succession duty tax;

(c) Death between January 1, 1959, and December 31, 1971 - the federal government collected estate tax;

(d) Death between January 1, 1972, and December 31, 1976 - the province collected succession duty tax.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

18 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

The practice has been to contact the appropriate government authority to obtain either the forms

regarding filing of the returns or a waiver of collection of the tax. Provincially, Saskatchewan

Finance has determined that, given the very few estates that would require processing in this

fashion this many years post-1976, it is not expedient to retain this requirement. As such,

Saskatchewan Finance has authorized the Information Services Corporation to automatically

allow transfers to proceed without the filing of the return/waiver. Given the provincial position,

Canada Revenue Agency likewise considers the matter to be a non-issue. Therefore, from a

practical perspective, neither returns nor waivers will be in effect regarding succession duty or

estate taxes for death occurring in the period April 1, 1947 through December 31, 1976, the

years respecting which such taxes have in the past been collected. Rule 702 may then possibly

be read as precautionary, in the event that succession duty or estate taxes are ever reinstated in

the future.

2. Applications for Grants of Probate

The following discusses the Rules and sections of the Administration of Estates Act applicable to

applications for grants of probate.

(a) Section 8 of the Administration of Estates Act: “8(1) The due execution of a will is to be proved in the form and manner prescribed in the rules of court. (2) In addition to the proof mentioned in subsection (1), a judge may require: (a) an affidavit of plight and condition; (b) any further or other proof that the judge considers necessary; or (c) proof in solemn form.”

Further information concerning proof of execution of the will is found in Rule 707.

(b) Rules 704 through 710.

This portion of the Rules directs itself to the documentary evidence which must be produced for

proof in common form. A Will is said to have been proved in common form when it is proven

upon the oath of the executor. That is, the technical requirements for validity are proven by

affidavit rather than viva voce evidence. Proof in solemn form therefore occurs when a trial of

the issue is taken and the evidence proving the Will is heard in open court.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 19 Wills and Estates – Estate Administration

Many of the technical requirements of this portion of the Rules are clearly embodied in Form 98

which is the application for grant of probate form. These requirements come, for the most part,

from Rule 706. Form 98 is quite detailed and draws attention to potential problem areas. The basic minimum information required by Form 98 must in all cases be supplied. However, in

certain circumstances where there is an unusual element to the estate, additional information may be

required. For example, if one of the primary beneficiaries has died after the testator but before the

application, special mention should be made of this fact in the application. As a general rule, the

solicitor may add information to the application but should never delete any information required by

the form. In some circumstances, the solicitor may be aware of a potential problem with the Will which

will likely require proof in solemn form. Often unhappy family members will give notice to the

court of the potential problem by placing a caveat against the estate leading to an order for proof

in solemn form. Occasionally, however, there is no one who is sufficiently disturbed by the

issue who wishes to file the caveat. The solicitor for the estate then must decide as to the

appropriate manner of placing the issue before the court. The accepted practice in this province appears to be to present an application in common form

drawing attention to the problem area by the presentation of the additional necessary facts in the

application or by separate affidavit. If the examining judge feels proof in solemn form or other

evidence is necessary to decide the issue, an order to that effect is made [Rule 707(7)]. The application for grant is always made by the executor named in the Will. An executor cannot

give a power of attorney to someone else to apply on his behalf. If an executor does not wish to

act, he may renounce prior to applying for Letters Probate. The renunciation must be in Form

105 [Rule 704(2)]. If an alternate executor is named, that alternate may then apply for Letters

Probate. The application, however, must show the reason why the alternate executor is applying

instead of the primary executor [Rule 704(3)]. If the executor or executors all renounce such

that there is no named executor to apply for Letters Probate, the application to be made is that for

Letters of Administration with Will Annexed.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

20 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

By Rule 705, the testamentary document in respect of which the grant is sought must be

exhibited to the affidavit of the applicant. Execution of the Will is proven by one of the

subscribing witnesses thereto by an affidavit in Form 107 [Rule 707(1)]. It is therefore usually

necessary to locate one of those witnesses. If no witness can be located, then Rule 707(2)

permits verification of the execution of the Will by other means. Where such other means are

employed, an affidavit should also be provided setting out the facts as to why the witnesses

cannot be located and what search was made for them.

