1/21

A generalized model of ground lease pricing

Marcin Anholcer1 and Maria Trojanek2

July 16, 2017

Abstract

In the paper we presented a generalization of Mandell’s Model for the estimation of ground lease

pricing. We adjusted the model so that it fits in particular the Polish legal regulations and situation on

Polish real estate market. Our model involves in particular two issues. The first is the perpetual

usufruct, a form of possessing the ground similar to the long-term lease, but having some specific

features. Another generalization consists in allowing the lease rent adjustments made after some fixed

periods (i.e., we consider the situation where the payments are fixed during some periods defined in

the contract).

Keywords: ground lease, ground rent, perpetual usufruct

1. Intoduction

The public real estate management in Poland is governed by the Act on Real Estate Management

(Journal of Laws of 2014, item 518) and private ones in the Civil Code (Journal of Laws 1964, item 93,

as amended).

Legal regulations provide that real estate may be the subject of sale, lease and perpetual usufruct (this

right applies only to properties owned by the public, i.e. Treasury and local government units).

The right of perpetual usufruct possesses features similar to the perpetual lease rights of other

countries, although these rights vary. In Poland, in addition, there is the right of long-term lease, used

in very limited way. Choice of forms of real estate management (sale, perpetual usufruct or lease)

should be made taking into account the legal provisions and the objectives and criteria for the

1 Poznań University of Economics and Business

Faculty of Informatics and Electronic Economy Al. Niepodległości 10, 61-875 Poznań, Poland Email: [email protected]. Corresponding author.

2 Poznań University of Economics and Business Faculty Management Al. Niepodległości 10, 61-875 Poznań, Poland Email: [email protected].

2/21

management of landowners, as well as the expectations and benefits of potential buyers, perpetual

usufructors and tenants.

The study attempted to identify the parameters determining the choice of management form (sales,

perpetual usufruct or lease) of land, taking into account the interests of each party to the transaction

(owner and tenant / perpetual usufructor). The presented model enables the determination of limit

rents, which equates to updated revenues from perpetual usufruct or sale of real estate.

1.1. Legal basis for perpetual usufruct

Perpetual usufruct is one of the forms of management of public real estate (properties owned by the

State Treasury and local government units or their unions). In the Polish legal system perpetual

usufruct occurred more than half a century ago (1961), when the system of state ownership was the

dominant form of ownership. The legislature intended this right to regulate the ownership relations

between the state and the entities of the private sector. The current regulations of perpetual usufruct

significantly differ from those introduced in 1961 with the Law on the Economy of Land in Cities and

Settlements (Journal of Laws of 1961 no. 32 item 159; see Winiarz 1967, Truszkiewicz 2006 for details).

In addition, despite the decreasing presence of the political reasons for the introduction of this right,

the perpetual usufruct continues to play an important role in the system of rights in rem and affects

various aspects of social and economic life.

Perpetual usufruct is an instrument permitting long-term (40 to 99 years) usage of land without the

need to involve capital in the amount equivalent to the acquisition of the ownership.

For land property put into perpetual usufruct, the first fee and annual fees are collected (Real Estate

Management Act of 21 August 1997, Article 71, item 1). These fees are determined at a percentage of

the land price determined in accordance with the provisions of art. 67 of the cited Act i.e. price

determined on the basis of value. If land property is given for perpetual usufruct by auction, the basis

for the calculation of such fees is the price obtained during the auction. On the other hand, if the right

of perpetual usufruct is established by the open market rules, the price that is the basis for the

calculation of the first and the annual fee is the price of the property determined at a level not lower

than its market value. The amount of first and annual fees varies and depends on the specific purpose

of the contract. The first fee amounts to 15-25% of the land price. On the other hand, the percentage

of annual fees may be e.g. (Art.72, item 3):

3/21

− for land properties committed to the defense and security of the state including fire protection –

0.3% of the price,

− for land properties committed for charity purposes and for non-profit caring, cultural, curative,

educational, scientific or research and development activities – 0.3% of the price,

− for land properties made for agricultural purposes – 1% of the price,

− for land properties completed for residential purposes, for the implementation of technical

infrastructure and other public purposes and sports activities – 1% of the price,

− for land properties for tourism – 2% of the price,

− for other land properties – 2% of the price.

The annual fee may be increased (Article 76, item 1) by the governor (in relation to property owned by

the State Treasury) or by a resolution of the appropriate council or regional government. An increase

in the rate may take place before the property is handed over for perpetual usufruct and is for real

estate for which the annual fee, due to the purpose of putting the property, is 3%. In some cases, the

competent authority may grant a discount (Article 73, Paragraph 2a, item 3).

The first payment is made in the year in which the perpetual usufruct was established, and the annual

fees are paid during the perpetual usufruct, until 31 March of each year, in advance for the given year.

Thus, the amount of proceeds from these charges is dependent on:

− regulations that the municipality does not influence (interest rates),

− the level of prices achieved on auctions or the value of real estate delivered in perpetual usufruct

in the open market mode,

− the adopted resolutions on granting discounts on established fees.

Annual fees for perpetual usufruct vary over time, taking into account changes in the value of land

properties. According to Art. 77 item 1, the annual fee for perpetual usufruct is subject to updating no

more than once every 3 years, provided the value of the property changes. The updated annual fee is

determined using the fixed percentage of the current level from the market value as of the update

date.

