C H A P T E R 10 ACQUISITION AND DISPOSITION OF PROPERTY, PLANT, AND EQUIPMENT

This IFRS Supplement provides expanded discussions of accounting guidance underInternational Financial Reporting Standards (IFRS) for the topics in IntermediateAccounting. The discussions are organized according to the chapters in IntermediateAccounting (13th or 14th Editions) and therefore can be used to supplement the U.S. GAAPrequirements as presented in the textbook. Assignment material is provided for each sup-plement chapter, which can be used to assess and reinforce student understanding of IFRS.

GOVERNMENT GRANTSMany companies receive government grants. Government grants are assistance re-ceived from a government in the form of transfers of resources to a company in returnfor past or future compliance with certain conditions relating to the operating activi-ties of the company.1 For example, ABInBev NV (BEL) received government grantsrelated to fiscal incentives given by certain Brazilian states, based on the company’soperations and investments in these states. Danisco A/S (DEN) notes that it receivesgovernment grants for such items as research, development, and carbon-dioxide (CO2)allowances and investments.

In other words, a government grant is often some type of asset (such as cash; secu-rities; property, plant, and equipment; or use of facilities) provided as a subsidy to a com-pany. A government grant also occurs when debt is forgiven or borrowings are providedto the company at a below-market interest rate. The major accounting issues with gov-ernment grants are to determine the proper method of accounting for these transfers onthe company’s books and how they should be presented in the financial statements.

Accounting ApproachesWhen companies acquire an asset such as property, plant, and equipment through agovernment grant, a strict cost concept dictates that the valuation of the asset shouldbe zero. However, a departure from the cost principle seems justified because the onlycosts incurred (legal fees and other relatively minor expenditures) are not a reasonablebasis of accounting for the assets acquired. To record nothing is to ignore the economicrealities of an increase in wealth and assets. Therefore, most companies use the fairvalue of the asset to establish its value on the books.

What, then, is the proper accounting for the credit related to the government grantwhen the fair value of the asset is used? Two approaches are suggested—the capital(equity) approach and the income approach. Supporters of the equity approach believethe credit should go directly to equity because often no repayment of the grant isexpected. In addition, these grants are an incentive by the government—they are notearned as part of normal operations and should not offset expenses of operations onthe income statement.

Supporters of the income approach disagree—they believe that the credit should bereported as revenue in the income statement. Government grants should not go directly

1Recognize that there is a distinction between government grants and governmentassistance. Government assistance can take many forms, such as providing advice related to technical legal or product issues or being a supplier for the company’s goods or services.Government grants are a special part of government assistance where financial resourcesare provided to the company. In rare situations, a company may receive a donation (gift).The accounting for grants and donations is essentially the same. IFRS does provide anoption of recording property, plant, and equipment at zero cost although it appears thispractice is rarely followed.

U.S. GAAP PERSPECTIVE

Under U.S. GAAP, companiesreport grants at fair value. Ingeneral, companiesrecognize grants as revenuein the period received.

Chapter 10 Acquisition and Disposition of Property, Plant, and Equipment · 10–1

10–2 · IFRS Supplement

to equity because the government is not a shareholder. In addition, most governmentgrants have conditions attached to them which likely affect future expenses. They should,therefore, be reported as grant revenue (or deferred grant revenue) and matched withthe associated expenses that will occur in the future as a result of the grant.

Income ApproachIFRS requires the income approach and indicates that the general rule is that grants shouldbe recognized in income on a systematic basis that matches them with the related coststhat they are intended to compensate. [1] This is accomplished in one of two ways foran asset such as property, plant, and equipment:

1. Recording the grant as deferred grant revenue, which is recognized as income on asystematic basis over the useful life of the asset, or

2. Deducting the grant from the carrying amount of the assets received from the grant,in which case the grant is recognized in income as a reduction of depreciation expense.

To illustrate application of the income approach, consider the following three examples.

