Queensland Sustainable Lifestyle Horticulture Project

Final report

Feb 2008

Page 2Sustainable Lifestyle Horticulture Project – Final report Feb 08

Table of Contents

28Implementation rationale & funding10

30-31Implementation plan - Stakeholder responsibilities12

57Glossary16

17-18Urban landscape benefits3

56References15

26Opportunities and strategy rationale8

24-25Key issues and strategy implications7

19-20Product diversification4

38-55Support Appendices14

32-37Implementation plan13

29Alignment with existing programs11

27Vision Statement, value proposition and future role9

10-16Trends shaping the future • Water availability• Regulatory impact• Skills• Supply Chain dynamics • Stakeholder roles • Environmental awareness

2

22-23Export opportunities 6

21Regional development5

6-9Industry structure & profile1

Table of contents Page

Page 3Sustainable Lifestyle Horticulture Project – Final report Feb 08

Introduction

Project Background & Purpose

• Freshlogic has been commissioned by the Department of Primary Industries and Fisheries (DPI&F) to assist the lifestyle horticulture industry

adjust to the current challenges being experienced by businesses in the industry.

• This project is required to develop a strategic direction for the future sustainability, growth, and profitability of the lifestyle horticulture

industry.

Methodology

• This project is known as the Sustainable Lifestyle Horticultural Project and has drawn on the expertise of a support working group.

• All relevant available industry information was assessed, and a structured questionnaire (see page 51-51)was used to obtain detailed input

from both the working group and selected commercial enterprises. Based on the analysis of this information, the strategy planning

implications were identified, developed into a set of strategic planning outputs and then extended into an implementation plan.

Key Findings

• The lifestyle horticulture industry is made up of a diverse range of industries that span from primary production to retailing, and include the

provision of professional services. The larger sectors of the lifestyle horticulture industry - nursery and landscape - are characterised by high

numbers of smaller enterprises that are strong voices in industry associations.

• The changes in availability of water has adversely impacted the Queensland lifestyle horticulture market. It has created declines in both the

commercial landscape and home garden sectors, with the decline in plant use being a contributing factor. The market downturn has also

been impacted by longer term trends in domestic dwelling design, lower interest in gardening as a hobby by new home owners and reduced

levels of mainstream garden media. Based on the information available, the sum impact is a decline in market value of $260M or 18% of

market value for the year ending June 2007.

• Despite low or negative growth, there are still some positive demand signals from the market, many of which are related to increased

consumer awareness to environmental issues.

• Industry information levels are weak and methods to categorise and define market size, structure and supply chain value are evolving. As a

result, the levels of collaboration across industry sectors varies.

Page 4Sustainable Lifestyle Horticulture Project – Final report Feb 08

Introduction

Key Findings (Continued)

• While increased exports to Europe and Asia have been targeted, exports have declined in recent years. This decline has been impacted by

higher local labour costs, adverse exchange rates and technology and scale advantages being captured by competing exporters.

• One blanket set of improvement strategies will not work across all of Queensland. Regional variations will be required to ensure state wide

improvement.

• Despite challenging market conditions, some enterprises have diversified and generated growth. Capturing the capabilities of these

businesses is targeted in what is the cornerstone of growth strategy. This strategy is based on supporting those who are prepared to invest,

and in doing so, set examples for others to follow.

• Making alternative water sources available is a priority. Improved water availability will flow directly into stimulating consumption of lifestyle

horticulture products and services.

• Another priority is to communicate and gain acknowledgement of the environmental, health, psycho social and economic benefits that can be

attributed to urban landscapes. Indications are that awareness of these type of benefits is lifting, and the intent is to reach and influence

community decision makers. Another strategy will be seeking leverage from this awareness by developing packages of lifestyle horticulture

products and services that will satisfy the demand from enterprises and consumers to take action on sustainability.

• Value can also be added by cross sector collaboration. Specific strategies are proposed to consolidate the regulatory burdens on enterprises,

and to give greater scale and course range scope to skills and training providers. The latter is designed to reduce the risk of a longer term

skills gap.

• A total of $5.5m funding over 5 years is sought to implement these improvements, with 90% of these funds planned to be used in matching

the investments of those businesses who are prepared to invest in generating growth. It is also recommended that industry working groups

provide the human resources to manage other improvement strategies.

Page 5Sustainable Lifestyle Horticulture Project – Final report Feb 08

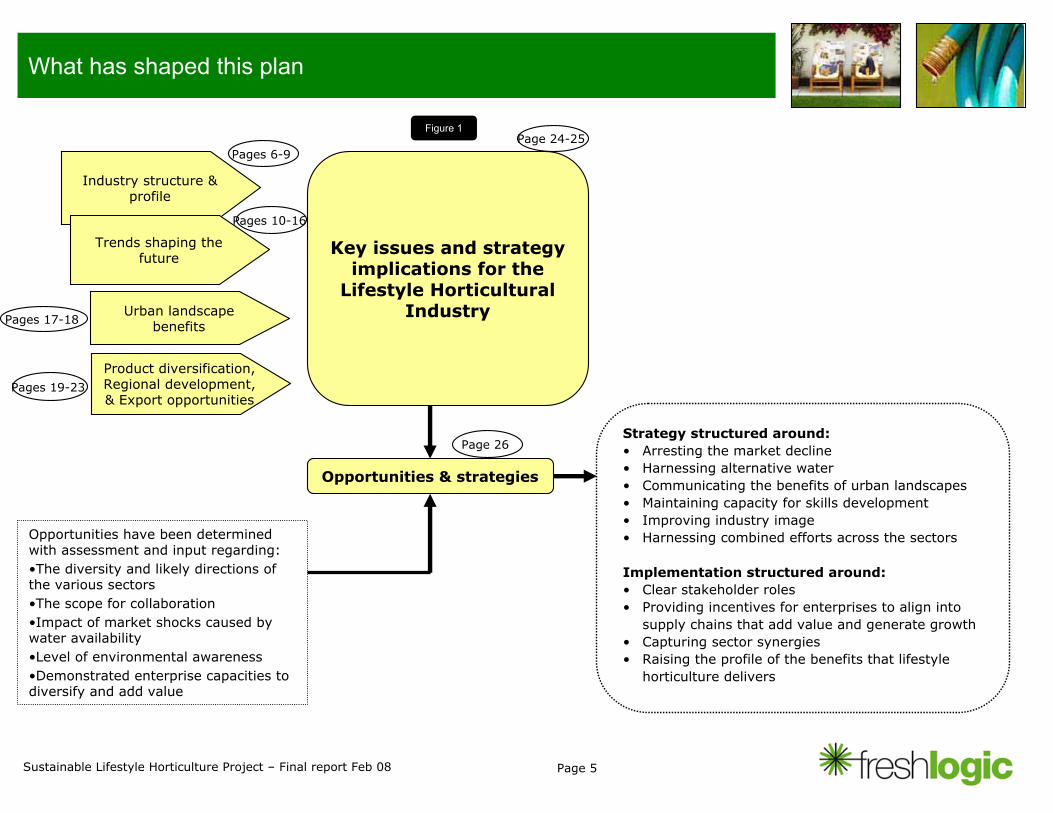

Industry structure & profile

What has shaped this plan

Trends shaping the future

Key issues and strategy implications for the

Lifestyle Horticultural Industry

Opportunities & strategies

Strategy structured around:• Arresting the market decline• Harnessing alternative water • Communicating the benefits of urban landscapes• Maintaining capacity for skills development• Improving industry image • Harnessing combined efforts across the sectors

Implementation structured around: • Clear stakeholder roles• Providing incentives for enterprises to align into

supply chains that add value and generate growth • Capturing sector synergies• Raising the profile of the benefits that lifestyle

horticulture delivers

Opportunities have been determined with assessment and input regarding: •The diversity and likely directions of the various sectors •The scope for collaboration•Impact of market shocks caused by water availability •Level of environmental awareness•Demonstrated enterprise capacities to diversify and add value

Product diversification, Regional development, & Export opportunities

Urban landscape benefits

Pages 6-9 Page 24-25

Pages 10-16

Pages 17-18

Pages 19-23

Page 26

Figure 1

Page 6Sustainable Lifestyle Horticulture Project – Final report Feb 08

Forestry & ProductionHorticulture

Nursery(A high level of inter

trading)

Industry structure & profile

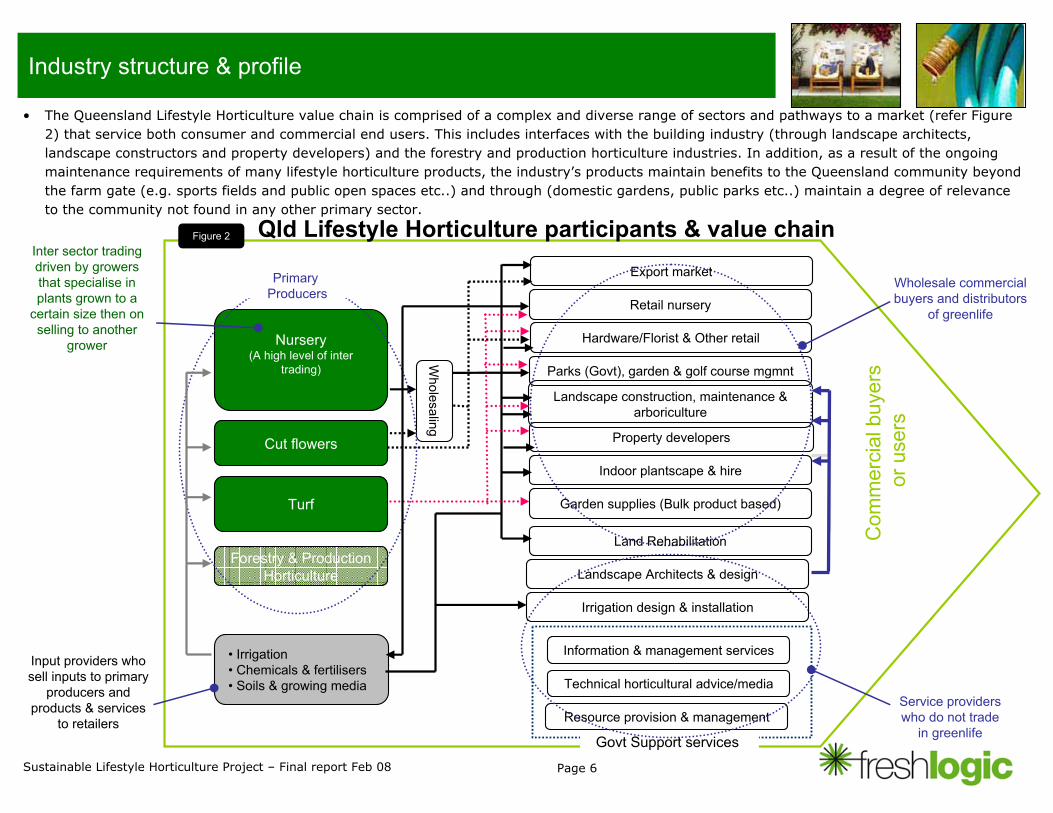

• The Queensland Lifestyle Horticulture value chain is comprised of a complex and diverse range of sectors and pathways to a market (refer Figure 2) that service both consumer and commercial end users. This includes interfaces with the building industry (through landscape architects, landscape constructors and property developers) and the forestry and production horticulture industries. In addition, as a result of the ongoing maintenance requirements of many lifestyle horticulture products, the industry’s products maintain benefits to the Queensland community beyond the farm gate (e.g. sports fields and public open spaces etc..) and through (domestic gardens, public parks etc..) maintain a degree of relevance to the community not found in any other primary sector.

Com

mer

cial

buy

ers

or u

sers

Turf

Cut flowers

Garden supplies (Bulk product based)

Landscape Architects & design

Indoor plantscape & hire

Parks (Govt), garden & golf course mgmnt

Retail nursery

Wholesaling

Landscape construction, maintenance & arboriculture

Govt Support services

Hardware/Florist & Other retail

Information & management services

Technical horticultural advice/media

Qld Lifestyle Horticulture participants & value chain

Resource provision & management

Property developers

• Irrigation • Chemicals & fertilisers• Soils & growing media

PrimaryProducers

Inter sector trading driven by growers that specialise in plants grown to a

certain size then on selling to another

grower

Service providers who do not trade

in greenlife

Input providers who sell inputs to primary

producers and products & services

to retailers

Wholesale commercial buyers and distributors

of greenlife

Export market

Figure 2

Land Rehabilitation

Irrigation design & installation

Page 7Sustainable Lifestyle Horticulture Project – Final report Feb 08

Industry structure & profile

High labour intensity

• The Australian lifestyle horticulture industry also faces potential competition from low-cost countries due to the advance of globalisationreflected in free trade agreements, and international capital and technology movements. Labour-intensive production sectors are particularly vulnerable to countries with relatively low-cost labour. This weakness is a core challenge when exploring international export markets for products.

Dominance of small family owned businesses

• The lifestyle horticulture industry is highly fragmented, comprising mostly of small to micro-businesses that operate independently. Many of these business owners entered the industry for lifestyle reasons. Such business structures and capabilities are generally not conducive to the development of export capabilities and value-added strategies, access to finance and marketing and product differentiation initiatives.

Domestic market focus and increasing level of imports

• The Queensland lifestyle horticulture industry currently exports on an opportunistic basis. An estimated 98 cents in every dollar of the industry’s gross sales are currently from domestic trade in Australia. Due to a high proportion of products sold into other states, the market conditions in each state - including water restrictions, drought conditions and gardening awareness - impact on the Queensland industry’s gross sales. Import trends reflect that increasing volumes of cut flowers are being imported to compete with locally produced product.

Steady growth until 2004-05

• Credible industry statistics are scant. Best information indicates that growth over the past 15 years has been steady at an average 6%+, with highs and lows being a reflection of optimum spring weather. During this time, the industry enjoyed the peak of lifestyle TV and the creation of the garden makeover concept, and a steady flow of new houses that required gardens and minimal restrictions on domestic water use in gardens. However, from 2005-06 (refer Figure 3), when lifestyle TV eased, new time-poor home owners appeared to have lost interest in gardening as an activity, new houses came with complete gardens and water restrictions commenced, the market slowed and then declined.

Garden market share movement

• As home gardeners have changed the way they purchase garden products, market share has moved away from retailers (who have beenservicing the DIY gardeners) to landscaper and property developers, who are supplying combinations of product and service. Within the retail supply channel, the large format hardware stores have rapidly expanded in the last 10 years and now dominate the retail market. The once dominant retail nurseries/garden centres are struggling in these conditions.

Synergies between sectors

• Synergies are strong in sectors that service public and private garden amenity needs. The products and services to meet these needs are commonly combined, and larger scale solutions are aligned in a common design phase. However, the cut flowers sector does not achieve the same level of synergies with the balance of lifestyle horticulture. This sector requires a different distribution pathway typical of a short life perishable food product.

