8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 1/15

Savills Research | Residential Autumn 2011

SavillsResearch

savills.co.uk/research

PrimeCentral LondonResidentialSpotlight

Six years of volatility A performance review2005 to 2011

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 2/15

Ths pblcto

This document was published in October 2011. It contains a review o all the key housing market

indicators and news to the end o September 2011. The data used in the charts and tables is the

latest available at the time o going to press. Sources are included or all the charts. We have used a

standard set o notes and abbreviations throughout the document.

Glossr o trms

nMstrm: mainstream property reers to the bulk o the UK housing market with, or example,

price movements monitored by reerence to national and regional average values.

nPrm: the prime market consists o the most desirable and aspirational property by reerence to

location, standards o accommodation, aesthetics and value. Typically it comprises properties in

the top ve per cent o the market by house price.

nThe Savills PCL index ocuses on resale properties so average values given in this document donot refect the prices being achieved or some o the very high quality new build schemes in core

prime central London locations.

nPCL = Prime central London

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 3/15

“Prime central London’sresidential stock hasseparated into grades.”Savills Research

Svlls Rsrch | Prime Central London Residential 2005/2011

Wh w strt

th prm ctrl

Loo x

th lt 1970s, w

s tht ‘prm’

ws th bst proprt th bst

loctos. Lttl col w hv

thoght t th tm how mch ths

prm mrkt wol chg

sbsqt cs.

When I started analysing property

markets in the 1980s, prime London

centred around Knightsbridge.

The markets o South Kensington,

Chelsea and Belgravia were its‘acolytes’ while Mayair (now the

star perormer o ultra prime) and

Kensington were distinctly ‘ringe’.

Most o Notting Hill and Marylebone

was denitely ‘beyond the ringe’.

The Savills prime London index has

thereore changed and expanded

over the years to refect these new

prime geographies.

What we have seen is the real

estate equivalent o the continuous

replacement o old companies with

new ones within the FT100 share

index to refect the share prices o onlythe biggest companies. In 2010, we

replaced our old sample o lower grade

properties with higher grade ones.

The ongoing reurbishment and

renewal o stock means a property

that might have been highly desirable

in the 1980s simply doesn’t cut the

mustard now. Prime central London’s

residential stock has separated into

grades, an evolution that has had as

proound an eect as the physical

expansion o prime central London.

Last year we changed our sampleo index properties to refect this.

Dark basement fats and second-

foor walk-ups disappeared and

we increased the weighting o now

more numerous lateral conversions,

reurbished, high quality and new

developments that have changed the

ace o certain neighbourhoods – and

in many ways changed the nature o

what we now call prime.

These ‘grade A starred’ properties

are among the World Class property

‘gold standard’. In seeking to

understand the prime central London

market it is important to understand

the divergent perormances o the

dierent grades. Lucian Cook’s

excellent new analysis (page 8)

reveals the huge disparity betweenthe perormance o top grade and

lower grade properties.

It is this disparity in perormance that

has led us to review retrospectively

and re-state our prime central London

index, using the 2010 sample and

rebasing it at 100 in June 2005. This

was a relatively stable date in the

otherwise volatile market o the last

decade and a good place at which to

base our review o the last six years.

Replacing our old sample with the

new, ‘upgraded’ sample rom this date

has had the eect o liting the index tonew heights.

Like the shares within the FT 100

share index, the sample o properties

within the Savills indices will continue

to change in order to refect the

changing nature o the prime London

market. Our analysis o the market

rom the point o view o grades, as

well as location; looking at values,

not just prices; and considering all

stock, not just traded properties, has

given us a multidimensional view o

the market. This helps us to makesense o the, sometimes surprising,

market movements o the last ew

years and the nature o the market

going orward. n

Foreword

HiGH fLyeRS

GeT an uPGRade

The Savills prime London index has changed andexpanded over the years to refect the new primegeography o London’s gold standard property

yol Brs

Head o Residential

Research020 7409 8899

Contents04 Evolution and expansion

06 Six years o volatility

08 A divergence in perormance

10 All prime but not all equal

12 Prime Central London ranking

14 What lies ahead or PCL?

www.savills.co.uk/research 03

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 4/15

04

Market prole

evolution and

expansion

While the boundaries o prime have extendedbeyond central London, areas such asKnightsbridge and Belgravia remain at its core

th s rm r

l h

h 80

mr y h

10 r f h

mrk by , h mrk

fr h ’ b r

r h b g

g r .

Average values o the properties in

our index stood at around £176,000

when the index launched and now

exceed £4 million. What we frst

described as ‘prime’ defned the best

property in the best neighbourhoods

o core central London.

