debt relief or debt restructuring? evidence from an ... · debt relief or debt restructuring?...

TRANSCRIPT

Debt Relief or Debt Restructuring? Evidence from an Experiment

with Distressed Credit Card Borrowers∗

Will DobbiePrinceton University and NBER

Jae SongSocial Security Administration

August 2016

Abstract

This paper reports results from a randomized field experiment that offered distressed creditcard borrowers more than $50 million in debt forgiveness and over 27,500 additional monthsto repay their debts. The experimental variation effectively randomized debt write-downs andminimum payments for borrowers at eleven large credit card issuers. Merging information fromthe experiment to administrative tax and bankruptcy records, we find that the debt write-downsincreased debt repayment and decreased bankruptcy filing. The debt write-downs also increasedformal sector employment for the most financially distressed borrowers. In contrast, we find littleimpact of the lower minimum payments on debt repayment, bankruptcy, or employment. Weshow that this null result can be explained by the positive short-run effect of increased liquiditybeing offset by the unintended, negative effect of exposing borrowers to more default risk. Weconclude that debt relief is more effective than debt restructuring for distressed credit cardborrowers, even when these borrowers are liquidity constrained.

∗We are extremely grateful to Ann Woods and Robert Kaplan at Money Management International, David Jones atthe Association of Independent Consumer Credit Counseling Agencies, Ed Falco at Auriemma Consulting Group, andGerald Ray and David Foster at the Social Security Administration for their help and support. We thank Tal Gross,Matthew Notowidigdo, and Jialan Wang for providing the bankruptcy data used in this analysis. We also thank HankFarber, Paul Goldsmith-Pinkham, Tal Gross, Larry Katz, Ben Keys, Patrick Kline, Alex Mas, Jesse Shapiro, AndreiShleifer, Crystal Yang, Jonathan Zinman, Eric Zwick, and numerous seminar participants for helpful comments andsuggestions. Daniel Herbst, Disa Hynsjo, Samsun Knight, Kevin Tang, Daniel Van Deusen, Amy Wickett, and YiningZhu provided excellent research assistance. Financial support from the Washington Center for Equitable Growth isgratefully acknowledged. Correspondence can be addressed to the authors by e-mail: [email protected] [Dobbie]or [email protected] [Song]. Any opinions expressed herein are those of the authors and not those of the Social SecurityAdministration.

During the 2007-2009 financial crisis, both lenders and policymakers introduced a series of new

debt relief and debt restructuring programs to help distressed borrowers. For example, in the

mortgage market, policymakers implemented reforms such as the Home Affordable Modification

Program (HAMP) that combined elements of both debt relief and debt restructuring in an attempt

to decrease the number of new foreclosures. Over the same time period, a number of large credit

card issuers independently introduced a similar set of debt relief and debt restructuring programs

to decrease the number of new delinquencies, although their efforts were hampered by government

regulations that prevented principal write-downs for most cardholders.1 In both markets, however,

there was little agreement about whether distressed borrowers were most likely to benefit from debt

relief, debt restructuring, or a combination of both.

The relative effectiveness of debt relief and debt structuring depends on the types of constraints

borrowers face at the margin. Debt write-downs benefit borrowers to the extent that long-run

insolvency concerns, and not short-run liquidity constraints, determine borrower behavior at the

margin. Conversely, restructuring debt contracts to reduce or defer payments can address any

short-run liquidity constraints, but at the cost of extending the repayment period and exposing

borrowers to new default risk in the future. To date, there is little empirical evidence on which

type of debt modification is most likely to benefit borrowers in practice.2

This paper provides new evidence on this question using data from a large randomized field

experiment matched to administrative tax and bankruptcy records. The experiment was designed

and implemented by a large non-profit credit counseling organization in the context of a preexist-

ing repayment program, called the Debt Management Plan (DMP). The DMP allows distressed

borrowers to simultaneously repay all of their outstanding credit card debt over a three to five year

period. In exchange for enrolling in the repayment program, credit card issuers will usually lower

the minimum payment amount and provide a partial write-down of any interest payments and

late fees. With more than 600,000 individuals enrolling in these repayment programs each year,

the DMP is one of the most important alternatives to consumer bankruptcy in the United States

(Wilshusen 2011).

In the experiment, control borrowers were offered the status quo repayment program that

had been offered to all borrowers prior to the experiment, while treated borrowers were offered a

modified repayment program that included some combination of two different treatments. The first

1In the United States, banking regulations prevent credit card issuers from simultaneously reducing the originalprincipal and lengthening the repayment period unless a debt is first classified as impaired. During the financial crisis,a group of credit card issuers proposed amending these regulations to allow them to introduce a pilot program thatwould have included both types of debt modifications. Reports indicate that many large card issuers were interestedin participating in the proposed pilot program. For example, see http://www.huffingtonpost.com/2008/10/30/

banks-asking-for-credit-c_n_139478.html2There is both theoretical and empirical work showing that debt relief and debt restructuring can increase

aggregate consumption and employment by decreasing debt overhang, potentially making these policies ex-postefficient during economic downturns (e.g. Hall 2011, Eggertsson and Krugman 2012, Mian, Rao, and Sufi 2013, Mianand Sufi 2014). Debt modifications can also be ex-post efficient in regular economic conditions if debt contracts areincomplete (e.g. Bolton and Scharfstein 1996, Bolton and Rosenthal 2002) or there are negative spillovers of loandefault (e.g. Campbell, Giglio, and Pathak 2011, Mian, Sufi, and Trebbi 2015), although ex-ante responses can offsetthese benefits (e.g. Bolton and Rosenthal 2002, Mayer et al. 2014).

1

treatment increased the typical borrower’s debt write-down amount by an extra $1,712 by dropping

the last four payments of the repayment program and holding the minimum payment constant.

This “debt write-down” treatment is therefore likely to decrease insolvency-based defaults at the

beginning of the repayment program by promising a future debt write-down, and decrease defaults

at the end of the repayment program by deceasing exposure to default risk. Conversely, the second

treatment decreased the typical borrower’s minimum payment amount by an extra $26.68 by adding

an extra four months to the repayment program. This “minimum payment” treatment is therefore

likely to decrease liquidity-based defaults at the beginning of the repayment program by lowering

the minimum payment amount, but increase defaults at the end of the repayment program by

increasing the exposure to default risk. The combination of the two randomized treatments in a

real-world setting makes the experiment an ideal laboratory to measure the effects of debt relief

and debt restructuring.

In total, about 40,000 treated borrowers were offered more than $50 million in new debt write-

downs and more than 27,500 additional months to repay their debts as a part of the experiment.

We measure the effects of the randomized treatments using three administrative datasets matched

for the purposes of this study. Debt repayment is measured using administrative records from the

credit counseling organization that implemented the experiment. Financial distress is measured

using court bankruptcy records. Earnings, employment, and 401k contributions are measured

using tax data from the Social Security Administration (SSA). The matched dataset allows us to

estimate the medium-run effects of the debt write-downs and lower minimum payments across a

range of important outcomes.

We begin our analysis by estimating intent-to-treat effects that measure the impact of being

offered a combination of both treatments. We find that the experiment increased debt repayment

and decreased bankruptcy filing, particularly for borrowers with the highest debt-to-income ratios.

Treatment eligibility increased the probability of finishing a repayment program by 2.97 percentage

points for these high debt-to-income borrowers, a 20.01 percent increase from the control mean.

Bankruptcy filing over the first five years following the experiment also decreased by 1.19 percent-

age points for these borrowers, an 8.40 percent decrease from the control mean. There were no

detectable effects on labor market outcomes or 401k contributions for either high or low debt-to-

income borrowers, although large standard errors mean that we cannot rule out modest treatment

effects in either direction.

While these intent-to-treat estimates show that a more generous repayment program increases

debt repayment and decreases bankruptcy, they do not allow us to identify the separate impact of

debt write-downs and lower minimum payments — the parameters that are most relevant to both

economic theory and policy. Ideally, the experiment would have provided different debt modifi-

cations to different, randomly selected individuals. Some borrowers could have been offered debt

write-downs, but not lower minimum payments. Other borrowers could have been offered lower

minimum payments, but not debt write-downs. In this scenario, we could identify the separate im-

pact of debt write-downs and lower minimum payments by comparing the intent-to-treat estimates

2

across these different treatment groups. However, this experimental design was not feasible for the

non-profit credit counselor implementing the experiment.

We therefore develop an empirical design that identifies the separate impact of each treatment

using the combination of the randomized experiment and the significant across-borrower variation

in potential treatment intensity in our data; that is, the hypothetical write-down and minimum

payment treatments that each borrower in our sample would have received if they had been assigned

to the treatment group. Potential treatment intensity varies across borrowers in our data because

each of the eleven credit card issuers participating in the experiment offered a different combination

of treatments, and because borrowers varied in their propensity to borrower from each of these

credit card issuers. We measure these borrower-specific treatment intensities using detailed data

from the non-profit credit counselor to calculate the difference between each borrower’s hypothetical

treatment and hypothetical control repayment program offers. We then isolate the effects of the

debt write-down and minimum payment treatments by comparing the impact of the randomized

experiment across borrowers that differed in their potential treatment intensity. While our research

design is not a pure experiment (as potential treatment intensity is not randomly assigned to

borrowers), the randomization of treatment eligibility combined with highly accurate measures of

potential treatment intensity allows us to avoid the most likely threats to causal inference.3

