Canterbury Procurement ForumThe forward pipeline – fifth edition – November 2013

Content

• National Pipeline – initial results• Auckland Pipeline – making the two regional reports look similar• Canterbury Pipeline – next iteration of the data and commentary on

how this data compares with the National Pipeline

• See previous versions of the Canterbury pipeline for a description of the method and major assumptions for the data presented here.

National Pipeline

National Pipeline

Two pronged approach in analysis:

Bottom up – Pacifecon “known” projects based on leads detected from a national network of analysts (and corroborated with Auckland and Christchurch pipeline data sets)

Top down BRANZ “economic forecast” based on modelling of historic building consents and economic data for residential construction and their approach to modelling gross fixed capital formation

High level results:

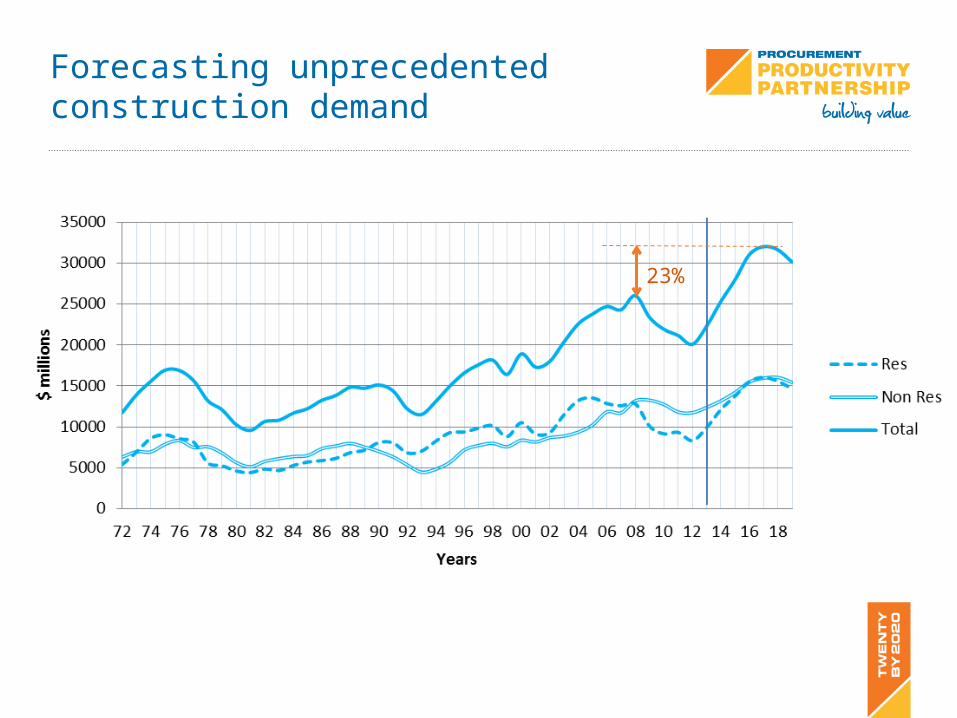

Forecasting an unprecedented level of building and construction activity

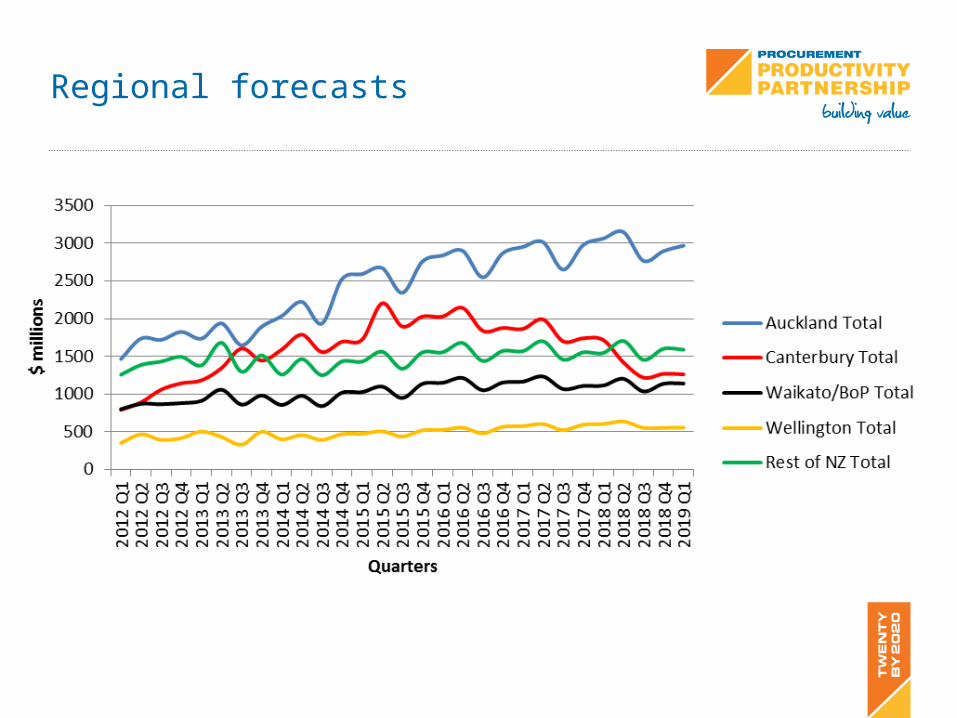

Peaking in 2016 nationally – 2016 in Canterbury

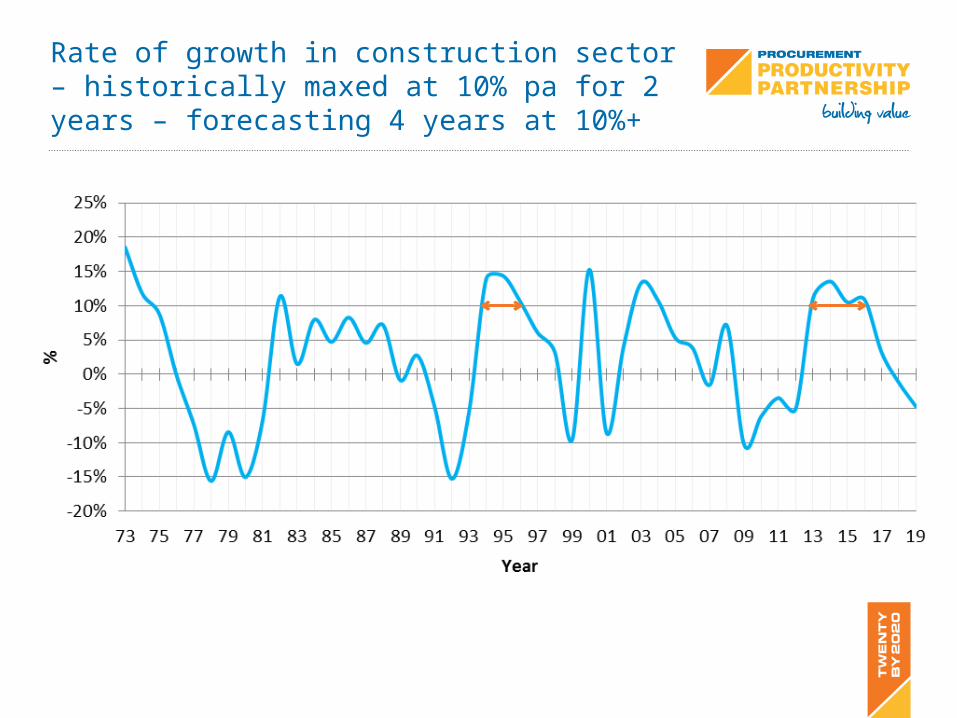

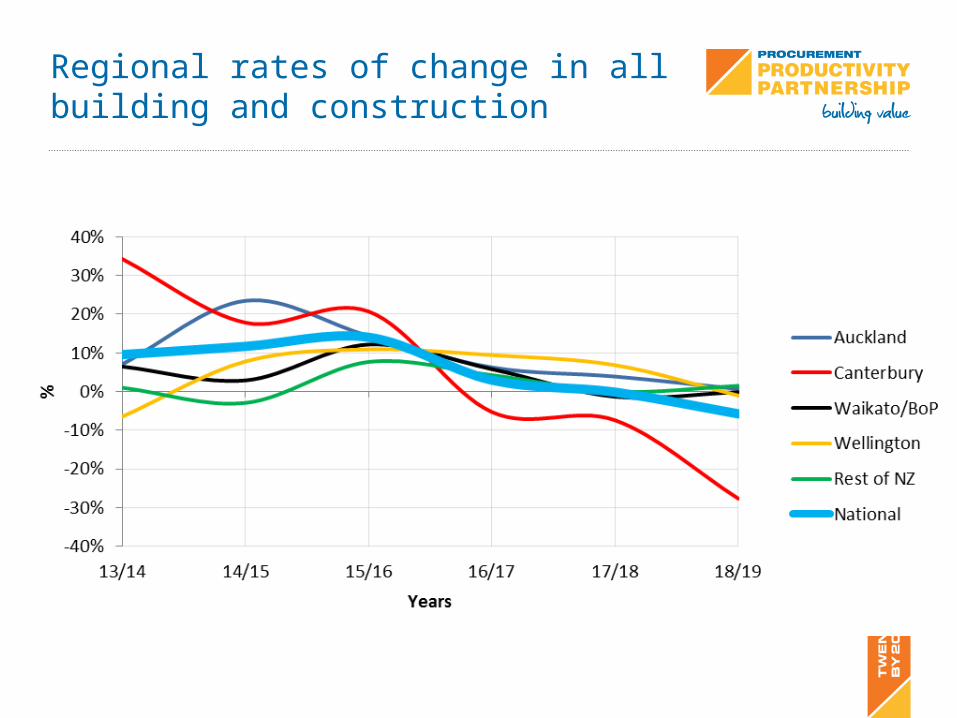

Forecast rate of growth in construction also very high in comparison with historic rates – haven’t seen rate of growth for as long in past 40 years.

Auckland the largest and fastest growing region – 150% increase in residential building over the forecast period

Forecasting unprecedented construction demand

23%

Rate of growth in construction sector – historically maxed at 10% pa for 2 years – forecasting 4 years at 10%+

Regional forecasts

Regional rates of change in all building and construction

Auckland Pipeline

Connections between the two procurement fora

Auckland pipeline report

Intention to make both reports more comparable, where useful and possible

Canterbury Pipeline

Updated this report for easy to make changes to align with the Auckland pipeline report

Note – key differences between the three pipelines. Auckland and national pipeline are most directly comparable with Stats NZ ‘fixed capital formation’ – this is about 2x higher than the Canterbury pipeline which is most comparable with the ‘building work put in place’ series.

