edible oils in south africa - fmcg suppliers · pdf fileedible oils in south africa food 2012...

TRANSCRIPT

Media

Feedback

Edible Oils

in South Africa

Food 2012

Product Definitions

2

Product Definition

General Purpose Oils

A vegetable oil is a fat of vegetable origin which is liquid at room temperature. In

South Africa, oils labelled “pure” are from one single vegetable source whereas

those labelled “vegetable” are blends of two or more vegetable oil types. There are

three main methods of oil preparation:

• Cold Press

• Centrifugation

• Solvent Extraction

In South Africa, cooking oil is normally made from sunflower oil, but blends with

other oil, such as maize or peanut, are also produced.

Pan Release Agents

Non-stick pan release sprays are used to stop food from sticking to the cookware.

Retail products are marketed as aerosols but industrial consumers make use of a

liquid preparation.

Speciality Oils

This category comprises mainly olive oil. Unlike most seed oils, olive oil can be

consumed in its natural and completely unrefined state, thus retaining all its

natural healthfulness and flavour without the addition of preservatives or

colourants.

3

• The edible oil market remains a staple food, that has shown consistent growth. General purpose oils

form the bulk of the market volumes

• Demand for general purpose oil is highest within the retail sector. Although the channel did not see

retail growth in the last year, there was an increase in industrial and wholesale consumption, which are

relatively equal in volume.

• The pan release agents market has remained stable and is expected to continue to do so in the short

term. The market is divided into two. Firstly, the retail aerosol sprays for home use, with the

introduction in the last few years of olive oil based products, as well as non-salty versions for dessert

applications. And secondly, bulk liquid release agents for industrial use

• Speciality oils saw volume growth in the last year, but much of this was driven by the increase in

lower priced olive oil/seed blends. Many consumers are unaware of the difference and it is believed

that the much lower price of these blends has contributed to the increased demand

