delivering value - arpico insurance · delivering value through innovative growth having entered a...

TRANSCRIPT

Delivering value through innovative growth

Having entered a phase of innovative growth, Arpico Insurance

continues to provide every Sri Lankan the opportunity of life-long

protection against life’s risks and financial uncertainties. We are

deeply invested in delivering value that promulgates trust and

confidence in insurance carved into hearts and minds to last a

lifetime. We aim to achieve this vision through innovation that

commends and complements the true needs of Sri Lankans

across all walks of life. As a relatively new player in the industry

with a longstanding affiliation to one of Sri Lanka’s pioneering

conglomerates, we stand resilient in our innovations while taking

concentrated steps to focus only on quality of service and product

diversification that deliver value through innovative growth.

FINANCIAL INFORMATION

42 Annual Report of the Board of Directors on the Affairs of the Company

45 Director ’s Responsibility for Financial Reporting

46 Actuary’s Report

47 Independent Auditor ’s Report

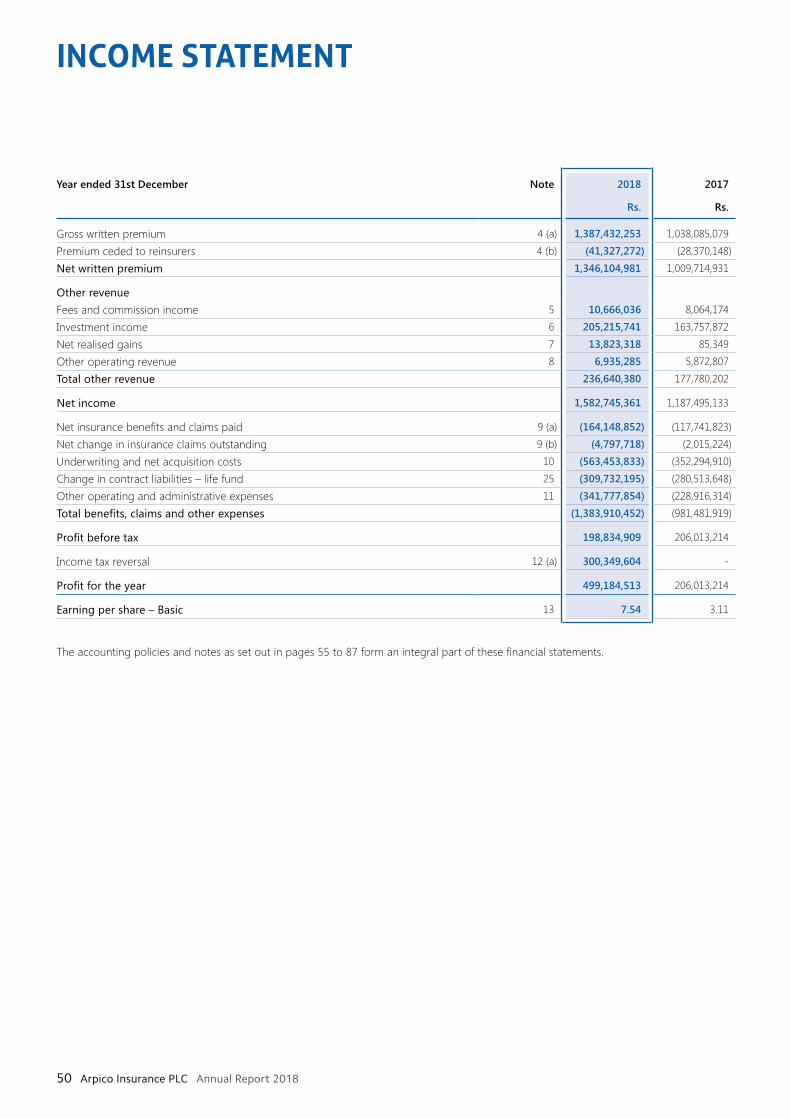

50 Income Statement

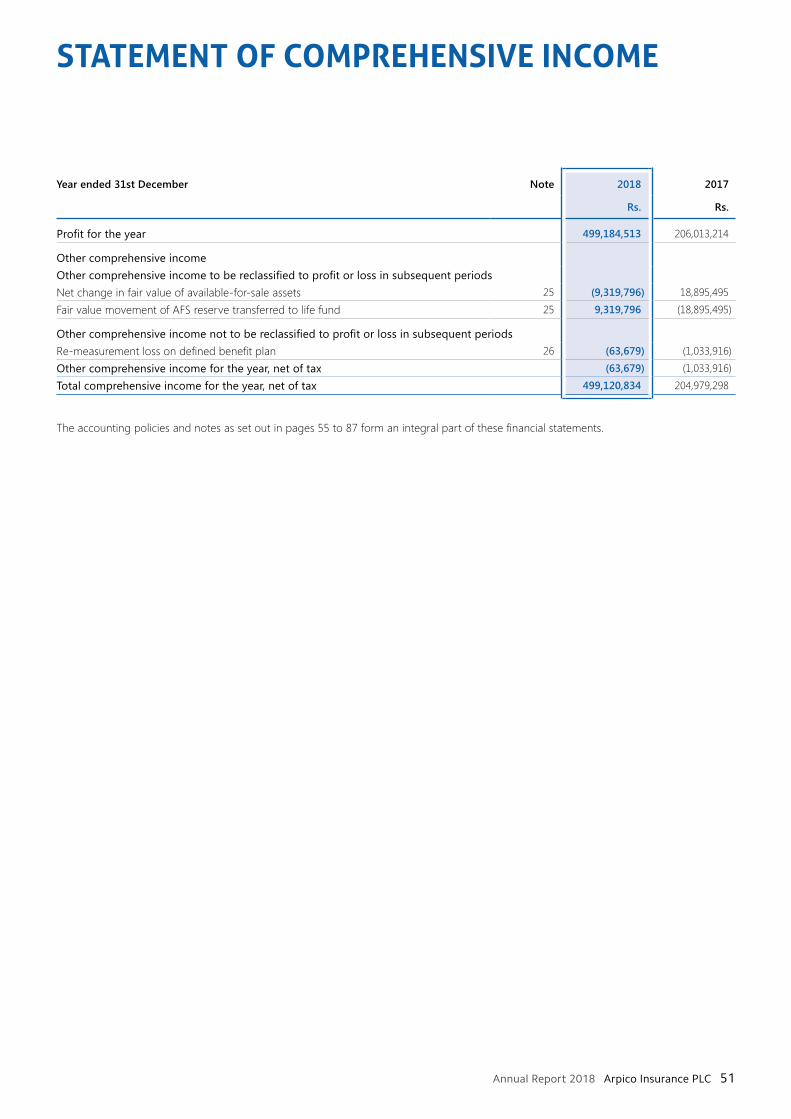

51 Statement of Comprehensive Income

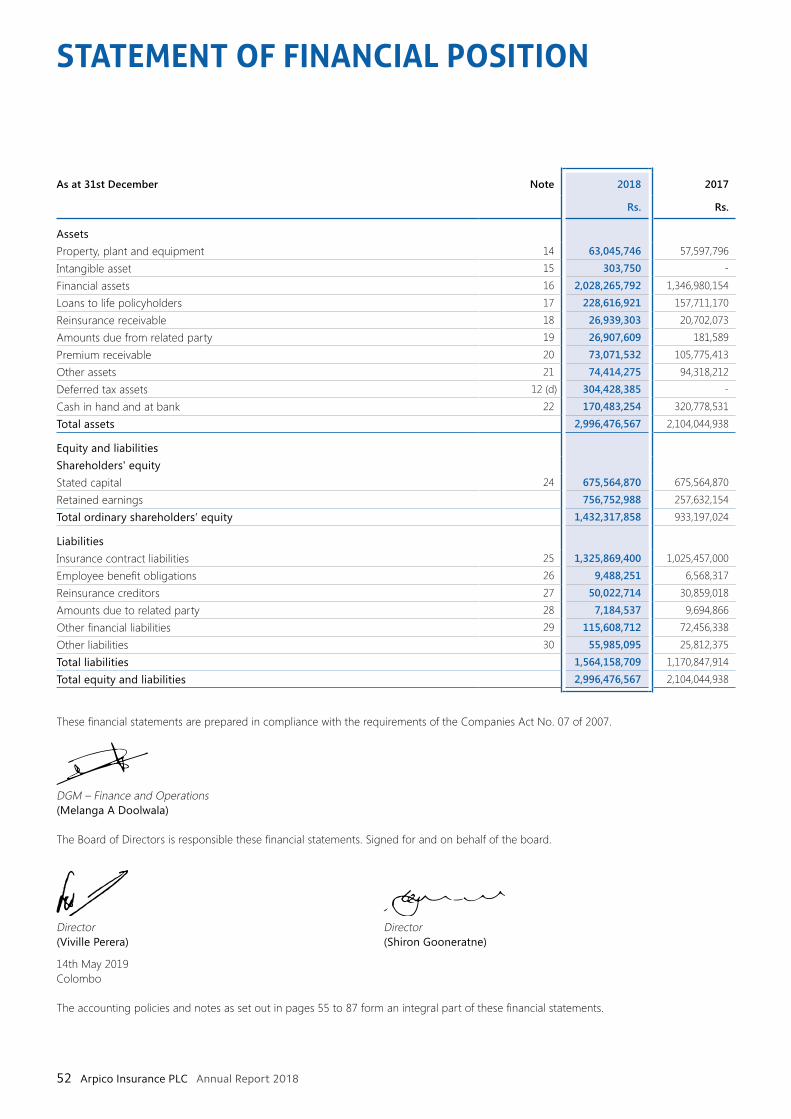

52 Statement of Financial Position

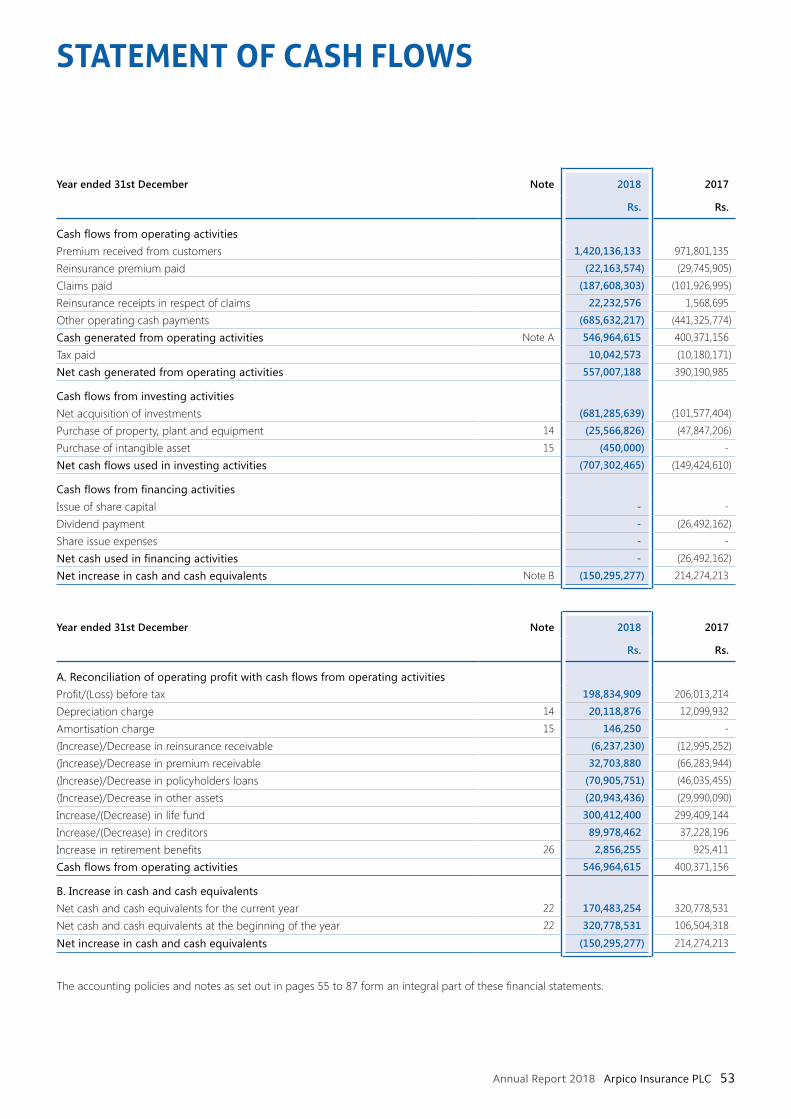

53 Statement of Cash Flows

54 Statement of Changes in Equity

55 Notes to the Financial Statement

90 Shareholder Information

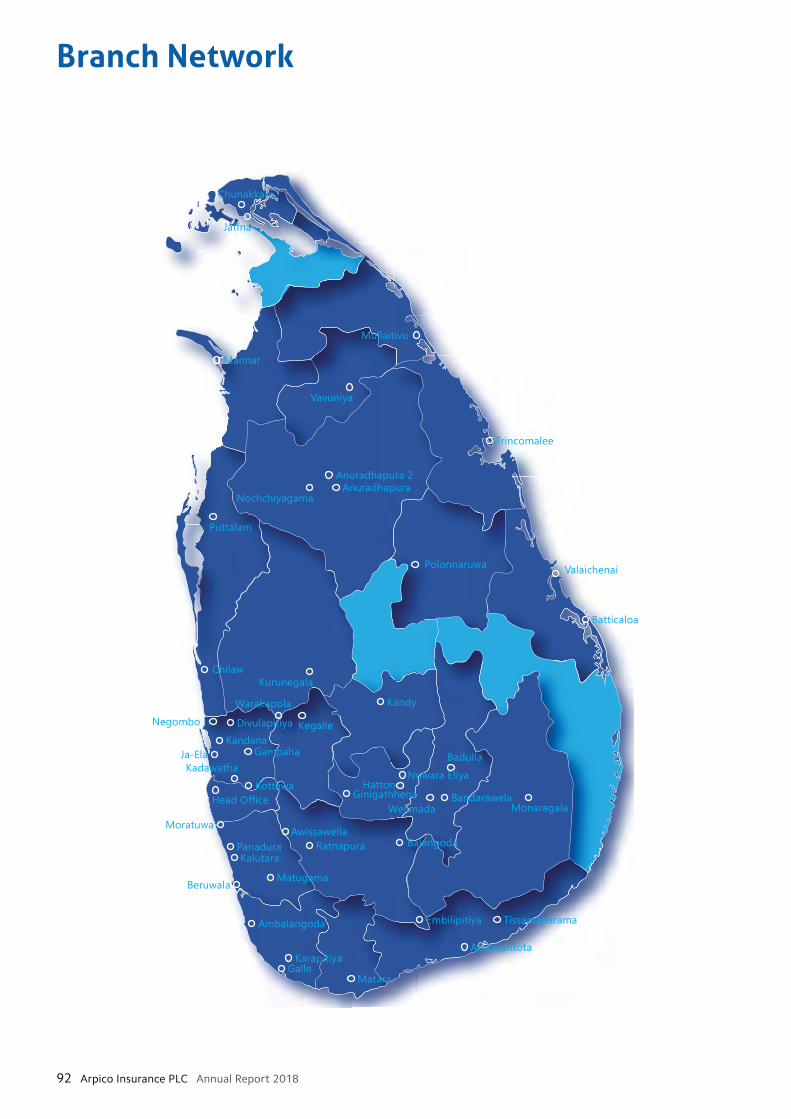

92 Branch Network

93 Glossary of Insurance Terms

95 Notice of Meeting

96 Notes

Form of Proxy – Enclosed

Corporate Information – Inner Back Cover

MANAGEMENT INFORMATION

Vision, Mission and Values of the Company 03

Highlights of the Year 04

Key Milestones 06

Acting Chairman’s Message 08

Board of Directors 10

Corporate Management Team 13

MANAGEMENT DISCUSSION & ANALYSIS

Operating Environment 18

Financial Review 26

GOVERNANCE

Corporate Governance 30

Audit Committee Report 33

Remuneration Committee Report 35

Related Party Transactions Review Committee Report 36

Risk Management 37

Contents

Vision, Mission and Values of the Company