Key difference is fixed capital formation accounts for non-building construction – and construction related costs such as legal fees, planning and consent costs etc.

Canterbury Pipeline

Contributing organisation and sector distribution

Vertical or Horizontal Sector OrganisationVertical Central Government Ministry of Justice

CERA

Hospitals Canterbury District Health BoardMinistry of Health

Education Ministry of EducationUniversity of Canterbury

Residential Housing New ZealandPMOs

Vertical and Horizontal Transport Lyttleton Port CompanyChristchurch International Airport Ltd

Urban redevelopment

CERAChristchurch City Council

Horizontal Horizontal – including roads, water, waste water, electricity

SCIRTSelwyn District CouncilWaimakariri District Council

Roading (including bridges) NZTAChristchurch City CouncilSelwyn District CouncilWaimakariri District Council

Construction Intentions

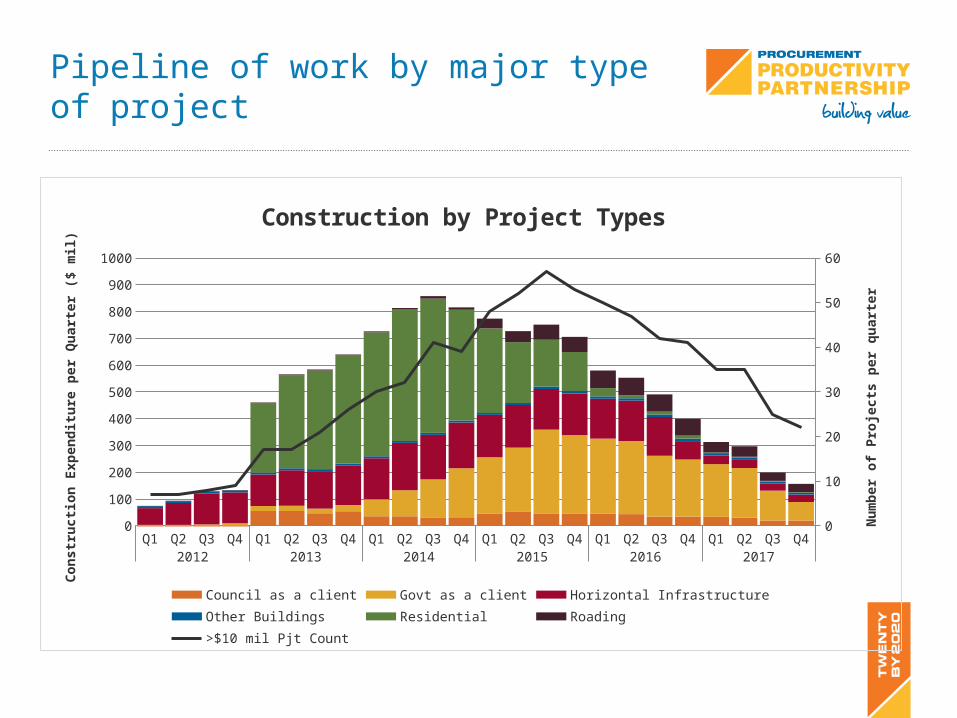

Pipeline of work by major type of project

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42012 2013 2014 2015 2016 2017

0

100

200

300

400

500

600

700

800

900

1000

0

10

20

30

40

50

60

Construction by Project Types

Council as a client Govt as a client Horizontal Infrastructure Other BuildingsResidential Roading >$10 mil Pjt Count

Cons

truc

tion

Expe

nditu

re p

er Q

uart

er ($

mil)

Num

ber o

f Pro

ject

s per

qua

rter

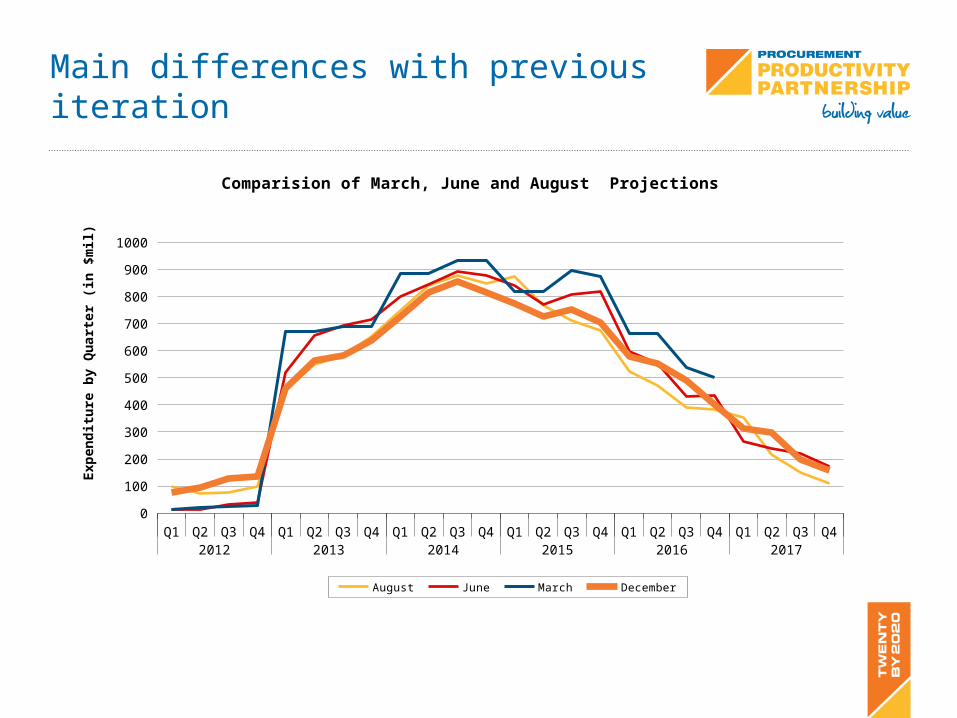

Main differences with previous iteration

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42012 2013 2014 2015 2016 2017

0

100

200

300

400

500

600

700

800

900

1000

Comparision of March, June and August Projections

August June March December

Exp

end

itu

re b

y Q

uar

ter

(in

$m

il)

Comment on major sources of difference between this and the August report

Education peak about 2 years later than previous version, and longer and lower (by $15m) per quarter (taken $195m out of peak between mid 2014 and end of 2015)

CERA – project values lower and a later peak (6 months)

SCIRT – data correction regarding start of financial year. This has reduced total value of what captured by about $200m

CCC – reduced number of projects (1) and SCIRT impact – Peak shifted out by a year, and a little lower.

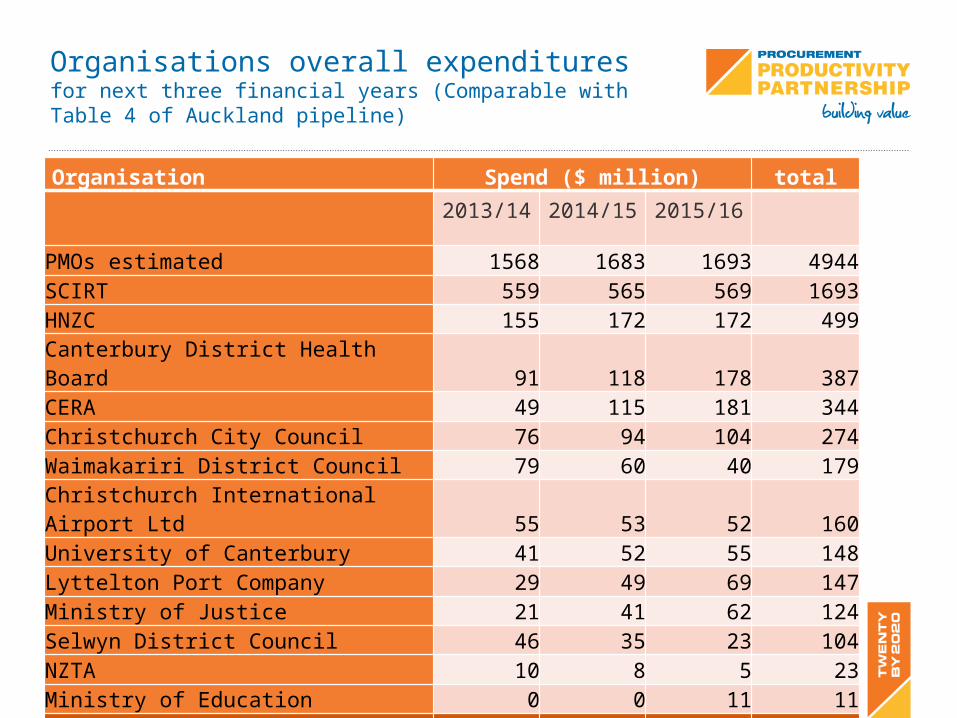

Organisations overall expenditures for next three financial years (Comparable with Table 4 of Auckland pipeline)

Organisation Spend ($ million) total2013/14 2014/15 2015/16

PMOs estimated 1568 1683 1693 4944SCIRT 559 565 569 1693HNZC 155 172 172 499Canterbury District Health Board 91 118 178 387CERA 49 115 181 344Christchurch City Council 76 94 104 274Waimakariri District Council 79 60 40 179Christchurch International Airport Ltd 55 53 52 160University of Canterbury 41 52 55 148Lyttelton Port Company 29 49 69 147Ministry of Justice 21 41 62 124Selwyn District Council 46 35 23 104NZTA 10 8 5 23Ministry of Education 0 0 11 11Total Industry Spend 2763 3037 3213 9013

