Supporting the competitiveness of the European

food and drink industry

CIAA CompetItIveness RepoRt 2010

Scope and objectives of the 2010 Competitiveness Report

This report analyses and sets out the priority areas which are critical for the long-term competitiveness of food and drink manufacturers in the EU.

The analysis has been done on several levels, by:

1. Presenting key competitiveness indicators; 2. Identifying the opportunities and threats for the EU food and drink industry compared to other

countries and regions;3. Assessing the extent to which the Recommendations of the Commission’s High Level Group for the

Competitiveness of the Agro-Food Industry have been implemented; and4. Identifying, and in some cases, confirming areas of action for policy-makers.

This report presents EU-27 data unless otherwise specified.

CIA

A C

ompe

titiv

enes

s Re

port

201

0

3

Foreword

The 2010 CIAA Competitiveness Report aims to assess the performance of the EU food and drink industry in light of political and economic developments in Europe and globally.

A pillar of the EU economy, the European food and drink sector is a stable employer and manufacturer. Despite this solid base and stable but low growth in production, the EU food and drink sector growth is being outpaced by the performance of emerging economies. This is due, among other things, to:

• Low levels of R&D in EU food and drink companies; • Lower labour productivity growth in the EU;• Uneven industry-retail relations within the EU food

chain leading to unfair practices;• Currently stable but relatively high input prices for

raw materials in the EU; and• A highly-regulated business environment in the EU.

At the same time, the EU food and drink industry remains the largest exporter globally, although its export market share on global markets is declining. Surprisingly, after eight years of decreasing trade balance, in 2009 the EU food and drink sector registered an upswing due to a sharp decrease in imports during the economic crisis.

As a non-cyclical sector, minimally subjected to the flow of markets and the economy, the EU food and drink industry has been less affected by the economic crisis than other industrial sectors, allowing it to continue to operate well in a challenging economic environment without state support. Food and drink companies have continued to provide healthy and nutritious products to their consumers throughout the crisis, while maintaining their commitments, among others, to the promotion of healthy lifestyles and balanced diets, sustainable consumption and production as well as research and innovation.

Finally, the EU food and drink industry calls for enhanced political support for the implementation of all actions aiming to increase the industry’s competitiveness as identified by CIAA in this report. For the EU food and drink industry, this is the way forward towards fulfilling the objectives of the EU 2020 Strategy.

Jesús Serafín Pérez PRESIDEnT

CIA

A C

ompe

titiv

enes

s Re

port

201

0C

IAA

Com

petit

iven

ess

Repo

rt 2

010

CIA

A C

ompe

titiv

enes

s Re

port

201

0

CIA

A C

ompe

titiv

enes

s Re

port

201

0

4

Table of Contents

Foreword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32009 at a glance: Food and drink companies in the EU . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1. Setting the scene: The food and drink industry – a pillar of the European economy . . . . . . . . . . . . . . . . 6

2. Main food and drink competitiveness indicators – an international comparison . . . . . . . . . . . . . . . . . . . . 8

2.1 Production value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82.2 Labour productivity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92.3 Export market share . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102.4 R&D investment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Special Section: High Level Group on the Competitiveness of the Agro-Food Industry . . . . . . . . . . . . . . . . 12

3. Specific food and drink industry benchmarks and requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143.1 Food supply chain issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143.2 Regulatory environment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 183.3 Business input costs, including agricultural raw materials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 213.4 Environmental policy and sustainability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 233.5 Trade competitiveness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Annexes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Acronyms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30List of tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30List of figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31List of boxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Table of Contents

CIA

A C

ompe

titiv

enes

s Re

port

201

0

5

Key sector characteristics

• Stable manufacturing sector and employer, true pillar of the EU economy• Mature sector operating mainly in a mature market (EU Single Market), although in need of policy-makers’

support to maintain its export competitiveness• Competitive industry compared to other developed countries but losing competitiveness against emerging

economies• Robust non-cyclical sector, less affected by the economic crisis than other business sectors in the EU

Key competitiveness indicators

Quantitative Indicators

Production Value Slow increase in production growth compared to emerging markets but keeping pace with developed economies

Labour Productivity Increased labour productivity, but still lagging behind other developed economies

Export Market Share EU still first exporter, but with a decreasing export market share

R&D Investment EU lagging behind its competitors and not growing

Qualitative Indicators

Functioning of the Food Chain Uneven industry-retail relations within the food chain leading to the proliferation of unfair practices

Private Labels The dual role of retail and the misuse of Private Labels

Regulatory Impact Highly-regulated business environment and low predictability for business decisions due to regulatory change

Access to Input Products Currently stable, but relatively high price levels of input products

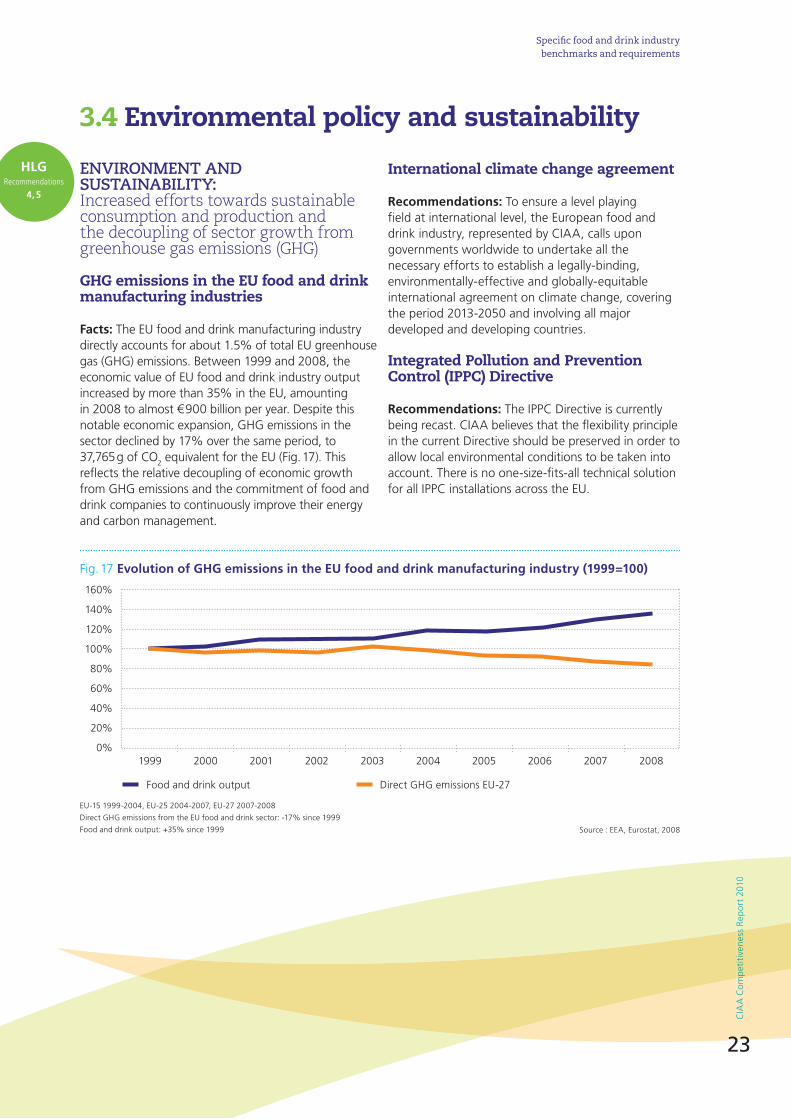

Environment and Sustainability Increased efforts towards sustainable consumption and production and towards decoupling growth from greenhouse gas emissions

Food and drink companies in the EU 2009 at a glance

CIA

A C

ompe

titiv

enes

s Re

port

201

0

6

Setting the scene: the food and drink industry – a pillar of the European economy

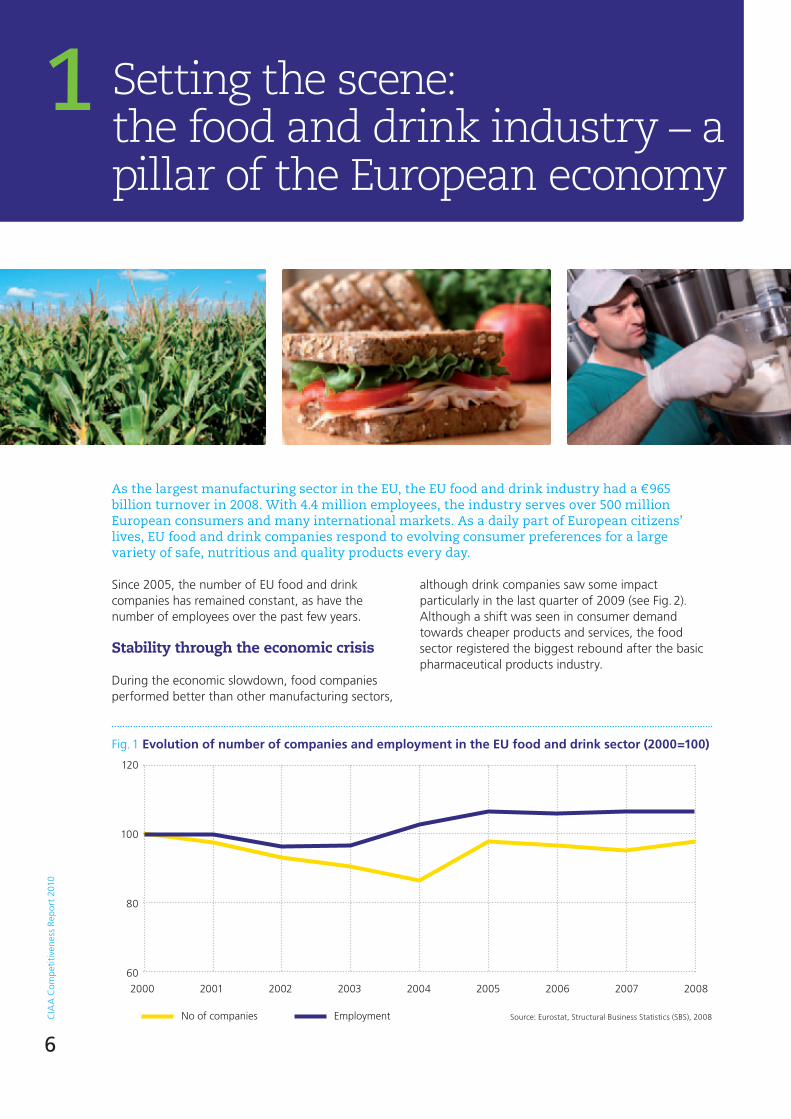

As the largest manufacturing sector in the eU, the eU food and drink industry had a € 965 billion turnover in 2008. With 4.4 million employees, the industry serves over 500 million european consumers and many international markets. As a daily part of european citizens’ lives, eU food and drink companies respond to evolving consumer preferences for a large variety of safe, nutritious and quality products every day.