A detailed regulation was introduced in two cases. If the value of the property as at the date of

updating the annual fee would be lower than the price of that real estate determined on the date of

its submission for perpetual usufruct, then the update of the fee will not be made. This provision shall

apply to immovable property transferred for perpetual usufruct of property for a period of 5 years

from the date of conclusion of the contract for the transfer of land title to perpetual usufruct (Article

77 item 2). If the updated annual fee is at least twice the current annual fee, the perpetual user pays

an annual fee equal to twice the current annual fee. On the other hand, the remaining amount, more

4/21

than double the current fee, is divided into two equal parts, which increase the annual fee in

subsequent years.

The annual fee is updated ex officio or at the perpetual usufructor application (the reason is usually

the reduction of the value of the property). To reassume the above, the updating of annual fees for

perpetual usufruct is possible:

− no more than once every three years,

− provided that there has been a change in the market value of the land property.

1.2. Legal basis for lease

Unlike perpetual usufruct, the lease institution is a form of ownership known not only in Poland, but

also in other European countries as well as in other continents.

In Poland, legal regulations of lease agreements, as civil law institutions, are contained in the provisions

of the Civil Code Act of 23 April 1964 (Articles 659-709). As stated in Article 693 of the Civil Code by

the lease agreement, the landlord undertakes to give the tenant the property to use and retrieve the

property for a specified or unspecified period of time, and the tenant agrees to pay the rentee the

agreed rent. The lessee has the right to use the property, i.e. the income it earns, but is obliged to take

care of the proper condition of the leased property (e.g. carry out repairs at its own expense) and

return the object at the end of the lease term in a specified contract.

The subject of the lease may be real estate, machinery, equipment, means of transport and other

property. The most often leased property is a public or private real estate. In the case of public

properties, because of the presence of the perpetual usufruct, long-term lease (up to 30 years) is used

in relatively small terms.

Communes usually lease land for a fixed term (up to three years) with the option of renewing the lease.

Leases are usually applied to land whose destination is different (they are reserves of land for future

public purposes) or not specified (no local land use plans). When land is leased, the landlord does not

bear the cost of maintaining property, providing security, and is gaining the rent for the duration of

the lease.

The scope of use of lease or detailed decisions vary from country to country and changes over time.

However, the most common issues that are resolved when entering into a lease agreement include

the following (see e.g. Trojanek 2015):

− property of buildings or objects made by the lessee,

− duration of the contract and the possibility of its renewal,

5/21

− settlements for expenditures incurred on the ground,

− level and updates of lease rental rates,

− basis for determining the rent of the lease,

− possibility to buy land by the lessee,

− possibility of subletting,

− way of land management,

− other arrangements such as the proper maintenance of buildings located on land, real estate

insurance, etc. (Trojanek 2015).

The source of potential problems associated with operating the lease may be (see e.g. Mandell 2001,

Nystrom 2007):

− lack of adequate change in lease rates in relation to changes in land value,

− resistance and opposition of tenants caused by changes in lease rates,

− difficulties and costs involved in valuing and securing the interest of each of the parties to the

lease,

− problems with how to set lease rates (most often are estimates rather than market rates)

− widespread presence of individual negotiations instead of market or auction procedures,

− costs associated with the lease being sometimes higher than the cost of selling the land,

− lack of benefit for the owner in the case of non-economic use of land by the lessee.

1.3. Lease vs. perpetual usufruct

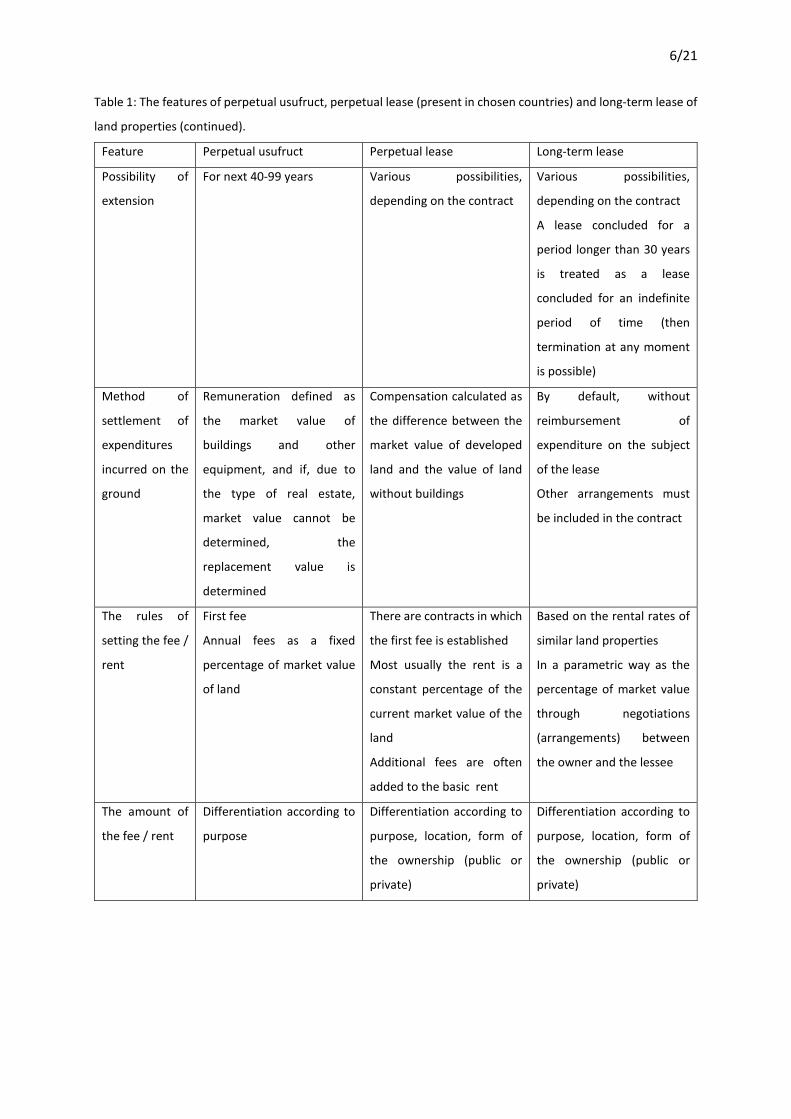

We summarized the basic features of lease and perpetual usufruct in Table 1.

