Council Initiated Investigation

CDM Contract Compliance Report

Felton Financial Forensics, LLC

5200 Tifton Drive, Minneapolis, MN 55439 Phone: 612.490.1940

www.feltonforensics.com

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Table of Contents

I. Executive Summary ............................................................................................................................... 1

II. Background ........................................................................................................................................... 2

III. CDM Noncompliant Contract Findings ............................................................................................. 3

A. Non-Allowable Expenses ................................................................................................................... 3

IV. Conclusion ....................................................................................................................................... 12

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 1

I. Executive Summary

The Honorable Jannquell Peters, Mayor

The Honorable Sharon Shropshire, Council Member, Ward A – At Large

The Honorable Alexander Gothard, Council Member, Ward A

The Honorable Karen René, Council Member, Ward B – At Large

The Honorable Lance Rhodes, Council Member, Ward B

The Honorable Nanette Saucier, Council Member, Ward C – At Large

The Honorable Myron B. Cook, Council Member, Ward C

The Honorable Deana Holiday-Ingraham, Council Member, Ward D – At Large

The Honorable LaTonya Martin, Council Member, Ward D

Dear Honorable Mayor and Council Members:

The City Council retained me to prepare a report on the results of the following Council Initiated

Investigation – Phase II Tasks:

1. Test CDM Smith’s Capital Project Program Billings Compliance with Contract Terms.

2. Test the 59 Missing Boxes Containing Paid Vendor Invoices for Compliance with the City’s

Procurement Code and Policies.

Detailed findings are in the report body. I prepared a separate report for the missing boxes, due to

the length of the report. This report dated May 12, 2014 and titled Council Initiated Investigation

– Missing Boxes Report was previously submitted.

I would like to thank the current mayor and council members, as well as the former mayor

Earnestine D. Pittman, and former council members Sharonda D. Hubbard, Pat Langford, Marcel

L. Reed, and Jackie Slaughter-Gibbons, for this opportunity to serve them and the East Point

residents.

I would also like to thank senior management, the City Attorney’s Office, the Procurement

Office, the East Point staff, and the City’s outside legal counsel, Randy Turner, for their help and

support during Phases I and II of the Council Initiated Investigation.

Respectfully,

Mark A. Felton, CPA, CFE, MAFF, CVA, MBA

Felton Financial Forensics and Valuations, LLC

cc: Ellis Mitchell, Interim City Manager

Brad Bowman, Acting City Attorney

Randy Turner, Esq., Turner & Ross, LLC.

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 2

II. Background

In late summer 2012, a City of East Point employee contacted the new city attorney, Corliss

Lawson, and alleged certain improprieties in the City of East Point’s bidding and procurement

process. Based upon this initial allegation an investigation was conducted, which included

reviews of relevant records and interviews of appropriate personnel.

In a report dated June 3, 2013, I provided my results to the Mayor, City Council and City

Attorney. I also presented the results at the July 1, 2013 City Council Meeting. Based on these

report results, the Council in its July 1, 2013 Executive Session authorized Phase II of the Council

Initiated Investigation, and directed the City Attorney to negotiate the scope and agreement terms

with my firm, Felton Financial Forensics.

Former City Attorney Corliss Lawson and I agreed my firm would perform the following:

1. Examine and validate the accuracy of all Camp, Dresser & McKee, Inc. (herein referred

to as CDM Smith) billings related to the Capital Improvement Program.

2. Examine and report on the contents of 59 missing boxes paid vendor invoices located

July 9, 2013 by city staff.

My CDM Smith billings finding summary is:

Based on my reading of the contract between the City of East Point and CDM dated

September 6, 2006, non-allowable contract expenses appeared on CDM Smith billing

invoices to the City of East Point. In the almost seven-year contract period, these non-

allowable expenses totaled $5,390.88.

My findings of the 59 missing boxes of paid vendor invoices contents are: (Note: See my

separate confidential report on the missing boxes dated May 12, 2014.)

1. Prohibited Capital Expenditures.

2. Travel and Other Expenditures without Proper Documented Justification.

3. City’s Credit Card Used for Personal Purchases.

4. Miscellaneous Purchase with Incomplete or No Documented Business Purpose.

My detailed findings are presented in the body of this report.

