Information asymmetry and small business in online auction marketAuthor(s): Chia-Hung Sun and Kang E. LiuSource: Small Business Economics, Vol. 34, No. 4 (May 2010), pp. 433-444Published by: SpringerStable URL: http://www.jstor.org/stable/40650975 .

Accessed: 15/06/2014 13:44

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Springer is collaborating with JSTOR to digitize, preserve and extend access to Small Business Economics.

http://www.jstor.org

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

Small Bus Econ (2010) 34:433-444 DOI 10.1007/sl 1187-008-9160-8

Information asymmetry and small business in online auction market

Chia-Hung Sun * Kang E. Liu

Accepted: 17 November 2008 / Published online: 6 January 2009 © Springer Science+Business Media, LLC. 2008

Abstract This paper explores how seller reputation affects auction prices using detailed Taiwanese data. Our empirical results show that returns to reputation are nonlinear and differ considerably across different reputation scores. Marginal returns to scores drop sharply after the first reputation quartile, indicating that building up sellers' reputation is extremely important, especially in the early stage. Our study reveals that the mechanism of seller reputations is effective in mitigating asymmetric information in online auctions.

Keywords Internet auction • Buy it now •

Spline regression • Taiwan

JEL Classifications D8 D44 L26 L86

1 Introduction

Small businesses and entrepreneurship are the most important parts of the industrial world, as shown in 2004 whereby more than 99% of all companies in the

C.-H. Sun (IS) • K. E. Liu National Chung Cheng University, Min-Hsiung, Chia-Yi, Taiwan, ROC e-mail: ecdchs@ ccu.edu. tw

USA were small businesses. Entrepreneurship has become a better option for people to increase income on their own and to improve their quality of life. Moreover, the changing economy (globalization, increased competition, and advanced computer tech- nology) fertilizes the business environment for entrepreneurs. The dramatic growth of Internet usage has especially changed consumers' purchasing behavior and hence has created enormous potential opportunities for entrepreneurs.

The rise of eBay and several other Internet auction sites provides channels for individuals and small businesses to trade goods at real-time market prices around the globe.1 With almost no setup costs, an Internet auction offers instant product exposure and global marketing for entrepreneurial sellers to achieve a great advantage over other marketing strategies. Despite growing at an impressive pace, the increase in Internet scams should come as no surprise. According to Internet Fraud Watch's 2006 report, Internet scams of online auctions (mainly goods never delivered or misrepresented) ranked at the top of overall com- plaints, accounting for 34% of total complaints, and the average loss was US $1,3 3 1.2

1 For instance, one online auction site (www.ebay.com.au) is the primary source of income for more than 17,000 Australians, according to The Australian newspaper (March 17, 2007).

Internet Fraud Watch's website: www.fraud.org/internet/ intset.htm.

Ô Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

434 C.-H. Sun, K. E. Liu

When bidders cannot personally inspect an item's

quality before bidding in an online auction, low-

quality and cheaper products (or lemons) may drive

high-quality products out of markets (Akerlof 1970). Such asymmetric information commonly occurs in used car markets, online auction markets, labor markets (Spence 1973; Harris and Holmstrom 1982), insurance markets (Rothschild and Stiglitz 1976), and credit markets (Jaffee and Russell 1976; Stiglitz and Weiss 198 1).3 To alleviate this informa- tion asymmetry problem, online auction sites (such as

eBay and Yahoo! Auction) adopt the feedback mechanism of self-enforcement, using the seller

reputation measured by the number of ratings posted by bidders. How these publicly available com- ments - that is, seller reputation scores - mitigate asymmetric information has become an interesting empirical issue to study.

A growing number of studies have examined the

relationship between seller characteristics and auction

prices in recent economic literature, many of which focus on how seller reputation influences prices when

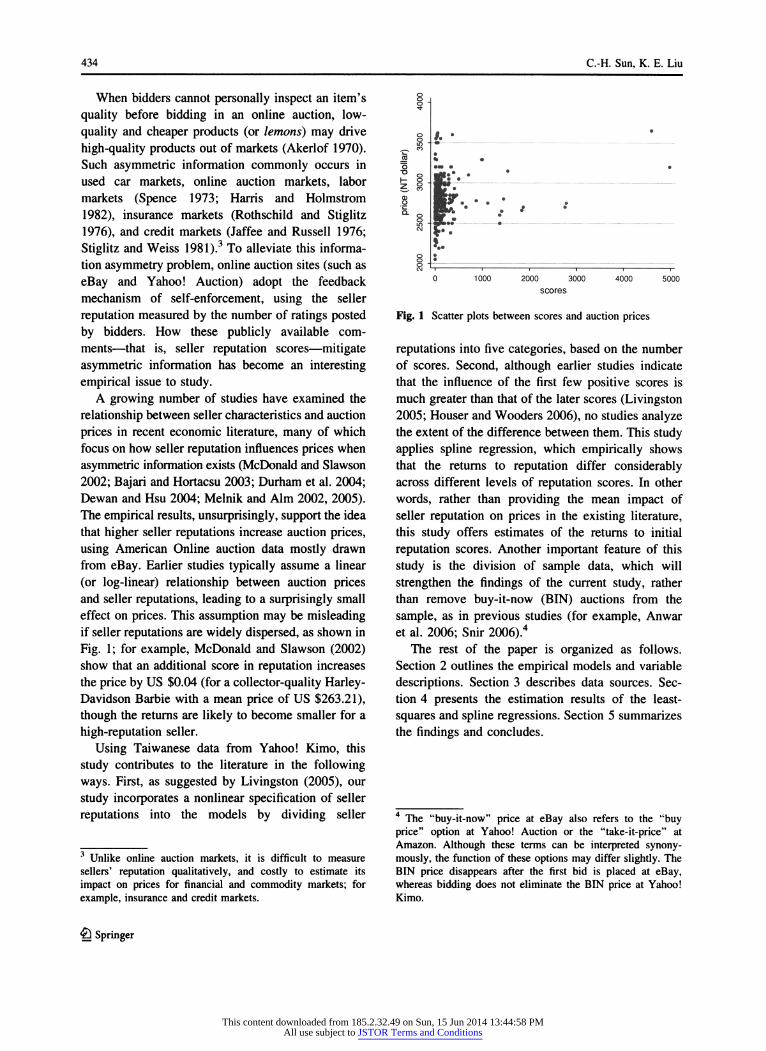

asymmetric information exists (McDonald and Slawson 2002; Bajari and Hortacsu 2003; Durham et al. 2004; Dewan and Hsu 2004; Melnik and Aim 2002, 2005). The empirical results, unsurprisingly, support the idea that higher seller reputations increase auction prices, using American Online auction data mostly drawn from eBay. Earlier studies typically assume a linear (or log-linear) relationship between auction prices and seller reputations, leading to a surprisingly small effect on prices. This assumption may be misleading if seller reputations are widely dispersed, as shown in

Fig. 1; for example, McDonald and Slawson (2002) show that an additional score in reputation increases the price by US $0.04 (for a collector-quality Harley- Davidson Barbie with a mean price of US $263.21), though the returns are likely to become smaller for a

high-reputation seller.

