ED revenue recognition from contracts with customers

An overview of the revised proposals

2 October 2012

Page 2 ® 2012 Ernst & Young

Disclaimer

This presentation contains information in summary form and is therefore not intended to be a substitute for detailed research or the exercise of professional judgment. It is also not intended and should not be relied upon as an absolute advice. Consultation with advisor for each specific matter is recommended.Neither Ernst Young nor any other members of the global Ernst & Young network accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this presentation.The views expressed by speakers in this presentation are likely general views and may not be appropriate for every situations despite of being considered similar facts.

Revenue from Contracts with Customers Agenda

Overview and project statusKey messages for accounting professionsScopeThe five-step modelOther aspects of the modelImplementation issues

Page 4 ® 2012 Ernst & Young

Overview – new proposal for revenue recognition

The Boards issued a new revenue recognition Exposure Draft (ED) that will replace all existing revenue recognition standards and interpretations

The proposed model addresses revenue arising from contracts with customersAll industries will be affected

Core principleRecognise revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services

Page 5 ® 2012 Ernst & Young

Project status

Based on discussion paper issued in December 2008Boards’ redeliberations of the original Exposure Draft were completed in October 2011The latest Exposure Draft issued 14 November 2011

Open for comment until 13 March 2012The Boards will continue re-deliberations in September 2012Final standard may be issued in 1H 2013

Retrospective application, with some relief providedAdditional disclosures required if reliefs are applied

Not expected to be effective before 1 January 2015

Revenue from Contracts with Customers Agenda

Overview and project statusKey messages for accounting professionsScopeThe five-step modelOther aspects of the modelImplementation issues

Page 7 ® 2012 Ernst & Young

Key messages for accounting professions

The new standard will result in significant changes in practice in various industries.The proposal would require many companies to allocate more revenue than they currently doImplementation would require many companies to track and update pricing information as contracts are modified and as they offer new products and services.The new model would require capitalisation of incremental costs to obtain a contract.Require significant estimates and judgment (bundle of goods & services, over time and at a point in time, standalone price, onerous performance obligation test, forwarding looking information disclosures etc.)

Revenue from Contracts with Customers Agenda

Overview and project statusKey messages for accounting professionsScopeThe five-step model Other aspects of the modelImplementation issues

Page 9 ® 2012 Ernst & Young

Scope and scope exceptions

• Revenue arising from contracts with customers • The sale of some non-financial assets that are

not an output of the entity’s ordinary activities (i.e., sale of property, plant and equipment (PPE) or intangibles)

Applies to:

• Leasing contracts• Insurance contracts• Financial instruments contracts• Non-monetary exchanges entered into for the

purposes of facilitating the sale to another entity• Put options on sale and repurchase agreements

where the customer has a significant economic incentive to exercise

• Collaborative arrangements

Does not apply to:

Page 10 ® 2012 Ernst & Young

Replacement of current standards

To be superseded Thai standard Current status

IAS 11 Construction Contracts

TAS 11 Effective

IAS 18 Revenue, TAS 18 Effective

IFRIC13 Customer Loyalty Programmes,

TFRIC 13 Draft

IFRIC15 Agreements for the Construction of Real Estate,

TFRIC 15 Effective

IFRIC18 Transfers of Assets from Customers

TFRIC 18 Transfers of Assets from Customers

In process of finalizing the draft

SIC 31 Revenue – Barter Transaction involving Advertising Services.

SIC 31 - Effective

Revenue from Contracts with Customers Agenda

Overview and project statusKey messages for accounting professionsScopeThe five-step model Other aspects of the modelImplementation issues