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 3

III. CDM Noncompliant Contract Findings

A. Non-Allowable Expenses

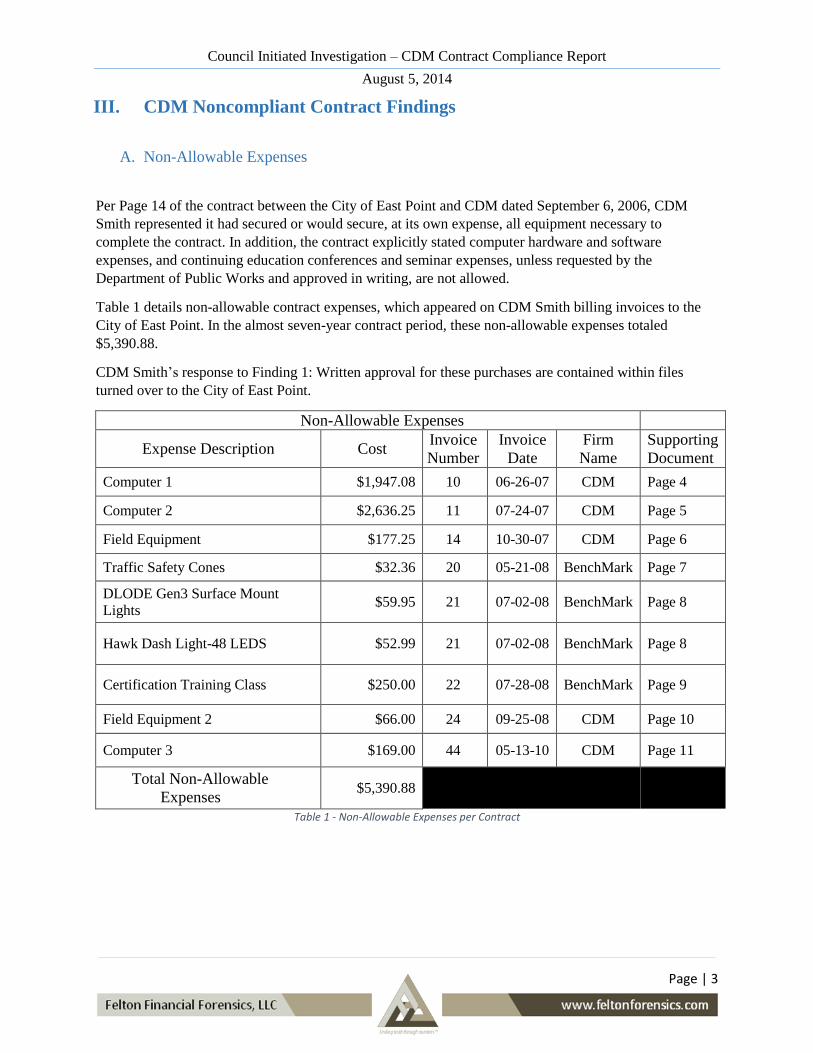

Per Page 14 of the contract between the City of East Point and CDM dated September 6, 2006, CDM

Smith represented it had secured or would secure, at its own expense, all equipment necessary to

complete the contract. In addition, the contract explicitly stated computer hardware and software

expenses, and continuing education conferences and seminar expenses, unless requested by the

Department of Public Works and approved in writing, are not allowed.

Table 1 details non-allowable contract expenses, which appeared on CDM Smith billing invoices to the

City of East Point. In the almost seven-year contract period, these non-allowable expenses totaled

$5,390.88.

CDM Smith’s response to Finding 1: Written approval for these purchases are contained within files

turned over to the City of East Point.

