HOME COUNTRY NETWORKS AND FOREIGN EXPANSION:EVIDENCE FROM THE VENTURE CAPITAL INDUSTRY

ISIN GULERUniversity of North Carolina

MAURO F. GUILLENUniversity of Pennsylvania

We propose that home country network advantages shape firms’ foreign expansion.We argue that a social status advantage is transferable from one market to another asa signal of quality but that a brokerage advantage is more context-specific and difficultto transfer. Furthermore, the value of network advantages changes as networks evolve.Data on the foreign market entries of 1,010 U.S. venture capital firms provide robustsupport for the effects of social status. We also find that brokerage reduces foreignentry in the absence of home country partners in a new market and increases it whenpartners are already operating in that market.

Foreign market entry is a process fraught withdifficulty for firms, given the unknowns of operat-ing in settings that can be very different from theirhome countries. The literature on internationalmanagement suggests that home country advan-tages allow firms to compensate for the difficultiesassociated with operating abroad. This stream ofresearch has tended to emphasize the advantagesassociated with the possession of brands, technol-ogy, know-how, and general management skills(see Caves [1996] and Helfat and Lieberman [2002]for reviews of this literature). Little attention, how-ever, has been paid to the effect on foreign expan-sion of network-based advantages in a firm’s homecountry, in spite of the large body of evidence doc-umenting the influence of social networks on firmstrategy and performance (e.g., Burt, 1992; Na-hapiet & Ghoshal, 1998; Podolny, 2005). There issome international evidence indicating that bothvertical relationships with suppliers or buyers andties within business groups in a home country areassociated with entry into specific foreign markets.This line of research shows that firms follow theirpeers, customers, or partners into foreign markets;

it does not, however, examine the impact of firm-specific advantages arising from firms’ network po-sitions in the home countries (e.g. Guillen, 2002;Martin, Mitchell, & Swaminathan, 1995; Martin,Swaminathan, & Mitchell, 1998).

Our theoretical point of departure is the theory offoreign expansion and its emphasis on firm-leveladvantages developed in a home country (Hymer,1976; Kindleberger, 1969). We seek to show that thesocial network approach can offer a comprehensiveand insightful analysis of the impact of a firm’shome country on its pattern of internationalization.The network literature has identified two main ad-vantages associated with a firm’s position in a so-cial structure. First, networks confer social status(Podolny, 1993, 2001). One common way of think-ing about social status is in terms of centrality,which refers to the extent to which a node in anetwork is linked to other nodes, especially thosealso characterized by high social status. Social sta-tus serves as a signal of the quality and trustwor-thiness of a focal firm, thus reducing so-called al-tercentric uncertainty—that is, the uncertainty thatpotential customers, suppliers, or partners mightfeel about the firm (Jensen, 2003; Podolny, 2001).Second, the focal firm may be a broker or interme-diary between clusters of firms otherwise discon-nected from each other (Burt, 1992; Podolny, 2005).A broker occupies a distinctly advantageous posi-tion, as other firms depend on it to obtain crucialinformation, conclude deals, or get things done(Burt, 1992, 2005).

We argue that the advantages arising from afirm’s network position in its home country canaffect both its propensity to pursue foreign oppor-

We thank Editor Duane Ireland and three anonymousreviewers for their valuable comments. Funding from theMack Center for Technological Innovation at the Whar-ton School is gratefully acknowledged. We also thankBoston University School of Management for support inacquiring the data. Seminar participants at Boston Uni-versity, Kellogg, London Business School, MIT, Rutgers,and Wharton; participants at various conferences; andVit Henisz provided excellent comments and sugges-tions. We thank Simone Polillo for his help with thecalculation of the network variables.

� Academy of Management Journal2010, Vol. 53, No. 2, 390–410.

390

Copyright of the Academy of Management, all rights reserved. Contents may not be copied, emailed, posted to a listserv, or otherwise transmitted without the copyright holder’s expresswritten permission. Users may print, download or email articles for individual use only.

tunities and its choice of foreign markets to enter,two of the most fundamental research issues in theinternational management field. We propose to an-alyze the home country social structure withinwhich a firm is embedded as a determinant, amongothers, of foreign expansion and market choice. Wealso examine how the impact of network-relatedadvantages on foreign market entry changes as net-works evolve over time.

Our core argument is that network-related advan-tages differ in their transferability to foreign loca-tions. Only advantages of universal applicability orappeal can be exploited in a large number of mar-kets, industries, or locations (Buckley & Casson,1976; Caves, 1996; Helfat & Lieberman, 2002; Hen-nart, 1982). Some advantages may be more loca-tion-specific (e.g., marketing skills), whereas others(e.g., technology or organizational capabilities) aretransferable to many locations (Chatterjee &Wernerfelt, 1991; Helfat & Lieberman, 2002; Teece,1980, 1982). We argue a social status advantagearising from network position is valuable in multi-ple contexts and so widely transferable as a signalof the overall quality or competence of a firm(Podolny, 2005). By contrast, brokerage advantageis context-specific in that it is local and contingentin nature (Burt, 1997; Gabbay & Zuckerman, 1998;Xiao & Tsui, 2007).

To examine the transferability of network-relatedadvantages to new settings, we follow Bourdieuand Wacquant’s definition of network advantages(which are also called “social capital”): “The sumof the resources, actual or virtual, that accrue to anindividual or group by virtue of possessing a dura-ble network of more or less institutionalized rela-tionships of mutual acquaintance and recognition”(1992: 119). The idea that advantages originatingfrom a network’s structure may be portable beyondthe original structure is not new. Coleman providedseveral examples in which “an organization thatwas initiated for one purpose is available for appro-priation for other purposes, constituting importantsocial capital for the individual members” (1988:S108). In a similar vein, Uzzi and Gillespie ex-plored “how actor A acquires resources or compe-tencies from actor B that are of value in its inde-pendent transactions with actor C” (2002: 23;emphasis in the original). More recently, Jensen(2003, 2008) examined the transferability of net-work-based advantages from one product market toanother. We extend and complement the literatureon the transferability of network-based advantagesby examining the impact of these advantages onfirms’ propensity to expand abroad and on theirchoice of foreign markets to enter. Most impor-tantly, we examine how focal firms with various

levels of social status and brokerage advantagesreact to the entry of home country partners intoforeign markets, thus providing a dynamic perspec-tive that takes into account how networks and theadvantages associated with them change over time.

Our theoretical development is grounded in em-pirical evidence from the venture capital industry.We tested our arguments using systematic empiri-cal data on the foreign market entry decisions ofU.S. venture capital firms between 1991 and 2002.We calculated the social status and brokerage ad-vantages of firms on the basis of their structuralpositions in the domestic syndication network—which accounts for more than 95 percent of allinvestments by U.S. firms—and examined the ef-fects of these advantages on entry into foreign mar-kets. In the final section of the article, we discussour findings and their generalizability to otherindustries.

By integrating theories of international businesswith those from the field of social network analysis,we strive to contribute to both research traditions.We extend prior work on foreign market entry byemphasizing firm-specific advantages that origi-nate from network structure as opposed to advan-tages that firms develop within their boundaries.This study also contributes to the research on in-terfirm networks by examining the portability ofadvantages originating from a given network out-side the boundaries of the network. We argue andempirically demonstrate that network-based ad-vantages differ in transferability, leading to vary-ing rates of foreign market entry. We also com-plement prior research by highlighting how theimpact of network advantages on foreign marketentry changes as a network evolves.

RESEARCH CONTEXT

For the purposes of this study, we focus ourattention on venture capital firms located in theUnited States and their investments abroad. Ven-ture capitalists raise money from investors of vari-ous types, placing it into a fund that they use toacquire equity stakes in entrepreneurial ventures.At the end of a predetermined period—typicallyseven to ten years—the investments are liquidatedand the proceeds are returned to the investors, lessa management fee of about 20 percent.

In addition to funding, venture capitalists pro-vide entrepreneurs and their ventures with strate-gic advice, contacts, and reputation (Gompers &Lerner, 2000, 2001). The venture capital industry is“an intensely social business” (Freeman, 2005:163), as venture capital firms often syndicate theirinvestments with others. They do so in order to

2010 391Guler and Guillen

share information, access to ventures, resources,expertise, and risk (Castilla, 2005; Gompers & Le-rner, 2000; Sorenson & Stuart, 2001). The wide-spread practice of syndicating venture capital in-vestments provides a unique opportunity to assessthe impact of each firm’s social status and broker-age advantages (e.g., Podolny, 2001; Sorenson &Stuart, 2000).

Network-related advantages in the venture capi-tal industry have been documented in earlier work.Social status provides firms with a key advantagein the venture capital community, because invest-ments involve a high level of uncertainty, a “leap offaith” (Gompers & Lerner, 2001). Endorsement by ahigh social status venture capitalist greatly en-hances a venture’s chances of success by providinga signal of the venture’s underlying quality to po-tential partners and investors (Lerner, 1994; Stuart,Hoang, & Hybels, 1999). High social status venturecapital firms typically attract other high social sta-tus firms to investment syndicates (Piskorski,2004), and they help ventures perform better sub-sequent to financing (Hochberg, Ljungqvist, & Lu,2007). Hsu (2004) demonstrated that entrepreneursoften “accept a discount” in order to bring a highsocial status venture capital firm on board, mean-ing that they are willing to pay a price to be asso-ciated with higher social status actors.

