Download - 2015 Aerospace & Defense Market Survey

2015 A&DMARKETSURVEY

Perspectives of A&D Leaders on Key Business and Technology Trends

Pricing pressures and government regulations affect R&D

Demand for product innovation and modernization grows

Cybersecurity threats and costs rise

Skills shortage continues

SPONSORED BY CSC AND AIA

EXECUTIVE SUMMARYThe recovery of the global economy and increased demand for commercial aircraft are lifting the aerospace and defense (A&D) industry out of a challenging market. A&D companies are continuing to invest in product innovation and technology modernization for commercial operations, while government and defense contracts are focused on cost control and more targeted capital investments, according to the 2015 Aerospace and Defense Market Survey, conducted jointly by CSC and the Aerospace Industries Association (AIA). The 14th annual survey on business, economic and technology trends polled senior executives and senior managers at A&D companies. Key takeaways include the following:

• Designing and producing innovative products and up-selling and cross-sellingproducts continue to be top goals in the commercial sector. However, pricingpressures are forcing organizations to pursue continuous-improvement andcost-containment measures, slowing the rate of innovation.

• Sequestration has taken a toll on overall defense spending, with 64.5% ofrespondents citing budget uncertainty for decreased investments in R&D.Only 50% of respondents say they are investing in R&D, with cybersecurity,UAVs and electronic warfare topping the list of R&D investments.

• A majority of respondents (67.8%) report increased spending to protectagainst cyberthreats, with nearly half of those (29%) increasing their spend-ing by 25% or more on cybersecurity in the past year.

• Technology modernization continues to be a major initiative, focusing onapplication replacement or modernization, and IT infrastructuremodernization. Cloud computing is cited as a priority for implementingmodernized applications by 41% of respondents.

• Finding skilled workers to replace the industry’s graying workforce continuesto be a key factor affecting A&D companies. Critical areas include aerospaceengineering, mechanical engineering and cybersecurity.

• More than 71% of respondents in the government sector report at least a 10%increase in product costs related to complying with government acquisitionregulations. Thirty percent reported cost increases of at least 26%.

In response to pricing pressures and lower government spending, A&D companies are becoming more selective in their R&D investments and are more focused on product innovation, continuous improvement, cybersecurity and technology modernization.

TABLE OF CONTENTS

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Demographics: Company Size and Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Commercial Sector Market Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Commercial Sector Demographics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Commercial Sector Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Government Sector Market Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Government Sector Demographics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Government Sector Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Technology Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Regulatory Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

1

2015 A&D MARKET SURVEY

The survey provides a solid distribution across company size, though biased toward larger companies, with 22.3% of respondents having an employee base between 10,000 and 50,000. Companies with more than 50,000 employees represent 27.7% of the total respondents. Companies with 10,000 or fewer employees represent the remaining 51% responding to the survey. Commercial sector respondents represent 51% of the total, and government-sector respondents represent 49%. Many of the respondents are in an “Executive Management” role, followed by “Business Development,” “R&D/Product Development” and “Supply Chain” personnel.

COMMERCIAL SECTOR MARKET OVERVIEW

The commercial airline industry continues to grow. Emerging economies con-tinue to industrialize, expanding the middle class and increasing demand for commercial flights, transportation and logistics.

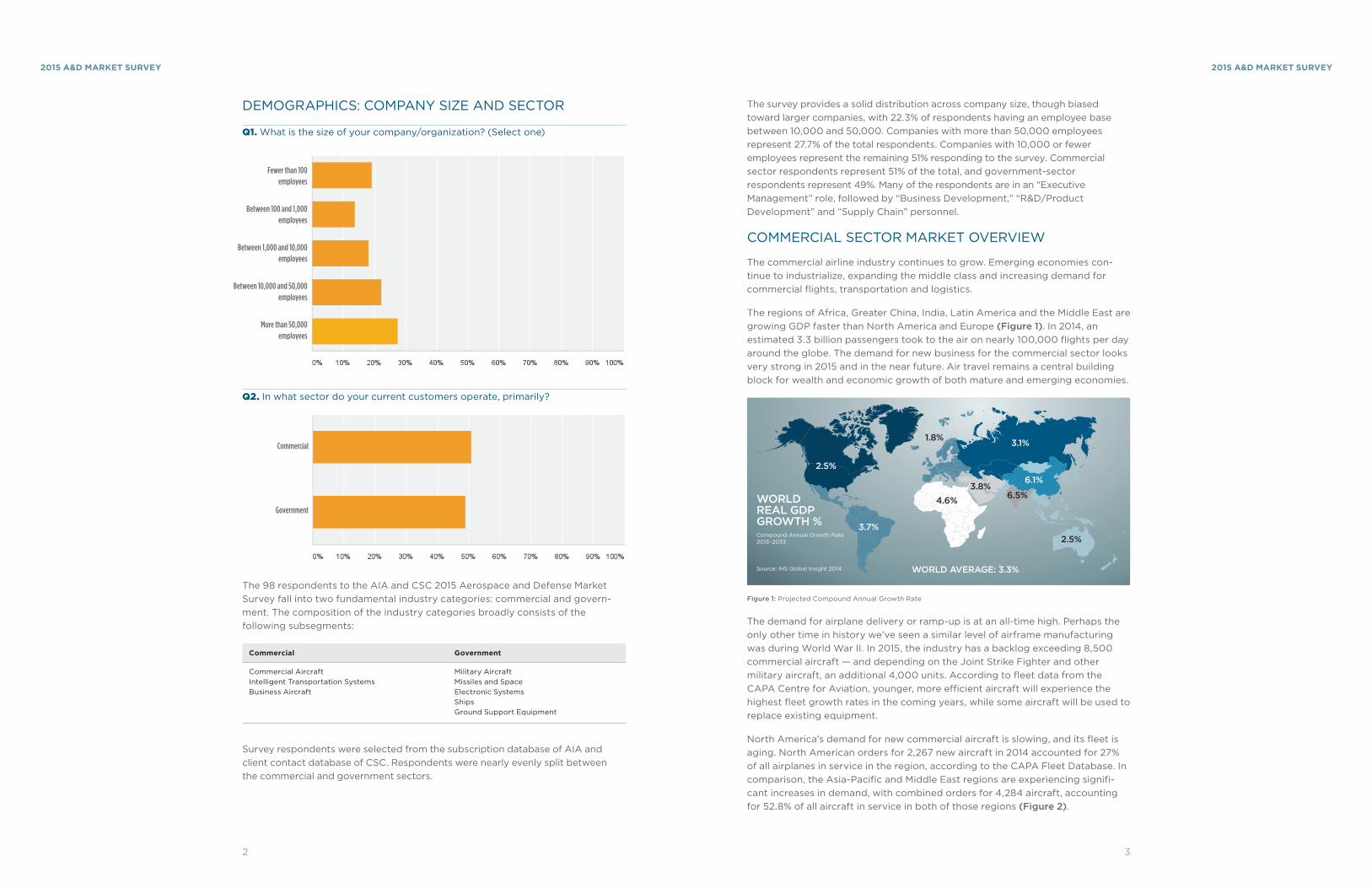

The regions of Africa, Greater China, India, Latin America and the Middle East are growing GDP faster than North America and Europe (Figure 1). In 2014, an estimated 3.3 billion passengers took to the air on nearly 100,000 flights per day around the globe. The demand for new business for the commercial sector looks very strong in 2015 and in the near future. Air travel remains a central building block for wealth and economic growth of both mature and emerging economies.

