Income Statement PresentationMay 20, 2009

Intermediate Accounting 303

Team 3: Ryan McKay

Cheer Cheng

Kristen Jeffries

Dr. Kirch

Acct 303

What is an Income Statement?

Attributed to FASB Statement of accounting concept 5 ¶ 30:51

AKA Earnings Statement

Discloses changes to the company including: Causes of changes to assets and liabilities

Results of major or ongoing operations

Results of the company’s transactions

Uses of the Income Statement Performance report for stated period.

Used to analyze future performance as well (5 ¶ 36) Considers risk and financial standing of the

company in its current period Limitations of an Income Statement

The Net income reported is a best “estimation” Takes into account several assumptions and

considerations Net income can be altered by different

accounting methods Example: Enron : Mark-to-Market

What is an Income Statement?

Three Types of Income Statements

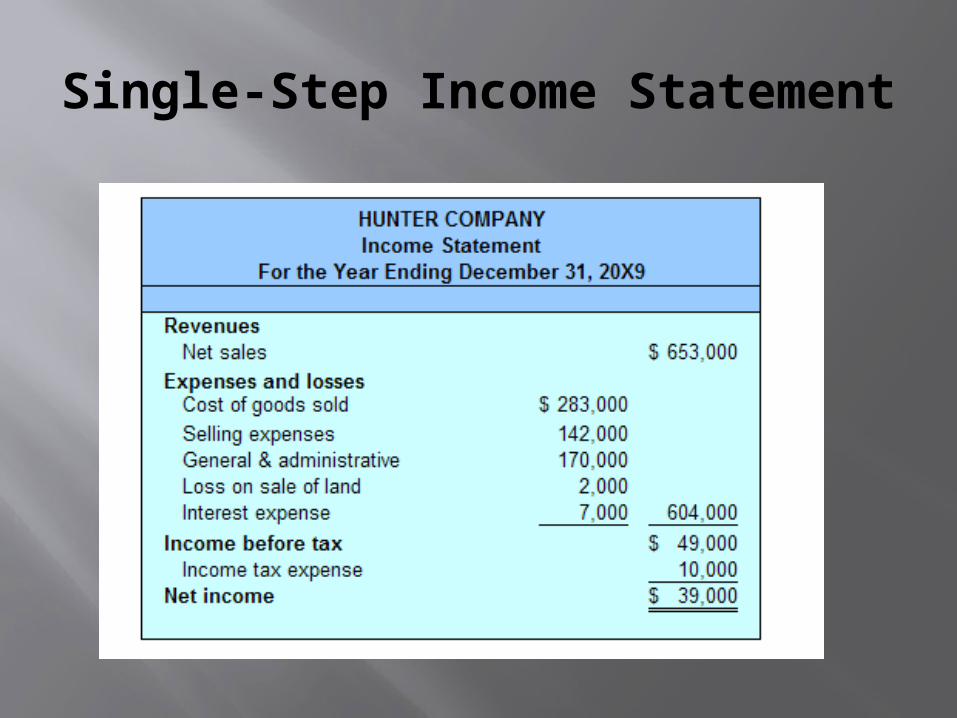

Single Step Income Statement Expenses are deducted from revenue to get