As such locations have increasingly

become the domain o international

owners and a store o global wealth,

so more central London property and

locations have achieved prime status.

In the early 80s only certain roads

or properties in then ringe central

London locations such as Notting Hill

were considered prime, but by the late

Noughties the bulk o housing stock

in the better roads had graduated to

‘prime’ status.

As international equity has colonised

portions o prime central London, so

domestic wealth has been displaced

into new areas, extending the

■Over the past six years to the end o June 2011,

prime residential property prices in central Londonrose by 87%, even accounting or the downturn

o 2008. This growth compares to an average o

just 25% across the residential stock o London

as a whole.

■Within the prime market the variance in

perormance has been signifcant. The top 10%

o properties by price growth rose by 151%.

The bottom 10% rose by just 42%. Much o the

variation relates to the period rom June 2005 to

June 2011 when price growth varied rom 33%

to 99%, though post downturn growth has varied

rom 31% to 54%.

■While the variation between value per sq t was

modest in 2005, it has widened considerably as

dierent parts o the market have responded to

dierent demand drivers. As a result the premium

or scale has widened with units over 5,000 sq t

averaging over £2,300 per sq t and those below

1,000 sq t averaging less than £1,350 per sq t.

■The highest growth has been seen by prime

property in Mayair, a market which has risen up

the rankings to deliver values competing with

Knightsbridge and Belgravia.

■St John’s Wood has been more o a slow burner,with growth in line with the wider central London

residential market but below the average or prime

property in the area.

■Looking orward, we do not anticipate a repeat

o the extraordinary growth o the past six years.

Nonetheless we expect prime property in central

London to lead the housing market recovery.

■We expect the nature o the prime market to

continue to change as the organic expansion o

prime central London accelerates in response to

demand rom new sources o global wealth.

executive suMMaRY

The key ndings in this issue

“Within the prime marketthe variance in perormance

has been signicant.”Savills Research

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 5/15

s Rrh | Prime Central London Residential 2005/2011

savills.co.uk/research 05

“A location-sensitive and

property-sensitive, ultra primemarket has emerged.”Lucian Cook, Savills Research

boundaries o prime beyond central

London. Swathes o south-west

London have been gentrifed and

‘primed’. First locations such

as Fulham and, more recently,

areas such as Clapham and

Wandsworth. New developments

have oten played their part in

extending prime boundaries or, as

with Wapping and Canary Whar,

created new prime markets. But,

without doubt, it is central London

that remains core prime.

cr l yTwo boroughs, Kensington and

Chelsea and the City o Westminster,

contain just 6.3% o London’s housing

stock but account or 15.6% o its

value. Each hectare o Kensington and

Chelsea has on average more than

£50 million o housing stock and that

despite all the parks and green spaces

within the borough.

Other boroughs across prime

central London do not have the same

concentration o high value residential

real estate and the depth o the

prime market varies signifcantly rom

neighbourhood to neighbourhood.

Within core locations such as

Knightsbridge and Belgravia the

prime market is at its deepest. Away rom these areas the prime

market is more diluted, and there is

considerable variation in the nature

o housing stock.

Dierent grades o prime have

developed which have reacted

dierently to the volatile market orces

o the past six years. In this report we

explain how the importance o grade

has increased. Growth in prime central

London values has been signifcant

over the period, even accounting or

the downturn o 2008. But our new

analysis demonstrates that averagestell only part o the story.

A location-sensitive and property–

sensitive ultra prime market has

emerged where addresses matter.

Certain markets, such as those

in Mayair, have risen rapidly up the

rankings in the past six years. Others,

such as St John’s Wood, are yet to

achieve quite such ashionable status

MAP 1.1

arg r l (r £750,000) Values refect the depth o the prime market

and have seen much lower growth

and arguably, thereore, have greater

potential or mid term growth.

Other locations which saw

gentrifcation and associated huge

value growth in the 90s, such as

Kensington and Holland Park, were

less responsive to the growth drivers

o 2006/07 than prime central London

as a whole. Subsequently they were

more aected by the downturn and

less responsive to recovery drivers.

Against this context we have

conducted a detailed review o the

composition o our prime central

London index and the perormance

o individual properties within it.