Occasionally you may be presented with an Affidavit of Execution of Will which was prepared

and sworn at the time of the signature of the Will. This Affidavit is only acceptable if the Will

and the Affidavit were deposited in the local registrar’s office, pursuant to Rule 707(3). If the

Affidavit and Will were not deposited, then the Affidavit cannot be submitted with the Petition,

and a fresh Affidavit must be obtained.

The execution of a holograph Will is proven in accordance with Rule 707(5) with the use of

Form 108, which establishes that the entire Will, including the signature, is wholly in the

handwriting of the deceased.

Any interlineations, erasures or omissions on the Will, whether initialled or not, require that an

affidavit as to plight and condition in Form 109 be filed [Rule 707(6)].

All documents referred to in the Will or other documents believed to form part of the Will must

be produced or their non-production accounted for [Rule 708].

The common law respecting wills does allow a copy of Will to be probated or a Will to be

reconstructed from verbal evidence, where the court is satisfied that the original has not been

destroyed for the purpose of revocation. Rule 709 therefore allows a grant upon such evidence

as the court may require.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 21 Wills and Estates – Estate Administration

If the Will is in another language, it must be translated and accompanied by an affidavit of

translation in Form 110 [Rule 710].

There is no requirement in Saskatchewan that an executor, whether resident in province or out of

province, must be bonded. However, some other jurisdictions do impose a bonding requirement

on non-resident executors.

3. Grants of Administration

The legislative provisions relating grants of administration include sections 13, 16, 20 and 21 of

the Administration of Estates Act and reference should be made to these provisions.

As with the application for Letters Probate, the forms set out in the Rules for application for

Letters of Administration are very complete and self-explanatory. Many of the technical

requirements set out in Rules 711 through 720 are embodied in the forms.

Rule 712 sets out the priority of the persons who are entitled to apply for Letters of

Administration. Essentially, the grant will be given to that person who is the next of kin of the

deceased, as it is that person who had the most immediate interest in the due administration of

the estate. It must be shown that the person applying has a beneficial interest in the estate or that

she has a power of attorney for a person having a beneficial interest. The person must also be

considered to be fit in accordance with section 17 of the Administration of Estates Act

[Rule 713]. A trust company cannot, therefore, apply for Letters of Administration in its own

right. It is neither in the list set out in Rule 712 nor does it have a beneficial interest. A trust

company, therefore, can only apply by means of a power of attorney, in accordance with section

16 of the Administration of Estates Act.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

22 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

At certain levels there may be more than one person who is entitled to apply; for example, the

deceased may have died leaving children but no spouse. In such a case, all the persons of the

same level have an equal right to apply. Therefore, either all of the persons of the same level

will be applying to act as joint administrators or those who do not wish to apply will renounce.

The renunciation is in Form 105 or 106.

No grant will be made to an applicant unless all persons having an equal or prior right to apply

have been cleared off by renunciation or by court order [Rule 714(1)]. No grant will be made to

more than three persons [Rule 715]. If there is a dispute as to who should be applying, an

application may be made to a judge for a determination [Rule 714(4)].

If the solicitor is in the position of having one or more persons entitled to apply, but that person

or those persons wish someone lower on the list to apply, there are only two alternatives. First,

all those of equal entitlement with or priority to the person wishing to act can renounce. In that

case, however, they are taken to have renounced absolutely, and this may cause problems if the

person appointed then dies without completing the administration. Alternatively, the person or

persons entitled to act can give a power of attorney to the person they wish to act. The power of

attorney is effective for so long as those giving it do not wish to apply. Therefore, if a problem

arises in the administration, those originally entitled can step back into the administration of the

estate. Rule 716 authorizes execution of such a power of attorney, which is to be in Form 111.