Using Taiwanese data from Yahoo! Kimo, this

study contributes to the literature in the following ways. First, as suggested by Livingston (2005), our

study incorporates a nonlinear specification of seller

reputations into the models by dividing seller

Fig. 1 Scatter plots between scores and auction prices

reputations into five categories, based on the number of scores. Second, although earlier studies indicate that the influence of the first few positive scores is much greater than that of the later scores (Livingston 2005; Houser and Wooders 2006), no studies analyze the extent of the difference between them. This study applies spline regression, which empirically shows that the returns to reputation differ considerably across different levels of reputation scores. In other words, rather than providing the mean impact of seller reputation on prices in the existing literature, this study offers estimates of the returns to initial reputation scores. Another important feature of this

study is the division of sample data, which will

strengthen the findings of the current study, rather than remove buy-it-now (BIN) auctions from the sample, as in previous studies (for example, Anwar et al. 2006; Snir 2006).4

The rest of the paper is organized as follows. Section 2 outlines the empirical models and variable descriptions. Section 3 describes data sources. Sec- tion 4 presents the estimation results of the least- squares and spline regressions. Section 5 summarizes the findings and concludes.

3 Unlike online auction markets, it is difficult to measure sellers' reputation qualitatively, and costly to estimate its impact on prices for financial and commodity markets; for example, insurance and credit markets.

4 The "buy-it-now" price at eBay also refers to the "buy price" option at Yahoo! Auction or the "take-it-price" at Amazon. Although these terms can be interpreted synony- mously, the function of these options may differ slightly. The BIN price disappears after the first bid is placed at eBay, whereas bidding does not eliminate the BIN price at Yahoo! Kimo.

Ô Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

Information asymmetry and small business in online auction market 435

2 Econometric analysis

To examine the determinants of prices in online auctions, the existing literature utilizes various approaches. Empirical studies that include least- squares regression in the analyses include those of Standifird (2001), Ba and Pavlou (2002), Eaton (2002), Bajari and Hortacsu (2003), Durham et al. (2004), Dewan and Hsu (2004), Lucking-Reiley et al. (2007), Dewally and Ederington (2006), and Andrews and Benzing (2007).5

Basic intuition suggests that, if an auction attracts a higher number of bids or a seller has a better reputation, then there should be an increase in auction prices. It is possible to test for these effects using the following regression:

PRICE,- = a0 + <*iXu + 0L2X2i + . . . 4- aMXm/ 4- £/, / = i,2,..., r, (l)

where / indexes the individual auction. The depen- dent variable, PRICE, is the winning bid plus shipping cost. Other key variables (Xmi) of interest include BIDS, OPENBID, VOLUME, DURATION, BONUS, BT/j = 2, 3, . . ., 5), and so on. Table 5 in the Appendix defines the variables used in this study.

2.1 Nonlinear (in reputation variable) estimation

To capture the nonlinearity as described in the "Intro- duction," we augment the regression by replacing SCORE for reputation dummies (Qk, k= 1, 2, 3, 4) in equation (1). Table 5 defines the reputation dum- mies. Sellers who have zero scores only make up approximately 2% of the sample, and the sellers classified in the first quartile (ßi) have scores between 1 and 14. The other three quartiles exhibit wider ranges of scores received. The auctions at the 50th, 75th, and 100th percentiles have sellers with 42, 116, and 4,982 scores, respectively.

2.2 Spline estimation

The spline regression, which relaxes the assumption of constant coefficients at different levels of reputa- tion scores, is specified as follows:

PRICE, - ß0 + jMi + ò'd{S2 4- ö2d2S3 4 S3d3S4 4 ß2X2i. . . 4- ßmXmi + e,-,

1 - 12 T

where the specific values for the thresholds or knots are 15, 42, and 1 16. These knots are chosen based on the reputation quartiles for simplicity. Table 5 in the Appendix defines the reputation score variables (Si, S2, S3, S4) and dummy variables (d', d2, d3).