This has allowed us to urther our

understanding o the market and itsdiversity and nuances. Our fndings

are detailed in the ollowing pages ■

Data source: Land Registry / Savills Research

£1.5m b

£1.0m £1.5m

£750k £1.0m

arg pr

Hyde Park

Regent’s Park

Rg’ prk

creates value hotspot

Myfr has developed

as a prime location over

the past six years

Kghbrg and

Bgr remain core

locations or overseas

investment

s Jh’ W yet to

maximise value potential

Kg and Hprk less responsive to

growth drivers since 2005

R i v e r T h

a m e s

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 6/15

06

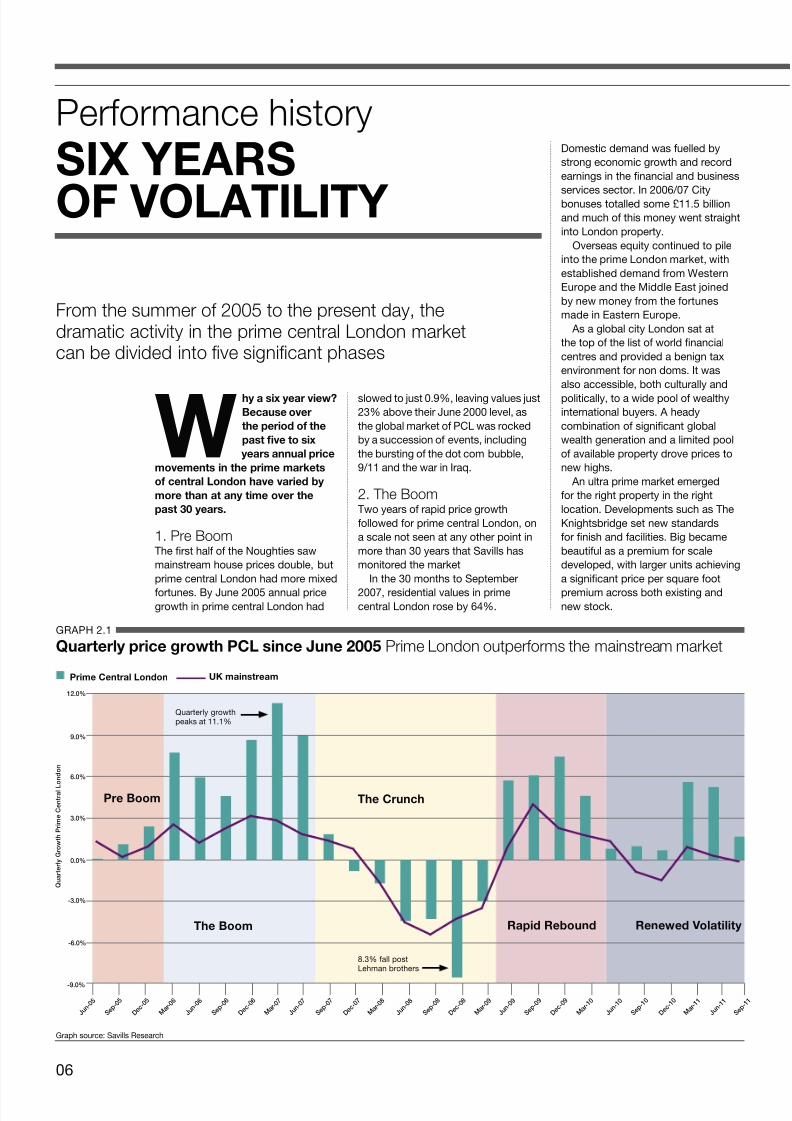

Perormance history

Six YearS

o volatilitY

From the summer o 2005 to the present day, thedramatic activity in the prime central London marketcan be divided into fve signifcant phases

Why s y w?

Bcus

h pd h

ps f s

ys nnu pc

mmns n h pm mks

cn lndn h d by

m hn ny m h

ps 30 ys.

1. Pre BoomTe st al o te Nougties saw

mainsteam ouse pices double, but

pime cental London ad moe mixed

otunes. By June 2005 annual picegowt in pime cental London ad

Domestic demand was uelled by

stong economic gowt and ecod

eanings in te nancial and business

sevices secto. In 2006/07 City

bonuses totalled some £11.5 billion

and muc o tis money went staigt

into London popety.

Oveseas equity continued to pile

into te pime London maket, wit

establised demand om Westen

Euope and te Middle East joined

by new money om te otunes

made in Easten Euope.

As a global city London sat at

te top o te list o wold nancial

centes and povided a benign tax

envionment o non doms. It was

also accessible, bot cultually and

politically, to a wide pool o wealty

intenational buyes. A eady

combination o signicant global

wealt geneation and a limited pool

o available popety dove pices to

new igs.

An ulta pime maket emeged

o te igt popety in te igt

location. Developments suc as Te

Knigtsbidge set new standads

o nis and acilities. Big became

beautiul as a pemium o scale

developed, wit lage units acieving

a signicant pice pe squae oot

pemium acoss bot existing andnew stock.

slowed to just 0.9%, leaving values just

23% above tei June 2000 level, as

te global maket o PCL was ocked

by a succession o events, including

te busting o te dot com bubble,

9/11 and te wa in Iaq.

