debt management for student borrowers nancy faucett and mike smith student loan guarantee foundation...

TRANSCRIPT

Debt Management for Student Borrowers

Nancy Faucett and Mike Smith Student Loan Guarantee Foundation of Arkansas

High Debt StatisticsAverage credit card debt for undergraduate students

is $2748One third of undergraduate students carry four or

more credit cardsNearly 10% of undergraduate students report credit

card debt of $7000 or moreA credit card debt of $1400 with 18% interest rate

and paid at minimum monthly payment would take eight years to repay, with interest costing the borrower $2607

Last year approximately 461,000 Americans under age 35 filed for bankruptcy

Managing Your Credit Card Debt

Use only one credit cardChoose a credit card without an annual feeChoose a credit card with the lowest rate

availableUse credit cards for emergencies onlyKeep receipts of all charges, keep total of

amount owedPay off charges in full each month

Managing Your Credit Card Debt

Do not purchase on impulse with credit card

Do not charge more than you can afford to pay off the next month

Know when your credit card payments are due

Do not live a lifestyle you can not afford

Save Money and Live Within Your Budget

Private ScholarshipsCookLive with roommatesTuition reimbursementShare class materialsDepartmental grantsResearch assistantshipsWork for the schoolLoans

Debt Management Strategies

Realize credit cards are issued to students, even if the student has no credit history and no income

Involve parents in discussing credit card use Stress importance of good credit historyEncourage families to obtain a debit card for

college bound teenagers instead of a credit cardDiscourage credit card solicitation on campus

Debt Management StrategiesRealize reasons college students fall into debt

Peer pressure to spend moneyExtensions of credit limitsHigher education-related expensesBelief that well paying job will pay off credit card

debtUtilize Gradfree.com to help students reduce college

loan debtEnsure borrower’s debt does not exceed 8% of

income

10 Greatest Myths about Credit and Debt

Myth 1: If I don’t use credit, I will never be able to buy anything

Myth 2: Credit is badMyth 3: I’m a failure because I’m in financial troubleMyth 4: If my debt is too much, I will file for

bankruptcyMyth 5: The credit card companies would not send

me applications if I could not afford it

10 Greatest Myths about Credit and Debt

Myth 6: I will be okay if I make my minimum monthly payment

Myth 7: I can pay off my credit card debt with a home equity loan

Myth 8: I can take a cash advance to keep me from falling behind on my payments

Myth 9: If I cosign a loan, the lender will not charge me with the liability

Myth 10: My financial condition is so bad it is hopeless

Ten Steps to Financial Fitness

Educate students about personal finance

Help in determining financial fitnessGive advice on using credit wiselyTips on avoiding loan defaults

PURPOSE

BorrowerSchoolLender/servicer/holderGuaranty agency (Guarantor)U.S. Department of Education (USDE)

Learn about your role and the role of others

Step One

Default: 270 days delinquentLoans carry a legal obligation

Avoid Consequences of Default

Step Two

Damage to your credit ratingWithheld federal treasury payments, including

tax refunds Garnishment of wagesLawsuits, collection costs, legal expensesNo additional financial aidProfessional licenses could be in jeopardy

Step TwoConsequences

How do you take control?Make a budget and stick to itOpen checking and savings accountsGet the best deal on a credit cardUse credit cards responsibly

Control Your Finances

Step Three

Make loan payments on timePay monthly services promptlyReview credit reportSeek help if things get out of hand

Control Your Finances

Step Three

1. Compare statement to daily register

2. Check off register items that appear on statement

3. Add all deposits together from register and compare to statement

Balance Your Checkbook

Step Four

4. Add all deductions together and compare to statement

5. Update your statement information

6. Do it EVERY month

Balance Your Checkbook

Step Four

List the things that are most important to you

Set some goalsDetermine your incomeDetermine your expensesCreate a “spending plan”

Establish a Budget

Step Five

Pay yourself firstWatch using the “plastic”Keep track of expensesRe-think your spending plan periodically

Establish a Budget

Step Five

Pay yourself first

Establish a savings account

Learn about your investment options

Pay Yourself and Invest

Step Six

How to Establish a Savings Account

On paydays, make a check out to yourself and deposit it in your savings account

Use payroll direct deposit and have money deposited in your savings account automatically

If you save $100 a month beginning at age 22, you will have saved $100,000 by age 55

Ways to SaveCertificates of deposit

U.S. Savings bonds

Money market accounts

Determine your risk tolerance before you make

investment decisions

Use Credit Cards Wisely1.You are borrowing money when you use a

credit card

2.You will pay a finance charge if you do not pay your balance in full each month

3.Shop around for the credit card that suits your budget and repayment habits

4. Use your credit cards wisely to help you establish a solid credit rating and avoid financial problems

Step Seven

Selecting a Credit Card

1. A low annual percentage interest rate

2. The interest calculation method: low or no annual fees

3. All other charges: late fees, transaction fees, over the limit fees

4. A grace period

5. Credit limit: start off small

6. Wide acceptance

Know your credit report and how to request one

Step Eight

Who can access your credit report?

1. Creditors (banks, finance companies, credit card companies, etc)

2. Landlords

3. Employers

4. Government licensing agencies

What does your credit report tell creditors?

1. How promptly you pay your bills

2. How many credit cards you own

3. What is the total amount of credit extended

4. How much you actually owe on all your accounts

What is on your credit report?

1. Personal identifying information

2. Credit account information

3. Public record information

4. Inquiries

Negative information stays on your credit report for seven to 10 years, positive information indefinitely, and inquires six months to 12 years

How do you request a credit report?