3 Data

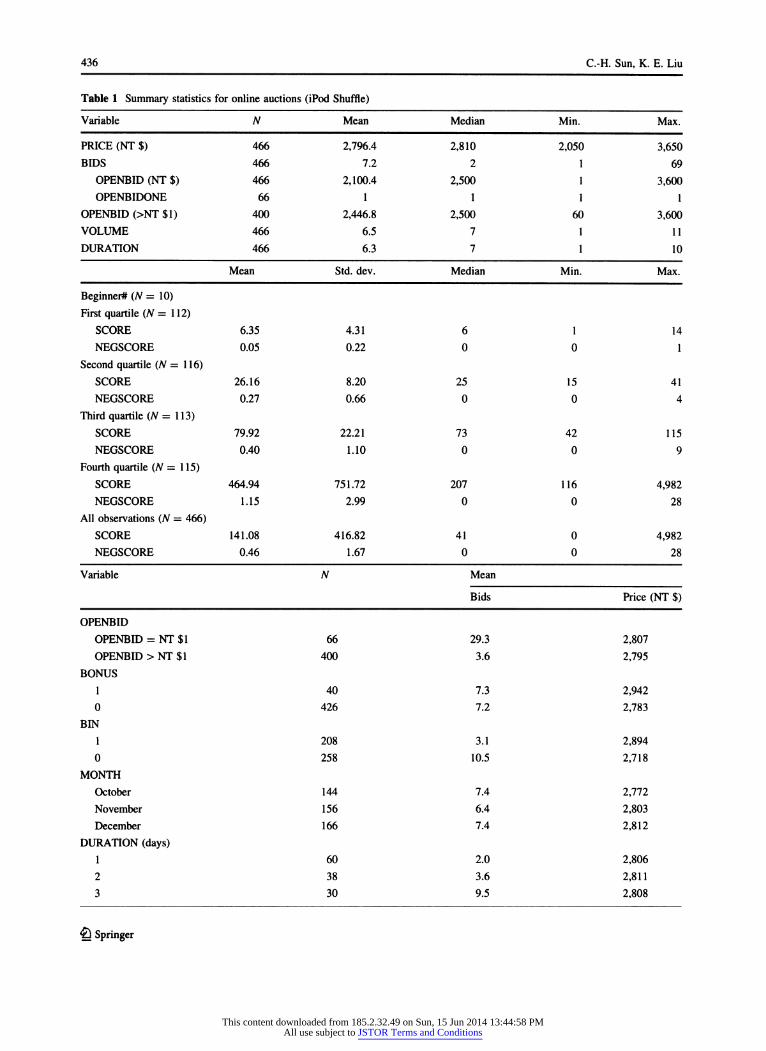

To control for product heterogeneity, this study investigates auctions of brand-new Apple iPod Shuffle 512-Mb MP3 players and disregards auctions selling second-hand iPod Shuffles. The dataset was collected directly from tw.bid.yahoo.com (Yahoo! Kimo) auc- tions between 5 October 2005 and 31 December 2005. 6 The sample used in the econometric analysis includes 466 auctions. Data in earlier studies were mostly collected from eBay, and the items examined include electronic goods, coins, stamps, Barbie dolls, and so on. The average price of items sold in the earlier studies varies substantially from US $9.72 (American Eagle Silver Dollars, Durham et al. 2004), US $311 (3Com Palm Pilot V, Standifird 2001) to US $6,437 (used car, Andrews and Benzing 2007).

Table 1 depicts descriptive statistics for 466 auc- tions.7 The range of winning bids in these auctions, including shipping cost, is from NT $2,050 to NT $3,650; the mean price is NT $2,796, and the average number of bids and bidders are 7.2 and 3.7,

5 Lucking-Reiley et al. (2007) employ the censored-normal

maximum-likelihood estimation procedure, exactly like a standard Tobit regression, except that the censoring point is different across observations. Instead of using the winning bid, Houser and Wooders (2006) utilize the second-highest bid plus the shipping cost as the dependent variable. They then estimate the coefficients of the system equations through generalized least-squares (GLS) procedures.

6 Unlike eBay' s auctions, which are variations of Vickrey's second-price sealed-bid auction, Yahoo! Kimo uses an English auction with proxy bidding, and the winning bidder pays the highest bid plus shipping and handling cost.

Our study excludes unsuccessful auctions, because auctions that attract no bids and automatically relist would be difficult to distinguish. Studies by Standifird (2001), McDonald and Slawson (2002), and Houser and Wooders (2006) also focus on successful auctions only. Without accounting for unsuc- cessful auctions, the ordinary least-squares (OLS) estimation introduces a slight downward bias in the estimated coefficients.

Ö Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

436 C.-H. Sun, K. E. Liu

Table 1 Summary statistics for online auctions (iPod Shuffle)

Variable N Mean Median Min. Max.

PRICE (NT $) 466 2,796.4 2,810 2,050 3,650 BIDS 466 7.2 2 1 69

OPENBID(NT$) 466 2,100.4 2,500 1 3,600 OPENBIDONE 66 1 1 11

OPENBID (>NT $1) 400 2,446.8 2,500 60 3,600 VOLUME 466 6.5 7 1 11 DURATION 466 6.3 7 1 10

Mean Std. dev. Median Min. Max.

Beginner# (N = 10) First quartile (N = 112)

SCORE 6.35 4.31 6 1 14 NEGSCORE 0.05 0.22 0 0 1

Second quartile (N = 116) SCORE 26.16 8.20 25 15 41 NEGSCORE 0.27 0.66 0 0 4

Third quartile (N = 113) SCORE 79.92 22.21 73 42 115 NEGSCORE 0.40 1.10 0 0 9

Fourth quartile (N = 115) SCORE 464.94 751.72 207 116 4,982 NEGSCORE 1.15 2.99 0 0 28

All observations (N = 466) SCORE 141.08 416.82 41 0 4,982 NEGSCORE 0.46 1.67 0 0 28

Variable N Mean

Bids Price (NT $)

OPENBID OPENBID = NT $1 66 29.3 2,807 OPENBID > NT $1 400 3.6 2,795

BONUS 1 40 7.3 2,942 0 426 7.2 2,783

BIN 1 208 3.1 2,894 0 258 10.5 2,718

MONTH October 144 7.4 2,772 November 156 6.4 2,803 December 166 7.4 2,812

DURATION (days) 1 60 2.0 2,806 2 38 3.6 2,811 3 30 9.5 2,808

£} Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

Information asymmetry and small business in online auction market 437

Table 1 continued

Variable N Mean

Bids Price (NT $)

4 31 12.2 2,864 5 33 5.8 2,874 6 30 7.3 2,836 7 48 9.9 2,769 8 22 4.1 2,785 9 23 7.7 2,846 10 151 8.5 2,770

WEEKEND 1 109 7.8 2,788 0 357 6.8 2,802

Bidding type N OPENBIDONE OPENBID > NT $1 Mean

OPENBID (NT $) BIDS PRICE (NT $)

BT! 73 0 73 2,610 1.0 2,716 BT2 61 1 60 2,505 1.0 2,928 BT3 95 0 95 2,822 1.0 2,869 BT4 185 49 136 1,601 14.2 2,718 BT5 52 16 36 1,370 9.3 2,901

respectively. Seller reputation is not directly obser- vable, but it can be measured by the number of positive (or negative) scores posted by bidders. The mean positive score for all sellers is 141.53, in contrast to a small mean negative score of 0.46. There are 66 auctions with a starting bid of NT $1, and they receive an average of 29.3 bids per auction, contrast- ing with the remaining 400 auctions with an average of 3.6 bids per auction. The mean score ranges from 6.35 in the first quartile to 464.94 in the fourth quartile, and the average negative score is very small, although it increases slightly from 0.05 to 1.15. Unlike many electronic goods, the mean price for an iPod Shuffle does not fall during the sample period.