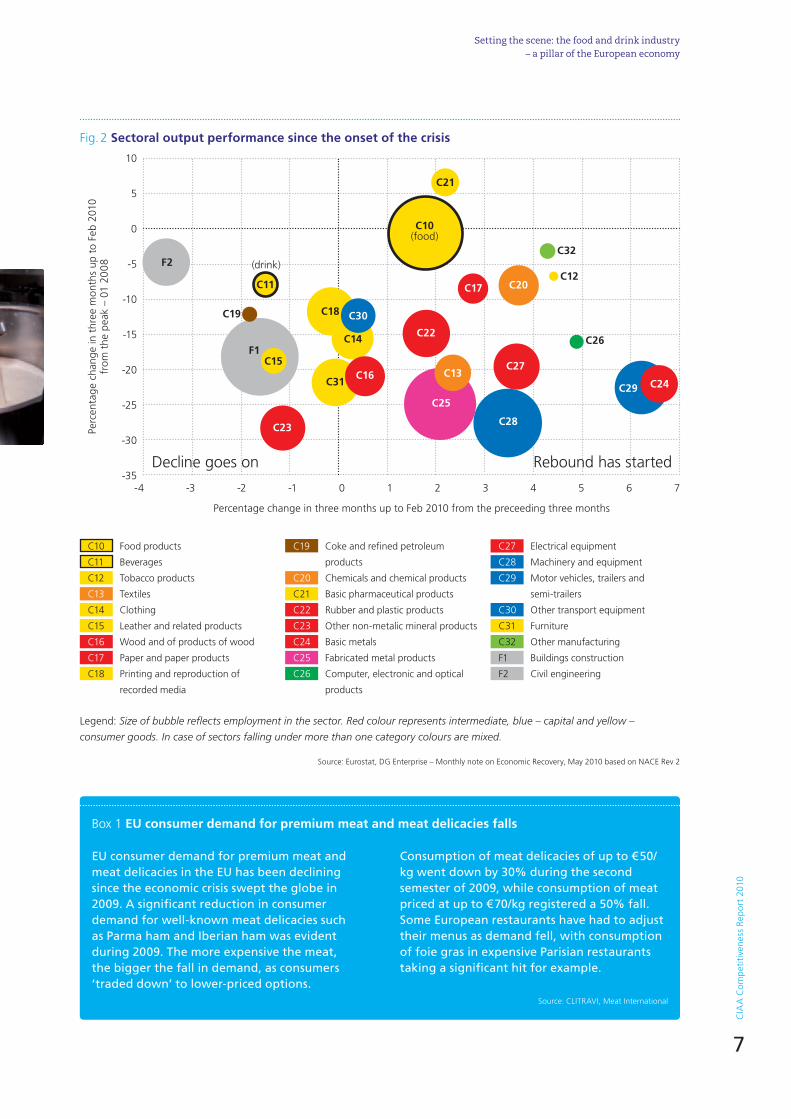

although drink companies saw some impact particularly in the last quarter of 2009 (see Fig. 2). Although a shift was seen in consumer demand towards cheaper products and services, the food sector registered the biggest rebound after the basic pharmaceutical products industry.

Fig. 1 Evolution of number of companies and employment in the EU food and drink sector (2000=100)

120

100

80

60

2000 2001 2002 2003 2004 2005 2006 2007 2008

no of companies Employment Source: Eurostat, Structural Business Statistics (SBS), 2008

Since 2005, the number of EU food and drink companies has remained constant, as have the number of employees over the past few years.

Stability through the economic crisis

During the economic slowdown, food companies performed better than other manufacturing sectors,

1

CIA

A C

ompe

titiv

enes

s Re

port

201

0

7

Box 1 EU consumer demand for premium meat and meat delicacies falls

10

5

0

-5

-10

-15

-20

-25

-30

-35

C21

F2

F1C15

C11

C10(food)

C18

C14

C31

C19

C32

C12

C26

C23

C30

C28

C20

C24C29C16

C22

C17

C27

C25

C13

-4 -3 -2 -1 0 1 2 3 4 5 6 7

Percentage change in three months up to Feb 2010 from the preceeding three months

Legend: Size of bubble reflects employment in the sector. Red colour represents intermediate, blue – capital and yellow –

consumer goods. In case of sectors falling under more than one category colours are mixed.

Perc

enta

ge c

hang

e in

thr

ee m

onth

s up

to

Feb

2010

fr

om t

he p

eak

– 01

20

08

Decline goes on Rebound has started

Source: Eurostat, DG Enterprise – Monthly note on Economic Recovery, May 2010 based on nACE Rev 2

Fig. 2 Sectoral output performance since the onset of the crisis

setting the scene: the food and drink industry – a pillar of the european economy

EU consumer demand for premium meat and meat delicacies in the EU has been declining since the economic crisis swept the globe in 2009. A significant reduction in consumer demand for well-known meat delicacies such as Parma ham and Iberian ham was evident during 2009. The more expensive the meat, the bigger the fall in demand, as consumers ‘traded down’ to lower-priced options.

Consumption of meat delicacies of up to € 50/kg went down by 30% during the second semester of 2009, while consumption of meat priced at up to € 70/kg registered a 50% fall. Some European restaurants have had to adjust their menus as demand fell, with consumption of foie gras in expensive Parisian restaurants taking a significant hit for example.

Source: CLITRAVI, Meat International

(drink)

C10 Food products

C11 Beverages

C12 Tobacco products

C13 Textiles

C14 Clothing

C15 Leather and related products

C16 Wood and of products of wood

C17 Paper and paper products

C18 Printing and reproduction of

recorded media

C19 Coke and refined petroleum

products

C20 Chemicals and chemical products

C21 Basic pharmaceutical products

C22 Rubber and plastic products

C23 Other non-metalic mineral products

C24 Basic metals

C25 Fabricated metal products

C26 Computer, electronic and optical

products

C27 Electrical equipment

C28 Machinery and equipment

C29 Motor vehicles, trailers and

semi-trailers

C30 Other transport equipment

C31 Furniture

C32 Other manufacturing

F1 Buildings construction

F2 Civil engineering

CIA

A C

ompe

titiv

enes

s Re

port

201

0

8

Main food and drink competitiveness indicators – an international comparison

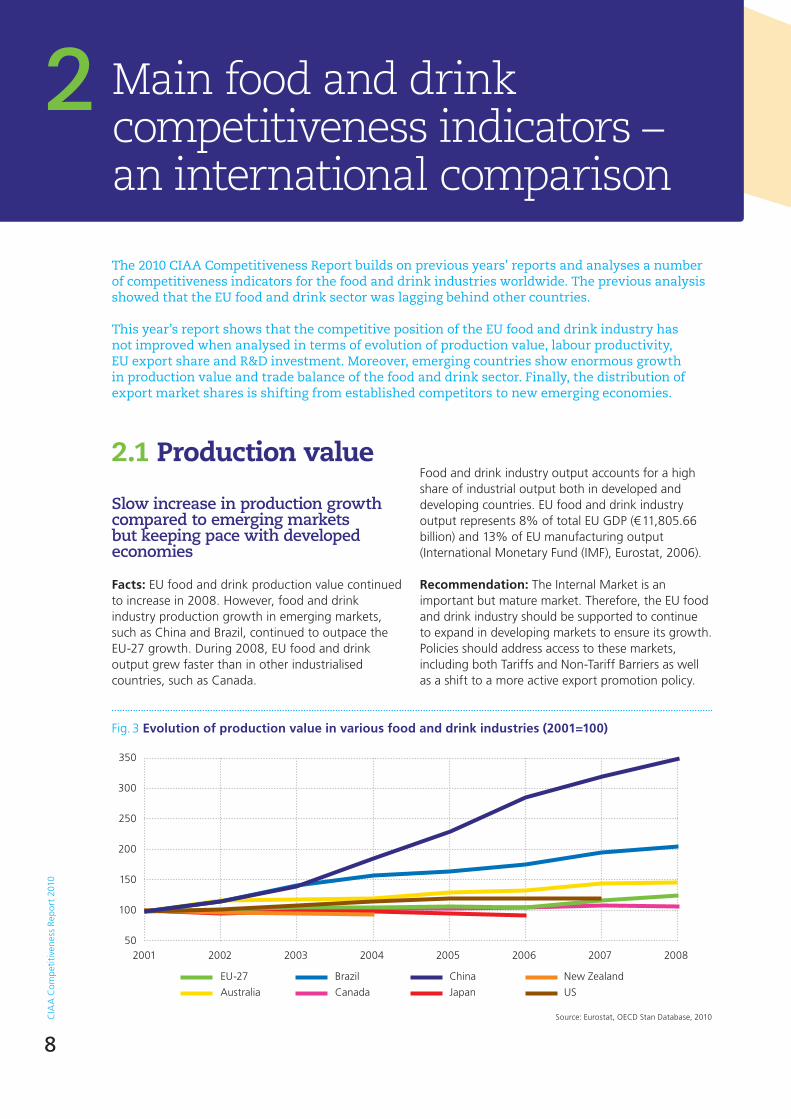

the 2010 CIAA Competitiveness Report builds on previous years’ reports and analyses a number of competitiveness indicators for the food and drink industries worldwide. the previous analysis showed that the eU food and drink sector was lagging behind other countries.

this year’s report shows that the competitive position of the eU food and drink industry has not improved when analysed in terms of evolution of production value, labour productivity, eU export share and R&D investment. moreover, emerging countries show enormous growth in production value and trade balance of the food and drink sector. Finally, the distribution of export market shares is shifting from established competitors to new emerging economies.

