engaging with innovators

TRANSCRIPT

Engaging with Innovators: The FCA’s Innovation Hub

Bob Ferguson

Financial Conduct Authority

Global Fintech Opportunities in Financial Services Edinburgh, 24 February 2015

1

Agenda

• Part I – The Innovation Hub 1. What is the FCA? 2. Who do we regulate? 3. Supporting innovation at the FCA 4. Setting up the Innovation Hub 5. The Innovation Hub’s roles 6. Our work so far

• Part II – Getting Support 1. Eligibility criteria 2. How to ask for our support 3. Good practice 4. Case study – AIRE

2

Part I

The Innovation Hub

3

What is the FCA?

• The Financial Conduct Authority (FCA) regulates the Financial Services industry in the UK.

• More than 70,000 firms are FCA regulated.

• Many fintech companies require being FCA regulated.

4

Examples of firms the FCA regulates

• Deposit taking institutions (e.g. banks)

• Peer-to-peer lending platforms

• Equity crowdfunding platforms

• Insurance brokers

• Financial advisors

• Consumer credit firms

• Payment systems providers

• Credit reference agencies

• …and many more.

5

Why does FCA support innovation?

• Promoting competition FCA statutory objective since April 2013.

• Regulators’ historical view - innovation equals risk.

• With new competition objective – seeing opportunities as well as risks.

6

Setting up the Innovation Hub

• Proposals set out in June 2014 and published call for inputs.

• 6 roundtables with 84 innovators during August/September 2014.

• Innovation Hub launched on October 28th.

7

What the Innovation Hub does

• The Hub’s two main roles:

1. Direct support

2. Policy and process change

8

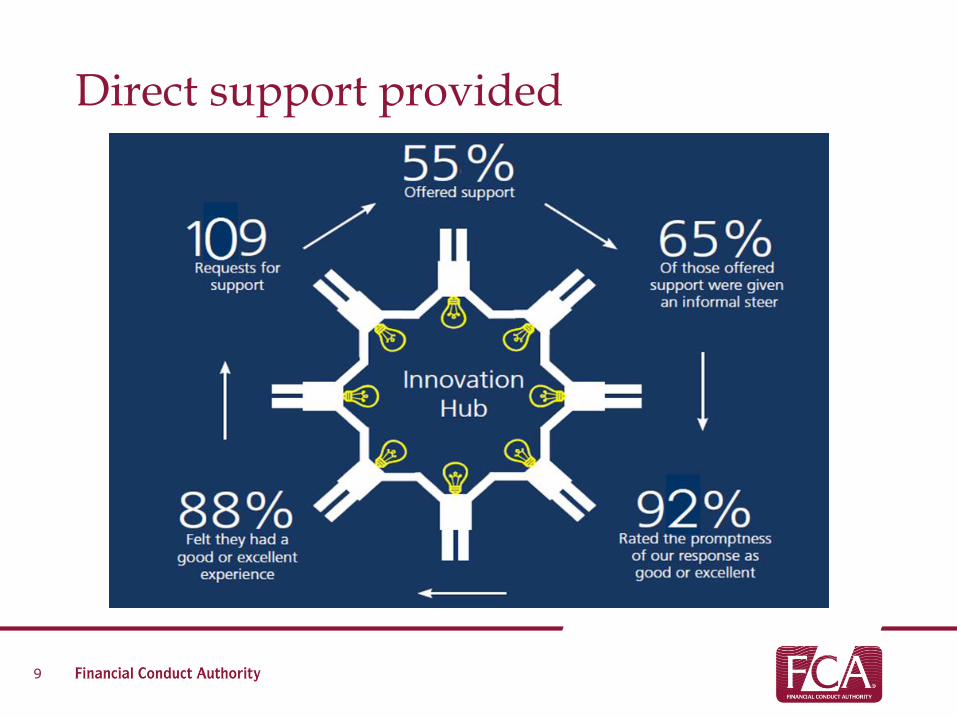

Direct support provided

9

Areas for regulatory change identified

• Some policy challenges to be tackled:

• Access to bank accounts

• Regulatory uncertainty

10

Part II

Getting support

11

Getting support - Eligibility

• Innovation is genuine.

• Innovation prospectively benefits consumers (directly or via competition).

• Innovator has done some background research.

• Innovator needs support.

12

Getting support – Contacting us

• To help us assess what help we can offer, submit a ‘Request for Support’, or send basic info + pitch deck.

• Our contacts:

Phone: +44 (0)2070664488

Email: [email protected]

• Happy to meet face-to-face if needed.

13

Getting support – Good practice

• Providing good description of your offering.

• “We designed an app that allows users of our pre-loaded credit card to send money to each other”

• Asking specific questions.

• “Do we need to apply for an e-money license or a payment system provider license, or both?”

14

Getting support – Not-so-good practice

• Vague descriptions of your offering.

• “We sell a unique and innovative way for users to manage their money using an app and a credit card.”

• Asking for support we cannot offer.

• “Do you think there is demand for this service?”

• “How can the FCA help us promote our product?”

15

Case study – Aire

16

Case study – Aire’s eligibility criteria

• Is it innovative? • Uses social networks and other unconventional

sources of info to assess credit worthiness.

• Consumer benefit • Allows access to credit for people with no UK credit

history.

• Background research? • Questions were specific and made reference to

sections of the FCA Handbook.

• Need for support • New start-up with staff of 7.

17