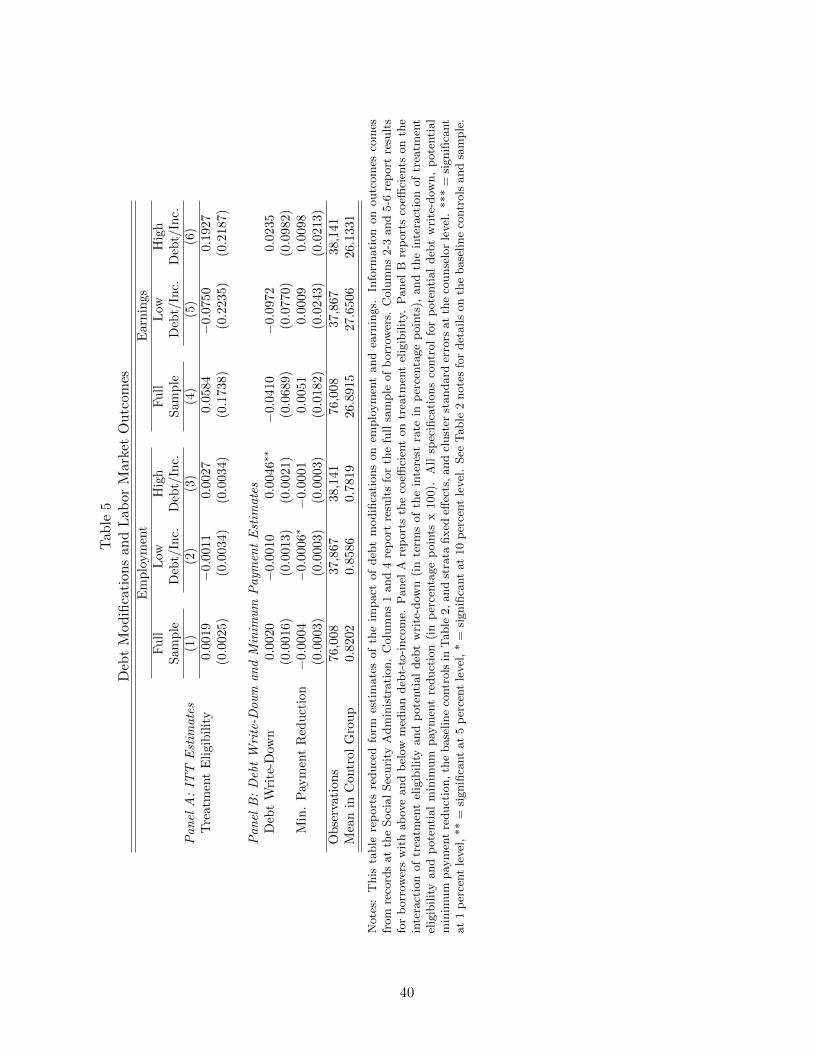

Using this empirical design, we find that the debt write-down treatment had an economically

and statistically large effect on most outcomes. For high debt-to-income borrowers, the median

write-down increased the probability of finishing a repayment program by 2.51 percentage points, a

16.91 percent increase from the control mean, and decreased the probability of filing for bankruptcy

in the first five years by 1.37 percentage points, a 9.64 decrease from the control mean. Employ-

ment over the same time period also increased by 1.70 percentage points for high debt-to-income

borrowers, a 2.17 percent increase from the control mean. The estimated effects for earnings and

401k contributions are small and not statistically significant for most borrowers, however.

In sharp contrast, there were no economically or statistically significant effects of the minimum

payment treatment. There was no discernible effect of the minimum payment treatment on debt

repayment, with the 95 percent confidence interval ruling out treatment effects larger than 0.15

percentage points. The median treatment also increased the probability of filing for bankruptcy by

a statistically insignificant 0.70 percentage points, a 6.76 percent increase from the control mean.

There were also no detectable effects of the minimum payment treatment on employment, earnings,

or 401k contributions for any borrowers in our sample.

In the final part of the paper, we use a simple economic model to explore the possible mech-

anisms driving our reduced form results. The model clarifies that the write-down and minimum

3Our empirical strategy is closely related to earlier work using the interaction of state or federal law changes withstate- or individual-level variation in treatment intensity. For example, Card (1992) estimates the impact of minimumwage laws on wages, employment, and education using across-state variation in the fraction of workers earning lessthan a new federal minimum wage. Similarly, Currie and Gruber (1996) estimate the impact of health insuranceeligibility on health care utilization and child health using across-state and across-group variation in the number ofchildren eligible for Medicaid. However, in contrast to these earlier studies, the treatment and control groups in oursetting are determined by random assignment.

3

payment treatments can affect repayment rates through three distinct channels: (1) by decreasing

forward-looking defaults early in the repayment program through the promise of future debt relief,

(2) by decreasing liquidity-based defaults through a lower minimum payment, and (3) by either

decreasing or increasing exposure to default risk at the end of the experiment through either a

shorter or longer repayment program. We then use the model to show that it is possible to test the

relative importance of these competing channels using treatment effects at different points during

the repayment program.

Surprisingly, we find that the effects of the write-down treatment on debt repayment are largely

explained by forward-looking behavior. Taken at face value, our point estimates suggest at least

85.1 percent of the effect of debt write-downs on repayment can be explained by forward-looking

decisions made early in the repayment program. While we are unable to distinguish between the

different types of forward-looking behavior that could be driving our results, these results stand in

stark contrast to the widespread view that distressed credit card borrowers are completely present-

focused.

We also find that the minimum payment treatment modestly decreased liquidity-based defaults

early in the repayment program. However, the positive short-run effect of increased liquidity is

nearly exactly offset by the negative long-run effect of exposing borrowers to more default risk.

The net effect of a lower minimum payment on debt repayment is therefore a statistical zero.

These results help to reconcile our reduced form estimates with a large literature documenting

liquidity constraints in a variety of settings (e.g. Gross and Souleles 2002, Johnson, Parker, and

Souleles 2006, Agarwal, Souleles, and Liu 2007, Parker et al. 2013, Agarwal et al. 2015). We view

our findings as being consistent with this literature, while suggesting that lower minimum payments

are an ineffective way to address liquidity constraints in the credit card market.

Our results are also related to an important literature examining the effect of loan modifica-

tions in the mortgage market. Agarwal et al. (2012) show that mortgage modifications made

through HAMP modestly decreased both mortgage and non-mortgage defaults, although it is un-

clear whether the effects were driven by lower interest rates, principal reductions, or repayment

period extensions.4 Similarly, recent work shows that anticipated mortgage interest rate reductions

during this time period decreased mortgage defaults and increased non-durable consumption (e.g.

Di Maggio, Kermani, and Ramcharan 2014, Keys et al. 2014, Fuster and Willen 2015), although

it is again unclear whether the effects were driven by a lower minimum payment or a lower debt

burden. There are also a number of differences between the secured and unsecured debt markets

that make it difficult to generalize results across these settings. For example, it is possible that liq-

uidity constraints may be relatively more important for mortgage debt, where delinquent borrowers

often have to choose between repayment or foreclosure, while strategic concerns may dominate for

unsecured credit card debt, where borrowers also have the option of filing for bankruptcy (e.g.

4Cross-sectional regressions suggest that principal forgiveness is more effective than other types of mortgagemodifications (Haughwout, Okah, and Tracy 2010), and recent theoretical work suggests that mortgage paymentdeferrals are likely to increase mortgage defaults unless paired with some sort of debt relief (Eberly and Krishnamurthy2014).

4

Mahoney 2015).

Our results are also related to recent work estimating the effects of consumer bankruptcy pro-

tection, which combines elements of both debt relief and debt restructuring for unsecured debts.

Exploiting the random assignment of bankruptcy filings to judges, Dobbie and Song (2015) and

Dobbie, Goldsmith-Pinkham, and Yang (2015) show that bankruptcy protection increases earn-

ings and decreases financial distress, respectively. There is also evidence that the availability of

consumer bankruptcy as an outside option provides implicit health (Gross and Notowidigdo 2011,

Mahoney 2015) and consumption insurance (Dobbie and Goldsmith-Pinkham 2014) to distressed

borrowers, and that filing rates respond to financial incentives (Fay, Hurst, and White 2002). How-

ever, none of these papers are able to identify the mechanisms through which debt relief or debt

restructuring benefits debtors.

There is also a substantial literature on consumer debt more generally. For example, recent

work shows that debt overhang can affect labor supply (Bernstein 2016), entrepreneurial activity

(Adelino, Schoar, and Severino 2013), and home investment (Melzer forthcoming), and that loan

demand is sensitive to interest rates in the credit card (Gross and Souleles 2002), home equity

(Bhutta and Keys 2014), and mortgage markets (DeFusco and Paciorek 2014); to the down payment

amount in the auto loan market (Adams, Einav, and Levin 2009); and to the available loan amount

in the payday loan market (Dobbie and Skiba 2013). There is also work showing that both savings

and borrowing can be affected by the presence of social insurance programs (e.g. Hurst and Ziliak

2006, Hurst and Willen 2007) and by the race of the borrower (e.g. Charles and Hurst 2002,

Charles, Hurst, and Stephens 2008). See Zinman (2015) for a detailed review of the literature.

The remainder of this paper is structured as follows. Section I describes the institutional setting

and experimental design. Section II provides a simple conceptual framework for interpreting the

experimental results. Section III describes our data and empirical design. Section IV presents our

main results of how the randomized experiment affected debt repayment, bankruptcy, labor market

outcomes, and savings. Section V explores the potential mechanisms driving our results. Section

VI concludes.

I. Background and Experimental Design

A. Background

The randomized experiment described in this paper was implemented by Money Management

International (MMI), the largest non-profit credit counseling agency in the United States. In the

early 1950s, credit card issuers helped establish the first non-profit credit counseling organizations

to increase recovery rates and decrease the number of new bankruptcy filings. Today, non-profit

credit counseling organizations such as MMI provide a wide range of services to its clients via phone

and in-person sessions, including general financial advice, credit counseling, bankruptcy counseling,

and housing counseling.

One of the most important products offered by non-profit credit counselors is the debt manage-

5

ment plan (DMP), a structured repayment program that simultaneously repays all of a borrower’s

outstanding credit card debt over three to five years.5 Under the DMP, the credit counseling agency

negotiates directly with each of the borrower’s creditors to lower the minimum payment amount

and partially write-off interest payments and late fees. In most cases, creditors will also agree to

stop recording the debt as delinquent on the borrower’s credit report. The borrower then makes

one monthly payment to the counseling agency that is disbursed to his or her creditors according

to the terms of the restructured agreements. The minimum payment for each credit card account is

typically about two to three percent of the original balance, although borrowers can make additional

payments to reduce the length of the repayment program. In our sample, the average minimum

payment for the control group is 2.38 percent of original balance, or about $437 per month. The

average length of repayment programs for the control group is 52.7 months.

