CHAPTER 26

Systemic Contingent Claims Analysis

ANDREAS A. JOBST • DALE F. GRAY

This chapter introduces a new framework for macroprudential analysis using a risk- adjusted balance sheet approach that supports policy eff orts aimed at mitigating systemic risk from linkages between institutions and the extent to which they precipitate or amplify general market dis-

tress. In this regard, a forward- looking framework for mea sur ing systemic solvency risk using an advanced form of contingent claims analysis (CCA), known as “Systemic CCA,” is presented for the systemwide capital assessment in top- down stress testing. The magnitude of joint default risk of multiple fi nancial institutions falling into distress is modeled as a portfolio of individual market- implied expected losses (with individual risk pa ram-e ters) calculated from equity market and balance sheet information. An example of Systemic CCA applied to the U.K. banking sector delivers useful insights about the magnitude of systemic losses in the context of macroprudential stress testing. In addition, the framework also helps quantify the individual contributions of institutions to systemic risk of the fi nancial sector during times of stress.

METHOD SUMMARY

Overview The Systemic Contingent Claims Analysis (Systemic CCA) model extends the traditional risk- adjusted balance sheet model (based on contingent claims analysis) to analyze systemic risk from the interlinkages among institutions, including time- varying dependence of default risk. This approach helps quantify the contribution of individual institutions to systemic (sol-vency) risk and to assess spillover risks from the fi nancial sector to the public sector (and vice versa). In addition, Systemic CCA can be applied to macroprudential stress testing using the historical dynamics of market- implied expected losses.

Application The method is appropriate in situations where access to prudential data is limited but market information is readily available.

Nature of approach Model- based (option pricing, multivariate parametric/nonparametric estimation, credit default swap [CDS] curve pricing).

Data requirements • Accounting information (amounts/maturities) of outstanding liabilities. • Market data on equity and equity option prices. • Various market rates and macro data for satellite model underpinning the stress test. • Sovereign CDS term structure/debt level and debt repayment schedule (if fi nancial sector- sovereign spillover risk is

tested).

Strengths • The model integrates market- implied expected losses (and endogenizes loss given default) in a multivariate specifi cation of joint default risk.

• The approach is highly fl exible and can be used to quantify an individual institution’s time- varying contribution to sys-temic solvency risk under normal and stressed conditions.

Weaknesses • Assumptions are required regarding the specifi cation of the option pricing model (for the determination of implied asset and asset volatility of fi rms).

• Technique is complex and resource intensive.

Tool The Excel VBA- based tool is available with this book. Contact author: A. Jobst.

Large parts of the material in this chapter are published in the Sveriges Riksbank Economic Review, No. 2, pp. 68– 106 (Gray and Jobst, 2011b) and IMF Working Paper 13/54 ( Jobst and Gray, 2013).

536-57355_IMF_StressTestHBk_ch03_3P.indd 409 11/5/14 2:06 AM

Systemic Contingent Claims Analysis 410

former, the contribution to systemic risk arises from the initial eff ect of direct exposures to the failing institution (e.g., defaults on liabilities to counterparties, investors, or other market par-ticipants), which could also spill over to previously unrelated institutions and markets as a result of greater uncertainty or the reassessment of fi nancial risk (i.e., changes in risk appetite and/or the market price of risk). Table 26.1 summarizes the distinguishing features of both approaches.

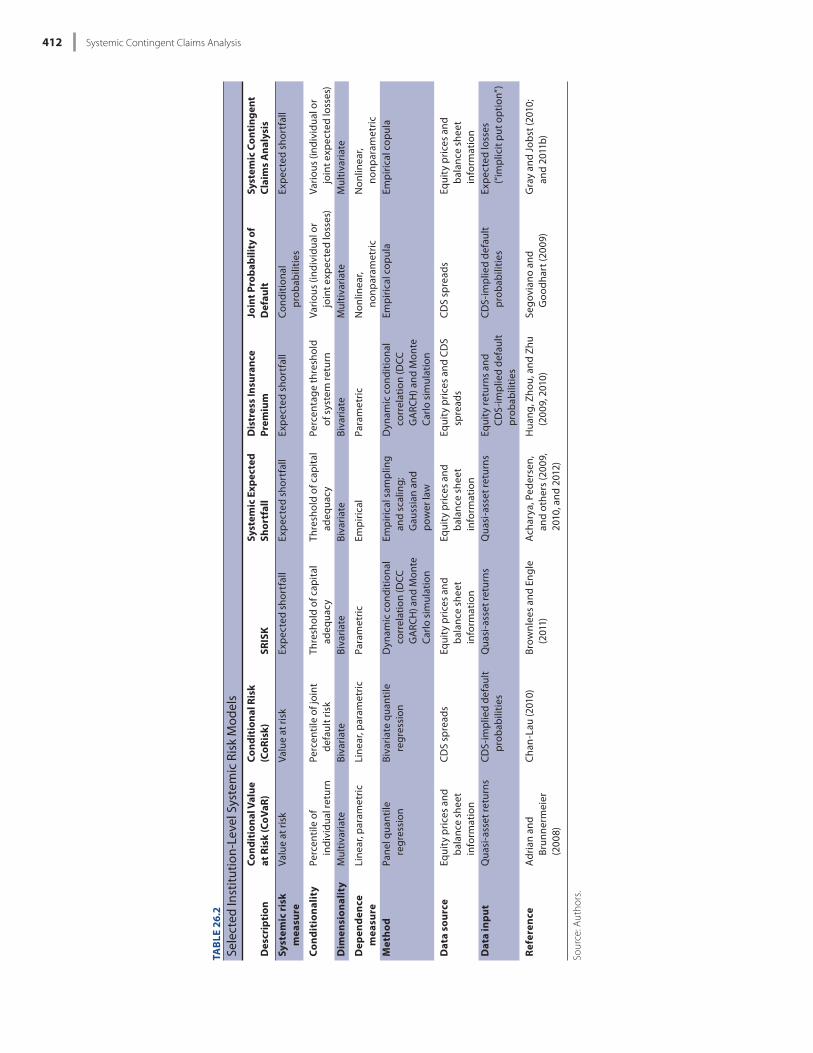

Th e growing literature on systemic risk mea sure ment has responded to greater demand placed on the ability to develop a better understanding of the interlinkages between fi rms and their implications for fi nancial stability (see Table 26.2). Th e specifi cation of dependence between fi rms helps identify common vulnerabilities to risks as a result of the (assumed) collective behavior under common distress ( Jobst, 2013). Most of the prominent institution- level mea sure ment approaches have focused on the contribution approach by including an implicit or explicit treatment of statistical dependence in de-termining joint default risk or expected losses. For instance, Acharya, Pedersen, and others (2009, 2010, 2012) estimate potential losses as marginal expected shortfall (MES) of in-dividual banks in the event of a systemic crisis, which is de-fi ned as the situation when the aggregate equity capital of sample banks falls below some fraction of aggregate assets. Brownlees and Engle (2011) apply the same defi nition for a systemic crisis and formulate a capital shortfall mea sure (“SRISK index”) that is similar to MES; however, they pro-vide a closed- form specifi cation of extreme value dependence underpinning MES by modeling the correlations between the fi rm and market returns using the dynamic conditional correlation (DCC)- GARCH model (Engle and Sheppard, 2001; Engle, 2002). Also, Huang, Zhou, and Zhu (2009, 2010) derive correlation of equity returns via DCC- GARCH as statistical support to motivate the specifi cation of the dependence structure for default probabilities within a sys-tem of fi rms. Both CoVaR and CoRisk (Adrian and Brun-nermeier, 2008; Chan- Lau, 2010) follow the same logic of deriving a bivariate mea sure of dependence between a fi rm’s fi nancial per for mance and an extreme deterioration of market conditions (or that of its peers). For instance, the CoVaR (CoRisk) for a certain fi rm is defi ned as the value at risk (VaR) (as a mea sure of extreme default risk) of the whole sector (fi rm) conditional on a par tic u lar institution being in distress.

However, only a few models estimate multivariate (fi rm- by- fi rm) dependence through either a closed- form specifi ca-tion or the simulation of joint probabilities using historically informed mea sures of association. None of those include a structural defi nition of default risk. A chapter of a recent issue of the Global Financial Stability Report provides comparative analysis of several of these systemic risk mea sures in the con-text of designing early- warning indicators for MPS (IMF,

institution being part of it, which determines the institution’s marginal contribution to systemic risk.

In the wake of the global fi nancial crisis, there has been in-creased focus on systemic risk as a key aspect of macro- prudential policy and surveillance (MPS) with a view toward enhancing the resilience of the fi nancial sector.1 MPS is pred-icated on (1) the assessment of systemwide vulnerabilities and the accurate identifi cation of threats arising from the buildup and unwinding of fi nancial imbalances, (2) shared exposures to macro- fi nancial shocks, and (3) possible conta-gion/spillover eff ects from individual institutions and mar-kets owing to direct or indirect connectedness. Th us, it aims to limit, mitigate, or reduce systemic risk, thereby minimizing the incidence and impact of disruptions in the provision of key fi nancial ser vices that can have adverse consequences for the real economy (and broader implications for economic growth). Systemic risk refers to individual or collective fi -nancial arrangements— both institutional and market- based—which could either lead directly to systemwide distress in the fi nancial sector or signifi cantly amplify its conse-quences (with adverse eff ects on other sectors, in par tic u lar capital formation in the real economy). Typically, such dis-tress manifests itself in disruptions to the fl ow of fi nancial ser vices because of an impairment of all or parts of the fi -nancial system that are deemed material to the functioning of the real economy.2

Although there is still no comprehensive theory of MPS re-lated to the mea sure ment of systemic risk, existing approaches can be distinguished broadly on the basis of their conceptual underpinnings regarding several core principles. Th ere are two general approaches: (1) a par tic u lar activity causes a fi rm to fail, whose importance to the system imposes marginal distress on the system owing to the nature, scope, size, scale, concentra-tion, or connectedness of its activities with other fi nancial in-stitutions (“contribution approach”), or (2) a fi rm experiences losses from a single (or multiple) large shock(s) because of a signifi cant exposure to the commonly aff ected sector, country, and/or currency (“participation approach”).3 In the case of the

1 In a progress report to the G20 (Financial Stability Board, International Monetary Fund, and Bank for International Settlements [FSB, IMF, and BIS], 2011a), which followed an earlier update on macro- prudential policies (FSB/IMF/BIS, 2011b), the FSB takes stock of the development of governance structures that facilitate the identifi cation and monitor-ing of systemic fi nancial risk as well as the designation and calibration of instruments for macroprudential purposes aimed at limiting sys-temic risk. Th e Committee on the Global Financial System (2012) pub-lished a report on operationalizing the selection and application of macroprudential policies, which provides guidance on the eff ectiveness and timing of banking sector– related instruments (aff ecting the treat-ment of capital, liquidity, and assets for the purposes of mitigating the cyclical impact of shocks and enhancing systemwide resilience to joint distress events). See Acharya, Cooley, and others (2010) as well as Acharya, Santos, and Yorulmazer (2010) for the implications of systemic risk in MPS in the U.S. context.