Table 1: The features of perpetual usufruct, perpetual lease (present in chosen countries) and long-term lease of

land properties.

Feature Perpetual usufruct Perpetual lease Long-term lease

Ownership of

buildings

Pepretual usufructor Lessee Lessor

(If the lessee built the

building, they can claim for

reimbursement)

Duration 40-99 years Depending on country, e.g.

20-30 years, 50-99 years,

200 or 999 years

No longer than 30 years

6/21

Table 1: The features of perpetual usufruct, perpetual lease (present in chosen countries) and long-term lease of

land properties (continued).

Feature Perpetual usufruct Perpetual lease Long-term lease

Possibility of

extension

For next 40-99 years Various possibilities,

depending on the contract

Various possibilities,

depending on the contract

A lease concluded for a

period longer than 30 years

is treated as a lease

concluded for an indefinite

period of time (then

termination at any moment

is possible)

Method of

settlement of

expenditures

incurred on the

ground

Remuneration defined as

the market value of

buildings and other

equipment, and if, due to

the type of real estate,

market value cannot be

determined, the

replacement value is

determined

Compensation calculated as

the difference between the

market value of developed

land and the value of land

without buildings

By default, without

reimbursement of

expenditure on the subject

of the lease

Other arrangements must

be included in the contract

The rules of

setting the fee /

rent

First fee

Annual fees as a fixed

percentage of market value

of land

There are contracts in which

the first fee is established

Most usually the rent is a

constant percentage of the

current market value of the

land

Additional fees are often

added to the basic rent

Based on the rental rates of

similar land properties

In a parametric way as the

percentage of market value

through negotiations

(arrangements) between

the owner and the lessee

The amount of

the fee / rent

Differentiation according to

purpose

Differentiation according to

purpose, location, form of

the ownership (public or

private)

Differentiation according to

purpose, location, form of

the ownership (public or

private)

7/21

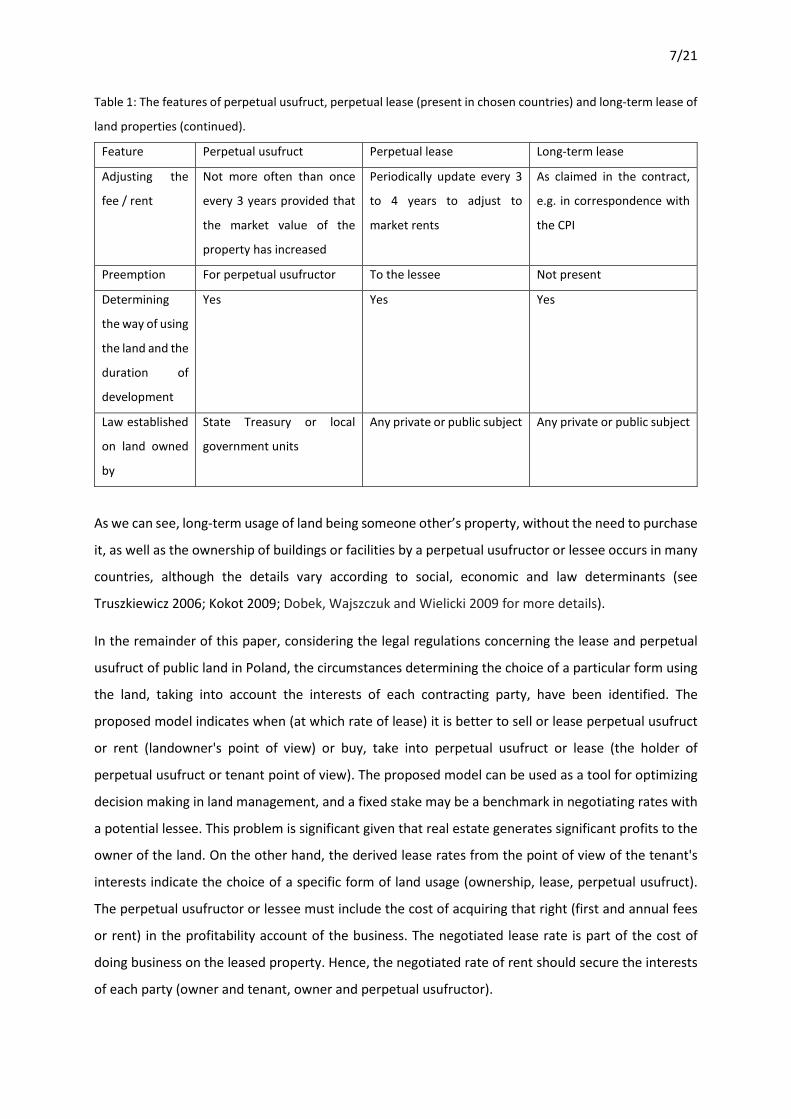

Table 1: The features of perpetual usufruct, perpetual lease (present in chosen countries) and long-term lease of

land properties (continued).