Page 8Sustainable Lifestyle Horticulture Project – Final report Feb 08

DPI&F Gross Value of Lifestyle Horticulture Sector& forecast to June 2008

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2001-02 2002-03 2003–04 2004–05 2005–06 2006–07 2007-08

Gro

ss V

alue

($m

)

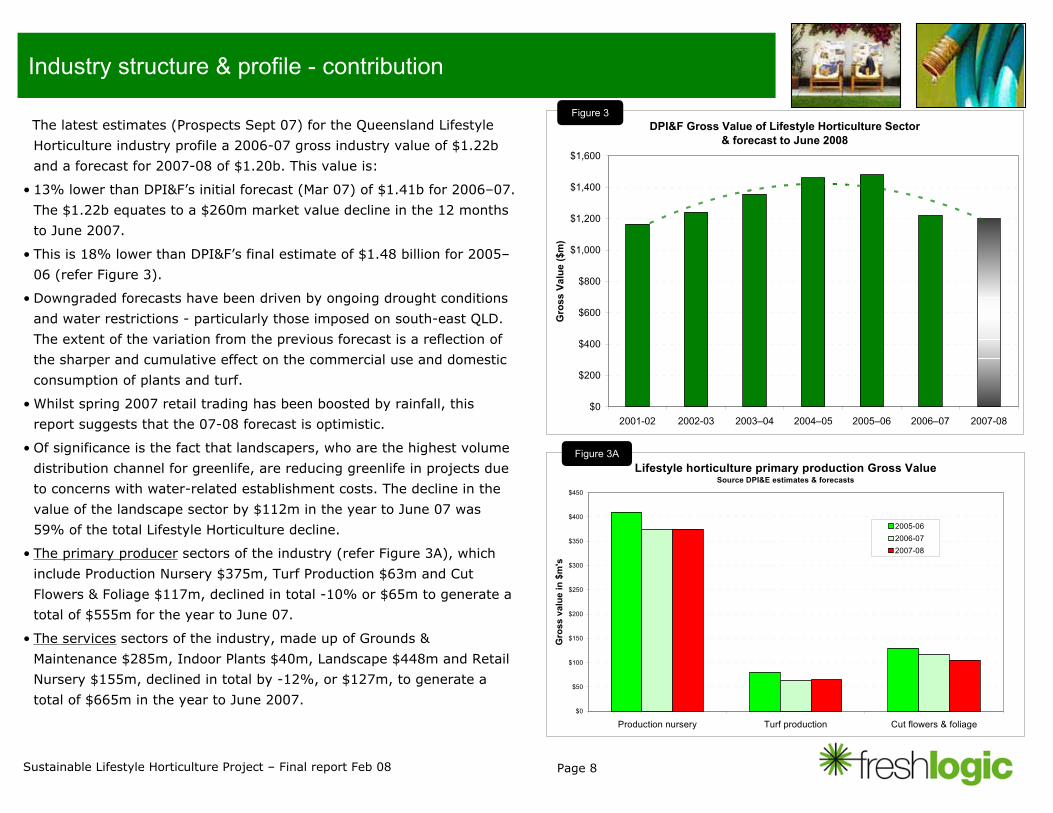

Industry structure & profile - contribution

The latest estimates (Prospects Sept 07) for the Queensland Lifestyle

Horticulture industry profile a 2006-07 gross industry value of $1.22b

and a forecast for 2007-08 of $1.20b. This value is:

• 13% lower than DPI&F’s initial forecast (Mar 07) of $1.41b for 2006–07.

The $1.22b equates to a $260m market value decline in the 12 months

to June 2007.

• This is 18% lower than DPI&F’s final estimate of $1.48 billion for 2005–

06 (refer Figure 3).

• Downgraded forecasts have been driven by ongoing drought conditions

and water restrictions - particularly those imposed on south-east QLD.

The extent of the variation from the previous forecast is a reflection of

the sharper and cumulative effect on the commercial use and domestic

consumption of plants and turf.

• Whilst spring 2007 retail trading has been boosted by rainfall, this

report suggests that the 07-08 forecast is optimistic.

• Of significance is the fact that landscapers, who are the highest volume

distribution channel for greenlife, are reducing greenlife in projects due

to concerns with water-related establishment costs. The decline in the

value of the landscape sector by $112m in the year to June 07 was

59% of the total Lifestyle Horticulture decline.

• The primary producer sectors of the industry (refer Figure 3A), which

include Production Nursery $375m, Turf Production $63m and Cut

Flowers & Foliage $117m, declined in total -10% or $65m to generate a

total of $555m for the year to June 07.

• The services sectors of the industry, made up of Grounds &

Maintenance $285m, Indoor Plants $40m, Landscape $448m and Retail

Nursery $155m, declined in total by -12%, or $127m, to generate a

total of $665m in the year to June 2007.

Figure 3

Lifestyle horticulture primary production Gross ValueSource DPI&E estimates & forecasts

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

Production nursery Turf production Cut flowers & foliage

Gro

ss v

alue

in $

m's

2005-062006-072007-08

Figure 3A

Page 9Sustainable Lifestyle Horticulture Project – Final report Feb 08

Industry structure & profile - contribution

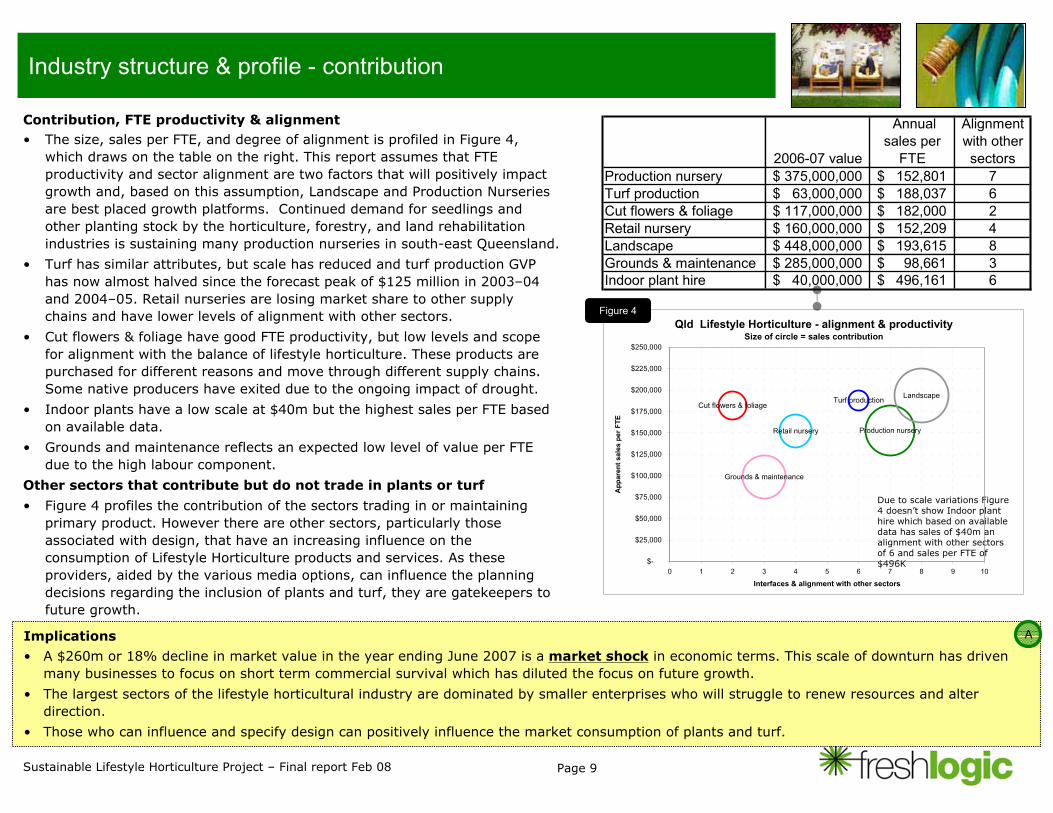

Contribution, FTE productivity & alignment• The size, sales per FTE, and degree of alignment is profiled in Figure 4,

which draws on the table on the right. This report assumes that FTE productivity and sector alignment are two factors that will positively impact growth and, based on this assumption, Landscape and Production Nurseries are best placed growth platforms. Continued demand for seedlings and other planting stock by the horticulture, forestry, and land rehabilitation industries is sustaining many production nurseries in south-east Queensland.

• Turf has similar attributes, but scale has reduced and turf production GVP has now almost halved since the forecast peak of $125 million in 2003–04 and 2004–05. Retail nurseries are losing market share to other supply chains and have lower levels of alignment with other sectors.

• Cut flowers & foliage have good FTE productivity, but low levels and scope for alignment with the balance of lifestyle horticulture. These products are purchased for different reasons and move through different supply chains. Some native producers have exited due to the ongoing impact of drought.

• Indoor plants have a low scale at $40m but the highest sales per FTE based on available data.

• Grounds and maintenance reflects an expected low level of value per FTE due to the high labour component.

Other sectors that contribute but do not trade in plants or turf

• Figure 4 profiles the contribution of the sectors trading in or maintaining primary product. However there are other sectors, particularly those associated with design, that have an increasing influence on theconsumption of Lifestyle Horticulture products and services. As these providers, aided by the various media options, can influence the planning decisions regarding the inclusion of plants and turf, they are gatekeepers to future growth.

Implications

• A $260m or 18% decline in market value in the year ending June 2007 is a market shock in economic terms. This scale of downturn has driven many businesses to focus on short term commercial survival which has diluted the focus on future growth.

• The largest sectors of the lifestyle horticultural industry are dominated by smaller enterprises who will struggle to renew resources and alter direction.

• Those who can influence and specify design can positively influence the market consumption of plants and turf.

A

Due to scale variations Figure 4 doesn’t show Indoor plant hire which based on available data has sales of $40m an alignment with other sectors of 6 and sales per FTE of $496K

Qld Lifestyle Horticulture - alignment & productivitySize of circle = sales contribution

Production nurseryRetail nursery

Grounds & maintenance

Cut flowers & foliageLandscapeTurf production

$-

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

$175,000

$200,000

$225,000

$250,000

0 1 2 3 4 5 6 7 8 9 10

Interfaces & alignment with other sectors

App

aren

t sal

es p

er F

TE

Figure 4

2006-07 value

Annual sales per

FTE

Alignment with other sectors

Production nursery 375,000,000$ 152,801$ 7Turf production 63,000,000$ 188,037$ 6Cut flowers & foliage 117,000,000$ 182,000$ 2Retail nursery 160,000,000$ 152,209$ 4Landscape 448,000,000$ 193,615$ 8Grounds & maintenance 285,000,000$ 98,661$ 3Indoor plant hire 40,000,000$ 496,161$ 6

Page 10Sustainable Lifestyle Horticulture Project – Final report Feb 08

Trends shaping the future - Water availability

Changes in water availability

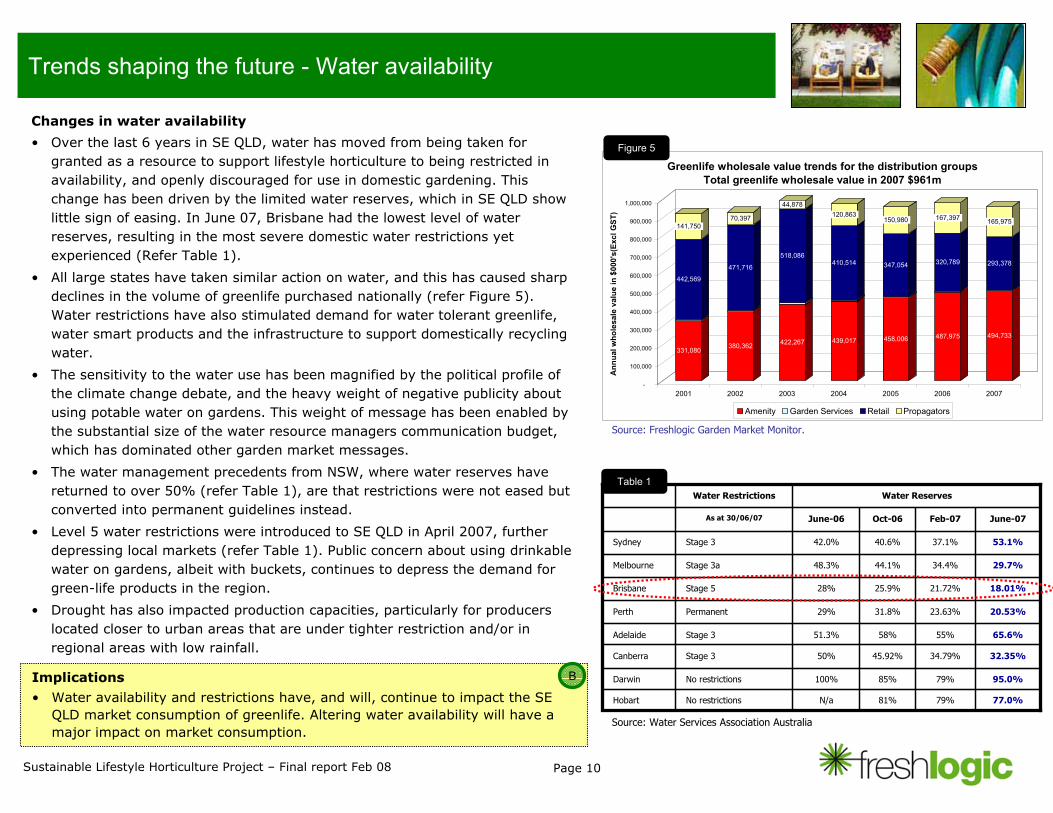

• Over the last 6 years in SE QLD, water has moved from being taken for granted as a resource to support lifestyle horticulture to being restricted in availability, and openly discouraged for use in domestic gardening. This change has been driven by the limited water reserves, which in SE QLD show little sign of easing. In June 07, Brisbane had the lowest level of water reserves, resulting in the most severe domestic water restrictions yet experienced (Refer Table 1).

• All large states have taken similar action on water, and this has caused sharp declines in the volume of greenlife purchased nationally (refer Figure 5). Water restrictions have also stimulated demand for water tolerant greenlife, water smart products and the infrastructure to support domestically recycling water.

• The sensitivity to the water use has been magnified by the political profile of the climate change debate, and the heavy weight of negative publicity about using potable water on gardens. This weight of message has been enabled by the substantial size of the water resource managers communication budget, which has dominated other garden market messages.

• The water management precedents from NSW, where water reserves have returned to over 50% (refer Table 1), are that restrictions were not eased but converted into permanent guidelines instead.

• Level 5 water restrictions were introduced to SE QLD in April 2007, further depressing local markets (refer Table 1). Public concern about using drinkable water on gardens, albeit with buckets, continues to depress the demand for green-life products in the region.

• Drought has also impacted production capacities, particularly for producers located closer to urban areas that are under tighter restriction and/or in regional areas with low rainfall.

77.0%79%81%N/aNo restrictionsHobart

95.0%79%85%100%No restrictionsDarwin

32.35%34.79%45.92%50%Stage 3Canberra

65.6%55%58%51.3%Stage 3Adelaide

20.53%23.63%31.8%29%PermanentPerth

18.01%21.72%25.9%28%Stage 5Brisbane

29.7%34.4%44.1%48.3%Stage 3aMelbourne

53.1%37.1%40.6%42.0%Stage 3Sydney

June-07Feb-07Oct-06June-06As at 30/06/07

Water ReservesWater Restrictions

Source: Water Services Association Australia

Implications

• Water availability and restrictions have, and will, continue to impact the SE QLD market consumption of greenlife. Altering water availability will have a major impact on market consumption.

331,080

442,569

141,750

380,362

471,716

70,397

422,267

518,086

44,878

439,017

410,514

120,863

458,006

347,054

150,980

487,975

320,789

167,397

494,733

293,378

165,975

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Ann

ual w

hole

sale

val

ue in

$00

0's(

Excl

GST

)

2001 2002 2003 2004 2005 2006 2007

Greenlife wholesale value trends for the distribution groupsTotal greenlife wholesale value in 2007 $961m

Amenity Garden Services Retail Propagators

Figure 5

Table 1

Source: Freshlogic Garden Market Monitor.

B

Page 11Sustainable Lifestyle Horticulture Project – Final report Feb 08

Trends shaping the future - Water availability

Alternative water sources

• Captured rain water: The need for water and new water sources is going full circle again, with a renewed push for the backyard water tank. A recent report prepared by economists Marsden Jacobs Associates (“MJA”) concluded that a mass roll-out of water tanks would be cost-competitive against major new water infrastructure projects, such as new dams and desalination plants. Key findings from the report concluded the following:

– Rainwater tanks are a cost-effective solution to the urban water problems in SE QLD, i.e. rainwater tanks are 5 times more energy efficient than desalination plants.

– If governments deployed rainwater tanks to 5 per cent of households each year in Sydney and South-East QLD (SEQ), dams and desalination plants planned for 2010 could be delayed past 2026 (Sydney) and 2019 (SEQ)

• 38% of households in Adelaide have rainwater tanks (2006)

• Less than 6% of houses in Melbourne, Sydney, South-East Queensland and Perth have tanks installed (2006)

• Recycled water: This is recycled and treated water derived from sewerage waste. Whilst this is a mature source of water in many developed countries, it is yet to be harnessed in Australia.

• Grey-water: Refers to the domestic capture and use of water that has been used domestically for cleaning and washing. There are minimum holding periods for this water source, and challenges lie in ensuring that they are used.

