e-filing of income tax return - live on vrindavan tvestv.in/icai/20072017/ppt.pdfe-filing of income...

TRANSCRIPT

e-filing of Income tax return

CA. D K Bholusaria

Disclaimer

This presentation has been prepared for academic use only for sharing knowledge on the subject. Though every effort has been made to avoid errors or omissions in this presentation yet any error or omission may creep in.

It is suggested that to avoid any doubt the user should cross check the correctness of text, contents and the law with the original documents and to dispel confusion should seek professional help/opinion.

2

Agenda

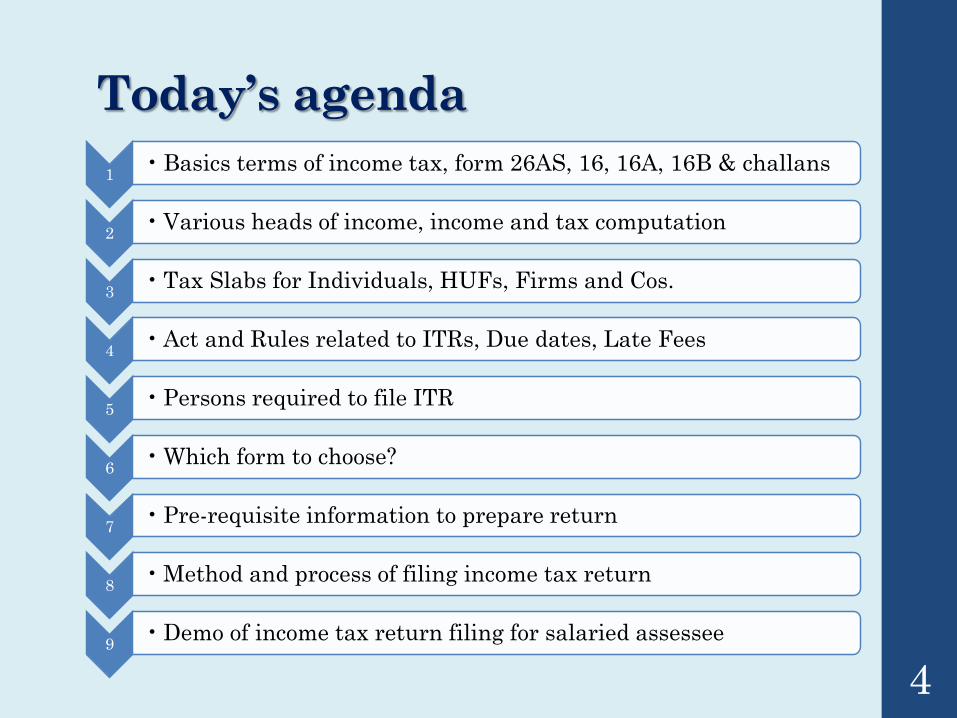

Today’s agenda

1• Basics terms of income tax, form 26AS, 16, 16A, 16B & challans

2• Various heads of income, income and tax computation

3• Tax Slabs for Individuals, HUFs, Firms and Cos.

4• Act and Rules related to ITRs, Due dates, Late Fees

5• Persons required to file ITR

6• Which form to choose?

7• Pre-requisite information to prepare return

8• Method and process of filing income tax return

9• Demo of income tax return filing for salaried assessee

4

Let’s start with some basic concepts…

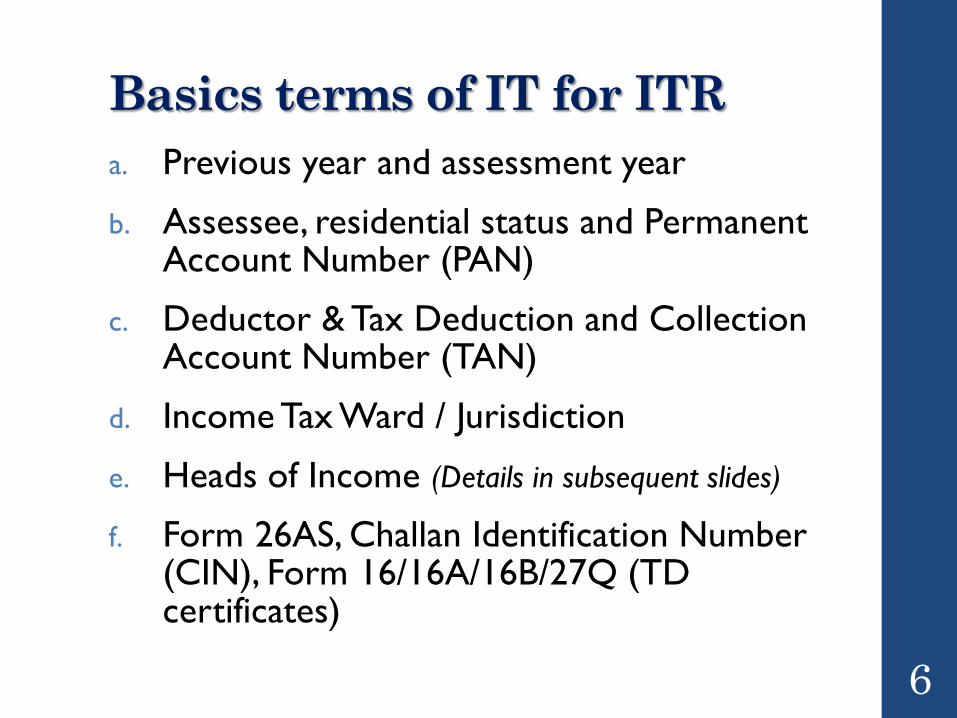

Basics terms of IT for ITR

a. Previous year and assessment year

b. Assessee, residential status and Permanent Account Number (PAN)

c. Deductor & Tax Deduction and Collection Account Number (TAN)

d. Income Tax Ward / Jurisdiction

e. Heads of Income (Details in subsequent slides)

f. Form 26AS, Challan Identification Number (CIN), Form 16/16A/16B/27Q (TD certificates)

6

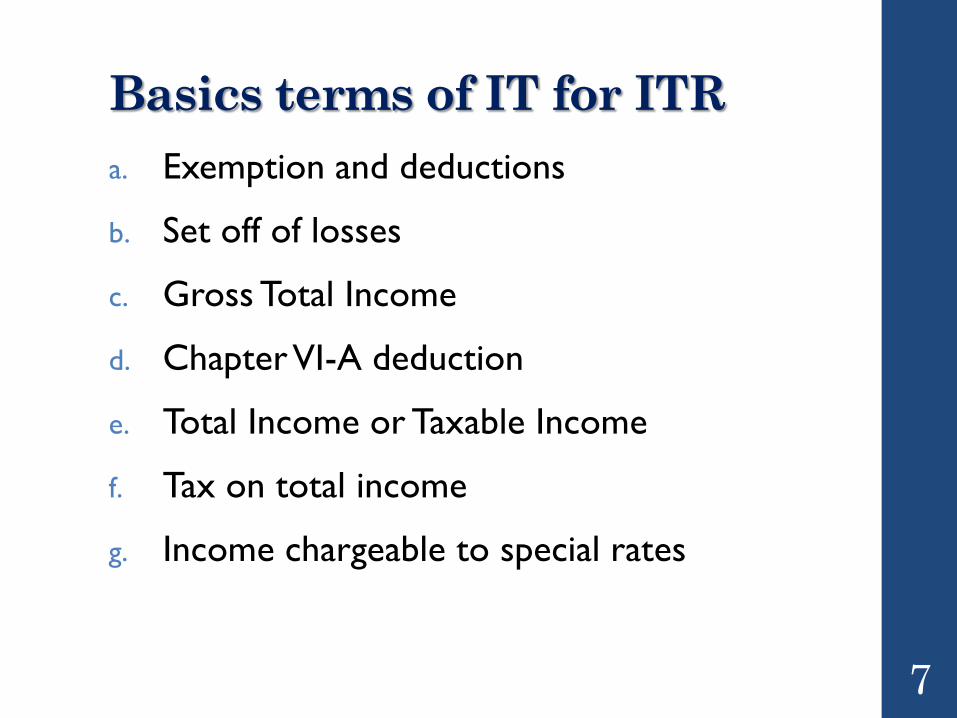

Basics terms of IT for ITR

a. Exemption and deductions

b. Set off of losses

c. Gross Total Income

d. Chapter VI-A deduction

e. Total Income or Taxable Income

f. Tax on total income

g. Income chargeable to special rates

7

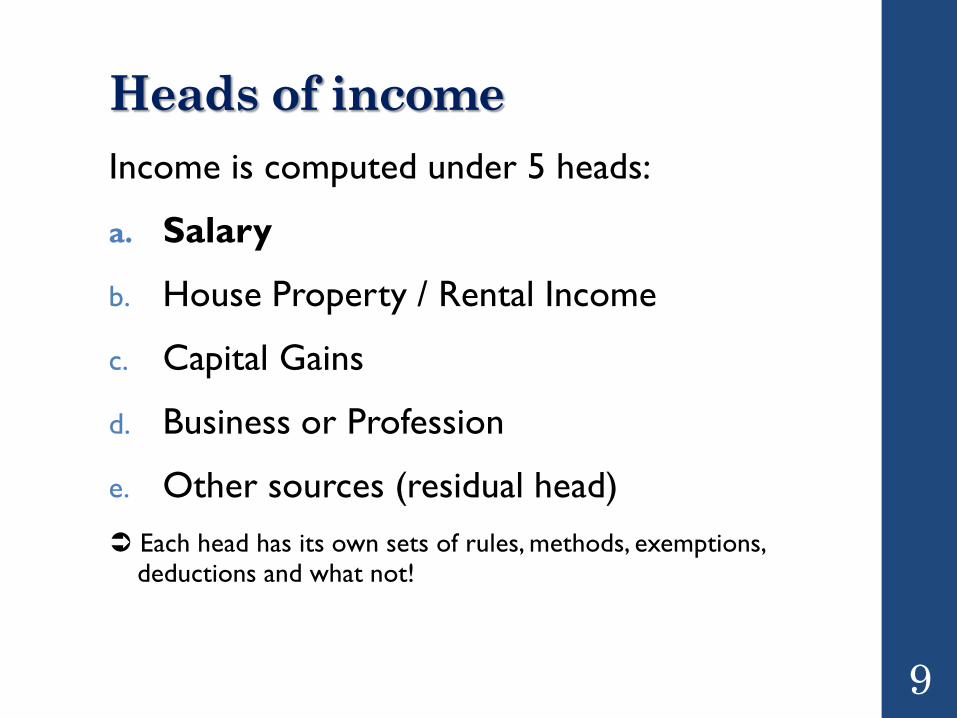

Heads of income

Heads of income

Income is computed under 5 heads:

a. Salary

b. House Property / Rental Income

c. Capital Gains

d. Business or Profession

e. Other sources (residual head)

Each head has its own sets of rules, methods, exemptions, deductions and what not!

9

Tax slabs

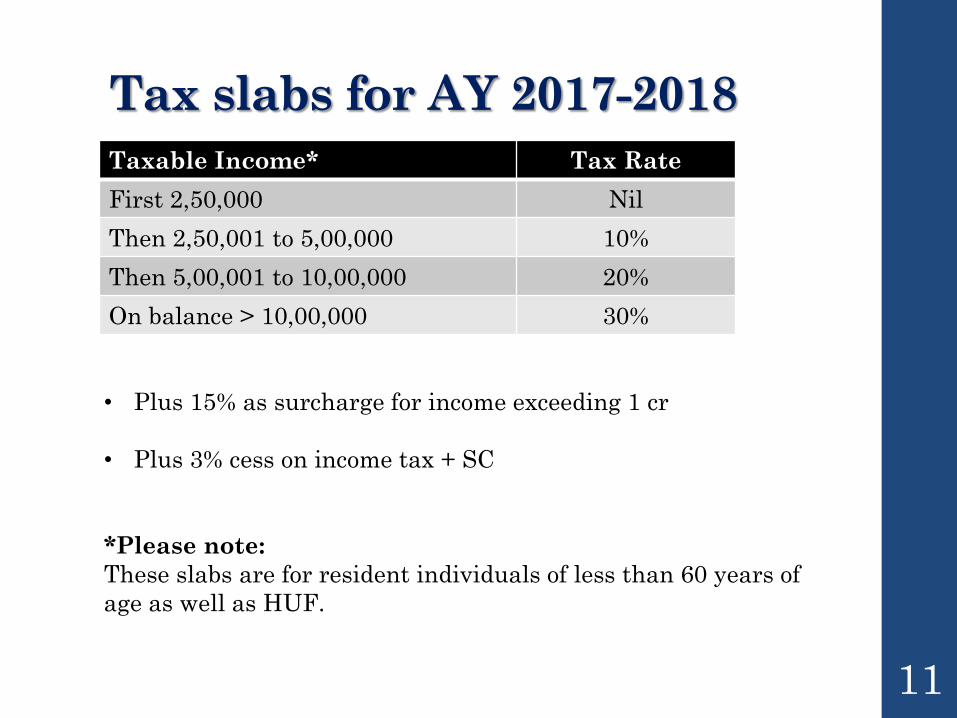

Tax slabs for AY 2017-2018

Taxable Income* Tax Rate

First 2,50,000 Nil

Then 2,50,001 to 5,00,000 10%

Then 5,00,001 to 10,00,000 20%

On balance > 10,00,000 30%

• Plus 15% as surcharge for income exceeding 1 cr

• Plus 3% cess on income tax + SC

*Please note:

These slabs are for resident individuals of less than 60 years of

age as well as HUF.