2 For a discussion of ways to assess the systemic importance of fi nancial institutions and markets, see IMF, FSB, and BIS (2009).

3 Drehmann and Tarashev (2011) refer to this as a “bottom- up approach,” whereas as a “top- down approach” would be predicated on the quantifi -cation of expected losses of the system, with and without a par tic u lar

536-57355_IMF_StressTestHBk_ch03_3P.indd 410 11/5/14 2:06 AM

Andreas A. Jobst and Dale F. Gray 411

Systemic CCA identifi es market- implied linkages aff ect-ing joint expected losses during times of stress, which can deliver important insights about the joint tail risk of multiple entities. A sample of fi rms (as proxy for an entire fi nancial system or parts thereof ) is viewed as a portfolio of individual expected losses (with individual risk pa ram e ters) whose sensi-tivity to common risk factors is accounted for by including the statistical dependence of their individual expected losses (“dependence structure”). Like other academic proposals, this approach helps assess individual fi rms’ contributions to systemic solvency risk (at diff erent levels of statistical con-fi dence). However, by accounting for the time- varying de-pendence structure, this method links the market- based assessment of each fi rm’s risk profi le with the risk characteris-tics of other fi rms that are subject to common changes in market conditions. Based on the expected losses arising from the variation of each individual fi rm’s expected losses, the joint probability of all fi rms experiencing distress simultane-ously can be estimated.

In addition, the Systemic CCA framework can generate closed- form solutions for market- implied estimates of capital adequacy under various stress test scenarios. By modeling how macroeconomic conditions and bank- specifi c income and loss elements (net interest income, fee income, trading income, operating expenses, and credit losses) have infl uenced the changes in market- implied expected losses (as mea sured by implicit put option values), it is possible to link a par tic u lar macroeconomic path to fi nancial sector per for mance in the future and derive estimates of joint capital needed to main-tain current capital adequacy. As a result, the market- implied joint capital need arises from the amount of expected losses relative to current (core) capital levels as well as its escalation

2011d).4 Th ere also are several studies on network analysis and agent- based models that are more closely related to the partici-pation approach by modeling how interlinked asset holdings matter in the generation and propagation of systemic risk (Al-len, Babus, and Carletti, 2010; Espinosa- Vega and Solé, 2011; Or ga ni za tion for Economic Cooperation and Development, 2012). Haldane and Nelson (2012) underscore this observa-tion by arguing that networks can produce nonlinearity and unpredictability with the attendant extreme (or fat- tailed) events.5

We propose a forward- looking, analytical, market data– based framework for estimating systemic risk in order to fi ll this gap in the literature. Th e suggested approach (“Systemic Contingent Claims Analysis” or “Systemic CCA”) extends the risk- adjusted (or economic) balance sheet approach to gener-ate estimates of the joint default risk of multiple institutions. Under this approach, the magnitude of systemic risk depends on the fi rms’ size and interconnectedness and is defi ned by the multivariate density of combined expected losses within a given system of fi nancial institutions.

4 A comparison of three mea sures of institution- level systemic risk exposure (Sedunov, 2012) suggests that CoVaR shows good forecasting power of the within- crisis per for mance of fi nancial institutions during two systemic crisis periods (Long- Term Capital Management in 1998 and Lehman Brothers in 2008). In contrast, Systemic Expected Shortfall (SES) is based on MES after considering diff erent degrees of fi rm leverage (Acharya, Ped-ersen, and others, 2012) and Granger causality does not seem to forecast the per for mance of fi rm per for mance reliably during crises.

5 One empirical example of the network literature is based on a Federal Reserve (Fed) data set, which allowed for the mapping of bilateral expo-sures of 22 global banks that accessed Fed emergency loans in the pe-riod 2008 to 2010 (Battiston and others, 2012). Th e authors fi nd that size is not a relevant factor to determine systemic importance.

TABLE 26.1

General Systemic Risk Mea sure ment ApproachesContribution approach (“Risk Agitation”) Participation approach (“Risk Amplifi cation”)

Concept Systemic resilience to individual failure Individual resilience to common shock

DescriptionA contribution to systemic risk conditional on

individual failure due to knock- on eff ectExpected loss from systemic event due to common

exposure and risk concentration

Risk transmission

“Institution- to- institution” “Institution- to- aggregate”Economic signifi cance of asset holdings (“size”) Claims on other fi nancial sector participants (credit

exposure)Intra- and intersystem liabilities (“connectedness”) Market risk exposure (interest rates, credit spreads,

currencies)

Risk indicators

Degree of transparency and resolvability (“complexity”)

Risk- bearing capacity (solvency and liquidity buff ers, leverage)

Participation in system- critical function/ser vice, e.g., payment and settlement system (“substitutability”)

Economic signifi cance of asset holdings, maturity mismatches debt pressure (“asset liquidation”)

Policy objectivesAvoid/mitigate contagion eff ect (by containing

systemic impact upon failure)Maintain overall functioning of system and maximize

survivorshipAvoid moral hazard Preserve mechanisms of collective burden sharing

Sources: Drehmann and Tarashev (2011); FSB, IMF, and BIS (2011a, 2011b); Jobst (2014); Tarashev, Borio, and Tsatsaronis (2009); and Weistroff er (2011).Note: The policy objectives and diff erent indicators to mea sure systemic risk under both contribution and participation approaches are not exclusive to each concept. Moreover, the availability of certain types of balance sheet information and/or market data underpinning the various risk indicators varies between diff erent groups of fi nancial institutions, which requires a certain degree of customization of the mea sure ment approach to the distinct charac-teristics of a par tic u lar group of fi nancial institutions.

536-57355_IMF_StressTestHBk_ch03_3P.indd 411 11/5/14 2:06 AM

Systemic Contingent Claims Analysis 412

TAB

LE 2

6.2

Sele

cted

Inst

itutio

n- Le

vel S

yste

mic

Ris

k M

odel

s

Des

crip

tio

nC

on

dit

ion

al V

alu

e at

Ris

k (C

oV

aR)

Co

nd

itio

nal

Ris

k (C

oR

isk)

SRIS

KSy

stem

ic E

xpec

ted

Sh

ort

fall

Dis

tres

s In

sura

nce

Pr

emiu

mJo

int P

rob

abili

ty o

f D

efau

ltSy

stem

ic C

on

tin

gen

t C

laim

s A

nal

ysis

Syst

emic

ris

k m

ea su

reVa

lue

at ri

skVa

lue

at ri

skEx

pec

ted

shor

tfal

lEx

pec

ted

sho

rtfa

llEx

pec

ted

sho

rtfa

llC

ond

itio

nal

pro

bab

iliti

esEx

pec

ted

shor

tfal

l

Co

nd

itio

nal

ity

Perc

enti

le o

f in

div

idua

l ret

urn

Perc

enti

le o

f joi

nt

def

ault

risk

Thre

shol

d o

f cap

ital

ad

equa

cyTh

resh

old

of c

apit

al

adeq

uacy

Perc

enta

ge

thre

shol

d

of s

yste

m re

turn

Vari

ous

(ind

ivid

ual o

r jo

int e

xpec

ted

loss

es)

Vari

ous

(ind

ivid

ual o

r jo

int e

xpec

ted

loss

es)

Dim

ensi

on

alit

yM

ulti

vari

ate

Biva

riat

eBi

vari

ate

Biva

riat

eBi

vari

ate

Mul

tiva

riat

eM

ulti

vari

ate

Dep

end

ence

m

ea su

reLi

near

, par

amet

ric

Line

ar, p

aram

etri

cPa

ram

etri

cEm

pir

ical

Para

met

ric

Non

linea

r, no

npar

amet

ric

Non

linea

r, no

npar

amet

ric

Met

ho

dPa

nel

qua

ntile

re

gre

ssio

nBi

vari

ate

qua

ntile

re

gre

ssio

nD

ynam

ic c

ond

itio

nal

corr

elat

ion

(DCC

G

ARC

H) a

nd

Mon

te

Car

lo s

imul

atio

n

Emp

iric

al s

amp

ling

and

scal

ing;

G

auss

ian

and

pow

er la

w

Dyn

amic

con

dit

iona

l co

rrel

atio

n (D

CC

GA

RCH

) an

d M

onte

C

arlo

sim

ulat

ion

Emp

iric

al c

opul

aEm

pir

ical

cop

ula

Dat

a so

urc

eEq

uity

pri

ces

and

bal

ance

she

et

info

rmat

ion

CD

S sp

read

sEq

uity

pri

ces

and

b

alan

ce s

heet

in

form

atio

n

Equi

ty p

rice

s an

d b

alan

ce s

heet

in

form

atio

n

Equi

ty p

rice

s an

d C

DS

spre

ads

CD

S sp

read

sEq

uity

pri

ces

and

b

alan

ce s

heet

in

form

atio

nD

ata

inp

ut

Qua

si- a

sset

retu

rns

CD

S- im

plie

d d

efau

lt

pro

bab

iliti

esQ

uasi

- ass

et re

turn

sQ

uasi

- ass

et re

turn

sEq

uity

retu

rns

and

CD

S- im

plie

d d

efau

lt

pro

bab

iliti

es

CD

S- im

plie

d d

efau

lt

pro

bab

iliti

esEx

pec

ted

loss

es

(“im

plic

it p

ut o

pti

on”)

Ref

eren

ceA

dri

an a

nd

Brun

nerm

eier

(2

008)

Cha

n- L

au (2

010)

Brow

nlee

s an

d En

gle

(201

1)A

char

ya, P

eder

sen,

an

d ot

hers

(200

9,

2010

, an

d 20

12)

Hua

ng, Z

hou,

an

d Z

hu

(200

9, 2

010)

Seg

ovia

no a

nd

Go

od

hart

(200

9)G

ray

and

Job

st (2

010;

an

d 20

11b)

Sour

ce: A

utho

rs.

536-57355_IMF_StressTestHBk_ch03_3P.indd 412 11/5/14 2:06 AM

Andreas A. Jobst and Dale F. Gray 413

variate distribution that formally captures the potential of extreme realizations of joint expected losses as a conditional tail expectation (CTE) as a result of systemwide eff ects on solvency conditions.

Th e model comprises two sequential estimation steps in order to mea sure joint market- implied expected losses. First, each fi rm’s expected losses (and associated change in existing capital levels) are estimated using an enhanced form of CCA, which has been applied widely to mea sure and evaluate credit risk at fi nancial institutions.8 Second, these expected losses are assumed to follow a generalized extreme value (GEV) dis-tribution, which are combined with a multivariate solution by utilizing a novel application of a nonparametric dependence mea sure in order to derive the amount of joint expected losses (and changes in corresponding capital levels).