Brokerage provides equally important advan-tages to venture capital firms. Information on po-tential deals flows from one venture capital firm toanother through the syndication network, as firmsinvest together. Brokers mediate between multipleinvestment syndicates that do not often invest witheach other, and this mediation enables the brokersto access diverse investment opportunities, re-sources, and potential partners (Piskorski & Anand,2005; Podolny, 1993). Illustrating the importance ofsuch access, a venture capitalist at Internet CapitalGroup (ICG) observed this: “Several recent partnercompanies encouraged ICG to acquire an interest inthem despite the fact that they were adequatelycapitalized because these companies wanted accessto our partner company network” (eBrandedbooks,2000: 233–234). Broker firms take advantage of theweak ties in their networks by obtaining ideas andparticipating in deals through referrals. “VCs knowthat something that comes in as a referral is usuallymuch better on average than something whichcomes in purely over the transom” (eBranded-books, 2000: 160–161). In short, brokerage advan-tage provides venture capital firms with access to alarger set of opportunities and resources.

Our theoretical perspective focuses on the trans-ferability of social status and brokerage advantagesacross national boundaries and on the way that

these advantages change as a network evolves overtime. We begin by examining the central role thathome country advantages play in the theory of for-eign market entry.

THEORY AND HYPOTHESES

International business scholars have long main-tained that a firm’s decision to go abroad is a mo-mentous one (Aharoni, 1966; Caves, 1996; Dun-ning, 1993). Firms’ leaders ponder very carefullywhether to go abroad and which foreign markets toenter, taking into account a variety of factors, in-cluding geography, culture, politics, and econom-ics (Caves, 1996; Dunning, 1993). According to eco-nomic theory, firms go abroad only when theexpected benefits of operating in a foreign marketoutweigh the expected costs of doing so (Caves,1996; Hymer, 1976). When entering a new foreignmarket, firms face a “liability of foreignness” in thatthey experience a higher cost of operating thantheir domestic competitors (Hymer, 1976; Kindle-berger, 1969; Zaheer, 1995). There are two mainsources of this liability. First, a firm entering aforeign country may not fully know or understandlocal rules, practices, and patterns of behavior inthe new market; and second, it may lack the legit-imacy needed to operate in the new market, sincelocal actors do not know how reliable or trustwor-thy the entering firm is (Zaheer, 1995). Because theliability of foreignness makes it costly for firms tooperate in foreign markets, firms tend to go abroadonly when they possess firm-specific advantagesthat are valuable in the host country and can offsetor reduce these costs (Buckley & Casson, 1976;Caves, 1996; Hennart, 1982). For instance, firmswith technological capabilities, marketing know-how, branding skills, and/or organizational capa-bilities tend to enter new foreign markets in orderto exploit these advantages across borders.

In spite of decades of research, the literature oninternational business has placed little emphasison whether and how advantages related to networkposition influence patterns of international expan-sion. When a firm enters a foreign market, it alsoenters a new system of relationships, which arecritical to its operations and success in the newmarket. The success of the firm in the foreign mar-ket partly depends on the demand that the firm cangarner, the supplier relationships it can establish,and the human resources it can attract. Prior re-search documents the importance of attracting buy-ers and suppliers in the new markets. Martin et al.(1995), for example, showed that most Japaneseautomobile manufacturers and suppliers have re-created their links in expanding to North America.

392 AprilAcademy of Management Journal

Chang (1995) and Guillen (2002) similarly demon-strated that business group ties have helped firmsinvest abroad by enabling sharing of technology,resources, and experience. Other studies have in-dicated that the tendency of professional servicefirms to invest abroad increases with their access tohuman capital, and with their links to corporateand government clients (Hitt, Bierman, Uhlen-bruck, & Shimizu, 2006). These studies have under-scored the importance of both new and prior net-work ties in the international investment decisionsof firms, but they have not examined the effect ofadvantages arising from a firm’s network positionin its home country. Therefore, it is germane to askwhether the network advantages developed in thehome country influence the firm’s decision to entera foreign market by helping it secure access tocustomers, inputs, or other types of resources. Al-though the impact of network advantages has beenexplored in the context of firms’ entries into newproduct lines (e.g., Jensen, 2003, 2008), no previousstudy has undertaken either theory development orempirical testing of their effect on foreign marketentry.

The literature on international management haslong emphasized that the home country of a firmexerts a defining influence on its pattern of inter-national expansion (Guillen & Suarez, 2005). Yetnot all firms relate to their home country environ-ment in the same way. In particular, the extent andpattern of their embeddedness in local social net-works vary. We focus our attention on the way inwhich the advantages from two key network posi-tions in a firm’s home country—social status andbrokerage—affect two types of decisions: the deci-sion to go abroad, and the choice of foreign marketto enter. Our theory development proceeds in twosteps: First, we examine the effects of social statusand brokerage advantages on foreign market entry,given a specific network structure. Second, we in-vestigate the impact of social status and brokerageon foreign market entry in a dynamic context,namely, the context that exists after a home countrypartner of the focal firm enters the foreign market.In this latter step, we build on recent research em-phasizing the evolution of networks as a result ofcontinuing exchange (e.g., Burt, 2007; Piskorski &Anand, 2005; Soda, Usai, & Zaheer, 2004).

Social Status

Social status is the standing, worth, esteem, orprestige of an actor arising from its position in agiven setting—that is, its relationships to others(Burt, 1982). Podolny noted that in its sociologicalsense, “The concept of [social] status invokes the

imagery of a hierarchy of positions—a pecking or-der—in which an individual’s location within thathierarchy shapes others’ expectations and actionstoward the individual and thereby determines theopportunities and constraints that the individualconfronts” (2005: 11). One frequent approach toassessing an individual’s or a firm’s social statusinvolves examining the extent to which its relation-ships with others enhance its centrality in the so-cial structure (Podolny, 2001). In other words, afirm’s social status depends on the social status ofthe other firms or actors to which it relates (Stuartet al., 1999).

It is important to note that social status is differ-ent from reputation. Reputation is based on the pastperformance of a focal actor and is a more directindicator of quality (e.g., Jensen & Roy, 2008; Wash-ington & Zajac, 2005; Wilson, 1985). In contrast,social status is a structural attribute of individualsor firms that are embedded in a certain social struc-ture (Gould, 2002; Podolny & Phillips, 1996). Socialstatus is loosely linked to actual quality or perfor-mance, because information on changes in actualperformance diffuses through the social structureonly slowly and in an incomplete or biased fashion(Bothner, Kang, & Lee, 2007; Podolny, 1993). Socialstatus may only exhibit a weak link to actual per-formance, but it positively influences the collectiveperceptions of potential partners in regard to thefocal firm and its outputs (Perrow, 1961), espe-cially in the absence of any information about thefirm’s actual quality or trustworthiness (Jensen,2003; Podolny, 1993, 1994; Stuart et al., 1999). AsPodolny argued, the social status of an actorhelps others assess its quality or trustworthinessin situations in which those attributes are only“imperfectly observable” (2005: 18).

Firms with high social status enjoy several ben-efits as a result of their perceived quality, whichhelp them improve their performance and reinforceperceptions of high quality through a “virtuous cy-cle” (Merton, 1968). First, high social status firmsare more desirable as exchange partners, becauseaffiliation with high social status actors enhancesthe social status of the partners (Podolny, 1993;Stuart et al., 1999). Second, they enjoy legitimacyand deference from others thanks to their standingin the social hierarchy (Gould, 2002; Phillips &Zuckerman, 2001; Podolny & Phillips, 1996). Fi-nally, high social status provides firms with favor-able access to resources, such as information (Both-ner, Kim, & Smith, 2008), financial capital (Stuartet al., 1999), and human capital (Bothner et al.,2008; Phillips & Zuckerman, 2001; Podolny, 1993).

The advantages that accrue from a social statusordering not only persist over time, with a loose

2010 393Guler and Guillen

link to prior performance (Podolny, 1993), but alsocan be exploited outside the network in which theyoriginated, including in new markets. Although afirm’s status is defined and measured in relationalterms, signals of quality that emanate from statusare available to all market participants, even tothose that are not connected to the focal firm di-rectly or indirectly because they are not part of thenetwork. Research documents that status is partic-ularly valuable as a signal of quality when potentialexchange partners in a new market are uncertainabout the quality or trustworthiness of the enteringactor and seek information about the focal actor(Podolny, 2005: 18, 35, 38). The social status signaldiffuses to potential partners even when direct tiesare not present, by attracting “the attention of in-dustry analysts and the business press, as well aspotential employees, suppliers and customers”(Stuart et al., 1999: 319). Podolny (2005) providedillustrations of how potential exchange partnersnot connected to a firm or its network may usestatus to infer quality in a variety of contexts, in-cluding the diamond trade, investment banking,and the British shipping industry. Similarly, Jensen(2003) found that high social status in commercialbanking facilitated entry into investment banking, amarket in which commercial banks had no pres-ence, and hence no ties, for legal reasons. Thebanks’ social status in their original market sig-naled the quality of their products or services innew markets, especially during the initial period ofentry, when other firms had little informationabout the entering banks and no prior market tiesto them.

We argue that high social status firms are morelikely to enter foreign markets than their low socialstatus counterparts because social status–relatedadvantages help alleviate the lack of knowledgeregarding the quality of the entering firms. As notedabove, one of the key sources of the liability offoreignness is entering firms’ lack of legitimacy inthe foreign market, since potential collaborators,suppliers, and customers in that market do notknow or do not yet trust the new entrants (Hymer,1976; Kindleberger, 1969; Zaheer, 1995). Enteringfirms thus face a hurdle in that they must success-fully convey their intent and operational ability todeliver their promised outputs (Zaheer, 1995).These observations echo the findings in the net-work literature that firms entering foreign mar-kets face a high degree of altercentric uncertainty(Podolny, 1993: 16 –17).

In such cases, social status in the home countrymay provide a valuable advantage by reducing theliability of foreignness. A firm’s affiliations withother high social status actors in its home country

assure potential exchange partners in the foreignmarket about the quality and reliability of its out-put, and hence they foster trust. Social status mayincrease the firm’s legitimacy and desirability as aninvestment partner and subsequently enhance itsaccess to local resources (Podolny, 1994; Stuart,2000; Stuart et al., 1999). For instance, a high socialstatus venture capital firm may be in a better posi-tion than a lower social status counterpart to attractinvestment partners, suppliers, customers, and inturn, high-quality investment opportunities in aforeign market (Merton, 1968).

