equilibrium effects of pay transparency · equilibrium effects of pay transparency ... d47, d83,...

TRANSCRIPT

EQUILIBRIUM EFFECTS OF PAY

TRANSPARENCY∗

Zoe B. Cullen and Bobak Pakzad-Hurson

September 12, 2017

Click For Latest Version

The public conversation about increasing pay transparency largely ignores equilibrium effects,namely how it leads firms to change hiring and wage-setting policies and workers to adjust bar-gaining strategies. In this paper, we study these effects with a methodologically diverse approach.Our analysis combines longitudinal study of thousands of workers and employers facing differentlevels of pay transparency carrying out short term contract work, matched through an online la-bor platform, with a parsimonious equilibrium model of dynamic wage setting and negotiation.We find, theoretically and empirically, that increasing pay transparency can increase employment,decrease inequality in earnings, and shift surplus away from workers and toward their employer.Intermediate levels of pay transparency, achieved through a permissive environment to discuss rel-ative pay, can exacerbate the gender pay gap by virtue of network effects. External interventionmay be necessary to maintain a desirable level of transparency. We also conduct a field experimenton internet workers to investigate an alternative model in which wage compression is driven bysocial aversion to observed wage inequality. Our findings are consistent with our bargaining modelbut not with this alternative.

Keywords: Pay Transparency, Online Labor Market, Dynamic Bargaining, Field Experiment

JEL Classification Codes: C78, C93, D47, D83, J21, J33, J78, L22

∗We are very grateful for guidance from Susan Athey, Nick Bloom, Matt Jackson, Fuhito Kojima, EdLazear, Luigi Pistaferri, and Al Roth. We are indebted to James Flynn for technical support. We alsothank Mohammad Akbarpour, Jose Maria Barrero, Doug Bernheim, Eric Budish, Gabriel Carrol, ArunChandrasekhar, Isa Chaves, Bo Cowgill, Piotr Dworczak, Jack Fanning, Chiara Farronato, Bob Hall, Gre-gor Jarosch, Scott Kominers, Maciej Kotowski, Jon Levin, Shengwu Li, Erik Madsen, Davide Malacrino,Alejandro Martinez, Paul Milgrom, Muriel Niederle, Kareen Rozen, Ilya Segal, Isaac Sorkin, Jesse Shapiro,Takuo Sugaya, Emmanuel Vespa, Alistair Wilson, and various seminar attendees for helpful comments andsuggestions. We appreciate TaskRabbit for providing essential data access. Pakzad-Hurson acknowledgesfinancial support by the B.F. Haley and E.S. Shaw Dissertation Fellowship through a grant to the StanfordInstitute for Economic Policy Research. This paper subsumes two earlier drafts: Equal Pay for UnequalWork? and Is Pay Transparency a Good Idea?.

I. Introduction

Recent policy proposals to mitigate wage inequality include increasing pay transparency,

the amount of information workers have about each others wages.1 In many settings, the

first step has been to protect the right of co-workers to communicate pay information and

extend the time frame during which information from peers is permissible as court evidence

of pay discrimination. Following the signing of the 2009 Lilly Ledbetter Fair Pay Act, which

removed the statute of limitation for pay discrimination law suits, the federal government

has prohibited federal contractors from punishing workers who discuss pay at the workplace,

and several states have passed similar laws (including California and Massachusetts in 2016).

The stated purpose of these laws is to ensure that “victims of pay discrimination can effec-

tively challenge unequal pay” through negotiations, by informing them of their employer’s

willingness to pay for labor.2

However, the debate around pay transparency has paid little attention to equilibrium

effects, namely how firms might change their hiring and wage-setting policies in reaction to

transparency mandates and how workers might adjust their initial salary negotiations. It

also lacks a theory as to why some firms institute transparent pay structures in the absence

of any mandate at all. Our research aims to fill this void.

In this paper, we combine empirical analysis of local contract workers and their employers

over a four year horizon with a simple equilibrium model of dynamic wage negotiations

tailored to our empirical setting.

Workers and employers in our sample find each other and transact over an online platform,

TaskRabbit, which specializes in homogeneous, low-skill household tasks, and is active in 19

U.S. cities. The labor platform requires workers to bid for tasks but also allows for on-

the-job wage renegotiation leading employers to increase worker pay above the initial bids

through the platform. Our administrative data allows us to observe all bids, final wages, job

characteristics, and worker evaluations between 2010 and 2014.

The advent of large online spot markets for labor, like TaskRabbit, presents new oppor-

1The rise of wage inequality in the United States has been well documented (egs. Katz and Autor, 1999;Saez and Zucman, 2014; Piketty, 2014). Wage inequality has been linked to social and economic costs, suchas under-investment in human capital, misallocation of labor, and even infant mortality (Chen et al., 2014).Citing these economic and social costs, the Equal Pay Act of 1963 and subsequent legislation has increasinglymade it illegal for firms to pay workers based on factors other than performance.

These measures have not had the desired effect. In a well-cited statistic on wage inequality, full-timeworking American women currently earn on average 79% of what their male counterparts make (Blau andKahn, 2017). The gap is even larger for minority women. This is especially puzzling given convergence ineducational attainment. Indeed, the “unexplained” wage gap – the premium that cannot be explained aftercontrolling for observables – is approximately 8%, which is the highest it has been since the wage gap hasbeen noted in modern times (Blau and Kahn, 2017; Goldin, 2014).

2https://www.whitehouse.gov/blog/2009/01/25/now-comes-lilly-ledbetter accessed 11/7/2016.

1

tunities for the study of the wage determination process in an environment largely stripped

of career concerns and non-pecuniary benefits. In our empirical setting, pay transparency

varies by the ability of co-workers to communicate about pay on-the-job and by salary

announcements in the job posting. For example, in some multi-worker jobs, workers are

co-located packing boxes in the same office where they might share wage information, and

in others they are physically separated distributing marketing materials to different vendors

and are therefore unable to share information about their pay. Some employers choose to

use a transparent posted price to advertise their job, and others accept private bids from

interested workers.3

We assess the equilibrium costs and benefits of increasing pay transparency along three

dimensions: wage equality, employment rate, and profit split between workers and their

firm. We find that increasing transparency compresses the wages of similarly productive

workers. Some transparency increases employment, but too much reduces employment.

Higher transparency shifts expected surplus away from workers and toward the firm. We

also find that regulation may be necessary to ensure desirable transparency levels.

To support these claims, we propose and analyze a simple model of dynamic wage ne-

gotiations with three important bases: workers do not initially know their value to their

employer, workers are able to renegotiate their pay, and workers know how much they can

successfully demand in renegotiations upon learning the wages of their peers. Many specifics

of our model are based on institutional details of TaskRabbit (which we discuss in more

detail in Section IV.), nevertheless, its simplicity allows for many generalizations and ex-

tensions which preserve our main findings. While it is unfeasible to precisely describe every

market in a single paper, we believe that different formulations of our model may be good

approximations of some entry-level labor markets.

Formally, we study a continuous time game between a continuum of workers and a

firm(s).4 Bargaining takes the form of a directed take-it-or-leave-it (TIOLI) offer from a

worker to the firm, as in TaskRabbit, and akin to a phenomenon in the general labor market

where workers are asked to put forth their salary expectations to assess whether a match is

within the realm of possibilities. Employed workers are able to renegotiate with the firm

at will, but workers whose offers are rejected are permanently unmatched with the firm and

receive their heterogeneous, exogenous outside options.5 The level of pay transparency af-

3Wage bargaining and transfer of information via transparency are common in many labor markets.Hall and Krueger (2012) find that one-third of workers surveyed explicitly bargain when accepting a job,one-third face posted wages set by their employers, and nearly one-half report that previous wages were usedto set current wages. We observe both types of wage-setting, in similar proportions, in TaskRabbit.

4For simplicity, we present our model as containing a single firm. We generalize and extend our resultsto the case with multiple firms in Appendix D..

5Farrell and Greig (2016) find that online labor platform users earn on average one-third of their totalincome on platform, leading to heterogeneous outside options.

2

fects the rate at which information about co-worker pay arrives over time to employees. The

firm has a value for labor which is common across workers, but unknown to the workers.6

Therefore, seeing the pay of a higher paid co-worker is an indication of being underpaid.

We study the unique equilibrium in which the maximum wage offer a firm is willing to

accept is a linear function of its value for labor. In it, workers initially bid linear premia

over their outside options. Regardless of the level of transparency, workers will only choose

to renegotiate their wage once they learn the wage profile within the firm, at which point

in time they (successfully) demand pay that is equal to that of the highest earning worker.

Therefore, transparency causes an information externality; if a worker finds out that her

colleague receives a high wage, she will use this information to negotiate a higher wage for

herself. This affects the way that initial wages are set.

There are two major equilibrium effects of increasing transparency: a demand effect and

a supply effect. The demand effect reduces the firm’s willingness to pay for labor. Higher

transparency increases the chances of information spillovers over time across workers. As

such, the firm is able to commit to pay lower wages at the onset of the game. In equilibrium

with a fully secret pay structure (workers never learn the pay of their peers), the firm accepts

all wage offers that are less than the value of labor because there are no information spillovers.

With full transparency the firm chooses a posted wage below its value for labor that it pays

to all workers, analogously to a monopsonist maximizing its profits. The highest wage the

firm is willing to pay for labor is strictly decreasing in transparency.

With increased transparency, the supply effect dictates that workers are willing to work

at lower initial wages. The option value of waiting to renegotiate once more information

arrives is increasing in the level of transparency, and the premium a worker asks for over

her outside option in her initial negotiation is decreasing in the level of transparency and

converges to 0 in the limit of full transparency.

We first consider the effect of pay transparency on wage equality. Increasing pay trans-

parency initially (at the time of hiring) increases the wage gap between employed workers

with high and low outside options. The supply effect causes all workers to lower their initial

wage offers, but low outside option workers reduce initial offers more than workers with high

outside options. However, over time, each worker becomes more likely to receive wage in-

formation and negotiate for the highest wage the firm is willing to offer, equalizing workers’

earnings. This latter effect dominates the former in the long run, and so discounted lifetime

earnings are compressed as transparency increases.

The combination of supply and demand effects lead to a non-monotonic overall effect

of increasing transparency on expected employment level. When transparency is low, the

6We discuss in Section II. how the analysis is unchanged if we instead assume that workers have differentproductivities but know relative productivity differences.

3

supply effect dominates, leading fewer workers to over-negotiate and be rejected by the firm.

