dermatological drugs market forecast 2015-2025

TRANSCRIPT

©noticeThis material is copyright by visiongain. It is against the law to reproduce any of this material without the prior written agreement of visiongain. You cannot photocopy, fax, download to database or duplicate in any other way any of the material contained in this report. Each purchase and single copy is for personal use only.

Dermatological Drugs Market Forecast 2015-2025

Opportunities for Leading Companies

www.visiongain.com

Contents

1. Report Overview

1.1 Global Dermatological Drugs: Market Overview

1.2 Global Dermatological Drugs Market Segmentation

1.3 Why You Should Read This Report

1.4 How This Report Delivers

1.5 Key Questions Answered By This Analytical Report

1.6 Who Is This Report For?

1.7 Methodology

1.8 Frequently Asked Questions (FAQ)

1.9 Associated Reports

1.10 About Visiongain

2.1 The Pharmaceutical Industry: A Brief Introduction

2.2 An Introduction To Dermatology

2.2.1 The Structural Lay-out Of The Skin, Hair, And Nails

2.2.2 Hair And Nails

2.2.3 Sweat And Sebaceous Glands

2.2.4 Functions Of The Skin

2.3 Common Skin Diseases

2.4 Acne: The Most Common Skin Disease

2.4.1 Acne: Epidemiology

2.4.2 Acne: Causes And Pathogenesis

2.4.3 Acne: Treatment

2.5 Dermatitis: Inflammation Of The Skin

2.5.1 Atopic Dermatitis

2.5.2 Contact Dermatitis

1. Report Overview

2. An Introduction To Dermatological Drugs

www.visiongain.com

Contents

2.5.3 Seborrhoeic Dermatitis

2.5.4 Nummular Dermatitis

2.5.5 Perioral Dermatitis

2.6 Psoriasis: A Complex Multi-factorial Disease

2.7 Rosacea: Vascular Instability

2.8 Alopecia: Excessive Shedding Of Hair

2.9 Skin Infections: A Serious Healthcare Threat

2.9.1 Bacterial Skin Infections

2.9.2 Fungal Skin Infections

2.9.3 Viral Skin Infections

2.10 Common Skin Treatments

2.10.1 Creams and Semisolid Emulsions

2.10.2 Ointments

2.10.3 Lotions

2.10.4 Solutions

2.10.5 Occlusive Therapy

2.10.6 Cleansing Agents

2.10.7 Powders and Hydrophilic Polymer

2.10.8 Anti-Infective Agents

2.10.9 Anti-Inflammatory Agents

2.11 Phases Of Clinical Trials

2.12 Dermatological Drugs: Market Definition In This Report

3.1 The Global Dermatological Drugs Market: Market Overview

3.2 Categorisation Of The Global Dermatological Drugs Market

3.3 The Global Dermatological Drugs Market In 2014

3.4 The Global Dermatological Drugs Market: Market Forecast 2015-2025

3.5 Dermatological Drugs: Changing Market Shares By Sector 2015-2025

3. The Global Dermatological Drugs Market, 2015-2025

www.visiongain.com

Contents

4.1 Psoriasis Treatments: The Dominance Of Biologics

4.1.1 Leading Products In The Psoriasis Drugs Market, 2014

4.2 Psoriasis: Market Trends And Developments, 2015

4.2.1 Biological Drugs In Psoriasis Treatment: A Brief Overview

4.2.2 Issues Around Patent Protection, The Threat Of Biosimilars And Pricing

4.2.3 The Disadvantages Of Biologics In Psoriasis Treatment

4.3 Psoriasis Drugs: Market Forecast 2015-2025

4.3.1 Psoriasis Drugs: Changing Market Shares By Leading Drugs 2015-2025

4.4 Leading Drugs Used In The Treatment Of Psoriasis

4.5 Humira (adalimumab) - AbbVie

4.5.1 Humira: Historical Sales Analysis, 2010-2014

4.5.2 Humira: Sales Forecast 2015-2025

4.5.3 Future Prospects For Biosimilar Versions Of Humira

4.6 Stelara (ustekinumab) – Johnson & Johnson

4.6.1 Stelara: Historical Sales Analysis, 2010-2014

4.6.2 Stelara: Sales Forecast 2015-2025

4.6.3 Intensifying Competition For Stelara

4.7 Enbrel (etanercept) - Amgen/ Pfizer/ Takeda

4.7.1 Enbrel: Co-Promotions And Marketing Rights

4.7.2 Enbrel: Historical Sales Analysis, 2008-2014

4.7.3 Enbrel: Patent Expiries and Potential Competition, 2015-2025

4.7.4 Enbrel: Sales Forecast 2015-2025

4.7.5 Enbrel Auto-injector Pens: A Driver Of Growth In Recent Years

4.7.6 Competition From Other Drugs

4.7.7 Biosimilar Competition For Enbrel

4.8 Remicade (infliximab) – Johnson & Johnson

4. The Psoriasis Drugs Market: Market Analysis And Forecast 2015-

2025

www.visiongain.com

Contents

4.8.1 Remicade: Historical Sales Analysis, 2010-2014

4.8.2 Remicade: Patent Expiries and Potential Competition, 2015-2025

4.8.3 Remicade: Sales Forecast 2015-2025

4.9 Daivobet (betamethasone/calcipotriene) - LEO Pharma

4.9.1 Daivobet: Sales Forecast 2015-2025

4.9.2 LEO Pharma’s Life Cycle Management Of Daivobet