Creditors will usually allow borrowers to resume a repayment program if they miss just one or

two payments. However, if a borrower misses too many payments or withdraws from the program,

the remaining credit card debt is usually sent to collection. At this point, either the original

creditor or a third-party debt collector will use a combination of collection letters, phone calls,

wage garnishment orders, and asset seizure orders to collect the remaining debt. Borrowers can

make these collection efforts more difficult by ignoring collection letters and calls, changing their

telephone number, or moving without leaving a forwarding address. Borrowers can also leave

the formal banking system to hide their assets from seizure, change jobs to force creditors to

reinstate a garnishment order, or work less so that their earnings are not subject to garnishment.

Most borrowers also have the option of discharging the remaining credit card debt through the

consumer bankruptcy system. In all of these scenarios, however, borrowers’ credit scores are likely

to deteriorate significantly, at least in the short run.

The costs of administering the DMP are covered by a combination of a small administrative

fee of about $10 to $50 paid by the borrower, and a “fair share” payment paid by the credit card

issuers. Fair share payments have become somewhat less generous over time, falling from an average

of twelve to fifteen percent of the recovered debt in the 1990s, to about five to ten percent of the

recovered debt today (Wilshusen 2011). To the best of our knowledge, both the fair share payments

and administrative fees remained relatively constant throughout the experiment.

To help ensure that creditors benefit from their participation in the repayment program, the

counseling agency screens potential clients to make sure that (1) the borrower has a sufficient cash

flow to repay his or her debts over the three to five year period of the repayment program, and (2)

that the borrower cannot reasonably repay his or her debts without a repayment program. Histor-

ically, creditors have given credit counseling agencies the incentive to effectively screen potential

clients through a combination of monitoring and the fair share payments discussed above. To

strengthen the counseling agencies’ incentive to effectively screen clients, many creditors also con-

5Under current regulatory guidelines, the term length for a DMP cannot exceed five years. If borrowers cannotfully repay their credit card debts within this five year limit, they cannot participate in a DMP unless the creditor iswilling to write off a portion of the original balance and recognize the loan as impaired. To date, however, creditorshave typically been unwilling to do this (Wilshusen 2011).

6

dition their fair share payments on the borrower’s completion of the repayment program (Wilshusen

2011).

Creditor participation in a DMP is voluntary, and creditors may choose to participate in only

a subset of the DMPs proposed by the credit counseling agencies. In principle, a creditor will only

participate in a repayment program if doing so increases the expected repayment rate, presumably

because the borrower is likely to default or file for bankruptcy (Wilshusen 2011).6 Creditors can

also directly refer borrowers to a credit counseling agency if the risk of default or bankruptcy is

particularly high. In our sample, approximately 15.5 percent of individuals report that they learned

about MMI from a creditor. In comparison, 33.7 percent of individuals in our sample report that

they learned about MMI from an internet search, 19.8 percent from a family member or friend,

and 20.0 percent from a paid advertisement.

Each year, MMI administers over 75,000 DMPs that repay nearly $600 million in unsecured debt.

Nationwide, it is estimated that non-profit credit counselors administer approximately 600,000

DMPs that repay unsecured creditors between $1.5 and $2.5 billion each year (Hunt 2005, Wilshusen

2011).

B. Experimental Design

Overview: In 2003, MMI and eleven large credit card issuers agreed to offer lower minimum pay-

ments and new debt write-downs to a subset of borrowers interested in a structured repayment

program. The purpose of the experiment was to evaluate the effect of more borrower-friendly

terms on repayment rates, particularly for the most financially distressed borrowers.

The resulting randomized experiment was conducted between January 2005 and August 2006.

The experimental population consisted of the approximately 80,000 prospective clients that con-

tacted MMI during this time period. The experiment only included individuals contacting MMI

for the first time during this time period; individuals who had already enrolled in a DMP before

January 2005 were excluded from the randomized trial. Individuals working with counselors with

less than six months of experience were also excluded from the experiment.

Sequence of the Experiment: First, each prospective client was randomly assigned to a credit

counselor conditional on the contact date, the client’s state of residence, and the reference type

(i.e. web vs. phone). For each counselor, the MMI computer system would automatically switch

from the control group concessions to the treatment group concessions every two weeks. This

automated rotation procedure was meant to ensure that experimental procedures were followed by

the counselors, and to ensure that any counselor-specific effects would not bias the experiment.

Counselors were also strictly instructed not to inform prospective clients about the experiment. A

senior credit counselor conducted frequent audits of the counselors to ensure that the experimental

procedures were followed, and that the treatment and control populations remained relatively

6Consistent with this view, individuals enrolled in a DMP are less likely to file for bankruptcy (Staten and Barron2006) and less likely to report financial distress (O’Neill et al. 2006) than observably similar individuals who are notenrolled in a DMP.

7

similar. MMI worked with the participating credit card issuers to design the automated rotation

procedure, but none of the issuers were directly involved with the implementation of the experiment

or the auditing process.

Following the assignment of an individual to a counselor, the assigned counselor collected in-

formation on the prospective client’s unsecured debts, assets, liabilities, monthly income, monthly

expenses, homeownership status, number of dependents, and so on. Identical information was

collected from both the treatment and control groups, and there was no indication of treatment

status communicated to the prospective clients. Using the information collected by the counselor,

the MMI computer system would then calculate the terms of the individual’s repayment program,

including the minimum payment amount, the length of the program, and the total financing costs.

These terms depended on the individual’s specific credit card debts, and whether the individual

was assigned to the treatment or control group.

Next, the credit counselor would explain the individual’s options for repaying his or her debts.

The details of this process closely followed MMI’s usual procedures, and were identical for the

treatment and control groups.7 In most cases, the repayment options were explained in the following

way. First, individuals were told that they could liquidate their assets and repay their debts

immediately, although relatively few individuals in our sample had enough assets to make this a

viable option. Next, individuals were told that they could file for Chapter 7 bankruptcy, which

would allow them to discharge their unsecured debts and avoid debt collection in exchange for any

non-exempt assets and the required court fees. Third, individuals were told what would happen

if they continued paying only the minimum payment on their credit cards. In a representative

call provided to the research team, the MMI counselor explained that “if you continue making the

minimum payment of $350, it will take you 348 months to repay your credit cards, and you will

have to spend about $21,300 in financing charges.” Finally, individuals were told about the benefits

of enrolling in a structured repayment program. In the same representative call, the MMI counselor

explained that if the individual enrolled in a DMP, her payments would “drop to $301, you would

repay all of your credit cards in 56 months, and only have $3,800 in financing charges. That is a

savings of about $17,500.”

Following the counselor’s explanation of the repayment options, the individual would then

indicate whether or not to enroll in the offered repayment program. Individuals could also call

back at a later date to enroll in the repayment program under the same terms.

Treatment Intensity: Compared to control borrowers, treated borrowers were offered repayment

programs with some combination of (1) larger debt write-downs to address any long-run debt

overhang concerns, and (2) lower minimum payments to address any short-run liquidity constraints.

7The internal validity of the experiment is not affected by the details of this procedure, as the framing of therepayment options was identical for treated and control borrowers. Of course, the effects of the two treatments maybe mediated through the specific way the DMP terms were presented to borrowers. For example, it is possible thatindividuals view a debt debt write-down as being more valuable if it is framed as a financing fee reduction. It is alsopossible that individuals view a given treatment as more or less valuable after being told about their outside options.All of our results should be interpreted with these potential framing issues in mind.

8

Table 1 provides an illustrative example of how each treatment could have impacted the typical

borrower’s repayment program. Each row presents DMP terms for a hypothetical borrower with

the mean amount of credit card debt ($18,212), minimum payment requirements (2.38 percent of

initial debt), and interest rate (8.50 percent). We first calculate the DMP terms for the hypo-

thetical borrower under the control conditions. We then recalculate the DMP terms applying the

median write-down treatment (a 3.69 percentage point decrease in the implied interest rate), and

then applying the median minimum payment treatment (a 0.14 percentage point decrease in the

minimum payment percentage).

For this hypothetical borrower, the control repayment program would have required a minimum

payment of $433.45 for 50.05 months, with the financing fees totaling $3,482. The median write-

down treatment would have decreased these financing fees by an additional $1,712, or 49.17 percent,

by dropping the last four payments of the borrower’s repayment program. Importantly, however,

the write-down treatment would not have affected the borrower’s minimum payment amount. As

a result, the treatment should only increase enrollment in the repayment program if borrowers

value debt forgiveness at the end of the repayment program, about three to five years in the

future. The treatment could also increase the probability of completing the repayment program by

mechanically reducing the treatment group’s default rates to zero during the approximately four

month time period when their payments are forgiven.

Conversely, the median minimum payment treatment would have decreased the hypothetical

borrower’s minimum payment by an additional $26.68, or 6.15 percent, by adding an additional

four months to the repayment program. The longer repayment period also would have increased the

financing fees for this borrower by $289, or 8.30 percent. Thus, the minimum payment treatment

should decrease liquidity-based defaults at the beginning of the repayment program by lowering the

minimum payment amount, but increase defaults at the end of the repayment program by increasing

the exposure to default risk. This implies that the net effect of the minimum payment treatment

depends on the relative importance of short-run liquidity constraints and long-run default risk.

The example from Table 1 describes the impact of the median write-down and minimum pay-

ment treatments. In practice, however, there is considerable variation in treatment intensity due to

the different combination of the write-down and minimum payment treatments offered by the eleven

credit card issuers participating in the experiment (see Appendix Table 1). For example, three card

issuers only offered write-down treatment, with all three choosing a different write-down intensity.

While none of the participating issuers offered the minimum payment reduction, one credit card

issuer offered the smallest write-down (i.e. a 4.0 percentage point decrease in the implied interest

rate) and the largest minimum payment reduction (i.e. a 0.5 percentage point decrease in the

minimum payment percentage). In total, seven different combinations of the two treatments were

offered by participating issuers.

