Employee Share Schemes –

What you Need to Know about the New Tax Rules

Page 1

1. Introduction

As we all know, the Government announced some significant unexpected changes to the

taxation of employee share plans as part of the May 2009 Federal budget, which were then

significantly revised. Legislation introducing those changes became law on 14 December

2009.

Instead of discussing each of the changes in isolation, this paper will look at the changes

on a plan by plan basis, focussing on the key issues that arise under different kinds of

plans. Against that background, the topics to be covered are:

(a) Types of ESS plans under the new rules.

(b) Impact of the new rules on restricted share plans and, in particular, good leaver

issues.

(c) Impact of the new rules on performance rights plans and, in particular, the

interaction of the taxing time with the company's insider dealing policy.

(d) Impact of the new rules on options with an exercise price and, in particular, the

practical issues that can arise where options are taxed before exercise.

(e) Impact of the new rules on share purchase plans and, in particular, how strict

disposal restrictions have to be to be considered 'genuine restrictions'.

(f) Impact of the new rules on awards granted before 1 July 2009.

(g) The new employer reporting and withholding rule, focussing in particular on the

14 July 2010 deadline to provide employees with their first ESS Statements.

2. Types of ESS plans under the new tax rules

Very generally, ESS plans can now be categorised into the following tax categories.

2.1 Plans to which the new tax rules do not apply

Employee incentive plans which fall outside the new Division 83A may, depending on the

circumstances, be subject to fringe benefits tax, PAYG and/or capital gains tax. The three

main categories of incentive plans which fall outside Division 83A are:

(a) Where the award is not an ESS interest in a company

Division 83A only applies where there is an ESS interest in a company. An ESS

interest in a company is a beneficial interest in a share in the company or a right to

acquire a beneficial interest in a share in the company. This means that Division

83A does not apply, for example, to units in a unit trust or to rights to cash settled

awards.

It is important to distinguish 'cash settled' awards in this context from:

(i) a right to acquire a share in a company which, in certain defined

circumstances, may be cancelled for cash; and

Page 2

(ii) a right to shares where the shares may, on exercise of the right, be

immediately sold on your behalf instead of being delivered.

(b) Where the shares are not in the employer or a holding company of the

employer

Division 83A will not apply if the award is not granted in relation to an 'employment'

relationship, or if the shares are in the wrong entity.

'Employee' is widely defined to include any individual who provides services to an

entity under an arrangement with the entity, notwithstanding those services may

not be provided as a common law employee. This means that Division 83A will

apply to independent contractors who are hired in an individual capacity. It will

also apply to awards made to former employees, and awards made to associates

of employees. However fringe benefits tax rather than Division 83A will apply to

employees who receive shares in relation to their employment where those shares

are not in their employer or a holding company of their employer. For example, if

an employee was employed by a company which was only 40% owned by another

company (and not a 'subsidiary'), and received an award of shares in the

shareholder of the employer, fringe benefits tax rather than income tax would apply

to that award of shares.

(c) Where the shares/rights to shares are not provided at a discount to market

value

Division 83A will not apply where the employee pays market value consideration

for the grant of the award. It is important to distinguish here between consideration

on a 'pre-tax' compared with post-tax basis. Where consideration is provided on a

'pre-tax' basis (eg salary sacrificed) the employee will be treated as having

acquired the award at a 'discount' under these rules.

This means that Division 83A will not apply where:

(i) shares are purchased at market value by the employee using post-tax

funds or by the employee being provided with a loan to purchase the

shares at market value; or

(ii) the exercise price of options is more than double the market value of the

shares on grant (or lower where the maximum life of the options is 6 years

or less).

2.2 $1,000 tax exempt schemes

Under such plans, a participant who satisfies a new $180,000 'income' test is entitled to an

income tax exemption for up to $1,000 of shares. Any increase or decrease in the value of

the shares is then subject to capital gains tax on disposal of the shares. This may be

considered the only true 'concessional' tax treatment which Australia offers to employee

share schemes and is a very limited concession by international standards.

Employees are entitled to an exemption for up to $1,000 of shares/rights to shares a year if

(s.83A-35):

Page 3

(a) the shares are ordinary shares in a company which is the current employer (or the

holding company of the current employer);

(b) the predominant business of the company is not the acquisition and holding of

securities or, if it is, the employee is not employed by the company and a related

company;

(c) the scheme is offered on a non-discriminatory basis to at least 75% of Australian

resident employees of the relevant employer who have at least 3 years of service

with the employer;

(d) there is no real risk under the scheme that the employee will forfeit the shares;

(e) the scheme is operated to not permit disposal of the shares before the earlier of 3

years and cessation of the relevant employment;

(f) immediately after the ESS interest is acquired the employee does not hold a

beneficial interest in more than 5% of the shares in the company and is not in a

position to cast or control the casting of more than 5% of the maximum number of

votes that may be cast at a general meeting of the company; and

(g) the employee has 'adjusted' income of not more than $180,000.

These conditions are very similar to the conditions which applied under the old law, with

the exception of the 'income' test. 'Adjusted' income is the sum of taxable income,

reportable fringe benefits total, reportable superannuation contributions (generally salary

sacrifice superannuation contributions) and total net investment losses (deductions relating

to financial investments and rental properties, less gross income from those assets).

It is important to remember that the 75% offer test must be satisfied even if it is likely that

more than 25% of employees will breach the income test.

2.3 Taxed up-front schemes

Under such plans, the participant is taxed on the market value of an ESS interest on grant.

Any increase or decrease in the value of the award from grant is subject to capital gains

tax. If the award is forfeited, a refund of the tax paid on grant may be available.

ESS plans where an amount is required to be included in income in the year shares/rights

to shares are granted include the following.

(a) Where the shares are not 'ordinary' shares.

The EM notes that shares that are not 'ordinary shares', such as preference

shares, may have less risk associated with them and are therefore less likely to

align the employee's interest with that of the company. ATO ID 2010/62 states that

shares that have priority as to dividends or distributions in the event of winding up

are preference shares and, if shares are not preference shares, they are ordinary

shares. It would therefore be expected that 'non-voting' shares which do not have

any preference to dividends or distributions would be considered 'ordinary' for

these purposes.

(b) Where the employee holds a greater than 5% interest in the employer.

(c) Where the participant is a former employee.

Page 4

(d) If the ESS interest is a beneficial interest in shares (instead of just a right to get

shares), where the employer does not operate a general share or rights plan open

to at least 75% of its employees.

(e) Where the shares are acquired under a 'tax exempt' plan but the employee has

adjusted income greater than $180,000.

(f) Where neither the real risk of forfeiture test or the $5,000 salary sacrifice deferral

conditions are satisfied.

2.4 Real risk of forfeiture tax deferred schemes

Under such plans, the participant is able to defer the taxing time on awards which, on

grant, are subject to a real risk of forfeiture.

'Real risk of forfeiture' is not defined. There are a number of non-tax cases where the

meaning of 'real risk' is discussed. These cases given the general impression that a risk

can be 'real' even if it is considered that there is very little chance of it occurring.

The Explanatory Memorandum to Tax Laws Amendment (2009 Budget Measures No. 2)

Bill 2009 which introduced Division 83-A (EM) explains the 'real risk' of forfeiture test in the

following way:

1.156 The ‘real risk of forfeiture’ test does not require employers to provide

schemes in which their employee share scheme benefits are at a significant or

substantial risk of being lost. However, ‘real’ is regarded as something more than a

mere possibility. Something is not a real risk if a reasonable person would

disregard the risk as highly unlikely to occur or as nothing more than a rare

eventuality or possibility. (emphasis added)

….

1.158 The ‘real risk of forfeiture’ test is intended to provide for deferral of tax when

there is a real alignment of interests between the employee and employer, through

the employee’s benefits being at risk. The test is a principle based test, intended to

deny deferral of tax where schemes contrive to present a nominal risk of forfeiture,

without complying with the intent of the proposed law. (emphasis added)

….

1.159 Real risk includes situations in which a share or right is subject to meaningful

performance hurdles or the securities will be forfeited if a minimum term of

employment is not completed. (emphasis added)

The EM makes it clear that the risk of forfeiture does not have to be significant or

substantial. However the chance of forfeiture occurring has to be more than a 'mere

possibility' or a 'nominal risk'. A general rule of thumb to apply is that forfeiture is not a real

risk if a reasonable person would consider forfeiture as highly unlikely to occur. Both

performance and service conditions can be taken into account in determining whether or

not the real risk of forfeiture test is satisfied on grant of an ESS interest.

