Download - TPL May 29 15

ABRAHAM [email protected]

2015 issue 10May 29, 2015

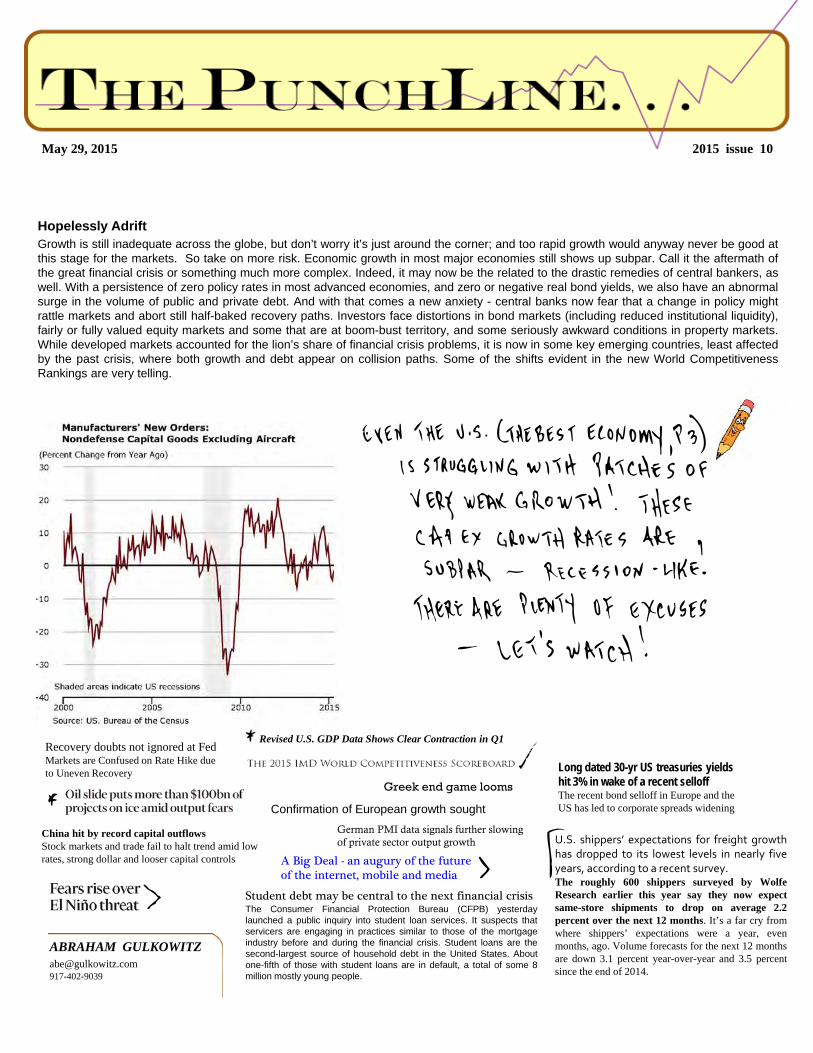

Hopelessly AdriftGrowth is still inadequate across the globe, but don’t worry it’s just around the corner; and too rapid growth would anyway never be good atthis stage for the markets. So take on more risk. Economic growth in most major economies still shows up subpar. Call it the aftermath ofthe great financial crisis or something much more complex. Indeed, it may now be the related to the drastic remedies of central bankers, aswell. With a persistence of zero policy rates in most advanced economies, and zero or negative real bond yields, we also have an abnormalsurge in the volume of public and private debt. And with that comes a new anxiety - central banks now fear that a change in policy mightrattle markets and abort still half-baked recovery paths. Investors face distortions in bond markets (including reduced institutional liquidity),fairly or fully valued equity markets and some that are at boom-bust territory, and some seriously awkward conditions in property markets.While developed markets accounted for the lion’s share of financial crisis problems, it is now in some key emerging countries, least affectedby the past crisis, where both growth and debt appear on collision paths. Some of the shifts evident in the new World CompetitivenessRankings are very telling.

Student debt may be central to the next financial crisisThe Consumer Financial Protection Bureau (CFPB) yesterdaylaunched a public inquiry into student loan services. It suspects thatservicers are engaging in practices similar to those of the mortgageindustry before and during the financial crisis. Student loans are thesecond-largest source of household debt in the United States. Aboutone-fifth of those with student loans are in default, a total of some 8million mostly young people.

Confirmation of European growth sought

Long dated 30-yr US treasuries yields hit 3% in wake of a recent selloffThe recent bond selloff in Europe and the US has led to corporate spreads widening

China hit by record capital outflowsStock markets and trade fail to halt trend amid lowrates, strong dollar and looser capital controls

German PMI data signals further slowing of private sector output growth

Recovery doubts not ignored at FedMarkets are Confused on Rate Hike due to Uneven Recovery

U.S. shippers’ expectations for freight growthhas dropped to its lowest levels in nearly fiveyears, according to a recent survey.The roughly 600 shippers surveyed by WolfeResearch earlier this year say they now expectsame-store shipments to drop on average 2.2percent over the next 12 months. It’s a far cry fromwhere shippers’ expectations were a year, evenmonths, ago. Volume forecasts for the next 12 monthsare down 3.1 percent year-over-year and 3.5 percentsince the end of 2014.

Greek end game looms

Revised U.S. GDP Data Shows Clear Contraction in Q1

A Big Deal - an augury of the future of the internet, mobile and media

The PunchLine...

2

May 29, 2015

In This Issue

Headlines and data appearing in The Punch Line came from widely available publications including national and international newspapers, trade journals, economic and industrial bulletins and news websites.

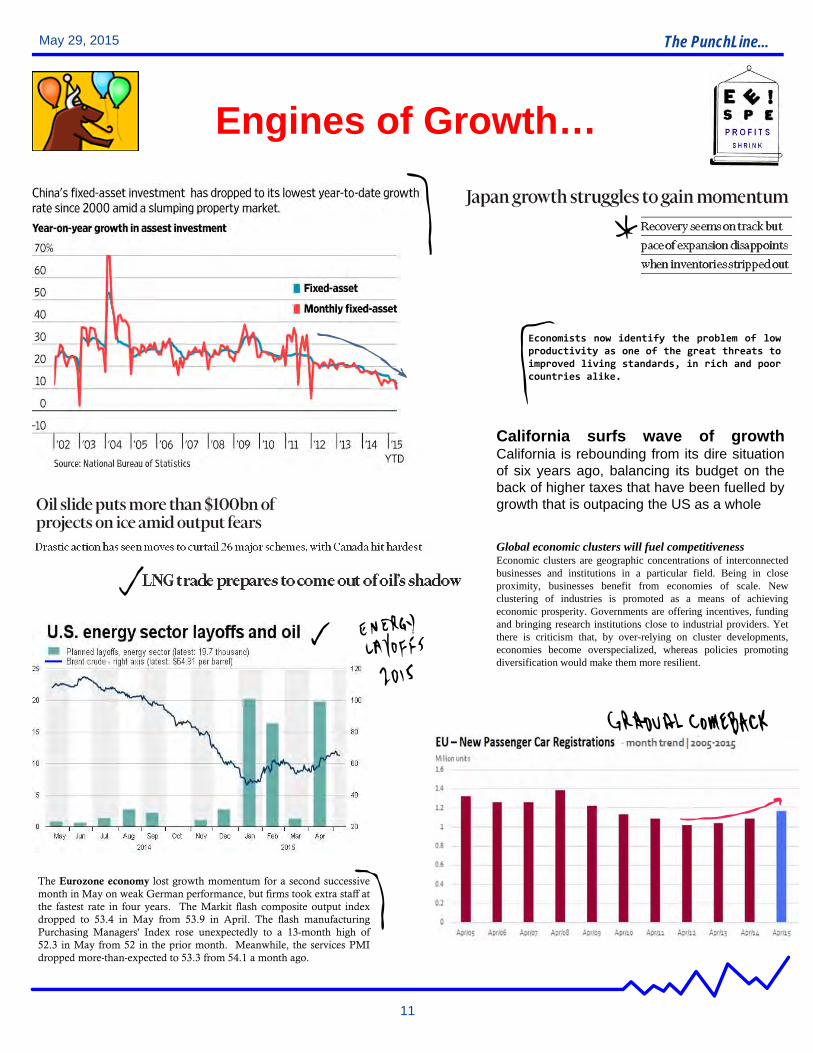

• Engines of GrowthConflicting economic signals emanating around the globe have confoundedinvestors and contributed to intermittent bouts of volatility, even in governmentbond markets. Despite massive easing, most of the global economy faceswoefully inadequate growth prospects and difficult policy options. Very obviousfinancial vulnerabilities, and serious geopolitical concerns are aggravating theuncertainty. And let’s not forget that many of the challenges are not fleetingand cannot be resolved easily … (pg 11)

