enhancing transparency and accountability in indian … transparency and ... the tax payers ’...

TRANSCRIPT

Enhancing Transparency andAccountability in Indian Corporates

KPMG IN INDIA

The global financial crisis has led to an

intense debate on the adequacy of

corporate governance regulations and

practices the world over. In developed

markets such as US and UK, the tax payers’

money has been used to bail out tainted

corporations that were on the verge of

extinction.

In India, we faced a corporate governance

challenge of a different nature in the

aftermath of the Satyam episode – that of

promoter-induced frauds. The question that

has since kept cropping up is whether there

are more skeletons in the closet.

In the context of debating corporate

governance failures and corporate frauds, a

lot of questions have been raised about the

effectiveness of independent directors and

auditors. Regulators, particularly in the UK

and US have responded to public pressure

and pressure from shareholder activists by

strengthening regulations. Some of these

regulations have cast tremendous duties

and responsibilities on the non-executive

directors. The UK has even gone to the

extent of prescribing a new governance

code for leading audit firms. But it is also

important to look at the role of

promoters/executives in ensuring good

governance and consider how the lines

should be drawn in terms of the

responsibilities of the board and that of

management.

More regulations may inevitably lead to

more ‘box ticking’, as past experiences tell

us. Corporate governance is an extension of

the overall governance eco-system and

hence cannot be viewed in isolation. It is

important to therefore look at the entire

value chain comprising regulators,

shareholders, employees, rating agencies

and consumers and introspect where the

improvement levers lie.

Foreword

Deepankar SanwalkaCo-Chairman, ASSOCHAM Expert Committeeon Corporate Fraud and Internal Audit andHead, Risk and Compliance Group, KPMG in India

Shri D. S. Rawat Secretary General ASSOCHAM

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

The relevance of good Corporate Governance 01

Managing stakeholder expectations 04

Weak governance is a pre-cursor to a heightened risk of fraud 06

Financial statement fraud is a major concern 07

Bribery and corruption 08

Emerging fraud risks 09

Addressing today’s challenges in corporate governance and fraud 10

Improving corporate governance holistically 10

Strong and objective Internal Audit function 12

Pro-active approach to Fraud Risk Management 14

Effective whistle-blowing systems and processes 15

Conclusion 16

Table of contents

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

A key aspect that is being debated in the corridors of India Inc. is

whether we need major regulatory changes to improve corporate

governance, or whether improved standards of corporate governance

could be achieved through adoption of principle-based standards

underpinned by greater levels of transparency and disclosures. But there

is also the question – are we mature enough to move to a principle-

based approach?

“Corporate Governance isconcerned with holding thebalance between economic andsocial goals and betweenindividual and communal goals.The corporate governanceframework is there to encouragethe efficient use of resources andequally to require accountabilityfor the stewardship of thoseresources. The aim is to align asnearly as possible the interests ofindividuals, corporations andsociety.”

Sir Adrian Cadbury in'Global CorporateGovernance Forum', WorldBank, 2000

Source:

http://www.corpgov.net/library/library.html -

December 2008

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

1

The relevance of goodCorporate Governance

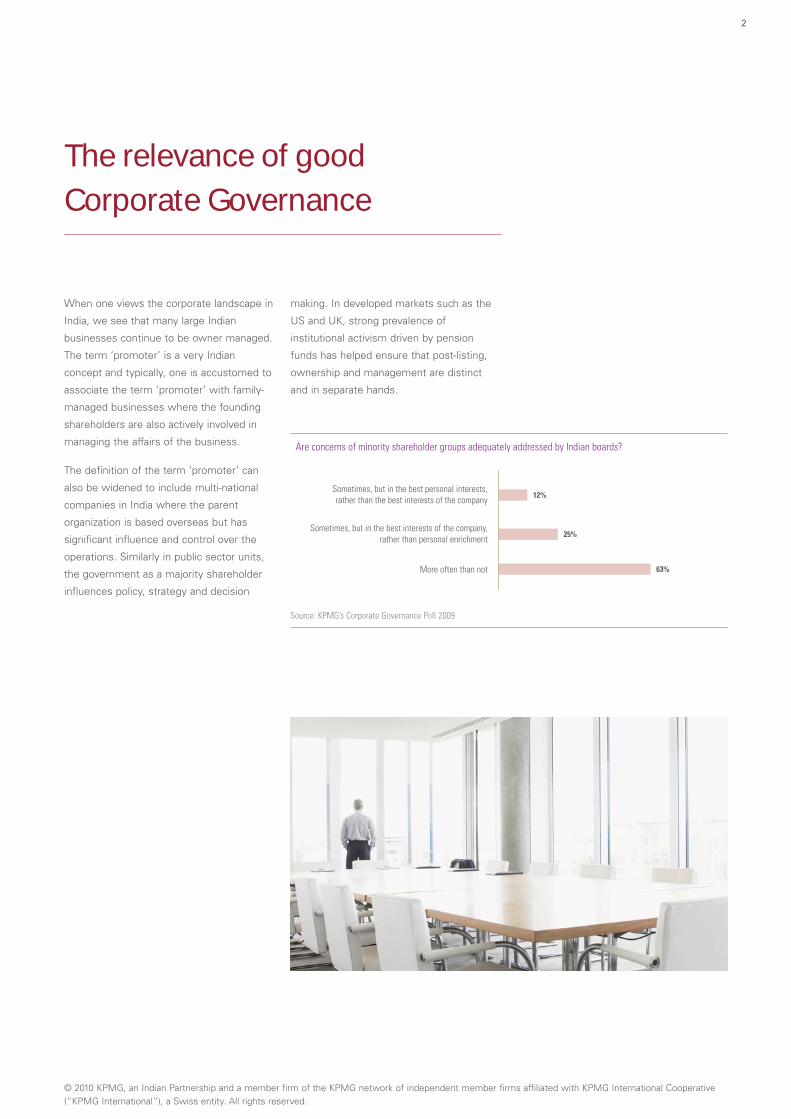

When one views the corporate landscape in

India, we see that many large Indian

businesses continue to be owner managed.

The term ‘promoter’ is a very Indian

concept and typically, one is accustomed to

associate the term ’promoter’ with family-

managed businesses where the founding

shareholders are also actively involved in

managing the affairs of the business.

The definition of the term ’promoter’ can

also be widened to include multi-national

companies in India where the parent

organization is based overseas but has

significant influence and control over the

operations. Similarly in public sector units,

the government as a majority shareholder

influences policy, strategy and decision

making. In developed markets such as the

US and UK, strong prevalence of

institutional activism driven by pension

funds has helped ensure that post-listing,

ownership and management are distinct

and in separate hands.