Provided the real risk of forfeiture test is satisfied on grant, the taxing time will not generally

arise until the earlier of cessation of employment and when the shares are no longer

Page 5

subject to genuine restrictions on disposal, with a maximum deferral period of 7 years. The

amount which is subject to tax when the deferral ends is the market value of the shares at

the end of the deferral period. This means that the deferral comes at the cost of the loss of

the 50% CGT concession on any capital growth during the deferral period.

2.5 $5,000 salary sacrifice tax deferred schemes

Under such plans, the participant is able to defer the taxing time on up to $5,000 per year

of shares acquired from salary sacrificed monies. The deferral requires that the shares be

subject to genuine restrictions on disposal for the duration of the deferral, with a maximum

deferral period of 7 years. The amount which is subject to tax when the deferral ends is

the market value of the shares at the end of the deferral period. This means that, as with

real risk of forfeiture plans, the deferral comes at the cost of the loss of the 50% CGT

concession on any capital growth during the deferral period.

3. Impact of the New Rules on Restricted Share Plans

3.1 Example

Z Co's remuneration policy dictates that a certain percentage of remuneration of selected

management employees is to be provided in the form of forfeitable ordinary shares in Z Co under a

Restricted Share Plan. Z Co also separately operates a share purchase plan with employer match

which is offered to all employees.

Alternative 1

Shares awarded under the Plan are not able to be sold for 3 years after the shares are awarded. If

the employee leaves the employment before 3 years from the award of the shares (other than as a

result of redundancy, disability, death or retirement with the approval of the Board (collectively

referred to below as 'good leavers') the employee forfeits the Z Co shares. If the employee is a good

leaver before the vesting date, the employee gets to keep all the shares, but they remain subject to

disposal restrictions until the vesting date.

Alternative 2

As for Alternative 1 except that, after the 3 year vesting period, the employee remains prohibited from

selling the vested shares for a further 2 year period and good leavers who leave before the vesting

date only get to keep a pro-rated number of the shares, which become unrestricted on the leaving

date.

3.2 Real risk of forfeiture?

In this example, there are no performance conditions, but, subject to the good leaver

provisions, the award is generally forfeited if the employee leaves the employment before 3

years from grant of the award.

The EM clearly indicates that real risk of forfeiture includes situations in which the award

will be forfeited if a minimum term of employment is not completed. For example, at

paragraph 1.162 it is stated:

'A condition that ESS interests will be forfeited if the employee leaves to work for

any other employer, will constitute a real risk of forfeiture in most circumstances.'

Page 6

This should mean that, in practice, service conditions for a sufficient period should satisfy

the real risk test even for employees who may objectively be seen as more likely to remain

in their current employment than other employees. An interesting question arises as to

whether the value of the awards to be forfeited if the employee were to resign is relevant to

determining whether the real risk is satisfied on grant. In general I would expect that not to

be a critical issue, having regard to the fact that new employers may be prepared to

compensate new employees for forfeited awards.

The examples in the EM of service conditions (refer examples 1.9 to 1.13) indicate that a

12 month service condition is likely to be sufficient to satisfy the real risk of forfeiture test

(refer example 1.9), that a 3 month service period will not be sufficient (refer example 1.12)

and that a 6 month service period may not be sufficient (refer example 1.11).

ATO Interpretative Decision ID 2010/61 may be seen as an indication that while the 'safe

harbour' rule is 12 months, 6 months may be acceptable in some circumstances (in that

case where the period of deferral was no more than 3 years and where the majority of

participants had a service condition of more than 6 months). It would appear from the

reasoning in the ID that the ATO considers that a period of deferral of more than 3 years,

with only a 6 month forfeiture period, would be more likely to be 'contrived' forfeiture (rather

than real forfeiture) designed to achieve a later taxing time. Of course whether or not that

was the case would depend on the specific facts.

In this example, the service testing period is 3 years so that would, on its face, appear

sufficient to satisfy the real risk test. What though about the 'good leaver' clauses?

Examples in the EM indicate that the presence of a good leaver clause will not stop a

participant satisfying the 'real risk of forfeiture test' on grant of the awards where the good

leaver scenarios are 'beyond the employee's control' (refer example 1.10). It would

generally be expected that good leaver scenarios covering redundancy and sickness would

be beyond the employee's control. However example 1.11 in the EM indicates that there

may be a question about whether the real risk test is satisfied on grant for an employee

who, on grant, is potentially entitled to activate a 'retirement' good leaver clause.

There are in practice various kinds of retirement good leaver clauses, but in our experience

they often fall into the following three categories.

(a) No fixed retirement age but employer must have genuine belief employee is

permanently leaving the work force

This appears to be a common 'Australian' plan retirement clause (due to our age

based discrimination laws).

My view of such clauses is that there should not be a tax on grant issue for 'older'

employees, unless the employer and employee have, prior to the grant, agreed a

retirement date. I consider this view is consistent with example 1.11 of the EM

which appears to assume that, prior to the grant, the employer and employee have

agreed a retirement date (as it refers to Gary being 'within 6 months of

retirement').

For the employer to form a view on grant of the award that it is 'highly unlikely' that

forfeiture will occur, the employer would have to form a view that, if the employee

Page 7

was to leave the employment before the vesting date, that would almost certainly

be to permanently leave the work force rather than to take up another job. In this

day and age where we are all expected to work until we have one foot in the grave

(as evidenced by the recent Government announcement to extend the SGC age

from 70 to 75), it would I think be difficult for an employer to form a view that if an

older employee was to leave before vesting it would be highly unlikely that would

be other than to permanently leave the work force. The only circumstances where

I can see an employer might be in a position to form that view would be if the

employer has agreed a retirement date with the employee before the grant occurs.

If the employer were to make such an assumption without have agreed in advance

a retirement date with the employee, they could well be open to age based

discrimination complaints from the affected employee. It may be assumed that

'older' employees may feel discriminated against if their employers started formally

assuming they are of an age where they are unlikely to seek alternative

employment.

(b) Fixed retirement conditions

Foreign plans may contain good leaver retirement clauses where an employee can

access the clause simply by being a certain age and/or having served a minimum

period of employment, regardless of whether the employee is resigning or

permanently leaving the workforce. If such plans do not have a minimum service

period post grant (eg a 6 month minimum period), or a pro-rata vesting outcome for

leaving before the vesting date, then that seems to me to be within example 1.11

for any employee who satisfies the fixed conditions at the time of grant. Perhaps

there is also a tax on grant issue for any employee who will, within 6 months of

grant, satisfy the fixed conditions?

What though if the vesting outcome for good leavers under such plan is a time

based pro-rata outcome? If you apply a 6 month service condition rule of thumb,

perhaps 6 months worth of the grant does not satisfy the real risk test, but that the

remainder of the grant does. However if the vesting date is 3 years or more from

grant it is a lot of hassle to report tax on grant for 16% or less of the grant and a

later taxing time for the remainder of the award (assuming the employee remains

employed for more than 6 months). Surely there becomes a 'de minimus' point

where the employer should not be required to split the grant between a small

portion of the grant as not being at a sufficient risk? I would suggest that a suitable

administrative approach in such circumstances would be to treat the whole grant

as having sufficient risk attached where the potential 'not at real risk' proportion is

less than, say, 20% of the grant. It is hoped that the ATO may be able to come up

with some suitable administrative approach in this regard.

(c) Retirement with the approval of the Board

Another common retirement clause in Australian based plans is to provide the

Board with a discretion to approve a good leaver outcome.

On one view it might be said that if a participant was not entitled to activate the

good leaver retirement clause without Board approval, there must be a real risk

Page 8

that the Board will not approve the activation of the clause. However I suspect the

reality is that, in determining whether or not such a clause causes a tax on grant

issue for any employees, the employer will need to think about how in practice that

clause is likely to be used. If the Board is only likely to approve retirement where it

has a genuine belief that the employee is permanently leaving the workforce, then

the analysis per (a) above should apply. If the Board is likely to approve retirement

if a person is of a certain seniority, age, or has a certain period of service, then the

analysis per (b) above should apply.

In alternative 1 of this example, the retirement has to be approved by the Board. If it is

approved, the employee gets to keep all the shares, but the disposal restrictions continue

to apply. Whether or not any participants have a tax on grant issue in this scenario is likely

to depend on how in practice the Board is likely to exercise its discretion. The question

becomes, would a reasonable person consider it highly unlikely that forfeiture will occur for

a particular participant in the event they were to leave the employment before the vesting

date? If the answer is no, then the real risk test should be satisfied. Factors which are

likely to be relevant to a reasonable person in assessing the risk level in this context

include the company's history of forfeiture outcomes for employees with similar fact

patterns to the participant (eg similar role, age and length of service with the company) who

have left the employment before the vesting date and, for listed companies, relevant

corporate governance trends (at the time of grant of the award) of Boards exercising or not

exercising vesting discretions in favour of employees.