Another increasingly popular feature of online auctions offered by eBay and other online auction sites is called "buy it now."8 It allows buyers to end

the auction early at a predetermined price, and people who are impatient or risk averse may find this function beneficial. The average price of auctions ended with BIN is NT $2,894, which is relatively higher than non-BIN auctions by roughly 6.5% or NT $176, and the impact of BIN persists for the following bidding types: BT2, BT3, and BT5. How- ever, BT4 has the highest average bids of 14.2 per auction, but its mean price is reported to be the second lowest at NT $2,718. Figure 2 shows scatter- plots between scores and auction prices by bidding types, illuminating some of the factors of interest in studying these online auctions. Finally, auctions ending during the weekend draw more bids than weekdays, and auctions ending on day four have the highest average bids of 12.2 and a price of NT $2,864.

8 The theoretical explanations of BIN' s impact on an auction price from the viewpoint of sellers have been analyzed by Budish and Takeyama (2001), Mathews (2004), and Reynolds and Wooders (2009). For instance, Budish and Takeyama (2001) explain that, when bidders are risk averse, an optimally set BIN price can raise the expected profits of the seller. Our

Footnote 8 continued empirical examination does not include the risk attitude of bidders as a variable in the regression, because risk measure- ment is unavailable from the online auction sites.

Ö Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

438 C.-H. Sun, K. E. Liu

Fig. 2 Scatter plots between scores and auction prices by bidding types

4 Empirical results

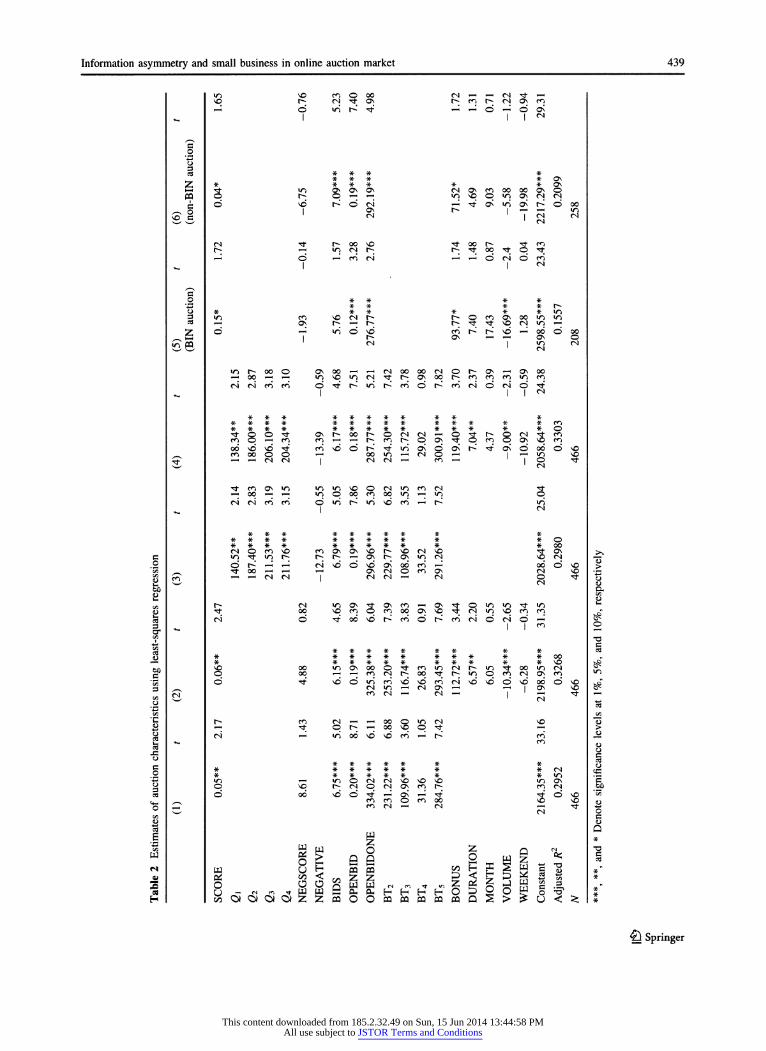

Table 2 reports the empirical results of the estimation of equation (1). Parameter estimates of SCORE are positive and statistically significant at the 5% level in models 1-2. Our finding that reputation is positively related to prices is consistent with the existing literature. In line with Ba and Pavlou (2002) and Bajari and Hortacsu (2003), NEGSCORE (or NEG- ATIVE) does not produce any significantly negative impact on auction prices.9 The insignificant coeffi- cients of NEGSCORE indicate that bidders do not penalize sellers with a few negative feedbacks. Two possible explanations are offered. First, the fear of retaliation tends to reduce the frequency of negative comments, leading to the insignificant impact of NEGSCORE. Second, if a seller has received several negative feedbacks, then there is an incentive for the seller to obtain a new account to continue the online auction business. As a result, the number of negative scores recorded in the dataset may not truly reflect the overall sellers' negative reputation.

The estimates for the coefficients of BIDS, OPENBID, and OPENBIDONE are positive and statistically significant at the 1% level, suggesting that auctions with a higher opening bid generate higher auction prices. The effects of MONTH and WEEKEND on prices are insignificant. As expected, the number of quantity supplied, VOLUME, nega- tively impacts auction prices, which is consistent with fundamental economic principles, that is, large sup- ply lowers prices. Finally, positive effects of BONUS and DURATION are evident, indicating that a longer auction length generates greater revenue.

When seller reputations are divided into four quartiles and sellers with zero scores, it is shown that seller reputations represented by four dummy vari- ables (Qk) are positively and significantly related to prices, that is, a seller who has a score between 1 and 14 (or between 15 and 41) receives an additional NT $141 (or $187) more than a seller who has no scores in model 3, Table 2. In other words, sellers whose scores are classified in the second quartile receive NT $46 more than those in the first quartile; sellers whose scores are classified in the third quartile receive only NT $24 more than those in the second quartile. There is little difference evident in prices received for sellers whose scores are classified in the last two quartiles (model 3, Table 2). The empirical finding implies the marginal effects of subsequent scores become much smaller.

9 Several studies find evidence that negative scores reduce auction prices, such as those of Houser and Wooders (2006), Standifird (2001), McDonald and Slawson (2002), Cabral and Hortacsu (2004), Melnik and Aim (2002, 2005), and Lucking- Reliey et al. (2007).

£} Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

Information asymmetry and small business in online auction market 439

c #o "3

e

CT

Ï C/5 O

1 o

•a CO

'S

1 i «s o> 3

»n so co o oo cm <- > - cm ^f - • so r^ cm rf on h f) h (S O) fi - ö »ri h Tt h h d h d »

«J *• #■ -X- * . * -X- * #• ON . Z * * * * * # on G^- m On On ON CM On CO 00 00 On © PQO r-; p^H^H »O SO © in On CM CM ¿Ö so r-* © cm T-írtosuSoN r-'öoo

SS ' N '

| <S CM

r^ '- ' >o cm r^ h Tt oo ^ q Ti; ~ Ö -h' <T> CM ^ ^ Ö CM Ö CO

I I ^

O * * * * 'o * * * * r- o* ** # * * »n 3«o en vccMr- r^omoNoo»oio cö ^h on r- ^ r- r- tj- «3- so cm »o ^ G i r* on^^hono

g« G i 'CM r* on^^hono

I JO CM

lOr-OOO ONOO^H^CMOOOOCMOr-ON^ONOO

cMcMcncn ö^t^iot^cnör^cocMÖcMÖTt I I I o«

•*•** * * * * * * * * * * * * * * * * * * * # * *co * * -x- * * *■•*#•* # * * -x- * O ^õo^ ONr-oor-ocMCM^-HO^-r-õcM^m cop'- 'co co'^^^r^cor^pON'^tpcopONsqco o¿v¿'o^t covoor^TtínoÑooÑr^rfoÑooóovo

g --HCMCM | CMCM~ CO- '

| O *■

^■COONiO »OIOVOOCMIOCOCM Tf - oo - - »opoqcooo»o - in p CMCMCOCO O <ii h- IO VO C) «-Î t^ «O

I ^

* * * -)f * •)(• -X- * -X- ■* * * * * -x--***-* * *O ■X-*** ***** * -K00 CMOCOVO cOONONVOr-VOCMSO ^ON >^ lOTtior«; r^r^ - ONr-ON»ocM ^^ ^ or»: ^^ cMvûovooNoôco- ooovo>

^^ Tt 00 h h h ONCMOCOON CM SO • -3 frT ^^ - - CMCM| CM CM - CM O^o

S f- CM »OON^-ONCOi-HON^tOiOlO^íO ^ rt oo vocopcoooONvq^-cMirjsqcoco ^ cm* ö Tf oo vo r-- co c" r*»" co cm ö cm ö - §£

11^2 'S

* * * * * * * * * tf

* * * * * * * # * * -KSD fcg »nONooOTfcoiocMr^íOTj-ooiocM .^

00 - - COCMt^OO Ttr-lOpCOCMONCO iri

Ö Tt VOOlOCOSOSOfOCM'sOSOOsOOOOSOvcT _^ rj in - 1 cm on ^- > ^^ionso^ Ínj _^

CO CM - • CM »-h I ' i- ' ^ »- ' Ínj w

CO CM - • CM »-h ' I CM i- ^ »-

^ cd

r- co cm- ' i- • oo o »o cm so 13 ^ T^- p r^ - oo sq p ^t - > cm - »o oô so so co - r-' co Jà

g •x- -x-íe-x-x-** *cMfc •x- **#*#-x- -x-io^S IT) i- iíOOCMCMSOsOSO IOON C p sq r- cm p cm on co r-># co cm ûû Ö 00 SO Ö TÍ - ON - Tf rt Ö SO '™

_. COCOOCOOO SOSOfl)

S w o S Q ^ "§

rj -(NwrrWPQtíOuCuHHHHODSOÍJo-? î coOlCllOlOtZÎZPQOOPQPQPQPQPQÛ^^U^^ *

â Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

440 C.-H. Sun, K. E. Liu

Vi I e« (A I i f

•B CO

'S w

¡

vo co oo m r- *- < i^ vo © co cn co on r^ rn vq «-• vp «-4 *-* oj î w h o' -< ò ci h h vi /i ö ^^-¡ööö^' I I I I ^

| Z * 55 * *

* «

5 o Z * * * « * 00 HH ^HOO^^mO *O N ^ - 00 Tf 00 M

-. ¿ *-*'©© *-^ oo © ^' uSsOrfcn^voooo eso - « i oo i ' <m oo m eso h §

- I

i i ' I CO m <N

ooTtt^t^'- loo ri- oo(Nmtnr^Tfcn P t ^ ^. t 1 ~*. °) *-*. ~*. ̂ °°. ̂ "1 rf d ^ Ò ^' d cn ri w ri d ^ d pi

I 11^

o * * ^ * 'S * * *** *O o * « **■**••*<- «

* in n ^ en On O vo h^NOONOOMN -.Z cnöörJTfö oo hföd^NKridoo

^1 I I 11^

I s * * *

* * (N * * -X- * t-

^ n M in t oooo© rj m n ^ ^o x h n pQvovqcnp ^

vpp^H Tt » » « «n oe ^ N ^.c rn Ö Ö Ö -h'ooÖ rf ^ iri ^ w (S ^' d « g| ^.c rn i - rf i w i 7

(S s; a

«

pi ^ d ^ ö^ri co ri rô (S d ^ d N I II«

o * * * * * ^ '¿3-K- -X- «■ -K- •}(• ^ * -< ^

2 w 'o oo m r^for-« © »OMhinH^in^t > 00 r-;O'vq*-< en »- i © co h<-iooosinpjOPj 'S ^ Tfcsö© (N«o© o< vor4oN^trioNfo©oog

£« ^ « S ^ g in©ooi-H vosooo cot^Q^f^-H^ioTi-csoo ^ o ^ «n in TfTfTj- ^NO^oovû^^vori o <s^©ín ©»n»n h'^d^wpiopidyo *^

- I I I ^ -g

** ***** * _r * * ** *******^O^i * * ** *******© in ^■^»nr«- m © os (NO>«om»nr-cnoNt^ooON oo«o(sj© oorn© ooHHOo^qh;>nooo'ri ^ «o^©© ri r^ d - îwdoN<x>oô-îoô^«-!dvo i

(Al

(S in «n <n »nvoro ^ «. -^ ^ "^ "l ^ « r4©©ci ©TtTf on ro ri d ri d O ^

*. i ii^8 * * * * * .g * * *** ****«- *5 * * *** ****in"c

r*oocnt^> r^t-»t*- m o ^ n a ci ^û ^c où intuís© »n ^-j© en in « h oo oo 'O pi «g vo©©© covo© »n oovc>oo"oNQN»n©vo.-

S ' s 2 ' ' § * 1

g «S ¡ »g * i (Õ to%%%%%^ ffl O ë « « « Ö W « Û S > ^ U < ^ I

ö Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

Information asymmetry and small business in online auction market 441

To test the robustness of the empirical results, this study further divides the sample into two groups on the basis of BIN auctions. Model 5 in Table 2 shows the estimated coefficients for BIN auctions (208 observations) and model 6 for non-BIN auctions. The empirical results do not vary considerably, except that the impact of BIDS turns out to be insignificant for BIN auctions (model 5).