• Credit… (pg 12)

• A New Geography of Business… (pg 13)

• Pumping Iron … (pg 14)

• The DNA of Business… (pg 15)

• Real Estate and Construction… (pg 16)

• Will Life Ever be the Same? (pg 17)

• Hopelessly Adrift… Growth is still inadequate across the globe, but don’t worry it’s just around

the corner; and too rapid growth would anyway never be good at this stagefor the markets. So take on more risk. Economic growth in most majoreconomies still shows up subpar. Call it the aftermath of the great financialcrisis or something much more complex. Indeed, it may now be the related tothe drastic remedies of central bankers, as well. With a persistence of zeropolicy rates in most advanced economies, and zero or negative real bondyields, we also have an abnormal surge in the volume of public and privatedebt. And with that comes a new anxiety - central banks now fear that achange in policy might rattle markets and abort still half-baked recoverypaths. Investors face distortions in bond markets (including reducedinstitutional liquidity), fairly or fully valued equity markets and some that are atboom-bust territory, and some seriously awkward conditions in propertymarkets. While developed markets accounted for the lion’s share of financialcrisis problems, it is now in some key emerging countries, least affected bythe past crisis, where both growth and debt appear on collision paths. Someof the shifts evident in the new World Competitiveness Rankings are verytelling. (pg 1)

• In This Issue (pg 2)

• New World Rankings… (pg 3)

• Dislocation, Dislocation… (pg 4)

• The Return to Normal… (pg 5)

• You Can’t Handle the Truth ! (pg 6)

• Market Roar… (pg 7)

• Households… (pg 8)

• Think it Through… (pg 9)

• The Likelihood of Unlikely Events... (pg 10)

Contact information:

Abraham Gulkowitz

phone: 917-402-9039 email: [email protected]

The PunchLine...

3

May 29, 2015

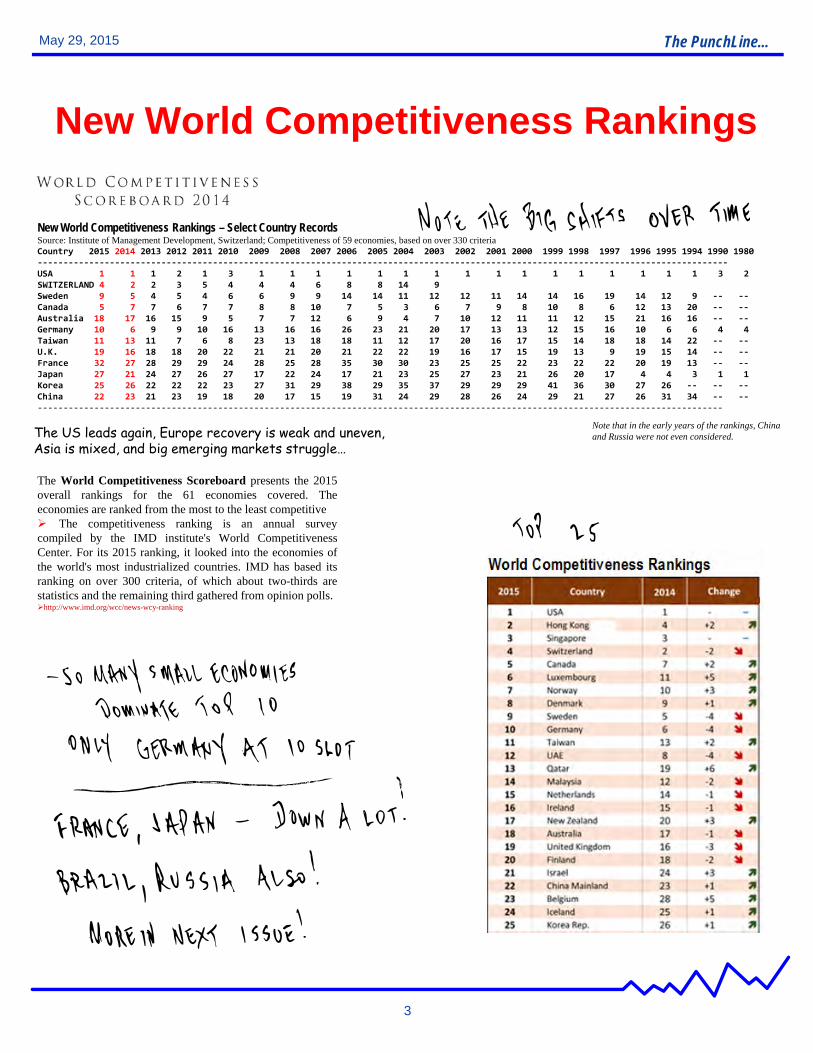

New World Competitiveness Rankings

The World Competitiveness Scoreboard presents the 2015overall rankings for the 61 economies covered. Theeconomies are ranked from the most to the least competitive The competitiveness ranking is an annual surveycompiled by the IMD institute's World CompetitivenessCenter. For its 2015 ranking, it looked into the economies ofthe world's most industrialized countries. IMD has based itsranking on over 300 criteria, of which about two-thirds arestatistics and the remaining third gathered from opinion polls.http://www.imd.org/wcc/news-wcy-ranking

New World Competitiveness Rankings – Select Country RecordsSource: Institute of Management Development, Switzerland; Competitiveness of 59 economies, based on over 330 criteria Country 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1990 1980‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐USA 1 1 1 2 1 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 3 2SWITZERLAND 4 2 2 3 5 4 4 4 6 8 8 14 9 Sweden 9 5 4 5 4 6 6 9 9 14 14 11 12 12 11 14 14 16 19 14 12 9 ‐‐ ‐‐Canada 5 7 7 6 7 7 8 8 10 7 5 3 6 7 9 8 10 8 6 12 13 20 ‐‐ ‐‐Australia 18 17 16 15 9 5 7 7 12 6 9 4 7 10 12 11 11 12 15 21 16 16 ‐‐ ‐‐Germany 10 6 9 9 10 16 13 16 16 26 23 21 20 17 13 13 12 15 16 10 6 6 4 4Taiwan 11 13 11 7 6 8 23 13 18 18 11 12 17 20 16 17 15 14 18 18 14 22 ‐‐ ‐‐U.K. 19 16 18 18 20 22 21 21 20 21 22 22 19 16 17 15 19 13 9 19 15 14 ‐‐ ‐‐France 32 27 28 29 29 24 28 25 28 35 30 30 23 25 25 22 23 22 22 20 19 13 ‐‐ ‐‐Japan 27 21 24 27 26 27 17 22 24 17 21 23 25 27 23 21 26 20 17 4 4 3 1 1Korea 25 26 22 22 22 23 27 31 29 38 29 35 37 29 29 29 41 36 30 27 26 ‐‐ ‐‐ ‐‐China 22 23 21 23 19 18 20 17 15 19 31 24 29 28 26 24 29 21 27 26 31 34 ‐‐ ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐

Note that in the early years of the rankings, China and Russia were not even considered.The US leads again, Europe recovery is weak and uneven,

Asia is mixed, and big emerging markets struggle…

The PunchLine...

