de martini - ucla smerc conf. mar 22, 2013

TRANSCRIPT

© 2012, Newport Consulting Group

Evolution of Distributed Power Systems

Paul De Martini

March 22, 2013

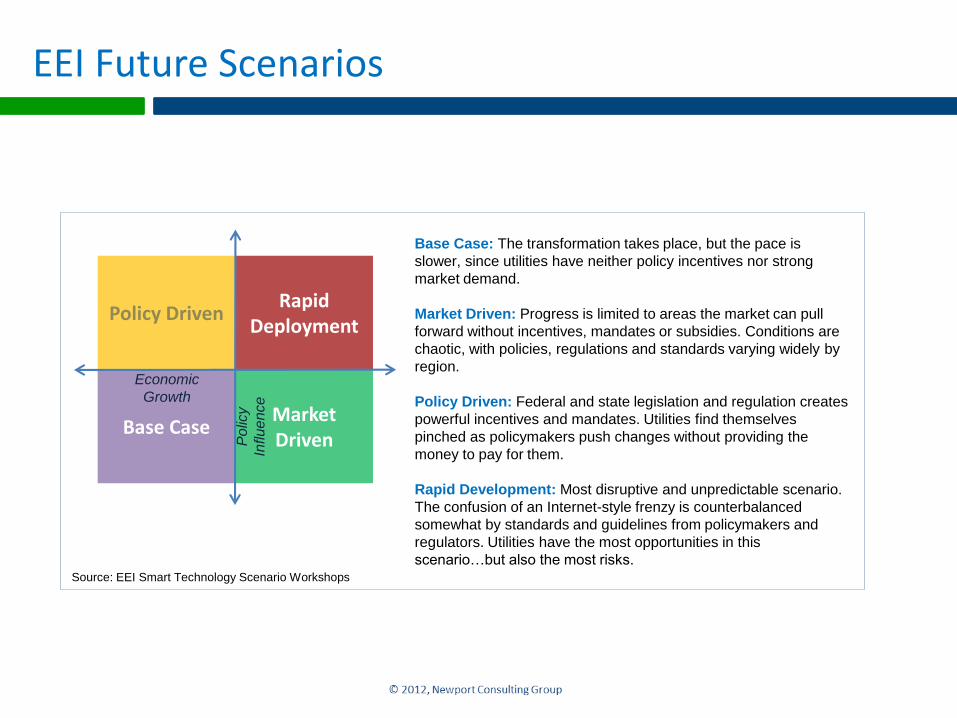

Base Case: The transformation takes place, but the pace is

slower, since utilities have neither policy incentives nor strong

market demand.

Market Driven: Progress is limited to areas the market can pull

forward without incentives, mandates or subsidies. Conditions are

chaotic, with policies, regulations and standards varying widely by

region.

Policy Driven: Federal and state legislation and regulation creates

powerful incentives and mandates. Utilities find themselves

pinched as policymakers push changes without providing the

money to pay for them.

Rapid Development: Most disruptive and unpredictable scenario.

The confusion of an Internet-style frenzy is counterbalanced

somewhat by standards and guidelines from policymakers and

regulators. Utilities have the most opportunities in this

scenario…but also the most risks.