However, increasing transparency beyond a point means that the demand effect dominates,

causing the firm to reduce the highest wage it offers faster than workers reduce their initial

offers. We show that the expected employment level is concave in transparency, meaning

that either full secrecy or full transparency is expected employment minimizing. An inter-

mediate level of transparency, in which workers learn wage information after joining the firm,

maximizes expected employment. This maximizer is falling in both the expected value of

labor and the expectation of worker outside options. We also show that a higher level of

transparency raises the employment level relatively more when the value of labor is lower.

Pay transparency also changes the division of surplus between workers and the firm. The

combination of firm commitment to paying a lower maximum wage and more conservative

initial bargaining by workers shifts bargaining power away from workers and toward the

firm. Under full secrecy workers never renegotiate in equilibrium. Therefore, negotiations

involve workers making only an initial offer to the firm, maximizing their expected surplus.

On the other hand, the equilibrium outcome under full transparency is equivalent to the

firm selecting the optimal posted wage. Despite not changing the bargaining protocol, full

transparency actually shifts the de facto bargaining power to the firm by allowing it to

effectively make a TIOLI offer to workers, maximizing its expected profits. We find that this

intuition holds for intermediate levels of transparency as well; increasing pay transparency

increases ex-ante firm profit while decreasing ex-ante worker surplus.

A policy maker can select an “optimal” ex-ante level of pay transparency, by weighing

these three criteria: pay equality, employment level, and the division of surplus between the

firm and workers. However, the firm may be able to exert some control over information

spillovers on site. A firm also has access to more information about its own value of labor

than a policy maker. Because of this information asymmetry, it is not inconceivable that the

firm could endogenously choose a profit maximizing level of transparency in a manner that

improves upon the social planner’s objectives as well.

We turn our attention to the objective of the firm to maximize profits, and identify

the level of transparency selected by the firm in the absence of regulation. Because the

profitability of transparency is a function of the firm’s value of labor, the firm’s choice

of transparency signals the firm value to workers, which in turn affects their negotiation

tactics, leading to a unique equilibrium outcome in which the firm pools on full transparency

regardless of its value of labor. The reasoning for this is unraveling. In any alternative

scheme, the lowest value firm type that selects pay secrecy earns zero profits, as workers will

always offer no less than this firm type’s value for labor in their initial negotiations. This firm

type could deviate to full transparency, and post a price below its value to make positive

profits, but this would result in a new “lowest value firm type” that receives zero profits

4

when is adheres to equilibrium strategies. This logic unravels toward the firm choosing full

transparency for any value.

We use unique back-end data from TaskRabbit from 2010 to 2014 to test our model

predictions and study the importance of phenomenon outside our model. We observe all

transactions on this platform over this time period, as well as job postings, worker bids,

on-the-job bonuses, employer ratings of workers, worker and employer demographics, and

cancellations. TaskRabbit staggered its entrance into metropolitan areas, allowing us to

analyze the evolution of multiple marketplaces starting from their origin. The dynamics of

these labor markets offers a novel window into equilibrium outcomes.

Pay transparency is affected by communication channels on-the-job, such as the co-

location of workers, and salary descriptions in the job posting. Employers are also able to

endogenously opt into full transparency by posting a price publicly in the job listing.

We conduct a field experiment in which we randomize pay transparency between co-

workers.7 We hire 347 “managers” and 1047 “workers” from an online labor market who are

tasked with negotiating wages for a real-effort task. We vary transparency by restricting wage

negotiations to either a common chat room containing a manager and multiple workers, or

separate each worker into her own chat room. The experiment relies on free-form bargaining

between workers and managers, which differs from the bargaining protocol in TaskRabbit.

The added control we have in this experiment allows us to directly measure worker outside

options, productivity, and employer profits. It also lets us explore additional measures of

interest, for example, compression in worker surplus in addition to compression in earnings.

We find the following in our empirical analysis, both in TaskRabbit and our field exper-

iment, which are consistent with the predictions of our model.

Pay equity: TaskRabbit jobs with partial pay transparency induced by worker co-location

result in final pay that is approximately two-thirds as dispersed than in jobs that are

otherwise similar, but in which wages are less transparent due to worker separation.

An illuminating observation is that the distance between workers’ initial contracts, or

the extent of inequality between initial bids, does not predict whether the employer

will make adjustments to pay to reduce disparities. However, conditional on adjusting

pay, the amount almost always closes the full distance between co-worker bids. These

facts confirm key predictions of our bargaining model, and together they distinguish

our model of re-bargaining from alternative models of social concerns as an explanation

for compressed wages.

We find in our experiment that pay is nearly always equalized when workers negotiate

in a transparent, common chat room, and rarely done so under secrecy.

7Additional details, including the code used to run the experiment, can be found on our academicwebsites.

5

Employment: On average, the match rate is higher among jobs with transparent prices

embedded in the job posting. We show that as employer household income falls (a

proxy for willingness to pay for labor in this marketplace for chores), the employment

gains from higher transparency rise.

In our experimental setting, we vary the marginal value of labor for the employer

directly and confirm that transparency has a larger positive impact on the hiring rate

when employers’ value for labor is high.

Profit sharing: While we cannot directly observe the profits of employers, we do observe

the wage bill and the match rate of tasks. Under transparent pay, holding constant

other job factors, the total wage bill is approximately 10% lower with no change in the

likelihood of completing a job.

We directly observe profits rise by 50% in our experiment when negotiations are moved

from an environment of pay secrecy to one of full transparency.

Endogenous transparency: The labor platform staggered entry into metropolitan areas

across America and we observe a striking linear progression toward transparent posted

wages month-over-month across all markets; for every month on the platform, the

fraction of jobs using a transparent posted price in a city increases by 1%. This trend

is not explained by the changing composition of jobs or employers on the platform,

nor do we find it to be consistent with stories of employer learning. This dynamic

unraveling is consistent with the unraveling result from our theory.

We combine theory and empirics to run a horse race between our model and a competing

theory of social costs of pay inequality. If workers face a morale cost after learning they

are underpaid, resulting in low effort, proactive employers may increase the wages of these

workers to recuperate high effort.

To assess the impact of morale we build endogenous effort and the morale cost specifica-

tion of Breza et al. (2016) into our model. Theoretically, only very extreme and discontinuous

morale cost functions could replicate our empirical finding that renegotiation does not depend

on the extent of the wage gap, but conditional on renegotiating, wages are equalized–pay

equalization can only be explained within a model including morale costs if workers quit the

job (expend 0 effort) upon finding out they are paid even small amounts less than a peer.

This is inconsistent with the findings of our field experiment.

Finally, we consider the effects of worker heterogeneity along gender lines. We find that

women have outside options that are 9.7% lower than those of men. We find that the

gender pay gap caused by this difference in outside options is mitigated with higher levels

of transparency. However, we also find evidence of network effects within jobs; men are

6

more likely to receive bonuses than women when there are communication channels between

workers, even within a job, and jobs with more men result in more bonuses overall. One

explanation for this is that men are more likely to discuss their wages than women, which we

support with survey evidence. We nest these network differences between men and women

into our model and show that intermediate levels of transparency can lead to very different

arrival rates of wage information for men and women, potentially increasing the gender way

gap. Even with these additions, approaching full transparency levels the playing field on

this front and equalizes wages. This evidence may be of interest to proponents of open

communication channels about pay within firms as a way to mitigate the gender pay gap.

I.A. Related Literature

At the heart of our paper is the notion that wages may be tied to factors unrelated to

productivity. Frank (1984) is an early paper that demonstrates this claim, and there has

been a wide literature investigating why this may be. Burdett and Mortensen (1998), Postel-

Vinay and Robin (2002), Postel-Vinay and Robin (2006), Cahuc et al. (2006), and Bagger

et al. (2014) explain wage dispersion using search models: similar workers naturally receive

different job offers over time due to randomness. Those who luck into better offers benefit

compared to their unlucky peers. Therefore, wage dispersion in these models is endogenous

to the arrival process of offers. Bewley (1999), Abowd et al. (1999), and, more recently, Song

et al. (2016) show that wages within firms are compressed relative to the wages across firms.

We endogenize wage-setting through the bargaining process between worker and employer. In

doing so, we microfound wage compression–transparency increases the cost of pay inequality

within a firm as workers will be able to use this information to negotiate higher wages. We

observe significant heterogeneity in the distribution of wages across employers in our data set,

which we attribute to exogenous and endogenous differences in bargaining across different

employment settings.

There is also an empirical literature on the effects of pay transparency. This literature

builds on the fair wage-effort hypothesis introduced to economics by Akerlof and Yellen

(1990) which posits a morale cost and associated reduction of effort when a worker believes

she is underpaid. Card et al. (2012), Mas (2016a), Mas (2016b) Perez-Truglia (2016), and

Breza et al. (2016) conduct field and natural experiments on transparency, and document

worker dissatisfaction upon learning of peers with higher pay. Charness and Kuhn (2004),

(2007) investigate similar claims in laboratory settings. Nevertheless, these papers do not

explicitly investigate how (if at all) workers use information of higher paid co-workers to

negotiate higher wages for themselves. We find evidence of this morale effect in a field

experiment, but by combining our empirical findings with theory, we show that the observed

wage compression is more consistent with a bargaining mechanism than a morale mechanism.

7

Economists have long studied bargaining, and including a comprehensive review of this

literature is infeasible. Our paper most closely relates to the double auction literature be-

ginning with a well-known paper by Chatterjee and Samuelson (1983). In this model, a

buyer and a seller have private values for a particular good. Both agents simultaneously

place bids, and if the bid of the buyer is higher than that of the seller, the two exchange

the good at a price that is a predetermined convex combination of the two bids. Williams

(1987), Satterthwaite and Williams (1989), and Leininger et al. (1989) further examine the

equilibria of the double auction game. Radner and Schotter (1989) conduct an experimental

study to determine the focality of linear equilibria. The study of simple double auctions

stagnated partially because it was determined by Satterthwaite and Williams (1989) that

double auctions are generally inefficient means of bargaining within the space of all bargain-

ing mechanisms. Although the double auction model is a static bargaining game, we show

a connection to the equilibria of our dynamic game. Therefore, double auctions appear to

be a compact representation of a natural bargaining situation, and maximizing desirable

properties within the realm of double auctions may be relevant to policy creation. Our main

results are related to answering this type of question.

There is also a large, recent literature on the effects of transparency in dynamic markets.

Horner and Vieille (2009), Fuchs et al. (2016), and Kim (2017) study the efficiency effects

of price transparency in sales markets with asymmetric information. Kaya and Liu (2015)

investigates the role of transparency on efficiency and division of surplus in a dynamic bar-

gaining environment. Asriyan et al. (2016) examine the equilibrium effects of transparency

when objects to be sold have correlated values, similarly to our model with a common value

of labor. Moellers et al. (2017) experimentally study the effects of open communication in a

dynamic bargaining environment with externalities.

