© 1991-2010 00391878CV

Macro Asset PerspectiveMacro Asset Perspective®

A Wealth Accumulation SeminarA Wealth Accumulation Seminar

© 1991-2010 00391878CV

Presented byPresented by

Vanessa DiegoVanessa DiegoAgent, New York Life Insurance CompanyAgent, New York Life Insurance Company

WA Lic# 745908WA Lic# 745908

Seattle G.O, (Seattle West Campus) 500 Yale Ave. N Seattle G.O, (Seattle West Campus) 500 Yale Ave. N Suite 400 Seattle, WA 98109Suite 400 Seattle, WA 98109

Presented forPresented for

This seminar is for informational purposes only. Neither New York Life Insurance This seminar is for informational purposes only. Neither New York Life Insurance Company, its subsidiaries, nor any of its agents are in the business of offering tax, Company, its subsidiaries, nor any of its agents are in the business of offering tax, legal or accounting advice. You should consult with your own professional advisors legal or accounting advice. You should consult with your own professional advisors

for tax, legal or accounting advice.for tax, legal or accounting advice.

© 1991-2010 00391878CV

Today’s Agenda

Charting Your Course with Charting Your Course with MAPMAP

““Wonder” of Tax Deductible Wonder” of Tax Deductible InvestingInvesting

Annual Asset ReallocationAnnual Asset Reallocation

A Financial EKGA Financial EKG

© 1991-2010 00391878CV

A Financial EKG

© 1991-2010 00391878CV

Financial EKG Financial EKG WorksheetWorksheetCurrent AgeCurrent Age

Desired Retirement Desired Retirement AgeAgeYears to Accomplish Years to Accomplish GoalGoalCurrent IncomeCurrent Income

Anticipated Rate of Anticipated Rate of ReturnReturnMonthly ContributionMonthly Contribution

Desired Retirement Desired Retirement IncomeIncome

5 More 5 More YearsYears

5 Less Years5 Less Years

404065652525

$80,000$80,000

8%/5%8%/5%$1,367$1,367

$60,000$60,000

$882$882 $2,185$2,185

$60K$60K

$30K$30K

$15K$15K

$120$120KK

$240$240KK

$1,200,000

55 7272)

1144

Income from Income from workingworking

Income from assetsIncome from assetsAccumulation Phase

Conservation Phase

Hypothetical example for illustrative purposes only.

© 1991-2010 00391878CV

A Wealth Accumulation A Wealth Accumulation Strategy Strategy

Macro Asset Perspective®®

© 1991-2010 00391878CV

MAP is designed to give you a visual picture of where assets can be placed and why.

© 1991-2010 00391878CV

The vertical arrangement of boxes represents the concept of vertical diversification.

s s

M M

A A

Paper Assets

Real Wealth

A A

© 1991-2010 00391878CV

Your personal diversification depends upon such factors as your age, risk tolerance and holding period.s s

M M

A A

Paper Assets

Real Wealth

© 1991-2010 00391878CV

A Wall Street “Rule of Thumb” suggests a percentage of assets equal to one’s age below the line. s s

M M

A A

Paper Assets

Real Wealth

© 1991-2010 00391878CV

One of the primary objectives of vertical diversification over time is to convert “paper assets” into “real wealth.”

s s

M M

A A

Paper Assets

Real Wealth

Vertical diversification has been touted for decades.

© 1991-2010 00391878CV

Recently another issue has emerged.- The concept of horizontal diversification.

That is, diversification between tax treatments.

