PRCA Membership Benchmarking Survey:Key Findings 2008

June 2008

2

Background

• Annual PR industry benchmarking survey undertaken by Russell Bell (independent research consultant)

• 141 PRCA members contacted (incl. 10 new contacts after interviewing began)

• Three elements in the survey:– 65 HR Director questionnaires– 73 MD/CEO questionnaires– 67 FD questionnaires

• Four consultancy size bands defined by income:– Small: up to £850K– Medium: £851K - £2.5 million– Large: £2.51 - £5 million– Very large: greater than £5 million

Russell Bell, Research [email protected]

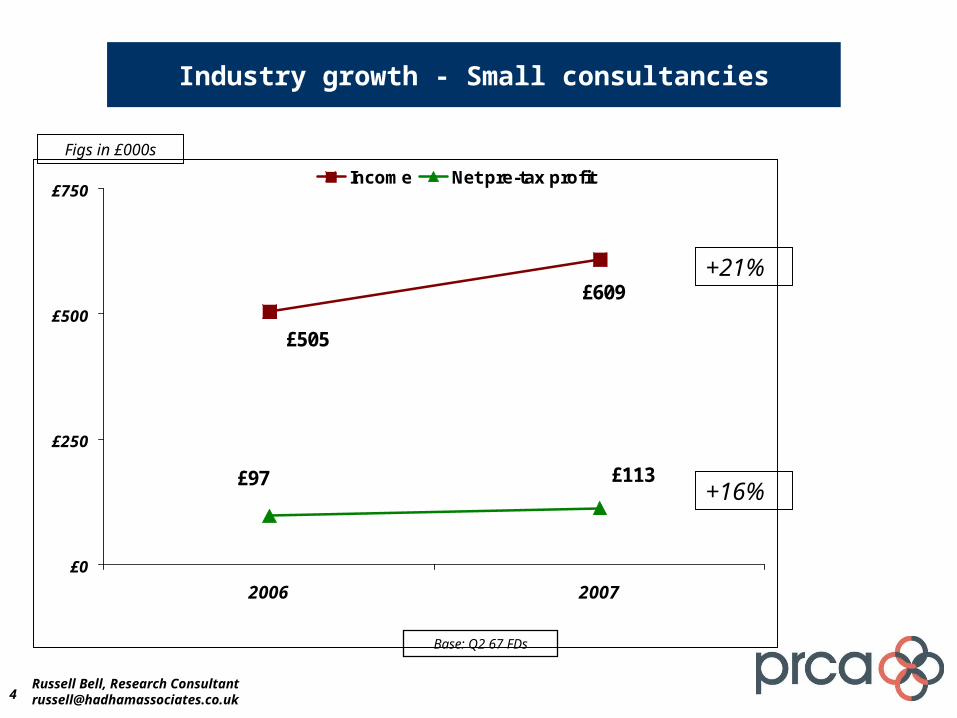

Finance Directors

4

Industry growth - Small consultancies

£609

£505

£113£97

£0

£250

£500

£750

2006 2007

Income Net pre-tax profit

+21%

Figs in £000s

Base: Q2 67 FDs

+16%

Russell Bell, Research [email protected]

5

Industry growth - Medium consultancies

£1,484£1,396

£208£210

£0

£250

£500

£750

£1,000

£1,250

£1,500

£1,750

2006 2007

Income Net pre-tax profit

Figs in £000s

+6%

-1%

Base: Q2 67 FDs

Russell Bell, Research [email protected]

6

Industry growth - Large consultancies

£3,608£3,372

£609£534

£0

£500

£1,000

£1,500

£2,000

£2,500

£3,000

£3,500

£4,000

£4,500

2006 2007

Income Net pre-tax profit

Base: Q2 67 FDs

Figs in £000s

+7%

+14%

Russell Bell, Research [email protected]

7

Industry growth – Very large consultancies

£8,655£8,110

£1,347£1,337

£0

£2,000

£4,000

£6,000

£8,000

£10,000

2006 2007

Income Net pre-tax profit

+7%

+1%

Figs in £000s

Base: Q2 67 FDs

Russell Bell, Research [email protected]

8

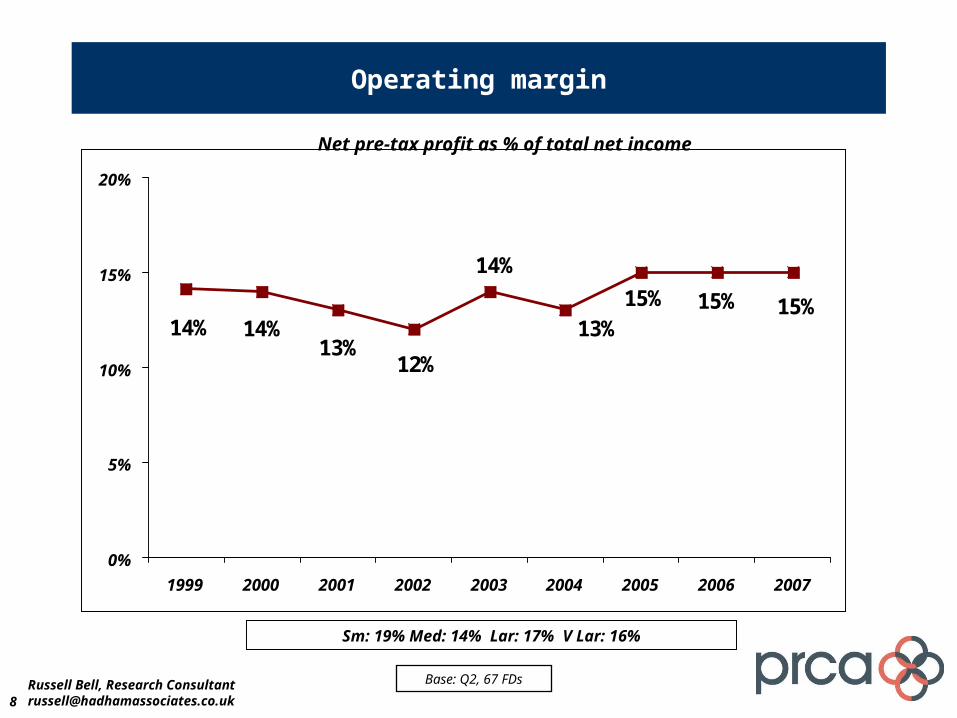

Operating margin

15%15%15%13%

14%

12%13%

14%14%

0%

5%

10%

15%

20%

1999 2000 2001 2002 2003 2004 2005 2006 2007

Base: Q2, 67 FDs

Sm: 19% Med: 14% Lar: 17% V Lar: 16%

Net pre-tax profit as % of total net income

Russell Bell, Research [email protected]