VisionTo be the most trusted and innovative solutions provider for life insurance needs.

MissionProvide unparalleled services to clients through team spirit nourished by passion and developing innovative life insurance solutions, technical expertise, value additions and unique service capability.

Values of the CompanyTo serve customers with care, compassion and respect.

To do the right thing for the right reason.

Always think to lead in new ways and introduce result oriented solutions to customers.

Always nurture and value team spirit along with satisfaction.

Ensure maintenance of high ethical standard in all professional aspects and practices of the Company.

4 Arpico Insurance PLC Annual Report 2018

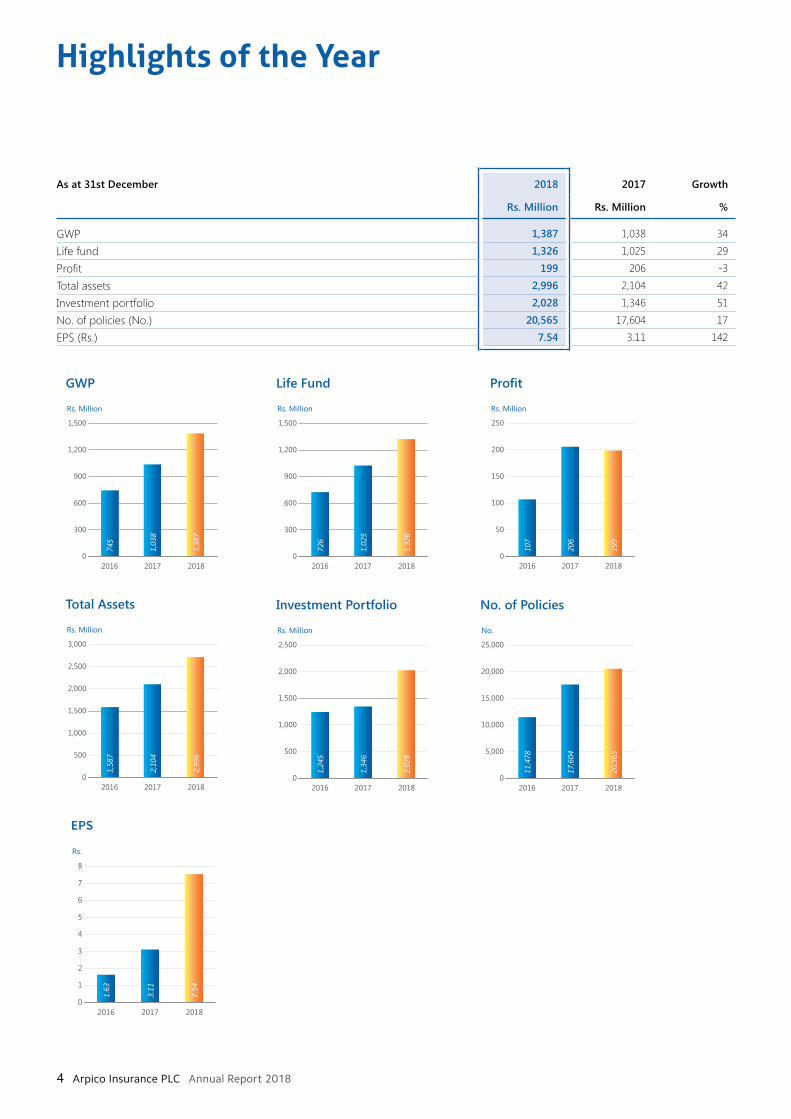

Highlights of the Year

As at 31st December 2018 2017 Growth

Rs. Million Rs. Million %

GWP 1,387 1,038 34

Life fund 1,326 1,025 29

Profit 199 206 -3

Total assets 2,996 2,104 42

Investment portfolio 2,028 1,346 51

No. of policies (No.) 20,565 17,604 17

EPS (Rs.) 7.54 3.11 142

2016 2017 2018

GWP

Rs. Million

0

300

600

900

1,200

1,500

745

1,03

8

1,38

7

2016 2017 2018

Life Fund

Rs. Million

0

300

600

900

1,200

1,500

726

1,02

5

1,32

6

2016 2017 2018

Profit

Rs. Million

0

50

100

150

200

250

107

206

199

2016 2017 2018

Total Assets

Rs. Million

0

500

1,000

1,500

2,000

2,500

3,000

1,58

7

2,10

4

2,99

6

2016 2017 2018

Investment Portfolio

Rs. Million

0

500

1,000

1,500

2,000

2,500

1,24

5

1,34

6

2,02

8

2016 2017 2018

No. of Policies

No.

0

5,000

10,000

15,000

20,000

25,000

11,4

78

17,6

04

20,5

65

EPS

Rs.

0

1

2

3

4

5

6

7

8

1.63

3.11

7.54

2016 2017 2018

Annual Report 2018 Arpico Insurance PLC 5

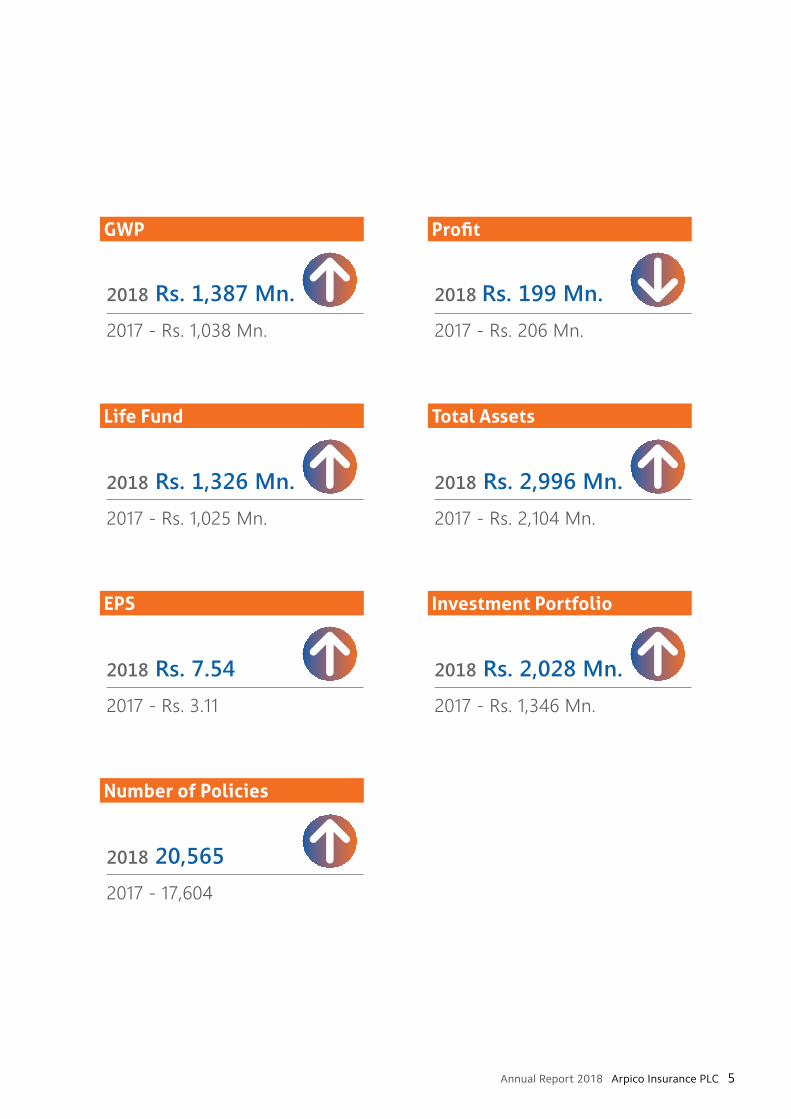

GWP

2018 Rs. 1,387 Mn.2017 - Rs. 1,038 Mn.

Life Fund

2018 Rs. 1,326 Mn.2017 - Rs. 1,025 Mn.

Number of Policies

2018 20,5652017 - 17,604

EPS

2018 Rs. 7.542017 - Rs. 3.11

Total Assets

2018 Rs. 2,996 Mn.2017 - Rs. 2,104 Mn.

Investment Portfolio

2018 Rs. 2,028 Mn.2017 - Rs. 1,346 Mn.

Profit

2018 Rs. 199 Mn.2017 - Rs. 206 Mn.

6 Arpico Insurance PLC Annual Report 2018

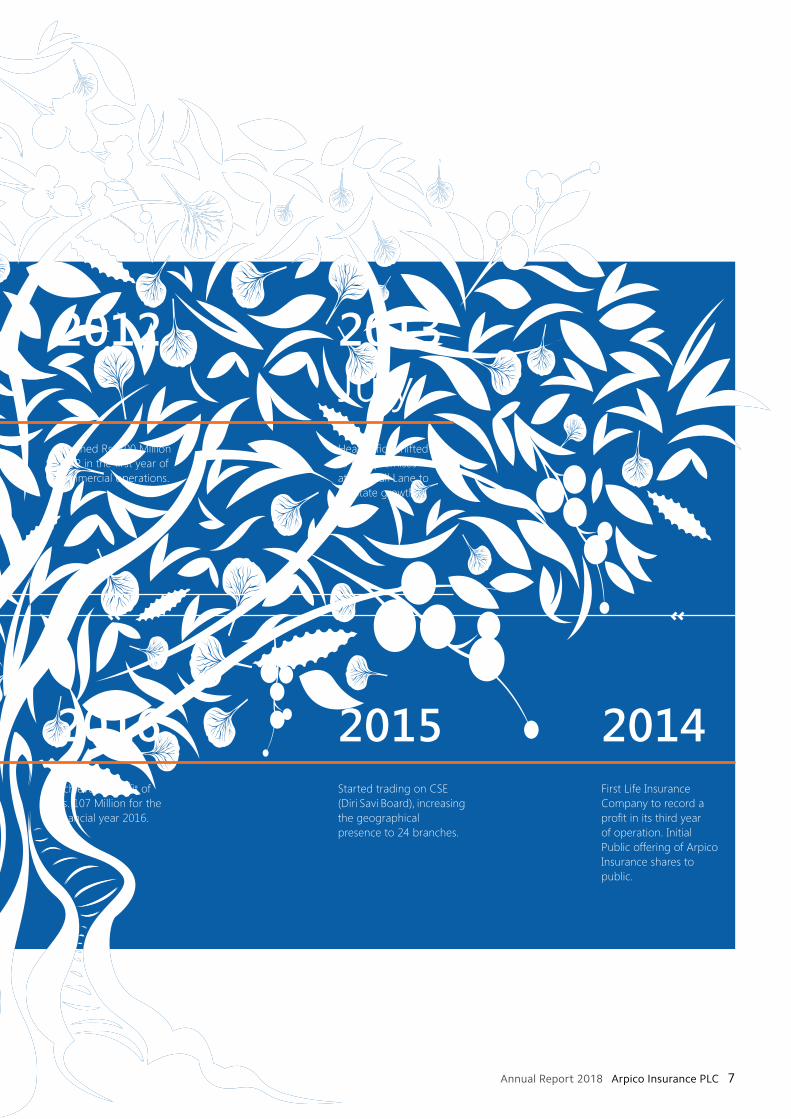

Key Milestones

Incorporated as Public Limited Company under the name “Arpico Insurance Limited”.