Market Driven

Policy DrivenRapid

Deployment

Base Case

Po

licy

Influe

nce

Economic

Growth

Source: EEI Smart Technology Scenario Workshops

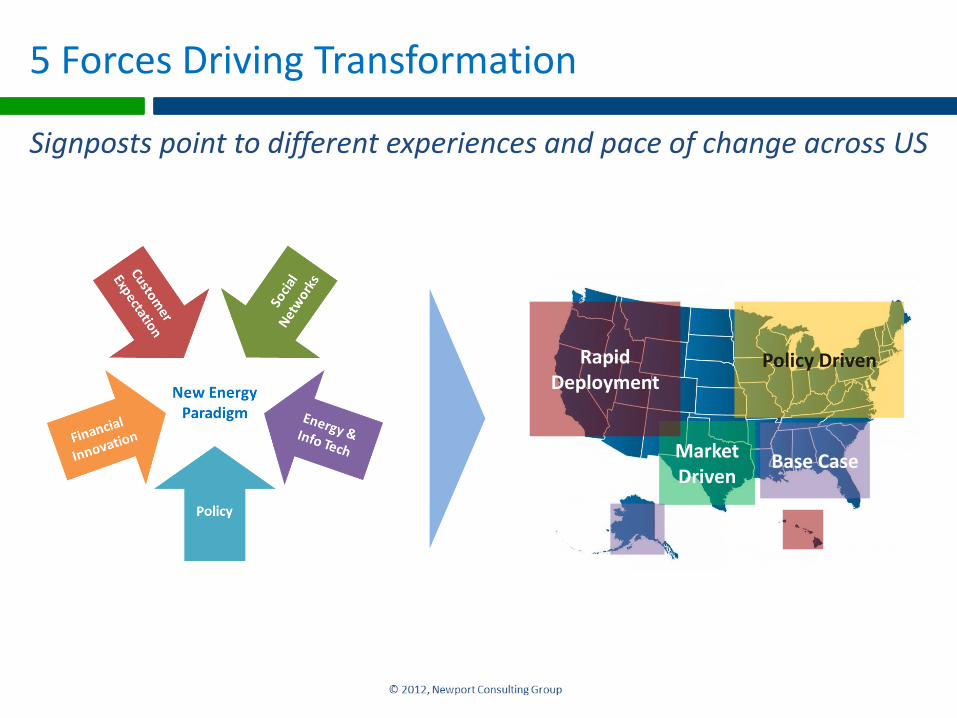

EEI Future Scenarios

Signposts point to different experiences and pace of change across US

Market Driven

Policy DrivenRapid Deployment

Base Case

5 Forces Driving Transformation

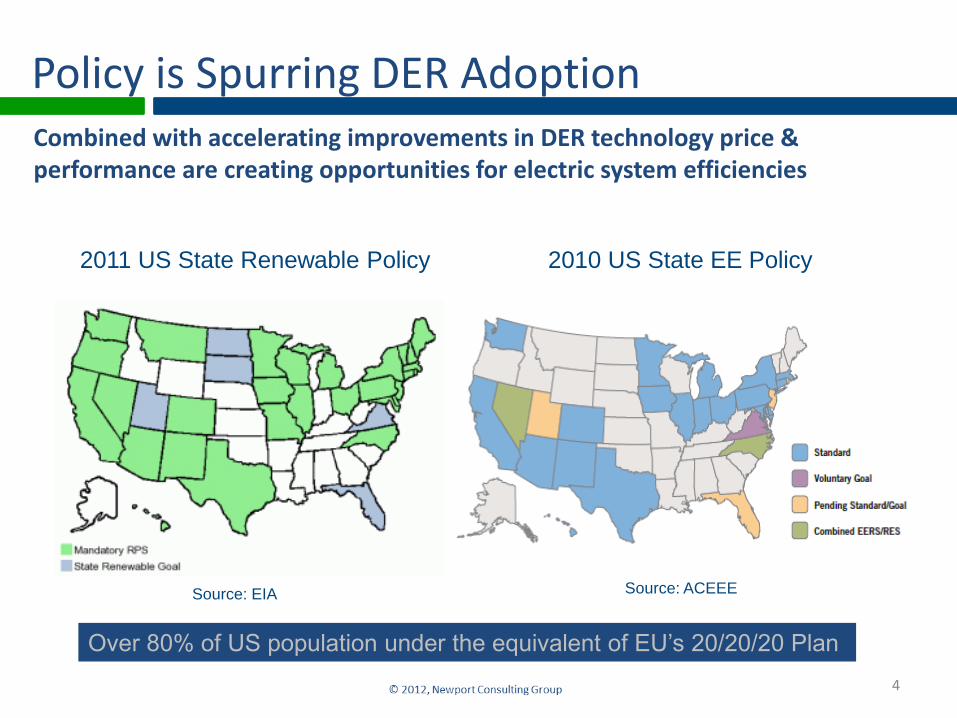

Source: ACEEESource: EIA

2011 US State Renewable Policy 2010 US State EE Policy

Policy is Spurring DER AdoptionCombined with accelerating improvements in DER technology price & performance are creating opportunities for electric system efficiencies