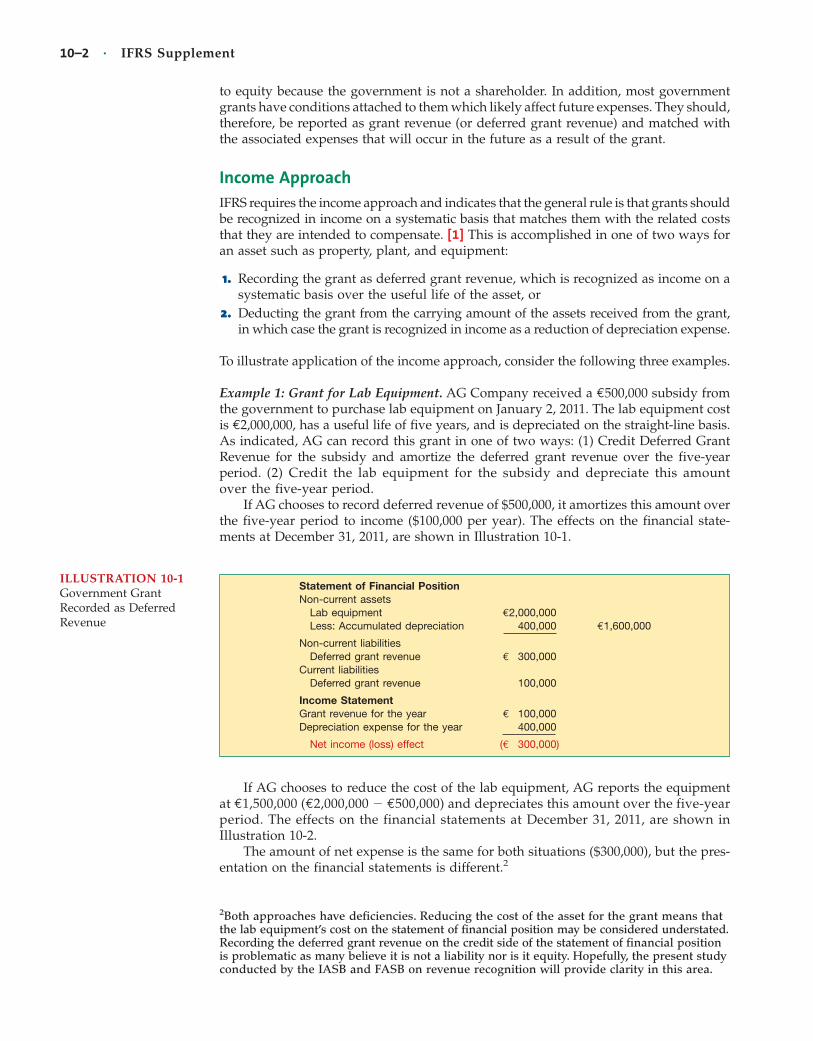

Example 1: Grant for Lab Equipment. AG Company received a €500,000 subsidy fromthe government to purchase lab equipment on January 2, 2011. The lab equipment costis €2,000,000, has a useful life of five years, and is depreciated on the straight-line basis.As indicated, AG can record this grant in one of two ways: (1) Credit Deferred GrantRevenue for the subsidy and amortize the deferred grant revenue over the five-yearperiod. (2) Credit the lab equipment for the subsidy and depreciate this amountover the five-year period.

If AG chooses to record deferred revenue of $500,000, it amortizes this amount overthe five-year period to income ($100,000 per year). The effects on the financial state-ments at December 31, 2011, are shown in Illustration 10-1.

Statement of Financial PositionNon-current assets

Lab equipment €2,000,000Less: Accumulated depreciation 400,000 €1,600,000

Non-current liabilitiesDeferred grant revenue € 300,000

Current liabilitiesDeferred grant revenue 100,000

Income StatementGrant revenue for the year € 100,000Depreciation expense for the year 400,000

Net income (loss) effect (€ 300,000)

ILLUSTRATION 10-1Government GrantRecorded as DeferredRevenue

2Both approaches have deficiencies. Reducing the cost of the asset for the grant means thatthe lab equipment’s cost on the statement of financial position may be considered understated.Recording the deferred grant revenue on the credit side of the statement of financial positionis problematic as many believe it is not a liability nor is it equity. Hopefully, the present studyconducted by the IASB and FASB on revenue recognition will provide clarity in this area.

