elasticity and its applications. overview elasticity refers to the responsiveness of quantity...

TRANSCRIPT

ELASTICITY AND ITS APPLICATIONS

Overview

• Elasticity refers to the responsiveness of quantity demanded or quantity supplied.

• Elasticity is a critical analytical tool for businesses and policy analysts

• The most common elasticity measures are:

– Price elasticity of demand

– Price elasticity of supply

– Income elasticity

– Cross price elasticity

Price Elasticity of Demand

• Price elasticity of demand is a measure of how responsive the quantity demanded of a good is to a change in the price of that good

• The price elasticity of demand is the percentage change in quantity demanded divided by the percentage change in price.

P rice e las tic ity o f d em an d =P ercen tag e ch an g e in q u an tity d em an d ed

P ercen tag e ch an g e in p rice

Computing the Price Elasticity of Demand

P rice e las tic ity o f d em an d =P ercen tag e ch an g e in q u an tity d em an d ed

P ercen tag e ch an g e in p rice

X10020,000]20,000)000,18([QuantityinChange%

X1001.50]1.50)00.2([PriceinChange%

Example: Suppose the price of gas increases from $1.50 to $2.00. As a result, quantity demand decreases from 20,000 to 18,000. What is the price elasticity of demand for gas?

30.0%33.33

%10DemandofElasticityPrice

Computing the Price Elasticity of Demand

X10018,000]18,000)000,20([QuantityinChange%

X1002.00]2.00)50.1([PriceinChange%

One problem with the formula we just used is that the price elasticity of demand depends of the direction of the change in price.

Example: Suppose the price of gas decreases from $2.00 to $1.50. As a result, quantity demand increases from 18,000 to 20,000. What is the price elasticity of demand for gas?

44.0%25

%11.11DemandofElasticityPrice

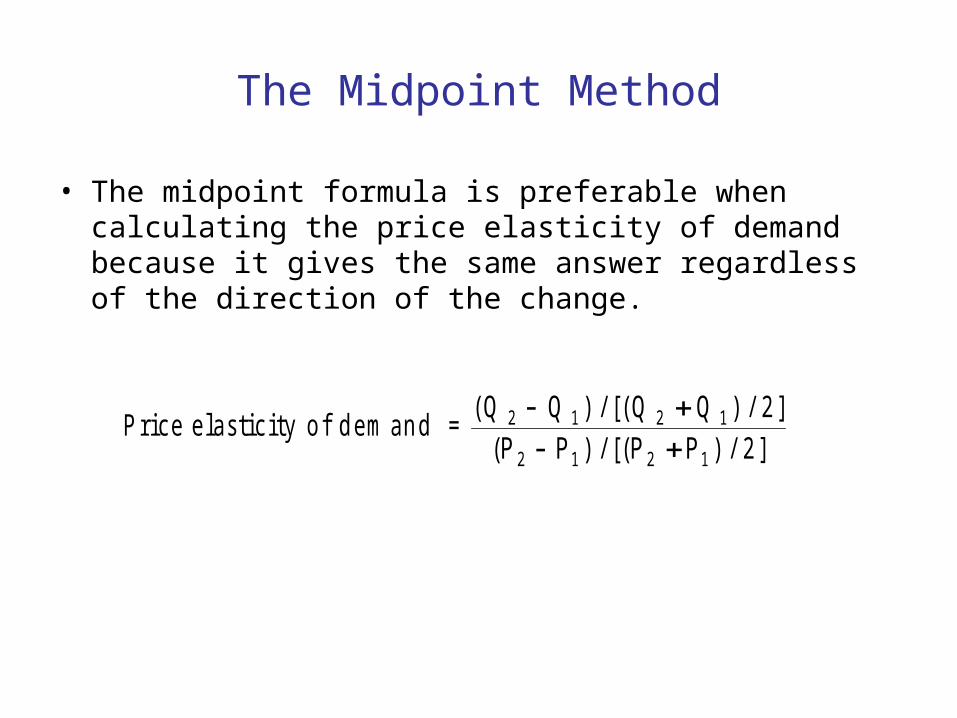

The Midpoint Method

• The midpoint formula is preferable when calculating the price elasticity of demand because it gives the same answer regardless of the direction of the change.