In alternative 2 of this example, the retirement has to be approved by the Board but, if it is

approved, the employee only gets to keep a time based pro-rated number of the shares.

So, for example, if the employee was granted 1,000 shares and retired 6 months from

grant, the employee would only get to keep 167 of the shares (6 months/36 months x 1,000

shares). The first issue to be considered is the same issue as for alternative 1 – ie, is it

highly unlikely that the shares will all be forfeited, having regard to the need for the Board

to approve the retirement? If the answer to that is yes, the next issue to consider is how

much of the awards is it highly unlikely will be forfeited? Based on a 6 month minimum

service test period, I would expect that at least 833 of the shares (ie 30/36) would satisfy

the real risk test (as they would require at least 6 months service). However where do you

draw the line at the number of shares that may not satisfy the test (assuming the person is

a potential retiree at the time of grant)?

3.3 Taxing time?

The 'ESS deferred taxing point' for shares under the new rules will occur at the earliest of:

(a) when the shares are no longer subject to real risk of forfeiture or genuine disposal

restrictions;

(b) cessation of employment; and

(c) 7 years from grant of the award.

Page 9

(a) When the shares are no longer subject to real risk of forfeiture or genuine

disposal restrictions

In alternative 1 of this example, the taxing time under this head is likely to be on

vesting of the award at year 3, as disposal restrictions do not continue to apply

after that time. However in alternative 2, the taxing time under this head is likely to

be at year 5. The difference to note with these two alternatives is that alternative 2

allows a continued tax deferral for shares for lock-up periods after the shares have

vested. Importantly however that continued deferral will only apply where the real

risk of forfeiture test was satisfied on grant and the lock-up period has applied from

grant. Therefore, while it is possible to offer employees the choice of the lock-up

period to apply post vesting of their awards, the employees would have to choose

that period prior to the awards being granted (rather than on vesting of the

awards).

I will consider how Insider Dealing rules fit within 'genuine restrictions' later in this

paper when I consider performance rights plans and I will consider plans which

contain discretions for the Board to lift disposal restrictions when I discuss share

purchase plans.

(b) Cessation of employment

Unfortunately the new law, as with the old law, provides that an employee who has

not already paid tax on ESS interests will be taxed on those interests on leaving

the relevant employment, even though those ESS interests may not at that time be

vested and/or may be prohibited from sale.

In this example, if an employee forfeits the shares as a result of resigning before

vesting, no tax will be payable on leaving the employment. However if an

employee is a 'good leaver' before vesting, tax will be payable on leaving the

employment, based on the market value of the shares on the leaving date,

notwithstanding that, in alternative 1, the shares continue to be locked up until the

vesting date. If the share price reduces between the leaving date and the vesting

date, the employee is not entitled to reduce the taxable amount on the leaving date

(but will be entitled to a capital loss if the shares are sold on vesting). Alternative 2

of this example may be seen to better deal with the tax bill payable on cessation of

employment by providing for a vesting outcome on leaving the employment.

However care needs to be taken to ensure that the bringing forward of a vesting

outcome in these circumstances does not result in some or all of the vesting being

subject to the new limitation on termination payment rules.

It is important to remember that while cessation of employment may be a taxing

time, tax is generally only payable after assessment of the tax return in the year in

which employment ceases. So, for example, if an employee ceases employment

in November 2011, and the employee lodges their tax return for the year ended 30

June 2012 with a tax agent, the employee may not be required to pay tax on the

awards until receipt of the assessment for that year which could be as late as May

2013 (ie 18 months after the employment has ceased).

Page 10

(c) 7 years from acquisition of the share or right.

An employee who has not already paid tax on ESS interests will be taxed on those

interests 7 years from acquisition. This is a reduction of the maximum tax deferral

period from 10 years to 7 years.

(d) The 30 day rule changes the ESS deferred taxing point

If shares are sold within 30 days of what would otherwise be the ESS deferred

taxing point, the disposal of the shares will be the ESS deferred taxing point rather

than the earlier event. For example, if shares vested on 20 June 2010, and the

employee sold the shares between 1 and 20 July 2010, the employee would be

taxed on those shares in the year ended 30 June 2011 rather than the year ended

30 June 2010.

Importantly the 30 day rule will only apply to that portion of the shares sold within

30 days of what would otherwise be the ESS deferred taxing point. For example, if

an employee only sells sufficient shares to met the tax liability at the ESS deferred

taxing point, the sale proceeds will be the taxable amount for those shares sold

within 30 days, but the market value of the shares at the earlier ESS deferred

taxing point will remain the taxable value for the shares not so sold.