4

May 29, 2015

Dislocation, Dislocation, Dislocation

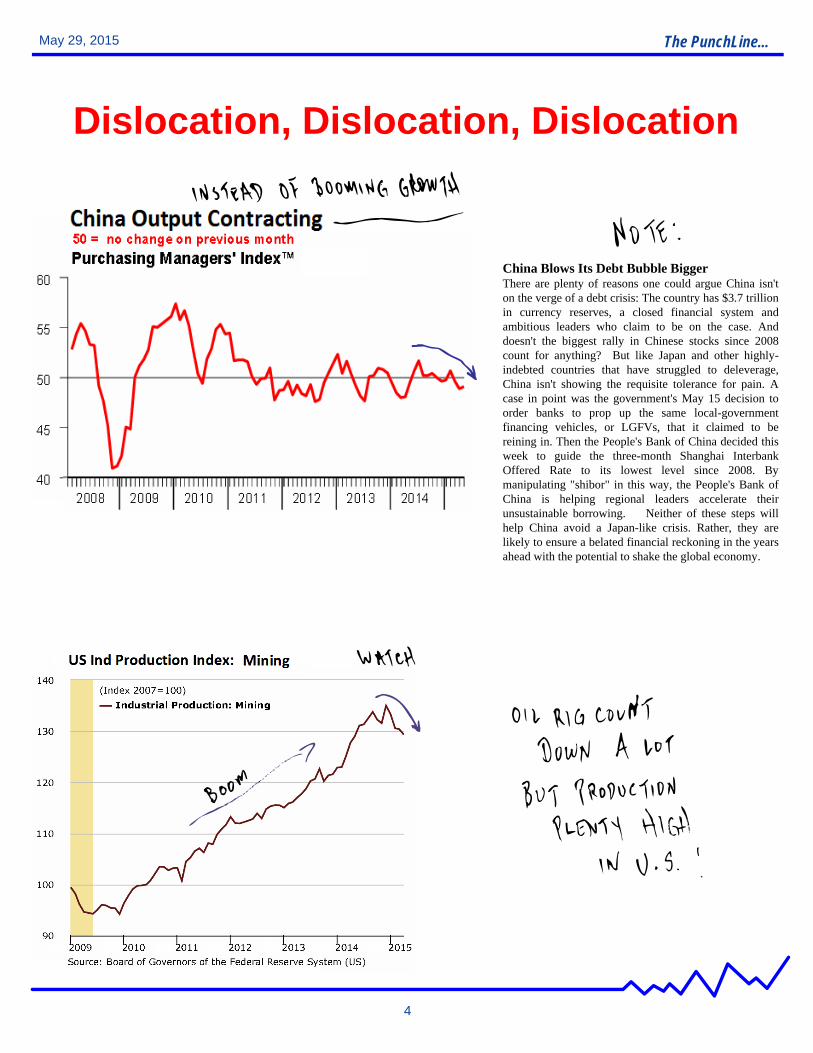

China Blows Its Debt Bubble BiggerThere are plenty of reasons one could argue China isn'ton the verge of a debt crisis: The country has $3.7 trillionin currency reserves, a closed financial system andambitious leaders who claim to be on the case. Anddoesn't the biggest rally in Chinese stocks since 2008count for anything? But like Japan and other highly-indebted countries that have struggled to deleverage,China isn't showing the requisite tolerance for pain. Acase in point was the government's May 15 decision toorder banks to prop up the same local-governmentfinancing vehicles, or LGFVs, that it claimed to bereining in. Then the People's Bank of China decided thisweek to guide the three-month Shanghai InterbankOffered Rate to its lowest level since 2008. Bymanipulating "shibor" in this way, the People's Bank ofChina is helping regional leaders accelerate theirunsustainable borrowing. Neither of these steps willhelp China avoid a Japan-like crisis. Rather, they arelikely to ensure a belated financial reckoning in the yearsahead with the potential to shake the global economy.

The PunchLine...

5

May 29, 2015

The Return to Normal ?

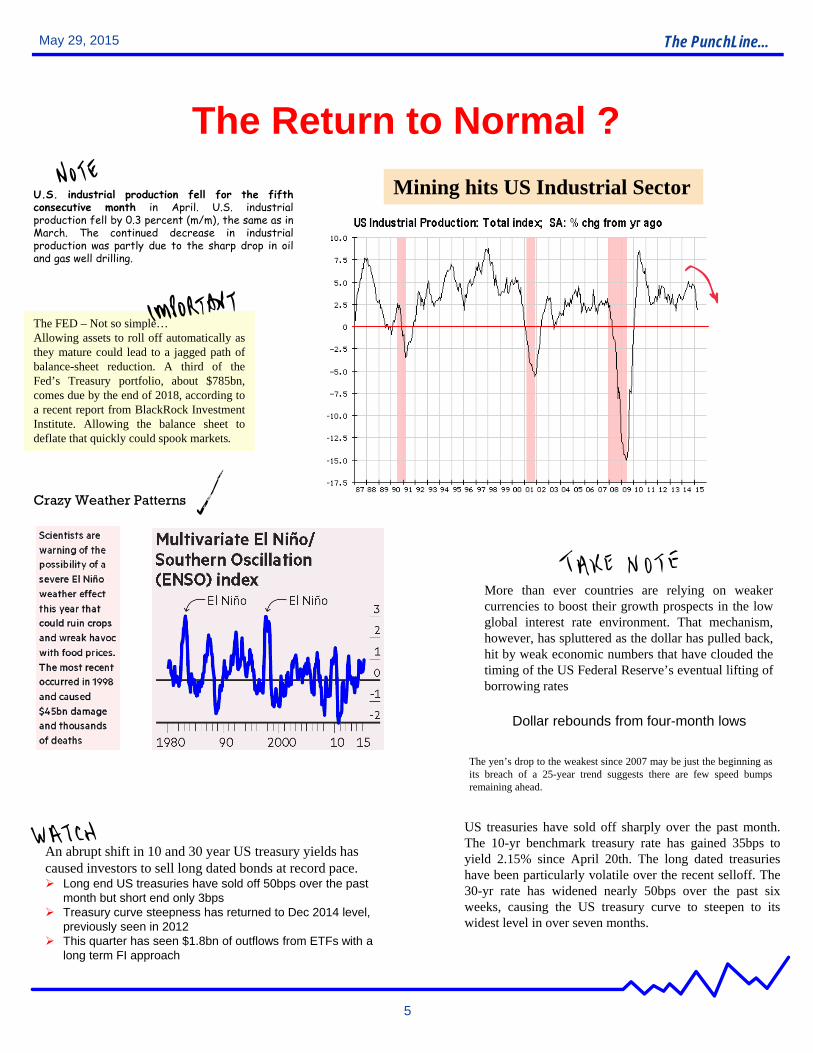

U.S. industrial production fell for the fifthconsecutive month in April. U.S. industrialproduction fell by 0.3 percent (m/m), the same as inMarch. The continued decrease in industrialproduction was partly due to the sharp drop in oiland gas well drilling.

Crazy Weather Patterns

US treasuries have sold off sharply over the past month.The 10-yr benchmark treasury rate has gained 35bps toyield 2.15% since April 20th. The long dated treasurieshave been particularly volatile over the recent selloff. The30-yr rate has widened nearly 50bps over the past sixweeks, causing the US treasury curve to steepen to itswidest level in over seven months.

Dollar rebounds from four-month lows

An abrupt shift in 10 and 30 year US treasury yields has caused investors to sell long dated bonds at record pace. Long end US treasuries have sold off 50bps over the past

month but short end only 3bps Treasury curve steepness has returned to Dec 2014 level,

previously seen in 2012 This quarter has seen $1.8bn of outflows from ETFs with a

long term FI approach

The yen’s drop to the weakest since 2007 may be just the beginning asits breach of a 25-year trend suggests there are few speed bumpsremaining ahead.