11

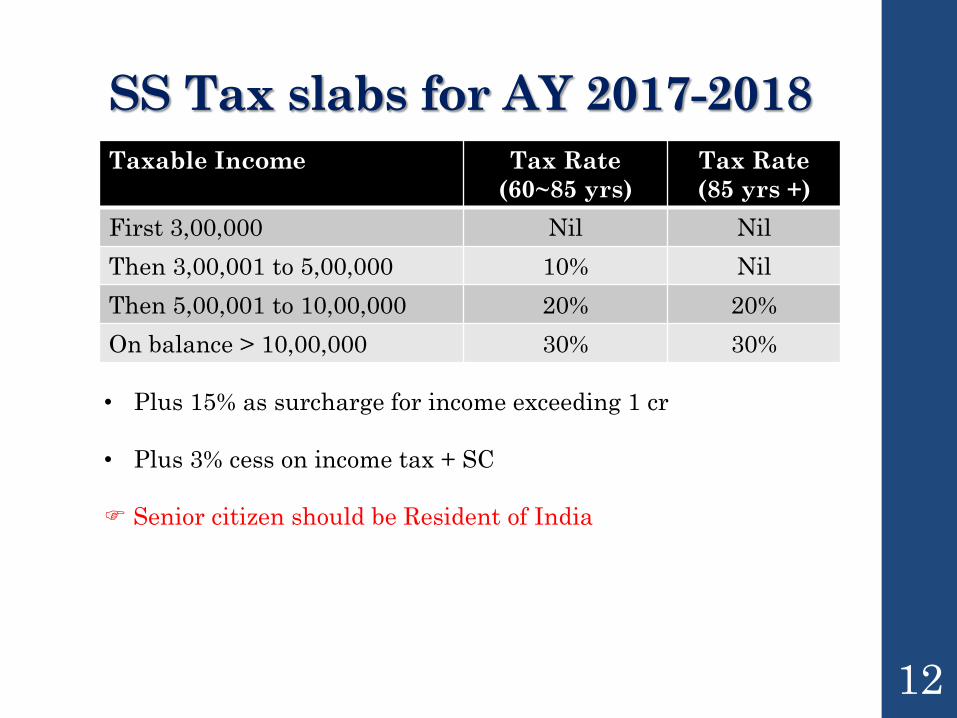

SS Tax slabs for AY 2017-2018

Taxable Income Tax Rate

(60~85 yrs)

Tax Rate

(85 yrs +)

First 3,00,000 Nil Nil

Then 3,00,001 to 5,00,000 10% Nil

Then 5,00,001 to 10,00,000 20% 20%

On balance > 10,00,000 30% 30%

• Plus 15% as surcharge for income exceeding 1 cr

• Plus 3% cess on income tax + SC

Senior citizen should be Resident of India

12

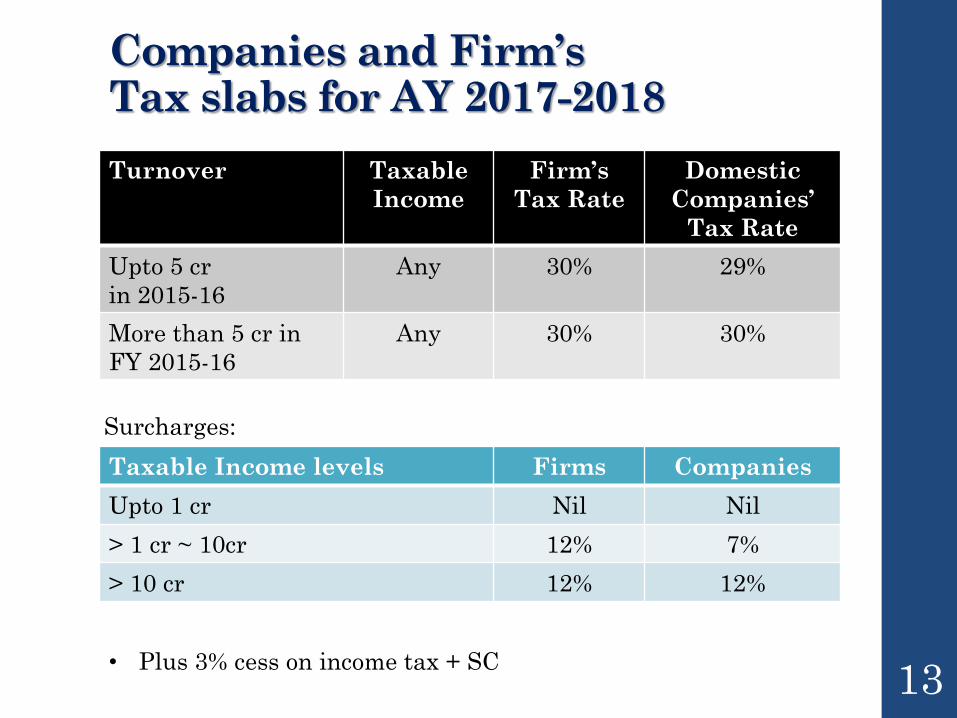

Companies and Firm’s Tax slabs for AY 2017-2018

Turnover Taxable

Income

Firm’s

Tax Rate

Domestic

Companies’

Tax Rate

Upto 5 cr

in 2015-16

Any 30% 29%

More than 5 cr in

FY 2015-16

Any 30% 30%

13

Taxable Income levels Firms Companies

Upto 1 cr Nil Nil

> 1 cr ~ 10cr 12% 7%

> 10 cr 12% 12%

Surcharges:

• Plus 3% cess on income tax + SC

Income under salary

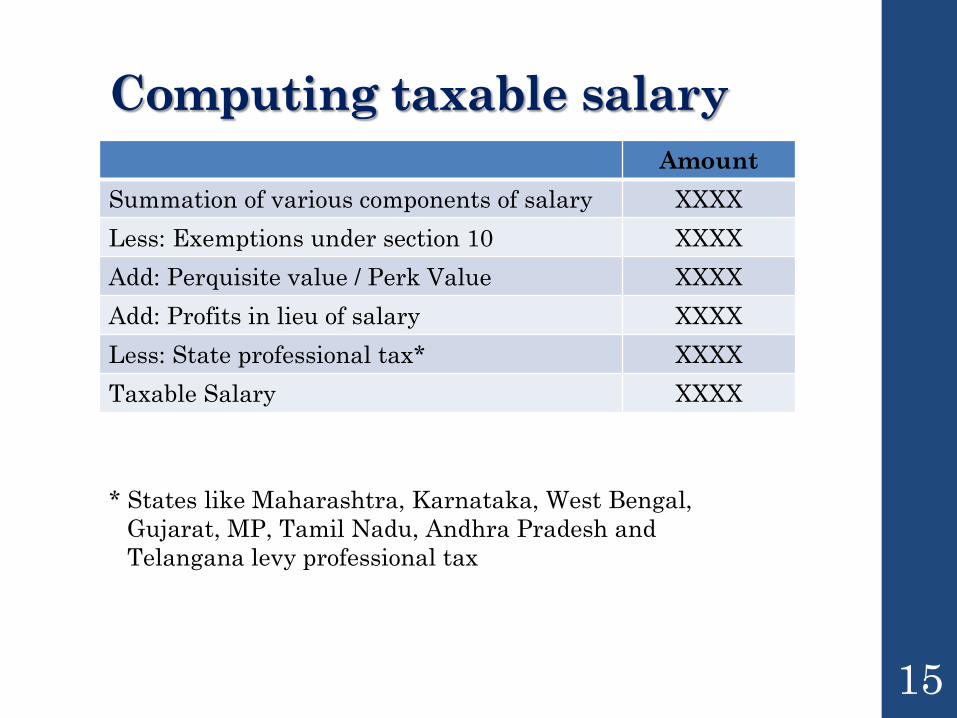

Computing taxable salary

Amount

Summation of various components of salary XXXX

Less: Exemptions under section 10 XXXX

Add: Perquisite value / Perk Value XXXX

Add: Profits in lieu of salary XXXX

Less: State professional tax* XXXX

Taxable Salary XXXX

* States like Maharashtra, Karnataka, West Bengal,

Gujarat, MP, Tamil Nadu, Andhra Pradesh and

Telangana levy professional tax

15

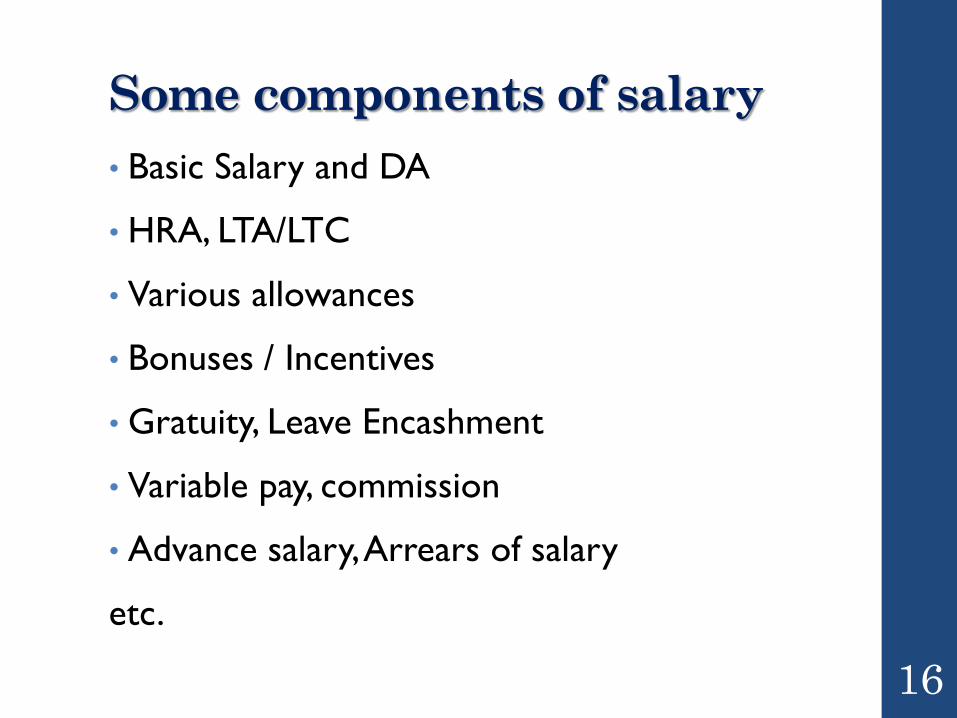

Some components of salary

• Basic Salary and DA

• HRA, LTA/LTC

• Various allowances

• Bonuses / Incentives

• Gratuity, Leave Encashment

• Variable pay, commission

• Advance salary, Arrears of salary

etc.

16

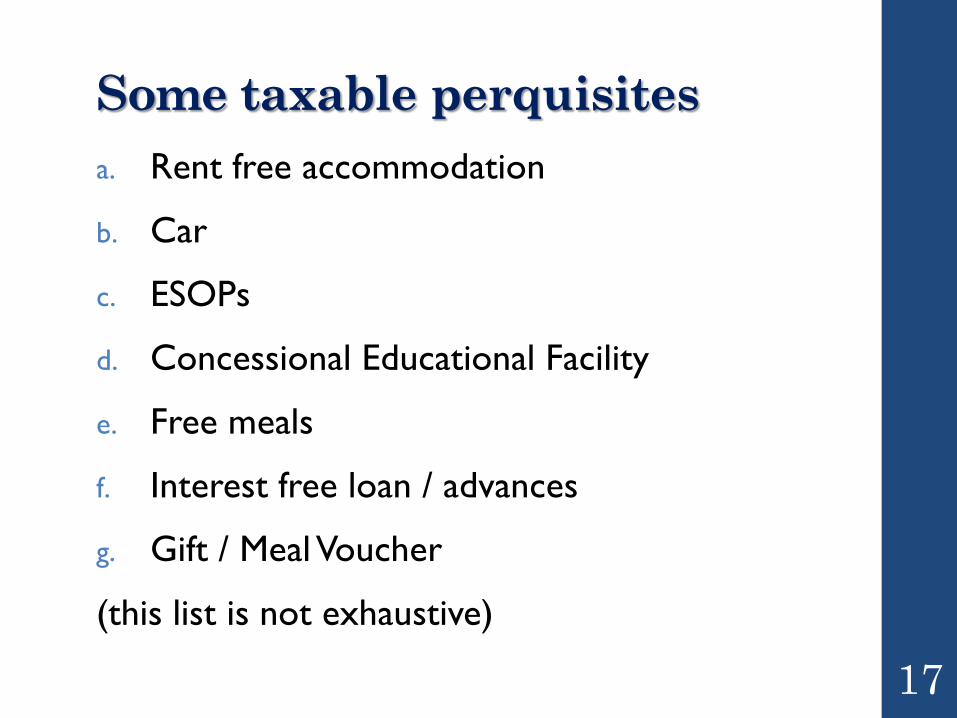

Some taxable perquisites

a. Rent free accommodation

b. Car

c. ESOPs

d. Concessional Educational Facility

e. Free meals

f. Interest free loan / advances

g. Gift / Meal Voucher

(this list is not exhaustive)