Awarded as the fastest growing Life Insurance Company Sri Lanka 2017 at the Global Banking and Finance Review in 2017.

Awarded on the fastest growing life insurance company in Sri Lanka for the second consecutive year in 2018 from Global Banking Finance Review and awarded on the most successful life insurance company in Sri Lanka 2018 by Global Brand Magazine.

IRCSL granted the license to Arpico Insurance to act as a Life Insurer primarily conducting Life Insurance business in Sri Lanka.

Launching of Arpico Insurance and commencement of its Operations at the Hyde Park Corner Office.

2011June

20172018

2011October

2012January

Annual Report 2018 Arpico Insurance PLC 7

Achieved a profit of Rs. 107 Million for the financial year 2016.

Reached Rs. 100 Million GWP in the first year of commercial operations.

Head office shifted to new premises at Vauxhall Lane to facilitate growth.

Started trading on CSE (Diri Savi Board), increasing the geographical presence to 24 branches.

First Life Insurance Company to record a profit in its third year of operation. Initial Public offering of Arpico Insurance shares to public.

2016

2012 2013July

2015 2014

8 Arpico Insurance PLC Annual Report 2018

Acting Chairman’s Message

In 2018, Arpico Insurance as one of the fastest growing life insurance companies in the country, maintained a robust momentum gained in 2017. In spite of the industry challenges. The company recorded an increase in profitability and steady performance which augurs well for the years to come. Backed by our parent Group, Richard Pieris & Company PLC and the strength that comes from being part of the legacy, we are well on our way to create value for all our stakeholders. As such, I am pleased to present the highlights of the year ’s performance and discuss our overall vision for the future.

Within short 7 years, we’ve grown by leaps and bounds yet with a steadiness that bodes well for the future. Our vision for the future incorporate viable growth strategies, calculated to create value for all stakeholders. We plan to expand our presence across the island to provide our services to a wider audience.

GLOBAL AND SRI LANKAN ECONOMIC BACKDROPIn the global context, economic activity picked up pace in 2017. However, the recovery remains incomplete with growth in individual countries continuing to be weak. In most advanced countries, inflation is below target. Short term risks remain broadly balanced; however medium risks require further intervention. The cyclical pickup in activity provides an opportunity to manage policy challenges in order to improve potential of output and ensure that benefits are shared.

Annual Report 2018 Arpico Insurance PLC 9

CUSTOMERSThe rapidly evolving nature of the insurance requirements, call on us to adopt a perceptive, customer-centric approach. Hence, we consistently analyse market trends to gain insights into the nature of our customers’ needs in order to fulfill those needs. While we ensure customer service excellence at all times, our capacity to do so has always been enhanced by our connection with Richard Pieris & Company PLC, a name that is trusted across the island.

CORPORATE GOVERNANCE In our efforts to create value for all our stakeholders, Corporate Governance plays a key role. Our Corporate Governance framework has been designed to ensure transparency and integrity of purpose at all levels of the Company. The Corporate Governance structure that we’ve adopted serves well to ensure smooth functioning of the Company. The Company’s code of conduct applies to all senior and junior members of the Company equally, a fact which assists us maintain a robust corporate culture. The Board of Directors of Arpico Insurance steers the Corporate Governance process in order to engage all stakeholders of the Company to pursue sustainable growth. Our Corporate Governance framework is the key that holds the Board’s accountability to all stakeholders.

FUTURE OUTLOOK Within short 7 years, we’ve grown by leaps and bounds yet with a steadiness that bodes well for the future. Our vision for the future incorporate viable growth strategies, calculated to create value for all stakeholders. We plan to expand our presence across the island to provide our services to a wider audience.

ACKNOWLEDGMENT Our journey of growth has been one of great resilience, vision and integrity. We would not have been able to achieve the success we’ve experienced during the past 7 years, if it was not for the inspirational leadership of our Group Chairman Dr. Sena Yaddehige. I would like to offer him my sincere gratitude for his able assistance and visionary guidance. Our employees have always showed great professionalism and dedication, without which, Arpico Insurance would not be able to pursue growth. I would like to offer all our employees my appreciation and gratitude for their hard work and commitment. I am also grateful to the Board of Directors for their perceptive steering of the Company. I would also like to thank our shareholders for being with us as we collectively seek progress.

Mr. Viville PereraActing Chairman

14th May 2019

Sri Lanka’s GDP growth slowed down to a 3.1 percent in 2017 from 4.4 percent recorded in 2016. Agricultural activities narrowed by 0.8 percent largely due to adverse weather conditions. Manufacturing, construction as well as mining and quarrying activities contributed to the 3.9 percent growth in industry related activities. In 2017, construction related activities which supported economic growth in the post-conflict period, slowed down. Services sector grew by 3.2 percent during the year under review as a result of growth in the financial service activities, wholesale and retail trade, and other personal service activities. The industry sector accounts for 26.8 percent of the overall value of real GDP while the Services sector contributes to 56.8 percent of the overall value of real GDP.

SECTOR REVIEWAccording to the review by the Central Bank of Sri Lanka, the assets base of the insurance expanded in 2017, while earnings declined. The life insurance industry achieved a growth of 12.2 percent of overall Gross Written Premium (GWP) in the year under review, in comparison to the previous year. Arpico Insurance posted a policy growth of 17 percent during the year under review. The growth opportunities in the retirement planning product sector promises to infuse momentum to industry growth in the near future.

COMPANY GROWTH AND STRATEGIC REALIGNMENT In 2018, Arpico Insurance recorded a 34 percent growth posting a GWP of Rs. 1,387 Million. This year we saw a regression in the profitability of -3 percent compared to last year recording a profit before tax of Rs. 199 Million. This was mainly due to deliberate investments company took on developing its sales force. Fuelled by the insightful strategic framework we’ve adopted, the Company succeeded in increasing profitability within the year to be awarded as the most successful Company in Sri Lanka by Global Brand Magazine. The Global Banking and Financial Review ranked Arpico Insurance as the fastest growing Life Insurance Company in Sri Lanka for the second consecutive year in 2018 for the Company’s performance in 2017. Our growth strategy is based on current market research and predictions. As such, in addition to strengthening our workforce with timely encouragement and training, we’ve begun to reinforce our digital capability. We will also continue to leverage on the brand strength of Richard Pieris & Company PLC as we pursue sustainable growth.

EMPLOYEES Employees are the linchpin to our sustainable growth. Their success and growth naturally fuels the Company’s growth. As a rule, we ensure that all our employees receive above industry income. In addition, we provide them with career growth opportunities coupled with necessary training and skills development opportunities spaced throughout the year. Our corporate culture promotes efficiency and productivity through rewards and recognition given to employees in a timely and just manner.

10 Arpico Insurance PLC Annual Report 2018

Mr. Viville PereraActing Chairman

Mr. Viville Perera is a science graduate from the University of Kelaniya with Second Class Honours and a Fellow Member of The Chartered Institute of Management Accountants and an Associate Member of the Chartered Institute of Marketing, UK. Mr. Perera has over 34 years of experience in the Senior Managerial capacity at leading business organisations such as Associated Newspapers of Ceylon Limited, Middleway Ltd (Ceylinco Group), Amico Group of Companies and Alliance Finance Co. PLC. He has served at the Sri Lanka Institute of Packaging as Treasurer from 1992 to 1997 and as Vice President from 1999 to 2002. Mr. Perera has been representing the Company on the Executive Committee of the Industrial Association of Sri Lanka, an affiliated trade association under the aegis of the Ceylon Chamber of Commerce since 2011. He is also on the Board of Directors of Several Companies of Richard Pieris Group.

Mr. S SirikananathanIndependent Non-Executive Director

Mr. Sirikananathan is a retired partner of KPMG, an international firm of chartered accountants and is presently a sole practitioner under the firm name Sarasiri & Company. He also served on the Boards of Associated News Papers of Ceylon Ltd. (ANCL) as Director/Financial Consultant and Bartleet Finance PLC, as Independent Non-Executive Director, Audit Committee Chairman and Remuneration Committee Member.

Mr. Sirikananathan possesses over 40 years of audit experience with KPMG and has engaged in audits of star class Hotels, Conglomerates, Development Organisations, Multinational Banks, Finance Companies, Insurance Companies and several listed Companies.

Mr. Sirikananathan is a Fellow Member of The Institute of Chartered Accountants of Sri Lanka (FCA) and is also a Fellow Member of the Institute of Certified Management Accountants of Sri Lanka (FCMA). He holds a Bachelor of Science Honours Degree in Physical Science from the University of Peradeniya and has served on the Accounting Standards and Auditing Standards Committee of The Institute of Chartered Accountants of Sri Lanka for eleven (11) and seven (7) years respectively.

Board of Directors

Annual Report 2018 Arpico Insurance PLC 11

Mr. Shiron GooneratneNon-Executive Director

Mr. Shiron Gooneratne is a Fellow Member of the Institute of Chartered Accountants of Sri Lanka and holds a MBA from the University of Leicester, United Kingdom.

He has held Senior Finance positions both locally and overseas.

Mr. Gooneratne began his career at GlaxoSmithKline, Consumer Health Care (former SmithKline Beecham) which is a Fortune 500 Company, as the Financial Accountant and through his dedication and expertise, rose up to the position of Finance Director. Thereafter, Mr. Gooneratne had held the positions of Chief Financial Officer at Sri Lanka Telecom PLC, Chief Financial Officer of Dilmah Ceylon Tea Company PLC and currently he is the Group Chief Financial Officer of Richard Pieris & Company PLC.

Mrs. Lasinee SerasinheIndependent Non-Executive Director

Mrs. Serasinhe is a Fellow Member of The Chartered Institute of Management Accountants (UK), Fellow Member of the Chartered Global Management Accountants and a Diploma Holder in Computer Programming. Mrs. Serasinhe has garnered over 20 years of regulatory experience serving the Securities and Exchange Commission of Sri Lanka and the Insurance Regulatory Commission of Sri Lanka (IRCSL)(former Insurance Board of Sri Lanka). She took up duties as the Director General of IRCSL during a time when IRCSL had set up its office independently, and worked at the IRCSL until her retirement.

Whilst being the Director General of IRCSL, she served as a Board Member of the National Insurance Trust Fund in the capacity of an Ex-Officio Member. Subsequently, she served the Ministry of Finance in the capacity of an advisor for a short period of time. Prior to taking up the post of Director General, IRCSL she served the Securities and Exchange Commission as a Director. Mrs. Serasinhe has several years of experience in the field of Finance in the Private Sector prior to her entry into the regulatory arena. She also functioned as a consultant to the private sector and was attached to SSP Corporate (Pvt) Ltd.

