Download - Webcast 4Q14

RESULTS ANNOUNCEMENT

4th Quarter and

2014 Year End Results

__

Conference Call / Webcast

April, 23rd 2015

DISCLAIMER

FORWARD-LOOKING STATEMENTS:

DISCLAIMER

The presentation may contain forward-looking statements about future

events within the meaning of Section 27A of the Securities Act of 1933, as

amended, and Section 21E of the Securities Exchange Act of 1934, as

amended, that are not based on historical facts and are not assurances of

future results. Such forward-looking statements merely reflect the

Company’s current views and estimates of future economic circumstances,

industry conditions, company performance and financial results. Such

terms as "anticipate", "believe", "expect", "forecast", "intend", "plan",

"project", "seek", "should", along with similar or analogous expressions, are

used to identify such forward-looking statements. Readers are cautioned

that these statements are only projections and may differ materially from

actual future results or events. Readers are referred to the documents filed

by the Company with the SEC, specifically the Company’s most recent

Annual Report on Form 20-F, which identify important risk factors that

could cause actual results to differ from those contained in the forward-

looking statements, including, among other things, risks relating to general

economic and business conditions, including crude oil and other

commodity prices, refining margins and prevailing exchange rates,

uncertainties inherent in making estimates of our oil and gas reserves

including recently discovered oil and gas reserves, international and

Brazilian political, economic and social developments, receipt of

governmental approvals and licenses and our ability to obtain financing.

We undertake no obligation to publicly update or revise any forward-

looking statements, whether as a result of new information or future

events or for any other reason. Figures for 2015 on are estimates or

targets.

All forward-looking statements are expressly qualified in their entirety

by this cautionary statement, and you should not place reliance on any

forward-looking statement contained in this presentation.

NON-SEC COMPLIANT OIL AND GAS RESERVES:

CAUTIONARY STATEMENT FOR US INVESTORS

We present certain data in this presentation, such as oil and gas

resources, that we are not permitted to present in documents filed with

the United States Securities and Exchange Commission (SEC) under

new Subpart 1200 to Regulation S-K because such terms do not

qualify as proved, probable or possible reserves under Rule 4-10(a) of

Regulation S-X.