Under section 20 of the Administration of Estates Act, every person receiving a grant of

administration must post a bond to ensure due performance. Rule 719 sets out the technical

requirements for the bond. However, in most circumstances, the estate will bee seeking an order

dispensing with the posting of the bond. The bond will only be dispensed with if the conditions

in subsections (3) and (4) of section 20 of the Administration of Estates Act are met. These are

as follows:

(a) the value of estate does not exceed $5,000; (b) the proposed administrator is the sole beneficiary; or (c) all of the beneficiaries and creditors have consented to dispensing with a bond.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 23 Wills and Estates – Estate Administration

This information must be set out in affidavit form with the application [Rule 720(1)]. As well,

the application must clearly request the dispensing of the bond.

In circumstances where the ground for dispensing with the bond is that all parties have consented

to such dispensation, this consent is often merged into the renunciation form if it is one and the

same person who is giving a consent and a renunciation. In order to give the consents, all of the

beneficiaries must be ascertained of full age and have sufficient mental capacity. If any of the

beneficiaries are children or dependent adults, the Public Guardian and Trustee may consent on

their behalf [Rule 720(3)]. If some of the beneficiaries are contingent and therefore

unascertained, it may be impossible to meet the requirements of the Rules and a bond will

therefore be required.

If the next of kin who would have been entitled to apply for administration appoints a trust

company as his attorney, this must be a trust company within the meaning of the Trust and

Loans Corporations Act, 1997. Under section 41(5) of that Act, the following is noted:

“(5) Notwithstanding any rule or practice or any provision of any Act of Saskatchewan requiring security, but subject to an order of a court or judge, no trust corporation licensed pursuant to this Act is required to give security for the performance of its duty in any office described in subsection (1).”

4. Letters of Administration with Will Annexed

The requirements for obtaining a grant of Letters of Administration with Will Annexed are a

hybrid of the requirements for Letters Probate and Letters of Administration. By Rule 711, the

application for grant of Administration with Will Annexed “shall also comply with the

applicable rules relating to grants of probate”.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

24 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

Under Rule 704, the priority is established for those persons entitled to apply for Letters of

Administration with Will Annexed. This is as follows:

(a) executors;

(b) residuary legatees or devisees in trust;

(b) residuary legatees or devisees for life;

(d) ultimate residuary legatees or devisees or where the residue is not wholly disposed of, the person entitled upon an intestacy;

(e) the legal personal representative of persons named in (d);

(f) legatees or devisees or creditors;

(g) contingent residuary legatees of devisees or contingent legatees or devisees or persons having no interest in the estate, who would have been entitled to a grant had the deceased died wholly intestate; and

(h) the Crown.

Clearly, this priority list differs substantially from that ordering used for Letters of

Administration on an intestacy.

The balance of the requirements, including the provisions regarding the bond, relating to an

application for Letters of Administration also apply to an application for Letters of

Administration with Will Annexed.

5. Resealed Letters Probate or Letters of Administration

Theoretically, a resealing should be a procedure of less formality than an ancillary grant because

it assumes that the original grant came from a country, province or state whose laws have their

origin in British common law. However, in practice the procedure is just as complicated as

applying for an ancillary grant. The applicable Rules and sections of the Administration of

Estates Act are discussed in the following.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 25 Wills and Estates – Estate Administration

(a) Sections 38 and 39 of the Administration of Estates Act

“38(1) A person who has been granted letters probate, letters of administration or another document purporting to be of the same nature by a court of competent jurisdiction in any province or territory of Canada, in the United Kingdom, in any other member of the British Commonwealth or in any of the states of the United States of America may apply for resealing pursuant to this section.

(2) An applicant for resealing shall: (a) produce the document to be resealed to a local registrar and deposit a copy of it with the local registrar; and (b) pay the fees as prescribed in the regulations for a grant of letters probate or letters of administration.

(3) Subject to subsection 39, under the direction of the court, the letters probate, letters of administration or other document shall be resealed by the local registrar with the seal of the court.

(4) A document resealed pursuant to subsection (3): (a) has the same effect in Saskatchewan as if it had been originally granted by the court; and (b) is subject to any orders of the court or the Court of Appeal as if letters probate or letters of administration had been granted in Saskatchewan.