Non-Allowable Expenses

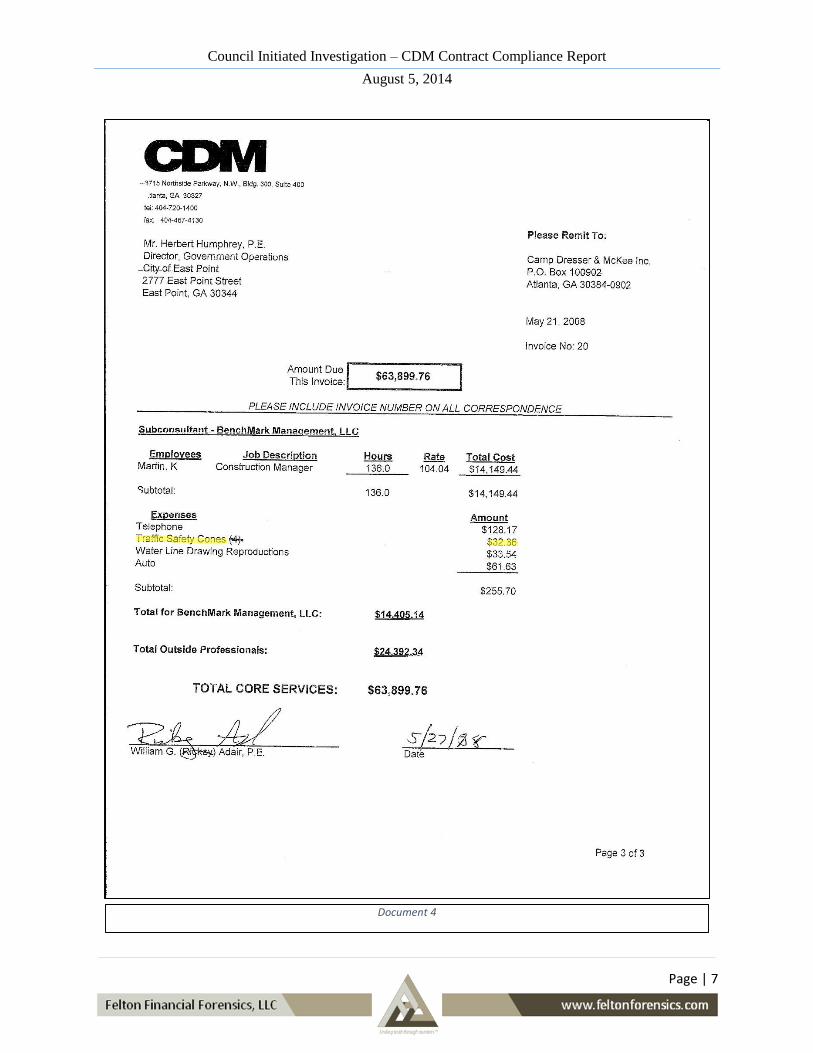

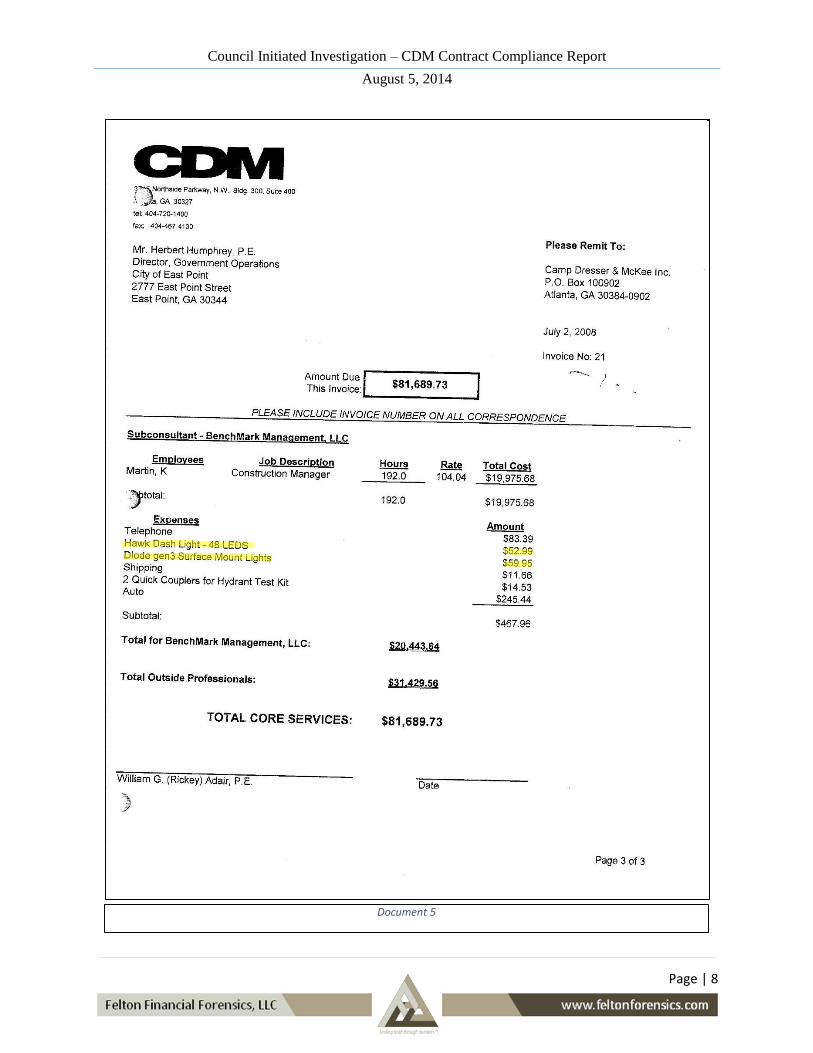

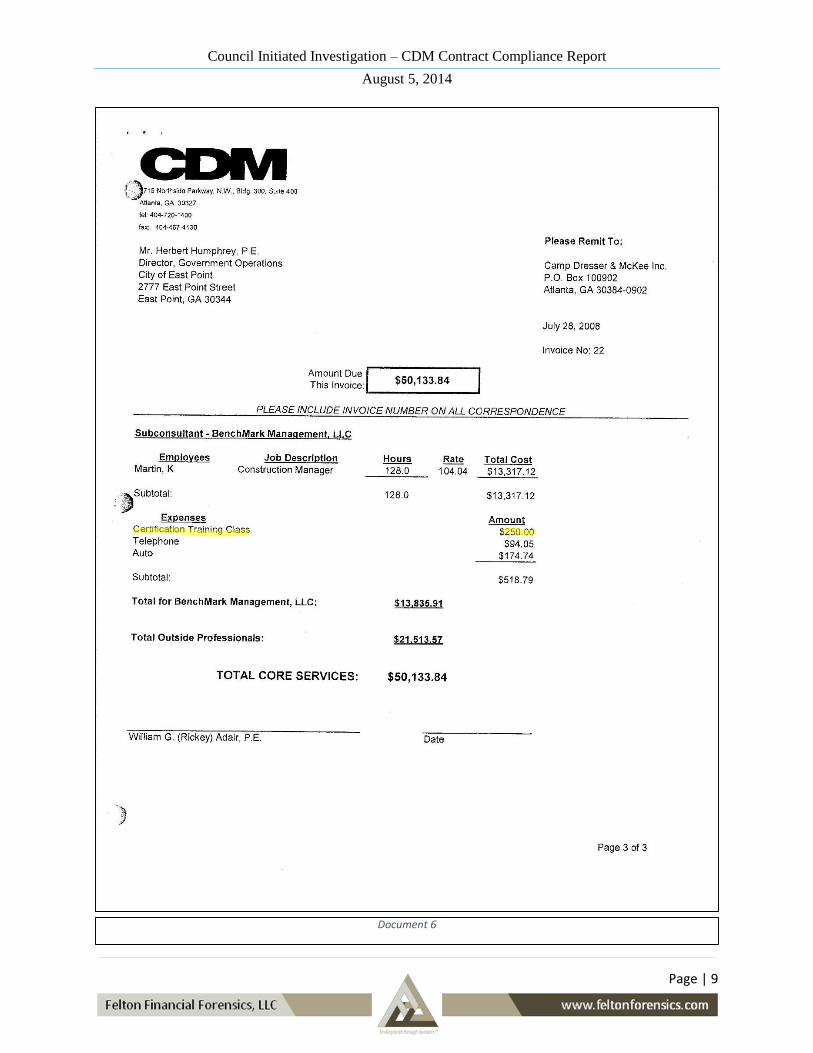

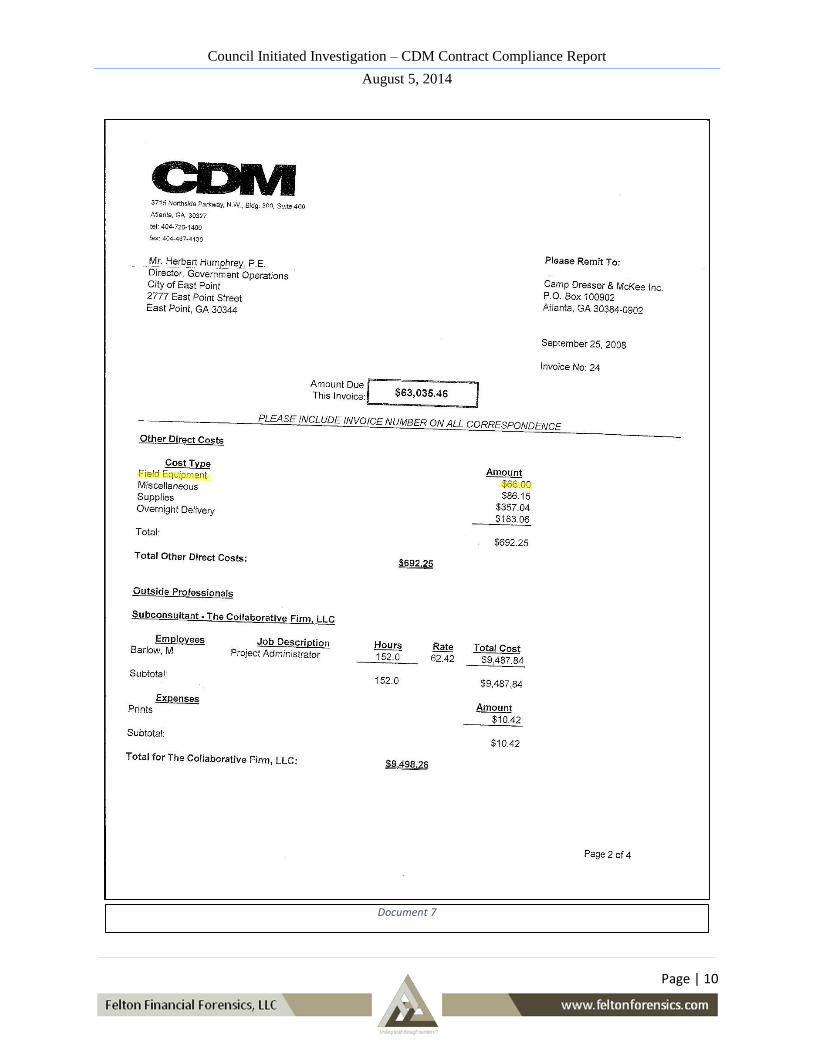

Expense Description Cost Invoice

Number

Invoice

Date

Firm

Name

Supporting

Document

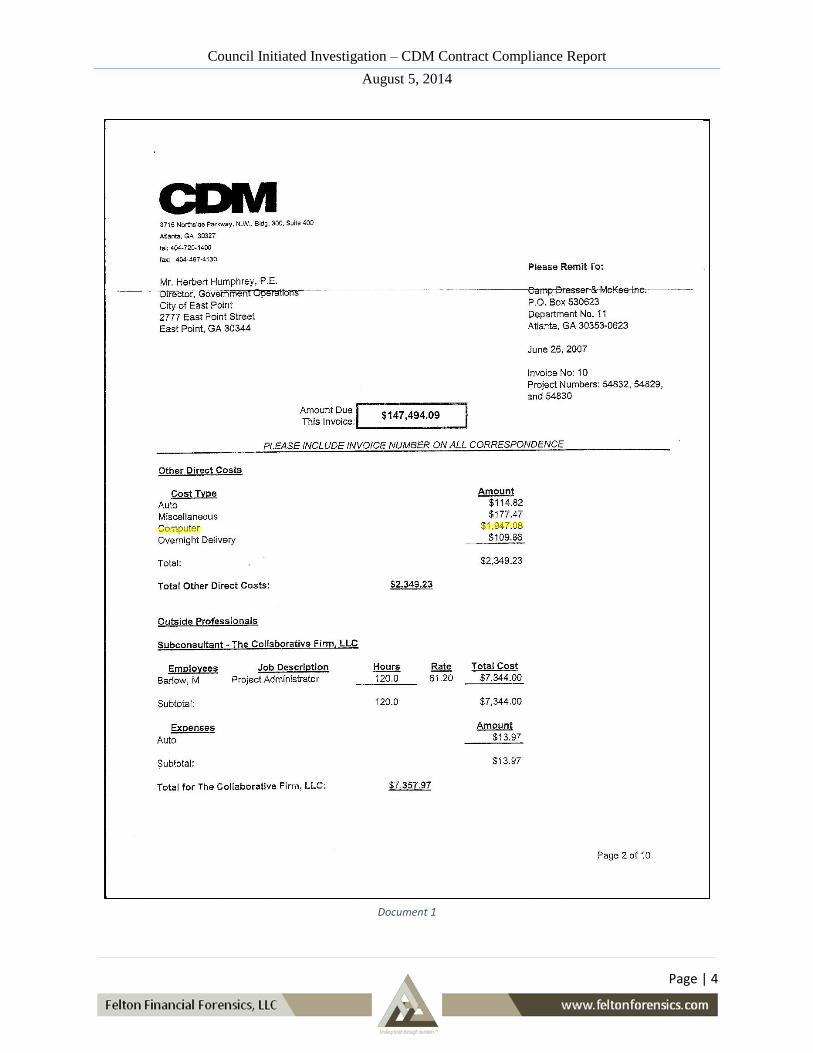

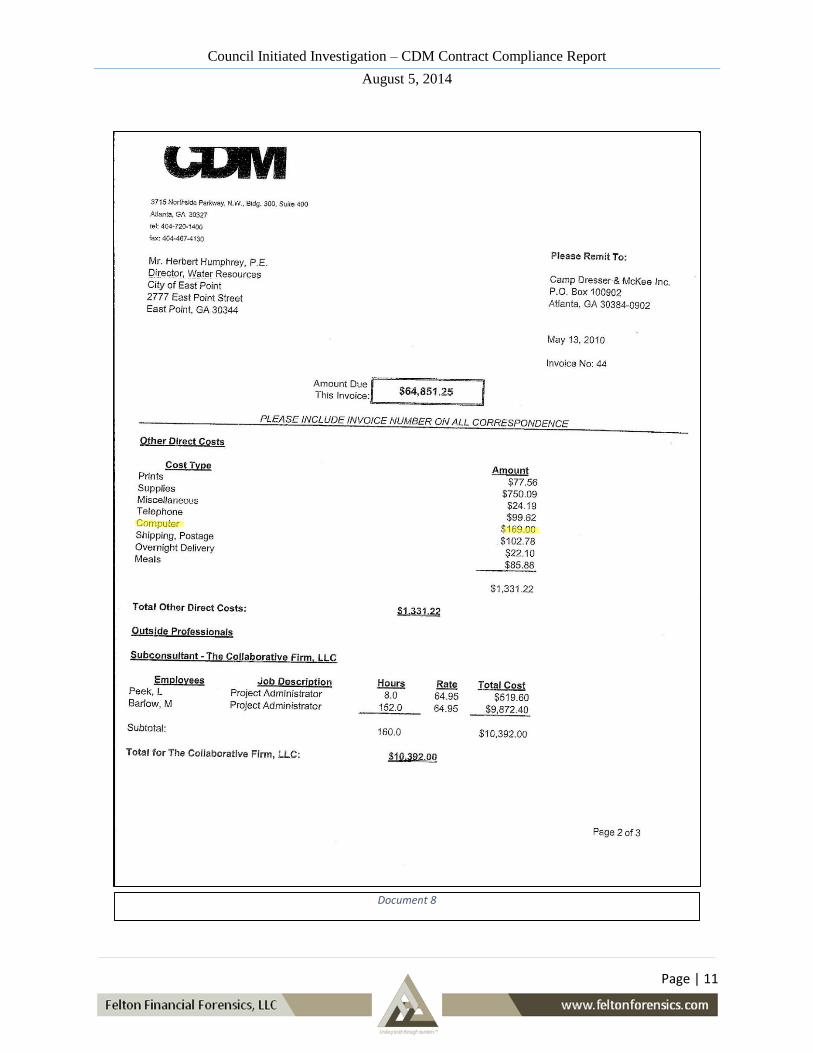

Computer 1 $1,947.08 10 06-26-07 CDM Page 4

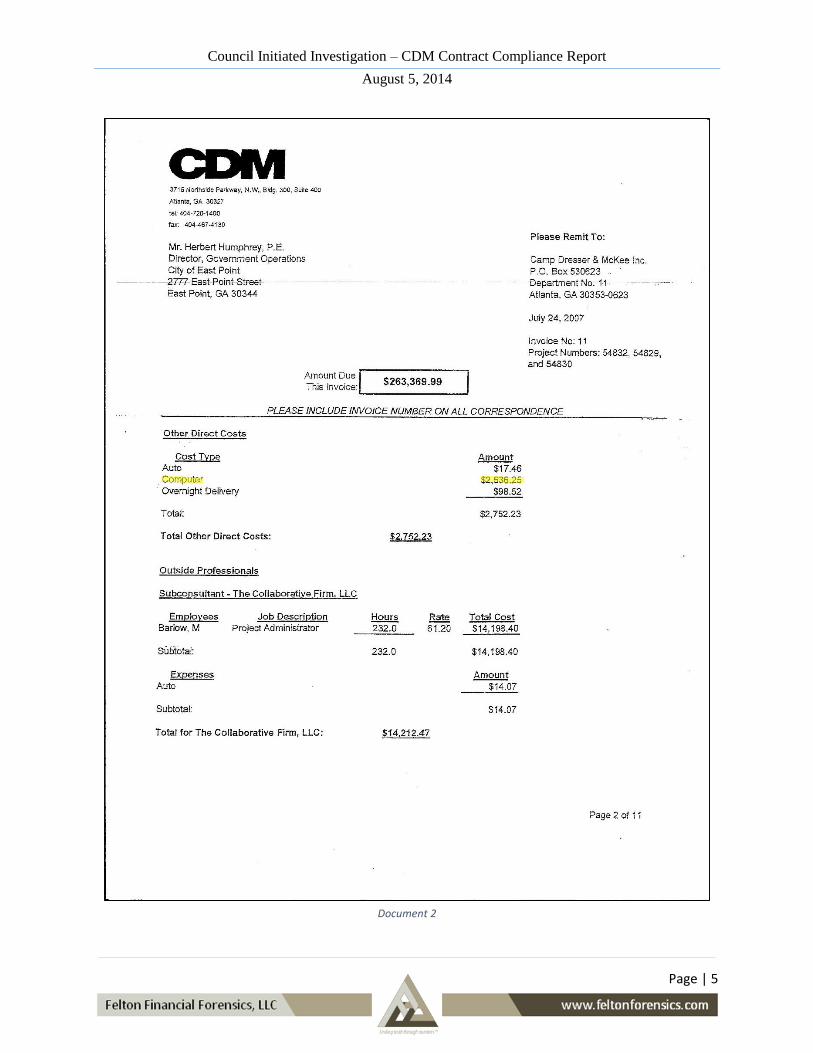