Source: KPMG’s Corporate Governance Poll 2009

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

2

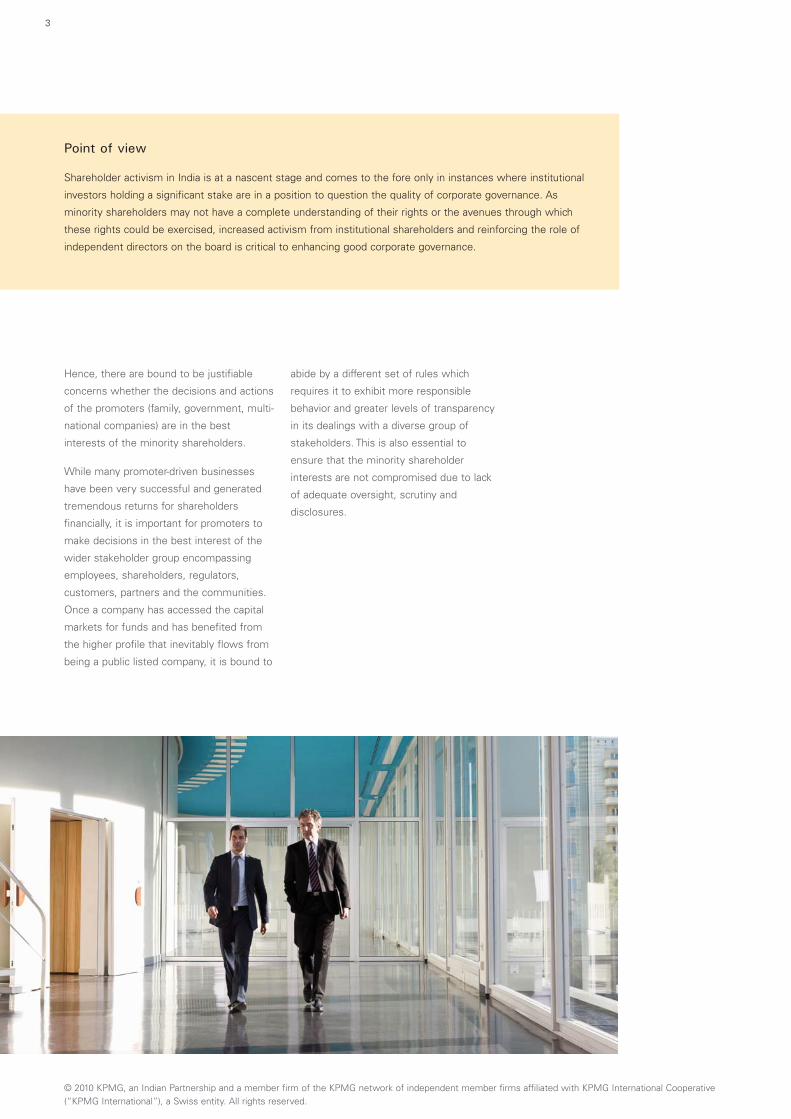

Point of view

Shareholder activism in India is at a nascent stage and comes to the fore only in instances where institutional

investors holding a significant stake are in a position to question the quality of corporate governance. As

minority shareholders may not have a complete understanding of their rights or the avenues through which

these rights could be exercised, increased activism from institutional shareholders and reinforcing the role of

independent directors on the board is critical to enhancing good corporate governance.

Hence, there are bound to be justifiable

concerns whether the decisions and actions

of the promoters (family, government, multi-

national companies) are in the best

interests of the minority shareholders.

While many promoter-driven businesses

have been very successful and generated

tremendous returns for shareholders

financially, it is important for promoters to

make decisions in the best interest of the

wider stakeholder group encompassing

employees, shareholders, regulators,

customers, partners and the communities.

Once a company has accessed the capital

markets for funds and has benefited from

the higher profile that inevitably flows from

being a public listed company, it is bound to

abide by a different set of rules which

requires it to exhibit more responsible

behavior and greater levels of transparency

in its dealings with a diverse group of

stakeholders. This is also essential to

ensure that the minority shareholder

interests are not compromised due to lack

of adequate oversight, scrutiny and

disclosures.

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

3

Point of view

The Ministry of Corporate Affairs (MCA) has proposed the New Companies Bill which aims to improve

corporate governance by vesting greater powers in shareholders. Additionally the proposed Companies Bill

heralds an era of shareholder democracy through an emphasis on self regulation, minimization of regulatory

approvals and, increased and more transparent disclosures.

Managing stakeholderexpectations

Corporate governance should be seen as a

tool to strike the right balance by

supplementing an entrepreneurial approach

with greater professionalism, rather than as

stringent rules that are ‘policed’ across. It is

important to provide a certain level of

independence and flexibility so as to allow

companies to abide by the regulations that

have been put in place.

Governance regulations may beadequate but governance practicesmay not be in tune with stakeholderexpectations

The existing Clause 49 of the SEBI Listing

Agreement and ensuing Companies Bill

legislations do cover the fundamentals of

effective corporate governance where India

compares favorably with many other

developing and Asian economies as far as

the adequacy of corporate governance

regulations are concerned.

Improved corporate governance, however,

does not solely rest on control through

increased regulations. What is required is a

principle-based approach developed on

fundamentals preventing moral fragility that

is enforced through pragmatic levels of

regulations.