2. The BoomTwo yeas o apid pice gowt

ollowed o pime cental London, on

a scale not seen at any ote point in

moe tan 30 yeas tat Savills as

monitoed te maket

In te 30 monts to Septembe

2007, esidential values in pimecental London ose by 64%.

GrAPh 2.1

Quy pc gwh PCl snc Jun 2005 Prime London outperorms the mainstream market

Gap souce: Savills reseac

J u n - 0 5

S e p - 0 5

D e c - 0 5

M a r

- 0 6

J u n - 0 6

S e p - 0 6

D e c - 0 6

M a r

- 0 7

J u n - 0 7

S e p - 0 7

D e c - 0 7

M a r

- 0 8

J u n - 0 8

S e p - 0 8

D e c - 0 8

M a r

- 0 9

J u n - 0 9

S e p - 0 9

D e c - 0 9

M a r

- 1 0

J u n - 1 0

S e p - 1 0

D e c - 1 0

M a r

- 1 1

J u n - 1 1

S e p - 1 1

-6.0%

-3.0%

0.0%

3.0%

6.0%

9.0%

12.0%

-9.0%

Pm Cn lndn UK mnsm

Q u a r t e r l y G r o w t h P r i m e C e n t r a l L

o n d o n

P Bm

Quately gowtpeaks at 11.1%

8.3% all postLeman botes

th Cunch

rpd rbund rnwd vyth Bm

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 7/15

Ss rsch | Pime Cental London residential 2005/2011

savills.co.uk/eseac 07

“It is unlikely that we have seen the end o

price volatility even though the undamentalslook sound in the medium term.”

Yolande Barnes, Savills Research

3. The CrunchTe cedit cunc bougt tis

dizzying gowt to an adupt alt.

As City eanings and employment

secuity plummeted and te wealt

o te intenational elite was eoded,

so tansaction levels ell damaticallyand buye condence in te

undelying wot o cental London

popety waned. Values ell 21% in

just 18 monts, ecoding a single

quate all o 8.3% in te wake o te

Leman Botes collapse.

4. Rapid ReboundIn Mac 2009 pospects looked bleak

and ew commentatos anticipated

te tunaound to come – as a

staggeing pice gowt o 25.5%

occued in just 12 monts.

Te excange ate advantage tataccompanied te weakness in te UK

economy was a stong ealy catalyst

o oveseas investment, mioing

wat ad been seen ate pevious

maket downtuns.

Pime cental London esidential

popety came to be viewed as a

distinctly sae aven o intenational

wealt and an attactive altenative

to gold. Even te intoduction o a

non doms levy ad little i any impact

on sentiment.

Economic uncetainty in te

Euozone dove wealt to te makettoug 2009 and 2010. Demand

came om acoss Westen Euope,

but most notably om Italy as a tax

amnesty at ome tiggeed an infux

o Italian money eleased om Swiss

bank accounts, and om Geece,

as it became evident tei domestic

economy was singled out as te

most likely to deault.

Te ebuilding o global wealt onte back o stong commodity makets

pumped moe equity into cental

London. By 2010/11 bot te numbe

and collective wealt o US dolla

billionaies ad isen above its 2007/08

level accoding to Fobes.

In bie, demand om tose looking

to potect existing wealt was again

joined by tose looking to invest new

money eaned lagely outside o te

westen economy.

A unnelling o demand allowed

new luxuy developments to take

advantage o a sotage o top endnew build stock. New developments,

most notably One hyde Pak, ave

done muc to ewite te istoy o

pime cental London, and even in te

wake o te cedit cunc new ecods

o picing wee being set.

5. Renewed Volatility Volatility in pice gowt as been

one o te key eatues o te pime

cental London maket in te past six

yeas and was expected to impact

negatively on values ealy tis yea.

Te second al o 2010 saw pice

gowt slow on te tail o a secondslip in UK mainsteam pices, but

signicant pice gowt etuned,

unexpectedly, to London in te st

two quates o 2011.

Te ‘sae aven eect’ as

been ute einoced by political

uncetainty in te Middle East,

attacting buyes om a egion

long-amilia wit cental London,

wile continued uncetainty in te

Euozone as ute enanced

London’s appeal elative to ote

Euopean capitals.

heigtened concens ove teglobal economy and te eosion

o wealt eld in te wold’s stock

makets could test te ‘sae aven’

eect on values, and impact on

undelying demand.

It is unlikely tat we ave seen te

end o pice volatility even toug

te undamentals look sound in te

medium tem. n

In Eaton Squae,pice gowt asaveaged 130% ovete past six yeas,compaed to a PCLaveage o 87%.