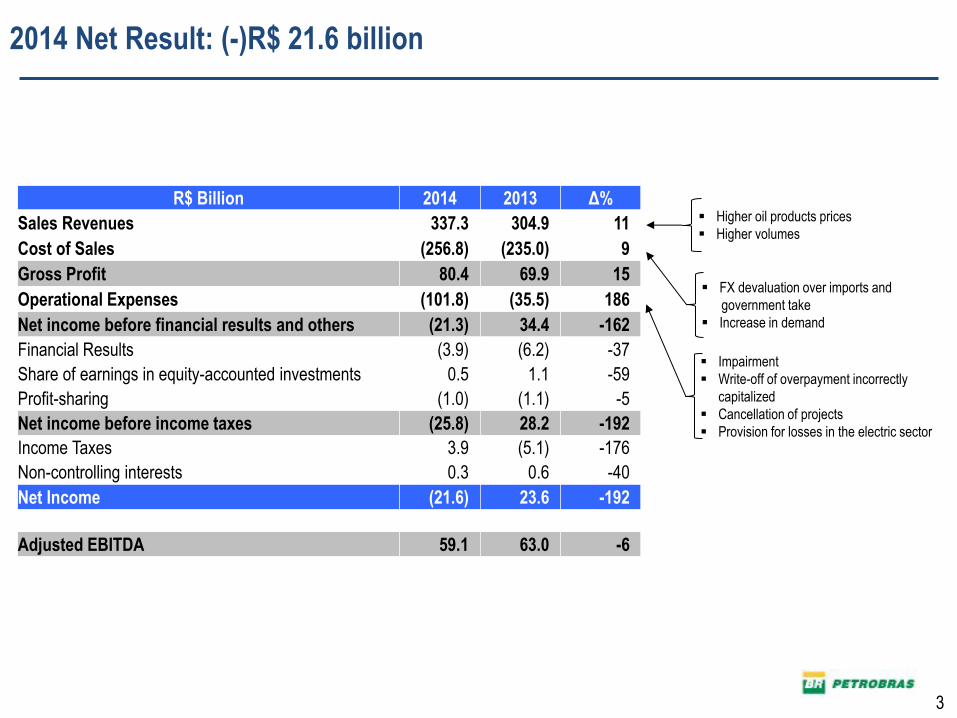

R$ Billion 2014 2013 Δ%

Sales Revenues 337.3 304.9 11

Cost of Sales (256.8) (235.0) 9

Gross Profit 80.4 69.9 15

Operational Expenses (101.8) (35.5) 186

Net income before financial results and others (21.3) 34.4 -162

Financial Results (3.9) (6.2) -37

Share of earnings in equity-accounted investments 0.5 1.1 -59

Profit-sharing (1.0) (1.1) -5

Net income before income taxes (25.8) 28.2 -192

Income Taxes 3.9 (5.1) -176

Non-controlling interests 0.3 0.6 -40

Net Income (21.6) 23.6 -192

Adjusted EBITDA 59.1 63.0 -6

FX devaluation over imports and

government take

Increase in demand

Impairment

Write-off of overpayment incorrectly

capitalized

Cancellation of projects

Provision for losses in the electric sector

Higher oil products prices

Higher volumes

2014 Net Result: (-)R$ 21.6 billion

3

R$ Billion 3Q14

Reviewed

3Q14

Not Reviewed Δ%

Sales Revenues 88.4 88.4 0

Cost of Sales (67.9) (67.3) 1

Gross Profit 20.4 21.1 -3

Operational Expenses (25.4) (16.5) 54

Net income before financial results and others (4.9) 4.6 -207

Financial Results (1.0) (1.0) 0

Share of earnings in equity-accounted investments 0.2 0.2 0

Profit-sharing (0.1) (0.2) -50

Net income before income taxes (5.8) 3.6 -261

Income Taxes (0.1) (1.1) -91

Non-controlling interests (0.6) (0.6) 0

Net Income (5.3) 3.1 -271

Adjusted EBITDA 8.5 11.7 -27

Change in provision, mainly due to losses in

the electric sector

Write-off of overpayment incorrectly

capitalized

Additions to provision for losses in the

electric sector

Comparison between Reviewed and Not Reviewed 3Q14

4

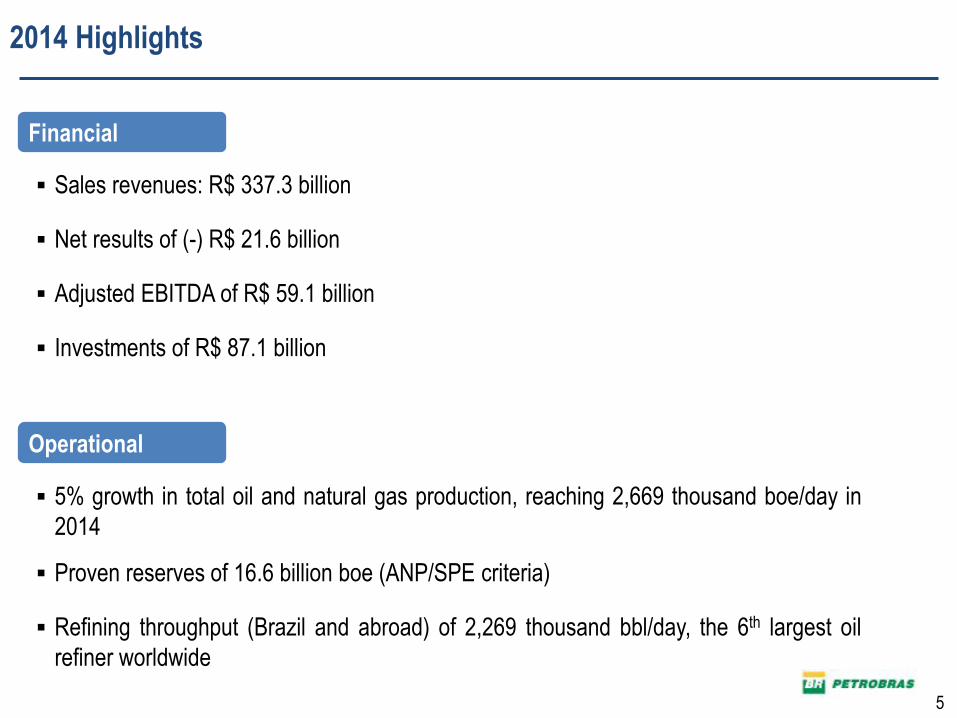

Financial

2014 Highlights

Sales revenues: R$ 337.3 billion

Net results of (-) R$ 21.6 billion

Adjusted EBITDA of R$ 59.1 billion

Investments of R$ 87.1 billion

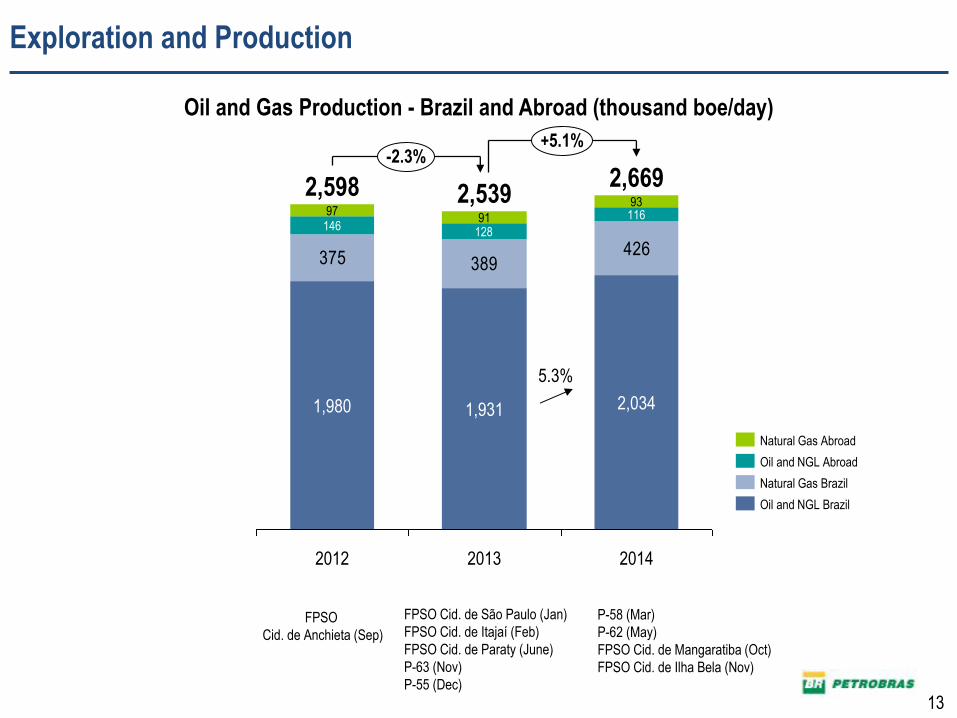

5% growth in total oil and natural gas production, reaching 2,669 thousand boe/day in

2014

Proven reserves of 16.6 billion boe (ANP/SPE criteria)

Refining throughput (Brazil and abroad) of 2,269 thousand bbl/day, the 6th largest oil

refiner worldwide

5

Operational

2014 Highlights

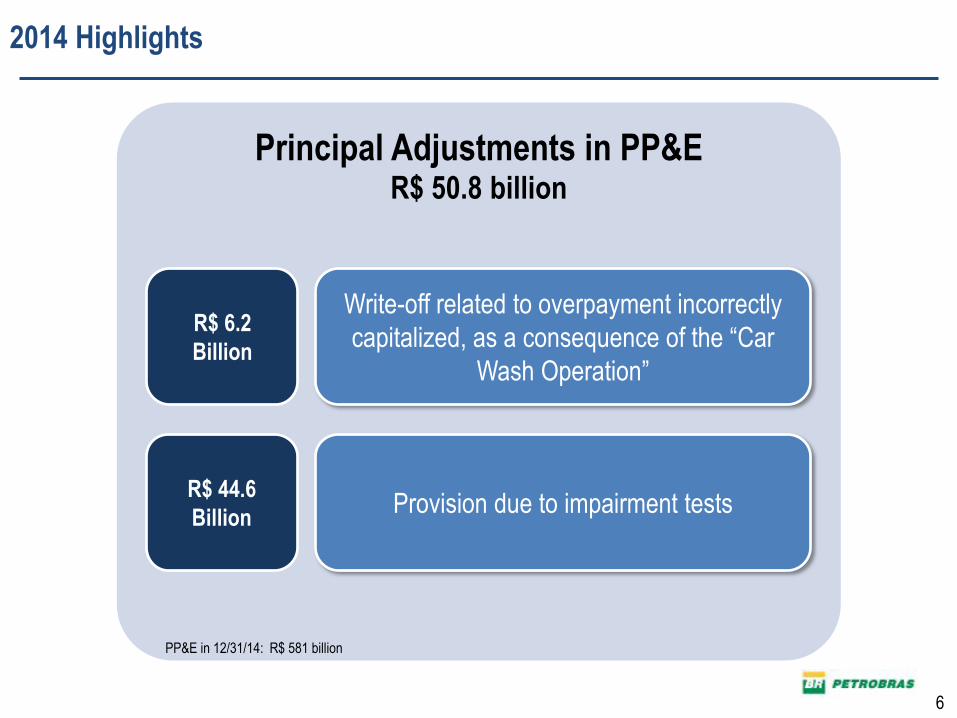

6

Principal Adjustments in PP&E R$ 50.8 billion

R$ 6.2

Billion

Write-off related to overpayment incorrectly

capitalized, as a consequence of the “Car

Wash Operation”

Provision due to impairment tests R$ 44.6

Billion

PP&E in 12/31/14: R$ 581 billion

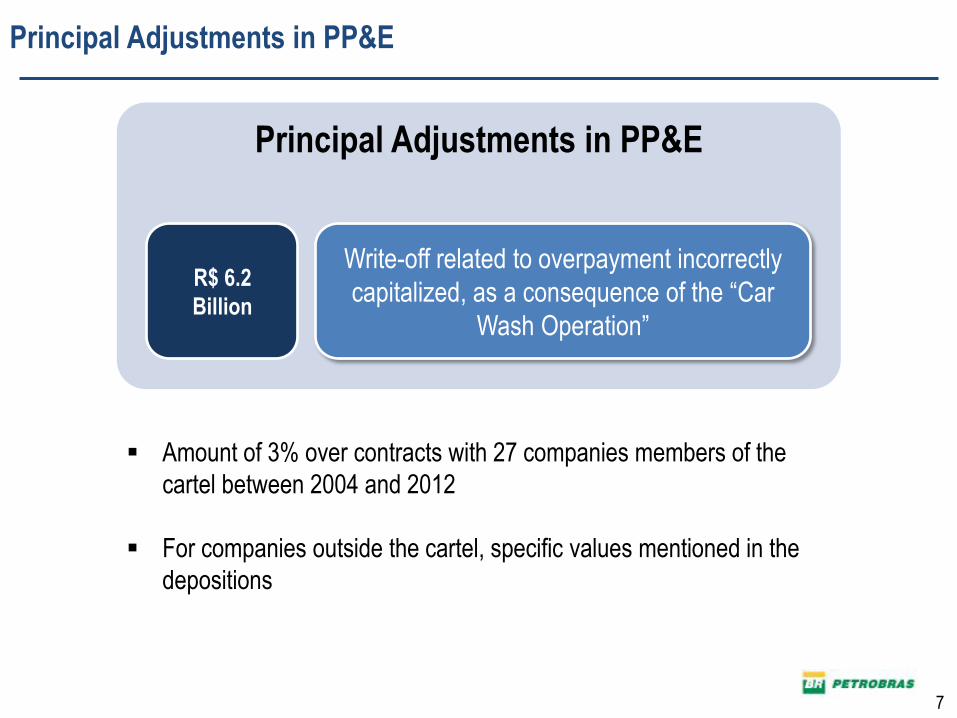

7

Principal Adjustments in PP&E

R$ 6.2

Billion

Write-off related to overpayment incorrectly

capitalized, as a consequence of the “Car

Wash Operation”