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

4

Source: KPMG’s Corporate Governance Poll 2009

Source: KPMG’s Corporate Governance Poll 2009

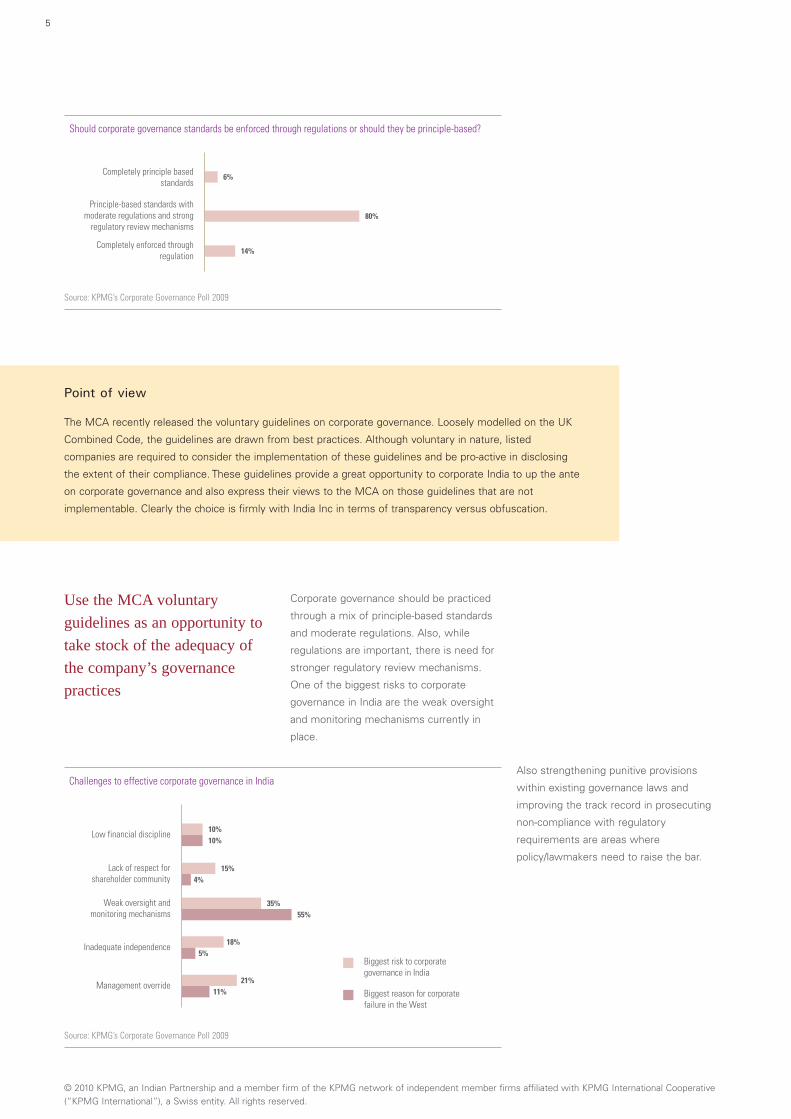

Point of view

The MCA recently released the voluntary guidelines on corporate governance. Loosely modelled on the UK

Combined Code, the guidelines are drawn from best practices. Although voluntary in nature, listed

companies are required to consider the implementation of these guidelines and be pro-active in disclosing

the extent of their compliance. These guidelines provide a great opportunity to corporate India to up the ante

on corporate governance and also express their views to the MCA on those guidelines that are not

implementable. Clearly the choice is firmly with India Inc in terms of transparency versus obfuscation.

Use the MCA voluntaryguidelines as an opportunity totake stock of the adequacy ofthe company’s governancepractices

Corporate governance should be practiced

through a mix of principle-based standards

and moderate regulations. Also, while

regulations are important, there is need for

stronger regulatory review mechanisms.

One of the biggest risks to corporate

governance in India are the weak oversight

and monitoring mechanisms currently in

place.

Also strengthening punitive provisions

within existing governance laws and

improving the track record in prosecuting

non-compliance with regulatory

requirements are areas where

policy/lawmakers need to raise the bar.

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

5

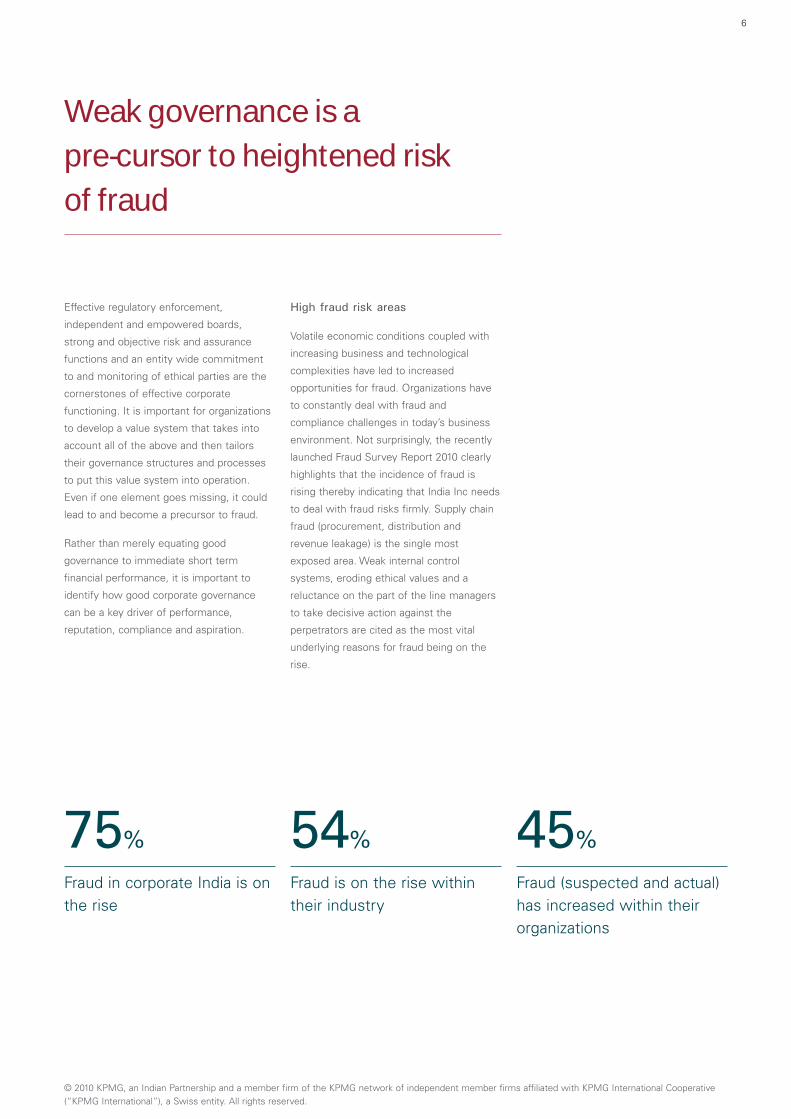

Weak governance is a pre-cursor to heightened riskof fraud

Effective regulatory enforcement,

independent and empowered boards,

strong and objective risk and assurance

functions and an entity wide commitment

to and monitoring of ethical parties are the

cornerstones of effective corporate

functioning. It is important for organizations

to develop a value system that takes into

account all of the above and then tailors

their governance structures and processes

to put this value system into operation.

Even if one element goes missing, it could

lead to and become a precursor to fraud.

Rather than merely equating good

governance to immediate short term

financial performance, it is important to

identify how good corporate governance

can be a key driver of performance,

reputation, compliance and aspiration.