Market Trends

Total Market Volume

Edible Oils - 2011

4

98.4%

0.4% 1.2%

General Purpose Oils

Pan Release Agents

Speciality Oils

Channel Distribution of

Edible Oils - 2011

5

8.6%

3.3%

20.2%

41.9%

26.0%

Export

Foodservices Direct

Industrial

Retail

Wholesale

Local Regional Distribution of

Edible Oils - 2011

6 Note: Excludes exports

Percentages may not add to 100%, due to rounding

6.0%

3.7%

33.0%

38.0%

3.1%

3.2%

2.1% 2.1%

8.5%

Eastern Cape

Free State

Gauteng

KwaZulu-Natal

Limpopo Province

Mpumalanga

North West Province

Northern Cape

Western Cape

Packaging Demand Pack Size

General Purpose Oils - 2011

7

20.8%

1.7%

3.7%

24.4% 19.6%

18.2%

11.6%

750ml or less

1 Litre

1.5 Litres

2 Litres - 4 Litres

5 Litres

10 Litres - 25 Litres

Bulk/As Required

Packaging Demand Pack Type

General Purpose Oils - 2011

8

1.5% 10.5%

0.2%

87.8%

Bag in Box

Bulk/As Required

Can/Glass

Rigid Plastic

Packaging Demand Pack Size

Pan Release Agents - 2011

9

32.7%

67.3%

500ml or less

25 Litres

Packaging Demand Pack Type

Release Agents - 2011

10

67.3%

32.7%

Bulk/As Required

Tin

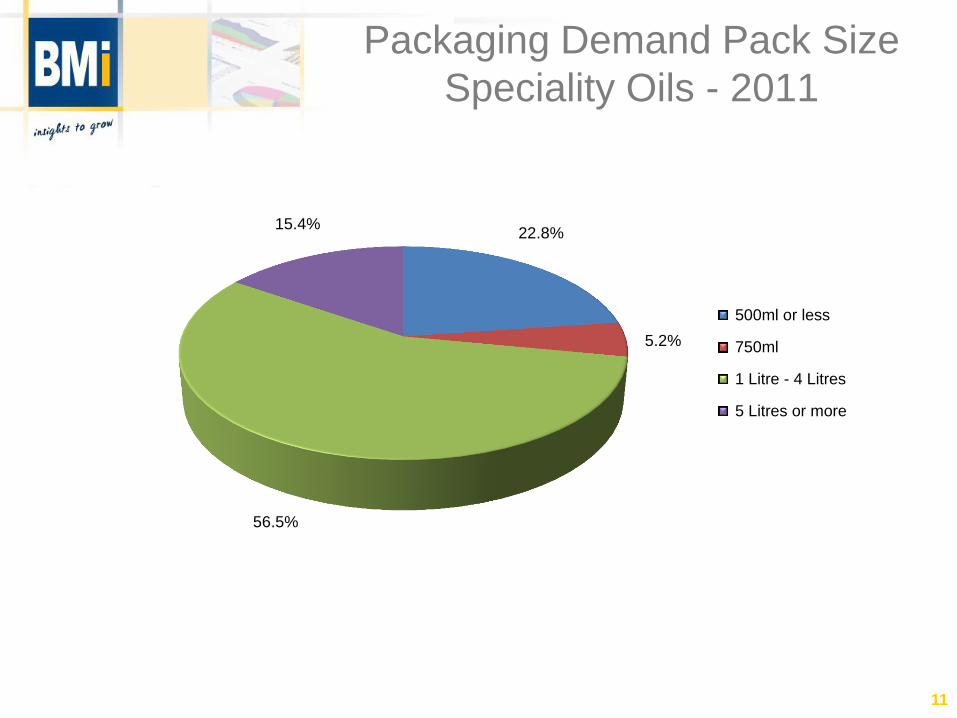

Packaging Demand Pack Size

Speciality Oils - 2011

11

22.8%

5.2%

56.5%

15.4%

500ml or less

750ml

1 Litre - 4 Litres

5 Litres or more

Packaging Demand Pack Type

Speciality Oils - 2011

12

0.2%

42.6%

29.9%

27.3%

Bag in Box

Glass

Rigid Plastic

Tin

BMI Research

Information

13

Annual Quantifications

Total Market Quantification for 140 CPG Categories

What are the latest market trends? And:

• Is the category growing or declining?

• What does the future hold for the category?

• What are packaging trends for the market?

• Are category sales growing or declining in retail, wholesale or export?

• How is your product performing in foodservices?

Market Quantification involves sizing up markets annually to see volume, value and consumption trends.

The service is available for most food, beverage, confectionery and snack products. We have more than

10 years of historical data in tracking each market. Using these insights, you’re able to harness the

potential in your market by understanding strategic category trends across the total market.

A unique offering incorporating formal and informal market components.

Total market includes retail, wholesale, foodservices, industrial and exports.

14

BMI Tracking Report Schedule

2012

Non-Alcoholic

Beverages

Bottled Water

Carbonated Soft Drinks

Cordials and Squashes

Fruit Juice

Iced Tea

Mague

Sport Drinks and Energy Drinks

Dairy Beverages

Dairy Juice Blends

Drinking Yoghurt

Flavoured Milk

Maas

Milk

For further enquiries please contact [email protected]

REPORT NAME PUBLICATION

Packaging

All Reports

Packaging Overview

Paper & Board

QPM

Quarterly Import

Annual Beverage

Reports Full Report (all reports below)

Alcoholic Beverages

Flavoured Alcoholic

Beverages

Malt Beer

Sorghum Beer

Spirits

Wine

REPORT NAME PUBLICATION

15

BMI Tracking Report Schedule

2012 (Cont.)

REPORT NAME PUBLICATION

On Request

Baked Products

Baking Aids

Eggs

Frozen and Par-Baked Products

Maize and Wheat

Premixes

Processed Meat Products

Confectionery and Snacks

Ice Cream

Packaging of Snack Foods

South African Confectionery Market

The Impulse Market in South Africa

For further enquiries please contact [email protected]

REPORT NAME PUBLICATION

Annual Food

Publications

Biscuits and Rusks

Breakfast Foods, Pasta and Rice

Dairy

Desserts

F&C Beverages

Fats and Oils

Pre-prepared Meals

Protein

Sauces

Soups and Condiments

Sweet and Savoury Spreads

Value Added Meals

16

ISOS

(In Store Observation Services)

How is your brand performing in-store?