In sum, we expect that social status will increasethe expected returns to market entry by reducingthe firm-specific costs of establishing legitimacyand desirability as an exchange partner. A firm’spossession of a social status advantage in its homecountry will facilitate international expansion byreducing altercentric uncertainty and the liabilityof foreignness. Therefore, we predict:

Hypothesis 1. The greater the social status of aventure capital firm in its home country net-work, the greater its rate of foreign marketentry.

Brokerage

High social status firms are more likely to enterforeign markets, but we suggest that firms that en-joy a brokerage advantage in their home country areless likely to invest abroad. The reason has to dowith the local nature of brokerage, the difficulty ofusing this advantage in a foreign market, and thesuperior returns to leveraging brokerage advantagein the home market.

Brokerage advantage refers to the benefits ob-tained from regulating information flows. A brokerbenefits from its ability to bring together separategroups from opposite sides of the “structural holes”in a network. The broker enjoys three interrelatedadvantages over other firms, namely, “access to awider diversity of information, early access to thatinformation, and control over information diffu-sion” (Burt, 2005: 16) (see also Adler & Kwon,2002). Such firms generate more innovative ideasand enjoy more entrepreneurial opportunities bybringing together disparate parties (Burt, 1992; Na-hapiet & Ghoshal, 1998; Walker, Kogut, & Shan,1997). In contrast, a firm with many redundantties—that is, few structural holes in its network—ismore constrained in the extent to which it canbenefit from its network position.

Compared to social status advantage, which canbe transferred from one setting to another, broker-age advantage is much harder to transfer. Previous

394 AprilAcademy of Management Journal

research has noted several mutually reinforcingreasons for the “stickiness” of brokerage advan-tages. First, as a key theorist in the network litera-ture has pointed out, brokerage “provides a tempo-rary, local advantage” (Burt, 2005: 233). In contrastto social status advantage, which can carry overwithout a firm’s actually being present in the newnetwork, the benefits that accrue to a brokerthrough accessing, relaying, or withholding infor-mation are limited by the boundaries of its networkand can change as actors pursue new relationships.For instance, a firm that bridges ties between twodisparate clusters may come up with innovativeideas that span both clusters (e.g., Ahuja, 2000), butits brokerage role does not necessarily transfer to athird cluster with which it has no prior affiliation.Recent empirical evidence suggests that brokerageadvantage is concentrated within an actor’s imme-diate network, with brokerage between indirect tiesbeing of little value (Burt, 2007). Brokerage advan-tage is local and context-specific, and not applica-ble beyond the actor’s immediate network.

Second, the existence of brokerage advantagesmay lead potential partners to perceive the brokerfirm as opportunistic and as a less desirable poten-tial partner in a new network. Brokerage advan-tages exist in social networks that are “open struc-tures,” networks that are far from being saturatedwith redundant ties. As Coleman observed, it isdifficult to enforce appropriate patterns of behav-ior and prevent opportunism in an open socialstructure because the “collective sanctions thatwould ensure trustworthiness cannot be applied”(Coleman, 1988: S108; see Portes [1998] for a re-view of the lineage of this concept). As a result,broker firms may find it hard to forge new partner-ships. In this vein, Jensen (2008) found that incum-bent investment banks preferred to partner withentering commercial banks characterized by weakbrokerage advantages in their own networks, be-cause the commercial banks viewed entering bankswith strong brokerage advantages as threats to thestability of the industry’s network.

The third reason that a brokerage advantage en-joyed in one setting is difficult to transfer to an-other setting has to do with potential differences inthe normative legitimacy associated with the dis-criminatory regulation of information flows. A va-riety of network scholars have found that an actor’sability to take advantage of its brokerage advantagecan vary greatly depending on how legitimate orappropriate this exploitation is perceived to be(Burt, 1997; Fernandez & Gould, 1994; Gabbay &Zuckerman, 1998). Given our focus on foreign mar-ket entry, it is important to consider what networkresearchers have found about the normative legiti-

macy of brokers in different settings. A recent studyusing data on social networks inside Chinese or-ganizations showed that the benefits derived frombrokerage in China were very small or even nonex-istent because the concept of brokerage was at oddswith the value placed on cooperation and informa-tion sharing in a collectivistic culture (Xiao & Tsui,2007). Thus, an actor enjoying a brokerage advan-tage in its home country may be unable to use itin a foreign market in which the self-interestedmanipulation of information flows is seen asinappropriate.

Drawing on these interrelated arguments fromthe literature, we propose that firms enjoying abrokerage advantage in their home countries willrefrain from entering new markets. All else heldequal, such firms will be more likely to exploitbrokerage advantage in their local, home countrynetworks through domestic operations rather thanto incur the costs and face the difficulties associ-ated with international operations.

The venture capital industry provided us with anappropriate context in which to examine the localnature of brokerage advantages. In their home mar-kets, venture capital firms occupying brokerage po-sitions gain access to information on investmentopportunities from their diverse syndicate partners(Piskorski & Anand, 2005; Podolny, 1993). How-ever, since venture capital firms often invest inventures in close geographic proximity (Sorenson &Stuart, 2001), their brokerage advantages in localsyndicate networks are not likely to extend intointernational markets. We therefore expect a ven-ture capital firm that acts as a broker in its localnetwork to continue pursuing local opportunitiesrather than to explore international ventures, be-cause in international markets it does not possess astructural advantage and faces the additional costsof expansion. Given that the benefits associatedwith brokerage are context-specific, and thus diffi-cult to transfer from one location to another, andthat a firm occupying a niche rich in structuralholes in its home country has little incentive toenter a new system of relationships in a foreigncountry, we predict the following:

Hypothesis 2. The greater the brokerage advan-tage of a venture capital firm in its home coun-try network, the smaller its rate of foreign mar-ket entry.

Two important qualifications to these argumentsare necessary. First, the advantage related to highsocial status or brokerage in one setting might helpa firm attain greater performance, grow in size, andaccumulate experience. Greater size and experi-ence have been found to correlate with a greater

2010 395Guler and Guillen

propensity to enter foreign countries (Caves, 1996;Dunning, 1993). Our argument is focused on thedirect effect of social status and brokerage advan-tages on foreign market entry, with the size, expe-rience, and prior performance of a firm controlledfor. The second qualification is that the continuityor sustainability of social status and brokerage ad-vantages over time depends on the actions of boththe focal firm and those connected to it in the homecountry, as home country partners can reduce oreven eliminate the firm’s advantages (Burt, 2005).Although our first two hypotheses rest on the as-sumption of a stable network structure, we nowturn to an examination of how social status andbrokerage advantages change as a network evolvesover time.

Dynamics of Social Status andBrokerage Advantages

One of the key findings in the international busi-ness literature is that the presence of partners inforeign markets is an important determinant of afirm’s choice of foreign markets to enter (e.g.,Guillen, 2002; Henisz & Delios, 2001; Shaver,Mitchell, & Yeung, 1997). Few studies, however,have examined how partners’ impact on marketchoices may vary according to the characteristics ofan entering firm, and in particular, its network po-sition. Social status and brokerage advantages stemfrom the way in which the firm relates to others. Itis therefore important to assess how a home coun-try partner’s decision to enter a given foreign mar-ket changes the social status and brokerage advan-tages of a focal firm, and how these changes, inturn, affect its decision to enter that foreign market.

The value of social status and the presence ofhome country partners in a foreign market. Whena firm’s home country partner enters a foreign mar-ket, actors located in that market gain access to awider array of information from which to drawinferences about the quality of the focal firm. Thehome country partner may possess informationabout the focal firm that can be of use to actors inthe foreign market. The new information that thepartner makes available to these actors can changethe potency and relevance of the focal firm’s homecountry social status in reducing altercentric uncer-tainty, because actors in that market no longer haveto rely on social status alone as a signal. As Podolnyobserved, social networks influence the use of so-cial status as a signal of quality “by serving asaccess constraints, inhibiting contacts which couldpotentially alter perceptions” (1993: 833). If actorsin the foreign market can learn about the focalfirm through direct experience with its home

country partners, the value of social status insignaling the quality and trustworthiness of thefocal firm declines.

This argument in no way implies that the firm’ssocial status is eroded by the entry of a home coun-try partner, but rather that the value of its status toactors in the foreign market partly dissipates. Asargued above, social status is a noisy measure ofquality because it is a lagging and biased indicatorof changes in quality (Bothner et al., 2007; Podolny,1993). Prior to the arrival of a home country part-ner, actors in the foreign market have little choicebut to assess the quality of the focal firm on thebasis of its social status. The availability of alterna-tive sources of information reduces the extent towhich firms in the foreign market use social statusto cope with the altercentric uncertainty abouttransactions or collaboration with the focal firm(Jensen, 2003). When less noisy signals of qualitybecome available, home country social status losesat least some of its significance as a firm-specificsource of advantage that can be exploited in foreignmarkets. For example, Podolny argued that “previ-ous exchange partners of an investment bankshould rely less on status as a signal of quality tomake inferences about the desirability of a subse-quent exchange relation since they have privateknowledge of the bank’s quality” (2005: 38). As aresult, higher social status firms will see the signal-ing advantage of social status erode as one or moreof their home country partners enter a foreign mar-ket. It is of fundamental importance to note that wepredict an erosion of a firm’s social status advan-tage only in those foreign markets in which at leastone of its home country partners has established apresence. In other markets, social status continuesto be a practical way for local firms to draw infer-ences about the quality of the focal firm.

On the basis of our prediction, stated in Hypoth-esis 1, that social status reduces altercentric uncer-tainty in foreign markets and thus accelerates therate of foreign expansion, we cast our argumentconcerning the entry of a home country partner intoa foreign market as an interaction effect that mod-erates the positive effect of social status:

Hypothesis 3. The presence of a home countrypartner of a venture capital firm in a specificforeign market reduces the positive impact ofsocial status on the focal firm’s rate of entry.