12 Arpico Insurance PLC Annual Report 2018

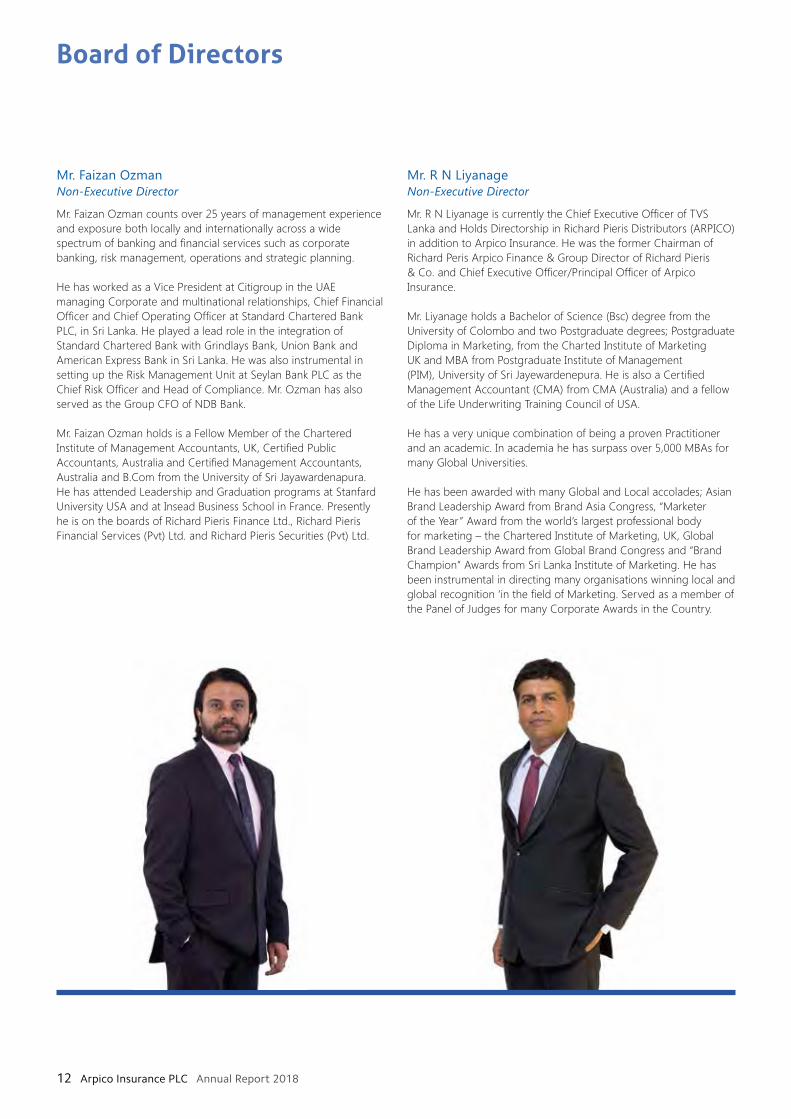

Mr. Faizan OzmanNon-Executive Director

Mr. Faizan Ozman counts over 25 years of management experience and exposure both locally and internationally across a wide spectrum of banking and financial services such as corporate banking, risk management, operations and strategic planning. He has worked as a Vice President at Citigroup in the UAE managing Corporate and multinational relationships, Chief Financial Officer and Chief Operating Officer at Standard Chartered Bank PLC, in Sri Lanka. He played a lead role in the integration of Standard Chartered Bank with Grindlays Bank, Union Bank and American Express Bank in Sri Lanka. He was also instrumental in setting up the Risk Management Unit at Seylan Bank PLC as the Chief Risk Officer and Head of Compliance. Mr. Ozman has also served as the Group CFO of NDB Bank.

Mr. Faizan Ozman holds is a Fellow Member of the Chartered Institute of Management Accountants, UK, Certified Public Accountants, Australia and Certified Management Accountants, Australia and B.Com from the University of Sri Jayawardenapura. He has attended Leadership and Graduation programs at Stanfard University USA and at Insead Business School in France. Presently he is on the boards of Richard Pieris Finance Ltd., Richard Pieris Financial Services (Pvt) Ltd. and Richard Pieris Securities (Pvt) Ltd.

Mr. R N LiyanageNon-Executive Director

Mr. R N Liyanage is currently the Chief Executive Officer of TVS Lanka and Holds Directorship in Richard Pieris Distributors (ARPICO) in addition to Arpico Insurance. He was the former Chairman of Richard Peris Arpico Finance & Group Director of Richard Pieris & Co. and Chief Executive Officer/Principal Officer of Arpico Insurance.

Mr. Liyanage holds a Bachelor of Science (Bsc) degree from the University of Colombo and two Postgraduate degrees; Postgraduate Diploma in Marketing, from the Charted Institute of Marketing UK and MBA from Postgraduate Institute of Management (PIM), University of Sri Jayewardenepura. He is also a Certified Management Accountant (CMA) from CMA (Australia) and a fellow of the Life Underwriting Training Council of USA.

He has a very unique combination of being a proven Practitioner and an academic. In academia he has surpass over 5,000 MBAs for many Global Universities.

He has been awarded with many Global and Local accolades; Asian Brand Leadership Award from Brand Asia Congress, “Marketer of the Year” Award from the world’s largest professional body for marketing – the Chartered Institute of Marketing, UK, Global Brand Leadership Award from Global Brand Congress and “Brand Champion” Awards from Sri Lanka Institute of Marketing. He has been instrumental in directing many organisations winning local and global recognition ‘in the field of Marketing. Served as a member of the Panel of Judges for many Corporate Awards in the Country.

Board of Directors

Annual Report 2018 Arpico Insurance PLC 13

Mr. Doolwala counts over 18 years of experience in finance with 14 years committed to the Insurance Industry. He is an Associate Member of the Chartered Institute of Management Accountants, UK and holds an MBA from Cardiff Metropolitan University UK. He also holds a Diploma in Computer Studies from the National Centre for Computing, UK and has completed the Licentiate Exams from Insurance Institute of India.

Mr. Nishan counts over 26 years of experience in the industry. He has completed (AMTC) – LIMRA, LUTC Diploma in Insurance – LIMRA, Management Skills Course – IMS and Diploma in Marketing from Singapore Institute of Marketing.

Mr. Sampath counts over 27 years of experience in the industry. He has completed Agency Management Training Course (AMTC) – LIMRA, Life Underwriter Training Council (LUTC) Diploma in Insurance – LIMRA and Management Skills Course – Institute of Management Studies (IMS).

Mr. M A DoolwalaDGM – Finance and Operations

Mr. W N C P NishanGeneral Manager – Sales

Mr. H E T SampathGeneral Manager – Sales

Corporate Management Team

Mr. Bandara Counts over 38 years of experience in the industry in the executive grade out of which 11 years experience in Actuarial & Life Reinsurance. He is a BSc.(Hons), A.C.I.I. Chartered Insurer and over 27 years post qualification experience with SLIC. He is an Associate Member of the Chartered Insurance Institute London since 1991 and served two years with Richard Pieris & Company PLC as Group Insurance Manager.

Mr. K BandaraSpecified Officer

14 Arpico Insurance PLC Annual Report 2018

Mr. Perera counts over 21 years of experience in the Insurance Industry. He is an Associate Member of Chartered Insurance Institute and a Life Fellow Member of Insurance Institute of India. He holds a BSc. in Mathematics and Statistics degree from the University of South Africa and an MBA in Finance from the University of Colombo.

Mr. Kaushal Fernando counts over 18 years of experience in Life Underwriting, Claims and holds responsibility for the technical operations of the policy processing. Prior to joining Arpico he served in many capacities at leading Insurance companies.

Mrs. Priyanthi counts over 20 years of experience in the Insurance Industry. She holds a BSc. Degree with First Class Honors in Mathematics and Statistics from University of Colombo and holds a M.Sc. in Actuarial Science also from the University of Colombo.

Ms. Edirisinghe counts over 4 years of experience in the Insurance Industry. She is an Associate Member of the Chartered Accountants of Sri Lanka and holds a BBA Degree with a Second Class Upper Division, specialised in the stream of Accounting from the Faculty of Management of the University of Colombo.

Mr. T PereraAssistant General Manager Technical/Principal OfficerResigned W.E.F. 31.12.2018

Mr. K FernandoManager – Life

Mrs. L A C PriyanthiManager – Actuarial

Ms. I A EdirisingheManager – FinanceResigned W.E.F. 29.03.2019

Corporate Management Team

Annual Report 2018 Arpico Insurance PLC 15

Fastest Growing Life Insurance Company 2017/2018

Most Successful Life Insurance Company in Sri Lanka 2018

16 Arpico Insurance PLC Annual Report 2018

Annual Report 2018 Arpico Insurance PLC 17

Management Discussion & AnalysisOperating Environment 18

Financial Review 26

18 Arpico Insurance PLC Annual Report 2018

Operating Environment

Global growth for 2018/19 while projected to maintain the level achieved in 2017, appears to have slackened pace with downside risks rising. The projected growth is at 3.7 for the year 2018 and 2019 which is a 0.2 percentage lower than the predictions in April 2018. This downward trend illustrates suppressed activity in several advanced economies driven by changing socio-political factors. Numerous trade measures implemented and approved from April to September in advanced economies along with tighter financial conditions, geopolitical issues and higher oil prices, contributed to the downward revision.

Driven by the downward trend in advanced economies as well as pick up in emerging markets and growth in developing economies, global growth is projected to remain steady at 3.7 percent in 2020.

Growth in World Output

%

2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F 2022F0

1

2

3

4

5

3.51

3.49

3.58

3.45

3.27

3.74

3.73

3.65

3.66

3.64

3.58

Growth rate of emerging market and developing Asia is expected to decrease to 6.3 percent in 2019 and 2020 in comparison to 6.5 percent in 2018. In spite of fiscal stimuli and no further increase in tariffs from the United States, China’s growth is projected to slow down. This illustrates the impact of trade tensions with the US. The economic growth of emerging market and developing Asia depends on the easing of conflicts and geopolitical tension. In this backdrop, economic prospects in countries such as Sri Lanka too remain subject to uncertainty.

IndonesiaThailandSri Lanka

2017

Malaysia Pakistan Vietnam India

Peer Country GDP Growth

0

1

2

3

4

5

6

7

8

2018 Updated

%

3.3

3.9

5.1

5.9

5.4

6.8

6.7

3.8

4.5

5.2

5.5

5.8

6.9

7.3

Source: Asian Development Bank

Global financial conditions are expected to tighten driven by monetary policy changes in advanced economies and other risks that affect market sentiment. Economic experts call for countries to work together to successfully manage challenges that are global in nature. Reducing trade costs and settling disputes in place of raising distorted barriers will pave the way for a less troubled future. Cooperation from all countries are required to complete financial regulatory reform agenda, improve cyber security, strengthen international taxation and tackle climate change.

SRI LANKAN ECONOMY Changes in the market economy triggered by various geopolitical acts across the globe, gave rise to fresh challenges to the Sri Lankan economy during the year 2018. Following the low growth rate of 3.1 percent experienced in 2017, the Sri Lankan economy grew at a moderate rate of 3.3 percent during the first half of 2018. Agricultural activities which contracted in 2017, picked up pace in 2018 supported by more favourable weather conditions. Industrial activity growth contracted due to the slowdown of construction, mining and quarrying activities. Services sector expanded as a result of growth in financial services, wholesale and retail trade and other personal services activities. Agriculture, forestry and fishing activities grew at a rate of 4.9 percent during the first half of 2018 while industrial activities only recorded an expansion of 1.6 percent. Services activities on the other hand grew by 4.8 percent during the first half of 2018.

Industry Services

Sri Lankan Economy

%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20170

20

40

60

80

100

Agriculture

Annual Report 2018 Arpico Insurance PLC 19

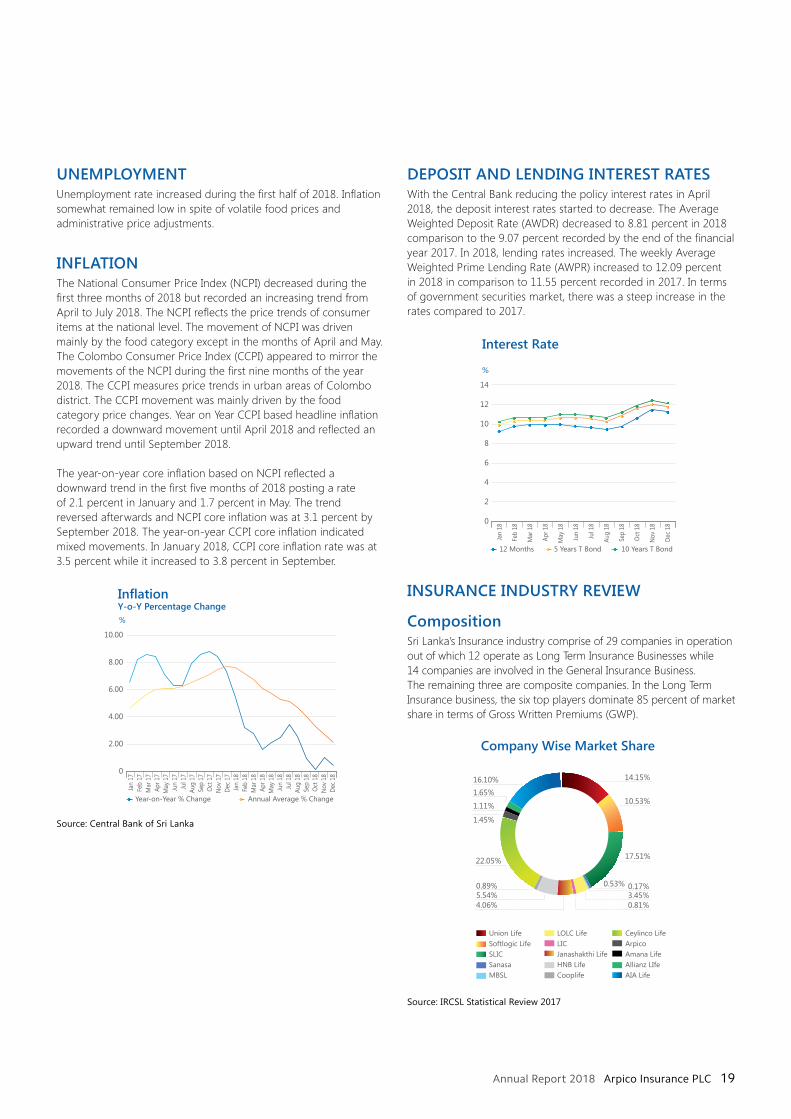

UNEMPLOYMENTUnemployment rate increased during the first half of 2018. Inflation somewhat remained low in spite of volatile food prices and administrative price adjustments.