Individuals also varied in their propensity to borrow from each of these card issuers, leading

to even more variation in the potential write-down and minimum payment treatments offered to

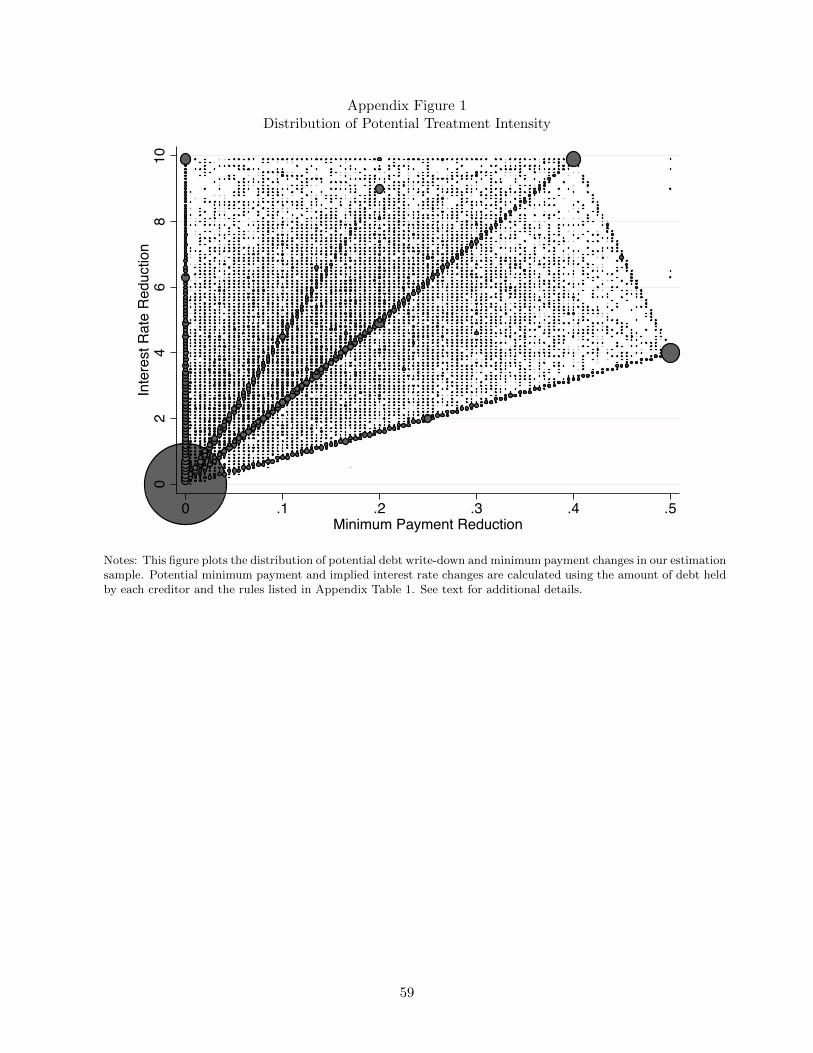

borrowers. Appendix Figure 1 plots potential treatment intensity for every borrower in our sample.

9

The data reveal significant independent across-borrower variation in the both the write-down and

minimum payment treatments. For example, only 30 percent of borrowers have potential write-

down and minimum payment treatments that are both above the median. Nineteen percent of

borrowers only have an above median potential write-down treatment, and 9.9 percent only have an

above median potential minimum payment treatment. The remainder of the sample have potential

write-down and minimum payment treatments that are both below the median. In total, there

are nearly 50,000 different unique combinations of potential write-down and minimum payment

treatments in our sample.

To illustrate the magnitude of the across-borrower variation in dollar terms, we recalculate the

DMP terms for the hypothetical borrower from Table 1 with various treatment intensities. This

exercise reveals that, for the hypothetical borrower described above, the 75th percentile write-

down treatment is $1,521 larger than the 25th percentile write-down treatment. In other words,

the difference between the 75th and 25th percentile treated borrowers is nearly as large as the

difference between treated and control borrowers at the median. Similarly, the 75th percentile

minimum payment treatment is $33 larger than the 25th percentile minimum payment treatment,

or more than double the difference between treated and control borrowers at the median. In Section

III.C, we explain how we use this variation in treatment intensity to estimate the separate effects

of each treatment.

II. Conceptual Framework

This section develops a simple economic model to better understand the randomized experiment.

The model highlights two broad forms of default risk that may influence borrower behavior: (1)

strategic, forward-looking default risk from debt overhang and (2) non-strategic, liquidity-based

default risk from potentially binding liquidity constraints. We do not attempt to model every

possible mechanism that could affect debt repayment, such as whether the forward-looking default

decisions are due to strategic default or moral hazard in repayment effort. We also do not attempt

to separate these more subtle types of mechanisms empirically. The conclusions we draw in this

section should be interpreted with these modeling choices in mind.8

The model shows how the promise of a future debt write-down increases repayment by (1)

decreasing individuals’ incentive to strategically default at the beginning of the experiment through

increased solvency, and (2) by decreasing individuals’ exposure to default risk at the end of the

experiment through a shorter repayment period. In contrast, a lower minimum payment has an

ambiguous impact on repayment rates due to two competing channels: (1) a decrease in non-

strategic default and an ambiguous change in strategic default at the beginning of the experiment

8A large literature examines the causes and consequences of individual default using quantitative models of thecredit market. For example, see Chatterjee et al. (2007) for a general model of consumer default, and Benjamin andMateos-Planas (2014) for a model that distinguishes between formal and informal consumer default. There is also anemerging literature that estimates the separate impact of different forms of hidden information and hidden action.See Adams et al. (2009) and Karlan and Zinman (2009) for examples of these approaches using observational andexperimental data, respectively.

10

through increased liquidity, and (2) an increase in exposure to default risk at the end of the

experiment through a longer repayment period.

A. Model Setup

We omit individual subscripts from the model parameters to simplify notation. Individuals are risk

neutral and maximize the present discounted value of disposable income at a subjective discount

rate β. In each period t, individuals receive earnings yt = µ + εt, where ε are i.i.d. shocks drawn

from a known mean zero distribution f(ε) and µ is assumed to be both known and positive. Debt

payments begin at t = 0 and are set at a constant level d for the repayment program of length P ,

so that dt = d for t ≤ P and dt = 0 for t > P .

In each time period 0 ≤ t ≤ P , individuals observe their income draw yt and decide whether

to make the required debt payment d or default on the remaining debt payments. If an individual

defaults on the remaining payments in period t for any reason, she loses her current income draw yt

and receives a constant amount x in period t and all future time periods. To capture the idea of a

potentially binding liquidity or credit constraint, we assume that individuals automatically default

if net income yt − dt falls below threshold v , regardless of the value of future cash flows.

Let V q(t, y) denote the continuation value of making repayment decision q in period t given

income draw y. For periods 0 ≤ t < P , the continuation value of default V d(t, y) is equal to the

discounted value of receiving x in both the current period and all future periods:

V d(t, y) =x

1− β(1)

The continuation value of repayment V r(t, y) consists of the contemporaneous value of repayment

y − d and the option value of being able to either repay or default in future periods:

V r (t, y) = y − d+ β

[∫ ∞v+d

max{V r(t+ 1, y

′), V d(t, y)

}dF(y′)

+ F (v + d)V d(t, y)

](2)

The contemporaneous value of repayment y − d is unaffected by the time period t, while the

option value of continuing repayment, and hence the total value of continuing repayment, is weakly

increasing in t for t < P . This is because the option value of repayment increases as individuals

become closer to the “risk-free” time periods after the completion of the repayment program.

Repayment and default behavior is described by a path of cutoff values φt, where an individ-

ual defaults if yt < φt. The default cutoff φt combines the optimal strategic response of liquid

individuals to low income draws and the non-strategic response of illiquid individuals based on v

that may or may not be optimal. Following the above logic, the strategic default cutoff is weakly

decreasing over time, reflecting the decreased incentive to default as individuals’ remaining loan

balances shrink. Appendix A provides additional details on the derivations of the above results.

The reduced form treatment effects documented below likely combine a number of these po-

tential channels. In Section V, we provide a more tentative discussion of which of these broad,

11

competing channels are most important empirically.

B. Model Predictions

Motivated by the experiment, we consider the comparative statics of the write-down and minimum

payment treatments on debt repayment.

Debt Write-Down Prediction: In the model, the write-down treatment increases debt repay-

ment through two complimentary effects: (1) a decrease in treated individuals’ incentive to strate-

gically default while both treatment and control individuals are enrolled in the repayment program,

and (2) a decrease in treated individuals’ exposure to default risk while control individuals are still

enrolled in the repayment program and treatment individuals are not.

Proof – See Appendix A.

Recall that the write-down treatment decreased treated borrowers’ financing charges by short-

ening the repayment period and holding the minimum payment constant. In other words, the

write-down treatment forgave treated borrowers’ monthly payments at the end of the structured

repayment program. As a result, the treatment will increase debt repayment to the extent that

borrowers value debt forgiveness three to five years in the future. Conditional on enrolling in the

program, it is also possible that the write-down treatment will increase the probability of finishing

repayment by decreasing exposure to default risk at the end of the repayment program. This is

because the write-down treatment makes it impossible for treated borrowers to default when their

payments have been forgiven.

Formally, let dWD and PWD denote the monthly debt payment d and repayment period P for

the write-down treatment WD, and dC and PC denote the monthly debt payment and repayment

period for the control group C. In the context of the model, the write-down treatment reduced the

overall cost of the debt by shortening the repayment period for treated individuals relative to control

group individuals, PWD < PC , without changing the monthly debt payments dWD = dC = d. For

0 ≤ t ≤ PWD, shortening the length of the repayment period brings individuals in any given period

PC − PWD periods closer to finishing the repayment program, increasing the expected value of

continuing the repayment program. This increase in the expected value of repayment decreases the

strategic, forward-looking default cutoff for liquid individuals during this time period. However,

disposable income for 0 ≤ t ≤ PWD remains the same, so there is no difference in the probability

that a individual defaults due to the liquidity constraint v during this time period. In other words,

there will only be an increase in repayment for 0 ≤ t ≤ PWD if the forward-looking default cutoff

is the relevant margin for at least some individuals.

For PWD < t ≤ PC , default rates mechanically drop to zero for treated individuals as they have

completed the repayment program. However, control individuals can still default on their debt if

either the liquidity-based or forward-looking cutoffs bind over this time period. The write-down

treatment can therefore increase debt repayment even if individuals never strategically default (i.e.