Amount of 3% over contracts with 27 companies members of the

cartel between 2004 and 2012

For companies outside the cartel, specific values mentioned in the

depositions

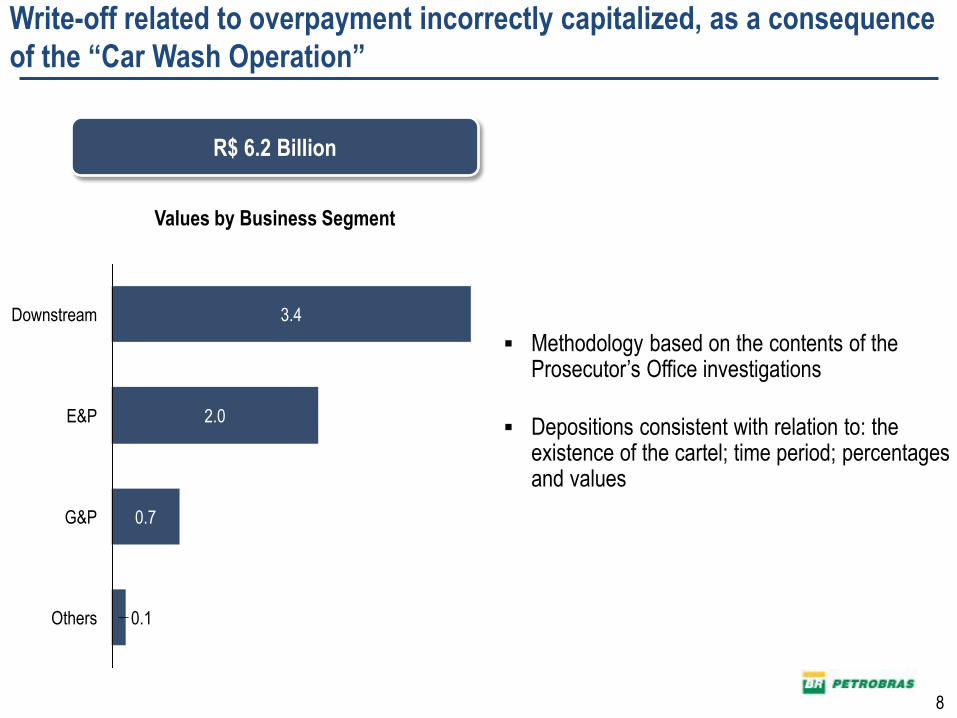

Principal Adjustments in PP&E

Methodology based on the contents of the Prosecutor’s Office investigations

Depositions consistent with relation to: the existence of the cartel; time period; percentages and values

Values by Business Segment

0.1

0.7 G&P

2.0

Others

E&P

Downstream 3.4

8

R$ 6.2 Billion

Write-off related to overpayment incorrectly capitalized, as a consequence

of the “Car Wash Operation”

9

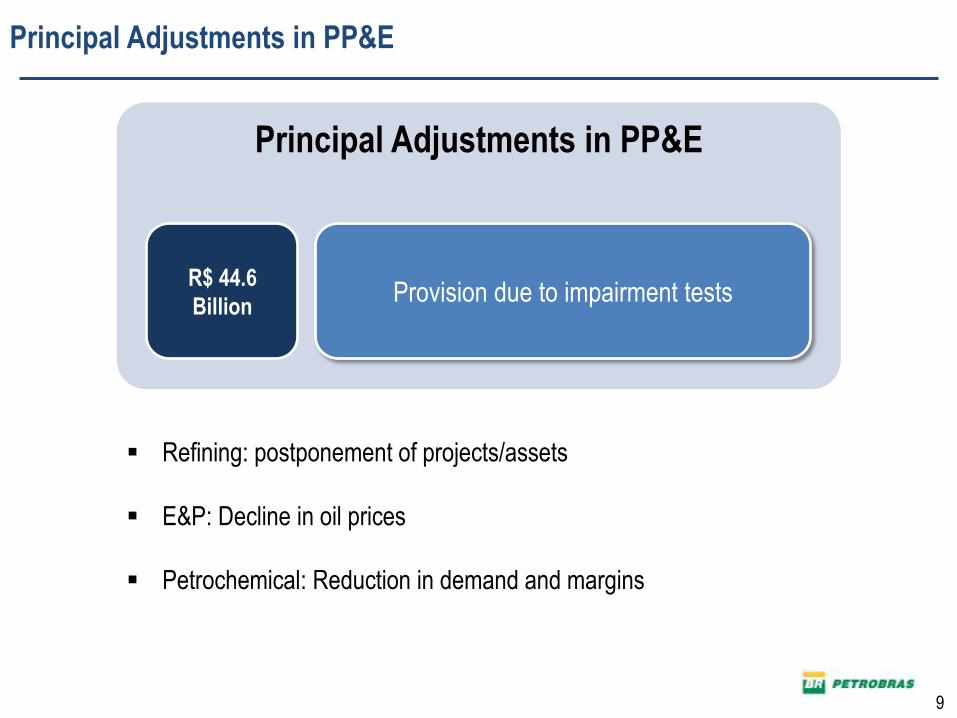

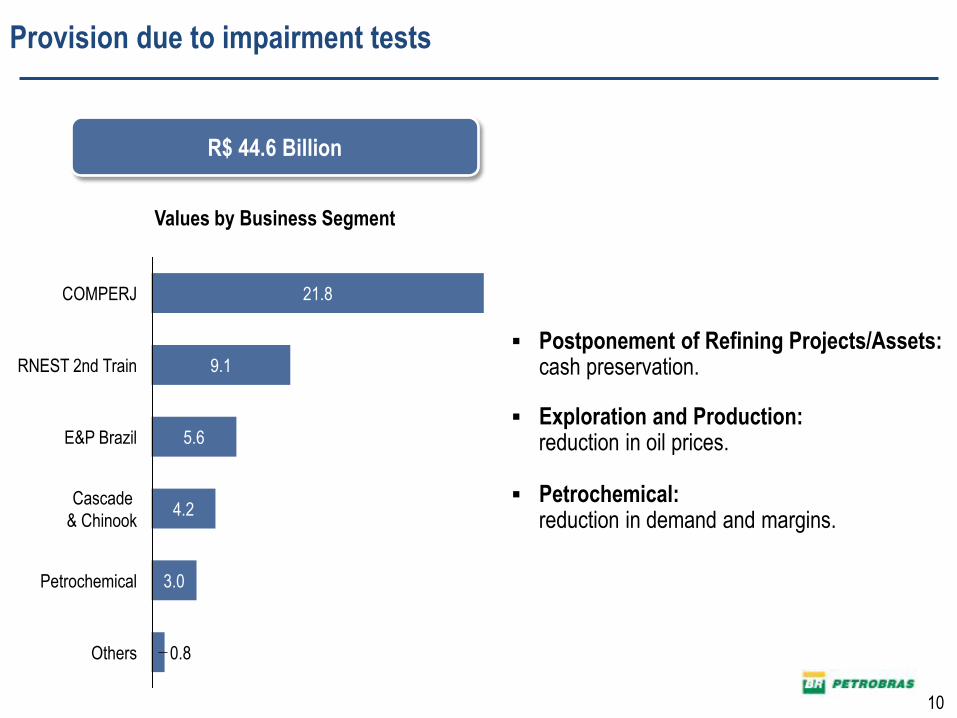

Principal Adjustments in PP&E

R$ 44.6

Billion Provision due to impairment tests

Refining: postponement of projects/assets

E&P: Decline in oil prices

Petrochemical: Reduction in demand and margins

Principal Adjustments in PP&E

Postponement of Refining Projects/Assets: cash preservation.