Figure 1: Projected Compound Annual Growth Rate

The demand for airplane delivery or ramp-up is at an all-time high. Perhaps the only other time in history we’ve seen a similar level of airframe manufacturing was during World War II. In 2015, the industry has a backlog exceeding 8,500 commercial aircraft — and depending on the Joint Strike Fighter and other military aircraft, an additional 4,000 units. According to fleet data from the CAPA Centre for Aviation, younger, more efficient aircraft will experience the highest fleet growth rates in the coming years, while some aircraft will be used to replace existing equipment.

North America’s demand for new commercial aircraft is slowing, and its fleet is aging. North American orders for 2,267 new aircraft in 2014 accounted for 27% of all airplanes in service in the region, according to the CAPA Fleet Database. In comparison, the Asia-Pacific and Middle East regions are experiencing signifi-cant increases in demand, with combined orders for 4,284 aircraft, accounting for 52.8% of all aircraft in service in both of those regions (Figure 2).

DEMOGRAPHICS: COMPANY SIZE AND SECTOR

Q1. What is the size of your company/organization? (Select one)

Q2. In what sector do your current customers operate, primarily?

The 98 respondents to the AIA and CSC 2015 Aerospace and Defense Market Survey fall into two fundamental industry categories: commercial and govern-ment. The composition of the industry categories broadly consists of the following subsegments:

Commercial Government

Commercial Aircraft Intelligent Transportation Systems Business Aircraft

Military Aircraft Missiles and Space Electronic Systems Ships Ground Support Equipment

Survey respondents were selected from the subscription database of AIA and client contact database of CSC. Respondents were nearly evenly split between the commercial and government sectors.

WORLD REAL GDP GROWTH %Compound Annual Growth Rate 2013–2033

Source: IHS Global Insight 2014 WORLD AVERAGE: 3 .3%

2 .5%

3 .7%

6 .1%

3 .1%

4 .6%3 .8%

1 .8%

6 .5%

2 .5%

Fewer than 100 employees

Between 100 and 1,000 employees

Between 1,000 and 10,000 employees

Between 10,000 and 50,000 employees

More than 50,000 employees

Commercial

Government

2 3

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

CONTINUOUSLY IMPROVING MANUFACTURING PROCESSES

The design-to-order, build-to-order A&D manufacturing environment poses challenges to continuous-improvement techniques. While organizations have invested heavily in production improvements, they have not achieved long-term benefits of lower costs and improved efficiency. Many companies are currently exploring the following approaches to cost containment:

Systems Engineering Systems engineering focuses on how complex engineering projects should be designed and managed over the lifecycle of the project. This interdisciplinary approach applies to managing complex issues such as logistics, the coordina-tion of globally disperse teams, automated shop-floor control and aftermarket services.

Synchronous Manufacturing In commercial and military markets, leading innovators have adopted a systematic and synchronized approach to the entire manufac-turing value chain that addresses materials, workforce, machines and methods. It helps prime contractors become predictable and more reliable suppliers. The key is to understand the need for dynamic planning, scheduling and executing all parts of the manufacturing process — and when a disruption occurs, to deliver discrete actionable information to quickly resolve problems such as late materials, disabled machinery or inadequate staffing.

Integrated Products and Processes The management and collaboration of design engineering, manufacturing engineering, and planning is critical to reducing waste. Collaboration allows engineers and production planners to define how highly complex products are manufactured, modified and maintained during product support and end-of-life requirements.

Region Orders In service Orders as % of number in service

Middle East 946 1,247 76%

Asia-Pacific 3,338 6,862 49%

Europe 2,118 6,744 31%

Latin America 645 2,078 31%

North America 2,267 8,544 27%

Africa 188 1,329 14%

Figure 2: Aircraft Orders and Aircraft in Service by Region, 18 Feb. 2014 Source: CAPA Centre for Aviation

The market for commercial aircraft is forecast to grow over the next 8 to 10 years in regions such as Asia-Pacific and the Middle East. Growth in these emerging regions is one of the key market drivers for commercial aircraft sales, MRO, logistics and support/field service, and aftermarket programs.

COMMERCIAL SECTOR DEMOGRAPHICS

Q3. Identify your organization’s aerospace and defense business segment(s). (Select all that apply)

Q4. Select your primary function area. (Select one)

More than half of respondents report working for a “Commercial Aircraft Manufacturer/Integrator” (51.5%). Other key segments include “Tier 1 and Tier 2 Component Supplier,” “Business Aircraft Manufacturer/Integrator,” “Aftermarket Components Manufacture and Repair,” and “Logistics, Field Service, MRO Service Provider.”

Executive management, R&D and sales are strongly represented in the survey. Executive management (45.5%) is responsible for leading the enterprise and achieving the expected financial results of the corporation. Business develop-ment/sales (12.1%) must bring the right product to the right market with a price point to meet market demand. It then falls on the R&D/product engineering discipline (15.2%) to take those business and market requirements, target costs and schedule to launch a successful product.

Commercial airline

Commercial aircraft manufacturer/integrator

Business aircraft manufacturer/integrator

Commercial space systems, lift vehicles, payloads & launch services

Tier-1 component supplier

Tier-2 component supplier

Tier-3 component supplier

Logistics, field service, MRO service provider

Aftermarket components manufacture and repair

Other

Executive management

Business development/sales

R&D/product engineering

Program management

Supply chain management/sourcing

Field service

Other

4 5

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

COMMERCIAL SECTOR TRENDS

Q5. Rank your organization’s three most important strategic business objectives over the next 1 to 2 years. (1 being the highest objective, 2 the second highest objective, 3 the third highest objective)

Respondents were asked to rank their top three business objectives for the next 1 to 2 years. For the third consecutive year, the goal to “Design and Produce Innovative Products” was ranked as the No. 1 objective, followed by “Up-Sell/Cross-Sell More Products into the Existing Customer Base” (No. 2) and “Improve Internal Efficiency/Lower Cost” (No. 3).

A variety of market conditions are focusing commercial sector firms on innova-tion, including:

• Fuel Efficiency . For U.S. airlines, domestic flights now average 0.54 aircraft miles per gallon of jet fuel, an improvement of more than 40% since 2000. Heavier jets on international flights experienced a 17% improvement to 0.27 miles per gallon. However, more work can be done. Innovation in aerodynam-ics and the use of lightweight composite materials in airframes and airfoils have led to significant improvements. Replacing mechanical components with electronics improves weight-to-thrust ratios.