Feature Perpetual usufruct Perpetual lease Long-term lease

Adjusting the

fee / rent

Not more often than once

every 3 years provided that

the market value of the

property has increased

Periodically update every 3

to 4 years to adjust to

market rents

As claimed in the contract,

e.g. in correspondence with

the CPI

Preemption For perpetual usufructor To the lessee Not present

Determining

the way of using

the land and the

duration of

development

Yes Yes Yes

Law established

on land owned

by

State Treasury or local

government units

Any private or public subject Any private or public subject

As we can see, long-term usage of land being someone other’s property, without the need to purchase

it, as well as the ownership of buildings or facilities by a perpetual usufructor or lessee occurs in many

countries, although the details vary according to social, economic and law determinants (see

Truszkiewicz 2006; Kokot 2009; Dobek, Wajszczuk and Wielicki 2009 for more details).

In the remainder of this paper, considering the legal regulations concerning the lease and perpetual

usufruct of public land in Poland, the circumstances determining the choice of a particular form using

the land, taking into account the interests of each contracting party, have been identified. The

proposed model indicates when (at which rate of lease) it is better to sell or lease perpetual usufruct

or rent (landowner's point of view) or buy, take into perpetual usufruct or lease (the holder of

perpetual usufruct or tenant point of view). The proposed model can be used as a tool for optimizing

decision making in land management, and a fixed stake may be a benchmark in negotiating rates with

a potential lessee. This problem is significant given that real estate generates significant profits to the

owner of the land. On the other hand, the derived lease rates from the point of view of the tenant's

interests indicate the choice of a specific form of land usage (ownership, lease, perpetual usufruct).

The perpetual usufructor or lessee must include the cost of acquiring that right (first and annual fees

or rent) in the profitability account of the business. The negotiated lease rate is part of the cost of

doing business on the leased property. Hence, the negotiated rate of rent should secure the interests

of each party (owner and tenant, owner and perpetual usufructor).

8/21

2. Literature review

Various legal and financial aspects of leasing attracted some attention of the researchers in the past

years. Let us recall some of the works.

Long (1977) studied the relationships between leasing and the cost of capital. Lewis and Schallheim

(1992) studied the question whether leases and debts should be treated as substitutes (which is a

rather common assumption) or rather as complements. The same issue was studied by Yan (2006). Liu,

Liu and Zhang (2016) investigated the relation between the asset liquidation values and real estate

firm’s financing choice. Clapham and Gunnelin (2003) considered the term structure of lease rates,

where both rents and interest rates are were stochastic. In particular, they derived equilibrium

relationships in a general continuous time setting. Lally and Randal (2004) investigated the influence

of a ratchet clause on the rental rate for a lease of periodically re-evaluated ground.

Fallis (1988) discussed the legal issues of lease, in particular he performed the public choice analysis of

the rent control. Mooradian and Yang (2002) studied the influence of the assymetric information on

the choice of lease type. Özdilek (2016) studied the property valuation with separate values of land

and buildings, based on example of Montreal. Pope, Gallimore and Shi (2016) investigated the risk

related to a leasehold property from the investor’s point of view. Similar topic were investigated by

Rabbani et al. (2015). Sevelka (2011) studied the influence of the rent reset clause on the valuation in

the ground lease problem. Yoshida, Seko and Sumita (2016) studied the rent term premium for

cancellable leases, by modelling the lessor’s tradeoff between the costs of leasing and the costs of

cancellation.

Benjamin and Chinloy (2004) developed an option – theoretic model of a retail lease. In particular, they

studied economic tradeoffs between base rent, security deposit and percentage rent provisions.

Capozza and Sick (1991) developed the model for valuing leased properties that involved the option to

upgrade or redevelop. Similar topic was studied by Dale-Johnson (2001). Halim and Jaaman (2013)

developed a mathematical model for a specific type of contract, named AITAB. McCann and Ward

(2004) analyzed the rental payments using a multi-period stock inventory model and show that the

factor that influences most the tenat’s value of the land is the duration of the lease. Stanton and

Wallace (2009) proposed a no-arbitrage based lease pricing model. Steele (1984) considered a lease

valuation model using difference equations. Wheaton (2000) presented a two-period model for retail

rental contracts. Country-specific models and case studies with respect to chosen factors were

presented also e.g. by Walters and Kent (2000), Guntermann and Thomas (2005), Tian (2006),

Kaganova, Akmatov and Undeland (2008), Guarino, Chehrazi and Bohl (2014), Irumba (2015).

9/21

Several papers in this subject were published by Jefferies (1997a, 1997b, 1998, 2005a, 2005b, 2005c).

In particular, he considered Lessor’s Return Model and used it to analyze various aspects of the real

estate market, in particular in New Zealand. The model was further developed by Mandell (2001,

2002). A similar approach, but with simplified formulae, were used by Trybusz (1993). See next section

for further discussion of this topic.

3. The Model of Mandell

As we already mentioned above, the main goal of our paper is presentation of a model for ground

lease pricing that would be applicable in countries having legal situation similar to Poland. Our model

is a generalization of the combined model applied by Mandell (2002). In particular, it involves

additional form of ground rental, called the right of perpetual usufruct (RPU).

The model of Mandell involves two sides of the contract: lessor and lessee. Let us first recall the

Lessor’s Return Model (LRM) presented in this article. It was firstly introduced by Brown. Although not

published, it was referred to by Jeffries (1997) and a similar model was considered by Brown in another

context (Brown 1995).

Let � denote the initial ground rent, that is fixed for � periods and then may be changed according to

a growth rate that lessors expects to be equal to �. Then the present value of the future stream of

perpetual payments equals to (c.f. Mandell 2002, formulae (1-2)):

���� = � 1 − 1 + ���� � �1 + �1 + ������� = � 1 + �� − 11 + �� − 1 + ���.