• Desalination: There are 14,000 desalination plants in place around the world. It is a mature source of alternative of water, and a plant is planned for completion in 2008 to ease water supply pressure into the SE Qld region.

Implications

• Given water availability is the key enabler of market growth for lifestyle horticulture products and services, alternative water resources are opportunities that warrant more investment.

• The distribution solution and a grading system based on “fit for purpose” are key enablers for recycled water use.

C

Page 12Sustainable Lifestyle Horticulture Project – Final report Feb 08

Trends shaping the future - Regulatory Impact

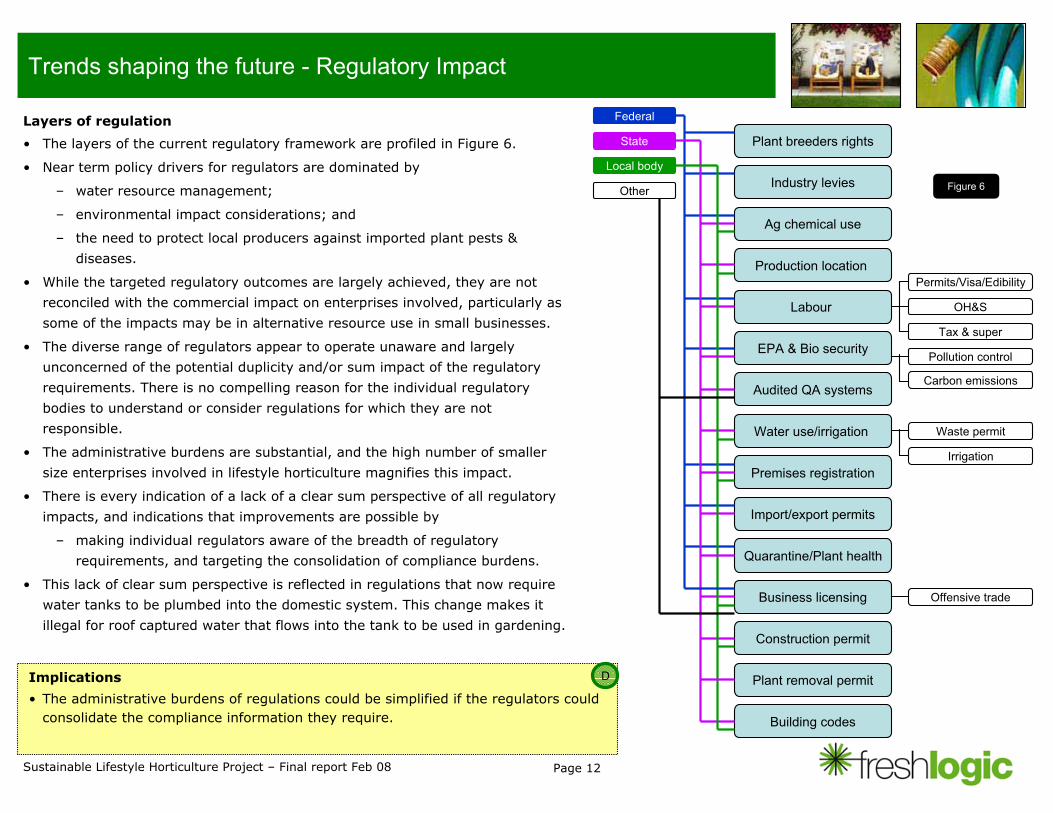

Layers of regulation

• The layers of the current regulatory framework are profiled in Figure 6.

• Near term policy drivers for regulators are dominated by

– water resource management;

– environmental impact considerations; and

– the need to protect local producers against imported plant pests &

diseases.

• While the targeted regulatory outcomes are largely achieved, they are not

reconciled with the commercial impact on enterprises involved, particularly as

some of the impacts may be in alternative resource use in small businesses.

• The diverse range of regulators appear to operate unaware and largely

unconcerned of the potential duplicity and/or sum impact of the regulatory

requirements. There is no compelling reason for the individual regulatory

bodies to understand or consider regulations for which they are not

responsible.

• The administrative burdens are substantial, and the high number of smaller

size enterprises involved in lifestyle horticulture magnifies this impact.

• There is every indication of a lack of a clear sum perspective of all regulatory

impacts, and indications that improvements are possible by

– making individual regulators aware of the breadth of regulatory

requirements, and targeting the consolidation of compliance burdens.

• This lack of clear sum perspective is reflected in regulations that now require

water tanks to be plumbed into the domestic system. This change makes it

illegal for roof captured water that flows into the tank to be used in gardening.

Implications

• The administrative burdens of regulations could be simplified if the regulators could consolidate the compliance information they require.

Plant breeders rights

Ag chemical use

Production location

Labour

EPA & Bio security

Quarantine/Plant health

Permits/Visa/Edibility

OH&S

Industry levies

Premises registration

Import/export permits

Business licensing

Tax & super

Construction permit

Audited QA systems

Plant removal permit

Water use/irrigation

Building codes

Federal

State

Local body

Other

Waste permit

Pollution control

Offensive trade

Carbon emissions

Figure 6

D

Irrigation

Page 13Sustainable Lifestyle Horticulture Project – Final report Feb 08

Trends shaping the future - Skills

Status

• Skilled labour is a vital resource. It is not possible to invest in mechanisation to entirely eliminate the necessity of this resource. If it is not available, industry capacity will be compromised.

• Numerous previous studies relating to the training needs of individual sectors have drawn the following common conclusions:

– Other industries are paying higher wages, resulting in the loss of some long term skilled employees.

– Training institutions that offer higher level courses are experiencing a downward spiral in enrolments, which threatens course viability.

– More mature age students are involved in training for horticulture, and these students are increasingly selecting course content based on general interest or specific workplace competencies, and not completing full courses.

– The industry is not viewed as an attractive career option. This is affected by the level of remuneration, smaller business structures, older generation of management, and, more recently, the adverse messages about responsible water use.

– Employment programs have directed lower skilled applicants into horticultural courses, and this has pressured down the course content. This is an influence on the number of enrolments for qualifications in Amenity Horticulture (RTF), which has increased by 41% from 2,940 to 4,160 for 2004 to 2005 respectively. The number of completions for qualifications in Amenity Horticulture(RTF), however, are not so high, with 150 and 810 completions in2004 and 2005 respectively.

– These conclusions remain valid in Nov 2007.

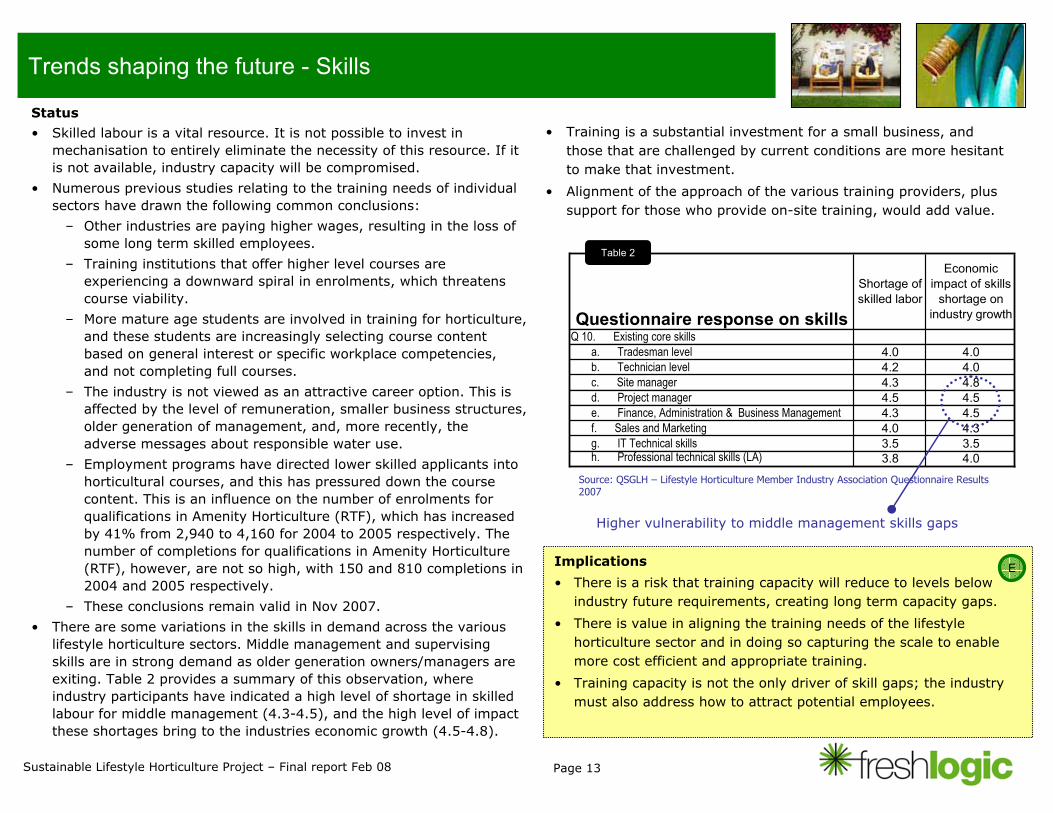

• There are some variations in the skills in demand across the various lifestyle horticulture sectors. Middle management and supervising skills are in strong demand as older generation owners/managers are exiting. Table 2 provides a summary of this observation, where industry participants have indicated a high level of shortage in skilled labour for middle management (4.3-4.5), and the high level of impact these shortages bring to the industries economic growth (4.5-4.8).

Implications

• There is a risk that training capacity will reduce to levels below industry future requirements, creating long term capacity gaps.

• There is value in aligning the training needs of the lifestyle horticulture sector and in doing so capturing the scale to enable more cost efficient and appropriate training.

• Training capacity is not the only driver of skill gaps; the industry must also address how to attract potential employees.

Questionnaire response on skills

Shortage of skilled labor

Economic impact of skills

shortage on industry growth

Q 10. Existing core skills a. Tradesman level 4.0 4.0b. Technician level 4.2 4.0c. Site manager 4.3 4.8d. Project manager 4.5 4.5e. Finance, Administration & Business Management 4.3 4.5f. Sales and Marketing 4.0 4.3g. IT Technical skills 3.5 3.5h. Professional technical skills (LA) 3.8 4.0

Higher vulnerability to middle management skills gaps

Table 2

• Training is a substantial investment for a small business, and those that are challenged by current conditions are more hesitant to make that investment.

• Alignment of the approach of the various training providers, plus support for those who provide on-site training, would add value.

Source: QSGLH – Lifestyle Horticulture Member Industry Association Questionnaire Results 2007

E

Page 14Sustainable Lifestyle Horticulture Project – Final report Feb 08

Trends shaping the future – Distribution channel dynamics

Market share movement

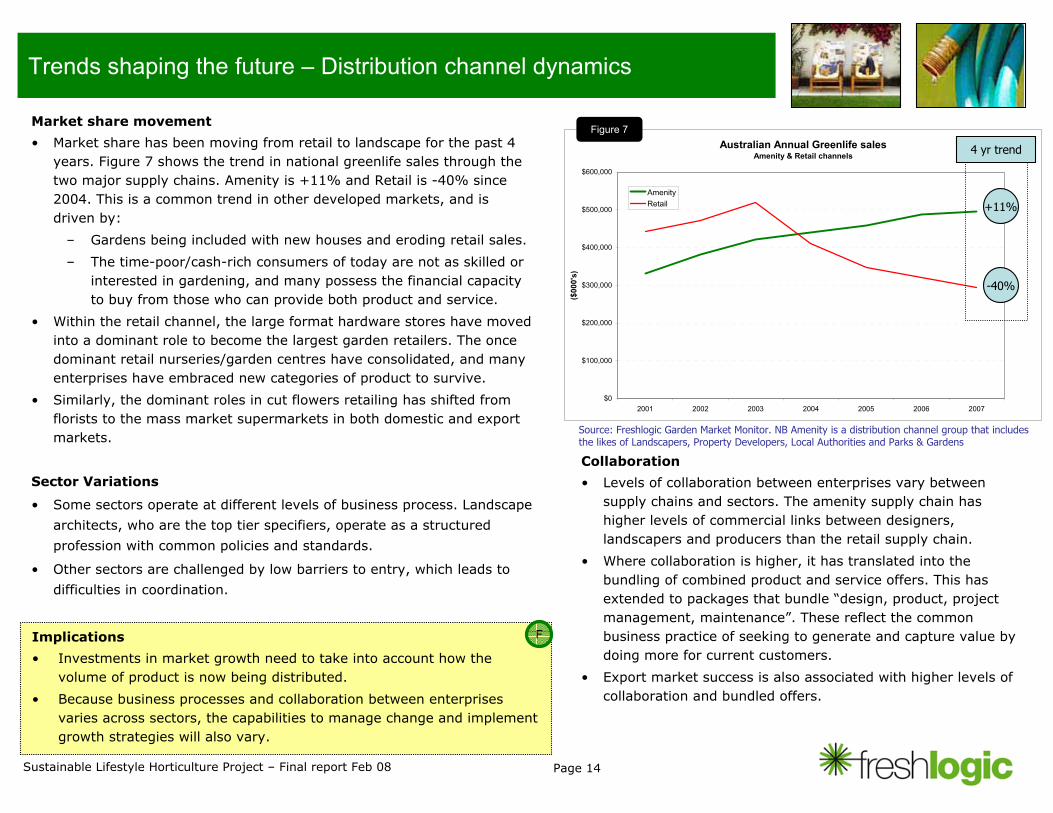

• Market share has been moving from retail to landscape for the past 4 years. Figure 7 shows the trend in national greenlife sales through the two major supply chains. Amenity is +11% and Retail is -40% since 2004. This is a common trend in other developed markets, and is driven by:

– Gardens being included with new houses and eroding retail sales.

– The time-poor/cash-rich consumers of today are not as skilled or interested in gardening, and many possess the financial capacityto buy from those who can provide both product and service.

• Within the retail channel, the large format hardware stores have moved into a dominant role to become the largest garden retailers. The once dominant retail nurseries/garden centres have consolidated, and many enterprises have embraced new categories of product to survive.

• Similarly, the dominant roles in cut flowers retailing has shifted from florists to the mass market supermarkets in both domestic and export markets.

Sector Variations

• Some sectors operate at different levels of business process. Landscape

architects, who are the top tier specifiers, operate as a structured

profession with common policies and standards.

• Other sectors are challenged by low barriers to entry, which leads to

difficulties in coordination.

Australian Annual Greenlife sales Amenity & Retail channels

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

2001 2002 2003 2004 2005 2006 2007

($00

0's)

AmenityRetail

-40%

+11%

4 yr trend

Implications

• Investments in market growth need to take into account how the volume of product is now being distributed.

• Because business processes and collaboration between enterprisesvaries across sectors, the capabilities to manage change and implement growth strategies will also vary.

Collaboration

• Levels of collaboration between enterprises vary between supply chains and sectors. The amenity supply chain has higher levels of commercial links between designers, landscapers and producers than the retail supply chain.

• Where collaboration is higher, it has translated into the bundling of combined product and service offers. This has extended to packages that bundle “design, product, project management, maintenance”. These reflect the common business practice of seeking to generate and capture value by doing more for current customers.

• Export market success is also associated with higher levels of collaboration and bundled offers.

Figure 7

Source: Freshlogic Garden Market Monitor. NB Amenity is a distribution channel group that includes the likes of Landscapers, Property Developers, Local Authorities and Parks & Gardens

F

Page 15Sustainable Lifestyle Horticulture Project – Final report Feb 08

Trends shaping the future - Stakeholder roles & dynamics

Types of stakeholders

• The Lifestyle Industry has four types of stakeholders;

– Enterprises comprises both private and public entities that undertake commercial activity in the lifestyle horticultural market.

– Industry sector organisations (Nursery, Landscape, Irrigation, etc)

– Regulators and Government support agencies.

– ACLH, which provides a common forum and voice for sector industry organisations, resource providers, and regulators that operate in the lifestyle horticulture market.

• This mixture of stakeholders, particularly the ACLH role, requires consideration in determining the planning agenda and the scope for complimentary action from each stakeholder. The scope of value that can be added by each stakeholder must also be considered.