Every week, we answer questions like:

• Is my product available on shelf?

• Does my brand have its fair share of shelf space?

• Is my product listed and available in all stores?

• Is my gondola end in store?

• Do I have promotional activity in that particular store?

ISOS: Gives first-hand insight into your brand’s performance in-store. Monitor your products versus your

competitors’ to assess your performance and remedy gaps. Ensure accurate data which translates into

tactical competitive advantages.

17

Print Ads Promotional

Pricing and Share of Spend

Is your product visible enough in promotional print Media?

Assess whether your brand is gaining sufficient share, relative to your spend on promotional print

advertising. Track competitor promotional pricing to tactically react on your own product pricing.

Daily, we answer questions like:

• What is the promotional pricing?

• What is the regional promotional pricing variance?

• What are competitors’ pricing tactics?

• What Rand value is spent on our brand versus competitor brands by retailers?

• Are we losing market share because of this?

Coverage:

• National daily and weekly newspapers

• Weekly community newspapers

• Consumer magazines

• In-store broadsheets

Print Ads: Covers all brands advertised in all regions by retailer by month. The analysis provides an inside

picture of the retail promotional environment. Track competitor promotions and pricing, offering top line or

granular data.

18

Commissioned Research

Need to investigate the market regarding other issues?

If your research need is not covered by our standard set of services, we will tailor-make a study specifically

for you.

BMI’s Commissioned Research is designed specifically to answer your questions in your particular

market. From industrial assessments to traditional consumer studies, we have the expertise to grow your

business.

These may include:

• Consumer Research

• Qualitative Research including Focus Groups and In-depth discussions

• Quantitative Research solutions across various target markets

• Service Quality Measurement (SQM)

• Pack Type Testing and Preference

• Product Testing includes taste tests and new product development

19

LISP

(Liquor In Store Pricing)

How is your liquor brand performing in-store?

Each week, we answer questions like:

• Is my product available on shelf?

• Does my brand have its fair share of shelf space?

• Is my product listed and available in all stores?

• Is my gondola end in store?

• Do I have promotional activity in that particular store?

LISP: Gives first-hand insight into your brand’s performance in-store. Monitor your products versus your

competitors to assess your performance and remedy gaps. Ensuring accurate data which translates into

tactical competitive advantage.

20

Consumer Research

Getting into the hearts and minds of Consumers through interaction, stimulation and discussion.

Qualitative and Quantitative solutions including:

• Focus groups

• Depth interviews

• Workshops

• Store visits

• In home visits

• Consumer surveys

• Online research

• Mystery shopping

• International project management

BMI Research: Consumer Division has a passionate focus on consumer behaviour, combining professional

skills with optimal technology and products to complement insights. Project teams are hand picked based

on their knowledge and expertise of the subject matter and offers a range of research methodologies that

aim to give you a multi-dimensional and insightful solution to the understanding of your product/brand. The

division has the ability to draw on BMI Research’s established experience in the retail and wholesale

sectors, providing a unique and customized solution to understanding consumer behaviour.

21

For further information please

contact

BMI Research

(Pty) Ltd

Tel: +27 11 615 7000

Fax: +27 11 615 4999

Email: [email protected]

Visit our website on

www.bmi.co.za

22

Copyright and Disclaimer:

All rights reserved. No part of this

publication may be reproduced,

photocopied or transmitted in any

form, nor may any part of this report

be distributed to any person not a full-

time employee of the Subscriber,

without the prior written consent of

the Consultants. The Subscriber

agrees to take all reasonable

measures to safeguard this

confidentiality.

NOTE:

Although great care has been taken

to ensure accuracy and completeness

in this project, no legal responsibility

can be accepted by BMI for the

information and opinions expressed in

this report.

Copyright © 2012

BMI Research (Pty) Ltd

Reg No. 2008/004751/07

23