Finally, as pay transparency is often aimed at closing the gender pay gap, our paper fits

in to the long literature on gender differences in economic environments. We find a similar

gender pay gap in TaskRabbit as in standard economic markets (Blau and Kahn, 2017;

Goldin, 2014). We also find network effects between men and women (as in Keister, 2014)

and differences in the likelihood of successful negotiation (as in Babcock and Laschever,

2003; Niederle and Vesterlund, 2007).

The remainder of the paper is organized in standard fashion. Section II. lays out our

theoretical model. Section III. presents our main theoretical findings. Section IV. describes

the TaskRabbit market and contains empirical tests of our main findings using TaskRabbit

data. Section V. discusses our field experiment and related findings. Section VI. examines an

alternative model based on the fair wage-effort hypothesis and morale costs associated with

pay transparency. Section VII. investigates heterogeneity of workers across gender lines, and

the effects of transparency on the gender pay gap. Section VIII. concludes. Omitted proofs,

8

regression tables, and extensions are contained in the Appendix.

II. Model

II.A. Preliminaries

Time is continuous, and is indexed by t ∈ R+. There is a single firm in the economy.8

At each time t, a ρ mass of workers enters the market, and existing workers exogenously

depart the market via a Poisson process with rate ρ. Each worker i has a private outside

option θi ∼ G[0, 1] i.i.d., which is the flow payment i receives when not matched to the firm.

Productivity of labor is v ∼ F [0, 1], which is common across workers, and is known only

to the firm.9 The firm faces a constant returns to scale production function, and receives a

flow surplus v from each employed worker. All agents discount the future at rate δ, are risk

neutral, and seek to maximize discounted expected flow payments. We assume that F and

G are C2 over the interior of their supports.

At t = 0 (and before any workers enter the market) the firm selects a maximum wage it is

willing to pay for a worker as a function w(v) ∈ [0, 1], where the choice of w is not immediately

observed by workers. Each worker bargains for wages by making take-it-or-leave-it (TIOLI)

offers to the firm at any point during her employment, potentially renegotiating infinitely

often. For simplicity of exposition, we require a worker to make an offer immediately upon

meeting with the firm. Two things can happen when a worker i makes a wage offer wi,t at

time t. If wi,t ≤ w then i receives a flow wage wi,t for all time periods t′> t until she departs

or attempts to renegotiate. If wi,t > w then i is permanently unmatched with the firm for

all time periods t′> t and consumes her outside option until she departs.

Let Wt denote the set of wages the firm pays to employed workers at time t, where

W0 ≡ {w}. We model transparency as a random arrival process; at time t matched workers

observe Wt according to an independent Poisson arrival process with rate λ ∈ [0,∞)∪{∞},where we take λ =∞ to mean that the process arrives at every time t.10

The timing of the stage game is as follows at each time t ≥ 0:

8We generalize our model to include multiple firms in Appendix D..9The assumption of a common v is made for ease of exposition. The analysis relies only on the assumption

that workers can observe their relative productivities. We could complicate the analysis by supposing eachworker has a known type τ ∈ T where T is some countable set. Let vτ ∼ F [0, 1] i.i.d. but unknown toworkers. The analysis is almost entirely unchanged, other than additional notation, with this modification.Similarly, we could allow for changes in (assessed) worker productivity as in Kahn and Lange (2016).

10For much of the paper, we abstract away from the genesis of this arrival process. It can be thought of asthe frequency with which there is an information leak, that existing workers see the offers of incoming workers,or wage gossip between workers. We discuss endogenous information arrival in Section VII.. Alternatively, ifworkers are not able to initiate renegoitation at will (e.g. workers have to wait for a scheduled performancereview to renegotiate), λ can be thought of as the rate at which workers both learn the wages of their peersand have the ability to renegotiate.

9

1. New workers enter the market and are matched with the firm.

2. Each matched worker i learns Wt independently with arrival rate λ.

3. Workers bargain according to the protocol laid out above.

4. Existing workers depart at rate ρ.

In Appendix B.1. we allow the firm to accept or reject each offer as it arrives, and show

that all of the results of this paper are unchanged (under a proper selection of “Markov”

equilibria). In Appendix D. we expand our model to allow workers to search for work between

multiple firms, and show that many results are robust to this extension. In Appendix E.

we discuss alternative bargaining protocols and show that our results are robust to these

settings.

II.B. Equilibrium Selection

We investigate pure strategy perfect Bayesian Equilibria of the game. We restrict our

attention to equilibria satisfying the following conditions:

A1 0 ≤ w ≤ v. Let w∗i be the initial wage offer of worker i during the first period she meets

the firm according to equilibrium strategies. If v ≤ w∗i for every worker i then w = v.

A2 θi ≤ w∗i ≤ 1. If there is no v such that θi ≤ w in equilibrium strategies then w∗i = θi.

A3 w and w∗i are strictly increasing and continuous functions of v and θi, respectively

A4 Off path, every worker i believes with probability 1 that w = θi until i learns all wages.

A5 If worker i re-negotiations at time t′> t then wi,t′ > wi,t.

A1 and A2 restrict actions for agents who never match in equilibrium, because either its

value for labor is too low (the firm) or her outside option is too high (a worker), ruling out

pathological equilibria in which, for example, w = 0 and all workers choose w∗i = 1.

A3 limits our study to continuous equilibria, and removes equilibria in which workers

and the firm pool on a predetermined wage from consideration.11

A4 pins down off-path beliefs. If an unanticipated offer is accepted, the worker believes

she is extremely lucky and is receiving the highest possible wage until she is presented with

evidence to the contrary. These are the most favorable beliefs to the firm allowable in a

PBE, so any equilibrium sustainable under A4 is sustainable for any off-path beliefs.

11Leininger et al. (1989) suggest similarities between the set of continuous equilibria and a set of discon-tinuous equilibria of a game similar to our own, and so we do not believe this to be a conceptually limitingconstraint. We discuss this similarity in Section II.D..

10

A5 rules out a multiplicity of essentially equivalent equilibria by preventing a worker

from “renegotiating” infinitely often by just offer the same wage over and over again.

II.C. How do workers renegotiate?

Workers learn the wages of their co-workers over time and are able to initiate bargaining

infinitely often if they wish. There is reason for concern in dynamic relationships of a

“ratchet effect” (Weitzman, 1980) – that successful negotiation will lead to an increased

desire on the part of workers to initiate bargaining in future periods. We find, however, that

in equilibrium, a worker will only negotiate at most twice:

Proposition 1. In equilibrium workers only negotiate wages in the first instant they are

hired and the first instant they receive information about wages of co-workers. Upon renego-

tiating, workers offer and receive w.

The intuition for this result is that workers do not learn about v (and hence do not learn

about w) if their offer is accepted. Any worker strategy that says “offer w when initially hired

at time t and offer w′ > w at time t′ > t if I have not learned the wages of my co-workers”

cannot be optimal, because even if offering w′ at time t′ improves the expected utility of the

worker, she would have been better off asking for w′ at time t as w is fixed over time.12

Due to the continuum of workers entering the market at each time, in addition to our

equilibrium selection criteria, workers trace out the entire set [0, 1] with their initial offers at

each time t. Therefore, the highest wage paid by the firm is w for all t ≥ 0. As a result, the

maximum wage that any worker observes upon information arrival is w. Clearly, a worker

will then demand this amount from the firm.

II.D. Equilibrium conditions

Given that workers negotiate at most twice in equilibrium, we are able to use standard

techniques to solve for the optimal bargaining strategies of agents. Letting F (x) = P (w ≤ x),

for all λ <∞ worker i negotiates at the first moment she is hired to:

argmaxw∗i

(w∗i

ρ+ δ + λ+

λ

ρ+ δ + λ

E (w|w ≥ w∗i )

δ + ρ

)(1− F (w∗i )

)+

θiδ + ρ

F (w∗i ) (1)

where the first term represents the expected discounted wage the worker receives, given

the arrival rate of information, if matched with the firm. The second term represents the

lifetime earnings of the worker if she exceeds w and instead consumes her outside option for

12This reasoning is shared in Tirole (2016).

11

her lifetime. When λ = ∞, the pricing scheme is a posted price in which all workers can

elect to make an offer w∗i = w or unmatch with the firm.

In a series of steps (shown in Appendix B.2.), we modify the objective function without

affecting the maximizer, and show that this is equivalent to solving:

argmaxw∗i

1ˆ

w∗i

((1− Λ)w∗i + Λx− θi) f(x)dx (2)

where Λ = λρ+δ+λ

for all λ ∈ [0,∞) and Λ ≡ 1 for λ =∞. For λ <∞ the firm solves:

argmaxw

´ w0

(v − y) g(y)dy

ρ+ δ + λ+ G(w)

λ

ρ+ δ + λ

1

ρ+ δ(v − w) (3)

where G(x) = P (w∗i ≤ x). The first term gives the total discounted profits made by the firm

given the arrival rate of information and the second term is the profit made from workers

after renegotiating their wages to w over the rest of their lifetimes in the firm. When λ =∞the firm will hire every worker i with θi ≤ w at a constant wage w. We can similarly

manipulate the objective as with the worker problem:

argmaxw

w

0

(v − (1− Λ) y − Λw) g(y)dy (4)

These manipulations collapse the set of equilibria of our problem into that of the well-

known Chatterjee and Samuelson (1983) “double auction” in which a seller (worker) with

a private value for a good (θi) and a buyer (firm) with a private value for a good (v)

submit sealed bids. If the bid of the buyer is at least as large as that of the seller, the

good switches hands at a price set be a predetermined convex combination of the two bids

(determined by Λ). The first order conditions for workers and the firm are, respectively:

w∗i − θi = (1− Λ)1− F (w∗i )

f(w∗i )(5)

v − w = ΛG(w)

g(w). (6)

We know from Satterthwaite and Williams (1989) that the set of equilibria corresponds

to solutions of the first order equations for distributions F and G with strictly increasing

virtual values, i.e. θ+ G(θ)g(θ)

is strictly increasing in θ and v− 1−F (v)f(v)

is strictly increasing in v.