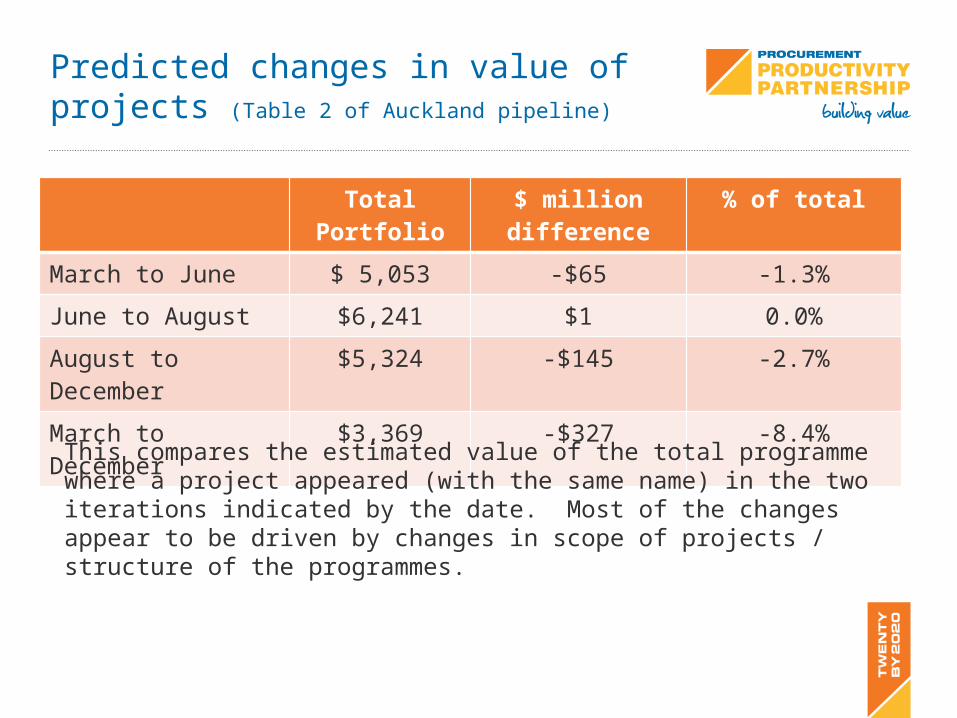

Predicted changes in value of projects (Table 2 of Auckland pipeline)

Total Portfolio $ million difference % of total

March to June $ 5,053 -$65 -1.3%

June to August $6,241 $1 0.0%

August to December $5,324 -$145 -2.7%

March to December $3,369 -$327 -8.4%

This compares the estimated value of the total programme where a project appeared (with the same name) in the two iterations indicated by the date. Most of the changes appear to be driven by changes in scope of projects / structure of the programmes.

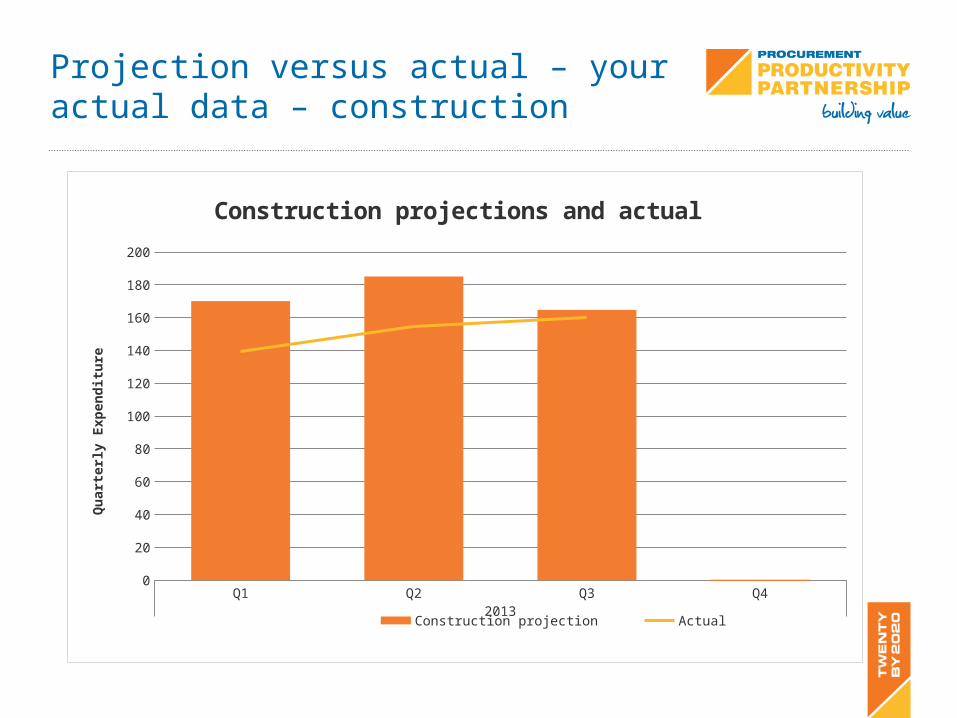

Projection versus actual – your actual data – construction

Q1 Q2 Q3 Q42013

0

20

40

60

80

100

120

140

160

180

200

Construction projections and actual

Construction projection Actual

Qua

rter

ly E

xpen

ditu

re

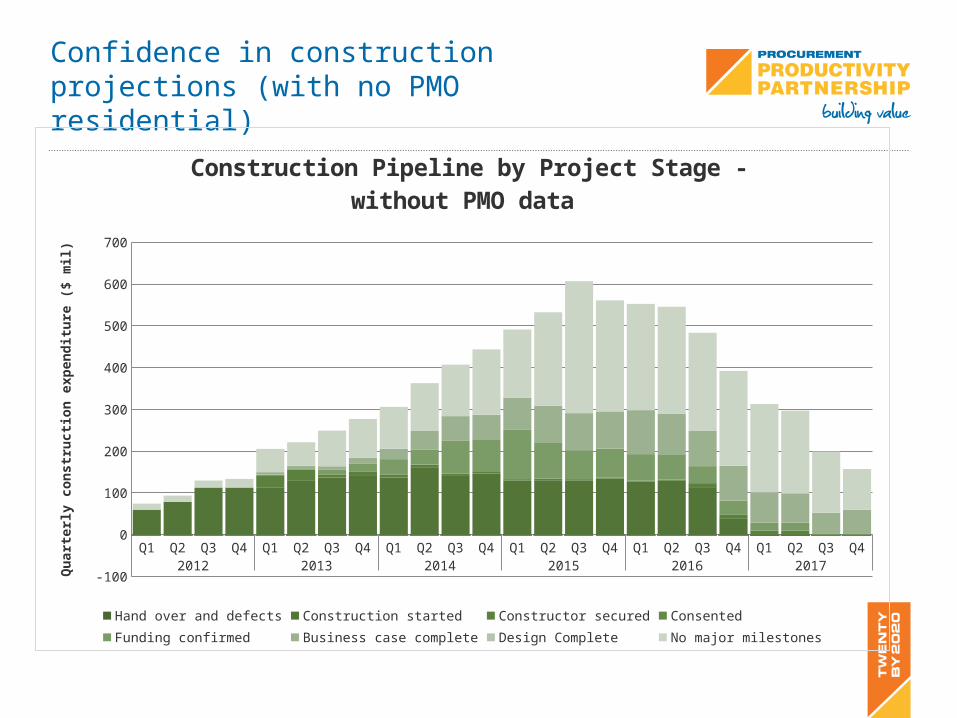

Confidence in construction projections (with no PMO residential)

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42012 2013 2014 2015 2016 2017

-100

0

100

200

300

400

500

600

700

Construction Pipeline by Project Stage - without PMO data

Hand over and defects Construction started Constructor secured ConsentedFunding confirmed Business case complete Design Complete No major milestones

Qua

rter

ly co

nstr

uctio

n ex

pend

iture

($ m

il)

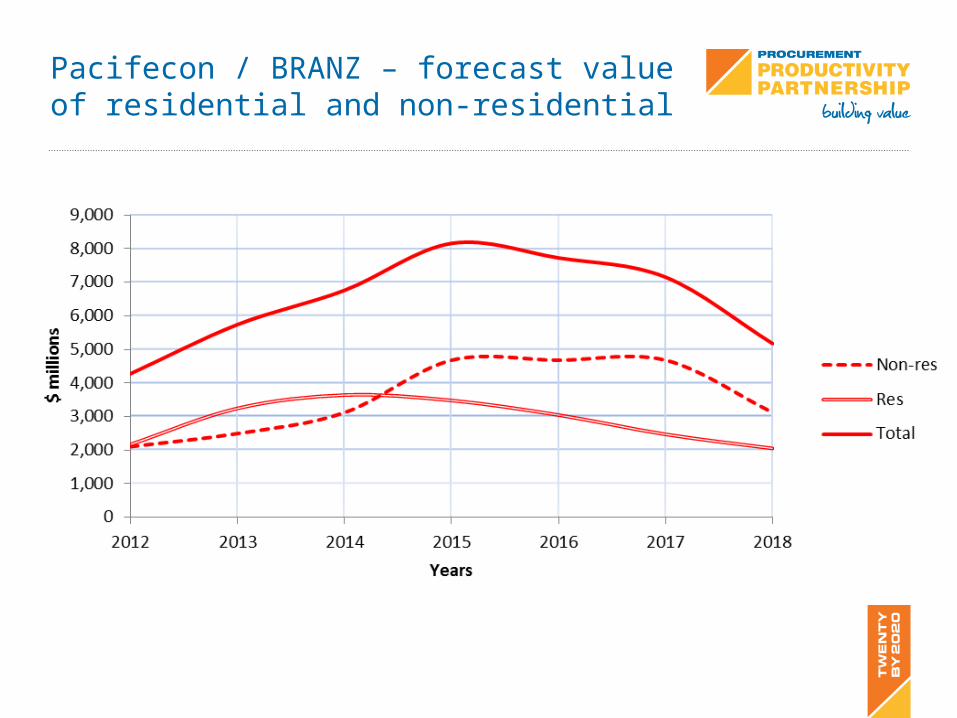

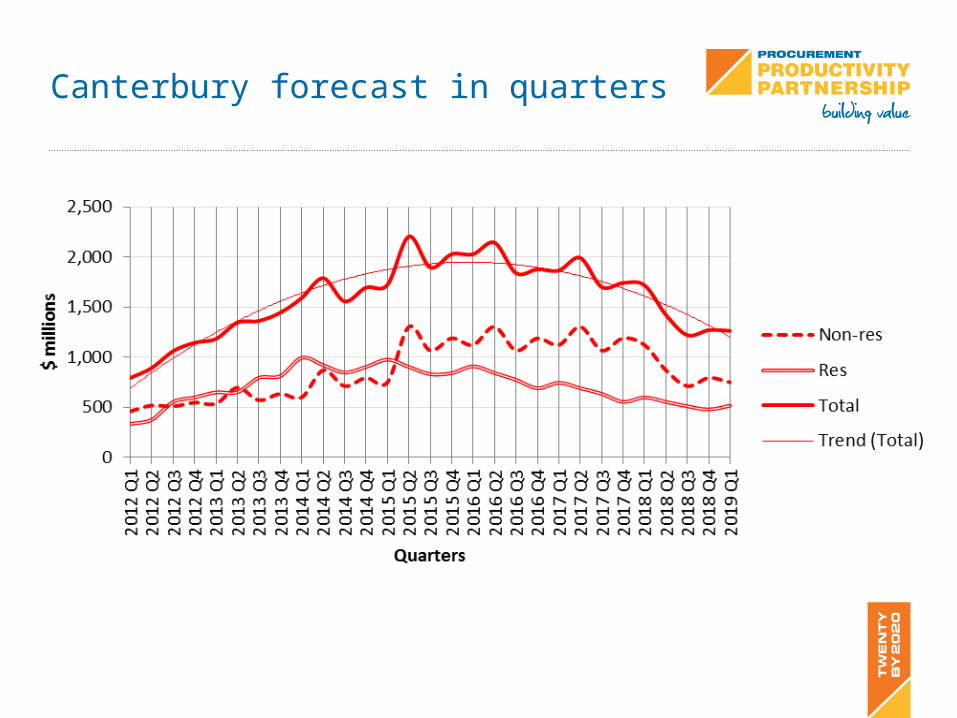

Comparison between this pipeline and the national pipeline forecast for Canterbury