17

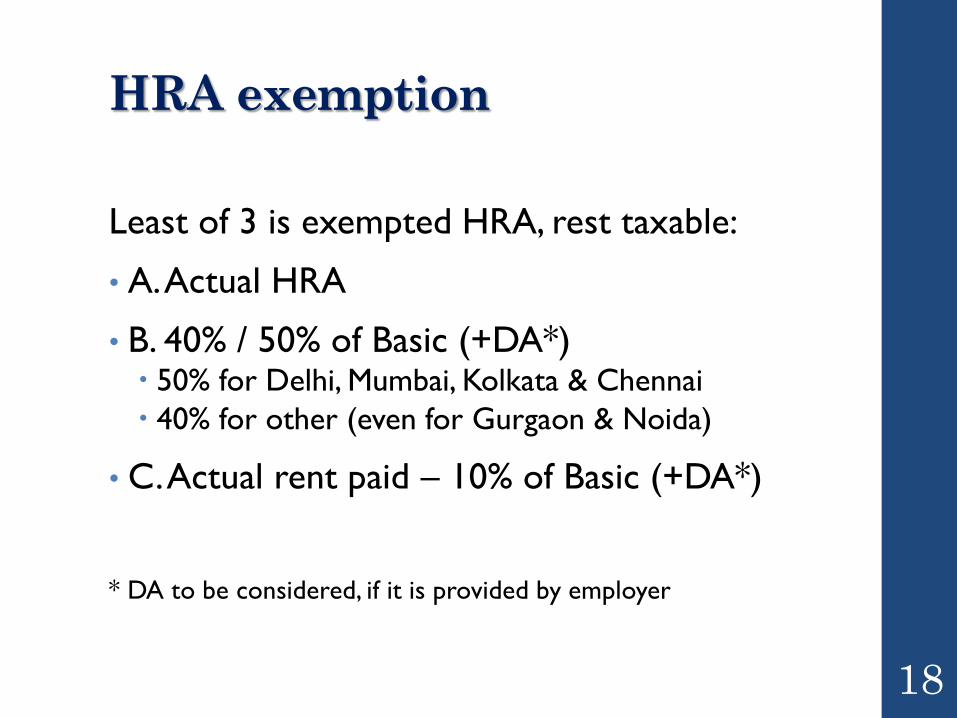

HRA exemption

Least of 3 is exempted HRA, rest taxable:

• A. Actual HRA

• B. 40% / 50% of Basic (+DA*) 50% for Delhi, Mumbai, Kolkata & Chennai

40% for other (even for Gurgaon & Noida)

• C. Actual rent paid – 10% of Basic (+DA*)

* DA to be considered, if it is provided by employer

18

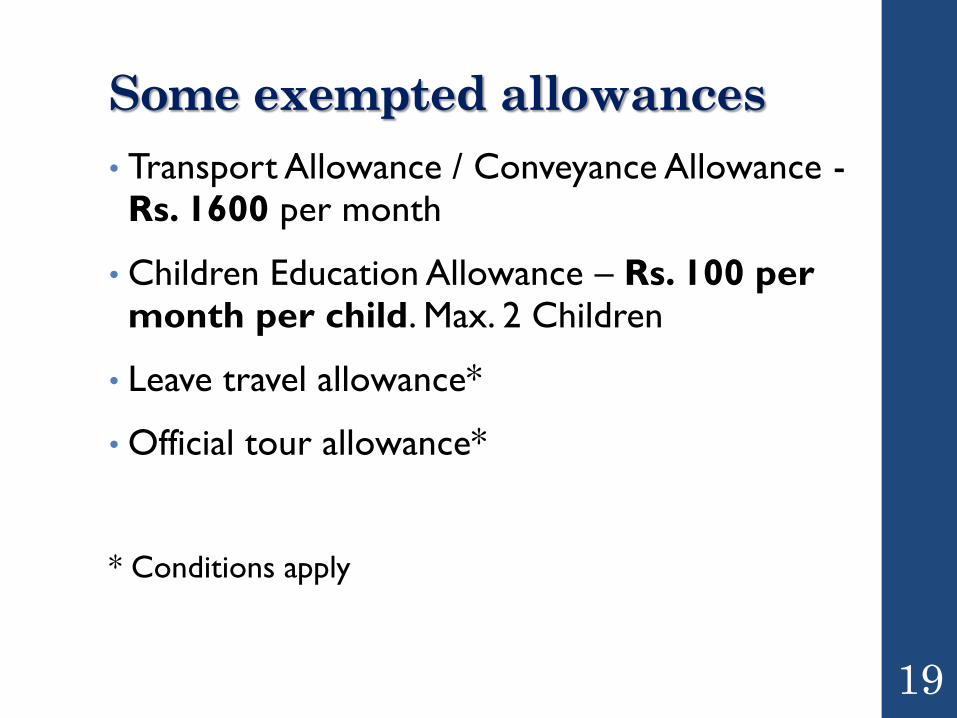

Some exempted allowances

• Transport Allowance / Conveyance Allowance -Rs. 1600 per month

• Children Education Allowance – Rs. 100 per month per child. Max. 2 Children

• Leave travel allowance*

• Official tour allowance*

* Conditions apply

19

Taxable income

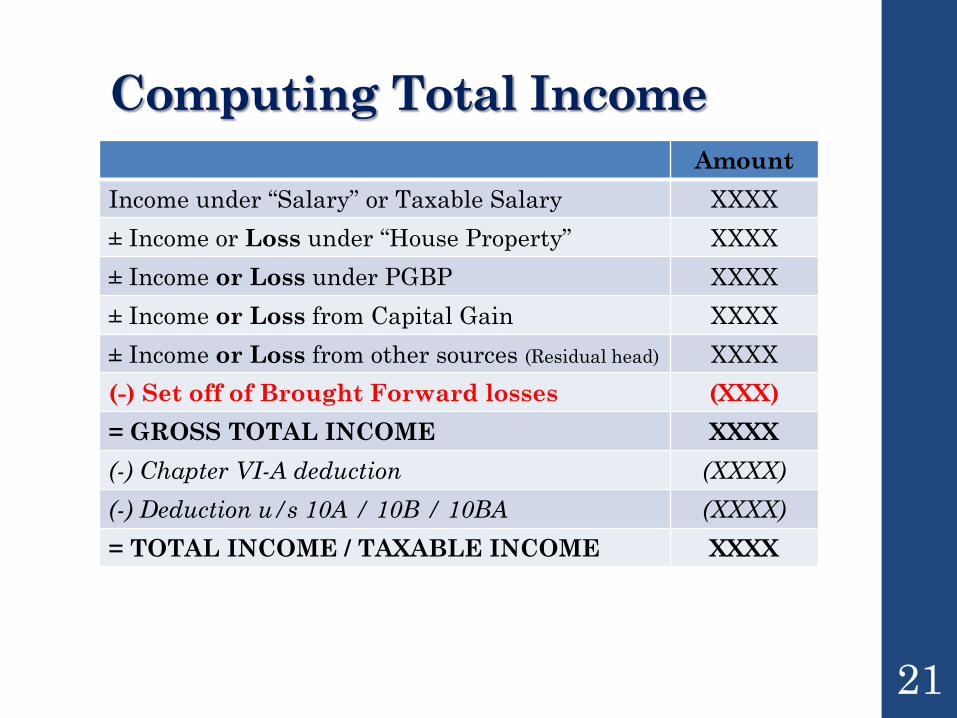

Computing Total Income

Amount

Income under “Salary” or Taxable Salary XXXX

± Income or Loss under “House Property” XXXX

± Income or Loss under PGBP XXXX

± Income or Loss from Capital Gain XXXX

± Income or Loss from other sources (Residual head) XXXX

(-) Set off of Brought Forward losses (XXX)

= GROSS TOTAL INCOME XXXX

(-) Chapter VI-A deduction (XXXX)

(-) Deduction u/s 10A / 10B / 10BA (XXXX)

= TOTAL INCOME / TAXABLE INCOME XXXX

21

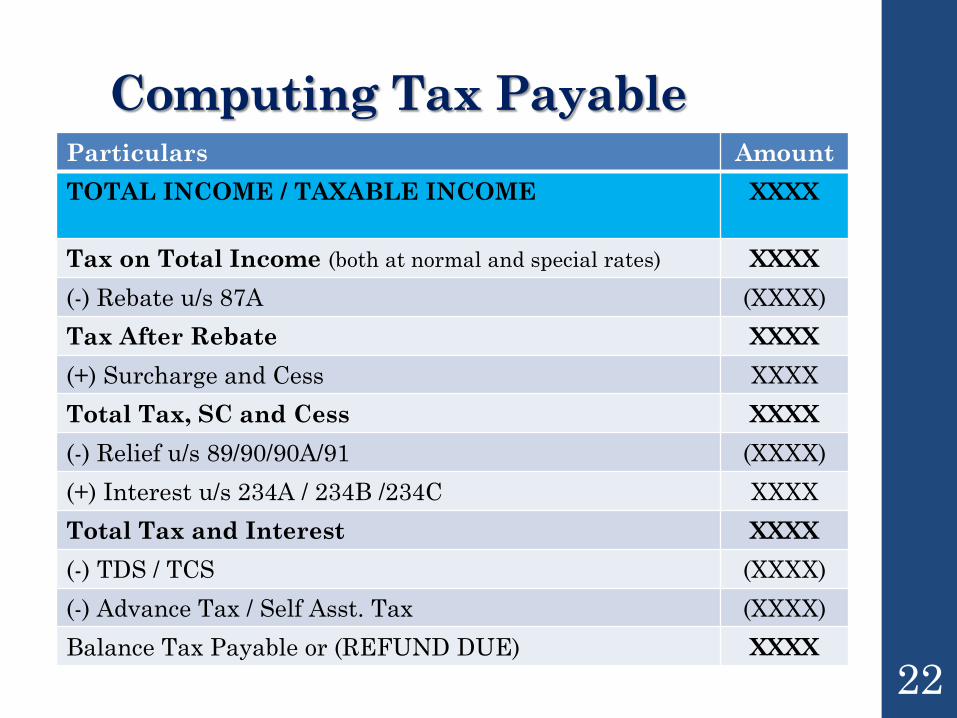

Computing Tax PayableParticulars Amount

TOTAL INCOME / TAXABLE INCOME XXXX

Tax on Total Income (both at normal and special rates) XXXX

(-) Rebate u/s 87A (XXXX)

Tax After Rebate XXXX

(+) Surcharge and Cess XXXX

Total Tax, SC and Cess XXXX

(-) Relief u/s 89/90/90A/91 (XXXX)

(+) Interest u/s 234A / 234B /234C XXXX

Total Tax and Interest XXXX

(-) TDS / TCS (XXXX)

(-) Advance Tax / Self Asst. Tax (XXXX)

Balance Tax Payable or (REFUND DUE) XXXX

22

Law on ITR in brief

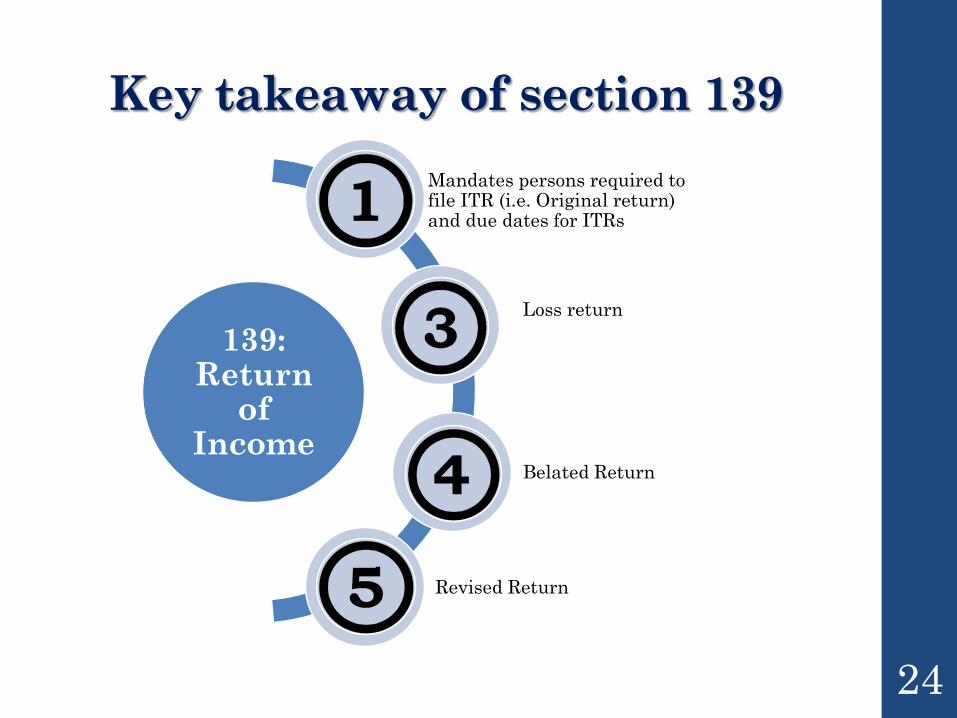

Key takeaway of section 139

139: Return

of Income

Mandates persons required to file ITR (i.e. Original return) and due dates for ITRs