The value of brokerage and the presence ofhome country partners in a foreign market. Theentry of a focal firm’s home country partner into anew foreign market may have two related effects onthe firm’s brokerage advantage. The first effect con-cerns the ability of the focal (broker) firm to enter

396 AprilAcademy of Management Journal

the new market. The entry of a home country part-ner into a foreign market extends the informationreach of the broker’s network. The partner, whichnow has access to information about conditions,opportunities, and possible collaborations in thatmarket, can relay this information to the focal firm.Let us illustrate with an example. Assume that firmX is a broker that bridges a structural hole betweenfirm A and firm B and that all three firms arelocated in the same home country. Firm X enjoysaccess to diverse information from both firms Aand B, and it is therefore in an advantageous posi-tion vis-a-vis its two partners.1 If firm B enters anew foreign market and establishes a relationshipwith firm C in the new market, this will expand theinformational content of firm X’s network and in-crease firm X’s advantage. Although firm X had noinformational access to the new market prior tofirm B’s entry, firm B can now provide informationabout suppliers, buyers, collaborators, and otherfirms that firm X can pursue as potential partners inthis market. In a way, firm B’s presence in theforeign market reduces the cost of entry for firm Xby decreasing the liability of foreignness. It is im-portant to note that although brokerage advantagesare still local to the network, the expansion of theboundaries of the network as a result of firm B’sforeign market entry increases the scope of infor-mation available to firm X. Therefore, we proposethat the first effect of the presence of a partner in aforeign market is to increase the broker firm’s abil-ity to enter the new market.

As we suggested above, existing research docu-ments that firms frequently use their network tiesto reduce the uncertainty associated with enteringnew foreign markets (e.g., Guillen, 2002; Henisz &Delios, 2001; Shaver et al., 1997). In the venturecapital industry, firms expand their geographicreach by coinvesting with other venture capitalfirms that have a presence in more distant markets(Sorenson & Stuart, 2001). Extending previous evi-dence that firms tend to follow their partners intoforeign markets, we argue that broker firms aremore likely to benefit than other firms from thepresence of a partner in the new market. Becausebroker firms tend to search proactively for di-

verse information and exploit their ties to gainearlier access to opportunities, they are morelikely than firms without a brokerage advantageto exploit their partners’ presence when expand-ing into foreign markets.

The second effect of a partner’s entry into a for-eign market has to do with the impact of new tieson preexisting brokerage advantages. Such new re-lationships in a foreign market can create a situa-tion in which “high returns to the brokers whobridge one structural hole can move to brokers whobridge a different structural hole” (Burt, 2005: 235,note 9). It is useful to think of brokerage advantageas the opposite of network constraint (Burt, 2005).In our example, when firm B establishes a nonre-dundant tie with a new partner in the foreign mar-ket (firm C), it gains an additional degree of struc-tural autonomy, therefore making firm X moreconstrained (Jensen, 2008). By establishing its owndirect relationship with firm C, firm X can increasethe structural constraint of firm B and reduce itsown, although not to the original level existingprior to the establishment of firm B’s link to firm C.Both firm X and firm B end up being more struc-turally constrained, but firm X regains part of itsoriginal brokerage advantage (Burt, 2005).

This sequence of dynamic change in a network isclearly relevant to the foreign market entry of afocal firm’s home country partner. The brokerageadvantage stemming from the bridging of a struc-tural hole in the home country changes when thepartner establishes a presence in a given foreignmarket. Although the presence of a partner in theforeign market offers the focal firm an opportunityto exploit the available investment opportunities inthat market, it also limits the focal firm’s ability tocontrol the information flow from the foreign mar-ket, since brokerage through indirect ties is of littleor no value (Burt, 2007). The very presence of thepartner in the foreign market has the potential toundermine the original brokerage advantage, as thepartner can bypass or circumvent the focal firm andconvey information about opportunities in the for-eign market directly to its own contacts back in thehome country. If the partner obtains information ordevelops relationships in the foreign market thatcan be of value to other firms in the home country,the brokerage advantage enjoyed by the focal firmin the home country can become less profitable(Burt, 2007). The entry of the partner into a newforeign market thus creates an incentive for thefocal firm to follow its partner into the new mar-ket in order to sustain its preexisting brokerageadvantage.

The replication of the actions of one’s networkpartners has been extensively discussed in the lit-

1 The very act of brokering between firms A and B mayin time create a link between these two firms, erodingfirm X’s brokerage advantage. It is in this sense thatbrokerage advantages are transient (Burt, 2005). It is pos-sible that firm X might bridge many structural holes andproactively look for new holes in its network in order topursue a brokerage “strategy” (Burt, 2005). For simplic-ity, we focus here on what happens with respect to asingle structural hole.

2010 397Guler and Guillen

erature on social networks. As Bothner noted,“When a social actor’s proximate rivals haveadopted an advantageous trait, that actor is thenlikely to adopt it in order to avert the probablesocial and economic costs of falling behind” (2003:1180). Actors are especially likely to emulate theirrivals when they perceive the potential threat thatthe rivals will replace them in a social structure(Burt, 1987; White, 2002). At the organizationallevel, the pattern of competitive emulation to avertthe threat of substitution has been empirically doc-umented in the contexts of campaign contributions(Mizruchi, 1992), the adoption of new technologiesor organizational practices (Bothner, 2003; Guler,Guillen, & MacPherson, 2002), and new market en-try (Baum & Korn, 1996). We extend this logic ofcompetitive network evolution to the context offoreign market entry and argue that, when con-fronted with the possibility that a partner mightaccumulate a brokerage advantage of its own bybridging home and foreign clusters of relationships,a firm will seek to establish its own presence in theforeign market to preserve at least part of its origi-nal home country brokerage advantage.

Since we predicted above that firms enjoying abrokerage advantage have less inclination to pursueforeign expansion (Hypothesis 2), we cast our argu-ment concerning a focal firm’s reaction to the pres-ence of a home country partner in a foreign marketas an interaction effect that moderates the negativeeffect of brokerage. Thus, we propose:

Hypothesis 4. The presence of a home countrypartner of a venture capital firm in a specificforeign market reduces, and possibly reverses,the negative impact of brokerage on the focalfirm’s rate of entry.

DATA AND METHODS

We compiled international venture capital in-vestment data from the VentureXpert database pro-vided by Thomson Financial,2 which collects infor-mation through an annual survey of over 1,000private equity partnerships in the United States.This database has been used extensively in venturecapital research, although mostly to examine in-vestments in the United States (e.g., Gompers &Lerner, 2000; Guler, 2007; Hochberg et al., 2007;

Shane & Stuart, 2001). Each of the firms surveyedhas a presence in the venture capital industry, al-though some also invest in other forms of later-stage private equity. We focused on the foreigninvestments of the 1,010 U.S.-domiciled venturecapital firms active between 1990 and 2002.3 Ac-cording to VentureXpert, U.S. venture capital firmsbegan making cross-border investments in 1989, soconcern regarding left-censoring of data on eventswas minimal. The U.S. venture capital industrygrew significantly during this period, in terms ofboth capital available for investment and the num-ber and amounts of actual investments. Activity inthe United States and abroad peaked in the year2000, which lay within our sample for analysis.

We compiled data on the economic and politicalcharacteristics of the complete population of 207countries from the World Bank’s (2004) WorldDevelopment Indicators database, Henisz’s(2000) Index of Political Constraints, and theCentre d’Etudes Prospectives et d’InformationsInternationales (CEPII) geographic distance data-base for the 1990–2002 period. We merged theventure capital investment data with country-leveldata and excluded observations in which country-level data were missing through a casewise dele-tion procedure. The final data set included all ac-tual and potential investments of the sample of1,010 venture capital firms in the 95 countries forwhich we have complete information.

To capture causal relationships between the in-dependent and dependent variables, we lagged allleft-hand-side variables by one year.4 We thereforeexamined investments over the 12 years between1991 and 2002. As of the end of 2002, 216 of the1,010 venture capital firms had made 1,714 roundsof investment in 920 ventures located in 40 differ-ent foreign countries.5 The largest investors wereWarburg Pincus, Advent International Corporation,and Japan/America Ventures. The distribution of

2 VentureXpert includes “standard U.S. venture in-vesting” in portfolio companies (ventures), as long as theventure is domiciled in the United States, at least one ofthe investors is a venture capital firm, venture invest-ment is a primary investment, and the investment entailsan equity transaction.

3 Although the number of venture capital firms repre-sented in the sample may seem high, it should be notedthat not all firms were active during the entire period ofobservation. We checked the sensitivity of our results byexcluding venture capital firms that made fewer thanthree investments in the United States in each year. Thisyielded a sample of 552 firms and 242,017 firm-country-years. The results of the analyses with the reduced sam-ple were qualitatively similar to those reported here.

4 To ensure the best model fit, we estimated the mod-els using three-, two-, and one-year lags. Independentvariables with a one-year lag provided the best overall fit.

5 The location of the ventures refers to the location oftheir headquarters, not to the countries in which theventure may have additional operations or sales.

398 AprilAcademy of Management Journal

rounds by investment stage is as follows: start-up orseed, 6 percent; early stage, 22 percent; expansion,51 percent; later stage, 7 percent; buyout or acqui-sition, 7 percent; and other, 6 percent. We includedall of these rounds in our primary analysis. Sinceinvestment stage may affect the level of investmentuncertainty (Gompers, 1995; Podolny, 2001), werepeated the analysis excluding the last three cate-gories. Our results were robust to this exclusion.We excluded from all analyses the 17 investmentsin ventures that had gone public before the U.S.venture capital firm invested. However, we re-tained in the sample the 794 firms that never in-vested abroad and the 55 countries in which noinvestments took place, because their exclusionwould have introduced sample selection bias intoour analyses. We nevertheless assessed the robust-ness of our results by repeating the analyses on areduced sample that excluded these firms andcountries, as reported below.