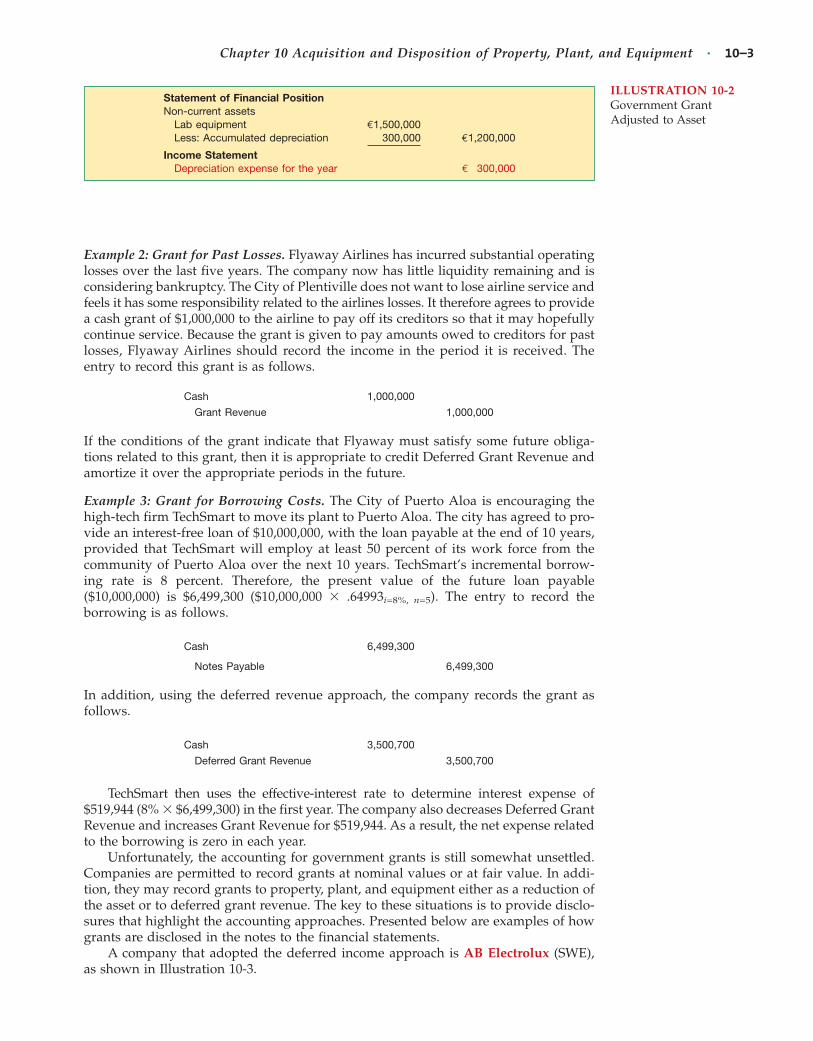

If AG chooses to reduce the cost of the lab equipment, AG reports the equipmentat €1,500,000 (€2,000,000 � €500,000) and depreciates this amount over the five-yearperiod. The effects on the financial statements at December 31, 2011, are shown inIllustration 10-2.

The amount of net expense is the same for both situations ($300,000), but the pres-entation on the financial statements is different.2

Example 2: Grant for Past Losses. Flyaway Airlines has incurred substantial operatinglosses over the last five years. The company now has little liquidity remaining and isconsidering bankruptcy. The City of Plentiville does not want to lose airline service andfeels it has some responsibility related to the airlines losses. It therefore agrees to providea cash grant of $1,000,000 to the airline to pay off its creditors so that it may hopefullycontinue service. Because the grant is given to pay amounts owed to creditors for pastlosses, Flyaway Airlines should record the income in the period it is received. Theentry to record this grant is as follows.

Cash 1,000,000

Grant Revenue 1,000,000

If the conditions of the grant indicate that Flyaway must satisfy some future obliga-tions related to this grant, then it is appropriate to credit Deferred Grant Revenue andamortize it over the appropriate periods in the future.

Example 3: Grant for Borrowing Costs. The City of Puerto Aloa is encouraging thehigh-tech firm TechSmart to move its plant to Puerto Aloa. The city has agreed to pro-vide an interest-free loan of $10,000,000, with the loan payable at the end of 10 years,provided that TechSmart will employ at least 50 percent of its work force from thecommunity of Puerto Aloa over the next 10 years. TechSmart’s incremental borrow-ing rate is 8 percent. Therefore, the present value of the future loan payable($10,000,000) is $6,499,300 ($10,000,000 � .64993i=8%, n=5). The entry to record theborrowing is as follows.

Cash 6,499,300

Notes Payable 6,499,300

In addition, using the deferred revenue approach, the company records the grant asfollows.

Cash 3,500,700

Deferred Grant Revenue 3,500,700

TechSmart then uses the effective-interest rate to determine interest expense of$519,944 (8% � $6,499,300) in the first year. The company also decreases Deferred GrantRevenue and increases Grant Revenue for $519,944. As a result, the net expense relatedto the borrowing is zero in each year.

Unfortunately, the accounting for government grants is still somewhat unsettled.Companies are permitted to record grants at nominal values or at fair value. In addi-tion, they may record grants to property, plant, and equipment either as a reduction ofthe asset or to deferred grant revenue. The key to these situations is to provide disclo-sures that highlight the accounting approaches. Presented below are examples of howgrants are disclosed in the notes to the financial statements.