net income

Not the best form to use Gives a very rough estimate

Very easy to use and simple

Single-Step Income Statement

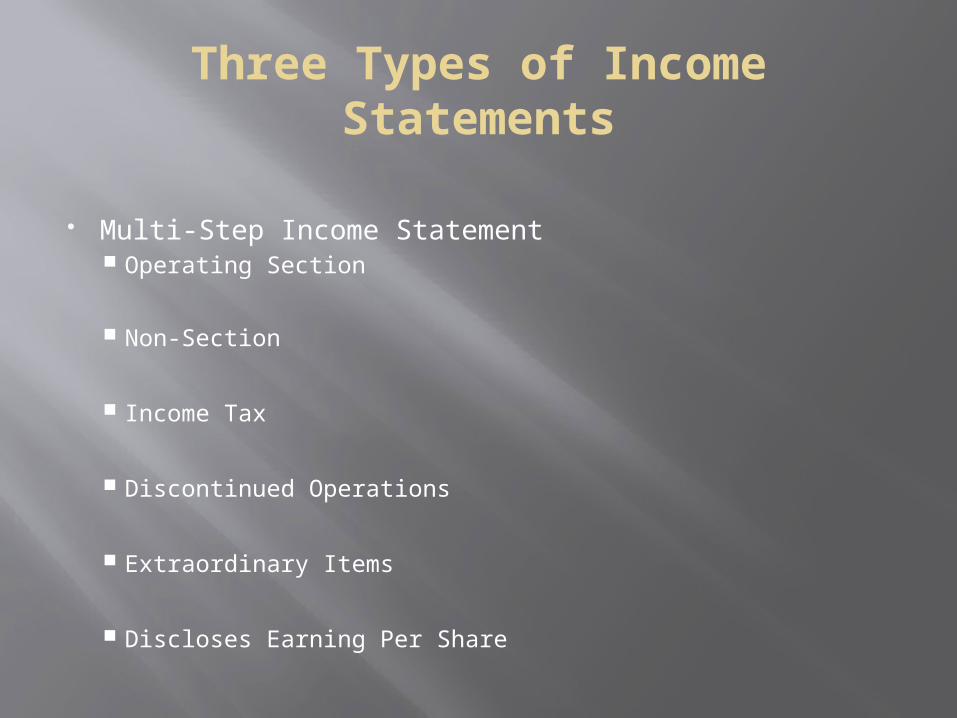

Multi-Step Income Statement Operating Section

Non-Section

Income Tax

Discontinued Operations

Extraordinary Items

Discloses Earning Per Share

Three Types of Income Statements

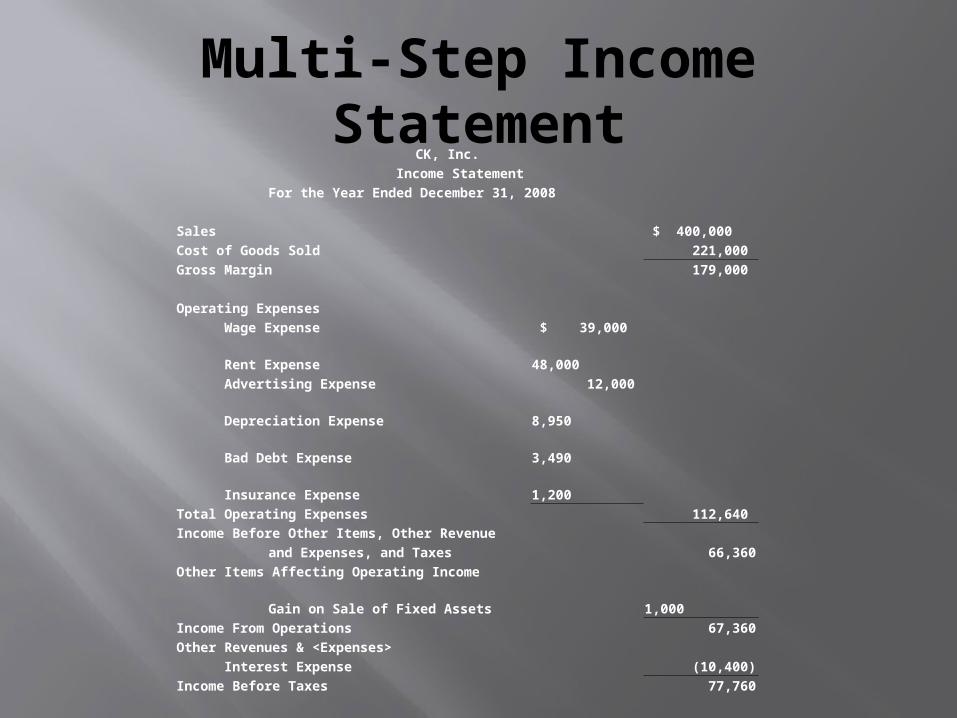

Multi-Step Income Statement

CK, Inc.

Income Statement

For the Year Ended December 31, 2008

Sales $ 400,000

Cost of Goods Sold 221,000

Gross Margin 179,000

Operating Expenses

Wage Expense $ 39,000

Rent Expense 48,000

Advertising Expense 12,000

Depreciation Expense 8,950

Bad Debt Expense 3,490

Insurance Expense 1,200

Total Operating Expenses 112,640

Income Before Other Items, Other Revenue

and Expenses, and Taxes 66,360

Other Items Affecting Operating Income

Gain on Sale of Fixed Assets 1,000

Income From Operations 67,360

Other Revenues & <Expenses>

Interest Expense (10,400)