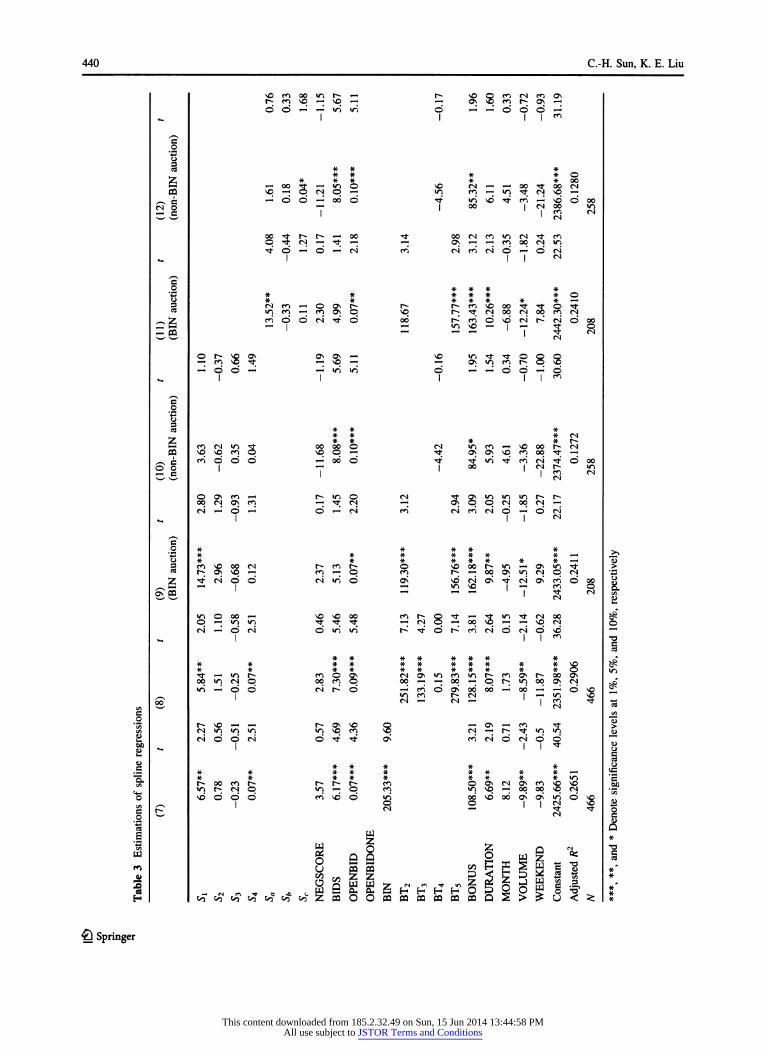

4.1 Spline regression

Table 3 presents the results of the spline regression. Models 7 and 8 in Table 3 report the results of the spline estimation for seller reputations on auction prices under different specifications. The impact of seller reputations Sx (SCORE < 15) and 54 (SCORE > 1 16) on prices is positive and statistically significant, but, surprisingly, scores between 15 and 116 (52 and S3) do not generate any significant effects on prices. These knots were chosen based on reputation quartiles, and the focus of the spline regression is to demonstrate that the returns to reputation scores differ substantially across four reputation quartiles, rather than choosing the cutoff points or knots.10

Unlike models 5 and 6, the empirical results in models 9 and 10 are sensitive to data separation due mainly to the choice of knots. Hence, this study divides the reputation scores into three groups (three tertiles). The estimated coefficients of the reputation scores, 5a (SCORE < 20) in model 1 1 and Sc (SCORE > 81) in model 12, then become statisti- cally significant in the separated samples. The significance of coefficient 5a implies that inexperi- enced sellers tend to set a low BIN price in an attempt to attract bidders, resulting in very high returns to reputation for BIN auctions, in particular for the first few scores. In contrast, for non-BIN auctions, returns to reputation are statistically insignificant unless a seller has established at least 81 reputation scores or more, as shown in model 12. Earlier studies suggest that the first few scores have a stronger effect, but the returns to reputation between Si (5.84) and S4 (0.07), as shown in model 8 (Table 3) are incomparable, and this has never been empirically analyzed in the existing literature.

10 Even based on different knots (25, 75, and 125, arbitrarily chosen), we also reach a similar conclusion to models 7 and 8.

Table 4 Tests of the coefficients of quartile dummies

Null hypothesis Model (3) Model (4)

F p- F p- value value

Ö! coefficient = g2 coefficient 3.20 0.0742 3.40 0.0657 Qi coefficient = g3 coefficient 6.94 0.0087 6.54 0.0109 Ö, coefficient = 04 coefficient 6.44 0.0115 5.59 0.0185 g2 coefficient = g3 coefficient 0.88 0.3479 0.64 0.4240 g2 coefficient = g4 coefficient 0.86 0.3539 0.49 0.4821 g3 coefficient = g4 coefficient 0.00 0.9930 0.00 0.9456 Coefficients of g, = g2 = g3 3.58 0.0288 3.42 0.0335 Coefficients of g2 = g3 = g4 0.58 0.5580 0.38 0.6817 Coefficients of 2.88 0.0354 2.63 0.0499