12

II.E. Solving for equilibrium

The optimal bidding and wage setting policies of the firms and workers are interdepen-

dent; workers decide how aggressively to bid depending on how the firm sets w, while the

firm sets w as a function of how aggressively the workers bid. Satterthwaite and Williams

(1989) show that there exists a continuum of equilibria satisfying Equations 5 and 6. Our set

lacks natural ordering, limiting the possibility for general claims about the entire set of equi-

libria, but we build from experimental evidence in Radner and Schotter (1989) suggesting

that equilibria in which w∗i and w are linear functions of θi and v, are focal and most likely

to be equilibria outcomes in practice. We produce similar evidence in a setting similar to

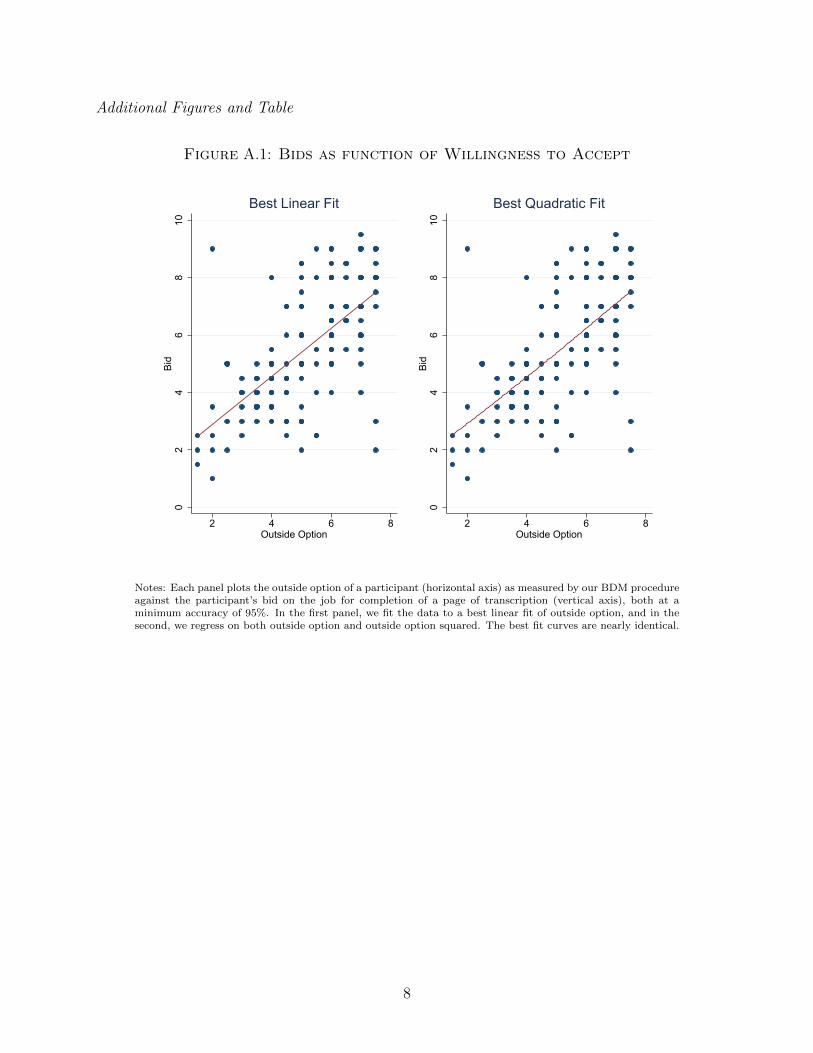

TaskRabbit in Figure A.1. Therefore, we focus our analysis on linear equilibria, and restrict

attention to a two parameter family of power law distributions of worker outside options and

firm values, which we show admit a unique linear equilibrium.13 We then study the proper-

ties of this equilibrium, and analyze the effects of transparency. The class of distributions

we study are:

F (v) = 1− (1− v)r, r > 0

G(θ) = θs, s > 0(7)

As r increases, v is on average lower and as s increases, θ is on average higher. Therefore,

increasing r or s reduces the average benefits from employment. We define a linear equilib-

rium below and show that distributions of this type admit a unique linear equilibrium.

Definition 1. A linear equilibrium is a pure strategy perfect Bayesian equilibrium satisfying

A1-5, where w is a linear function of v whenever a positive mass of workers offers w∗i ≤ v,

and where w∗i is a linear function of θi whenever there is positive probability that θi ≤ w.

Proposition 2. For any pair of distributions within the family described in Equation 7

there exists a unique linear equilibrium.

What can we say about the equilibrium bargaining strategies of workers and firms, and

how are they affected by transparency? First, equilibrium wages lie in an interval [a, h] ⊂[0, 1]. This means firm types with values below a will not hire any workers, and all workers

with outside options above h will remain unemployed. Second, we can see from Equations

5 and 6 that all workers and firm types with positive probability of matching in equilibrium

charge a premium, that is, v − w ≥ 0 and w∗i − θi ≥ 0. We show high outside option

workers and low value firm types face higher risks of being unmatched in equilibrium. As

13The approach of making parametric assumptions to ensure linear equilibrium is common. One recentexample on CEO pay is Edmans et al. (2016). Power law distributions are commonly observed in economicsituations such as ours, including worker income and firm productivities. See Gabaix (2009, 2016) for details.

13

a result, the markup charged by each worker is decreasing in θi and the markdown set

by the firm is increasing in v. We further show that both w and w∗i are decreasing in Λ;

with increased transparency the firm reduces the highest worker offer it accepts to avoid

information spillovers across workers (which we call the demand effect), and workers make

more conservative initial offers because with higher transparency the option value of waiting

to receive a high wage is increasing relative to the risk of securing a high initial wage (which

we call the supply effect). The following proposition formalizes these arguments.

Proposition 3.

1. v − w ≥ 0 and strictly increasing in v for all v ∈ [a, 1],

2. w∗i − θi ≥ 0 and strictly decreasing in θi for all θi ∈ [0, h],

3. w is strictly decreasing in Λ for all v ∈ [a, 1]. As Λ→ 0, w → v for all v ∈ [0, 1], and

4. w∗i is strictly decreasing in Λ for all θi ∈ [0, h]. As Λ→ 1, w∗i → θi for all θi ∈ [0, 1].

The decline of w in Λ is similar to the strategy of a monopsonist that optimally limits

demand. Due to the externality caused by transparency, the firm is able to commit to

reducing w, thus restricting the extensive margin of labor (the number of workers it hires)

while increasing the intensive margin (profit per worker hired). For clarification, consider

full secrecy (Λ = 0) and full transparency (Λ = 1). In the full secrecy case, there are no

information spillovers. Therefore, in the unique equilibrium the firm must set w = v,meaning

that the firm sets the highest acceptable wage equal to the marginal product of labor. In the

full transparency case, there are perfect information spillovers, and every worker learns the

wages of others within the firm at the instant they are hired. Since all workers will learn w

before their first negotiation, this is equivalent to posting a profit maximizing wage w given

a supply curve of labor (the distribution of outside options), which is the exact problem that

a traditional monopsonist faces. If the firm instead sets w = v as in the full secrecy case,

it would earn zero profits. We graphically represent the demand and supply effects in

Figure III as Λ increases.

III. Main results - Effects of transparency on equilibrium

We analyze the equilibrium effects of transparency along three dimensions: Does trans-

parency lead to pay equity? Does transparency increase employment? and Does trans-

parency benefit workers or firms?

III.A. Income Inequality

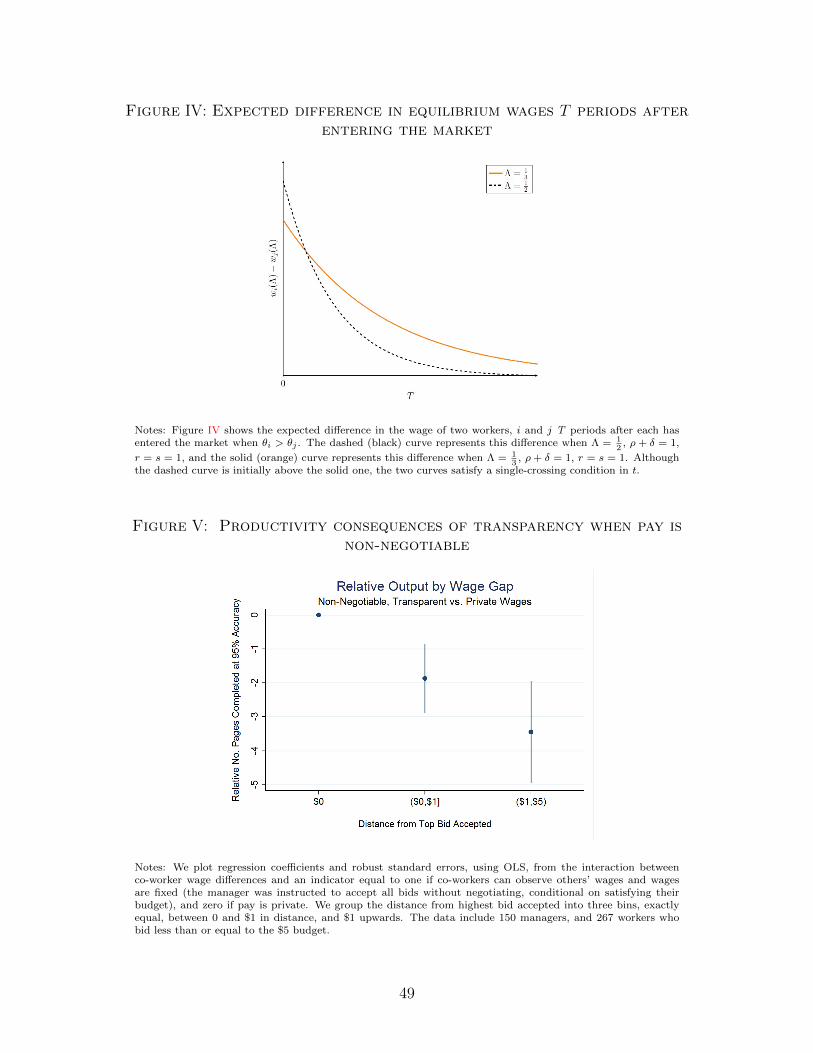

In our theoretical analysis of wage equalization we compare the lifetime earnings of work-

ers i and j who are hired by the firm under two transparency levels Λ′< Λ

′′so we do not

14

confound compression effects with employment effects.14 For any two workers i and j with

θi > θj who are hired under both Λ′

and Λ′′, there are two effects. First, as shown in Propo-

sition 3, the supply effect incentivizes agents to reduce initial wage offers. We show in

equilibrium, since j has a lower outside option than i, j reduces her initial offer more than

i. Figure III shows that the relative impact of the supply effect on w∗i is smaller the larger

θi is. Second, increasing transparency augments the rate both workers receive w, reducing

dispersion of their lifetime earnings as the raise to w is larger the smaller θi is. The first

effect increases the initial wage gap between i and j, however, we show that the latter effect

dominates in the long run, leading to more compressed expected lifetime earnings.15 We

document these two effects by plotting the expected difference in wages between workers i

and j over time and for different levels of transparency in Figure IV.