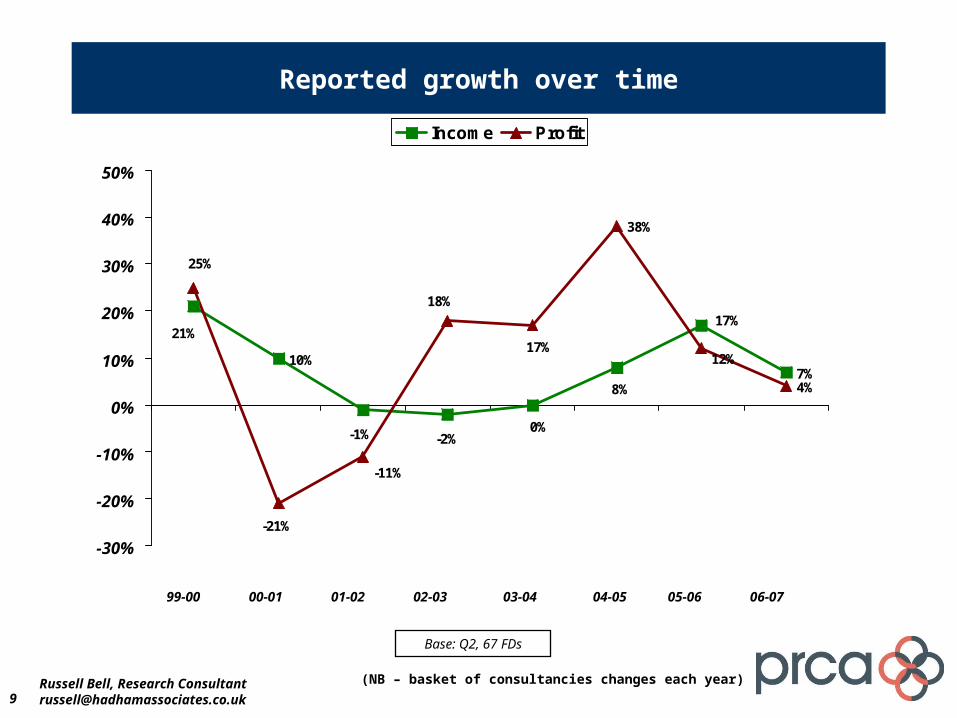

9

Reported growth over time

Base: Q2, 67 FDs

(NB – basket of consultancies changes each year)

10%7%4%

17%

8%

0%-2%-1%

21%

12%

38%

17%

18%

-11%

-21%

25%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Income Profit

05-0604-0503-0402-0301-0200-0199-00

Russell Bell, Research [email protected]

06-07

10

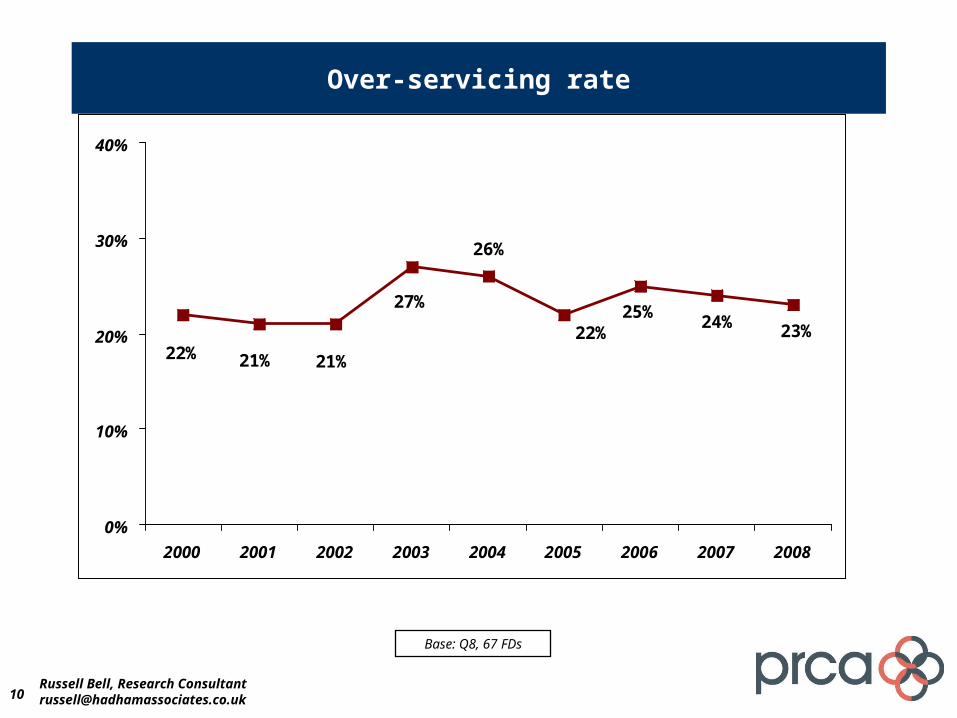

Over-servicing rate

23%24%25%

22%

26%

27%

21%21%22%

0%

10%

20%

30%

40%

2000 2001 2002 2003 2004 2005 2006 2007 2008

Base: Q8, 67 FDs

Russell Bell, Research [email protected]

11

Offer payment by results/performance related pricing

28%

38%

35%36%

27%29%

19%

0%

10%

20%

30%

40%

2002 2003 2004 2005 2006 2007 2008

Base: Q17, 67 FDs

Russell Bell, Research [email protected]

HR Directors

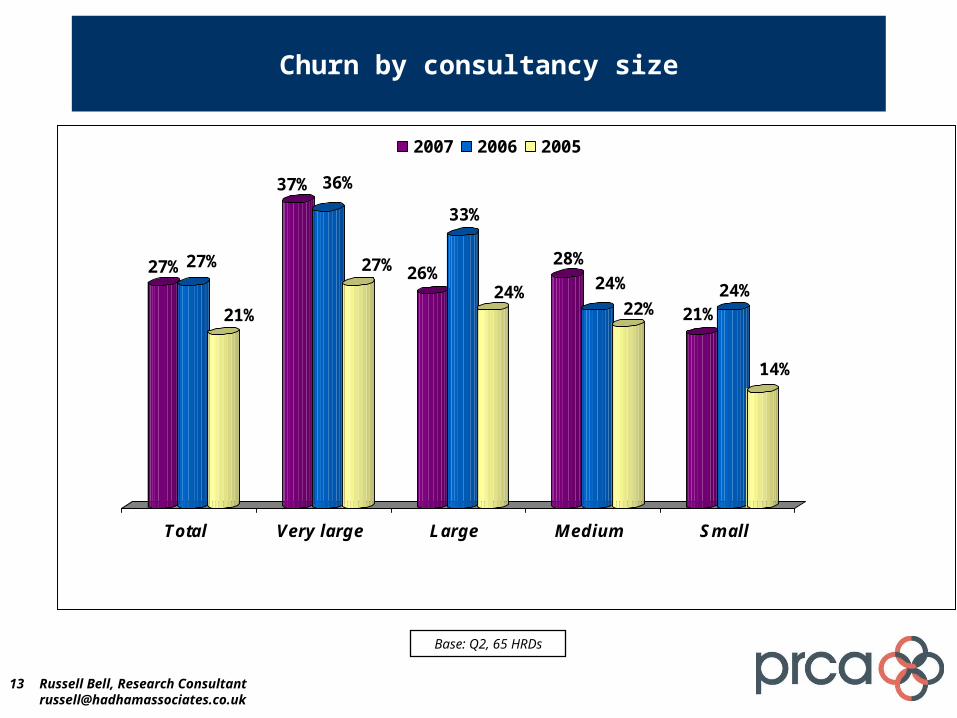

13

Churn by consultancy size

27% 27%

21%

37% 36%

27% 26%

33%

24%

28%

24%

22% 21%24%

14%

Total Very large Large Medium Small

2007 2006 2005

Base: Q2, 65 HRDs

Russell Bell, Research [email protected]