P rice e las tic ity o f d em an d =( ) / [( ) / ]

( ) / [( ) / ]

Q Q Q QP P P P2 1 2 1

2 1 2 1

2

2

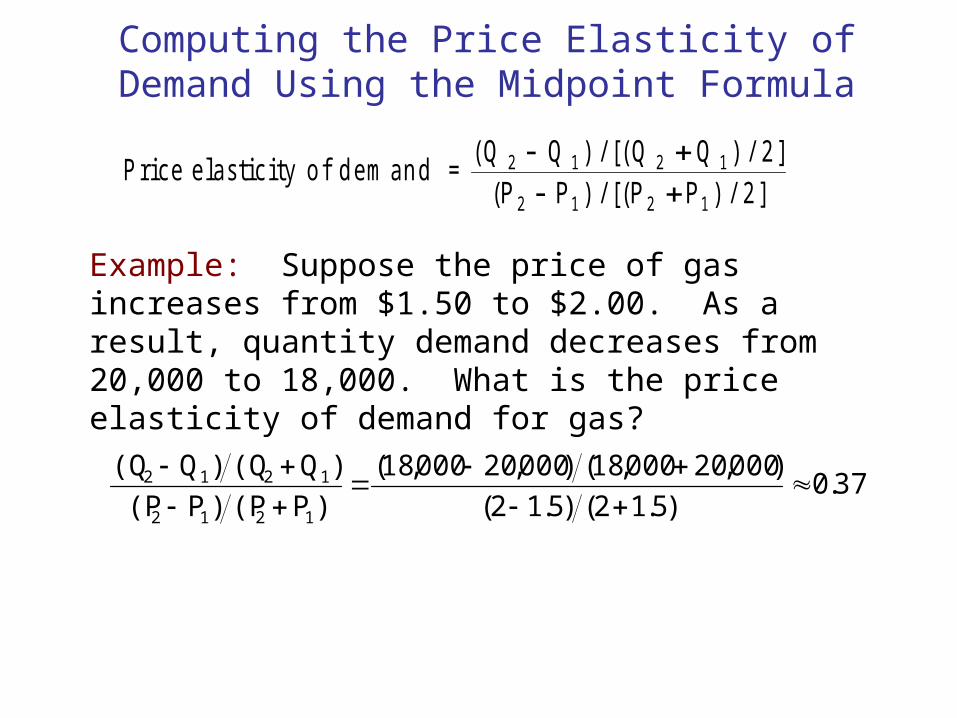

Computing the Price Elasticity of Demand Using the Midpoint Formula

Example: Suppose the price of gas increases from $1.50 to $2.00. As a result, quantity demand decreases from 20,000 to 18,000. What is the price elasticity of demand for gas?

P rice e las tic ity o f d em an d =( ) / [( ) / ]

( ) / [( ) / ]