Computer 2 $2,636.25 11 07-24-07 CDM Page 5

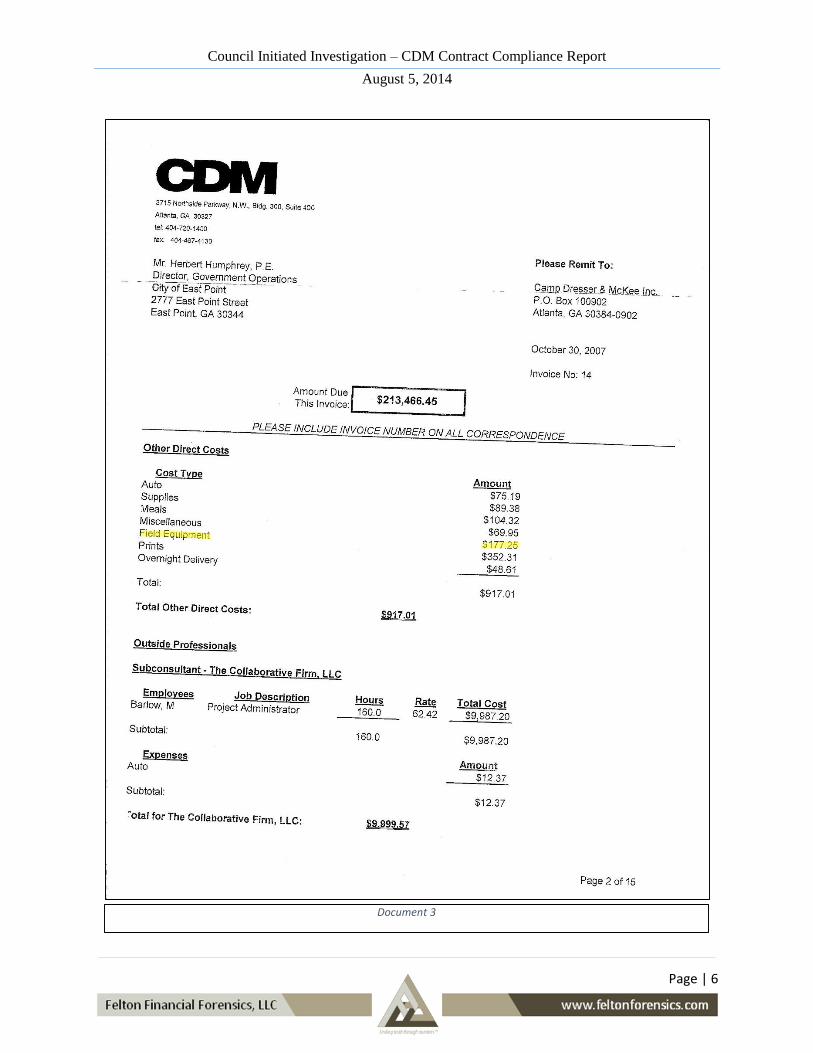

Field Equipment $177.25 14 10-30-07 CDM Page 6

Traffic Safety Cones $32.36 20 05-21-08 BenchMark Page 7

DLODE Gen3 Surface Mount

Lights $59.95 21 07-02-08 BenchMark Page 8

Hawk Dash Light-48 LEDS $52.99 21 07-02-08 BenchMark Page 8

Certification Training Class $250.00 22 07-28-08 BenchMark Page 9