2.1 Production value

Slow increase in production growth compared to emerging markets but keeping pace with developed economies

Facts: EU food and drink production value continued to increase in 2008. However, food and drink industry production growth in emerging markets, such as China and Brazil, continued to outpace the EU-27 growth. During 2008, EU food and drink output grew faster than in other industrialised countries, such as Canada.

350

300

250

200

150

100

502001 2002 2003 2004 2005 2006 2007 2008

Fig. 3 Evolution of production value in various food and drink industries (2001=100)

Source: Eurostat, OECD Stan Database, 2010

EU-27

Australia

Brazil

Canada

China

Japan

new Zealand

US

2

Food and drink industry output accounts for a high share of industrial output both in developed and developing countries. EU food and drink industry output represents 8% of total EU GDP (€ 11,805.66 billion) and 13% of EU manufacturing output (International Monetary Fund (IMF), Eurostat, 2006).

Recommendation: The Internal Market is an important but mature market. Therefore, the EU food and drink industry should be supported to continue to expand in developing markets to ensure its growth. Policies should address access to these markets, including both Tariffs and non-Tariff Barriers as well as a shift to a more active export promotion policy.

CIA

A C

ompe

titiv

enes

s Re

port

201

0

9

2.2 Labour productivity

main food and drink competitiveness indicators – an international comparison

Increased labour productivity, but still lagging behind peers

Facts: Labour productivity (expressed as output in euros per employee) in the EU food and drink industry increased by 3% in 2008 compared to 2007. The EU continues to lag behind productivity levels in the food and drink sector in the US, Australia, new Zealand and Canada. Equally, EU labour productivity growth lags behind growth levels in emerging countries like China and Brazil. The main causes of lower labour productivity in the EU food and drink industries are the lack of exposure to global best practices1, low competitive intensity and the promotion of legitimate social objectives, which bear a high economic cost. As a result, Europe experiences lower investment when compared to its competitors in developed countries.

1 Due to product market barriers such as trade restrictions, price constraints, land ownership regulation etc.

Table 1 Labour productivity (output in € 1,000/employee/year)

Labour productivity (€ 1,000)

(%)

2007 2008 2008/2007

EU-27 214 220 3

US 285 – –

Australia 256 238 -7

New Zealand 220 252 15

Canada 205 242 18

Japan 157* – –

Mexico 103* – –

Brazil 59 74 25

China 42 49 17

* For Mexico and Japan 2006

Source: CIAA (details available on request)

Recommendations: Policies should focus on improving the overall labour productivity of the EU food and drink sector as part of the EU manufacturing industry, by addressing areas that affect the exposure to global best practices.

CIA

A C

ompe

titiv

enes

s Re

port

201

0

10

2.3 Export market share

Source: Eurostat Comext, WITS Database, 2008

Fig. 5 Evolution of various countries share in world food and drink exports (% in total)

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

EU-27

US

Brazil

China

Canada

Australia

new Zealand

Others

Fig. 4 EU food and drink sector export market share 1998-2008

Source: Eurostat Comext, WITS Database, 2008

EU-27

US

Brazil

China

Canada

Australia

new Zealand

Others

24.6%

1998

14.9%

4.9%4.6%

5.0%3.9%2.9%

39.1%

17.5%

200811.0%

7.3%

6.0%

3.9%3.0%2.9%

48.4%

EU still first exporter, but with a decreasing export market share

Facts: The EU is still the world’s largest food and drink exporter although the share of EU exports to world markets fell from 24.6% to 17.5% in the ten-year period from 1998 to 2008. This followed the general trend that, with the exception of new Zealand, the export market share of developed countries decreased and that of emerging economies grew.

Recommendations: An improved trade environment is required if the EU food and drink industry is to maintain its global share and take advantage of expanding emerging markets. This environment would include measures to prevent and remove regulatory barriers and the conclusion of well-balanced free trade agreements, both multilateral and bilateral.

CIA

A C

ompe

titiv

enes

s Re

port

201

0

11

2.4 R&D investment

EU industry is lagging behind the competition

Company-based R&D expenditure

Facts: Traditionally R&D investment in EU food and drink companies has been very low compared both to other EU industries and other countries’ food sectors. R&D expenditure levels are higher and continue to rise in Japan, the US, Australia and South Korea, while the EU has experienced relative stagnation at 0.37% of industry output in 2006.

Recommendations: CIAA supports that both public and private actors increase their spending on R&D. EU food and drink companies support the development

Fig. 6 R&D as a percentage of industry output for the food and drink industry in various countries (%)

Source: OECD Main Science and Technology Indicators, 2009

1.2%

1.0%

0.8%

0.6%

0.4%

0.2%

0.0%2000 2001 2002 2003 2004 2005 2006

Australia Canada EU-15 Japan Korea norway US

of a coherent EU strategy2 for the agri-food sector with the aim of sustaining the levels of investment in R&D reaching the 3% envelope for R&D3, promoting inter-EU knowledge transfer and leading to job creation. This will ensure the development of the Knowledge Based Bio-Economy (KBBE)4 and of a true ‘Innovation Union’, both of which are objectives declared by the European Commission.

2 The EU food and drink industry is highly committed to research through the European Technology Platform “Food for Life”. This platform brings together academia, researchers and industry representatives to explore research possibilities based on a clearly identified Strategic Research Agenda. More information on this initiative is available at: http://etp.ciaa.be/asp/home/welcome.asp.

3 The EU 2020 Strategy proposed a 3% envelope for R&D through public-private partnerships.

4 The Knowledge-Based Bio-Economy concept focuses on research and technology through public and private partnerships for the sustainable management, production and use of biological resources. The term “bio-economy” includes all industries and economic sectors that produce, manage and otherwise exploit biological resources (e.g. agriculture, food, forestry, fisheries and other bio-based industries) – European Commission.

main food and drink competitiveness indicators – an international comparison

CIA

A C

ompe

titiv

enes

s Re

port

201

0

12

CIA

A C

ompe

titiv

enes

s Re

port

201

0

12

Polic

y ar

eaH

LG R

eco

mm

end

atio

nD

G/E

uro

pea

n In

stit

uti

on

res

po

nsi

ble

Stat

us

July

201

0

Gen

era

lN

° 1: E

nsur

e a

holis

tic a

ppro

ach

for

the

Euro

pean

ag

ri-fo

od in

dust

ryD

G E

nter

pris

eO

ngoi

ng

• A

t C

omm

issi

on le

vel -

con

tinuo

us•

At

stak

ehol

der

leve

l, in

c. C

IAA

: “A

hol

istic

app

roac

h to

foo

d po

licy

– co

nsum

er in

form

atio

n: a

ca

se s

tudy

” –

to b

e pu

blis

hed

by e

nd 2

010

aG

ricu

ltu

ral

poli

cyN

° 2: C

ontin

ued

supp

ort

for

an a

mbi

tious

dev

elop

-m

ent

of t

he C

omm

on A

gric

ultu

ral P

olic

y (C

AP)

DG

Agr

icul

ture

& R

ural

Dev

elop

men

tO

ngoi

ng

• St

akeh

olde

rs c

onsu

ltatio

n an

d C

onfe

renc

e on

the

fut

ure

of t

he C

AP

post

-201

3 •

Com

mis

sion

Com

mun

icat

ion

on C

AP

post

-201

3 du

e to

be

rele

ased

in n

ovem

ber

2010

N° 3

: Suf

ficie

nt s

uppl

y of

raw

mat

eria

ls

at c

ompe

titiv

e pr

ices

DG

Agr

icul

ture

& R

ural

Dev

elop

men

tD

G H

ealth

& C

onsu

mer

sO

ngoi

ng

• Se

vera

l act

ions

with

FFC

(Foo

d an

d Fe

ed C

oalit

ion)

as

rega

rds

to G

MO

s•

new

Com

mis

sion

GM

O p

olic

y pr

opos

ed in

Jul

y 20

10, w

hich

incl

udes

gui

delin

es f

or c

ultiv

atio

n•

Stak

ehol

ders

wor

k to

war

ds t

he in

clus

ion

of f

ood

in t

he s

cope

of

the

impl

emen

ting

mea

sure

s to

ad

dres

s th

e is

sue

of a

sync

hron

ous

auth

oris

atio

ns f

or G

MO

s in

fee

d

envi

ron

men

tal

poli

cyN

° 4: D

esig

n an

env

ironm

enta

l and

sus

tain

able

in

dust

rial p

olic

yD

G E

nter

pris

eO

ngoi

ng•

Roun

d Ta

ble

esta

blis

hed

for

2009

-201

1•

EC s

tudy

on

eco

-labe

l crit

eria

for

foo

d by

201

1

N° 5

: Pro

mot

e en

ergy

effi

cien

cy f

or t

he E

urop

ean

agri-

food

indu

stry

DG

Ent

erpr

ise

DG

Res

earc

hO

ngoi

ng

• Im

plem

enta

tion

2007

-201

3•

Entr

epre

neur

ship

and

Inno

vatio

n Pr

ogra

mm

e as

par

t of

the

Com

petit

iven

ess

and

Inno

vatio

n Fr

amew

ork

Prog

ram

me

inte

rna

l m

ark

et

for

foo

d

N° 6

: Hig

h qu

alit

y an

d co

mpr

ehen

sive

impa

ct

asse

ssm

ents

Secr

etar

iat

Gen

eral

Euro

pean

Foo

d Sa

fety

Aut

horit

yC

ontin

uous

N° 7

: Har

mon

ised

inte

rpre

tatio

n an

d im

plem

enta

tion

of E

urop

ean

food

legi

slat

ion

DG

Hea

lth &

Con

sum

ers

Ong

oing

N° 8

: Effi

cien

t au

thor

isat

ion

proc

edur

es f

or n

ovel

fo

ods

DG

Hea

lth &

Con

sum

ers

Euro

pean

Foo

d Sa

fety

Aut

horit

yO

ngoi

ng

• Fo

llow

-up

by m

eans

of

the

Euro

pean

Foo

d Sa

fety

Aut

horit

y (E

FSA

) Ann

ual R

epor

t•

Ong

oing

con

cilia

tion

30 n

ovem

ber,

outc

ome

not

yet

clea

r

N° 9

: Enh

ance

the

Eur

opea

n in

cide

nt

man

agem

ent

syst

emD

G H

ealth

& C

onsu

mer

sO

ngoi

ng•

2010

con

sulta

tion

on t

he f

unct

ioni

ng o

f th

e Ra

pid

Ale

rt S

yste

m fo

r Fo

od a

nd F

eed

(RA

SFF)