Note different scales – fixed capital formation – so will be higher (by at least 2x)

Also this is annual data so need to multiply this pipeline scales by x4.

Pacifecon / BRANZ – forecast value of residential and non-residential

Canterbury forecast in quarters

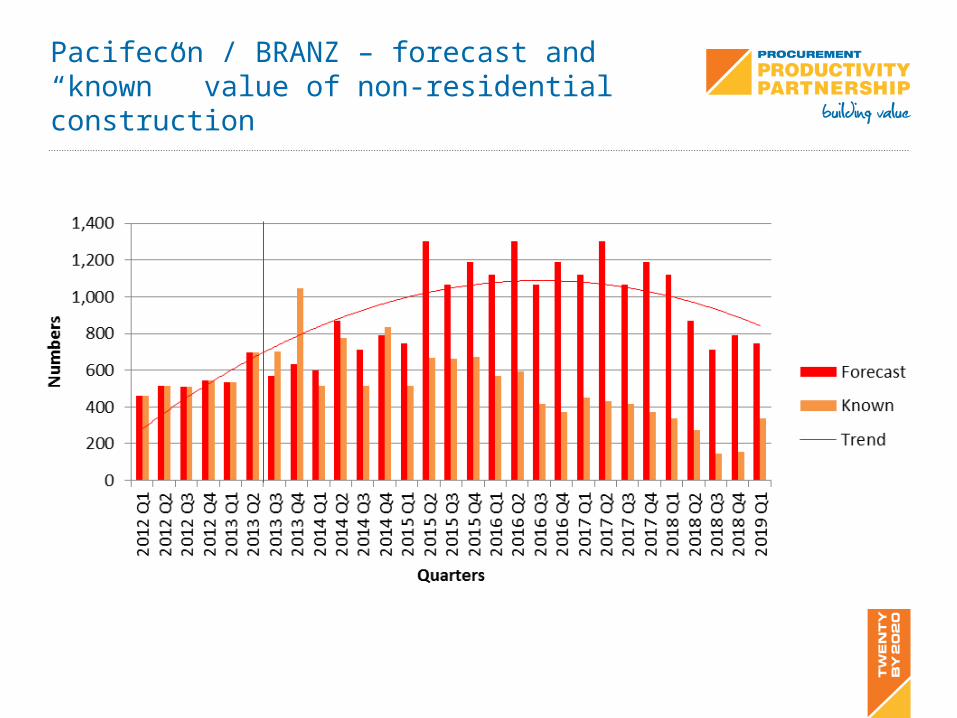

Pacifecon / BRANZ – forecast and “known” value of non-residential construction

Comparison of pipeline with building work put in place

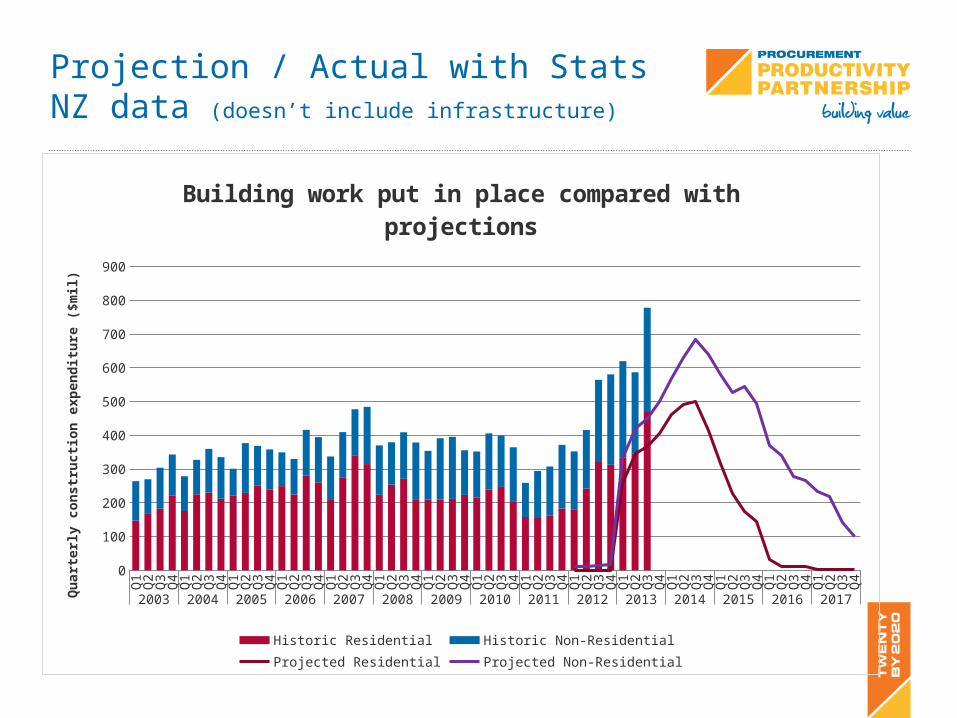

Significant step up in building work put in place for Q3 2013.

Have yet to understand any cost increases on the measured level of activity.

On average the pipeline is explaining about 80% of residential construction observed and about 1/3rd of non-residential building being done.

See previous pipelines for commentary on method for the following two slides.

Projection / Actual with Stats NZ data (doesn’t include infrastructure)

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

0

100

200

300

400

500

600

700

800

900

Building work put in place compared with projections

Historic Residential Historic Non-Residential Projected Residential Projected Non-Residential

Qua

rter

ly co

nstr

uctio

n ex

pend

iture

($m

il)

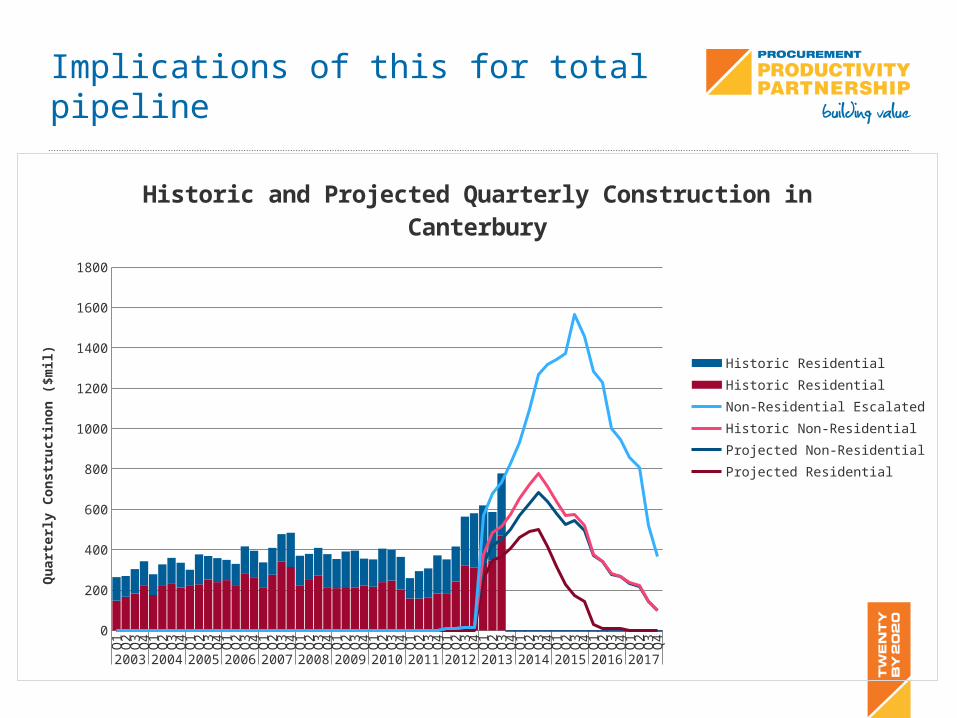

Implications of this for total pipelineQ

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

0

200

400

600

800

1000

1200

1400

1600

1800

Historic and Projected Quarterly Construction in Canterbury

Historic Non-ResidentialHistoric ResidentialNon-Residential EscalatedResidential ExcalatedProjected Non-ResidentialProjected Residential

Qua

rter

ly C

onst

ructi

non

($m

il)

Understanding the implications of S curve analysis

Previously noted that S curve analysis would affect the shape of the pipeline.