Field Equipment 2 $66.00 24 09-25-08 CDM Page 10

Computer 3 $169.00 44 05-13-10 CDM Page 11

Total Non-Allowable

Expenses $5,390.88

Table 1 - Non-Allowable Expenses per Contract

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 4

Document 1

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 5

Document 2

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 6

Document 3

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 7

Document 4

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 8

Document 5

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 9

Document 6

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 10

Document 7

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 11

Document 8

Council Initiated Investigation – CDM Contract Compliance Report

August 5, 2014

Page | 12

IV. Conclusion

I have concluded my work on Phases I and II of the Council Initiated Investigation.

Summary findings for both phases are listed below.

Phase I Summary Findings of the Council Initiated Investigation:

1. Invoices were paid without properly approved requisitions and purchase orders.

2. Artificial division of invoices was used to circumvent procurement purchasing

threshold requirements.

3. “Field” purchase orders were improperly used.

4. Vendor payments were under reported.

5. Some invoices were paid twice.

Phase II Summary Findings of the Council Initiated Investigation:

1. Non-allowable expenses, as defined by the contract dated September 6, 2006

between the City of East Point and CDM Smith, appeared on CDM Smith invoice

billings to the City of East Point.

I thank the management and City Staff for their assistance and courtesies extended throughout

this Council Initiated Investigation.