Download - ACCT 2310 Accounting Principles I Chapter 2

ACCT 2310 Accounting Principles I Chapter 2

Dr. Robert R. OlivaProfessor and ChairpersonDepartment of Accounting

University of Arkansas at Little Rock

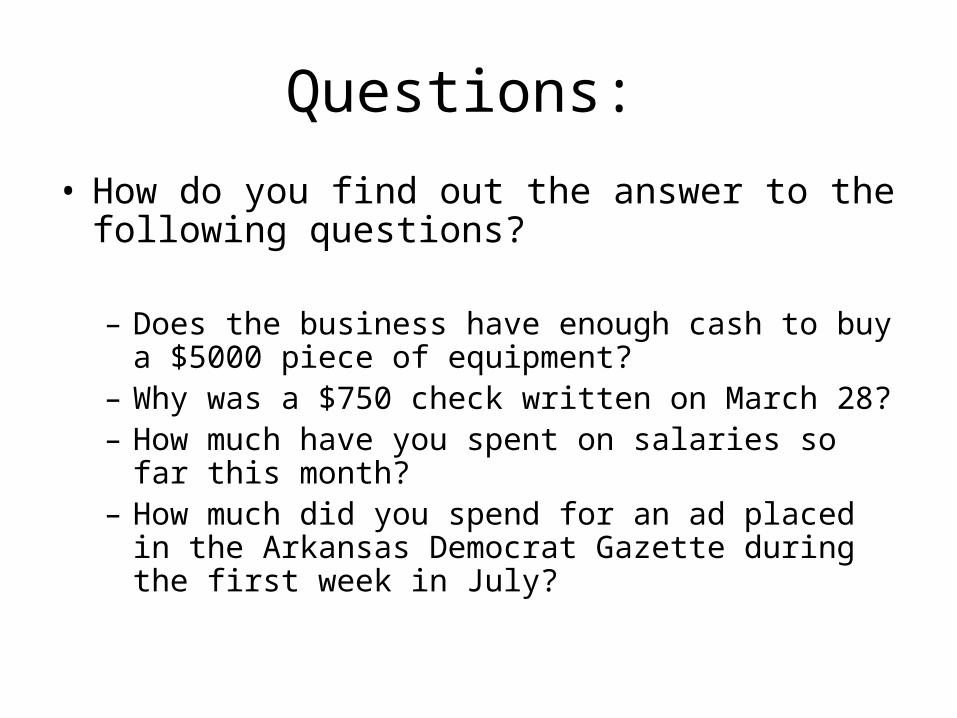

Questions:

• How do you find out the answer to the following questions?

– Does the business have enough cash to buy a $5000 piece of equipment?

– Why was a $750 check written on March 28?– How much have you spent on salaries so far this

month?– How much did you spend for an ad placed in the

Arkansas Democrat Gazette during the first week in July?

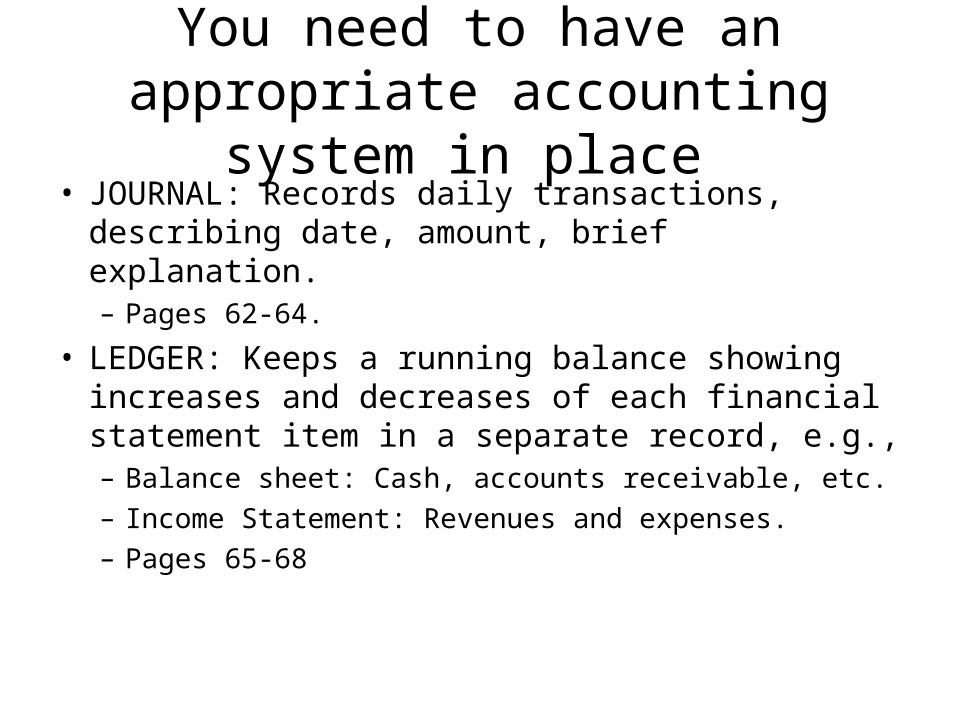

You need to have an appropriate accounting system in place

• JOURNAL: Records daily transactions, describing date, amount, brief explanation. – Pages 62-64.

• LEDGER: Keeps a running balance showing increases and decreases of each financial statement item in a separate record, e.g., – Balance sheet: Cash, accounts receivable, etc.– Income Statement: Revenues and expenses.– Pages 65-68

