45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge1

The European Commission’s (EC’s) decision in the Apple State aid case has concluded that tax

rulings of 1991 and 2007 issued by Irish Revenue in favour of two Apple sales and

marketing/manufacturing subsidiaries in Ireland conferred a “selective advantage”. The EC held

that the profit allocation methods endorsed by Irish Revenue resulted in lowering corporate tax

liability in Ireland for the two subsidiaries, as all the profits, except for a limited mark-up on a

reduced cost base, were allocated outside Ireland. Apple and Ireland claimed that the two

subsidiaries were non-resident in Ireland, despite being incorporated there, and that intellectual

property (IP) rights were allocable to subsidiaries’ head offices in the United States, as related

management functions were not carried out in Irish branches. Questioning Irish Revenue’s

acceptance of Apple’s unsubstantiated assumption that intellectual property (IP) licences held by

the two subsidiaries should be allocated to head offices outside of Ireland, the EC held that it

was incumbent on Irish Revenue to first properly examine the assets used, the functions

performed and the risks assumed by those companies through their Irish branches and through

the other parts of those companies, including IP held by the company as a whole. Noting that, at

the relevant time, the head offices were only present on paper, as there was no physical

presence of employees outside Ireland, the EC perused the minutes of meetings of board of

directors to concludes that “[n]ot only did those head offices not perform active or critical

functions with regard to the management of the Apple IP licenses, they also did not have the

capacity to perform such functions during the period that the contested tax rulings were in

force”. The EC also disagreed with the methodology used to arrive at taxable profits in Ireland in

the contested rulings, considering the choice of the Irish branches as the “tested party”,

premised on the unsubstantiated assumption of their performing a “less complex function” as

compared to their head offices, the choice of “operating expenses” as the PLI, despite significant

activities and risks assumed by the Irish branches, and the lack of contemporaneous

documentation justifying IP returns in the two rulings.

This decision concerns two tax rulings issued by Irish Revenue, on 29 January 1991 and on 23 May

2007, in favour of two Apple group companies – Apple Sales International (ASI) and Apple Operations

Europe (AOE).

Summary of conclusions

• The Commission held that the tax rulings issued by Ireland on 29 January 1991 and 23 May 2007

in favour of ASI and AOE, which enable the latter to determine its tax liability in Ireland on a yearly basis,

constitute aid within the meaning of Article 107(1) of the Treaty. That aid was unlawfully put into effect by

Ireland in breach of Article 108(3) of the Treaty and is incompatible with the internal market.

• The Commission directed Ireland to recover the aid from ASI and AOE, along with interest, from

the date on which they were put at the disposal of the beneficiaries until their actual recovery. It was

directed that recovery shall be immediate and effective.

• The Commission also directed Ireland to ensure that the decision is implemented within four

months following the date of its notification.

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge2

• The Commission ruled that, within two months following notification of the decision, Ireland shall

submit information to the Commission regarding the method used to calculate the exact amount of aid.