Q Q Q QP P P P2 1 2 1

2 1 2 1

2

2

37.0)5.12()5.12(

)000,20000,18()000,20000,18(

)P(P)P(P

)Q(Q)Q(Q

1212

1212

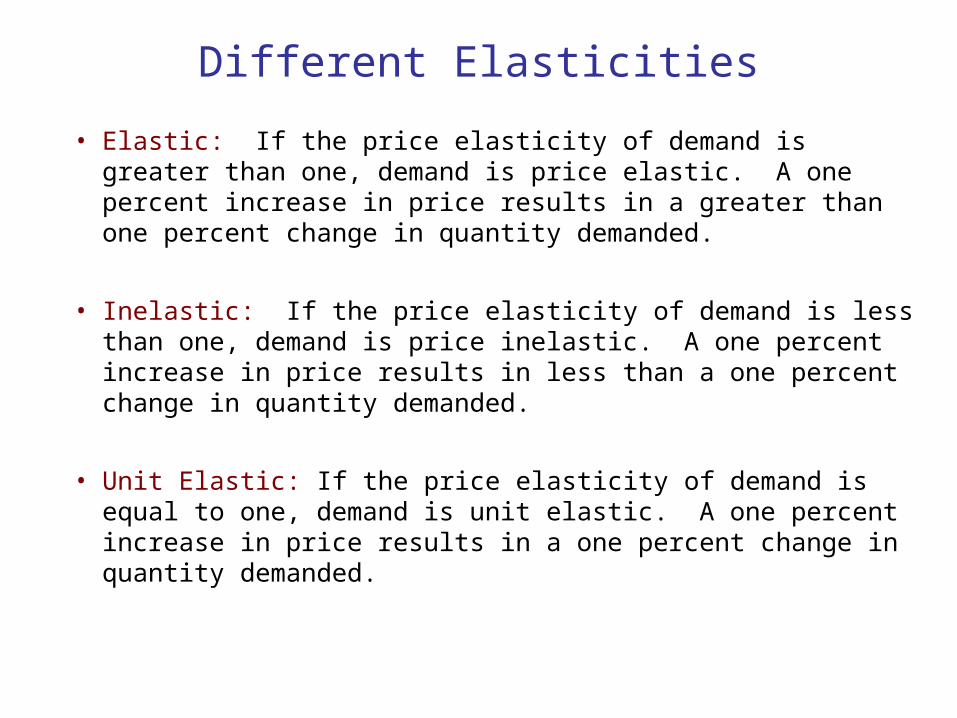

Different Elasticities

• Elastic: If the price elasticity of demand is greater than one, demand is price elastic. A one percent increase in price results in a greater than one percent change in quantity demanded.

• Inelastic: If the price elasticity of demand is less than one, demand is price inelastic. A one percent increase in price results in less than a one percent change in quantity demanded.

• Unit Elastic: If the price elasticity of demand is equal to one, demand is unit elastic. A one percent increase in price results in a one percent change in quantity demanded.

Different Elasticities

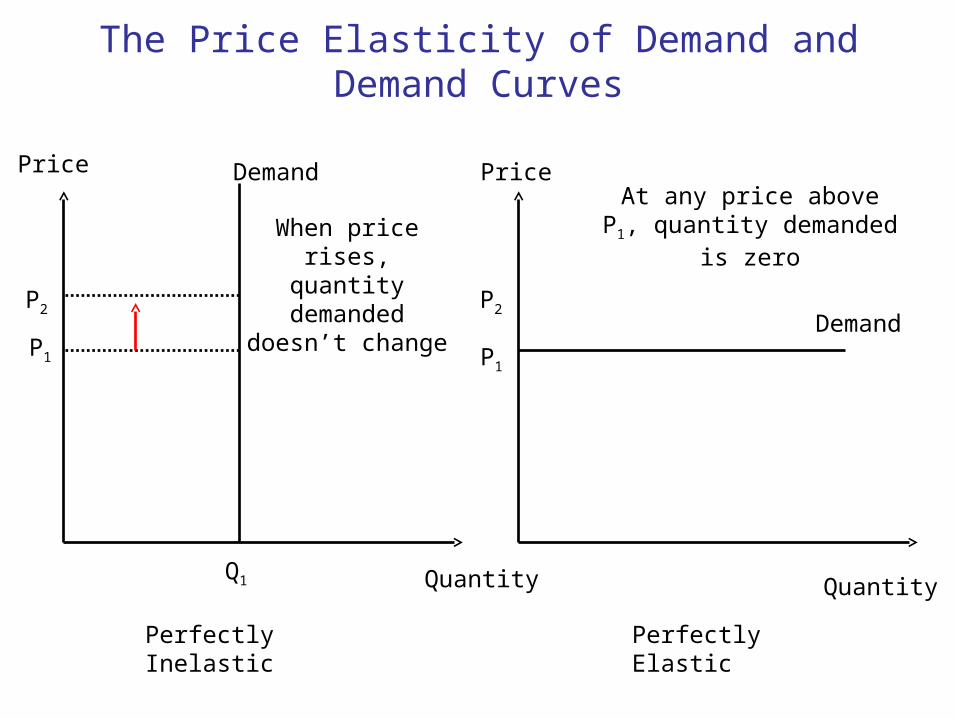

• Demand is perfectly inelastic if the price elasticity of demand equals zero. When price changes, quantity demanded stays the same.

– A perfectly inelastic demand curve is vertical.

• Demand is perfectly elastic if the price elasticity of demand approaches infinity. In that case, small changes in price lead to huge changes in quantity demand.