• Eco-Efficiency . This requires continued commitment to sustainability by both manufacturers and airlines. Innovative solutions are aiming at reducing an aircraft’s carbon footprint throughout its entire lifecycle — from design and manufacture to in-flight operations and end-of-life management.

• Noise . The “quiet aircraft” for both the airframe and propulsion systems continues to be a priority. Manufacturers continue to focus on dominant sources of engine noise: the blades of the fan at the front and the jet exhaust-ing at the rear. Opportunities for innovation also exist in airfoil and nacelle design and configuration.

• Materials . Materials science is at the forefront in the commercial segment and even more so in the government segment. All manufacturers are investing in research and development for lightweight materials with superior strength that can be produced easily. To reduce parts inventories, a set of discrete parts in a sub-assembly can be configured into a single part. R&D is also exploring composite ceramics and 3D printing techniques.

Increasing Up-Sell and Cross-Sell

The emphasis on cross-selling and up-selling in the 2015 survey implies that all commercial aircraft companies, including original equipment integrators and Tier 1 and Tier 2 suppliers, are focused on how they go to market. Up-selling and cross-selling generally includes additional products or services that customers want and use. Cross-selling involves offering additional products to support or complement the product the customer has already decided to buy. Up-selling involves persuading a customer to switch to a more expensive product to improve quality, availability and new features.

Effective cross-selling and up-selling can:

• Increase the initial aircraft order total

• Increase the conversion rates of existing customers

• Achieve higher margins

• Improve overall customer satisfaction

Continued Focus on Internal Efficiency and Lower Costs

The A&D industry’s focus on operational efficiency and cost take-out has been a continual theme in every Aerospace and Defense Survey. Highly engineered and complex aircraft products are typically produced in low volumes using high-touch labor, and because of their complexity, the manufacturing process may involve parts that are subject to continuous design changes and regulatory requirements that drive up costs.

Design and produce innovative products

Find new customer opportunities by growing into new market segments

Develop new channels for new and existing products

Up-sell/cross-sell more products into the existing customer base

Improve internal efficiency/lower cost

Grow the sustainment/ aftermarket business

Other

“We must increase our expenditure on R&D if we want to maintain our tech-nological superiority.”

– Respondent, 2015 A&D Survey

6 7

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

Q6. Rank the top three aerospace and defense industry macroforces affecting your organization over the next 2 to 3 years. (1 being the largest, 2 the second largest, 3 the third largest)

Survey respondents were asked to identify the top three macroforces affecting their organization over the next 2 to 3 years. For the third year in a row, “Pricing Pressures in Commercial Markets” was ranked No. 1, indicating the increasing competitiveness in the commercial sector. The No. 2 macroforce, also impacted by competition, was “Mergers, Acquisitions and Divestitures.”

In the 2015 survey, the “Growing Shortage of Skilled Talent” was ranked third. The graying of the A&D workforce first emerged as a concern in 2010, when it became one of the top macroforces. This factor is closely followed by “Reductions and Reallocations in Defense Spending.” The impact of shrinking defense budgets continues to influence the industry but has fallen in the ranking since 2010, possibly reflecting the new normal of uncertainty in defense markets. The expected growth in emerging markets will challenge executive managers on product localization, global supply chain and product support. While a similar number of respondents identified the impact of “Mergers, Acquisitions and Divestitures Reshaping the Industry” as a macroforce, the responses indicate that M&A activity is still expected to continue.

Q7. Looking at your business applications and IT infrastructure, what is your modernization strategy going forward? (Select all that apply)

Technology modernization continues to be a major initiative, according to survey respondents. Asked about their “Modernization Strategy,” respondents across the board identified three clear strategies: “Application Replacement or Modernization” (No. 1), “IT Infrastructure Modernization” (No. 2) and “Integrating What We Have for Better Data Sharing” (No. 3).

These results tie into the industry’s overall goals to improve business operations, increase internal efficiency and lower cost. Revitalized applications and modern-ized infrastructure provide better data sharing and collaboration, which collectively contribute to lower costs.

To compete at scale on products, services and location at ever-decreasing target costs, business needs are putting more pressure on IT organizations. Business leaders look to IT to enable and unlock new revenue streams across the enter-prise — and at lower costs.

Globalization

Reductions and reallocations in defense spending

Pricing pressures in commercial markets

Mergers, acquisitions and divestitures are reshaping the industry

A growing shortage of skilled talent

Compliance with export, tariff/trade, intellectual property, environmental and security regulations

Influence from emerging market, technology or business disruption

Application replacement or modernization

IT infrastructure modernization

Migration off the mainframe onto less expensive platforms

Transitioning our applications to a virtualized infrastructure

Moving our applications to the cloud

Integrating what we have for better data sharing

All of the above

None, we don’t have an application or IT infrastructure

modernization strategy

Other

8 9

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

GOVERNMENT SECTOR MARKET OVERVIEWThe backdrop for the government sector contrasts sharply with the commercial sector. Broad-base instability in all industry subsegments is resulting from a mix of sociopolitical upheaval, accelerated growth of emerging markets, introduction of advancements in technology and fiscal headwinds in mature markets. With so much change occurring so rapidly, A&D companies have seen downward pressure on pricing, which is lowering profitability. The tough environment has executive management searching for solutions frequently, as business strategies that once may have had a 5-year forecast must be refreshed more often.

The continued impact of shrinking defense budgets has resulted in a declining forecast for both fixed-wing and rotary military aircraft over the next 10 years. According to Forecast International, “Yearly production will peak at 1,367 units in 2014, drop to a low of 1,095 in 2018, and then rise slightly to 1,122 by 2020 before tapering off for the remainder of the period. Rotorcraft will account for 52 percent of all units produced during the 2013-2022 timeframe, with fixed-wing aircraft accounting for the remaining 48 percent.”

While there is a decline in the fixed-wing and rotary military aircraft business, the U.S. military UAV market is projected to grow at a 12% CAGR, reaching $18.7 billion in 2018. New budget and political realities facing the U.S. government are calling for smaller, more effective and less risky military solutions. Despite the general downturn trend in the defense market, the UAV segment is forecast to survive relatively intact.

The global space subsegment is growing despite the economic downturn, with an average predicted annual growth rate of 12%. Figure 3 represents the global military space requirements market forecast by technology type.