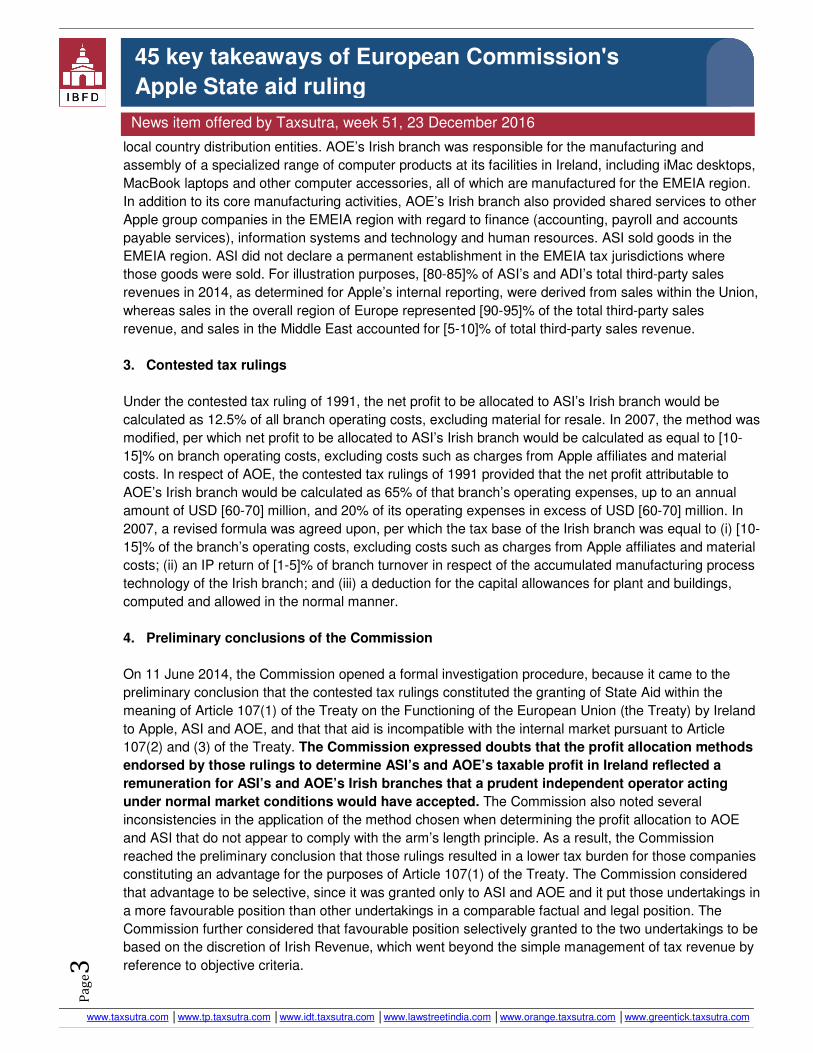

1. Tax status of the two Irish subsidiaries

These two companies are incorporated in Ireland but not resident of Ireland in terms of Section 23A of

the Taxes Consolidation Act 1997 (TCA 97), which provides certain exceptions to the rule that

companies incorporated in Ireland are, in principle, liable to tax in Ireland, even if they are managed and

controlled outside of Ireland. Both ASI and AOE are considered not resident under Section 23A of TCA

97, as they were both ultimately controlled by a company that is resident in a tax treaty country, namely

Apple Inc., which is a tax resident of the United States, and since ASI and AOE had a trading activity in

Ireland through their respective branches and were managed and controlled outside Ireland. Thus, the

companies were considered to be non-resident companies in Ireland under the “trading exception” of

Section 23A of TCA 97.

Apple’s corporate structure in Ireland (as provided in the EC ruling order) is as under:

2. Profile of ASI and AOE

ASI and AOE are incorporated in Ireland but were not tax resident in Ireland during the time that the

contested tax rulings were in force. However, these companies were not tax resident in any other tax

jurisdiction during that period, since their activities in other jurisdictions, and in particular the activities of

their head offices, which lacked any physical presence or employees, did not give rise to a taxable

presence in the United States or any other jurisdiction under the applicable taxation rules.

ASI’s Irish branch was mainly responsible for the execution of procurement, sales and distribution

activities associated with the sale of Apple products to related parties and third-party customers across

the EMEIA and APAC regions. ASI’s Irish branch also fulfilled the purchase orders placed by the APAC

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge3

www.taxsutra.com │www.tp.taxsutra.com │www.idt.taxsutra.com │www.lawstreetindia.com │www.orange.taxsutra.com │www.greentick.taxsutra.com

local country distribution entities. AOE’s Irish branch was responsible for the manufacturing and

assembly of a specialized range of computer products at its facilities in Ireland, including iMac desktops,

MacBook laptops and other computer accessories, all of which are manufactured for the EMEIA region.

In addition to its core manufacturing activities, AOE’s Irish branch also provided shared services to other

Apple group companies in the EMEIA region with regard to finance (accounting, payroll and accounts

payable services), information systems and technology and human resources. ASI sold goods in the

EMEIA region. ASI did not declare a permanent establishment in the EMEIA tax jurisdictions where

those goods were sold. For illustration purposes, [80-85]% of ASI’s and ADI’s total third-party sales

revenues in 2014, as determined for Apple’s internal reporting, were derived from sales within the Union,

whereas sales in the overall region of Europe represented [90-95]% of the total third-party sales

revenue, and sales in the Middle East accounted for [5-10]% of total third-party sales revenue.

3. Contested tax rulings

Under the contested tax ruling of 1991, the net profit to be allocated to ASI’s Irish branch would be

calculated as 12.5% of all branch operating costs, excluding material for resale. In 2007, the method was

modified, per which net profit to be allocated to ASI’s Irish branch would be calculated as equal to [10-

15]% on branch operating costs, excluding costs such as charges from Apple affiliates and material

costs. In respect of AOE, the contested tax rulings of 1991 provided that the net profit attributable to

AOE’s Irish branch would be calculated as 65% of that branch’s operating expenses, up to an annual

amount of USD [60-70] million, and 20% of its operating expenses in excess of USD [60-70] million. In

2007, a revised formula was agreed upon, per which the tax base of the Irish branch was equal to (i) [10-

15]% of the branch’s operating costs, excluding costs such as charges from Apple affiliates and material

costs; (ii) an IP return of [1-5]% of branch turnover in respect of the accumulated manufacturing process

technology of the Irish branch; and (iii) a deduction for the capital allowances for plant and buildings,

computed and allowed in the normal manner.