S curve would tend to generate a lower costs at beginning and end of projects and a higher peak in the middle period of a project

Following graph has ‘s curved’ every project – in reality programmes of small projects – eg SCIRT / Residential repairs by PMOs / council programmes of <$10 million may be better represented with straight line analysis

An area for further work

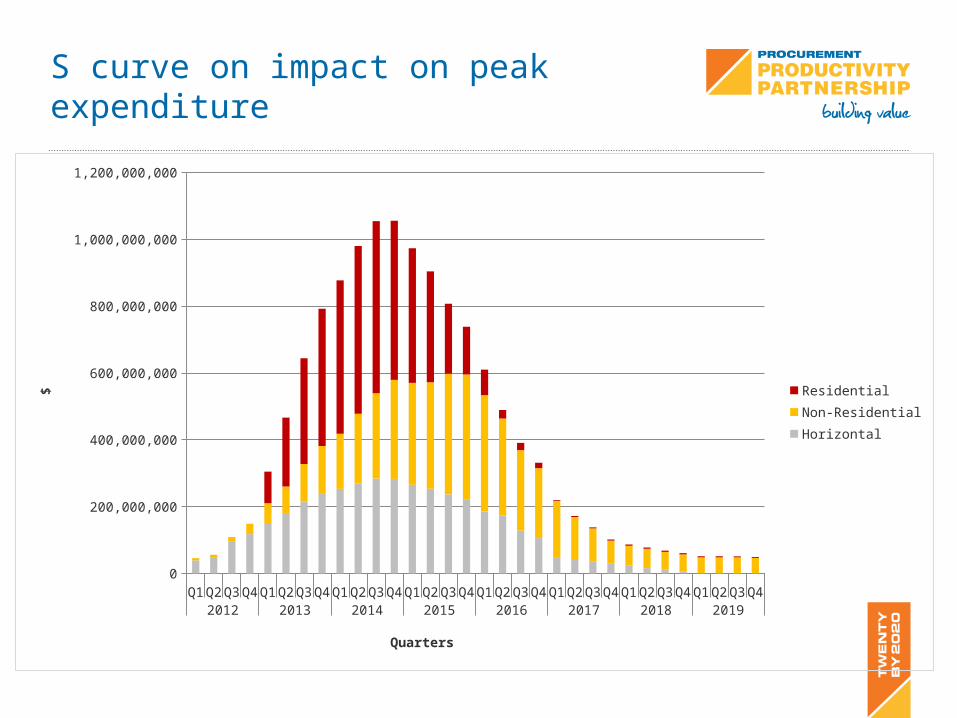

S curve on impact on peak expenditure

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42012 2013 2014 2015 2016 2017 2018 2019

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

ResidentialNon-ResidentialHorizontal

Quarters

$

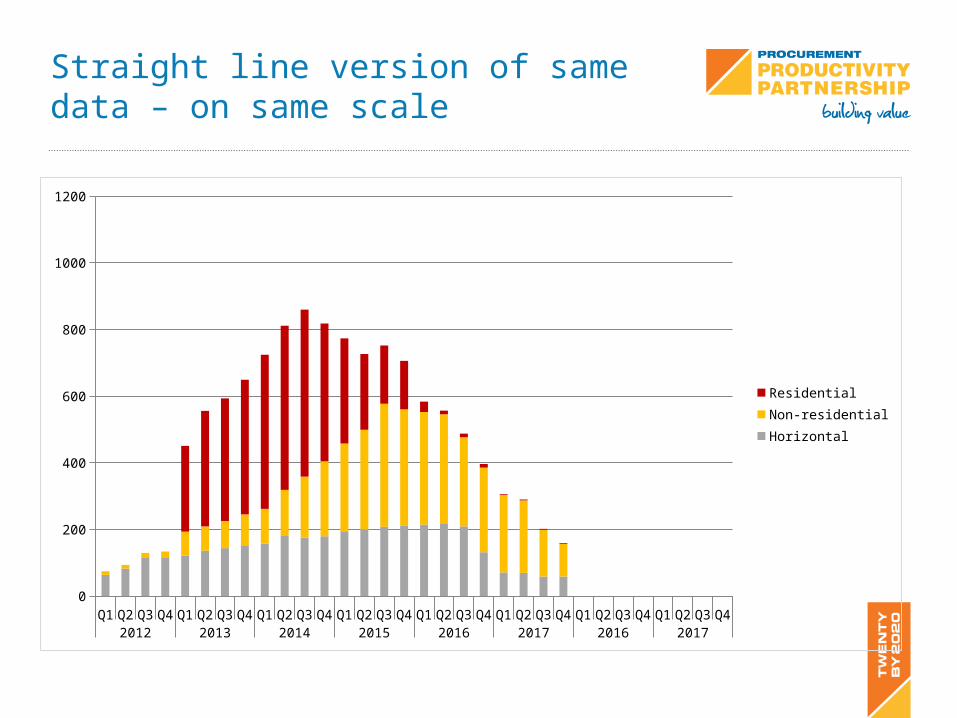

Straight line version of same data – on same scale

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42012 2013 2014 2015 2016 2017 2016 2017

0

200

400

600

800

1000

1200

ResidentialNon-residentialHorizontal

Structure of the programme based on value of projects

The following graphs are comparable with the Auckland pipeline

They are designed to demonstrate what value of work falls within low / medium and high price bands

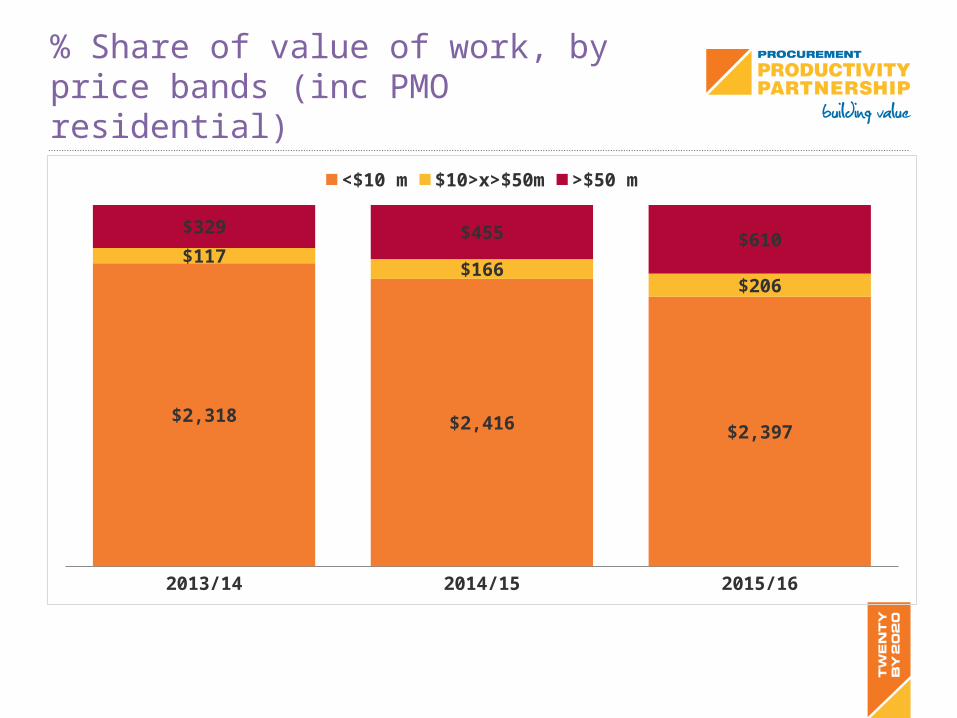

% Share of value of work, by price bands (inc PMO residential)

2013/14 2014/15 2015/16

$2,318 $2,416 $2,397

$117 $166

$206

$329 $455 $610

<$10 m $10>x>$50m >$50 m

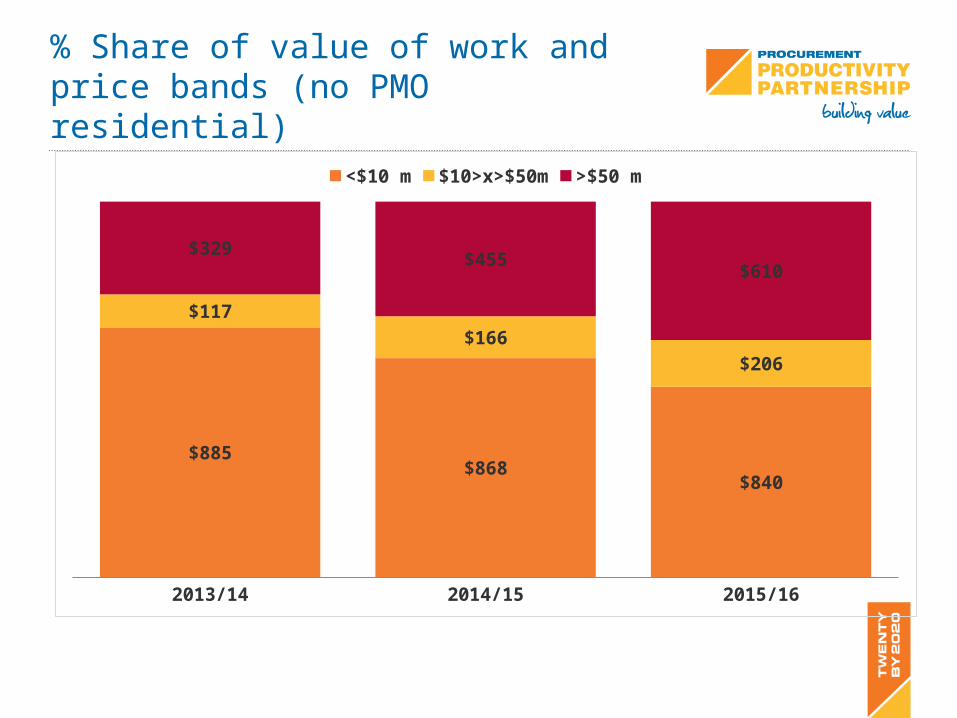

% Share of value of work and price bands (no PMO residential)

2013/14 2014/15 2015/16

$885 $868

$840

$117 $166

$206

$329 $455

$610

<$10 m $10>x>$50m >$50 m

Gantt chart analysis

These slides represent how project start dates / durations have changed across the programme.

The first slide sorts the projects by start date for construction and shows whether / how the start date has changed (and associated value in the project has changed)

Red = previous construction phase

Blue = new construction phase

Purple = construction phases overlap / no change

Interpretation

More red to the left - the more the projects have been delayed (if matched by blue – construction deferred – if not construction time contracted

The more purple – the more the project specifications haven’t changed

More blue to the left – projects start have been brought forward.