More than ever countries are relying on weakercurrencies to boost their growth prospects in the lowglobal interest rate environment. That mechanism,however, has spluttered as the dollar has pulled back,hit by weak economic numbers that have clouded thetiming of the US Federal Reserve’s eventual lifting ofborrowing rates

The FED – Not so simple…Allowing assets to roll off automatically asthey mature could lead to a jagged path ofbalance-sheet reduction. A third of theFed’s Treasury portfolio, about $785bn,comes due by the end of 2018, according toa recent report from BlackRock InvestmentInstitute. Allowing the balance sheet todeflate that quickly could spook markets.

Mining hits US Industrial Sector

The PunchLine...

6

May 29, 2015

YouCan’t Handle the Truth…Let's Take the “Con” out of Economics

Financial sector in advanced economies is too big, says IMFThe role of the financial sector in the US, Japan and otheradvanced economies has grown too big, the InternationalMonetary Fund has warned. They pointed to growingevidence that at a certain stage banks and otherfinancial institutions assume too big a share ineconomies and end up contributing more to financialinstability than economic growth.

U.S. Corporate Bond Market Tallies Record New IssuanceFavorable borrowing conditions for U.S. companies in the bond market,despite a slight rise in both coupons and spreads for riskier credits, continue tosupport strong issuance. Corporate bonds outstanding total $3.8 trillion, with$200 billion in new bond issuance recorded in the first quarter. The share ofcorporates affected by downgrades in the first quarter of this year was 2.8%.Upgrades impacted just 0.8% of the market in the first quarter, with nearly alloccurring in high yield.

Artificial Sweetener

EMEA Corporates Benefit from Search for Yield as Funding Costs FallCompanies continued to benefit from tightening spreads in early 2015as the ECB's sovereign bond‐buying program kicked off. Investorsplowed into blue‐chip credits to shelter from negative yields on anincreasing amount of eurozone sovereign debt and as measured "risk‐on" returned to European high yield.

European Leveraged Loan Borrowers Enter a New CycleRising leverage and weaker underwriting standards in theEuropean leveraged loan market are offset by amplebalance sheet liquidity and long-dated maturity profiles.

Eurozone consumer confidence deteriorated for asecond straight month in May and at a faster-than-expected pace, preliminary estimates from theEuropean Commission showed Thursday. Theflash consumer confidence index dropped to -5.5from -4.6 in April. Economists had forecast ascore of -4.8. The indicator had dropped for thefirst time in five months in April.

The combined real GDP for Organization for EconomicCooperation and Development (OECD) countries advanced 0.3percent in Q1, slower than the 0.5 percent expansion in Q4.Among the G7 economies, growth slowed most significantly inthe United States to 0.1 percent from 0.5 percent in Q4 and that inGermany fell to 0.3 percent from 0.7 percent. Growth halved inthe United Kingdom to 0.3 percent from 0.6 percent. In contrast,economic growth picked up strongly in France to 0.6 percent aftershowing flat growth in Q4. Growth also accelerated in Japan,doubling from 0.3 percent to 0.6 percent.

European officials downplayed the prospectsof any imminent releasing of funding for cash-strapped Greece

China’s Shanghai Composite Index plunged 6.5 percent in record highturnover, one of its steepest single-day drop in 15 years, as investorsrushed to sell after several major brokerages tightened margin financingrequirements for client and the central bank drained money marketliquidity through an “unusual” bond sale mechanism. Another factor wasreports that Chinese sovereign wealth fund sold shares in the country’stwo largest state-owned banks for the first time. Japan’s Nikkei 225stock index closed 0.4% higher after gaining nearly 10 percent in thepast three months, helped by a cheaper yen that benefits exporterstocks. U.S. and European shares were mostly lower after a volatileAsian session.

The PunchLine...

7

May 29, 2015

The Market Roar…

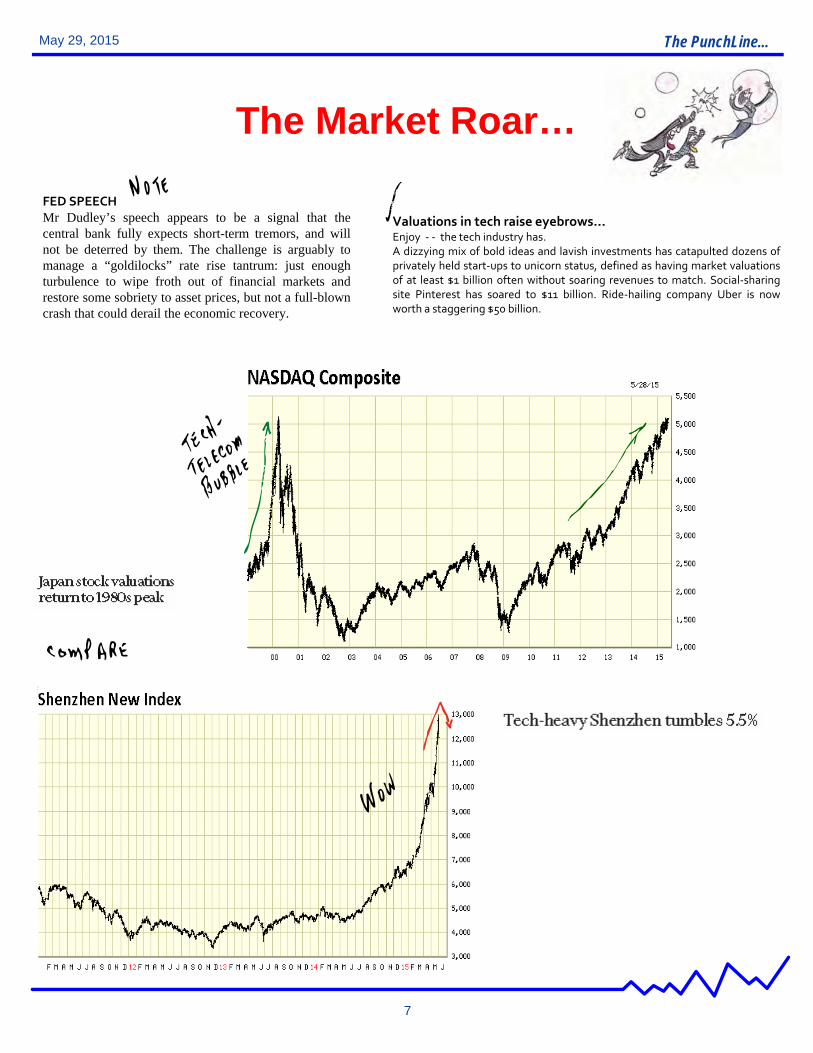

Valuations in tech raise eyebrows… Enjoy ‐ ‐ the tech industry has. A dizzying mix of bold ideas and lavish investments has catapulted dozens ofprivately held start‐ups to unicorn status, defined as having market valuationsof at least $1 billion often without soaring revenues to match. Social‐sharingsite Pinterest has soared to $11 billion. Ride‐hailing company Uber is nowworth a staggering $50 billion.

FED SPEECHMr Dudley’s speech appears to be a signal that thecentral bank fully expects short-term tremors, and willnot be deterred by them. The challenge is arguably tomanage a “goldilocks” rate rise tantrum: just enoughturbulence to wipe froth out of financial markets andrestore some sobriety to asset prices, but not a full-blowncrash that could derail the economic recovery.

The PunchLine...