In order to understand individual risk exposures, fi rst, CCA is applied to construct risk- adjusted (economic) balance sheets of fi nancial institutions and estimate their expected losses. In its basic concept, CCA quantifi es default risk on the assumption that own ers of corporate equity in leveraged fi rms hold a call option on the fi rm value after outstanding liabilities have been paid off . Th e pricing of these state- contingent contracts is predicated on the risk- adjusted valu-ation of the balance sheet of fi rms whose assets are stochastic and may be above or below promised payments on debt over a specifi ed period of time. When there is a chance of default, the repayment of debt is considered “risky”— to the extent that it is not guaranteed in the event of default— and thus generates expected losses conditional on the probability and the degree to which the future asset value could drop below the contemporaneous debt payment. Higher uncertainty about changes in future asset value, relative to the default barrier, increases default risk, which occurs when assets de-cline below the barrier. Th us, the expected loss from default can be valued as an implicit put option.

Th us, the marginal distributions of individual expected losses are combined then with their time- varying dependence structure to generate the multivariate distribution of joint ex-pected losses of all sample fi rms. Th is approach of analyzing extreme linkages of multiple entities links the univariate marginal distributions in a way that formally captures both linear and nonlinear dependence and its impact on joint tail risk behavior over time. Given that the simple summation of implicit put option values would presuppose perfect correla-tion, that is, a coincidence of defaults, the correct estimation of aggregate risk requires knowledge about the dependence structure of individual balance sheets and associated expected

8 Th e CCA is a generalization of option pricing theory pioneered by Black and Scholes (1973) and Merton (1973, 1974). It is based on three principles that are applied in this chapter: (1) the values of liabilities are derived from assets; (2) assets follow a stochastic pro cess; and (3) liabili-ties have diff erent priorities (se nior and ju nior claims). Equity can be modeled as an implicit call option, while risky debt can be modeled as the default- free value of debt less an implicit put option that captures expected losses. In the Systemic CCA model, advance option pricing is applied to account for biases in the Black- Scholes- Merton specifi cation.

during extreme market stresses at a very high statistical con-fi dence level (expressed as “tail risk”).6

Because its mea sure of systemic risk is derived from the joint distribution of individual risk profi les, Systemic CCA addresses the general identifi cation problem of existing ap-proaches. It does not rely on stylized assumptions aff ecting asset valuation, such as linearity and normally distributed pre-diction errors, and it generates point estimates of systemic risk without the need of reestimation for diff erent levels of desired statistical confi dence. None of the recently published systemic risk models, such as Adrian and Brunnermeier (2008), Acha-rya, Pedersen, and others (2009, 2010, 2012), and Huang, Zhou, and Zhu (2009, 2010), apply multivariate density esti-mation, which allows the determination of the marginal contribution of an individual institution to concurrent changes of both the severity of systemic risk and the dependence struc-ture across any combination of sample institutions for any level of statistical confi dence.

Th e chapter is structured as follows: Section 1 explains the general concept of the Systemic CCA framework and provides a detailed description of how joint default risk is modeled via a portfolio- based approach using CCA. Section 2 introduces various extensions to the Systemic CCA framework, includ-ing the estimation of contingent claims to the fi nancial sector and the assessment of capital adequacy using market- implied mea sures of systemwide solvency in the context of macro- prudential stress testing. Section 3 presents the estimation results of the Systemic CCA framework for the U.K. banking sector from the IMF’s 2011 Financial Sector Assessment Pro-gram (FSAP). Th e chapter concludes with possible extensions to the presented methodology (and its scope of application) and provides some caveats on systemic risk mea sure ment.

1. METHODOLOGY

A. Overview

Systemic CCA models joint solvency risk by combining the multivariate extension to CCA with the concept of extreme value theory (EVT).7 Th e magnitude of systemic risk jointly posed by multiple fi rms falling into distress is modeled as a portfolio of individual expected losses (with individual risk pa ram e ters) calculated from equity market and balance sheet information. More specifi cally, these expected losses and the dependence between them are combined to generate a multi-

6 See also Gray and Jobst (2011a, 2011b, 2011c) for a more general applica-tion of this approach to the integrated balance sheets of an entire econ-omy. For fi rst versions of the model, see Gray and Jobst (2009a, 2009b, 2010); Gray and Malone (2010); as well as González- Hermosillo and others (2009). An application of the Systemic CCA approach in the con-text of Financial Sector Assessment Program stress tests and spillover analysis are published in IMF (2010, 2011a, 2011c, 2011d, 2011e, 2011f, 2012a, 2012b). For an earlier application of the methodology underpin-ning this framework, see also IMF (2009a, 2009b).

7 EVT is a useful statistical concept to study the tail behavior of heavily skewed data, which specifi es residual risk at high percentile levels through a generalized parametric estimation of order statistics.

536-57355_IMF_StressTestHBk_ch03_3P.indd 413 11/5/14 2:06 AM

Systemic Contingent Claims Analysis 414

able cash fl ows from operations and asset sales) falls below the amount of required funding to satisfy debt payment obligations— is assessed not only for indi-vidual institutions but for all fi rms within a system in order to generate estimates of systemic risk.

B. Model specifi cation and estimation steps

Th e Systemic CCA framework follows a two- step estimation pro cess. First, the changes to default risk causing a bank to fail (i.e., future debt payments exceeding the asset value of the fi rm) are modeled as a put option in order to estimate the market- implied expected losses over a certain time horizon (consistent with the application of CCA). Second, these indi-vidually estimated expected losses are combined into a multi-variate distribution that determines the probabilistic mea sure of joint expected losses at a systemwide level for a certain level of statistical confi dence. Finally, the sensitivity of systemic sol-vency risk to changes in individual default risk of a single fi rm (and its implications for the dependence structure of expected losses across all fi rms) quantifi es the degree to which a par tic-u lar fi rm contributes to total default risk.

Calculating Expected Losses from CCA Using Option Pricing

CCA is a generalization of the option pricing theory pioneered by Black and Scholes (1973) as well as by Merton (1973, 1974) to the corporate capital structure context. When applied to the analysis and mea sure ment of credit risk, it is commonly called the Black- Scholes- Merton (BSoM) model.11 In its basic concept, it quantifi es default risk on the assumption that own ers of equity in leveraged fi rms hold a call option on the fi rm value after outstanding liabilities have been paid off . Th e concept of a risk- adjusted balance sheet is instrumental in understanding default risk. Th e total market value of fi rm assets, A, at any time, t, is equal to the sum of its equity mar-ket value, E, and its risky debt, D, maturing at time T. Th e asset value follows a random, continuous pro cess and may fall below the bankruptcy level (“default threshold” or “distress barrier”), which is defi ned as the present value of promised payments on risky debt B, discounted at the risk- free rate. Th e variability of the future asset value relative to promised debt payments is the driver of credit and default risk. Default happens when assets are insuffi cient to meet the amount of debt owed to creditors at maturity. Th us, the market- implied

11 Th e Merton approach assumes that the fi rm’s debt consists of a zero- coupon bond B with a notional value F and a maturity term of T peri-ods. Th e fi rm’s outstanding liabilities constitute the bankruptcy level, whose standard normal density defi nes the “distance to default” relative to the fi rm value. Th is capital structure– based evaluation of contingent claims on fi rm per for mance implies that a fi rm defaults if its asset value is insuffi cient to meet the amount of debt owed to bondholders at matu-rity. Conversely, if the distance to default is positive, and the asset value of the fi rm exceeds the bankruptcy level, the call option held by equity holders on fi rm value has intrinsic value (in addition to its time value until the maturity of debt).

losses. Th e expected losses of each fi rm are assumed to be “fat- tailed” and fall within the domain of the GEV distribu-tion, which identifi es asymptotic tail behavior of normalized extremes.9 Th e joint distribution is estimated iteratively over a prespecifi ed time window with the frequency of updating determined by the periodicity of available data. Th e specifi ca-tion of a closed- form solution can then be used to (1) deter-mine point estimates of joint expected losses as a multivariate CTE and (2) quantify the contribution of specifi c institu-tions to the dynamics of systemic risk.

Systemic CCA accounts for changes in fi rm- specifi c and common factors determining individual default risk, their implications for the market- implied linkages between fi rms, and the resulting impact on the overall assessment of systemic risk. Th us, it accomplishes the essential goal of mea sur ing the extent to which an institution contributes to systemic risk (in keeping with the contribution approach as shown in Table 26.1).10 Th e systemic dimension of the model is captured by three properties:

1. Drawing on the market’s evaluation of a fi rm’s risk profi le. Given that the framework combines market prices and balance sheet information to inform a risk- adjusted mea sure of individual default risk, the evaluation of solvency conditions is inherently linked to investor perception as implied by the institution’s equity and equity options (which determine the im-plied asset value of the fi rm conditional on its lever-age and debt level).

2. Controlling for common factors aff ecting the fi rm’s sol-vency. Th e implied asset value of a fi rm (which un-derpins the estimation of implied expected losses) is modeled as being sensitive to the same markets as the implied asset value of every other institution but by varying degrees because of a par tic u lar capital struc-ture (and its implications for the market’s perception). Changes in market conditions (and their impact on the perceived risk profi le of each fi rm via its equity price and volatility) establish market- induced linkages among sample fi rms. Th us, mea sur ing the joint ex-pected losses via option prices links institutions im-plicitly to the markets in which they obtain equity capital and funding.

3. Quantifying the chance of simultaneous default via joint probability distributions. Th e probability that multiple fi rms experience a realization of expected losses simul-taneously is made explicit by computing their joint probability distributions (which also account for dif-ferences in the magnitude of individual expected losses). Hence, the default risk— that is, the likeli-hood that the implied asset value (including avail-

9 Th e choice of the empirical distribution function of the underlying data to model the marginal distributions avoids problems associated with us-ing specifi c pa ram e ters that may or may not fi t these distributions well (Gray and Jobst, 2009a, 2009b).