4. Preliminary conclusions of the Commission

On 11 June 2014, the Commission opened a formal investigation procedure, because it came to the

preliminary conclusion that the contested tax rulings constituted the granting of State Aid within the

meaning of Article 107(1) of the Treaty on the Functioning of the European Union (the Treaty) by Ireland

to Apple, ASI and AOE, and that that aid is incompatible with the internal market pursuant to Article

107(2) and (3) of the Treaty. The Commission expressed doubts that the profit allocation methods

endorsed by those rulings to determine ASI’s and AOE’s taxable profit in Ireland reflected a

remuneration for ASI’s and AOE’s Irish branches that a prudent independent operator acting

under normal market conditions would have accepted. The Commission also noted several

inconsistencies in the application of the method chosen when determining the profit allocation to AOE

and ASI that do not appear to comply with the arm’s length principle. As a result, the Commission

reached the preliminary conclusion that those rulings resulted in a lower tax burden for those companies

constituting an advantage for the purposes of Article 107(1) of the Treaty. The Commission considered

that advantage to be selective, since it was granted only to ASI and AOE and it put those undertakings in

a more favourable position than other undertakings in a comparable factual and legal position. The

Commission further considered that favourable position selectively granted to the two undertakings to be

based on the discretion of Irish Revenue, which went beyond the simple management of tax revenue by

reference to objective criteria.

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge4

Both the Irish Government and Apple made detailed arguments before the Commission.

Final ruling

(The infographic above has been sourced from the European Commission website and can be accessed

here.)

The Commission ruled as under:

Existence of aid

5. Noting the provisions of Article 107 of the Treaty, the Commission observed that the following

conditions are to be fulfilled for categorization as State aid: (i) there must be an intervention by the State

or through State resources; (ii) the intervention must be liable to affect trade between Member States;

(iii) it must confer a selective advantage on an undertaking; and (iv) it must distort or threaten to distort

competition.

6. The Commission noted that the contested tax rulings were issued by the Irish tax administration.

Further, relying on Commission v. Deutsche Post (EU:C:2010:481), the Commission observed that a

measure by which the public authorities grant certain undertakings a tax exemption which, although not

involving a positive transfer of State resources, places the persons to whom it applies in a more

favourable financial situation than other taxpayers constitutes State aid. The Commission held that the

contested tax rulings resulted in a lowering of ASI’s and AOE’s tax liability in Ireland by deviating from

the tax that those undertakings would otherwise have been obliged to pay under the ordinary rules of

taxation of corporate profit in Ireland. Thus, by renouncing tax revenue that Ireland would otherwise have

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge5

www.taxsutra.com │www.tp.taxsutra.com │www.idt.taxsutra.com │www.lawstreetindia.com │www.orange.taxsutra.com │www.greentick.taxsutra.com

been entitled to collect from ASI and AOE under those rules, the contested tax rulings gave rise to a loss

of State resources.

7. The Commission noted that ASI and AOE are both part of a globally active multinational group

operating in all Member States; therefore, any aid in their favour is liable to affect intra-Union trade.

Noting the business profile of ASI and AOE, the Commission held that, to the extent the contested tax

rulings relieve ASI and AOE of a tax liability they would otherwise have been obliged to pay under the

ordinary rules of taxation of corporate profit in Ireland, the aid granted under those rulings constitutes

operating aid, in that it relieves those undertakings from a charge that they would normally have had to

bear in their day-to-day management or normal activities. Relying on multiple rulings of the Court of

Justice, the Commission held that operating aid in principle would distort competition. The Commission

held that, by relieving such tax liability, the rulings free up the resources of these entities to invest in their

business operations and thereby distort the competition in the market.

8. As regards third condition for finding State aid, the Commission noted that an “advantage” for the

purposes of Article 107(1) of the Treaty is any economic benefit that an undertaking would not have

obtained under normal market conditions, that is to say, in the absence of the State intervention. Thus,

whenever the financial situation of an undertaking is improved as a result of State intervention, an

advantage is present. The Commission held that the contested tax rulings resulted in a lowering of ASI’s

and AOE’s corporation tax liability in Ireland by reducing their annual taxable profits, and thus their

taxable bases, for the purposes of levying corporation tax on those profits under the ordinary rules of

taxation of corporate profit in Ireland. The contested tax rulings therefore confer an economic advantage

on these companies through a reduction in their taxable base.

Existence of a selective advantage

9. With respect to the selective nature of the advantage, the Commission held that, since the

contested tax rulings are individual aid measures granted only to ASI and AOE, a finding that

those measures grant an advantage to ASI and AOE already suffices to conclude that that

advantage is selective in nature.

10. However, for completeness purposes, the Commission also carried out a three-step analysis devised

by the Court of Justice for a fiscal aid scheme to demonstrate its selective nature. The three steps

involved are: (i) identification of the common or normal tax regime applicable in the Member State (the

reference system); (ii) determining whether the tax measure in question constitutes a derogation from

that system, insofar as it differentiates between economic operators who, in light of the objectives

intrinsic to the system, are in a comparable factual and legal situation; and (iii) if the measure constitutes

a derogation from the reference system, then establishing whether that measure is justified by the nature

or the general scheme of the reference system. A tax measure which constitutes a derogation from the

application of the reference system may be justified if the Member State concerned can show that that

measure results directly from the basic or guiding principles of that tax system. If that is the case, the tax

measure is not selective. The burden of proof in the third step lies with the Member State.