Page 12 ® 2012 Ernst & Young

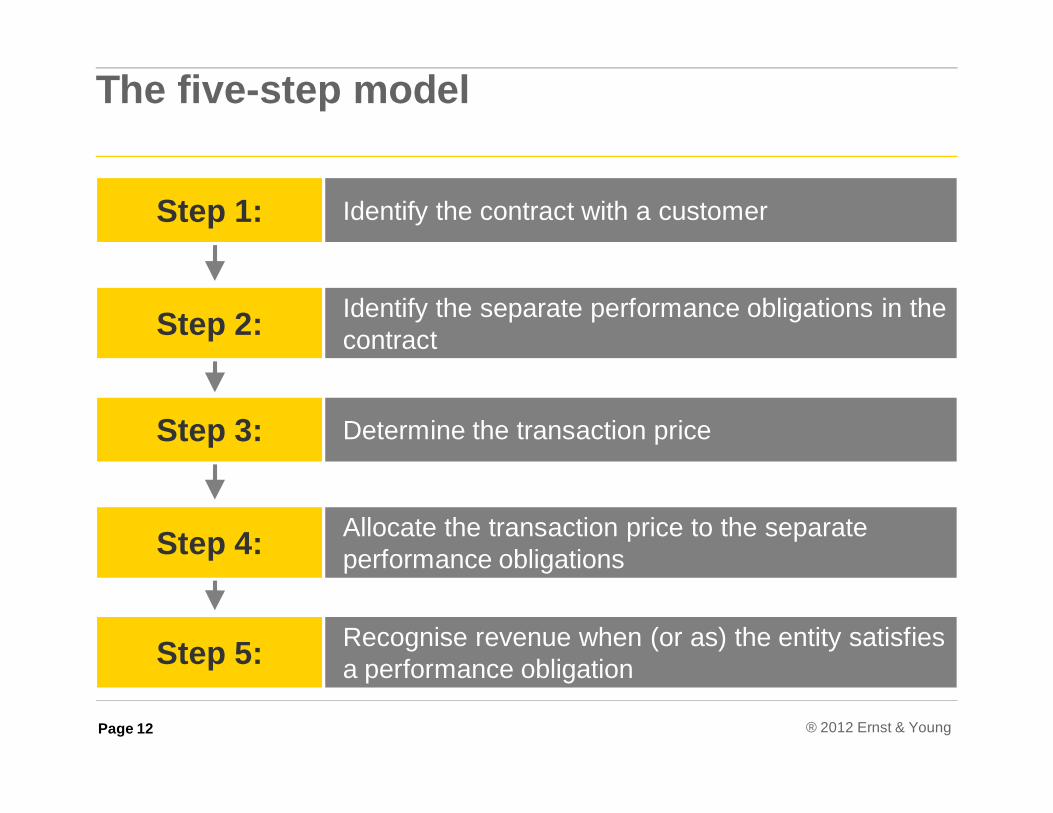

The five-step model

Step 1: Identify the contract with a customer

Step 2: Identify the separate performance obligations in the contract

Step 3: Determine the transaction price

Step 4: Allocate the transaction price to the separate performance obligations

Step 5: Recognise revenue when (or as) the entity satisfies a performance obligation

Page 13 ® 2012 Ernst & Young

Contract(s) with customers diagram

The entity Customers

Contract(s)

Performance obligation#1

Performance obligation#2

Performance obligation#3

Bundle distinct?

Customer is to obtain goods & services that are output of the entity’s ordinary activities

Page 14 ® 2012 Ernst & Young

Step 1: Identifying the contract

Model is applied to each contract Can be written, oral or impliedDoes not exist if both parties can cancel without penalty

Can combine contracts if entered into at or near the same time with the same customer (or related parties), provided any of the following criteria are met:

Negotiated as a packageConsideration depends on other contractGoods and services are interrelated

Page 15 ® 2012 Ernst & Young

Step 1: Identifying the contract (cont.)

A contract modification would be any change in the scope or price of a contractIf only a price change, allocate the transaction price to all performance obligations using original allocationTreat as a separate contract if the modification both:

Adds a separate performance obligation(s)Consideration reflects the standalone selling price

Otherwise, treat as part of the original contract Accounted for differently depending on the attributes of the remaining goods and services to be provided

Page 16 ® 2012 Ernst & Young

Step 2: Identifying the performance obligations

A performance obligation is a promise (explicit or implicit) to transfer a good or service to the customerIdentified at contract inception based on:

contractual termscustomary business practicePattern of transfer differs from other goods / services