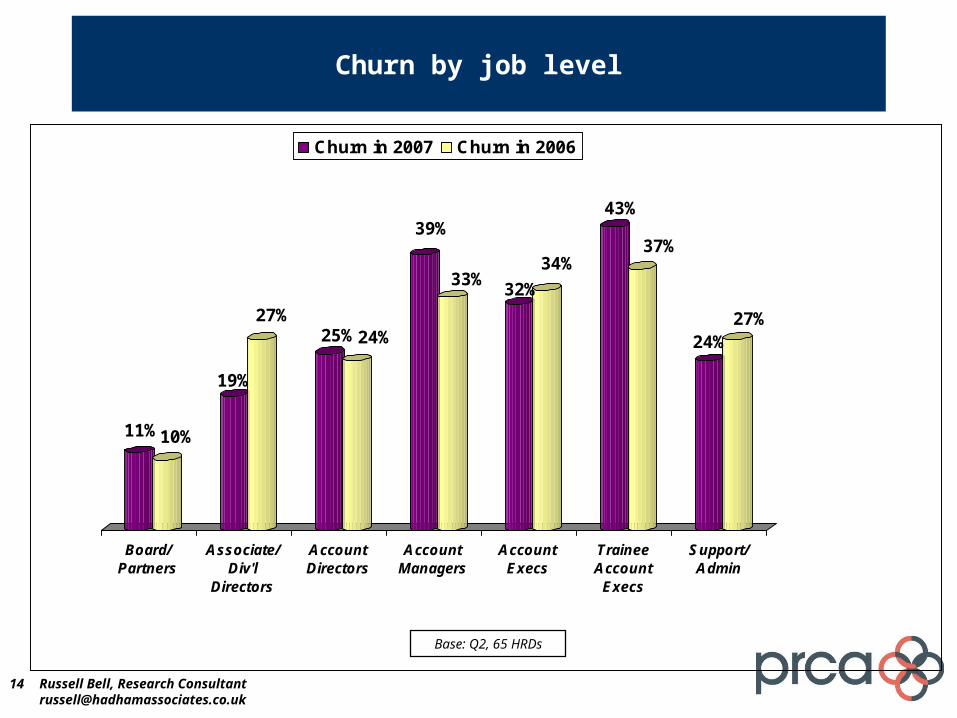

14

Churn by job level

11%10%

19%

27%25%24%

39%

33%32%

34%

43%

37%

24%27%

Board/Partners

Associate/Div'l

Directors

AccountDirectors

AccountManagers

AccountExecs

TraineeAccount

Execs

Support/Admin

Churn in 2007 Churn in 2006

Base: Q2, 65 HRDs

Russell Bell, Research [email protected]

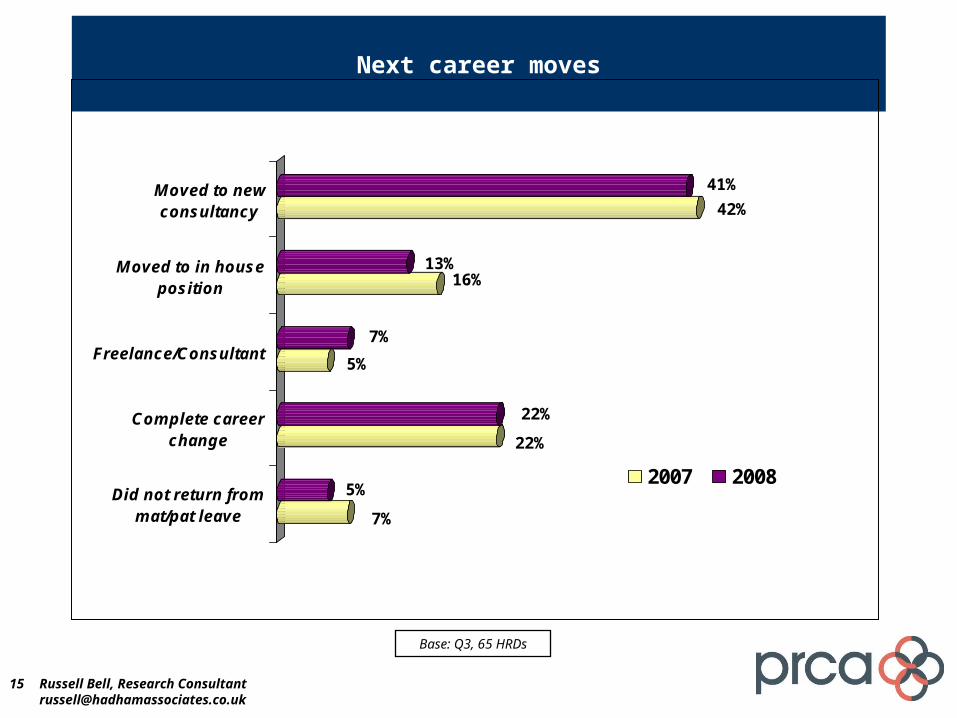

15

Next career moves

7%

5%

22%

22%

5%

7%

16%13%

42%

41%

Did not return frommat/pat leave

Complete careerchange

Freelance/Consultant

Moved to in houseposition

Moved to newconsultancy

2007 2008

Base: Q3, 65 HRDs

Russell Bell, Research [email protected]

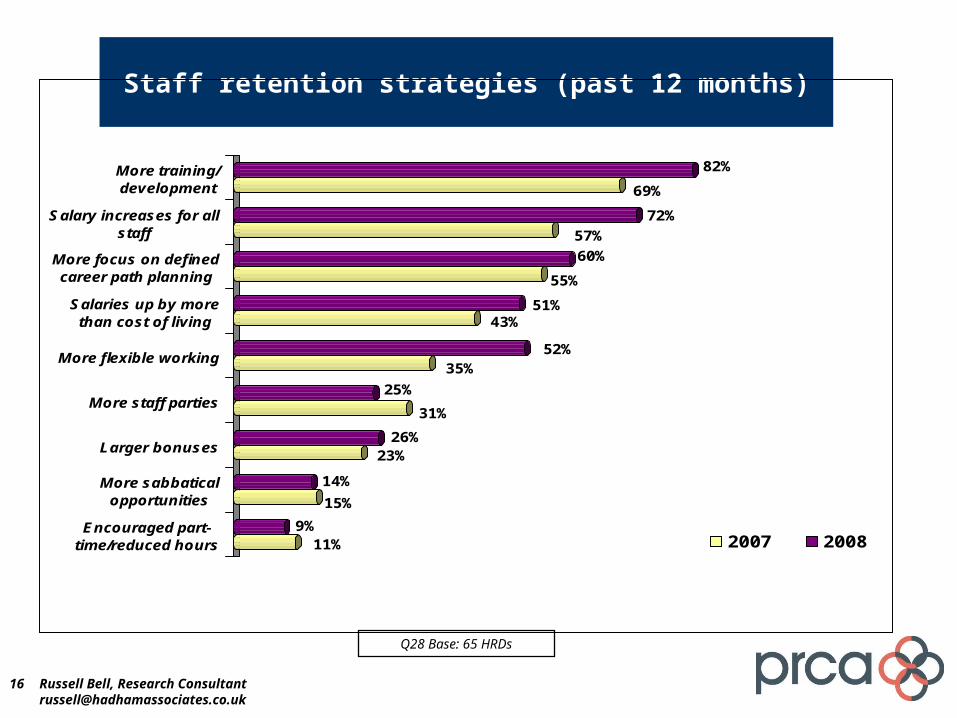

16

Staff retention strategies (past 12 months)

11%9%

15%

14%

23%26%

31%

25%

35%52%

43%51%

55%

60%

57%

72%

69%

82%

Encouraged part-time/reduced hours

More sabbaticalopportunities

Larger bonuses

More staff parties

More flexible working

Salaries up by morethan cost of living

More focus on definedcareer path planning

Salary increases for allstaff

More training/development

2007 2008

Q28 Base: 65 HRDs

Russell Bell, Research [email protected]

17

Employment prospects: coming 12 months

8%

18%

2%

2%

0

5%

69%

54%

83%

77%

Not clear yet

Redundancies/staffcuts likely

Reduce staffnumbers throughnon-replacement

Likely to berecruiting senior

staff

Likely to berecruiting junior

staff

2007 2008

Q29 Base: 65 HRDs

Russell Bell, Research [email protected]