Determination of the reference system

11. On the issue of identification of the reference system, the Commission held that the ordinary rules of

taxation of corporate profit in Ireland were to be considered as the reference system. The Commission

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge6

www.taxsutra.com │www.tp.taxsutra.com │www.idt.taxsutra.com │www.lawstreetindia.com │www.orange.taxsutra.com │www.greentick.taxsutra.com

held that all companies subject to tax in Ireland, whether resident or non-resident, are in a comparable

factual and legal situation as regards the ordinary rules of taxation of corporate profit in Ireland. The

Commission noted that the Irish corporate tax system does not distinguish between companies which

derive their profit from market transactions only, such as non-integrated stand-alone companies, and

companies which derive their profit through internal dealings between companies of the same corporate

group or between parts of the same company, such as integrated companies. The Commission held that

differences in the manner of determination of taxable profits of non-integrated and integrated companies

or of branches cannot be observed in a reliable way from the statutory accounts.

Selective advantage resulting from a derogation from the ordinary rules of taxation of corporate profit in

Ireland giving rise to a reduction of the taxable base

12. Regarding Ireland’s contention that Irish tax law does not allow taxes to be imposed on the

basis of general principles, the Commission observed that the arm’s length principle flows from

Article107(1) of the Treaty, which binds the Member States, and from the scope of which national

tax rules are not excluded. The Commission held that “any fiscal measure a Member State adopts,

including a tax ruling endorsing a profit allocation method for determining a branch’s taxable base, must

comply with the State aid rules, which bind the Member States and enjoy primacy over their national

legislation”. Thus, the Commission held that the arm’s length principle applies independently of whether

the Member State in question has incorporated the arm’s length principle into its national legal system.

The Commission clarified that it had not directly applied Article 7(2) and/or Article 9 of the OECD Model

Tax Convention or the guidance provided by the OECD on profit allocation or transfer pricing.

13. Therefore, the Commission held that, if it can be shown that the profit allocation methods

endorsed by Irish Revenue in the contested tax rulings resulted in a taxable profit for ASI and

AOE in Ireland that departs from a reliable approximation of a market-based outcome in line with

the arm’s length principle, those rulings should be considered to confer a selective advantage on

those companies for the purposes of Article 107(1) of the Treaty to that extent.

Selective advantage resulting from Irish Revenue’s acceptance of the unsubstantiated assumption that

the Apple IP licences held by ASI and AOE should be allocated outside of Ireland

14. The Commission held that Irish Revenue’s acceptance of the unsubstantiated assumption that the

Apple IP licences held by ASI and AOE should be allocated outside of Ireland (upon which the profit

allocation methods endorsed by the contested tax rulings are based) results in an annual taxable

profit for ASI and AOE in Ireland that departs from a reliable approximation of a market-based

outcome in line with the arm’s length principle.

15. The Commission observed that the contested tax rulings were issued in the absence of a profit

allocation report or transfer pricing report prepared by Apple. It further noted that, subsequent to its

opening decision, Ireland and Apple produced ad hoc profit allocation reports, prepared by

PricewaterhouseCoopers and Apple’s tax advisor, respectively, to justify the profit allocation methods

endorsed by the contested tax rulings ex post facto, but that they were not available to Irish Revenue at

the time of issue of contested rulings.

16. The Commission noted that, even though Ireland argued that Section 25 of TCA 97 does not require

Irish Revenue to follow the guidance provided by the OECD framework when issuing tax rulings, the

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge7

www.taxsutra.com │www.tp.taxsutra.com │www.idt.taxsutra.com │www.lawstreetindia.com │www.orange.taxsutra.com │www.greentick.taxsutra.com

one-sided methods of profit allocation endorsed in the rulings appear to resemble a transfer pricing

arrangement based on TNMM and operating expenses as profit level indicator as described in the OECD

TP Guidelines.

17. The Commission disagreed with Ireland’s argument that the Apple IP licences held by ASI and AOE

should not be allocated to the Irish branches for tax purposes, since there are no management activities

associated with those licences in those branches. The Commission observed that it was incumbent on

Irish Revenue to first properly examine the assets used, the functions performed and the risks assumed

by those companies through their Irish branches and through the other parts of those companies.

18. The Commission agreed with the territoriality principle concerning the right to tax; however, it

held that the principle does not obviate the need for a tax administration to determine the

allocation of assets used, functions performed and risks assumed by a non-resident company

through its branch and through the other parts of the company, including IP held by the company

as a whole, for the purposes of allocation of profits in line with the arm’s length principle. The

Commission held that Ireland and Apple appeared to confuse the territoriality principle of taxing source

income generated through the Irish branches with a diligence to gather factual information on the

operations of ASI and AOE so as to ensure an arm’s length allocation of assets, functions and risks

within those companies for determining their taxable profit in Ireland.