10 See also Tarashev, Borio, and Tsatsaronis (2009).

536-57355_IMF_StressTestHBk_ch03_3P.indd 414 11/5/14 2:06 AM

Andreas A. Jobst and Dale F. Gray 415

First, the amount of expected loss is modeled as a put option based on the individual risk- adjusted balance sheet. Th e expected loss can be quantifi ed then by viewing de-fault risk as if it were a put option written on the amount of outstanding liabilities, where the present value of debt (i.e., the default barrier) represents the “strike price,” with the value and volatility of assets determined by changes in the equity and equity option prices of the fi rm. Th e value of the put option increases the higher the probability of the implied asset value falls below the default barrier over a predefi ned horizon. Such probability is infl uenced by changes in the level and the volatility of their implied asset value refl ected in the institution’s equity and equity option prices conditional on its capital structure. Th us, the present value of market- implied expected losses associated with out-standing liabilities in keeping with the traditional BSM model can be valued as an implicit (Eu ro pe an) put option value:

PE (t ) = Be r (T t ) d A T t( )( ) A(t ) ( d), (26.1)

with the present value of debt B as strike price on the asset value A(t) and asset return volatility:

A =E(t ) E

A(t ) (d)= 1

Be r (T t ) d A T t( )A(t ) (d) E , (26.2)

over time horizon T t, where E is the (observable) equity volatility, E(t) is the equity price, r is the risk- free discount rate, and (d) is the cumulative probability of the standard normal density function of the leverage:

d = lnA(t )B

+ r + A2

2(T t ) A T t , (26.3)

changes in A(t) relative to outstanding debt claims. Th is spec-ifi cation of option price- based expected losses, however, does not incorporate skewness, kurtosis, and stochastic volatility, which can account for implied volatility smiles of equity prices. Th ese shortcomings of the conventional Merton model can be addressed with more advanced valuation models, such as the Gram- Charlier expansion of the density function of asset changes (Backus, Foresi, and Wu, 2004) or a jump diff usion pro cess of asset value changes in order to achieve

expected losses associated with outstanding liabilities can be valued as an implicit put option (and its cost refl ected in a credit spread above the risk- free rate that compensates inves-tors for holding risky debt). Th e put option value is infl uenced by the duration of the total debt claim, the leverage of the fi rm, and the volatility of its asset value.

In the traditional defi nition of bank balance sheets, a change in accounting assets entails a one- for- one change in book equity. Assets comprise cash and cash equivalents, invest-ments, loans, mortgages, and other cash claims on counter-parties as well as noncash claims (derivatives and contingent assets), and liabilities consist of book equity and book value of debt and deposits. When assets change, the full change aff ects book equity (see Table 26.3). In the conventional defi nition of credit risk, the concept of “expected losses” re-fers to impairments arising from exposures on the asset side of the bank’s balance sheet. In this context, expected loss is calculated as the probability of default (PD) times a loss- given- default (LGD) times the exposure at default. Th e ex-pected losses of diff erent exposures are aggregated (using certain assumptions regarding correlation, etc.) and used as an input into loss distribution calculations, which are in turn used for the estimation of risk- weighted assets (RWAs) and the assessment of regulatory capital adequacy.

CCA constructs a risk- adjusted (economic) balance sheet by transforming accounting identities into exposures so that changes in the value of assets are linked directly to changes in the market value of equity and expected losses in an inte-grated framework. A decline in the value of assets increases expected losses to creditors and leads to less than one- to- one decline in the market value of equity; the amount of change in equity depends on the severity of fi nancial distress (i.e., the perceived impact of anticipated operating— or accounting— losses on equity returns), the degree of leverage, and the volatility of asset returns over time. Th e underlying “expo-sure” is represented by the default- free value of the bank’s total debt and deposits after accounting for the (now) higher probability of assets creating insuffi cient cash fl ows to meet debt payments (without compromising the integrity of the deposit base) (see Table 26.4). Th us, the integrated modeling of default risk via CCA can quantify the impact on bank borrowing costs of higher (or lower) levels of equity and the market- implied capital assessment. A lower market value of equity would increase the probability of a bank to generate capital losses, which is directly related to higher funding costs.

TABLE 26.3

Traditional Accounting Bank Balance SheetAssets Liabilities

Accounting assets Debt and deposits(i.e., cash, reserves, loans, credits, and other

exposures)Book equity

Source: Authors.

TABLE 26.4

Risk- Adjusted (CCA) Bank Balance SheetAssets Liabilities

(Implied) market value of assets (A) “Risky” debt (D)(i.e., cash, reserves, and implied

market value of “risky” assets)(= default- free value of

debt and deposits minus expected losses to bank creditors)

(Observable) market value of equity (E)

(= market capitalization)

Source: Authors.Note: CCA = contingent claims analysis.

536-57355_IMF_StressTestHBk_ch03_3P.indd 415 11/5/14 2:06 AM

Systemic Contingent Claims Analysis 416

sets and asset volatility, and assumptions about the default barrier) could fail to capture some relevant economics that are needed to fully understand default risk and thus could generate biased estimators of expected losses. Moreover, eq-uity prices might not only refl ect fundamental values be-cause of both shareholder dilution and trading behavior that obfuscate proper economic interpretation.16

Estimating the Joint Expected Losses from Default Risk

Second, the individually estimated expected losses are com-bined to determine the magnitude of default risk on a sys-temwide level. Th e distribution of expected losses is assumed to be “fat- tailed” in keeping with EVT. Th is specifi cation of individual loss estimates then informs the estimation of the dependence function. As part of a three- step subpro cess, we defi ne the univariate marginal density functions of all fi rms, which are then combined with their dependence function in order to generate an aggregate mea sure of default risk. Th is multivariate setup underpinning the Systemic CCA frame-work formally captures the realizations of joint expected losses. We can then use tail risk estimates, such as the conditional VaR (or expected shortfall, or ES), in order to gauge systemic solvency risk in times of stress.

1. Estimating the Marginal Distributions of Individual Expected Losses. We fi rst specify the statistical distribution of individual expected losses (based on the series of put op-tion values obtained for each fi rm) in accordance with EVT. Th is is a general statistical concept of deriving a limit law for sample maxima. Let the vector- valued series

Xmn = PE,1

i (t ),…,PE,mn (t ) (26.4)

denote in de pen dent, identically distributed random observa-tions of expected losses (i.e., a total of n- number of daily put option values PE,m

i (t ) up to time t), each estimated according to equation (26.1) over a rolling window of observations with periodic updating (e.g., a daily sliding window of 120 days) for j m fi rms in the sample. Th e individual asymptotic tail behavior is modeled in accordance with the Fisher- Tippett- Gnedenko theorem (Fisher and Tippett, 1928; Gnedenko, 1943), which defi nes the attribution of a given distribution of normalized maxima (or minima) to be of extremal type (as-suming that the underlying function is continuous on a closed interval). Given

Xn = max PE, j1 (t ),…,PE, j

n (t )( ), (26.5)

there exists a choice of normalizing constants n > 0 and n, such that the probability of each ordered n- sequence of nor-malized sample maxima (Xn– n)/ n converges to the nonde-generate limit distribution H(x) as n and x , so that

16 For instance, during the fi nancial crisis, rapid declines in market capital-ization of fi rms were not only a signal about future solvency risk but also refl ected a “fl ight to quality” motive that was largely unrelated to expec-tations about future fi rm earnings or profi tability.

more robust and reliable estimation results.12 Some of these approaches have been applied in the empirical use of the Sys-temic CCA framework in this chapter.13

Given that the asset value is infl uenced by the empirical irregularities contained in the Merton model (which also af-fects the model- based calibration of implied asset volatility), it is estimated directly from observable equity option prices.14 Th e state- price density (SPD) of the implied asset value is estimated from the risk- neutral probability distribution of the underlying asset price at the maturity date of equity op-tions with diff erent strike prices, without any assumptions on the underlying asset diff usion pro cess (which is assumed to be log- normal in the Merton model). Th e implied asset value is defi ned as the expectation over the empirical SPD by adapting the well- established Breeden and Litzenberger (1978) method, together with a semiparametric specifi cation of the Black- Scholes option pricing formula (Aït- Sahalia and Lo, 1998). More specifi cally, this approach uses the second derivative of the call pricing function (on Eu ro pe an options) with respect to the strike price (rather than option price). Estimates are based on option contracts with identical time to maturity, assuming a continuum of strike prices.15 Th e SPD of the equity price includes the risk- neutral expectation of the implied asset value and removes the impact of diff er-ences of higher moments of both the equity price and the implied asset value dynamics over the chosen time horizon. Th us, the current implied asset value can be transposed from the SPD of the equity price conditional on the contempora-neous leverage of the fi rm.

Note, however, that the presented valuation model is sub-ject to varying degrees of estimation uncertainty and paramet-ric assumptions. Th e option pricing model (given its specifi c distributional assumptions, the derivation of both implied as-

12 Th e suggested approach takes into account the nonlinear characteristics of asset price changes, which deviate from normality and are frequently infl uenced by stochastic volatility. Th e BSM model has been shown to consistently understate spreads ( Jones, Mason, and Rosenfeld, 1984; Ogden, 1987), with more recent studies pointing to considerable pric-ing errors because of its simplistic nature.

13 Other extensions are aimed at imposing more realistic assumptions, such as the introduction of stationary leverage ratios (Collin- Dufresne and Goldstein, 2001) and stochastic interest rates (Longstaff and Schwartz, 1995). Incorporating early default (Black and Cox, 1976) does not repre-sent a useful extension in this context given the short estimation and forecasting time window.

14 Given that the implied asset value is derived separately, this approach avoids the (problematic) “two- equations- two- unknowns” approach to de-rive implied assets and asset volatility based on Jones, Mason, and Rosen-feld (1984), which was subsequently extended by Ronn and Verma (1986) to a single equation to solve two simultaneous equations for asset value and volatility as two unknowns. Duan (1994) shows that the volatility relation between implied assets and equity could become redundant if the equity volatility is stochastic. An alternative estimation technique for asset volatility introduces a maximum likelihood approach (Erics-son and Reneby, 2004, 2005).

15 Because available strike prices always are discretely spaced on a fi nite range around the actual asset value, interpolation of the call pricing function inside this range and extrapolation outside this range are per-formed by means nonparametric (local polynomial) regression of the implied volatility surface (Rookley, 1997).

536-57355_IMF_StressTestHBk_ch03_3P.indd 416 11/5/14 2:06 AM

Andreas A. Jobst and Dale F. Gray 417

case and adjusting the margins according to Hall and Taj-vidi (2000) so that

( )=min 1, max n j=1m yi, j y

i j

ji=1

n1

, , 1 , (26.10)

where yi j = yi , j ni=1

n refl ects the average marginal density of all i n put option values and 0 max ( 1,…, m−1)

( j ) 1 for all 0 j 1.19 (i) represents a convex func-tion on [0,1] with (0) = (1) = 1, that is, the upper and lower limits of (i) are obtained under complete dependence and mutual in de pen dence, respectively. It is estimated iteratively (over a rolling window of observations with periodic up-dating at a frequency that is consistent with that in equation (26.5), subject to the optimization of the (m 1)-dimensional unit simplex:

Sm = ( 1,…, m 1) +

m: j 0,1 j m 1;

j 1 and m = 1 jj=1

m 1

j=1

m 1

, (26.11)

which establishes the degree of coincidence of multiple series of cross- classifi ed random variables similar to a chi- statistic that mea sures the statistical likelihood that observed values diff er from their expected distribution. Th is specifi cation stands in contrast to a general copula function that links the marginal distributions using only a single (and time- invariant) dependence pa ram e ter.