4.9.3 Daivobet/Dovobet/Taclonex – Generic Competition

4.10 Soriatane (acitretin) – GlaxoSmithKline

4.10.1 Soriatane: Sales Forecast 2015-2025

4.11 Other Psoriasis Drugs

4.11.1 Cimzia (certolizumab) - UCB

4.11.2 Cosentyx (secukinumab) – Novartis

4.11.3 Otezla (apremilast) - Celgene

4.11.4 Sorilux (calcipotriene foam) - GSK

4.11.5 Other Psoriasis Drugs: Sales Forecast 2015-2025

4.12 Psoriasis Drugs Market: Summary

5.1 Skin Infection Drugs: Abundant Growth Opportunities

5.1.1 Leading Products In The Skin Infection Drugs Market, 2014

5.2 Skin Infection Drugs: Market Forecast 2015-2025

5.2.1 Skin Infection Drugs: Changing Market Shares By Leading Drugs 2015-2025

5.3 Leading Drugs Used In The Treatment Of Skin Infections

5.4 Cubicin (daptomycin) - Cubist Pharmaceuticals/ Merck & Co

5.4.1 Acquisition By Merck & Co

5.4.2 Generic Competition For Cubicin

5.4.3 Cubicin: Sales Forecast 2015-2025

5. Skin Infection Drugs Market: Market Analysis And Forecast 2015-

2025

www.visiongain.com

Contents

5.4.4 Lifecycle Management Strategies For Cubicin

5.5 Zyvox (linezolid) - Pfizer

5.5.1 Zyvox: Historical Sales Analysis, 2010-2014

5.5.2 Zyvox: Sales Forecast 2015-2025

5.5.3 The Threats To Zyvox Sales From Competing New Drugs

5.6 Valtrex (valaciclovir) - GSK

5.6.1 Valtrex: Historical Sales Analysis, 2010-2014

5.6.2 Valtrex: Sales Forecast 2015-2025

5.7 Canesten (clotrimazole) - Bayer

5.7.1 Canesten: Historical Sales Analysis, 2011-2014

5.7.2 Canesten: Sales Forecast 2015-2025

5.8 Lamisil (terbinafine) - Novartis

5.8.1 Lamisil Patent Expiry

5.8.2 Lamisil Sales Affected By Novartis Manufacturing Problems

5.8.3 Lamisil: Sales Forecast 2015-2025

5.9 Bactroban (mupirocin) - GSK

5.9.1 Bactroban: Historical Sales Analysis, 2010-2013

5.9.2 Bactroban: Sales Forecast 2015-2025

5.10 Other Skin Infection Drugs

5.10.1 Dalvance (dalbavancin) - Durata Therapeutics

5.10.2 Jublia (efinaconazole) - Valeant

5.10.3 Kerydin (tavaborole) - Anacor

5.10.4 Sivextro (tedizolid) – Cubist Pharmaceuticals

5.10.5 Zovirax (acyclovir) - Valeant/GSK

5.10.5.1 Valeant Acquires Zovirax In US And Canada

5.10.5.2 Mylan’s Generic Zovirax And Actavis’ Authorised Generic

5.10.6 Other Skin Infection Drugs: Sales Forecast 2015-2025

5.11 Skin Infection Drugs: Market Summary

www.visiongain.com

Contents

6.1 Acne Drugs: A Diversified Market

6.1.1 Leading Products In The Acne Drugs Market, 2014

6.2 Acne Drugs Market: Recent Trends and Developments

6.2.1 The Rise Of Combination Therapies In Acne Treatment

6.2.2 Oral Contraceptives In Treating Acne

6.2.3 The Threat Of Generic Competition In The Acne Drugs Market

6.3 Acne Drugs: Market Forecast 2015-2025

6.3.1 Acne Drugs: Changing Market Shares By Leading Drugs 2015-2025

6.4 Leading Drugs In The Acne Drugs Market

6.5 Solodyn (minocycline) - Valeant

6.5.1 Solodyn: Sales Forecast 2015-2025

6.5.2 Antitrust Action Over Solodyn Pay-For-Delay Deals

6.5.3 Impax And Medicis Collaborating On Advanced Solodyn

6.5.4 Medicis And Lupin Settle

6.6 Epiduo (adapalene/benzoyl peroxide) – Galderma/ Nestlé Skin Health

6.6.1 Epiduo: Sales Forecast 2015-2025

6.6.2 Galderma Settlement Agreement Over Generic Epiduo

6.6.3 Paediatric Approval For Epiduo

6.7 Claravis (isotretinoin) - Teva

6.7.1 Claravis: Sales Forecast 2015-2025

6.8 Aczone (dapsone) - Allergan

6.8.1 Aczone: Sales Forecast 2015-2025

6.9 Differin (adapalene) – Galderma/ Nestlé Skin Health

6.9.1 Recent Generic Competition To Differin

6.9.2 Differin: Sales Forecast 2015-2025

6.9.3 Federal Circuit Court Invalidates Differin Patents

6.10 Absorica/Epuris (CIP-isotretinoin) – Cipher/ Sun Pharma

6.10.1 Absorica/Epuris: Sales Forecast 2015-2025

6. Acne Drugs Market: Market Analysis And Forecast 2015-2025

www.visiongain.com

Contents

6.11 Ziana (clindamycin/tretinoin) – Valeant Pharmaceuticals International

6.11.1 Valeant’s Patent Settlement With Actavis Over Ziana

6.11.2 Ziana: Sales Forecast 2015-2025

6.12 Doryx (doxycycline) – Actavis/ Mayne Pharma

6.12.1 Lifecycle Management Strategies For Doryx

6.12.2 Divestment Agreement With Mayne Pharma

6.12.3 Generic Competition For Doryx

6.12.4 Doryx: Sales Forecast 2015-2025

6.13 Other Acne Drugs

6.13.1 Acanya (clindamycin/benzoyl peroxide) – Dow / Valeant

6.13.1.1 Acanya: Financial Analysis

6.13.1.2 Actavis Claims First-to-File Exclusivity for its Acanya ANDA