– A perfectly elastic demand curve is horizontal.

The Price Elasticity of Demand and Demand Curves

Price

Quantity Quantity

PriceDemand

DemandP1

Q1

P2

When price rises, quantity demanded

doesn’t change

Perfectly Inelastic Perfectly Elastic

P1

P2

At any price above P1, quantity demanded is zero

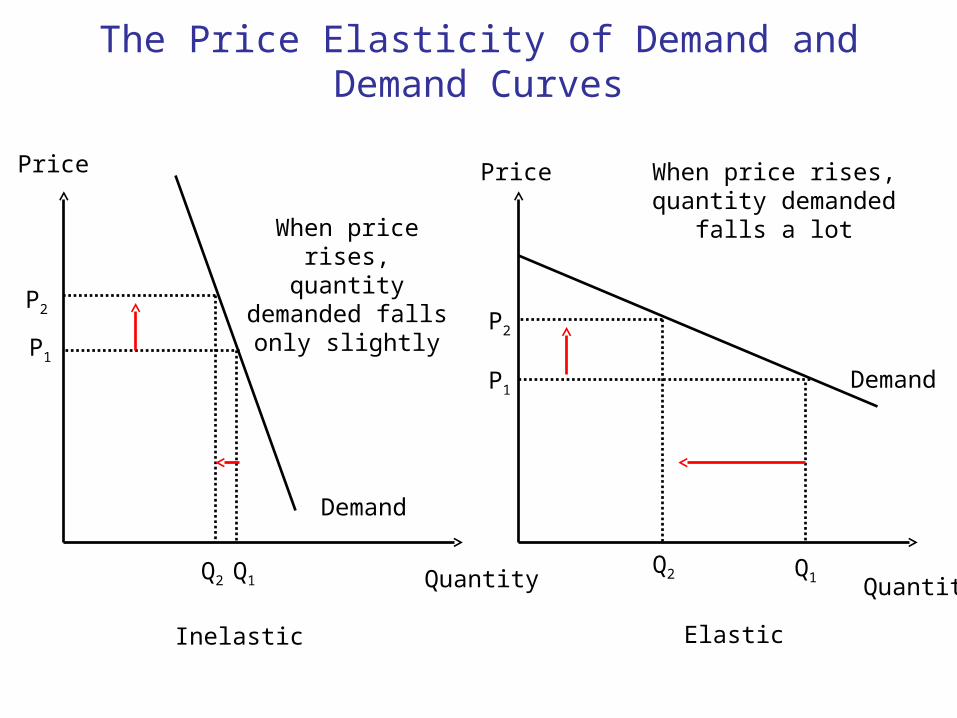

The Price Elasticity of Demand and Demand Curves

Price

Quantity Quantity

Price

Demand

DemandP1

Q1

P2

When price rises, quantity demanded falls only slightly

Inelastic Elastic

P1

P2

When price rises, quantity demanded falls a lot

Q2Q1

Q2

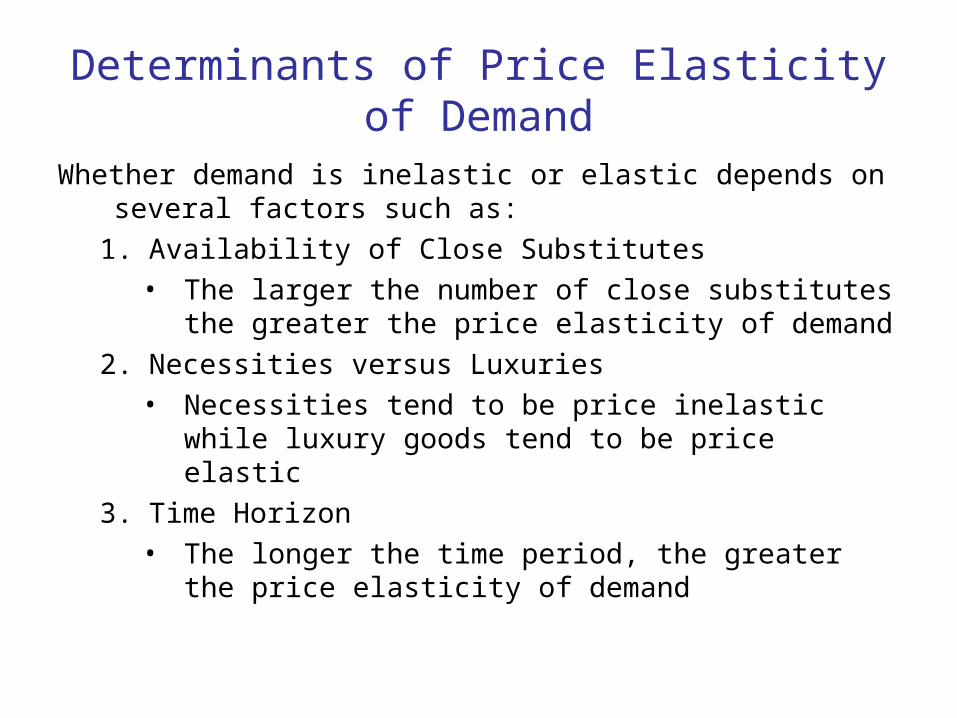

Determinants of Price Elasticity of Demand

Whether demand is inelastic or elastic depends on several factors such as:

1. Availability of Close Substitutes

• The larger the number of close substitutes the greater the price elasticity of demand

2. Necessities versus Luxuries

• Necessities tend to be price inelastic while luxury goods tend to be price elastic

3. Time Horizon

• The longer the time period, the greater the price elasticity of demand

Total Revenue and Price Elasticity of Demand

• If we know the price elasticity of demand for a good, we can determine how a change in price will affect a firm's total revenue.

• Total revenue is simply the price of a good multiplied by the quantity of the good sold.