3. Estimating the Joint Distribution and a Tail Risk Mea-sure of Joint Expected Losses. We then combine the mar-ginal distributions of these individual expected losses with their dependence structure to generate a multivariate ex-treme value distribution over the same estimation period as earlier.20 Th e resultant cumulative distribution function is specifi ed as

Gt,m(x ) = exp yt, jj=1

m

t ( ) , (26.12)

19 Note that the marginal density of a given extreme relative to the average marginal density of all extremes is minimized (“ ”) across all fi rms j m, subject to the choice of factor j. A bivariate version of this ap-proach has been implemented in Jobst and Kamil (2008).

20 Th e analysis of dependence in this presented approach is completed separately from the analysis of marginal distributions and thus diff ers from the classical approach, where multivariate analysis is performed jointly for marginal distributions and their dependence structure by considering the complete variance– covariance matrix, using techniques like the Multivariate Generalized AutoRegressive Conditional Hetero-skedasticity approach. To obtain a multivariate distribution function, the dependence function combines several marginal distribution func-tions in accordance with Sklar’s (1959) theorem on constructing joint distributions with arbitrary marginal distributions via copula functions (which completely describes the dependence structure and contains all the information to link the marginal distributions). For the formal treatment of copulas and their properties, see Hutchinson and Lai (1990); Dall’Aglio, Kotz, and Salinetti (1991); and Joe (1997).

Fnnx+ n

(x ) = limn

PrXn n

ny

= F( ny + n )[ ]n H(x ) (26.6)

falls within the maximum domain of attraction (MDA) of the GEV as limiting distribution of maxima of dependent random variables (Coles, Heff ernan, and Tawn, 1999; Poon, Rockinger, and Tawn, 2003; Jobst, 2007) with the cumula-tive distribution function

H , , (x )=exp 1+ (x )

1/

if 1+ (x )0

exp expx

if x , = 0

(26.7)

and diff erencing equation (26.7) above as H , , (x) =ddx

H , , (x) yields the probability density function,

h , , (x ) =1

1+(x )

( 1/ ) 1

exp 1+(x )

+

1/

. (26.8)

Th us, the jth univariate marginal density function of each expected loss series converging to GEV in the limit is de-fi ned as

y j (x ) = 1+ ˆj

(x ˆ j )ˆ j

+

1/ j

(for j = 1,…, m) (26.9)

where 1 + j (x j)/ j > 0, scale pa ram e ter j > 0, location pa-ram e ter j , and shape pa ram e ter i 0.17 Th ese moments are estimated concurrently by means of numerical iteration via maximum likelihood (ML), which identifi es possible limiting laws of asymptotic tail behavior, that is, the likeli-hood of even larger extremes as the level of statistical confi -dence approaches certainty. Th e ML estimator in the GEV model is evaluated numerically by using an iteration proce-dure (e.g., over a rolling window of observations with peri-odic updating) to maximize the likelihood h , , (x | )i=1

n over all three pa ram e ters = ( , , ) simultaneously, where the linear combinations of ratios of spacings estimator serves as an initial value ( Jobst, 2014).18

2. Estimating the Dependence Structure of Individual Expected Losses. Second, we defi ne a nonparametric, multi-variate dependence function between the marginal distribu-tions of expected losses by expanding the bivariate logistic method proposed by Pickands (1981) to the multivariate

17 Th e upper tails of most (conventional) limit distributions (weakly) con-verge to this parametric specifi cation of asymptotic behavior, irrespec-tive of the original distribution of observed maxima (unlike parametric VaR models).

18 Note that the ML estimator fails for 1 since the likelihood function does not have a global maximum in this case. However, a local maximum close to the initial value can be attained.

536-57355_IMF_StressTestHBk_ch03_3P.indd 417 11/5/14 2:06 AM

Systemic Contingent Claims Analysis 418

where the relative weight of institution j is defi ned as the marginal contribution,

,m, a =

2Gt, ,m1 (a)

yt, j t ( )

s.t. , j, aj

m

=1 and , j, a z , j z ,m ,

(26.19)

attributable to the joint eff ect of both the marginal density and the change of the dependence function owing to the presence of institution j m in the sample.

2. EXTENSIONS OF THE SYSTEMIC CCA FRAMEWORK

A. Integrated market- implied capital assessment using CCA and Systemic CCA

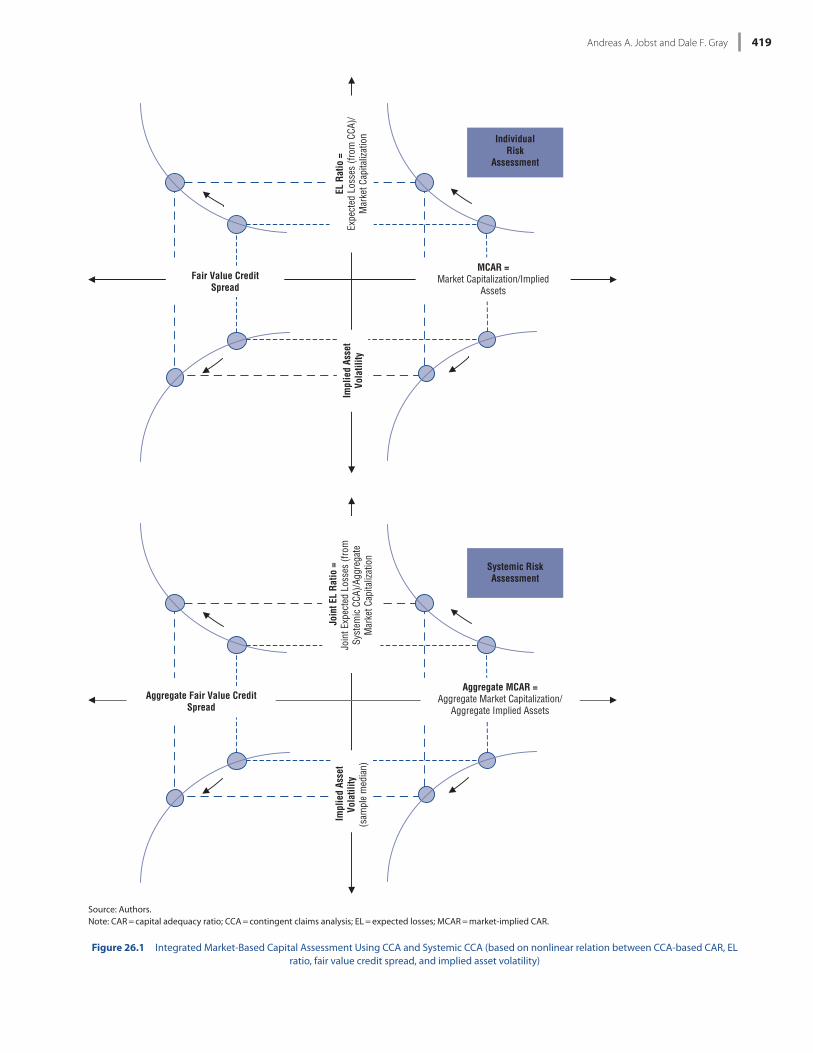

Given that the evaluation of default risk is inherently linked to perceived riskiness as implied by the changes in equity and equity option prices, the risk- adjusted (economic) balance sheet approach— and its multivariate extension in the form of Systemic CCA— provides an integrated analytical frame-work for a market- based assessment of individual and sys-temwide solvency. Higher expected losses to creditors lead to less than a one- to- one decline in the market value of equity, depending on the severity of the perceived (and actual) de-cline in the value of assets, the degree of leverage, and the vola-tility of assets. Th us, the interaction between these constituent elements of the risk- adjusted (economic) balance sheet gives rise to a market- based capital assessment, which links changes in the value of assets directly to the market value of equity.