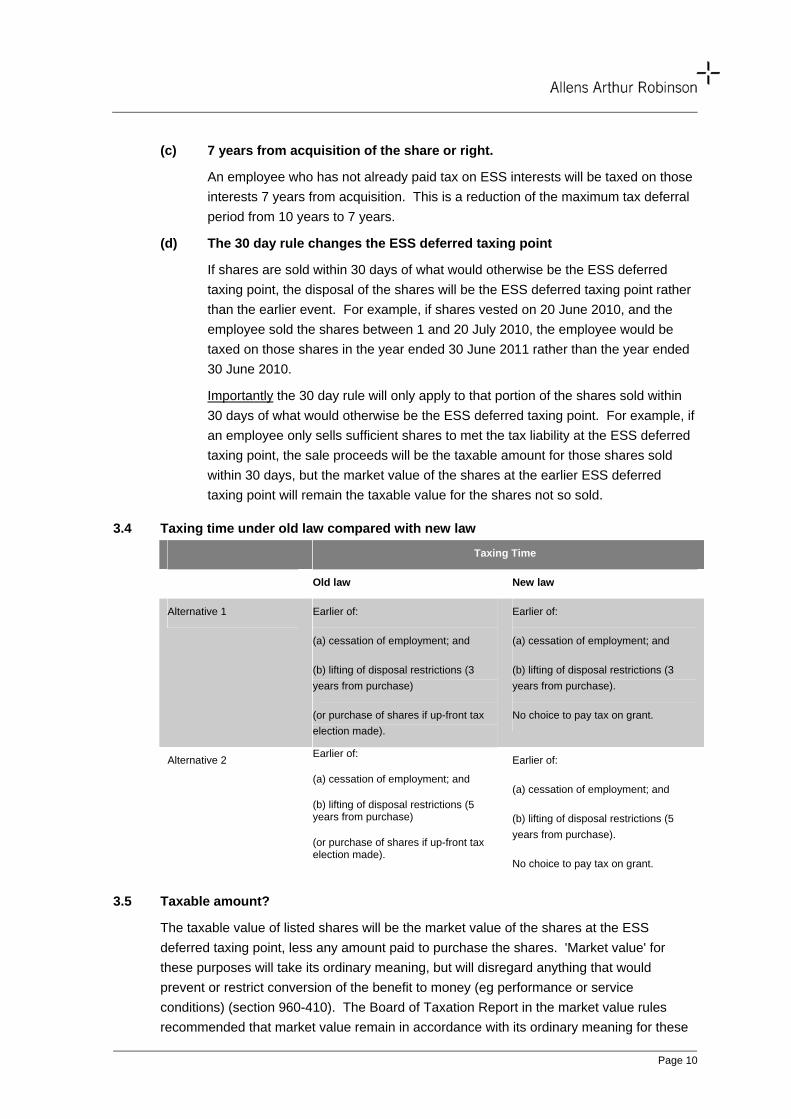

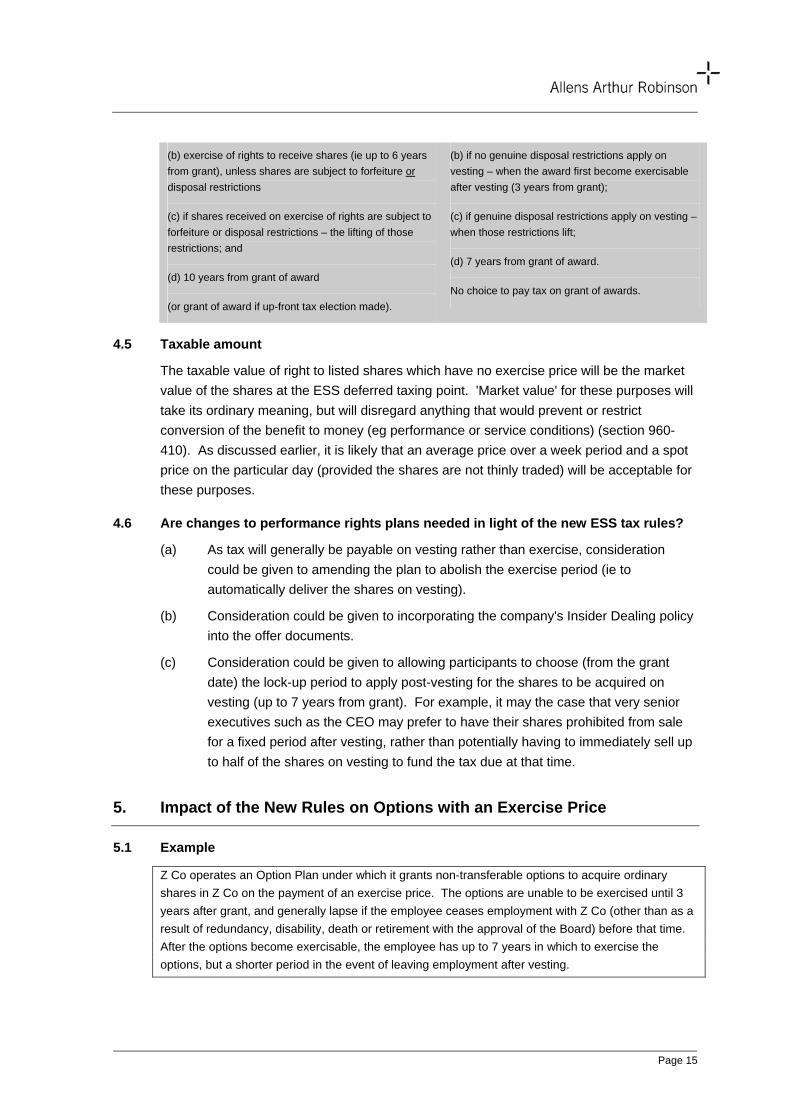

3.4 Taxing time under old law compared with new law

Taxing Time

Old law New law

Alternative 1 Earlier of:

(a) cessation of employment; and

(b) lifting of disposal restrictions (3

years from purchase)

(or purchase of shares if up-front tax

election made).

Earlier of:

(a) cessation of employment; and

(b) lifting of disposal restrictions (3

years from purchase).

No choice to pay tax on grant.

Alternative 2 Earlier of:

(a) cessation of employment; and

(b) lifting of disposal restrictions (5 years from purchase)

(or purchase of shares if up-front tax election made).

Earlier of:

(a) cessation of employment; and

(b) lifting of disposal restrictions (5

years from purchase).

No choice to pay tax on grant.

3.5 Taxable amount?

The taxable value of listed shares will be the market value of the shares at the ESS

deferred taxing point, less any amount paid to purchase the shares. 'Market value' for

these purposes will take its ordinary meaning, but will disregard anything that would

prevent or restrict conversion of the benefit to money (eg performance or service

conditions) (section 960-410). The Board of Taxation Report in the market value rules

recommended that market value remain in accordance with its ordinary meaning for these

Page 11

purposes and that the ATO release guidelines on value methods it is prepared to accept as

reasonable for these purposes.

The ATO is currently working on the market value guidelines which are likely to provide a

number of acceptable methods of calculating market value for these purposes, including an

average price over a week period and a spot price on the particular day, provided the

shares are not thinly traded.

3.6 Capital gains tax

Restricted share plan participants will generally be treated as having acquired their shares

for capital gains tax purposes at the ESS deferred taxing point for the market value of the

shares at that time. This means that the shares will need to be held for more than 12

months from the ESS deferred taxing point in order to benefit from the 50% capital gains

tax discount on any capital growth from the ESS deferred taxing point.

In the event a capital return occurs prior to the ESS deferred taxing point, the restricted

share plan participant will generally be expected to make a capital gain under CGT Event

G1 equal to that part of the capital return which is not a dividend for tax purposes (as the

participant will not, at that time, have a cost base of the shares – refer section 130-

80(4)(a)). It would appear if a demerger event occurs prior to the ESS deferred taxing

point, the participant will have a nil cost base of the shares in the demerged entity (but the

net effect will still be, as it was under the old law, to effectively move the value of the

demerged share from employment tax to capital gains tax).

Consideration should be given to the capital gains tax implications associated with the

allocation of any purchased or previously forfeited shares to participants from an employee

share trust. If the shares have only just been purchased at market price by the trustee just

before the allocation, there is unlikely to be any adverse CGT implications (as the market

value of the shares on allocation should be the same as the purchase price of the shares,

so no deemed gain for the trustee). However if the trustee has pre-purchased the shares

for a lower price than the market value when the shares are allocated (eg if shares have

been forfeited and are later reallocated), there is a potential CGT issue. We understand

this issue may be unintentional and is currently being reviewed. If the issue is not fixed it

may be able to be dealt with in practice by not pre-funding the purchase of shares (other

than for delivery under rights plans) and, in the event a forfeiture of shares under a share

plan occurs, use those shares to satisfy rights (as there is a CGT exemption for that) rather

than reallocating them to share plan participants.

3.7 Are changes to restricted share plans needed in light of the new ESS tax rules?

(a) A review should be undertaken of the operation of the good leaver provision in

practice to ensure that the real risk of forfeiture provision is likely to be able to be

satisfied for all participants. If there is a possible issue with retirement scenarios,

consideration could be given to adding in a minimum 6 month from grant service

condition for retirees.

(b) Consideration could be given to allowing participants to choose (from the grant

date) the lock-up period to apply post-vesting (up to 7 years from grant).

Page 12

(c) Consideration should be given to incorporating the Insider Dealing policy into the

offer documents.

(d) If, as in the example, the restricted share plan is operated as a share plan rather

than a rights plan, it must be remembered that, as under the old law, a later taxing

time for those shares is only available where the employer satisfies the 75% offer

test. Therefore care would need to be taken to ensure that test continues to be

satisfied for further awards under the retention share plan if the employer proposed

to not continue with its general share plans as a result of the introduction of the

new tax laws. Importantly though, if the retention share plan is operated as a

'rights' plans, the 75% offer test does not have to be satisfied to be entitled to a

later taxing time.

4. Impact of the New Rules on Performance Rights Plans

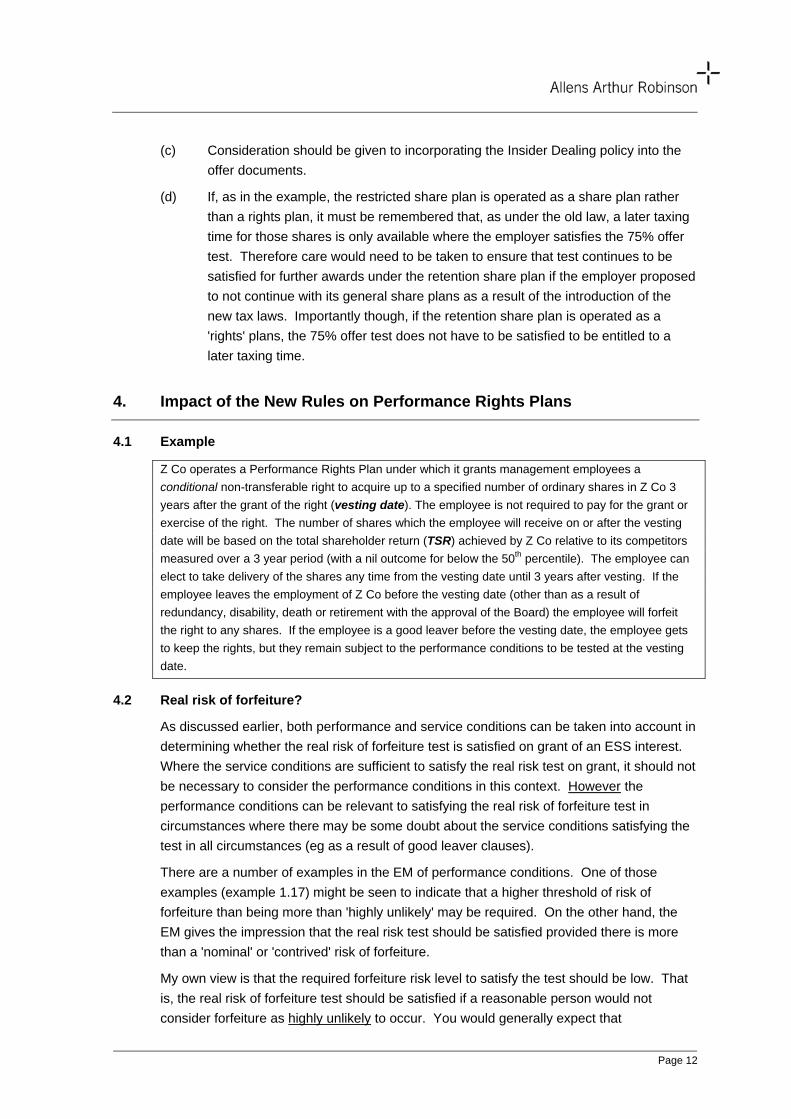

4.1 Example

Z Co operates a Performance Rights Plan under which it grants management employees a

conditional non-transferable right to acquire up to a specified number of ordinary shares in Z Co 3

years after the grant of the right (vesting date). The employee is not required to pay for the grant or

exercise of the right. The number of shares which the employee will receive on or after the vesting

date will be based on the total shareholder return (TSR) achieved by Z Co relative to its competitors

measured over a 3 year period (with a nil outcome for below the 50th percentile). The employee can

elect to take delivery of the shares any time from the vesting date until 3 years after vesting. If the

employee leaves the employment of Z Co before the vesting date (other than as a result of

redundancy, disability, death or retirement with the approval of the Board) the employee will forfeit

the right to any shares. If the employee is a good leaver before the vesting date, the employee gets

to keep the rights, but they remain subject to the performance conditions to be tested at the vesting

date.