Left had column -

Darker blue = more increase in estimated cost of project

Darker red = more decrease in estimated cost of project

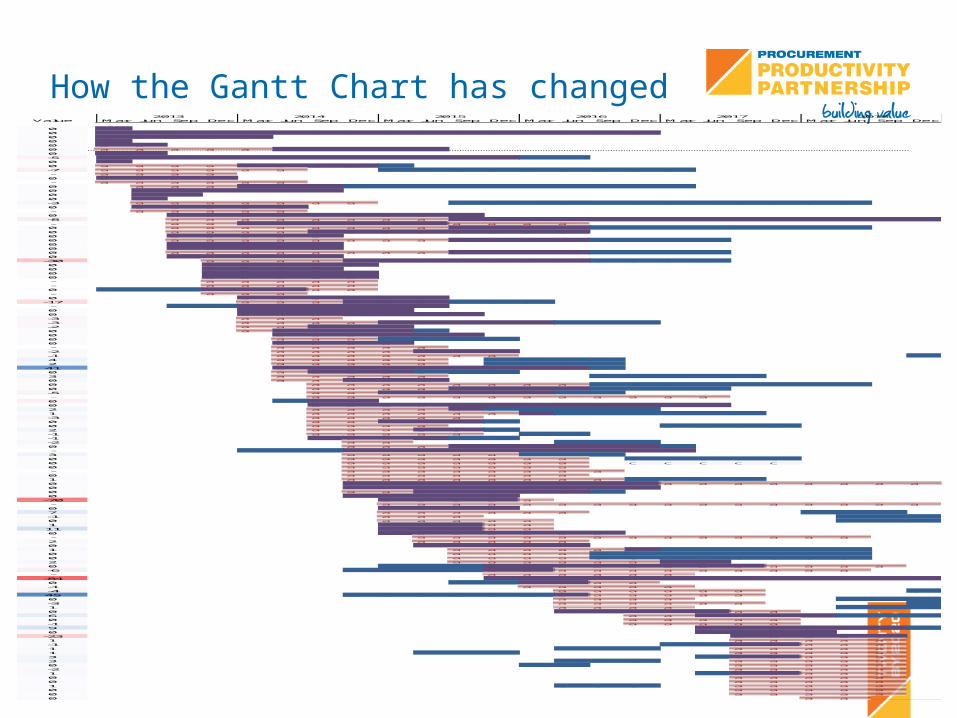

How the Gantt Chart has changedValue Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec

0 bb0 bb b b b b b b b b b b b b b b b0 bb b b b b0 bb0 bb b0 aa a a a a b b b b b0 bb b-5 b b b b b b b b b b b b c c0 b0 a a a a b b b b c-7 a a a a a a c c c c c c c c c- a a a a0 b b b b- a a a a a a0 a a a b b b c c c c c c c c c c0 b b b b b b0 b b0 b-3 a a a a a a a c c c c c c c c c c c c0 b b b b b- a a a a a0 b b b b b b b b b-8 a a a a a a a a b b b b b b b b b b b b b b- a a b b b b b b a a a a0 a a a a a a a a b b b b c c c c c c c c0 a a a a b b b b b b b b0 b b b b b0 a a a a a a a a b b b b c c c c0 b b b b b0 b b b b b0 a a a a a a a a b b b b c c c c0 b b b b b

-30 a a a a b b b b b b b c c c c0 b b b b b0 b b b b0 b b b b b0 b b b b b- a a a a a- a a a a a0 c c c b b b a a- a a a0 b b b b b b

-17 a a a b b b c c c- c c b b b b b b0 b b b b b0 b b b b b b b-3 a a a-3 a a a a b b b b b c c c-2 a a b b b0 a b b b b c0 b b b b b b0 a a a c c c c0 b b b b- a a a a a-2 a a a a b b b-1 a a a a a a a c4 a a a a a c c c c2 a a a a a c c c c41 b b b b b b b b b c0 a b b b c c c3 a a a a a c c c c c0 a a b b b0 a a a a a a a a c c c c c c c c0 a a a a b b b b c c c c-5 a a b b b b b c c- a a a a a a a a a a a a0 c b b0 b b b b b b b b b b b b2 a a a a b c c c c c1 a a a a a a b c c c c c c-3 a a a a a0 a a b b b c0 a a a a c c c c2 a a a b b c-1 a a a a a c c-1 c b b b c c-2 a a c c c0 a a a b b b b b b c- c c c b b b b b b b b b b3 a a a a a c c c0 a a a a a a a c c c c c0 a a a a a a a c c c c c0 a a a a a a a- a a a a a a a a0 a a a a a a a1 a a a a a a a a c c c c0 b b b b b b b b b a a a a a a a a0 b b b b b b b b b0 a a b b b b b c0 b b b b b

-70 b b b b a- a a a a a a a a a a a a a a a a0 b b b b7 a a a a a a c c c-1 a a a c c c0 a a a a a c c c1 b b b a a11 b b b a a0 b b b b b b b- a a a a a a a a a a a a a2 a a a a a0 b b b b b1 a a a a a b c c c c c c0 a a a a c c c c c c c c0 a a a a c c c c c c c c2 a a a a a a b b0 c c c b b b b b b b b a a a a-6 c c c c b b a a a a a a a a a- a a a a a a

-84 b b b b b b b b b b b b b0 c c b b a a-1 a a a a a-4 a a a a a a c45 c c c c c c b a a a a a0 a a a a c c c-3 a a a a a a c1 a a a a c c c0 b b b b b a a6 a a b b b b c c c0 a a a a a-1 a a a a a9 b b b b b b c0 b b b b

-23 b b b b b1 a a a a a-1 c c b b a a a1 c c c a a a a a1 c c c a a a a a3 c b b a a a3 c c c a a a a a0 c c a a a a a-2 a a a a a1 c b b a a a0 a a a a a0 a a a a a1 c c c a a a a a0 a a a a a0 a a a a a0 a a

2013 2014 2015 2016 2017 2018

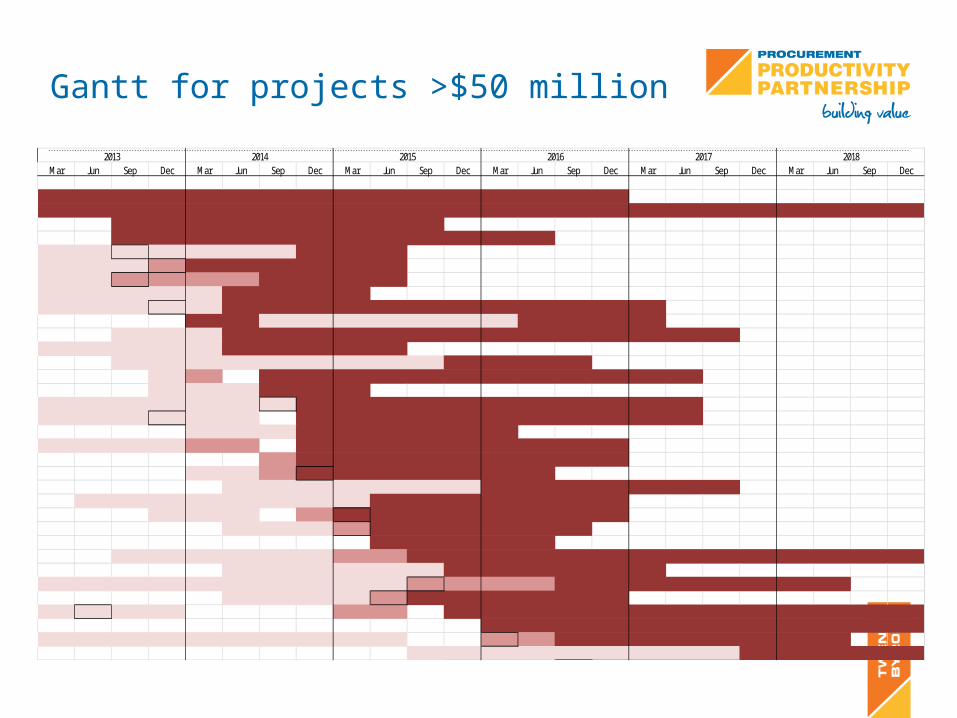

Gantt for projects >$50 million

Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec

C C C C C C C C C C C C C C C CC C C C C C C C C C C C C C C C C C C C C C C C

C C C C C C C C CC C C C C C C C C C C C

D D DA D D D D C C CD D D TA C C C C C CD D TA T T T C C C CD D D D D C C C CD D D DA D C C C C C C C C C C C C

C C D D D D D D D C C C CD D D C C C C C C C C C C C C C C

D D D D D C C C C CD D D D D D D D D C C C C

D T C C C C C C C C C C C CD D D C C C

D D D D D D DA C C C C C C C C C C CD D D DA D D C C C C C C C C C C C

D D D C C C C C CD D D D T T C C C C C C C C C

T C C C C C C C C CD D T CA C C C C C C

D D D D D D D C C C C C C CD D D D D D D D C C C C C C C

D D D T CA C C C C C C CD D D TA C C C C C C

C C C C CD D D D D D T T C C C C C C C C C C C C C C

D D D D D D C C C C C CD D D D D D D D D D TA T T T C C C C C C C C

D D D D TA C C C C C CD DA D D T T C C C C C C C C C C C C C

C C C C C C C C C C C CD D D D D D D D D D TA T C C C C C C C C

D D D D D D D D D C C C C C

20182013 2014 2015 2016 2017

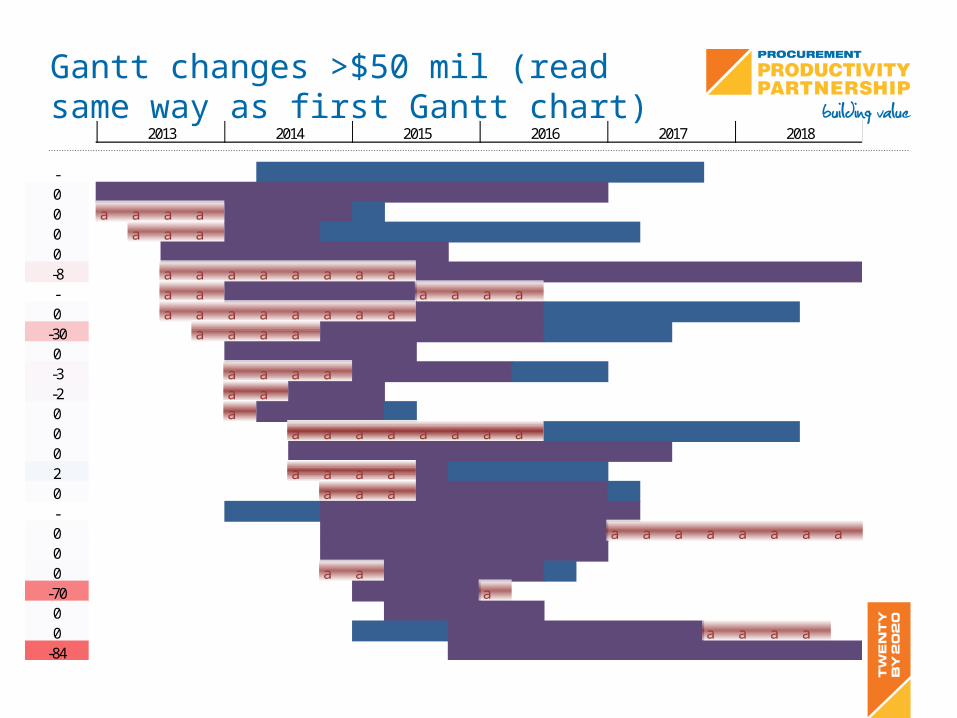

Gantt changes >$50 mil (read same way as first Gantt chart)