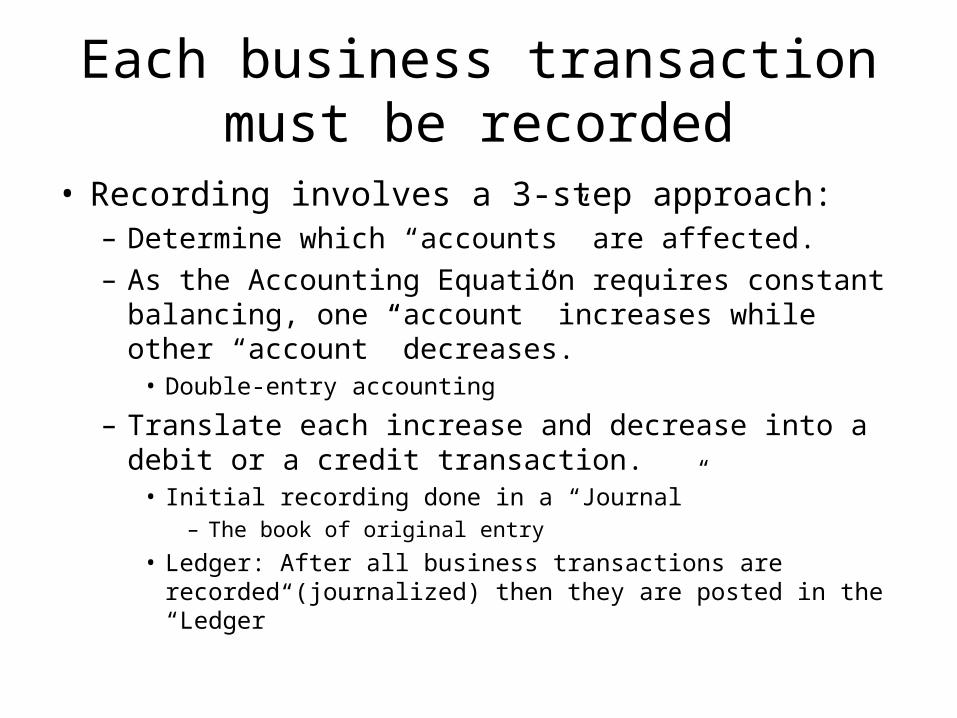

Each business transaction must be recorded

• Recording involves a 3-step approach:– Determine which “accounts” are affected.– As the Accounting Equation requires constant

balancing, one “account” increases while other “account” decreases.

• Double-entry accounting

– Translate each increase and decrease into a debit or a credit transaction.

• Initial recording done in a “Journal”– The book of original entry

• Ledger: After all business transactions are recorded (journalized) then they are posted in the “Ledger”

Flow of business transactions

• Exhibit 2, page 56

Will proper recording prevent fraud?

• Bottom of page 54

But before we can record in a journal or post to a ledger

• We need to know what to call each business transaction– We need to separate business transactions

into “Accounts”

Account classification

• Classification depends on the business transaction and the type of business.

• Business transactions may be classified as affecting – Assets– Liabilities– Owners’ Equity– Revenues– Expenses

Chapter 1: Lawn Mowing example

• Many transactions were recorded in Owner’s Equity– Hard to separate and analyze– OK for a very small business. But in reality not

very efficient.

• More efficient approach: Separate “Owner’s Equity” into various accounts.

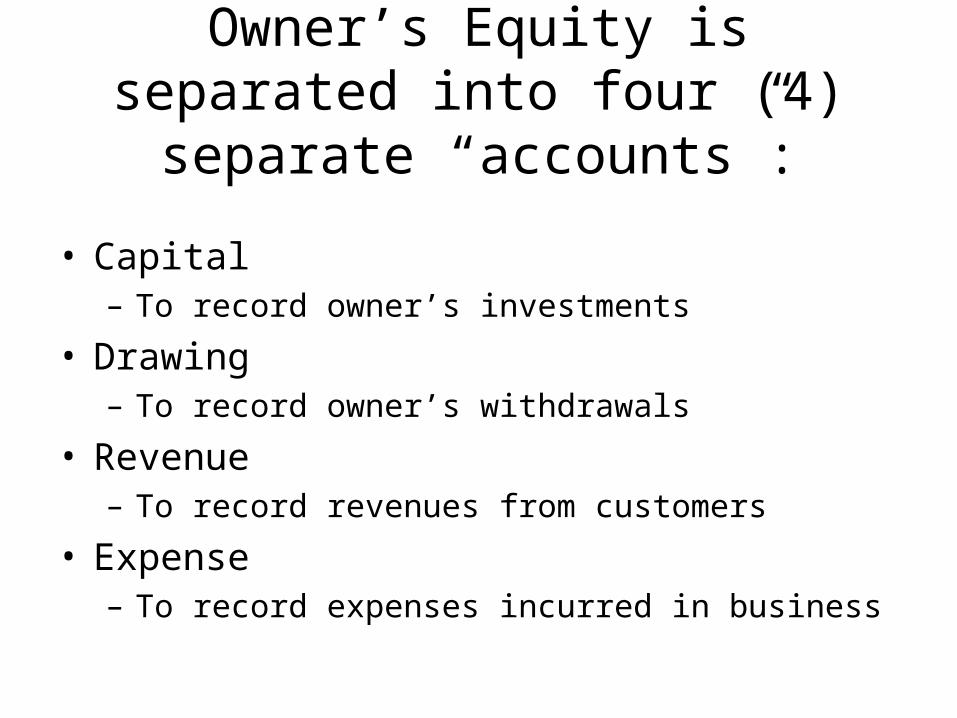

Owner’s Equity is separated into four (4) separate “accounts”:

• Capital– To record owner’s investments

• Drawing– To record owner’s withdrawals

• Revenue– To record revenues from customers

• Expense– To record expenses incurred in business

Examples of other “accounts”:

• Cash

• Supplies

• Accounts Payable

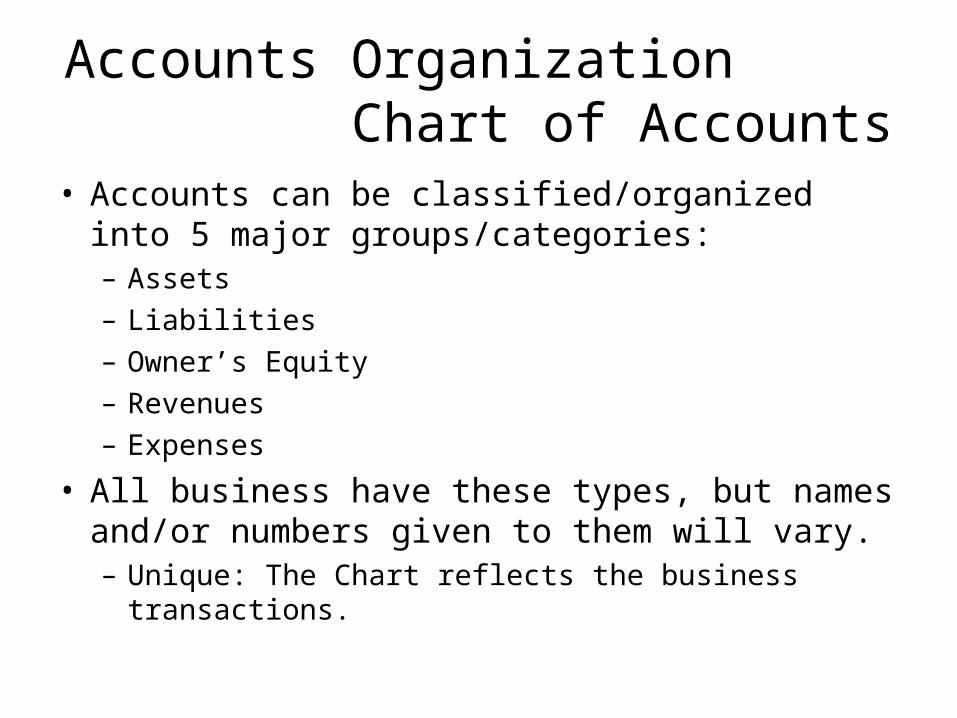

Accounts Organization Chart of Accounts

• Accounts can be classified/organized into 5 major groups/categories:– Assets– Liabilities– Owner’s Equity– Revenues– Expenses

• All business have these types, but names and/or numbers given to them will vary.– Unique: The Chart reflects the business transactions.