6.13.1.3 Legal Battles Involving Dow/Valeant, Perrigo, And Watson

6.13.2 Amnesteem (isotretinoin) - Mylan

6.13.2.1 Amnesteem: Financial Analysis

6.13.3 Diane (cyproterone/ethinyl estradiol) - Bayer

6.13.4 Duac (clindamycin/benzoyl peroxide) – GlaxoSmithKline

6.13.4.1 Duac: Financial Analysis

6.13.5 Veltin (tretinoin/clindamycin) - GSK

6.13.6 Other Acne Drugs: Sales Forecast 2015-2025

6.14 Acne Drugs: Market Summary

7.1 Dermatitis Drugs: High Generic Penetration

7.1.1 Leading Products In The Dermatitis Drugs Market, 2014

7.2 Dermatitis Drugs: Market Forecast 2015-2025

7.2.1 Dermatitis Drugs: Changing Market Shares By Leading Drugs 2015-2025

7. Dermatitis Drugs Market: Market Analysis And Forecast 2015-

2025

www.visiongain.com

Contents

7.3 Leading Drugs In The Dermatitis Drugs Market

7.4 Bepanthen (dexpanthenol)/ Bepanthol - Bayer

7.4.1 Bepanthen: Sales Forecast 2015-2025

7.5 Protopic (tacrolimus) - Astellas Pharma/ Roche

7.5.1 Protopic Benefits From Expanded Indication

7.5.2 Generic Competition For Protopic

7.5.3 Protopic: Sales Forecast 2015-2025

7.6 Elidel (pimecrolimus) – Meda Pharma/ Valeant

7.6.1 Elidel: Sales Forecast 2015-2025

7.7 Elocon (mometasone) - Merck & Co

7.7.1 Elocon: Sales Forecast 2015-2025

7.8 Other Dermatitis Drugs: Sales Forecast 2015-2025

7.9 Dermatitis Drugs: Market Outlook

8.1 The Dermatological Drugs Market By Region

8.1.1 The Global Distribution Of Dermatological Drugs In 2014

8.2 Leading National Markets: Forecast 2015-2025

8.2.1 Changing Market Shares By Region, 2015-2025

8.3 Regional Dermatological Drugs Markets: Analysis And Forecasts, 2015-2025

8.4 United States: The Largest Dermatological Drugs Market

8.4.1 The Impact Of An Expanding Medicare Coverage

8.4.2 Legislative Environment Stimulating Biosimilars Market?

8.4.3 US Dermatological Drugs Market: Market Forecast 2015-2025

8.5 The EU5 Markets: Growth Expected In Each Country

8.5.1 EU5 Dermatological Drugs Market: Market Forecast 2015-2025

8.5.1.1 EU5 Markets: Changing Market Shares By Country, 2015-2025

8.5.2 Germany

8.5.2.1 German Dermatological Drugs Market: Market Forecast 2015-2025

8. Leading National Markets For Dermatological Drugs, 2015-2025

www.visiongain.com

Contents

8.5.3 France

8.5.3.1 French Dermatological Drugs Market Forecast 2015-2025

8.5.4 UK

8.5.4.1 UK Dermatological Drugs Market Forecast 2015-2025

8.5.5 Italy

8.5.5.1 Italian Dermatological Drugs Market Forecast 2015-2025

8.5.6 Spain

8.5.6.1 Spanish Dermatological Drugs Market Forecast 2015-2025

8.6 Japan

8.6.1 The Cost Of Treatment In Japan

8.6.2 Japanese Pharmaceutical Industry Regulatory Reform

8.6.3 Japanese Dermatological Drugs Market Forecast 2015-2025

8.7 China

8.7.1 Expansion Of Healthcare Coverage And Reimbursement In China

8.7.2 Improving Public Perception Of Dermatology In China

8.7.3 Price Controls And The Anhui Model

8.7.4 Chinese Dermatological Drugs Market Forecast 2015-2025

8.8 India

8.8.1 The Effects Of The Drug Prices Control Order Of 2013

8.8.2 India’s Expansion Of Healthcare Provision

8.8.3 Indian Dermatological Drugs Market Forecast 2015-2025

8.9 Brazil

8.9.1 The Growth In Brazil’s Healthcare Landscape

8.9.2 Clearer Access To Medicines In Brazil

8.9.3 Brazilian Dermatological Drugs Market Forecast 2015-2025

8.10 Russia

8.10.1 Pharma2020 Strategy - Healthcare And Industry Reform

8.10.2 Russian Dermatological Drugs Market Forecast 2015-2025

8.11 Mexico

8.11.1 Seguro Popular: Mexican Healthcare Reform

www.visiongain.com

Contents

8.11.2 Are Multinationals Waking Up To Mexico’s Potential?

8.11.3 Mexican Dermatological Drugs Market Forecast 2015-2025

8.12 Rest of the World

8.12.1 The Rest of the World Dermatological Drugs Market Forecast 2015-2025

9.1 Dermatological Drugs – A Rapidly Consolidating Market

9.2 Galderma (Nestle Skin Health S.A.)

9.2.1 Galderma: Dermatological Drugs Portfolio, 2015

9.2.2 Galderma: Recent Developments

9.2.2.1 Nestlé’s Acquisition Of Galderma

9.2.2.2 Approval Of Soolantra For Rosacea

9.2.2.3 Mirvaso Launched For Rosacea

9.3 Johnson & Johnson

9.3.1 Johnson & Johnson: Dermatological Drugs Portfolio, 2015

9.3.2 Johnson & Johnson Dermatological Drugs Sales Forecast 2015-2025

9.3.3 Johnson And Johnson: Dermatological Drug Development Efforts, 2015

9.4 AbbVie

9.4.1 AbbVie: Dermatological Drugs Portfolio, 2015