Goods or services are distinct

orVendor sold them separately

Customer can use them on its own or with readily available resources

Account separately unless:(a) Highly integrated

(b) Bundle is significantly customised

and

Page 17 ® 2012 Ernst & Young

Step 2: Identifying the performance obligations (cont)

The proposals contain specific application guidance on:

Rights of returnProduct warrantiesLicences and rights to useOptions to acquire additional goods and services (e.g., discount vouchers, customer loyalty points)Principal vs. agent considerations

Page 18 ® 2012 Ernst & Young

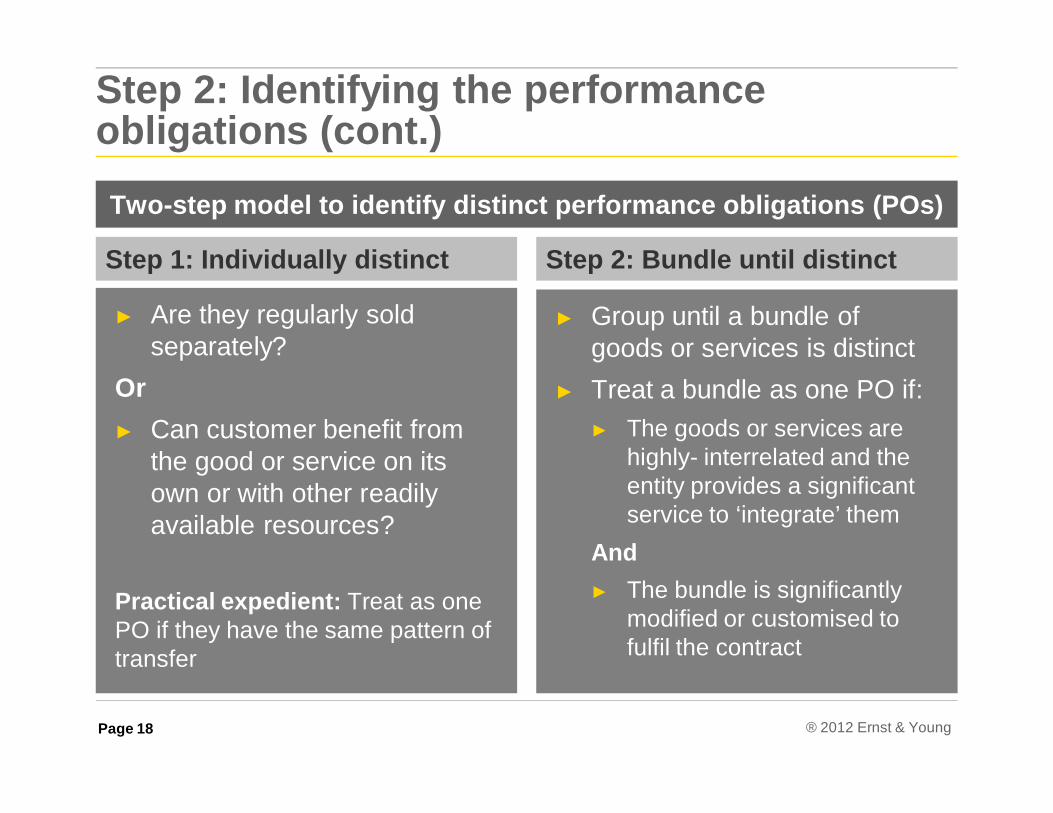

Step 2: Identifying the performance obligations (cont.)

Two-step model to identify distinct performance obligations (POs)

Step 1: Individually distinct Step 2: Bundle until distinct

Are they regularly sold separately?

OrCan customer benefit from the good or service on its own or with other readily available resources?

Practical expedient: Treat as one PO if they have the same pattern of transfer

Group until a bundle of goods or services is distinctTreat a bundle as one PO if:

The goods or services are highly- interrelated and the entity provides a significant service to ‘integrate’ them

AndThe bundle is significantly modified or customised to fulfil the contract

Page 19 ® 2012 Ernst & Young

Step 2: Identifying the performance obligations (cont.)

Performance Obligations?