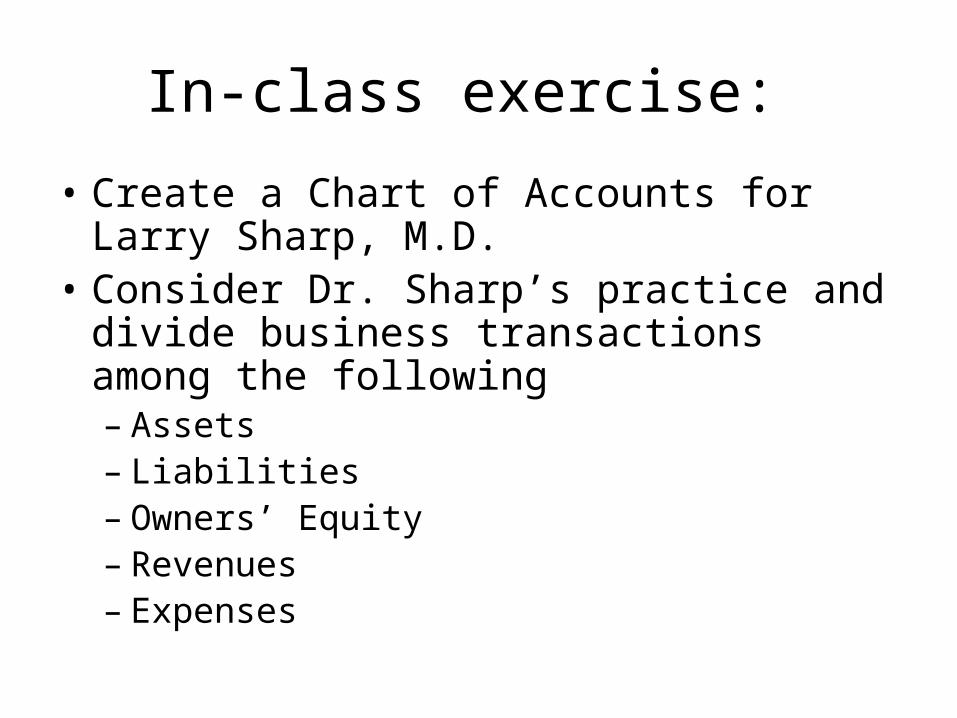

In-class exercise:

• Create a Chart of Accounts for Larry Sharp, M.D.

• Consider Dr. Sharp’s practice and divide business transactions among the following– Assets– Liabilities– Owners’ Equity– Revenues– Expenses

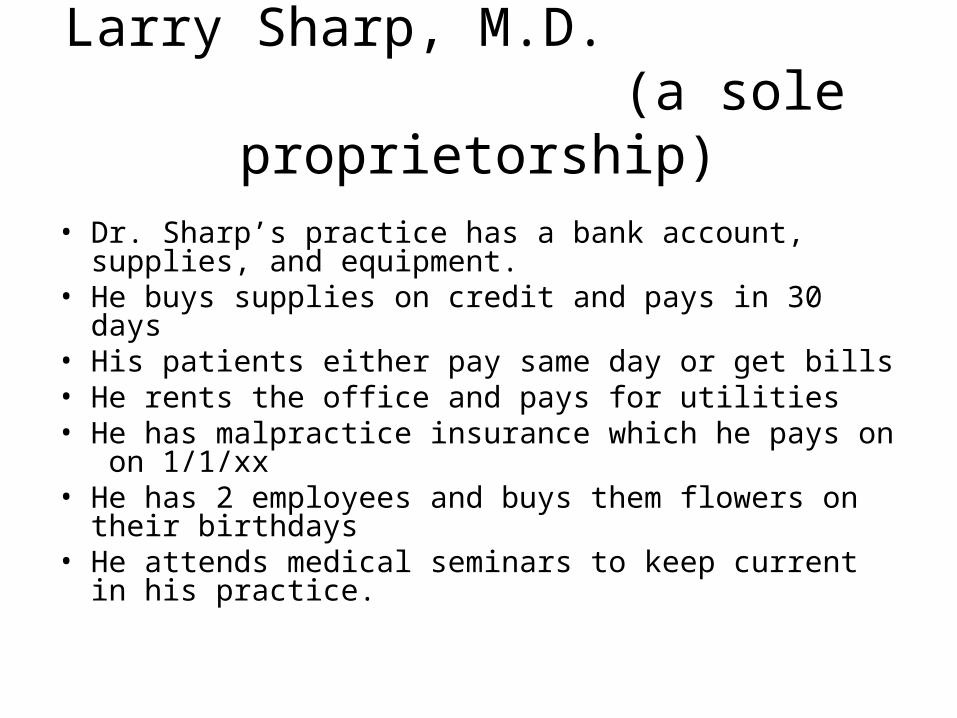

Larry Sharp, M.D. (a sole proprietorship)

• Dr. Sharp’s practice has a bank account, supplies, and equipment.

• He buys supplies on credit and pays in 30 days• His patients either pay same day or get bills • He rents the office and pays for utilities• He has malpractice insurance which he pays on on

1/1/xx• He has 2 employees and buys them flowers on their

birthdays• He attends medical seminars to keep current in his

practice.