Loss return

Belated Return

Revised Return

24

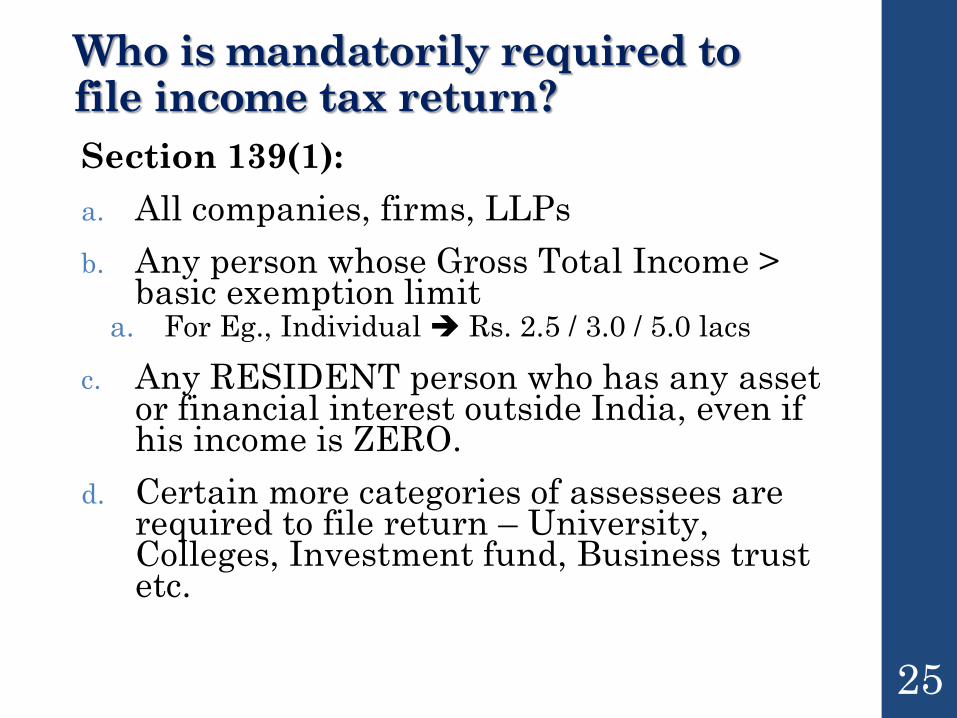

Who is mandatorily required to file income tax return?

Section 139(1):

a. All companies, firms, LLPs

b. Any person whose Gross Total Income > basic exemption limit

a. For Eg., Individual Rs. 2.5 / 3.0 / 5.0 lacs

c. Any RESIDENT person who has any asset or financial interest outside India, even if his income is ZERO.

d. Certain more categories of assessees are required to file return – University, Colleges, Investment fund, Business trust etc.

25

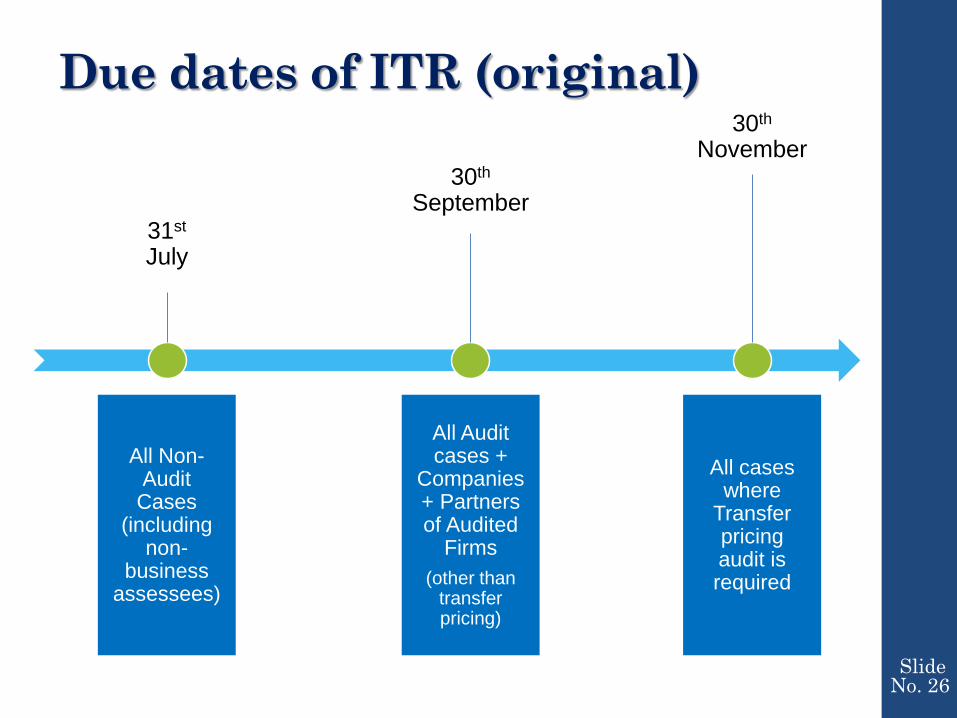

Due dates of ITR (original)

31st

July

30th

September

30th

November

Slide No. 26

All Non-Audit Cases

(including non-

business assessees)

All Audit cases +

Companies + Partners of Audited

Firms

(other than transfer pricing)

All cases where

Transfer pricing audit is required

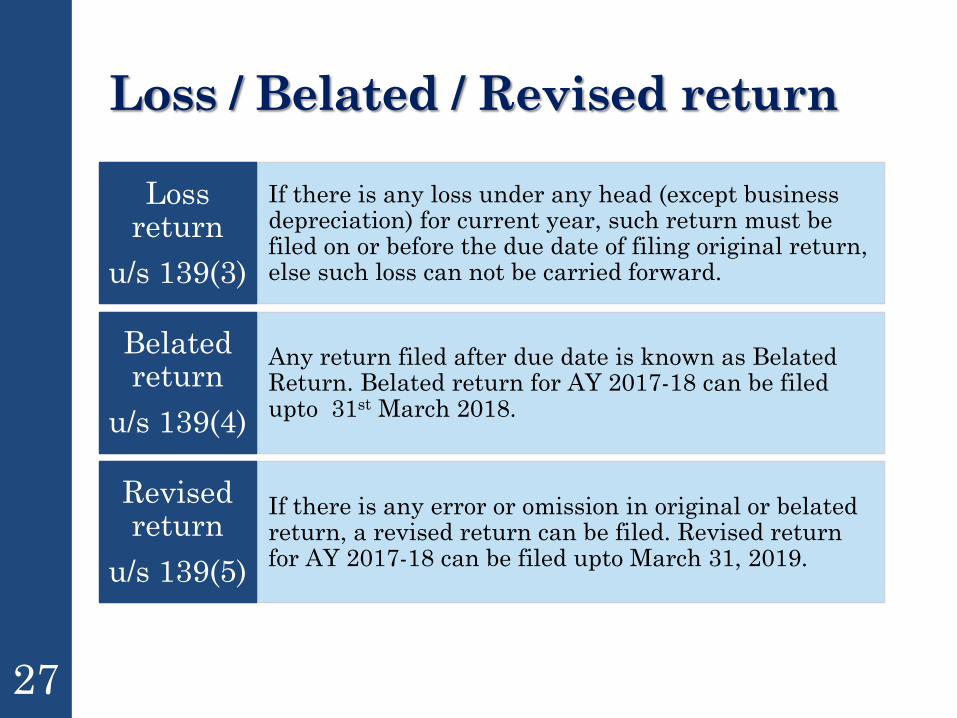

Loss / Belated / Revised return

If there is any loss under any head (except business depreciation) for current year, such return must be filed on or before the due date of filing original return, else such loss can not be carried forward.

Loss return

u/s 139(3)

Any return filed after due date is known as Belated Return. Belated return for AY 2017-18 can be filed upto 31st March 2018.

Belated return

u/s 139(4)

If there is any error or omission in original or belated return, a revised return can be filed. Revised return for AY 2017-18 can be filed upto March 31, 2019.

Revised return

u/s 139(5)

27

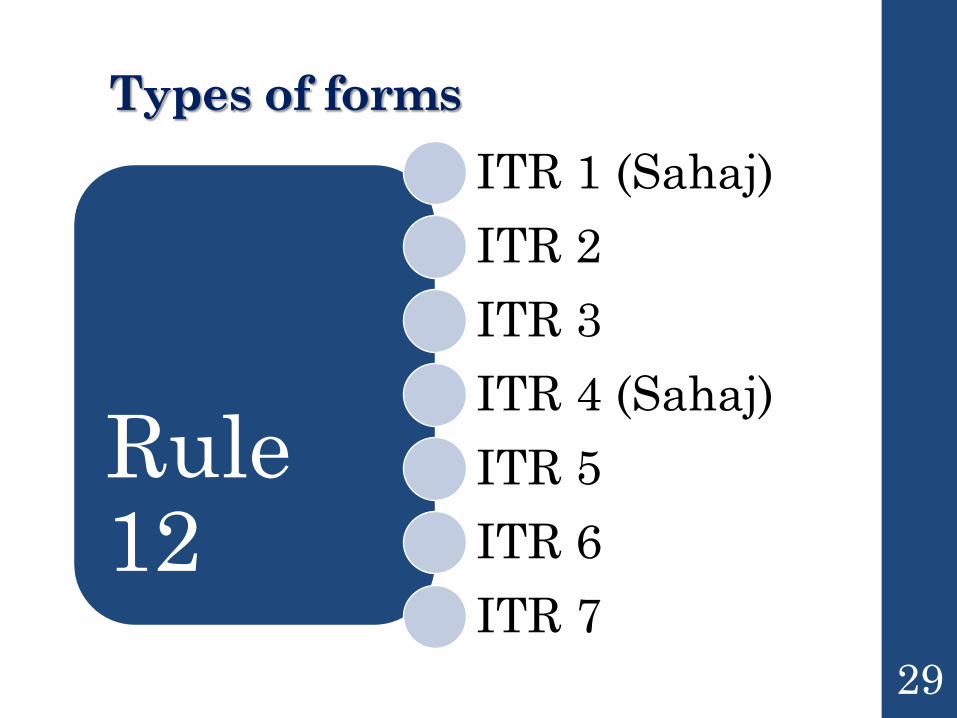

ITR Forms

Types of forms

Rule 12

ITR 1 (Sahaj)

ITR 2

ITR 3

ITR 4 (Sahaj)

ITR 5

ITR 6

ITR 7

29

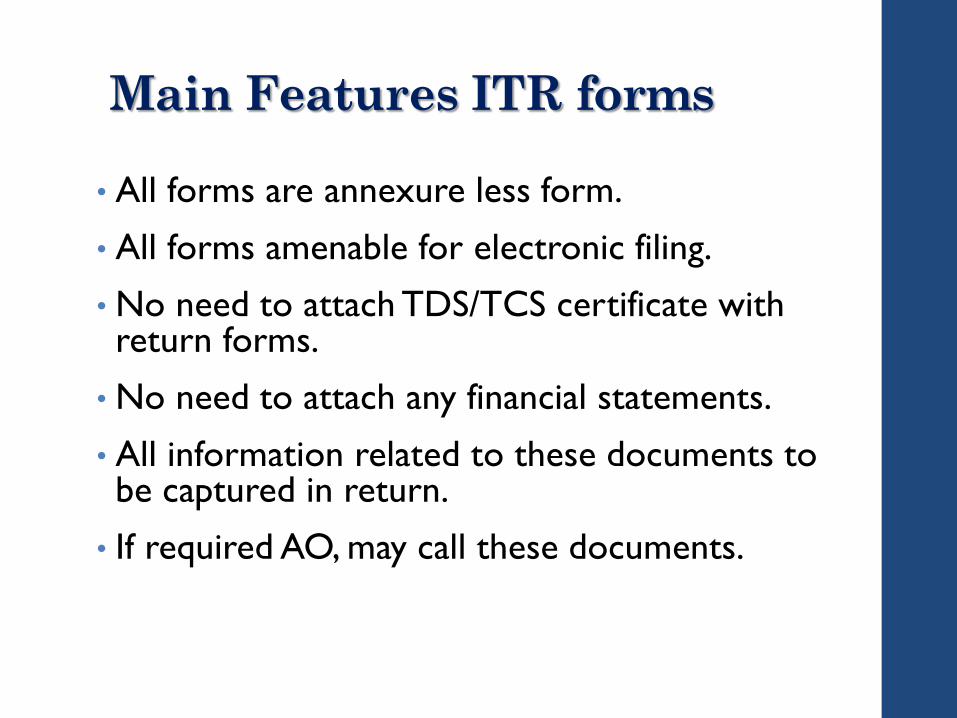

Main Features ITR forms

• All forms are annexure less form.