Total Revenue = P x Q

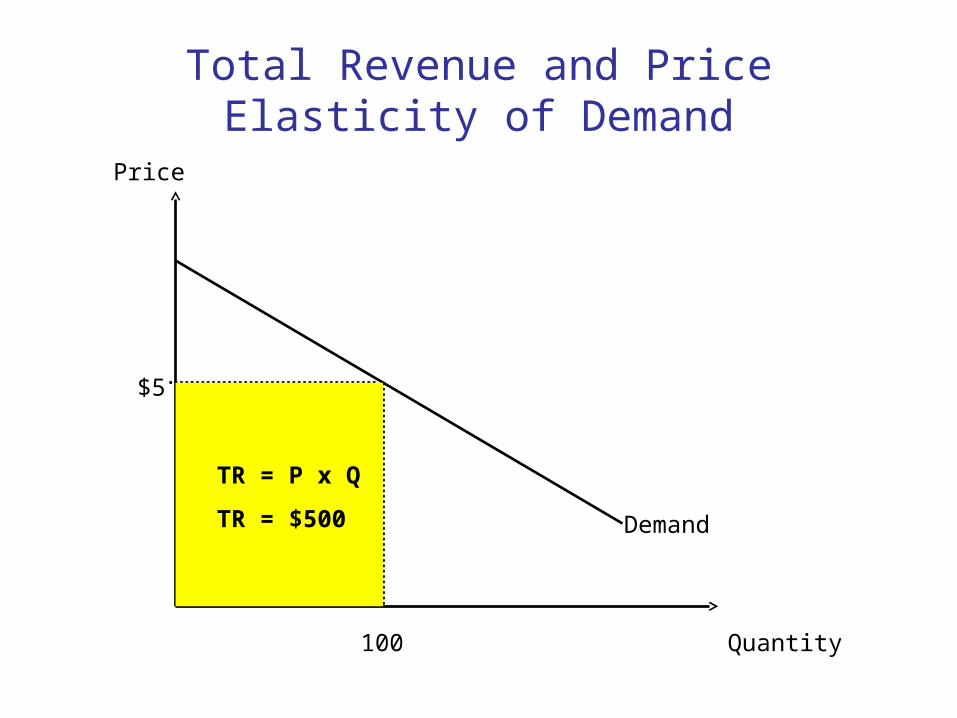

Total Revenue and Price Elasticity of Demand

Price

Quantity

Demand

100

$5

TR = P x Q

TR = $500

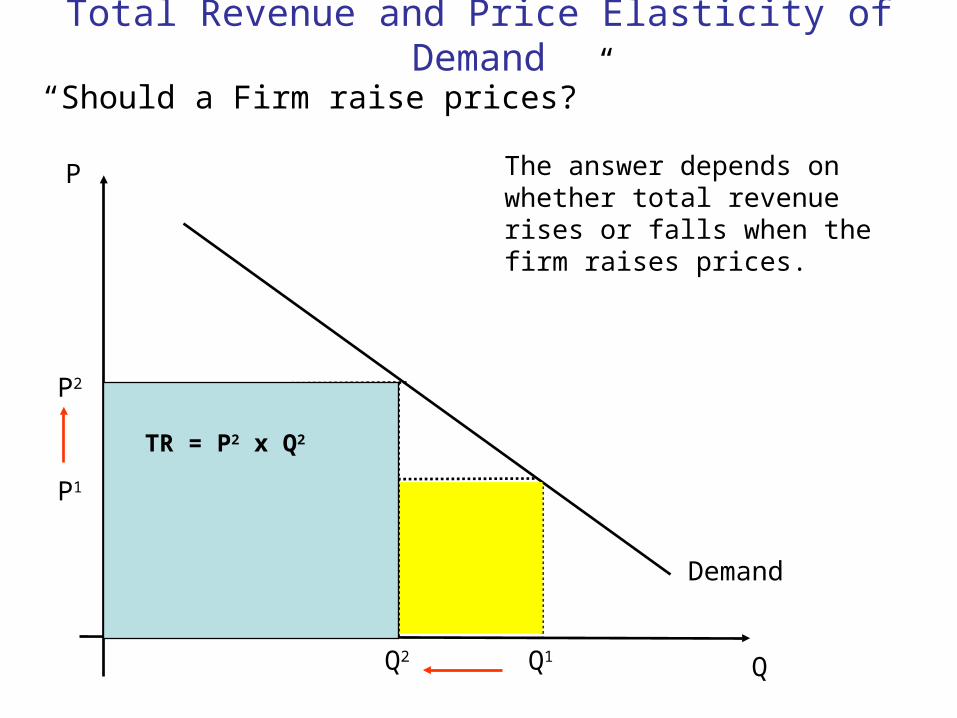

Total Revenue and Price Elasticity of Demand

“Should a Firm raise prices?”

Demand

P1

Q1 Q

P

P2

Q2

TR = P1 x Q1

TR = P2 x Q2

The answer depends on whether total revenue rises or falls when the firm raises prices.