19. The Commission remarked that, when the contested rulings were in force, both ASI and AOE could

be described as “stateless” for the purpose of residency. The Commission further observed that, during

this period, ASI had no other branches outside of Ireland and the only other branch AOE had outside of

Ireland was in Singapore; however, that branch was never presented by Ireland or Apple as performing

functions that generate the overall profits of AOE.

20. The Commission, based on facts presented to it, observed that, at the relevant time, the head

offices of AOE and ASI were only present on paper, as there was no physical presence of

employees outside Ireland during that period. Thus, the people who performed the functions of the

head office would have been the board of directors. Based on perusal of the minutes of meetings of the

boards of directors, the Commission held that those minutes do not demonstrate that ASI’s and AOE’s

boards of directors performed active and critical roles with regard to the management and effective

control of the Apple IP licenses. The Commission observed that “[i]n a submission to the Commission

describing the discussions in those board meetings, Apple itself did not identify any IP-related

discussions in those minutes when summarizing the activities of the boards”.

21. The Commission also observed that the minutes did not document any discussion relating to cost

sharing arrangements (CSAs), which has been amended several times since 1991. Thus, the

Commission held that, “[c]ontrary to the claim made by Ireland that the boards of ASI and AOE made the

critical decisions to participate in the CSA and also to fund the significant costs arising from participating

in that agreement and the claim made by Apple that the boards decided on various amendments to the

CSA, the minutes of the board meetings do not record any discussion on the 2009 amendment or any

other discussion regarding the CSA or the Apple IP, until the new structure of Apple in Ireland was being

discussed at the end of 2014”. The Commission further observed that, “[w]ith the exception of one

business decision to transfer assets from AOE’s Singapore branch to another Apple group company,

those minutes show that the discussions in the boards of ASI and AOE consisted mainly of

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge8

www.taxsutra.com │www.tp.taxsutra.com │www.idt.taxsutra.com │www.lawstreetindia.com │www.orange.taxsutra.com │www.greentick.taxsutra.com

administrative tasks, that is to say approving accounts and receiving dividends, not active or critical

functions with regard to the management of the Apple IP licenses”.

22. The Commission further noted that the minutes indicated that various functions, including

those of the Board, were outsourced to Apple employees in Ireland, which is contrary to Ireland’s

claim that no business decisions were taken in Ireland. The Commission further held that the fact

that board members of ASI received no remuneration also confirmed that their activities were not

valuable to ASI. Thus, the Commission concluded that, “[n]ot only did those head offices not perform

active or critical functions with regard to the management of the Apple IP licenses, they also did not have

the capacity to perform such functions during the period that the contested tax rulings were in force”.

23. The Commission held that a part of a company that is in no position to manage, control and monitor

a risk should not be allocated such a risk for tax purposes. This reflects the economic reality that a

rational economic operator would not entrust a risk to a counterparty that is not able to assume and

manage such a risk. Thus, the Commission also rejected the allocation of risks and IP functions to the

head office as done in transfer pricing reports submitted by Apple before it.

24. Thus, the Commission held, “[i]n sum, had Irish Revenue properly confirmed whether the Apple IP

licenses held by ASI and AOE should be allocated outside of Ireland before endorsing profit allocation

methods premised on that assumption, it should have concluded that the head offices of ASI and AOE

did not control or manage, nor were they in a position to control or manage, the Apple IP licenses in such

a manner as to derive the type of income recorded by those companies. Consequently, ASI’s and AOE’s

Irish branches, if they were separate and independent companies engaged in the same or similar

activities under the same or similar conditions and taking into account the assets used, the functions

performed and the risks assumed by those companies through their branches and through their

respective head offices, would not have accepted a profit allocation method based on that assumption,

which results in all the profit of ASI and AOE beyond a limited mark-up on a reduced cost base being

allocated to the head offices instead of to those branches”.

25. The Commission noted that ASI’s Irish branch was responsible for executing procurement, sales and

distribution activities associated with the sale of Apple products to related parties and third-party

customers across the EMEIA and APAC regions. Thus, the Commission held that the Irish branch

performs functions crucial to the development of the Apple brand in the local market. Further, the

functions performed by it, like adapting the brand strategy and incurring marketing expenditure, were key

functions for the development of the brand in a given region. Further, the Irish branch assumed a large

risk relating to the performance of the products and technology. In addition, the employees located in

Ireland were classified by Apple as R&D personnel.

26. In respect of AOE, the Commission noted that the Irish branch was responsible for the manufacturing

and assembly of a specialized range of computer products for the EMEIA region. In that capacity, AOE’s

Irish branch developed Apple-specific processes and manufacturing expertise and ensured quality

assurance and quality control functions, which were needed to preserve the value of the brand.

27. Thus, the Commission concluded that allocation of IP licences of Apple outside Ireland could not

have been agreed under an arm’s length condition. Accordingly, the Commission rejected Ireland’s claim

that profit derived from IP should be subtracted from taxable profit in line with the territoriality principle.