Figure 3: Space Requirements Market Forecast

Source: Market Info Group LLC

GOVERNMENT SECTOR DEMOGRAPHICS

Q8. Identify your organization’s aerospace and defense business segment(s). (Select all that apply)

Q9. Select your primary functional area. (Select one)

Space Based Space Surveillance

Earth Observation

Military Communications

2012

2015

2017

$78 .2B

$174 .1B

$323 .6B

Aircraft

Space

Electronics/IT systems

Ships

Ground

Mid-tier supplier

Small supplier

Other

Executive management

Business development/sales

R&D/product engineering

Program management

Supply chain management/sourcing

Manufacturing/quality engineering

Repair operations and management

Field service

Manufacturing operations

Other

10 11

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

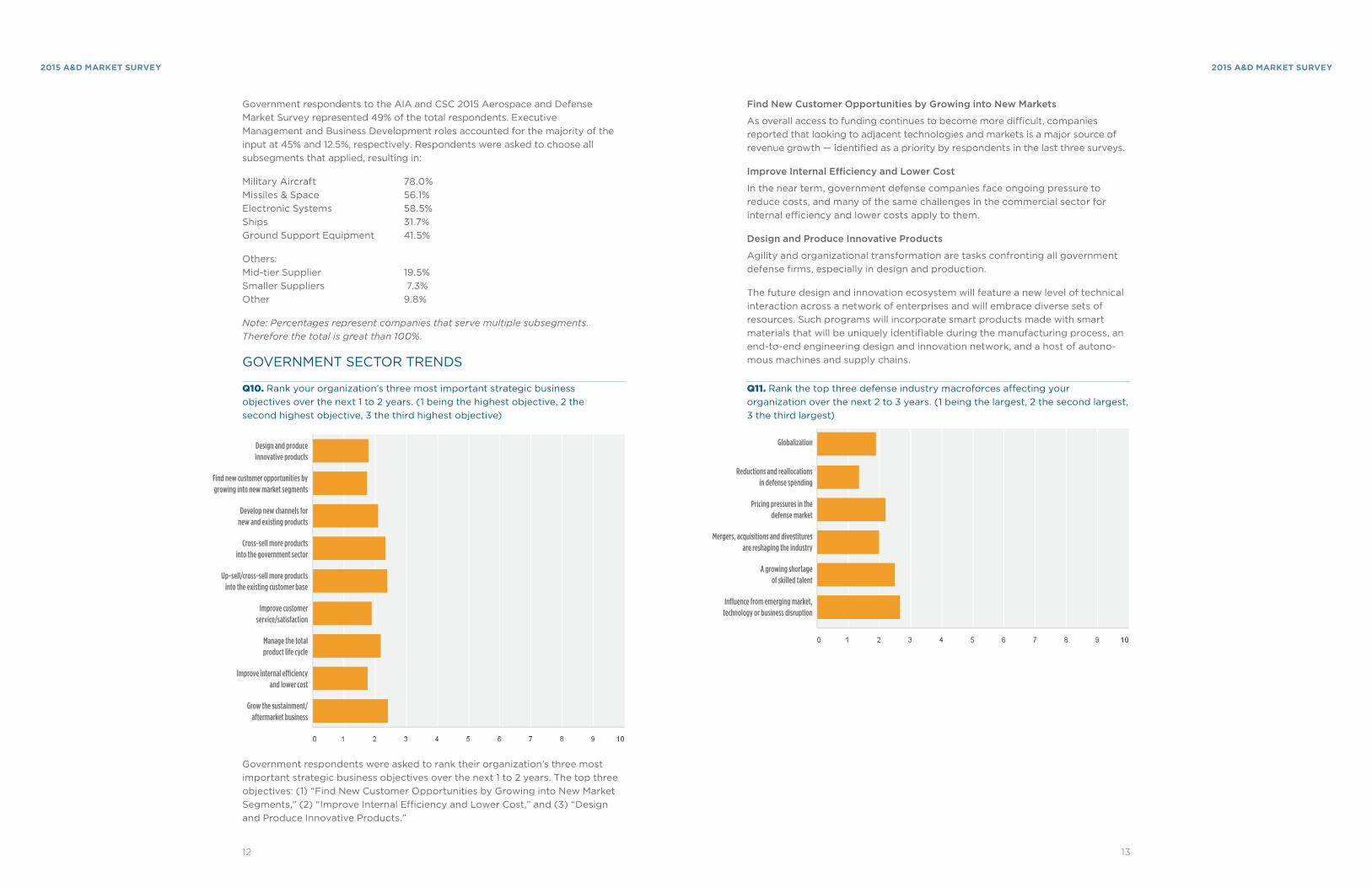

Government respondents to the AIA and CSC 2015 Aerospace and Defense Market Survey represented 49% of the total respondents. Executive Management and Business Development roles accounted for the majority of the input at 45% and 12.5%, respectively. Respondents were asked to choose all subsegments that applied, resulting in:

Military Aircraft 78.0%Missiles & Space 56.1%Electronic Systems 58.5%Ships 31.7%Ground Support Equipment 41.5%

Others:Mid-tier Supplier 19.5%Smaller Suppliers 7.3%Other 9.8%

Note: Percentages represent companies that serve multiple subsegments. Therefore the total is great than 100%.

GOVERNMENT SECTOR TRENDS

Q10. Rank your organization’s three most important strategic business objectives over the next 1 to 2 years. (1 being the highest objective, 2 the second highest objective, 3 the third highest objective)

Government respondents were asked to rank their organization’s three most important strategic business objectives over the next 1 to 2 years. The top three objectives: (1) “Find New Customer Opportunities by Growing into New Market Segments,” (2) “Improve Internal Efficiency and Lower Cost,” and (3) “Design and Produce Innovative Products.”

Find New Customer Opportunities by Growing into New Markets

As overall access to funding continues to become more difficult, companies reported that looking to adjacent technologies and markets is a major source of revenue growth — identified as a priority by respondents in the last three surveys.

Improve Internal Efficiency and Lower Cost

In the near term, government defense companies face ongoing pressure to reduce costs, and many of the same challenges in the commercial sector for internal efficiency and lower costs apply to them.

Design and Produce Innovative Products

Agility and organizational transformation are tasks confronting all government defense firms, especially in design and production.

The future design and innovation ecosystem will feature a new level of technical interaction across a network of enterprises and will embrace diverse sets of resources. Such programs will incorporate smart products made with smart materials that will be uniquely identifiable during the manufacturing process, an end-to-end engineering design and innovation network, and a host of autono-mous machines and supply chains.