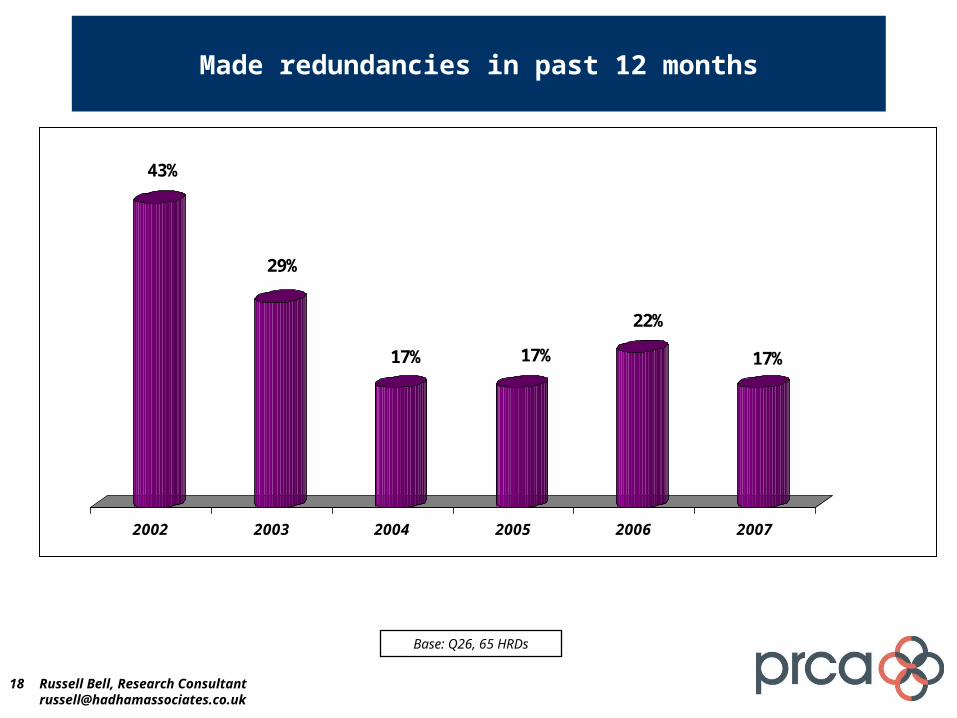

18

Made redundancies in past 12 months

43%

29%

17% 17%

22%

17%

2002 2003 2004 2005 2006 2007

Base: Q26, 65 HRDs

Russell Bell, Research [email protected]

19

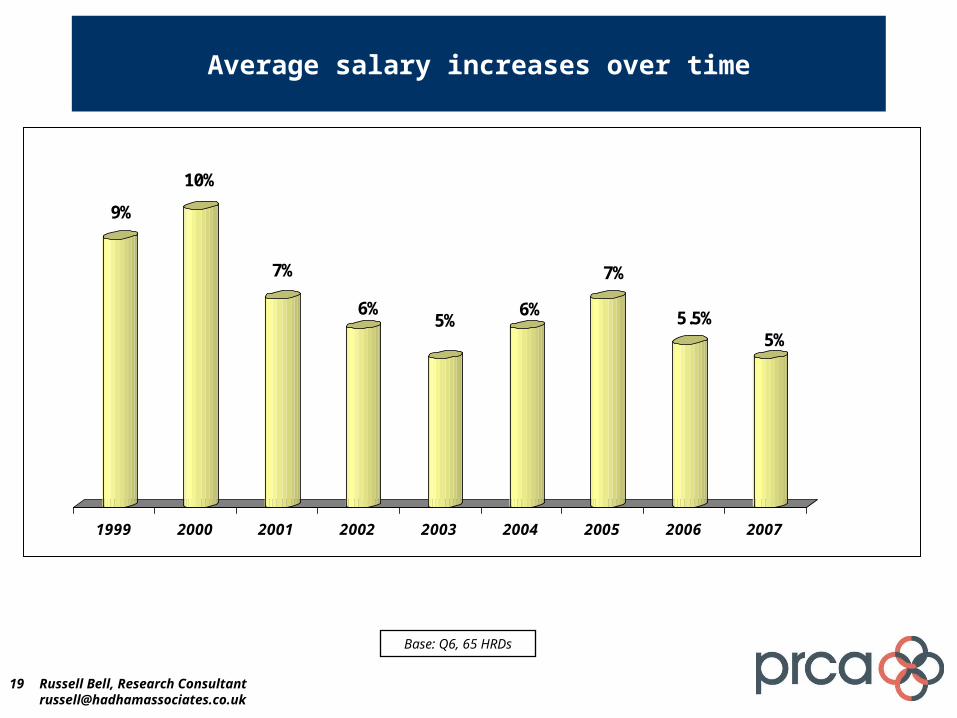

Average salary increases over time

9%

10%

7%

6%5%

6%

7%

5.5%5%

1999 2000 2001 2002 2003 2004 2005 2006 2007

Base: Q6, 65 HRDs

Russell Bell, Research [email protected]

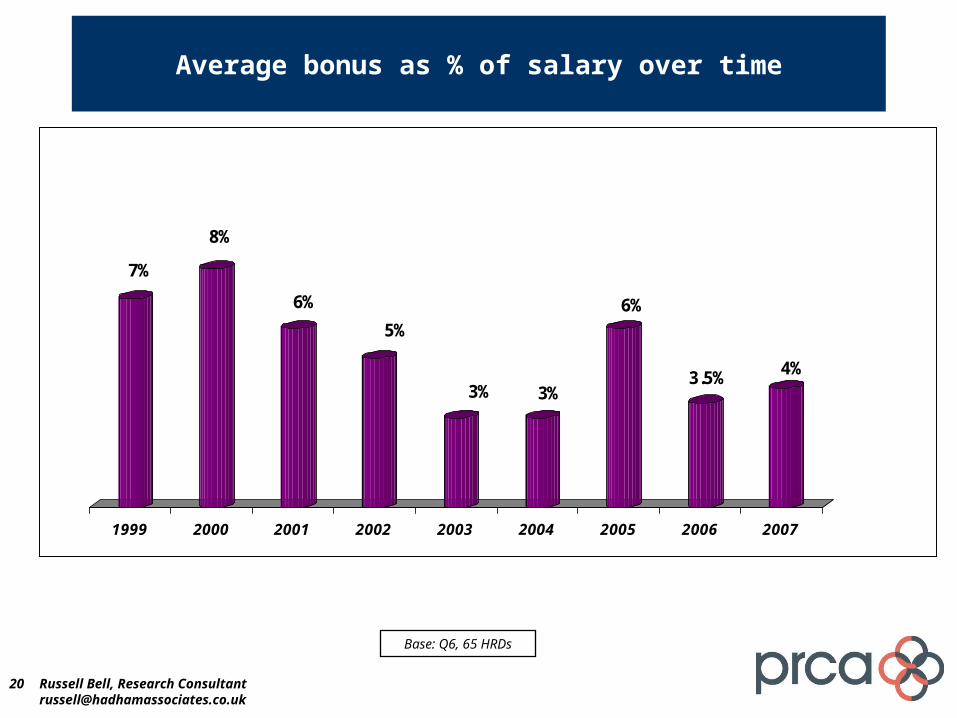

20

Average bonus as % of salary over time

7%

8%

6%

5%

3% 3%

6%

3.5% 4%

1999 2000 2001 2002 2003 2004 2005 2006 2007

Base: Q6, 65 HRDs

Russell Bell, Research [email protected]