Measures

Dependent variable and unit of analysis. Thesample consisted of firm-country-year observa-tions. Each venture capital firm was at risk of en-tering a country during a given year. The depen-dent variable (an event) equaled 1 if firm i enteredcountry j during year t. We had complete data for517,981 firm-country-year observations, represent-ing 847 unique country-years, and estimated ourmodels using two different samples. For the firstsample, we excluded firm-country-year observa-tions subsequent to a focal venture capital firm’sfirst entry into each country j. This sample com-prised 516,493 observations. For our second sam-ple, we included repeated entries by the same ven-ture capital firm into the same market, to test forrobustness. Within the 12-year period, we observed688 nonzero firm-country-year combinations, 465of which were first entries into a given country.

Independent variables. As noted above, priorresearch has established the importance of venturecapital syndication networks in the flow of invest-ment information and the establishment of socialstatus in an industry (Castilla, 2005; Gompers &Lerner, 2000; Hochberg et al., 2007; Sorenson &Stuart, 2001). We therefore measured the networkadvantages in the industry by examining the posi-tion of each venture capital firm in its home coun-try syndication network. We considered a networktie to exist only if two firms invested together in thesame U.S. venture and in the same round. Follow-ing previous research, we measured social statususing Bonacich’s (1987) eigenvector centrality mea-sure. This indicator takes into account the central-

ity of the actors to which a focal actor is connected.Because it captures affiliation with other high so-cial status actors, it is a better measure of socialstatus than alternative centrality measures (Jensen,2003; Nerkar & Paruchuri, 2005; Podolny, 1993,1994). We only considered a tie to exist if two firmsinvested together in the same U.S. venture and inthe same round. For each year t, we calculated thecentrality score using the information for both two(t � 2) and one (t � 1) years earlier and for t itself(Castilla, 2005; Hochberg et al., 2007; Piskorski &Anand, 2005). The centrality score ranges between0 (for isolated firms with no contacts) and 1 (forfirms that syndicated with other central firmsonly). Thus, the centrality score for firm i in year twas modeled as follows:

ci � ��Aijcj,

where � is the reciprocal of an eigenvalue and A isthe adjacency matrix denoting the existing ties be-tween firms i and j. The centrality of each firm i isa function of the centrality of the other firms towhich it is connected. We assigned a 0 to isolatedfirms with no ties to others.

We also followed prior research in measuringbrokerage advantage in using Burt’s (1992) reverse-signed index of constraint, using UCINET to per-form the calculations. In our brokerage measure, weassigned a value of 0, the maximum, to isolatednodes. The measure approaches �1 as the nodebecomes more constrained—that is, as the observedfirm loses brokerage advantage. Thus, the measureis increasing in brokerage advantage. For each year,we calculated brokerage advantage as follows:

Bi � � �j�pij�

q

piqpqj� 2

,

where pij is the proportion of i’s network that re-lates to j, piq is the proportion of i’s network thatrelates to q, and pqj is the proportion of q’s networkthat relates to j, with i � j � q.6

Presence of syndicate partners in each country.We measured the presence of firm i’s syndicatepartners in country j with a dummy variable coded1 if any of firm i’s syndicate partners in its homecountry network had made at least one investmentin country j up until year t � 1.

6 We tested the possibility that isolates might bias theresults by estimating a two-stage model that first esti-mated the probability that a firm would be an isolate andthen the rate of entry conditional on not being an isolate.The results remained unchanged.

2010 399Guler and Guillen

Interaction terms. We included two interactionterms in the full models. We tested the moderatingeffect of home country partners on the social sta-tus–foreign market entry relationship (Hypothesis3) by multiplying the dummy for the presence offirm i’s syndicate partners in each country j by thesocial status measure for firm i. We tested the pro-posed moderating effect of home country partnerson the brokerage-entry relationship (Hypothesis 4)by multiplying the dummy for the presence of firmi’s syndicate partners in country j with the broker-age measure for firm i. To reduce multicollinearitybetween main and interaction effects, we centeredeach continuous main effect (i.e., social status andbrokerage) by subtracting the mean before calculat-ing the interaction terms (Jacard & Turrisi, 2003).This correction reduces multicollinearity withoutaffecting significance testing (Cronbach, 1987).

Firm-level control variables. We included fivecontrols in all models to address concerns aboutthe potential endogeneity of the network measuresand other firm-level unobserved heterogeneity.First, we controlled for the performance of venturecapital firm i in the home country (i.e., the UnitedStates) to account for the possibility that the firmmight enter foreign markets because of its capabil-ities and its prior performance, regardless of itsnetwork advantages. We measured performance asthe ratio of the cumulative number of ventures infirm i’s portfolio that had gone public through aninitial public offering to the total number of theventures that the firm had funded as of year t � 1(Hochberg et al., 2007). Second, we included thenumber of ventures funded by firm i in the UnitedStates as of year t � 1 to account for unobservedfirm heterogeneity in experience or capabilities—what researchers have called venture capital firm“sophistication”—as well as size (Bottazzi, Da Rin,& Hellmann, 2009; Gompers & Lerner, 2000: 236;Kaplan, Martel, & Stromberg, 2005). Third, we in-cluded the number of ventures funded by firm i inforeign countries as of year t � 1, which controlledboth for unobserved firm heterogeneity in generaland for the propensity to invest abroad in particu-lar. Fourth, we added to all models the number ofcountries entered by firm i up until year t � 1,which served as an additional control for firm het-erogeneity concerning the pursuit of foreign oppor-tunities and a greater propensity to go abroad. Andfifth, we controlled for the age of venture capitalfirm i in year t to account for differences in firms’propensities to enter foreign markets based on theirage and cohort. As an additional sensitivity check,we repeated the analysis with a shared frailty termgrouped over venture capital firms to account forunobserved heterogeneity (Gutierrez, 2002). The re-

sults were similar to those reported. We report theresults without the frailty term.

Country-level control variables. We includedcontrols for the size of the economy of each countryrepresented in the data set, measured as gross do-mestic product (GDP) in constant 1995 U.S. dollars,and for the size and development of the local stockmarket, measured by total stock market capitaliza-tion as a percentage of GDP (World Bank, 2004). Wealso controlled for the level of regulatory instabilityin each country, measured as the reverse-signedpolitical constraint index, which captures checksand balances on policy makers that prevent unilat-eral changes in a policy regime (Henisz, 2000). Wecontrolled for the geographic proximity of countryj to the United States, measuring proximity as thesimple distance in kilometers between Washing-ton, DC, and the most populous city in country j,made available by the CEPII. We added a dummyvariable indicating whether English was the officialor most widely spoken language in the country. Wealso included the number of previous entries incountry j by other U.S. venture capital firms upuntil year t � 1 as a control for the attractiveness ofthe country. Lastly, a summary analysis of the datarevealed that the venture capital entries were concen-trated in 11 countries. We therefore included 11dummy variables, one for each of these countries, toaccount for other country-specific factors. As an ad-ditional sensitivity check, we repeated the modelswith fixed effects for each country. The results of theanalyses were qualitatively similar. We report themodels with the 11 country dummies. Table 1 sum-marizes investments in these top 11 host countries.

TABLE 1U.S. Firms’ Foreign Venture Capital Investments, by

Host Country, 1991–2002a

CountryNumber ofVentures

Number ofVentures,

Sample forAnalysis

Number ofRounds

Number ofRounds,

Sample forAnalysis

UnitedKingdom

183 176 441 431

Canada 135 128 242 233Israel 109 107 147 145Japan 91 86 103 95France 55 41 101 83Germany 54 53 96 95China 43 38 81 73India 35 35 95 95Ireland 31 30 50 48Netherlands 30 29 65 63Singapore 25 22 49 46

Total 791 745 1,470 1,407

a Only the top 11 host countries are shown.

400 AprilAcademy of Management Journal

Estimation method. We estimated venture capi-tal firms’ rates of entry into new countries usingtwo different approaches to ensure that our resultswere robust. First, we used a hazard model (Alli-son, 1995; Tuma & Hannan, 1984). The hazardfunction is defined as

h(t) � lim�t30

Pr�t � T � t � �t�T � t��t

and specifies the instantaneous rate at which entryoccurs at time t, given that the event has not yetoccurred (Allison, 1995; Kalbfleisch & Prentice,2002). We used a hazard rate model because it accom-modates time-varying independent variables and al-lows right censoring in the data (Allison, 1995).

We first estimated the hazard rate using a Coxproportional hazards model. However, a test of theproportional hazards assumption using Schoenfeldresiduals revealed that the model did not satisfy thenonproportionality assumption, making signifi-cance testing difficult. We therefore modeled thehazard rate of entering a new country using thepiecewise exponential model in Stata (Sorensen,1999). Piecewise exponential models are semipara-metric models in which the baseline hazard rate isallowed to vary in an unconstrained way in eachpredefined time period. The benefit of this ap-proach is the ability to model time dependencewithout the more restrictive assumptions of para-metric models.

To estimate the hazard rate in each time period,we divided the data into yearly spells (Hannan &Freeman, 1989) and treated the observations as cen-sored unless an event (i.e., an entry) occurred. Inestimating repeated entries, we allowed observa-tions to stay at risk for subsequent events instead ofdropping them from the sample. Thus, we allowedeach subject to experience multiple entries (Alli-son, 1995; Kalbfleisch & Prentice, 2002). In defin-ing the risk set at each failure time, we utilized thecounting process approach developed by Andersenand Gill (1982), in which entry events are assumedto be equivalent and the models predict the “timeto event” (the hazard of experiencing event k afterhaving experienced prior event k � 1. For moredetail on estimating repeated events in Stata, seeCleves [1999]).