Q11. Rank the top three defense industry macroforces affecting your organization over the next 2 to 3 years. (1 being the largest, 2 the second largest, 3 the third largest)

Design and produce innovative products

Find new customer opportunities by growing into new market segments

Develop new channels for new and existing products

Cross-sell more products into the government sector

Up-sell/cross-sell more products into the existing customer base

Improve customer service/satisfaction

Manage the total product life cycle

Improve internal efficiency and lower cost

Grow the sustainment/ aftermarket business

Globalization

Reductions and reallocations in defense spending

Pricing pressures in the defense market

Mergers, acquisitions and divestitures are reshaping the industry

A growing shortage of skilled talent

Influence from emerging market, technology or business disruption

12 13

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

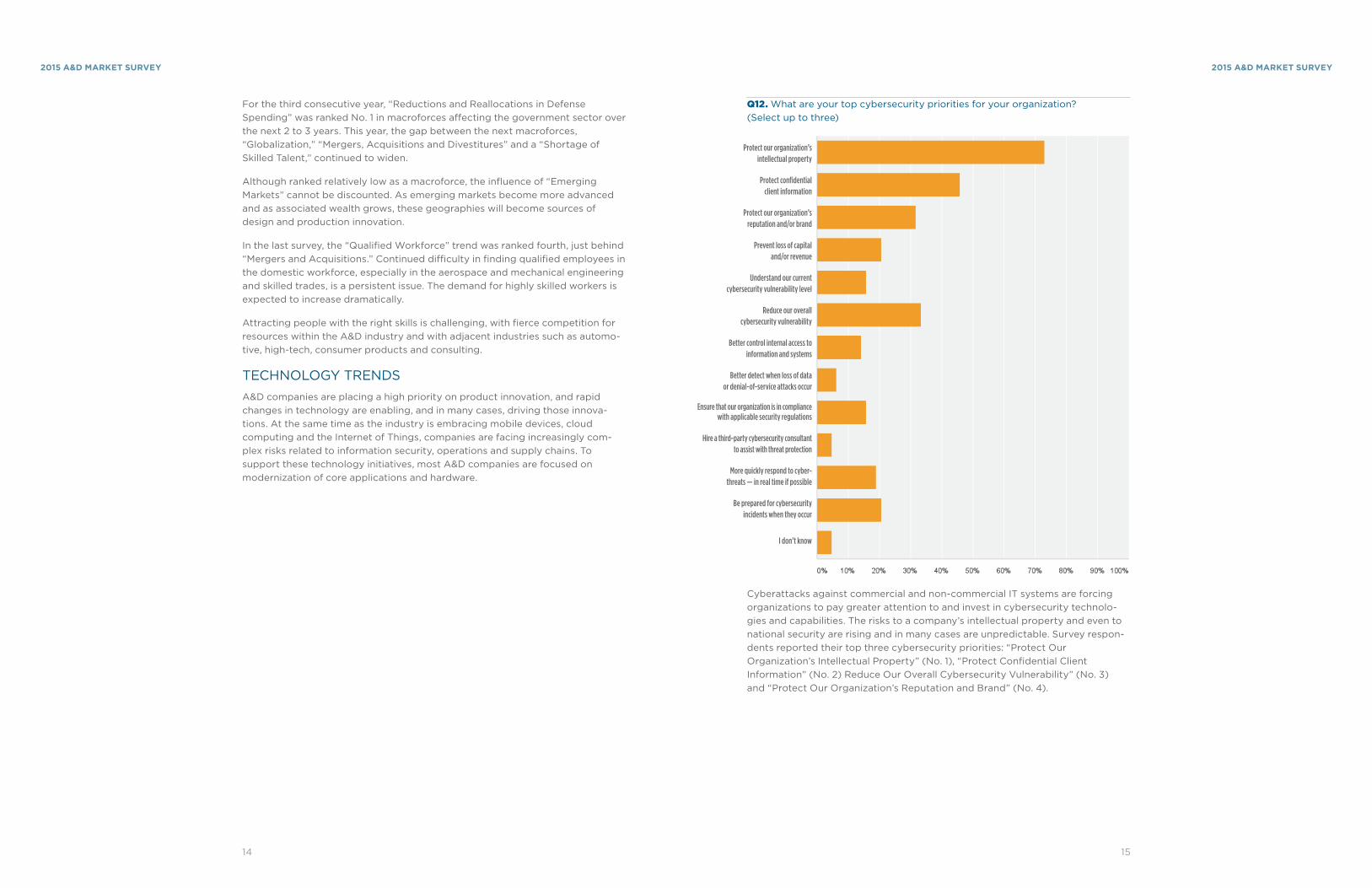

For the third consecutive year, “Reductions and Reallocations in Defense Spending” was ranked No. 1 in macroforces affecting the government sector over the next 2 to 3 years. This year, the gap between the next macroforces, “Globalization,” “Mergers, Acquisitions and Divestitures” and a “Shortage of Skilled Talent,” continued to widen.

Although ranked relatively low as a macroforce, the influence of “Emerging Markets” cannot be discounted. As emerging markets become more advanced and as associated wealth grows, these geographies will become sources of design and production innovation.

In the last survey, the “Qualified Workforce” trend was ranked fourth, just behind “Mergers and Acquisitions.” Continued difficulty in finding qualified employees in the domestic workforce, especially in the aerospace and mechanical engineering and skilled trades, is a persistent issue. The demand for highly skilled workers is expected to increase dramatically.

Attracting people with the right skills is challenging, with fierce competition for resources within the A&D industry and with adjacent industries such as automo-tive, high-tech, consumer products and consulting.

TECHNOLOGY TRENDSA&D companies are placing a high priority on product innovation, and rapid changes in technology are enabling, and in many cases, driving those innova-tions. At the same time as the industry is embracing mobile devices, cloud computing and the Internet of Things, companies are facing increasingly com-plex risks related to information security, operations and supply chains. To support these technology initiatives, most A&D companies are focused on modernization of core applications and hardware.

Q12. What are your top cybersecurity priorities for your organization? (Select up to three)

Cyberattacks against commercial and non-commercial IT systems are forcing organizations to pay greater attention to and invest in cybersecurity technolo-gies and capabilities. The risks to a company’s intellectual property and even to national security are rising and in many cases are unpredictable. Survey respon-dents reported their top three cybersecurity priorities: “Protect Our Organization’s Intellectual Property” (No. 1), “Protect Confidential Client Information” (No. 2) Reduce Our Overall Cybersecurity Vulnerability” (No. 3) and “Protect Our Organization’s Reputation and Brand” (No. 4).

Protect our organization’s intellectual property

Protect confidential client information

Protect our organization’s reputation and/or brand

Prevent loss of capital and/or revenue

Understand our current cybersecurity vulnerability level

Reduce our overall cybersecurity vulnerability

Better control internal access to information and systems

Better detect when loss of data or denial-of-service attacks occur

Ensure that our organization is in compliance with applicable security regulations

Hire a third-party cybersecurity consultant to assist with threat protection

More quickly respond to cyber- threats — in real time if possible

Be prepared for cybersecurity incidents when they occur

I don’t know

14 15

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

Q13. Over the past year, our overall vulnerability against cybersecurity threats has ... (Select one)

Nearly half of respondents (46.8%) reported that cybersecurity threats had increased “Somewhat” or “Significantly.” Only 11.3% said cyberthreats had decreased over the past year.

These results are no doubt partly in response to a series of high-profile attacks on A&D companies, retailers, banks and Internet service providers. Increasingly, cybersecurity efforts are focused on deterring such attacks before they take place, especially in the government sector, which has the necessary resources and tools to focus on prevention.