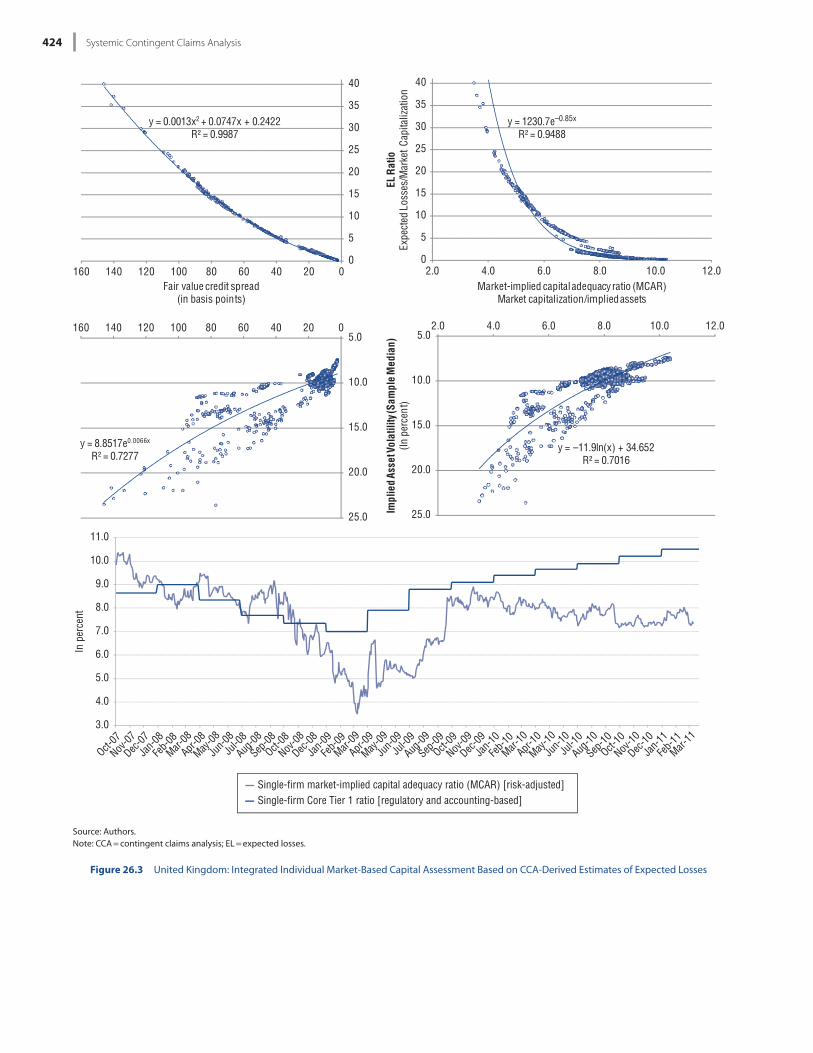

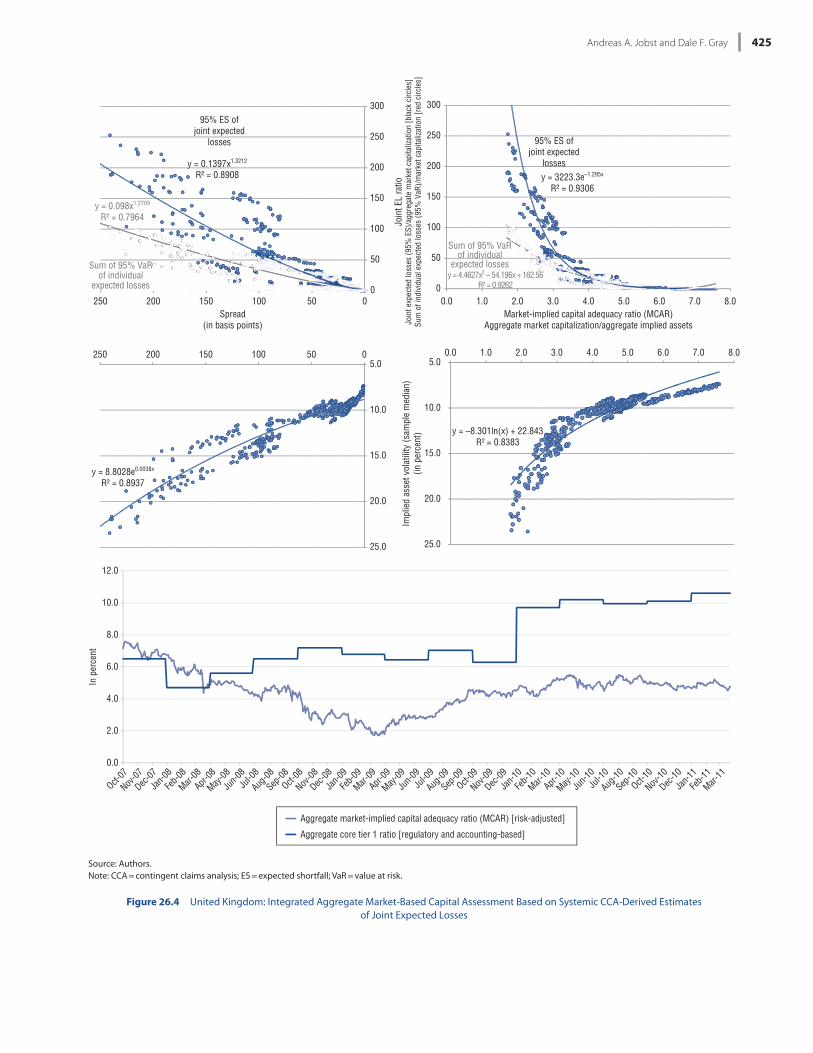

As opposed to the regulatory defi nition of capitalization (based on the discrete nature of accounting identities), the CCA- based capital assessment hinges on the historical dynam-ics of implied asset values and their eff ect on the magnitude of expected losses. Two broad indicators serve to illustrate this point: (1) the market- implied capital adequacy ratio (MCAR), which is defi ned as the ratio between the amount of market capitalization divided by the implied asset value of a fi rm; and (2) the expected loss ratio (“EL ratio”) between individual expected losses (at a defi ned percentile of statistical confi -dence) and the amount of market capitalization (see Figure 26.1, fi rst panel). Both ratios also can be generated on a sys-temwide basis, with inputs defi ned as sample aggregates of input variables to the multivariate specifi cation of the Sys-temic CCA. In this case, the EL ratio is defi ned by magnitude of joint expected losses (at the 95th percentile, for instance) relative to aggregate market capitalization of all sample fi rms (see Figure 26.1, second panel).

Th e market- implied capital assessment also can help iden-tify a capital shortfall. Th e MCAR represents an important analogue to the regulatory defi nition of capital adequacy, which refl ects the market’s perception of solvency (based on the implied value of assets relative to the prevailing default risk) and is completely removed from prudential determi-nants of default risk aff ecting a bank’s capital assessment,

with corresponding probability density function

(26.13)

at time t = + 1 by maximizing the likelihood gt,m(x | )j =1m

over all three pa ram e ters = ( , , ) simultaneously so that the ML estimate of the true values 0 is

ˆMLE = arg maxˆ( | x ) 0 . (26.14)

Finally, we obtain the joint ES (or conditional VaR) as a mea sure of CTE. ES defi nes the probability- weighted residual density (i.e., the average aggregate expected losses) beyond a prespecifi ed statistical confi dence level (“severity threshold”) over a given estimation time period. Given the dependence structure defi ned in equation (26.10), we can calculate ES in a multivariate context as

ESt, ,m, a = E z | z Gt, ,m1 (a) = VaRt, a , (26.15)

where G 1(a) is the quantile corresponding to probability 0 < a < 1 (say, a = 0.95), z and G 1(a) = G (a) with G (a)

inf (x|G(x a)) so that

VaRt, a = sup Gt, ,m1 (a) |Pr[z > Gt, ,m

1 (a)] a = 0.95{ }, (26.16)

with the point estimate of joint potential losses of m fi rms at time t defi ned as

Gt, ,m1 (a)= ˆ t,m + ˆ t,m / ˆ

t,m

ln(a)

t ( )

ˆt,m

1 . (26.17)

Th e contribution of each fi rm can be determined by calcu-lating the cross- partial derivative of the joint distribution of expected losses. Th e joint ES also can be written as a linear combination of individual ES values, ESt, , j,a, where the rela-tive weights , m, a (in the weighted sum) are given by the second order cross- partial derivative of the inverse of the joint probability density function Gt, ,m

1 (i) to changes in both the dependence function t (i) and the individual marginal severity yi, j of expected losses. Th us, the contribution can be derived as the partial derivative of the multivariate density to changes in the relative weight of the univariate marginal distri-bution of expected losses and its impact on the dependence function (of all expected losses of sample fi rms) at the specifi ed percentile. By rewriting ESt, ,m,a, in equation (26.15), we ob-tain the following:

ESt, ,m, a = ,m, aj

m

E z , j | z ,m Gt, ,m1 (a)=VaRt, a , (26.18)

21 ES is an improvement over VaR, which, in addition to being a pure fre-quency mea sure, is “incoherent,” that is, it violates several axioms of monotonicity, subadditivity, positive homogeneity, and translation in-variance found in coherent risk mea sures. For the application of this kind of coherent risk mea sure, we refer to Artzner and others (1999) as well as Wirch and Hardy (1999).

exp yt , jj=1

m

t ( ) ,

gt ,m(x )= 1ˆ t ,m

yt , jj=1

m

t ( )

1

536-57355_IMF_StressTestHBk_ch03_3P.indd 418 11/5/14 2:06 AM

Andreas A. Jobst and Dale F. Gray 419

MCAR =Market Capitalization/Implied

AssetsFair Value Credit

Spread

EL R

atio

=Ex

pect

ed L

osse

s (fr

om C

CA)/

Mar

ket C

apita

lizat

ion

Impl

ied

Asse

tVo

latil

ity

IndividualRisk

Assessment

Source: Authors.Note: CAR = capital adequacy ratio; CCA = contingent claims analysis; EL = expected losses; MCAR = market- implied CAR.

Figure 26.1 Integrated Market- Based Capital Assessment Using CCA and Systemic CCA (based on nonlinear relation between CCA- based CAR, EL ratio, fair value credit spread, and implied asset volatility)

Systemic RiskAssessment

Aggregate MCAR =Aggregate Market Capitalization/

Aggregate Implied Assets

Joi

nt E

L Ra

tio =

Join

t Exp

ecte

d Lo

sses

(fro

mSy

stem

ic C

CA)/A

ggre

gate

Mar

ket C

apita

lizat

ion

Impl

ied

Asse

tVo

latil

ity(s

ampl

e m

edia

n)

Aggregate Fair Value CreditSpread

536-57355_IMF_StressTestHBk_ch03_3P.indd 419 11/5/14 2:06 AM

Systemic Contingent Claims Analysis 420

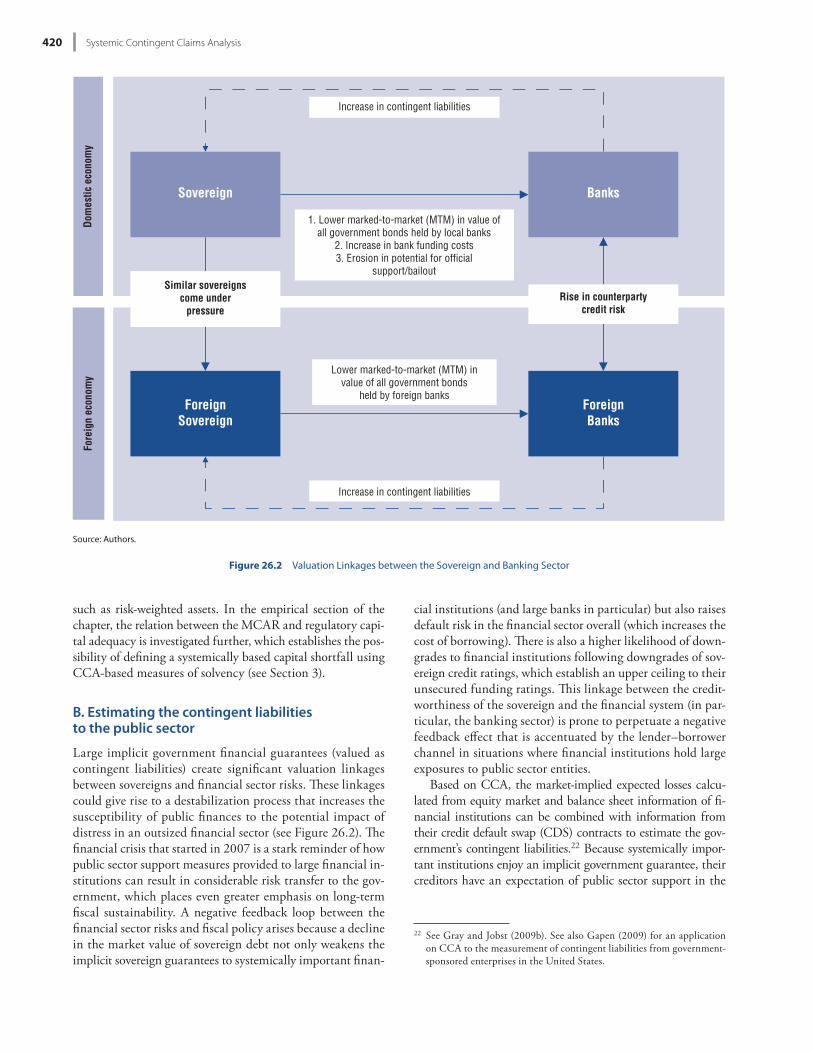

cial institutions (and large banks in par tic u lar) but also raises default risk in the fi nancial sector overall (which increases the cost of borrowing). Th ere is also a higher likelihood of down-grades to fi nancial institutions following downgrades of sov-ereign credit ratings, which establish an upper ceiling to their unsecured funding ratings. Th is linkage between the credit-worthiness of the sovereign and the fi nancial system (in par-tic u lar, the banking sector) is prone to perpetuate a negative feedback eff ect that is accentuated by the lender– borrower channel in situations where fi nancial institutions hold large exposures to public sector entities.