Theorem 1. Let θi > θj, 1 > Λ′′> Λ

′, and suppose workers i and j are both hired in

equilibrium under Λ′

and Λ′′.

1. The difference in initial offers w∗i − w∗j is higher under Λ′′

than Λ′, and

2. Let T (Λ, v, θk) be the equilibrium expected discounted lifetime earnings of a worker k

with outside option θk under transparency level Λ and firm value v conditional on k

being employed at the firm. Then T (Λ′′, v, θi)−T (Λ

′′, v, θj) < T (Λ

′, v, θi)−T (Λ

′, v, θj)

and T (Λ′′, v, θi)− T (Λ

′′, v, θj)→ 0 as Λ

′′ → 1.

Note that w∗i −w∗j = 0 and T (Λ′, v, θi)−T (Λ

′, v, θj) = 0 when Λ

′= 1. Wage equality may

be a reasonable notion of fairness when θi represents a worker’s outside option. However,

compression of expected surplus, that is, the difference between wage and θi, is another notion

of fairness which may be particularly relevant to consider in cases when θi represents the

flow cost a worker bears for completing the job.16 Does transparency lead to a compression

of expected surplus across workers? Simply put, the wage compression results in Theorem

14The restriction that workers be hired by the firm is necessary as we show in Theorem 2; increasingtransparency can increase employment, meaning that a previously unemployed, high outside option workermay find employment only when transparency is increased. To make this point concrete, take some smallε > 0 and consider increasing transparency from Λ

′to Λ

′′= Λ

′+ ε, such that more workers are employed

in equilibrium under Λ′′. In Appendix C. we show that w∗

i and w are continuous in Λ and so the expectedlifetime earnings of any worker j hired under both transparency regimes is barely affected by an ε increasein transparency. However, a worker i who over-negotiates at level Λ

′receives her outside option θi for her

entire lifetime, while if she manages to find employment at the firm under Λ′′

her average lifetime earningswill be greater than and bounded away from θi (as she always asks for a premium w∗

i − θi > 0). But notethat θi > θj , so the lifetime earnings of i and j are not compressed by increased transparency.

15This point is perhaps easiest to intuit in the context of a Samuelson Chatterjee double auction. Increas-ing Λ reduces the bargaining weight of workers, and therefore, the different bargaining positions of workerswith heterogeneous outside options make up a smaller proportion of their expected lifetime earnings.

16We show in Section VI. that the equilibrium outcome in a game in which all workers have an outsideoptions equal to zero and θi represents a flow cost to being employed is identical to that of the game presentedabove.

15

1 are reversed when we consider surplus compression as low θi workers are those who enjoy

the largest surplus when employment.

Corollary 1. Let θi > θj, 1 > Λ′′> Λ

′, and suppose workers i and j are both hired in

equilibrium under Λ′

and Λ′′.

1. The difference in initial surplus (w∗j − θj)− (w∗i − θi) is smaller under Λ′′

than Λ′

and

2. Let S(Λ, v, θk) be the equilibrium expected discounted lifetime surplus of a worker k

with outside option θk under transparency level Λ and firm value v conditional on k

being employed at the firm. Then S(Λ′′, v, θj)−S(Λ

′′, v, θi) > S(Λ

′, v, θj)−S(Λ

′, v, θi),

and S(Λ′′, v, θj)− S(Λ

′′, v, θi)→ θi−θj

ρ+δas Λ

′′ → 1.

III.B. Employment

Consider an increase in transparency from Λ to Λ′. In an abuse of notation, let wΛ denote

the maximum wage the firm pays and w∗i,Λ the initial offer of worker i for transparency level

Λ. The demand effect lowers employment as wΛ′ ≤ wΛ means that there are fewer workers

with θi ≤ wΛ′ who are eligible for employment. The supply effect increases employment

as w∗i,Λ′≤ w∗i,Λ for all i so fewer workers over-negotiate by initially offering w∗

i,Λ′> wΛ. As

such, increasing Λ neither obviously nor (necessarily) monotonically affects employment.

Theorem 2. Ex-ante equilibrium employment is concave in Λ and maximized at

Λ∗ =1− E(θ)

1 + E(v)− E(θ)(8)

and the ex-post employment maximizing level of transparency is weakly decreasing in v.17

We see several important effects of transparency on employment. First, an interior level

of transparency Λ ∈ (0, 1) maximizes employment. In fact, due to the concavity of the

employment in Λ either full secrecy or full transparency is employment minimizing.

Second, Λ∗ is decreasing in both E(v) and E(θ). Indeed, as E(v) converges to 0 full

transparency becomes close to employment maximizing, and as E(θ) converges to 1 full

secrecy becomes close to employment maximizing. For intuition, we return to Proposition 3.

As E(v) decreases, the firm’s markdown v−w is likely to be small regardless of Λ. Therefore,

increasing transparency does not greatly reduce the number of workers with θi < w. But by

increasing transparency, workers will shade down their initial offers w∗i , reducing the number

of workers who over-negotiate. Similarly, as E(θ) increases, most workers are offer small

17The expected match surplus is E(v)− E(θ), so Λ∗ =1−expected outside option1+expected match surplus

.

16

premia (w∗i − θi) regardless of Λ. The effect of increasing transparency does little to affect

these premia, but instead discourages the firm from setting a large markdown.

Third, both the ex-ante and ex-post optimal levels of transparency are in some sense

decreasing in v. We have already discussed how Λ∗ is strictly decreasing in E(v), and in-

creasing transparency is more beneficial for the employment level when v is small. Given

that workers’ initial offers are not affected by the realization of v (they do not observe it),

high transparency causes firms to reduce w more significantly when v is high, leading to

relatively less employment. Additionally, this comparative static on the ex-post employment

maximizing level of transparency also holds for the ex-post social surplus maximizing level

of transparency. In fact, the ex-post maximizer of employment also maximizes ex-post social

surplus; because each employed worker earns a wage weakly greater than her outside option,

in equilibrium each employed worker increases social surplus by v − θi > 0, implying that

social surplus is proportional to employment level. Therefore, increasing transparency is also

more beneficial from a social surplus perspective when v is small.

III.C. Profit share: who benefits from transparency?

Does increasing pay transparency increase worker or firm utility? In light of Theorem 2

we may suspect that the employment gains from increasing transparency could make both

parties better off. Nevertheless, perhaps counter intuitively, we find that increasing pay

transparency increases the expected profit of the firm while decreasing the expected welfare

of workers. Note that this statement is made ex-ante, before the realizations of v and θi.

Theorem 3. The ex-ante expected equilibrium profit of the firm is strictly increasing in Λ

and the ex-ante expected equilibrium profit of workers is strictly decreasing in Λ.

Although increasing Λ increases the rate at which workers receive wage w, it lowers both

w∗i and w in equilibrium. The overall effect is to shift de facto bargaining power to the firm,

benefiting the firm at the expense of workers. For clear intuition, consider the extreme cases

of full secrecy and full transparency. In the full secrecy equilibrium, each worker makes a

once-and-for-all offer to the firm. Under full transparency, the firm selects a single wage all

employed workers receive, essentially allowing it to make a once-and-for-all offer to workers.

The main result of Myerson (1981) implies that each party prefers to be the one making the

once-and-for-all offer to the other.

We do not view the shift of profit from workers to firm as an inherently good or bad

thing.18 However, there may be macro-level effects of changing the profit split that we

18Indeed, if we adopt the point-of-view that workers own the firm (perhaps in proportions that are notcorrelated with outside options) then the split of profit is likely not a first-order concern.

17

do not capture in our model. We point out this effect of pay transparency and leave its

consequences on other economic measures to future work.

III.D. Endogenous firm transparency choice

Until now, we have been studying the effects of increasing transparency ex-ante (before

seeing the draw of v) on employment, wage compression, and profit share. These results

give insights into the effects of governmental policy instituting pay transparency measures.

Although there has been recent state and federal action in the United States to increase pay

transparency, many industries remain unregulated. Without regulations, the firm can select

transparency to maximize its profits after seeing the draw of v. We do not allow workers to

directly observe the level of transparency selected by the firm,19 however, the results of this

section are not greatly changed if we instead assume workers can observe the selected level

of transparency.

In Example 1 in the appendix we show that full transparency is not the profit maximizing

(exogenous) level of transparency for every draw of v. Indeed, the profit maximizing level

of Λ is not even monotonic in v. Nevertheless, when firms are able to endogenously select

transparency, we find that the unique equilibrium that does not involve employed workers

renegotiating in the absence of learning the wages of their coworkers is one in which the

firm selects full transparency regardless of its draw of v. As wage negotiations are relatively

rare,20 we believe this to be a reasonable class of equilibria to consider. Our findings suggest

that in the absence of governmental regulation, observed levels of transparency may be very

different than employment maximizing levels.

Theorem 4. When the firm can privately select Λ as a function of v, there is an essentially

unique equilibrium outcome in which each no worker renegotiates in the absence of coworker

wage information on equilibrium path. In equilibrium, the firm selects Λ = 1 for all v > 0.

Because workers do not directly observe the selected Λ, each worker’s belief of the value

of Λ decreases continuously in the length of time since being hired without learning the

wages of coworkers. Because of this, workers will renegotiate their wages in the absence of

learning the wages of their coworkers. Therefore, we have ruled out any strategy in which

the firm selects any Λ ∈ (0, 1). Can it be the firm only selects from Λ ∈ {0, 1}? We show

that the firm cannot set Λ = 0 in equilibrium due to unraveling. To see this, let vL be the

infemum value for which the firm selects Λ = 0. Then upon arriving at the firm, all workers

will immediately deduce that the firm has chosen Λ = 0 since they do not initially observe

19It is likely to be viewed as cheap talk for an employer to say, “our firm has a high degree of transparency,so don’t worry, you’re likely to learn the wages of your coworkers very soon” at a job interview.

20Hall and Krueger (2012) find that about 70% of workers have not negotiated raises at their current jobs.

18

the wage profile of the firm. Workers will infer that the firm’s value is at least vL, and so

every worker will bid at least vL. As a result, when the value of the firm is (close to) vL it will

make (approximately) 0 profits unless it deviates to selecting Λ = 1. But if this firm type

deviates, there is a new “vL.” Inductively there cannot be an equilibrium in which there is

a positive measure of firm types playing Λ = 0. The equilibrium in which the firm selects

Λ = 1 for all v can be supported with the off-path beliefs that a deviating firm has value

v = 1 with probability 1. As w = v when Λ = 0, a deviating firm will make zero profits.

