Excise and concept of excise goods Excise-is an indirect (consumption) tax included in the sale price of excise goods stipulated by the legislation.

Following goods are subject to excise tax in the Republic of Azerbaijan: · drinking alcohol, beer and all types of alcoholic beverages;· tobacco products;· oil products;· light vehicles (excluding the special appointed motor transports with

special sign and equipment); · leisure and sports yachts and other floating transports for these purposes;· imported platinum, gold, jewelery and other products made from it,

processed, sorted, framed and mounted diamond. Who are the taxpayers? · producers of excise goods in the Republic of Azerbaijan;·����importers of excise goods in the Republic of Azerbaijan;·� � � �residents of the Republic of Azerbaijan involved in the production of

excise goods directly or via contractor outside of the territory of Azerbaijan, who are not registered as taxpayers at the manufacturing location of such goods are payers of excise tax.

It should be noted that manufacturers (contractors) of goods produced in the territory of Azerbaijan Republic from raw materials delivered by customer are excise taxpayers. In this case the manufacturer (contractor) holds the right to request the compensation for the amount of excise from the customer.

If the producers and buyers of excisable goods are residents with mutual dependence, the owner (buyer) of the goods is excise payer. Taxable object· for the excise goods produced in the territory of the Republic of

Azerbaijan, their release outside the boundaries of their production facilities; · for imported goods it is their passage through customs service con-trol.Production facilities include warehouses, secondary storage areas and other

similar premises located in the production territory. Amount of taxable operation· With respect to the goods produced in the territory of the Republic:a) For oil products - the compensation (including barter) received, or

receivable, by the taxpayer from a customer or any other person, the amount of which is not less than the wholesale market price of the relevant goods (excluding the VAT, road tax and excise amounts);

b) For other excise goods-the quantity of the produced goods.· With respect to the goods imported to the Republic:a) For imported light vehicles, leisure and sports yachts and other floating

transport - the volume of their engine;b) For platinium - Every gram of platinium c) for gold, jewellery and other products made from it –volume of gold in

1000 weight unit; for processed, sorted, framed and mounted diamond - carat of diamond;

d) For other import goods-the customs value of the goods not less than the wholesale market price (excluding the excise, road tax and VAT).

Date of the taxable operation·����With respect to goods produced in the territory of the Republic of

Azerbaijan -the time when the goods are released outside the boundaries of their production facilities.·� � �With respect to the import of goods-the time when excise goods pass

through the customs service control. With respect to the import of goods-the time when excise goods pass through the customs service control.

Exemptions from excise: ·� import of three litres of alcoholic beverage, 600 cigarettes, 20 gram gold, jewelery and other products made from it, 0,5 carat processed, sorted, framed and mounted diamond by a physical person for personal consumption;