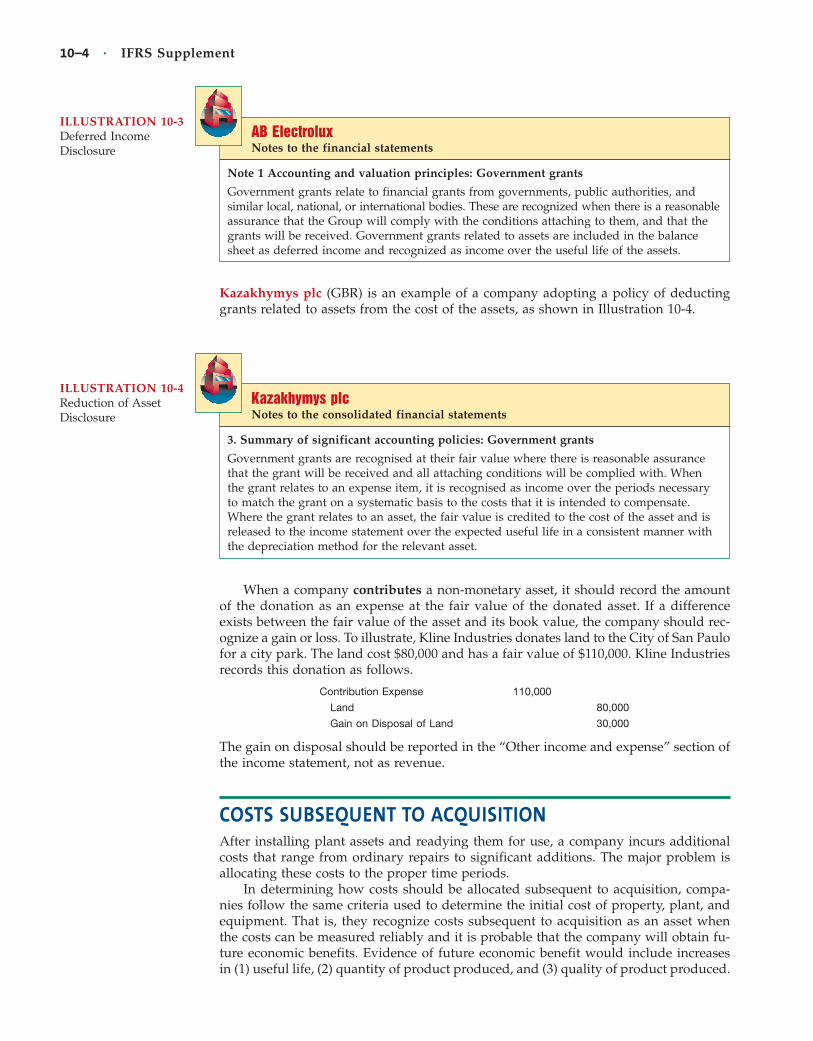

A company that adopted the deferred income approach is AB Electrolux (SWE),as shown in Illustration 10-3.

Statement of Financial PositionNon-current assets

Lab equipment €1,500,000Less: Accumulated depreciation 300,000 €1,200,000

Income StatementDepreciation expense for the year € 300,000

ILLUSTRATION 10-2Government GrantAdjusted to Asset

Chapter 10 Acquisition and Disposition of Property, Plant, and Equipment · 10–3

10–4 · IFRS Supplement

When a company contributes a non-monetary asset, it should record the amountof the donation as an expense at the fair value of the donated asset. If a differenceexists between the fair value of the asset and its book value, the company should rec-ognize a gain or loss. To illustrate, Kline Industries donates land to the City of San Paulofor a city park. The land cost $80,000 and has a fair value of $110,000. Kline Industriesrecords this donation as follows.

Contribution Expense 110,000

Land 80,000

Gain on Disposal of Land 30,000

The gain on disposal should be reported in the “Other income and expense” section ofthe income statement, not as revenue.

COSTS SUBSEQUENT TO ACQUISITIONAfter installing plant assets and readying them for use, a company incurs additionalcosts that range from ordinary repairs to significant additions. The major problem isallocating these costs to the proper time periods.

In determining how costs should be allocated subsequent to acquisition, compa-nies follow the same criteria used to determine the initial cost of property, plant, andequipment. That is, they recognize costs subsequent to acquisition as an asset whenthe costs can be measured reliably and it is probable that the company will obtain fu-ture economic benefits. Evidence of future economic benefit would include increasesin (1) useful life, (2) quantity of product produced, and (3) quality of product produced.