9.4.2 AbbVie Dermatological Drugs Sales Forecast 2015-2025

9.4.3 AbbVie: Dermatological Drugs Development Pipeline, 2015

9.4.3.1 BT-061 (tregalizumab) For The Treatment Of Psoriasis

9.5 GlaxoSmithKline (GSK)

9.5.1 GSK: Dermatological Drugs Portfolio, 2015

9.5.2 GlaxoSmithKline (GSK) Dermatological Drugs Sales Forecast 2015-2025

9.5.3 GlaxoSmithKline (GSK): Recent Developments

9.5.3.1 Business Restructuring Arrangements With Novartis

9. Leading Companies In The Dermatological Drugs Market, 2015-

2025

www.visiongain.com

Contents

9.5.3.2 Tafinlar and Mekinist Combination Approved by FDA, Withdrawn in EU

9.5.4 GlaxoSmithKline (GSK): Dermatological Drugs Development Pipeline, 2015

9.6 Pfizer

9.6.1 Pfizer: Dermatological Drugs Portfolio, 2015

9.6.2 Pfizer Dermatological Drugs Sales Forecast 2015-2025

9.6.3 Pfizer: Dermatological Drugs Development Pipeline, 2015

9.7 LEO Pharma

9.7.1 LEO Pharma: Dermatological Drugs Portfolio, 2015

9.7.2 LEO Pharma Dermatological Drugs Sales Forecast 2015-2025

10.1 Innovative Products Currently In Development Will Drive Growth

10.1.1 New Technology In R&D Pipeline Activities

10.1.1.1 Reformulation

10.1.1.2 Combination Treatments

10.1.1.3 New Mechanisms And Drug Delivery Technologies

10.1.1.4 Potential Market Entrants

10.2 Psoriasis Drugs Development Pipeline, 2015

10.2.1 Psoriasis Drugs In Phase 3 Development

10.2.1.1 000-0551 Lotion (halobetasol) - Therapeutics, Inc

10.2.1.2 AMG 827 (brodalumab) - AstraZeneca/ Amgen

10.2.1.3 CF101 (IB-MECA) - Can-Fite BioPharma

10.2.1.4 CNTO 1959 (guselkumab) - MorphoSys/ Janssen

10.2.1.5 LAS41008 (dimethyl fumarate) - Almirall

10.2.1.6 LEO 90100 - LEO Pharma

10.2.1.7 LY2439821 (ixekizumab) - Eli Lilly

10.2.1.8 MK-3222/SCH 900222 (tildrakizumab) - Merck

10. Dermatological Drugs: Research And Development Pipeline,

2015-2025

www.visiongain.com

Contents

10.2.1.9 STF 115469 (calcipotriene foam) - GSK

10.2.1.10 Xeljanz (tofacitinib) - Pfizer

10.2.2 Psoriasis Drugs In Phase 2 Development

10.2.2.1 AN2728 (PDE-4 inhibitor) - Anacor Pharmaceuticals

10.2.2.2 CT327 (TrkA inhibitor) - Creabilis Therapeutics

10.2.2.3 ASP015K (JAK inhibitor) – Astellas Pharma

10.2.2.4 Jakavi/Jakafi (ruxolitinib) - Incyte/ Novartis

10.2.2.5 LY3009104 (baricitinib) - Incyte/ Eli Lilly

10.2.2.6 PH-10 (Rose Bengal) - Provectus Biopharmaceuticals

10.2.3 Psoriasis Drugs In Phase 1 And Pre-clinical Development

10.3 Skin Infection Drugs Development Pipeline, 2015

10.3.1 Drugs In Phase 3 Development For Skin Infections

10.3.1.1 Delafloxacin (delafloxacin) - Melinta Pharmaceuticals

10.3.1.2 NB-001 - NanoBio Corporation

10.3.1.3 Orbactiv/ Nuvocid (oritavancin) - The Medicines Company

10.3.1.4 Luliconazole - Topica Pharmaceuticals

10.3.2 Drugs In Phase 2 Development For Skin Infections

10.3.3 Drugs In Phase 1 And Preclinical Pipeline For Skin Infections

10.4 Acne Drugs Development Pipeline, 2015

10.4.1 Drugs In Phase 3 Development For Acne

10.4.1.1 Duac low dose (clindamycin/ benzoyl peroxide) - GlaxoSmithKline

10.4.1.2 Visonac (photodynamic therapy) - Photocure

10.4.2 Drugs In Phase 2 Development For Acne

10.4.3 Drugs In Phase 1 And Pre-clinical Development For Acne

10.4.4 A Possible Vaccine For Acne

10.5 Dermatitis Drugs Development Pipeline, 2015

10.5.1 Drugs In Phase 3 Development For Dermatitis

10.5.1.1 Toctino (alitretinoin) - GSK

10.5.1.2 Dermadexin and Pruridexin (P3CGM) – Cipher Pharmaceuticals

10.5.1.3 Dexeryl Cream (glycerol/paraffin emollient) - Pierre Fabre

www.visiongain.com

Contents

10.5.1.4 REGN668/SAR231893 (dupilumab) - Regeneron/ Sanofi

10.5.1.5 Soriatane (acitretin) - InnovaDerm/Tribute Pharmaceuticals

10.5.2 Drugs In Phase 2 Development For Dermatitis

10.5.3 Drugs In Phase 1 And Preclinical Stages Of Development For Dermatitis

10.6 Other Dermatological Drugs Development Pipeline, 2015

10.6.1 Other Dermatological Drugs: Filed or Recently Launched

10.6.1.1 Actikerall (fluorouracil/salicylic acid) - Almirall

10.6.1.2 Ameluz (5-ALA photodynamic therapy) - Biofrontera

10.6.1.3 Keytruda (MK-3475, Pembrolizumab) - Merck

10.6.1.4 Mirvaso (brimonidine) - Galderma

10.6.1.5 Picato (ingenol mebutate) - LEO Pharma

10.6.1.6 Xolair (omalizumab) - Novartis/ Roche

10.6.2 Other Dermatological Drugs: Phase 3 Pipeline Products, 2015

10.6.2.1 Atralin (tretinoin) - Valeant