INFLATION The National Consumer Price Index (NCPI) decreased during the first three months of 2018 but recorded an increasing trend from April to July 2018. The NCPI reflects the price trends of consumer items at the national level. The movement of NCPI was driven mainly by the food category except in the months of April and May. The Colombo Consumer Price Index (CCPI) appeared to mirror the movements of the NCPI during the first nine months of the year 2018. The CCPI measures price trends in urban areas of Colombo district. The CCPI movement was mainly driven by the food category price changes. Year on Year CCPI based headline inflation recorded a downward movement until April 2018 and reflected an upward trend until September 2018.

The year-on-year core inflation based on NCPI reflected a downward trend in the first five months of 2018 posting a rate of 2.1 percent in January and 1.7 percent in May. The trend reversed afterwards and NCPI core inflation was at 3.1 percent by September 2018. The year-on-year CCPI core inflation indicated mixed movements. In January 2018, CCPI core inflation rate was at 3.5 percent while it increased to 3.8 percent in September.

InflationY-o-Y Percentage Change%

0

2.00

4.00

6.00

10.00

8.00

Jan

17Fe

b 17

Mar

17

Apr 1

7M

ay 1

7Ju

n 17

Jul 1

7Au

g 17

Sep

17O

ct 1

7N

ov 1

7De

c 17

Jan

18Fe

b 18

Mar

18

Apr 1

8M

ay 1

8Ju

n 18

Jul 1

8Au

g 18

Sep

18O

ct 1

8N

ov 1

8De

c 18

Year-on-Year % Change Annual Average % Change

Source: Central Bank of Sri Lanka

DEPOSIT AND LENDING INTEREST RATES With the Central Bank reducing the policy interest rates in April 2018, the deposit interest rates started to decrease. The Average Weighted Deposit Rate (AWDR) decreased to 8.81 percent in 2018 comparison to the 9.07 percent recorded by the end of the financial year 2017. In 2018, lending rates increased. The weekly Average Weighted Prime Lending Rate (AWPR) increased to 12.09 percent in 2018 in comparison to 11.55 percent recorded in 2017. In terms of government securities market, there was a steep increase in the rates compared to 2017.

12 Months 5 Years T Bond 10 Years T Bond

Interest Rate

%

0

2

6

10

14

12

8

4

Jan

18

Feb

18

Mar

18

Apr 1

8

May

18

Jun

18

Jul 1

8

Aug

18

Sep

18

Oct

18

Nov

18

Dec

18

INSURANCE INDUSTRY REVIEW

CompositionSri Lanka’s Insurance industry comprise of 29 companies in operation out of which 12 operate as Long Term Insurance Businesses while 14 companies are involved in the General Insurance Business. The remaining three are composite companies. In the Long Term Insurance business, the six top players dominate 85 percent of market share in terms of Gross Written Premiums (GWP).

Company Wise Market Share

14.15%

10.53%

17.51%

0.53% 0.17%3.45%0.81%

5.54%4.06%

0.89%

22.05%

1.65%

1.11%

1.45%

16.10%

Union LifeSoftlogic LifeSLICSanasaMBSL

LOLC LifeLICJanashakthi LifeHNB LifeCooplife

Ceylinco LifeArpicoAmana LifeAllianz LIfeAIA Life

Source: IRCSL Statistical Review 2017

20 Arpico Insurance PLC Annual Report 2018

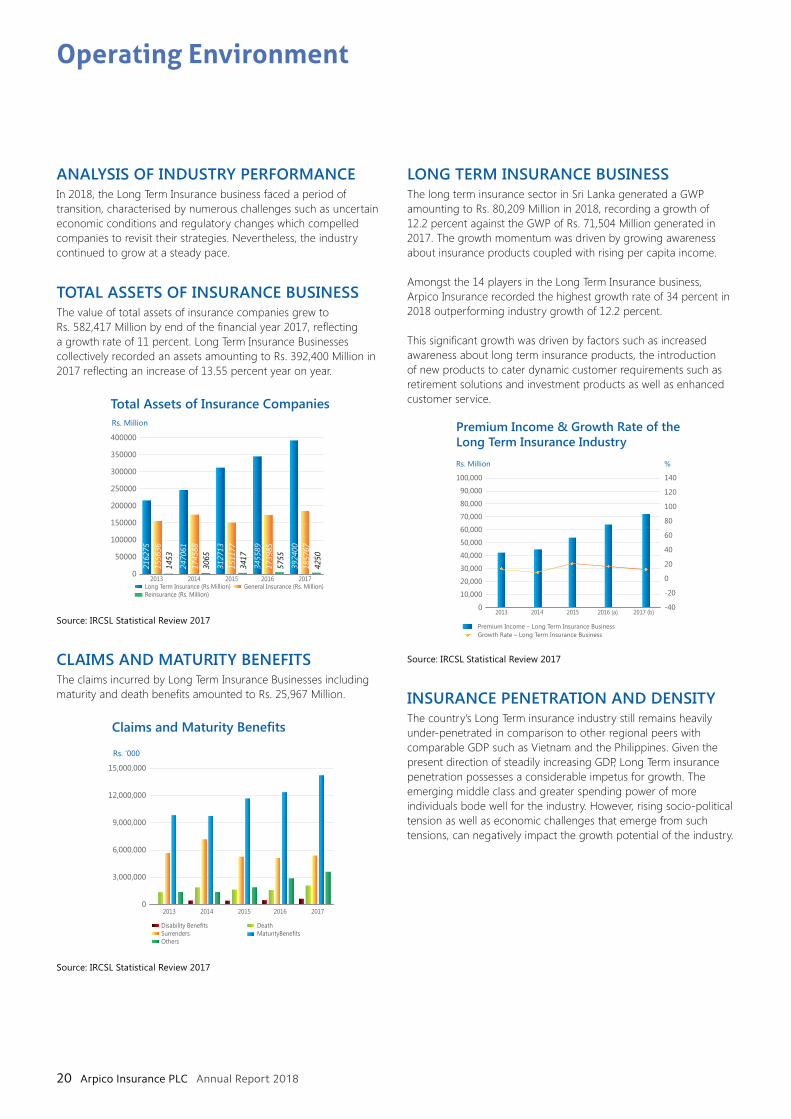

ANALYSIS OF INDUSTRY PERFORMANCE In 2018, the Long Term Insurance business faced a period of transition, characterised by numerous challenges such as uncertain economic conditions and regulatory changes which compelled companies to revisit their strategies. Nevertheless, the industry continued to grow at a steady pace.

TOTAL ASSETS OF INSURANCE BUSINESSThe value of total assets of insurance companies grew to Rs. 582,417 Million by end of the financial year 2017, reflecting a growth rate of 11 percent. Long Term Insurance Businesses collectively recorded an assets amounting to Rs. 392,400 Million in 2017 reflecting an increase of 13.55 percent year on year.

Total Assets of Insurance CompaniesRs. Million

0

50000

100000

150000

200000

250000

300000

350000

400000

2162

75

2470

61

3127

13

3455

89

3924

00

1556

36

1745

88

1511

77

1739

85

1857

67

1453

3065

3417

5755

4250

Long Term Insurance (Rs Million) General Insurance (Rs. Million) Reinsurance (Rs. Million)

2013 2014 2015 2016 2017

Source: IRCSL Statistical Review 2017

CLAIMS AND MATURITY BENEFITSThe claims incurred by Long Term Insurance Businesses including maturity and death benefits amounted to Rs. 25,967 Million.

Claims and Maturity Benefits

Rs. ‘000

0

3,000,000

6,000,000

9,000,000

12,000,000

15,000,000

Disability Benefits Death Surrenders MaturityBenefitsOthers

2013 2014 2015 2016 2017

Source: IRCSL Statistical Review 2017

LONG TERM INSURANCE BUSINESSThe long term insurance sector in Sri Lanka generated a GWP amounting to Rs. 80,209 Million in 2018, recording a growth of 12.2 percent against the GWP of Rs. 71,504 Million generated in 2017. The growth momentum was driven by growing awareness about insurance products coupled with rising per capita income.

Amongst the 14 players in the Long Term Insurance business, Arpico Insurance recorded the highest growth rate of 34 percent in 2018 outperforming industry growth of 12.2 percent.

This significant growth was driven by factors such as increased awareness about long term insurance products, the introduction of new products to cater dynamic customer requirements such as retirement solutions and investment products as well as enhanced customer service.

Premium Income & Growth Rate of the Long Term Insurance IndustryRs. Million

0

10,000

20,000

30,000

40,000

50,000

60,000

80,000

70,000

100,000

90,000

%

-40

-20

0

20

40

60

100

80

140

120

2013 2014 2015 2016 (a) 2017 (b)

Premium Income – Long Term Insurance BusinessGrowth Rate – Long Term Insurance Business

Source: IRCSL Statistical Review 2017

INSURANCE PENETRATION AND DENSITY The country’s Long Term insurance industry still remains heavily under-penetrated in comparison to other regional peers with comparable GDP such as Vietnam and the Philippines. Given the present direction of steadily increasing GDP, Long Term insurance penetration possesses a considerable impetus for growth. The emerging middle class and greater spending power of more individuals bode well for the industry. However, rising socio-political tension as well as economic challenges that emerge from such tensions, can negatively impact the growth potential of the industry.

Operating Environment

Annual Report 2018 Arpico Insurance PLC 21

KEY CHALLENGES AND OPPORTUNITIES Sri Lanka’s aging population presents an opportunity for Long Term Insurers to offer insurance products to fulfill the requirements of the working population who seek to safeguard themselves against uncertainties of old age. The growing numbers of non-communicable diseases as well as epidemics have given rise to a need for health insurance products.

RISKS Slow economic growth and various socio-political tensions have negatively affected the purchasing power of customers. The volatile nature of interest rates impacts the investment income and demand for Long Term Insurance products.

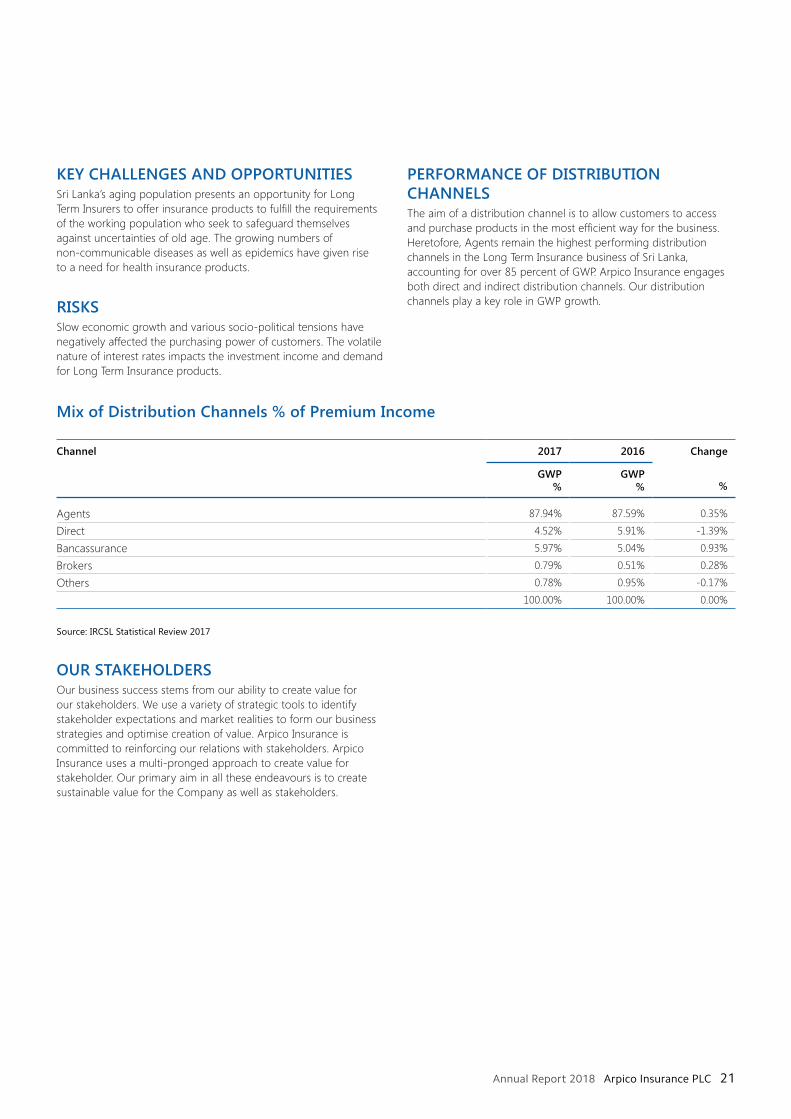

PERFORMANCE OF DISTRIBUTION CHANNELS The aim of a distribution channel is to allow customers to access and purchase products in the most efficient way for the business. Heretofore, Agents remain the highest performing distribution channels in the Long Term Insurance business of Sri Lanka, accounting for over 85 percent of GWP. Arpico Insurance engages both direct and indirect distribution channels. Our distribution channels play a key role in GWP growth.