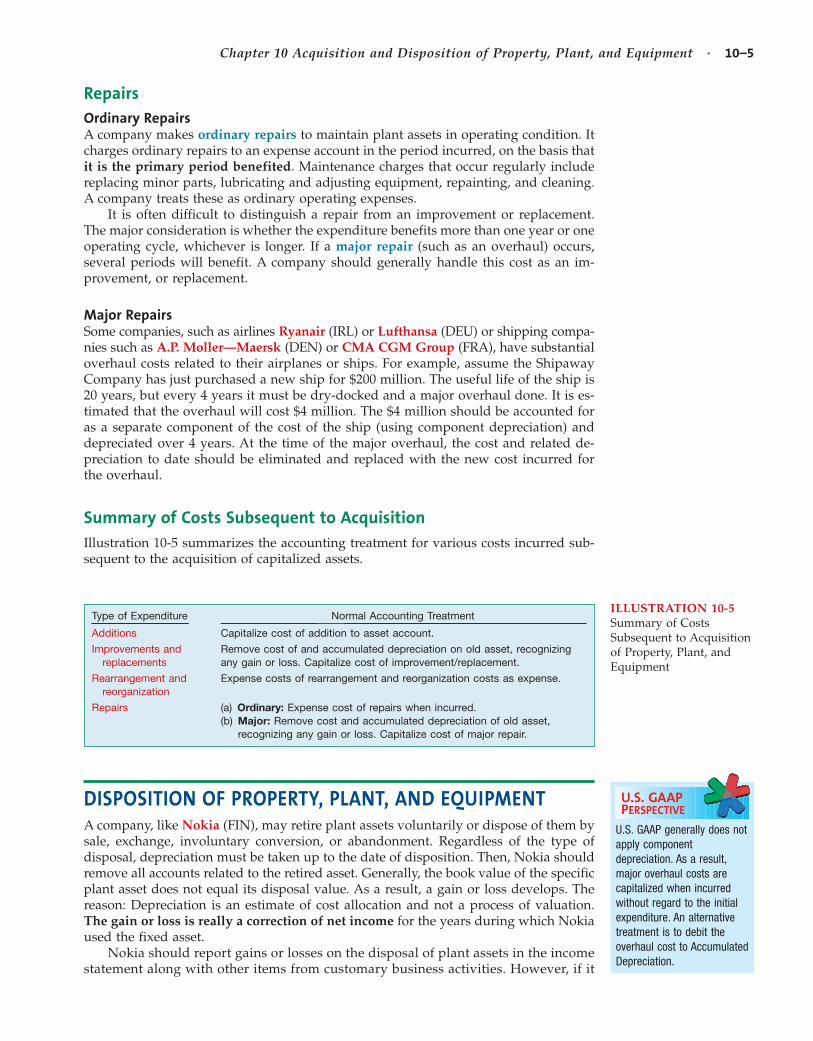

ILLUSTRATION 10-4Reduction of AssetDisclosure

Kazakhymys plcNotes to the consolidated financial statements

3. Summary of significant accounting policies: Government grants

Government grants are recognised at their fair value where there is reasonable assurancethat the grant will be received and all attaching conditions will be complied with. Whenthe grant relates to an expense item, it is recognised as income over the periods necessaryto match the grant on a systematic basis to the costs that it is intended to compensate.Where the grant relates to an asset, the fair value is credited to the cost of the asset and isreleased to the income statement over the expected useful life in a consistent manner withthe depreciation method for the relevant asset.

ILLUSTRATION 10-3Deferred IncomeDisclosure

AB ElectroluxNotes to the financial statements

Note 1 Accounting and valuation principles: Government grants

Government grants relate to financial grants from governments, public authorities, andsimilar local, national, or international bodies. These are recognized when there is a reasonableassurance that the Group will comply with the conditions attaching to them, and that thegrants will be received. Government grants related to assets are included in the balancesheet as deferred income and recognized as income over the useful life of the assets.

Kazakhymys plc (GBR) is an example of a company adopting a policy of deductinggrants related to assets from the cost of the assets, as shown in Illustration 10-4.

RepairsOrdinary RepairsA company makes ordinary repairs to maintain plant assets in operating condition. Itcharges ordinary repairs to an expense account in the period incurred, on the basis thatit is the primary period benefited. Maintenance charges that occur regularly includereplacing minor parts, lubricating and adjusting equipment, repainting, and cleaning.A company treats these as ordinary operating expenses.

It is often difficult to distinguish a repair from an improvement or replacement.The major consideration is whether the expenditure benefits more than one year or oneoperating cycle, whichever is longer. If a major repair (such as an overhaul) occurs,several periods will benefit. A company should generally handle this cost as an im-provement, or replacement.

Major RepairsSome companies, such as airlines Ryanair (IRL) or Lufthansa (DEU) or shipping compa-nies such as A.P. Moller—Maersk (DEN) or CMA CGM Group (FRA), have substantialoverhaul costs related to their airplanes or ships. For example, assume the ShipawayCompany has just purchased a new ship for $200 million. The useful life of the ship is20 years, but every 4 years it must be dry-docked and a major overhaul done. It is es-timated that the overhaul will cost $4 million. The $4 million should be accounted foras a separate component of the cost of the ship (using component depreciation) anddepreciated over 4 years. At the time of the major overhaul, the cost and related de-preciation to date should be eliminated and replaced with the new cost incurred forthe overhaul.

Summary of Costs Subsequent to AcquisitionIllustration 10-5 summarizes the accounting treatment for various costs incurred sub-sequent to the acquisition of capitalized assets.

Type of Expenditure Normal Accounting Treatment

Additions Capitalize cost of addition to asset account.

Improvements and Remove cost of and accumulated depreciation on old asset, recognizingreplacements any gain or loss. Capitalize cost of improvement/replacement.