12

if individuals only default due to a binding liquidity constraint) if there is sufficient default risk at

the end of the repayment program. We refer to this channel as the “exposure effect.”

Minimum Payment Prediction: The minimum payment treatment has an ambiguous impact

on repayment rates in the model due to three effects: (1) a decrease in treated individuals’ non-

strategic or liquidity-based default while both treatment and control individuals are enrolled in

the repayment program, (2) an ambiguous change in treated individuals’ incentive to strategically

default while both treatment and control individuals are enrolled in the repayment program, and

(3) an increase in treated individuals’ exposure to default risk while treated individuals are still

enrolled in the repayment program and control individuals are not.

Proof – See Appendix A.

The minimum payment treatment reduced borrowers’ minimum payment by increasing the

length of the repayment program. In the model, the minimum payment treatment therefore de-

creases liquidity-based defaults at the beginning of the repayment program through the lower re-

quired payments, but increases defaults at the end of the repayment program through the increased

exposure to all forms of default risk. In addition, the minimum payment treatment changes the

option value of repayment, and hence the incentive to strategically default. The direction of this

strategic effect is ambiguous as the minimum payment treatment both increases future flexibility

and transfers a portion of the debt burden into the future.

Formally, let dMP and PMP denote the monthly debt payment d and repayment period P for the

minimum payment treatment MP . We model the minimum payment treatment as a lengthening

of the repayment period from PC to PMP > PC that keeps the total sum of the monthly debt

payments the same∑PC

t=0 dt =∑PMP

t=0 dt. The model therefore implies that the minimum payment

treatment decreases the probability that the non-strategic cutoff binds for illiquid individuals for

0 ≤ t ≤ PC , increasing repayment rates over this time period if the liquidity-based default cutoff

is the relevant margin for at least some individuals.

There is also an effect of the minimum payment treatment on the incentive to strategically

default for 0 ≤ t ≤ PC . However, the direction of this effect is ambiguous, as the minimum payment

treatment both decreases per-period repayment costs, increasing the option value of repayment, and

increases the number of periods to repay, decreasing the option value of repayment. These opposing

effects on the option value of repayment are not unique to the minimum payment treatment; other

policies that target liquidity constraints such as payment deferrals or higher credit limits will also

exhibit these kinds of opposing effects. We therefore think of the “liquidity effect” as including both

the direct effects on liquidity-based defaults discussed above, and the indirect effects on the option

value of repayment discussed here. We assume throughout that the liquidity effect net of these two

channels is positive, although the basic results of the model do not rely on this assumption.

Finally, for PC < t ≤ PMP , default rates mechanically drop to zero for control individuals,

while treated individuals can still default on their debt if either the liquidity-based or strategic

cutoffs bind over this time period. This exposure effect allows for the possibility that the minimum

13

payment treatment will have a negative effect on repayment rates.

III. Data and Empirical Design

A. Data Sources and Sample Construction

To estimate the impact of the randomized treatments, we match counseling data from MMI to

administrative tax and bankruptcy records. This section describes the construction and matching

of each dataset.

The counseling data provided by MMI include information on all prospective clients eligible

for the randomized trial. The data include detailed information on each individual’s unsecured

debts, assets, liabilities, monthly income, monthly expenses, homeownership status, number of

dependents, treatment status, enrollment in a repayment program, and completion of a repayment

program. The data also include information on the date of first contact, state of residence, who

referred the individual to MMI, the assigned counselor, and an internal risk score that captures the

probability of finishing a repayment program. We normalize the risk score to have a mean of zero

and standard deviation of one in the control group and top-code all other continuous variables at

the 99th percentile.

We use the data provided by MMI to calculate potential treatment intensity for each individual

in our sample. Recall that there is significant variation in potential debt write-down and minimum

payment treatments as a result of the participating issuers offering different concessions to treated

borrowers. To measure this variation in treatment intensity, we first calculate the write-downs and

minimum payments for all individuals as if they had been assigned to the control group and as

if they had been assigned to the treatment group. In this step, we use the exact calculation that

MMI uses, repeating this calculation under both the control and treatment scenarios. We then

calculate the difference between the control write-downs and the treatment write-downs (in terms

of the implied interest rate) for each individual, and the control minimum payment and treatment

minimum payment (in terms of percent of the original balance) for each individual. These write-

down and minimum payment differences are our individual-level measures of potential treatment

intensity. Importantly, we observe virtually all of the same information that MMI uses to calculate

the terms of the structured repayment program.9

Information on bankruptcy filings comes from individual-level PACER bankruptcy records. The

bankruptcy records are available from 2000 to 2011 for the 81 (out of 94) federal bankruptcy courts

that allow full electronic access to their dockets. These data represent approximately 87 percent of

all bankruptcy filings during our sample period.10 We match the credit counseling data to PACER

data using name and the last four digits of the social security number. We assume that unmatched

9Specifically, we have information on interest rates and minimum payments for the nineteen largest creditors inthe sample, including all eleven of the credit card issuers participating in the experiment. For the 16.7 percent of debtholdings held by smaller creditors not participating in the experiment, we assume an interest rate of 6.7 percent anda minimum payment of 2.25 percent. These assumptions follow MMI’s internal guidelines for calculating expectedDMP payments. Results are also robust to a wide range of alternative assumptions.

10See Gross, Notowidigdo, and Wang (2014) for additional details on the bankruptcy data used in our analysis.

14

individuals did not file for bankruptcy protection during the sample period, and control for state

fixed effects in all specifications to account for the fact that we do not observe filings in all states.

We also pool Chapter 7 and Chapter 13 filings throughout the analysis. Results are similar if we

limit the sample to borrowers living in states with PACER data coverage.

Information on formal sector labor market outcomes and 401k contributions comes from ad-

ministrative tax records from the SSA. The SSA data are available from 1978 to 2013 for every

individual who has ever acquired a SSN, including those who are institutionalized. Illegal immi-

grants without a valid SSN are not included in the SSA data. Information on formal sector earnings

and employment and annual 401k contributions come from annual W-2s.11 The earnings and em-

ployment variables include all formal sector earnings, but do not include earnings from the informal

sector. The 401k variable includes all conventional, pre-tax contributions, but does not include con-

tributions to Roth accounts. Individuals with no W-2 in any particular year are assumed to have

had no earnings or 401k contributions in that year. Individuals with zero earnings or zero 401k

contributions are included in all regressions throughout the paper. We match the credit counseling

data to the tax data using the full social security number. We are able to successfully match 95.3

percent of the counseling data to the SSA data. The probability of being matched to the SSA data

is not significantly related to treatment status (see Panel C of Table 2).

We make two sample restrictions to the final dataset. First, we drop individuals that are not ran-

domly assigned to counselors because they need specialized services such as bankruptcy counseling

or housing assistance. Second, we drop individuals with less than $850 in unsecured debt or more

than $100,000 in unsecured debt to minimize the influence of outliers. These cutoffs correspond

to the 1st and 99th percentiles of the control group, respectively. The resulting estimation sample

consists of 40,496 individuals in the control group and 39,243 individuals in the treatment group.

Our sample for the labor market and 401k outcomes is further restricted to 76,008 individuals

matched to the SSA data.

B. Descriptive Statistics and Experiment Validity

Table 2 presents descriptive statistics for the treatment and control groups. The average borrower

in our sample is just over 40 years old with 2.15 dependents. Thirty-six percent of borrowers are

men, 63.5 percent are white, 17.2 percent are black, and 8.9 percent are Hispanic. Forty-one percent

are homeowners, 44.1 percent are renters, and the remainder live with either a family member or

friend. The typical borrower in our data has just over $18,000 in unsecured debt, with about $9,600

of that debt being held by a credit card issuer participating in the randomized experiment. Monthly

household incomes average about $2,450, and monthly expenses average about $2,150.

Panel B of Table 2 presents baseline outcomes for the year before contacting MMI. Individual

earnings in the SSA data are approximately $23,500, slightly lower than the self-reported household

11The SSA data also include information on mortality and Disability Insurance receipt. Very few individuals inour data die or receive Disability Insurance during our sample period, and estimates for these outcomes are smalland not statistically different from zero.

15

earnings reported in the MMI data. These results suggest that either some individuals in our sample

are not the sole earner in the household, that some individuals have earnings in the informal sector

not captured by the SSA data, or that there is upward bias in the self-reported earnings. Eighty-

five percent of borrowers in our sample are employed in the formal sector at baseline according to

the SSA data. Baseline bankruptcy rates are very low, 0.3 percent, likely because individuals are

unlikely to contact a credit counselor if they have already received bankruptcy protection. Finally,

baseline 401k contributions are $373 for borrowers in our sample.

Panel D of Table 2 presents measures of potential treatment intensity calculated using the MMI

data. Specifically, we calculate the implied interest rate, the minimum payment percentage, and

the program length in months for each borrower as if they had been assigned to the control group

and as if they had been assigned to the treatment group. As would be expected given the random

assignment, the treatment and control groups have similar potential program characteristics. If

assigned to the control group, the typical treated borrower would have had an implied interest rate

of 8.5 percent, a minimum payment of 2.4 percent of the initial balance, and a program length of

just over 52.6 months. Similarly, the typical control borrower actually had an implied interest rate

of 8.4 percent, a minimum payment of 2.4 percent of the initial balance, and a program length

of about 52.7 months. If assigned to the treatment group, those same control borrowers would

have had an implied interest rate of 6.0 percent, a minimum payment of 2.3 percent of the initial

balance, and a program length of 51.9 months, nearly exactly the program characteristics that the

treatment group actually had.

Column 3 of Table 2 tests for balance. We report the difference between the treatment and

control group controlling for state by reference group by date fixed effects — the level at which

prospective clients were randomly assigned to counselors. Standard errors are clustered at the

counselor level. The means of all of the baseline and treatment intensity variables in Panels A-D are

similar in the treatment and control groups. Only one of the 24 baseline differences is statistically

significant at the ten percent level and the p-value from a F-test of the joint significance of all of

the variables listed is 0.807, suggesting that the randomization was successful.12

Finally, Panel E of Table 2 presents measures of the actual program characteristics offered to

borrowers in the treatment and control groups (i.e., the “first stage” of the experiment). Consistent

with the results from Panel D, treated borrowers have implied interest rates that are 2.6 percentage

points lower than control borrowers, minimum payments that are 0.1 percentage points lower, and

program lengths that are 0.8 months shorter.