We updated the time-varying independent vari-ables in each annual spell, estimating the modelsusing maximum likelihood in Stata. Because therewere multiple observations for each venture capitalfirm and country, observations in the sample mightnot be independent. We therefore calculated robuststandard errors clustered on each country-firmpair, implemented by the “cluster” option in Stata

(Rogers, 1993; Wooldridge, 2002). We also esti-mated alternative models by clustering on firms orcountries only; the results were unchanged.

Next, to address the fact that our data include fewactual events and a large number of nonevents, weused rare events logistic regression analysis to es-timate the probability of each venture capital firm ientering country j during year t. This logistic modelallows prediction of the likelihood of entry andcorrects coefficients for the bias that arises from anexcessive number of zeros (nonevents) in a sample(King & Zeng, 2001). When estimating the piece-wise exponential models, we included 12 “time-pieces,” one for each year. When estimating therare events logistic models, we included 11 yeardummies, omitting the year 2002.

RESULTS

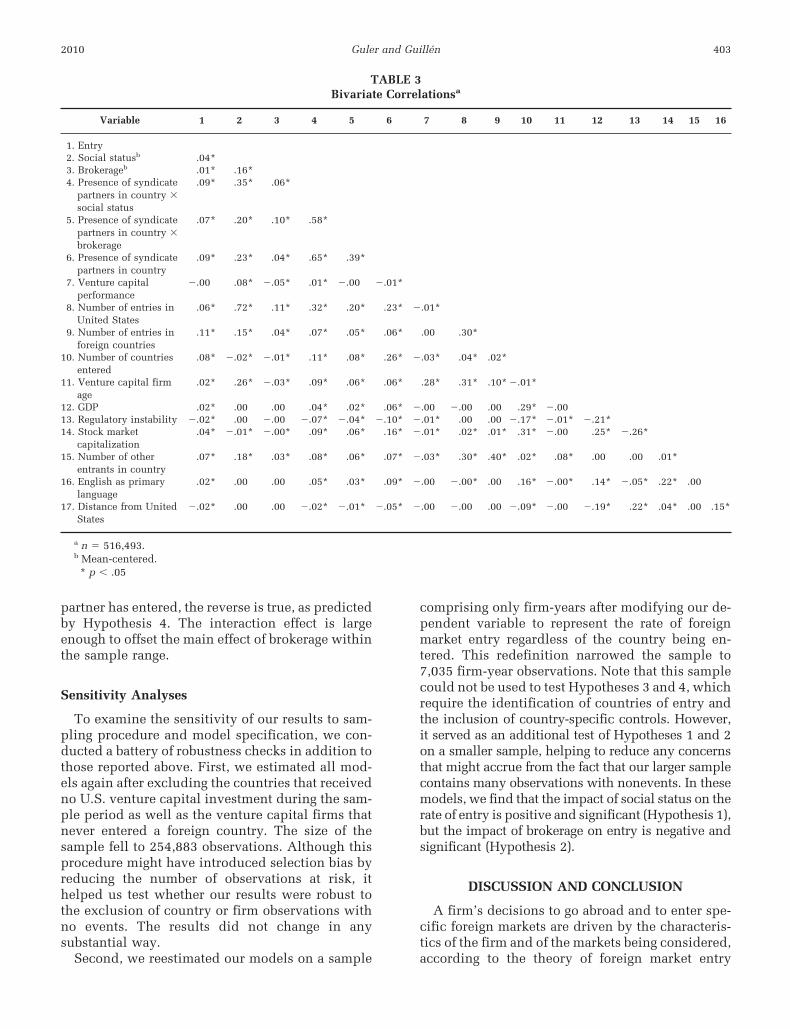

In Tables 2 and 3, we present the descriptivestatistics and the correlation matrix. Entry into acountry is positively correlated with both socialstatus (for which centrality served as proxy) andbrokerage, although the magnitude of the correla-tion is higher for the former than for the latter.Entry is also positively related to the number ofprevious entries into the country. Correlations be-tween most of the independent variables are low,reducing concerns about potential multicollinearity.The only exception is the .71 correlation betweensocial status and the number of ventures funded inthe United States. The exclusion of this last variabledid not change the results of our analyses; we there-fore report models with the number of venturesfunded in the United States as a control.7

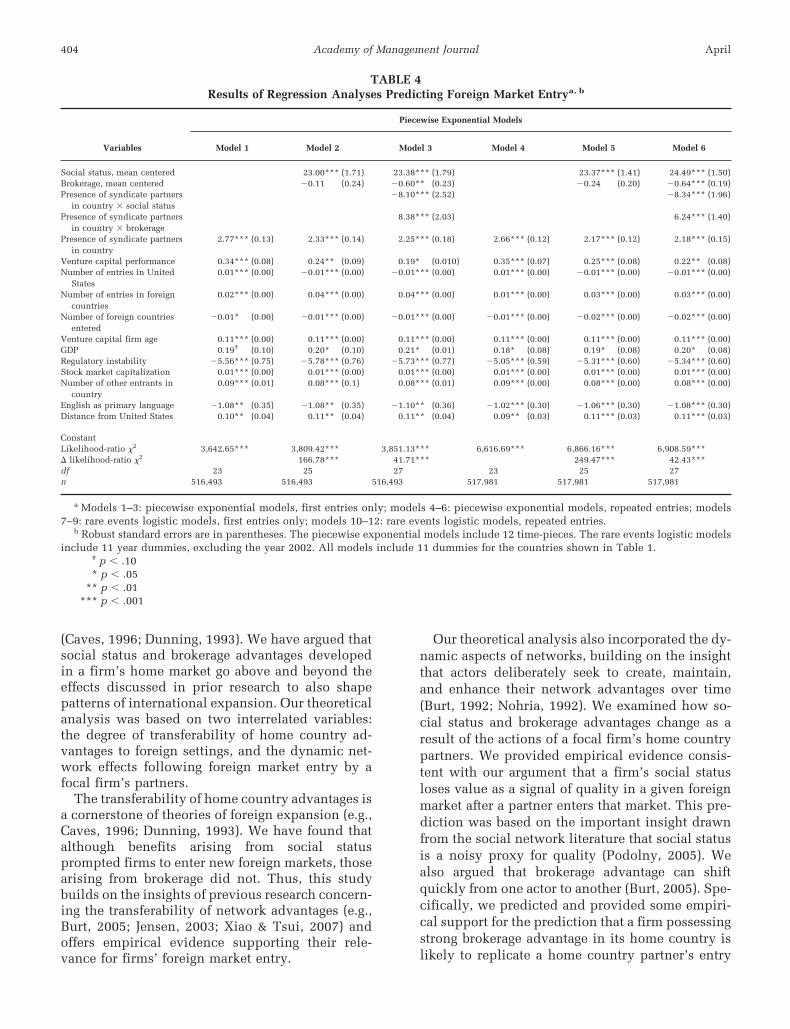

We present the empirical results in Table 4. Mod-els 1–3 predict the rate of first entry, and models4–6 predict the rate of repeated entry, both usingpiecewise exponential models. Models 7–9 predictthe likelihood of first entry, and models 10–12predict the likelihood of repeated entry, this timeusing rare events logistic models. Within each setof models, the first shows the results with controlsonly, the second adds the main effects, and thefinal one is the full model, with main effects andinteraction terms.

As predicted in Hypothesis 1, the higher the so-cial status of a venture capital firm in its homecountry, the greater the rate of foreign market entry.This finding is robust to estimation method and to

7 We also investigated whether the firms with thehighest centrality scores biased the results. Excludingthese firms from model 3, for instance, generated resultssimilar to those reported in Table 4.

2010 401Guler and Guillen

whether first or repeated entries are considered.The main effect of brokerage is negative but notsignificant in the main effects models (2 and 4),failing to provide support for Hypothesis 2.

In Hypotheses 3 and 4, we propose that the pres-ence of home country syndicate partners of a focalfirm in a focal foreign country moderates the rela-tionship between network advantages and marketentry. We found that the interaction between socialstatus and the presence of a home country partneris negative and significant in models 3, 6, and 12,though not in model 9, thus providing robust sup-port for Hypothesis 3. Therefore, the evidence in-dicates that the presence of a home country partnerin the foreign country reduces the value of a firm’ssocial status advantage. The term for the interactionbetween brokerage and the presence of a homecountry partner is positive and significant in mod-els 3 and 6, although it does not reach significance

in the rare events logistic regression models. Thus,we find some support for Hypothesis 4. It is impor-tant to note that the main effect of the presence ofat least one home country partner is positive andsignificant, confirming prior findings that firmsin general tend to enter countries that other homecountry firms have previously entered (e.g.,Guillen, 2002; Henisz & Delios, 2001; Shaver etal., 1997).

Given the mixed results on the effect of broker-age, as reported in Table 4, we further examined theinteraction between brokerage and partners by re-estimating our models using two separate sub-samples, one including firm-country-year observa-tions from before any of a focal firm’s partnersentered each specific foreign market (i.e., thedummy variable equals 0), and the other includingobservations from after the focal firm’s partner en-tered, if it ever did (the dummy variable equals 1).This procedure allowed us to examine the effect ofbrokerage in each subsample. In these regressions,the effect of brokerage is negative and significant inthe subsample with no prior entry by home countrypartners, and it is positive and significant in thesubsample with observations after one home coun-try partner had entered. Our tests reveal that eachof these models provides a significantly better sta-tistical fit than a corresponding model without thebrokerage effect, and the coefficient of the broker-age effect is significantly different from zero. Thus,we can safely conclude that the support for Hy-pothesis 4 reported in models 3 and 6 of Table 4 isnot a statistical artifact.