4.2 Real risk of forfeiture?

As discussed earlier, both performance and service conditions can be taken into account in

determining whether the real risk of forfeiture test is satisfied on grant of an ESS interest.

Where the service conditions are sufficient to satisfy the real risk test on grant, it should not

be necessary to consider the performance conditions in this context. However the

performance conditions can be relevant to satisfying the real risk of forfeiture test in

circumstances where there may be some doubt about the service conditions satisfying the

test in all circumstances (eg as a result of good leaver clauses).

There are a number of examples in the EM of performance conditions. One of those

examples (example 1.17) might be seen to indicate that a higher threshold of risk of

forfeiture than being more than 'highly unlikely' may be required. On the other hand, the

EM gives the impression that the real risk test should be satisfied provided there is more

than a 'nominal' or 'contrived' risk of forfeiture.

My own view is that the required forfeiture risk level to satisfy the test should be low. That

is, the real risk of forfeiture test should be satisfied if a reasonable person would not

consider forfeiture as highly unlikely to occur. You would generally expect that

Page 13

performance conditions for long term incentive plans for listed companies which are

considered appropriate by their remuneration committee should satisfy the 'real risk of

forfeiture' test. For example, you would generally expect that the standard TSR test which

requires a company to be in the top half of performers of a list of comparable companies in

order to achieve any vesting of LTI awards would satisfy the real risk of forfeiture test even

if the company has a long history of always being in the top half of performers. It seems

unlikely that a reasonable person would conclude in such circumstances that it is 'highly

unlikely' that the company might be in the bottom half of comparative performers,

notwithstanding past performance.

For the accountants amongst us, I have been trying to come up with what I would consider

a 'safe-harbour' forfeiture risk percentage on grant. My own view is that if the risk of

forfeiture is 20% or more, there should be little doubt that would be considered a 'real risk'

under the new rules, but that lower risk levels should also be acceptable, depending on the

circumstances. The value of the awards at grant for accounting purposes may give some

guidance as to the likelihood of forfeiture in this context.

4.3 Taxing time

The 'ESS deferred taxing point' for rights under the new rules will occur at the earliest of:

(a) when the rights first become 'exercisable' unless, at that time, the shares to be

acquired on exercise of the rights are subject to either genuine restrictions on

disposal or a real risk of forfeiture;

(b) when the shares are no longer subject to real risk of forfeiture or genuine disposal

restrictions;

(c) cessation of employment; and

(d) 7 years from grant of the award.

(a) When the rights become exercisable

In the example, the taxing time for the rights which vest is likely to be on vesting in

year 3, unless, at that time, the employee is either prohibited from exercising the

rights or, if allowed to exercise, is prohibited from selling the resulting shares.

If the Insider Dealing Policy prohibits the employee from exercising the rights at

vesting, that would generally be sufficient to defer the taxing time on the rights until

the first date after vesting that the employee is no longer prohibited under the

Insider Policy from exercising the rights. If the Insider Dealing Policy allows the

employee to exercise the rights (eg where the shares are to be issued to the

employee) but prohibits the disposal of any resulting shares, that should also be

sufficient to continue a tax deferral until the first time when the employee is no

longer prohibited under the policy from disposing of the shares. Importantly, as the

'scheme' has to genuinely restrict the exercise of the rights or the disposal of the

shares, the plan documents (either the rules themselves or the offer documents)

should provide that the employee is prohibited under the plan from either

exercising the rights or disposing of the resulting shares if the employee is so

prohibited under the dealing policy.

Page 14

Being 'prohibited' from exercising the rights or selling the resulting shares under

the Insider Policy needs to be distinguished from being required to seek clearance

to deal under the policy. If vesting occurs at a time when the employee is not

prohibited from dealing, but is required to seek clearance to deal, that is unlikely to

be sufficient to defer the taxing time unless the employee has reason to believe

that such clearance would not have been given. In practice, if an employee is

claiming that vesting of rights is not a taxing time as a result of an Insider Policy,

when vesting occurs at a date when the policy allowed clearance to deal to be

sought, the ATO might expect that the employee evidence the existence of a

prohibition on sale by way of asking permission to deal at that time and being

denied that permission.

Thus the taxing time will arise the first time an employee is able to deal with the

shares after the rights become exercisable. This means that if vesting of rights

occurs during an open period, that is likely to be a taxing time notwithstanding the

employee may exercise the rights at a later time when a black out period may

apply to prohibit the resulting shares from being sold.

If the rights lapse without ever becoming exercisable (and before cessation of

employment), no tax should be payable on the rights under Division 83A.

(b) Cessation of employment

As discussed with the restricted share plan, cessation of employment remains a

taxing time even though the ESS interests may not at that time be vested.

In this example, if an employee forfeits the rights as a result of resigning before

vesting, no tax will be payable on leaving the employment. However if an

employee is a 'good leaver' before vesting, tax will be payable on leaving the

employment, based on the market value of the shares on the leaving date,

notwithstanding that, the rights continue to be subject to the performance

conditions. If the share price reduces between the leaving date and the vesting

date, the employee is not entitled to reduce the taxable amount on the leaving date

(but will be entitled to a capital loss if the shares are sold on vesting).

If tax applies on cessation of employment, and the awards are later forfeited as a

result of the performance condition not being satisfied, a refund of the tax paid on

cessation of employment would generally be available. However a refund of the

tax paid on cessation of employment will not be available if the award vests but

later lapses as a result of the employee not 'exercising' the rights before the lapse

date.

4.4 Taxing time under old law compared with new law

Taxing Time

Old law New law

Earlier of:

(a) cessation of employment;

Earlier of:

(a) cessation of employment;

Page 15

(b) exercise of rights to receive shares (ie up to 6 years

from grant), unless shares are subject to forfeiture or

disposal restrictions

(c) if shares received on exercise of rights are subject to

forfeiture or disposal restrictions – the lifting of those

restrictions; and

(d) 10 years from grant of award

(or grant of award if up-front tax election made).

(b) if no genuine disposal restrictions apply on

vesting – when the award first become exercisable

after vesting (3 years from grant);

(c) if genuine disposal restrictions apply on vesting –

when those restrictions lift;

(d) 7 years from grant of award.

No choice to pay tax on grant of awards.

4.5 Taxable amount

The taxable value of right to listed shares which have no exercise price will be the market

value of the shares at the ESS deferred taxing point. 'Market value' for these purposes will

take its ordinary meaning, but will disregard anything that would prevent or restrict

conversion of the benefit to money (eg performance or service conditions) (section 960-

410). As discussed earlier, it is likely that an average price over a week period and a spot

price on the particular day (provided the shares are not thinly traded) will be acceptable for

these purposes.

4.6 Are changes to performance rights plans needed in light of the new ESS tax rules?

(a) As tax will generally be payable on vesting rather than exercise, consideration

could be given to amending the plan to abolish the exercise period (ie to

automatically deliver the shares on vesting).

(b) Consideration could be given to incorporating the company's Insider Dealing policy

into the offer documents.

(c) Consideration could be given to allowing participants to choose (from the grant

date) the lock-up period to apply post-vesting for the shares to be acquired on

vesting (up to 7 years from grant). For example, it may the case that very senior

executives such as the CEO may prefer to have their shares prohibited from sale

for a fixed period after vesting, rather than potentially having to immediately sell up

to half of the shares on vesting to fund the tax due at that time.

5. Impact of the New Rules on Options with an Exercise Price

5.1 Example

Z Co operates an Option Plan under which it grants non-transferable options to acquire ordinary

shares in Z Co on the payment of an exercise price. The options are unable to be exercised until 3

years after grant, and generally lapse if the employee ceases employment with Z Co (other than as a

result of redundancy, disability, death or retirement with the approval of the Board) before that time.

After the options become exercisable, the employee has up to 7 years in which to exercise the

options, but a shorter period in the event of leaving employment after vesting.