High fraud risk areas

Volatile economic conditions coupled with

increasing business and technological

complexities have led to increased

opportunities for fraud. Organizations have

to constantly deal with fraud and

compliance challenges in today’s business

environment. Not surprisingly, the recently

launched Fraud Survey Report 2010 clearly

highlights that the incidence of fraud is

rising thereby indicating that India Inc needs

to deal with fraud risks firmly. Supply chain

fraud (procurement, distribution and

revenue leakage) is the single most

exposed area. Weak internal control

systems, eroding ethical values and a

reluctance on the part of the line managers

to take decisive action against the

perpetrators are cited as the most vital

underlying reasons for fraud being on the

rise.

75%

Fraud in corporate India is onthe rise

54%

Fraud is on the rise withintheir industry

45%

Fraud (suspected and actual)has increased within theirorganizations

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

6

Financial statement fraud is a major concern

Considering the current economic environment, financial statement fraud is a major area of

concern. A desire to achieve/exceed targets and earnings of senior executives linked to

financial performance are the reasons for senior management involvement in such frauds.

Ineffective whistle-blowing systems, lack of objective and independent Internal Audit (IA)

functions with forensic skills, inadequate oversight of senior management activities by the

audit committee and weak regulatory environment are the reasons for growing worries in

respect of financial statement fraud.

81%

Financial statement fraud is amajor issue

63%

Desire to meet / exceedmarket expectations themost significant reason tocommit financial statementfraud

62%

Disagree that strictdisciplinary actions areimposed for cases involvingfinancial statement fraud

Source: KPMG in India’s Fraud Survey 2010

Source: KPMG in India’s Fraud Survey 2010

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

7

Bribery and corruption

Corruption is a serious offense, often not

appropriately recognized by many

organizations. The World Bank has

estimated that, globally, bribes paid each

year amount to over USD 1 trillion. Bribery

and Corruption is on the risk radar of

governments, regulators, law enforcement

agencies and businesses worldwide. With

the increase in public scrutiny of

multinational organizations, it is pertinent for

companies to adopt essential controls to

mitigate the risk of corruption.

Bribery and corruption in India is more

prevalent in seeking routine regulatory

approvals and to win new business from

prospective clients. Despite the presence of

anti-corruption laws, weak regulatory

enforcement has contributed to the current

impasse. With Indian companies going

global, we see an increasing trend of Indian

companies pro-actively taking measures to

adhere to international anti-bribery

laws/regulations (e.g.: Foreign Corrupt

Practices Act) and strengthening their code

of business ethics at the board and senior

management levels to regulate dealings

with external stakeholders.

37%

Bribes are mostly paid to getroutine administrativeapprovals from Government

38%

Bribery an integral feature ofindustry practices

56%

Tone at the top critical tocombat bribery andcorruption

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

8

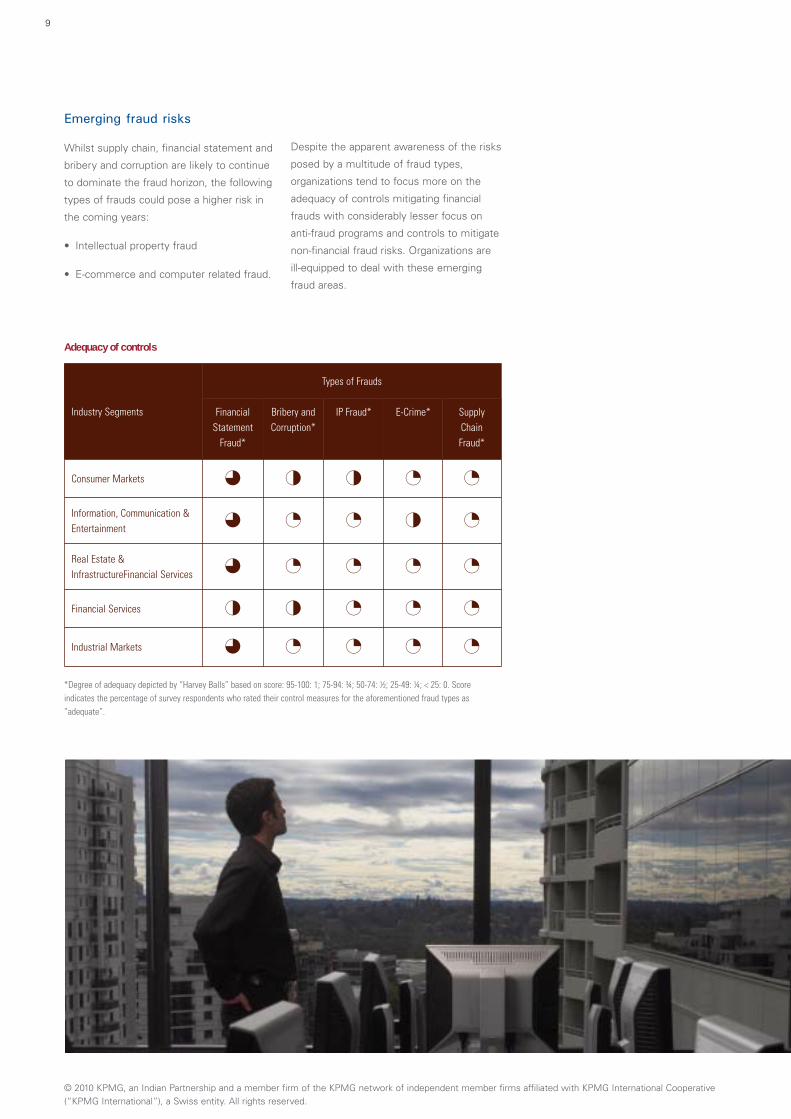

Emerging fraud risks

Whilst supply chain, financial statement and

bribery and corruption are likely to continue

to dominate the fraud horizon, the following

types of frauds could pose a higher risk in

the coming years:

• Intellectual property fraud

• E-commerce and computer related fraud.

Despite the apparent awareness of the risks

posed by a multitude of fraud types,

organizations tend to focus more on the

adequacy of controls mitigating financial

frauds with considerably lesser focus on

anti-fraud programs and controls to mitigate

non-financial fraud risks. Organizations are

ill-equipped to deal with these emerging

fraud areas.

Industry Segments

Types of Frauds

FinancialStatement

Fraud*

Bribery andCorruption*

IP Fraud* E-Crime* SupplyChainFraud*

Consumer Markets 3 2 2 1 1

Information, Communication &Entertainment

3 1 1 2 1

Real Estate &InfrastructureFinancial Services

3 1 1 1 1

Financial Services 2 2 1 1 1

Industrial Markets 3 1 1 1 1

*Degree of adequacy depicted by “Harvey Balls” based on score: 95-100: 1; 75-94: ¾; 50-74: ½; 25-49: ¼; < 25: 0. Scoreindicates the percentage of survey respondents who rated their control measures for the aforementioned fraud types as“adequate”.