Based on CCA, the market- implied expected losses calcu-lated from equity market and balance sheet information of fi -nancial institutions can be combined with information from their credit default swap (CDS) contracts to estimate the gov-ernment’s contingent liabilities.22 Because systemically impor-tant institutions enjoy an implicit government guarantee, their creditors have an expectation of public sector support in the

22 See Gray and Jobst (2009b). See also Gapen (2009) for an application on CCA to the mea sure ment of contingent liabilities from government- sponsored enterprises in the United States.

such as risk- weighted assets. In the empirical section of the chapter, the relation between the MCAR and regulatory capi-tal adequacy is investigated further, which establishes the pos-sibility of defi ning a systemically based capital shortfall using CCA- based mea sures of solvency (see Section 3).

B. Estimating the contingent liabilities to the public sector

Large implicit government fi nancial guarantees (valued as contingent liabilities) create signifi cant valuation linkages between sovereigns and fi nancial sector risks. Th ese linkages could give rise to a destabilization pro cess that increases the susceptibility of public fi nances to the potential impact of distress in an outsized fi nancial sector (see Figure 26.2). Th e fi nancial crisis that started in 2007 is a stark reminder of how public sector support mea sures provided to large fi nancial in-stitutions can result in considerable risk transfer to the gov-ernment, which places even greater emphasis on long- term fi scal sustainability. A negative feedback loop between the fi nancial sector risks and fi scal policy arises because a decline in the market value of sovereign debt not only weakens the implicit sovereign guarantees to systemically important fi nan-

Sovereign Banks

ForeignSovereign

ForeignBanks

1. Lower marked-to-market (MTM) in value ofall government bonds held by local banks

2. Increase in bank funding costs3. Erosion in potential for official

support/bailout

Increase in contingent liabilities

Similar sovereignscome under

pressureRise in counterparty

credit risk

Lower marked-to-market (MTM) invalue of all government bonds

held by foreign banks

Increase in contingent liabilities

Dom

estic

eco

nom

yFo

reig

n ec

onom

y

Source: Authors.

Figure 26.2 Valuation Linkages between the Sovereign and Banking Sector

536-57355_IMF_StressTestHBk_ch03_3P.indd 420 11/5/14 2:06 AM

Andreas A. Jobst and Dale F. Gray 421

below the bond spread.24 Conversely, a below- par bond price pushes up the implied recovery rate of CDS, causing a markup of CDS spreads over comparable bond spreads for the same estimated default risk.

Estimated expected losses derived from both equity prices and credit spreads can be combined to derive the market- implied degree to which potential public sector support de-presses the cost of credit. Given PCDS(t), the ratio

(t ) = 1PCDS (t )PE (t )

, (26.24)

defi nes the share of expected loss covered by implicit (or explicit) government guarantees that depress the CDS spread below the level that would be warranted by the equity- implied default risk.25 Th e following equation,

(t )PE (t ) = 1PCDS (t )PE (t )

PE (t ) = PE (t ) PCDS (t ), (26.25)

represents the fraction of default risk covered by the govern-ment (and no longer refl ected in the marked- implied default risk), and (1 (t))PE(t) is the risk retained by an institution and refl ected in the se nior CDS spread. Th us, the time pat-tern of the government’s contingent liabilities then can be used to replace the marginal densities of expected losses in equation (26.9) in order to derive the systemic risk from the implicit public sector support to the banking sector accord-ing to the specifi cation in equation (26.12).

Although this defi nition of market- implied contingent lia-bilities provides a useful indication of possible sovereign risk transfer, the presented estimation method depends on a vari-ety of assumptions that infl uence the assessment of the likeli-hood of public sector support, especially at times of extreme stress. Th e extent to which the equity put option values dif-fer from the one implied by CDS spreads might refl ect distor-tions stemming from the modeling choice (and the breakdown of effi cient asset pricing in situations of illiquidity), changes in market conditions, and the capital structure impact of gov-ernment interventions, such as equity dilution in the wake of capital injections, beyond the infl uence of explicit or implicit guarantees.

Even though the equality condition of default probabilities derived from equity prices and CDS spreads implies that posi-tive (t) values cannot exist in absence of arbitrage, empirical

24 Th e diff erence in recovery values (often referred to as “basis”) implied by a divergence of CDS and bond spreads is approximated by using the fair value CDS (FVCDS) spread and the fair value option adjusted spread (FVOAS) reported by Moody’s KMV (MKMV) CreditEdge. Both FVOAS and FVCDS represent credit spreads (in basis points) for the bond and CDS contract of a par tic u lar fi rm based on risk horizon of t years (where t = 1– 10 years). Both spreads imply an LGD determined by the industry category. In practice, this adjustment factor is very close to unity for most of the cases, with a few cases where the factor falls within a 20 percentage point range (0.9 to 1.1).

25 Note that the estimation assumes a Eu ro pe an put option, which does not recognize the possibility of premature execution. Th is might over-state the actual expected losses inferred from put option values in com-parison with the put option derived from CDS spreads.

case of failure.23 Conversely, the cost of insuring the nonguar-anteed debt (as refl ected in the se nior CDS spread) should capture only the expected loss retained by such fi nancial in-stitutions (and borne by unsecured se nior creditors), after ac-counting for any implicit public sector support that is due to their systemic signifi cance. Th us, the market- implied govern-ment guarantee for large banks (as prime candidates for the status of systemically important fi nancial institutions) can be derived heuristically as the diff erence between the total ex-pected loss (i.e., the value of a put option PE(t) derived from the bank’s equity price) and the value of an implicit put op-tion PCDS(t) derived from the bank’s CDS spread— assuming that equity values remain unaff ected (which is very likely when banks are close to the default barrier, as the call option value from the residual claim of equity to future profi ts after debt payment converges to zero).

By replacing individual expected losses with this mea sure of contingent liabilities, the Systemic CCA framework can be used to derive an estimate of systemic risk from joint contin-gent liabilities. Given that the put option value PCDS(t) PE(t), it refl ects the expected losses associated with default net of any fi nancial guarantees, that is, residual default risk on un-secured se nior debt. PCDS(t) can be written as

PCDS (t ) = 1 expsCDS (t )10,000

BD(t )

1 (T t ) Be r (T t ) , (26.20)

after rearranging the specifi cation of the CDS spread (in ba-sis points), sCDS(t), under the risk- neutral mea sure as

sCDS (t )=1

T tln 1

PCDS (t )Be r (T t )

BD(t )

1 10,000, (26.21)

assuming a default probability,

1 exp (u)du0

t

= 1 exp( t )PCDS (t )Be r (T t )

, (26.22)

at time t, constant hazard rate sCDS(t) , and the implied yield to maturity defi ned by

D(t ) = Be y (T t ) e y (T t ) = D(t )B

= Be r (T t ) PE (t )B

, (26.23)

so that (1 sCDS(t))Be r(T t) = PD × LGD over one period T t = 1. A linear adjustment of B/D (t) 1 is needed in order to control for the impact of any diff erence between the market price and the repayable face value of outstanding debt on the fair pricing of credit protection. If outstanding debt trades above par, D(t) > B, the recovery of the nominal value under the CDS contract (“recovery at face value”) drops below the recovery rate implied by the market price of debt (“recovery at market value”). As a result, the CDS spread, sCDS(t), drops

23 As a result, the cost of funding for these institutions remains below the level commensurate to their actual default risk.

536-57355_IMF_StressTestHBk_ch03_3P.indd 421 11/5/14 2:06 AM

Systemic Contingent Claims Analysis 422

2. capital shortfall based on the MCAR generated from the change in market capitalization relative to the as-set value under the impact of expected losses.

Th e fi rst mea sure is presented in the empirical section of this chapter (see Section 3), which illustrates the practical ap-plication of the Systemic CCA framework for macroprudential stress testing. Th e second mea sure of MCAR is presented in the descriptive part of the section but is not pursued further in the application of the stress test scenarios.

Second, empirical and theoretical (endogenous) models can be used to specify the macro- fi nancial linkages of expected losses. By modeling how the impact of macroeconomic condi-tions on income components and asset impairment (such as net interest income, fee income, trading income, operating ex-penses, and credit losses) has infl uenced a bank’s market- implied expected losses in the past, it is possible to link indi-vidual estimates of expected losses (and their implications for potential capital shortfall) to a par tic u lar macroeconomic path (and associated fi nancial sector per for mance) in the fu-ture (IMF, 2010, 2011a, 2001b, 2011d, 2012a, 2012b). Alter-natively, the historical sensitivity of the main components of the option pricing formula themselves (i.e., the implied asset value and asset volatility) can be determined by applying stress conditions directly to the theoretical specifi cation of market- implied expected losses. Also, the implied asset value underpinning the put option value of each sample bank could be adjusted by the projected profi tability under diff er-ent stress scenarios in order to determine the corresponding change in the level of market- implied expected losses (IMF, 2011c, 2011e).

Th ird, the joint potential capital shortfall is derived from estimating the multivariate density of each bank’s individual marginal distribution of forecast expected losses (if any) and their dependence structure. If the number of forecast expected losses is insuffi cient because of the low frequency of macroeco-nomic variables chosen for the specifi cation of macro- fi nancial linkages (e.g., quarterly values over a fi ve- year forecast hori-zon), the time series of expected losses could be supplemented by historical expected losses to a point when the number of observations are suffi cient for the estimation of joint capital shortfall.