10.6.2.2 BMS-936558 (nivolumab) - Bristol-Myers Squibb

10.6.2.3 CD5024 (ivermectin) - Galderma

10.6.2.4 Latisse (bimatoprost) – Allergan (Actavis)

10.6.2.5 LEE011, LGX818, and MEK162 - Novartis

10.6.2.6 Oleogel-S10 (triterpene extract) – Birken AG

10.6.2.7 PV-10 (Rose Bengal) - Provectus Pharmaceuticals

10.6.2.8 SR-T100 gel (Solanum incanum extract) - G&E Herbal Biotechnology

10.6.2.9 TVEC (talimogene laherparepvec) - Amgen

10.6.3 Other Dermatological Drugs: Phase 2 Pipeline Products, 2015

10.6.4 Other Dermatological Drugs: Phase 1 and Preclinical Pipeline

11.1 Market Factors Influencing Dermatological Drugs

11. Qualitative Analysis Of The Dermatological Drugs Market, 2015-

2025

www.visiongain.com

Contents

11.2 SWOT Analysis Of The Global Dermatological Drugs Market, 2015-2025

11.2.1 Strengths

11.2.1.1 The High Unmet Clinical Need In Dermatology

11.2.1.2 A Healthy Pipeline Of Development-Stage Products

11.2.1.3 Strong Industry-Physician Relationships

11.2.2 Weaknesses

11.2.2.1 Limited Efficacy And Adverse Effects May Impact Product Uptake

11.2.2.2 Patient Adherence – A Major Challenge To Treatment Design

11.2.2.3 Impending Patent Expiries And The Challenges Posed By Generic

Competition

11.2.3 Opportunities

11.2.3.1 The High-Growth Sectors In Dermatology

11.2.3.2 Personalised Dermatology: Technological Advances In Genomics

11.2.3.3 Advances In Topical Drug Delivery Methods Offers Product Differentiation

11.2.3.4 Consolidation Within Dermatology – Opportunity For Synergistic Growth?

11.2.4 Threats

11.2.4.1 Uncertain Surrounding Reimbursement And Payment Approvals

11.2.4.2 The Rising Cost Of Research And Development

11.2.4.3 Downward Pressures On Drug Prices

11.3 Porter’s Five Force Analysis Of The Global Dermatological Drugs Market, 2015-2025

11.3.1 Threat Of New Entrants

11.3.2 Threat Of Substitutes

11.3.3 Rivalry Among Competitors

11.3.4 Power Of Buyers

11.3.5 Power Of Suppliers

12.1 Interview With Kathleen Deardorff, Chief Operating Officer At Photocure ASA

12.1.1 Visonac As An Innovative First-In-Class Treatment

12. Expert Opinions from Our Primary Research

www.visiongain.com

Contents

12.1.2 Photocure’s Development Plans For Visonac

12.1.3 Commercialisation Strategy For Visonac

12.1.4 On The Geographical Reach Of Acne Treatments

12.1.5 The Key Unmet Needs Within Patient Populations For Acne

12.1.6 The Key Forces Driving And Restraining The Development Of Acne Therapies

12.1.7 On The Current Development Pipeline For Acne Therapies

12.1.8 On Photocure’s Plans For Future Growth

12.1.9 Future Prospects For The Acne Treatments Market

13.1 Overview Of Current Market Conditions And Market Forecast, 2014-2025

13.2 Leading Sectors In Dermatological Drugs In 2014

13.3 Leading Regions In The Dermatological Drugs Market In 2014

13.4 Future Outlook For The Various Sectors Within The Dermatological Drugs Market, 2015-2025

13.5 What Does The Future Hold For Dermatological Drugs?

13. Conclusions

Page 101

www.visiongain.com

Dermatological Drugs Market Forecast 2015-2025: Opportunities for Leading Companies

psoriasis. In April 2014 it was reported that Perrigo had begun the launch of authorised generic

Taclonex.

4.10 Soriatane (acitretin) – GlaxoSmithKline Soriatane is a small molecule systemic therapy indicated for the treatment of severe psoriasis in

adults. It is an oral retinoid that inhibits excessive cell growth and skin cell thickening that is seen in

psoriasis. It reduces plaque formation and scaling. It was launched in 1996 by Stiefel Laboratories

(now part of GSK). Patent protection has since expired for Soriatane, leaving it vulnerable to

generic competition.

Soriatane causes a wide range of side effects. These include dryness and cracking of the lips,

dryness of the nasal passages and loss of hair as well as more serious side effects such as

hepatitis and pancreatitis. The serious nature of these side effects restricts revenue generation;

Soriatane is only prescribed after treatment with another therapy has failed and is only given to

those patients suffering from severe psoriasis.

4.10.1 Soriatane: Sales Forecast 2015-2025 GSK reported that soriatane sales in 2014 were particularly affected by the generic competition in

the US which is said to have affected the company’s dermatology products cumulatively.