Value Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec

- c c c c c c c c c c c c c c0 bb b b b b b b b b b b b b b b b0 a a a a b b b b c0 a a a b b b c c c c c c c c c c0 b b b b b b b b b-8 a a a a a a a a b b b b b b b b b b b b b b- a a b b b b b b a a a a0 a a a a a a a a b b b b c c c c c c c c

-30 a a a a b b b b b b b c c c c0 b b b b b b-3 a a a a b b b b b c c c-2 a a b b b0 a b b b b c0 a a a a a a a a c c c c c c c c0 b b b b b b b b b b b b2 a a a a b c c c c c0 a a a b b b b b b c- c c c b b b b b b b b b b0 b b b b b b b b b a a a a a a a a0 b b b b b b b b b0 a a b b b b b c

-70 b b b b a0 b b b b b0 c c c b b b b b b b b a a a a

-84 b b b b b b b b b b b b b

2013 2014 2015 2016 2017 2018

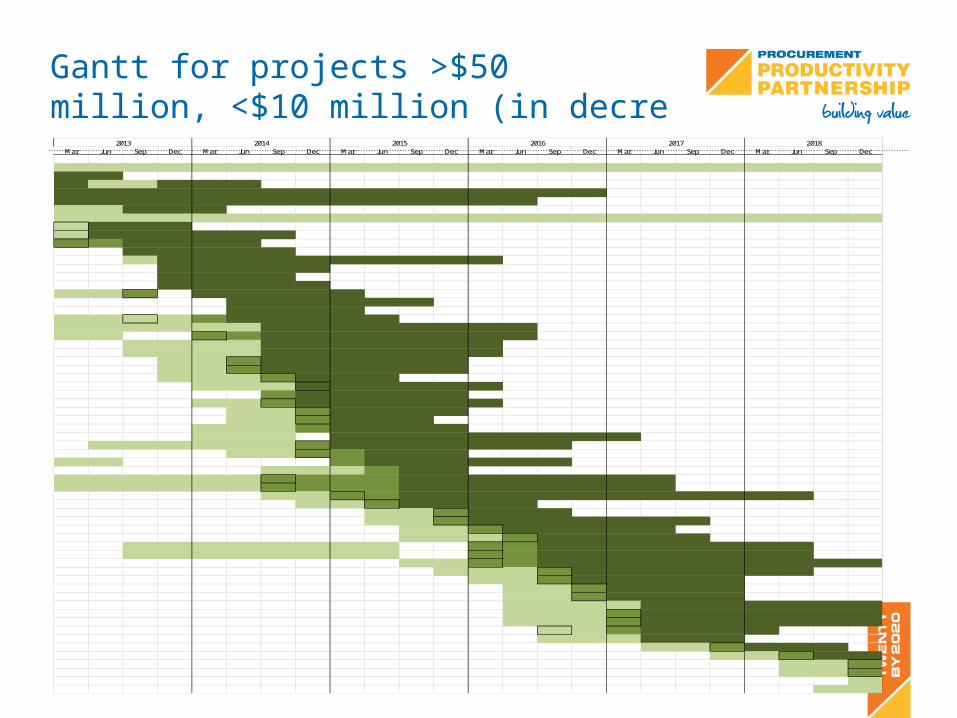

Gantt for projects >$50 million, <$10 million (in decre

Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec

D D D D D D D D D D D D D D D D D D D D D D D DC CC D D C C CC C C C C C C C C C C C C C C CC C C C C C C C C C C C C CD D C C CD D D D D D D D D D D D D D D D D D D D D D D DDA C C CDA C C C C C CTA T C C C C

C C C C CD C C C C C C C C C C

C C C C CC C C CC C C C C

D D TA C C C C CC C C C C CC C C C

D D DA D T C C C C CD D D D D D C C C C C C C CD D TA T C C C C C C C C

D D D D C C C C C C CD D D D C C C C C C C

D D TA C C C C C CD D TA C C C C C CD D D TA C C C

D D D CA C C C C CT C C C C C

D D TA C C C C C CD D TA C C C CD D TA C C C

D D D T C C C CD D D C C C C C C C C C

D D D D D D TA C C C C C C CD D TA T C C C

D D T C C C C C CD D D T C C

D D D D D D TA T T T C C C C C C C CD D D D D D TA T T T C C C C C C C C

D D TA T C C C C C C C C C C C CD D TA C C C C

D D TA C C CD D TA C C C C C C C

D D TA C C C C CD D D TA C C C C C

D D D D D D D D TA T C C C C C C C CD D D D D D D D TA T C C C C C C C C

D D TA T C C C C C C C C C CD D D TA C C C C C C C

D D TA C C C C CD D TA C C C CD D TA C C C CD D D D C C C C C C CD D D TA C C C C C C CD D D TA C C C C C C C

DA D T C C C CD D D C C C

D D TA C C CD D TA C C

D D TAD D TA

DD D

20182013 2014 2015 2016 2017

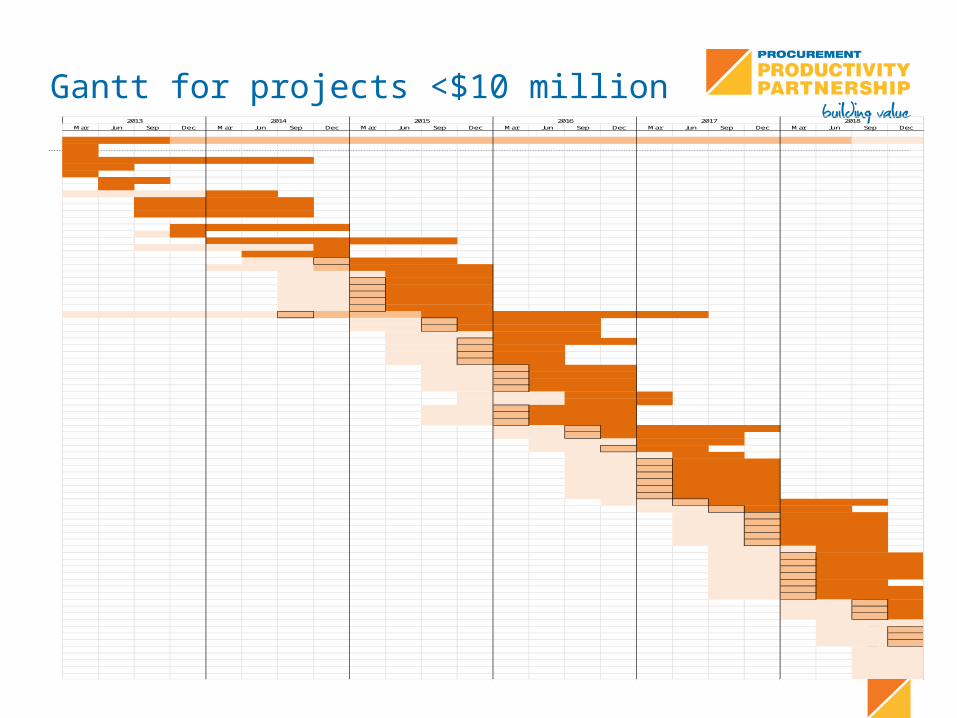

Gantt for projects <$10 millionMar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec

C C C T T T T T T T T T T T T T T T T T T T D DCCC C C C C C CC CC

C CC

D D D D C CC C C C CC C C C CC C C C C

C C C C CD C

C C C C C C CD D D D D C

C C CD D TA C C C

D D D T C C C CD D D C C CD D TA C C CD D TA C C CD D TA C C CD D TA C C CD D TA C C C

D D D D D D TA T T T C C C C C C C CD D TA C C C CD D TA C C C C

D D D C C CD D TA C C C CD D TA C CD D TA C CD D TA C C

D D TA C C CD D TA C C CD D TA C C CD D TA C C C

D D D C C CD D D C C C

D D TA C C CD D TA C C CD D TA C C C

D D TA C C C C CD D TA C C C C

D D D C C CD D TA C C

D D D C CD D TA C C CD D TA C C CD D TA C C CD D TA C C CD D TA C C CD D TA C C C

D D TA C C C C CD D TA C C C

D D TA C C CD D TA C C CD D TA C C CD D TA C C CD D TA C C C

D D D C CD D TA C C CD D TA C C CD D TA C C CD D TA C C CD D TA C CD D TA C C CD D TA C C C

D D TA CD D TA CD D TA C

D D DD D TAD D TAD D TA

D DD DD DD DD D

20182013 2014 2015 2016 2017

Design Intentions

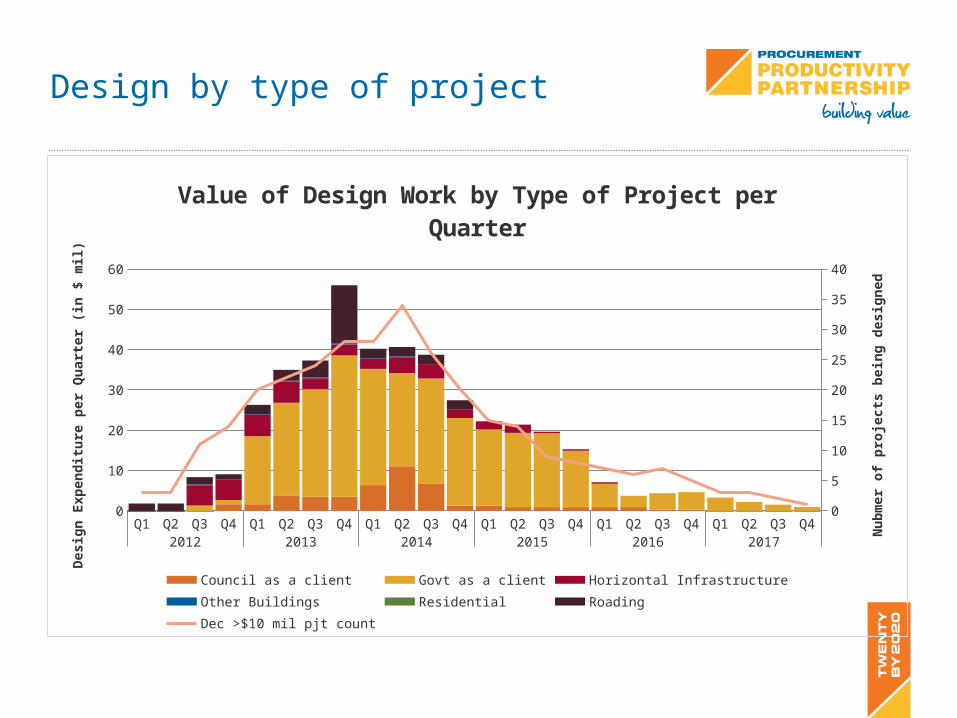

Design by type of project

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42012 2013 2014 2015 2016 2017