Preventing threats is a key goal in the A&D industry, which is an early adopter of cyber-physical systems, where intelligent software is embedded into hardware and usually connected to a network. Adding more software-defined and con-nected products to the aviation industry is making cybersecurity and physical security more difficult than ever.

Other threats focus on manufacturing infrastructure. Often not considered mainstream IT, manufacturing shop floor networks and devices are potentially vulnerable to attack. A breach of manufacturing process data in military and commercial systems could help attackers reverse-engineer critical proprietary systems.

Q14. Over the past year, the cost to protect our organization and intellectual property from cybersecurity threats has ... (Select one)

Increasing threats are translating into higher spending on cybersecurity. A majority of respondents (67.8%) reported increased spending to protect against cyberthreats, with nearly half of those (29%) increasing their spending by 25% or more on cybersecurity over the past year.

The primary initiatives for chief information security officers, in place at most A&D companies, include compliance, strategy and risk management. Key spending priorities are:

• Risk assessments

• Training and awareness

• Data protection

• Incident response

• Continuous event monitoring

Increasing pressures to adopt cloud-based and mobile applications to support business demands are posing new vulnerabilities. As threats grow, cybersecurity costs are expected to continue to rise.

Increased significantly

Increased somewhat

Remained the same

Decreased somewhat

Decreased significantly

I don’t know

Increased over 50%

Increased between 25% and 50%

Increased less than 25%

Decreased

I don’t know

“Cybersecurity standards are too lax. BYOD is a vulnerability on its own, and an effective platform to spread malware onto company systems.”

– Respondent, 2015 A&D Survey

16 17

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

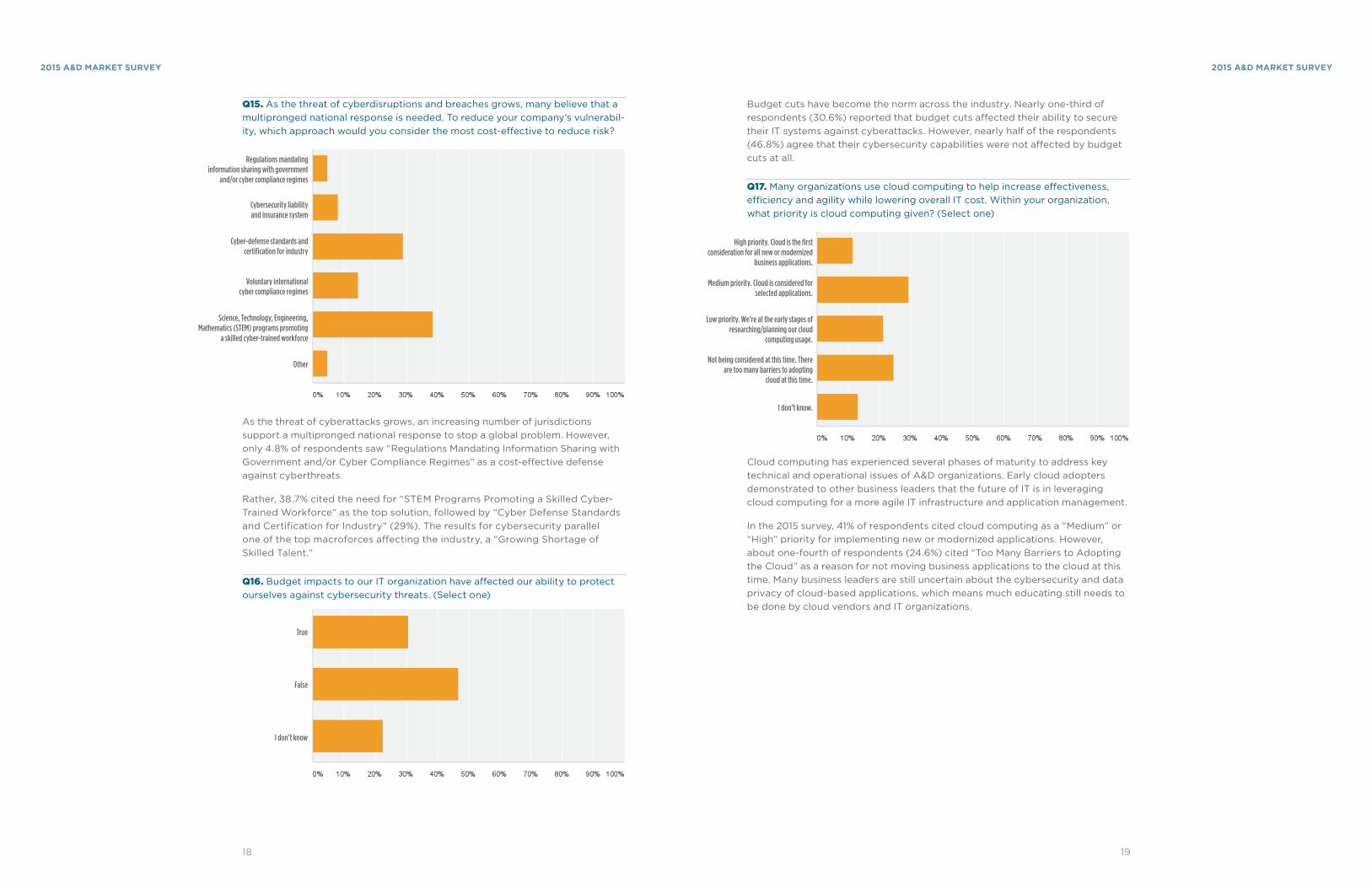

Q15. As the threat of cyberdisruptions and breaches grows, many believe that a multipronged national response is needed. To reduce your company’s vulnerabil-ity, which approach would you consider the most cost-effective to reduce risk?

As the threat of cyberattacks grows, an increasing number of jurisdictions support a multipronged national response to stop a global problem. However, only 4.8% of respondents saw “Regulations Mandating Information Sharing with Government and/or Cyber Compliance Regimes” as a cost-effective defense against cyberthreats.

Rather, 38.7% cited the need for “STEM Programs Promoting a Skilled Cyber-Trained Workforce” as the top solution, followed by “Cyber Defense Standards and Certification for Industry” (29%). The results for cybersecurity parallel one of the top macroforces affecting the industry, a “Growing Shortage of Skilled Talent.”

Q16. Budget impacts to our IT organization have affected our ability to protect ourselves against cybersecurity threats. (Select one)

Budget cuts have become the norm across the industry. Nearly one-third of respondents (30.6%) reported that budget cuts affected their ability to secure their IT systems against cyberattacks. However, nearly half of the respondents (46.8%) agree that their cybersecurity capabilities were not affected by budget cuts at all.

Q17. Many organizations use cloud computing to help increase effectiveness, efficiency and agility while lowering overall IT cost. Within your organization, what priority is cloud computing given? (Select one)

Cloud computing has experienced several phases of maturity to address key technical and operational issues of A&D organizations. Early cloud adopters demonstrated to other business leaders that the future of IT is in leveraging cloud computing for a more agile IT infrastructure and application management.