1

1 . X1 2

100 600

60

2

IT

IT

Page 20 ® 2012 Ernst & Young

Step 2: Identifying the performance obligations (cont.)

Performance Obligation?

3

90

3

3,200 400

90 100

Dr. / 3,600Cr. Contract liability

(service-type warranty) 400 3,200

Dr xxx Cr. xxx

Dr. 100Cr. 100

Page 21 ® 2012 Ernst & Young

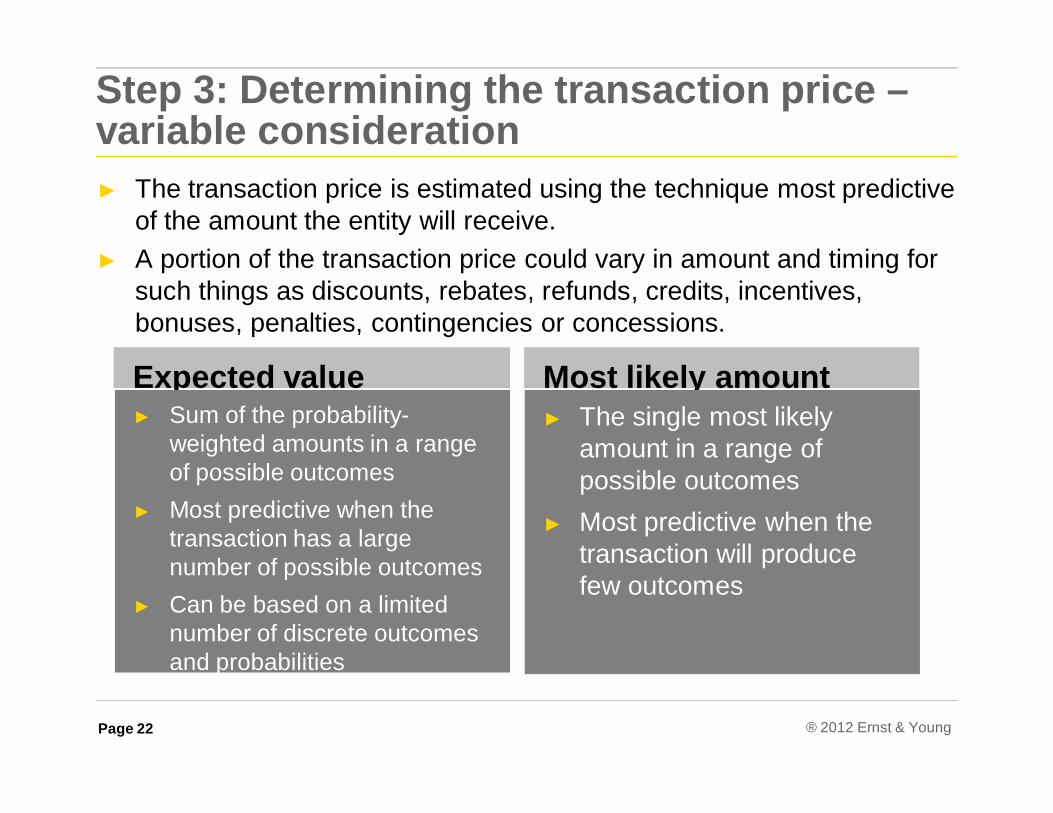

Step 3: Determining the transaction price

Transaction price The amount of consideration that an entity expects to be entitled in exchange for transferring a good or service to a customer.

Must consider the effects of all of the following:Variable considerationTime value of moneyNon-cash considerationConsideration payable to the customerCollectability (adjacent to revenue)

Page 22 ® 2012 Ernst & Young

Step 3: Determining the transaction price –variable consideration

The transaction price is estimated using the technique most predictive of the amount the entity will receive.A portion of the transaction price could vary in amount and timing for such things as discounts, rebates, refunds, credits, incentives, bonuses, penalties, contingencies or concessions.