Rearrangement and Expense costs of rearrangement and reorganization costs as expense.reorganization

Repairs (a) Ordinary: Expense cost of repairs when incurred.(b) Major: Remove cost and accumulated depreciation of old asset,

recognizing any gain or loss. Capitalize cost of major repair.

ILLUSTRATION 10-5Summary of CostsSubsequent to Acquisitionof Property, Plant, andEquipment

DISPOSITION OF PROPERTY, PLANT, AND EQUIPMENTA company, like Nokia (FIN), may retire plant assets voluntarily or dispose of them bysale, exchange, involuntary conversion, or abandonment. Regardless of the type ofdisposal, depreciation must be taken up to the date of disposition. Then, Nokia shouldremove all accounts related to the retired asset. Generally, the book value of the specificplant asset does not equal its disposal value. As a result, a gain or loss develops. Thereason: Depreciation is an estimate of cost allocation and not a process of valuation.The gain or loss is really a correction of net income for the years during which Nokiaused the fixed asset.

Nokia should report gains or losses on the disposal of plant assets in the incomestatement along with other items from customary business activities. However, if it

U.S. GAAP PERSPECTIVE

U.S. GAAP generally does notapply componentdepreciation. As a result,major overhaul costs arecapitalized when incurredwithout regard to the initialexpenditure. An alternativetreatment is to debit theoverhaul cost to AccumulatedDepreciation.

Chapter 10 Acquisition and Disposition of Property, Plant, and Equipment · 10–5

QUESTIONS

1. How should the amount of interest capitalized be dis-closed in the notes to the financial statements? Howshould interest revenue from temporarily invested excessfunds borrowed to finance the construction of assets beaccounted for?

2. Ito Company receives a local government grant to helpdefray the cost of its plant facilitates. The grant is providedto encourage Ito to move its operations to a certain area.Explain how the grant might be reported.

sold, abandoned, spun off, or otherwise disposed of the “operations of a component ofa business,” then it should report the results separately in the discontinued operationssection of the income statement. That is, Nokia should report any gain or loss fromdisposal of a business component with the related results of discontinued operations.

Authoritative Literature References[1] International Accounting Standard 20, Accounting for Government Grants and Disclosure of Government Assistance

(London, U.K.: International Accounting Standards Committee Foundation, 2001).

AUTHORITATIVE LITERATURE

10–6 · IFRS Supplement

EXERCISES

E10-1 (Government Grants) In 2010, Sato Corporation received a grant for ¥2 million to defray thecost of purchasing research equipment for its manufacturing facility. The total cost of the equipment is¥10 million.

InstructionsPrepare the journal entry to record this transaction, if Sato uses (a) the deferred revenue approach, and(b) the reduction of asset approach.

E10-2 (Government Grants) Rialto Group received a grant from the government of £100,000 toacquire £500,000 of delivery equipment on January 2, 2010. The delivery equipment has a useful lifeof 5 years. Rialto uses the straight-line method of depreciation. The delivery equipment has a zeroresidual value.

Instructions(a) If Rialto Group reports the grant as a reduction of the asset, answer the following questions.

(1) What is the carrying amount of the delivery equipment at December 31, 2010?(2) What is the amount of depreciation expense related to the delivery equipment in 2011?(3) What is the amount of grant revenue reported in 2010 on the income statement?

(b) If Rialto Group reports the grant as deferred grant revenue, answer the following questions.(1) What is the balance in the deferred grant revenue account at December 31, 2010?(2) What is the amount of depreciation expense related to the delivery equipment in 2011?(3) What is the amount of grant revenue reported in 2010 on the income statement?

E10-3 (Government Grants) Yilmaz Company is provided a grant by the local government to purchaseland for a building site. The grant is a zero-interest-bearing note for 5 years. The note is issued on Janu-ary 2, 2010, for €5 million payable on January 2, 2015. Yilmaz’s incremental borrowing rate is 6%. The landis not purchased until July 15, 2010.

Instructions(a) Prepare the journal entry(ies) to record the grant and note payable on January 2, 2010.(b) Determine the amount of interest expense and grant revenue to be reported on December 31, 2010.