Here denotes the discount rate assumed by the lessor. In the LRM, the lessor has to choose between

selling and leasing the property. Let us denote the present market value of the property by �. The

ground rent is usually defined as a percentage � of the market value:

� = ��. The lessor prefers leasing the land to selling it if the preset value of all the payments is not less than

the present market price i.e., when

���� ≥ �. This means that the ground rent rate � must satisfy the condition (c.f. Mandell 2002, formula (5)):

� ≥ ���� = 1 + �� − 1 + ���1 + �� − 1 .

10/21

On the other side of the market there is the lessee, who also considers two possible decisions: leasing

or buying the property. In the Lessee’s Affordability Model (LAM) presented by Jefferies (1997), the

present value of leasing the land and the present value of freehold are compared. It is assumed that

the buyer needs to finance the buying by through loans and the interest rate (i.e., the cost of capital)

equals to �. It is also assumed, however, that in the case when there is a choice between buying the

property for � and leasing it for ��, the psychological aspects will make the decision maker to choose

the freehold. For that reason, Jefferies assumes that the discount rate on the leasing side of the

equation should be less than �. To be more specific, it is defined as

� = ��, where � ∈ 0,1" is the reduction ratio (also called �-factor). The present value of leasing for one

period is equal to (c.f. Mandell 2002, formula (8)):

#�$ = %� 1 − 1 + �����

where % is the rent expressed as the percentage of the market value �. The present value of the

freehold financed with loan (for one period) is in turn expressed by the formula (c.f. Mandell 2002,

formulae (9-10)):

#�& = �� 1 − 1 + ����� = �1 − 1 + �����. Obviously, the lessee will prefer the leasing variant if

#�$ ≤ #�&

i.e., when (c.f. Mandell 2002, formula (13)):

% ≤ %� = � 1 − 1 + ����1 − 1 + ����. As indicated by Mandell (2002), this model is not satisfactory. The main disadvantage is that it is not

completely clear how to compute the �-factor. To be more specific, it is necessary to introduce LAM

to derive the correct value of �, but it is necessary to know the value of � in order to introduce LAM

(see Mandell (2002) for details and for the discussion of other disadvantages of Jefferies’ approach).

This is why another model was proposed. We fully agree with Mandell that this model reflects the

reality in a much better way. Let us assume that the lessee expects that the future growth rate (in the

period of length �) of the market value � of the property equals to ℎ. They also expect that the present

11/21

value of the benefits of possessing (not necessarily of being the owner of) the property is equal to ).

Under such assumptions, the present value of the net benefits of the freehold equals to

#�&* = ) + +1 + ℎ��1 + ��� − 1, �, while the present value of the leasing is (c.f. Mandell 2002, formula (14)):

#�$* = ) − %� 1 − 1 + ����� . Since the lessee chooses the lower value, the present value of the benefits from leasing must be not

less than the present value of the benefits from the freehold, which means that the following condition

must hold (c.f. Mandell 2002, formula (16)):

% ≤ %�-� = � 1 + ��� − 1 + ℎ��1 + ��� − 1 . The combined model assumes that the payment rate lies between ���� and %�-� . Let us present its

generalization, involving specific legal conditions present in Poland.

4. The Generalized Model

As mentioned above, third variant of possessing the land occurs in Poland – It is the perpetual usufruct.

In this case not only the regular rent, but also the initial payment . = /� has to be paid (here / is the

initial payment expressed as the ratio of the property’s market price �). Then the yearly rent is

calculated as the ratio of the market price �. The contract ends after 0 years and may be renewed. In

the remainder of this section we are going to present the estimations of the present value of all the

income from the perspective of the property’s owner, then from the perspective of the potential user.

In the last subsection we will compare the results in order to define the intervals to which the payment

rates should belong.

4.1. The Owner’s Perspective

First possible decision of the owner may be to sell the property. In such case, the present value of the

income may be estimated by the market price of the property:

#�1 = �.

12/21

Next possible choice is to lease the property. It may take two forms: the perpetual usufruct and the

regular lease. Let us start with the analysis of the first form of leasing. In the beginning, the initial

payment is made. As mentioned before, it is equal to . = /� i.e.,

. = /#�1. Then, each year, the lessee needs to pay the yearly rent � = �2�, where �2 denotes the rate and �

the market price. The payment is fixed during some period expressed in number of years (denoted by 32) and then is adjusted according to the yearly increment rent 42, often deduced from the increment

of the property’s market price. This means that the yearly payment (in constant prices) increases after

each 32 years by the growth factor

� = �1 + 421 + �56 , where is the expected discount rate. Since the total number of years 0 of the perpetual usufruct does

not need to be divisible by the number of years, where the rent is fixed, we need to distinguish the

number of full periods and the remainder. The number of full periods during which the payment is

fixed, will be denoted by 02� and may be computed from the formula:

02� = 7 0328 = 0 div 32, where ⌊⋅⌋ denotes the floor function i.e., the biggest integer not greater than the argument (e.g., ⌊1.2⌋ = 1, ⌊13.77⌋ = 13), while div is the integer division function. The number of remaining years

(i.e., the number of years in the last period not longer than 32, where the payment remains fixed) is

then equal to

02C = 0 − 3202� = 0 mod 32,

where mod denotes the remainder of the integer division. This means that the value of the yearly

payments during 32 years after 3 changes of the payment rate (3 = 0,1, … , , 02� − 1), at 332 years from

the beginning (i.e., after 3 fixed payment periods) equals to

� �2�1 + �G56

G�C = �2� × 1 − 1 + ��56 . This means that the present value of the stream of all the payments made during all the complete fixed

payment periods is equal to

13/21

�2� × 1 − 1 + ��56 × � �GI6JG�� = �2� × 1 − 1 + ��56 × � �1 + 421 + �56GI6J

G��

= �2� × 1 − 1 + ��56 × 1 − K1 + 421 + L56I6J

1 − K1 + 421 + L56 . The present value of the stream of the payments made during the remaining 02C years equals to

� �2�1 + 42�56I6J1 + �56I6JMGI6NG�C = �2� × 1 − 1 + ��I6N × �1 + 421 + �56I6J .