(5) For the purposes of this section, the following have the same effect as an original: (a) a duplicate or an exemplification of letters probate, letters of administration or other document purporting to be of the same nature that is sealed with the seal of the court that granted it; (b) a copy of letters probate, letters of administration or other legal document purporting to be of the same nature that is certified as correct by or under the authority of the court that granted it. 39(1) Letters of administration shall not be resealed pursuant to section 38 until: (a) a certificate of the clerk or registrar of the court that issued the letters is filed, stating that security has been given in that court in an amount that is sufficient to cover the assets within the jurisdiction of that court and the assets within Saskatchewan; or (b) in the absence of a certificate described in clause (a), security is given to the court that covers the assets in Saskatchewan in the same manner as for an original grant of letters of administration.

(2) Notwithstanding that a certificate has been filed pursuant to clause (1)(a), the court may refuse to reseal letters of administration until security is given in an amount that is sufficient to cover the assets in Saskatchewan.

(b) Rule 722

Under Rule 722(1) the application to reseal a foreign grant must be in Form 117 and verified by

an affidavit in Form 118. As noted in the instructions included in Form 117, the application

must generally comply with the provisions relating to an application for Letters Probate. If the

resealing is with respect to Letters of Administration or Letters of Administration with Will

Annexed then the provisions regarding the giving of security must also be met. Alternatively,

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

26 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

under section 39 of the Administration of Estates Act, it must be shown that sufficient security

was given in the original jurisdiction to cover the Saskatchewan assets. Even in such

circumstances the court, pursuant to section 39(2), may still refuse to reseal Letters of

Administration until security is given in an amount that is sufficient to cover the assets in

Saskatchewan.

Under Rule 722(2) if the resealing involves a Will which affects “immoveable property,

including real property and a leasehold or other interest in land in Saskatchewan”, the manner of

making the will, the validity and effect of the Will must be shown to be in accordance with the

laws of Saskatchewan. This may be proven by either an original Affidavit of Execution of Will

or by producing a court certified copy of the same affidavit which was filed in the original

jurisdiction.

However, Rule 722(2) itself causes some problems in interpretation as to what is to be provided.

The Rule states that the manner of making, the validity and effect must be proven. Does the

Affidavit of Execution of Will prove only the manner of making or does it also prove that the

validity and effect of the Will is the same as in Saskatchewan? Some judges have taken the

position that only an Affidavit of Execution has to be produced, as all other issues affecting the

validity and effect of the Will are verified in the application. Others take the position that an

additional document is required. For example, what if the originating jurisdiction does not

recognize holograph wills, and there was a holograph Will in existence which was not admitted

to probate in the original jurisdiction for that reason? The holograph Will would be recognized

in Saskatchewan as a valid Will, and therefore the wrong Will would be admitted for resealing.

Under Rule 722(3) at the time of the application the original grant or a court certified copy of the

same must be produced, together with a notarial copy of the original grant. The original or court

certified grant will be returned to the applicant, with the resealing endorsed on the grant. The

notarial copy is left as a record on the file.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 27 Wills and Estates – Estate Administration

6. Ancillary Grants

An ancillary grant amounts to an original grant from a second jurisdiction. Under Rule 723(1),

therefore, the application for an ancillary grant must comply with all the Rules relating to

probate or administration as the case may be.

Under Rule 723(2) a certified copy of the original foreign grant must be exhibited to the affidavit

of the applicant. Rule 723(3) also requires the applicant to show why an application is not being

made for a resealing.

7. Letters of Administration de bonis non

The term “de bonis non” is an abbreviation for “de bonis non administratis” which means “of the

goods not administered”. The materials required for an application for Letters of Administration

de bonis non are essentially the same as of an ordinary application for Letters of Administration

although the wording of the application varies slightly [see Form 114].

The rule specifically applying to an application of de bonis non is Rule 717. Subsection (5)

thereof requires that the original grant, or a court certified copy thereof if the original has been

lost, be submitted with the application as an exhibit to the affidavit verifying the application.