gi = Qi = Qi = Qa

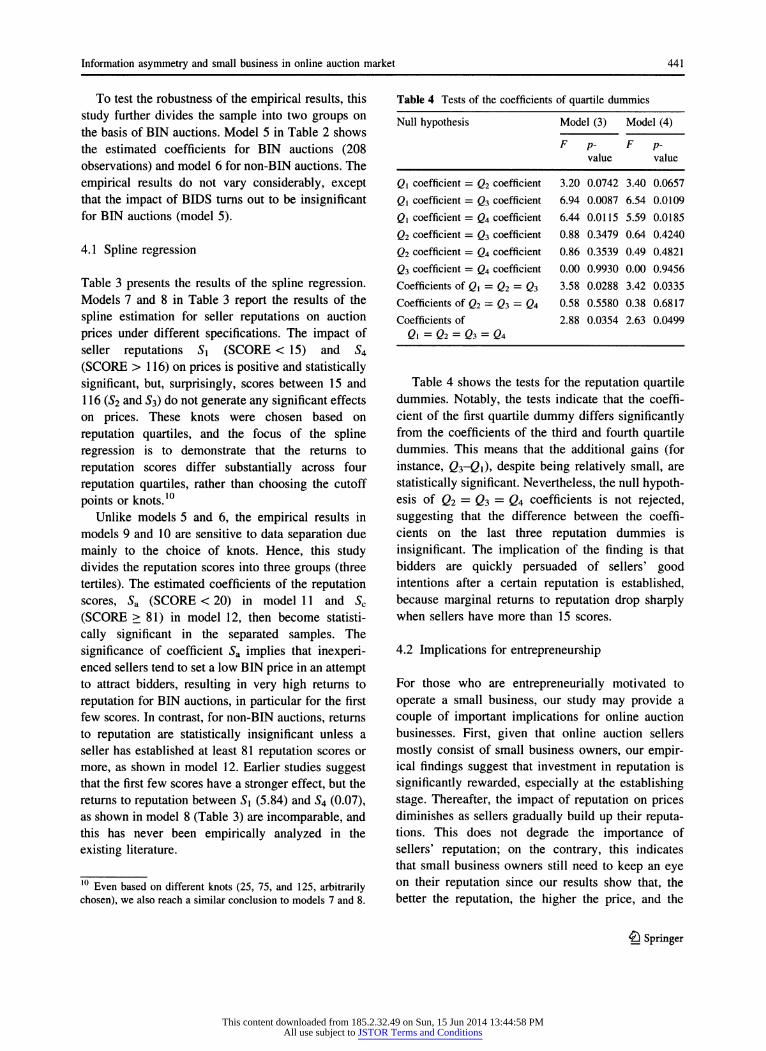

Table 4 shows the tests for the reputation quartile dummies. Notably, the tests indicate that the coeffi- cient of the first quartile dummy differs significantly from the coefficients of the third and fourth quartile dummies. This means that the additional gains (for instance, Q3-Q1), despite being relatively small, are statistically significant. Nevertheless, the null hypoth- esis of Ô2 = Ô3 = Ô4 coefficients is not rejected, suggesting that the difference between the coeffi- cients on the last three reputation dummies is insignificant. The implication of the finding is that bidders are quickly persuaded of sellers' good intentions after a certain reputation is established, because marginal returns to reputation drop sharply when sellers have more than 15 scores.

4.2 Implications for entrepreneurship

For those who are entrepreneurially motivated to operate a small business, our study may provide a couple of important implications for online auction businesses. First, given that online auction sellers mostly consist of small business owners, our empir- ical findings suggest that investment in reputation is significantly rewarded, especially at the establishing stage. Thereafter, the impact of reputation on prices diminishes as sellers gradually build up their reputa- tions. This does not degrade the importance of sellers' reputation; on the contrary, this indicates that small business owners still need to keep an eye on their reputation since our results show that, the better the reputation, the higher the price, and the

Ö Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

442 C.-H. Sun, K. E. Liu

greater the profitability. In addition, these entrepre- neurs may consider other marketing strategies, such as setting a high starting bid and providing a bonus, to increase their profits.

Second, established reputation may have a spill- over effect. Take our online auction as an example. A successful transaction in this iPod Shuffle online auction may encourage the small business owner to build up additional related businesses, such as cellular phones, electronic accessories, or video games. When consumers gain a positive purchasing experience with this online auction seller, the asym- metric information problem is alleviated and thus the consumers would trust to shop online with the same seller if other commodities are provided. As a consequence, this multiproduct entrepreneur may enjoy economies of scale and scope to make the small online auction business more profitable.

5 Conclusions

This paper has examined how bidders respond to seller reputation in online auctions using Taiwanese data. The contribution of the current paper is an empirical study in which the relationship is modeled in a less restrictive manner. The effect of reputation on price is allowed to be nonlinear. Our study reveals that the influence of reputation scores on auction prices is statistically significant in the least-squares and spline regressions, indicating that the mechanism of seller reputations is effective in mitigating asym- metric information in online auctions in Taiwan. Even though the sample is divided into two groups on the basis of BIN, the empirical results vary

moderately, suggesting that our findings are robust to the data separation.

Unlike existing studies, the use of spline regression in this study highlights that the impact of the first few positive scores on prices is much greater than that of the later scores quantitatively. Using reputation dum- mies, this study also finds that the incremental effects on the price level of moving from reputation quartile 1 to quartile 2, from quartile 2 to quartile 3, and from quartile 3 to quartile 4 are statistically insignificant, implying that marginal returns to scores drop sharply. Finally, BIN and other auction characteristics (for instance, opening bid and auction length) also signif- icantly impact auction prices.

It should be noticed that our findings may suffer from several potential econometric limitations, and consequently the empirical results need to be inter- preted with caution. With regard to a possible endogenous problem, it is possible that a seller who sets a BIN price also writes better descriptions of the items he/she is selling, and that it is these better descriptions which result in higher sale prices, rather than the use of BIN. As a result, the choice to use the BIN feature becomes an endogenous decision. None- theless, written description is not included in the analysis, because such a variable is difficult to quantify. Finally, the conclusions of this study are representative only for the iPod Shuffle, as the characteristics of bidders may vary from item to item, for instance, tennis rackets, collectible stamps, or Gucci handbags.

Appendix

Table 5 Definition of online auction variables

Variable Definition Expected effect on price

PRICE Highest winning bid in an auction plus shipping and handling cost (or NT $50 if not specified for shipping cost)

SCORE Positive scores minus negative scores +

51 SCORE if SCORE < 15 +

52 (SCORE - 15) if SCORE > 15 +

53 (SCORE - 42) if SCORE > 42 +

54 (SCORE - 1 16) if SCORE > 1 16 +

£} Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

Information asymmetry and small business in online auction market 443

Table 5 continued

Variable Definition Expected effect on price

d{ Dummy variable = 1, if SCORE > 15; = 0 otherwise

d2 Dummy variable = 1, if SCORE > 42; = 0 otherwise

d3 Dummy variable = 1, if SCORE > 1 16; = 0 otherwise

Sa SCORE if SCORE < 20 +

Sb (SCORE - 20) if SCORE > 20 +

Sc (SCORE - 81) if SCORE > 81 +

da Dummy variable = 1, if SCORE > 20; = 0 otherwise

db Dummy variable = 1, if SCORE > 81; = 0 otherwise

NEGSCORE Negative scores -

NEGATIVE Dummy variable = 1, if a seller has negative scores; = 0, otherwise -

BIDS Number of bids +

OPENBID Opening bid set by sellers +

OPENBIDONE Dummy variable = 1, if opening bid = NT $1; = 0, otherwise ?