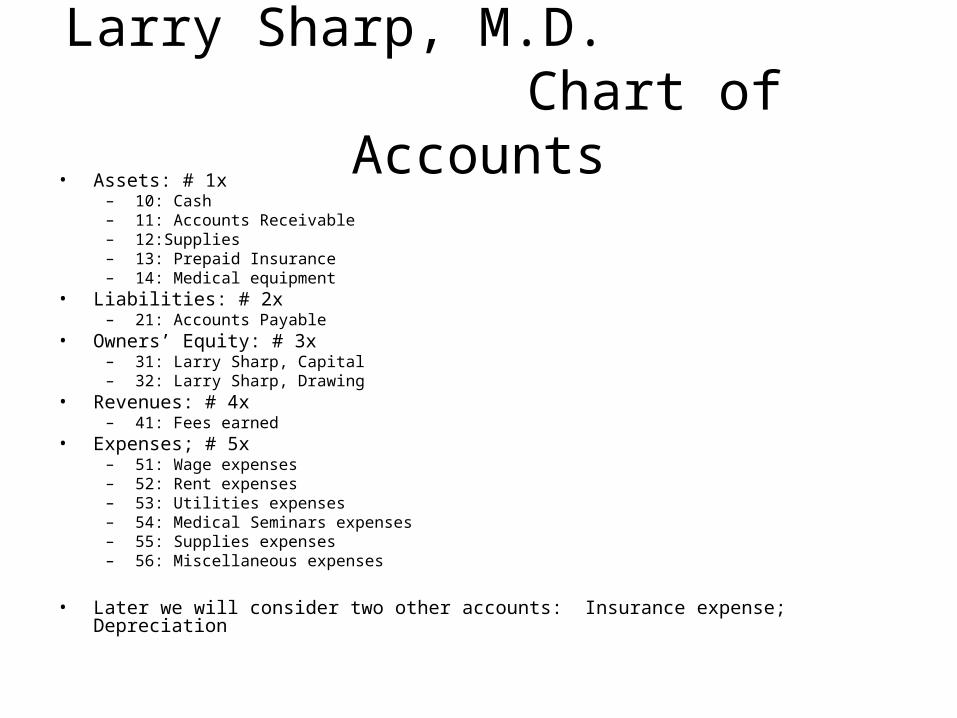

Larry Sharp, M.D. Chart of Accounts

• Assets: # 1x– 10: Cash– 11: Accounts Receivable– 12:Supplies– 13: Prepaid Insurance– 14: Medical equipment

• Liabilities: # 2x– 21: Accounts Payable

• Owners’ Equity: # 3x– 31: Larry Sharp, Capital– 32: Larry Sharp, Drawing

• Revenues: # 4x – 41: Fees earned

• Expenses; # 5x– 51: Wage expenses– 52: Rent expenses– 53: Utilities expenses– 54: Medical Seminars expenses– 55: Supplies expenses– 56: Miscellaneous expenses

• Later we will consider two other accounts: Insurance expense; Depreciation

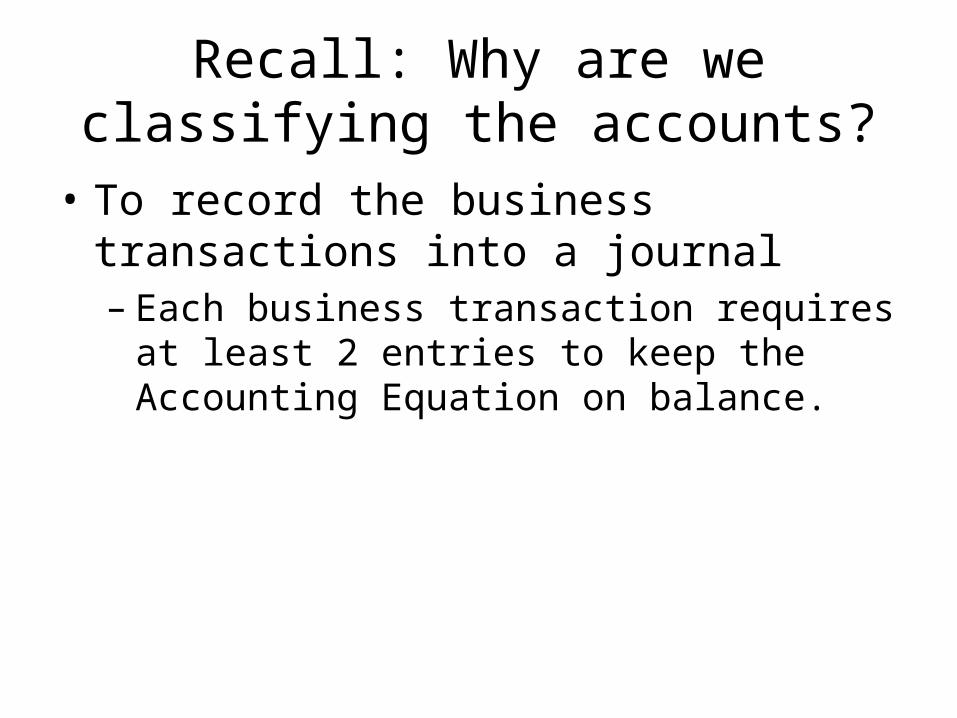

Recall: Why are we classifying the accounts?

• To record the business transactions into a journal– Each business transaction requires at least 2

entries to keep the Accounting Equation on balance.

What account increases and what account decreases?

The hijacking receivable

• Page 53

Account Characteristics: pp. 49-50

• Form: The “T’ account

• Two sides of the “T”– Left side: The debit side– Right side: The credit side

• Some accounts increase by “debit” entries

• Some account increase by “credit” entries

The top of the “T” Describes type of account

• Based on the Accounting Equation: Assets = Liabilities + Owner’s Equity

• The Accounting Equation determines the recording of an account’s increases and decreases, e.g., Debits and Credits

• Page 52

Assets’ Accounts:

• Assets increase with “debits”, e.g., increases recorded on the left side of the “T”.– AID

• Assets decrease with “credits”, e.g., decreases recorded on the left side of the “T”– ADC

Liabilities’ Accounts

• Liabilities and Owner’s Equity increase with “credits”, e.g., increases recorded on the left side of the “T”.– LIC

• Liabilities and Owners’ Equity decrease with “debits”, e.g., decreases recorded on the left side of the “T”– LDD

• Note: Rules mirror each other– Memorize only one

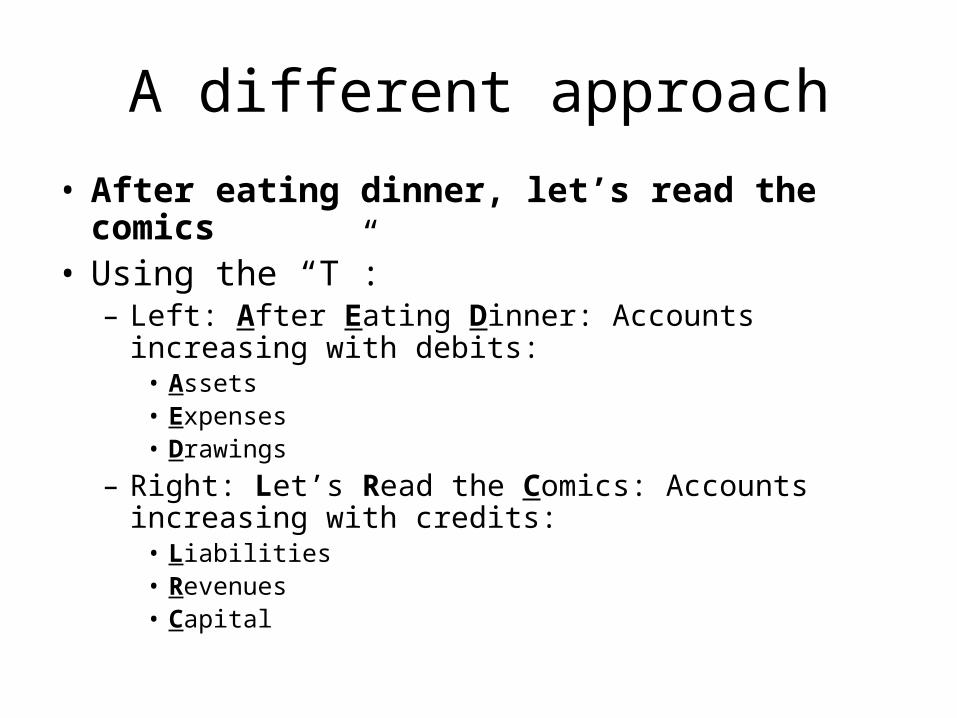

A different approach

• After eating dinner, let’s read the comics• Using the “T”:

– Left: After Eating Dinner: Accounts increasing with debits:

• Assets• Expenses• Drawings

– Right: Let’s Read the Comics: Accounts increasing with credits:

• Liabilities• Revenues• Capital

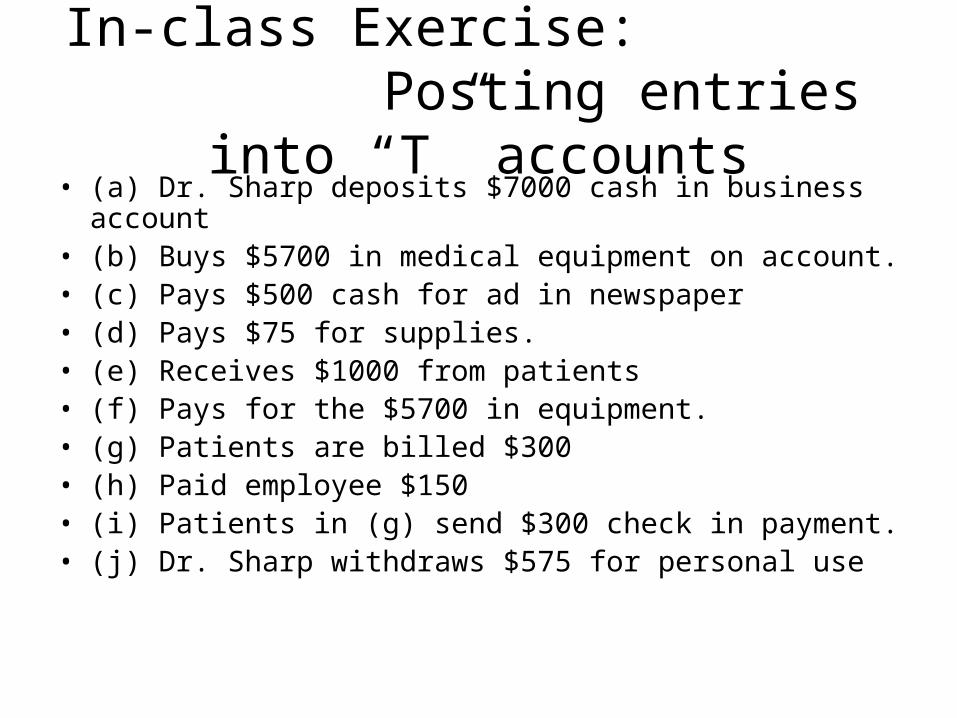

In-class Exercise: Posting entries into “T” accounts

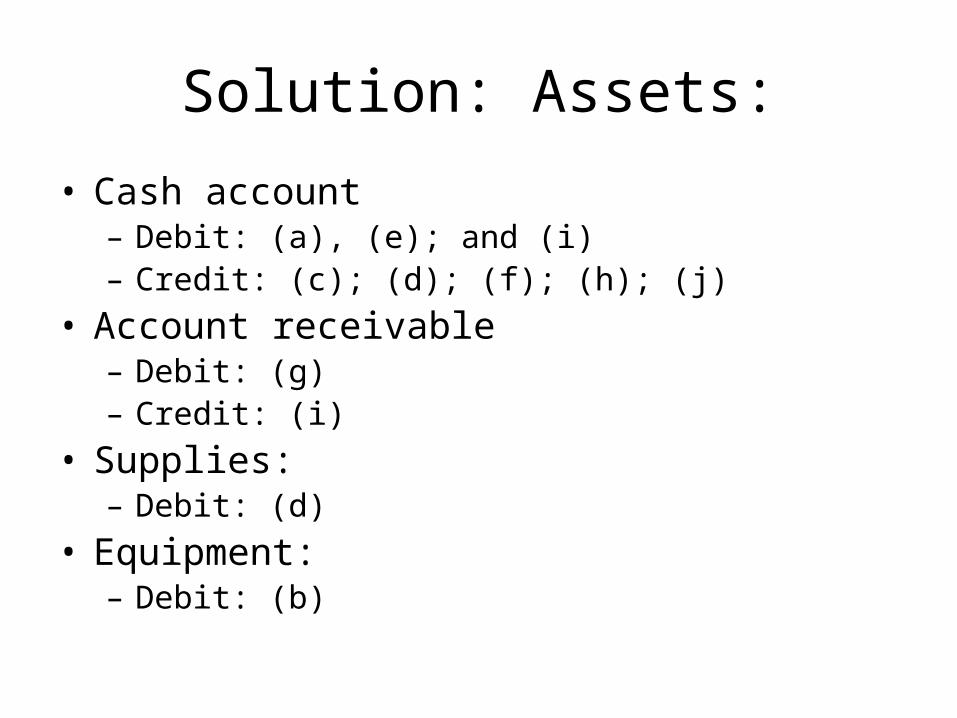

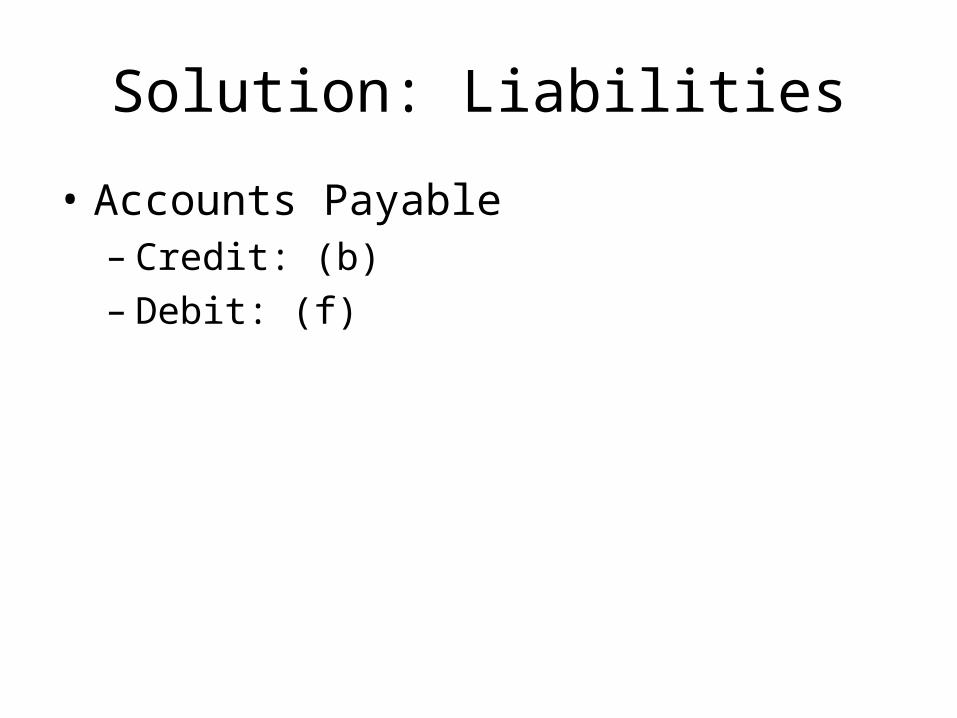

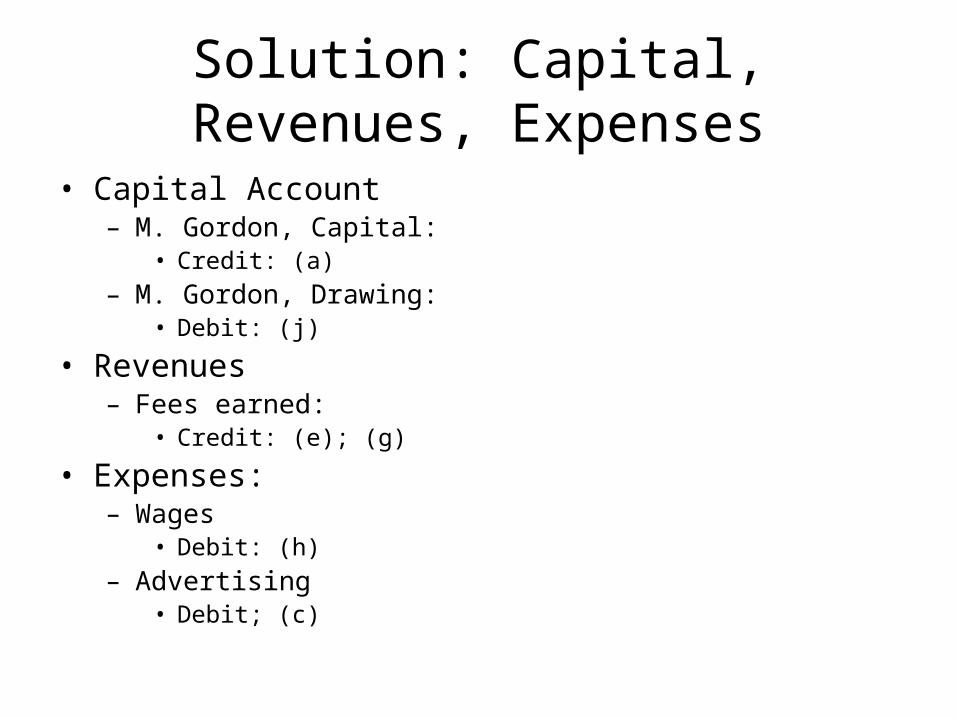

• (a) Dr. Sharp deposits $7000 cash in business account• (b) Buys $5700 in medical equipment on account.• (c) Pays $500 cash for ad in newspaper• (d) Pays $75 for supplies.• (e) Receives $1000 from patients• (f) Pays for the $5700 in equipment.• (g) Patients are billed $300• (h) Paid employee $150• (i) Patients in (g) send $300 check in payment.• (j) Dr. Sharp withdraws $575 for personal use