s s

M M

A A

Paper Assets

Real Wealth

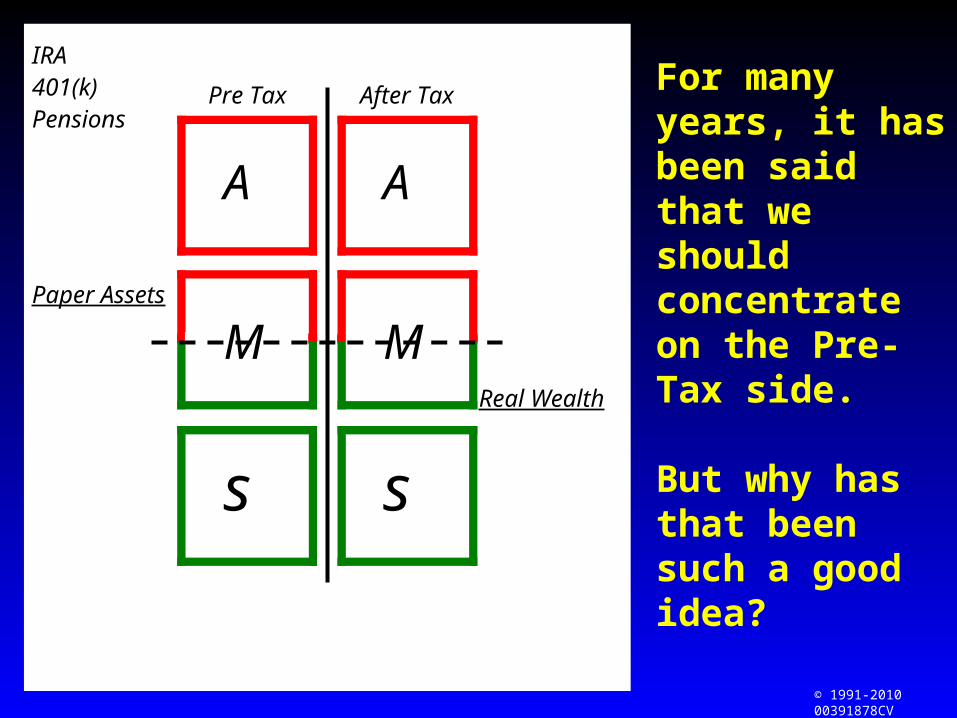

IRA401(k)Pensions

Pre Tax After Tax

© 1991-2010 00391878CV

For many years, it has been said that we should concentrate on the Pre-Tax side.

But why has that been such a good idea?

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

© 1991-2010 00391878CV

The top marginal tax bracket* in the eighties was 70 percent* *and there were 15 different brackets.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

$100,000

$80,000

25%-28%

70%

*Your MTB or marginal tax rate is the rate (%) at which your last dollar (last increment) of income is taxed.

**Source: Federal tax code 1981

© 1991-2010 00391878CV

Deferring taxes at 25 or 28 percent, to pay them later in a higher tax bracket would be a major mistake. s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

© 1991-2010 00391878CV

Don’t run out and cancel your 401(k) as some may be suggesting.

The pre-tax side can still be a great place to accumulate wealth if used properly.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

© 1991-2010 00391878CV

When you defer taxes at one bracket to pay them later in a lower bracket you make the pre-tax side work as it was intended to.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

Let’s see how to accomplish this.

© 1991-2010 00391878CV

The advantages found below-the-line are not generally needed on the pre-tax side.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

© 1991-2010 00391878CV

Historically, assets that have kept pace with inflation, or exceeded it, have been found above-the-line.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

© 1991-2010 00391878CV

The first rule of accumulation is simple –

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*Take the free money.Be sure to maximize any employer matching in pre-tax plans.Above-the-line is the key area on the Pre-Tax side.