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 8/15

08

Market segmentation

a divergence

in perormance

Value growth across the many different grades of prime central London residential real estate has varieddramatically, with ultra-prime property blazing a trail

Wht sttuts

‘’ s

stt stt

fux. dt

lts

ty tys wth

tl L s y

tly t t s,

whh ulttly sults th

y t

s ty.

Nw, dtaild analysis o th

individual omanc o ach

oty in th Savills im cntal

London indx nabls us to valth xtnt o th divgnc in

omanc btwn th dint

accoding to ic gowth w can s

th divgnc btwn th bst and

th st, analysis that highlights th

imotanc o looking byond

th avag.

Btwn Jun 2005 to Jun 2011

th to 10% o otis dlivd

ic gowth o 151%. At th oth

nd o th scal, th bottom dcil

oducd lss than a thid o this

agggat gowth, at just 42%.

Th gowth codd by th

to and bottom dcils vais

considably om th st o th

saml – thy could b considd

xtms comad to th st o th

saml wh gowth is mo closly

goud. But th signifcant vaiation

in omanc is not confnd to

vy bst and vy wost. Gowth

o th scond bst oming 10%

o otis is still twic that o th

scond wost oming 10%, at

119% comad to 60%.

Wh why A study o ic gowth in th ky

iods vals how that divgnc

has built u.

1 Pre crunch: Jun 05-Sep 07Much o th divgnc in ic

gowth omanc occudduing th initial iod o damatic

ic gowth.

locations and dint gads o

oty in th caital.

On manistation o this has bn

th outomanc by th to nd

o th makt. In th six yas to

Jun 2011 th valu o ulta im

otis in th Savills indx os

by 107%, against an avag 87%

gowth acoss th im cntal

London as a whol.

By th sHadlin gowth fgus ovid a

guid to th avag, but ou nw

analysis vals th ull xtnt o thvaiation aound that avag. By

dividing ou indx into tn qual ats

GrApH 3.1

d ss p ctl

Gah souc: Savills rsach

J u n - 0 5

S e p - 0 5

D e c - 0 5

M a r

- 0 6

J u n - 0 6

S e p - 0 6

D e c - 0 6

M a r

- 0 7

J u n - 0 7

S e p - 0 7

D e c - 0 7

M a r

- 0 8

J u n - 0 8

S e p - 0 8

D e c - 0 8

M a r

- 0 9

J u n - 0 9

S e p - 0 9

D e c - 0 9

M a r

- 1 0

J u n - 1 0

S e p - 1 0

D e c - 1 0

M a r

- 1 1

J u n - 1 1

70

90

110

130

150

170

190

210

230

250

50

T 10% Btt 10%

V a l u e

I n d e x

( J u n

2 0 0 5

= 1

0 0

)

To 10% o saml showssix ya gowth o 151%

Bottom 10% o saml showssix ya gowth o 42%

rang o th maining saml om 60% to 119%

100

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 9/15

Slls rsh | pim Cntal London rsidntial 2005/2011

savills.co.uk/sach 09

Th ofl o dmand damatically

changd, and th makt sondd

aidly and sggatd to th

gatst dg. pics os by

a thid in th bottom dcil but

doubld in th to dcil.

2 Market crash: Sep 07-Mar 09Th subsqunt iod o ic

alls oducd much low lvls

o vaianc, anging om 24% alls

among som o th wost oms

to 18% alls in th sgmnts that had

omd bst io to th downtun.

No location o oty ty was

immun to alls.

3 Recovery: Mar 09-Jun 11Sinc Mach 2009 omanc

has vaid much lss, though th

has bn idntifabl nwd

outomanc in th to 30%

o th saml.

Th bound has bn divn by

ovsas dmand and otis

ftting th ofl o that dmand hav

ld th way.

Looking owad a combination

o global conomic and social

actos will dtmin whth w

a nting a iod o low gowth

o nwd volatility. Whichv, a

continuation o th signifcant gowthsn in th ast 18 months sms

unlikly in th shot tm. n

TABLe 3.1

Th sx-y wth tl

Data souc: Savills rsach

a more

diScerningmarkeT

On o th main consquncs

o this divgnc is that th

is much gat vaiation in th

valus o dint otis in

dint locations.

In Jun 2005, th avag

ic o otis within tn

sgmnts o th makt angd

om £850 to £1,000 squa

oot. By Jun 2010, that ang

had ond u to £1,400 to£2,350 squa oot o th

to 10% o th makt.

Undstanding ths

dincs is citical to

thos invsting in this

makt. In th ight locations

th gatst ootunitis

to add valu com though

ubishmnt, modifcation and

th amalgamation o otis

to cat th holy gail - scal.