• Feedback gained in the project indicates that ACLH is yet to earn the full support of members and enterprises in the industry.

• In order to improve their effectiveness, ACLH should consider the following:

– The boundaries between commercial and industry organisation activity

– Dysfunction within the ACLH

– Stakeholder conflicts of interest

– A Queensland Government mandate to become an effective common industry voice

– Engaging the industry and facilitating market improvement through effective R&D and extension.

• The requirement is to define a set of planning outcomes and accountabilities that allow strategies to be undertaken with more focus. This would deliver more alignment across the ACLH membersand produce stronger and more complementary outputs.

R&D investments for stakeholders

• The management of R&D investment and extension is a key platform. The following principles are common in guiding these investments:

– An industry can have a shared vision, but it cannot move as one entity.

– Commercial improvement and growth is generated by stakeholders who operate as enterprises in supply chains.

– The activity of enterprises can be aided and enabled by the likes of industry organisations.

– Change is led by a few and followed by most.

• Given the above, the options for investment include:

Resources for ACLH

– Across Australian horticulture, there are precedents to invest R&D funds into sector based IDOs. This tendency is typically higher with many small enterprises as industry participants, who are the constituents of the sector organisations.

– Providing support for bodies that need to develop an effective structure.

Provide support for those who will co-invest

– This is enabled through programs that are based on providing support to those who will co-invest according to certain criteria. This criteria serves to direct the nature of the investment; and the participants’ commitment is captured by requiring matched investment.

Direct investment in market communications

– Designed to arrest declining consumption.

Project sub contracting

– Appropriate when specific short life projects may lend themselves to using external resources on a short term basis.

Implications • In developing growth strategy and implementation plans there is a

need to consider which stakeholders can effectively do what.

G

Page 16Sustainable Lifestyle Horticulture Project – Final report Feb 08

Trends shaping the future - Environmental awareness

Greening Consumer

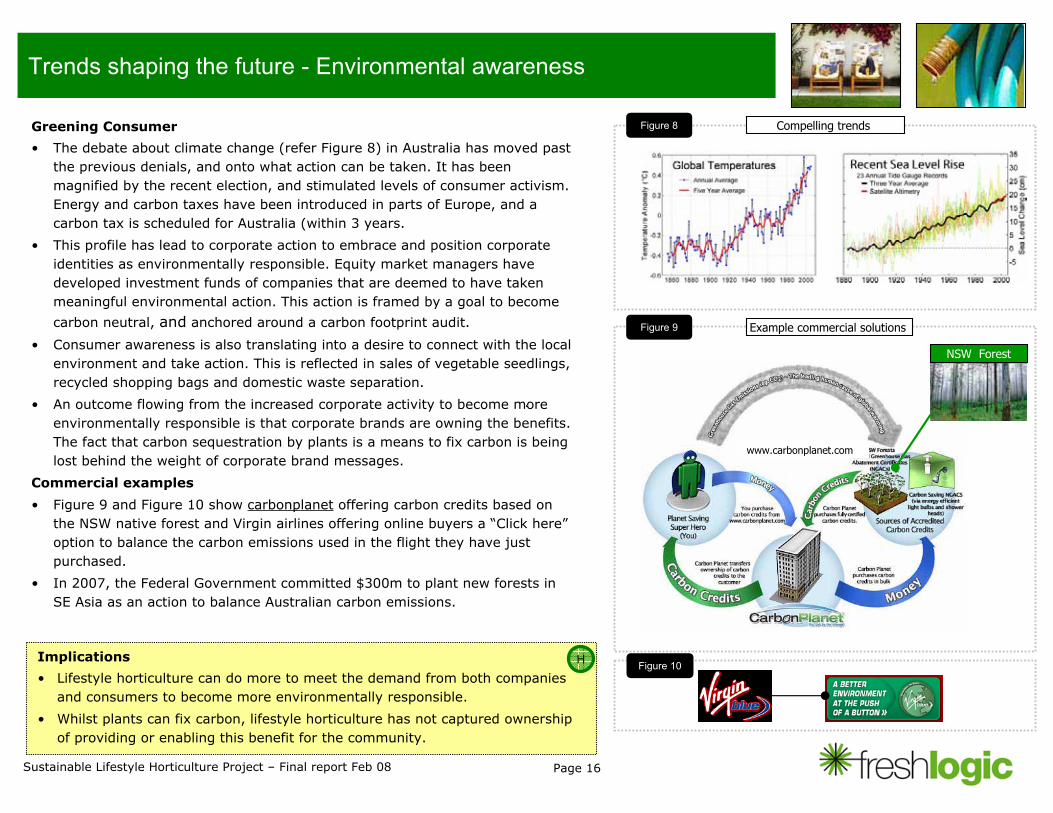

• The debate about climate change (refer Figure 8) in Australia has moved past the previous denials, and onto what action can be taken. It has been magnified by the recent election, and stimulated levels of consumer activism. Energy and carbon taxes have been introduced in parts of Europe, and a carbon tax is scheduled for Australia (within 3 years.

• This profile has lead to corporate action to embrace and position corporate identities as environmentally responsible. Equity market managers have developed investment funds of companies that are deemed to have taken meaningful environmental action. This action is framed by a goal to become

carbon neutral, and anchored around a carbon footprint audit.

• Consumer awareness is also translating into a desire to connect with the local environment and take action. This is reflected in sales of vegetable seedlings, recycled shopping bags and domestic waste separation.

• An outcome flowing from the increased corporate activity to become more environmentally responsible is that corporate brands are owning the benefits. The fact that carbon sequestration by plants is a means to fix carbon is being lost behind the weight of corporate brand messages.

Commercial examples

• Figure 9 and Figure 10 show carbonplanet offering carbon credits based on the NSW native forest and Virgin airlines offering online buyers a “Click here”option to balance the carbon emissions used in the flight they have just purchased.

• In 2007, the Federal Government committed $300m to plant new forests in SE Asia as an action to balance Australian carbon emissions.

Implications

• Lifestyle horticulture can do more to meet the demand from both companies and consumers to become more environmentally responsible.

• Whilst plants can fix carbon, lifestyle horticulture has not captured ownership of providing or enabling this benefit for the community.

NSW Forest

Compelling trends

Example commercial solutions

www.carbonplanet.com

Figure 8

Figure 9

Figure 10H

Page 17Sustainable Lifestyle Horticulture Project – Final report Feb 08

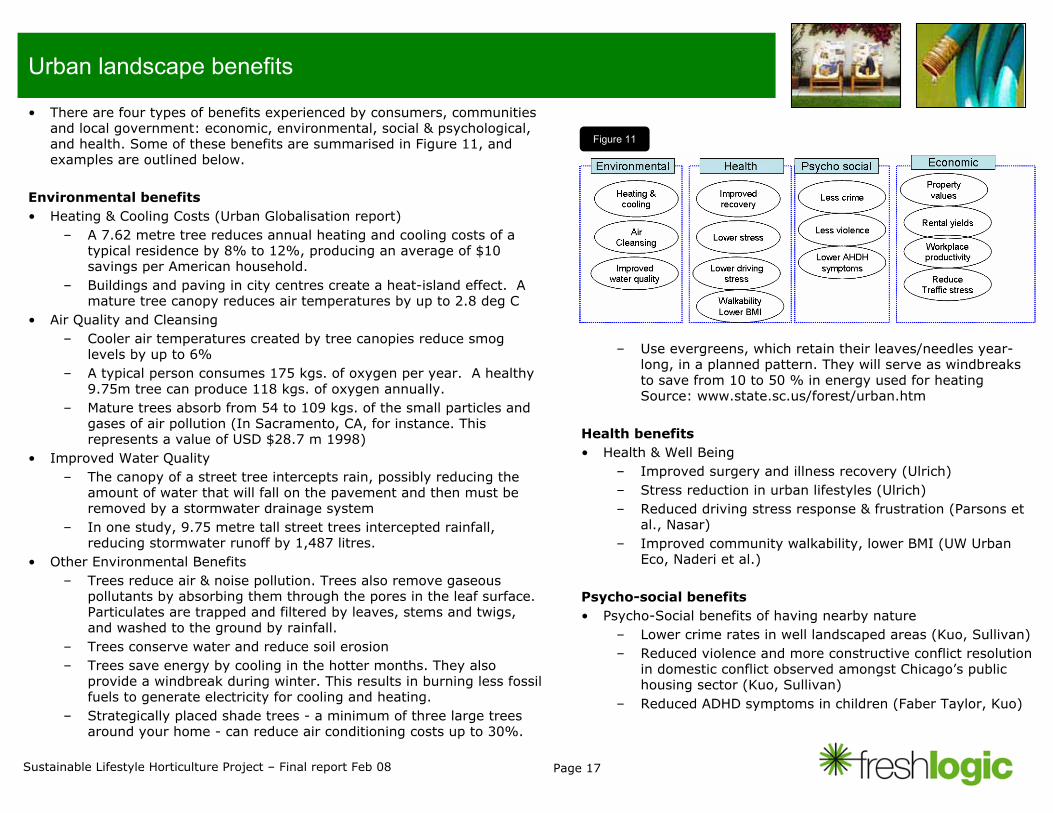

Urban landscape benefits

• There are four types of benefits experienced by consumers, communities and local government: economic, environmental, social & psychological, and health. Some of these benefits are summarised in Figure 11, and examples are outlined below.

Environmental benefits• Heating & Cooling Costs (Urban Globalisation report)

– A 7.62 metre tree reduces annual heating and cooling costs of a typical residence by 8% to 12%, producing an average of $10 savings per American household.

– Buildings and paving in city centres create a heat-island effect. A mature tree canopy reduces air temperatures by up to 2.8 deg C

• Air Quality and Cleansing– Cooler air temperatures created by tree canopies reduce smog

levels by up to 6%– A typical person consumes 175 kgs. of oxygen per year. A healthy

9.75m tree can produce 118 kgs. of oxygen annually.– Mature trees absorb from 54 to 109 kgs. of the small particles and

gases of air pollution (In Sacramento, CA, for instance. This represents a value of USD $28.7 m 1998)

• Improved Water Quality– The canopy of a street tree intercepts rain, possibly reducing the

amount of water that will fall on the pavement and then must be removed by a stormwater drainage system

– In one study, 9.75 metre tall street trees intercepted rainfall,reducing stormwater runoff by 1,487 litres.

• Other Environmental Benefits– Trees reduce air & noise pollution. Trees also remove gaseous

pollutants by absorbing them through the pores in the leaf surface. Particulates are trapped and filtered by leaves, stems and twigs, and washed to the ground by rainfall.

– Trees conserve water and reduce soil erosion– Trees save energy by cooling in the hotter months. They also

provide a windbreak during winter. This results in burning less fossil fuels to generate electricity for cooling and heating.

– Strategically placed shade trees - a minimum of three large trees around your home - can reduce air conditioning costs up to 30%.

– Use evergreens, which retain their leaves/needles year-long, in a planned pattern. They will serve as windbreaks to save from 10 to 50 % in energy used for heating Source: www.state.sc.us/forest/urban.htm

Health benefits• Health & Well Being

– Improved surgery and illness recovery (Ulrich)– Stress reduction in urban lifestyles (Ulrich)– Reduced driving stress response & frustration (Parsons et

al., Nasar)– Improved community walkability, lower BMI (UW Urban

Eco, Naderi et al.)

Psycho-social benefits• Psycho-Social benefits of having nearby nature

– Lower crime rates in well landscaped areas (Kuo, Sullivan)– Reduced violence and more constructive conflict resolution

in domestic conflict observed amongst Chicago’s public housing sector (Kuo, Sullivan)

– Reduced ADHD symptoms in children (Faber Taylor, Kuo)

Figure 11

Page 18Sustainable Lifestyle Horticulture Project – Final report Feb 08

Urban landscape benefits

Economic Benefits• Trees and Residential Property Values (2001 USA valuation &

benefits study)– Data from > 800 home sales - it was noted that houses with

large trees in the front yard enjoyed an increase in the sale price (0.88% or $1K per $115K home value) Anderson & Cordell

– Buyers are willing to pay 3-15% more for residential properties with ample trees

• Parks and Property values– Assessed value of properties - 10 to 20% higher– Conditions for higher value – must have good visibility, be well

maintained • Landscape & Commercial Building Rental Yields

– Office and industrial space in a wooded setting is in more demand and is more valuable to sell or rent.

– Quality landscaping lifted office rentals by 7% per annum (Davey Resource Group, USA, 2003)

• Urban Benefits in Retail Environments– higher willingness to pay for all types of goods i.e. higher in

districts with trees: 9-12%• Workplace Nature Views

– Well-being: desk workers without nature views reported 23% more ailments in the 6 months prior to the study

– Job Satisfaction: less frustrated and more patient; higher overall job satisfaction and enthusiasm / reduction in workplace fatigue

• Plants in the Workplace – Productivity: 12% quicker reaction on computer tasks & more

attentive– Stress Reduction: lower systolic blood – Higher job satisfaction, reduced absenteeism (R. Kaplan)

• Roadside Landscape & Traffic Stress Response – Roadside Features - driving simulations such as being

surrounded by nature, greenery, golf course, strip mall etc led to improved psychological response ie lower blood pressure, immunisation effect, less response to new stresses (study result)

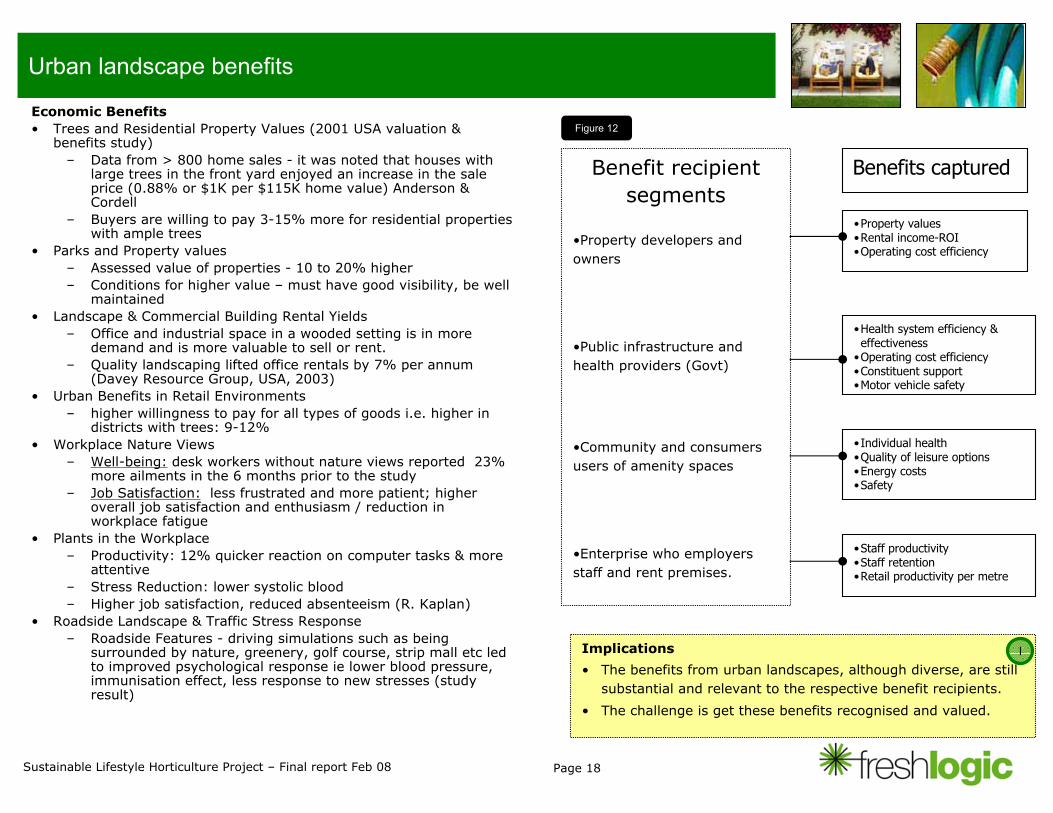

Implications

• The benefits from urban landscapes, although diverse, are still substantial and relevant to the respective benefit recipients.

• The challenge is get these benefits recognised and valued.