• All forms amenable for electronic filing.

• No need to attach TDS/TCS certificate with return forms.

• No need to attach any financial statements.

• All information related to these documents to be captured in return.

• If required AO, may call these documents.

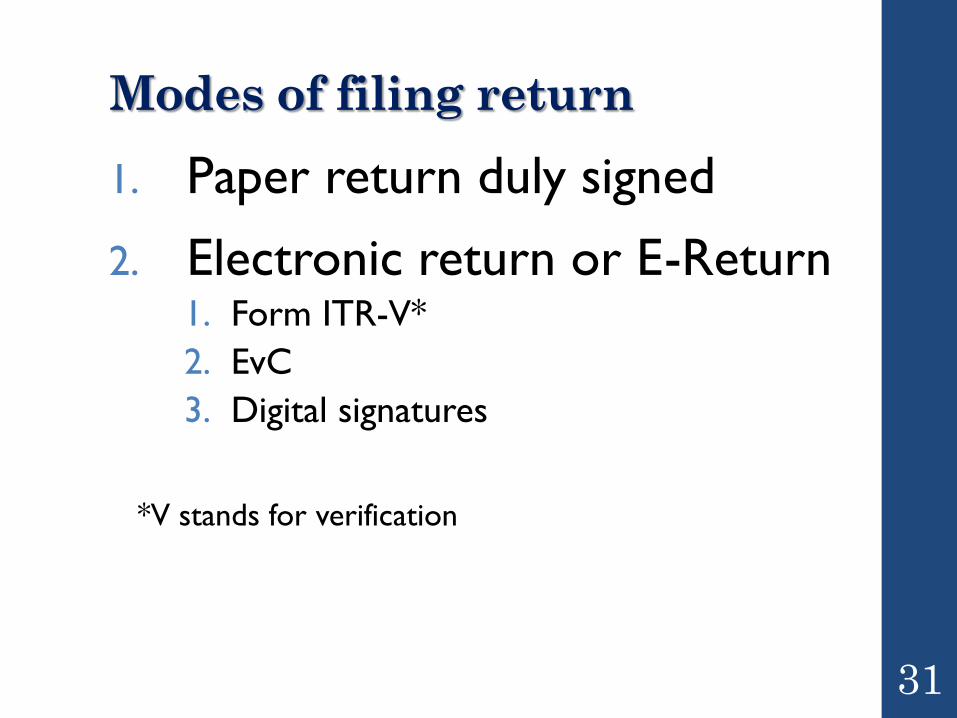

Modes of filing return

1. Paper return duly signed

2. Electronic return or E-Return1. Form ITR-V*

2. EvC

3. Digital signatures

*V stands for verification

31

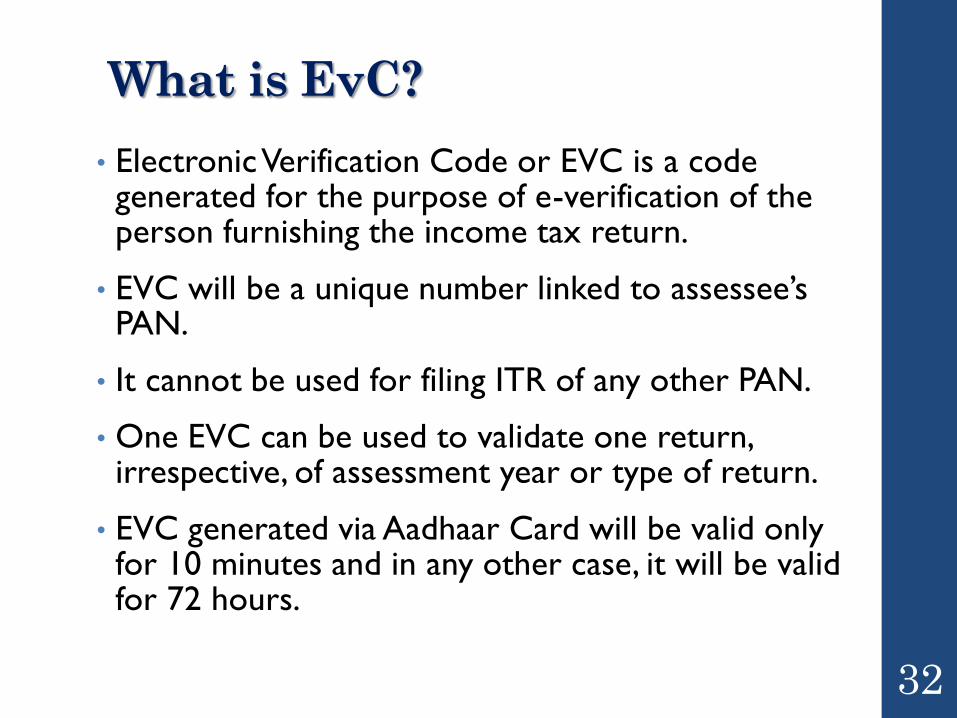

What is EvC?

• Electronic Verification Code or EVC is a code generated for the purpose of e-verification of the person furnishing the income tax return.

• EVC will be a unique number linked to assessee’s PAN.

• It cannot be used for filing ITR of any other PAN.

• One EVC can be used to validate one return, irrespective, of assessment year or type of return.

• EVC generated via Aadhaar Card will be valid only for 10 minutes and in any other case, it will be valid for 72 hours.