Adequacy of controls

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

9

Addressing today’schallenges in corporategovernance and fraud

Improving corporate governance holistically

1. Managing governance structures and processes to drive

performance

• A diverse, competent and independent board is a critical

resource to address the company’s growth-related challenges

and to align company goals and objectives to long-term

shareholder interests. Presence of independent directors on

the board can also provide a structure to deal with disputes

and thus helps resolve issues and bring balance to decisions. It

is true that promoter-appointed independent directors do not

challenge the promoter’s decisions. Therefore, it is important to

establish formal processes for appointing executive and non-

executive directors. Adopting a formal process that involves

the use of specialist human capital advisors to map company’s

strategic priorities with skills required at the board level is a

good way of having a diverse group of directors who can add

value. An environment of constructive challenge and dissent in

the board room is vital if it ultimately results in a better

strategy

• Establish clear roles and responsibilities for the board and

management as a whole and put in place robust induction

processes to maximize non-executive director (NED) input. It is

also vital for promoters to put in place structures for NED

interaction outside the regular board meetings because the

promoters and the organization as a whole stands to gain from

these discussions

• The subject of CEO and board chair segregation has been a

contentious one in the Indian context. Many Indian promoters

look at it as a way of boards becoming more powerful in the

way the organization is run. In many Indian companies where

the CEO/Managing Director is not the chairman of the board, a

closer examination is likely to reveal that the non-executive

chairman of the board is usually the ex-CEO or the founding

promoter. Promoters should be more receptive to the idea of

having a non-executive board chair outside the promoter club.

If the expectations from and role of the board chair is clearly

defined, this practice can actually yield dividends. Non-

Executive board chairs can take on the role of mentoring

promoters and CEOs on strategy and help them deal with

growing complexities in business by offering advice and

external perspectives. An empowered board chair can actually

get more out of his other NED colleagues, bring to the issue a

wider range of issues that represent the concerns of

stakeholders and as a result enhance the dynamics of board

functioning. Additionally, such a practice is likely to be viewed

favorably by the investor community and stakeholders

• Exposure of company senior executives to other

companies’ boards as NEDs could help develop the horizons

of senior executives and develop the leadership gene pool for

meeting future challenges. It is also a great way for promoters

to expose their senior personnel to external challenges and

motivating people to stay with the organization. Unfortunately,

very few Indian companies adopt these practices

• Make the board responsible for CEO performance

evaluation – although this may result in the CEO reporting to

the board, this process also has its benefits in terms of

improving the CEO’s performance and having the board taking

a more hands-on role in terms of mentoring the CEO

• Compensate NEDs well – to do all of the above, it is

imperative that promoters compensate their NEDs well. It is

important to have a balance of fixed and variable pay and

introduce an objective process of board evaluation facilitated

by external experts.

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

10

2. Succession planning

As promoter-driven businesses introduce second generation

family members into their business, they often face the challenge

of smoothly transitioning the next generation into the business.

This involves creating an environment where family managers

and professional managers can co-exist and work together to

achieve the chosen objectives. The right time to induct

professional managers in the business is also an important

aspect as the next generation may not be yet ready to assume

critical senior management roles. This is easier said than done

and warrants attention which explains the importance of

succession planning. Developing transparent human capital

processes where professional managers do not feel insecure is

essential. However difficult the exercise may be, the

consequences of not having a succession plan for the CEO may

be extremely damaging for the business. Additionally, aspects

such as attracting the right talent, incentivising professional

managers, adequate delegation of authority and grooming

second and third generation family managers in the company of

professionally qualified managers need to be considered. These

are areas where the promoter together with the NEDs on the

board should be actively involved.

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

11

Strong and objective IA functionto support boards in theiroversight priorities

Corporate frauds, governance failures,

regulatory scrutiny and globalization have all

contributed to an increased focus on the IA

function and the role it plays in enabling the

board achieve its oversight objectives. There

is considerable re-thinking on IA’s role in

terms of how it can successfully make the

transition from value preservation to value

creation. This has led to a paradigm shift in

expectations from IA today compared to

what it was a few years ago.

With IA roles becoming increasingly broad

based, IA’s reporting relationship and its

communication with the board/audit

committee needs to improve in order to

provide it with the independence it needs.

In many Indian companies, management

continues to play a key role in oversight of

the IA function.

Source: KPMG in India and BSE’s Internal Audit Survey 2009

Point of view

Enhancing Independence of IA

• The head of IA should have clear authority to communicate directly and on their initiative to the board and

members of the Audit Committee (AC). For instance, head of IA should meet privately with the board / AC

without the presence of management. This should reinforce the independence and direct nature of the

reporting relationship

• The reporting line should facilitate open and direct communications with the CEO, the senior executive

group and line management

• The board / AC should have the final authority to review and approve the annual audit plan

• The board / AC should also review the performance of the head of IA and the overall internal audit function

at least once a year, and approve the compensation levels for head of IA.

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

12

Source: KPMG in India and BSE’s Internal Audit Survey 2009

Point of view

Continuous Auditing and Continuous Monitoring

Transforming IA and Management Monitoring to create value

The economic crisis clearly

demonstrates that changes are often

fast and dramatic, and that there is a

real need for management and directors

to understand the velocity of risk—the

speed at which an emerging risk can be

manifested and have a catastrophic

impact on the business. In this

environment, management should

assess the company’s critical

alignments (strategy, goals, risks,

incentives, performance measures and

internal controls) on a regular, frequent

basis; annual or semi-annual

assessments may not be adequate.

Many have begun to advance their efforts by implementing Continuous Auditing (CA) and Continuous Monitoring

(CM) disciplines around their organizational processes, transactions, systems, and controls. Leveraging proactive,

technology-based applications to manage performance and key areas of risk and control has become a practical and

necessary alternative to meet the growing needs of the organization. Together, CA and CM offer a broad range of

benefits that can help organizations add value and improve business performance. CA/CM can deliver regular insight

into the status of controls and transactions across the global enterprise, enhancing risk and control oversight

capability through monitoring and detection.