Page 16

5.2 Real risk of forfeiture?

The 3 year service condition in this plan should be sufficient to satisfy the real risk test,

subject to the 'good leaver' retirement issue discussed earlier. It is important to note that

the fact that the options may never be exercised as a result of never being 'in the money'

does not appear to be something which can be taken into account in determining whether

or not there is a 'real risk' on grant of the options that the options will be forfeited or lost (as

'lose' in this context is defined to exclude letting the options lapse). It would appear

therefore that even where an option lapses on the expiry date having never been 'in the

money', but the employee could have, in theory, exercised the option before the lapse date,

the employee will be considered to be 'letting' the option lapse as a result of having not

exercised the option.

5.3 Taxing time?

Consistent with the analysis for performance rights plans, you would generally expect the

taxing time for the options to be the date the options first become exercisable unless, at

that time, the employee was prohibited from selling the resulting shares. In this example

however, the question arises as to whether a later taxing time than vesting is available

given the plan rules provide for the options to lapse early on cessation of employment after

vesting.

While this issue is not as clear as it could be in the drafting, it seems to us that the lapse of

options after vesting for cessation of employment will be unlikely to result in a taxing time

later than vesting. This is because a taxing time later than vesting would require that the

rights continue, post vesting of the rights, to be subject to a 'real risk' that the rights will be

forfeited or lost after vesting 'other than by letting the rights lapse'. Where the rights

become exercisable on vesting, it may be difficult to say that the rights continue after

vesting to be subject to a real risk that the rights will be lost other than by letting the rights

lapse. This view is consistent with the EM which clearly indicates that the intention is for

the taxing time to be when the option holder is first entitled to exercise the options,

notwithstanding the options may lapse after that time (eg see para 1.200).

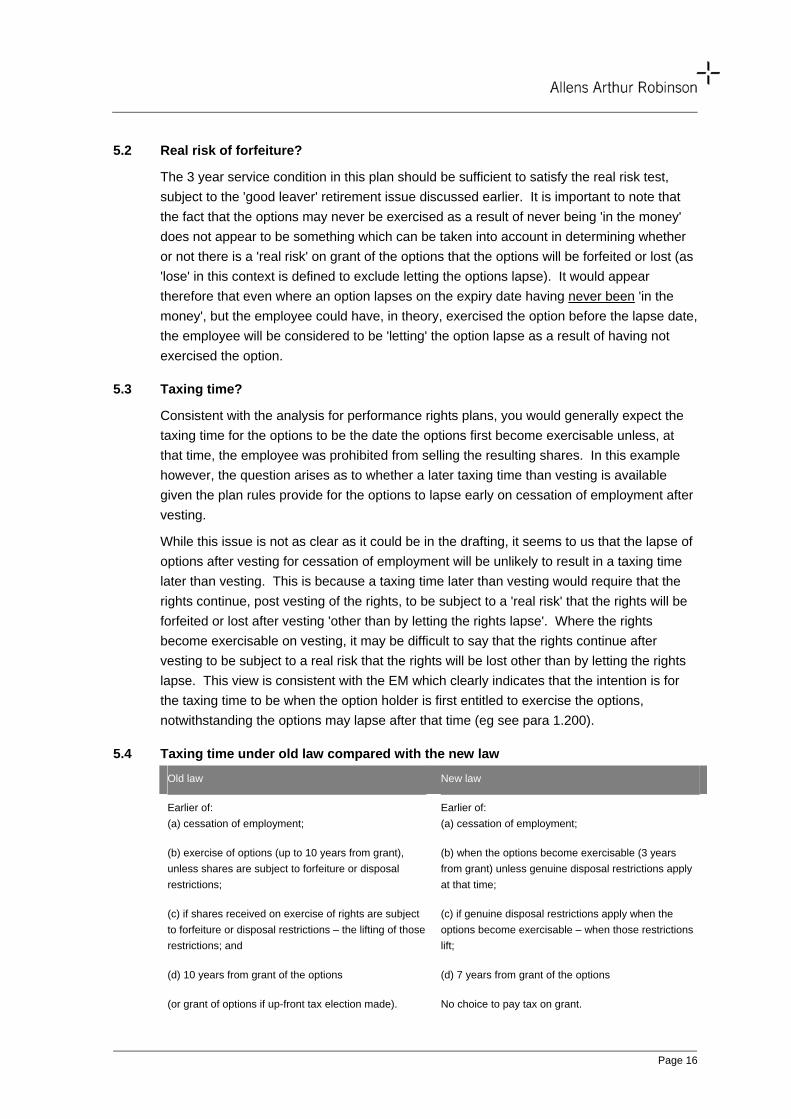

5.4 Taxing time under old law compared with the new law

Old law New law

Earlier of:

(a) cessation of employment;

(b) exercise of options (up to 10 years from grant),

unless shares are subject to forfeiture or disposal

restrictions;

(c) if shares received on exercise of rights are subject

to forfeiture or disposal restrictions – the lifting of those

restrictions; and

(d) 10 years from grant of the options

(or grant of options if up-front tax election made).

Earlier of:

(a) cessation of employment;

(b) when the options become exercisable (3 years

from grant) unless genuine disposal restrictions apply

at that time;

(c) if genuine disposal restrictions apply when the

options become exercisable – when those restrictions

lift;

(d) 7 years from grant of the options

No choice to pay tax on grant.

Page 17

5.5 Taxable amount

The taxable value of options at the ESS deferred taxing point will be, at the choice of the

taxpayer, either:

(a) the market value of the options in accordance with its ordinary meaning (but

disregarding anything that would prevent or restrict conversion of the benefit to

money – refer s.960-410 of ITAA 1997); or

(b) the value of the options in accordance with the regulations.

The regulations currently provide for options to be valued at the greater of the market value

of the shares less the exercise price of the options (ie the spread) and an amount

calculated in accordance with statutory tables. As a general rule of thumb:

(a) The taxable value of options under the tables will be nil where the market value of

the shares at the ESS deferred taxing point is less than 50% of the exercise price

of the options.

(b) 'Spread' rather than the table amount usually comes into play when the market

value of the share at the ESS deferred taxing point is more than 152% of the

exercise price of the option.

(c) Where the market value of the share at the ESS deferred taxing point is between

50% and 152% of the exercise price of the options, there will often be a taxable

value of the options under the tables. This means that options can have a value

under the tables even though the options are out of the money at the taxing point.

For example, if an option is able to be exercised for up to 3 years from vesting, the

option will have a taxable value on vesting under the tables even if the market

value of the share on exercise of the option is only 70% of the exercise price of the

option (ie the options are 30% 'out of the money').

The Board of Taxation has recommended the continued use of the 'safe harbour'

methodology of valuing options with an exercise price at the greater of spread and the

value derived from statutory valuation tables, due to the complexity and compliance costs

associated with valuing such options. However the Board noted that the basis and

assumptions underpinning the statutory valuation tables be reviewed from time to time.

The Government has announced that the tables will remain in place at this stage and that it

will make a decision in relation to whether to revise the tables in the context of the 2011-12

Budget (ie in May 2011).

The Board notes the following in the discussion in the Report about the statutory valuation

tables (chapter 5).

(a) While the tables are based on a Black Scholes valuation model, the Government

Actuary have acknowledged that they have not found any direct evidence that

points to a preferred used of the Black Scholes model over that of other option

pricing models, such as Binominal or Monte Carlo models.

(b) While Black Scholes usually requires company specific inputs (dividend yield and

volatility) and time specific inputs (time to expiry and risk free rate of return), the

tables have assumed a 'constant' for dividend yield (4% pa – the high the yield the

Page 18

lower the value of the option), volatility (10% - the higher the volatility rate, the

higher the value of the options) and risk free rate of return (7.6% pa – the higher

the rate, the higher the value of the option). With the exception of the risk free rate

of return, those assumed constants may be considered in the current environment

to be potentially concessional.

The idea of the safe harbour rule is that employers and employees should be able to use

the tables without incurring the expense to separately have the options valued. While it is

of course open for an employee to separately establish the market value of options other

than by using the tables, a couple of notes of warning in this context:

(a) The Board of Taxation Report clearly rejects the market value of the options as

being simply the 'intrinsic' value of the option (market value of share less exercise

price of the option), except in very limited circumstances (refer para 5.25).

(b) As noted earlier, while market value is to take its ordinary meaning, it disregards

anything that would prevent or restrict conversion of the benefit to money. So, for

example, if the options are to be valued before the vesting date (eg on cessation of

employment) any remaining performance conditions would not seem to be able to

be taken into account in valuing the options. However an interesting question

arises as to whether the fact that the life of an option may be cut short by cessation

of employment after vesting can be taken into account in a valuation of the option

at vesting. I would have thought that it could, given the life of the option at vesting

is clearly relevant to its market value according to ordinary concepts at vesting and

should not be something which prevents or restrict conversion of the benefit to

money at the vesting date.