8

May 29, 2015

Households – Brave New World

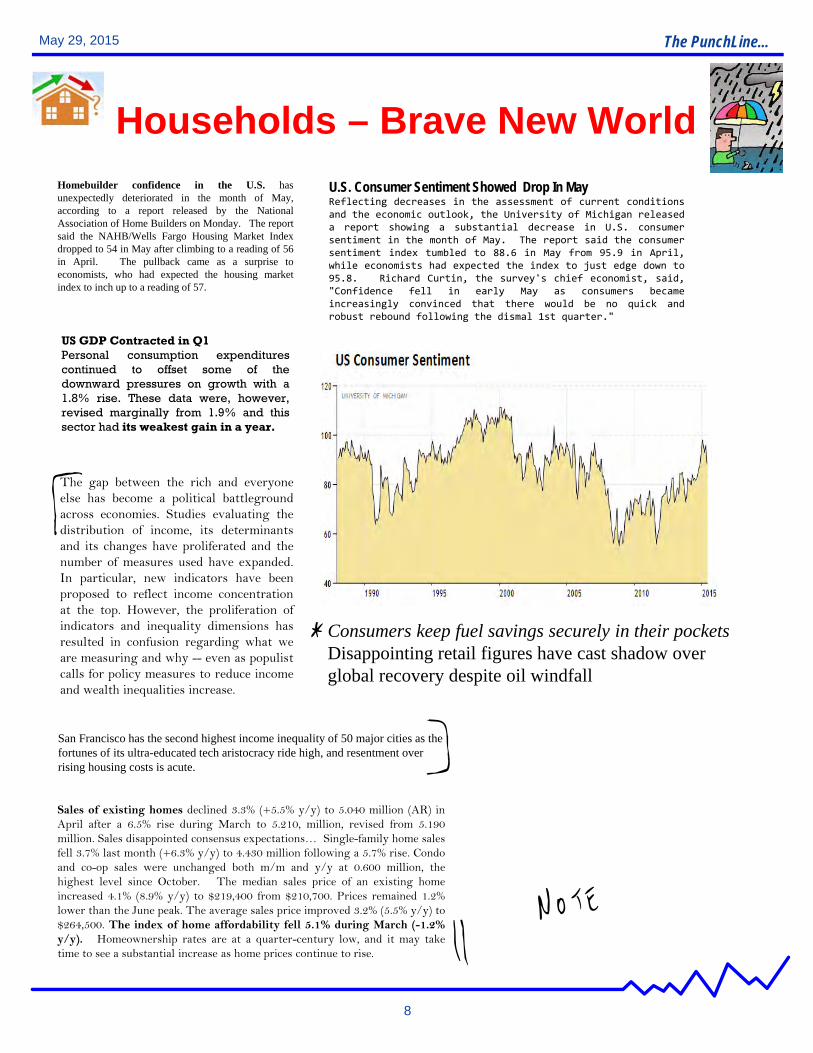

Homebuilder confidence in the U.S. hasunexpectedly deteriorated in the month of May,according to a report released by the NationalAssociation of Home Builders on Monday. The reportsaid the NAHB/Wells Fargo Housing Market Indexdropped to 54 in May after climbing to a reading of 56in April. The pullback came as a surprise toeconomists, who had expected the housing marketindex to inch up to a reading of 57.

U.S. Consumer Sentiment Showed Drop In MayReflecting decreases in the assessment of current conditionsand the economic outlook, the University of Michigan releaseda report showing a substantial decrease in U.S. consumersentiment in the month of May. The report said the consumersentiment index tumbled to 88.6 in May from 95.9 in April,while economists had expected the index to just edge down to95.8. Richard Curtin, the survey's chief economist, said,"Confidence fell in early May as consumers becameincreasingly convinced that there would be no quick androbust rebound following the dismal 1st quarter."

The gap between the rich and everyoneelse has become a political battlegroundacross economies. Studies evaluating thedistribution of income, its determinantsand its changes have proliferated and thenumber of measures used have expanded.In particular, new indicators have beenproposed to reflect income concentrationat the top. However, the proliferation ofindicators and inequality dimensions hasresulted in confusion regarding what weare measuring and why -- even as populistcalls for policy measures to reduce incomeand wealth inequalities increase.

Sales of existing homes declined 3.3% (+5.5% y/y) to 5.040 million (AR) inApril after a 6.5% rise during March to 5.210, million, revised from 5.190million. Sales disappointed consensus expectations… Single-family home salesfell 3.7% last month (+6.3% y/y) to 4.430 million following a 5.7% rise. Condoand co-op sales were unchanged both m/m and y/y at 0.600 million, thehighest level since October. The median sales price of an existing homeincreased 4.1% (8.9% y/y) to $219,400 from $210,700. Prices remained 1.2%lower than the June peak. The average sales price improved 3.2% (5.5% y/y) to$264,500. The index of home affordability fell 5.1% during March (-1.2%y/y). Homeownership rates are at a quarter-century low, and it may taketime to see a substantial increase as home prices continue to rise.

Consumers keep fuel savings securely in their pocketsDisappointing retail figures have cast shadow over global recovery despite oil windfall

San Francisco has the second highest income inequality of 50 major cities as the fortunes of its ultra-educated tech aristocracy ride high, and resentment over rising housing costs is acute.

US GDP Contracted in Q1Personal consumption expenditurescontinued to offset some of thedownward pressures on growth with a1.8% rise. These data were, however,revised marginally from 1.9% and thissector had its weakest gain in a year.

The PunchLine...

9

May 29, 2015

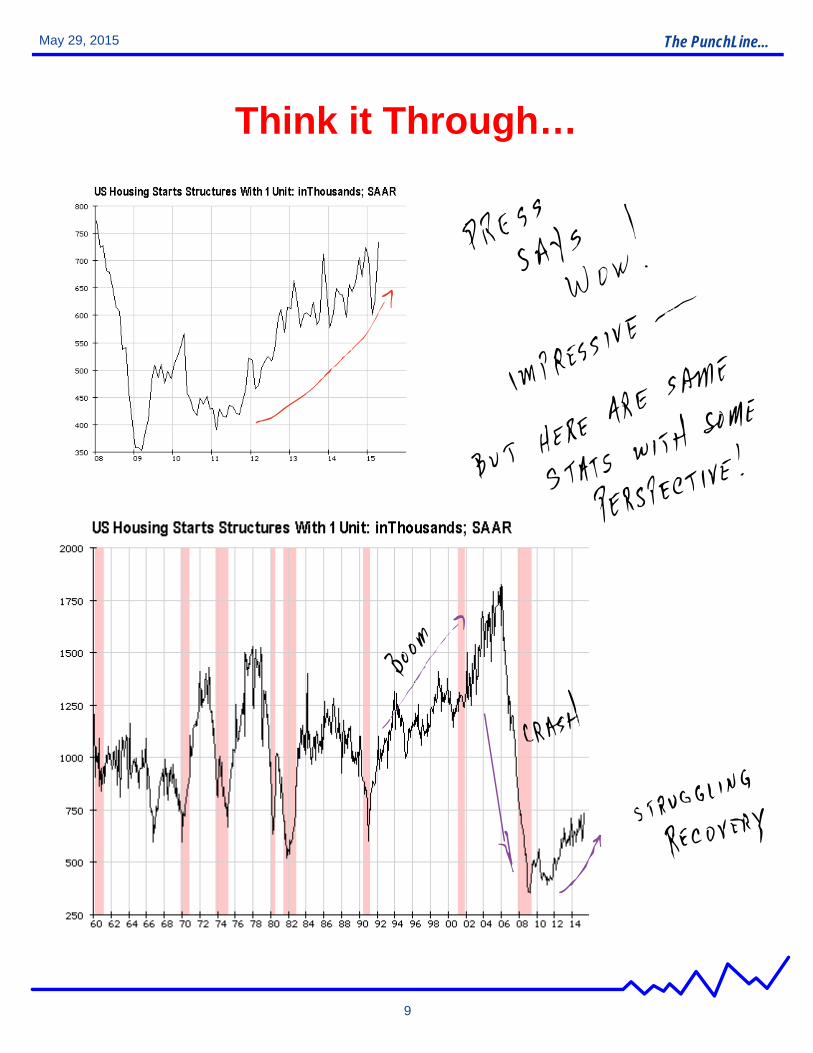

Think it Through…

The PunchLine...