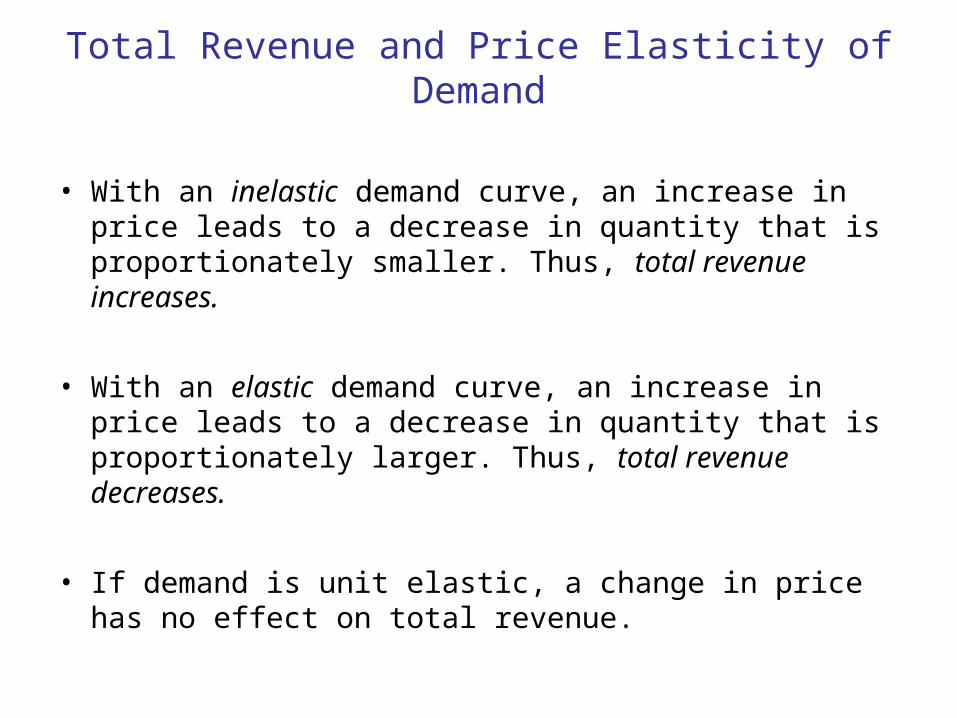

Total Revenue and Price Elasticity of Demand

• With an inelastic demand curve, an increase in price leads to a decrease in quantity that is proportionately smaller. Thus, total revenue increases.

• With an elastic demand curve, an increase in price leads to a decrease in quantity that is proportionately larger. Thus, total revenue decreases.

• If demand is unit elastic, a change in price has no effect on total revenue.

Total Revenue and Price Elasticity of Demand

Price Elasticity of Demand

Implied Elasticity

Impact of a Price Increase on Total Revenue

Impact of a Price Decrease on Total Revenue

Elastic Greater than 1 Total revenue decreases Total revenue increases

Inelastic Less than 1 Total revenue increases Total revenue decreases

Unit Elastic Equal to 1 Total revenue is unchanged Total revenue is unchanged

The Change in Total Revenue when Demand is ElasticP

D

P1

Q1Q

P2

Q2

When demand is price elastic, an increase in price reduces total revenue

The Change in Total Revenue when Demand is InelasticP

D

P0

Q0 Q

P1

Q1

When demand is price inelastic, an increase in price increases total

revenue

Income Elasticity of Demand

• Income elasticity of demand measures how much the quantity demanded of a good responds to a change in consumers’ income.

• It is computed as the percentage change in the quantity demanded divided by the percentage change in income.

In co m e e la stic ity o f d em an d =

P ercen tag e ch an g e in q u an tity d em an d ed

P ercen tag e ch an g e in in co m e

Income Elasticity of Demand

Types of Goods:

A. Normal Goods: If a good is normal, quantity demanded increases when income increases

• For a normal good, the income elasticity of demand is positive

B. Inferior Goods: If a good is inferior, quantity demanded decreases when income increases

• For an inferior good, the income elasticity of demand is negative

Income Elasticity of Demand

• Goods consumers regard as necessities tend to be income inelastic (income elasticity of demand less than one).

– Examples include food, fuel, clothing, utilities, and medical services.

• Goods consumers regard as luxuries tend to be income elastic (income elasticity of demand greater than one).

– Examples include sports cars, furs, and expensive foods.

Price Elasticity of Supply

• Price elasticity of supply is a measure of how much the quantity supplied of a good responds to a change in the price of that good.

• Price elasticity of supply is the percentage change in quantity supplied resulting from a percent change in price.