This result is particularly applicable to online labor markets in which employers can

only select from a coarse grid of transparency levels. In our data sample from TaskRabbit,

employers can either accepting bids or post a wage. In settings that do not allow workers to

otherwise gain wage information, accepting bids is equivalent to setting Λ = 0 and posting

a wage is akin to choosing Λ = 1. Here, the unraveling result holds without any caveats.

Corollary 2. When the firm can select Λ ∈ {0, 1} as a function of v there is an essentially

unique equilibrium outcome. In equilibrium, the firm selects Λ = 1 for all v > 0.

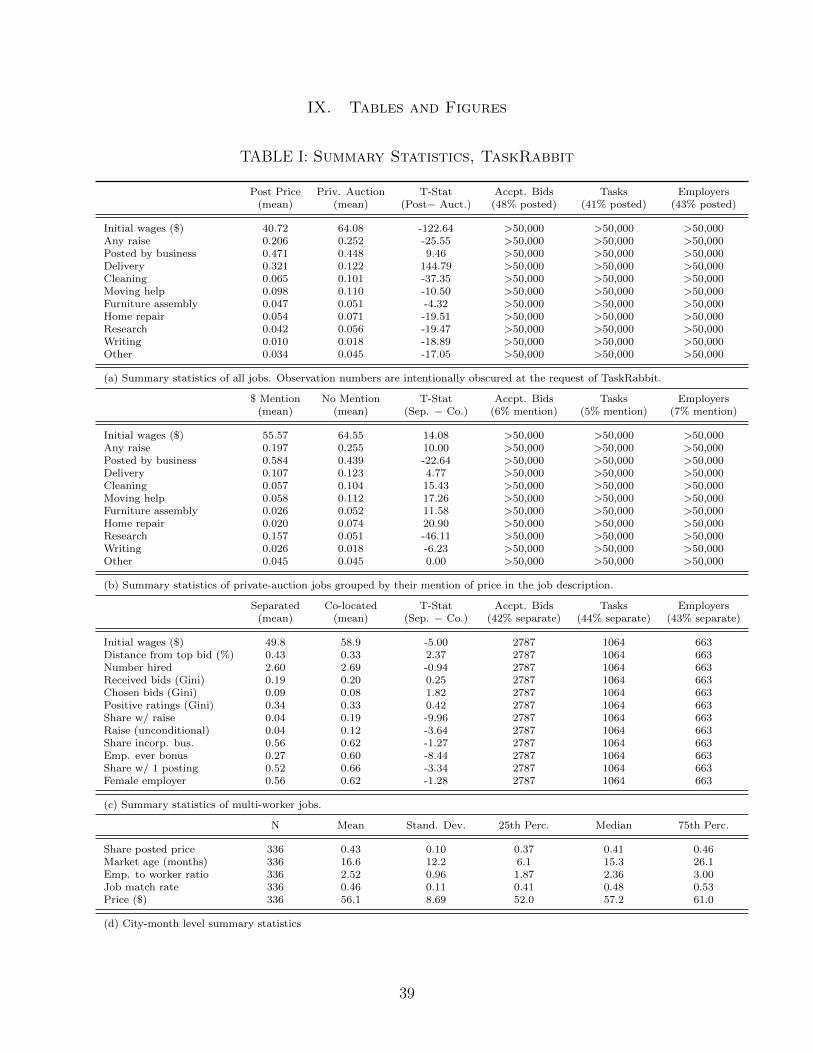

IV. Study I: Evidence from TaskRabbit

IV.A. Platform

We use administrative data from an online labor platform, TaskRabbit, between June

of 2010 and May of 2014. TaskRabbit differentiates itself from other online labor platforms

by specializing in local jobs, which account for 89% of jobs completed. The platform was

active in 19 U.S. metropolitan areas across the U.S. during this period. To participate in

the marketplace, workers must pass a criminal background check and cursory screening to

join the platform and employers must enter a valid credit card.

Our research concentrates on jobs that are posted as one-time tasks.21 Most jobs on

TaskRabbit do not require expertise, and as such, labor is relatively homogeneous and low-

skill. Employers can observe workers’ profiles, which include the number of prior jobs com-

pleted on the platform, a rating out of five stars and a short bio.

Employers post a description of the task, details about the exact location, number of

workers needed, frequency of task, and a deadline for completion. Workers search through

these postings and submit bids for the project. Alternatively, the employer can choose to

post a take-it-or-leave it price, and the first worker to accept is matched.

21We classify one-off tasks two ways. In the main specification we limit tasks to those the employerindicates as “non-repeating” when filling out the vacancy forms, and as a robustness check we include thesurvey responses of several thousand Mechanical Turk workers who read the job descriptions and answeredthe question, “what is the likelihood that a worker could be rehired for a similar job by this employer?”

19

IV.B. Bargaining Environment

Employers can elect to increase wages through the platform once the job is completed.

This allows for the possibility of on-the-job bargaining between worker and employer.

Once the job begins, several frictions make canceling costly for both parties. TaskRabbit

is a spot market designed for urgent tasks; conditional on completion, 97% of tasks are

finished within three days of posting. On average, the median job receives 1 offer in the

first hour per vacancy, and 1 every 4 hours over the first day. Taken altogether, finding a

replacement worker once the job began would likely result in costly delays.

Similarly, workers cannot costlessly transition to another job. Because these are in-person

tasks, we observe high travel costs relative to the final transaction price.22 At the time that

a worker is assigned a job, the worker and employer enter a contract that can be cancelled

by contacting the platform and providing a reason. TaskRabbit has a three strike rule.

After three cancellations a user will not be permitted to use the site again. About 8% of

assignments are canceled. During the window between when the match is made and the

job is complete, money is held in escrow and will be released to workers by default when a

pre-determined close date passes.23

Employers have the opportunity to leave a public rating for the worker, not vice-versa

(during this window). In practice, with very few exceptions, dissatisfied employers decline

to review a worker rather than leave a negative review, and such action does not appear

publicly. While this is not by design, TaskRabbit and many other platforms that facilitate

in-person interactions experience this phenomenon. Our measure of individual productivity

includes these “missing” reviews by looking the Effective Percent Positive (EPP), the share

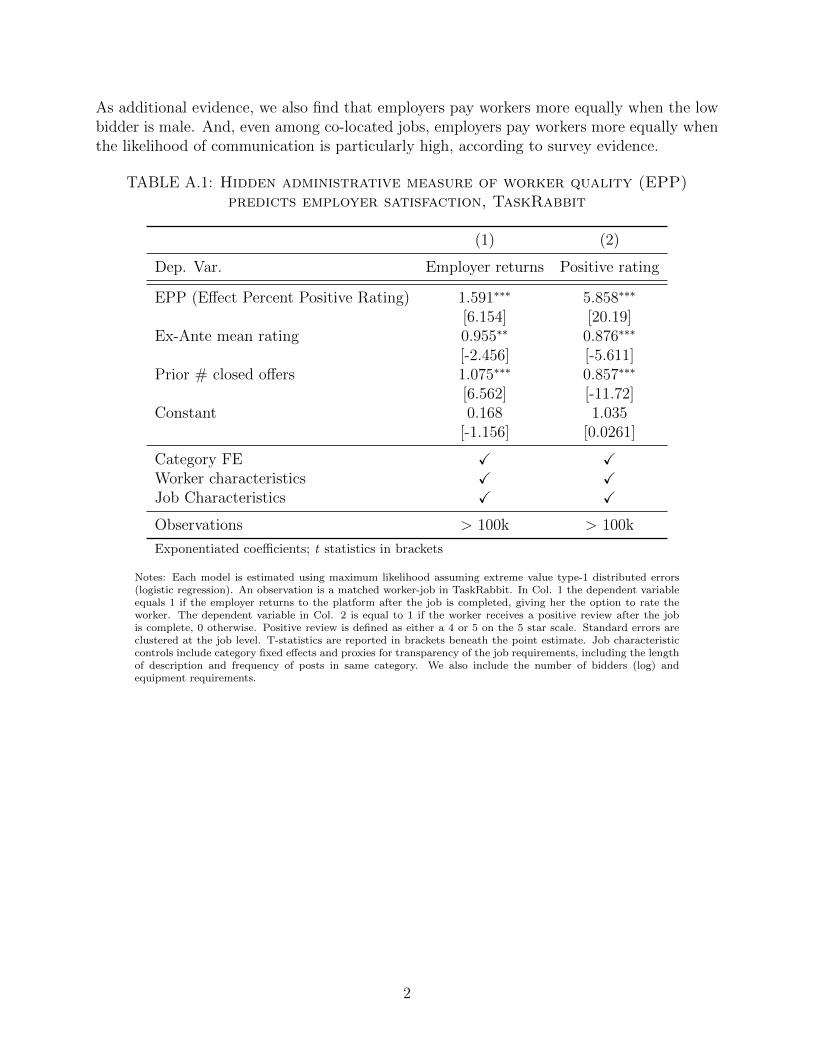

of positive reviews received on all completed jobs.24

IV.C. Measuring Transparency

We measure pay transparency on TaskRabbit several ways. Our first measure is whether

the job post itself includes a take-it-or-leave-it posted price publicly visible to all workers.

22We calculate travel costs based on distance between worker residence and work location.23The platform reserves the right to revoke user privileges should any activity suggest circumventing the

online contract. However, we do not rule out the possibility that working relationships continue off theplatform. For robustness, we replicate results to exclude and include employers that never return to the siteafter their initial jobs are completed.