• C

IAA

con

trib

utio

n to

the

con

sulta

tion

ope

rati

on

s in

th

e fo

od

ch

ain

N° 1

0: B

ette

r su

ppor

t fo

r SM

EsD

G E

nter

pris

eO

ngoi

ng•

Com

mis

sion

rev

iew

of

the

impl

emen

tatio

n of

the

Sm

all B

usin

ess

Act

(SBA

) (Ju

ne 2

010)

• Fo

llow

-up

by m

eans

of t

he Y

early

Act

ivity

Rep

ort o

f the

Exe

cutiv

e A

genc

y fo

r Com

petit

iven

ess

and

Inno

vatio

n (E

AC

I) a

wel

l as

by S

MEs

feed

back

mec

hani

sm e

xist

ing

with

in E

nter

pris

e Eu

rope

net

wor

k.

N° 1

1: B

ette

r ac

cess

to

finan

ceD

G B

udge

tEu

rope

an In

vest

men

t Ba

nk (E

IB)

Ong

oing

be

twee

n

2007

-201

3

• EI

B se

t up

3 fi

nanc

ing

inst

rum

ents

to

be f

urth

er im

plem

ente

d: lo

an s

chem

e, r

isk

shar

ing

an

d m

ezza

nine

fina

ncin

g•

Mic

rocr

edit:

est

ablis

hing

JA

SMIn

E m

icro

cred

it fa

cilit

y (f

or t

he n

on-b

ank

sect

or)

N° 1

2: S

impl

ify

acce

ss t

o fu

ndin

g re

sear

ch

prog

ram

mes

DG

Res

earc

hn

atio

nal T

echn

olog

y Pl

atfo

rms

Ong

oing

N° 1

3: F

acili

tate

acc

ess

of a

gri-f

ood

SMEs

to

glob

al

mar

kets

DG

Tra

deD

G E

nter

pris

eO

ngoi

ng•

Part

ially

ach

ieve

d th

roug

h th

e Sm

all B

usin

ess

Act

and

the

Com

mis

sion

Mar

ket

Acc

ess

Adv

isor

y C

omm

ittee

reg

ular

mee

tings

N° 1

4: S

uppo

rt e

ffec

tive

inte

grat

ion

of S

MEs

in t

he

food

cha

inD

G E

nter

pris

eO

ngoi

ng•

Part

ially

ach

ieve

d th

roug

h th

e Sm

all B

usin

ess

Act

N° 1

5: E

nsur

e pr

oper

and

opt

imal

fun

ctio

ning

of

the

foo

d ch

ain

DG

Ent

erpr

ise

Ong

oing

• C

omm

issi

on C

omm

unic

atio

n C

OM

(20

09)5

91 p

ublis

hed

in O

ctob

er 2

009

• H

igh

Leve

l For

um o

n th

e be

tter

fun

ctio

ning

foo

d su

pply

cha

in la

unch

ed in

Jul

y 20

10. F

irst

mee

ting

of t

he F

orum

exp

ecte

d to

con

vene

in n

ovem

ber

2010

• C

omm

issi

on f

ood

pric

e m

onito

ring

tool

con

tinuo

us u

pdat

e (la

st M

ay 2

010)

N° 1

6: S

tudy

the

eff

ect

of P

rivat

e La

bels

DG

Ent

erpr

ise

Ong

oing

• St

udy

resu

lts e

xpec

ted

Sum

mer

201

0 (d

elay

ed)

N° 1

7: In

crea

se a

ttra

ctiv

enes

s of

Eur

opea

n ag

ro-f

ood

indu

stry

to

wor

kers

DG

Em

ploy

men

tSo

cial

Aff

airs

& E

qual

Opp

ortu

nitie

sO

ngoi

ng•

Com

mis

sion

pro

gram

mes

for

you

ng e

ntre

pren

eurs

and

wor

kers

• C

omm

issi

on d

isse

min

atio

n of

the

res

ults

of

the

netw

ork

for

exce

llenc

e

N° 1

8: E

stab

lish

a so

cial

dia

logu

e in

the

agr

o-f

ood

indu

stry

DG

Em

ploy

men

t, S

ocia

l Aff

airs

& E

qual

O

ppor

tuni

ties,

Soc

ial P

artn

ers

Ong

oing

• A

firs

t m

eetin

g to

ok p

lace

ahe

ad o

f es

tabl

ishi

ng t

he s

ocia

l dia

logu

e•

Furt

her

mee

tings

to

be c

onve

ned

in 2

010

N° 1

9: E

ncou

rage

ICTs

use

in t

he a

gri-f

ood

indu

stry

DG

Res

earc

hO

ngoi

ng•

eBus

ines

s Su

ppor

t n

etw

ork

mee

tings

to

be d

isse

min

ated

by

end

of 2

010

N° 2

0: P

rom

ote

clar

ity

and

cohe

renc

e of

info

rmat

ion

to c

onsu

mer

sD

G H

ealth

& C

onsu

mer

sO

ngoi

ng

• Fo

od In

form

atio

n to

Con

sum

ers

Regu

latio

n un

der

revi

sion

: 1st r

eadi

ng in

the

Eur

opea

n Pa

rliam

ent

Plen

ary

was

on

16 J

une

2010

, with

2nd

rea

ding

exp

ecte

d du

ring

2011

rese

arc

h a

nd

in

no

vati

on

N° 2

1: E

nhan

ce r

esea

rch

and

inno

vatio

n ef

fort

sD

G R

esea

rch

Ong

oing

• In

the

cur

rent

7th F

ram

ewor

k Pr

ogra

mm

e (2

007

-201

3)•

New

CIA

A d

irect

invo

lvem

ent

in t

wo

proj

ects

(nuA

ge a

nd P

rom

ethe

us)

N° 2

2: B

ette

r us

e th

e in

stru

men

ts a

vaila

ble

in r

esea

rch

and

inno

vatio

n po

licy

DG

Res

earc

h, E

urop

ean

Tech

nolo

gy

Plat

form

Foo

d fo

r Li

fe, E

urop

ean

Inst

itute

of

Inno

vatio

n &

Tec

hnol

ogy

Ong

oing

• Th

e fir

st K

now

ledg

e an

d In

form

atio

n C

omm

uniti

es (K

ICs)

pub

lishe

d: C

limat

e, IC

T La

bs•

Com

mis

sion

to

refle

ct o

n an

ann

ual b

asis

on

the

Wor

k Pr

ogra

mm

e of

the

DG

Res

earc

h•

ETP

refle

cted

in t

he D

G r

esea

rch

wor

k pr

ogra

mm

e

N° 2

3: S

uppo

rt d

evel

opm

ent

of n

ew fo

od t

echn

olog

ies

DG

Res

earc

hO

ngoi

ng20

09-2

013

tra

de

N° 2

4: P

ursu

e th

e ob

ject

ive

of r

each

ing

a W

TO

bala

nced

agr

eem

ent

DG

s Tr

ade/

Ente

rpris

e/A

gric

ultu

re &

Ru

ral D

evel

opm

ent

Ong

oing

Acc

ordi

ng t

o th

e W

TO n

egot

iatio

ns r

oadm

ap:

• C

omm

issi

on 6

th R

epor

t on

Tra

de R

estr

ictiv

e M

easu

res,

incl

udin

g m

easu

res

affe

ctin

g fo

od t

rade

, pu

blis

hed

in M

ay 2

010.