4

Over 80% of US population under the equivalent of EU’s 20/20/20 Plan

Source: DoE EERE

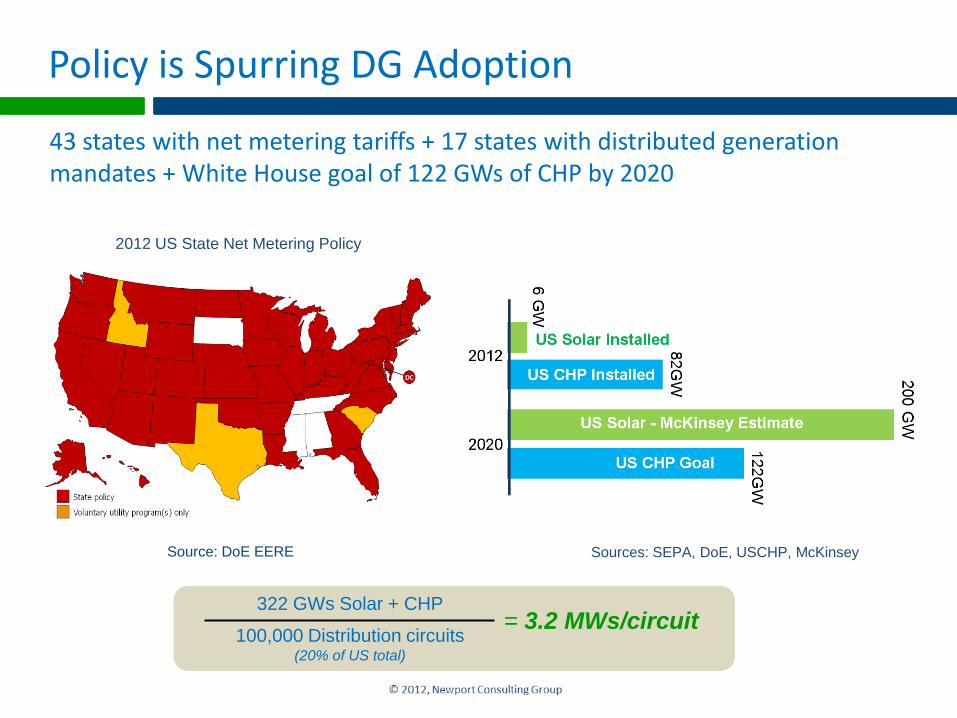

2012 US State Net Metering Policy

Policy is Spurring DG Adoption

43 states with net metering tariffs + 17 states with distributed generation mandates + White House goal of 122 GWs of CHP by 2020

Sources: SEPA, DoE, USCHP, McKinsey

322 GWs Solar + CHP

100,000 Distribution circuits(20% of US total)