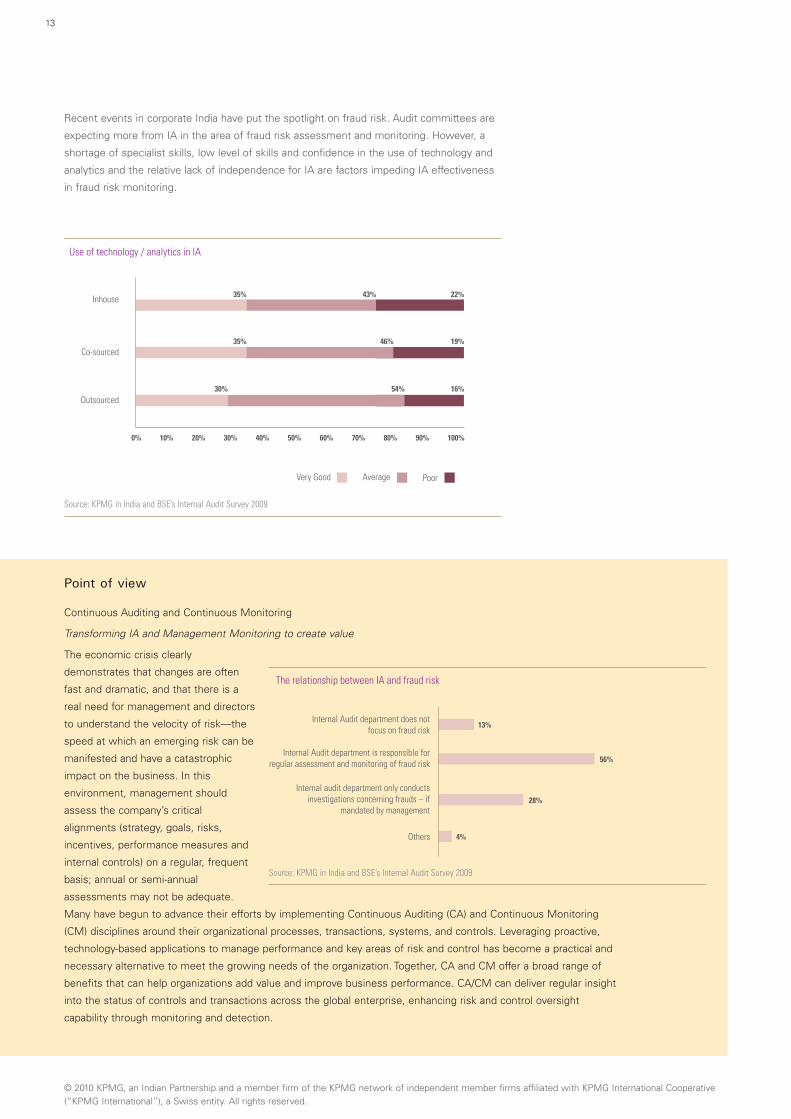

Recent events in corporate India have put the spotlight on fraud risk. Audit committees are

expecting more from IA in the area of fraud risk assessment and monitoring. However, a

shortage of specialist skills, low level of skills and confidence in the use of technology and

analytics and the relative lack of independence for IA are factors impeding IA effectiveness

in fraud risk monitoring.

Source: KPMG in India and BSE’s Internal Audit Survey 2009

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

13

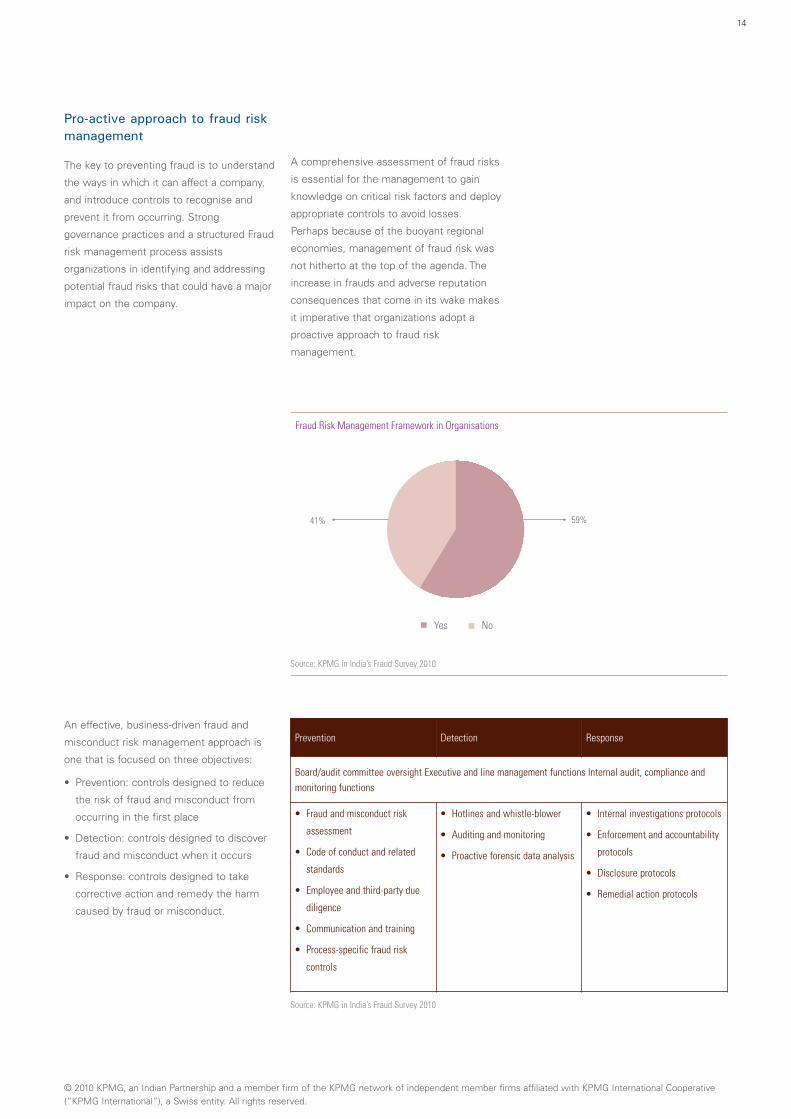

Pro-active approach to fraud riskmanagement

The key to preventing fraud is to understand

the ways in which it can affect a company,

and introduce controls to recognise and

prevent it from occurring. Strong

governance practices and a structured Fraud

risk management process assists

organizations in identifying and addressing

potential fraud risks that could have a major

impact on the company.

A comprehensive assessment of fraud risks

is essential for the management to gain

knowledge on critical risk factors and deploy

appropriate controls to avoid losses.

Perhaps because of the buoyant regional

economies, management of fraud risk was

not hitherto at the top of the agenda. The

increase in frauds and adverse reputation

consequences that come in its wake makes

it imperative that organizations adopt a

proactive approach to fraud risk

management.