10

May 29, 2015

The Likelihood of Unlikely Events

Scenario modelling Needs major rethinkForecasting failures over the past decade have accelerated methodological changes,moving away from point estimates towards a larger use of forecast ranges and alternativescenarios. More risk indicators have been added to forecasters' watch list, developingearly warning signals. Given estimates for key economic determinants, many othervariables' outcomes are predictable based on these key factors, thanks to the importanceof dominant drivers and the slow‐moving nature of some underlying trends. Forecastersare looking for better ways of predicting and assessing combinations of events that pushoutcomes beyond 'normal boundaries'.

The other element of difficulty is the lack of focus on micro or sectoral triggers for riskconsideration. Missing inadequacies in the housing and mortgage markets, in tech ortelecom, or in select emerging markets will often translate into missing the major turningpoints. Very few excel in this new world…

Local international considerations are also a major deficiency… For example, the Russiaeconomic downturn is aggravated by the difficulties in the budgets of regional and localauthorities. On March 30, four regional governments announced that they planned toissue bonds. The federal government was reported to be restructuring regions' debts tothe federal budget, with a long grace period and a refinancing rate of 0.1% at a time ofdouble‐digit inflation. On April 1, the federal government said it would be giving 16.9billion rubles in small‐business subsidies to the regional authorities and plans formortgage subsidies to halt the 30‐40% drop in the pace of construction in the regions.

Mario Draghi has warned central banks to beware of the risk thataggressive monetary easing, including mass bond buying, could lead tofinancial instability and worsen income inequality. The EuropeanCentral Bank president said the apparent success of policies such as theECB’s €1.1tn quantitative easing package should not “blind” policymakers to the potential consequences of their actions on risk-taking infinancial markets and in exacerbating wealth disparities. “Because theuse of these new instruments can have different consequences thanconventional monetary policy, in particular with respect to thedistribution of wealth and the allocation of resources, it has become moreimportant that those consequences are identified, weighed and wherenecessary mitigated,” Mr Draghi said at the International Monetary Fundin Washington.

China slowdown deepens provincial divideHardest-hit regions are those that relied on debt-fuelled investment binges

US-China sea disputes will draw in alliesSecretary of Defense Ashton Carter on May 27 said that the UnitedStates "will remain the principal security power in the Asia-Pacificfor decades to come", a day after the Chinese State Councilreleased a white paper placing greater priority on its navy and"open seas protection". Increased anxiety over Chinese landreclamation in the South China Sea, particularly its construction ofan airstrip and harbour on Fiery Cross Reef, is drawingconsiderable attention to US policy in the region where US allieshave been pressing for greater involvement.

The PunchLine...

11

May 29, 2015

Engines of Growth…

California surfs wave of growthCalifornia is rebounding from its dire situationof six years ago, balancing its budget on theback of higher taxes that have been fuelled bygrowth that is outpacing the US as a whole

Global economic clusters will fuel competitivenessEconomic clusters are geographic concentrations of interconnectedbusinesses and institutions in a particular field. Being in closeproximity, businesses benefit from economies of scale. Newclustering of industries is promoted as a means of achievingeconomic prosperity. Governments are offering incentives, fundingand bringing research institutions close to industrial providers. Yetthere is criticism that, by over-relying on cluster developments,economies become overspecialized, whereas policies promotingdiversification would make them more resilient.

The Eurozone economy lost growth momentum for a second successivemonth in May on weak German performance, but firms took extra staff atthe fastest rate in four years. The Markit flash composite output indexdropped to 53.4 in May from 53.9 in April. The flash manufacturingPurchasing Managers' Index rose unexpectedly to a 13-month high of52.3 in May from 52 in the prior month. Meanwhile, the services PMIdropped more-than-expected to 53.3 from 54.1 a month ago.

Economists now identify the problem of lowproductivity as one of the great threats toimproved living standards, in rich and poorcountries alike.

The PunchLine...

12

May 29, 2015

Credit Matters-Know RiskMany Excel in Strategy, Few in the Management of Risk

The international norms that have evolved over timepoint to the factors that determine when debt should bereduced. Most important, when a country’s debts are solarge, and its economic prospects so poor, that there isno realistic prospect of its debt being paid back in full,it is accepted that debt reduction is appropriate as amatter of burden sharing and as a way to reduce theeffect of overhanging debt on growth. Things becomeclearer in cases when debt reduction would not be asource of systemic risk to the global financial system orlicense widespread defaults.

Euro-area bond sell-off may be just a technical correctionThe sharp fall in the prices of government bonds, which has wiped 450 billiondollars off the value of sovereign debt over the past month, is attributable tocrowded positioning by investors. It is unlikely to be the start of a 'reflationtrade' stemming from a sudden improvement in the prospects for global growthand inflation. While there is debate about whether the sell-off in longer-datedgovernment debt since mid-April amounts to the start of a bond bear market, themodest recovery in the euro-area and the renewed weakness of the US economysuggest technical factors are at work.

US panel highlights ETFs, bond funds as potential risks

Canadian Finance Minister Joe Oliver said that the 'Volcker Rule' inthe Dodd-Frank financial reform act violates the North AmericanFree Trade Act (NAFTA). The United States continues to export regulatoryparadigms to other countries, which either adopt US ideas as national statutes orendorse multilateral standards. Challenges to regulatory innovation willcomplicate corporate compliance efforts, by introducing additional uncertainty intoan increasingly complex regulatory universe.

The trend out of high yield and intoinvestment grade corporate credit this yearhas been matched by the decreasing yieldpremium between the two underlying indices.High yield credits in the US have seen yieldsdecrease 44bps this year as represented by theiBoxx $ Liquid High Yield Index, in part due toa stabilisation in oil prices. In contrastinvestment grade yields have increased, asrepresented by the iBoxx $ Liquid InvestmentGrade Index.

FITCH: This year U.S. institutional leveraged loan new issuance had its slowest start since 2010.

The MCDX, a credit index referencing 50 municipalsingle name CDS, continues to creep higher. Thelatest spread, 97bps, is 13bps higher than at thestart of the year. The widening credit spreadsignals that cost to protect against municipal bondsdefaulting is becoming more expensive.

The PunchLine...

13

May 29, 2015

A New Geography of Business

Fracking tensions pit US cities against statesLocal communities that try to ban drilling are coming up against strong resistance

Saudi Arabia’s oil exports to the US have fallen to thelowest level since the financial crisis, highlighting the impact ofthe shale boom and fast-growing imports from Canada. TheUS has bought an average of less than 1m barrels a day ofSaudi crude over the past year, weekly and monthly USgovernment data show. The kingdom has beencompensating for the sales dip by accelerating its pivot to Asia,as China vies with the US as one of the biggest buyers ofSaudi crude. But any weakening of the economic ties thatbolster Saudi’s relations with the US may still provoke concernin Riyadh, as it undergoes a major power shift.

Britain’s inflation rate fell below zero for the first time in more than half a century, as the drop in food and energy prices depressed the cost of living.

The prolonged state of low oil prices is beginning to adversely affect the Alberta Canada housing market, where prices are currently 17% overvalued.

The Thai baht has gone from being Asia’s best-performingcurrency to its worst this quarter, falling 2.5 percent. While theBank of Thailand denies it is trying to weaken the baht, it haslowered borrowing costs and loosened capital controls in thepast two weeks. Interest-rate swaps signal further easing asthe Thai junta, led by former military leader Prime MinisterPrayuth Chan-Ocha, struggles to boost growth and domesticconfidence after taking power in a coup on May 22 last year.

The chief executive of Royal Dutch Shell on May 19 pledged at anannual general meeting to pursue oil reserves in the Arctic despiteongoing protests in Seattle, Washington, from where the company'sArctic equipment will depart. The Department of the Interior on May 11gave Shell conditional approval to drill in Alaska's Chukchi Sea. Mostsupermajor oil companies have cut capital expenditure in the wake ofthe recent fall in oil prices, but Shell views developing Arctic resourcesas essential to ensuring energy security in future decades. The companyexpects to spend 1 billion dollars on Arctic exploration this year.