21

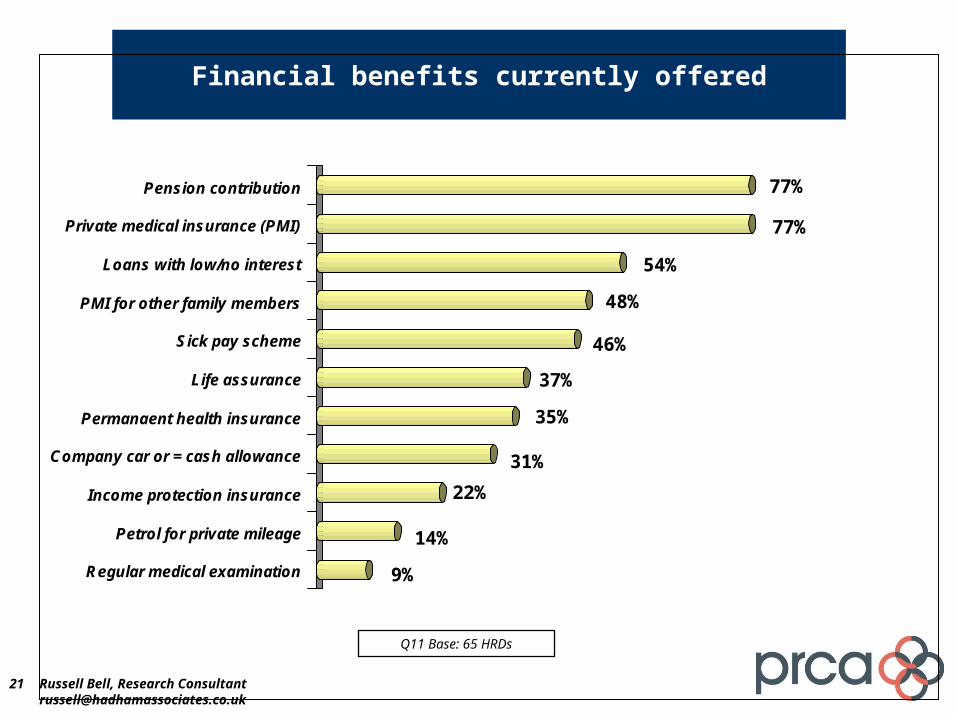

Financial benefits currently offered

9%

14%

22%

31%

35%

37%

46%

48%

54%

77%

77%

Regular medical examination

Petrol for private mileage

Income protection insurance

Company car or = cash allowance

Permanaent health insurance

Life assurance

Sick pay scheme

PMI for other family members

Loans with low/no interest

Private medical insurance (PMI)

Pension contribution

Q11 Base: 65 HRDs

Russell Bell, Research [email protected]

22

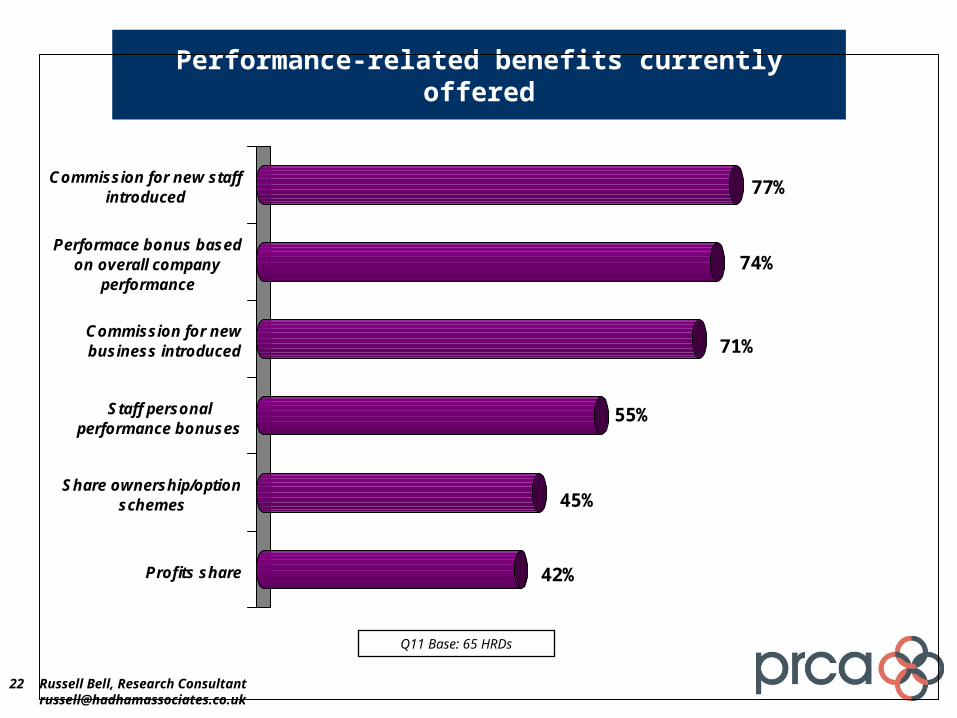

Performance-related benefits currently offered

42%

45%

55%

71%

74%

77%

Profits share

Share ownership/optionschemes

Staff personalperformance bonuses

Commission for newbusiness introduced

Performace bonus basedon overall company

performance

Commission for new staffintroduced

Q11 Base: 65 HRDs

Russell Bell, Research [email protected]

23

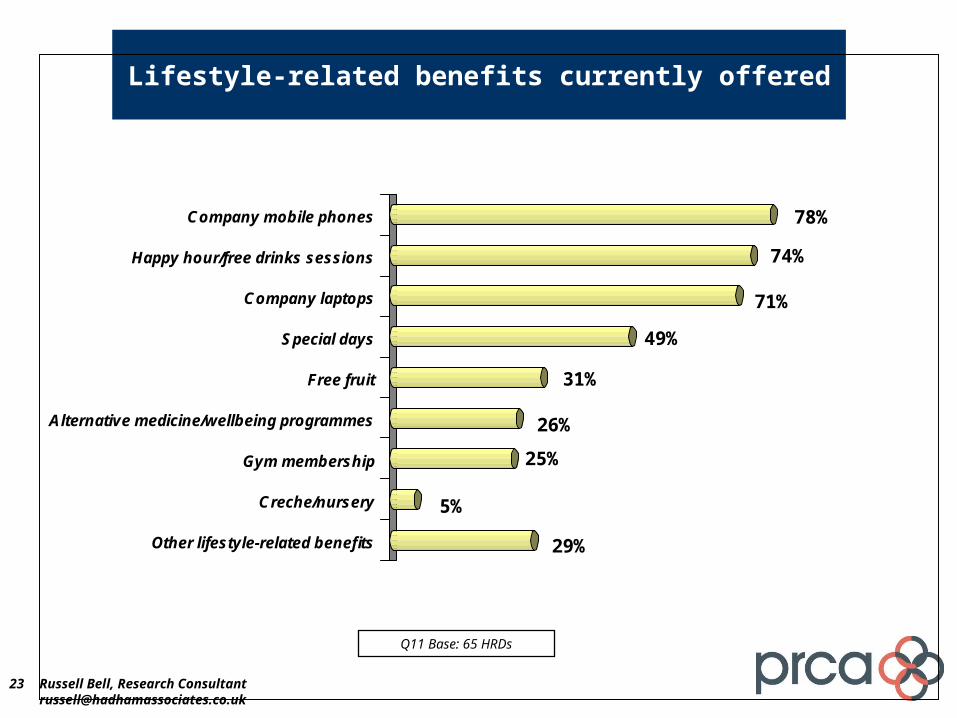

Lifestyle-related benefits currently offered

29%

5%

25%

26%

31%

49%

71%

74%

78%

Other lifestyle-related benefits

Creche/nursery

Gym membership

Alternative medicine/wellbeing programmes

Free fruit

Special days

Company laptops

Happy hour/free drinks sessions

Company mobile phones

Q11 Base: 65 HRDs

Russell Bell, Research [email protected]