Exploration and Production: reduction in oil prices.

Petrochemical:

reduction in demand and margins.

Others 0.8

Petrochemical 3.0

Cascade

& Chinook 4.2

E&P Brazil 5.6

RNEST 2nd Train 9.1

COMPERJ 21.8

10

Values by Business Segment

R$ 44.6 Billion

Provision due to impairment tests

11

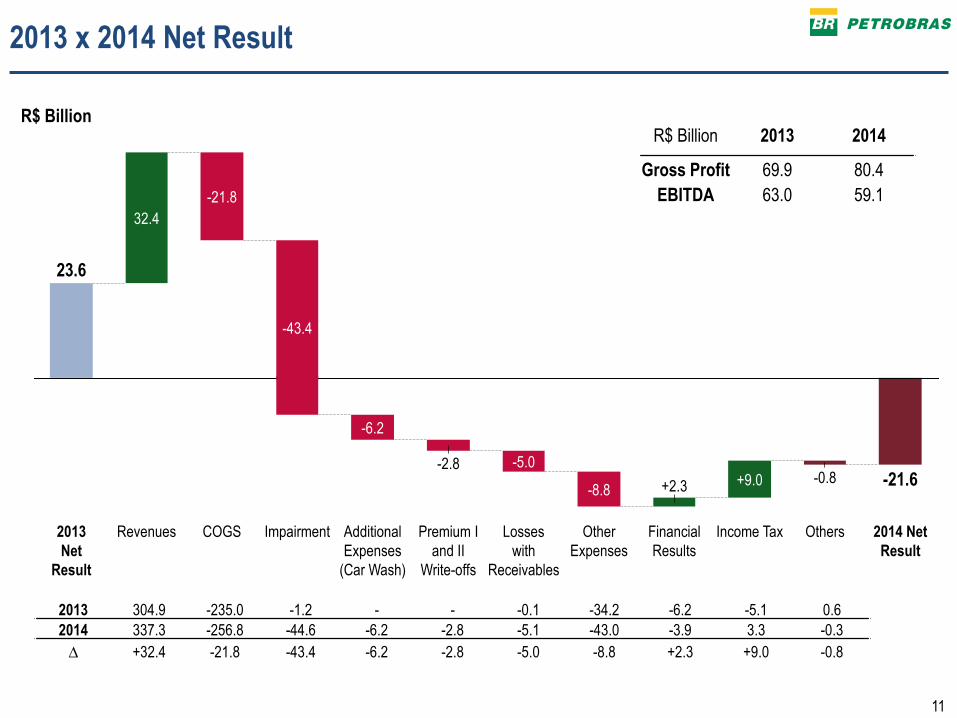

2013 x 2014 Net Result

R$ Billion

-21.6

Others

-0.8

Income Tax

+9.0

Financial

Results

+2.3

2014 Net

Result

Other

Expenses

-8.8

Losses

with

Receivables

-5.0

Premium I

and II

Write-offs

-2.8

Additional

Expenses

(Car Wash)

-6.2

Impairment

-43.4

COGS

-21.8

Revenues

32.4

2013

Net

Result

23.6

2013 304.9 -235.0 -1.2 - - -0.1 -34.2 -6.2 -5.1 0.6

2014 337.3 -256.8 -44.6 -6.2 -2.8 -5.1 -43.0 -3.9 3.3 -0.3

∆ +32.4 -21.8 -43.4 -6.2 -2.8 -5.0 -8.8 +2.3 +9.0 -0.8

R$ Billion 2013 2014

Gross Profit 69.9 80.4

EBITDA 63.0 59.1

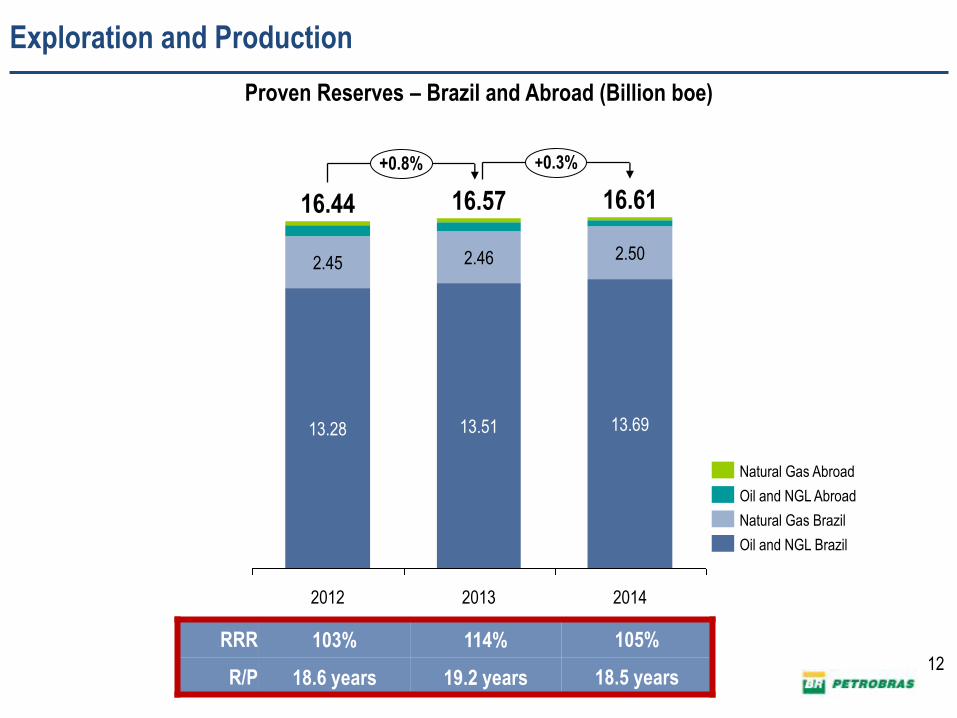

Proven Reserves – Brazil and Abroad (Billion boe)

Exploration and Production

+0.8% +0.3%

2014

16.61

13.69

2.50

2013

16.57

13.51

2.46

2012

16.44

13.28

2.45

Natural Gas Abroad

Natural Gas Brazil

Oil and NGL Brazil

Oil and NGL Abroad

12

RRR 103% 114% 105%

R/P 18.6 years 19.2 years 18.5 years

Exploration and Production

375 389426

146 128

1169793

2,034

2014

+5.1%

2013

1,931

-2.3%

2,669 2,539

91

2012

2,598

1,980

Oil and NGL Brazil

Natural Gas Brazil

Oil and NGL Abroad

Natural Gas Abroad

5.3%

Oil and Gas Production - Brazil and Abroad (thousand boe/day)

13

FPSO

Cid. de Anchieta (Sep)

FPSO Cid. de São Paulo (Jan)

FPSO Cid. de Itajaí (Feb)

FPSO Cid. de Paraty (June)

P-63 (Nov)

P-55 (Dec)

P-58 (Mar)

P-62 (May)

FPSO Cid. de Mangaratiba (Oct)

FPSO Cid. de Ilha Bela (Nov)