Benefit recipient segments

•Property developers and owners

•Public infrastructure and health providers (Govt)

•Community and consumers users of amenity spaces

•Enterprise who employers staff and rent premises.

•Property values•Rental income-ROI•Operating cost efficiency

•Health system efficiency & effectiveness

•Operating cost efficiency•Constituent support•Motor vehicle safety

•Individual health •Quality of leisure options•Energy costs•Safety

•Staff productivity•Staff retention•Retail productivity per metre

Benefits captured

Figure 12

I

Page 19Sustainable Lifestyle Horticulture Project – Final report Feb 08

Product diversification

Status & drivers• Product and service diversification has been driven by what is seen as

normal commercial behaviour responding to market demand signals. The level of activity signals that commercial gains have been created in current market conditions.

Examples

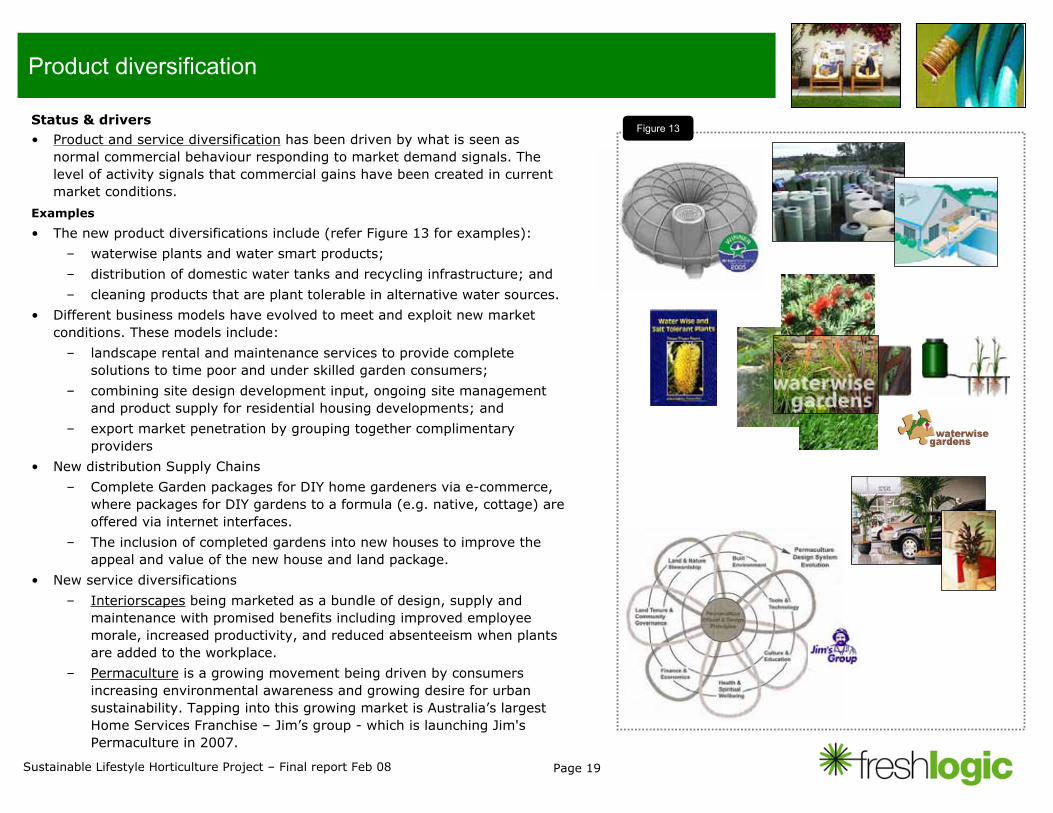

• The new product diversifications include (refer Figure 13 for examples):

– waterwise plants and water smart products;

– distribution of domestic water tanks and recycling infrastructure; and

– cleaning products that are plant tolerable in alternative water sources.

• Different business models have evolved to meet and exploit new market conditions. These models include:

– landscape rental and maintenance services to provide complete solutions to time poor and under skilled garden consumers;

– combining site design development input, ongoing site managementand product supply for residential housing developments; and

– export market penetration by grouping together complimentary providers

• New distribution Supply Chains

– Complete Garden packages for DIY home gardeners via e-commerce, where packages for DIY gardens to a formula (e.g. native, cottage) are offered via internet interfaces.

– The inclusion of completed gardens into new houses to improve the appeal and value of the new house and land package.

• New service diversifications

– Interiorscapes being marketed as a bundle of design, supply and maintenance with promised benefits including improved employee morale, increased productivity, and reduced absenteeism when plants are added to the workplace.

– Permaculture is a growing movement being driven by consumers increasing environmental awareness and growing desire for urban sustainability. Tapping into this growing market is Australia’s largest Home Services Franchise – Jim’s group - which is launching Jim's Permaculture in 2007.

Figure 13

Page 20Sustainable Lifestyle Horticulture Project – Final report Feb 08

Product diversification - continued

Future Options The rooftop gardens (refer Figure 14)• In the urban centers of Australia, rooftop gardens may have potential. The

global experience thus far has shown that:– Government support has led to 12 per cent green roof coverage in

some European cities. – Germany alone has more than 2,000 new and retrofitted green roof

suppliers– Green roofing is a strong growth industry in many cities like Toronto.– In some areas of Chicago, green roofs are mandatory

• A well-engineered rooftop garden costing around US$14 a square foot (approx A$100 a square meter) would result in benefits of:

– Reduction in ambient temperatures in cities: 8% green roof top coverage over the city landscape would reduce the city’s heat island effect by 2 Deg C (2005 Canada's Ryerson University study)

– Slower runoff of rainfall at peak times – meaning cost savings of Can$79 million a year from reduced capital costs for storm-water management, erosion control and sewer overflows

– Direct energy savings of CAN$12 million a year in buildings fromreduced cooling demand in summer & indirect city-savings at peak load demand of CAN$80 million a year.

• Australian market options are evolving to provide this new style see www.rooftopgardens.com.au in figure 14. This provider is introducing a Voluntary program for Green Roofs to assist stabilise Climate Change.

– This proposition is made by Newtec concrete constructions includes the following:

– “Newtec” can now play an important role to assist introduce a green roof program for future urban development that will in the long term assist to stabilise climate change and provide many benefits in the short term.

– To establish a green roof on top of a Newtec concrete structure will have little effect on the construction costs because it is simply replacing the conventional roof with a concrete slab that sits on top of the load bearing concrete walls. Only the access stairs, rooftopprivacy, soil retaining walls, selected greenery and soil will vary the initial costs.

Implications • Some enterprises have read market signals and diversified. This

indicates there are market opportunities as well as capacities within some enterprises to generate growth in current market conditions

Figure 14

J

www.rooftopgardens.com.au

Page 21Sustainable Lifestyle Horticulture Project – Final report Feb 08

Regional development

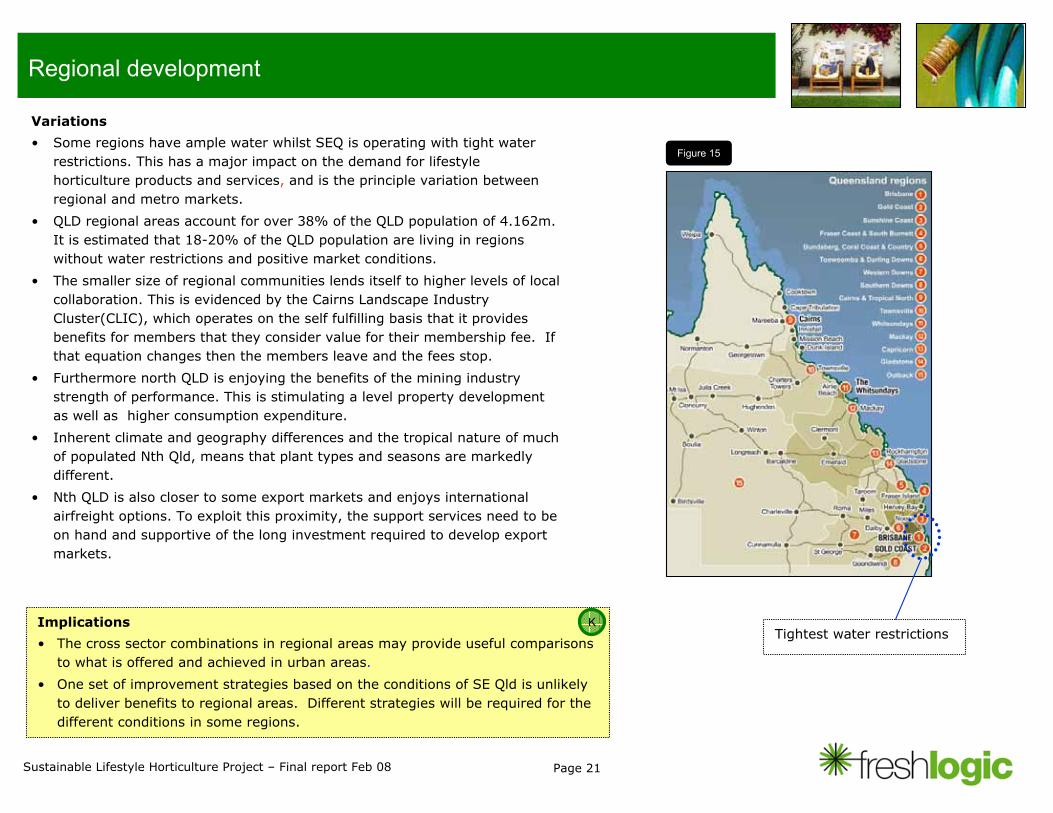

Variations

• Some regions have ample water whilst SEQ is operating with tight water restrictions. This has a major impact on the demand for lifestyle horticulture products and services, and is the principle variation between regional and metro markets.

• QLD regional areas account for over 38% of the QLD population of 4.162m. It is estimated that 18-20% of the QLD population are living in regions without water restrictions and positive market conditions.

• The smaller size of regional communities lends itself to higher levels of local collaboration. This is evidenced by the Cairns Landscape Industry Cluster(CLIC), which operates on the self fulfilling basis that it provides benefits for members that they consider value for their membership fee. If that equation changes then the members leave and the fees stop.

• Furthermore north QLD is enjoying the benefits of the mining industry strength of performance. This is stimulating a level property development as well as higher consumption expenditure.

• Inherent climate and geography differences and the tropical nature of much of populated Nth Qld, means that plant types and seasons are markedly different.

• Nth QLD is also closer to some export markets and enjoys international airfreight options. To exploit this proximity, the support services need to be on hand and supportive of the long investment required to develop export markets.

Implications

• The cross sector combinations in regional areas may provide useful comparisons to what is offered and achieved in urban areas.

• One set of improvement strategies based on the conditions of SE Qld is unlikely to deliver benefits to regional areas. Different strategies will be required for the different conditions in some regions.

Tightest water restrictions

Figure 15

K

Page 22Sustainable Lifestyle Horticulture Project – Final report Feb 08

Plant Export ValueTotal Australia & Qld

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

$11,000

$12,000

FY2003 FY2004 FY2005 FY2006 FY2007

Period

Valu

e (A

$'00

0)QueenslandTotal Australia

Plant Export ValueTotal Australia by category

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

FY2003 FY2004 FY2005 FY2006 FY2007

Period

Valu

e (A

$'00

0)

Bulbs & tubers dormant Bulbs & tubers in growth Unrooted cuttings and slipsTrees & shrubs Rhododendrons & azaleas RosesLive plants (excl live cuttings and slips)

Export opportunities

Performance

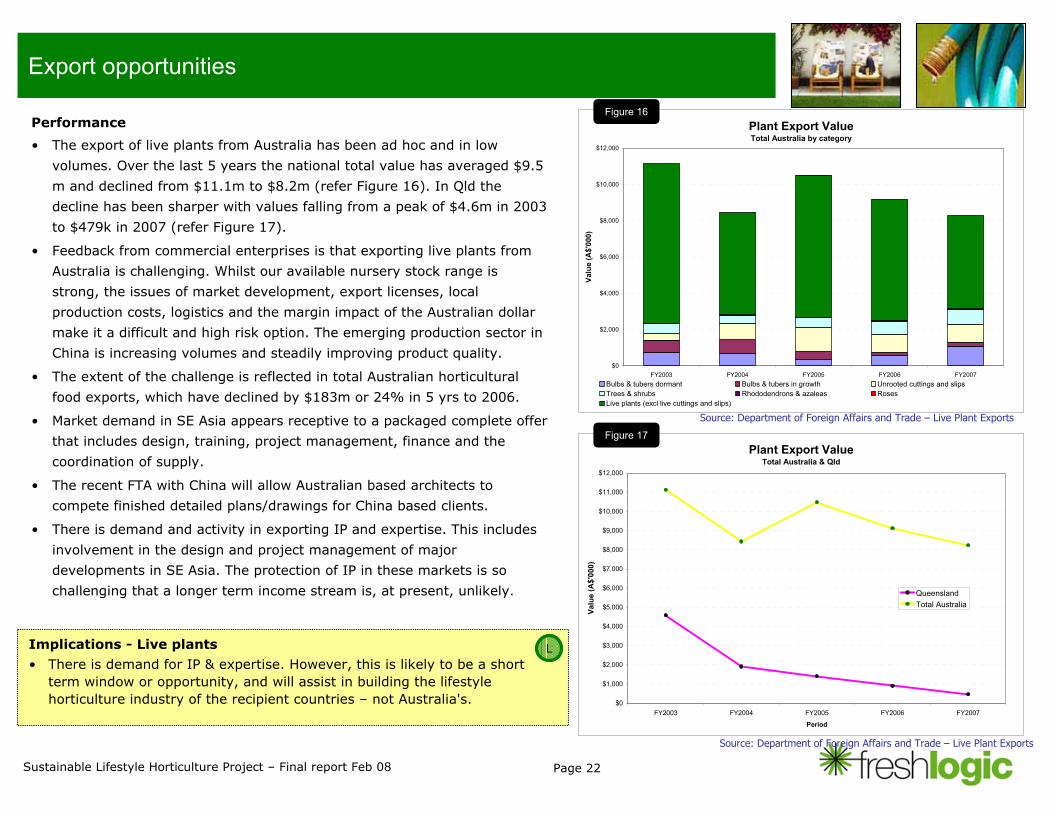

• The export of live plants from Australia has been ad hoc and in low

volumes. Over the last 5 years the national total value has averaged $9.5

m and declined from $11.1m to $8.2m (refer Figure 16). In Qld the

decline has been sharper with values falling from a peak of $4.6m in 2003

to $479k in 2007 (refer Figure 17).

• Feedback from commercial enterprises is that exporting live plants from

Australia is challenging. Whilst our available nursery stock range is

strong, the issues of market development, export licenses, local

production costs, logistics and the margin impact of the Australian dollar

make it a difficult and high risk option. The emerging production sector in

China is increasing volumes and steadily improving product quality.

• The extent of the challenge is reflected in total Australian horticultural

food exports, which have declined by $183m or 24% in 5 yrs to 2006.

• Market demand in SE Asia appears receptive to a packaged complete offer

that includes design, training, project management, finance and the

coordination of supply.

• The recent FTA with China will allow Australian based architects to

compete finished detailed plans/drawings for China based clients.

• There is demand and activity in exporting IP and expertise. This includes

involvement in the design and project management of major

developments in SE Asia. The protection of IP in these markets is so

challenging that a longer term income stream is, at present, unlikely.

Implications - Live plants

• There is demand for IP & expertise. However, this is likely to be a short term window or opportunity, and will assist in building the lifestyle horticulture industry of the recipient countries – not Australia's.

Figure 16

Figure 17

Source: Department of Foreign Affairs and Trade – Live Plant Exports

Source: Department of Foreign Affairs and Trade – Live Plant Exports

L

Page 23Sustainable Lifestyle Horticulture Project – Final report Feb 08

Export opportunities

Performance

• Cut Flowers & Foliage enjoys a larger global market than live plants. This is influenced by their perishable nature and the ensuing repeat consumption patterns. As a participant in this market, Australia has some advantages in product, growing conditions and seasonal supply windows.