Most of the control variables behaved as ex-pected. Entry rates increase with the number ofprevious entries by a venture capital firm intoother foreign countries; with the age and perfor-mance of the venture capital firm; with the GDPof the country; and with the size of the stockmarket. Neither the use of English as a primarylanguage nor countries’ geographical distancefrom the United States exerts a robust effectacross models.

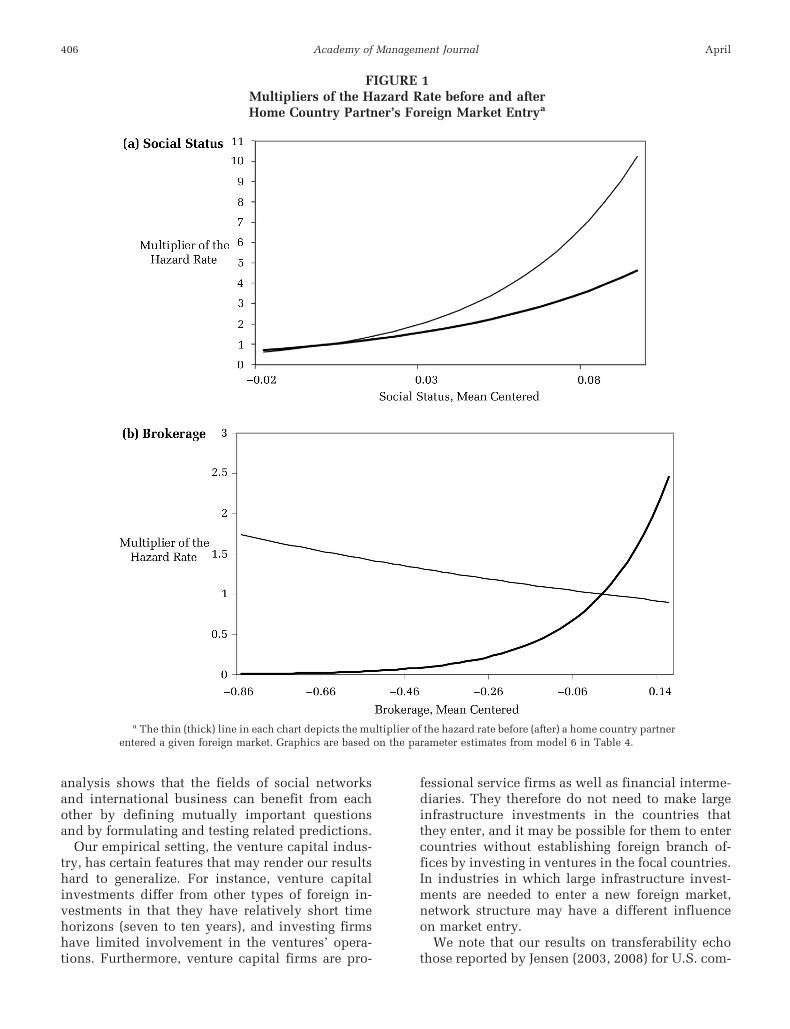

The effects of social status and brokerage arelarge in magnitude. In Figure 1 we depict the effecton the multiplier rate of different levels of socialstatus and brokerage before and after a home coun-try partner has entered each country. The upperpanel shows that higher social status firms are morelikely to go abroad (as indicated by the upward-sloping curves) and that this effect is much largerbefore the entry of a home country partner, as pre-dicted by Hypothesis 3. In the lower panel weobserve that before the entry of a partner, thegreater a firm’s brokerage advantage, the lower themultiplier of its rate of entry. However, after a

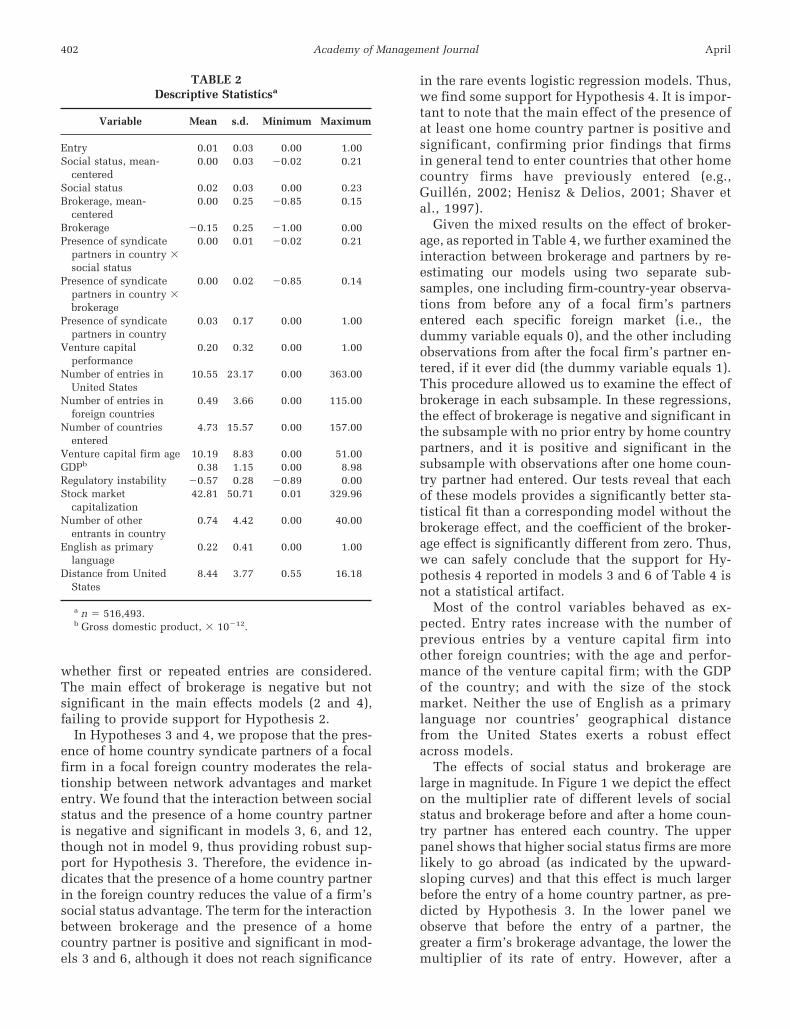

TABLE 2Descriptive Statisticsa

Variable Mean s.d. Minimum Maximum

Entry 0.01 0.03 0.00 1.00Social status, mean-

centered0.00 0.03 �0.02 0.21

Social status 0.02 0.03 0.00 0.23Brokerage, mean-

centered0.00 0.25 �0.85 0.15

Brokerage �0.15 0.25 �1.00 0.00Presence of syndicate

partners in country �social status

0.00 0.01 �0.02 0.21

Presence of syndicatepartners in country �brokerage

0.00 0.02 �0.85 0.14

Presence of syndicatepartners in country

0.03 0.17 0.00 1.00

Venture capitalperformance

0.20 0.32 0.00 1.00

Number of entries inUnited States

10.55 23.17 0.00 363.00

Number of entries inforeign countries

0.49 3.66 0.00 115.00

Number of countriesentered

4.73 15.57 0.00 157.00

Venture capital firm age 10.19 8.83 0.00 51.00GDPb 0.38 1.15 0.00 8.98Regulatory instability �0.57 0.28 �0.89 0.00Stock market

capitalization42.81 50.71 0.01 329.96

Number of otherentrants in country

0.74 4.42 0.00 40.00

English as primarylanguage

0.22 0.41 0.00 1.00

Distance from UnitedStates

8.44 3.77 0.55 16.18

a n 516,493.b Gross domestic product, � 10�12.

402 AprilAcademy of Management Journal

partner has entered, the reverse is true, as predictedby Hypothesis 4. The interaction effect is largeenough to offset the main effect of brokerage withinthe sample range.

Sensitivity Analyses

To examine the sensitivity of our results to sam-pling procedure and model specification, we con-ducted a battery of robustness checks in addition tothose reported above. First, we estimated all mod-els again after excluding the countries that receivedno U.S. venture capital investment during the sam-ple period as well as the venture capital firms thatnever entered a foreign country. The size of thesample fell to 254,883 observations. Although thisprocedure might have introduced selection bias byreducing the number of observations at risk, ithelped us test whether our results were robust tothe exclusion of country or firm observations withno events. The results did not change in anysubstantial way.

Second, we reestimated our models on a sample

comprising only firm-years after modifying our de-pendent variable to represent the rate of foreignmarket entry regardless of the country being en-tered. This redefinition narrowed the sample to7,035 firm-year observations. Note that this samplecould not be used to test Hypotheses 3 and 4, whichrequire the identification of countries of entry andthe inclusion of country-specific controls. However,it served as an additional test of Hypotheses 1 and 2on a smaller sample, helping to reduce any concernsthat might accrue from the fact that our larger samplecontains many observations with nonevents. In thesemodels, we find that the impact of social status on therate of entry is positive and significant (Hypothesis 1),but the impact of brokerage on entry is negative andsignificant (Hypothesis 2).