24

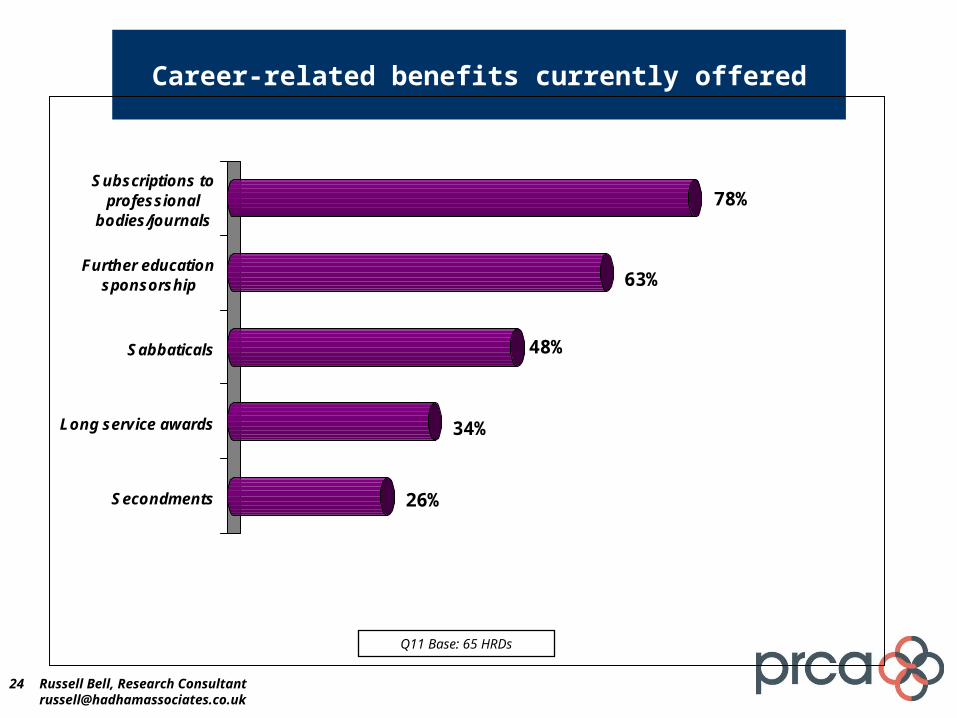

Career-related benefits currently offered

26%

34%

48%

63%

78%

Secondments

Long service awards

Sabbaticals

Further educationsponsorship

Subscriptions toprofessional

bodies/journals

Q11 Base: 65 HRDs

Russell Bell, Research [email protected]

MDs/CEOs

26

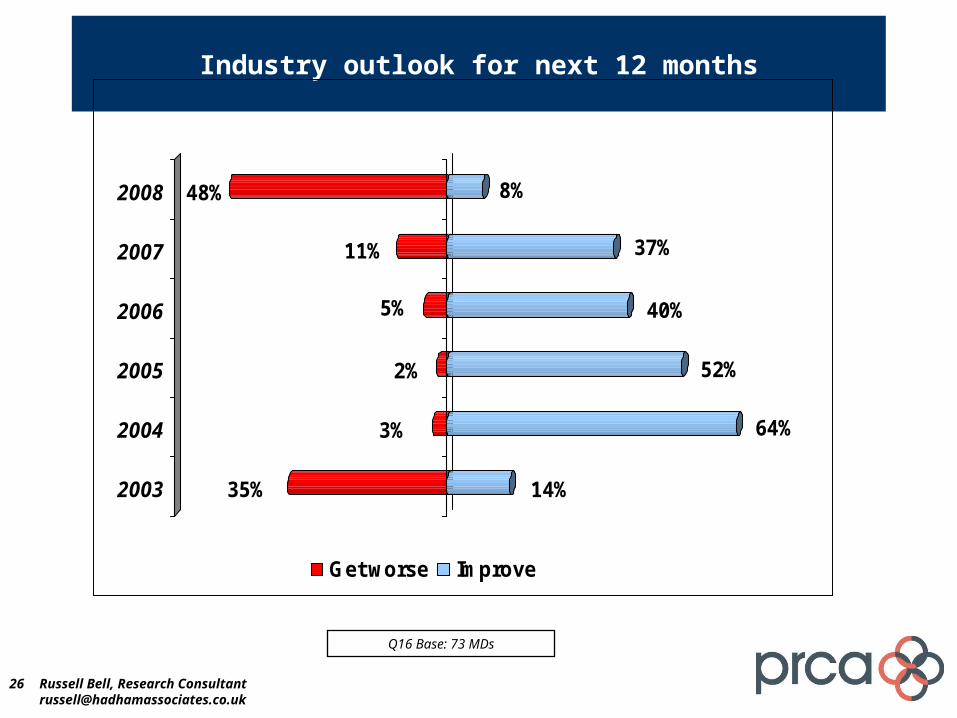

Industry outlook for next 12 months

35% 14%

3% 64%

2% 52%

5% 40%

11% 37%

48% 8%2008

2007

2006

2005

2004

2003

Get worse Improve

Q16 Base: 73 MDs

Russell Bell, Research [email protected]

27

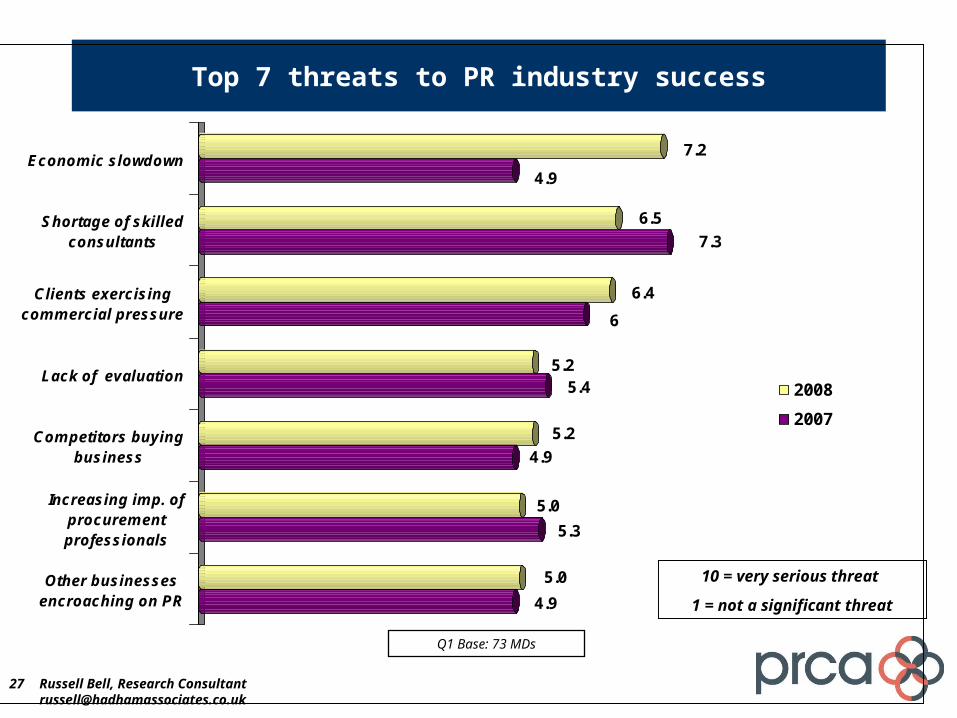

Top 7 threats to PR industry success

4.9

5.0

5.3

5.0

4.9

5.2

5.45.2

6

6.4

7.3

6.5

4.9

7.2

Other businessesencroaching on PR

Increasing imp. ofprocurementprofessionals

Competitors buyingbusiness

Lack of evaluation

Clients exercisingcommercial pressure

Shortage of skilledconsultants

Economic slowdown

2008

2007

10 = very serious threat

1 = not a significant threat

Q1 Base: 73 MDs

Russell Bell, Research [email protected]