12Appendix Table 2 presents additional tests for balance. Following our main specification described below,we regress each baseline variable in Panels A-D on the interaction of treatment eligibility and potential treatmentintensity. All regressions control for potential treatment intensity and strata fixed effects, and cluster standarderrors at the counselor level. We find no statistically significant relationships between our baseline measures and theinteraction of treatment eligibility and potential treatment intensity, further suggesting that the randomization wassuccessful.

16

C. Empirical Strategy

Intent-to-Treat Estimates: We begin our empirical analysis by estimating the impact of treatment

eligibility using the following reduced form specification:

yit = α0 + α1Treati + α2Xi + ηit (3)

where yit is the outcome of interest for individual i in year t, Treati is an indicator variable equal to

one if individual i was assigned to the treatment group, and Xi is a vector of state by reference group

by date fixed effects that account for the stratification used in the randomization of individuals to

counselors. We also include the individual controls listed in Table 2 and cluster the standard errors

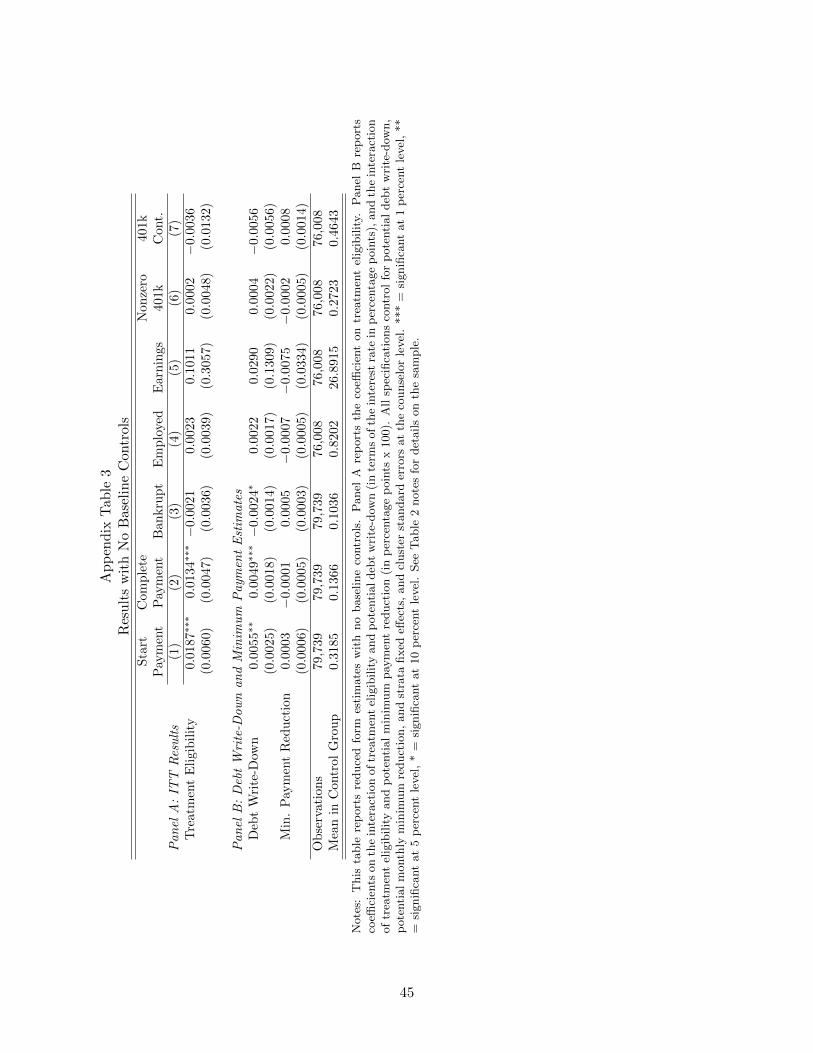

at the counselor level in all specifications. Estimates without individual controls are available in

Appendix Table 3.

Estimates of α1 measure the impact of being offered a more generous repayment program.

However, two important issues complicate the interpretation of these intent-to-treat estimates.

First, treated borrowers were offered a repayment program that included a combination of both the

debt write-down and minimum payment treatments. Thus, the intent-to-treat estimates measure

the combined effect of both treatments, and do not allow us to separately identify the impact of

debt write-downs and lower minimum payments. As a result, it is difficult to extrapolate from the

intent-to-treat estimates to other policies that offer different combinations of debt relief and debt

restructuring.

The second issue is that the intent-to-treat estimates likely understate the true impact of the

debt modifications because of the substantial variation in treatment intensity in our sample. For

example, over 25 percent of borrowers in our sample had zero credit card debt with the eleven credit

card issuers participating in the experiment, and were therefore offered the status quo, or “control”

repayment program even when they were assigned to the treatment group. In total, nearly 90

percent of borrowers received some less intensive treatment than originally intended because they

had at least some credit card debt with a non-participating issuer.

Isolating the Effect of Each Treatment: Ideally, the experiment would have provided different debt

modifications to different, randomly selected individuals to separately identify the effects of debt

write-downs and lower minimum payments. For example, a random subset of borrowers could have

received the write-down treatment, but not the minimum payment treatment. Another random

subset of borrowers could have received the minimum payment treatment, but not the write-down

treatment. In this scenario, we could identify the separate impact of each treatment using the

intent-to-treat estimates for each subgroup. However, this experimental design was not feasible for

MMI.

Our empirical design identifies the separate impact of each treatment using the combination of

the randomized experiment and the across-borrower variation in potential treatment intensity in

our data. Recall that we can measure borrower-specific treatment intensities using detailed data

from the non-profit credit counselor to calculate the difference between each borrower’s hypothetical

17

control and hypothetical treatment repayment program offers. We can then isolate the effects of

write-downs and lower minimum payments using the interaction of the randomized experiment and

these potential treatment intensities. In this specification, we interpret any differences in the effect

of treatment eligibility across borrowers as the independent, causal effect of debt write-downs and

lower minimum payments.

To fix ideas, consider a group of hypothetical borrowers who only borrow from one of two

possible credit card issuers: an issuer that offers treated borrowers only the write-down treatment,

and an issuer that offers treated borrowers both the write-down and minimum payment treatments.

In this simple example, we use the effect of the randomized treatment for borrowers at the first

issuer to identify the impact of the write-down treatment, and the difference between the effects

of the randomized treatment at the second and first issuers to identify the impact of the minimum

payment treatment.

Formally, we define the potential write-down and minimum payment treatment intensities as

the difference between hypothetical treatment and hypothetical control repayment program offers:

∆WriteDowni = WriteDownCi −WriteDownTi

∆Paymenti = PaymentCi − PaymentTi

where ∆WriteDowni is the percentage point difference between the control interest rateWriteDownCiand treatment interest rate WriteDownTi for borrower i, and ∆Paymenti is the percentage point

difference between the control minimum payment percentage PaymentCi and treatment minimum

payment percentage PaymentTi .

We then estimate the effects of the debt write-downs and lower minimum payments using the

following reduced form specification:

yit = β0 + β1Treati ·∆WriteDowni + β2Treati ·∆Paymenti+ β3∆WriteDowni + β4∆Paymenti + β5Xi + εit (4)

We control for any independent effects of ∆WriteDowni and ∆Paymenti because the variation in

these measures may reflect unobserved borrower characteristics that have an independent impact

on future outcomes yit. For example, it is possible that the decision to borrow from card issuers

with particularly high ∆WriteDowni or ∆Paymenti is correlated with risk aversion or financial

sophistication. As will be clear below, our approach does not assume that treatment intensi-

ties are randomly assigned. Rather, we assume that the interaction between treatment eligibility

and potential treatment intensity is conditionally random once we control for ∆WriteDowni and

∆Paymenti. Following the intent-to-treat results, we also include the individual controls listed in

18

Table 2 and cluster the standard errors at the counselor level.13,14

Estimates of β1 and β2 measure the effect of being offered each treatment by comparing the

impact of the randomized experiment across borrowers that differed in their potential treatment

intensities. Our interpretation of the estimates relies on two main assumptions. First, we assume

that treatment eligibility is, in fact, random. As with any non-experimental design, our estimates

will be biased if treatment eligibility is correlated with unobserved determinants of future outcomes

εit. However, this assumption is almost certainly satisfied in our setting, as treatment eligibility is

randomly assigned by the non-profit credit counselor. The balance tests from Table 2 and Appendix

Table 2 are also consistent with random assignment.

Our second identifying assumption is that the interaction of treatment eligibility and (measured)

treatment intensity only impacts borrower outcomes through an increase in (actual) treatment

intensity. Our identifying assumption would be violated if there is measurement error in our

potential treatment intensity variables ∆WriteDowni and ∆Paymenti, and that measurement

error is correlated with unobserved determinants of future outcomes εit. For example, our estimates

would be biased upwards if we systematically overestimate the potential treatment intensity of

borrowers who are most likely to repay their debts even in the absence of the treatment. Fortunately,

we use a nearly identical set of information as the non-profit organization to calculate potential

treatment intensity, making it unlikely that there is the kind of significant measurement error that

would bias our estimates.

Our identifying assumption would also be violated if there is substantial treatment effect het-

erogeneity across borrowers that is correlated with potential treatment intensity. For example,

our estimates would be biased upwards if individuals with a higher LATE from the randomized

treatments were more likely to borrow from the credit card issuers participating in the experiment.

This is because we would attribute the higher estimated effect solely to the higher treatment in-

tensity, not the combination of the higher treatment intensity and the higher LATE. Similarly, our

estimates would be biased downwards if individuals with a lower LATE were more likely to borrow

from the issuers participating in the experiment. These concerns are particularly salient given the

substantial across-borrower dispersion in credit card characteristics documented in prior work (e.g.