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge9

www.taxsutra.com │www.tp.taxsutra.com │www.idt.taxsutra.com │www.lawstreetindia.com │www.orange.taxsutra.com │www.greentick.taxsutra.com

28. Further, the Commission held that the income of ASI and AOE represented active trading income

arising from the branch activity, since there were no employees who could generate such income outside

of Ireland and none of the income could have been considered as income from royalty. The Commission

also observed, based on the annual accounts of ASI and AOE, that the entire income was considered by

Apple as trading income.

29. Ireland and Apple had argued that R&D and the management of Apple IP is centred in and directed

from Apple’s headquarters in the United States. According to Ireland and Apple, it is those contributions

by Apple Inc. employees that drive ASI’s and AOE’s profitability, so that Irish Revenue was right to

exclude profit deriving from those contributions from the taxable profit of ASI’s and AOE’s Irish branches.

However, the Commission rejected this argument, holding that the alleged contributions by Apple Inc.

employees in R&D and the management of Apple IP licences held by ASI and AOE cannot influence the

allocation of profit within ASI and AOE. The Commission noted that the R&D costs of Apple Inc. were

allocated to different entities in proportion to turnover and, consequently, that the profit of each company

– Apple Inc., ASI and AOE – is the difference between sales and all relevant costs, including the yearly

payments for the development of the Apple IP as determined in the CSA.

30. The Commission concluded that the contested tax rulings resulted in lowering corporate tax liability

in Ireland for ASI and AOE, as all profits, except limited mark-up on a reduced cost base, were allocated

outside Ireland as per these rulings. The Commission held that all profit from sales activities, other than

the interest income obtained by ASI and AOE under normal market circumstances, should have been

allocated to the Irish branches of ASI and AOE.

31. Thus, by endorsing the profit allocation methods premised on the unsubstantiated assumption, Irish

Revenue provided a selective advantage to AOE and ASI as compared to non-integrated companies

whose taxable profit reflects prices determined on the market negotiated at arm’s length and whose

taxable profit is subsequently taxed at the same standard corporate tax rate as ASI’s and AOE’s locally

sourced profit. The Commission held that a similar conclusion is reached following the authorized OECD

approach for profit allocation to a PE.

Undervaluation of ASI’s and AOE’s taxable profit due to the inappropriate methodological choices

underlying the one-sided profit allocation methods endorsed by the contested tax rulings

32. Without prejudice to the above-noted conclusions, the Commission held that, even if it is accepted

that Irish Revenue was right in accepting the unsubstantiated assumption about the allocation of Apple

IP held by AOE and ASI outside of Ireland, the methodology used to arrive at taxable profits in Ireland in

the contested ruling was also inappropriate for the following reasons:

• The choice of the Irish branches as the “tested party” is premised on the unsubstantiated

assumption that ASI’s and AOE’s Irish branches perform the “less complex function” as compared to

their respective head offices, since the Apple IP licences had been allocated to the latter for tax

purposes. The Commission held that the activities of the head offices were less complex than those of

the branches.

• The choice of operating expenses as PLI was inappropriate. The Commission noted that

operating expenses as PLI are suitable for a low-risk distributor. But, in view of significant activities

performed by ASI’s Irish branch and the risks assumed, it cannot be characterized as a low-risk

distributor. Thus, the sales-based PLI would have been more appropriate for ASI. Further, AOE, which

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge1

0

www.taxsutra.com │www.tp.taxsutra.com │www.idt.taxsutra.com │www.lawstreetindia.com │www.orange.taxsutra.com │www.greentick.taxsutra.com

was responsible for the manufacturing and assembly of specialized computer products, also assumed

significant risks. Thus, a PLI based on total cost instead of mere operating expenses would have been

appropriate for it.

• For ASI, the 1991 ruling accepted a 12.5% margin on operating expenses, while the 2007 ruling

accepted a 10-15% margin on branch operating expenses. Further, for AOE, the 1991 ruling accepted a

65% margin on branch operating expense up to USD [60-70] million and a 20% margin in excess of that

amount, whereas the 2007 ruling accepted a 10-15% margin on branch operating expense, with an IP

return of 1-5% of branch turnover in respect of the “accumulated manufacturing process technology” of

the Irish branch. The Commission noted that no contemporaneous documentation was prepared to

justify these returns. The Commission rejected employment consideration as a ground for a reduced

margin beyond expenses of USD 60-70 million for AOE. It also rejected the argument that a lower

margin beyond the threshold reflects the underlying economies of scale. It held that incentives similar to

rebates on effective taxation rates aimed at attracting increased activity and employment are not in the

logic of the tax system.