Fo dvlos, a ailu to

match oduct to dmand, by

cating duability o quality andamnitis, will os isks.

Th t ts

th t

Ttl sx y

wth t Ju 2011

p wth by

Ju 05 - St 07 St 07 - m 09 m 09 - Ju 11

Top 10% 151% 98% -18% 54%

2nd Decile 119% 82% -18% 47%

3rd Decile 108% 71% -19% 49%

4th Decile 98% 78% -23% 45%

5th Decile 90% 70% -19% 38%

6th Decile 83% 65% -22% 42%

7th Decile 75% 57% -24% 47%

8th Decile 68% 53% -21% 40%

9th Decile 60% 46% -23% 44%

Bottom 10% 42% 33% -19% 31%

Average 87% 64% 20.3% 43%

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 10/15

10

PCL performance

all prime but

not all equal

Prime houses in central Londonhave comfortably outperformed theremainder of the market. But whatlessons can be learnt from both the

best and the worst performers?

th c

dvd y

w dd y

d cs, sch

s c, y

y d sz, y dc,

y fsh d c d

gs hs.

These actors combined determine

whether a property is attractive to

the deepest and strongest strands

o demand and how it is judged, and

thereore priced, relative to competing

stock on the market.

Houses in prime central London

have substantially outperormed, with

average price growth o 92% in the

six years to June 2011. This compares

to an average price growth o 69%

across all residential sales in theboroughs o Kensington & Chelsea

and City o Westminster, as recorded

by the Land Registry.

While average growth or prime ats

is much more in line with the market as

a whole at 84%, there are clear sectors

o the ats market that have perormed

particularly strongly.

By studying the distribution o the

properties in the top and bottom

25% o our sample, we can build an

understanding o what has separated

the best and worst perorming.

The top perormer over the pastsix years has been Mayair, where

average prices have risen by 117%,

such that it is now competing with

some o the highest value locations

in central London. This is ollowed by

Marylebone at 107%, which remains

a slightly less mature market. Mayair

in particular has seen a signifcant

level o new capital investment and,

on the back o improved amenities or

residents, has the greatest share o

properties within the top perorming

quartile o our sample.By contrast, lowest placed St

John’s Wood saw average values rise

by only 69% in the six year period

and has 56% o its properties in the

bottom perorming quartile o our

sample. This suggests an area with a

greater mix o property grades, and

one with potentially greater scope orgrowth over the next ew years.

my vMayair sits right at the top o the

high perormers league and a high

proportion o both ats and houses

there have shown strong growth.

Detailed analysis shows size really

matters. Large Mayair houses, in

excess o 10,000 square oot, in

locations close to the amous Berkeley

and Grosvenor Squares (eg. Charles

Street, Hill Street and Upper Brook

Street), witnessed some o the highest

price growth, averaging 150%.

Average values or such properties

have risen to between £2,500 and

£3,000 per square oot, compared

to fgures o between £1,800 and

£2,500 per square oot or the best

perorming one and 2-bedroom ats,

in locations such as Mount Street.

The size phenomenon has been

repeated across prime central London.

The top 10% o properties by price

growth have been shown to be 29%

larger than the average or the sampleas a whole.

Kghsdg High proportions o ats within

Knightsbridge and Belgravia have

also eatured among the best

perormers. It is no coincidence

that these areas attract buyers rom

the Middle East / North Arica and

Eastern Europe / CIS regions to a

degree that is unmatched elsewhere

in central London.

Knightsbridge has become

a magnet or high net worthinternational buyers and a number o

high profle new build schemes have

broken all records.

The highest perorming ats in

Knightsbridge and Belgravia typically

all into two categories:

n Firstly, there are those developed

to meet the demands o the new

breed o ultra wealthy international

buyer. Flats in The Knightsbridge,

199 Knightsbridge, a new addition to

our index, are a good example. Here,

current values o between £3,500and £5,000 per square oot stand

head and shoulder above similar

sized traditional resale stock, and

are testament to a standard o

“The average price movement forMayfair properties is the greatest

of any over the period

from mid 2005 to mid2011.” Sophie Chick,

Savills Research

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 11/15

Svs rsch | Prime Central London Residential 2005/2011

savills.co.uk/research 11

fnish, range o amenities and level

o additional services that the more

traditional London stock cannot match.

Undoubtedly, however, as newluxury developments such as One

Hyde Park have broken new price

barriers, so values or the closest

comparable product have been

pulled up in their slipstream.

n Secondly, there are ats within the

most celebrated and aspirational

streets and squares where premiums

are well-established. Eaton Square,

where price growth has averaged

130% over the past six years, is a

perect example o this phenomenon.

th sw sBeyond the core o central London,

both the at and house markets o

St John’s Wood and Regent’s Park

have shown less aggressive growth

at around 75% on average across the

two areas over the past six years.