• Definitive data on export sales of cut flowers and foliage is not available. This is due to some Queensland produced product being exported out of other states and DFAT data capture of nominal pre auction consignment values rather than final selling price.

• However, best industry estimates place the value of cut flower & foliage exported overseas out of Queensland at $13m per annum for the calendar year 2007.

• Feedback from exporters indicates there is market price resistance due to the stronger AUD$ and/or pressure to trade in another currency.

• Japan, United States, and the Netherlands are the top three destinations for exports of Australian cut flowers. All three of these countries have been showing a decline in export value over the last five years.

• The information gap on market values for the Cut Flowers & Foliage sector is a vulnerability. It undermines the provision of support as the impact of market development investments cannot be measured.

Developing exports

• Trade missions that have built relationships with key property developers are reported to have delivered positive flow on results.

• Indications are that the enterprises who understand export markets and the basis on which they need to compete, are best placed to further develop export markets. However, several export development agencies have a performance measure based on the number of businesses exporting, which is in conflict with this conclusion.

• Recent activity on exporting tissue cultured stock has shown positive results.

Implications - Cut flowers exports

• The national exports of cut flowers are more substantial than live plants but still a small commercial base. There is demand for dried, died, bleached or impregnated cut flowers out of QLD.

• Given the export market conditions and Australian competitive disadvantages, generating growth by supporting existing exporters is a lower risk option than stimulating expansion in the number of businesses exporting.

M

Current ACLH export directions

• An ACLH draft export strategy has been defined an ACLH export

subcommittee. This plan identifies the impediments, which

include and range from lack of production and low market

knowledge to logistical shortfalls and weak IP protection.

• The confidence to invest in export is low and indications are a

high level of development is required to move non exporters into

competent and successful exporters.

• The plan confirms that export demand for services is stronger

than the overall for products, with the exception of wildflowers.

• Action plans address a diverse agenda of export culture,

capabilities, business structures, promotion, regulator liaison and

market research.

• This report concludes that the scope of these actions are

appropriate but optimistic and concludes that higher overall

industry growth is likely be achieved by supporting enterprises

who have the culture, capability and business structure.

Page 24Sustainable Lifestyle Horticulture Project – Final report Feb 08

Key issues and strategy implications

Growth options need to embrace support providers and not be limited to those who produce, trade, or maintain primary product.

6-9There is varying growth potential between the sectors that tradein primary product. However, some support providers like landscape architects, designers and government specifiers, who do not trade in plants, can generate substantial impact.

Combine lifestyle sector training needs to create scale and maintain a viable training infrastructure.

13The availability of skilled workers is under threat as training programs fail to meet industry skill gaps.

15

14

12

10-11

6-9

Page

Ease the regulatory burden and enterprises will have more time and resource to invest in improvement.

The regulatory burden is substantial and set to increase as carbon emission monitoring commences.

As many stakeholders are focused on short term survival, it will be challenging for them to respond to initiatives that allude to long term growth. This will effect the type of support that they will act upon.

The market has declined sharply (18%) in the last 12 months and this has brought commercial pressure to many enterprises.

ACLH need to be a cohesive group to be effective. Need to clarify stakeholder roles based on where value can be added, in particular,the involvement in commercial activity. Collaboration and diversification can add value for those who want it and understand what it can deliver.

The views of the stakeholders of ACLH vary significantly betweenthemselves and commercial enterprises on key industry issues and improvement solutions. Commercial enterprises endorse the merit of across sector collaboration and diversification activity but are skeptical as to what ACLH can deliver.

Strategy ImplicationsKey Issues

Retail supply chain has lost market share, and the medium term growth supply chains are providers of plant and service combinations

Gardening products are being purchased through different supply chains and this has resulted in varying performance and growth prospects between different distribution supply chains.

Water restrictions have evolved to a constant market condition.There will be more scope to using recycled water, and it will need clear guidelines for use and effective distribution systems.

Water resources and restrictions are, and will continue to be, amajor market impact. Water conservation and restriction messages have dominated other garden messages to consumers. There has been strong demand for water efficient plants, products, and the domestic water recycling infrastructure.

A

B

C

D

E

F

G

A

Page 25Sustainable Lifestyle Horticulture Project – Final report Feb 08

Key issues and strategy implications

Investing in “positioning” lifestyle horticulture as a provider of tangible environmental benefits has potential to generate returns through increasing sales and the attractiveness of employment inthe sector

16-18Environmental awareness is high and increasing, but lifestyle horticulture has not taken ownership of the urban landscape and environmental benefits it can deliver, and others are moving to own this space.

Shortage of skills/labor is being impacted by poor industry perception, low wages and the nature of work compared to other alternatives.

These precedents of enterprises diversifying to advantage themselves in the current conditions, point to capabilities that are strengths to harness, in effecting growth initiatives.

19-20Some enterprises have evolved new products and services to generate growth and cope with new market conditions.

22-23

21

Page

Export demand is strongest around a short term window of IP and services rather than product. Export growth options for plants and flowers will require targeted and aligned offers delivered by companies who understand their basis for competing.

There is limited export activity in plants and cut flowers but demand for IP and project management expertise. There are clear challenges, labour cost and exchange rate in exporting plants and cut flower products.

One approach will not suit all market conditions in Qld and different strategies will need to be developed to reflect the local variationsthat are best understood by local enterprises.

Regional & metro market conditions, dynamics, and potential improvement strategies vary significantly.

Strategy ImplicationsKey Issues

J

K

L

M

H

I

Page 26Sustainable Lifestyle Horticulture Project – Final report Feb 08

Opportunities and strategies

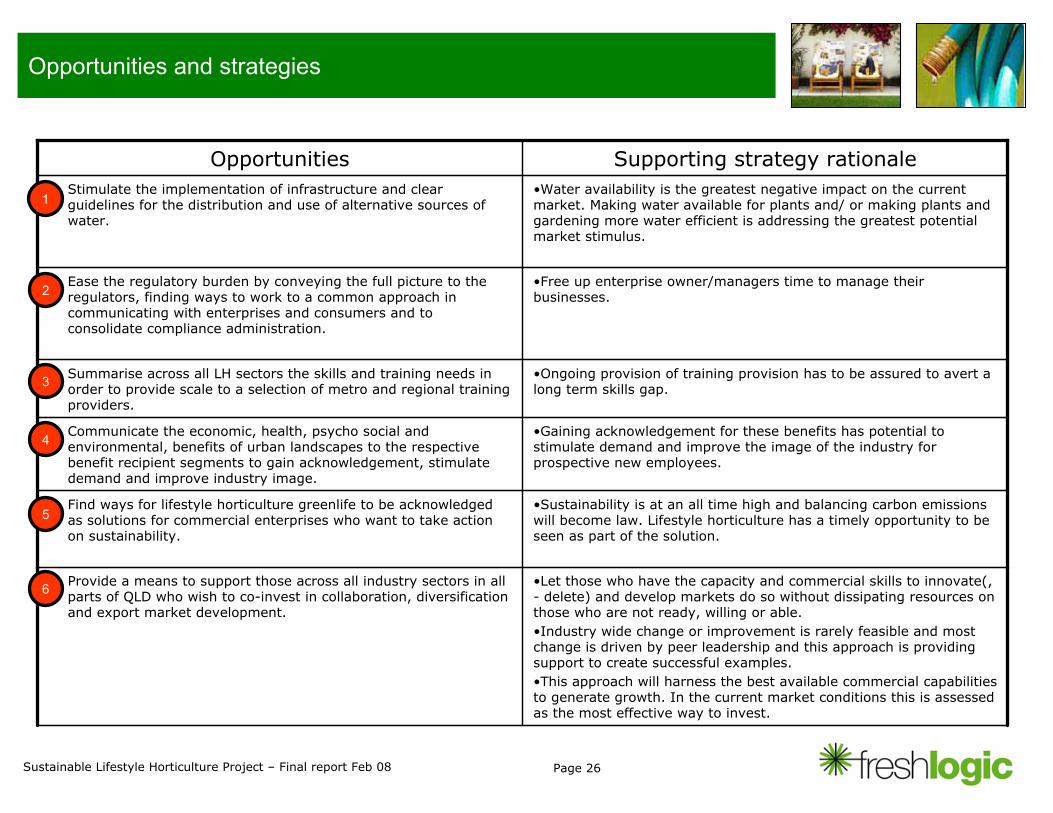

•Let those who have the capacity and commercial skills to innovate(, - delete) and develop markets do so without dissipating resources on those who are not ready, willing or able. •Industry wide change or improvement is rarely feasible and most change is driven by peer leadership and this approach is providing support to create successful examples. •This approach will harness the best available commercial capabilities to generate growth. In the current market conditions this is assessed as the most effective way to invest.

• Provide a means to support those across all industry sectors in all parts of QLD who wish to co-invest in collaboration, diversification and export market development.

•Sustainability is at an all time high and balancing carbon emissions will become law. Lifestyle horticulture has a timely opportunity to be seen as part of the solution.

• Find ways for lifestyle horticulture greenlife to be acknowledged as solutions for commercial enterprises who want to take action on sustainability.

•Gaining acknowledgement for these benefits has potential to stimulate demand and improve the image of the industry for prospective new employees.

• Communicate the economic, health, psycho social and environmental, benefits of urban landscapes to the respective benefit recipient segments to gain acknowledgement, stimulate demand and improve industry image.

•Ongoing provision of training provision has to be assured to avert a long term skills gap.

• Summarise across all LH sectors the skills and training needs inorder to provide scale to a selection of metro and regional training providers.

•Free up enterprise owner/managers time to manage their businesses.

• Ease the regulatory burden by conveying the full picture to the regulators, finding ways to work to a common approach in communicating with enterprises and consumers and to consolidate compliance administration.

•Water availability is the greatest negative impact on the current market. Making water available for plants and/ or making plants and gardening more water efficient is addressing the greatest potential market stimulus.

• Stimulate the implementation of infrastructure and clear guidelines for the distribution and use of alternative sources of water.

Supporting strategy rationale Opportunities

1

2

3

4

5

6

Page 27Sustainable Lifestyle Horticulture Project – Final report Feb 08

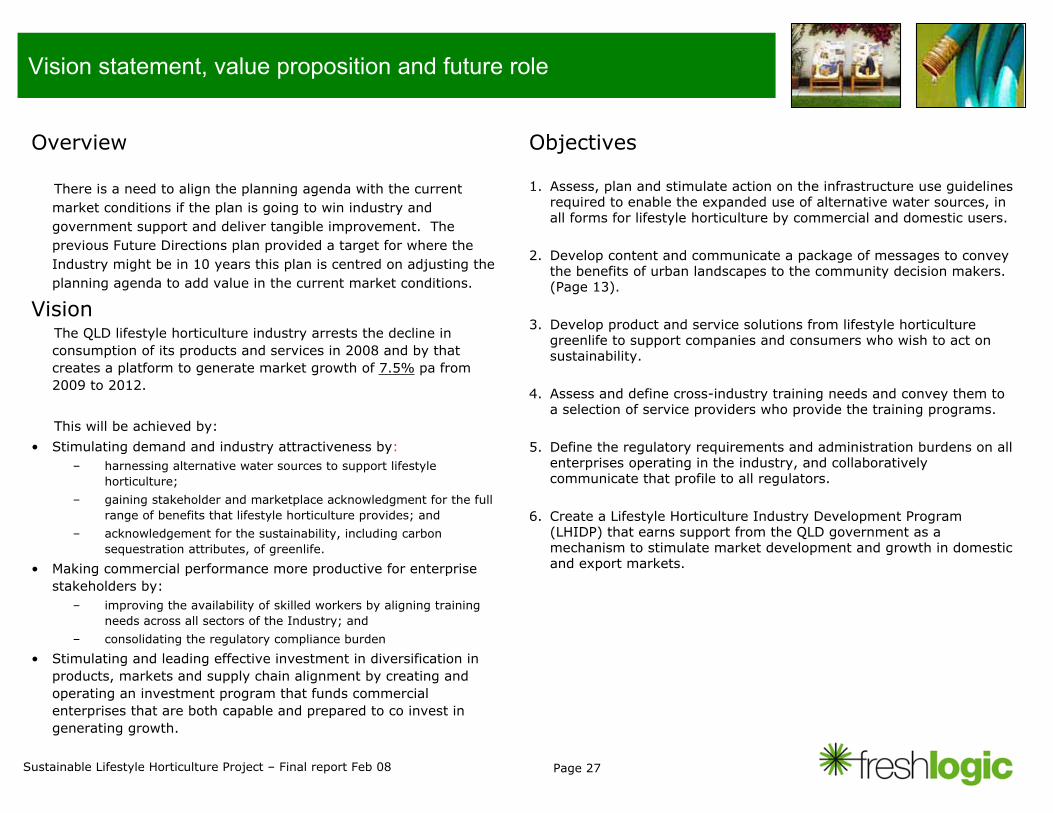

Vision statement, value proposition and future role

Overview

There is a need to align the planning agenda with the current market conditions if the plan is going to win industry and government support and deliver tangible improvement. The previous Future Directions plan provided a target for where the Industry might be in 10 years this plan is centred on adjusting the planning agenda to add value in the current market conditions.

VisionThe QLD lifestyle horticulture industry arrests the decline in consumption of its products and services in 2008 and by that creates a platform to generate market growth of 7.5% pa from 2009 to 2012.

This will be achieved by:

• Stimulating demand and industry attractiveness by:– harnessing alternative water sources to support lifestyle

horticulture;

– gaining stakeholder and marketplace acknowledgment for the full range of benefits that lifestyle horticulture provides; and

– acknowledgement for the sustainability, including carbon sequestration attributes, of greenlife.

• Making commercial performance more productive for enterprise stakeholders by:

– improving the availability of skilled workers by aligning training needs across all sectors of the Industry; and

– consolidating the regulatory compliance burden

• Stimulating and leading effective investment in diversification in products, markets and supply chain alignment by creating and operating an investment program that funds commercial enterprises that are both capable and prepared to co invest in generating growth.

Objectives

1. Assess, plan and stimulate action on the infrastructure use guidelines required to enable the expanded use of alternative water sources, in all forms for lifestyle horticulture by commercial and domestic users.

2. Develop content and communicate a package of messages to convey the benefits of urban landscapes to the community decision makers. (Page 13).

3. Develop product and service solutions from lifestyle horticulture greenlife to support companies and consumers who wish to act on sustainability.

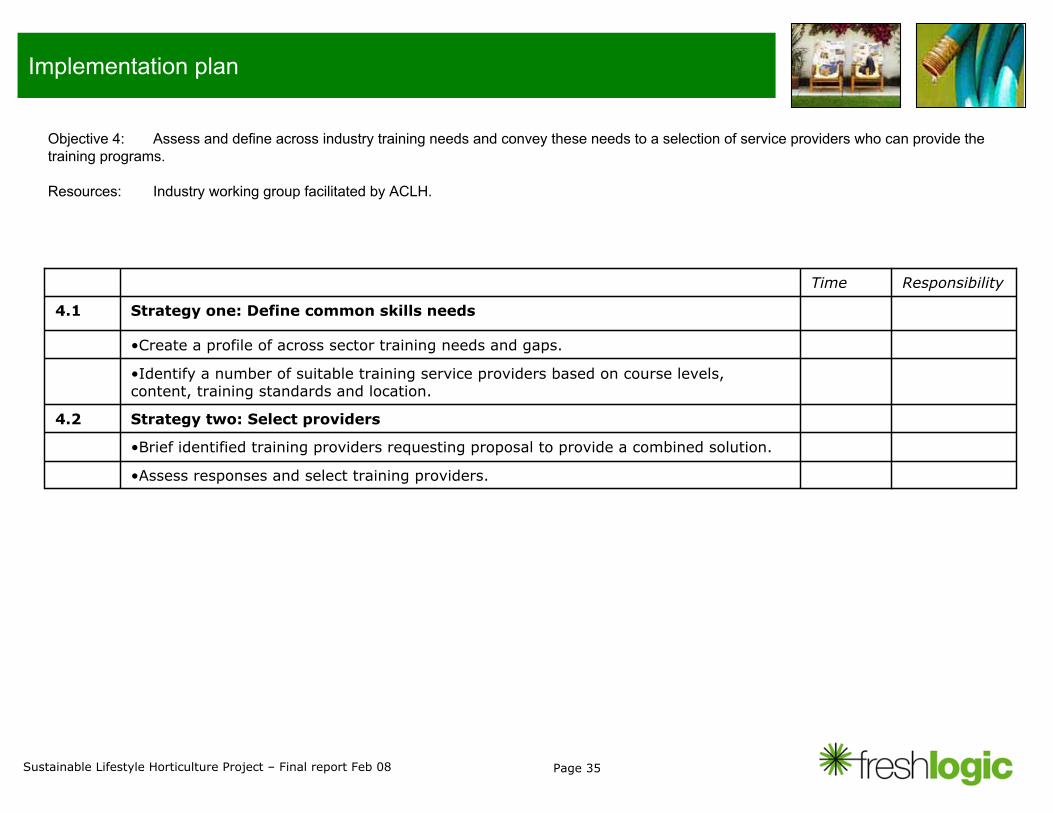

4. Assess and define cross-industry training needs and convey them to a selection of service providers who provide the training programs.