N° 2

5: S

eize

mar

ket

oppo

rtun

ities

by

mea

ns o

f bi

late

ral t

rade

neg

otia

tions

DG

s Tr

ade/

Ente

rpris

e/A

gric

ultu

re &

Ru

ral D

evel

opm

ent

Ong

oing

• A

nnua

l mee

ting

with

the

agr

i-foo

d in

dust

ry s

take

hold

ers

• C

omm

issi

on a

nnua

l bila

tera

l mee

tings

with

thi

rd c

ount

ries

on S

anita

ry a

nd P

hyto

sani

tary

(SPS

) m

easu

res

and

Tech

nica

l Bar

riers

to

Trad

e (T

BT)

N° 2

6: B

ette

r pr

omot

e in

tern

atio

nal t

rade

sta

ndar

ds

DG

Tra

deO

ngoi

ng

Com

mis

sion

act

ions

tow

ards

Afr

ican

, Car

ibbe

an a

nd P

acifi

c (A

CP)

cou

ntrie

s:•

To p

rom

ote

lega

l fra

mew

ork

for

harm

onis

ed in

tern

atio

nal s

tand

ards

and

• To

pro

vide

a h

ighe

r de

gree

of

assi

stan

ce t

hrou

gh c

apac

ity

build

ing

N° 2

7: E

nhan

ce r

espe

ct o

f in

telle

ctua

l pro

pert

y rig

hts

by t

hird

cou

ntrie

sD

G E

nter

pris

eO

ngoi

ng•

Com

mis

sion

to

esta

blis

h m

arke

t su

rvei

llanc

e or

gani

sms

by 2

010

• Se

t up

nat

iona

l org

anis

atio

ns t

o re

port

on

coun

terf

eite

d pr

oduc

ts b

y 20

11

N° 2

8: D

efine

bet

ter

the

posi

tion

of t

he E

urop

ean

agri-

food

indu

stry

in t

he g

loba

l mar

ket

DG

Tra

de &

DG

Agr

icul

ture

Ong

oing

• Im

prov

emen

t of

the

EU

pro

mot

ion

regi

me

will

be

part

of

the

Com

mis

sion

Com

mun

icat

ion

on t

he

CA

P po

st-2

013

• C

omm

issi

on t

o la

unch

SW

OT

anal

ysis

by

end

2010

. Res

ults

to

be m

ade

avai

labl

e by

201

1

N° 2

9: S

impl

ify

cust

oms

form

aliti

esD

G T

axat

ion

& C

usto

ms

Uni

onO

ngoi

ng•

Euro

pean

Com

mis

sion

to

defin

e a

stra

tegy

on

sing

le w

indo

w c

omm

unic

atio

n

N° 3

0: P

rom

ote

a se

ctor

-spe

cific

app

roac

h fo

r th

e ru

les

of o

rigin

DG

Tax

atio

n &

Cus

tom

s U

nion

Ong

oing

• Eu

rope

an C

omm

issi

on t

o in

clud

e th

is s

ecto

r-sp

ecifi

c ap

proa

ch o

n ru

les

of o

rigin

in t

he

fort

hcom

ing

refo

rm o

f ru

les

of o

rigin

to

be a

pplie

d in

the

con

text

of

the

Gen

eral

ised

Sys

tem

of

Pref

eren

ces

– by

201

0

Sour

ce: C

IAA

ana

lysi

s of

HLG

Rec

omm

enda

tion

s (D

G E

nter

pris

e, H

LG 0

06

and

HLG

007

)

(htt

p://e

c.eu

ropa

.eu

/ent

erpr

ise/

new

sro

om/c

f/do

cum

ent.

cfm

?act

ion

=di

spla

y&do

c_id

=26

05&

user

serv

ice_

id=1

)

Hig

h L

evel

Gro

up

on t

he

Com

peti

tive

nes

s of

th

e A

gro-

Food

Indu

stry

HLG

rec

omm

enda

tion

s sc

oreb

oard

In

crea

sin

g th

e C

omp

etit

iven

ess

of t

he

Agr

o-Fo

od in

dust

ry

th

e 20

08 C

omm

issi

on-d

rive

n H

igh

Lev

el G

rou

p (H

LG) o

n t

he

Com

pet

itiv

enes

s of

th

e A

gro

-Foo

d I

nd

ust

ry p

rese

nte

d in

Jun

e 20

09 a

set

of

30

Rec

omm

end

atio

ns

aim

ed a

t in

crea

sin

g th

e in

du

stry

’s c

omp

etit

iven

ess.

th

is s

ecti

on c

har

ts t

he

imp

lem

enta

tion

of

the

HLG

Rec

omm

end

atio

ns

to d

ate.

CIA

A

wil

l con

tin

ue

to m

onit

or t

he

HLG

Rec

omm

end

atio

ns

imp

lem

enta

tion

pro

cess

.

CIA

A b

elie

ves

that

fur

ther

con

sist

ency

is n

eede

d be

twee

n po

licie

s in

all

area

s w

hich

impa

ct o

n th

e fo

od a

nd d

rink

indu

stry

, inc

ludi

ng r

esea

rch

and

inno

vatio

n, c

omm

erci

al

law

, agr

icul

ture

, foo

d sa

fety

, env

ironm

ent

and

trad

e. T

his

is o

f pa

ram

ount

impo

rtan

ce if

the

EU

is t

o ai

m f

or a

n in

tegr

ated

foo

d po

licy.

In li

ne w

ith t

his

appr

oach

, the

se H

LG

Reco

mm

enda

tions

set

out

in t

he t

able

bel

ow w

ill b

e ex

plor

ed in

the

nex

t su

bsec

tions

of

this

rep

ort.

The

foo

d an

d dr

ink

indu

stry

is s

tron

gly

com

mitt

ed t

o co

ntrib

utin

g to

the

im

plem

enta

tion

of t

he H

LG R

ecom

men

datio

ns a

long

with

the

res

pons

ible

Inst

itutio

ns.

Tabl

e 2

Hig

h L

evel

Gro

up

rec

om

men

dat

ion

s im

ple

men

tati

on

(Red

= t

op C

IAA

prio

ritie

s)

CIA

A C

ompe

titiv

enes

s Re

port

201

0

13

CIA

A C

ompe

titiv

enes

s Re

port

201

0

13

Polic

y ar

eaH

LG R

eco

mm

end

atio

nD

G/E

uro

pea

n In

stit

uti

on

res

po

nsi

ble

Stat

us

July

201

0

Gen

era

lN

° 1: E

nsur

e a

holis

tic a

ppro

ach

for

the

Euro

pean

ag

ri-fo

od in

dust

ryD

G E

nter

pris

eO

ngoi

ng

• A

t C

omm

issi

on le

vel -

con

tinuo

us•

At

stak

ehol

der

leve

l, in

c. C

IAA

: “A

hol

istic

app

roac

h to

foo

d po

licy

– co

nsum

er in

form

atio

n: a

ca

se s

tudy

” –

to b

e pu

blis

hed

by e

nd 2

010

aG

ricu

ltu

ral

poli

cyN

° 2: C

ontin

ued

supp

ort

for

an a

mbi

tious

dev

elop

-m

ent

of t

he C

omm

on A

gric

ultu

ral P

olic

y (C

AP)

DG

Agr

icul

ture

& R

ural

Dev

elop

men

tO

ngoi

ng

• St

akeh

olde

rs c

onsu

ltatio

n an

d C

onfe

renc

e on

the

fut

ure

of t

he C

AP

post

-201

3 •

Com

mis

sion

Com

mun

icat

ion

on C

AP

post

-201

3 du

e to

be

rele

ased

in n

ovem

ber

2010

N° 3

: Suf

ficie

nt s

uppl

y of

raw

mat

eria

ls

at c

ompe

titiv

e pr

ices

DG

Agr

icul

ture

& R

ural

Dev

elop

men

tD

G H

ealth

& C

onsu

mer

sO

ngoi

ng

• Se

vera

l act

ions

with

FFC

(Foo

d an

d Fe

ed C

oalit

ion)

as

rega

rds

to G

MO

s•

new

Com

mis

sion

GM

O p

olic

y pr

opos

ed in

Jul

y 20

10, w

hich

incl

udes

gui

delin

es f

or c

ultiv

atio

n•

Stak

ehol

ders

wor

k to

war

ds t

he in

clus

ion

of f

ood

in t

he s

cope

of

the

impl

emen

ting

mea

sure

s to

ad

dres

s th

e is

sue

of a

sync

hron

ous

auth

oris

atio

ns f

or G

MO

s in

fee

d

envi

ron

men

tal

poli

cyN

° 4: D

esig

n an

env

ironm

enta

l and

sus

tain

able

in

dust

rial p

olic

yD

G E

nter

pris

eO

ngoi

ng•

Roun

d Ta

ble

esta

blis

hed

for

2009

-201

1•

EC s

tudy

on

eco

-labe

l crit

eria

for

foo

d by

201

1

N° 5

: Pro

mot

e en

ergy

effi

cien

cy f

or t

he E

urop

ean

agri-

food

indu

stry

DG

Ent

erpr

ise

DG

Res

earc

hO

ngoi

ng

• Im

plem

enta

tion

2007

-201

3•

Entr

epre

neur

ship

and

Inno

vatio

n Pr

ogra

mm

e as

par

t of

the

Com

petit

iven

ess

and

Inno

vatio

n Fr

amew

ork

Prog

ram

me

inte

rna

l m

ark

et

for

foo

d

N° 6

: Hig

h qu

alit

y an

d co

mpr

ehen

sive

impa

ct

asse

ssm

ents

Secr

etar

iat

Gen

eral

Euro

pean

Foo

d Sa

fety

Aut

horit

yC

ontin

uous

N° 7

: Har

mon

ised

inte

rpre

tatio

n an

d im

plem

enta

tion

of E

urop

ean

food

legi

slat

ion

DG

Hea

lth &

Con

sum

ers

Ong

oing

N° 8

: Effi

cien

t au

thor

isat

ion

proc

edur

es f

or n

ovel

fo

ods

DG

Hea

lth &

Con

sum

ers

Euro

pean

Foo

d Sa

fety

Aut

horit

yO

ngoi

ng

• Fo

llow

-up

by m

eans

of

the

Euro

pean

Foo

d Sa

fety

Aut

horit

y (E

FSA

) Ann

ual R

epor

t•

Ong

oing

con

cilia

tion

30 n

ovem

ber,

outc

ome

not

yet

clea

r

N° 9

: Enh

ance

the

Eur

opea

n in

cide

nt

man

agem

ent

syst

emD

G H

ealth

& C

onsu

mer

sO

ngoi

ng•

2010

con

sulta

tion

on t

he f

unct

ioni

ng o

f th

e Ra

pid

Ale

rt S

yste

m fo

r Fo

od a

nd F

eed

(RA

SFF)

• C

IAA

con

trib

utio

n to

the

con

sulta

tion

ope

rati

on

s in

th

e fo

od

ch

ain

N° 1

0: B

ette

r su

ppor

t fo

r SM

EsD

G E

nter

pris

eO

ngoi

ng•

Com

mis

sion

rev

iew

of

the

impl

emen

tatio

n of

the

Sm

all B

usin

ess

Act

(SBA

) (Ju

ne 2

010)

• Fo

llow

-up

by m

eans

of t

he Y

early

Act

ivity

Rep

ort o

f the

Exe

cutiv

e A

genc

y fo

r Com

petit

iven

ess

and

Inno

vatio

n (E

AC

I) a

wel

l as

by S

MEs

feed

back

mec

hani

sm e

xist

ing

with

in E

nter

pris

e Eu

rope

net

wor

k.