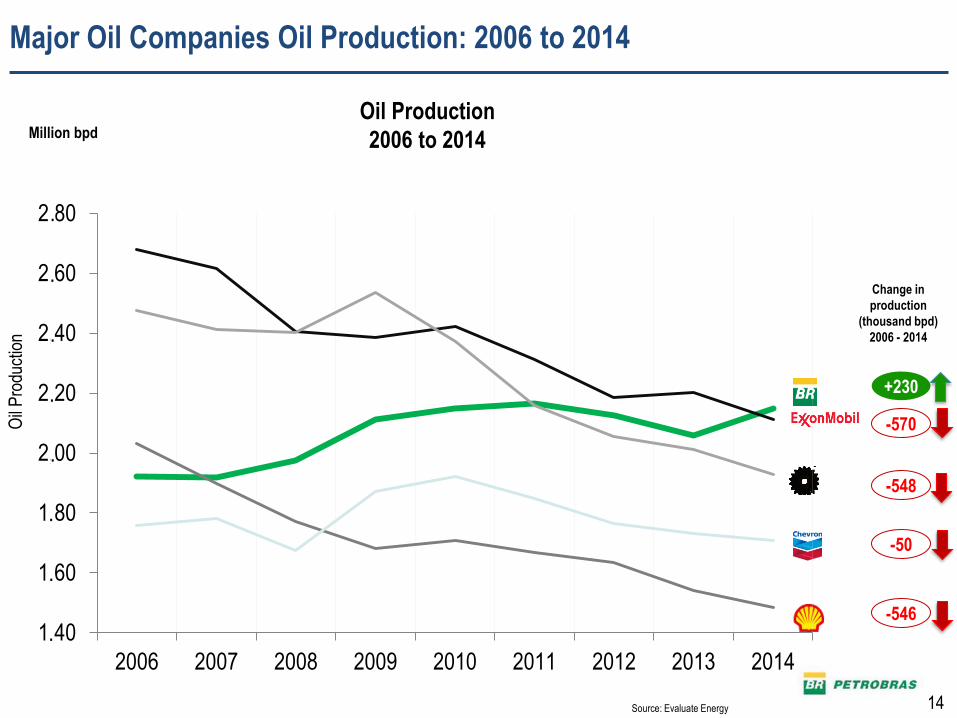

Million bpd

Source: Evaluate Energy

Change in

production

(thousand bpd)

2006 - 2014

Oil Production

2006 to 2014

Oil

Pro

duct

ion

+230

-570

-548

-50

-546 1,40

1,60

1,80

2,00

2,20

2,40

2,60

2,80

2006 2007 2008 2009 2010 2011 2012 2013 2014

Major Oil Companies Oil Production: 2006 to 2014

14

.

.

.

.

.

.

.

.

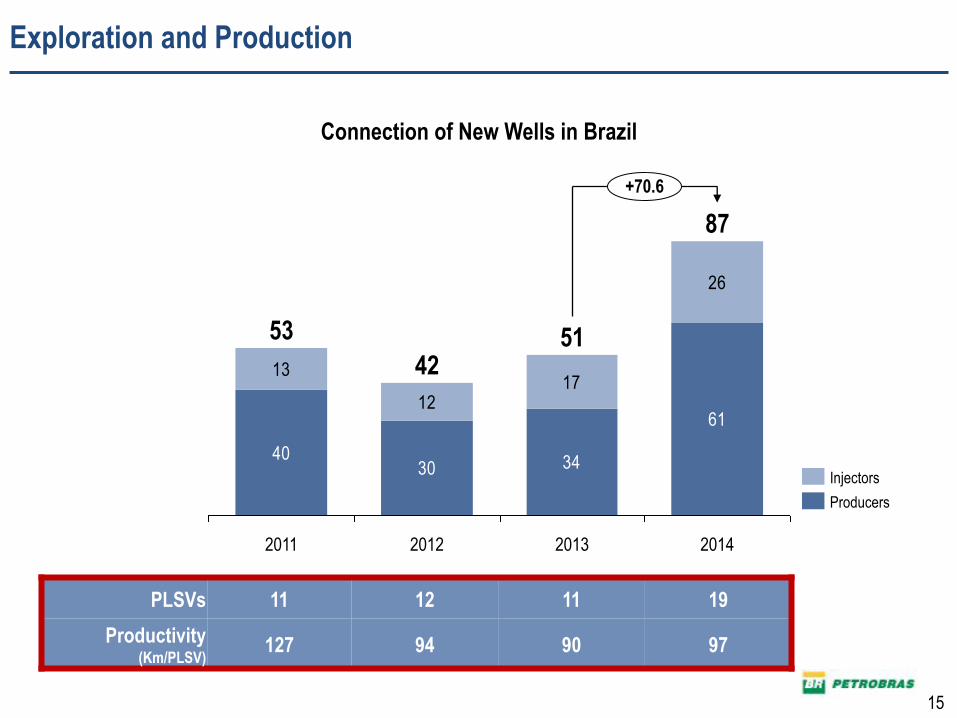

Exploration and Production

Connection of New Wells in Brazil

15

4030 34

61

13

1217

26

2014

87

+70.6

2013

51

2012

42

2011

53

Injectors

Producers

PLSVs 11 12 11 19

Productivity (Km/PLSV)

127 94 90 97

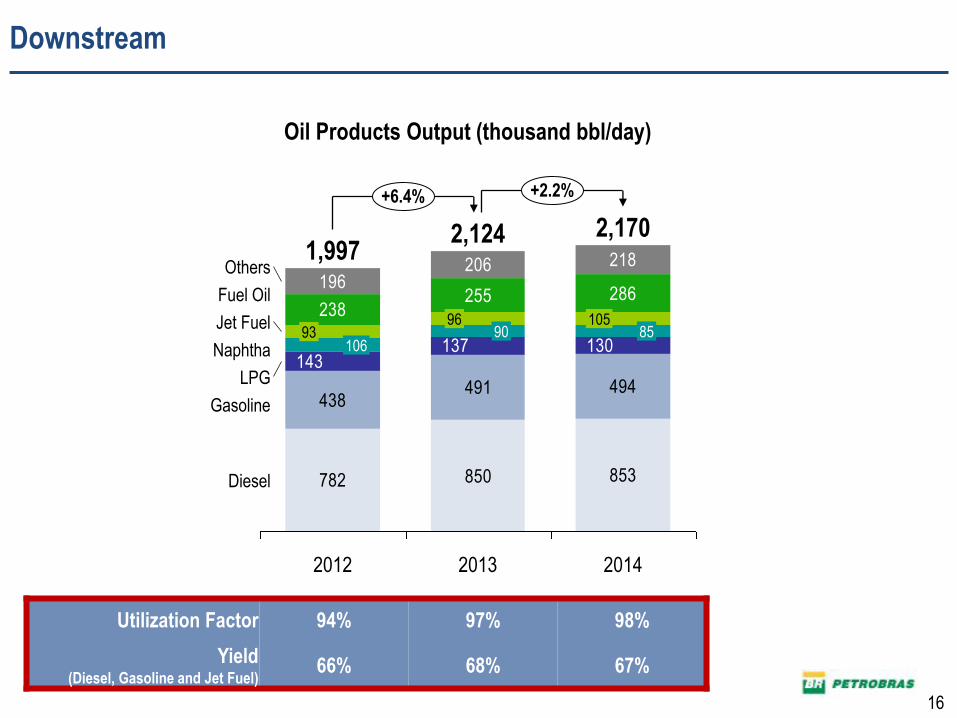

Downstream

782 850 853

438491 494

238255 286

196206 218

130137143

106 93

+6.4%

Gasoline

+2.2%

Diesel

90 96

2012

1,997

Jet Fuel

Fuel Oil

Others

2014

2,170

85 105

2013

2,124

Naphtha

LPG

Oil Products Output (thousand bbl/day)

16

Utilization Factor 94% 97% 98%

Yield (Diesel, Gasoline and Jet Fuel)