33. The Commission also observed that the 1991 ruling was open-ended, without any revision clause,

and effectively applied for 15 years, until the 2007 ruling was issued. The 2007 ruling, which did have a

revision clause, was also open-ended and applied, according to Apple, for 8 years, until Apple’s new

corporate structure in Ireland was put into place. The Commission observed that an agreement between

a tax administration and a taxpayer that has no end date makes predictions as to future conditions on

which that agreement is based less accurate, thereby casting doubt on the reliability of the method

endorsed by the agreement. The Commission also referred to advance pricing agreements, which are

valid as long as any critical assumptions on which they are based are in place, pointing out that the

contested rulings do not identify any such critical assumptions.

Selective advantage under the limited reference system of Section 25 TCA 97 only

34. Without prejudice to the above-mentioned observations, the Commission also considered whether

the rulings provided a selective advantage to Apple taking Section 25 of TCA 97 as a limited reference

system. Both Ireland and Apple had made such a claim.

35. Ireland had claimed that the application of Section 25 of TCA 97 is not governed by the arm’s length

principle, but rather requires Irish Revenue to exercise judgement by taking into account the particular

facts and circumstances of each case, which may include “the functions performed by any branch, its

interest (if any) in the assets of the company, the nature and level of any risks assumed by the branch,

and the overall contribution made by the branch to the company’s profits”. The Commission observed

that these criteria were the same as the principles laid down under Article 7 of the OECD Model for

allocating profits to a PE. Further, on analysis of Irish Revenue’s ruling practice on the allocation of profit

to the Irish branches of non-resident companies, the Commission observed that the arm’s length

principle underlies the profit allocation method endorsed by Irish Revenue in a number of rulings. Thus,

based on a detailed analysis conducted by the Commission in an earlier part of decision, it concluded

that there was a selective advantage under the contested ruling even if the limited reference system is

considered.

Selective advantage resulting from the exercise of discretion by Irish Revenue in the absence of

objective criteria related to the tax system

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge1

1

www.taxsutra.com │www.tp.taxsutra.com │www.idt.taxsutra.com │www.lawstreetindia.com │www.orange.taxsutra.com │www.greentick.taxsutra.com

36. The Commission further observed that the profit allocation ruling practice of Irish Revenue is too

inconsistent to constitute an appropriate reference system against which the contested tax rulings could

be examined for determining whether ASI and AOE received a selective advantage as a result of the

rulings. Thus, it rejected Apple and Ireland’s argument that the Commission must show that Apple has

been treated favourably as compared to other non-resident companies that have been granted tax

rulings by Irish Revenue for the purposes of applying Section 25 of TCA 97. The Commission held that

examination of such rulings confirmed that the contested tax rulings were issued on the basis of Irish

Revenue’s discretion, in the absence of objective criteria related to the tax system. Therefore, those

rulings should be considered to confer a selective advantage on ASI and AOE for the purposes of Article

107(1) of the Treaty.

Absence of justification by the nature and general scheme of the tax system

37. The Commission held that neither Apple nor Ireland has advanced a conclusive justification for the

provision of a selective advantage by way of the contested tax rulings, although the burden of proof in

that respect lies on the Member State. The Commission reasoned that “it is the endorsement by Irish

Revenue of the profit allocation methods proposed by Apple to determine the taxable profit of ASI and

AOE in Ireland that gives rise to a selective advantage, not the exercise of discretion as such in

endorsing those methods”. The Commission further held that the “conclusion that the contested tax

rulings confer a selective advantage on ASI and AOE does not depend on whether the discretion

afforded to Irish Revenue in granting those rulings is excessive or how Irish Revenue exercised that

discretion, but follows from the fact that those rulings selectively reduce ASI’s and AOE’s Irish

corporation tax liability as compared to economic operators in a comparable factual and legal situation”.

Conclusion on the existence of aid

38. The Commission thus concluded that the contested tax rulings issued by Irish Revenue in favour of

ASI and AOE confer a selective advantage on those companies that is imputable to Ireland and financed

through State resources, which distorts or threatens to distort competition and which is liable to affect

trade between Member States. The contested tax rulings therefore constitute State aid within the

meaning of Article 107(1) of the Treaty.

Beneficiaries of the contested measures

39. Noting that ASI and AOE are ultimately wholly-owned by Apple Inc. and the majority of the members

of ASI’s and AOE’s boards are Apple Inc. employees, the Commission held that Apple Inc., which is the

entity controlling the Apple Group, can also be said to control ASI and AOE through functional, economic

and organic links. It also noted that, since it is the Apple Group which took the decision to incorporate

ASI and AOE in Ireland and decided on the structure, it is the Apple Group as a whole that benefits from

the State aid Ireland granted to ASI and AOE by way of the contested tax rulings. The Commission thus

concluded that, “notwithstanding the fact that the Apple Group is organized in different legal

personalities, that group should nevertheless be considered as a single economic unit benefitting from

the State aid granted by Ireland by way of the contested tax rulings”.