N° 1

1: B

ette

r ac

cess

to

finan

ceD

G B

udge

tEu

rope

an In

vest

men

t Ba

nk (E

IB)

Ong

oing

be

twee

n

2007

-201

3

• EI

B se

t up

3 fi

nanc

ing

inst

rum

ents

to

be f

urth

er im

plem

ente

d: lo

an s

chem

e, r

isk

shar

ing

an

d m

ezza

nine

fina

ncin

g•

Mic

rocr

edit:

est

ablis

hing

JA

SMIn

E m

icro

cred

it fa

cilit

y (f

or t

he n

on-b

ank

sect

or)

N° 1

2: S

impl

ify

acce

ss t

o fu

ndin

g re

sear

ch

prog

ram

mes

DG

Res

earc

hn

atio

nal T

echn

olog

y Pl

atfo

rms

Ong

oing

N° 1

3: F

acili

tate

acc

ess

of a

gri-f

ood

SMEs

to

glob

al

mar

kets

DG

Tra

deD

G E

nter

pris

eO

ngoi

ng•

Part

ially

ach

ieve

d th

roug

h th

e Sm

all B

usin

ess

Act

and

the

Com

mis

sion

Mar

ket

Acc

ess

Adv

isor

y C

omm

ittee

reg

ular

mee

tings

N° 1

4: S

uppo

rt e

ffec

tive

inte

grat

ion

of S

MEs

in t

he

food

cha

inD

G E

nter

pris

eO

ngoi

ng•

Part

ially

ach

ieve

d th

roug

h th

e Sm

all B

usin

ess

Act

N° 1

5: E

nsur

e pr

oper

and

opt

imal

fun

ctio

ning

of

the

foo

d ch

ain

DG

Ent

erpr

ise

Ong

oing

• C

omm

issi

on C

omm

unic

atio

n C

OM

(20

09)5

91 p

ublis

hed

in O

ctob

er 2

009

• H

igh

Leve

l For

um o

n th

e be

tter

fun

ctio

ning

foo

d su

pply

cha

in la

unch

ed in

Jul

y 20

10. F

irst

mee

ting

of t

he F

orum

exp

ecte

d to

con

vene

in n

ovem

ber

2010

• C

omm

issi

on f

ood

pric

e m

onito

ring

tool

con

tinuo

us u

pdat

e (la

st M

ay 2

010)

N° 1

6: S

tudy

the

eff

ect

of P

rivat

e La

bels

DG

Ent

erpr

ise

Ong

oing

• St

udy

resu

lts e

xpec

ted

Sum

mer

201

0 (d

elay

ed)

N° 1

7: In

crea

se a

ttra

ctiv

enes

s of

Eur

opea

n ag

ro-f

ood

indu

stry

to

wor

kers

DG

Em

ploy

men

tSo

cial

Aff

airs

& E

qual

Opp

ortu

nitie

sO

ngoi

ng•

Com

mis

sion

pro

gram

mes

for

you

ng e

ntre

pren

eurs

and

wor

kers

• C

omm

issi

on d

isse

min

atio

n of

the

res

ults

of

the

netw

ork

for

exce

llenc

e

N° 1

8: E

stab

lish

a so

cial

dia

logu

e in

the

agr

o-f

ood

indu

stry

DG

Em

ploy

men

t, S

ocia

l Aff

airs

& E

qual

O

ppor

tuni

ties,

Soc

ial P

artn

ers

Ong

oing

• A

firs

t m

eetin

g to

ok p

lace

ahe

ad o

f es

tabl

ishi

ng t

he s

ocia

l dia

logu

e•

Furt

her

mee

tings

to

be c

onve

ned

in 2

010

N° 1

9: E

ncou

rage

ICTs

use

in t

he a

gri-f

ood

indu

stry

DG

Res

earc

hO

ngoi

ng•

eBus

ines

s Su

ppor

t n

etw

ork

mee

tings

to

be d

isse

min

ated

by

end

of 2

010

N° 2

0: P

rom

ote

clar

ity

and

cohe

renc

e of

info

rmat

ion

to c

onsu

mer

sD

G H

ealth

& C

onsu

mer

sO

ngoi

ng

• Fo

od In

form

atio

n to

Con

sum

ers

Regu

latio

n un

der

revi

sion

: 1st r

eadi

ng in

the

Eur

opea

n Pa

rliam

ent

Plen

ary

was

on

16 J

une

2010

, with

2nd

rea

ding

exp

ecte

d du

ring

2011

rese

arc

h a

nd

in

no

vati

on

N° 2

1: E

nhan

ce r

esea

rch

and

inno

vatio

n ef

fort

sD

G R

esea

rch

Ong

oing

• In

the

cur

rent

7th F

ram

ewor

k Pr

ogra

mm

e (2

007

-201

3)•

New

CIA

A d

irect

invo

lvem

ent

in t

wo

proj

ects

(nuA

ge a

nd P

rom

ethe

us)

N° 2

2: B

ette

r us

e th

e in

stru

men

ts a

vaila

ble

in r

esea

rch

and

inno

vatio

n po

licy

DG

Res

earc

h, E

urop

ean

Tech

nolo

gy

Plat

form

Foo

d fo

r Li

fe, E

urop

ean

Inst

itute

of

Inno

vatio

n &

Tec

hnol

ogy

Ong

oing

• Th

e fir

st K

now

ledg

e an

d In

form

atio

n C

omm

uniti

es (K

ICs)

pub

lishe

d: C

limat

e, IC

T La

bs•

Com

mis

sion

to

refle

ct o

n an

ann

ual b

asis

on

the

Wor

k Pr

ogra

mm

e of

the

DG

Res

earc

h•

ETP

refle

cted

in t

he D

G r

esea

rch

wor

k pr

ogra

mm

e

N° 2

3: S

uppo

rt d

evel

opm

ent

of n

ew fo

od t

echn

olog

ies

DG

Res

earc

hO

ngoi

ng20

09-2

013

tra

de

N° 2

4: P

ursu

e th

e ob

ject

ive

of r

each

ing

a W

TO

bala

nced

agr

eem

ent

DG

s Tr

ade/

Ente

rpris

e/A

gric

ultu

re &

Ru

ral D

evel

opm

ent

Ong

oing

Acc

ordi

ng t

o th

e W

TO n

egot

iatio

ns r

oadm

ap:

• C

omm

issi

on 6

th R

epor

t on

Tra

de R

estr

ictiv

e M

easu

res,

incl

udin

g m

easu

res

affe

ctin

g fo

od t

rade

, pu

blis

hed

in M

ay 2

010.

N° 2

5: S

eize

mar

ket

oppo

rtun

ities

by

mea

ns o

f bi

late

ral t

rade

neg

otia

tions

DG

s Tr

ade/

Ente

rpris

e/A

gric

ultu

re &

Ru

ral D

evel

opm

ent

Ong

oing

• A

nnua

l mee

ting

with

the

agr

i-foo

d in

dust

ry s

take

hold

ers

• C

omm

issi

on a

nnua

l bila

tera

l mee

tings

with

thi

rd c

ount

ries

on S

anita

ry a

nd P

hyto

sani

tary

(SPS

) m

easu

res

and

Tech

nica

l Bar

riers

to

Trad

e (T

BT)

N° 2

6: B

ette

r pr

omot

e in

tern

atio

nal t

rade

sta

ndar

ds

DG

Tra

deO

ngoi

ng

Com

mis

sion

act

ions

tow

ards

Afr

ican

, Car

ibbe

an a

nd P

acifi

c (A

CP)

cou

ntrie

s:•

To p

rom

ote

lega

l fra

mew

ork

for

harm

onis

ed in

tern

atio

nal s

tand

ards

and

• To

pro

vide

a h

ighe

r de

gree

of

assi

stan

ce t

hrou

gh c

apac

ity

build

ing

N° 2

7: E

nhan

ce r

espe

ct o

f in

telle

ctua

l pro

pert

y rig

hts

by t

hird

cou

ntrie

sD

G E

nter

pris

eO

ngoi

ng•

Com

mis

sion

to

esta

blis

h m

arke

t su

rvei

llanc

e or

gani

sms

by 2

010

• Se

t up

nat

iona

l org

anis

atio

ns t

o re

port

on

coun

terf

eite

d pr

oduc

ts b

y 20

11

N° 2

8: D

efine

bet

ter

the

posi

tion

of t

he E

urop

ean

agri-

food

indu

stry

in t

he g

loba

l mar

ket

DG

Tra

de &

DG

Agr

icul

ture

Ong

oing

• Im

prov

emen

t of

the

EU

pro

mot

ion

regi

me

will

be

part

of

the

Com

mis

sion

Com

mun

icat

ion

on t

he

CA

P po

st-2

013

• C

omm

issi

on t

o la

unch

SW

OT

anal

ysis

by

end

2010

. Res

ults

to

be m

ade

avai

labl

e by

201

1

N° 2

9: S

impl

ify

cust

oms

form

aliti

esD

G T

axat

ion

& C

usto

ms

Uni

onO

ngoi

ng•

Euro

pean

Com

mis

sion

to

defin

e a

stra

tegy

on

sing

le w

indo

w c

omm

unic

atio

n

N° 3

0: P

rom

ote

a se

ctor

-spe

cific

app

roac

h fo

r th

e ru

les

of o

rigin

DG

Tax

atio

n &

Cus

tom

s U

nion

Ong

oing

• Eu

rope

an C

omm

issi

on t

o in

clud

e th

is s

ecto

r-sp

ecifi

c ap

proa

ch o

n ru

les

of o

rigin

in t

he

fort

hcom

ing

refo

rm o

f ru

les

of o

rigin

to

be a

pplie

d in

the

con

text

of

the

Gen

eral

ised

Sys

tem

of

Pref

eren

ces

– by

201

0

Sour

ce: C

IAA

ana

lysi

s of

HLG

Rec

omm

enda

tion

s (D

G E

nter

pris

e, H

LG 0

06

and

HLG

007

)