Where the original grant has been lost, this needs to be stated in the affidavit. The affidavit must

also exhibit a statement in Form 104 showing all the property which remains to be administered,

pursuant to paragraph 3 of Form 115.

The application in Form 114 makes reference to the death of the first executor/administrator. In

circumstances where it is an executor who has died, the application goes on to explain that there

is no other executor to carry on the administration of the estate. This would occur in

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

28 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

circumstances where the first executor died without naming an executor for his own estate.

When the chain of executorship is broken in this fashion, then the application is really one for

Letters of Administration de bonis non with Will Annexed [Rule 717(2)].

An application for Letters of Administration de bonis non should be made to the same judicial

centre from which the original grant was issued. This is in accordance with section 26 of the

Administration of Estates Act that reads as follows:

“26(1) After letters probate or letters of administration are granted, all actions or matters with respect to the estate shall be carried on at the judicial centre where the grant is made, unless otherwise ordered by the court. (2) An application for a transfer of the records with respect to an estate from one judicial centre to another may be made ex parte or on any notice that a judge may direct.”

8. Letters of Administration by Power of Attorney

The rules and sections of the Administration of Estates Act applicable to this type of grant are as

follows:

(a) Section 16 of the Administration of Estates Act;

“16(1) The next of kin regularly entitled to administer an estate may appoint an individual or a trust corporation within the meaning of the Trust and Loan Corporations Act as his or her attorney to apply for and receive a grant of letters of administration. (2) A judge may grant letters of administration to an attorney appointed pursuant to subsection (1).”

(b) Rule 716.

The materials for an application for Letters of Administration (with or without Will Annexed)

which are intended to be granted pursuant to a power of attorney will be essentially the same as

that required in other grant applications. By Rule 716(2) the application is in Form 112. The

executed Power of Attorney must be in Form 111 [Rule 716(1)] and the application must be

verified by affidavit in Form 113 [Rule 716(3)].

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 29 Wills and Estates – Estate Administration

C. MATTERS CONCURRENT WITH THE APPLICATION

1. Notify the Beneficiaries

All beneficiaries who have not yet been notified should now be advised as to their interest in the

estate. For residual beneficiaries a copy of the Will and a copy of the Schedule of Assets should

be provided. Again, beneficiaries should be warned as to the possible time delays in the

distribution of the estate.

2. Advertising for Creditors

Sections 32 and 33 of the Administration of Estates Act state: “32(1) Subject to subsection (3), an executor or administrator may cause a notice to claimants in the form prescribed in the rules of court to be published once a week for two successive weeks in a newspaper described in subsection (2).

(2) A notice mentioned in subsection(1) is to be placed in : (a) the newspaper published nearest to the last residence of the deceased; or (b) any other newspaper designated by the court on an ex parte application by the executor or administrator.

(3) By an order that may be obtained on an ex parte application, a judge may dispense with publication of the notice in the case of: (a) an original grant of letters of probate or letters of administration, where the value of the estate does not exceed $5,000; or (b) letters probate, letters of administration or other legal documents purporting to be of the same nature that are duly resealed in Saskatchewan.

33(1) At the expiration of the time fixed in the notice mentioned in subsection 32(1), the executor or administrator may, unless otherwise ordered, distribute the assets of the deceased, or any part of the assets of the deceased among the persons entitled to them, having regard only to the claims of which the executor or administrator then has notice.

(2) An executor or administrator who distributes assets pursuant to subsection (1) is not liable for the assets so distributed to a person of whose claim the executor or administrator did not have notice at the time of distribution.

(3) Nothing in this section prejudices the right of a claimant to follow the assets into the hands of the person who receives them.”

According to Rule 736 the Notice to Creditors must be in a Form 122.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

30 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

As is evident from a reading of sections 32 and 33 of the Administration of Estates Act, the

principal purpose in advertising for creditors and other claimants is to protect the

executor/administrator from claims which appear after distribution has taken place. If

advertising for creditors has been properly undertaken, then the executor/administrator has no

liability to pay those creditors who appear after all of the assets have been distributed. Without

advertising for creditors, the executor/administrator can be held personally liable if any creditors

later appear, and there are insufficient assets to pay those debts.