© 1991-2010 00391878CV

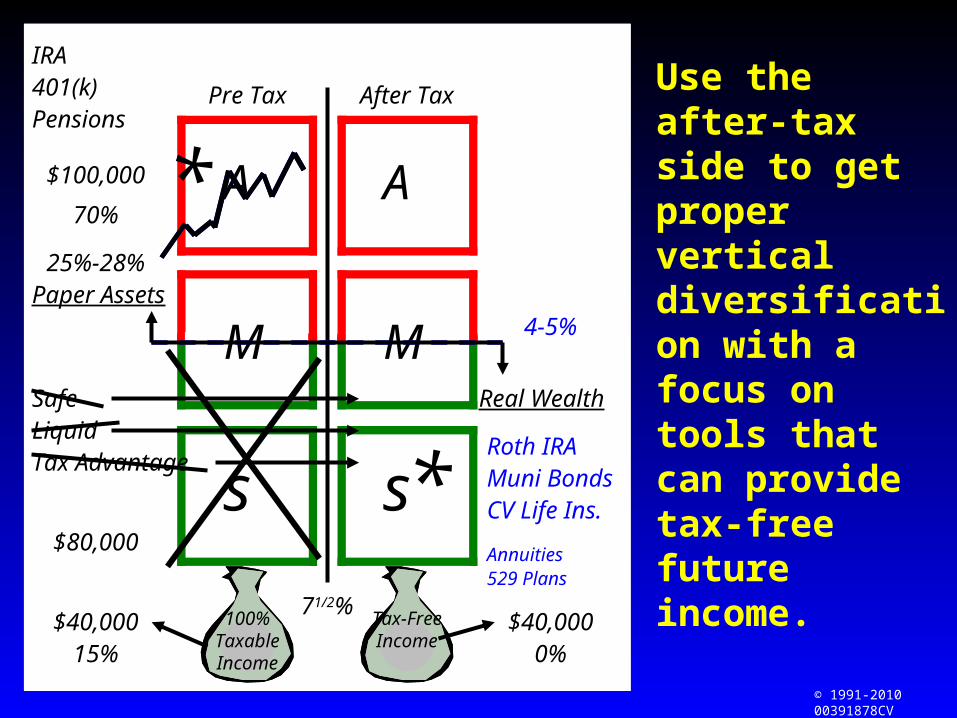

The advantages that were of little value on the pre-tax side, have great value on the after-tax side.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*

© 1991-2010 00391878CV

Use the after-tax side to get proper vertical diversification with a focus on tools that can provide tax-free future income.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*Roth IRAMuni BondsCV Life Ins.

Annuities529 Plans

4-5%

© 1991-2010 00391878CV

4 or 5 percent, tax-free, may be the equivalent of 7 or 8 percent taxable, depending upon your tax bracket.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*Roth IRAMuni BondsCV Life Ins.

Annuities529 Plans

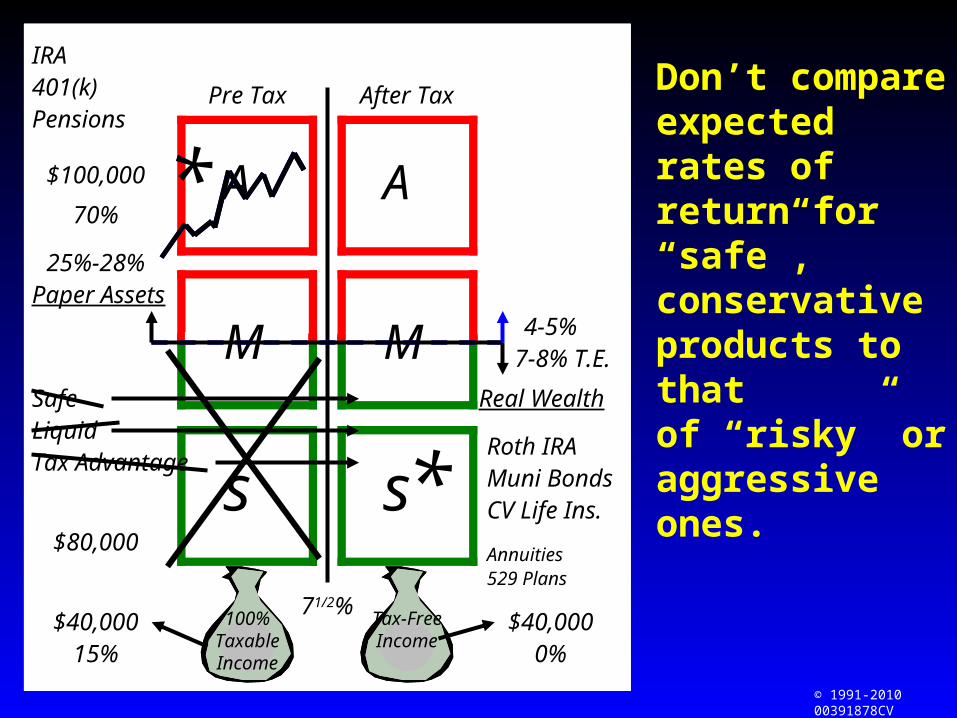

4-5%7-8% T.E.

© 1991-2010 00391878CV

Don’t compare expected rates of return for “safe”, conservative products to that of “risky” or aggressive ones.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*Roth IRAMuni BondsCV Life Ins.