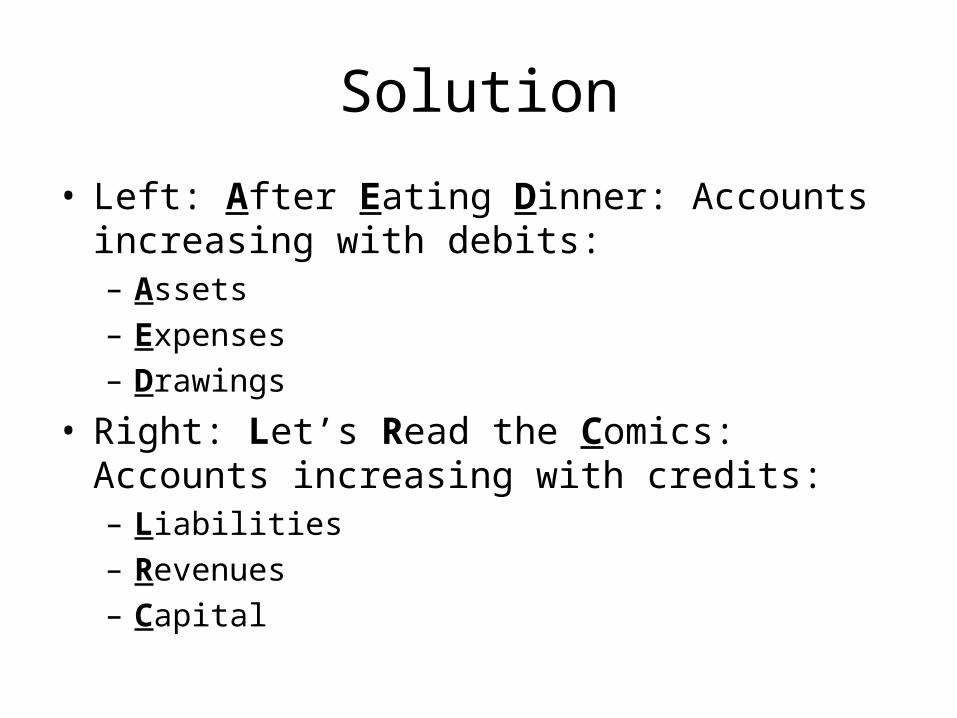

Solution

• Left: After Eating Dinner: Accounts increasing with debits:– Assets– Expenses– Drawings

• Right: Let’s Read the Comics: Accounts increasing with credits:– Liabilities– Revenues– Capital

Solution: Assets:

• Cash account– Debit: (a), (e); and (i)– Credit: (c); (d); (f); (h); (j)

• Account receivable– Debit: (g)– Credit: (i)

• Supplies:– Debit: (d)

• Equipment:– Debit: (b)

Solution: Liabilities

• Accounts Payable– Credit: (b)– Debit: (f)

Solution: Capital, Revenues, Expenses

• Capital Account– M. Gordon, Capital:

• Credit: (a)

– M. Gordon, Drawing: • Debit: (j)

• Revenues– Fees earned:

• Credit: (e); (g)

• Expenses:– Wages

• Debit: (h)