(c) Given the general flavour from the Board of Taxation Report that the statutory

tables may be 'concessional' in valuing options, it may be considered difficult in

practice to be able to convince the ATO that a 'market value' of less than the value

produced by the tables is correct without significant valuation evidence. That said,

there could be well be clear circumstances where a market value of the options at

vesting produces a lower value than the tables, particularly where, for example:

(i) the life of the options can be significantly shortened by cessation of

employment after vesting;

(ii) the company's dividend yield is more than 4%; and/or

(iii) the company's volatility is less than 10%;

It is important to remember that, if the employee exercises the options and sells the shares

within 30 days of what would otherwise be the ESS deferred taxing point, the taxable value

of the options will be the arm's length sale proceeds less the exercise price of the options.

However this 30 day rule will not apply where the employee exercises the options but does

not sell the shares within 30 days of the ESS deferred taxing point.

It seems likely that informed employees may well want to exercise and sell sufficient

shares to fund the tax bill payable soon after vesting of the options. However the fact that

those who exercise and sell within 30 days of vesting will only be required to pay tax on

their real profit whereas those who exercise within 30 days of vesting but do not

Page 19

immediately sell may have a taxable amount far greater than the 'real' gain made on their

options may be seen to make it unlikely that those who chose to exercise within a short

period of vesting will continue to hold the shares acquired on exercise of the options,

unless the options are sufficiently in the money on vesting that the taxable value of the

options at vesting is likely to be the spread rather than the amount per the statutory tables.

5.6 Refund rules

A refund of tax paid on options is not available where the options lapse as a result of a

choice made by the taxpayer (other than a choice to cease employment). If the options

have become exercisable and later lapse on their normal expiry date, it might be said that

the later lapse will effectively be as a result of a choice made by the option holder to not

exercise the options before the expiry date. However an interesting question arises in this

example, given options become exercisable but may later lapse 'early' on cessation of

employment. Do the options lapse in those circumstances as a result of a choice by the

employee to not exercise the options before ceasing employment or, rather, because the

employee has ceased employment? While both actions/inactions effectively lead to the

lapse of the options, the more direct cause would appear to be cessation of employment.

If a leaving employee can get into the refund rules for vested options as a result of those

options lapsing on cessation of employment, but not as a result of those options lapsing on

the expiry date, that may put employers at risk of significant resignations close to the expiry

date of options where the options are out of the money at that time. While it is relatively

common for vested options to lapse on cessation of employment after vesting, the EM

does not appear to deal with this common fact pattern in its discussion of the refund rule.

We understand the ATO may be currently considering this issue so hopefully we will at

least have some clarity of the ATO view on this in the next couple of months.

5.7 Are changes to option plans needed in light of the new ESS tax rules?

(a) Add share price condition?

Consideration could be given to, on grant, having a 'share price' condition as part

of the exercise conditions to the effect that the options do not become exercisable

until the options are 'in the money' (refer example 1.31 in the EM). If the condition

was not met at the 'normal' vesting date of the options, it could continue to be re-

tested say, on a monthly basis, until the earlier of when the condition was satisfied

and expiry of the options. As cessation of employment before the options become

exercisable can also be a taxing point (where the options do not lapse on ceasing

the employment), consideration could be given to adding a share price condition

for good leavers to be tested just prior to employment ceasing (with the options

lapsing at that time if the condition was not satisfied).

It is important to note that, if tax has applied prior to the share price condition being

satisfied (eg on cessation of employment or 7 years from grant), a refund of that

tax is unlikely to be available if the options are never exercised as a result of the

share price condition not being satisfied.

(b) Prohibit sale of shares acquired on exercise of options?

Page 20

The taxing time would not generally arise when the options become exercisable if

any shares to be acquired on exercise of the options were to prohibited from sale.

Instead, the taxing time would arise on the earlier of when that prohibition on sale

of the shares first lifted, and 7 years from grant of the options. Given this,

consideration could be given to imposing a prohibition on the sale of any shares

acquired on exercise of the options until the earlier of the day after the date the

options would have expired if they had not been exercised and 7 years from grant

of the options. If that occurred, and the options lapsed before the date any

prohibition on sale would have lifted (and the employee remained in employment),

not tax should be payable on the lapse of the options (as an ESS deferred taxing

point will have never arisen).

While adding a prohibition on the sale shares acquired on the exercise of options

may stop tax on vesting of underwater options, it would also mean that an

employee who chose to exercise the options soon after vesting would be prohibited

from selling any resulting shares for a period after exercise of the options, and

would continue to be subject to income tax (instead of capital gains tax) on any

further increase in the value of the shares from vesting of the options until the lifting

of the disposal restrictions.

(c) Reduce the exercise period?

Consideration could be given to reducing the exercise period, given tax is likely to

be payable on vesting rather than exercise of the options, and the taxable value at

vesting out of the money options will be lower if the exercise period is shorter.

(d) Refund on leaving employment after vesting?

Clarification is needed as to whether a refund of tax paid on vesting of the options

would be available in the event the lapsing date of the options was bought forward

as a result of the employee leaving the employment after vesting but before the

expiry date. If a refund is available in these circumstances, consideration should

be given as to wether the plan rules should be amended in light of this outcome.

(e) Stop granting options?

As tax will generally be payable on vesting of options, with no refund if the options

later lapse, consideration could be given to restructuring such awards to a reduced

number of 'performance rights' with no exercise price.

6. Impact of the New Rules on Share Purchase Plans

6.1 Example

Z Co operates a Share Purchase Plan which entitles all employees to purchase up to $5,000 of Z Co

ordinary shares a year. Employees who participate in the Plan are awarded with a 1 for 1 employer

match (or 50% discount on purchase price).

Alternative 1 ($5,000 post tax purchase with $5,000 forfeitable match)

The original $5,000 of shares are purchased at market value on an after tax basis. To receive the

employer match, the employee must hold the original shares for 2 years, and remain employed with Z

Page 21

Co for that period. If the employee leaves the employment of Z Co before 2 years from the purchase

of the original shares (other than as a result of redundancy, disability, death or approved retirement)

the employee forfeits the right to the Z Co matching shares.

Alternative 2 ($5,000 pre tax purchase with $5,000 forfeitable match)

As for Alternative 1, except the original $5,000 of shares are purchased at market value on a pre-tax

basis (ie salary sacrificed) and the employee is prohibited from selling the original shares until the

matched shares are awarded (ie 2 years from purchase of the original shares).

Alternative 3 ($2,500 pre tax purchase with $2,500 non-forfeitable discount)

As for Alternative 2 (ie employee salary sacrifices), except the employee is provided with $5,000 of

shares but is only required to salary sacrifice $2,500 for those shares. No forfeiture conditions apply

to any of the shares, but disposal of the shares is prohibited for 2 years from purchase (unless earlier

cessation of employment).

6.2 $5,000 post-tax purchase with $5,000 forfeitable match (Alternative 1)

These plans operated under the old tax laws and continue to operate in a similar way

under the new tax laws.

(a) Original shares

Provided the employee pays (on a post-tax basis) 'market value' (or more) for the

original shares, Division 83A will not be applicable. Capital gains tax will simply

apply when the shares are eventually sold. While market value for these purposes

was, under the old tax rules, locked into a one week weighted average price, it will

now take its ordinary meaning. As discussed earlier, we expect the ATO will

shortly issue guidelines on acceptable market values for these purposes. Such

guidelines may be expected to include, where shares are purchased on-market, a

value based on the average purchase cost of the shares, provided the shares are

allocated to the employee within a reasonable time frame of the commencement of

the buying period (eg within a couple of weeks).

(b) Matched shares

The 'matched shares' will be rights to shares on purchase of the original shares.

Those rights to shares should satisfy the real risk of forfeiture test as a result of the

2 year service testing (but subject to the good leaver issues discussed previously).

This means that the matched shares are likely to be taxable on delivery 2 years

after purchase of the original shares.

6.3 $5,000 pre-tax purchase with $5,000 forfeitable match (Alternative 2)

(a) Original shares

Even though the employee 'salary sacrifices' market value for these shares,

Division 83A will apply as the shares are acquired on a pre-tax basis. As forfeiture

conditions do not apply to the original shares, they will be taxed on purchase

unless the following conditions are satisfied.

(i) Reduction in salary required

Page 22

This condition requires that the shares are acquired by the employee because the

employee has agreed to receive the shares in return for a reduction in salary, or

the shares are received as part of the employee's remuneration package in

circumstances where it is reasonable to conclude that the salary would be greater

if the shares were not part of that package. This condition should be satisfied here

as the employee is choosing to salary sacrifice to purchase the shares.