In the 2015 survey, 41% of respondents cited cloud computing as a “Medium” or “High” priority for implementing new or modernized applications. However, about one-fourth of respondents (24.6%) cited “Too Many Barriers to Adopting the Cloud” as a reason for not moving business applications to the cloud at this time. Many business leaders are still uncertain about the cybersecurity and data privacy of cloud-based applications, which means much educating still needs to be done by cloud vendors and IT organizations.

High priority. Cloud is the first consideration for all new or modernized

business applications.

Medium priority. Cloud is considered for selected applications.

Low priority. We’re at the early stages of researching/planning our cloud

computing usage.

Not being considered at this time. There are too many barriers to adopting

cloud at this time.

I don’t know.

Regulations mandating information sharing with government

and/or cyber compliance regimes

Cybersecurity liability and insurance system

Cyber-defense standards and certification for industry

Voluntary international cyber compliance regimes

Science, Technology, Engineering, Mathematics (STEM) programs promoting

a skilled cyber-trained workforce

Other

True

False

I don’t know

18 19

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

Q18. BYOD (bring your own device) has grown tremendously in the past few years. What is your current IT policy concerning BYOD? (Select one)

The Bring Your Own Device (BYOD) mobility trend has sent shock waves across IT and business communities. Most CIOs are under high pressure to deliver the same experience on personal mobile devices as they do over company-issued devices. While cost restrictions have slowed the response of many companies, the security of data on mobile devices as well as the threats such devices pose to the organization have prevented many A&D firms from loosening BYOD policies. Many have reacted quickly to address real concerns around enterprise mobility management (EMM) and specifically around security and privacy.

Only 14.8% of respondents said their company encourages the use of whatever device they wish to support the business. In contrast, 21.3% report that their company provides specialized apps and 41% require separation between work and personal devices.

Over the past few years, many approaches and solutions have been imple-mented to help companies fully manage and secure the full lifecycle of mobile users, devices, apps and data. While EMM has made a lot of progress over the last few years, nearly 50% of respondents reported that they don’t embrace BYOD and are not allowed to connect personal devices to the company network.

While security and privacy remain the top reasons for not adopting BYOD, some companies are either issuing company-owned smartphones and tablets or allowing BYOD with separation between work and personal areas on the device and full encryption for the work partition. This approach has solved many technical issues while giving employees the freedom of choosing a preferred device.

Q19. Organizations recognize that success depends upon delivering new tech-nology innovations that provide measurable value and return on investment. With this in mind, in which of the following areas of IT innovation are you focused?

Tremendous advances in many hardware and software technologies over the last few years are causing seismic shifts across industries and creating new business opportunities in the A&D sector.

While IT and business leaders are overwhelmed with innovative technologies, focus is required to cost-effectively apply those innovations to products and services. The gap between existing infrastructure and business applications is widening faster than ever. Therefore, the No. 1 priority for respondents is to invest heavily in “Application Modernization” and the underpinning IT infrastruc-ture. Other priorities include “Mobility” (No. 2), “Manufacturing Automation” (No. 3), “Supply Chain Visibility” (No. 4) and “Big Data Analytics” (No. 5).

Investment in the “Internet of Things” (IoT) is a low priority, but this was not surprising given the lower maturity level of emerging IoT hardware, software, protocols and standards.

While manufacturing is becoming a global industry with global product design, sourcing and manufacturing plants, existing on-premises IT infrastructure is increasingly becoming a huge obstacle for businesses. “Virtualization and Cloud Computing” (ranked No. 6) are making it easy and cost efficient to expand and restructure business within a short time.

Users are encouraged to use whatever device(s) they wish to access email,

applications or other systems.

We provide specialized apps (such as GOOD) that users may download and use

on their own devices.

We ask our users to maintain separate work and personal devices.

Personal devices such as phones or iPads are not permitted at work.

I don’t know what our BYOD policy is.

Internet of things

Machine-to-machine communication

Application modernization

Mobility — access from anywhere

Virtualization and cloud computing

Big data analytics

Manufacturing automation

Outsourcing

Supplier/supply chain visibility

PLM

Other

20 21

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

Q20. To help control the rising costs of maintaining business applications, which of the following actions will you take? (Select all that apply)

CIOs face the dilemma of maintaining and supporting several generations of IT systems while having to respond to challenging business requirements defined by the latest technologies and user experiences. This is especially hard with limited budgets and skill sets.

This situation also hinders the company’s ability to leverage new technologies to create new business and promote innovation across the company. The results of this survey reflect strong awareness among IT leadership and show that “Analyzing the Application Portfolio to Eliminate Redundant Applications” is the No. 1 priority for IT investments. These investments are helping companies modernize IT infrastructure and open the doors to innovation.

The No. 2 approach to modernization is using “Commercially Available Software as a Service Where Possible” to accelerate efforts and leverage new technolo-gies, followed by “Migrating Applications to the Cloud,” “Rewriting Applications for Modernized Platforms” and "Transition Key Business Applications to Commercial-Off-the-Shelf Products."

The survey shows an important trend of using next-generation technologies and usage-based IT models to reduce costs and make more investments available for business and product innovation across the company.

REGULATORY TRENDS

Q21. The defense sector hopes to expand its access to technology and innova-tion through increased private research and development (R&D) investment, more competition for defense contracts, and the use of cash incentives to motivate performance. Is your company increasing R&D investment to capture future defense business?

Q22. If yes, which of these sectors are you focusing your R&D in?

Move existing applications as-is to newer, less expensive platforms

Rewrite existing applications to run on newer, less expensive platforms

Analyze the existing application portfolio to reduce or eliminate redundant or

unnecessary applications

Utilize commercially available Software-as-a-Service applications where possible

Transition key business applications to commercial-off-the-shelf products

Move applications management to a third-party provider (on-shore or off-shore)

Move to a centralized method of application distribution

Migrate applications to the cloud

Hire a third-party consultant to help formulate an applications strategy

None of the above — we don’t have an application modernization strategy

Cyber

UAVs

Electronic warfare

Hypersonics

Alternative energy

Directed energy

Anti-submarine warfare

Yes

No

“The government is obsessed with knowing everything about costs and profit, instead of being obsessed with allowing industry to provide prod-ucts and services that create the most value.”

– Respondent, 2015 A&D Survey

22 23

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

Q23. If no, which statement best describes your rationale for not increasing your R&D investment?

Only 50% of those in the government sector surveyed are “Planning Increased R&D Investments to Capture Defense Business.” These results do not factor in spending on new technologies that cannot be publicly discussed for security reasons.

For companies planning R&D investments, the top four areas of investment are “Cybersecurity,” “UAVs,” “Electronic Warfare” and “Directed Energy.”

Sequestration has taken a toll on overall R&D spending, with 64.5% of respon-dents citing “Instability and Uncertainty in the Defense Budget” as a reason for not investing in defense R&D projects.