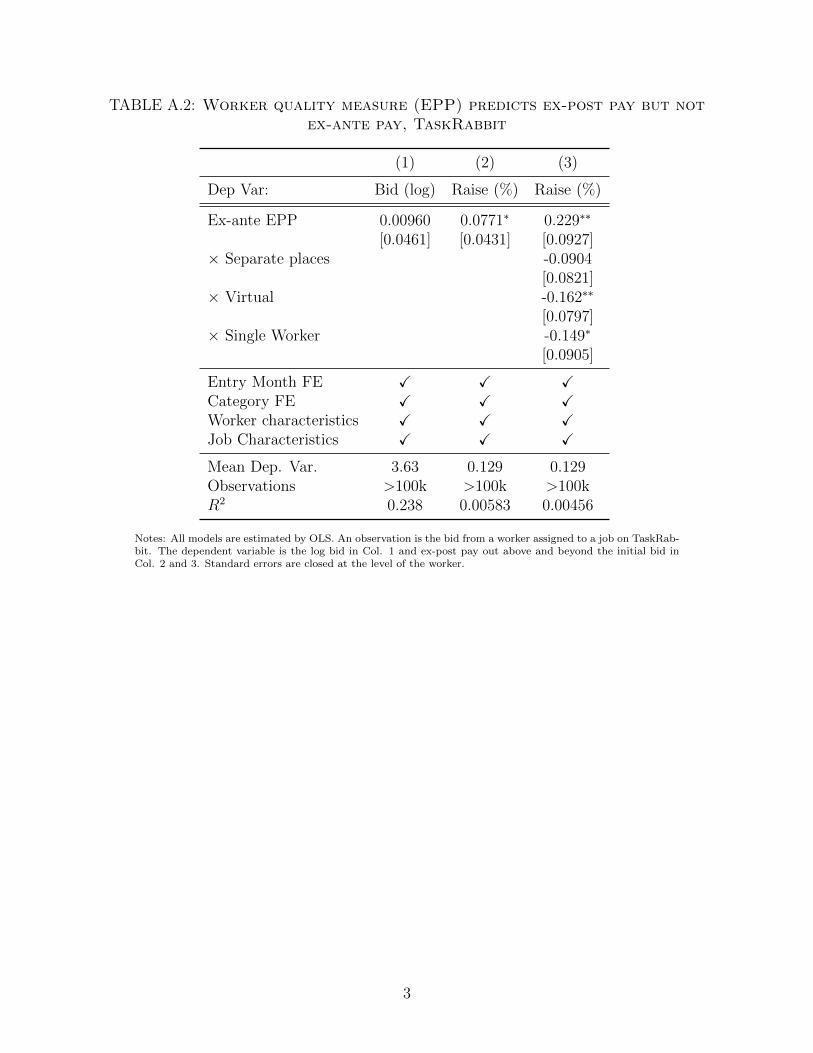

24The literature on user generated content has identified a number biases and manipulation techniquesthat we can address using data about performance that the platform collects but is not visible to the users.Nosko and Tadelis (2015) show the “sound of silence,” or missing reviews, on Ebay is skewed toward negativefeedback. We show the share of missing reviews on TaskRabbit predicts whether an employer returns to theplatform, TaskRabbit’s central measure of employer satisfaction, and the worker star-rating conditional onreceiving a rating (Table A.1 Col. 1 and Col. 2 respectively). Another important feature of this unobservedmeasure is that it is correlated with ex-post pay, but not the ex-ante bid accepted (Table A.2), suggestingthat we are really detecting the performance that the employer observes on-the-job.

20

The posted price can either be text embedded in a job description or a public price associated

with the job posting format selected. We classify these as full transparency.

Our second measure is based on the physical proximity of workers in multi-worker jobs

and the length of time they overlap in the same location. We distinguish settings inherently

suited for either co-located workers and physically separated workers, for example, a retail

branch might outsource the boxing of holiday gifts at the store (co-located workers) and or

outsource the distribution of catalogues in different neighborhoods (separated workers). We

use the street address to classify proximity and we supplement it with survey evidence. We

hire approximately five thousand online workers to read through the detailed job descriptions

and report key attributes, including how conducive the setting is to co-worker communication

about pay (length of time together, physical proximity, privacy). In expectation, workers

will learn about each others’ bids 47% of the time when co-located, and 7% of the time if the

job requires physical separation. In Table I we report characteristics of workers, employers

and tasks by our transparency classification.

IV.D. Verifying Bargaining Assumptions

The premise of our model has two clear empirical implications for the outcome of a

re-bargaining process in multi-worker, co-located tasks:

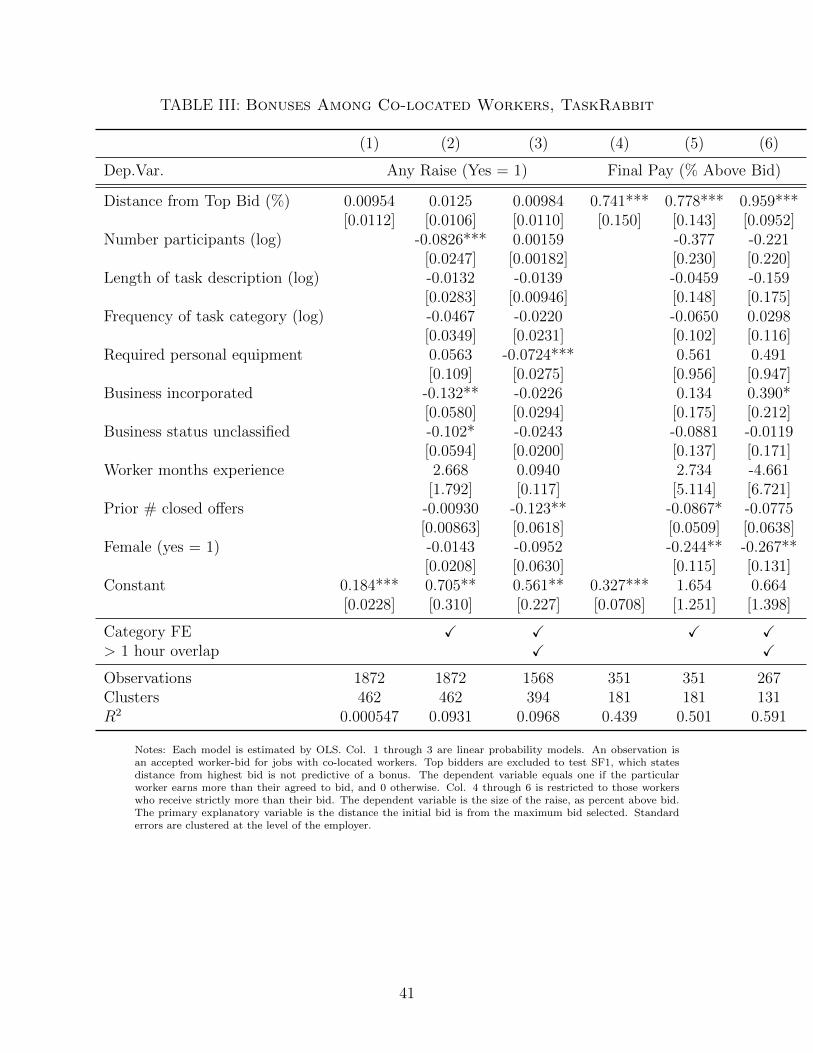

SF1: Workers are no more or less likely to receive a higher wage based on how far their bid

is from the highest accepted bid.

SF2: Workers who receive different wages than their initial bids receive a wage equal to the

highest accepted bid.

We use TaskRabbit data to test these two stylized facts, lending credence to our modeling

decisions, which we show in Table III. Conditional on renegotiating a higher wage than the

initial contract, similar workers negotiate pay nearly equal to that of the highest accepted

bidder (Col.4-6, SF1). At the same time, the distance between bidders adds no additional

predictive power as to whether or not a worker receives any raise at all (Col.1-3, SF2).

We argue that renegotiation is the cause of this wage compression, as opposed to al-

ternative mechanisms such as productivity spillovers or employer preferences for equity. In

Appendix Section A. we discuss the shortcomings of alternative explanations for the com-

pression patterns we observe. In Section V. we compare side-by-side the results from our

analysis of TaskRabbit with our results from an experiment in which we exogenously vary

transparency and observe negotiations directly. The results are strikingly similar.

21

IV.E. Quantifying Wage Compression

Theorem 1 states that increased transparency leads to compression in wages of employed

workers. We first present a visual depiction of wage compression across two types of tasks,

higher transparency jobs that require multiple workers to be situated together and lower

transparency jobs that can be carried out separately.

Figure I: Variance in final pay vs. bids

(a)

Variance of Accepted Bids ($)

Var

ian

ce o

f Ex

-Po

st P

ay (

$)

(b)

Differences Amplified

Variance of Accepted Bids ($)V

aria

nce

of

Ex-P

ost

Pay

($

)

Wages Compressed

Notes: Each observation summarizes the variance in pay among the workers that have been selected for multi-worker separated jobs (Panel a) and multi-worker co-located jobs (Panel b). The x-axis is the variance in thebids accepted for a job, in dollars. The y-axis is the variance in the final payout. An observation below the45 degree line indicates that wages are compressed on the job, while and observation above the 45 degree lineindicates that wages become dispersed on the job.

Figure I offers a visual depiction of the variance in wages for workers assigned to the

same job on TaskRabbit. The concentration of observations that fall beneath the 45 degree

line illustrate the tendency for employers to reduce the variance in ex-post payment relative

to the variance of ex-ante bids.

Among co-located workers, 19% receive pay that is higher than their bids, as opposed to

4% on average when workers are separated. The Gini coeffient of final pay is, on average,

two-thirds the Gini coefficient of selected offers when workers are co-located, and cannot be

statistically differentiated from 0 when separated. The average Gini coefficient of final pay

is more than 0.05 higher when workers are separated (population average is 0.08, Table IV).

In a regression at the level of an individual worker, we demonstrate a co-worker’s bid

impacts own final pay. To interpret co-workers’ bid as having a causal effect on own final

pay when workers are co-located, bidding cannot be strategic nor can employer’s selection

of workers as a function of co-location. Prima facie evidence supports these assumptions.

Multi-worker tasks comprise fewer than 5% of posted jobs and workers are often unaware

that more than one vacancy exists even when it does. Additionally, employers rarely have

more offers that the number necessary to complete a multi-worker job. In Appendix Section

A.1. we offer more empirical tests.

22

We run the specification in Equation 9. Each accepted bid placed by worker i is one

observation. The subscript s refers to the job and j to the employer.25 The dependent

variable is the difference between ex-post payment and ex-ante bid, ∆yijs, expressed as a

percentage raise above i’s initial bid. Distance between i’s initial bid and that of the highest

selected bidder is also expressed as the percentage above initial bid, Tijs.26 We interact

distance between bids with an indicator for whether workers are separated on the job.

∆yijs = α0 + αj + βXi + φXs + εijs

+ γθ1Tijs + γθ2Tijt1Separate(9)

These results can be seen in Table A.6. When workers are co-located, an additional 10%

gap between initial bids and the high bidder will result in a 4% increase in ex-post pay on

average. The effect of the distance between co-worker bids on the final pay when workers

are separated physically cannot be statistically distinguished from 0. Col. 4 demonstrates

this finding is robust within employer.27

IV.F. Employment

TaskRabbit administrative data includes those job posts that expired before they matched,

offering us a measure of unmet labor demand.28 We refer to the employment rate, in the

context of TaskRabbit, as the proportion of positions filled.