32

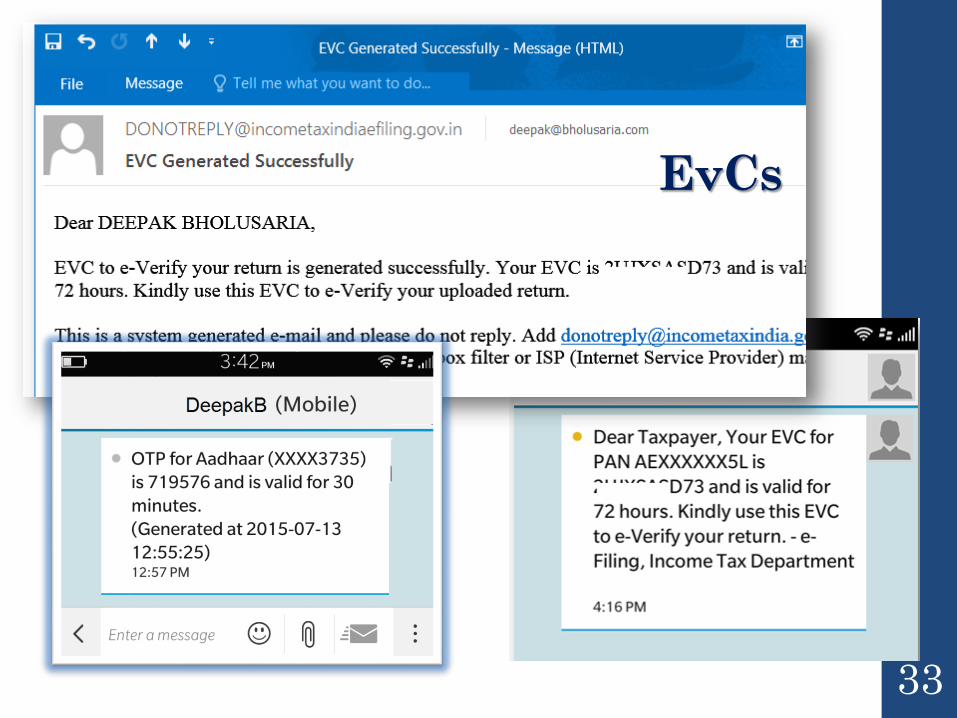

33

EvCs

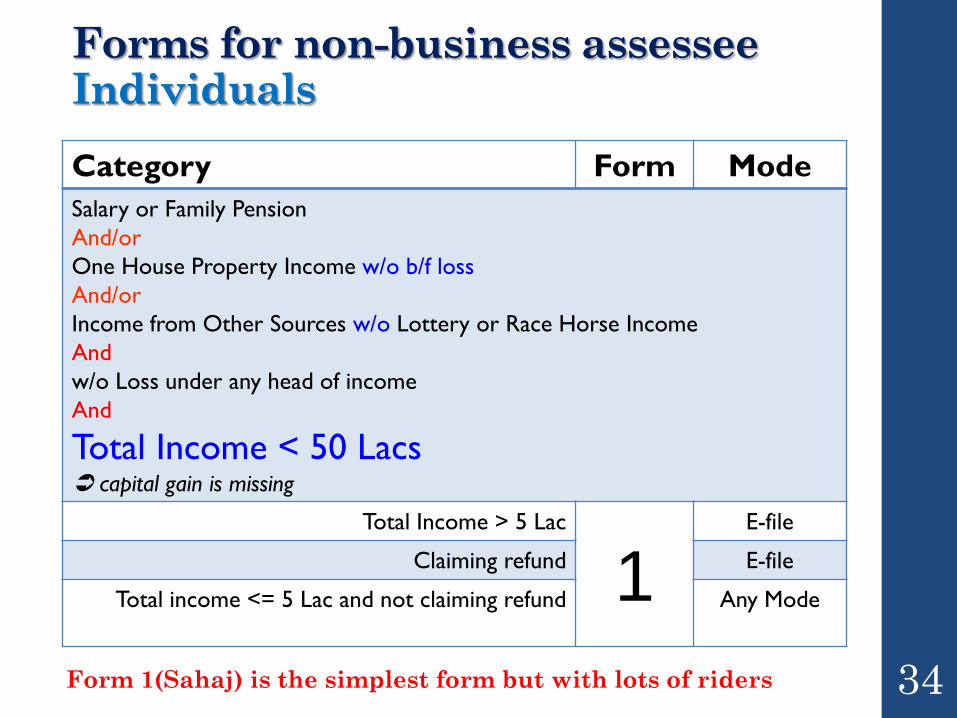

Forms for non-business assesseeIndividuals

Category Form Mode

Salary or Family Pension

And/or

One House Property Income w/o b/f loss

And/or

Income from Other Sources w/o Lottery or Race Horse Income

And

w/o Loss under any head of income

And

Total Income < 50 Lacs capital gain is missing

Total Income > 5 Lac

1E-file

Claiming refund E-file

Total income <= 5 Lac and not claiming refund Any Mode

Form 1(Sahaj) is the simplest form but with lots of riders 34

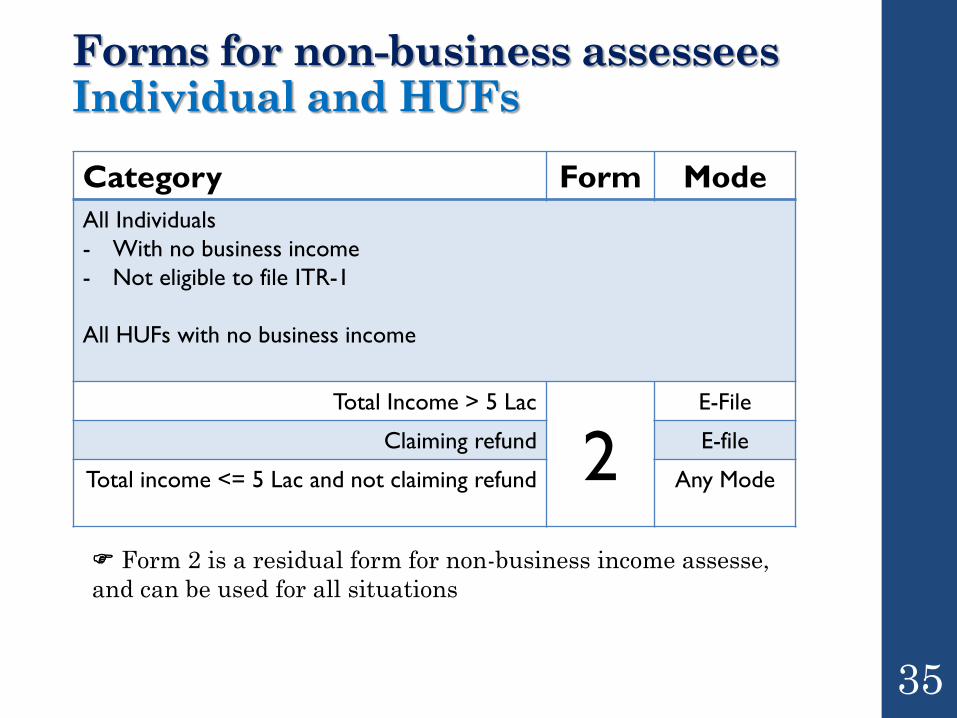

Forms for non-business assesseesIndividual and HUFs

Category Form Mode

All Individuals

- With no business income

- Not eligible to file ITR-1

All HUFs with no business income

Total Income > 5 Lac

2E-File

Claiming refund E-file

Total income <= 5 Lac and not claiming refund Any Mode

Form 2 is a residual form for non-business income assesse,

and can be used for all situations

35

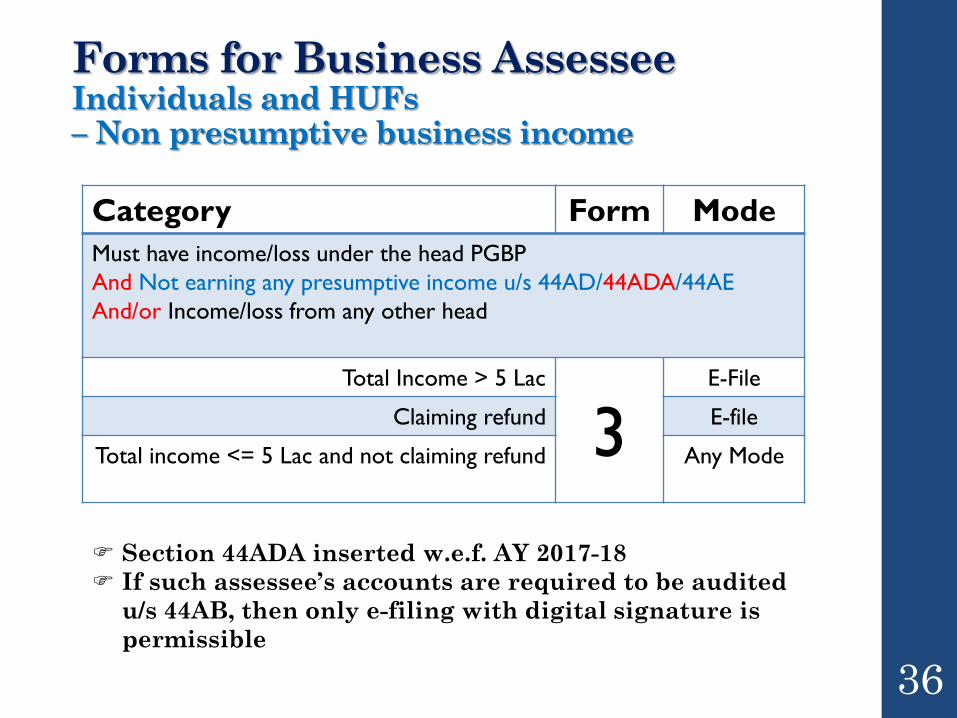

Forms for Business AssesseeIndividuals and HUFs – Non presumptive business income

Category Form Mode

Must have income/loss under the head PGBP

And Not earning any presumptive income u/s 44AD/44ADA/44AE

And/or Income/loss from any other head

Total Income > 5 Lac

3E-File

Claiming refund E-file

Total income <= 5 Lac and not claiming refund Any Mode

Section 44ADA inserted w.e.f. AY 2017-18

If such assessee’s accounts are required to be audited

u/s 44AB, then only e-filing with digital signature is

permissible

36

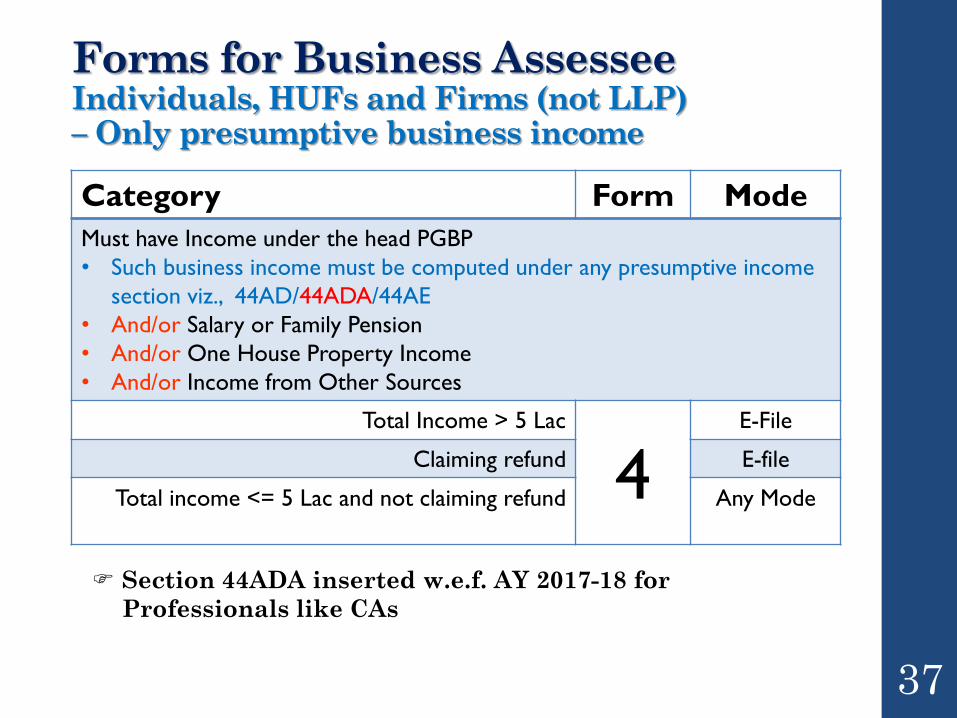

Forms for Business AssesseeIndividuals, HUFs and Firms (not LLP)– Only presumptive business income

Category Form Mode

Must have Income under the head PGBP

• Such business income must be computed under any presumptive income

section viz., 44AD/44ADA/44AE

• And/or Salary or Family Pension

• And/or One House Property Income

• And/or Income from Other Sources

Total Income > 5 Lac

4E-File

Claiming refund E-file

Total income <= 5 Lac and not claiming refund Any Mode

Section 44ADA inserted w.e.f. AY 2017-18 for

Professionals like CAs

37

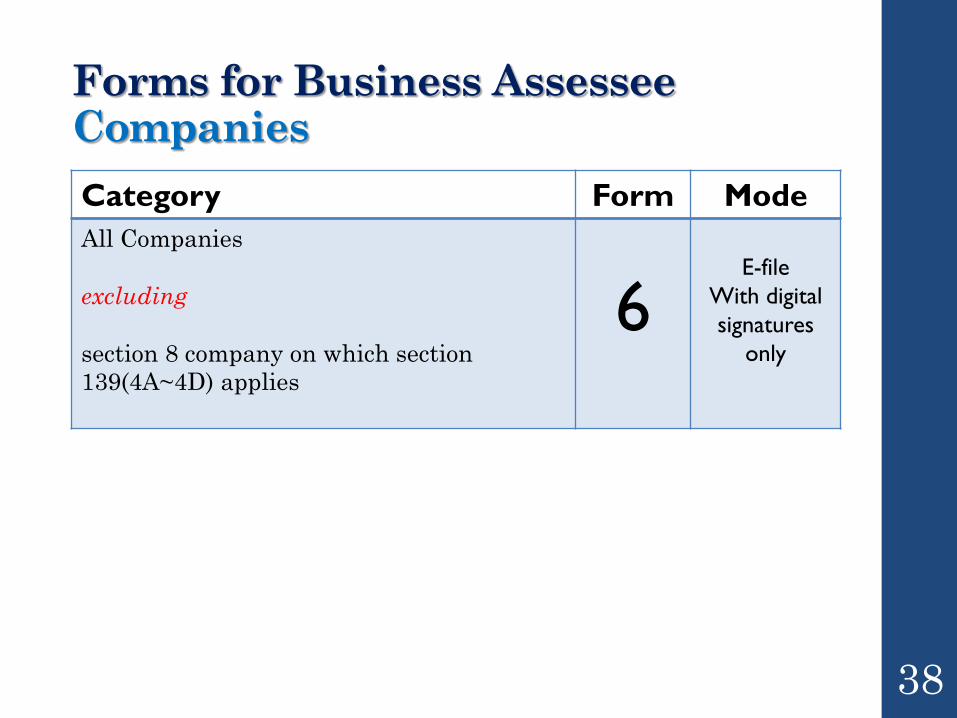

Forms for Business AssesseeCompanies

Category Form Mode

All Companies

excluding

section 8 company on which section

139(4A~4D) applies

6E-file

With digital

signatures

only

38

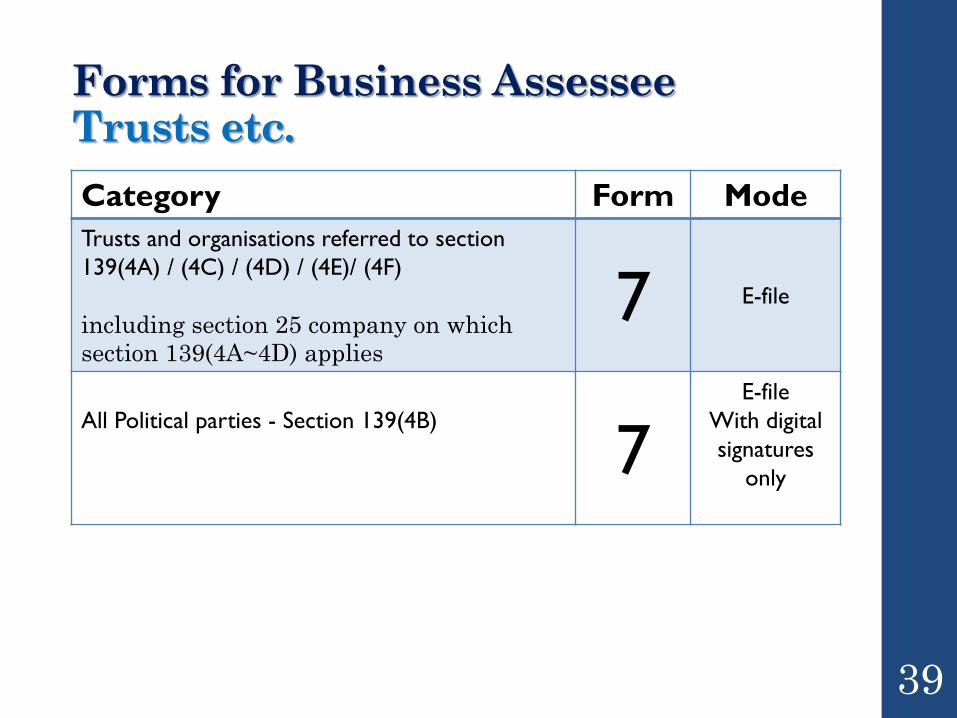

Forms for Business AssesseeTrusts etc.

Category Form Mode

Trusts and organisations referred to section

139(4A) / (4C) / (4D) / (4E)/ (4F)

including section 25 company on which

section 139(4A~4D) applies

7 E-file

All Political parties - Section 139(4B)

7E-file

With digital

signatures

only

39

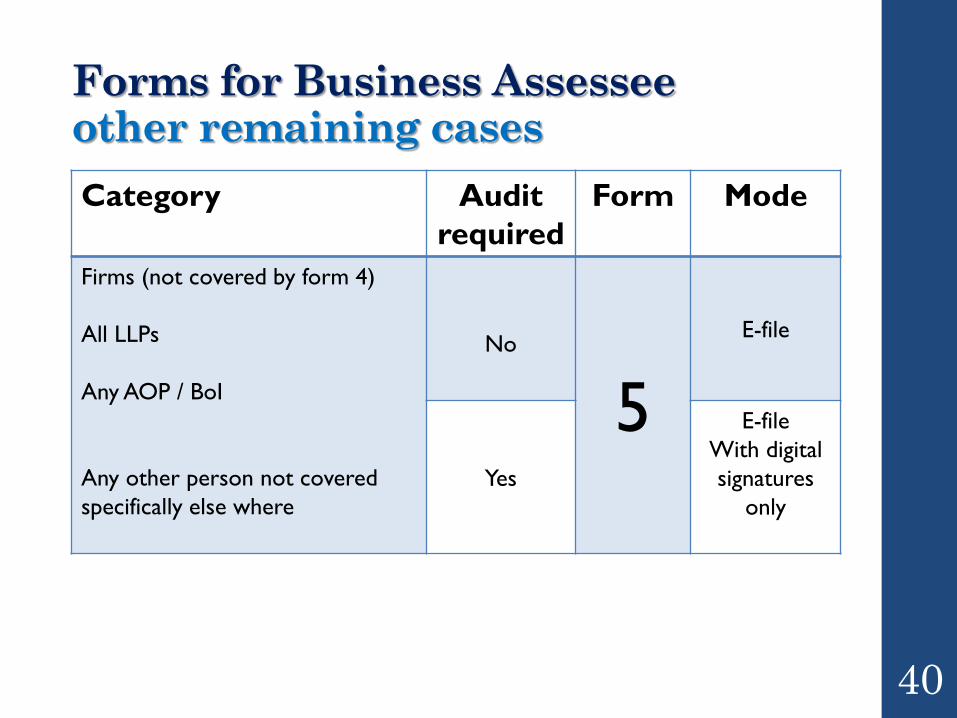

Forms for Business Assesseeother remaining cases

Category Audit

required

Form Mode

Firms (not covered by form 4)