For simplicity of the further notation, let us define the factor O2 as

O2 = 1 − 1 + ��56 × 1 − K1 + 421 + L56I6J

1 − K1 + 421 + L56 + 1 − 1 + ��I6N × �1 + 421 + �56I6J . The total income of the property’s owner is equal to the sum of the present values of the initial

payment, yearly payments and the discounted future value of the property, including the expected

average increase of its value 4. Taking into account the above considerations, the present value of the

income after choosing the variant of the perpetual usufruct is equal to

#�2 = /� + �2O2� + �1 + 41 + �I �. Note that if the payments may by adjusted each year i.e., when 32 = 1, the formula for O2 simplifies

to the form

O2 = 1 − K1 + 421 + LI − 42 .

Similar considerations allow us to analyze the case of regular lease contract. This time, the number of

years in a fixed payment period will be denoted by 3P. The number of such complete periods equals to

0P� = 7 03P8 = 0 div 3P ,

while the number of years in the remainder is equal to

0PC = 0 − 3P0P� = 0 mod 3P . As before, if we define the factor

14/21

OP = 1 − 1 + ��5Q × 1 − K1 + 4P1 + L5QIQJ

1 − K1 + 4P1 + L5Q + 1 − 1 + ��IQN × �1 + 4P1 + �5QIQJ , then the present value of the total income of the owner is equal to

#�P = �POP� + �1 + 41 + �I �, In particular, if 3P = 1 (i.e., if the yearly payments are adjusted each year), then

OP = 1 − K1 + 4P1 + LI − 4P .

Given the three variants, the owner will choose the lease if #�P ≥ maxT#�1, #�2U. This allows us to

derive the minimum payment rate that is acceptable for the owner. First, let us compare lease with

selling the property:

#�P ≥ #�1, �POP� + �1 + 41 + �I � ≥ �, �P ≥ 1 − K1 + 41 + LI

OP .

Similarly, the comparison with the perpetual usufruct allows us to find the following lower bound:

#�P ≥ #�2, �POP� + �1 + 41 + �I � ≥ /� + �2O2� + �1 + 41 + �I �

�P ≥ / + �2O2OP . Finally, the yearly payment rate must satisfy the condition

�P ≥ max V1 − K1 + 41 + LIOP , / + �2O2OP W.

if the owner is supposed to choose the leasing.

4.2. The User’s Perspective

The calculations similar to the ones performed in the previous subsection allow us to estimate also the

costs of the potential user (buyer or lessee). We assume that the user may cover part of the cost using

15/21

the loan with interest rate 4X, that must be paid back in 0X years. We assume that the loan is paid with

decreasing instalments, 0X fixed principal payments and respective interest payments (in case of

different payment schedule, one may easily transform the formulae given below using the elementary

rules of financial mathematics). We assume that part of the cost, Y1 < 1, must be paid in cash. Then

the total present value of the cost of buying the property is equal to

#�1⋆ = Y1� + 1 − Y1� × �0X × 1 − K1 + 4X1 + LI\1 − 1 + 4X1 + .

We may observe that

#�1⋆ = #�11 + ]1�, where

]1 = Y1 + 1 − Y1�0X × 1 − K1 + 4X1 + LI\1 − 1 + 4X1 + − 1 > 0

(i.e., #�1⋆ > #�1).

Similarly we can estimate the present value of the cost of perpetual usufruct and lease. In both cases

we take into account the fact that when the contract ends, the property goes back to the owner.

Let us consider the perpetual usufruct first. We assume that the potential user may cover part of the

initial payment (Y2) using the bank loan. This means that the present value of the cost of the perpetual

usufruct is equal to

#�2⋆ = /#�11 + ]2� + �2O2�, where

]2 = Y2 + 1 − Y2�0X × 1 − K1 + 4X1 + LI\1 − 1 + 4X1 + − 1 > 0.

Finally, the present value of the total cost corresponding with lease equals to

#�P⋆ = �POP� = #�P − �1 + 41 + �I �.

The reasoning similar as in the previous section leads us to the conclusion, that the user will accept the

form of leasing if #�P⋆ ≤ minT#�1⋆, #�2⋆U. This allows us to estimate the highest payment rate

acceptable by the user. We have

#�P⋆ ≤ #�1⋆, �POP� ≤ �1 + ]1�,

16/21

�P ≤ 1 + ]1OP , and

#�P⋆ ≤ #�2⋆, �POP� ≤ /�1 + ]2� + �2O2�, �P ≤ /1 + ]2� + �2O2OP .

Thus, if the user is supposed to choose the form of leasing, the following condition must be satisfied:

�P ≤ min `1 + ]1OP , /1 + ]2� + �2O2OP a.

4.3. The range of acceptable leasing rates

Taking together the inequalities deduced in the two preceding subsections, we obtain the following

interval for the leasing rate:

�P ∈ bmax V1 − K1 + 41 + LIOP , / + �2O2OP W , min `1 + ]1OP , /1 + ]2� + �2O2OP ac.

Only if the above interval is nonempty, the leasing may occur. This is not an obvious thing. Although it

is straightforward to see that

1 − K1 + 41 + LIOP < 1 + ]1OP

and

/ + �2O2OP < /1 + ]2� + �2O2OP , the relations between all four parts of the formula may be various in the general setting. This means,

that under some specific conditions, the leasing is not acceptable.