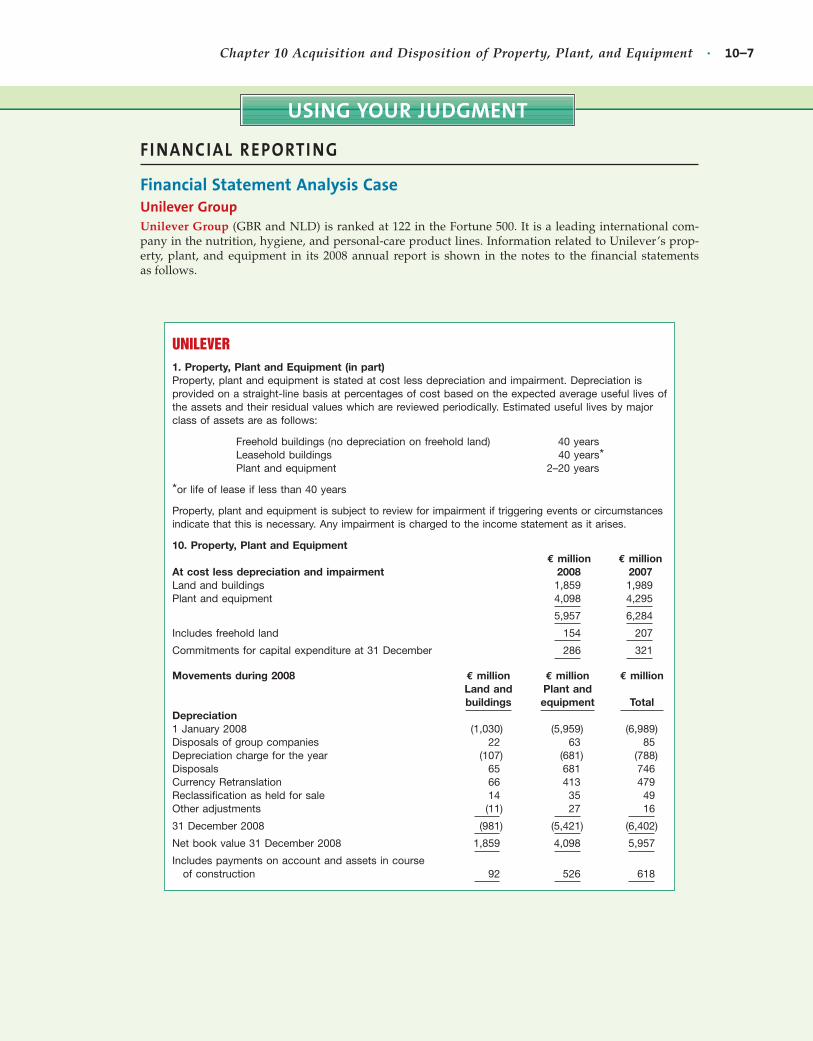

Chapter 10 Acquisition and Disposition of Property, Plant, and Equipment · 10–7

UNILEVER

1. Property, Plant and Equipment (in part)Property, plant and equipment is stated at cost less depreciation and impairment. Depreciation isprovided on a straight-line basis at percentages of cost based on the expected average useful lives ofthe assets and their residual values which are reviewed periodically. Estimated useful lives by majorclass of assets are as follows:

Freehold buildings (no depreciation on freehold land) 40 yearsLeasehold buildings 40 years*Plant and equipment 2–20 years

*or life of lease if less than 40 years

Property, plant and equipment is subject to review for impairment if triggering events or circumstancesindicate that this is necessary. Any impairment is charged to the income statement as it arises.

10. Property, Plant and Equipment€ million € million

At cost less depreciation and impairment 2008 2007Land and buildings 1,859 1,989Plant and equipment 4,098 4,295

5,957 6,284

Includes freehold land 154 207

Commitments for capital expenditure at 31 December 286 321

Movements during 2008 € million € million € millionLand and Plant andbuildings equipment Total

Depreciation1 January 2008 (1,030) (5,959) (6,989)Disposals of group companies 22 63 85Depreciation charge for the year (107) (681) (788)Disposals 65 681 746Currency Retranslation 66 413 479Reclassification as held for sale 14 35 49Other adjustments (11) 27 16

31 December 2008 (981) (5,421) (6,402)

Net book value 31 December 2008 1,859 4,098 5,957

Includes payments on account and assets in courseof construction 92 526 618

USING YOUR JUDGMENT

FI NANCIAL REPORTI NG

Financial Statement Analysis CaseUnilever GroupUnilever Group (GBR and NLD) is ranked at 122 in the Fortune 500. It is a leading international com-pany in the nutrition, hygiene, and personal-care product lines. Information related to Unilever’s prop-erty, plant, and equipment in its 2008 annual report is shown in the notes to the financial statementsas follows.