All LLPs

Any AOP / BoI

Any other person not covered

specifically else where

No

5

E-file

Yes

E-file

With digital

signatures

only

40

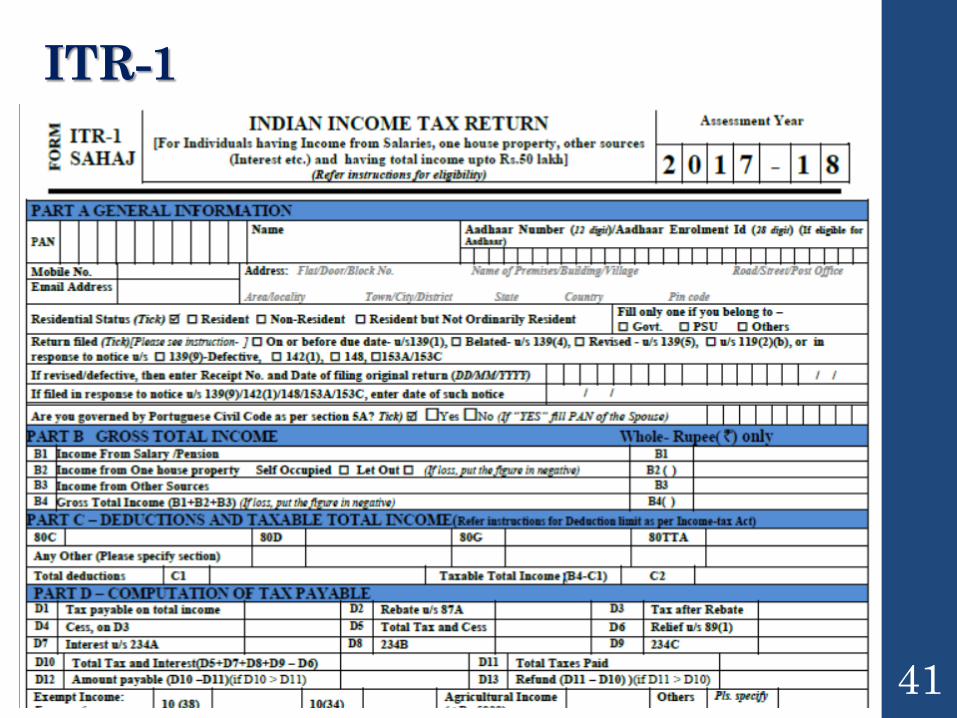

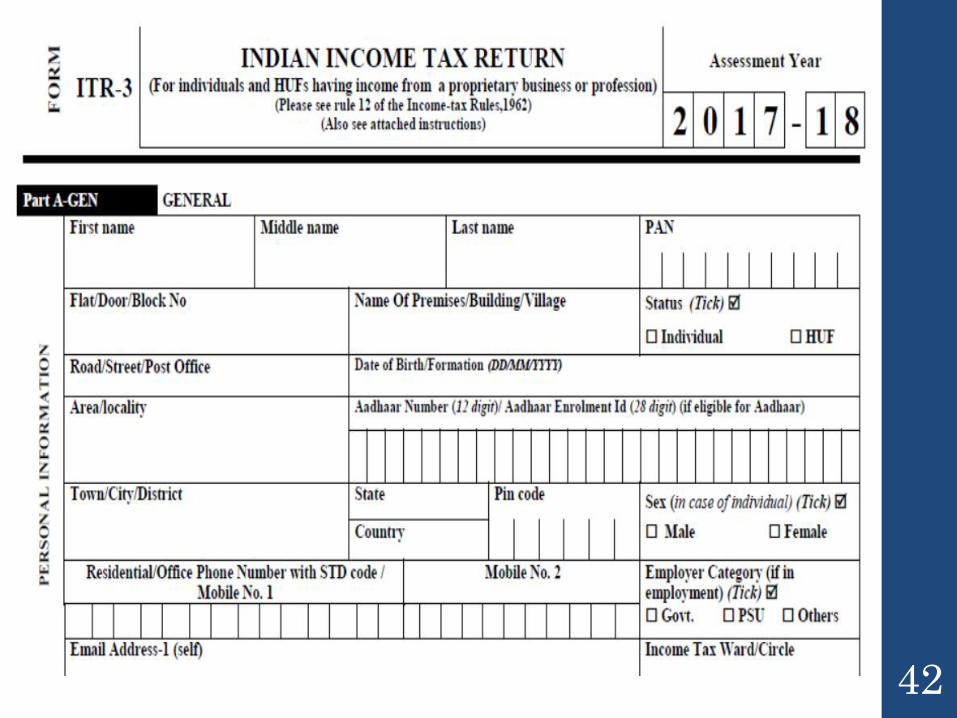

ITR-1

41

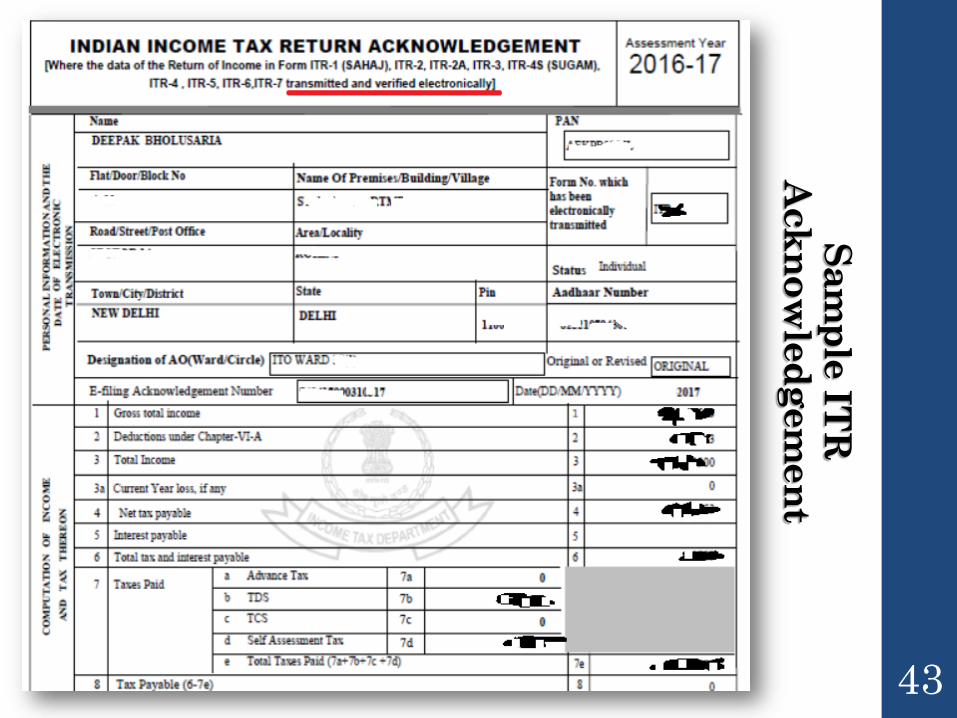

42

Sa

mp

le IT

R

Ack

no

wle

dg

em

en

t

43

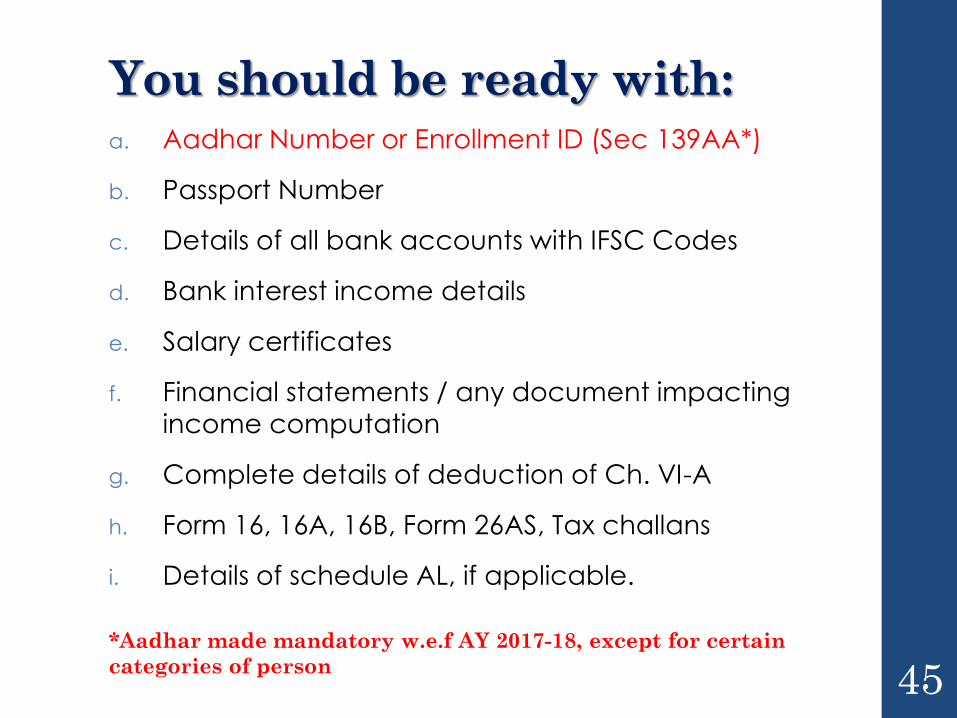

Pre-requisites

You should be ready with:a. Aadhar Number or Enrollment ID (Sec 139AA*)

b. Passport Number

c. Details of all bank accounts with IFSC Codes

d. Bank interest income details

e. Salary certificates

f. Financial statements / any document impacting

income computation

g. Complete details of deduction of Ch. VI-A

h. Form 16, 16A, 16B, Form 26AS, Tax challans

i. Details of schedule AL, if applicable.

45*Aadhar made mandatory w.e.f AY 2017-18, except for certain

categories of person

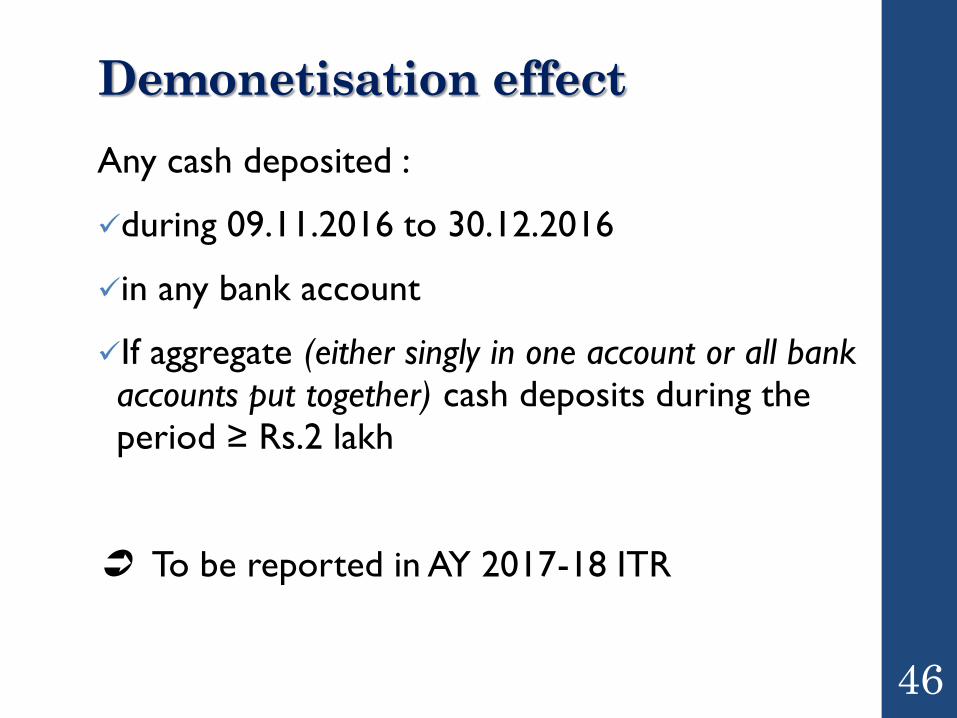

Demonetisation effect

Any cash deposited :

during 09.11.2016 to 30.12.2016

in any bank account

If aggregate (either singly in one account or all bank accounts put together) cash deposits during the period ≥ Rs.2 lakh

To be reported in AY 2017-18 ITR

46

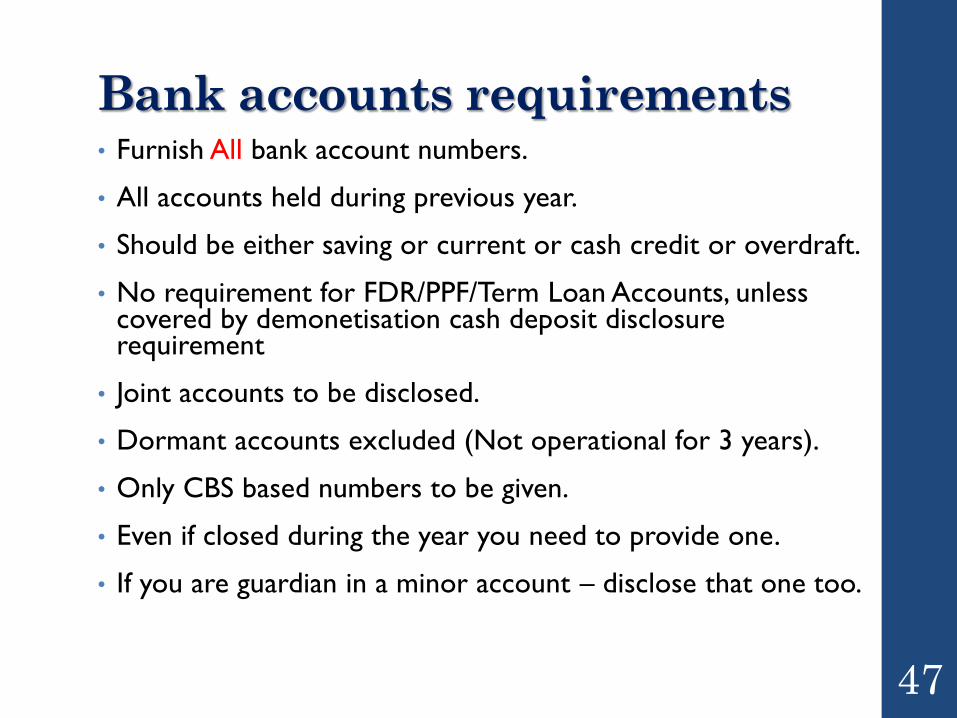

Bank accounts requirements• Furnish All bank account numbers.