An effective, business-driven fraud and

misconduct risk management approach is

one that is focused on three objectives:

• Prevention: controls designed to reduce

the risk of fraud and misconduct from

occurring in the first place

• Detection: controls designed to discover

fraud and misconduct when it occurs

• Response: controls designed to take

corrective action and remedy the harm

caused by fraud or misconduct.

Source: KPMG in India’s Fraud Survey 2010

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

Prevention Detection Response

Board/audit committee oversight Executive and line management functions Internal audit, compliance andmonitoring functions

• Fraud and misconduct risk

assessment

• Code of conduct and related

standards

• Employee and third-party due

diligence

• Communication and training

• Process-specific fraud risk

controls

• Hotlines and whistle-blower

• Auditing and monitoring

• Proactive forensic data analysis

• Internal investigations protocols

• Enforcement and accountability

protocols

• Disclosure protocols

• Remedial action protocols

Source: KPMG in India’s Fraud Survey 2010

14

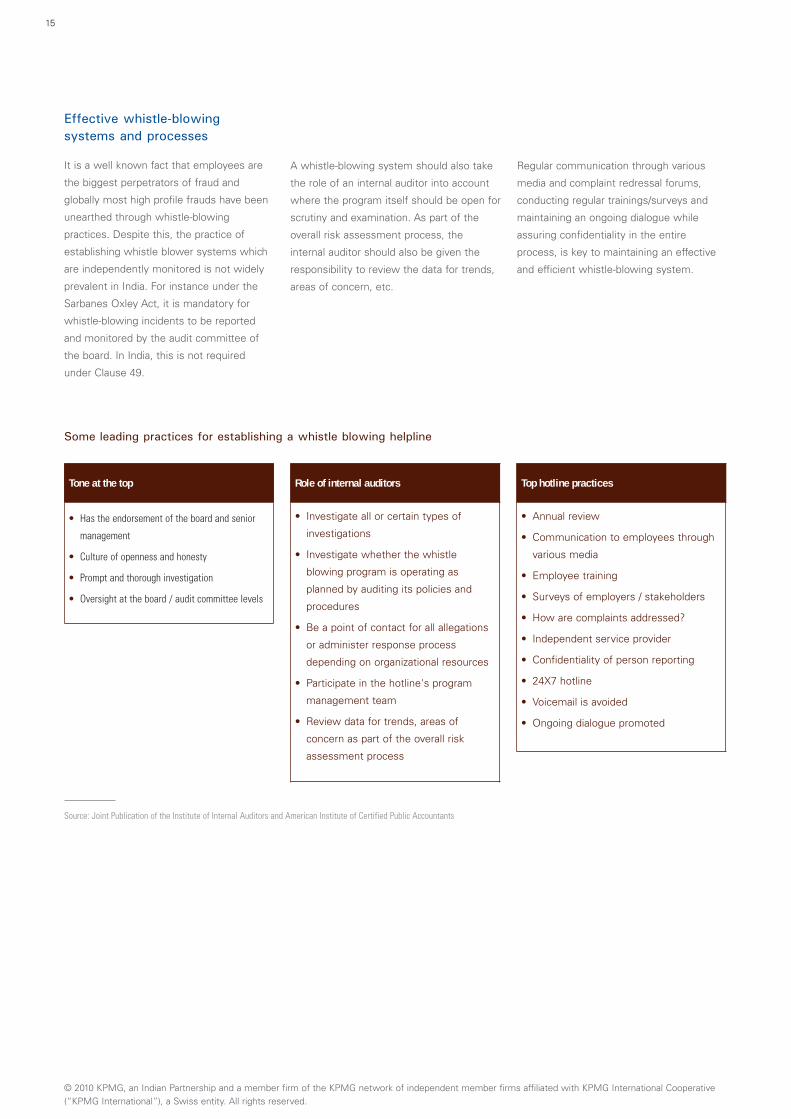

A whistle-blowing system should also take

the role of an internal auditor into account

where the program itself should be open for

scrutiny and examination. As part of the

overall risk assessment process, the

internal auditor should also be given the

responsibility to review the data for trends,

areas of concern, etc.

Regular communication through various

media and complaint redressal forums,

conducting regular trainings/surveys and

maintaining an ongoing dialogue while

assuring confidentiality in the entire

process, is key to maintaining an effective

and efficient whistle-blowing system.

Effective whistle-blowingsystems and processes

It is a well known fact that employees are

the biggest perpetrators of fraud and

globally most high profile frauds have been

unearthed through whistle-blowing

practices. Despite this, the practice of

establishing whistle blower systems which

are independently monitored is not widely

prevalent in India. For instance under the

Sarbanes Oxley Act, it is mandatory for

whistle-blowing incidents to be reported

and monitored by the audit committee of

the board. In India, this is not required

under Clause 49.

Some leading practices for establishing a whistle blowing helpline

Tone at the top

• Has the endorsement of the board and senior

management

• Culture of openness and honesty

• Prompt and thorough investigation

• Oversight at the board / audit committee levels

Role of internal auditors

• Investigate all or certain types of

investigations

• Investigate whether the whistle

blowing program is operating as

planned by auditing its policies and

procedures

• Be a point of contact for all allegations

or administer response process

depending on organizational resources

• Participate in the hotline's program

management team

• Review data for trends, areas of

concern as part of the overall risk

assessment process

Top hotline practices

• Annual review

• Communication to employees through

various media

• Employee training

• Surveys of employers / stakeholders

• How are complaints addressed?

• Independent service provider

• Confidentiality of person reporting

• 24X7 hotline

• Voicemail is avoided

• Ongoing dialogue promoted

Source: Joint Publication of the Institute of Internal Auditors and American Institute of Certified Public Accountants

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

15

Conclusion

In the wake of high profile

corporate scandals and a rising

concern over yet increasing risk of

corporate fraud and issues around

financial statement, it is now

necessary to step away from the

traditional approach and focus on

establishing a cohesive system,

delivering two important qualities:

transparency and honesty.

As companies grow in size and

complexity they need to take into

account several requirements –

internal monitoring controls,

corporate governance, and external

reporting activities - that are able

to function as a synergistic whole.

Moreover, as one increases their

stakeholder base the expectation

level also rises from regulators as

well as the society at large. It is

paramount that companies adopt

and implement a code of conduct

that re-enforces the culture of

transparency in business

transaction.

The mechanisms of corporate

governance have been built up

after a long history of responding

to the misconduct and failures of

management. Business reality and

fraud knowledge require to be

interwoven so as to develop a

consistent system of corporate

governance.