Annuities529 Plans

4-5%7-8% T.E.

© 1991-2010 00391878CV

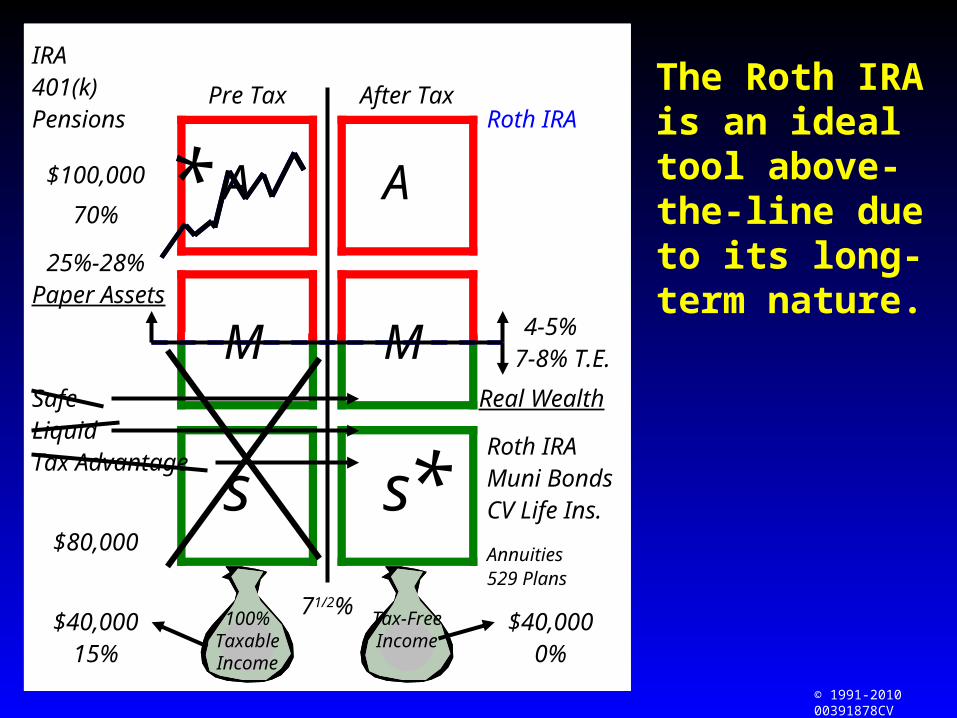

The Roth IRA is an ideal tool above-the-line due to its long-term nature.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*Roth IRAMuni BondsCV Life Ins.

Annuities529 Plans

4-5%7-8% T.E.

Roth IRA

© 1991-2010 00391878CV

Aside from the Roth, we are not generally looking for tax-free income above-the-line, but potential growth with a secondary consideration for tax advantages such as long-term capital gains.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*Roth IRAMuni BondsCV Life Ins.

Annuities529 Plans

4-5%7-8% T.E.