– Advertising • Debit; (c)

But many times proper recoding requires through analysis

• Payments in advance

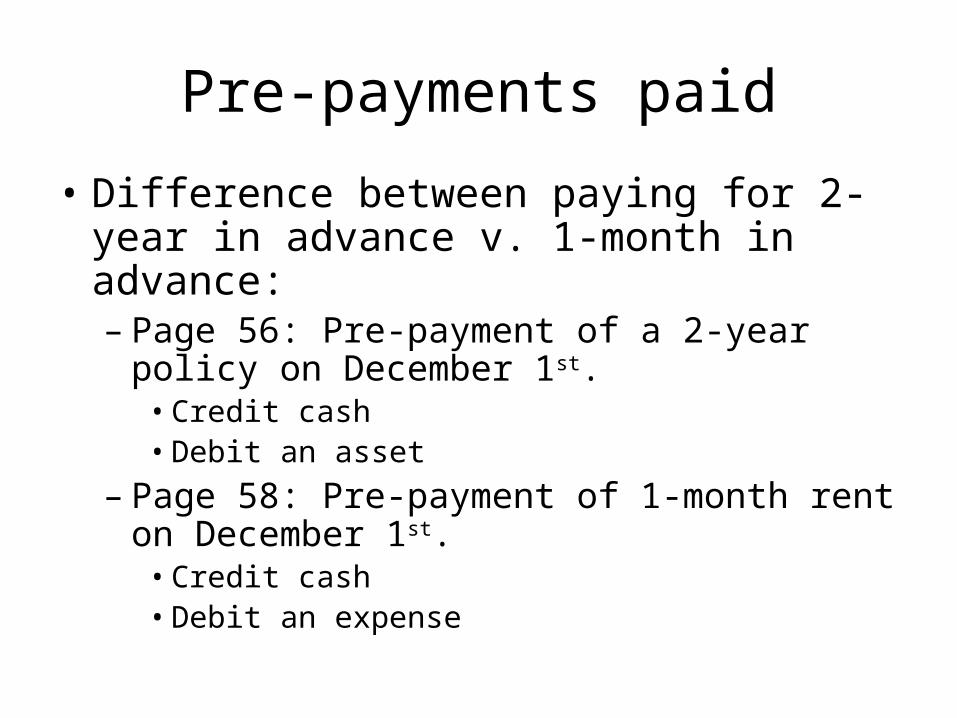

Pre-payments paid

• Difference between paying for 2-year in advance v. 1-month in advance: – Page 56: Pre-payment of a 2-year policy on

December 1st.• Credit cash• Debit an asset

– Page 58: Pre-payment of 1-month rent on December 1st.

• Credit cash• Debit an expense

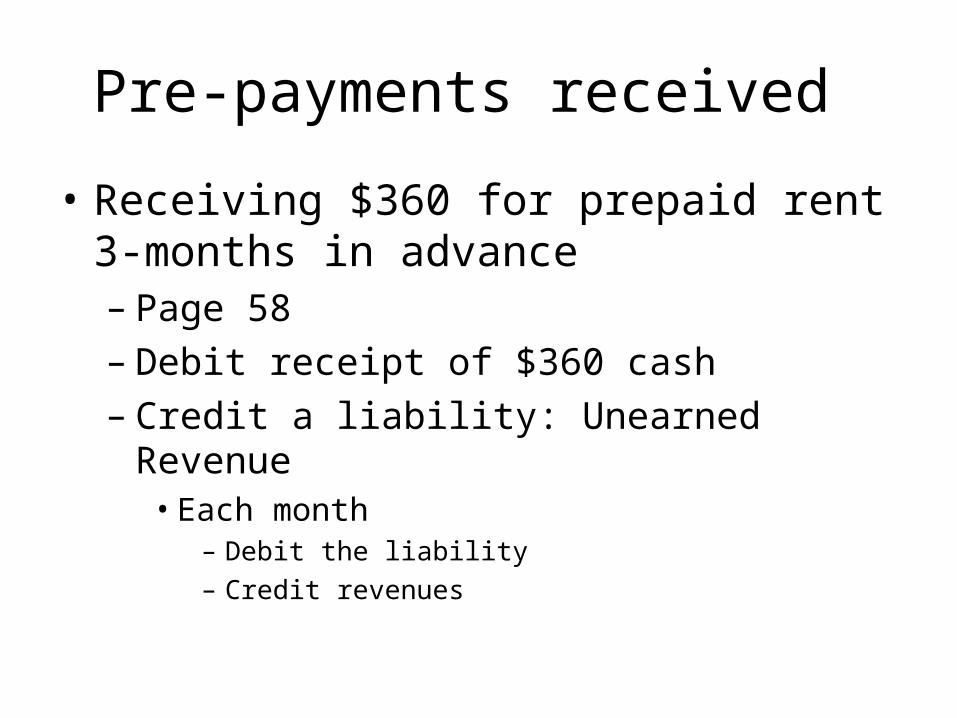

Pre-payments received

• Receiving $360 for prepaid rent 3-months in advance– Page 58– Debit receipt of $360 cash– Credit a liability: Unearned Revenue

• Each month – Debit the liability– Credit revenues

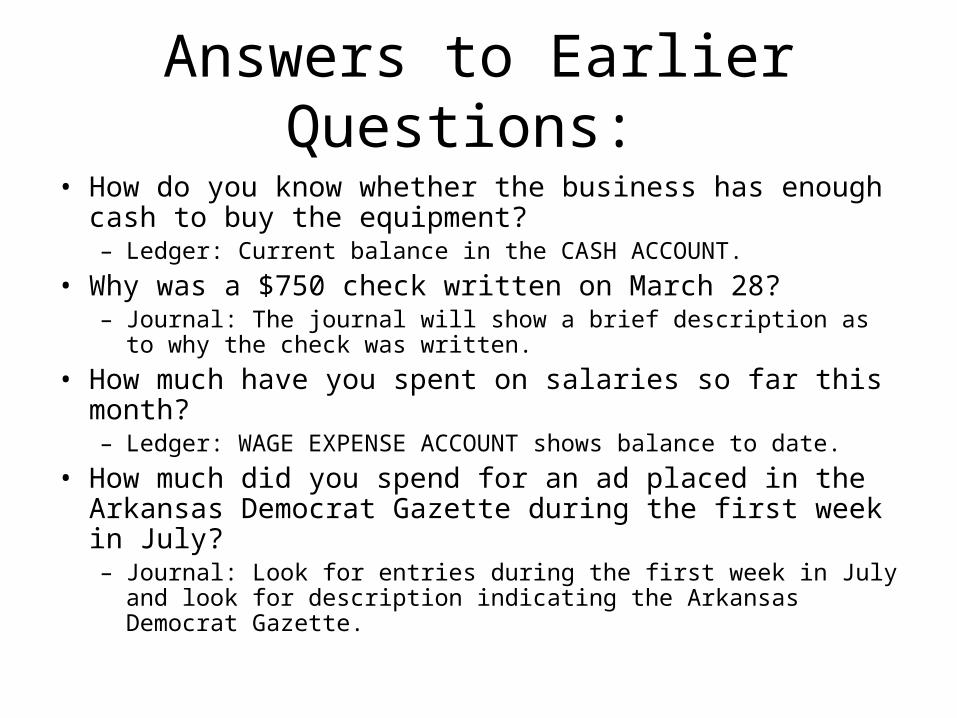

Answers to Earlier Questions:

• How do you know whether the business has enough cash to buy the equipment?– Ledger: Current balance in the CASH ACCOUNT.