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge1

2

www.taxsutra.com │www.tp.taxsutra.com │www.idt.taxsutra.com │www.lawstreetindia.com │www.orange.taxsutra.com │www.greentick.taxsutra.com

Compatibility of the contested measures

40. Stating that it is the Member State granting the aid which bears the burden of proving that State aid

granted by it is compatible with the internal market pursuant to Article 107(2) or (3) of the Treaty and that

Ireland has not invoked any of the grounds for a finding of compatibility, the Commission observed that

the State aid granted by Ireland through the contested tax rulings is incompatible with the internal

market. The Commission moreover remarked that, considering the contested tax rulings as granting

operating aid to ASI, AOE and the Apple group as a whole, such aid cannot normally be considered

compatible with the internal market under Article 107(3)(c) of the Treaty, in that it does not facilitate the

development of certain activities or of certain economic areas, nor are the tax incentives in question

limited in time, digressive or proportionate to what is necessary to remedy a specific economic handicap

of the areas concerned.

Unlawfulness of the aid

41. The Commission also held that, since Ireland had issued the contested rulings without notifying the

Commission, the same constituted unlawful aid put into effect in contravention of Article 108(3) of the

Treaty.

Alleged procedural irregularities

42. Rejecting Apple and Ireland’s argument that the Commission had infringed their right to be heard, as

the focus of the Commission’s investigation had changed since the adoption of the opening decision, the

Commission stated that the scope of its investigation had remained the same between the opening

decision and the adoption of the current decision, as both concerned the same measures (the 1991 and

2007 tax rulings issued by Irish Revenue), the same beneficiaries (ASI, AOE and the Apple Group) and

the same State aid concerns. The Commission further held that Ireland was given ample opportunity to

make its views known, whereas Apple, as an interested party, only had the right to submit observations

in response to the opening decision, which had duly been done.

Recovery

43. The Commission rejected parties’ accusation that the Commission had infringed the principle of legal

certainty due to prolonged lack of action, stating that, from the moment that the Commission could have

become aware of the rulings (21 May 2013), it took action within less than a month (12 June 2013).

44. The Commission concluded that recovery should include aid granted from 12 June 2003 until 27

September 2014, which is the date on which ASI’s and AOE’s 2014 fiscal year ended. The Commission

thus held that “all profits from the business activities of ASI and AOE should, as a starting point, be

allocated to their respective Irish branches for the period 12 June 2003 to 27 September 2014 for the

purposes of calculating ASI’s and AOE’s corporation tax liability under the ordinary rules of taxation of

corporate profit in Ireland. In addition, interest income from property of the Irish branches which has

been identified by Apple and Ireland in the statutory accounts should be allocated to the Irish branches

of ASI and AOE”.

45. The Commission allowed Apple to claim the following deductions from the profit to be allocated to the

Irish branches of ASI and AOE, to the extent it is sufficiently evidenced:

45 key takeaways of European Commission's

Apple State aid ruling

News item offered by Taxsutra, week 51, 23 December 2016

Pa

ge1

3

www.taxsutra.com │www.tp.taxsutra.com │www.idt.taxsutra.com │www.lawstreetindia.com │www.orange.taxsutra.com │www.greentick.taxsutra.com

a. interest and investment income attributable to ASI’s and AOE’s head offices derived from the

passive management of liquidity, which has been outsourced by the board of directors of ASI and

AOE to Braeburn, as reflected in the minutes of the board meetings; this does not include interest

income from property of the Irish branches which has been identified by Ireland and Apple in the

statutory accounts;

b. capital allowances under the 1991 ruling to the extent that the limitation of the drawing-down of

capital allowances leads to a disadvantage for Apple; and

c. the profits of AOE’s Singapore branch that were subject to taxation in Singapore.

Disclaimer:

The information contained in this communication is intended solely for the use of the individual or entity

to whom it is addressed and others authorized to receive it. If you are an un-intended recipient, please

notify us immediately by responding to this email and then delete it from your system. Any action based

on content in this communication shall be at the sole risk, responsibility and liability of the individual

taking such action. These updates shall not under any circumstance be construed as any kind of

professional advice or opinion and we expressly disclaim any and all liability for any harm, loss or

damage, including without limitation, indirect, consequential, special, incidental or punitive damages

resulting from or caused due to your reliance and actions/inactions on the basis of this communication.

© TAXSUTRA All rights reserved

23 December, 2016

About Taxsutra:

Taxsutra.com is a one stop destination that equips tax practitioners on a real-time basis with updates

and analysis of all income tax rulings and news both domestic and international. With its team of experts,

Taxsutra.com tracks developments in Income Tax Department, Central Board of Direct Taxes (CBDT)

and Finance Ministry, including rulings from Income Tax Appellate Tribunal, AAR, High Court and

Supreme Court to give you an information and competitive advantage on all tax related matters. Built on

an interactive platform, Taxsutra includes discussion forums, expert commentaries from industry

stalwarts, white papers and conversations that makes it the most vibrant source for tax practitioners,

taxpayers and tax regulators at once.

For further details relating to subscription to Taxsutra.com and pricing, contact [email protected].