Stango and Zinman forthcoming).15

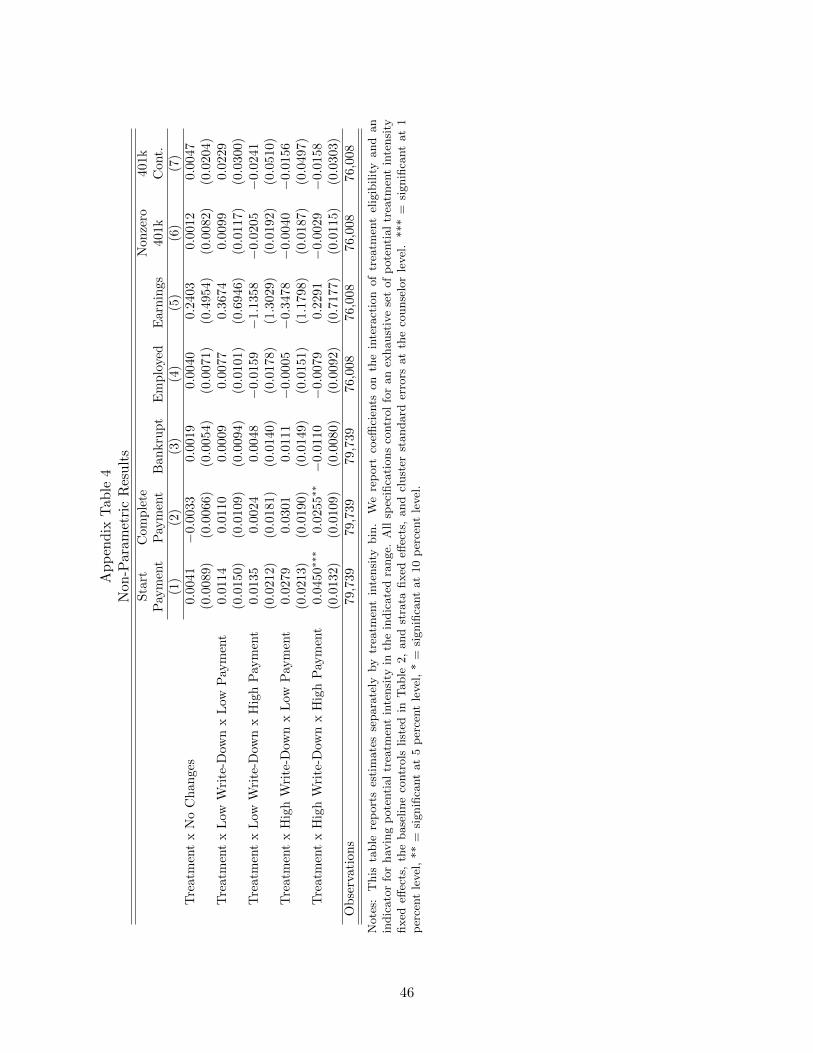

13Equation (4) implicitly assumes that there are no direct effects of treatment eligibility and that the effects of thetwo treatments are linear and additively separable. Consistent with the first assumption, our reduced form results areunchanged when we add an indicator for treatment eligibility. The coefficient on the indicator for treatment eligibilityis also small and not statistically different from zero. To partially test the assumption of linear and additively separabletreatment effects, Appendix Table 4 presents non-parametric estimates using bins of treatment intensity that do notrely on any functional form assumptions. The results are broadly consistent with linear and additively separabletreatment effects, although large standard errors makes a precise test of these assumptions impossible.

14We include all borrowers – including those with no debts with creditors participating in the experiment – whenestimating Equation (4) in order to identify the strata fixed effects. Results are similar if we restrict our sample toindividuals with at least one debt with a participating creditor.

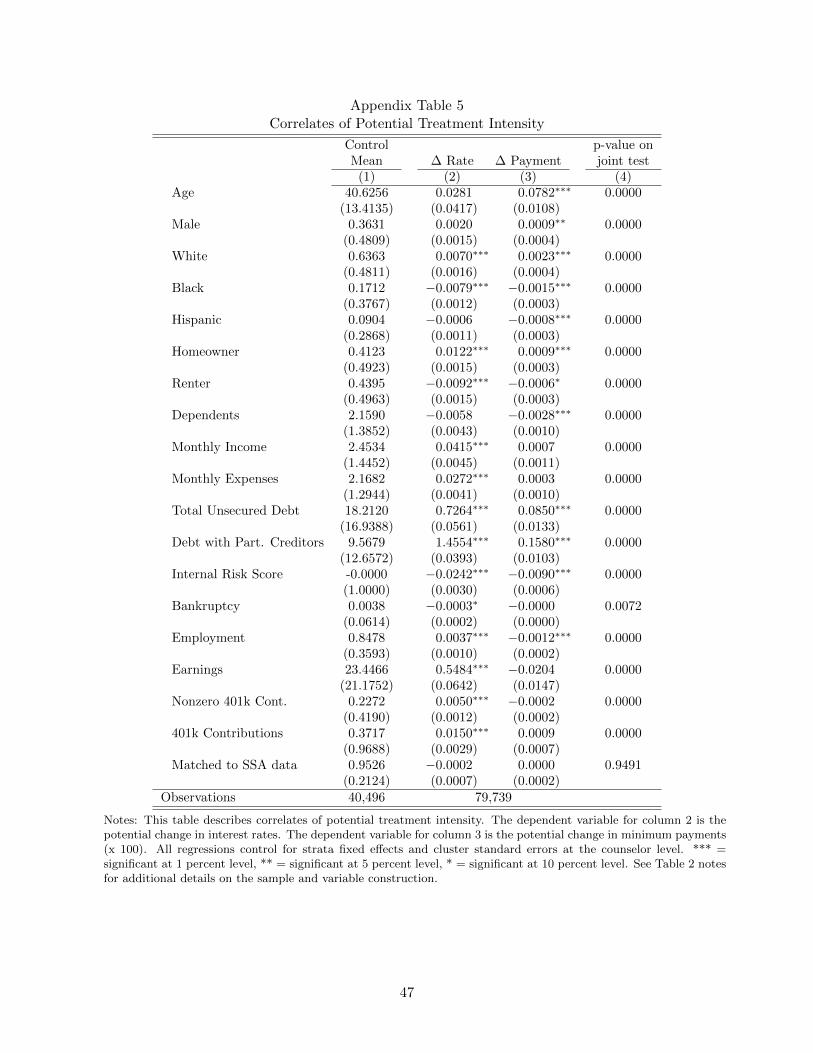

15Appendix Table 5 describes the correlates of potential treatment intensities. Borrowers with larger potentialwrite-down changes are less likely to be black, more likely to be homeowners, and have higher baseline earnings.Borrowers with larger potential minimum payment changes are also less likely to be black, are at lower risk of defaultas measured by MMI’s standardized risk score, and have lower baseline earnings. Not surprisingly, borrowers withmore debt with participating issuers also have larger potential treatment intensities.

19

To partially test the validity of this identifying assumption, Appendix Table 6 examines whether

our potential treatment intensity variables capture all of the relevant variation in the issuer-specific

treatment effects. Our identifying assumption would be violated if there are any significant creditor-

specific treatment effects after we control for the direct effects of treatment intensity. To test this

assumption, we estimate Equation (4) with an additional set of controls for treatment eligibility

interacted with eleven creditor-specific indicator variables equal to one if a borrower has nonzero

debt with the issuer. Consistent with our identifying assumption, the coefficients on the interaction

variables are typically small and not statistically different from zero. In a series of F-tests of the

joint significance of the reported coefficients, the p-values range from 0.369 to 0.986. None of

the results suggest that our identifying assumption is invalid. We will also show below that our

estimates are remarkably similar across gender, race, and homeownership status, suggesting that

our LATEs are relatively similar across observably different borrowers.

Subgroup Analyses: We are also interested in how the effects of the experiment vary across borrower

characteristics such as gender, race, and homeownership. However, we are likely to find a number

of statistically significant estimates purely by chance when performing multiple hypothesis tests.

We were also unable to file a pre-analysis plan, as the experiment was implemented by MMI, and

not the research team. In our main analysis, we therefore restrict ourselves to the single subgroup

analysis suggested by the experimental design: high and low levels of financial distress just prior to

contacting MMI. In the original experimental design, the treatments were only going to be offered

to the most financially distressed borrowers. Following the experiment, many of the credit card

issuers also offered the more borrower-friendly terms only to the most distressed borrowers. To test

how the effects of the experiment differ across this dimension, we estimate effects separately for

borrowers with below and above median debt-to-income. Results are similar if we split borrowers

by debt amount or by the predicted probability of default.16

IV. Results

A. Debt Repayment

Table 3 presents estimates of the impact of being offered larger debt write-downs and lower min-

imum payments on starting and completing a structured repayment program. Panel A reports

intent-to-treat estimates of the impact of treatment eligibility. Panel B reports the coefficient on

treatment eligibility interacted with the potential percentage point change in the implied interest

rate, and treatment eligibility interacted with the potential percentage point change in the required

minimum payment (multiplied by 100). All specifications control for potential treatment intensity,