Dermatology product sales for the company were reported to have decreased by 56% in 2014

compared to 2013. Although GSK has not publicly published individual sales for Soriatane,

visiongain have estimated sales for the product at $86m in 2014 (Table 4.13).

We forecast sales for Soriatane to continue its decline over the forecast period. The patents

granting the drug exclusivity in the major markets have expired for a number of years. This has

allowed generic versions to erode away large portions of the drugs sales since the first US generic

version was launched in April 2013. GSK reported in Q1 of 2015 that the sales erosion being

witnessed for Soriatane was a major contributing factor to the 56% decline that the company

experienced in the dermatological arm of its business.

Table 4.13 and Figure 4.15 show visiongain’s revenue forecast for Soriatane used in psoriasis and

psoriatic arthritis between 2015 and 2025.

Page 144

www.visiongain.com

Dermatological Drugs Market Forecast 2015-2025: Opportunities for Leading Companies

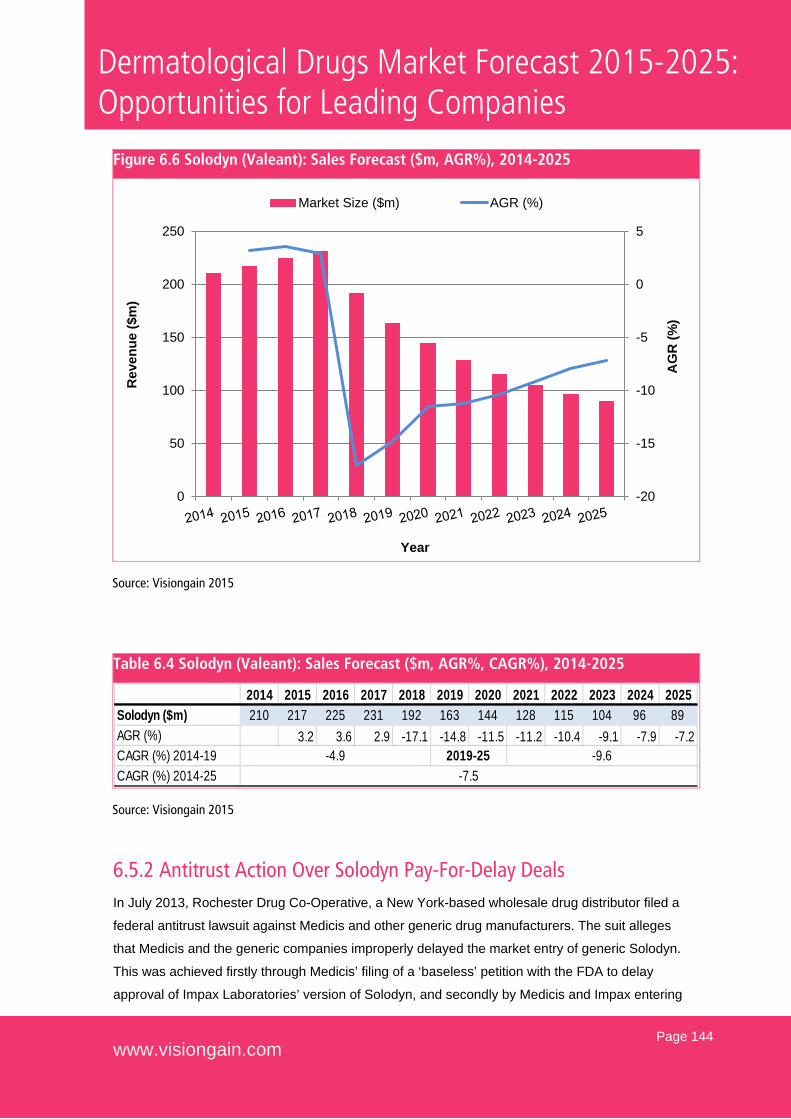

Figure 6.6 Solodyn (Valeant): Sales Forecast ($m, AGR%), 2014-2025

Table 6.4 Solodyn (Valeant): Sales Forecast ($m, AGR%, CAGR%), 2014-2025

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025Solodyn ($m) 210 217 225 231 192 163 144 128 115 104 96 89AGR (%) 3.2 3.6 2.9 -17.1 -14.8 -11.5 -11.2 -10.4 -9.1 -7.9 -7.2CAGR (%) 2014-19CAGR (%) 2014-25

-4.9 2019-25 -9.6-7.5

6.5.2 Antitrust Action Over Solodyn Pay-For-Delay Deals In July 2013, Rochester Drug Co-Operative, a New York-based wholesale drug distributor filed a

federal antitrust lawsuit against Medicis and other generic drug manufacturers. The suit alleges

that Medicis and the generic companies improperly delayed the market entry of generic Solodyn.

This was achieved firstly through Medicis’ filing of a ‘baseless’ petition with the FDA to delay

approval of Impax Laboratories’ version of Solodyn, and secondly by Medicis and Impax entering

-20

-15

-10

-5

0

5

0

50

100

150

200

250

AG

R (%

)

Rev

enue

($m

)

Year

Market Size ($m) AGR (%)

Source: Visiongain 2015

Source: Visiongain 2015

Page 202

www.visiongain.com

Dermatological Drugs Market Forecast 2015-2025: Opportunities for Leading Companies