• All accounts held during previous year.

• Should be either saving or current or cash credit or overdraft.

• No requirement for FDR/PPF/Term Loan Accounts, unless covered by demonetisation cash deposit disclosure requirement

• Joint accounts to be disclosed.

• Dormant accounts excluded (Not operational for 3 years).

• Only CBS based numbers to be given.

• Even if closed during the year you need to provide one.

• If you are guardian in a minor account – disclose that one too.

47

Process of E-Filing

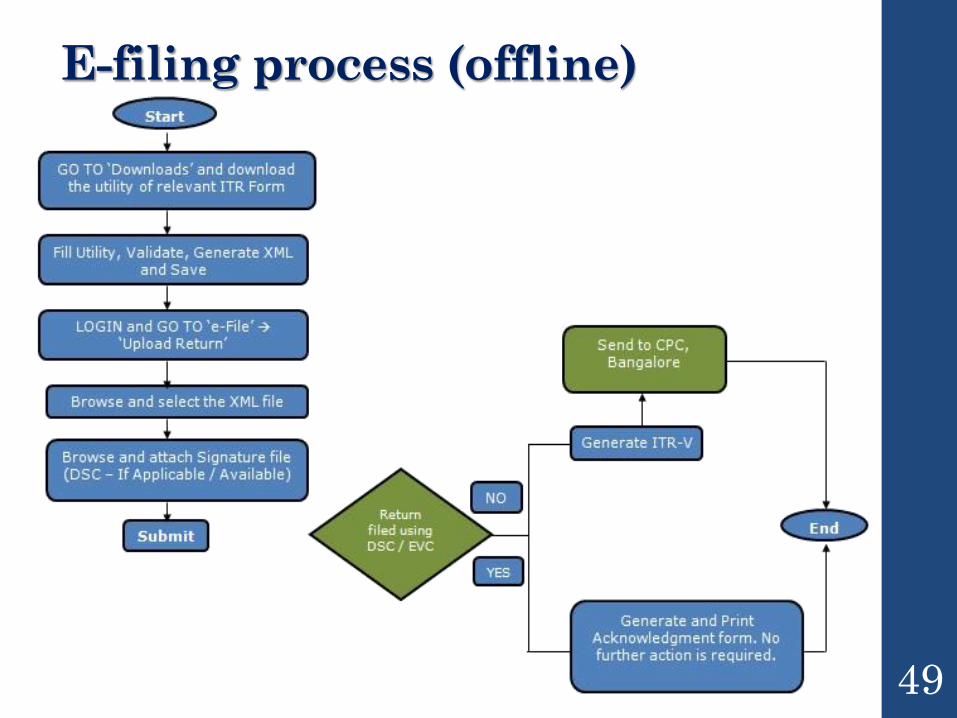

E-filing process (offline)

49

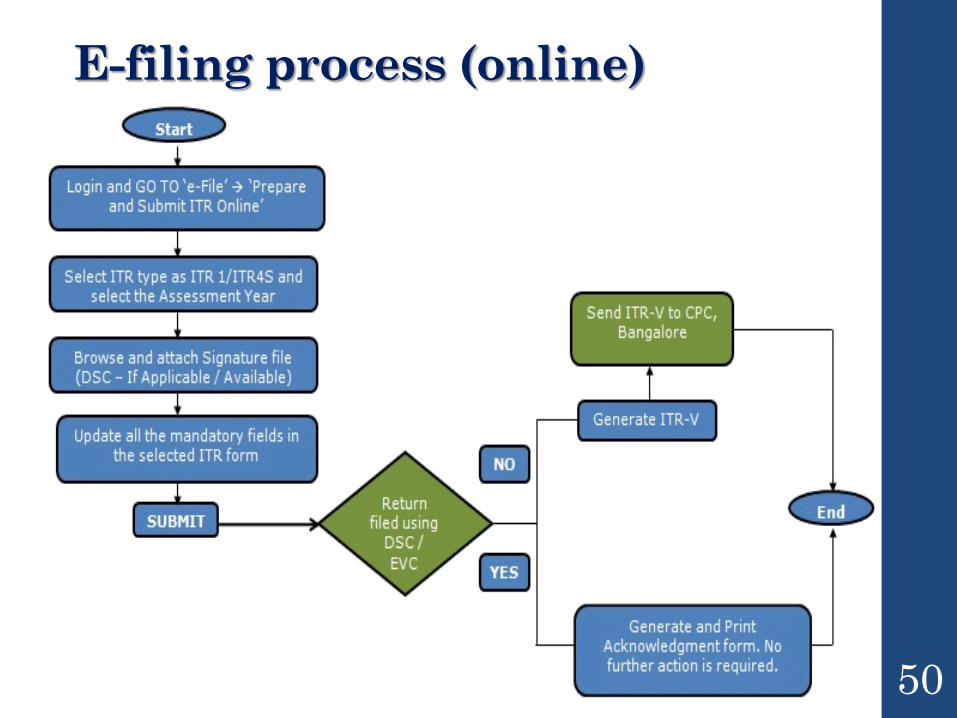

E-filing process (online)

50

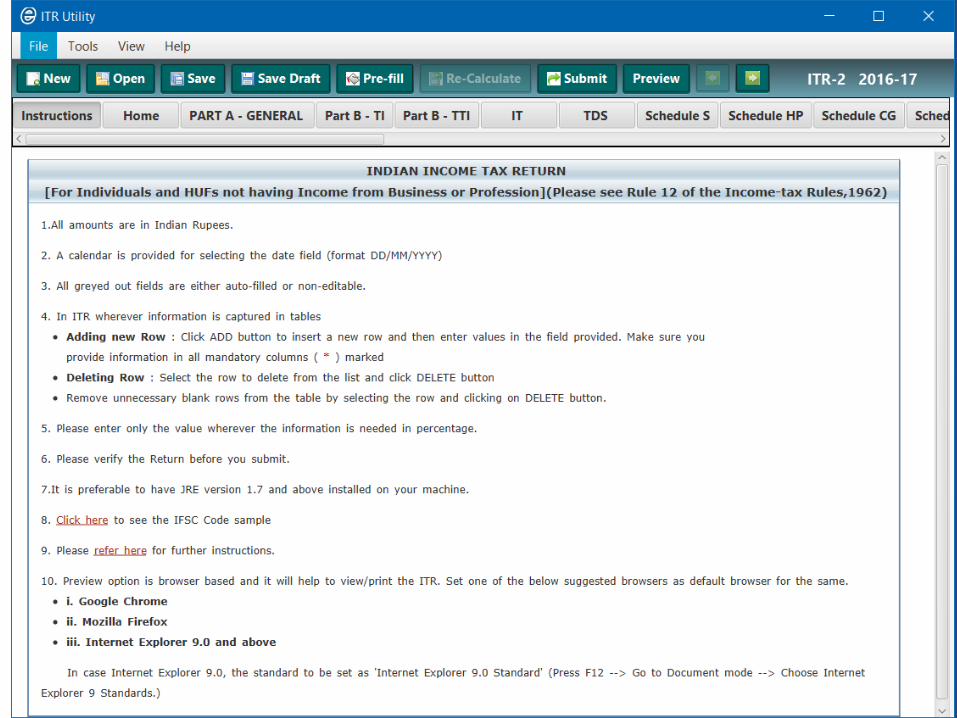

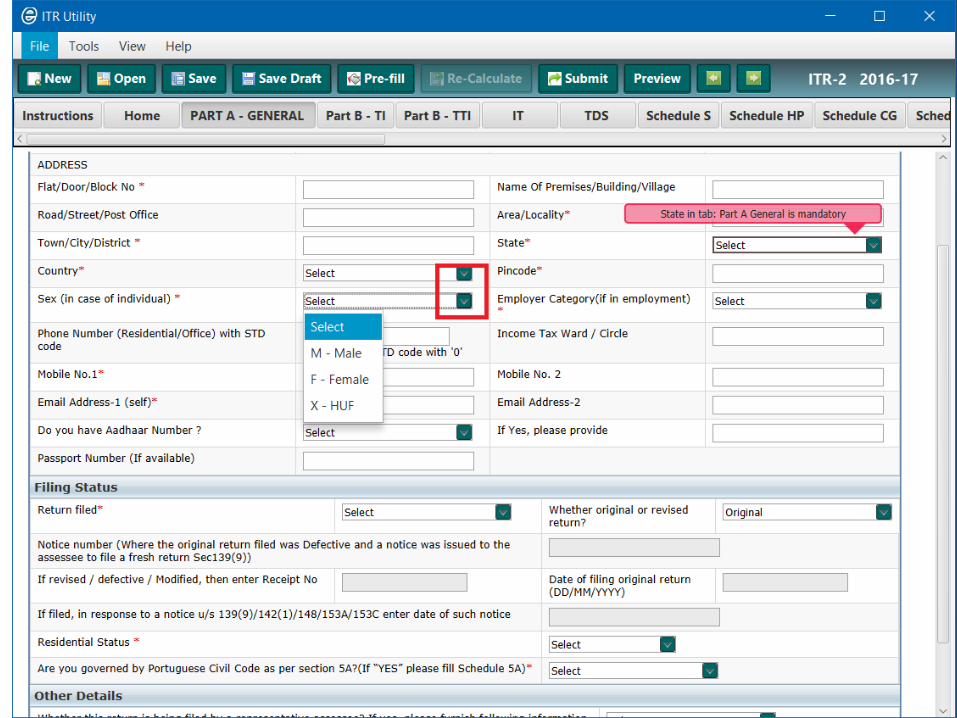

Offline XML preparation

52

53

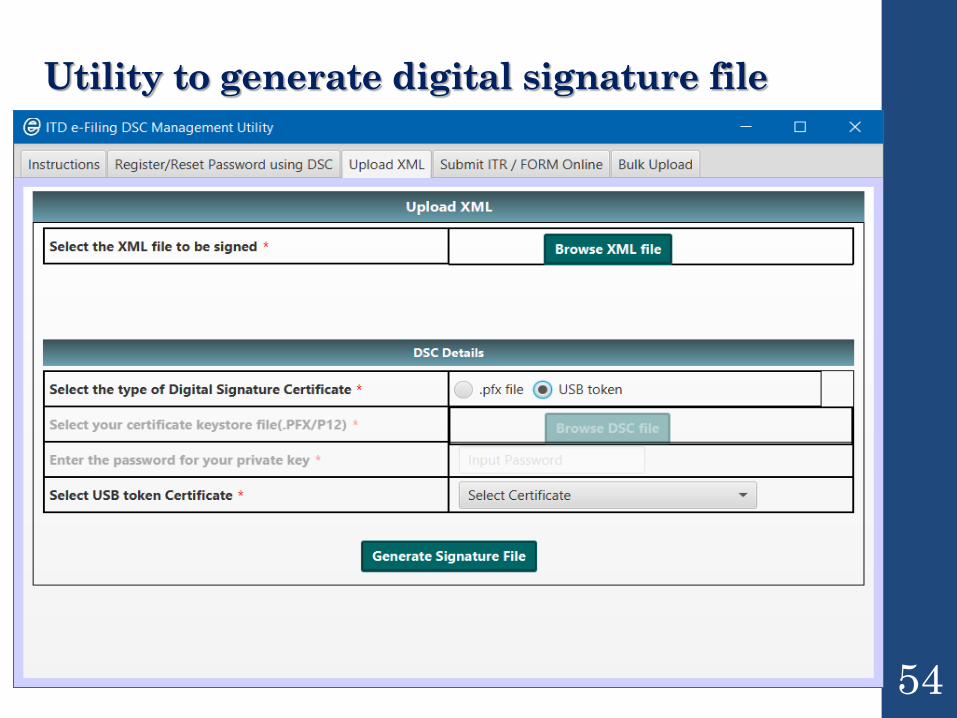

Utility to generate digital signature file

54

ITD Portal dashboard

55

Questions?

Thank you ! !