4.4. The perpetual usufruct payments

Although the yearly payments in perpetual usufruct are fixed by the law and thus not negotiable, one

could wonder whether they are set at the right level. Of course changing the law is much more difficult

17/21

than signing a contract, but they are still possible. The reasoning similar as above allow us to define

the acceptable range for the yearly payment in the perpetual usufruct. If it is the variant to choose

against the selling/buying the property, then the following must hold:

#�2 ≥ #�1, #�2⋆ ≤ #�1⋆. The first inequality is equivalent to

/� + �2O2� + �1 + 41 + �I � ≥ �, i.e.,

�2 ≥ 1 − / − K1 + 41 + LIO2 .

Similarly, the second one leads us to

/�1 + ]2� + �2O2� ≤ �1 + ]1�, �2 ≤ 1 + ]1 − /1 + ]2�O2 .

It follows that the rate of yearly payment in the perpetual usufruct should belong to the following

interval:

�2 ∈ b1 − / − K1 + 41 + LIO2 , 1 + ]1 − /1 + ]2�O2 c.

5. Conclusion

The generalization of Mandell’s model presented in the article allows to involve various additional

elements that are present e.g. in the Polish real estate market. In particular, we took under

consideration the third possible form of possessing the ground, which is the perpetual usufruct. We

also analyzed the more general setting, where the yearly payments are not adjusted every year, but

nay be fixed for some period, defined in the contract (which is also the case in Polish market).

This theoretical paper was used as a base for computational experiments. Currently we are preparing

a follow-up paper, in which we present the results of simulations performed for various scenarios, with

the data specific for Polish real estate market. The first conclusions from the experiments are proving

18/21

our suppositions that the leasing rates used in Poland in the leasing contracts between local

communities and individuals have been improperly defined.

Another conclusion is that the yearly payment rates in perpetual usufruct are often incorrect. We are

aware of the fact that any changes in the law are a difficult and time consuming process, but maybe

our conclusions could be a starting point to the further considerations in this area.

There are some limitations of the presented model. For instance, we assumed that the durations of

leasing and perpetual usufruct are equal. This could be overcome by introducing two, possibly distinct,

durations. However, since after ending one leasing contract, another may be started immediately, one

could treat such a leasing as a continuous process. Another limitation are the assumptions about the

constant character of the parameters. Of course, the parameters like interest rates change in time, but

it is almost impossible to predict their future values, especially in emerging markets like Poland. For

that reason some simplifications are necessary. On the other hand, we discuss the present situation

and decisions of the owner and possible user, so analyzing the possible scenarios based upon the

current market situation seems to be reasonable, if we assume the symmetry of information. Yet

another problem is how to estimate the values of the parameters, even if we assume that they will be

constant in the future. This is however not a significant problem, since we may assume again that both

sides of the contract have the same knowledge about the market and so if one of the sides

underestimates or overestimates any of the parameters then so will do the other, which finally will

increase or decrease both estimates of present values of income and cost and finally will have a small

influence on the estimation of rates.

As we mentioned in the beginning of this section, we performed some numerical experiments. We

think that also performing simulations for other countries, having similar legal situation, would be

interesting. We also think that the model itself could be further developed by introducing additional

parameters, as expected income of the user resulting from the possession of the property compared

with other possible forms of earning.

References

1. Benjamin J. D., Chinloy P. (2004), The Structure of a Retail Lease, Journal of Real Estate

Research 26(2), 223–236.

2. Brown G.R. (1995), Estimating effective rents, Journal of Property Finance 6(2), 33–42.

3. Capozza D. R., Sick G. A. (1991), Valuing Long-Term Leases: the Option to Redevelop, Journal

of Real Estate Finance and Economics 4, 209–223.

19/21

4. Clapham E., Gunnelin Å. (2003), Rental Expectations and the Term Structure of Lease Rates,

Real Estate Economics 31(4), 647–670.

5. Dale-Johnson D. (2001), Long-Term Ground Leases, the Redevelopment Option and Contract

Incentives, Real Estate Economics 29(3), 451–484.

6. Dobek A., Wajszczuk K., Wielicki W. (2009), Użytkowanie wieczyste. Perpetual usufruct, Polskie

Wydawnictwo Prawnicze, Warszawa – Poznań.

7. Fallis G. (1988), Rent Control: The Citizen, The Market, and The State, Journal of Real Estate

Finance and Economics 1, 309–320.

8. Guarino D., Chehrazi C., Bohl B. A., Ground Lease Provisions – A Case Study for Leasehold

Valuation, The Appraisal Journal, Spring 2014, 126–132.

9. Guntermann K. L., Thomas G. (2005), Parcel Size, Location and Commercial Land Values,

Journal of Real Estate Research 27(3), 343–354.

10. Halim, N. A., Jaaman, S. S. H. (2013), A Validation of Profit Sharing Ratio Determination

Mathematical Model for Islamic Hire–Purchase Contract, Applied Mathematical Sciences,

7(41), 2035–2046.

11. Irumba R. (2015), An empirical examination of the effects of land tenure on housing values in

Kampala, Uganda , International Journal of Housing Markets and Analysis, 8(3), 359–374.

12. Jefferies R. L. (1997a), Ground lessor’s interests investment yields: an empirical study, Paper

presented at the Pacific Rim Real Estate Society Conference, Massey University, Palmerston

North, NZ, January 20-22 1997.

13. Jefferies R. L. (1997b), Ground rental valuation models, Paper to be presented to the Pacific

Rim Real Estate Society Conference, Massey University, Palmerston North, NZ, January 20-22

1997.