Roth IRAStock Mkt.Real Estate

© 1991-2010 00391878CV

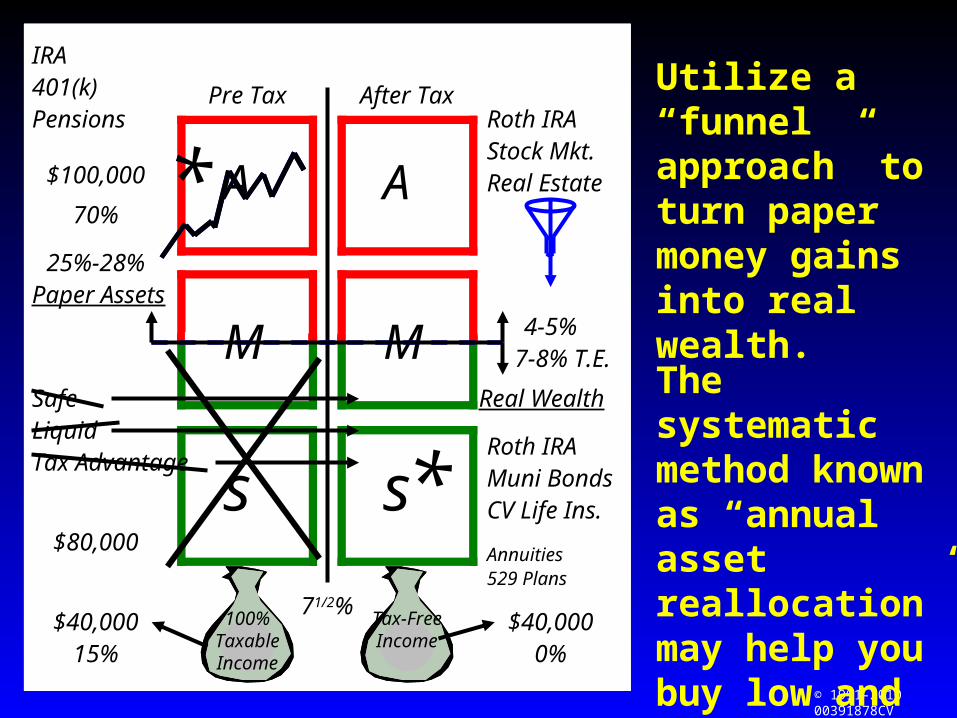

Utilize a “funnel approach” to turn paper money gains into real wealth.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*Roth IRAMuni BondsCV Life Ins.

Annuities529 Plans

4-5%7-8% T.E.

Roth IRAStock Mkt.Real Estate

The systematic method known as “annual asset reallocation” may help you buy low and sell high.

© 1991-2010 00391878CV

Possibly the best tool for the “funnel approach” is an Employee Stock Purchase Plan (ESPP).

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*Roth IRAMuni BondsCV Life Ins.

Annuities529 Plans

4-5%7-8% T.E.

Roth IRAStock Mkt.Real Estate

ESPP

An ESPP with a 15 percent discount provides a guaranteed minimum return-on-investment of 17.6 percent*.

*15 divided by 85 equals 17.6%

© 1991-2010 00391878CV

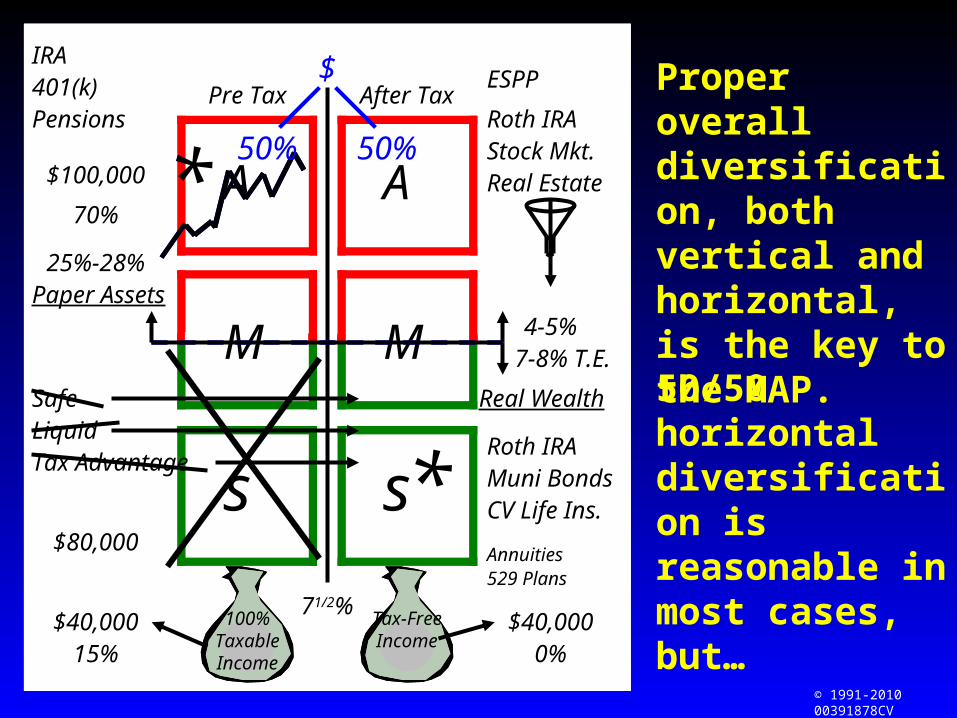

Proper overall diversification, both vertical and horizontal, is the key to the MAP.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*Roth IRAMuni BondsCV Life Ins.