There are also those practitioners who feel the wording of the sections is broad enough to protect

the executor or administrator from all types of claimants, for example, the illegitimate child of

whom no one was aware.

As with the Tax Clearance Certificate, it may be that where the executor or administrator is also

the sole beneficiary, he may decide to dispense with advertising for creditors, as it will no make

no difference whether he later pays creditors in his capacity as executor/administrator or as a

beneficiary.

There is some dispute among lawyers as to the appropriate time for advertising. Some feel that

advertising should never take place until after the grant is received, as the administrator, in

particular, has no authority to act until that time. Others, however, feel that no such restrictions

appear in the sections and will begin advertising concurrently with submission of the application

for the grant.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 31 Wills and Estates – Estate Administration

III. CALLING IN THE ASSETS AND THE PAYMENT OF DEBTS

A. TRANSMISSION OF THE ASSETS

Once Letters Probate or Letters of Administration have been obtained, the process of

transmitting the assets from the name of the deceased into the name of the executor or

administration can begin. For some assets, such as bank accounts, this will be as simple as

requesting the closure of the account or the transfer of the funds into an estate account. For other

assets, such as land, the preparation of formal transmission documents is required. Once all of

the assets have been transmitted (that is, reduced into the possession of the executor or

administrator), then the estate will be in the position of being able to complete the transfer of the

assets to the beneficiaries as it is required.

It would appear from the wording of Tariff Schedule I “C” that transmission of title to the

personal representative is one of the duties of the estate solicitor.

The checklist in the materials lists some of the most common assets, and the methods of their

transmission. On some occasions, for example, where the executor/administrator is the sole

beneficiary, transmission and transfer to the beneficiary may take place at the same time. Also,

the transmission and transfer of share certificates often occurs at the same time. Sometimes the

executor/administrator or the solicitor may choose to delay transmission until such time as the

estate is also in a position to transfer. However, in many circumstances there will be a lapse of

time between transmission and transfer.

Revised August 2004 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

32 Saskatchewan: Bar Admission Program Wills and Estates – Estate Administration

B. INVESTMENT OF ESTATE FUNDS

The lapse of time between transmission and transfer, or the nature of the estate itself, will

generally require that estate funds be invested until the time of distribution. The power of an

executor/administrator to invest arises from two different sources. First, there is a Will (where a

Will is involved). A testator may give any directions, discretions or powers to an executor to

invest as the testator sees fit. The executor may be limited in the types of permitted investments,

or may be given a complete discretion as to the types of permitted investments.

In addition, there are the investment powers given to executors/administrators under the

Trustee Act. If the Will does not stipulate the powers of investment, or if there is no Will, the

executor/administrator will be limited to investing in only those securities and in that manner

permitted under the Trustee Act.

Sometimes the solicitor will undertake to handle the matter of investment for the

executor/administrator. However, the solicitor must realize the power of investment is a

discretion which cannot be delegated. Therefore, while the solicitor may assist the

executor/administrator by advising what investment alternatives are available pursuant to the

Will and legislation and by assisting with the administrative details of investment, it is the

executor or administrator who must make the decision as to where and how the funds are to be

invested.

C. PAYMENT OF DEBTS

For most estates, there will be sufficient personal property in the residue that very little

consideration has to be given as to how the debts are to be paid. However, in those estates where

there is insufficient personal property in the residue to pay all the debts and any general or

specific legacies which have been given, then some thought must be given as to the order in

which assets will be used to pay the debts. This is called “marshalling the assets”.

Revised 2000 Not to be used or reproduced without permission – Saskatchewan Legal Education Society Inc.

Saskatchewan: Bar Admission Program 33 Wills and Estates – Estate Administration

Saskatchewan has very little case law which speaks to the marshalling of assets. There is no

current statute law which governs marshalling, and therefore Saskatchewan is governed by the

old English common law on this matter. Care must be taken in research, however, as the order

of marshalling was varied in England in 1925.