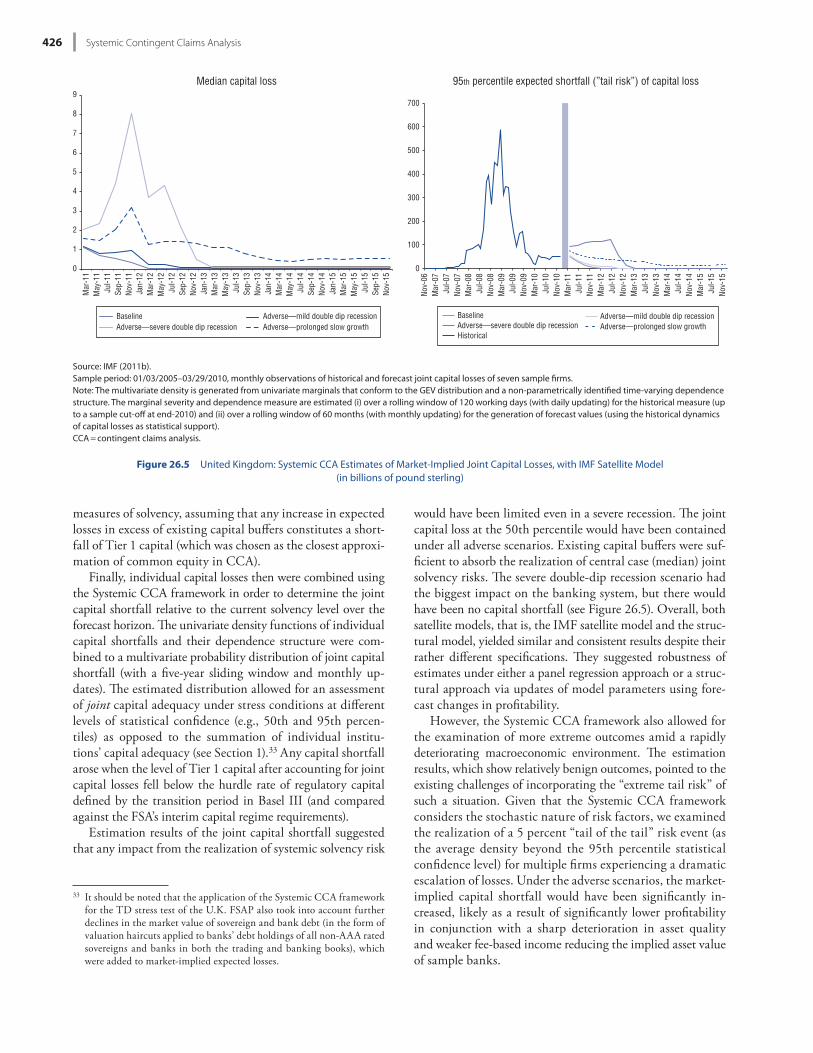

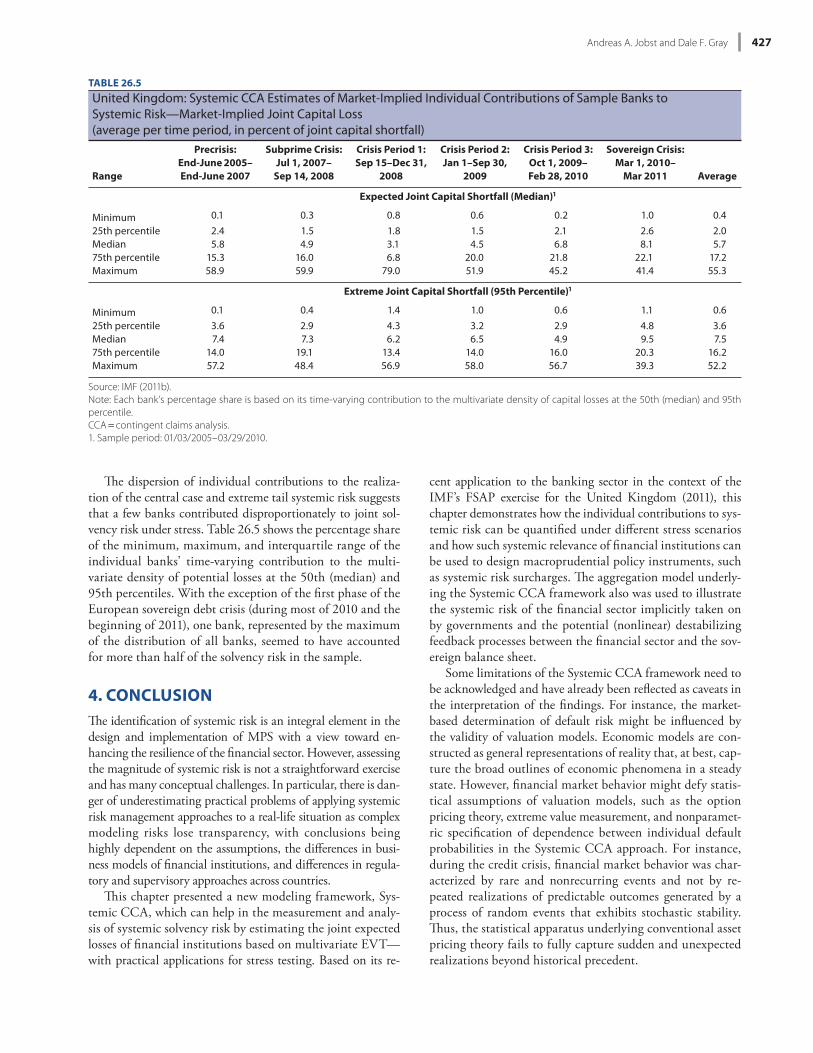

3. EMPIRICAL APPLICATION: STRESS TESTING SYSTEMIC RISK FROM EXPECTED LOSSES IN THE U.K. BANKING SECTORTh is section summarizes the fi ndings from applying the Sys-temic CCA framework as a market- based top- down (TD) sol-vency stress testing model as part of the IMF’s FSAP stress

valuation and, thus, individual estimates of market- implied capital shortfall. In the empirical application of Systemic CCA for capital as-sessment, Tier 1 capital was used for consistency purposes (because of divergent regulatory treatments of more ju nior capital tiers).

evidence during times of stress suggest otherwise.26 Carr and Wu (2007) show that for many fi rms the put option values from equity options and CDS are, indeed, closely related.27 In stress situations, however, the implicit put options from equity markets and CDS spreads can diff er in their capital structure impact and thus should be priced diff erently. Besides guar-antees, there are several distortions that could set apart put option values derived from CDS and equity prices, even if the risk- neutral default probability (RNDP) implied by the CDS spread (based on an exponential hazard rate) were the same as the RNDP component of the equity put option value. Some of these factors include (1) the recovery- at- face- value assumption underlying CDS spreads, and (2) diff erent risk horizons of put option values derived from CDS and equity prices. We address these two potential sources of dis-tortion via an adjustment for “basis risk” in equation (26.20).

C. Systemic CCA and stress testing

Th e Systemic CCA framework also can be used to project the dynamics of systemic solvency risk for the purposes of assess-ing capital adequacy under stress scenarios. Based on the his-torical distribution of fi rm- specifi c market- implied expected losses (which can be generated using conventional or more advanced option pricing techniques, future changes in market- implied default risk of each fi rm can be estimated over the selected forecast horizon (based on their macro- fi nancial link-ages under diff erent stress scenarios) and fi nally combined to defi ne systemwide solvency risk within the Systemic CCA framework.

First, a suitable univariate input is defi ned. Individual CCA- based estimates of market- implied expected losses can generate the following mea sures that support a fi rm- specifi c assessment of capital adequacy (and which have been applied empirically already):

1. capital shortfall based on the amount of expected losses in excess of existing common (core) equity Tier 1 capital above the regulatory minimum;28 and

26 Arbitrage trading between both prices shows that synthetic replication of credit protection on guaranteed bonds using equity can be obtained from combining a long position in an equity option “straddle” with a short CDS position.

27 Carr and Wu (2007) fi nd that equity options used in a modifi ed CCA seem to produce risk- neutral default probabilities (RNDP) that closely match RNDPs derived from CDS (sometimes higher, sometimes lower, and diff erences seem to predict future movements in both markets). Yu (2006) uses a less sophisticated model based on CreditGrades, which contains some simplifying assumptions.

28 Th e capital shortfall of each fi rm is defi ned as the amount of capital re-quired to preserve prestress solvency conditions, that is, the existing capital level above the regulatory minimum. It is mea sured as the mar-ginal change of expected losses over the forecast horizon relative to the expected losses mea sured at the end point of the historical sample of observations. Note that the market value of equity is considered equiva-lent to common equity Tier 1 capital because CCA does not specify re-ported capital tiers but implicitly assumes that any potential loss fi rst aff ects the most ju nior claims on fi rm assets. However, cross- sectional diff erences in the quality of capital held by fi rms will aff ect changes in

536-57355_IMF_StressTestHBk_ch03_3P.indd 422 11/5/14 2:06 AM

Andreas A. Jobst and Dale F. Gray 423

VaR values of individual expected losses or the joint 95 per-cent ES divided by the aggregate market capitalization) and the aggregate MCAR. Th e empirical results suggested an even higher sensitivity of MCAR to changes in systemwide expected losses than in the case of the single- fi rm example shown in Figure 26.3. In addition, the comparison of MCAR to the regulatory benchmark (Core Tier 1) indicates that the improvement of solvency conditions after the peak of the fi -nancial crisis in March 2009 appeared more protracted across all sample fi rms (see Figure 26.4, bottom chart).

B. Estimating expected losses under stress conditions based on macro- fi nancial linkages

Individual market- implied expected losses under stress condi-tions were derived from their historical sensitivity to changes in macro- fi nancial conditions and bank per for mance. Expected losses under diff erent stress scenarios were forecast using two diff erent methods for the specifi cation of the macro- fi nancial linkages of expected losses as mea sured by the implicit put option values of sample fi rms (see Section 2.B):

• In the fi rst model (“IMF satellite model”), expected losses were estimated using a dynamic panel regres-sion specifi cation with several macroeconomic vari-ables (short- term interest rate [+], long- term interest rate [ ], real GDP [ ], and unemployment [+]) and several bank- specifi c output variables (net interest income [+], operating profi t before taxes [ ], credit losses [+], leverage [+], and funding gap [+]).31

• In the second model (“structural model”), the value of implied assets of each bank as at end- 2010 is ad-justed by forecasts of operating profi t and credit losses generated in the Bank of En gland’s Risk As-sessment Model for Systemic Institutions (RAMSI) in order to derive a revised put option value (after reestimating implied asset volatility), which deter-mines the market- implied capital loss.32

Th e individually estimated expected losses then were trans-posed into a capital shortfall. Th e potential capital loss was determined on an individual basis as the marginal change of expected losses over the forecast horizon (2011– 2015) and evaluated for each macro- fi nancial approach and under each of the specifi ed adverse scenarios. As an alternative, the market- implied CAR (see Figures 26.3 and 26.4) could have been used as a basis for assessing capital adequacy and the extent to which expected losses result in potential capital shortfall. However, in the context of this exercise, the CCA- based results were transposed into conventional (regulatory)

31 Th e plus or minus signs indicate whether the selected variable exhibited a positive or negative regression coeffi cient. To be included in the model, the variables needed to be statistically signifi cant at least at the 10 per-cent level.

32 Th is approach also assumed a graduated increase of the default barrier consistent with the transition period to higher capital requirements for the most ju nior levels of equity under Basel III standards (Basel Com-mittee on Banking Supervision, 2012).