(htt

p://e

c.eu

ropa

.eu

/ent

erpr

ise/

new

sro

om/c

f/do

cum

ent.

cfm

?act

ion

=di

spla

y&do

c_id

=26

05&

user

serv

ice_

id=1

)

CIA

A C

ompe

titiv

enes

s Re

port

201

0

14

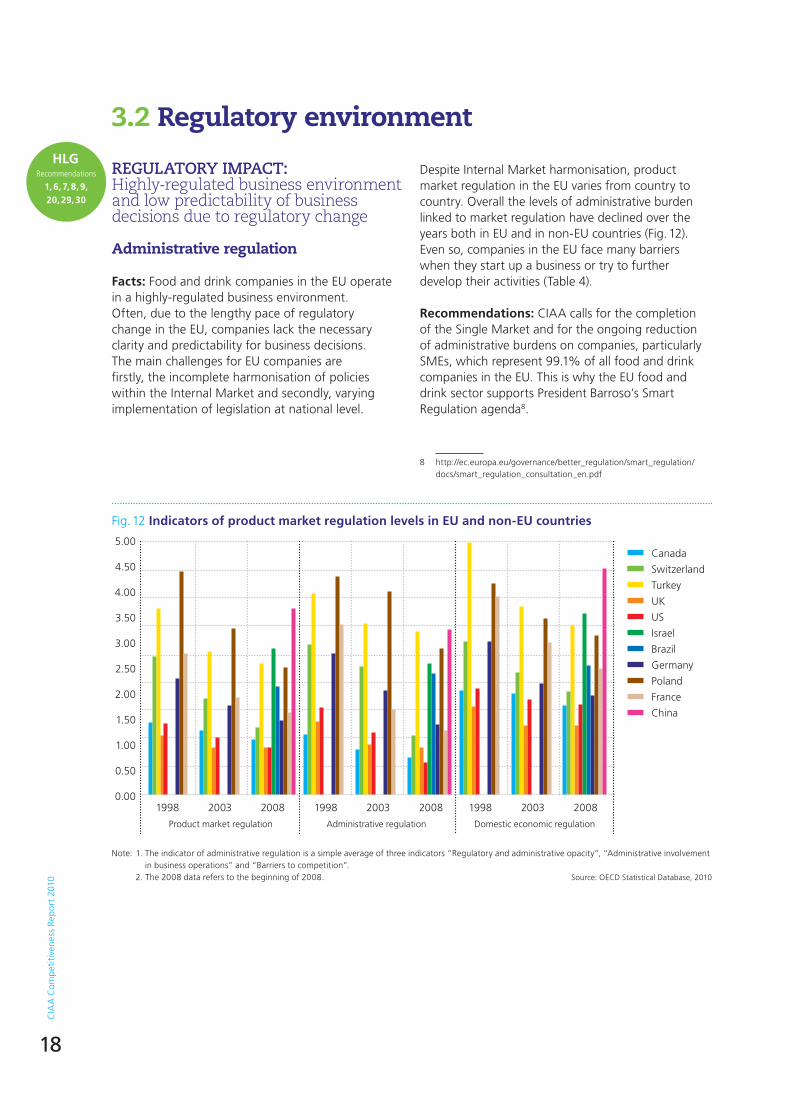

Specific food and drink industry benchmarks and requirements

and innovate, and longer-term, consumer economic welfare and choice are jeopardised. While the food and drink sector is in favour of strong competition, such unfair practices can only be solved if a new focus is put on the existing instruments of competition law.

Recommendations: CIAA fully supports the launch of the Forum for the Better Functioning Food Supply Chain, and of the Platform/Working Group on Contractual Relations, which will address the issue of manifest, unfair practices. CIAA recommends looking into the effects of Private Labels and international buying alliances, which are mutually reinforcing the buying power of retailers along the food chain.

HLG Recommendations

15, 16

3.1 Food supply chain

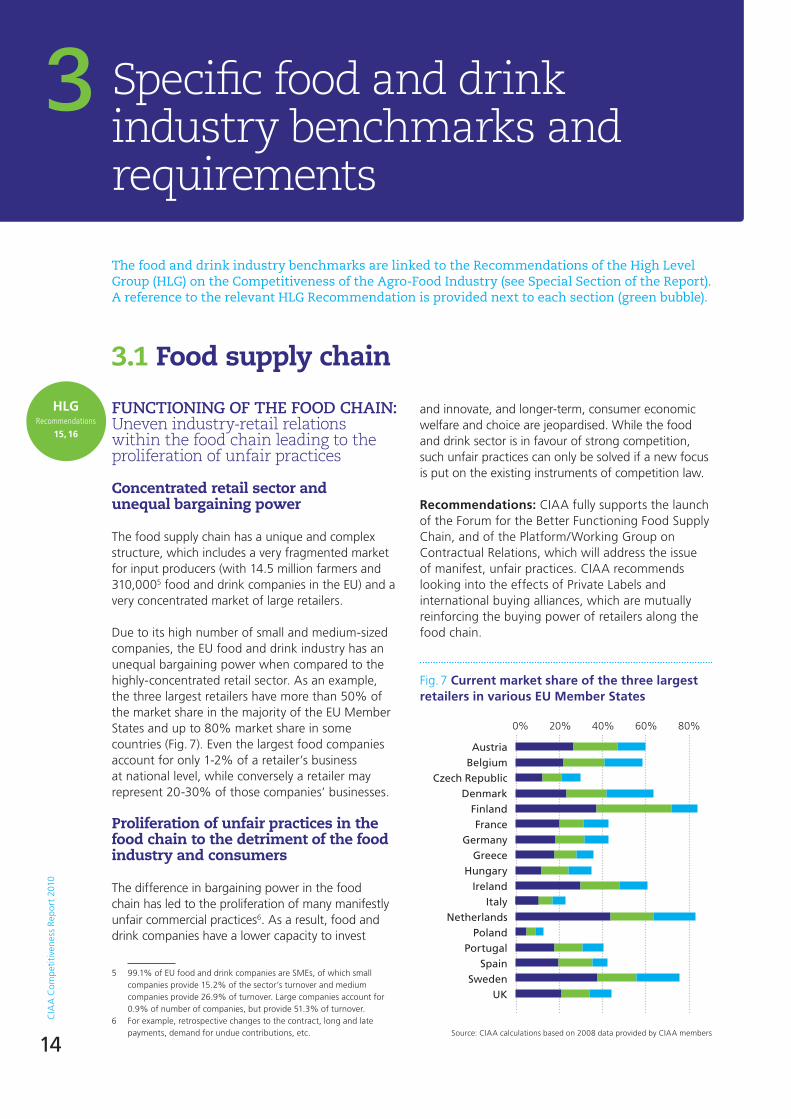

FUNCTIONING OF THE FOOD CHAIN: Uneven industry-retail relations within the food chain leading to the proliferation of unfair practices

Concentrated retail sector and unequal bargaining power

The food supply chain has a unique and complex structure, which includes a very fragmented market for input producers (with 14.5 million farmers and 310,0005 food and drink companies in the EU) and a very concentrated market of large retailers.

Due to its high number of small and medium-sized companies, the EU food and drink industry has an unequal bargaining power when compared to the highly-concentrated retail sector. As an example, the three largest retailers have more than 50% of the market share in the majority of the EU Member States and up to 80% market share in some countries (Fig. 7). Even the largest food companies account for only 1-2% of a retailer’s business at national level, while conversely a retailer may represent 20-30% of those companies’ businesses.

Proliferation of unfair practices in the food chain to the detriment of the food industry and consumers

The difference in bargaining power in the food chain has led to the proliferation of many manifestly unfair commercial practices6. As a result, food and drink companies have a lower capacity to invest

5 99.1% of EU food and drink companies are SMEs, of which small companies provide 15.2% of the sector’s turnover and medium companies provide 26.9% of turnover. Large companies account for 0.9% of number of companies, but provide 51.3% of turnover.

6 For example, retrospective changes to the contract, long and late payments, demand for undue contributions, etc.

Fig. 7 Current market share of the three largest retailers in various EU Member States

Source: CIAA calculations based on 2008 data provided by CIAA members

AustriaBelgium

Czech RepublicDenmark

FinlandFrance

GermanyGreece

HungaryIreland

ItalyNetherlands

PolandPortugal

SpainSweden

UK

0% 20% 40% 60% 80%

the food and drink industry benchmarks are linked to the Recommendations of the High Level Group (HLG) on the Competitiveness of the Agro-Food Industry (see special section of the Report). A reference to the relevant HLG Recommendation is provided next to each section (green bubble).