Annuities529 Plans

4-5%7-8% T.E.

Roth IRAStock Mkt.Real Estate

ESPP$

50% 50%

50/50 horizontal diversification is reasonable in most cases, but…

© 1991-2010 00391878CV

Those desiring high retirement income may want to lean heavier toward the after-tax side to avoid paying taxes later at higher income tax rates.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*Roth IRAMuni BondsCV Life Ins.

Annuities529 Plans

4-5%7-8% T.E.

Roth IRAStock Mkt.Real Estate

ESPP$

50% 50%

50%

In most cases, the pre-tax side can be entirely above-the-line.

© 1991-2010 00391878CV

Use the after-tax side to maintain the desired overall vertical diversification percentages.

s s

M M

A A

Paper Assets

Real Wealth

IRA401(k)Pensions

Pre Tax After Tax

70%

$100,000

$80,000

25%-28%

100%Taxable Income

Tax-Free

Income

$40,000 $40,00015% 0%

71/2%

SafeLiquidTax Advantage

*

*Roth IRAMuni BondsCV Life Ins.

Annuities529 Plans

4-5%7-8% T.E.

Roth IRAStock Mkt.Real Estate

ESPP$

50% 50%

50%

25-50%

0-25%

75%

25%

© 1991-2010 00391878CV

A Wealth Accumulation A Wealth Accumulation Strategy Strategy

Macro Asset Perspective®

© 1991-2010 00391878CV

The “Wonder” of Tax-Deductible Investing

© 1991-2010 00391878CV

RobertRobertTax-Deductible Tax-Deductible

401(k)401(k)

RobertaRobertaNon-Deductible Roth Non-Deductible Roth

IRAIRA

Annual AvailableAnnual AvailableContributionContribution

Tax Tax Paid Paid Account Balance Day Account Balance Day

11If Accessed Day If Accessed Day 22Tax PaidTax Paid

Net Balance Day 2Net Balance Day 2

Balance at Balance at RetirementRetirementIf Liquidated at If Liquidated at RetirementRetirementTax PaidTax Paid

Net Retirement Net Retirement BalanceBalancePost Retirement Post Retirement

Cash FlowCash FlowAnnual WithdrawalAnnual Withdrawal

Tax PaidTax Paid

Net Retirement Cash Net Retirement Cash FlowFlow

004,0004,000

1,001,00003,0003,000

1,0001,0003,0003,000

003,0003,000

400,00400,0000

300,00300,0000

100,00100,0000300,00300,0000

00300,00300,00

0040,00040,000 30,00030,00010,00010,00030,00030,000

0030,00030,000

6,0006,00034,00034,000

15%15%14,00014,000 35%35%

26,00026,000

$4,000$4,000

25%25%

10,00010,00030,00030,000

25%25%

© 1991-2010 00391878CV

Cash Flow ComparisonCash Flow ComparisonRobertRobert RobertaRoberta

$100,000$100,000Salary:Salary:

401(k) 401(k) Contribution:Contribution: $4,000$4,000

$96,000$96,000Taxable Income: Taxable Income:

$24,000$24,000Hypothetical Hypothetical Tax: Tax:

$72,000$72,000Net Spendable:Net Spendable:

$100,000$100,000Salary:Salary:

Hypothetical Hypothetical Tax: Tax: $25,000$25,000

$75,000$75,000After-Tax After-Tax Income:Income:

$3,000$3,000Roth Contribution:Roth Contribution:

$72,000$72,000Net Net Spendable:Spendable:

© 1991-2010 00391878CV

Annual Asset Reallocation

© 1991-2010 00391878CV

AA BB CC

Buy Buy HighHigh

Sell Sell LowLow

Buy Buy LowLow

Sell Sell HighHigh

CCCC

Annual Asset Reallocation

BalanceBalance

Re-Re-BalanceBalance

© 1991-2010 00391878CV

AA BB CCCCCC DDDD

Company Stock

Component

© 1991-2010 00391878CV

Macro Asset PerspectiveMacro Asset Perspective®®

A Wealth Accumulation SeminarA Wealth Accumulation Seminar