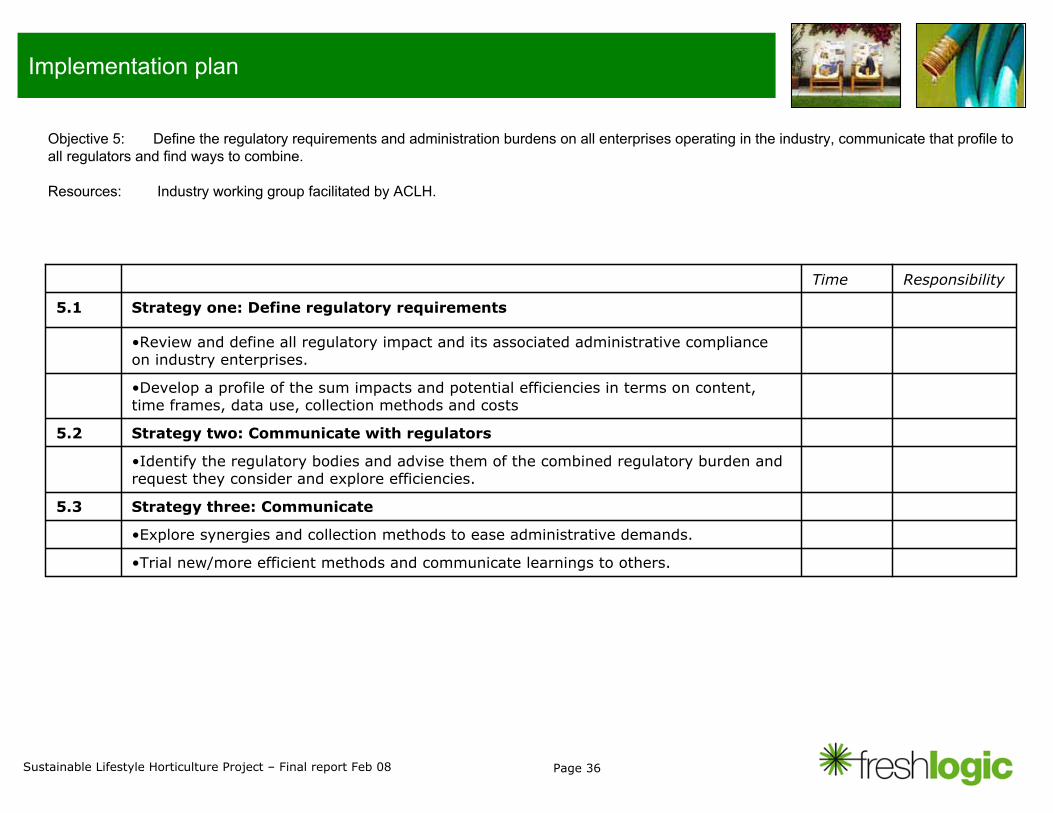

5. Define the regulatory requirements and administration burdens on all enterprises operating in the industry, and collaboratively communicate that profile to all regulators.

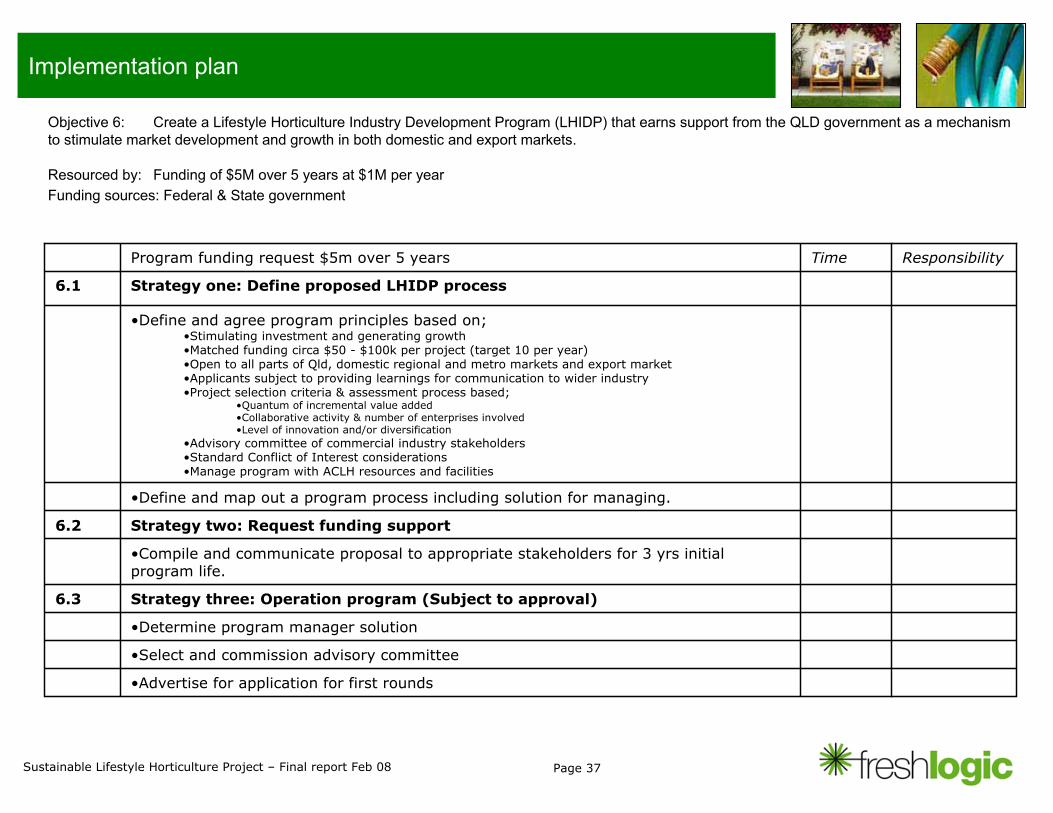

6. Create a Lifestyle Horticulture Industry Development Program (LHIDP) that earns support from the QLD government as a mechanism to stimulate market development and growth in domesticand export markets.

Page 28Sustainable Lifestyle Horticulture Project – Final report Feb 08

Implementation rationale and funding

Implementation plan frameworkThe approach to the implementation plan is based on using the following framework to achieve the objectives outlined on page 27.

• Market growth is most effectively generated by committed commercial enterprises.

• In the current lifestyle horticulture market conditions, the capabilities of those enterprises that can innovate, develop markets and manage investment risk need to be harnessed.

• Support resources in industry associations and government R&D are best utilised when directly aligned to across sector/industry issues but not necessarily active in the commercial arena.

• For ACLH to add incremental value, the industry sector associations in the Queensland lifestyle horticulture will need to commit to this plan, work together and in doing so capture synergies.

Applying this framework has led to drawing on existing resourcesfor the across industry agenda in the form of industry based working groups. Additional development funds are required to communicate the wider benefits of urban landscapes and deliver the development grant program.

Funding & return on investment This implementation plan requires $5.5m in funding over 5 years.

• $500k is required to invest in communicating the benefits of urban landscapes. It is recommended that this investment will be matched by the industry organisation in proportion to their wholesale market share to create a total of $1m. This investment is targeted to capitalise on the rising environmental awareness and concerns for sustainability. It is an attractive option as most sectors would benefit from any growth that was generated. If the gains are limited toproduction nurseries, turf, landscapers and indoor plants with amarket value of $926M, sales growth of 1.2 % or $11.1m and a netmargin of 10% would deliver a payback on the $1m invested in less than 1 year.

• $5m is requested for investment in the LHIDP. These funds are proposed to be invested at $1m per year for the next 5 years, with a maximum of $100k per grant and conditional to the grant amount invested being matched by recipients. This would generate $10m invested into growth initiatives over a 10 year period.

• Based on a ROI of 20%, new sales growth of 20% for the first 5 years and a net profit of 10%, would generate incremental sales of $21.4m in 5 years and $227m after 10 years. Based on sales per FTE of $250k this would generate the equivalent of 911 full time jobs over a 10 year period.

Other grant options

• All federal agribusiness grant programs are under review. However, the policy directions from the new federal government indicate a high priority for initiatives that aid climate change. Therefore, when these reviews are concluded some level of federal support appears possible. The proposed LHIDP is similar to the Federal Government New Industry Development Program (NIDP) that is currently under review.

Funding optionsGiven the stakeholders in this market are Qld based, it is most likely that the investment called for in this plan will appeal to those who have interests in the Qld wider community. Government agencies and regulators that influence the resources involved inlifestyle horticulture are clearly options.

Page 29Sustainable Lifestyle Horticulture Project – Final report Feb 08

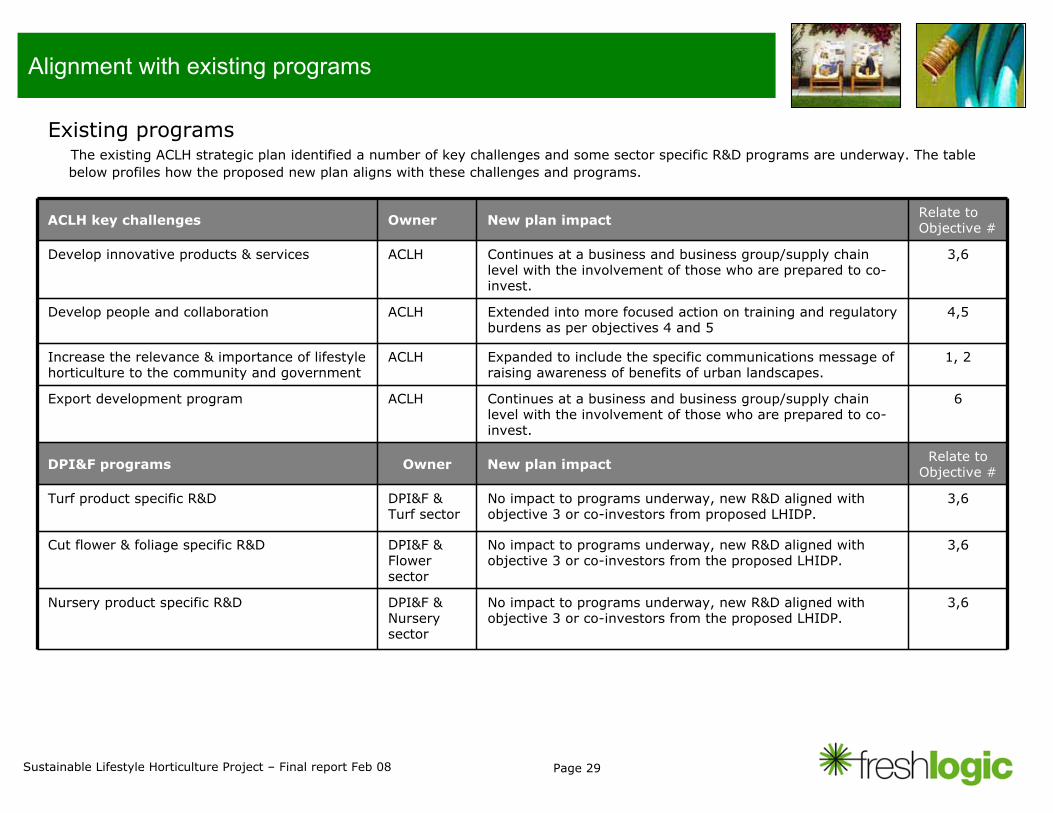

Alignment with existing programs

Existing programs The existing ACLH strategic plan identified a number of key challenges and some sector specific R&D programs are underway. The tablebelow profiles how the proposed new plan aligns with these challenges and programs.

3,6No impact to programs underway, new R&D aligned with objective 3 or co-investors from the proposed LHIDP.

DPI&F & Nursery sector

Nursery product specific R&D

3,6No impact to programs underway, new R&D aligned with objective 3 or co-investors from the proposed LHIDP.

DPI&F & Flowersector

Cut flower & foliage specific R&D

3,6No impact to programs underway, new R&D aligned with objective 3 or co-investors from proposed LHIDP.

DPI&F & Turf sector

Turf product specific R&D

Relate to Objective #New plan impactOwnerDPI&F programs

ACLH

ACLH

ACLH

ACLH

Owner

6Continues at a business and business group/supply chain level with the involvement of those who are prepared to co-invest.

Export development program

1, 2Expanded to include the specific communications message of raising awareness of benefits of urban landscapes.

Increase the relevance & importance of lifestyle horticulture to the community and government

4,5Extended into more focused action on training and regulatory burdens as per objectives 4 and 5

Develop people and collaboration

3,6Continues at a business and business group/supply chain level with the involvement of those who are prepared to co-invest.