Expected value Most likely amountSum of the probability-weighted amounts in a range of possible outcomesMost predictive when the transaction has a large number of possible outcomesCan be based on a limited number of discrete outcomes and probabilities

The single most likely amount in a range of possible outcomesMost predictive when the transaction will produce few outcomes

Page 23 ® 2012 Ernst & Young

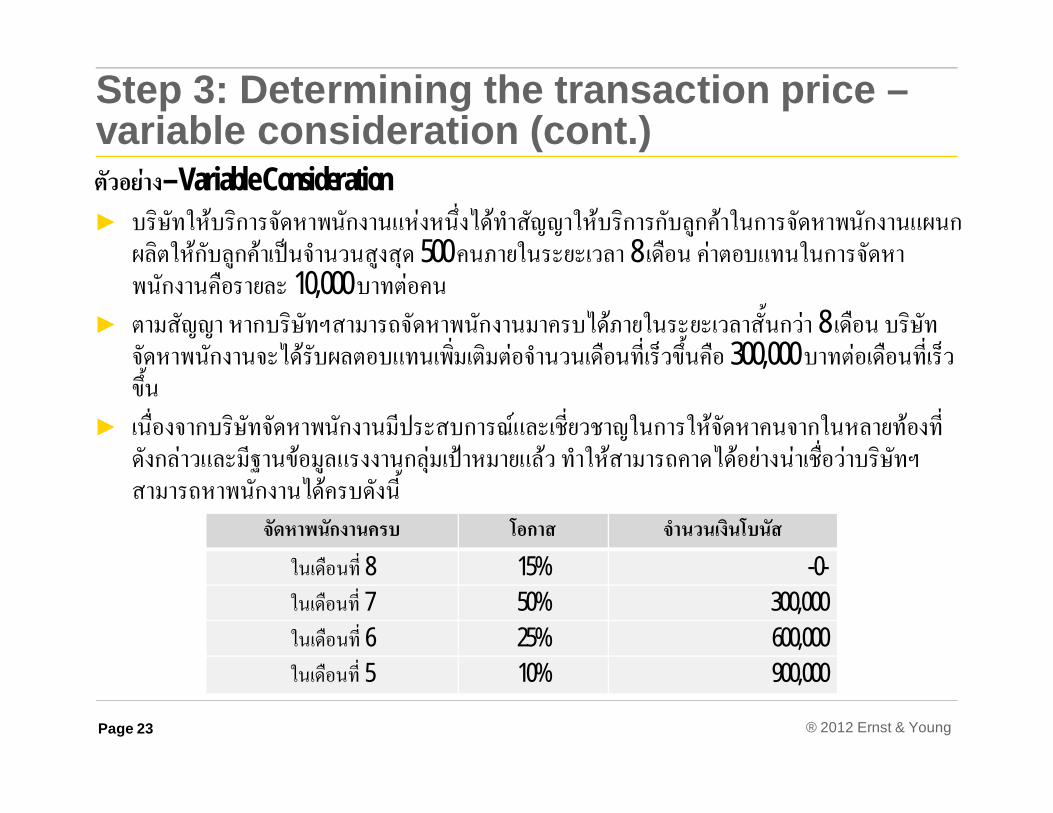

Step 3: Determining the transaction price –variable consideration (cont.)

– Variable Consideration

500 8 10,000

8 300,000

8 15% -0-

7 50% 300,000

6 25% 600,000

5 10% 900,000

Page 24 ® 2012 Ernst & Young

Step 3: Determining the transaction price –variable consideration (cont.)

Expected Value Approach

1

Weighted

expected value

8 15% -0- 10,000 1,500

7 60% 300,000 10,600 6,360

6 15% 600,000 11,200 1,680

5 10% 900,000 11,800 1,180

Expected value approach 10,720

Most likely approach

300,000 ( 60%)

1 10,600

Page 25 ® 2012 Ernst & Young

Step 3: Determining the transaction price –time value of money

Reflected as an adjustment to the transaction price when significant and the primary purpose of the payment terms would be to provide financing to one party in the contract

Evaluation not required if provision of services and receipt of payment are within one year of one another

Entity would use a separate financing rate that reflects the borrower’s credit riskEffect of financing would be reflected separately from revenue