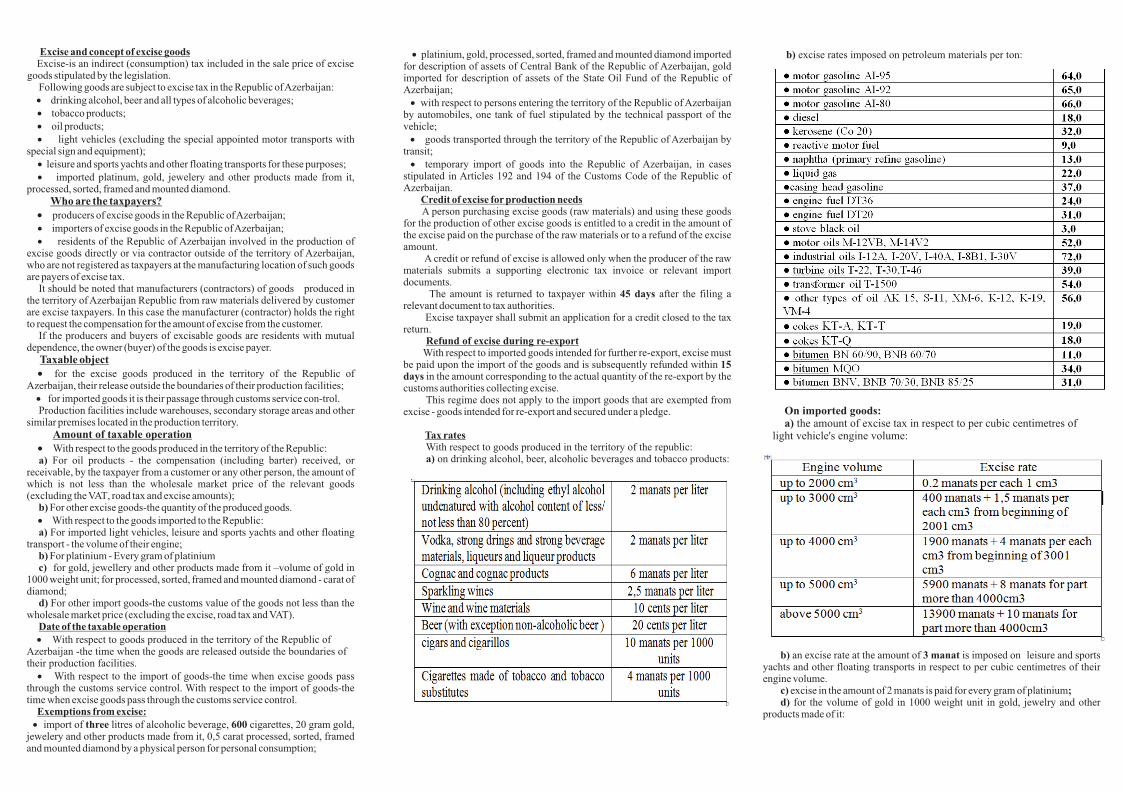

b) excise rates imposed on petroleum materials per ton:· platinium, gold, processed, sorted, framed and mounted diamond imported for description of assets of Central Bank of the Republic of Azerbaijan, gold imported for description of assets of the State Oil Fund of the Republic of Azerbaijan;·��with respect to persons entering the territory of the Republic of Azerbaijan

by automobiles, one tank of fuel stipulated by the technical passport of the vehicle;·� � �goods transported through the territory of the Republic of Azerbaijan by

transit;·� � temporary import of goods into the Republic of Azerbaijan, in cases

stipulated in Articles 192 and 194 of the Customs Code of the Republic of Azerbaijan. Credit of excise for production needs

A person purchasing excise goods (raw materials) and using these goods for the production of other excise goods is entitled to a credit in the amount of the excise paid on the purchase of the raw materials or to a refund of the excise amount.

A credit or refund of excise is allowed only when the producer of the raw materials submits a supporting electronic tax invoice or relevant import documents.

The amount is returned to taxpayer within 45 days after the filing a relevant document to tax authorities.

Excise taxpayer shall submit an application for a credit closed to the tax return.

Refund of excise during re-export With respect to imported goods intended for further re-export, excise must

be paid upon the import of the goods and is subsequently refunded within 15 days in the amount corresponding to the actual quantity of the re-export by the customs authorities collecting excise.

This regime does not apply to the import goods that are exempted from excise - goods intended for re-export and secured under a pledge.

Tax rates With respect to goods produced in the territory of the republic: a) on drinking alcohol, beer, alcoholic beverages and tobacco products:

On imported goods:a) the amount of excise tax in respect to per cubic centimetres of

light vehicle's engine volume:

b) an excise rate at the amount of 3 manat is imposed on leisure and sports yachts and other floating transports in respect to per cubic centimetres of their engine volume.

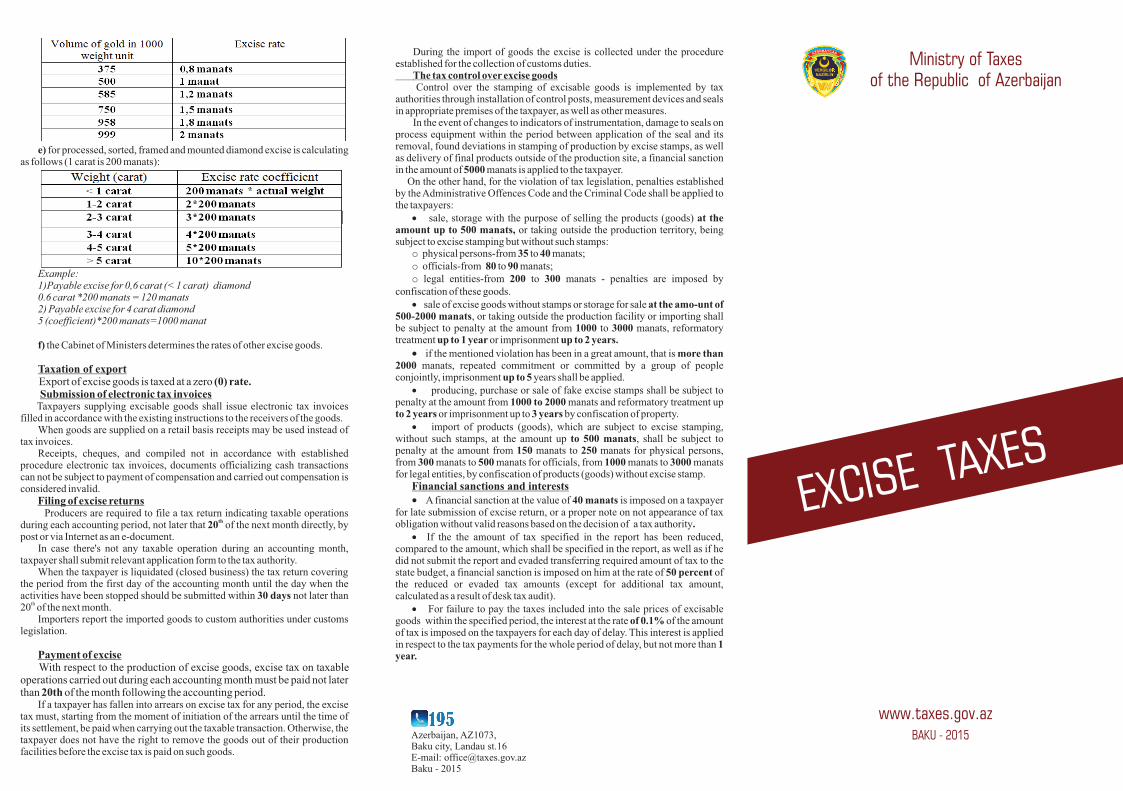

c) excise in the amount of 2 manats is paid for every gram of platinium;d) for the volume of gold in 1000 weight unit in gold, jewelry and other

products made of it:

e) for processed, sorted, framed and mounted diamond excise is calculating as follows (1 carat is 200 manats):