TURKEY Slowing growth and a central bank at odds with its increasinglypowerful president has left little to cheer for Turkish bond investors. Thecountry’s currency recently hit an all-time low against the dollar; a trend thatlooks set to continue should the central bank yield to president Erdogan’s lowinterest rate call.

Renminbi internationalisation will gather paceThe State Administration of Foreign Exchange on May 12 announcedthat it will adopt the latest international accounting standards for itsbalance of payments data. This may strengthen China's bid this yearfor inclusion in the IMF's Special Drawing Rights (SDR) currencybasket. Central bank governor Zhou Xiaochuan said last month thatChina is making the renminbi more 'freely usable' in order to qualify.Liberalisation of the renminbi has been accelerated since the globalfinancial crisis, as China seeks to establish a more balanced economy,including a larger and open financial sector and -- with it -- aconvertible currency and more open capital account.

Switzerland's economy contracted at the fastestpace in six years in the first quarter as strongfranc weighed heavily on exports. Grossdomestic product fell unexpectedly by 0.2percent sequentially in the first quarter,reversing the prior quarter's 0.5 percentincrease, data published by the State Secretariatfor Economic Affairs revealed Friday.

The PunchLine...

14

May 29, 2015

Pumping Iron…The Old Economy Revisited

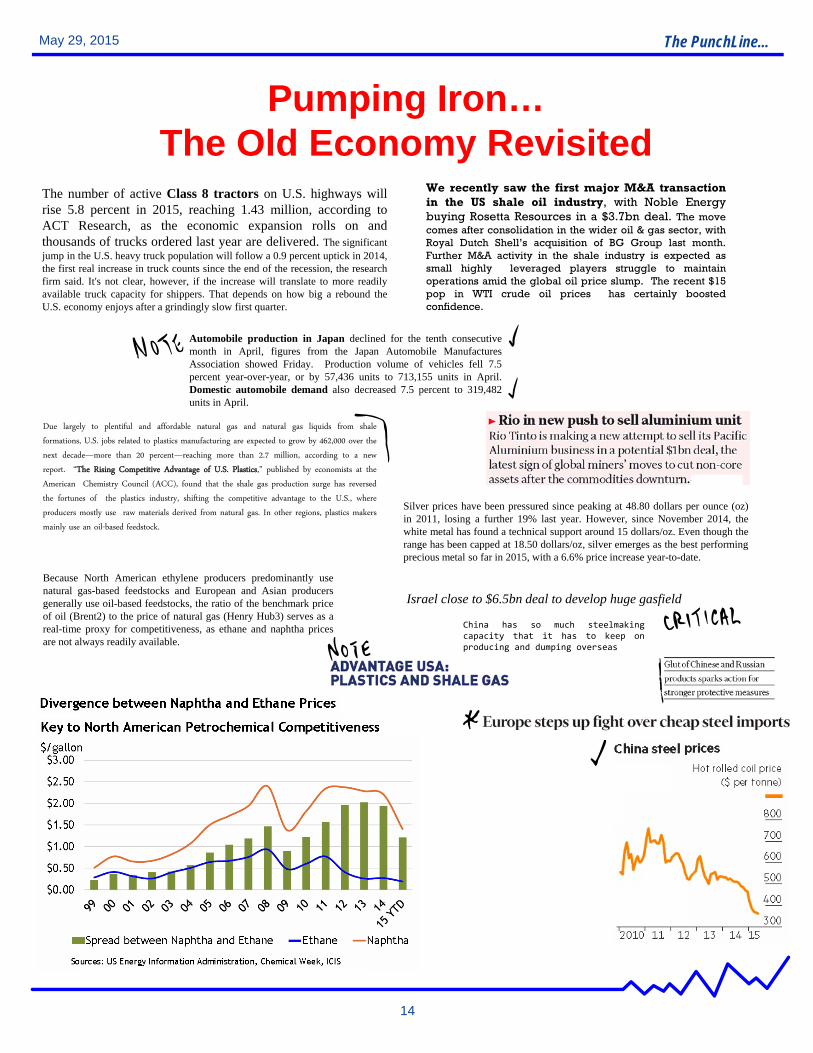

The number of active Class 8 tractors on U.S. highways willrise 5.8 percent in 2015, reaching 1.43 million, according toACT Research, as the economic expansion rolls on andthousands of trucks ordered last year are delivered. The significantjump in the U.S. heavy truck population will follow a 0.9 percent uptick in 2014,the first real increase in truck counts since the end of the recession, the researchfirm said. It's not clear, however, if the increase will translate to more readilyavailable truck capacity for shippers. That depends on how big a rebound theU.S. economy enjoys after a grindingly slow first quarter.

We recently saw the first major M&A transactionin the US shale oil industry, with Noble Energybuying Rosetta Resources in a $3.7bn deal. The movecomes after consolidation in the wider oil & gas sector, withRoyal Dutch Shell’s acquisition of BG Group last month.Further M&A activity in the shale industry is expected assmall highly leveraged players struggle to maintainoperations amid the global oil price slump. The recent $15pop in WTI crude oil prices has certainly boostedconfidence.

Due largely to plentiful and affordable natural gas and natural gas liquids from shaleformations, U.S. jobs related to plastics manufacturing are expected to grow by 462,000 over thenext decade—more than 20 percent—reaching more than 2.7 million, according to a newreport. “The Rising Competitive Advantage of U.S. Plastics,” published by economists at theAmerican Chemistry Council (ACC), found that the shale gas production surge has reversedthe fortunes of the plastics industry, shifting the competitive advantage to the U.S., whereproducers mostly use raw materials derived from natural gas. In other regions, plastics makersmainly use an oil-based feedstock.

Because North American ethylene producers predominantly usenatural gas-based feedstocks and European and Asian producersgenerally use oil-based feedstocks, the ratio of the benchmark priceof oil (Brent2) to the price of natural gas (Henry Hub3) serves as areal-time proxy for competitiveness, as ethane and naphtha pricesare not always readily available.

Silver prices have been pressured since peaking at 48.80 dollars per ounce (oz)in 2011, losing a further 19% last year. However, since November 2014, thewhite metal has found a technical support around 15 dollars/oz. Even though therange has been capped at 18.50 dollars/oz, silver emerges as the best performingprecious metal so far in 2015, with a 6.6% price increase year-to-date.

Israel close to $6.5bn deal to develop huge gasfield

China has so much steelmakingcapacity that it has to keep onproducing and dumping overseas

Automobile production in Japan declined for the tenth consecutivemonth in April, figures from the Japan Automobile ManufacturesAssociation showed Friday. Production volume of vehicles fell 7.5percent year-over-year, or by 57,436 units to 713,155 units in April.Domestic automobile demand also decreased 7.5 percent to 319,482units in April.

The PunchLine...

15

May 29, 2015

The DNA of BusinessReconfiguring Industries to Define Growth

Tech and media ventures mobilise for battleVerizon’s AOL deal and Facebook’s agreement with media groups highlight scale of realignment around smartphones Tracking the technology world’s upheavals is like studying

the shifting of tectonic plates: the direction of movement maybe obvious, but it takes periodic earthquakes to reveal themagnitude of the forces at work. Two sharp tremors thisweek brought home how far the tech, media andcommunications industries are realigning around mobile.The first came on Tuesday, when US telecoms companyVerizon announced a $4.4bn acquisition of AOL. The onlineservices pioneer is a mixed bag these days, which includesthe original internet connectivity business as well as webproperties such as Huffington Post. But Verizon’s sights werefirmly set on something else: a digital advertising platformthat AOL has been building with an eye to plantingcommercial messages into video streams. There has beena spate of similar acquisitions of “adtech” companies asdigital advertising has boomed. What set the AOL deal apart,however, was the fact that the buyer was a communicationscompany whose business is predominantly mobile. With itspurchase of AOL, and a nascent digital video serviceacquired last year from Intel, Verizon is on track for aconfrontation with internet advertising giants Google andFacebook in the battle for mobile video.