For the most part, respondents are more selective about where they place R&D funding and are investing in programs such as cybersecurity and electronic warfare that require lower capital and support costs.

Public announcements for new programs such as the Long Range Strike Bomber (LRS-B) in the United States, and orders for aircraft such as the F-35B jump-jet in the United Kingdom and the Gripen NG in northern Europe and Brazil have created the potential for more rapid adoption of next-generation technologies. A key objective for these aircraft is the ability to rapidly incorporate new sensor and threat detection technologies. With the first LRS-B expected to be fielded by 2025, designers hope to fundamentally change the industry’s traditional approach of periodic releases designed to improve performance and technology, but rather the aircraft would be able to rapidly adopt new technologies to combat threats as they evolve.

Cybersecurity and electronic warfare innovation will likely play a major role in the development of the LRS-B. The investment in cybersecurity reflects not only the money spent to combat the persistent threat from bad actors, but also the need to protect warfare equipment and systems from intrusion.

Not surprising is the investment in UAVs. Coupled with electronic warfare, UAVs are clearly in demand by defense for all branches. The ability to linger for long durations over a battlefield to gather and disseminate real-time data to the warfighter is very important for sustaining military advantage.

Q24. Have you declined to bid on defense or federal government contracts because acquisition regulations are too costly to comply with?

Survey responses related to interaction with government agencies indicate a growing number of A&D suppliers are declining to bid on defense or federal government contracts (36.7% of respondents) “Because Acquisition Regulations Are Too Costly to Comply With.”

Q25. How much does complying with government acquisition regulations add to your product’s cost?

A vast majority of A&D companies reported rising product costs caused by “Complying with Government Acquisition Regulations.” More than 71% of respondents reported at least an 11% increase in product costs. Thirty percent of respondents reported that regulations increased product cost by at least 26%.

1,800 PAGES OF FEDERAL ACQUISITION REGULATIONS

Federal Acquisition Regulation (FAR) includes more than 1,800 pages of regulations governing purchasing processes for goods and services. FAR’s rules and regulations are highly restrictive, not only affecting costs but also the level of risk that contractors are willing to assume.

According to Stan Soloway, president and CEO of the Professional Services Council and a former deputy undersecretary of Defense for Acquisition, “Professionals are under a lot of pressure to get things right and stay within the law.”

This environment makes it difficult for a company to be flexible and agile, and it serves as a potential headwind to innovation. The list of applicable regulations and policies includes:

• Federal Acquisition Regulation (FAR)

• General Services Acquisition Manual (GSAM)

• Office of Federal Procurement Policy (OFPP)

• AbilityOne

• Code of Federal Regulations

• Agency Supplemental Regulations

• Federal Register

• Regulations.gov

• Acquisition Center of Excellence (ACE) for Services

• Civilian Agency Acquisition Council (CAAC)

• Financial Management Service (FMS) Treasury Offset Program

• NAICS (North American Industry Classification System)

• Product Service Code Manual

• VETBIZ.gov

Low return/profit on military programs

The sale doesn’t justify giving up intellectual property

The cost of compliance with government regulations is too high

Instability and uncertainty in defense budget, programs, requirements and timelines

Yes

No

0–10%

11–25%

26–40%

Over 40%

“There has to be a cleaner way to compete via RFPs.”

– Respondent, 2015 A&D Survey

24 25

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY

Q26. Which aspect of compliance drives your costs?

Respondents were asked about costs related to compliance with federal rules and regulations. Many respondents selected multiple factors, but it was clear that “Costing and Pricing Requirements” was the No. 1 driver of compliance costs, followed by “Audits” (No. 2), “Quality Assurance” (No. 3) and “Information Security/Protection” (No. 4).

Q27. Has the number of DoD audits of your companies systems and processes grown over the past 5 years?

For the most part, the number of DoD audits among respondents has been relatively stable over the past 5 years, as 70% of those surveyed reported either no increase in audits over that time or just a 0 – 10% increase.

The remaining 30% reported audit increases of 11% or higher. There are many factors that come into play for this sample, including the amount spent on defense, the impact of large programs consuming the budget, and an increasing backlog of audits. The Defense Contract Audit Agency (DCAA) is significantly behind schedule in completing audits, and the lack of increase in the number of audits could be the result of a lack of workforce.

CONCLUSIONProduct innovation and cross-selling and up-selling will continue to be important sources of revenue for A&D companies. However, for the commercial sector to address the growing backlog for aircraft, organizations need to invest in process improvements, global collaboration and technology modernization. At the same time, the A&D industry continues to look for ways to attract and retain skilled workers, against a background of growing cybersecurity needs and emerging issues such as BYOD.

Investments in the government sector are declining at alarming rates, exacer-bated by uncertainty in defense spending and costly government procurement regulations. Contractors are making more selective investments in critical areas such as cybersecurity and UAVs; however, the key to success in the defense sector is designing more flexible aircraft and weapons systems that can readily adopt new technologies.

As the recovery of the global economy continues to lift the A&D industry out of a challenging market, continued investments in products, people and technology will help companies create competitive advantage and ensure long-term, sustain-able growth.

PRINCIPAL AUTHORS AND CONTRIBUTORSTim Ellis, Industry General Manager, Global Aerospace & Defense, CSC

Ahmed El Adl, Chief Technology Officer, Global Manufacturing, CSC

John Rassieur, Americas Consulting Leader, Aerospace & Defense, CSC

Dave Howells, Senior Principal Consultant, Aerospace & Defense, CSC

Bill Koss, Assistant Vice President, Contracts & Finance, National Security & Acquisition Policy, AIA

FEEDBACK? Contact us at csc .com/2015A&Dsurvey.

ABOUT CSCWith 50+ year heritage in aerospace and defense, CSC is a global leader of next-generation information technology (IT) services and solutions. CSC works closely with the world’s leading government and commercial A&D clients world-wide to transform traditional IT environments, manage and analyze data, and take advantage of mobility and emerging technologies. For more information, visit the company’s website at csc .com.

ABOUT AIABased in Arlington, Virginia, the Aerospace Industries Association (AIA) is led by a Board of Governors that meets twice a year and consists of senior representa-tives of member companies at the C-suite level, and an Executive Committee that meets more frequently. A hallmark of AIA is that it receives its policy guidance from the direct involvement of CEO-level officers of the country’s major aero-space and defense companies. The government frequently seeks advice from AIA on issues, and AIA provides a forum for government and industry representatives to exchange views and resolve problems on non-competitive matters related to the aerospace and defense industry. For more information, visit AIA’s website at aia-aerospace .org.

Audits

Cost and pricing requirements

Quality assurance

Information security/protection

Other

No

Yes, 0–10%

Yes, 11–25%

Yes, more than 25%

26 27

2015 A&D MARKET SURVEY 2015 A&D MARKET SURVEY