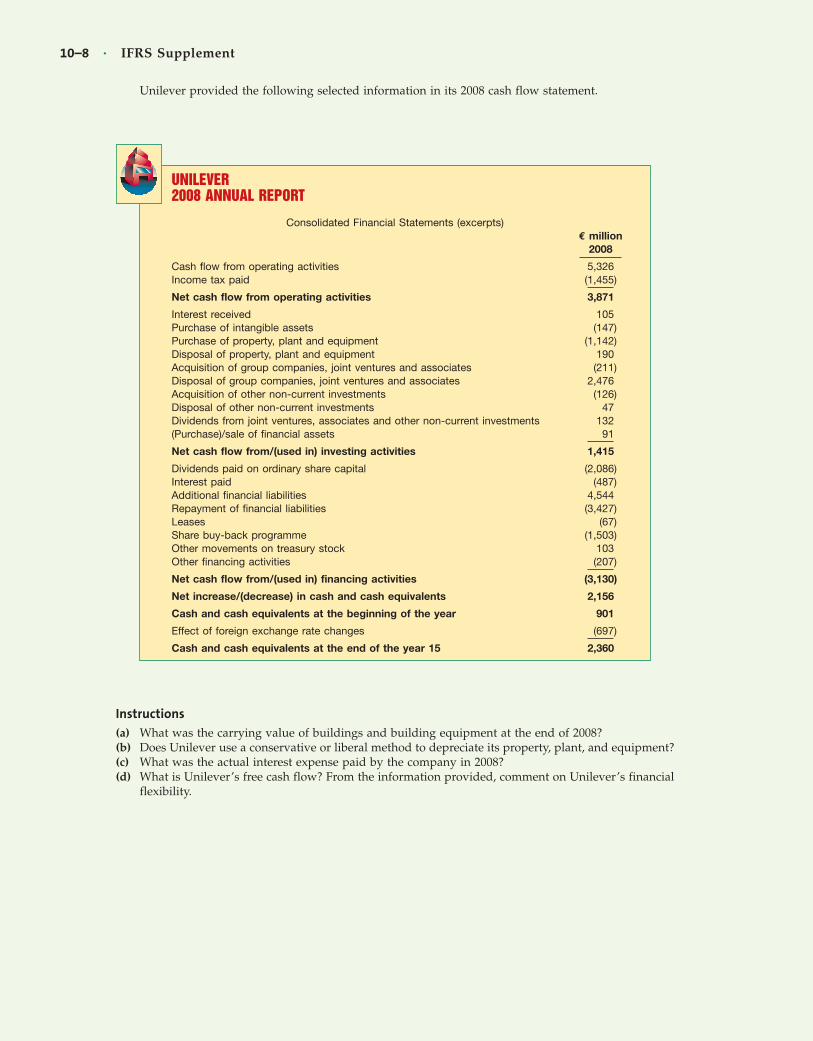

Unilever provided the following selected information in its 2008 cash flow statement.

UNILEVER 2008 ANNUAL REPORT

Consolidated Financial Statements (excerpts)€ million

2008

Cash flow from operating activities 5,326Income tax paid (1,455)

Net cash flow from operating activities 3,871

Interest received 105Purchase of intangible assets (147)Purchase of property, plant and equipment (1,142)Disposal of property, plant and equipment 190Acquisition of group companies, joint ventures and associates (211)Disposal of group companies, joint ventures and associates 2,476Acquisition of other non-current investments (126)Disposal of other non-current investments 47Dividends from joint ventures, associates and other non-current investments 132(Purchase)/sale of financial assets 91

Net cash flow from/(used in) investing activities 1,415

Dividends paid on ordinary share capital (2,086)Interest paid (487)Additional financial liabilities 4,544Repayment of financial liabilities (3,427)Leases (67)Share buy-back programme (1,503)Other movements on treasury stock 103Other financing activities (207)

Net cash flow from/(used in) financing activities (3,130)

Net increase/(decrease) in cash and cash equivalents 2,156

Cash and cash equivalents at the beginning of the year 901

Effect of foreign exchange rate changes (697)

Cash and cash equivalents at the end of the year 15 2,360

Instructions

(a) What was the carrying value of buildings and building equipment at the end of 2008?(b) Does Unilever use a conservative or liberal method to depreciate its property, plant, and equipment?(c) What was the actual interest expense paid by the company in 2008?(d) What is Unilever’s free cash flow? From the information provided, comment on Unilever’s financial

flexibility.

10–8 · IFRS Supplement

BRI DGE TO TH E PROFESSION

Professional ResearchYour client is in the planning phase for a major plant expansion, which will involve the construction ofa new warehouse. The assistant controller does not believe that interest cost can be included in the costof the warehouse, because it is a financing expense. Others on the planning team believe that some inter-est cost can be included in the cost of the warehouse, but no one could identify the specific authoritativeguidance for this issue. Your supervisor asks you to research this issue.

Instructions

Access the IFRS authoritative literature at the IASB website (http://eifrs.iasb.org/). When you have accessedthe documents, you can use the search tool in your Internet browser to respond to the following ques-tions. (Provide paragraph citations.)

(a) Is it permissible to capitalize interest into the cost of assets? Provide authoritative support for youranswer.

(b) What are the objectives for capitalizing interest?(c) Discuss which assets qualify for interest capitalization.(d) Is there a limit to the amount of interest that may be capitalized in a period?(e) If interest capitalization is allowed, what disclosures are required?

Chapter 10 Acquisition and Disposition of Property, Plant, and Equipment · 10–9