This relative perormance is

perhaps unsurprising, since they lie

to the north o central London, where

‘prime’ is less all-encompassing. This

results in a greater spread o values

and o quality o stock and location.

Elsewhere, a high proportion oKensington and Holland Park ats

are in the bottom quartile in terms o

price growth in the six years to mid

2011. These markets have seen less

high-value international demand

than core prime central London. In

the run up to the banking crisis they

relied more heavily on domestic

buyers employed in the fnancial

and business services sector. As a

result transactions were particularly

aected by the downturn.

Their dierent buyer profle is

also reected in much lower levelso investment and second home

purchase than in some o the top

perormers. Also, these areas have

seen ar lower levels o proft-driven

reurbishment and redevelopment

than the at markets in areas such

as Knightsbridge and Belgravia.

mk dsdgOver the past six years the depth and

nature o demand have dictated how

dierent properties have perormed

in a volatile market. Stock selectionhas been key to value growth in a

given location. All indications are that

this will continue to be the case. n

GRAPH 4.2

ics vg £ s y y sz

0 500 1,000 1,500 2,000 2,500

S i z e

o f p r o p e r t y

Average £ per sq ft

J 05 J 11

Data source: Savills Research (based on index valuation sample o resale properties)

Over 5,000 sq ft

4,000-5,000 sq ft

3,000-4,000 sq ft

2,000-3,000 sq ft

1,000-2,000 sq ft

Up to 1,000 sq ft

1,068

977

945

796

736

1,187 2,374

1,974

1,819

1,814

1,490

1,319

GRAPH 4.1

t cs kd y vg £ s s y

The core PCL locations of Knightsbridge and Belgravia continue to lead the rankings

It should be noted that the index ocuses on resale properties so the average values do not reect prices achieved or some

o the very high quality new build schemes. The limited pipeline has continued to apply upward pressure on the value o these

developments. Data source: Savills Research (based on valuation sample only)

1,039

1,023

902

898

928

904

848

825

826

608

2,007

1,982

1,960

1,713

1,672

1,601

1,593

1,558

1,393

1,256

Kghsdg1

bgv2

my3

Chs4

Ksg/Hd pk5

ShKsg6

rg’s pk7

ng H8

S Jh’s Wd9

my10

rank location Jun 05 Jun 11

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 12/15

12

Performance split

■T 25% t

■2 Qut

■3 Qut

■Btt 25% t

Market snapshot

prime cenTral

london rankings

Ranking prime central London real estate by six year price growthputs Mayfair in the lead, while Knightsbridge and Belgravia areahead in terms of £ per sq ft

T tb b

t

t t

l t

u

t bt Ju 2005

Ju 2011.

As performance varies dramatically

on a property by property basis, we

have examined the split of properties

in each location. In each case we

Locationrank

mayfair

maryleBone

Belgravia

knighTsBridge

chelsea

noTTing hill

regenT’s park

kensingTon/holland park

souTh kensingTon

sT. John’s wood

June 05 - June 11

117%

107%

94%

93%

91%

89%

88%

80%

77%

69%

£ per sq ft

1.960

1,256

1,982

2,007

1,713

1,558

1,593

1,672

1,601

1,391

performance

spLit

have looked at the percentage of

properties that fall into the four

quartiles of market by price growth.

So, for example, in Mayfair just

under 60% of properties were in

the top quartile by price growth. In

contrast, in St John’s Wood over 50%

of the properties were in the bottom

quartile but just 10% of properties

were in the top quartile. ■

1

2

3

4

5

6

7

8

9

10

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 13/15

s r | Prime Central London Residential 2005/2011

savills.co.uk/research 13

MAP 5.1

d t l b bu

st. J’ w

rt’ p

mb

m

B

c

ktb

sut kt

ntt h

kt/h p

1

107

2

34

5

9

86

Hyde

Park

Westminster

Battersea

Islington

King’s Cross

Paddington

Waterloo

Belsize Park

Queen’sPark

Hammersmith

Regent’sPark

N

S

E W

R i v e r T h a m e s

Fulham

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 14/15

14

Market outlook

what lies ahead for pcl?

Prime central London is set to outperorm the resto the UK housing market over the next fve years,but which areas are most likely to rise up the rankings?

w

mn

m n

lnn u

bu uu?

There are reasons to be confdent

that prime central London will

outperorm the rest o the UK housing

market over the next fve years, much

the same way as it has done in all

the early stages o previous housing

market cycles.

There is signifcant equity already

locked into the prime markets

meaning they are largely unshackledby the constraints o mortgage fnance

which dog the rest o us.