(ii) Employee pays no after tax money for the acquisition of the shares

Even though the employee is 'salary sacrificing' for the shares, the employee is not

paying any post-tax money for the shares.

(iii) Only shares under the plan or, if some rights, real risk of forfeiture test is

satisfied for the rights

This means that a salary sacrifice plan will be able to be offered with an employer

'match' to shares to be delivery in the future where that right to shares satisfies the

'real risk of forfeiture' test.

This condition will be satisfied here as the original shares will be shares from the

purchase date, and, while the matching shares are 'rights to shares' first, it would

generally be expected that those rights to shares will satisfy the real risk of

forfeiture test. Importantly however, this condition would not be satisfied for a

participant who was not, at grant, at sufficient risk in relation to the matched

shares. This would mean that tax would be payable on purchase of the original

shares on both the value of the original shares, and the value of the employer

match (ie $10,000 taxed on purchase of the original shares).

(iv) The 'governing rules of the scheme' provide that the subdivision applies

This can be included as part of the offer documents.

(v) $5,000 limit

No more than $5,000 of shares a year in that employer or holding company are

acquired by the employee under that plan (not including shares or rights which

satisfy the real risk of forfeiture test), or another plan which satisfies all of the

above conditions. If the $5,000 limit is exceeded, even if only by $1, a tax deferral

is not available on any of the shares.

(vi) Genuine disposal restrictions

Shares acquired under a salary sacrifice plan are only entitled to a later taxing time

where, at the time the shares are acquired, the scheme genuinely restricts the

shares being immediately sold. Here, the original shares will be prohibited from

sale until the matching shares are awarded (2 years from purchase of the original

shares, unless earlier cessation of employment). It may therefore be expected that

the taxing time for these shares will be when the disposal restrictions lift, generally

2 years after purchase.

'Genuinely restricted' is not defined in the legislation. The EM describes the

required restrictions as 'restrictions preventing disposal' which is the terminology

used in the old law. The EM goes on to explain that restrictions will be considered

Page 23

to be 'lifted' once an opportunity arises in which a taxpayer can dispose of the

share, even if the restriction is later reapplied. This implies that the word

'genuinely' in front of restricted is intended to mean that the employee is prohibited

from selling the shares.

We understand that the ATO are considering what genuinely restricted means

under the new law, with a view to issuing some guidance to employers shortly.

Consistent with the old law, we would expect that the ATO view will be that the

need to make a request to sell will not be considered a genuine disposal restriction

if such requests are routinely approved, and that such requests will be considered

to be routinely approved if it is unlikely that factors would exist which would cause

the request to be denied. Thus 'genuine restrictions' under the new law will clearly

require more than a rubber stamp approval process and are likely to require the

employee having a real sense that, absent unusual circumstances, the shares are

likely to be prohibited from sale for a fixed period.

(b) Matched shares

As discussed earlier, the 'matched shares' are likely to be taxable on delivery 2

years after purchase of the original shares, and the value of these shares is not

taken into account in the $5,000 test.

6.4 $2,500 pre tax purchase with $2,500 non-forfeitable discount (Alternative 3)

As there is no real risk of forfeiture on the 'discount' provided by the employer, that

discount will have to be provided as part of the $5,000 limit for the shares to be entitled to a

later taxing time. Importantly, the 'reduced salary' required to get a later taxing time does

not require that there be a 'match' between the amount of salary reduced and the value of

the shares awarded – just simply that, for each share acquired, the employee has

sacrificed some salary. In this example, the employee is having their salary reduced by

$2,500 but is receiving $5,000 of shares which should satisfy this requirement.

As the taxing time will arise when the disposal restrictions lift, the taxing time in this

example is likely to be 2 years from purchase of the shares (or cessation of employment if

earlier).

6.5 Are changes to share purchase plans needed in light of the new ESS tax rules?

(a) For Alternatives 1 and 2, a review should be undertaken of the operation of the

good leaver provision for the matching award in practice to ensure that the real risk

of forfeiture provision is likely to be able to be satisfied for all participants in relation

to the matched award.

(b) As the taxing time will arise when the disposal restrictions lift (but no longer than 7

years), the employee could, as part of the offer documents, be given the choice of

the lock up period to be applied to their shares acquired under the plan. However

the choice would have to be made prior to the shares being awarded and should

not extend beyond the earlier of cessation of employment and 7 years. So, for

example, consideration could be given to allowing participants to choose (from the

Page 24

grant date) the lock-up period to apply to the original shares for alternatives 2 and

3 and, in the case of Alternatives 1 and 2, to the matching shares.

(c) In Alternatives 2 and 3 extra care needs to be taken to ensure that no more than

$5,000 non-forfeitable shares are purchased each tax year ended 30 June. So, for

example, care would need to be taken that left-over amounts of sacrificed money

from one year of income (eg where that amount was not sufficient to purchase a

marketable bundle of shares) are not rolled into the next tax year without a

reduction of the sacrificed amount from that year to be used to purchase shares. A

cautious approach may be to limit sacrifice and discount amounts to, say, $4,800 a

year to give 'wriggle room' on this issue.

(d) In comparing Alternative 1 to alternatives 2 and 3, it must be remembered that

'deferral' of the taxing time on the original investment amount comes at the cost of

the loss of the 50% capital gains tax concession on the capital growth.

7. Impact of the New Rules on Awards Granted before 1 July 2009

7.1 ESS deferred taxing point for awards granted before 1 July 2009

The taxing time for awards granted before 1 July 2009 will generally remain the same

under the new law as it was under the old law, subject to the 30 day rule and indeterminate

right rule. This generally means that the taxing time for rights will remain the earlier of

cessation of employment and exercise of the rights and the taxing time of shares subject to

remote forfeiture conditions will generally remain when those remote forfeiture conditions

no longer apply.

7.2 Old refund rules

The 'old' refund rules will continue to apply to awards granted before 1 July 2009. This

means that a refund of tax will not be available in relation to a forfeiture of shares, but will

generally be available on the lapse of options, even if the options lapse as a result of being

'out of the money'.

7.3 Indeterminate right rule

If an award was not a right to acquire a share as at 30 June 2009 (eg as a result of a cash

discretion in the plan rules, or because the number of shares could not be calculated) but

becomes shares on or after 1 July 2009, the new law attempts to deem the right to have

always been a right to acquire a share. This can potentially result (subject to relevant time

limits) in taxing times arising before 1 July 2009 for awards where section 139E elections

have been made in previous years, or where the employee has ceased the relevant

employment before 1 July 2009.

7.4 Market value rules

The new 'market value' rules will apply to awards granted before 1 July 2009 which have

an ESS deferred taxing time on or after 1 July 2009. Importantly however, where the

taxing time for options with an exercise price is the exercise of the options, it should be

reasonable to assume that the taxable amount will be the spread on exercise of the options

Page 25

(or sale proceeds less the exercise price of the options if the shares are sold within 30 days

of exercise), even if that amount is less than the amount calculated in accordance with the

statutory valuation tables.

7.5 CGT acquisition date

Shares and rights which were acquired for CGT purposes before 1 July 2009 will be

deemed to have an acquisition date for CGT purposes of the date the shares and rights

were originally acquired.

7.6 New reporting rule

The new employer reporting rule (refer 8) will apply to shares and rights acquired before

1 July 2009 which have an ESS deferred taxing time on or after 1 July 2009. However the

new TFN withholding rule will not apply.

7.7 Cross border employees

If an employee acquired shares or rights before 1 July 2009 which have a taxing time on or

after 1 July 2009, and the employee works offshore for some part of the vesting period, the

employee should be entitled to a tax exemption for the 'foreign sourced' component of the

gain at the deferred taxing point, regardless of whether the foreign employment occurred

before or after 1 July 2009, regardless of the employee's residency status at the deferred

taxing point and regardless of whether the employee was working offshore as resident or

non-resident (s.83A-5(4)(a) of ITTPA 1997). This outcome is different to the s.23AG

transitional rule which would applies for cash settled awards.

8. New Employer Reporting and Withholding Rule

8.1 Annual reporting to employee and ATO

'Providers' of ESS interests are to provide an annual report by 14 July (to employees) and

14 August (to the ATO) of the year following the year in which:

(a) a grant of ESS interests has occurred; and/or

(b) an ESS deferred taxing point has arisen (including in relation to ESS interests

granted before 1 July 2009).

Very generally, the report is required to include information about awards granted in the tax

year and awards which have had a taxing time in the tax year.

8.2 Employee ESS Statements for FY10

The first ESS statements are required to be provided to employees by 14 July 2010 in