Develop innovative products & services

Relate to Objective #New plan impactACLH key challenges

Page 30Sustainable Lifestyle Horticulture Project – Final report Feb 08

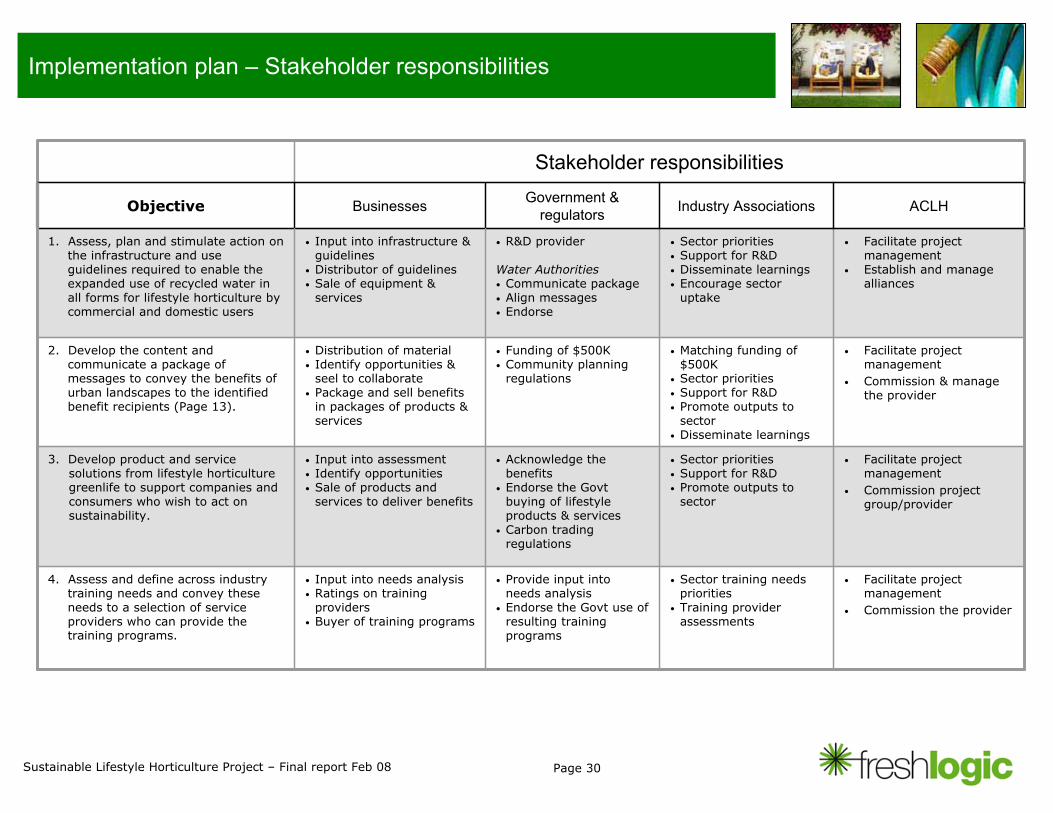

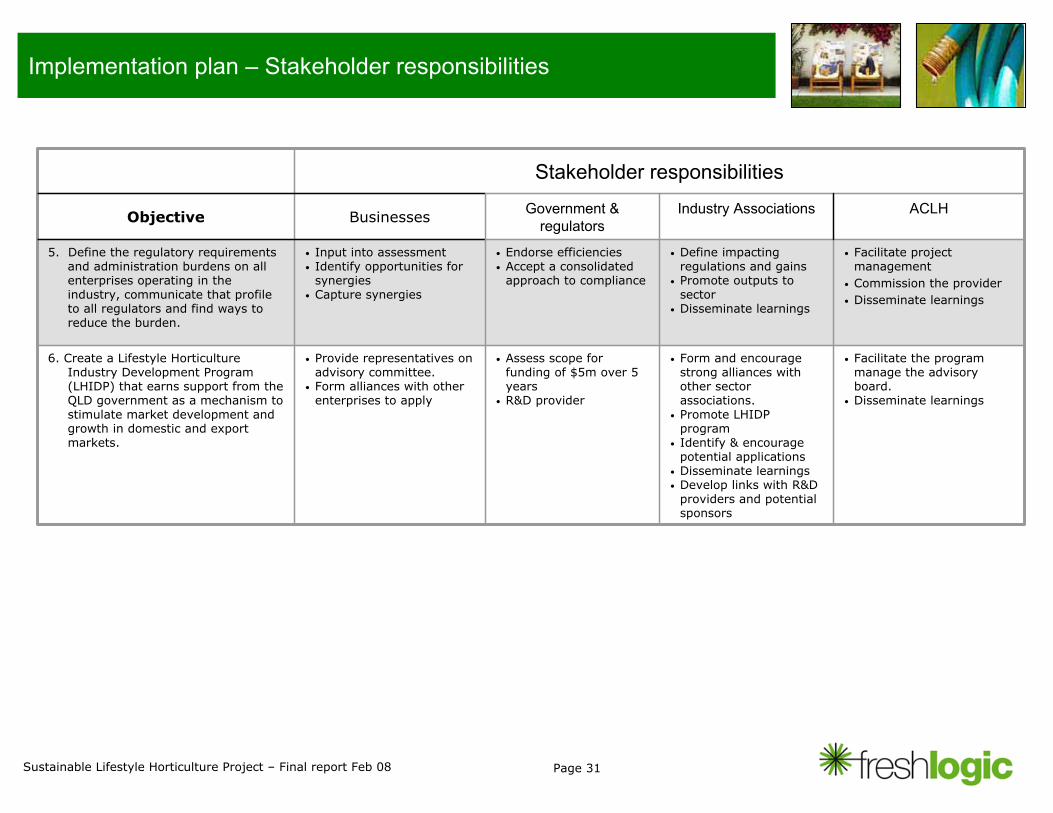

Implementation plan – Stakeholder responsibilities

• Sector training needs priorities

• Training provider assessments

• Sector priorities• Support for R&D • Promote outputs to

sector

• Matching funding of $500K

• Sector priorities• Support for R&D• Promote outputs to

sector• Disseminate learnings

• Sector priorities• Support for R&D• Disseminate learnings • Encourage sector

uptake

Industry Associations

Stakeholder responsibilities

ACLHGovernment & regulatorsBusinessesObjective

• Facilitate project management

• Commission the provider

• Provide input into needs analysis

• Endorse the Govt use of resulting training programs

• Input into needs analysis• Ratings on training

providers• Buyer of training programs

4. Assess and define across industry training needs and convey these needs to a selection of service providers who can provide the training programs.

• Facilitate project management

• Commission project group/provider

• Acknowledge the benefits

• Endorse the Govt buying of lifestyle products & services

• Carbon trading regulations

• Input into assessment• Identify opportunities• Sale of products and

services to deliver benefits

3. Develop product and service solutions from lifestyle horticulture greenlife to support companies and consumers who wish to act on sustainability.

• Facilitate project management

• Commission & manage the provider

• Funding of $500K• Community planning

regulations

• Distribution of material • Identify opportunities &

seel to collaborate• Package and sell benefits

in packages of products & services

2. Develop the content and communicate a package of messages to convey the benefits of urban landscapes to the identified benefit recipients (Page 13).

• Facilitate project management

• Establish and manage alliances

• R&D provider

Water Authorities• Communicate package• Align messages• Endorse

• Input into infrastructure & guidelines

• Distributor of guidelines• Sale of equipment &

services

1. Assess, plan and stimulate action on the infrastructure and use guidelines required to enable the expanded use of recycled water in all forms for lifestyle horticulture by commercial and domestic users

Page 31Sustainable Lifestyle Horticulture Project – Final report Feb 08

Implementation plan – Stakeholder responsibilities

• Form and encourage strong alliances with other sector associations.

• Promote LHIDP program

• Identify & encourage potential applications

• Disseminate learnings• Develop links with R&D

providers and potential sponsors

• Define impacting regulations and gains

• Promote outputs to sector

• Disseminate learnings

Industry Associations

Stakeholder responsibilities

ACLHGovernment & regulatorsBusinessesObjective

• Facilitate the program manage the advisory board.

• Disseminate learnings

• Assess scope for funding of $5m over 5 years

• R&D provider

• Provide representatives on advisory committee.

• Form alliances with other enterprises to apply

6. Create a Lifestyle Horticulture Industry Development Program (LHIDP) that earns support from the QLD government as a mechanism to stimulate market development and growth in domestic and export markets.

• Facilitate project management

• Commission the provider • Disseminate learnings

• Endorse efficiencies • Accept a consolidated

approach to compliance

• Input into assessment• Identify opportunities for

synergies• Capture synergies

5. Define the regulatory requirements and administration burdens on all enterprises operating in the industry, communicate that profile to all regulators and find ways to reduce the burden.

Page 32Sustainable Lifestyle Horticulture Project – Final report Feb 08

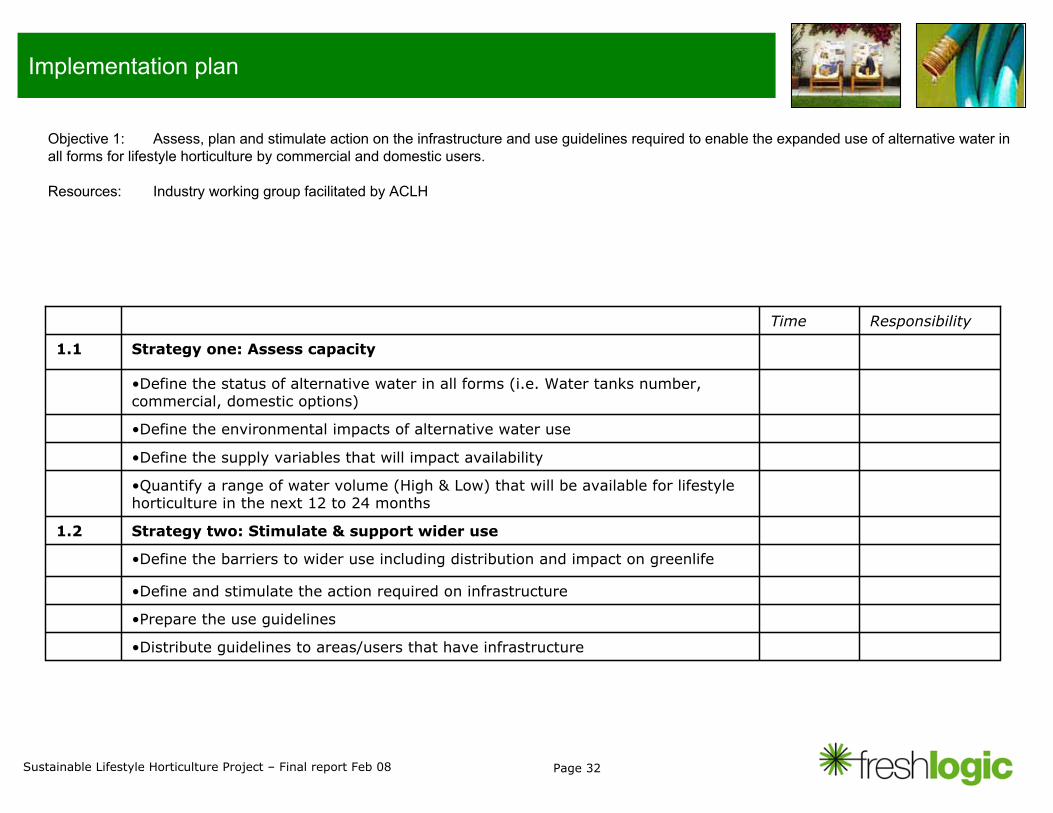

Implementation plan

•Define the status of alternative water in all forms (i.e. Water tanks number, commercial, domestic options)

Time

•Distribute guidelines to areas/users that have infrastructure

Strategy one: Assess capacity1.1

•Prepare the use guidelines

•Define and stimulate the action required on infrastructure

•Define the barriers to wider use including distribution and impact on greenlife

Strategy two: Stimulate & support wider use1.2

•Quantify a range of water volume (High & Low) that will be available for lifestyle horticulture in the next 12 to 24 months

•Define the supply variables that will impact availability

•Define the environmental impacts of alternative water use

Responsibility

Objective 1: Assess, plan and stimulate action on the infrastructure and use guidelines required to enable the expanded use of alternative water in all forms for lifestyle horticulture by commercial and domestic users.

Resources: Industry working group facilitated by ACLH

Page 33Sustainable Lifestyle Horticulture Project – Final report Feb 08

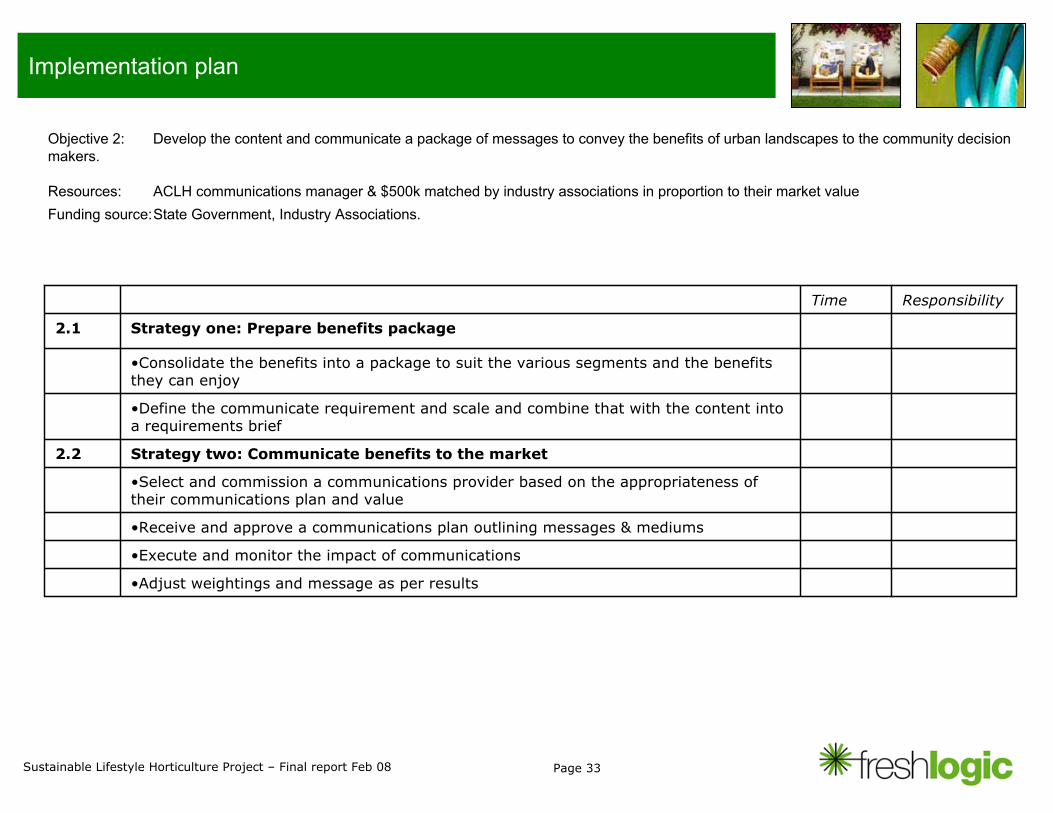

Implementation plan

•Adjust weightings and message as per results

Strategy one: Prepare benefits package2.1

•Execute and monitor the impact of communications

•Receive and approve a communications plan outlining messages & mediums

•Select and commission a communications provider based on the appropriateness of their communications plan and value

Strategy two: Communicate benefits to the market2.2

•Define the communicate requirement and scale and combine that with the content into a requirements brief

•Consolidate the benefits into a package to suit the various segments and the benefits they can enjoy

ResponsibilityTime

Objective 2: Develop the content and communicate a package of messages to convey the benefits of urban landscapes to the community decision makers.

Resources: ACLH communications manager & $500k matched by industry associations in proportion to their market valueFunding source:State Government, Industry Associations.

Page 34Sustainable Lifestyle Horticulture Project – Final report Feb 08

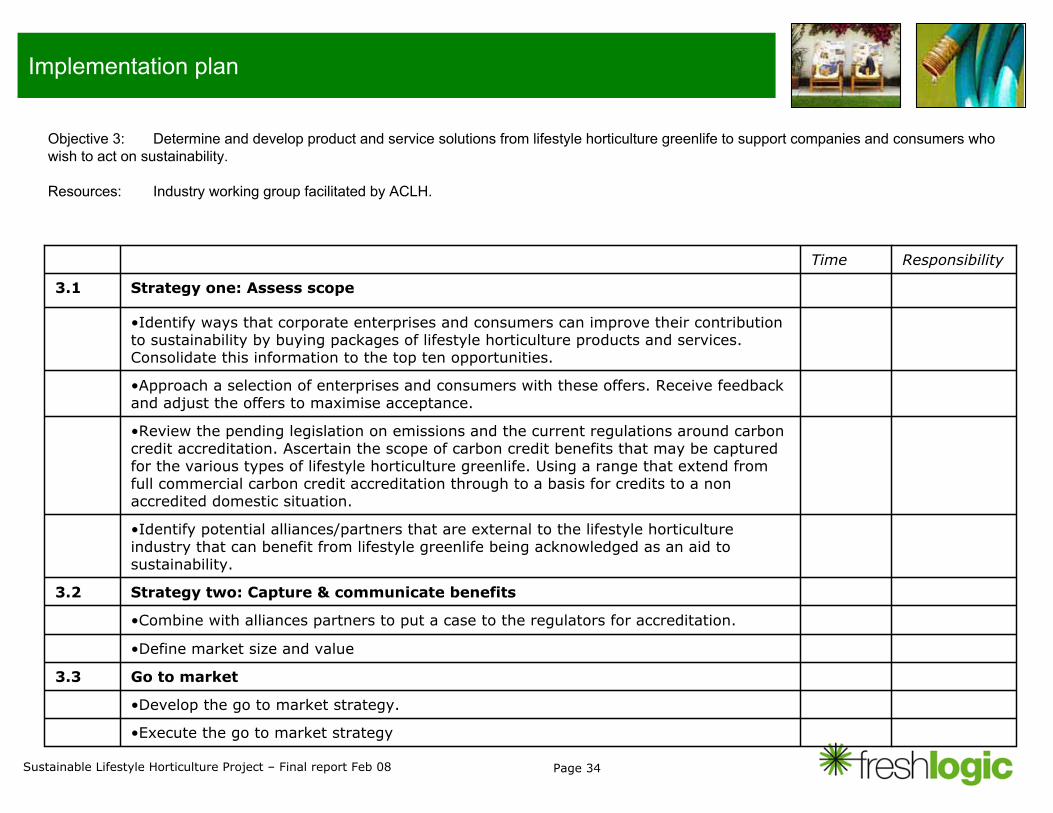

Implementation plan