66% 68% 67%

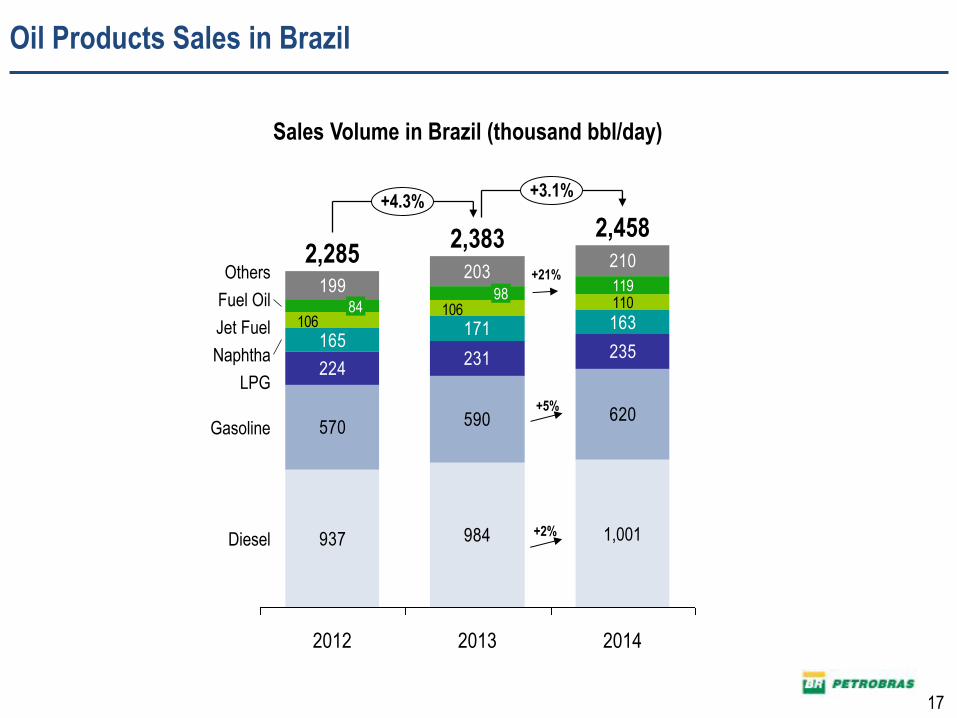

Oil Products Sales in Brazil

937 984

570 590 620

224231 235

165171 163

110199

203210

106106

119

+4.3% +3.1%

Diesel

Gasoline

LPG

Naphtha

Jet Fuel

Fuel Oil

Others

2014

2,458

1,001

2013

2,383

98

2012

2,285

84

+5%

+2%

+21%

Sales Volume in Brazil (thousand bbl/day)