DISCUSSION AND CONCLUSION

A firm’s decisions to go abroad and to enter spe-cific foreign markets are driven by the characteris-tics of the firm and of the markets being considered,according to the theory of foreign market entry

TABLE 3Bivariate Correlationsa

Variable 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

1. Entry2. Social statusb .04*3. Brokerageb .01* .16*4. Presence of syndicate

partners in country �social status

.09* .35* .06*

5. Presence of syndicatepartners in country �brokerage

.07* .20* .10* .58*

6. Presence of syndicatepartners in country

.09* .23* .04* .65* .39*

7. Venture capitalperformance

�.00 .08* �.05* .01* �.00 �.01*

8. Number of entries inUnited States

.06* .72* .11* .32* .20* .23* �.01*

9. Number of entries inforeign countries

.11* .15* .04* .07* .05* .06* .00 .30*

10. Number of countriesentered

.08* �.02* �.01* .11* .08* .26* �.03* .04* .02*

11. Venture capital firmage

.02* .26* �.03* .09* .06* .06* .28* .31* .10* �.01*

12. GDP .02* .00 .00 .04* .02* .06* �.00 �.00 .00 .29* �.0013. Regulatory instability �.02* .00 �.00 �.07* �.04* �.10* �.01* .00 .00 �.17* �.01* �.21*14. Stock market

capitalization.04* �.01* �.00* .09* .06* .16* �.01* .02* .01* .31* �.00 .25* �.26*

15. Number of otherentrants in country

.07* .18* .03* .08* .06* .07* �.03* .30* .40* .02* .08* .00 .00 .01*

16. English as primarylanguage

.02* .00 .00 .05* .03* .09* �.00 �.00* .00 .16* �.00* .14* �.05* .22* .00

17. Distance from UnitedStates

�.02* .00 .00 �.02* �.01* �.05* �.00 �.00 .00 �.09* �.00 �.19* .22* .04* .00 .15*

a n 516,493.b Mean-centered.* p .05

2010 403Guler and Guillen

(Caves, 1996; Dunning, 1993). We have argued thatsocial status and brokerage advantages developedin a firm’s home market go above and beyond theeffects discussed in prior research to also shapepatterns of international expansion. Our theoreticalanalysis was based on two interrelated variables:the degree of transferability of home country ad-vantages to foreign settings, and the dynamic net-work effects following foreign market entry by afocal firm’s partners.

The transferability of home country advantages isa cornerstone of theories of foreign expansion (e.g.,Caves, 1996; Dunning, 1993). We have found thatalthough benefits arising from social statusprompted firms to enter new foreign markets, thosearising from brokerage did not. Thus, this studybuilds on the insights of previous research concern-ing the transferability of network advantages (e.g.,Burt, 2005; Jensen, 2003; Xiao & Tsui, 2007) andoffers empirical evidence supporting their rele-vance for firms’ foreign market entry.

Our theoretical analysis also incorporated the dy-namic aspects of networks, building on the insightthat actors deliberately seek to create, maintain,and enhance their network advantages over time(Burt, 1992; Nohria, 1992). We examined how so-cial status and brokerage advantages change as aresult of the actions of a focal firm’s home countrypartners. We provided empirical evidence consis-tent with our argument that a firm’s social statusloses value as a signal of quality in a given foreignmarket after a partner enters that market. This pre-diction was based on the important insight drawnfrom the social network literature that social statusis a noisy proxy for quality (Podolny, 2005). Wealso argued that brokerage advantage can shiftquickly from one actor to another (Burt, 2005). Spe-cifically, we predicted and provided some empiri-cal support for the prediction that a firm possessingstrong brokerage advantage in its home country islikely to replicate a home country partner’s entry

TABLE 4Results of Regression Analyses Predicting Foreign Market Entrya, b

Variables

Piecewise Exponential Models

Model 1 Model 2 Model 3 Model 4 Model 5 Model 6

Social status, mean centered 23.00*** (1.71) 23.38*** (1.79) 23.37*** (1.41) 24.49*** (1.50)Brokerage, mean centered �0.11 (0.24) �0.60** (0.23) �0.24 (0.20) �0.64*** (0.19)Presence of syndicate partners

in country � social status�8.10*** (2.52) �8.34*** (1.96)

Presence of syndicate partnersin country � brokerage

8.38*** (2.03) 6.24*** (1.40)

Presence of syndicate partnersin country

2.77*** (0.13) 2.33*** (0.14) 2.25*** (0.18) 2.66*** (0.12) 2.17*** (0.12) 2.18*** (0.15)

Venture capital performance 0.34*** (0.08) 0.24** (0.09) 0.19* (0.010) 0.35*** (0.07) 0.25*** (0.08) 0.22** (0.08)Number of entries in United

States0.01*** (0.00) �0.01*** (0.00) �0.01*** (0.00) 0.01*** (0.00) �0.01*** (0.00) �0.01*** (0.00)

Number of entries in foreigncountries

0.02*** (0.00) 0.04*** (0.00) 0.04*** (0.00) 0.01*** (0.00) 0.03*** (0.00) 0.03*** (0.00)

Number of foreign countriesentered

�0.01* (0.00) �0.01*** (0.00) �0.01*** (0.00) �0.01*** (0.00) �0.02*** (0.00) �0.02*** (0.00)

Venture capital firm age 0.11*** (0.00) 0.11*** (0.00) 0.11*** (0.00) 0.11*** (0.00) 0.11*** (0.00) 0.11*** (0.00)GDP 0.19† (0.10) 0.20* (0.10) 0.21* (0.01) 0.18* (0.08) 0.19* (0.08) 0.20* (0.08)Regulatory instability �5.56*** (0.75) �5.78*** (0.76) �5.73*** (0.77) �5.05*** (0.59) �5.31*** (0.60) �5.34*** (0.60)Stock market capitalization 0.01*** (0.00) 0.01*** (0.00) 0.01*** (0.00) 0.01*** (0.00) 0.01*** (0.00) 0.01*** (0.00)Number of other entrants in

country0.09*** (0.01) 0.08*** (0.1) 0.08*** (0.01) 0.09*** (0.00) 0.08*** (0.00) 0.08*** (0.00)

English as primary language �1.08** (0.35) �1.08** (0.35) �1.10** (0.36) �1.02*** (0.30) �1.06*** (0.30) �1.08*** (0.30)Distance from United States 0.10** (0.04) 0.11** (0.04) 0.11** (0.04) 0.09** (0.03) 0.11*** (0.03) 0.11*** (0.03)

ConstantLikelihood-ratio �2 3,642.65*** 3,809.42*** 3,851.13*** 6,616.69*** 6,866.16*** 6,908.59***� likelihood-ratio �2 166.78*** 41.71*** 249.47*** 42.43***df 23 25 27 23 25 27n 516,493 516,493 516,493 517,981 517,981 517,981

a Models 1–3: piecewise exponential models, first entries only; models 4–6: piecewise exponential models, repeated entries; models7–9: rare events logistic models, first entries only; models 10–12: rare events logistic models, repeated entries.

b Robust standard errors are in parentheses. The piecewise exponential models include 12 time-pieces. The rare events logistic modelsinclude 11 year dummies, excluding the year 2002. All models include 11 dummies for the countries shown in Table 1.

† p .10* p .05

** p .01*** p .001

404 AprilAcademy of Management Journal

into a foreign market to preserve its network posi-tion in the social structure.

In our theory development regarding the ways inwhich social networks affect patterns of interna-tional expansion, we drew a series of connectionsbetween pairs of concepts proposed independentlyby international business and social network schol-ars over the past few decades. In so doing, weargued that social network concepts can enrichtheories of foreign expansion, and vice versa. Forinstance, we suggested that the concept of alter-centric uncertainty in social network analysis(Podolny, 2001) calls attention to an aspect of theliability of foreignness in international business re-search (Hymer, 1959; Zaheer, 1995) that has beenrelatively unemphasized. Firms entering a foreignmarket face an uphill battle not only because theylack knowledge about the local context, but alsobecause they must convey to local suppliers, col-laborators, and customers that they are trustworthy.Network advantages acquired in the firm’s homecountry may help reduce this aspect of the liabilityof foreignness.

We also established a parallel between the inter-national business and social network research tra-ditions in our argument that, under certain circum-stances, firms tend to follow each other’s entry into

foreign markets. The international business litera-ture provides ample evidence that the presence of afirm’s partners or competitors is an important de-terminant of its choice of countries to enter (e.g.,Guillen, 2002; Henisz & Delios, 2001; Shaver et al.,1997). However, few studies have examined howthe characteristics of entering firms may influencethe rate at which they follow partners into a foreigncountry. We extend this literature by arguing thatfirms enjoying a brokerage advantage are morelikely to follow their partners to specific marketsand that firms with high social status are less likelyto follow their partners to specific markets thantheir low social status counterparts. These argu-ments bridge an important gap between the interna-tional business and the social network literatures.Buyer-supplier relationships aside, the internationalbusiness theory expectation is that firms will followeach other to foreign markets when their homecountry industry is an oligopoly (Knickerbocker,1973). Following research on social networks (e.g.,Burt, 1992, 2005; Nohria, 1992), we have providedsome evidence to the effect that firms enjoying abrokerage advantage in their home countries reactto their partners’ foreign market entries by follow-ing them to the same locations abroad in order toprotect their existing brokerage advantages. Our

TABLE 4Continued

Rare Events Logistic Models

Model 7 Model 8 Model 9 Model 10 Model 11 Model 12

13.89*** (1.67) 14.56*** (1.75) 11.97*** (1.64) 12.97*** (1.68)0.23 (0.22) 0.10 (0.23) 0.17 (0.20) 0.02 (0.20)

�2.98 (2.00) 3.91* (1.93)

1.75 (1.33) 2.05† (1.17)

1.06*** (0.12) 0.70*** (0.13) 0.70*** (0.16) 1.03*** (0.11) 0.72*** (0.12) 0.73*** (0.14)

0.02 (0.07) �0.06 (0.08) �0.06 (0.08) �0.03 (0.06) �0.10 (0.07) �0.10 (0.07)0.01*** (0.00) �0.00 (0.00) �0.00 (0.00) 0.01*** (0.00) �0.00 (0.00) �0.00 (0.00)

0.04*** (0.00) 0.04*** (0.00) 0.04*** (0.00) 0.04*** (0.00) 0.04*** (0.00) 0.04*** (0.00)

0.01* (0.00) 0.01† (0.00) 0.01† (0.00) 0.01† (0.00) 0.01† (0.00) 0.01 (0.00)

�0.01 (0.01) �0.01 (0.01) �0.01 (0.01) �0.00 (0.01) 0.00 (0.01) 0.00 (0.01)0.00 (0.06) �0.00 (0.06) �0.01 (0.06) 0.02 (0.06) 0.01 (0.06) 0.01 (0.06)