Income Before Taxes 77,760

Tax Expense 9,240

Net Income $ 68,520

Earnings per Share $ 3.70

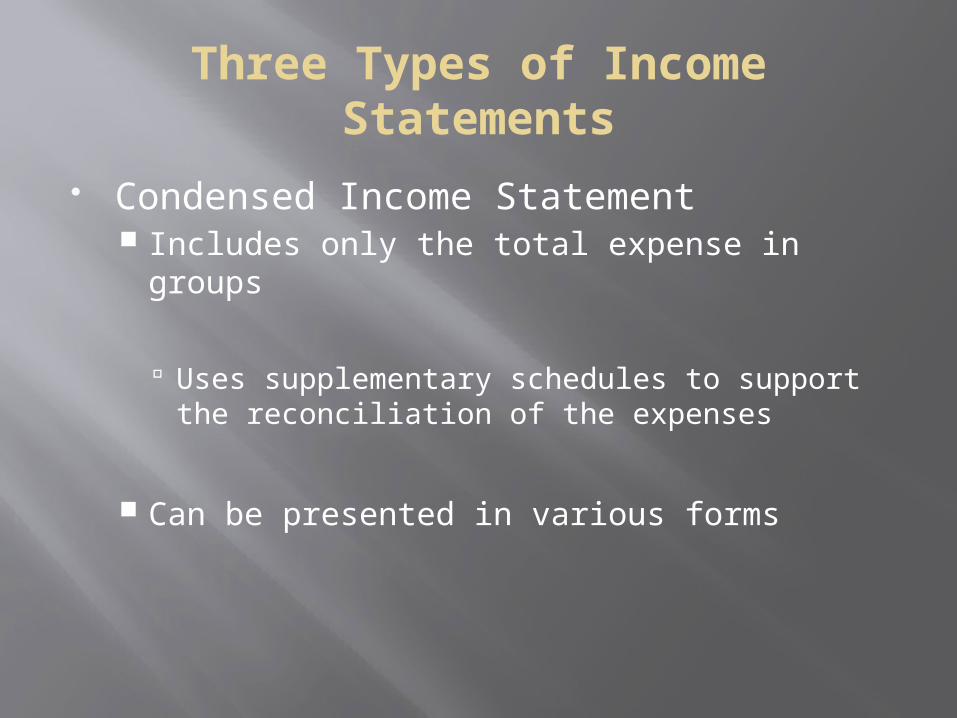

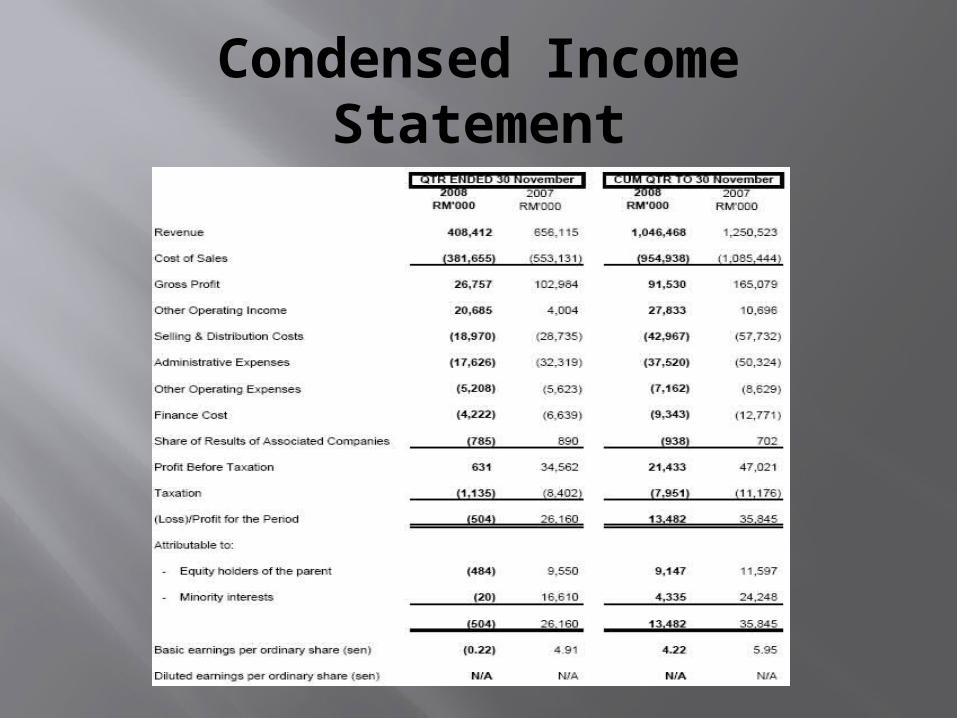

Condensed Income Statement Includes only the total expense in groups

Uses supplementary schedules to support the reconciliation of the expenses

Can be presented in various forms

Three Types of Income Statements

Condensed Income Statement

Irregular Items affecting Income

Irregular Items affecting an Income Statement

Discontinued Operations

Extraordinary Items

Unusual gains and/or losses

Disclosures and Notes of the Income Statement

Disclosure requirement-Items affecting earnings

Must state income tax

Change in accounting principles

Correction of previous errors

Thank You!

Questions ????