1. Call, write, or request online

2. Review once a year

3. If you find an error, contact the credit reporting company immediately

4. Credit Reporting Agencies:Equifax www.equifax.comTrans Union www.transunion.comExperian – formerly TRW www.experian.com

Clean up your credit

Step Nine

Tips to Clean up your Credit

Pay off your past-due accounts

Bring past due accounts up-to-date and keep them that way

Wait until the bad ratings are removed from your credit report before applying for more credit

Write a brief explanation for your poor credit rating (such as unemployment) to be included on future credit reports

What to do if you are in serious financial difficulty

Contact your creditors Find a debt counseling serviceConsumer Credit Counseling Service 800-388-2227 Consider loan consolidation Use bankruptcy as a last resort

There are no quick fixes to fix damaged credit. It takes time, sacrifice, and good money management.

BANKRUPTCYYou are asking a federal court to declare that you are unable to pay your debts

Your debts will be reduced or eliminated

Collection activities such as foreclosure, repossession, phone calls and letters from creditors, wage garnishment or disconnection of utilities will stop

The Cons of BankruptcyRemains on your credit for up to 10 years

If you can get additional credit, you may get less than you ask for, pay a higher interest rate, or make a larger down payment

May affect your ability to get a job

Cause feeling of guilt and embarrassment due to the stigma associated with an inability to control your finances

Student loans generally are not discharged through bankruptcy

Personal Bankruptcy

Chapter 7 - no steady income and few assets, debts are cancelled, assets are converted to cash and used to repay part of your debts

Chapter 13 - you have a steady income, are placed under a court approved repayment plan where they pay some or all of your debts in three to five years, and assets are not sold to pay creditors

Other Internet Resources•Career guidance / job search•Educational institutions•Financial aid estimators•Government agencies•Other valuable resources•Scholarships, grants, fellowships•Sites with information on financial fitness•Standardized tests / admissions.

Step Ten

Mapping Your Future

Paying for School Online Student Loan Counseling Ten Steps to Financial Fitness Loan Locator Deferment Navigator Budget Calculator Frequently Asked Questions Loan Calculator Additional Resources

Special Features

Paying for School

Paying for School

Online Student Loan Counseling

Online Student Loan Counseling

Ten Steps to Financial Fitness

Ten Steps to Financial Fitness

Loan Locator

Loan Locator

Deferment Navigator

Deferment Navigator

Deferment Eligibility Charts

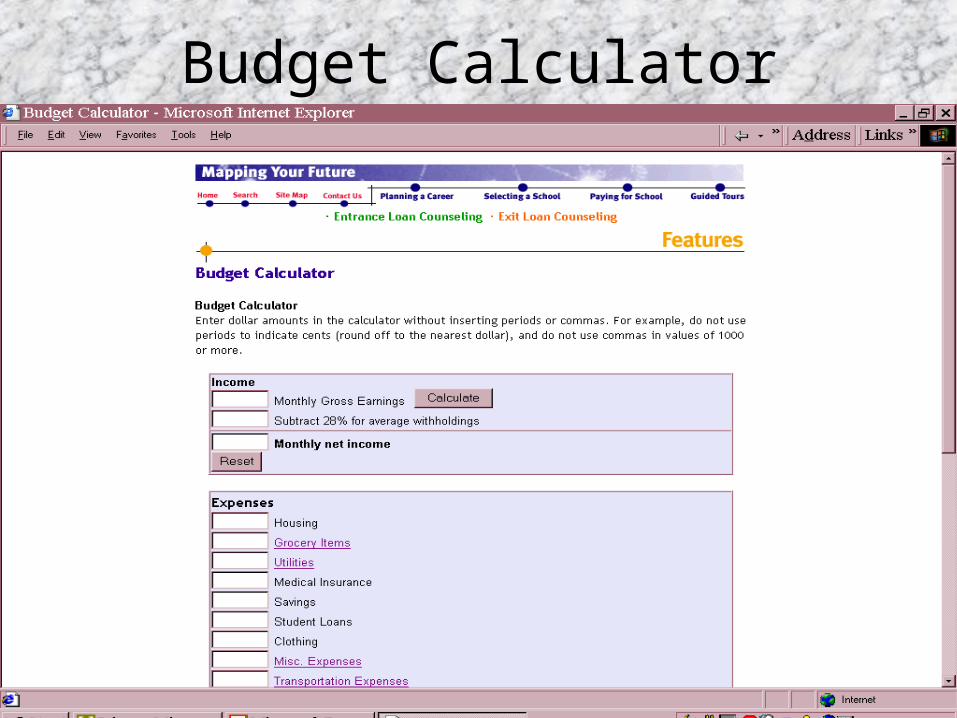

Budget Calculator

Budget Calculator

Frequently Asked Questions

Frequently Asked Questions

Loan Calculator

Student Loan Calculator

Additional Resources

Additional Resources

Chat Nights Careership Scholarship resources Conducting job search techniques Other Internet resources More special features

Chat Nights

New chat night every other month

Lists previous chat nights

Logs chat night topics

Careership Six different career regions

Multiple career fields

Frequently asked questions Gives the most frequently-asked questions

for that field, along with the answers

Scholarship Resources

Federal financial aid programs

Scholarships

Grants

Work-study

Loans

Conducting Job Search Techniques

Assesses skills and interestHelps determine career goals Links to The Occupational Handbook

Assists with resumes Gives sample resume Interview information

Links to Other Internet Resources

Career guidance/job search Educational institutions Financial aid estimatorsGovernment agencies Scholarships, grants, fellowships Information on financial fitness Standardized tests/ admissions

More Special Features

Glossary of Terms Online College Applications

Questions?