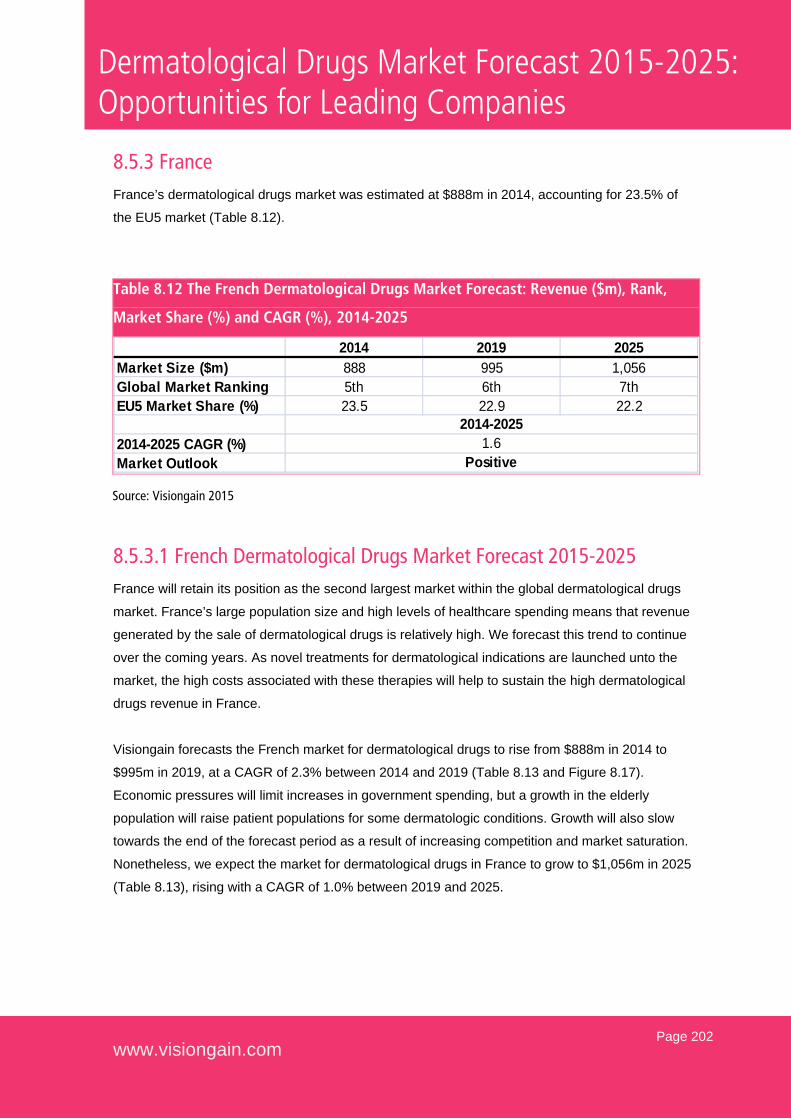

8.5.3 France France’s dermatological drugs market was estimated at $888m in 2014, accounting for 23.5% of

the EU5 market (Table 8.12).

Table 8.12 The French Dermatological Drugs Market Forecast: Revenue ($m), Rank,

Market Share (%) and CAGR (%), 2014-2025

2014 2019 2025Market Size ($m) 888 995 1,056Global Market Ranking 5th 6th 7thEU5 Market Share (%) 23.5 22.9 22.2

2014-2025 CAGR (%)Market Outlook

2014-20251.6

Positive

8.5.3.1 French Dermatological Drugs Market Forecast 2015-2025 France will retain its position as the second largest market within the global dermatological drugs

market. France’s large population size and high levels of healthcare spending means that revenue

generated by the sale of dermatological drugs is relatively high. We forecast this trend to continue

over the coming years. As novel treatments for dermatological indications are launched unto the

market, the high costs associated with these therapies will help to sustain the high dermatological

drugs revenue in France.

Visiongain forecasts the French market for dermatological drugs to rise from $888m in 2014 to

$995m in 2019, at a CAGR of 2.3% between 2014 and 2019 (Table 8.13 and Figure 8.17).

Economic pressures will limit increases in government spending, but a growth in the elderly

population will raise patient populations for some dermatologic conditions. Growth will also slow

towards the end of the forecast period as a result of increasing competition and market saturation.

Nonetheless, we expect the market for dermatological drugs in France to grow to $1,056m in 2025

(Table 8.13), rising with a CAGR of 1.0% between 2019 and 2025.

Source: Visiongain 2015

Page 241

www.visiongain.com

Dermatological Drugs Market Forecast 2015-2025: Opportunities for Leading Companies

In Europe, GSK has withdrawn its marketing application for combined Mekinist/Tafinlar after

regulators requested additional information. The company was reported to be looking to re-submit

its filing once it has additional results from its Phase 3 trial. However, in July 2014, GSK reported

that a Phase 3 study of its Tafinlar and Mekinist combination compared to vemurafenib in patients

with BRAF V600E or V600K mutation-positive unresectable or metastatic cutaneous melanoma

may be stopped early.