Mix of Distribution Channels % of Premium Income

Channel 2017 2016 Change

%GWP

%GWP

%

Agents 87.94% 87.59% 0.35%

Direct 4.52% 5.91% -1.39%

Bancassurance 5.97% 5.04% 0.93%

Brokers 0.79% 0.51% 0.28%

Others 0.78% 0.95% -0.17%100.00% 100.00% 0.00%

Source: IRCSL Statistical Review 2017

OUR STAKEHOLDERS Our business success stems from our ability to create value for our stakeholders. We use a variety of strategic tools to identify stakeholder expectations and market realities to form our business strategies and optimise creation of value. Arpico Insurance is committed to reinforcing our relations with stakeholders. Arpico Insurance uses a multi-pronged approach to create value for stakeholder. Our primary aim in all these endeavours is to create sustainable value for the Company as well as stakeholders.

22 Arpico Insurance PLC Annual Report 2018

Stakeholder Engagement The below table depicts our approach to stakeholder engagement.

Stakeholders Modes of Engagement Key Topics of Discussion Meeting Expectations

Customers(Private and corporate policyholders)

Market research/Interactions with Sales Managers and field staff/Corporate website/ Social media/Complaints management/Media releases

Prompt response and the quality of the service

Fulfilling the Company’s promise of long term protection

Expanding reach and distribution points

Product pricing reviews

Expediting the claim settlement process

Strengthening the sales workforce and back office staff to enhance the quality of service

Shareholders(Parent and retail investors)

Annual Report/Interim financial reports/Annual General Meeting/ Media Releases/Corporate website/Direct discussions with Senior Management and the Board

Financial performance and business expansion

Return on investments to shareholders

Premium growth strategies

Maintaining sound corporate governance practices

Effective performance management

Employees(Permanent and contractual staff )

Corporate Communication tools such as emails, newsletters, intranet/staff meetings/skip level interviews/Management meetings

Remuneration increments

Opportunities for career progress

A conducive working environment

Work – life balance

Timely salary increments and promotions based on merit

Ensuring a secure working environment

Creating opportunities for career growth

Increase efficiency and enhance technological systems to help create work-life balance

Suppliers and Business Partners(Reinsurance partners, Banks, Service suppliers and Financial intermediaries)

Meetings and visits/ Formal interactions

Forming long term and mutually beneficial partnerships

Contractual performance

Implementing risk management strategies

Strict pricing discipline

Building rapport and inducing long term trust

Government Institutions and RegulatorsInsurance Regulatory Commission of Sri Lanka (IRCSL), Central bank of Sri Lanka etc.

On-site surveillance

Filing returns

Directives and circulars

Regulatory changes Direct Communication with the Government and industry regulators

Compliance with regulatory requirements

Implementation of policies that affect the industry

Operating Environment

Annual Report 2018 Arpico Insurance PLC 23

Our Path to Success Sound risk management stratagems, timely market research and consistent yet sustainable expansion drives form the core of our drive towards profitability and long term success. While we seek to attract a wider customer base, we focus our attention on addressing current industry realities such as stronger reliance on digital platforms and technological prowess. We also consistently strive to strengthen our human capital.

OUR REACH Striving to reach out to a strong and wide spread customer base, Arpico Insurance conducted a focused expansion drive in the year under review. The current branch network of 47 branches islandwide cater to the insurance requirements of customers across the nation. We will continue to seek further business opportunities and offer our products to a wider audience through improving service excellence and convenience.

OUR PRODUCT MIXArpico Insurance product portfolio follows the core concept of ‘Insurance for the Living’ to offer insurance services that meet current market requirements. We offer variety of life insurance benefits that could be enjoyed during a person’s life rather than at death. Where possible we have extended the benefits from our Life Insurance products to immediate family members of policyholders.

Arpico Endowment PlanThe Arpico Endowment plan is a fund that is designed to fulfill a number of vital needs of the policyholder including education requirements, emergency capital requirements and retirement plans. The sum assured increases by 2.5 percent annually to accommodate inflation.

Benefits Offered y Accidental Death Benefit y Permanent & Total Disability Benefit y Permanent Partial Disability Benefit y Critical Illness Benefit y Additional Term Protection Benefit y Funeral Expenses Benefit y Family Income Benefit y Spouse Cover Benefit y Critical Illness Benefit on the Life of Spouse y Child Critical Illness Benefit y Waiver of Premium Benefit y Hospitalisation per Day Benefit y Hospitalisation Reimbursement Benefit

Arpico Relief PlanArpico Relief plan provides the customer with freedom of planning their premium payments so that they can enjoy the benefits with out paying at the latter stage of the policy term. Customer can select any benefit listed under endowment plan under this scheme as well.

Arpico Term Insurance Plan Arpico Term Insurance plan provides insurance payments in case of unforeseen death during the term of policy with additional benefits that can be added depending on the policyholder ’s requirement.

Benefits Offered y Accidental Death Benefit y Permanent & Total Disability Benefit y Permanent Partial Disability Benefit y Critical Illness Benefit y Funeral Expenses Benefit y Family Income Benefit y Spouse Cover Benefit y Critical Illness Benefit on the Life of Spouse y Child Critical Illness Benefit y Waiver of Premium Benefit y Hospitalisation per Day Benefit y Hospitalisation Reimbursement Benefit

Education Plan – School Fees PlanArpico School Fees plan ensures lessening the burden on parents with regard to children’s education in the event of an unforeseen circumstance. The monthly amount, which is to be paid to the policyholder ’s beneficiary, can be decided on at the time of obtaining the policy.

Arpico Hospitalisation Plan Arpico Hospitalisation contains two unique benefit options. The Arpico Hospitalisation per day plan pays an amount equal to the stated per day amount, multiplied by the number of completed hospitalised days, if hospitalised within Sri Lanka. If the policyholder has to undergo intensive care treatment the Company will pay double the benefit amount. The Arpico Reimbursement plan covers the policyholder and his/her family for surgical and hospitalisation expenses up to Rs. 1,000,000 per annum.

24 Arpico Insurance PLC Annual Report 2018

Operating Environment

Arpico Investment Plan The Arpico Investment Plan enables policyholders to benefit from attractive returns as a Living Benefit. While the rate of return is calculated annually to accommodate economic conditions, policyholders can also profit from additional benefits offered.

Benefits Offered y Accidental Death Benefit y Permanent & Total Disability Benefit y Permanent Partial Disability Benefit y Critical Illness Benefit y Additional Term Protection Benefit y Funeral Expenses Benefit y Family Income Benefit y Spouse Cover Benefit y Critical Illness Benefit on the Life of Spouse y Child Critical Illness Benefit y Waiver of Premium Benefit y Hospitalisation per Day Benefit

Arpico Group Assurance Plan The Arpico Group Assurance plan offers insurance benefits to a group of people with a common point of association such as employees of a single employer.

Benefits Offered y Accidental Death Benefit y Permanent & Total Disability Benefit y Permanent Partial Disability Benefit y Critical Illness Benefit y Funeral Expenses Benefit

Arpico Loan Protection Plan The Arpico Loan Protection plan ensures loan balance payments to relevant financial institution in the event of the policyholder ’s untimely death. The policy ensures that the policyholder ’s assets such as house, building etc, are free from mortgage as a Living Benefit to his/her dependents.

Privilege Customer Insurance SchemeThe Privilege Customer Insurance Scheme offers hospitalisation cover for the policyholder as well as benefits to the policyholder ’s dependent in the event of the policyholder ’s death.

OUR PEOPLE Our human capital remains a primary driver of success. The insurance industry in particular relies on highly skilled and experienced employees to pursue sustainable growth. We foster a work culture that enables employees to feel appreciated and rewarded. The growth of our employees in turn contributes to the growth of the Company. Our recruitment and people development processes have been designed to attract and retain the best in the industry.

We have long since established an ethical recruitment approach that considers gender equality and diversity of skills and experience.

Our People

746707

Male

Female

No.

Each employee at Arpico Insurance receives ample opportunities for training and skills development. Employees also receive timely rewards and recognition based on their individual performance.

Our team comprise of a balanced mix of senior, experienced individuals as well as fresh talent. Our performance based culture allows employees to receive opportunities for career growth and timely remuneration increments.

We maintain a confidential and effective channel of information and communication to allow employees to present their grievances to the management. During the year under review, there have been no reported incidents of discrimination in form.

Annual Report 2018 Arpico Insurance PLC 25

OUR CUSTOMERS With a branch network of 47 branches islandwide, we have enhanced our customer reach. In the meantime, we continue to upgrade our service excellence and resources to help customers enjoy a hassle free experience. We conduct market analysis periodically to determine evolving customer needs and cater to those accordingly.

We have commenced enhancing our product mix to allow customers to have access to products that suit the changing socioeconomic needs. Arpico Insurance adheres to all statutory and regulatory requirements as well as local and global standards to ensure business continuity and transparency to offer customers the best possible services.

FUTURE OUTLOOK From an industry perspective, the rising per capita income and low insurance penetration in the country as well as urbanisation combine to allow insurance companies to explore further growth. We have laid out strategic plans to leverage on the existing growth potential. Our future plans also include reinforcing our technological front and exploring digital platforms for insurance service purposes. We will further strengthen the Arpico Insurance brand whilst continuing to benefit from the brand reputation of the parent company. Arpico Insurance will steer forward on an upward trajectory, designed to create sustainable value for all stakeholders in the years to come.

26 Arpico Insurance PLC Annual Report 2018

Financial Review

Arpico Insurance continued on a commendable growth streak in 2018, outperforming the industry in premium growth and recording an increase in profitability. In the year under review, we attained a premium income of Rs. 1,387 Million recording a growth of 34 percent. As the Company continued to reap the rewards of strategic realignment put in place the year before, we were able to surpass various macro-economic challenges that negatively impacted the nation. The strong growth in our premium income, prudent underwriting practices and strategic alignment of our goals delivered desired financial results in the year 2018.

While we continued to strengthen the transition into Risk Based Capital (RBC), we also sought investment opportunities to craft viable growth.

Aligning with the rules published by IRCSL in 2015, which requires insurance companies to maintain a Capital Adequacy Ratio (CAR) above 120 percent to be considered solvent, the Company’s CAR was at 347 percent as at 31st December 2018.

Our ongoing and futuristic strategy for sustainable growth revolves around working towards high revenue growth, effective risk management and investment management. We continue to envision creating wealth for shareholders and value for stakeholders through maintaining a strategic framework that enhances our economic, social and environmental impact.

GROSS WRITTEN PREMIUM In 2018, we posted a Gross Written Premium of Rs. 1,387 Million, outperforming the industry average. Year on Year GWP growth rate was a commendable 34 percent in comparison to 2017. Posting Rs. 870 Million, First Year Premiums for the year 2018 recorded a growth of 21 percent. Signaling customer confidence in Arpico Insurance Renewal Premium reached Rs. 517 Million, recording a growth of 62 percent. In spite of slow economic growth in the country, focused efforts by Arpico Insurance increased the Company’s sales.

201620152014 2017 2018

GWP

0

300

600

900

1,200

1,500

297

482

745

1,03

8

1,38

7

Rs. Million

PROFITABILITY Arpico Insurance posted a Profit Before Tax of Rs. 199 Million in the year under review which has a degrowth of 3 percent compared to the previous year. In view of the changes in the Inland Revenue act from 2018, the Company recognises a differed tax asset of Rs. 304 which will be utilised against future income tax liability.

201620152014 2017 2018

Profit

Rs. Million

0

50

100

150

200

250

1225

107

206 198

199

206

107

2512

201620152014 2017 2018

No. of Policies

No.

0

5,000

10,000

15,000

20,000

25,000

6,88

5

9,24

4

11,3

09

17,6

04

20,5

65

Annual Report 2018 Arpico Insurance PLC 27

EARNINGS PER SHARE (EPS)The Company’s Earnings Per Share reached Rs. 7.54 in view of recognition of deferred tax asset resulted by the change in the Inland Revenue Act. The Year on Year growth rate of EPS stands at 142 percent.

201620152014 2017 2018

EPS

0

1

2

3

4

5

6

7

8

0.22 0.39

1.63

3.11

7.54 7.54

3.11

1.63 0.390.22

Rs.

ASSET BASEDuring the year under review, the Company’s Total Assets reached Rs. 2,996 Million from Rs. 2,104 recorded in 2017. Arpico Insurance’s steady net value can be attributed to the consistent Asset Base growth that the Company has witnessed since 2012.

201620152014

Total Assets

2017 2018

Asset Base

0

500

1,000

1,500

2,000

2,500

3,000

980

1,16

0

1,58

6

2,10

4

2,99

6

621

647

754

933

1,43

2

Shareholder Equity

Rs. Million

LIFE FUNDArpico Insurance’s Life Fund grew by 29 percent to reach Rs. 1,326 Million in 2018. The healthy growth of the Life Fund establishes the Company’s capability to fulfil obligations to policy holders and augurs well for future growth of the Company through building customer and shareholder confidence.

201620152014 2017 2018

Life Fund

0

300

600

900

1,200

1,500

287

436

726

1,02

5

1,32

6

Rs. Million

ENVISIONING THE FUTURE Reinforced by sound strategic goals and prudent management, Arpico Insurance succeeded in creating a stable platform for sustainable growth in the future. While the Company possess adequate levels of capital and effective risk management strategies to take advantage of market opportunities, we will continue to explore future avenues of growth through timely market research and product introduction. Ensuring revenue growth in an increasingly volatile economy in a highly saturated industry is a challenging task. However, our robust performance within the past few years and well-defined yet fluid growth strategies gives us confidence to envision business success in the years to come.