BIN (buy it now) Dummy variable = 1, auction ended with "buy it now"; = 0, otherwise +

BTi (bidding type 1) Dummy variable = 1, one bid until the end of the auction; = 0, otherwise ?

BT2 (bidding type 2) Dummy variable = 1, one bid and is ended with a BIN price; = 0, otherwise +

BT3 (bidding type 3) Dummy variable = 1, one bid and opening bid equals a BIN price; = 0, + otherwise

BT4 (bidding type 4) Dummy variable = 1, many bids until the end of the auction; = 0, otherwise +

BT5 (bidding type 5) Dummy variable = 1, many bids and is ended with a BIN price; = 0, otherwise +

go Dummy variable = 1, if a seller has zero score; = 0, otherwise

Ô, (first quartile) Dummy variable = 1, if a seller has scores between 1 and 14; = 0, otherwise +

Ô2 (second quartile) Dummy variable = 1, if a seller has scores between 15 and 41; =0, otherwise +

Ô3 (third quartile) Dummy variable = 1, if a seller has scores between 42 and 1 15; = 0, otherwise +

Q4 (fourth quartile) Dummy variable = 1, if a seller has scores between 116 and 4,982; = 0, + otherwise

BONUS Dummy variable = 1, scratch-resistant protector, and others; = 0, otherwise +

VOLUME Number of iPod Shuffles sold on the same day -

MONTH Time variable = 0, auction ended in October 2005; = 1, auction ended - in November 2005; = 2, auction ended in December 2005

DURATION Number of days that an item is sold in an auction + WEEKEND Dummy variable = 1, auction ended on Saturday or Sunday; = 0, otherwise +

As BIDS and BIDDERS are highly correlated, this paper does not include BIDDERS in the regression analysis "+", "- ", and "?" denote that the impact is positive, negative, and uncertain, respectively

References

Akerlof, G. A. (1970). The market for 'Lemons': Quality uncertainty and the market mechanism. Quarterly Journal of Economics, 84(3), 488-500.

Andrews, T., & Benzing, C. (2007). The determinants of price in internet auctions of used cars. Atlantic Economic Journal, 35(1), 43-57.

Anwar, S., McMillan, R., & Zheng, M. (2006). Bidding behavior in competing auctions: Evidence from eBay. European Economic Review, 50(2), 307-322.

Ba, S., & Pavlou, P. A. (2002). Evidence of the effect of trust building technology in electronic markets: Price premiums and buyer behavior. MIS Quarterly, 26(3), 243-268.

Bajan, P., & Hortacsu, A. (2003). The winner s curse, reserve prices, and endogenous entry: Empirical insights from eBay auctions. RAND Journal of Economics, 34(2), 329- 355.

Budish, E., & Takeyama, L. (2001). Buy prices in online auctions: Irrationality on the internet? Economics Letters, 72(3), 325-333.

4y Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions

444 C.-H. Sun, K. E. Liu

Cabral, L., & Hortacsu, A. (2004). The dynamics of seller reputation: Theory and evidence from eBay. NBER Working paper no. 10363.

Dewally, M, & Ederington, L. (2006). Reputation, certifica- tion, warranties, and information as remedies for seller- buyer information asymmetries: Lessons from the online comic book market. Journal of Business, 79(2), 693-729.

Dewan, S., & Hsu, V. (2004). Adverse selection in electronic markets: Evidence from online stamp auctions. Journal of Industrial Economics, 52(4), 497-516.

Durham, Y., Reolofs, M. R., & Standifird, S. (2004). eBay's Buy-It-Now function: Who, when, and how. Topics in Economic Analysis & Policy, 4, 1, Article 28.

Eaton, D. H. (2002). Valuing information: Evidence from Guitar auctions on eBay. Murray State University Work- ing paper.

Harris, M, & Holmstrom, B. (1982). A theory of wage dynamics. Review of Economic Studies, 49(3% 315-333.

Houser, D., & Wooders, J. (2006). Reputation in auctions: Theory, and evidence from eBay. Journal of Economics and Management Strategy, 15(2), 353-370.

Jaffee, D., & Russell, T. (1976). Imperfect information, uncertainty, and credit rationing. Quarterly Journal of Economics, 90(4), 651-666.

Livingston, J. A. (2005). How valuable is a good reputation? A sample selection model of internet auctions. Review of Economics and Statistics, 87(3), 453-465.

Lucking-Reiley, D., Bryan, D., Prasad, N., & Reeves, D. (2007). Pennies from eBay: The determinants of price in online auctions. Journal of Industrial Economics, 55(2), 223-233.

Mathews, T. (2004). The impact of discounting on an auction with a buyout option: A theoretical analysis motivated by eBay's Buy-It-Now feature. Journal of Economics, 81 ('), 25-52.

McDonald, C, & Slawson, C. Jr. (2002). Reputation in an internet auction market. Economic Inquiry, 40(3), 633- 650.

Melnik, M. I., & Aim, J. (2002). Does a seller's ecommerce reputation matter? Evidence from eBay auctions. Journal of Industrial Economics, 50(3), 337-350.

Melnik, M. I., & Alm, J. (2005). Seller reputation, information signals, and prices for heterogeneous coins on eBay. Southern Economic Journal, 72(2), 305-328.

Reynolds, S., & Wooders, J. (2009). Auctions with a buy-price. Economic Theory, 38. 9-39.

Rothschild, M., & Stiglitz, J. (1976). Equilibrium in competi- tive insurance markets: An essay on the economics of imperfect information. Quarterly Journal of Economics, 90(4), 630-649.

Snir, E. (2006). Online auctions enabling the secondary com- puter market. Information Technology and Management, 7(3), 213-234.

Spence, M. (1973). Job market signaling. Quarterly Journal of Economics, 87(3), 355-374.

Standifird, S. (2001). Reputation and E-commerce: eBay auc- tions and the asymmetrical impact of positive and negative ratings. Journal of Management, 27, 279-295.

Stiglitz, J., & Weiss, A. (1981). Credit rationing in markets with imperfect information. American Economic Review, 71(3), 393-410.

Ö Springer

This content downloaded from 185.2.32.49 on Sun, 15 Jun 2014 13:44:58 PMAll use subject to JSTOR Terms and Conditions