Page 26 ® 2012 Ernst & Young

Step 3: Determining the transaction price –consideration payable to the customer

Entity would determine whether amounts paid or payable to the customer are:

A reduction of the transaction price (and revenue)A payment for distinct goods and servicesA combination of the two

Page 27 ® 2012 Ernst & Young

Step 4: Allocating the transaction price

Allocate to each performance obligation based on relative standalone selling prices Estimate the standalone selling price if not directly observable

Maximise use of observable inputsApply estimation methods consistently for goods and services, and customers with similar characteristicsUse of a residual technique may be appropriate when prices are highly variable or uncertain

Transaction price is not reallocated for subsequent changes in standalone selling prices

Page 28 ® 2012 Ernst & Young

Step 4: Allocating the transaction price (cont.)

2

100

600 60

??

Consideration

Handset 100

Wireless Plan 1,440

Total 1,540

Standalone selling price

350

1,4401,790

Allocate Transaction Price

301

1,2391,540

Page 29 ® 2012 Ernst & Young

Step 4: Allocating the transaction price (cont.)

100

Dr. 100

Cr. 100

)

Dr. 60

Cr. 60

Exposure Draft

100

Dr. 100

Contract Asset 201

Cr. 301

)

Dr. 60.0

Cr. Contract Asset 8.4

51.6

Page 30 ® 2012 Ernst & Young

Step 5: Recognising revenue

Revenue is recognised When (or as) a performance obligation is satisfiedWhen (or as) the customer obtains control of a good or service.

Control of a performance obligation transfers either over time or at a point in time.

Page 31 ® 2012 Ernst & Young

Step 5: Recognising revenue – constraint on variable consideration

Recognition of variable consideration limited to amounts reasonably assured to be entitledAmounts are reasonably assured when:

The entity has experience with similar types of performance obligation (or other persuasive evidence); andThe entity’s experience is predictive of amount of consideration to which the entity will be entitledLicences of intellectual property - revenue based on customer’s subsequent sales (e.g., a sales-based royalty) is not reasonably assured until the uncertainty is resolved

Revenue from Contracts with Customers Agenda

Overview and project statusKey messages for telecom companiesThe five-step model Other aspects of the model Implementation issues

Page 33 ® 2012 Ernst & Young

Onerous performance obligations

Applies to performance obligations satisfied over time If, at inception, the entity expects the period to satisfaction to be greater than one year.

Onerous if:Lowest cost of settling* > allocated transaction price

* Lowest cost of settling is the lower of below 2 itemsa) costs directly related to satisfying the performance obligation b) cost to exit