28 Arpico Insurance PLC Annual Report 2018

Annual Report 2018 Arpico Insurance PLC 29

GovernanceCorporate Governance 30

Audit Committee Report 33

Remuneration Committee Report 35

Related Party Transaction Review Committee Report 36

Risk Management 37

30 Arpico Insurance PLC Annual Report 2018

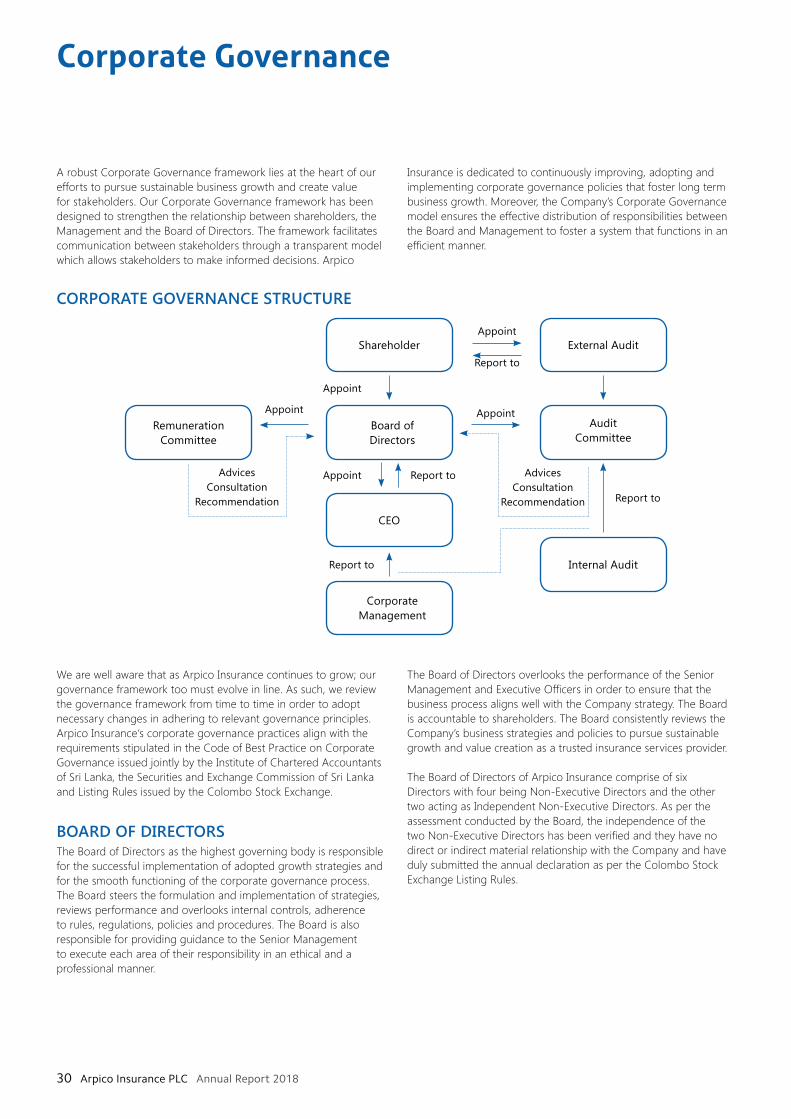

Corporate Governance

A robust Corporate Governance framework lies at the heart of our efforts to pursue sustainable business growth and create value for stakeholders. Our Corporate Governance framework has been designed to strengthen the relationship between shareholders, the Management and the Board of Directors. The framework facilitates communication between stakeholders through a transparent model which allows stakeholders to make informed decisions. Arpico

Insurance is dedicated to continuously improving, adopting and implementing corporate governance policies that foster long term business growth. Moreover, the Company’s Corporate Governance model ensures the effective distribution of responsibilities between the Board and Management to foster a system that functions in an efficient manner.

CORPORATE GOVERNANCE STRUCTURE

Remuneration Committee

Advices Consultation

Recommendation

Advices Consultation

Recommendation

Appoint

Appoint

Appoint

Appoint

Appoint

Report to

Report to

Report to

Report to

Corporate Management

CEO

Board of Directors

Shareholder External Audit

Audit Committee

Internal Audit

We are well aware that as Arpico Insurance continues to grow; our governance framework too must evolve in line. As such, we review the governance framework from time to time in order to adopt necessary changes in adhering to relevant governance principles. Arpico Insurance‘s corporate governance practices align with the requirements stipulated in the Code of Best Practice on Corporate Governance issued jointly by the Institute of Chartered Accountants of Sri Lanka, the Securities and Exchange Commission of Sri Lanka and Listing Rules issued by the Colombo Stock Exchange.

BOARD OF DIRECTORSThe Board of Directors as the highest governing body is responsible for the successful implementation of adopted growth strategies and for the smooth functioning of the corporate governance process. The Board steers the formulation and implementation of strategies, reviews performance and overlooks internal controls, adherence to rules, regulations, policies and procedures. The Board is also responsible for providing guidance to the Senior Management to execute each area of their responsibility in an ethical and a professional manner.

The Board of Directors overlooks the performance of the Senior Management and Executive Officers in order to ensure that the business process aligns well with the Company strategy. The Board is accountable to shareholders. The Board consistently reviews the Company’s business strategies and policies to pursue sustainable growth and value creation as a trusted insurance services provider.

The Board of Directors of Arpico Insurance comprise of six Directors with four being Non-Executive Directors and the other two acting as Independent Non-Executive Directors. As per the assessment conducted by the Board, the independence of the two Non-Executive Directors has been verified and they have no direct or indirect material relationship with the Company and have duly submitted the annual declaration as per the Colombo Stock Exchange Listing Rules.

Annual Report 2018 Arpico Insurance PLC 31

Profiles of each director are presented on pages 10 to 12 in this Annual Report.

Name of Director Non- Executive Director

Independent Non-Executive Director

Mr. Viville Perera

Mr. Shiron Gooneratne

Mr. R N Liyanage

Mr. Faizan Ozman

Mr. S Sirikananathan

Mrs. Lasinee Serasinhe

INDEPENDENT DIRECTORSMr. S Sirikananathan and Mrs. Lasinee Serasinhe operate as Independent Non-Executive Directors. Their diverse experience and expertise in commercial, corporate and regulatory activities provide an independent view and judgment to the board.

APPOINTMENT OF DIRECTORS Arpico Insurance adheres to the section 29 of the Articles of Association of the Company in appointing Directors to the Board. Accordingly, the Company passes an Ordinary Resolution for the authorisation of the appointments. In line with the Regulation of Insurance Industry Act, the Company obtains prior approval from the Insurance Regulatory Commission of Sri Lanka to appoint Directors to the Board.

ROLE AND RESPONSIBILITIES OF THE BOARDThe role and specific responsibilities of the Board are as follows:

y To ensure that the highest level of compliance is adhered to in all operations of the Company

y Be accountable to shareholders with regard to the governance of the Company

y To ensure that the highest standards of disclosure is maintained at all levels of the Company resulting in transparency in all business activities and operations

y Effective and efficient allocation of Company resources to create value for shareholders to effectively and efficiently direct company’s resources to bring about results for the shareholders

y To provide direction and guidance through approval of the Company’s medium and long term strategy, annual budgets and significant financial and operational policies

FUNCTIONS OF THE BOARDa. Direct the business and affairs of the Companyb. Formulate short and long term strategies, as a basis for the

operational plans of the Company and monitor implementationc. Report on their stewardship to shareholdersd. Identify the principal risks of the business and ensure that

adequate risk management systems are in placee. Ensure internal controls are adequate and effectivef. Approve the annual capital and operating budgets and review

performance against budgetsg. Approve the interim and annual financial statements of the

Companyh. Ensure compliance with laws and regulationsi. Sanction all material contracts, acquisitions or disposal of assets

MEETINGS OF THE BOARD OF DIRECTORS The Board of Directors meet periodically to analyse the business process of the Company and to review Company performance in order to establish whether the implanted strategies for the target period are being adhered to in a timely manner. In the year 2018, the Board met four times. In addition subcommittee meetings were held depending on the requirement. Each member of the Board receives board papers and required information prior to each meeting in order to ensure constructive and insightful communication on matters pertaining to the Company. Clear communication and discussion are essential aspects of issue identification which in turn paves the way for sound decision making.

INTERNAL CONTROLSThe internal control system focuses on the proper maintenance and protection of the Company assets. The internal control system maintains a well-defined record keeping approach to ensure the reliability of information regarding Company assets. The internal control system incorporate financial, operational and risk management controls.

The Internal Audit Division which reports to the Chairman of the Audit Committee periodically evaluates the internal control system across the organisation. The division reports its findings to the Board upon completion of the review. The Board is responsible to safeguarding the efficacy and the competence of the internal control system.

BOARD SUB COMMITTEES The Board delegates responsibilities to subcommittees to guarantee regulatory compliance and robust business process implementation. While each subcommittee is responsible for working within clearly defined terms of reference, the Board establishes subcommittees, appoints members and ensures the smooth functioning of each subcommittee.

32 Arpico Insurance PLC Annual Report 2018

AUDIT COMMITTEEThe Audit Committee overlooks the Company’s adherence and application of accounting policies, the financial reporting process and the execution of the internal control principles of the Company. An Independent Non-Executive Director leads the Audit Committee which comprises Independent Non-Executive Directors with ample experience and expertise in finance and business operations. The Audit Committee Report presented on pages 33 to 34 details the functions carried out by the committee in 2018.

INVESTMENT COMMITTEEConsisting of two Non-Executive Directors and an Independent Non-Executive Director, the Investment Committee is responsible for the smooth functioning of the investment activities of Arpico Insurance.

MEMBERS OF THE INVESTMENT COMMITTEE Mr. Viville Perera – Non-Executive DirectorMr. Shiron Gooneratne – Non-Executive DirectorMrs. Lasinee Serasinhe – Independent Non-Executive Director

REMUNERATION COMMITTEEArpico Insurance is one of the subsidiaries of Richard Pieris and Company PLC. As such, the Remuneration Committee of Richard Pieris and Company PLC acts as the Remuneration Committee for Arpico Insurance. The report of the Remuneration Committee is presented on page 35 of this report.

RELATED PARTY TRANSACTION REVIEW COMMITTEERelated Party Transaction Review Committee of Richard Pieris and Company PLC acts as the Related Party Transaction Review Committee for Arpico Insurance. The report of the Related Party Transaction Review Committee is presented on page 36 of this report.

SHAREHOLDING STRUCTUREShareholder Percentage

Kegalle Plantation PLC 40%Richard Pieris Distributors Limited 27%Richard Pieris and Company PLC 23%Public 10%

COMPLIANCEArpico Insurance is governed by mandatory rules and regulations which are established by Companies Act No. 07 of 2007, Listing Rules of the CSE and the regulation of Insurance Industry (RII) Act No. 43 of 2000 and subsequent amendments and rules, regulations, directives and circulars issued by the Insurance Regulatory Commission of Sri Lanka (IRCSL). The Company adheres to the guidelines issued by the Sri Lanka Accounting Standards (LKAS and SLFRS) and other statutory regulations in preparation of the financial statements of the Company. In line with the Listing Rules of the Colombo Stock Exchange, the Company publishes quarterly financial statements to give shareholders access to significant developments that took place during the reported period. Moreover, following IRCSL guidelines, the Company prepares and submits monthly and quarterly returns. The Board of Directors, to the best of their knowledge and belief, are satisfied that all statutory payments have been made to date.

GOING CONCERNFollowing in depth review of the financial position and cash flow status of Arpico Insurance, the Directors have continued to use the ‘Going Concern’ basis in the preparation of the financial statements.

Corporate Governance plays a vital role in determining the Company’s principal activities and enforces accountability and ethical conduct of business dealings in order to create sustainable value for shareholders. In view of this, Arpico Insurance is committed to consistent and effective execution and timely enhancement of the corporate governance framework. Based on the strongly-supported belief that a robust governance structure paves the way forward to business success and the success of all stakeholders of the Company, we will continue to adopt industry standards and go beyond those to implement our own standards for the betterment of future performance of the Company.

Corporate Governance

Annual Report 2018 Arpico Insurance PLC 33

The Audit Committee Charter dictates the purpose, authority, composition, meetings and responsibilities of the Committee. The Board of Directors are responsible for the approval and effective implementation of the audit committee charter.

PURPOSE The purpose of the Audit Committee is to

• Assist the Board of Directors in fulfilling its overall responsibilities for the Financial Reporting Process.

• Review the system of internal control and risk management procedures.

• Monitor the effectiveness of the internal audit function. • Review the Company’s process for monitoring compliance with

laws and regulations. • Assess the independence and performance of the Company’s

external auditors. • Make recommendations to the Board on the appointment of

external auditors, their remuneration and terms of appointment.

COMPOSITIONThe Audit Committee of Arpico Insurance PLC is appointed by the Board of Directors. The Committee comprises of the following directors of the Company as at 31st December 2018.