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

16

About KPMG in India

KPMG is a global network of

professional firms providing Audit,

Tax and Advisory services. We

operate in 146 countries and have

140,000 people working in

member firms around the world.

The independent member firms of

the KPMG network are affiliated

with KPMG International

Cooperative (“KPMG

International”), a Swiss entity. Each

KPMG firm is a legally distinct and

separate entity and describes itself

as such.

KPMG in India, the audit, tax and

advisory firm, is the Indian

member firm of KPMG

International Cooperative (“KPMG

International.”) was established in

September 1993. As members of a

cohesive business unit they

respond to a client service

environment by leveraging the

resources of a global network of

firms, providing detailed

knowledge of local laws,

regulations, markets and

competition. We provide services

to over 2,000 international and

national clients, in India. KPMG has

offices in India in Mumbai, Delhi,

Bangalore, Chennai, Hyderabad,

Kolkata, Pune and Kochi. The firms

in India have access to more than

2000 Indian and expatriate

professionals, many of whom are

internationally trained.

We strive to provide rapid,

performance-based, industry-

focused and technology-enabled

services, which reflect a shared

knowledge of global and local

industries and our experience of

the Indian business environment.

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

17

About KPMG’s ForensicPractice

Operating in both developed and

emerging markets, KPMG’s

Forensic Practice helps clients

protect their business from fraud,

misconduct and non-compliance

which could lead to reputation

risks and commercial losses.

KPMG's Forensic practice in India

was established in 1995. Our

practice endeavors to provide an

independent, proactive and

responsive service, by effectively

utilizing our investigative,

accounting and technology skills

towards the prevention, detection

and investigation of alleged fraud

and fraud-related issues in

resolving commercial and legal

disputes.

The practice has over time evolved

into a team of over 350 dedicated

professionals, each one bringing in

not only rich and extensive

experience but also a competitive

and specific skill set. Our team

includes certified fraud examiners,

former police officers, chartered

accountants, CPAs, MBAs,

business ethics professionals,

social workers, technology

professionals and lawyers. Our

forensic professionals have

working experience on

engagements both at national and

international levels in the US,

Canada, UK, Africa, Singapore,

Europe, Middle East, Mauritius and

South Asian countries, and are able

to provide practical and prudent

advice on various assignments

across industry sectors and

different lines of businesses.

We emphasize the need for

innovation, flexibility and quality

and provide evidence to help

companies make informed

decisions.

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

18

About ASSOCHAM

The Associated Chambers of

Commerce and Industry of India

(ASSOCHAM) acknowledged as

Knowledge Chamber of India has

emerged as a forceful, pro-active,

effective and forward looking

institution playing its role as a

catalyst between the Government

and Industry. ASSOCHAM

established in 1920, has been

successful in influencing the

Government in shaping India’s

economic, trade, fiscal and social

policies which will be of benefit to

the trade and industry.

ASSOCHAM renders its services

to over 3,50,000 members which

includes multinational companies,

India’s top corporates, medium and

small scale units and Associations

representing all the sectors of

Industry. ASSOCHAM is also

known as a Chamber of Chambers

representing the interest of more

than 300 Chambers & Trade

Associations from all over India

encompassing all sectors.

ASSOCHAM has over 100 National

Committees covering the entire

gamut of economic activities in

India. It has been especially

acknowledged as a significant

voice of Indian industry in the field

of Corporate Social Responsibility,

Environment & Safety, Corporate

Governance, Information

Technology, Agriculture,

Nanotechnology, Biotechnology,

Pharmaceutics, Telecom, Banking

& Finance, Company Law,

Corporate Finance, Economic and

International Affairs, Tourism, Civil

Aviation, Infrastructure, Energy &

Power, Education, Legal Reforms,

Real Estate, Rural Development

etc. The Chamber has its

international offices in China,

Sharjah, Moscow, UK and USA.

ASSOCHAM has also signed MoU

partnership with Business

Chambers in more than 45

countries.

© 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative(“KPMG International”), a Swiss entity. All rights reserved.

19

kpmg.com/in

© 2010 KPMG, an Indian Partnership and a member firm of theKPMG network of independent member firms affiliated withKPMG International Cooperative (“KPMG International”), a Swissentity. All rights reserved.

KPMG and the KPMG logo are registered trademarks of KPMGInternational Cooperative (“KPMG International”), a Swiss entity.

Printed in India.

The information contained herein is of a general nature and is not intended to address the circumstances of

any particular individual or entity. Although we endeavour to provide accurate and timely information, there

can be no guarantee that such information is accurate as of the date it is received or that it will continue to

be accurate in the future. No one should act on such information without appropriate professional advice

after a thorough examination of the particular situation.

The Associated Chambers ofCommerce and Industry of India

1, Community Centre, Zamrudpur, Kailash Colony, New Delhi - 110 048

Tel: +91 11 4655 0555Fax: + 91 11 4653 6481/82

Email: [email protected]

Website: www.assocham.org

ASSOCHAMKPMG in India

BangaloreMaruthi Info-Tech Centre11-12/1, Inner Ring RoadKoramangala, Bangalore – 560 071Tel: +91 80 3980 6000Fax: +91 80 3980 6999

ChennaiNo.10, Mahatma Gandhi RoadNungambakkamChennai - 600034Tel: +91 44 3914 5000Fax: +91 44 3914 5999

DelhiBuilding No.10, 8th FloorDLF Cyber City, Phase IIGurgaon, Haryana 122 002Tel: +91 124 307 4000Fax: +91 124 254 9101

Hyderabad8-2-618/2Reliance Humsafar, 4th FloorRoad No.11, Banjara HillsHyderabad - 500 034Tel: +91 40 3046 5000Fax: +91 40 3046 5299

Kochi4/F, Palal TowersM. G. Road, Ravipuram,Kochi 682 016Tel: +91 484 302 7000Fax: +91 484 302 7001

KolkataInfinity Benchmark, Plot No. G-110th Floor, Block – EP & GP, Sector VSalt Lake City, Kolkata 700 091Tel: +91 33 44034000Fax: +91 33 44034199

MumbaiLodha Excelus, Apollo MillsN. M. Joshi MargMahalaxmi, Mumbai 400 011Tel: +91 22 3989 6000Fax: +91 22 3983 6000

Pune703, Godrej CastlemaineBund GardenPune - 411 001Tel: +91 20 3058 5764/65Fax: +91 20 3058 5775

KPMG Contacts

Vikram UtamsinghHead of Markets+91 22 3090 [email protected]

Deepankar SanwalkaHead of Risk and Compliance Group+91 124 307 [email protected]