14. Jefferies, R. L. (1998), An equilibrium ground rental valuation model. Paper presented at the

European Real Estate Society & American Real Estate and Urban Economics Association

Conference, Maastricht University, Netherlands, June 1998.

15. Jefferies, R. L. (2005a), Developing a ground rental ‘indifference’ valuation model, Lincoln

University Commerce Division Working Paper No. 102, January.

16. Jefferies, R. L. (2005b), Ground rental valuation modelling, NZ Property Journal, April 8–17.

17. Jefferies, R. L. (2005c), Valuing ground rentals – modelling the land value percentage rate.

Paper presented at the 11th Annual Conference of the Pacific Rim Real Estate Society.

18. Kaganova O., Akmatov A., Undeland C. (2008), Introducing more transparent and efficient land

management in post-socialist cities: Lessons from Kyrgyzstan, International Journal of Strategic

Property Management 12(3), 161–181.

20/21

19. Kokot S. (2009), Ekonomiczne zagadnienia użytkowania wieczystego w gospodarce

nieruchomościami gmin. Studium diagnostyczno-statystyczne na przykładzie gmin

województwa zachodniopomorskiego, wyd. Uniwersytetu Szczecińskiego, Rozprawy i Studia,

T. (DCCCXXII) 748, Szczecin.

20. Lally M., Randal J. (2004), Ground rental rates and ratchet clauses, Accounting and Finance 44,

187–202.

21. Lewis C. M., Schallheim J.S. (1992), Are Debt and Leases Substitutes, The Journal of Financial

and Quantitative Analysis 27(4), 497–511.

22. Liu C. H., Liu P., Zhang Z. (2016), Real Assets, Liquidation Value and Choice of Financing, Real

Estate Economics, Early View, First published: 28 January 2016, DOI: 10.1111/1540-

6229.12148, 31 pp.

23. Long M. S. (1977), Leasing and the Cost of Capital, The Journal of Financial and Quantitative

Analysis 12(4), Proceedings of the 1977 Western Finance Association Meeting (Nov., 1977),

579–586.

24. Mandell S. (2001), Ground Leases & Local Property Taxes, Doctoral thesis, Stockholm: KTH

5:56, 147 pp.

25. Mandell S. (2002), Lessor and lessee perspectives on ground lease pricing. Journal of Property

Research 19(2), 145–157.

26. McCann P., Ward C. (2004), Real Estate Rental Payments: Application of Stock-Inventory

Modeling, Journal of Real Estate Finance and Economics 28(2/3), 273–292.

27. Mooradian R. M., Yang S. X. (2002), Commercial Real Estate Leasing, Asymmetric Information,

and Monopolistic Competition, Real Estate Economics 30(2), 293–315.

28. Nystrom S. L. (2007), Risk and Time in a Land Lease Economy, Proceedings of the FIG Working

Week 2007 in Hong Kong SAR China, 13-17 May 2007.

29. Özdilek Ü. (2016), Property Price Separation Between Land and Building Components, Journal

of Real Estate Research 38(2), 205–228.

30. Pope A., Gallimore P., Shi S. (2016), Leasehold Property And Investor Risk Misestimation, 22nd

Annual Pacific-Rim Real Estate Society Conference Sunshine Coast, Queensland, Australia 17-

20 January 2016.

31. Rabbani M., Gar S. S., Gaeini Z., Rafiei H., Dolatkhah M. (2015), Rent pricing decision support

mathematical model for finance leases under effective risks, Journal Of Engineering

Management And Competitiveness 5(1), 3–11.

32. Sevelka T. (2011), Ground leases: rent reset valuation issues (part I), The Appraisal Journal, Fall

2011, Volume LXXIX, Number 4, 314–326.

21/21

33. Stanton R., Wallace N. (2009), An Empirical Test of a Contingent Claims Lease Valuation Model,

Journal of Real Estate Research 31(1), 1–26.

34. Steele A., (1984), Difference Equation Solutions to the Valuation of Lease Contracts, The

Journal of Financial and Quantitative Analysis 19(3) 311–328.

35. Tian L. (2006), Impacts of Transport Projects on Residential Property Values in China: Evidence

from Two Projects in Guangzhou, Journal of Property Research 23(4), 347–365.

36. Trojanek M. (2015), Gospodarowanie nieruchomościami w gminach w aspekcie ich

dochodowości, Wydawnictwo Uniwersytetu Ekonomicznego w Poznaniu (UEP), Poznań.

37. Truszkiewicz Z. (2006), Użytkowanie wieczyste. Zagadnienia konstrukcyjne, Kantor

Wydawniczy Zakamycze, WoltersKluwer, Zakamycze.

38. Trybusz A. (1993), Wartościowy wymiar dzierżawy wieloletniej terenów zurbanizowanych,

Acta Academiae Agriculturae ac Technicae Olstenensis. Geodaesia et Ruris Regulatio, 24, 81–

91.

39. Walters M., Kent P. (2000), Institutional economics and property strata title – a survey and

case study, Journal of Property Research 17(3), 221–240.

40. Wheaton W. C. (2000), Percentage Rent in Retail Leasing: The Alignment of Landlord-Tenant

Interests, Real Estate Economics 28(2), 185–204.

41. Winiarz J. (1967), Użytkowanie wieczyste, Warszawa.

42. Yan A. (2006), Leasing and Debt Financing: Substitutes or Complements, Journal of Financial

and Quantitative Analysis 41(3), 709–731.

43. Yoshida J., Seko M., Sumita K. (2016), The Rent Term Premium for Cancellable Leases, The

Journal of Real Estate Finance and Economics 52, 480–511.