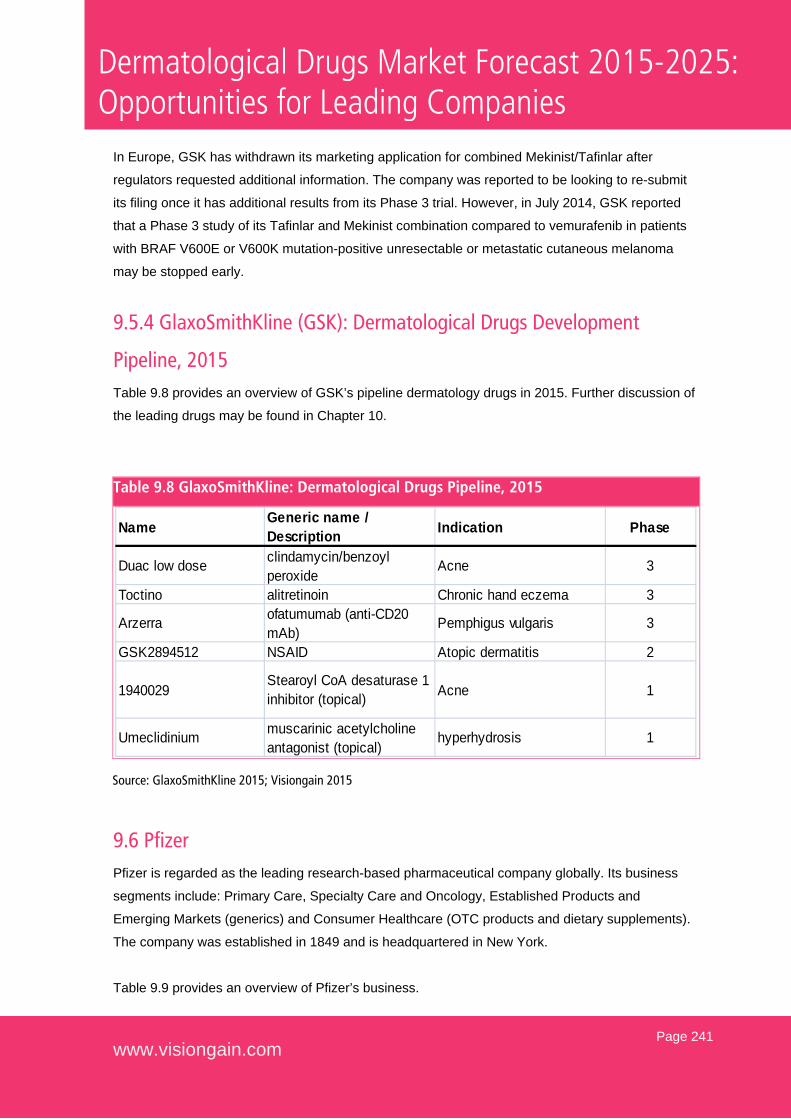

9.5.4 GlaxoSmithKline (GSK): Dermatological Drugs Development

Pipeline, 2015 Table 9.8 provides an overview of GSK’s pipeline dermatology drugs in 2015. Further discussion of

the leading drugs may be found in Chapter 10.

Table 9.8 GlaxoSmithKline: Dermatological Drugs Pipeline, 2015

Name Generic name / Description Indication Phase

Duac low dose clindamycin/benzoyl peroxide

Acne 3

Toctino alitretinoin Chronic hand eczema 3

Arzerra ofatumumab (anti-CD20 mAb)

Pemphigus vulgaris 3

GSK2894512 NSAID Atopic dermatitis 2

1940029Stearoyl CoA desaturase 1 inhibitor (topical) Acne 1

Umeclidinium muscarinic acetylcholine antagonist (topical)

hyperhydrosis 1

9.6 Pfizer Pfizer is regarded as the leading research-based pharmaceutical company globally. Its business

segments include: Primary Care, Specialty Care and Oncology, Established Products and

Emerging Markets (generics) and Consumer Healthcare (OTC products and dietary supplements).

The company was established in 1849 and is headquartered in New York.

Table 9.9 provides an overview of Pfizer’s business.

Source: GlaxoSmithKline 2015; Visiongain 2015

Page 272

www.visiongain.com

Dermatological Drugs Market Forecast 2015-2025: Opportunities for Leading Companies

evaluated in patients with Grade I-II actinic keratoses. The study is predicted to be completed in

August 2015.

10.6.1.2 Ameluz (5-ALA photodynamic therapy) - Biofrontera Ameluz (BF-200 ALA; 5-aminolevulinic acid photodynamic therapy) is a treatment for AKs which

gained approval in the EU in December 2011 and launched first in Germany in August 2012. The

treatment remains in clinical trials in the US after the FDA requested further studies to support

approval. It was reported recently that the company was to submit approval dossier for Ameluz in

the US in March 2015. US FDA approval is expected in around 2015. Four studies were

registered for Ameluz under the NIH’s clinical trial database in May 2015 when visiongain

enquired:

• A trial to compare Ameluz with Metvix (methyl aminolevulinate photodynamic therapy) in

basal cell carcinoma

• A trial of Ameluz treatment in entire fields of the skin surface and using Biofrontera’s own

PDT lamp BF-RhodoLED

• A trial testing the sensitising (allergic) potential of Ameluz, requested by the FDA

• A maximal-use pharmacokinetics study in which an entire tube of Ameluz is applied to

maximally damaged skin to observe its absorption and elimination

10.6.1.3 Keytruda (MK-3475, Pembrolizumab) - Merck Keytruda (Pembrolizumab) is a human PD-1-blocking antibody indicated for the treatment of

patients with unresectable or metastatic melanoma and disease progression following ipilimumab

or a BRAF inhibitor (if BRAF V600 mutation positive).

Keytruda’s efficacy was investigated in a multicentre, open-label, randomized, dose-comparative,

activity-estimating trial, where eligibility criteria were unresectable or metastatic melanoma with

progression of disease. Patients taking part in the trial were randomised to receive 2mg/kg

or10mg/kg of Keytruda every 3 weeks until unacceptable toxicity or disease progression. The

tumour status in these patients was assessed every 12 weeks. The results of the trial indicated an

overall response rate (ORR) of 24% in the 2mg/kg arm, consisting of 1 complete response and 20

partial responses.

The FDA evaluated Pembrolizumab in advanced melanoma under its Breakthrough Therapy

program and granted accelerated approval based upon this clinical trial results showing an overall

response rate of 24%. Multiple clinical trials are currently under way exploring pembrolizumab