• Why was a $750 check written on March 28?– Journal: The journal will show a brief description as to why the

check was written.

• How much have you spent on salaries so far this month?– Ledger: WAGE EXPENSE ACCOUNT shows balance to date.

• How much did you spend for an ad placed in the Arkansas Democrat Gazette during the first week in July? – Journal: Look for entries during the first week in July and look for

description indicating the Arkansas Democrat Gazette.

TRIAL BALANCE

• Reports the balance of each ledger account

• Aim: TO show that Debits = Credits

In-Class Exercise

• Trial balance for Dr. Sharp

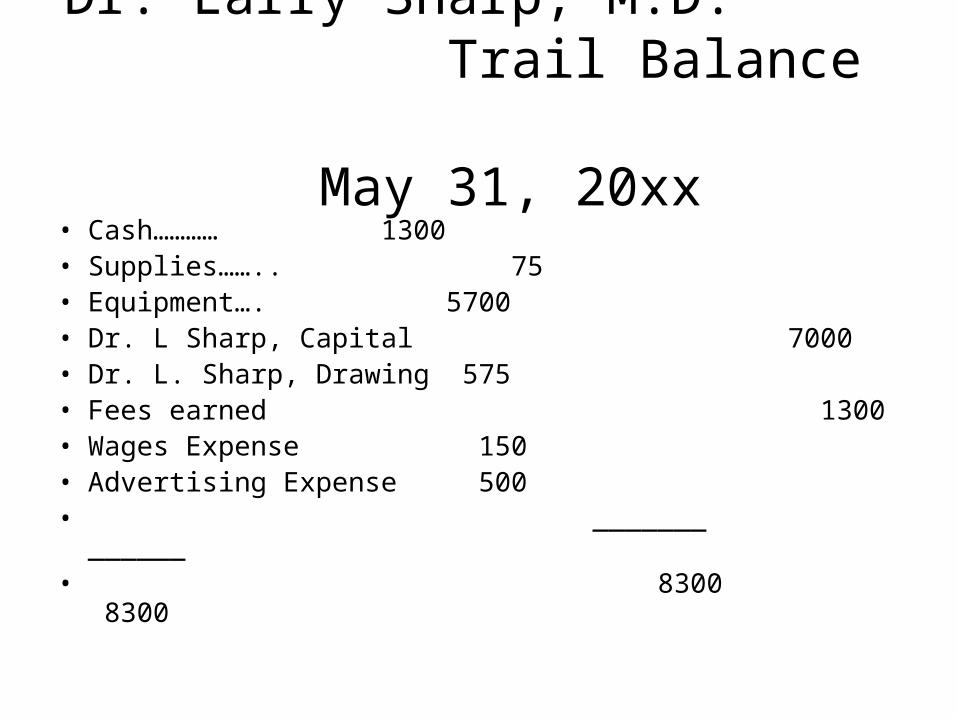

Dr. Larry Sharp, M.D. Trail Balance

May 31, 20xx• Cash………… 1300• Supplies…….. 75• Equipment…. 5700• Dr. L Sharp, Capital 7000• Dr. L. Sharp, Drawing 575• Fees earned 1300• Wages Expense 150• Advertising Expense 500 • _______ ______• 8300 8300

Possible errors Exhibit 6

• Transposition• Slide

Error Correction

• Exhibit 7

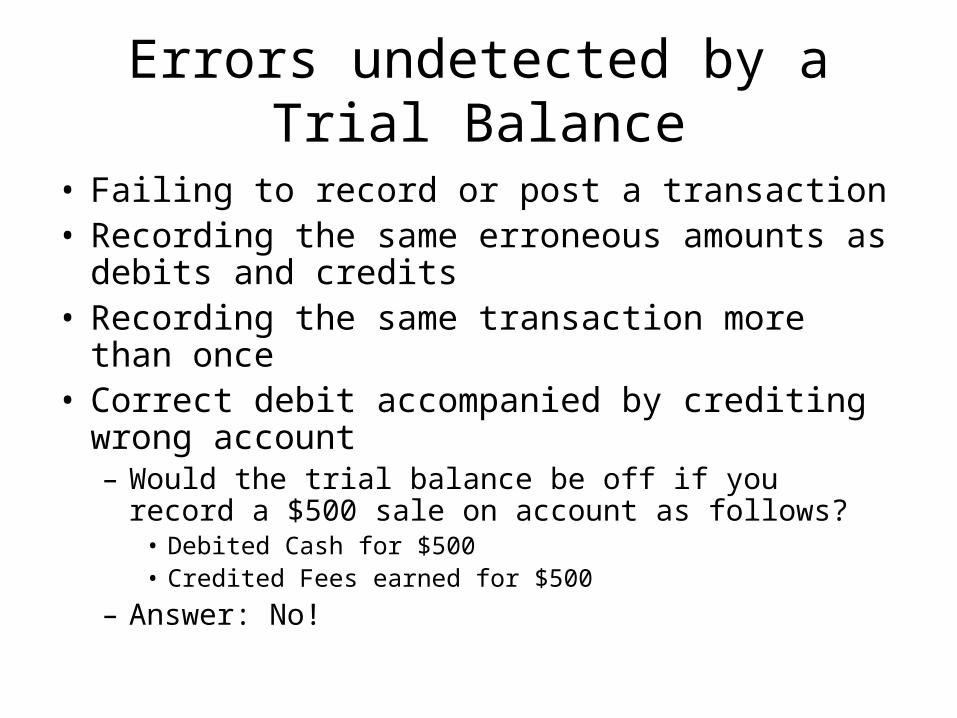

Errors undetected by a Trial Balance

• Failing to record or post a transaction• Recording the same erroneous amounts as

debits and credits• Recording the same transaction more than once• Correct debit accompanied by crediting wrong

account– Would the trial balance be off if you record a $500

sale on account as follows?• Debited Cash for $500• Credited Fees earned for $500

– Answer: No!

FINANCIAL ANALYSIS

• Horizontal analysis– Comparing time periods

• Exhibit 8