Example:1)Payable excise for 0,6 carat (< 1 carat) diamond0.6 carat *200 manats = 120 manats2) Payable excise for 4 carat diamond5 (coefficient)*200 manats=1000 manat

f) the Cabinet of Ministers determines the rates of other excise goods.

Taxation of exportExport of excise goods is taxed at a zero (0) rate.Submission of electronic tax invoices

Taxpayers supplying excisable goods shall issue electronic tax invoices filled in accordance with the existing instructions to the receivers of the goods.

When goods are supplied on a retail basis receipts may be used instead of tax invoices.

Receipts, cheques, and compiled not in accordance with established procedure electronic tax invoices, documents officializing cash transactions can not be subject to payment of compensation and carried out compensation is considered invalid.

Filing of excise returns Producers are required to file a tax return indicating taxable operations

thduring each accounting period, not later that 20 of the next month directly, by post or via Internet as an e-document.

In case there's not any taxable operation during an accounting month, taxpayer shall submit relevant application form to the tax authority.

When the taxpayer is liquidated (closed business) the tax return covering the period from the first day of the accounting month until the day when the activities have been stopped should be submitted within 30 days not later than

th20 of the next month.Importers report the imported goods to custom authorities under customs

legislation.

Payment of excise With respect to the production of excise goods, excise tax on taxable operations carried out during each accounting month must be paid not later than 20th of the month following the accounting period.

If a taxpayer has fallen into arrears on excise tax for any period, the excise tax must, starting from the moment of initiation of the arrears until the time of its settlement, be paid when carrying out the taxable transaction. Otherwise, the taxpayer does not have the right to remove the goods out of their production facilities before the excise tax is paid on such goods.

During the import of goods the excise is collected under the procedure established for the collection of customs duties. The tax control over excise goods Control over the stamping of excisable goods is implemented by tax authorities through installation of control posts, measurement devices and seals in appropriate premises of the taxpayer, as well as other measures.

In the event of changes to indicators of instrumentation, damage to seals on process equipment within the period between application of the seal and its removal, found deviations in stamping of production by excise stamps, as well as delivery of final products outside of the production site, a financial sanction in the amount of 5000 manats is applied to the taxpayer.

On the other hand, for the violation of tax legislation, penalties established by the Administrative Offences Code and the Criminal Code shall be applied to the taxpayers:

· sale, storage with the purpose of selling the products (goods) at the amount up to 500 manats, or taking outside the production territory, being subject to excise stamping but without such stamps:

o physical persons-from 35 to 40 manats;o officials-from 80 to 90 manats;o legal entities-from 200 to 300 manats - penalties are imposed by

confiscation of these goods.·� sale of excise goods without stamps or storage for sale at the amo-unt of

500-2000 manats, or taking outside the production facility or importing shall be subject to penalty at the amount from 1000 to 3000 manats, reformatory treatment up to 1 year or imprisonment up to 2 years.

·���if the mentioned violation has been in a great amount, that is more than 2000 manats, repeated commitment or committed by a group of people conjointly, imprisonment up to 5 years shall be applied.

·� � � �producing, purchase or sale of fake excise stamps shall be subject to penalty at the amount from 1000 to 2000 manats and reformatory treatment up to 2 years or imprisonment up to 3 years by confiscation of property.

·� � � import of products (goods), which are subject to excise stamping, without such stamps, at the amount up to 500 manats, shall be subject to penalty at the amount from 150 manats to 250 manats for physical persons, from 300 manats to 500 manats for officials, from 1000 manats to 3000 manats for legal entities, by confiscation of products (goods) without excise stamp.

Financial sanctions and interests· A financial sanction at the value of 40 manats is imposed on a taxpayer

for late submission of excise return, or a proper note on not appearance of tax obligation without valid reasons based on the decision of a tax authority.

· If the the amount of tax specified in the report has been reduced, compared to the amount, which shall be specified in the report, as well as if he did not submit the report and evaded transferring required amount of tax to the state budget, a financial sanction is imposed on him at the rate of 50 percent of the reduced or evaded tax amounts (except for additional tax amount, calculated as a result of desk tax audit).

· For failure to pay the taxes included into the sale prices of excisable goods within the specified period, the interest at the rate of 0.1% of the amount of tax is imposed on the taxpayers for each day of delay. This interest is applied in respect to the tax payments for the whole period of delay, but not more than 1 year.

Azerbaijan, AZ1073,Baku city, Landau st.16E-mail: [email protected] - 2015

www.taxes.gov.az

EXCISE TAXES

Ministry of Taxesof the Republic of Azerbaijan

BAKU - 2015