28

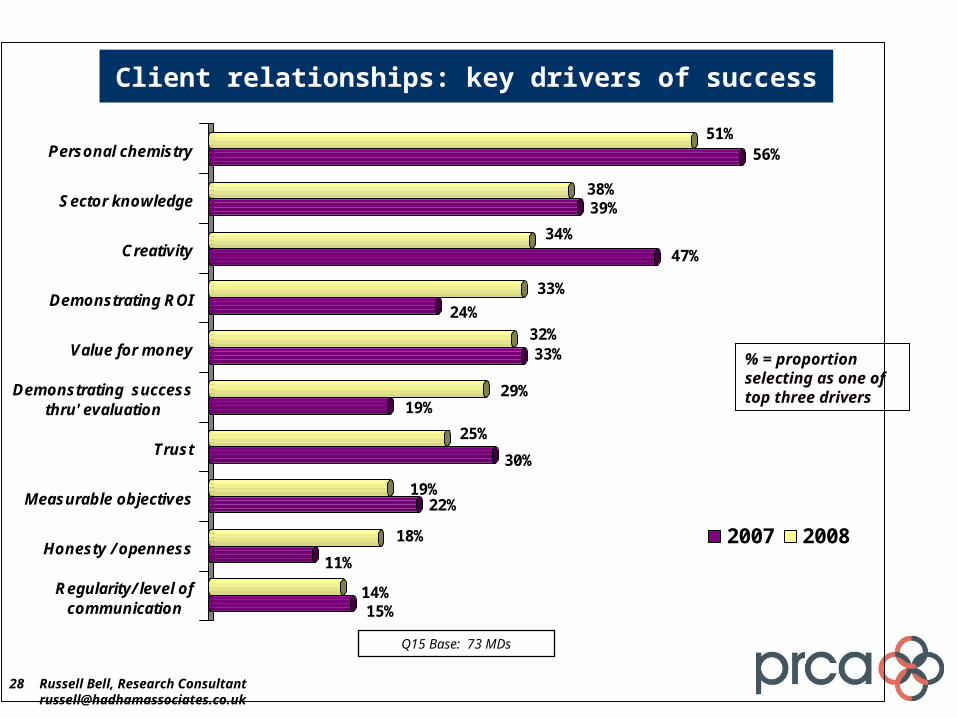

Client relationships: key drivers of success

15%14%

11%

18%

22%19%

30%

25%

19%29%

33%32%

24%

33%

47%34%

39%38%

56%51%

Regularity/ level ofcommunication

Honesty / openness

Measurable objectives

Trust

Demonstrating successthru' evaluation

Value for money

Demonstrating ROI

Creativity

Sector knowledge

Personal chemistry

2007 2008

% = proportion selecting as one of top three drivers

Q15 Base: 73 MDs

Russell Bell, Research [email protected]

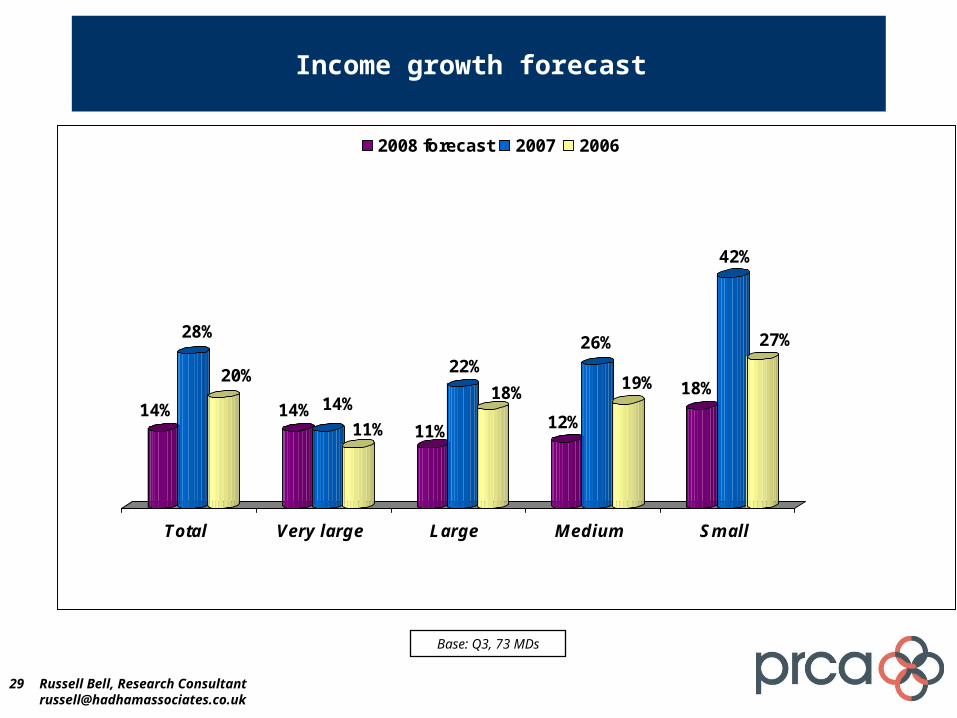

29

Income growth forecast

14%

28%

20%

14% 14%

11% 11%

22%

18%

12%

26%

19% 18%

42%

27%

Total Very large Large Medium Small

2008 forecast 2007 2006

Base: Q3, 73 MDs

Russell Bell, Research [email protected]

30

Operating margin growth forecast 2007 vs 2006

12%

22%21%

6%

21%

18% 19%17%

7%

11%

18%

24%

13%

32%

25%

Total Very large Large Medium Small

2008 forecast 2007 2006

Base: Q4, 73 MDs

Russell Bell, Research [email protected]

31

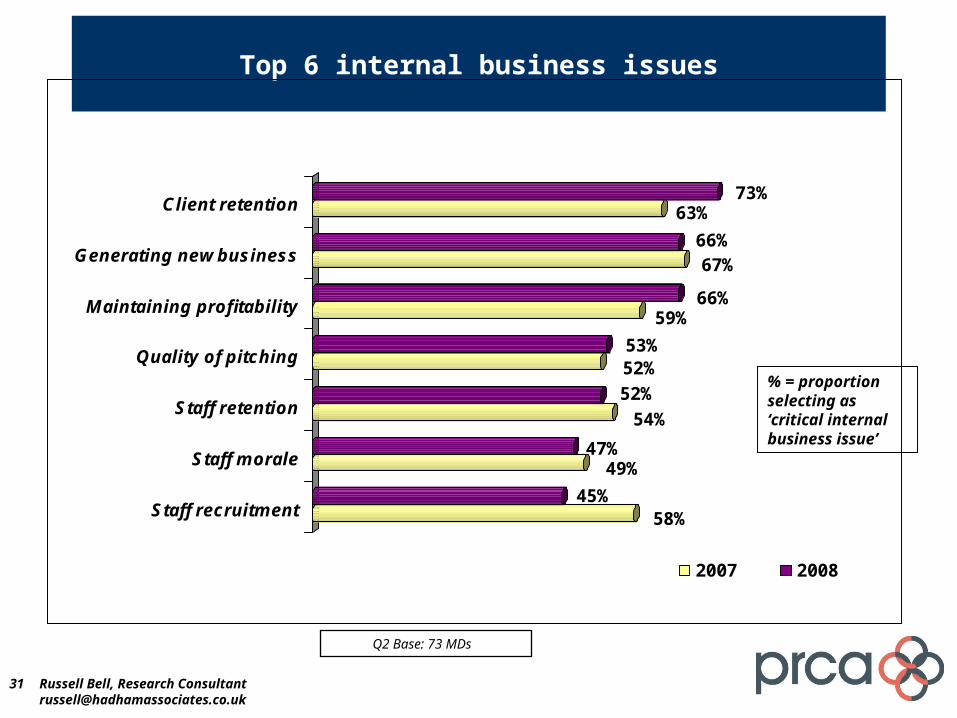

Top 6 internal business issues

58%45%

49%47%

54%

52%

52%53%

59%66%

67%66%

63%73%

Staff recruitment

Staff morale

Staff retention

Quality of pitching

Maintaining profitability

Generating new business

Client retention

2007 2008

% = proportion selecting as ‘critical internal business issue’

Q2 Base: 73 MDs

Russell Bell, Research [email protected]