0

10

20

30

40

50

60

0

5

10

15

20

25

30

35

40

Value of Design Work by Type of Project per Quarter

Council as a client Govt as a client Horizontal Infrastructure Other BuildingsResidential Roading Dec >$10 mil pjt count

Desig

n Ex

pend

iture

per

Qua

rter

(in

$ m

il)

Nub

mer

of p

roje

cts b

eing

des

igne

d

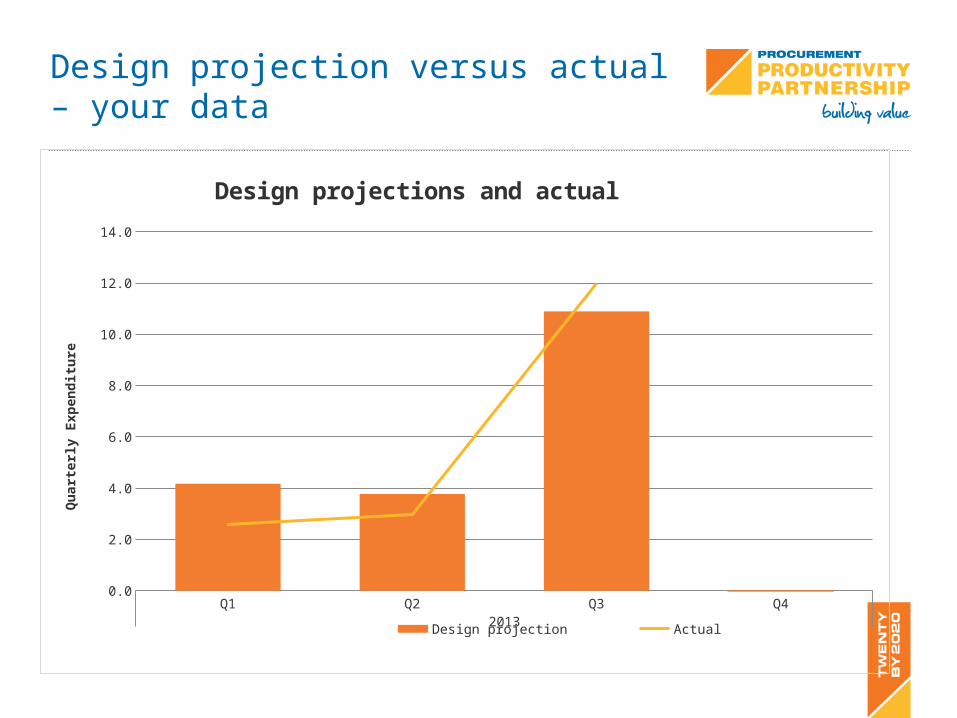

Design projection versus actual – your data

Q1 Q2 Q3 Q42013

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Design projections and actual

Design projection Actual

Qua

rter

ly E

xpen

ditu

re

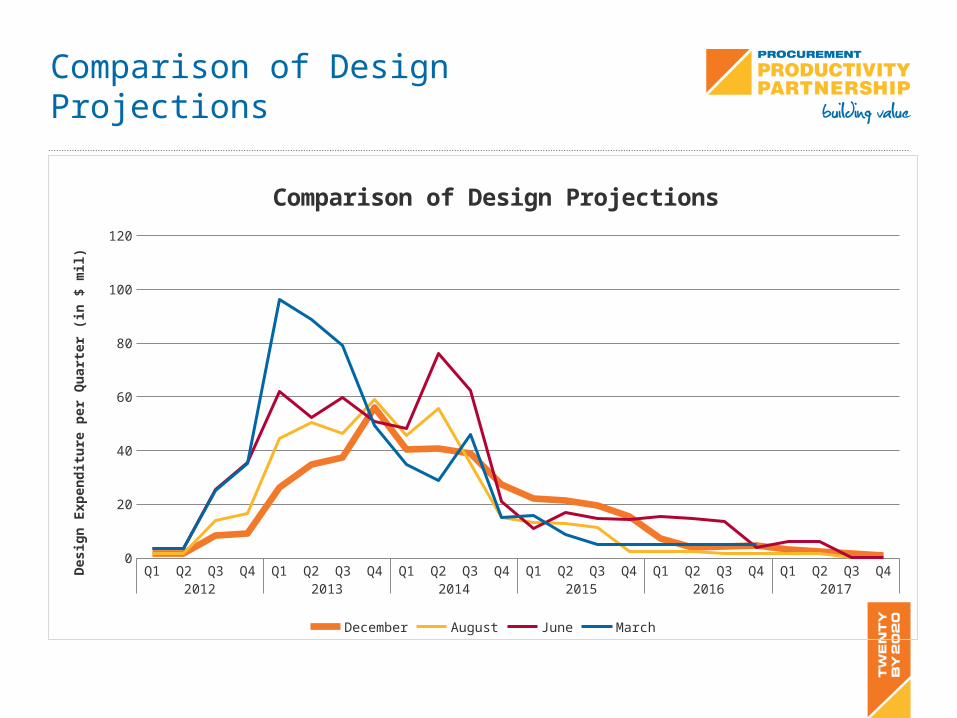

Comparison of Design Projections

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42012 2013 2014 2015 2016 2017

0

20

40

60

80

100

120

Comparison of Design Projections

December August June March

Desig

n Ex

pend

iture

per

Qua

rter

(in

$ m

il)

Comment on differences in design pipeline

‘Design peak’ remains about the same in terms of value and timing

Design peak continues to be at about the same time as reporting the data

Design has a higher value and longer “tail” than previous versions

Over all value of design work declined – consistent with the reduction in construction work.

Some of reduction in the design pipeline due to • reduction in scope / total value of projects (as seen in the construction

pipeline)• reduction in design intention data provided by some clients

But actual indicates that even this revised pipeline looks optimistic – although more consistent than the first version of this data

Tender / Procurement Intentions

Tendering by type of project

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42012 2013 2014 2015 2016 2017

0

100

200

300

400

500

600

700

0

2

4

6

8

10

12

14

16

Value of Tendered Work by Type of Project per Quarter

Council as a client Govt as a client Horizontal Infrastructure Other BuildingsResidential Roading Dec >$10 mil pjt count

Wor

k be

ing

Tend

ered

per

Qua

rter

(in

$ m

il)

Num

ber o

f pro

ject

s ten

dere

d pe

r qua

rter

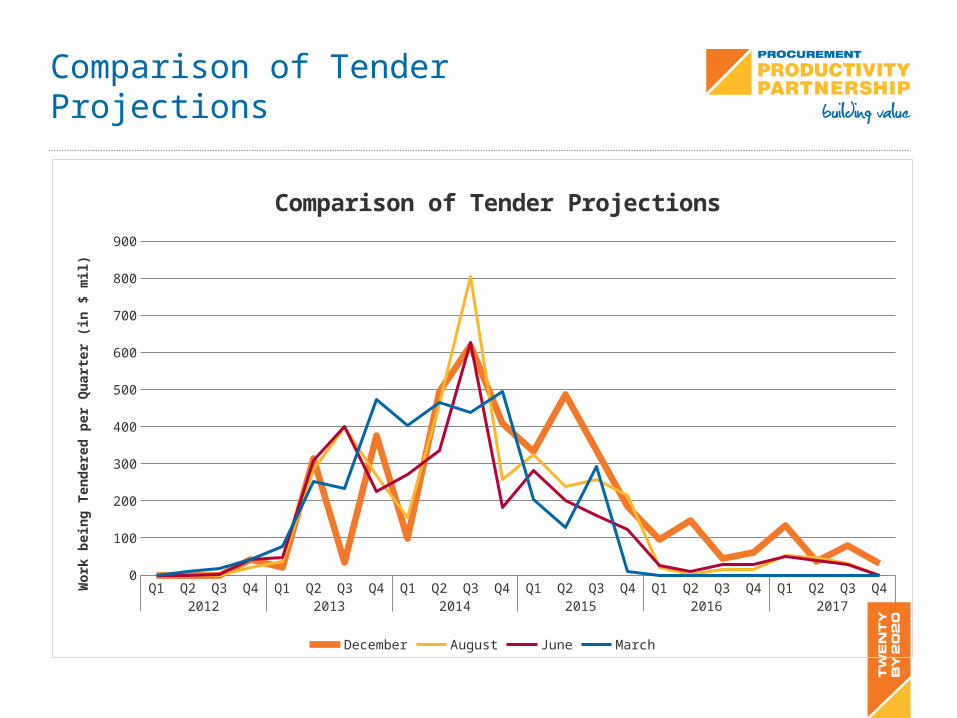

Comparison of Tender Projections

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42012 2013 2014 2015 2016 2017

0

100

200

300

400

500

600

700

800

900

Comparison of Tender Projections

December August June March

Wor

k be

ing

Tend

ered

per

Qua

rter

(in

$ m

il)

Comments on tender / procurement pipeline

This pipeline will always be lumpy because concentrates value of projects into shorter timeframes

Peak in mid June 2014 in part driven by a small number of very high value projects

Been some redistribution of procurement activity from late 2013 to early 2015 over the year of data – consistent with the delays in completing design work