17

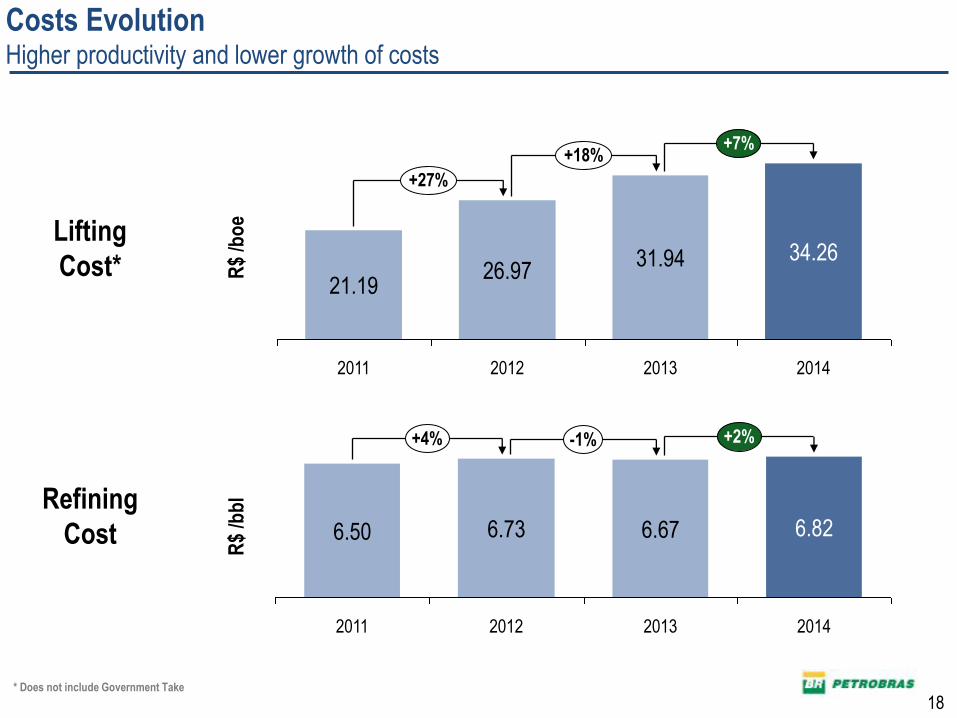

Costs Evolution Higher productivity and lower growth of costs

R$

/bb

l

-1% +4% +2%

2014

6.82

2013

6.67

2012

6.73

2011

6.50

Refining

Cost

R$

/bo

e

21.19

2014

+7%

+27%

34.26

2013

+18%

2012

26.97

2011

31.94 Lifting

Cost*

18 * Does not include Government Take

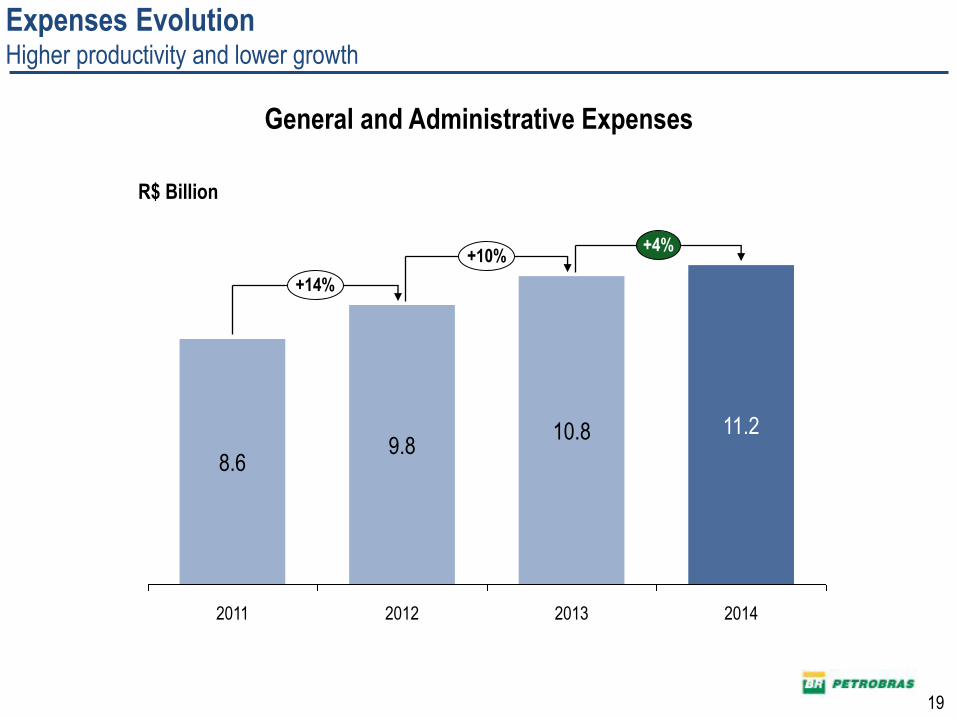

Expenses Evolution Higher productivity and lower growth

R$ Billion

9.8

+4%

11.2

2011 2014 2012

10.8

2013

+10%

+14%

8.6

General and Administrative Expenses

19

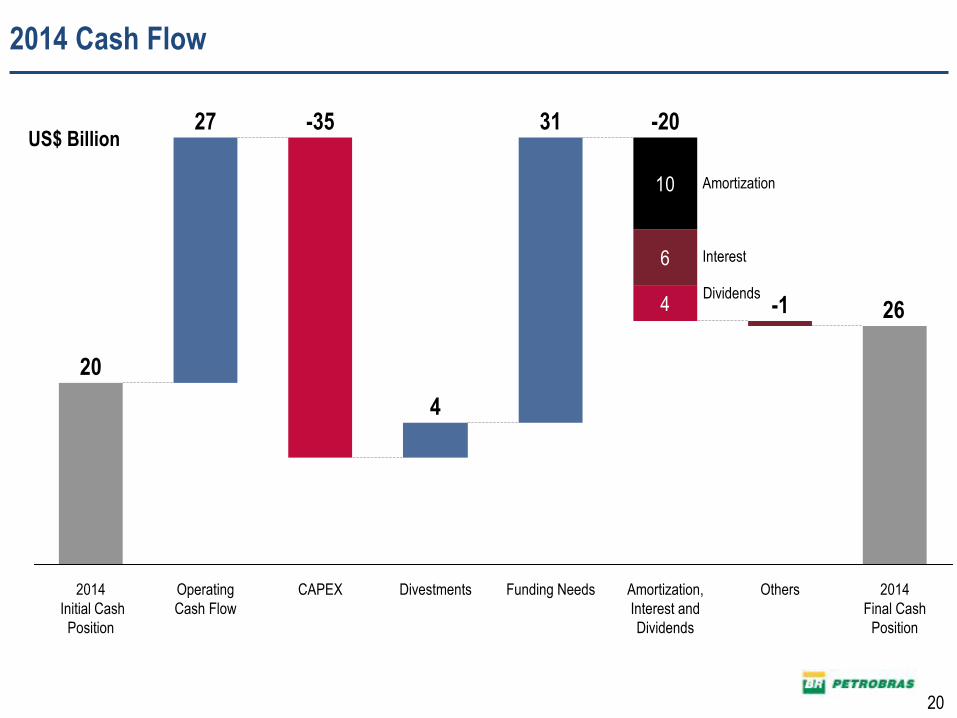

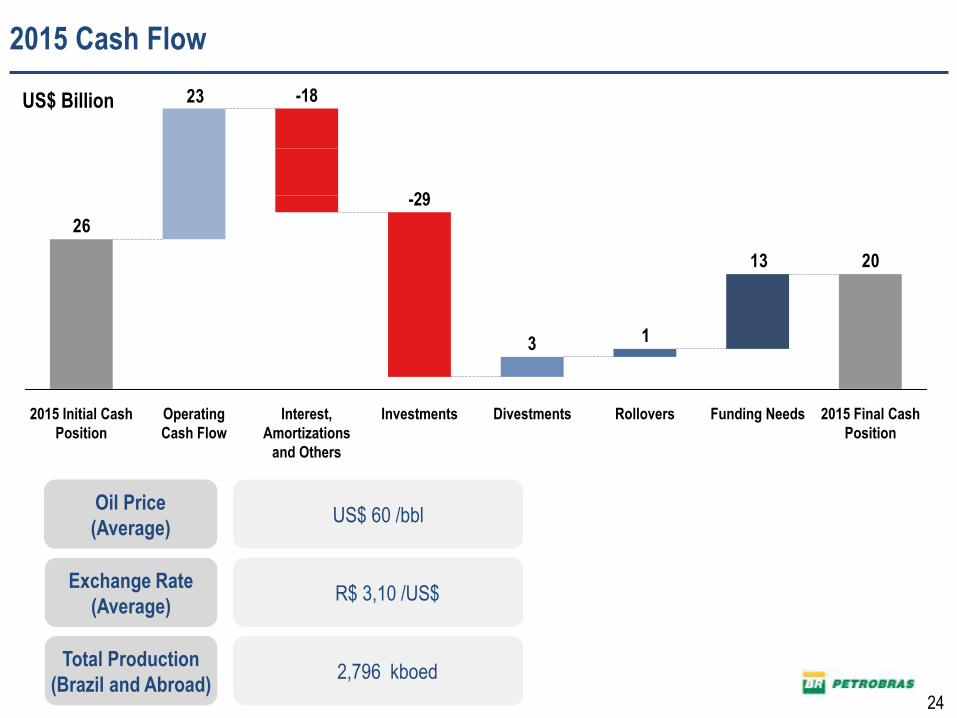

2014 Cash Flow

US$ Billion

26

31

4

27

20

4

6

10

2014

Final Cash

Position

Others Amortization,

Interest and

Dividends

-20

Funding Needs

-35

Divestments CAPEX Operating

Cash Flow

-1

2014

Initial Cash

Position

Amortization

Interest

Dividends

20

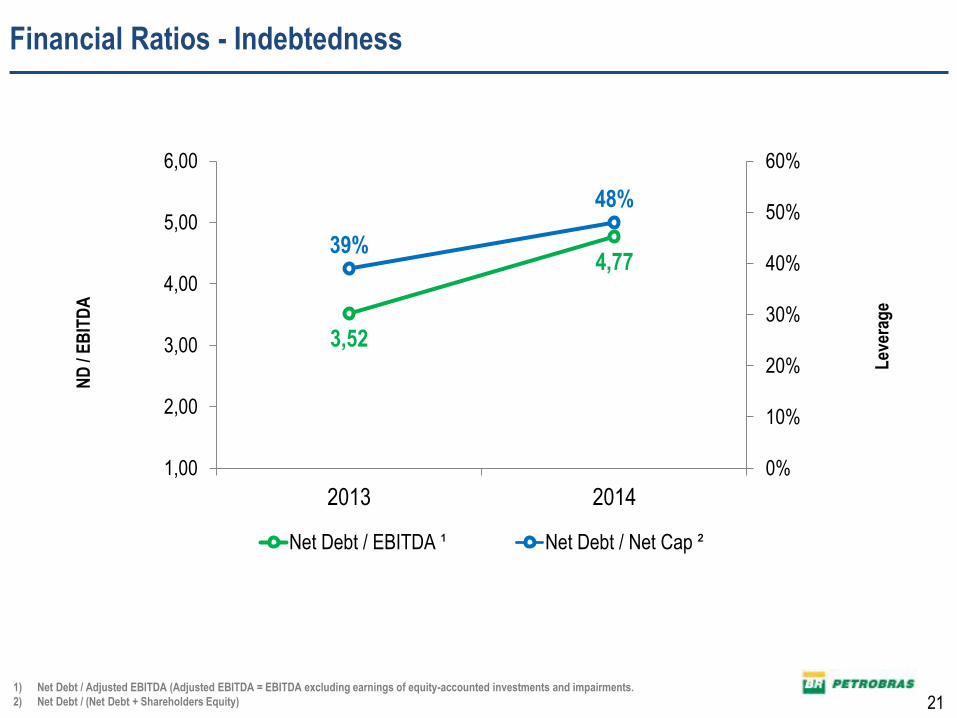

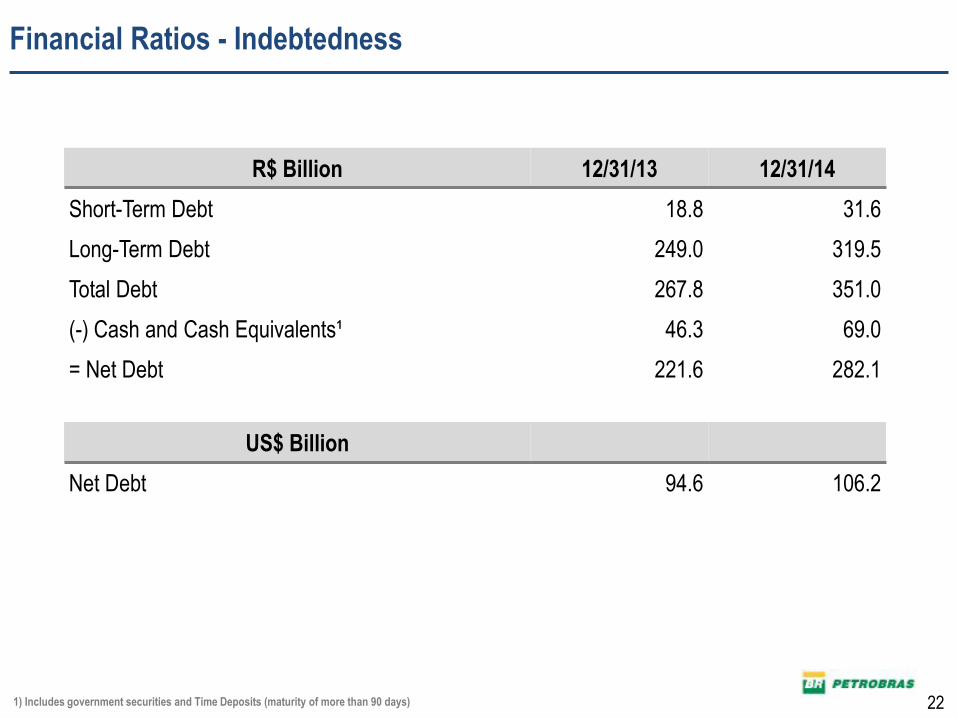

Financial Ratios - Indebtedness

Lev

erag

e

ND

/ E

BIT

DA

1) Net Debt / Adjusted EBITDA (Adjusted EBITDA = EBITDA excluding earnings of equity-accounted investments and impairments.