P rice e las tic ity o f su p p ly =

P ercen tag e ch an g e in q u an tity su p p lied

P ercen tag e ch an g e in p rice

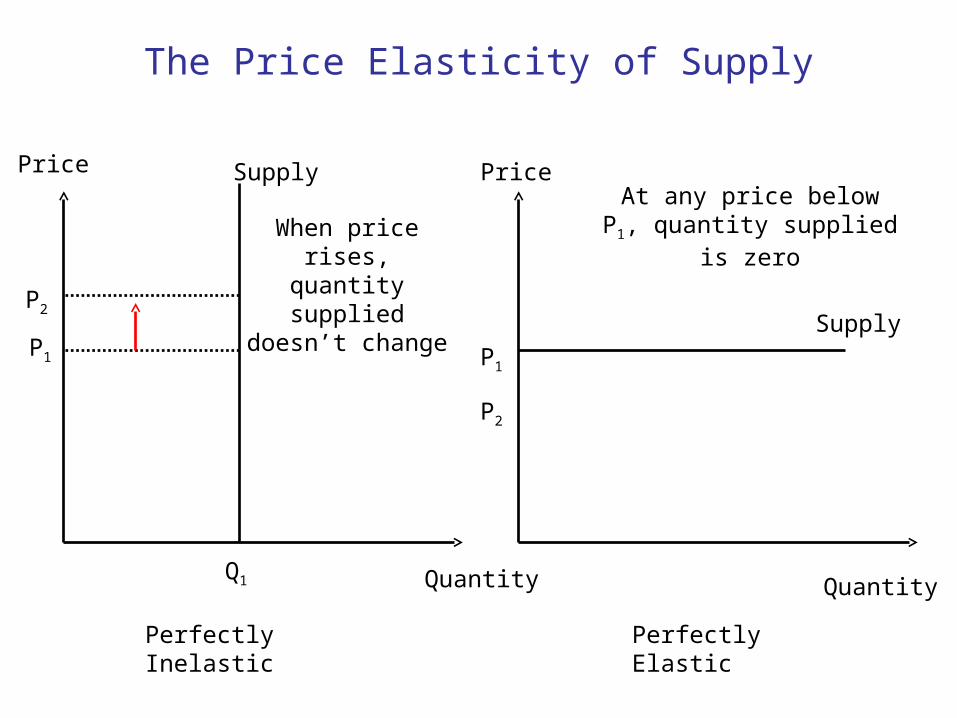

The Price Elasticity of Supply

Price

Quantity Quantity

PriceSupply

SupplyP1

Q1

P2

When price rises, quantity supplied doesn’t change

Perfectly Inelastic Perfectly Elastic

P1

P2

At any price below P1, quantity supplied is zero

The Price Elasticity of Supply

Price

Quantity Quantity

PriceSupply

Supply

P2

Q1

P1

When price falls, quantity supplied falls only slightly

Inelastic Elastic

P2

P1

When price fall, quantity supplied falls a lot

Q2Q1

Q2

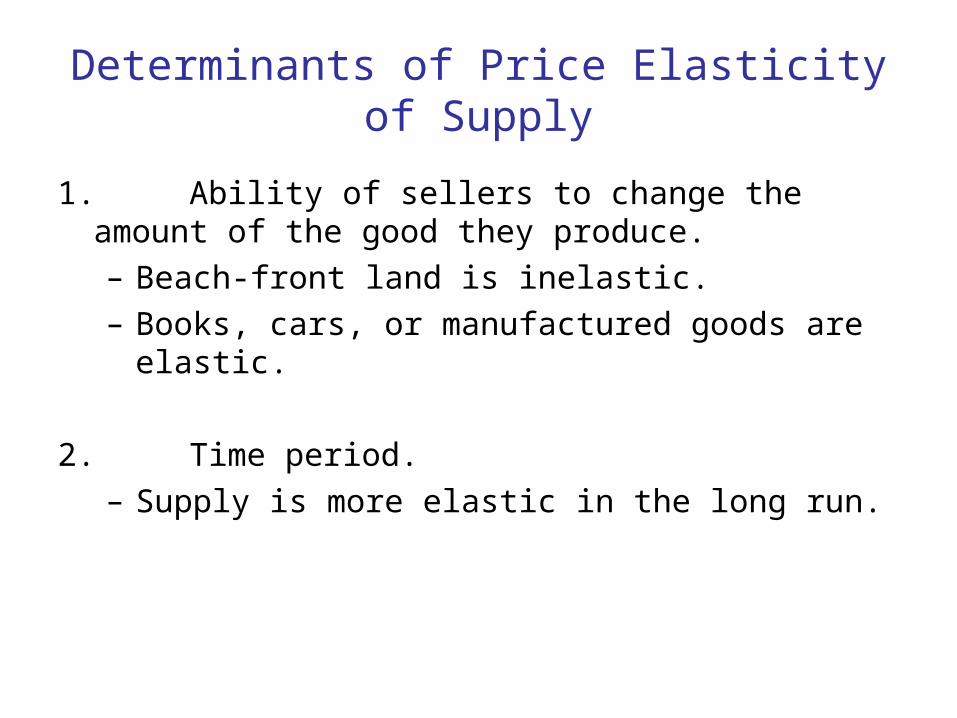

Determinants of Price Elasticity of Supply

1. Ability of sellers to change the amount of the good they produce.

– Beach-front land is inelastic.

– Books, cars, or manufactured goods are elastic.

2. Time period.

– Supply is more elastic in the long run.