Page 34 ® 2012 Ernst & Young

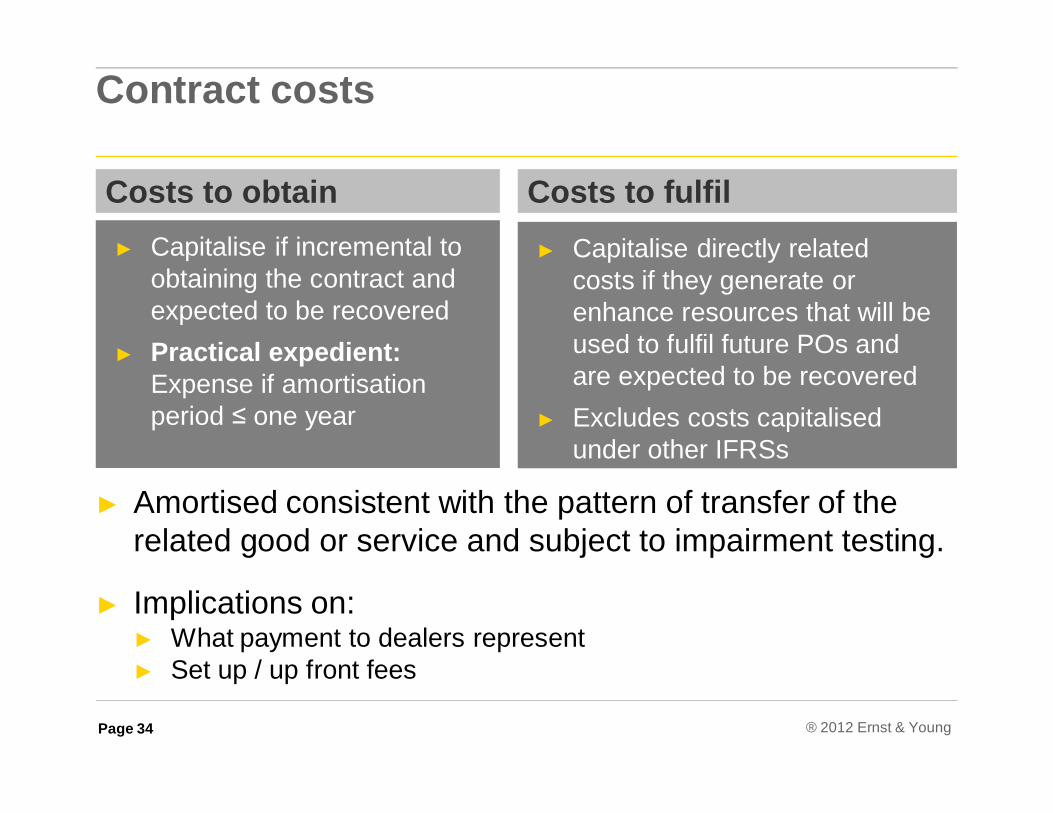

Contract costs

Amortised consistent with the pattern of transfer of the related good or service and subject to impairment testing.

Implications on:What payment to dealers represent Set up / up front fees

Costs to obtain Costs to fulfilCapitalise if incremental to obtaining the contract and expected to be recoveredPractical expedient: Expense if amortisation period one year

Capitalise directly related costs if they generate or enhance resources that will be used to fulfil future POs and are expected to be recovered Excludes costs capitalised under other IFRSs

Page 35 ® 2012 Ernst & Young

Breakage

Customer may make non-refundable prepayments to an entity for the right to receive future goods or servicesUnexercised rights are referred to as breakage

• Revenue would be recognised in proportion to pattern of rights exercised by customer

If an entity is reasonably assured of breakage amount

• Revenue would be recognised when the likelihood of exercising rights becomes remote

If an entity is notreasonable assured of breakage amount

Page 36 ® 2012 Ernst & Young

Bill-and-hold arrangements

Following criteria must be met to recognise revenue:The customer must have requested the contract to be on a bill-and-hold basisThe product must be identified separately as the customer’sThe product currently must be ready for delivery at the location and time specified, or to be specified, by the customerThe entity cannot use the product or sell it to another customer

The entity would also have to consider whether the custodial services are a material performance obligation to which some of the transaction price should be allocated

Page 37 ® 2012 Ernst & Young

Disclosure

Key principleTo help users of financial statements understand the amount, timing and uncertainty of revenue and cash flows arising from contracts with customers

Present both qualitative and quantitative information about:

Contracts with customersSignificant judgements and changes in judgements made in applying the requirements to those contractsAssets recognised from costs to obtain or fulfil a contract

Page 38 ® 2012 Ernst & Young

Disclosure (cont.)

Information about contracts with customersDisaggregation of revenueNature of performance obligations and additional information about onerous performance obligationsMaturity analysis if remaining performance obligations in contracts with original duration of more than a yearReconciliation from opening to closing total contract balances

Information about judgements and changes in judgements

Timing of revenue recognitionDetermining and allocating the transaction price

Revenue from Contracts with Customers Agenda

Overview and project statusKey messages for telecom companiesThe five-step model Other aspects of the model Implementation issues

Page 40 ® 2012 Ernst & Young

Implementation issues

Many current accounting systems do not have the capability to account for numerous individual contracts.Some information required by the proposal is not tracked by billing systems. Examples:

They do not track when a customer entered into a contract or when the contract expires.They do not hold information about stand-alone selling prices

To accurately account for for individual contracts billing and accounting systems are likely to require extensive and costly changes that would take a considerable period of time to implement.Continue to monitor the Boards’ deliberations (Last quarter of 2012)

End