Shale Set to Pummel Another Market as U.S. LNG Plants ArriveThe U.S. is about to change the global LNG market forever. When the first tanker carrying liquefiednatural gas from shale fields leaves the Sabine Pass terminal in Louisiana in December, it will turnconsumers into traders with more bargaining power. That will transform a market dominated bylong-term contracts into one where spot trading gains prominence, similar to crude oil. Since thefirst LNG cargo went to the U.K. from Algeria under a long-term contract in 1964, buyers opted forguaranteed supply because the fuel was scarce. That’s changing because gas from the Eagle Fordand other fields will transform the U.S. into the third-biggest exporter by 2020. Spot trading willprobably account for almost half of transactions by then, from 29 percent last year, and LNG ispoised to overtake iron ore as the most valuable commodity after oil. “We see the U.S. as a majorcontributor to the development of the LNG spot market as the volumes start to ramp up,” JamieBuckland, head of investor relations at GasLog Ltd. in London, which owns 22 LNG tankers, wrotein an e-mail May 14. “There should be a lot more flexibility and you could see some buyers of U.S.volumes selling product on to others.”

Outside investors swoop on insurance assetsThe year is on course to be the busiest for dealmaking in the sector since 2010

Boeing Wins $6.1 Billion Plane Order From China Carrier, Lessors

The world’s largest retailer posted resultsthat disappointed Wall Street and showedhow much work it has yet to do to catchrivals. Walmart has blamed a lot of externalfactors for its latest set of lacklusterfinancial results. Shoppers are using taxrefunds and savings from lower gas prices topay down debt instead of shopping more.The strong dollar will lower profit by $14billion this year. The company is grapplingwith food deflation. And on it went. Butwhat the world’s largest retailer , which alsoowns the Sam’s Club chain and WalmartInternational, made little mention of washow well its many competitors are doing,performances that showcase Walmart’sshortcomings and how much work it mustdo to regain its past sales momentum andprofit growth. Walmart’s U.S. comparablesales (includes e-commerce but excludesstores opened or closed in the past year),rose a meager 1.1%, and at Sam’s Club, abarely detectable 0.4%.

IN THE WORKSAvago Agrees to Buy Broadcom for $37 Billion The rival companies have little overlap in their chip and semiconductor products, but by combining, they could gain negotiating power with manufacturers.A merger could combine the two companies' wares to offer comprehensive products to big communications companies, while negotiating cheaper manufacturing costs from the third-party factories where both companies' chips are made.

Intel nears $15 bln deal to buy AlteraWith Liberty Media Chairman JohnMalone working two cable dealssimultaneously, the latest telecominvestment boom that's givenconsumers access to mobile, digitalTV looks to be firmly in itsconsolidation phase. The proposed$55 billion takeover of No. 2 TimeWarner Cable by No. 3 CharterCommunications — in whichLiberty has roughly a 25% stake —comes on the heels of AT&T's $48.5billion acquisition of DirecTV.

The PunchLine...

16

May 29, 2015

Real Estate and Construction Outlook

Office construction in London rises 24%Strong demand spurs second-largest increase in development 20 years

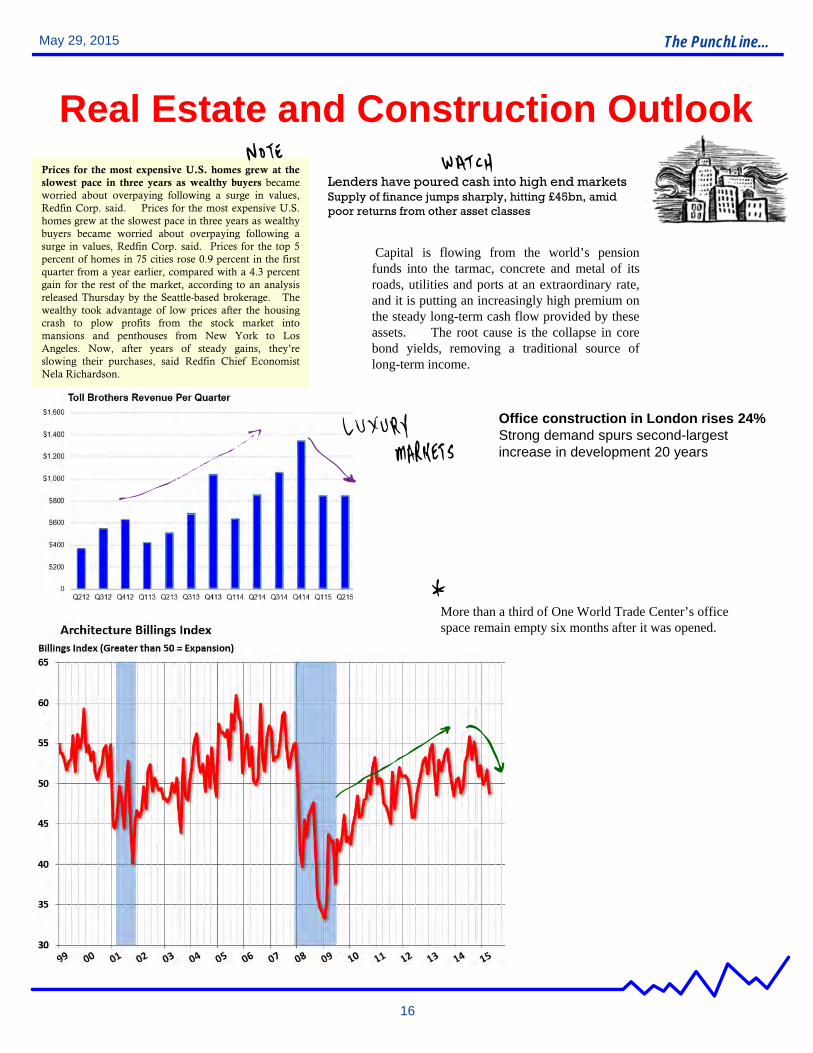

Prices for the most expensive U.S. homes grew at theslowest pace in three years as wealthy buyers becameworried about overpaying following a surge in values,Redfin Corp. said. Prices for the most expensive U.S.homes grew at the slowest pace in three years as wealthybuyers became worried about overpaying following asurge in values, Redfin Corp. said. Prices for the top 5percent of homes in 75 cities rose 0.9 percent in the firstquarter from a year earlier, compared with a 4.3 percentgain for the rest of the market, according to an analysisreleased Thursday by the Seattle-based brokerage. Thewealthy took advantage of low prices after the housingcrash to plow profits from the stock market intomansions and penthouses from New York to LosAngeles. Now, after years of steady gains, they’reslowing their purchases, said Redfin Chief EconomistNela Richardson.

Lenders have poured cash into high end marketsSupply of finance jumps sharply, hitting £45bn, amid poor returns from other asset classes

Capital is flowing from the world’s pensionfunds into the tarmac, concrete and metal of itsroads, utilities and ports at an extraordinary rate,and it is putting an increasingly high premium onthe steady long-term cash flow provided by theseassets. The root cause is the collapse in corebond yields, removing a traditional source oflong-term income.

More than a third of One World Trade Center’s office space remain empty six months after it was opened.

The PunchLine...

17

May 29, 2015

Will Life Ever Be the Same?

This publication is provided to you for information purposes and is not intended as an offer or solicitation for the purchase or sale of any financialinstrument. The information contained herein has been obtained from sources believed to be reliable but is not necessarily complete and itsaccuracy cannot by guaranteed. The views reflected herein are subject to change without notice. No one connected to this publication accepts anyliability whatsoever for any direct or consequential loss arising from any use of this publication or its contents. This publication may not bereproduced, distributed to any person for any purpose without express permission from TPL Advisory, LLC. Please cite source when quoting. Allrights are reserved.