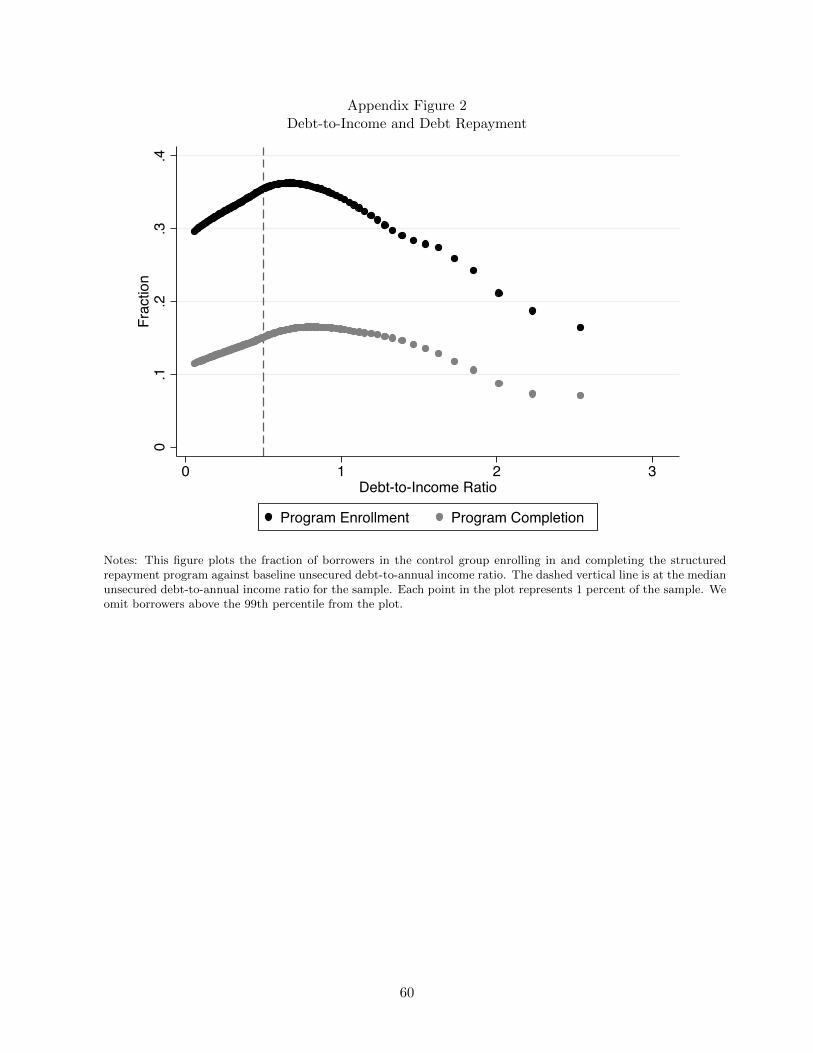

16Unfortunately we do not have information on the measure of financial distress used by credit card issuersfollowing the experiment. The median unsecured debt-to-annual income ratio in our sample is just over 0.5. AppendixFigure 2 plots repayment rates by debt-to-income ratio. Debt repayment is increasing in debt-to-income ratio untilapproximately 0.75, perhaps because relatively more indebted borrowers have more to gain from the repaymentprogram over this range. Debt repayment then decreases monotonically after a debt-to-income ratio of approximately0.75.

20

the baseline controls listed in Table 2, and strata fixed effects. Standard errors are clustered at the

counselor level throughout.

Intent-to-Treat Results: There is an economically and statistically significant effect of treatment

eligibility on debt repayment. Treatment eligibility increased the probability of starting a repayment

program by 1.86 percentage points, a 5.84 percent increase from the control mean of 31.85 percent.

The probability of finishing a repayment program also increased by 1.33 percentage points, a 9.74

percent increase from the control mean of 13.66 percent.

The effects of treatment eligibility are considerably larger for borrowers with above median

baseline debt-to-income, a proxy for financial distress. Treatment eligibility increased the proba-

bility of starting a repayment program by 1.67 percentage points more for borrowers with above

median debt-to-income compared to borrowers with below median debt-to-income. The probability

of finishing the repayment program also increased by 3.27 percentage points more for borrowers

with above median debt-to-income. These results suggest that, consistent with the priors of MMI

and the credit card issuers, the effects of the two treatments were substantially larger for financially

distressed borrowers.

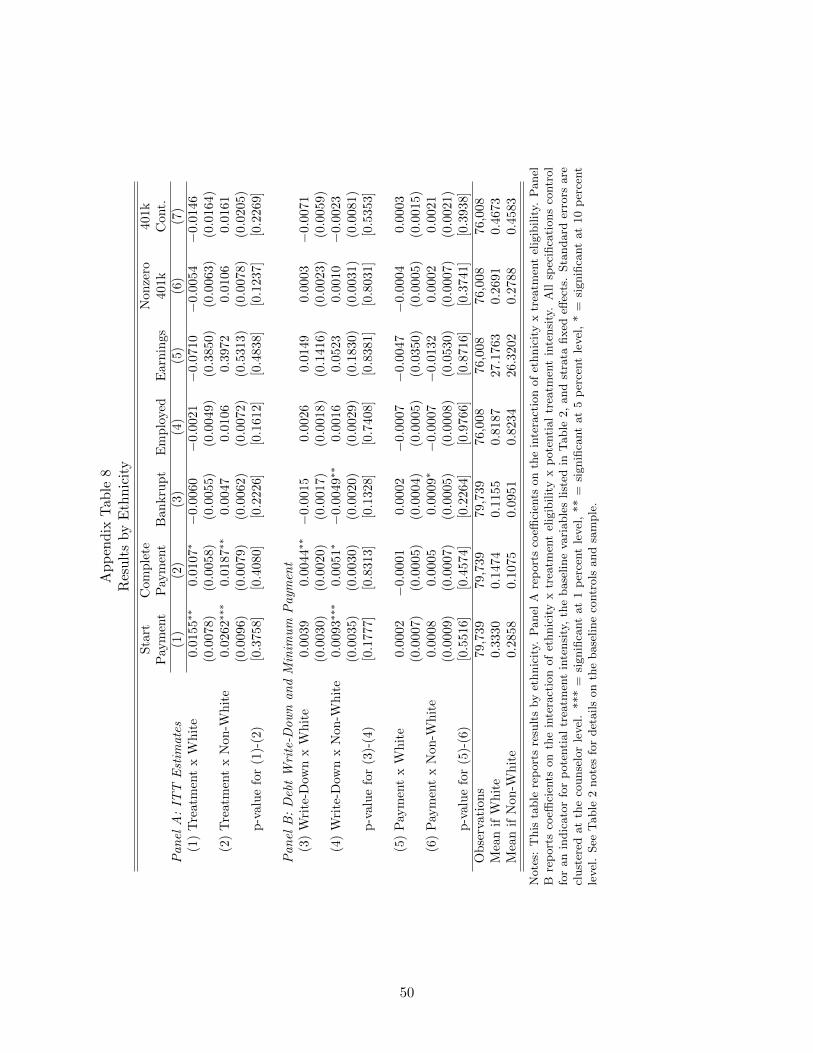

Appendix Tables 7-9 present additional subsample results by gender, ethnicity, and homeowner-

ship. For each of these three subgroups, there are no clear theoretical predictions as to which group

will benefit most from the experiment. We also do not find any evidence that the intent-to-treat

estimates differ across these subgroups.

Debt Write-Down Results: Consistent with the intent-to-treat estimates discussed above, we find

that the write-down treatment had an economically large impact on repayment rates. The median

write-down treatment (i.e. a 3.69 percentage point implied interest rate reduction) increased the

probability of starting a structured repayment program by 1.85 percentage points, a 5.79 percent

increase from the control mean. The probability of finishing the program also increased by 1.62

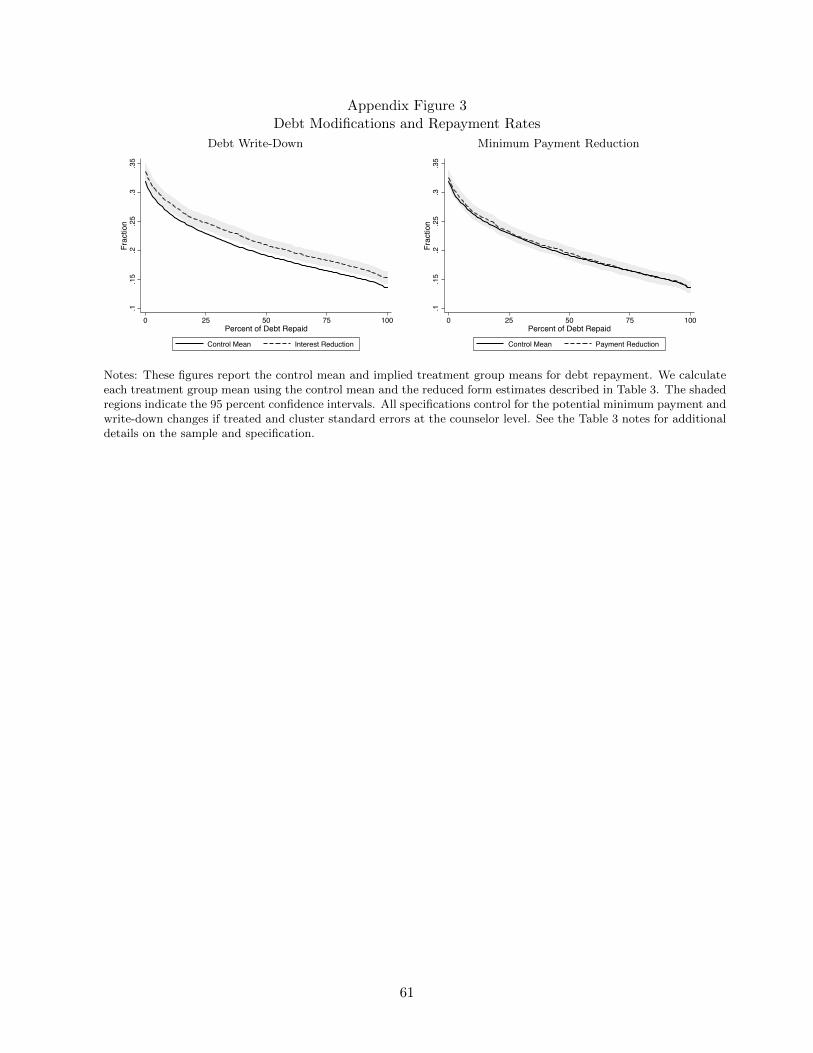

percentage points, an 11.89 percent increase from the control mean. In Appendix Figure 3, we

show that the effect of the write-down treatment remains roughly constant throughout the repay-

ment program. Appendix Figure 3 also shows that both treatment and control borrowers exit the

repayment program at high rates, with only 13.66 percent of the control group completely repaying

their debts. In Section V, we will discuss what mechanisms are most consistent with these results.

As with the intent-to-treat estimates, the effects of the write-down treatment are driven by

borrowers with above median debt-to-income. For these high debt-to-income borrowers, the median

write-down treatment increased the probability of starting a repayment program by 2.80 percentage

points, an 8.76 percent change, and increased the probability of finishing a repayment program by

2.51 percentage points, a 16.91 percent change. In comparison, there are no statistically significant