There are also urther prospects o

equity being introduced rom overseas

buyers, particularly rom emerging

economies. These have the greatest

o job losses in the banking sector all

contribute to the risk o slower growth

prices in the immediate uture.

Our index results or the third quarter

o 2011, show the immediate response

to these uncertainties has been slower

growth. Prices rose by 5.5% and 5.2%

in the frst and second quarters o 2011

respectively, but in the third quarter

they rose by 1.7%.

an ngng vunWill there be continued variation in

perormance? We believe so, i only

because ashions in prime property

change with almost the requency o

the seasons in haute couture.

The next set o winners and

losers will be determined by two key

drivers; the nature o demand and

buyer preerence in terms o product

and location.

Increased demand will almost

certainly continue to come rom newly

wealthy Asians and their preerences

will shape the market. Past evidence

shows this will accelerate the organic

extension o central London – already

underway in St James’ and ‘peripheral

Belgravia’ leading into northern Pimlico.

New demand is likely to avour new

developments which oer a superior

level o amenities and security. Suchdevelopments have the potential to

completely redefne areas – as has

been seen in Knightsbridge – or to

extend the boundaries o core prime.

The Lancasters may pave the way or a

greater international ocus on Bayswater,

while Chelsea Barracks is the one to

watch over the next ew years.

Ultimately, it is clear that the prime

London market will continue to evolve.

This will require our indices to evolve

with them as they approach their 40th

birthday over the next fve years. n

capacity to generate new wealth, and

have been seen to avour London as

a ‘sae haven’ store o wealth. There

is little to suggest they will cease to

view London in this way, especially

with global eyes on the 2012 Olympics.

Having said that, it would be unwise

to expect repeat levels o price growth

seen in the past fve years.

Recent price growth leaves London

looking near ull value in a global

context. Our World Cities review

suggests that it is second only to Hong

Kong in pricing among its peers.

Equally, uncertainty surrounds boththe global and domestic economy

meaning the potential wealth drivers

are more subdued. Domestic wealth

generated rom within the fnancial and

business services sector is likely to

underpin demand, but only as the UK

economy recovers. Uncertainty in the

UK economy will mean we have not

seen the end o the volatility that has

been a key eature o the market over

the period o this review.

Difculties in the economies o the

Eurozone and the US and the prospect

sv r m

Please contact us or urther inormation

Yn Bn

Head o Research

020 7409 8899

lun ck

Director

020 7016 3837

s ck

Analyst

020 7016 3786

sv Savills is a leading global real estate service provider listed on the LondonStock Exchange. The company established in 1855, has a rich heritage withunrivalled growth. It is a company that leads rather than ollows, and nowhas over 200 ofces and associates throughout the Americas, Europe, AsiaPacifc, Arica and the Middle East.

This report is or general inormative purposes only. It may not be published,reproduced or quoted in part or in whole, nor may it be used as a basis

or any contract, prospectus, agreement or other document without priorconsent. While every eort has been made to ensure its accuracy, Savillsaccepts no liability or any direct or consequential loss arising rom its use.The content is strictly copyright and reproduction o the whole or part o itin any orm is prohibited without written permission rom Savills Research.

“Ultimately, it is clear thatthe prime London marketwill continue to evolve.”

8/3/2019 Spotlight on Prime Central London Residential Oct 2011

http://slidepdf.com/reader/full/spotlight-on-prime-central-london-residential-oct-2011 15/15

sv r | Prime Central London Perormance 2005/2011

UnubbTo unsubscribe rom receiving this mailing please contact Jennier Lane

and we will ensure you are removed rom our database. I your details have

changed or they are incorrect please also contact Jennier Lane and we will

ensure these are amended.

Jennier Lane, Savills, Lansdowne House

57 Berkeley Square, London W1 6ER

T: 0207 016 3886 E: [email protected]

sv

Savills is a leading global real estate service provider listed on the London

Stock Exchange. The company established in 1855, has a rich heritage with

unrivalled growth. It is a company that leads rather than ollows, and now has

over 200 ofces and associates throughout the Americas, Europe, Asia Pacifc,

Arica and the Middle East.

This report is or general inormative purposes only. It may not be published,

reproduced or quoted in part or in whole, nor may it be used as a basis orany contract, prospectus, agreement or other document without prior consent.

While all eort has been made to ensure its accuracy, Savills accepts no liability

whatsoever or any direct or consequential loss arising rom its use.

The content is strictly copyright and reproduction o the whole or part o it in

any orm is prohibited without written permission rom Savills Research.

r ubnOur latest reports

n dvmn, invmn n N hm fu

n rn py fu

n ing | w c rv

For more inormation, visit savills.co.uk/research