2) Net Debt / (Net Debt + Shareholders Equity)

3,52

4,77 39%

48%

0%

10%

20%

30%

40%

50%

60%

1,00

2,00

3,00

4,00

5,00

6,00

2013 2014

Net Debt / EBITDA ¹ Net Debt / Net Cap ²

21

R$ Billion 12/31/13 12/31/14

Short-Term Debt 18.8 31.6

Long-Term Debt 249.0 319.5

Total Debt 267.8 351.0

(-) Cash and Cash Equivalents¹ 46.3 69.0

= Net Debt 221.6 282.1

US$ Billion

Net Debt 94.6 106.2

1) Includes government securities and Time Deposits (maturity of more than 90 days)

Financial Ratios - Indebtedness

22

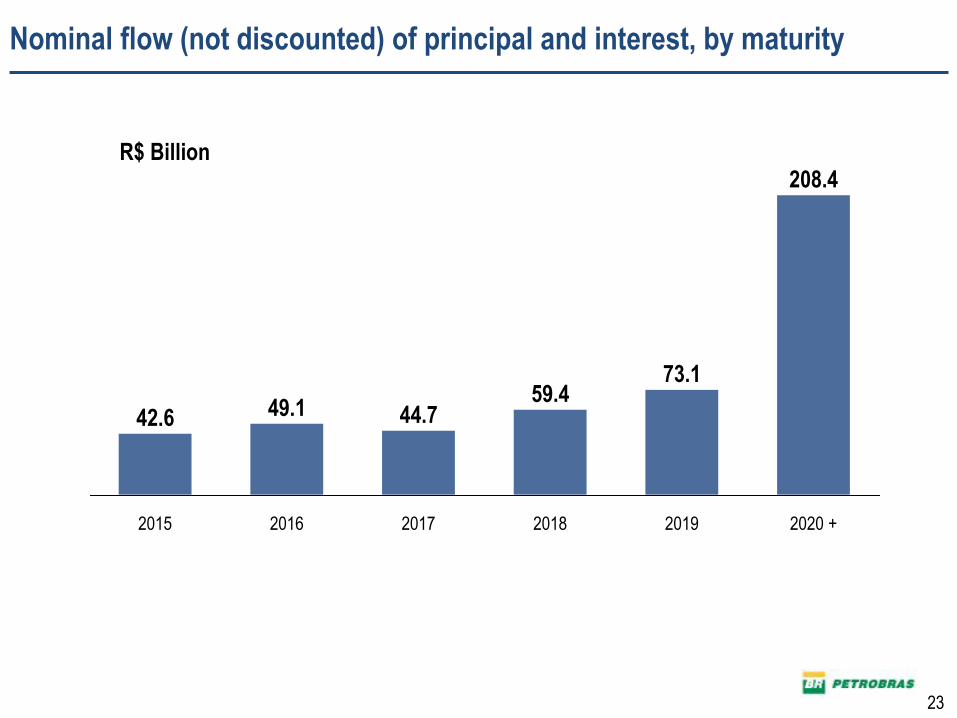

Nominal flow (not discounted) of principal and interest, by maturity

42.6

2015

73.1

2017 2018

44.7 49.1 59.4

2020 +

208.4

2019 2016

R$ Billion

23

24

US$ Billion

US$ 60 /bbl

R$ 3,10 /US$

Oil Price

(Average)

Exchange Rate

(Average)

2013

13

23

26

Funding Needs Rollovers 2015 Final Cash

Position

Divestments 2015 Initial Cash

Position

Investments

-29

Interest,

Amortizations

and Others

-18

Operating

Cash Flow

2015 Cash Flow

2,796 kboed Total Production

(Brazil and Abroad)

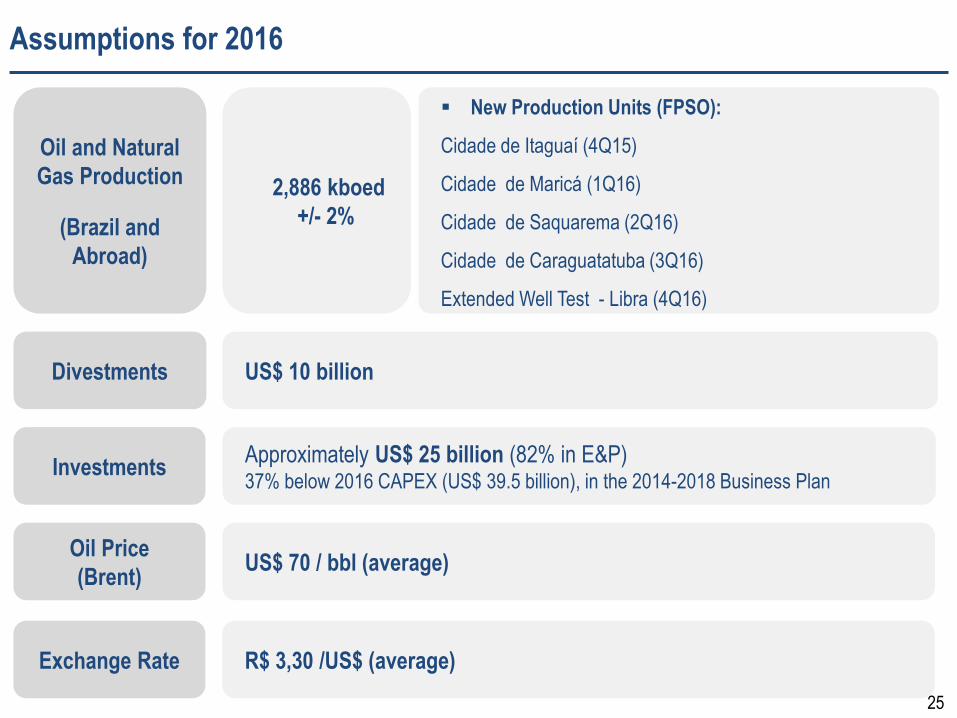

Assumptions for 2016

25

New Production Units (FPSO):

Cidade de Itaguaí (4Q15)

Cidade de Maricá (1Q16)

Cidade de Saquarema (2Q16)

Cidade de Caraguatatuba (3Q16)

Extended Well Test - Libra (4Q16)

Oil and Natural

Gas Production

(Brazil and

Abroad)

US$ 10 billion Divestments

Approximately US$ 25 billion (82% in E&P) 37% below 2016 CAPEX (US$ 39.5 billion), in the 2014-2018 Business Plan

Investments

2,886 kboed

+/- 2%

US$ 70 / bbl (average) Oil Price

(Brent)

R$ 3,30 /US$ (average) Exchange Rate

RESULTS ANNOUNCEMENT

4th Quarter and

2014 Year End Results

__

Information:

Investor Relations

+55 21 3224-1510