32

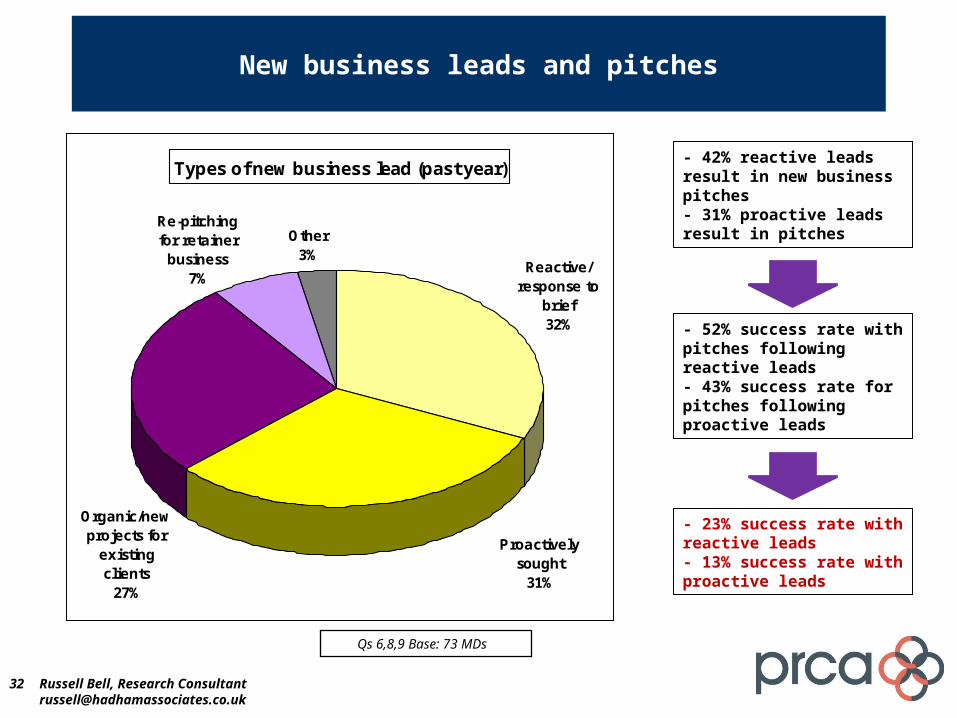

New business leads and pitches

Types of new business lead (past year)

Reactive/ response to

brief32%

Other 3%

Re-pitching for retainer

business7%

Proactively sought

31%

Organic/new projects for

existing clients

27%

- 42% reactive leads result in new business pitches- 31% proactive leads result in pitches

- 52% success rate with pitches following reactive leads- 43% success rate for pitches following proactive leads

Qs 6,8,9 Base: 73 MDs

Russell Bell, Research [email protected]

- 23% success rate with reactive leads - 13% success rate with proactive leads

33

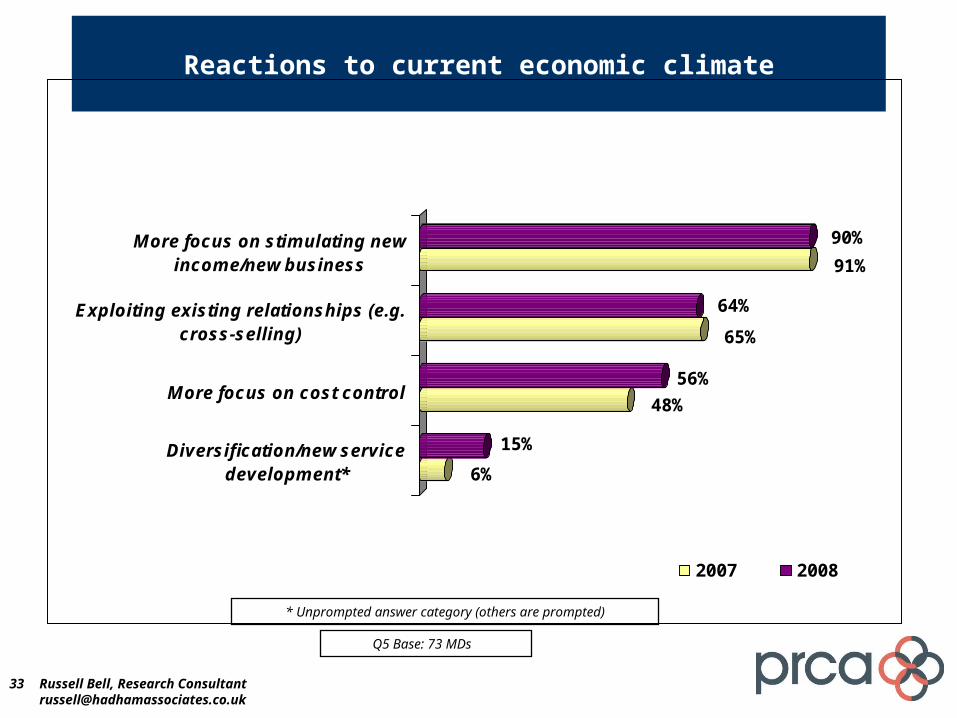

Reactions to current economic climate

6%

15%

48%

56%

65%

64%

91%

90%

Diversification/new servicedevelopment*

More focus on cost control

Exploiting existing relationships (e.g.cross-selling)

More focus on stimulating newincome/new business

2007 2008

Q5 Base: 73 MDs

Russell Bell, Research [email protected]

* Unprompted answer category (others are prompted)

34

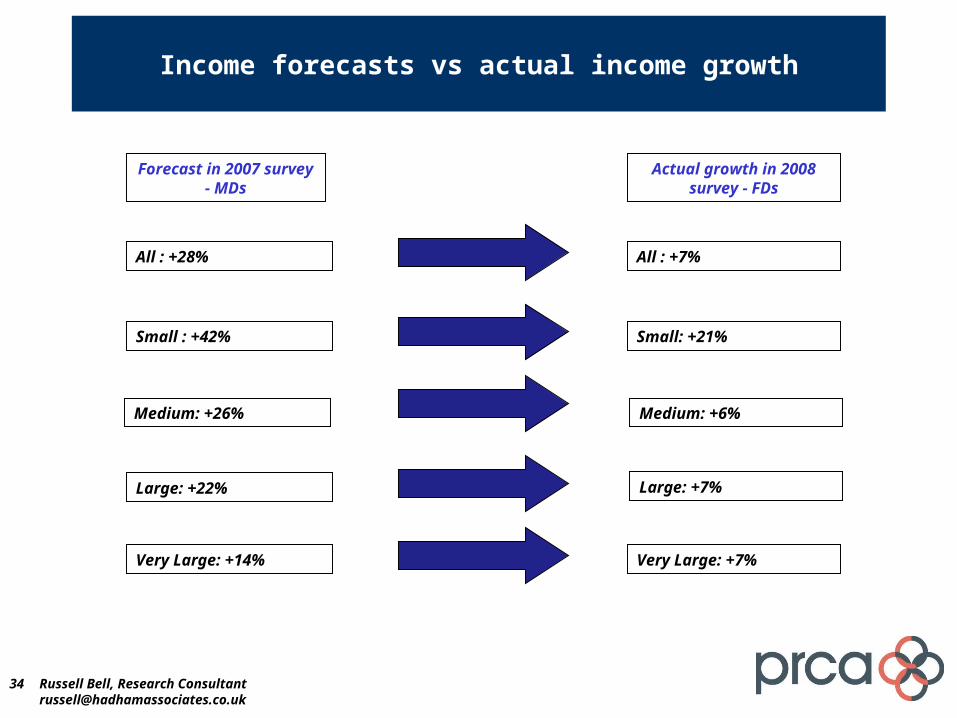

Income forecasts vs actual income growth

Forecast in 2007 survey - MDs

Actual growth in 2008 survey - FDs

All : +28% All : +7%

Small : +42%

Medium: +26%

Large: +22%

Very Large: +14%

Small: +21%

Medium: +6%

Large: +7%

Very Large: +7%

Russell Bell, Research [email protected]

End

For more information, please contact:Russell Bell on 07747 194581 or +44 7867 531557