3

CIA

A C

ompe

titiv

enes

s Re

port

201

0

15

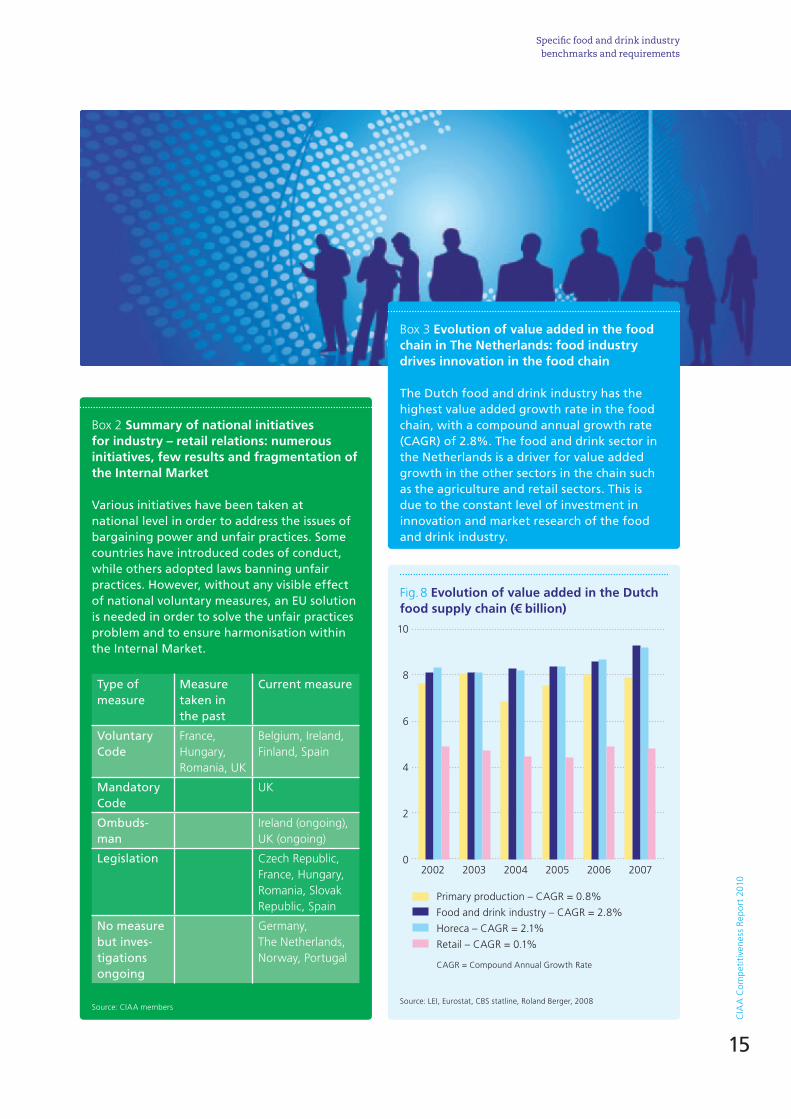

Box 2 Summary of national initiatives for industry – retail relations: numerous initiatives, few results and fragmentation of the Internal Market

Various initiatives have been taken at national level in order to address the issues of bargaining power and unfair practices. Some countries have introduced codes of conduct, while others adopted laws banning unfair practices. However, without any visible effect of national voluntary measures, an EU solution is needed in order to solve the unfair practices problem and to ensure harmonisation within the Internal Market.

Type of measure

Measure taken in the past

Current measure

Voluntary Code

France, Hungary, Romania, UK

Belgium, Ireland, Finland, Spain

Mandatory Code

UK

Ombuds-man

Ireland (ongoing), UK (ongoing)

Legislation Czech Republic, France, Hungary, Romania, Slovak Republic, Spain

No measure but inves-tigations ongoing

Germany, The netherlands, norway, Portugal

Source: CIAA members

Box 3 Evolution of value added in the food chain in The Netherlands: food industry drives innovation in the food chain

The Dutch food and drink industry has the highest value added growth rate in the food chain, with a compound annual growth rate (CAGR) of 2.8%. The food and drink sector in the Netherlands is a driver for value added growth in the other sectors in the chain such as the agriculture and retail sectors. This is due to the constant level of investment in innovation and market research of the food and drink industry.

10

8

6

4

2

02002 2003 2004 2005 2006 2007

Primary production – CAGR = 0.8%

Food and drink industry – CAGR = 2.8%

Horeca – CAGR = 2.1%

Retail – CAGR = 0.1%

CAGR = Compound Annual Growth Rate

Fig. 8 Evolution of value added in the Dutch food supply chain (€ billion)

Source: LEI, Eurostat, CBS statline, Roland Berger, 2008

specific food and drink industry benchmarks and requirements

CIA

A C

ompe

titiv

enes

s Re

port

201

0

16

PRIVATE LABELS: The dual role of retailers and the misuse of Private Labels

Facts: The increase in Private Labels (PL) gives rise to a series of issues, of which the ‘dual agent’ role where the retailer is both the customer and competitor is one of the most critical. Various negative effects can be seen, such as the effect on consumer choice and on prices, which are already evident today. Intra-brand and in-store competition are also hampered, which triggers similar concerns.

Recommendations: While policy-makers are examining the impact of Private Labels, CIAA calls on them to examine in particular the dual role of retailers on competitive practices across the food chain.

Switzerland

UK

Germany

Spain

Belgium

France

The netherlands

Australia

Canada

US

Italy

Japan

2013 (f) 2007

Fig. 9 Private Labels’ market share (value) 2007-2013 (f*) (%)

Source: Planet Retail, 2009

0 5 10 15 20 25 30 35 40 45

HLG Recommendation

16

Table 3 Private Labels’ share of world’s top retailers by retail banner sale

Ran

k

Co

mp

any

Priv

ate

lab

el

shar

e 20

07 (%

)

Priv

ate

lab

el

shar

e 20

08 (%

)

Ch

ang

e 08

/07

1 Wal-Mart 38 39

2 Carrefour 35 36

3 Metro Group 17 18

4 Tesco 48 50

5 Schwartz Group 61 60

6 Seven&I* 28 30

7 Target 15 16

8 Costco 16 18

9 Auchan 25 25

10 Kroger 25 26

11 Aldi 94 89

12 Safeway 25 25

13 SuperValu 18 16

* includes consolidated operations only

Source: Planet Retail ltd www.planetretail.net, “Economic Downturn spurs on

sophisticated private labelling”, Press release, 11 February 2009

*f = forecast

CIA

A C

ompe

titiv

enes

s Re

port

201

0

17

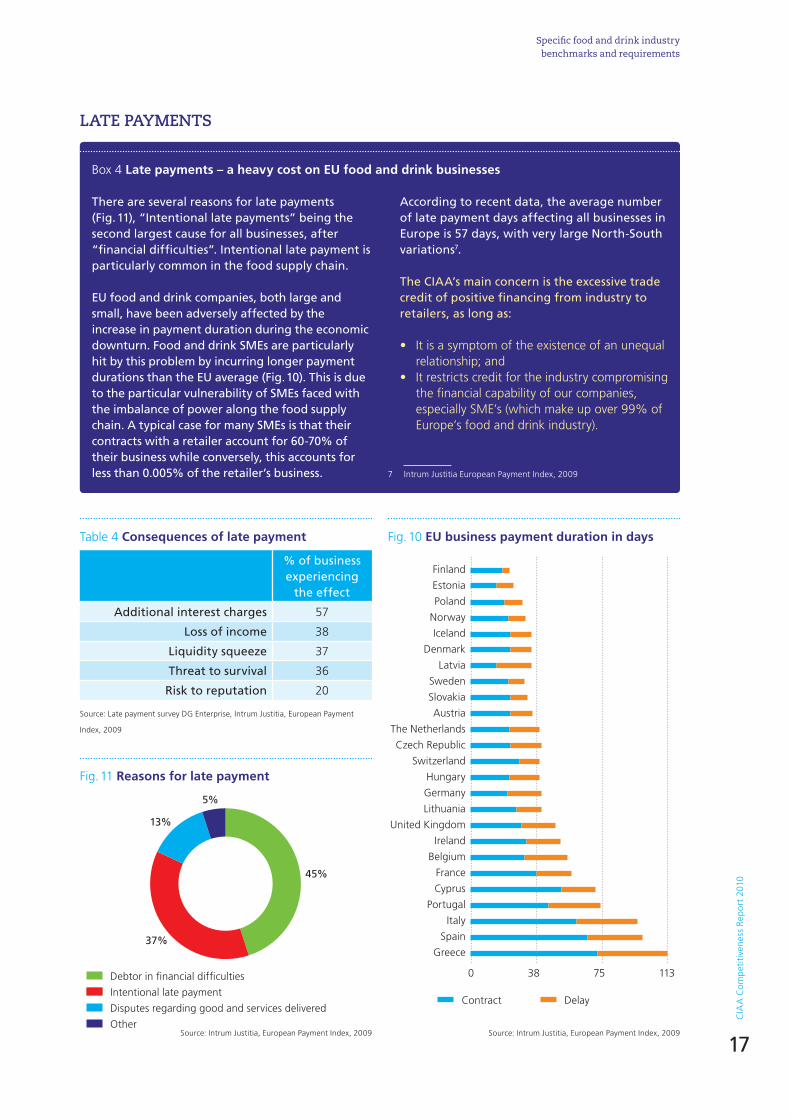

Table 4 Consequences of late payment

% of business experiencing

the effect

Additional interest charges 57

Loss of income 38

Liquidity squeeze 37

Threat to survival 36

Risk to reputation 20

Source: Late payment survey DG Enterprise, Intrum Justitia, European Payment

Index, 2009

Finland

Estonia

Poland

norway

Iceland

Denmark

Latvia

Sweden

Slovakia

Austria

The netherlands

Czech Republic

Switzerland

Hungary

Germany

Lithuania

United Kingdom

Ireland

Belgium

France

Cyprus

Portugal

Italy

Spain

Greece

0 38 75 113

Contract Delay

Fig. 10 EU business payment duration in days

Source: Intrum Justitia, European Payment Index, 2009

Fig. 11 Reasons for late payment

Source: Intrum Justitia, European Payment Index, 2009

Debtor in financial difficulties

Intentional late payment

Disputes regarding good and services delivered

Other

45%

37%

13%

5%

LATE PAYMENTS

Box 4 Late payments – a heavy cost on EU food and drink businesses

There are several reasons for late payments (Fig. 11), “Intentional late payments” being the second largest cause for all businesses, after “financial difficulties”. Intentional late payment is particularly common in the food supply chain.