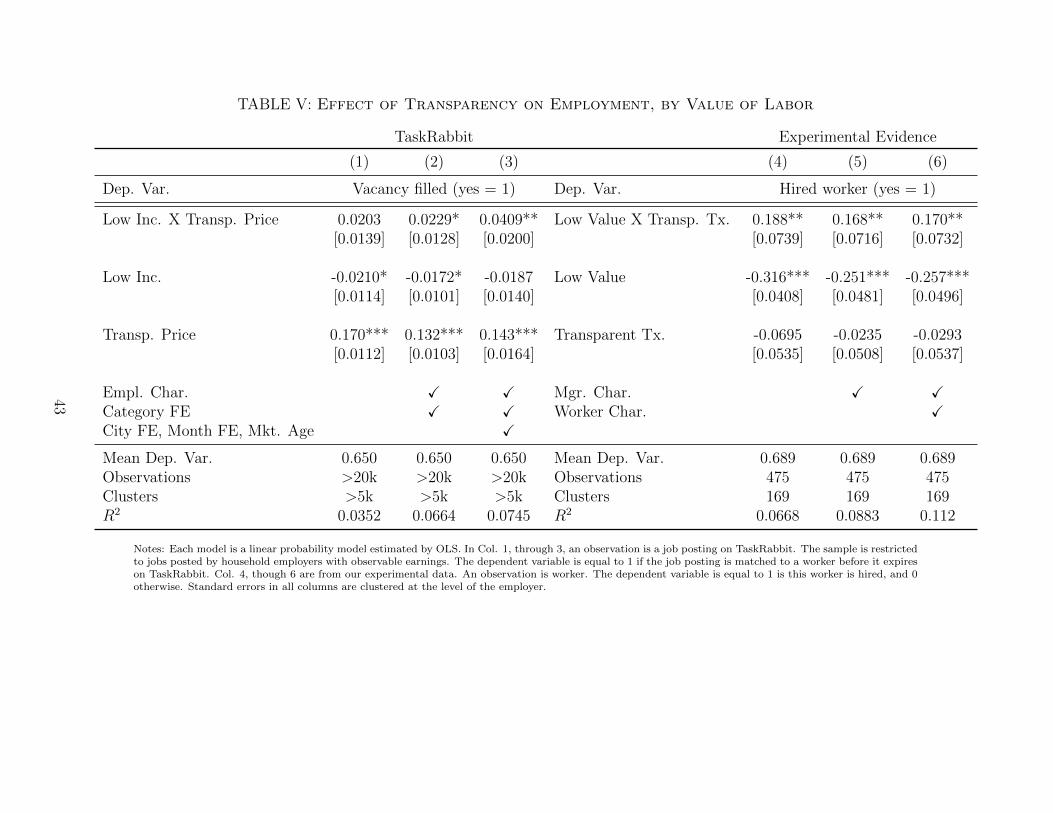

Theorem 2 finds that transparency raises employment by more when the value of labor

to the employer is low. To test this finding, we need to measure both employment and

employers’ value of labor. We do not directly observe the maximum an employer is willing to

pay to fill the job vacancy, but we do observe self-reported annual earnings from household

employers.29 We use annual earnings as a proxy for willingness to pay. One reason to

favor this measure is that, from a survey of employers conducted by TaskRabbit, the most

common alternative to using TaskRabbit to complete a task is to do it oneself. Using money

as measure of the opportunity cost of time, higher income employers are more likely to have

25We include employer fixed effects in our analysis, which also includes characteristics of the task itself.26We are confident that there is negligible measurement error in the bids, and are therefore comfortable

normalizing both the dependent and independent variables by the initial bid.27We observe slight compression among virtual jobs. Virtual jobs are substantially lower paying jobs, and

likely more challenging to monitor, so we hypothesize that employers choose efficiency wages that are higherthan the lowest bid, generating this compression.

28Cullen and Farronato (2016) find TaskRabbit to be a slack labor market with highly elastic laborsupply, supporting the notion that unfilled tasks reduce total work completed by workers and their wageson platform.

29TaskRabbit also hires third party companies to report socioeconomic characteristics of employers usinga combination of address, job title, and other public records.

23

higher time costs (i.e. leisure is a normal good).30

We find that below-median earners (under $150,000 annual income) who choose trans-

parent posted prices to advertise their job enjoy a higher match rate (relative to when they

solicit private bids) and that this boost is greater for low earners than for above-median in-

come employers (Table V). Below-median income employers also select a transparent posted

price more often than high earners (5% more often, Table VI). Overall employment is in-

creased by 12% under transparent posted prices. We reproduce this analysis restricting the

sample to the first three jobs posted by each employer to minimize the effects of learning

and strategic selection and find similar results.

IV.G. Profit Share

Theorem 3 predicts higher levels of transparency are associated with higher expected

employer profits. We note in Table IX that both bids and final pay are approximately 10%

lower when a price range is mentioned in a job post compared to those with no mention,

a result that is robust across specifications with worker fixed effects and job characteristic

controls. Combined with insignificant differences in close rates, this likely translates into

higher profits.31 We find similar differences in total wages if we compare posted price jobs

(high transparency) to private auctions (low transparency), and if we compare co-located,

multi-worker jobs (high transparency) to separated, multi-worker jobs (low transparency).

IV.H. Endogenous Choice of Transparency

When the firm selects the level of transparency endogenously, Corollary 2 argues that

the firm always chooses full transparency due to unraveling. The analogue in TaskRabbit

is the choice of the employer to advertise a job with a transparent posted price or to solicit

private bids without mentioning price in the job post. We observe the predicted unraveling

in TaskRabbit. All else equal, the proportion of posted price jobs rises by 1% per month,

which we show in Table VII. Observed unraveling in labor markets typically takes time.32

This is consistent with a bounded rationality explanation a la Kandori et al. (1993) in which

employers select to post a price or accept bids based on which scheme would have maximized

their expected profits in a previous period.33

30We directly manipulate the employer’s value of labor in our field experiment as described in Section V..31We directly observe employer profits in our field experiment which is described in Section V..32Roth and Xing (1994) discuss this timeline in a number of labor markets.33Employers need not even rely on their own experiences as TaskRabbit pricing discussion threads exist

on websites including Glassdoor, Quora, and Reddit, in addition to word-of-mouth information acquisition.Furthermore, a website including empirical analyses of “optimal” TaskRabbit pricing exists, meaning thatemployers can potentially use the data of previous job posters to optimally select their pricing strategies. Forexample, Kerzner (2013) contains publicly available empirical analyses of pricing strategies in TaskRabbit.

24

Figure II: Posted price and market age

Boston

SF Bay Area

San Antonio

Austin

Chicago

SeattlePortland

LA & OC

New York City

Atlanta

Dallas

Houston

Miami

Philadelphia

Phoenix

San Diego

Washington DC

Denver

Virtual.1

5.2

.25

.3.3

5

0 10 20 30 40 50Months Since Market Opened

Final Snapshot, June 2014Share of Jobs Per Month With Transparent Posted-Price

Notes: Figure II plots the age of each TaskRabbit market (horizontal axis) and the proportion of posted pricejobs in each market (vertical axis) at the end of our data sample in June, 2014. Older markets appear to beassociated with a higher proportion of posted price jobs. “Virtual” refers to tasks that are completed by workersonline. As location is not relevant for these types of markets, TaskRabbit rolled out virtual tasks country-wideat the same time. TaskRabbit entered Boston in 2008 nearly two years before the start of our data sample. Inour analysis we treat the Boston market as if it started at the same date as our data sample, but in reality,there are many observations that we do not observe.

Figure II shows the share of posted price jobs in each TaskRabbit market in June of 2014,

in which older markets are generally associated with a higher proportion of posted price

jobs. In June, 2014 TaskRabbit removed the bid acceptance procedure from all markets. We

discuss alternative hypotheses for this market trend, and why we do not believe these are

plausible, in Appendix A.2..

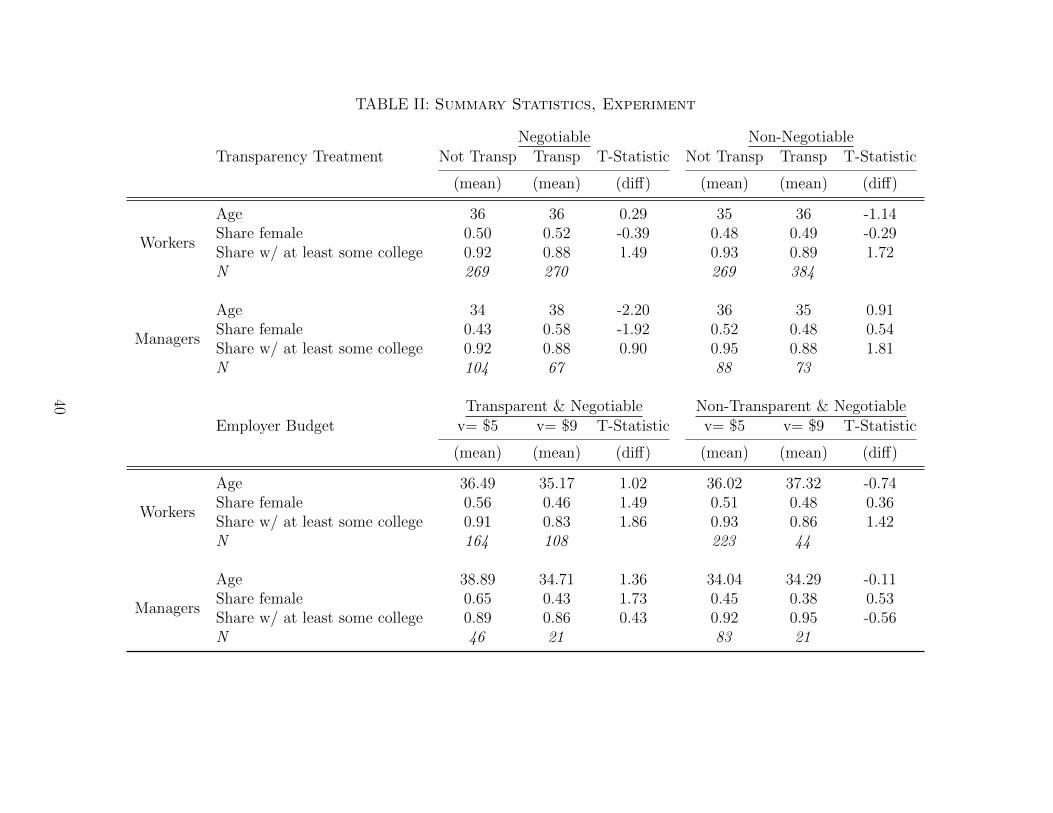

V. Study II: Evidence from Field Experiment

We conduct a field experiment to further test our findings in a controlled environment.34

We hire 347 “managers” and 1047 “workers” from an online labor market who are tasked