Mr. S Sirikananathan – Chairman and Independent Non-Executive Director Mrs. L Serasinhe – Independent Non-Executive Director

The profiles of the members of Audit committee are presented on pages 10 to 12 of this Annual Report. The Company Secretary carried out the duties as the Audit Committee Secretary.

MEETINGSThe Audit Committee held a total of 6 meetings during the year under review. Audit Committee meetings were conducted in attendance (upon invitation) of the DGM Finance and Operations and the Group Internal Auditors. The Audit Committee extended invitations to members of the management and external auditors whenever their presence was deemed necessary. Board members received updates of the Audit Committee activities via meeting minutes tabled at Board meetings held subsequently to each Audit Committee meeting.

Audit Committee Report

INTERNAL AUDIT AND RISK MANAGEMENTThe Audit Committee is responsible for the effective functioning of the internal audit programme which in turn ensures the efficacy of key operational aspects. The Audit Committee analysed the internal audit programme of 2018 to review internal audit findings and management responses in order to take corrective action when necessary and monitor implementation of required measures.

INTERNAL CONTROLSThe Audit Committee reviewed the Company’s internal control system and its approach to managing business and financial risks to identify potential inefficiencies and recommend corrective measures when necessary. The Audit Committee review ensured that necessary tools are in place to secure Company assets. The Audit Committee reviewed the financial reporting system to determine the effectiveness and accuracy of the preparation and presentation of financial statements. The Committee monitored the monthly comprehensive Financial Review Reports to ensure that all key performance criteria were prepared and reviewed by the Management.

FINANCIAL STATEMENTS AND RELATED DISCLOSURESIn line with its responsibility of overlooking the Company’s financial reporting, the Audit Committee reviewed the following areas to the extent it deemed necessary and appropriate, in discussion with the external auditors and the management:

i. Significant financial issues and judgments made in connection with the preparation of the Company’s financial statements.

ii. Consistency of the accounting policies and methods adopted and their compliance with the Sri Lanka Financial Reporting Standards (SLFRS/LKAS).

iii. Requirements of the Companies Act No. 07 of 2007 and the Regulation of Insurance Industry Act No. 43 of 2000 and amendments thereto.

The Audit Committee has reviewed all Interim Financial Statements and the Annual Financial Statements for the year ended 31st December 2018 before their issuance.

34 Arpico Insurance PLC Annual Report 2018

COMPLIANCE WITH LAWS AND REGULATIONThe Audit Committee reviewed all the compliance checklists signed off by the Management of the Company to ensure compliance with all applicable compliance submissions relating to the Department of Inland Revenue, the Insurance Regulatory Commission of Sri Lanka and Labour regulations.

EXTERNAL AUDITORSThe Audit Committee met External Auditors to analyse the Audited Financial Statements and look into all relevant and consequential matters. The Committee was satisfied that non-audit services facilitated by External Auditors did not intervene with their independence and objectivity. The Committee determined that such services were assigned in a manner calculated to prevent any conflict of interest. The Audit Committee has recommended to the Board of Directors that Messrs. Ernst and Young be reappointed as Auditors for the financial year ending 31st December 2019 subject to approval of shareholders at the next Annual General Meeting.

CONCLUSIONThe Audit Committee is satisfied that the internal controls and procedures in place for assessing and managing the risks provide reasonable assurance regarding the reliability of financial reporting of the Company and that the Company assets are safeguarded and that all relevant laws, rules, regulations, code of ethics and standards of conduct have been followed.

Mr. S SirikananathanChairmanAudit CommitteeColombo, Sri Lanka14th May 2019

Audit Committee Report

Annual Report 2018 Arpico Insurance PLC 35

Remuneration Committee Report

The Remuneration Committee of the Richard Pieris and Company PLC acted as the Remuneration Committee of Arpico Insurance PLC.

The Remuneration Committee, appointed by and responsible to the Board of Directors, consists of three independent Non-Executive Directors, Dr. Jayatissa De Costa P.C., Mr. Joseph Felix Fernandopulle and Mr. Prasanna Fernando. The Committee is chaired by Dr. Jayatissa De Costa P.C. The committee met on several occasions during the financial year.

The Remuneration Committee has reviewed and recommended the following to the Board of Directors:

1. Policy on remuneration of the Executive Staff.

The committee has taken into account the competitive environment in the insurance industry in determining the salary structure.

Dr. Jayatissa De Costa P.C.Chairman14th May 2019

36 Arpico Insurance PLC Annual Report 2018

The Related Party Transactions Review Committee of the Richard Peiris and Company PLC acts as the Related Party Transactions Review Committee of Arpico Insurance PLC.

The Related Party Transaction Review Committee, appointed by and responsible to the Board of Directors, consists of three Independent Non-Executive Directors including its Chairman Dr. Jayatissa De Costa P.C, Mr. Joseph Felix Fernandopulle and Mr. Prasanna Fernando.

OBJECTIVES OF THE COMMITTEE1. To exercise oversight on behalf of the Board that all Related

Party Transactions (“RPTs” Other than those exempted by the CSE listing rules on the Related Party Transactions) of Arpico Insurance PLC are carried out and disclosed in a manner consistent with CSE Listing rules.

2. To advise and update the Board of Directors on related party transactions of Arpico Insurance PLC on a quarterly basis.

3. To ensure compliance with CSE listing rules on Related Party Transactions.

4. To review policies and procedures of Related Party Transactions of Arpico Insurance PLC.

5. To ensure that shareholder interests are protected and that fairness and transparency are maintained.

All related party transactions entered into during the year were of a recurrent, trading nature and were necessary for day to day operations of the Company. In the opinion of the committee, the terms of these transactions were not more favorable to the related parties than those generally available to the public.

Related Party Transactions Review Committee Report

The committee held four meetings during the period under review. The activities and the views of the committee have been communicated to the Board of Directors where appropriate.

No related party transactions exceeded the limit of 10 percent of the equity or 5 percent of the total assets requiring immediate disclosure to CSE and a separate disclosure has been made in the annual report as required by Section 9.3.2 (b) of listing rules, and confirms that the Company has complied with all requirements as per Section 9 of the Listing Rules.

All details of such related party transactions entered in to during the year are given in Note 32 to the financial statements on pages 86 to 87 of this Annual Report.

Dr. Jayatissa De Costa P.C.Chairman14th May 2019

Annual Report 2018 Arpico Insurance PLC 37

Risk acceptance is part and parcel of the insurance industry. As such, managing risk becomes an integral part of protecting the Company’s capital and ensuring consistent value creation. Risk management strategies engage tools of identifying, assessing and mitigating risk to safeguard the Company’s core competencies. Realities of the current macro-economic conditions pose numerous industry specific challenges to Arpico Insurance. Hence, a robust risk management framework is an integral part of business growth and sustainability.

As we continue to grow in scale and complexity, the Company’s risk management strategies too must evolve co-currently. Mindful of this fact, we have adopted a risk management framework that identifies, evaluates and creates strategies to successfully manage both internal and external risks. While the Company has laid down precautionary measures to address risks that are beyond our control, we understand that risk management is an ongoing process. As such, the Board of Directors and Senior Management of Arpico Insurance consistently monitor the risk management process to identify evolving risk situations, measure the impact and control risk factors.

We promote a sound risk culture at all levels of the Company through creating opportunities for employees to understand potential risks and act according to the shared values and knowledge of the Company. The Board of Directors maintains a consistent focus on promoting a sound and effective risk culture within the organisation.

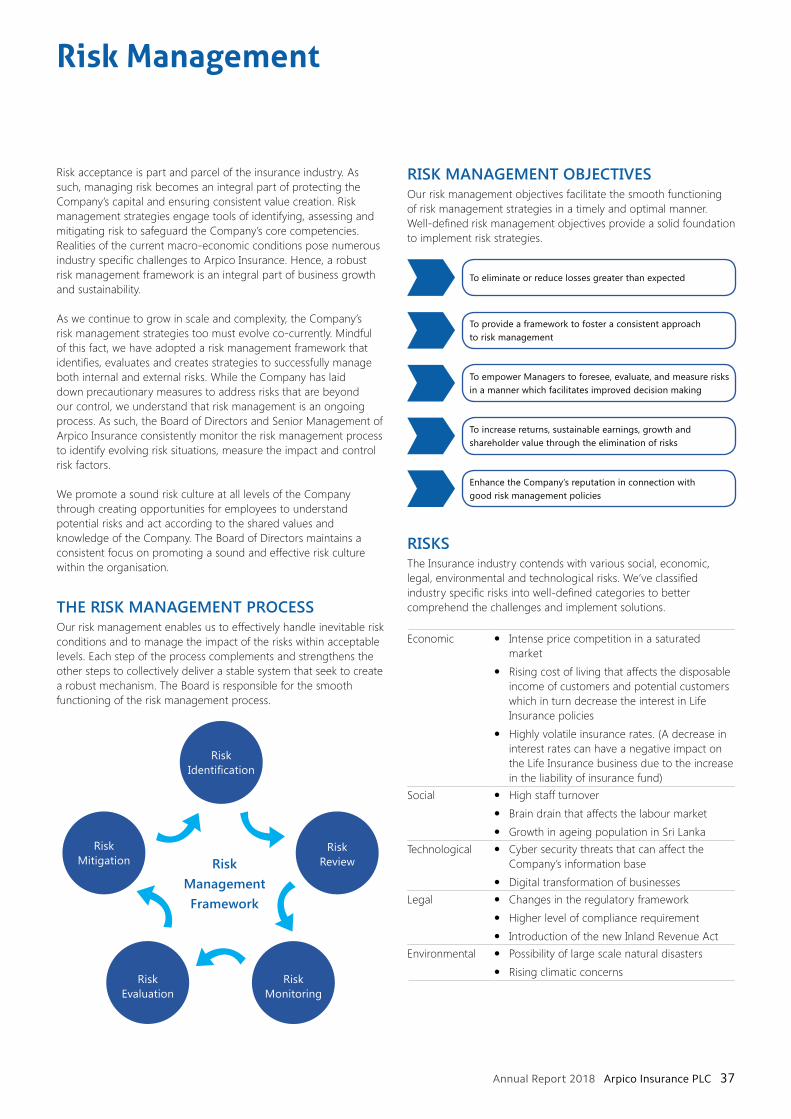

THE RISK MANAGEMENT PROCESSOur risk management enables us to effectively handle inevitable risk conditions and to manage the impact of the risks within acceptable levels. Each step of the process complements and strengthens the other steps to collectively deliver a stable system that seek to create a robust mechanism. The Board is responsible for the smooth functioning of the risk management process.

Risk Management Framework

Risk Identification

Risk Review

Risk Monitoring

Risk Evaluation

Risk Mitigation

Risk Management

RISK MANAGEMENT OBJECTIVESOur risk management objectives facilitate the smooth functioning of risk management strategies in a timely and optimal manner. Well-defined risk management objectives provide a solid foundation to implement risk strategies.

To eliminate or reduce losses greater than expected

To provide a framework to foster a consistent approach to risk management

To empower Managers to foresee, evaluate, and measure risks in a manner which facilitates improved decision making

To increase returns, sustainable earnings, growth and shareholder value through the elimination of risks

Enhance the Company’s reputation in connection with good risk management policies

RISKS The Insurance industry contends with various social, economic, legal, environmental and technological risks. We’ve classified industry specific risks into well-defined categories to better comprehend the challenges and implement solutions.

Economic y Intense price competition in a saturated market

y Rising cost of living that affects the disposable income of customers and potential customers which in turn decrease the interest in Life Insurance policies

y Highly volatile insurance rates. (A decrease in interest rates can have a negative impact on the Life Insurance business due to the increase in the liability of insurance fund)

Social y High staff turnover y Brain drain that affects the labour market y Growth in ageing population in Sri Lanka

Technological y Cyber security threats that can affect the Company’s information base

y Digital transformation of businessesLegal y Changes in the regulatory framework

y Higher level of compliance requirement y Introduction of the new Inland Revenue Act

Environmental y Possibility of large scale natural disasters y Rising climatic concerns

38 Arpico Insurance PLC Annual Report 2018

Company categorises the risks identified in to following broad categories.

Liquidity Risk

Compliance Risk

Re-insurance Risk

Operational Risk

Market Risk

Underwriting Risk

Credit Risk

Risk Categories

Our risk management process involves a set risk management policy that enables the Company to continuously analyse the conditions to identify the challenges presented by the current macro-economic environment and prioritise the Company risk management strategies to froster business growth and eliminate unwelcome interruptions to the value creation process.

RISK PRIORITISATION AND MITIGATION Our risk prioritising system allows us the streamline the process of addressing risks.

Transference (Moderate Risk)

Acceptance (Low Risk)

Avoidance (High Risk)

Reduction (Moderate Risk)

Impact

Likelihood

High

High

Low

Low

Risk Category Risk Description Risk Rating Risk Mitigation

Underwriting Risk This refers to the risk of accepting insurance business that carries an unacceptably high exposure to the risk of claims and accepting risks at rates that do not contain an adequate risk premium. Underwriting risk could also arise due to a lack of understanding regarding changes in the environment such as the effect of climate change.

High y An adequate level of segregation of duties is ensured between underwriting and sales. The underwriting function is centralised and operates from the Head Office.

y Manual of Financial Authority is available to give guidance on underwriting limits.