= 3.2 MWs/circuit

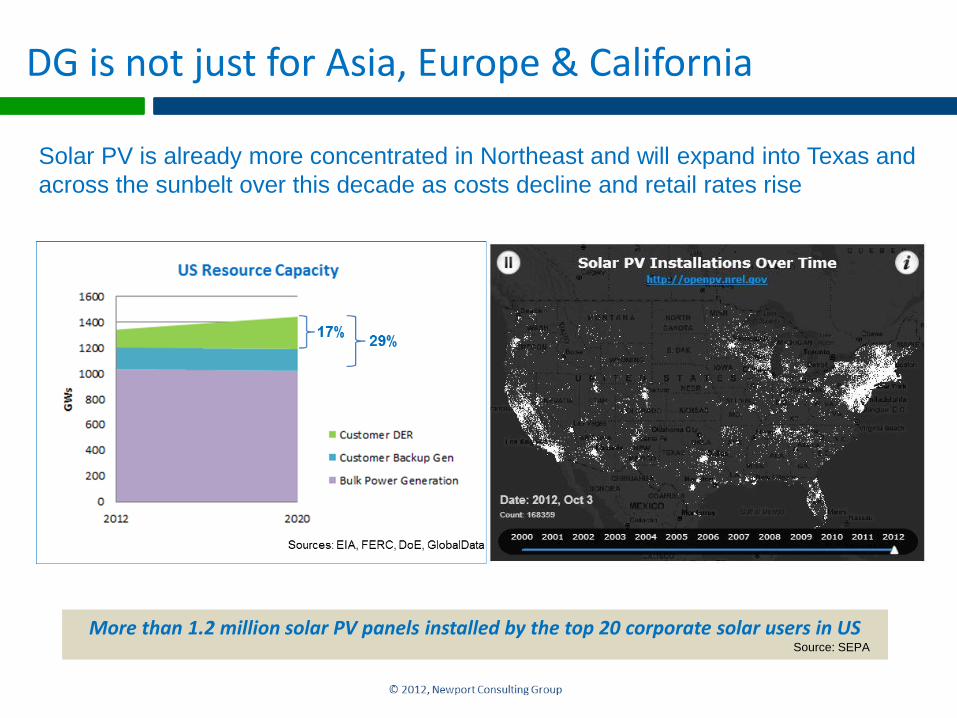

DG is not just for Asia, Europe & California

Solar PV is already more concentrated in Northeast and will expand into Texas and

across the sunbelt over this decade as costs decline and retail rates rise

More than 1.2 million solar PV panels installed by the top 20 corporate solar users in US Source: SEPA

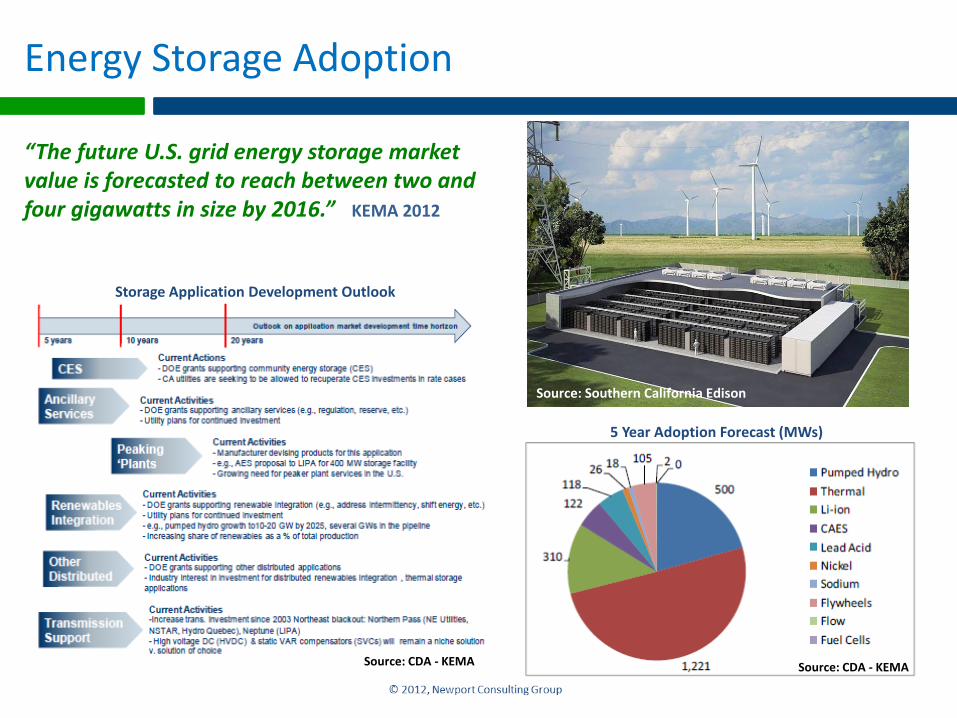

Energy Storage Adoption

Source: CDA - KEMA Source: CDA - KEMA

5 Year Adoption Forecast (MWs)

Storage Application Development Outlook

Source: Southern California Edison

“The future U.S. grid energy storage market value is forecasted to reach between two and four gigawatts in size by 2016.” KEMA 2012

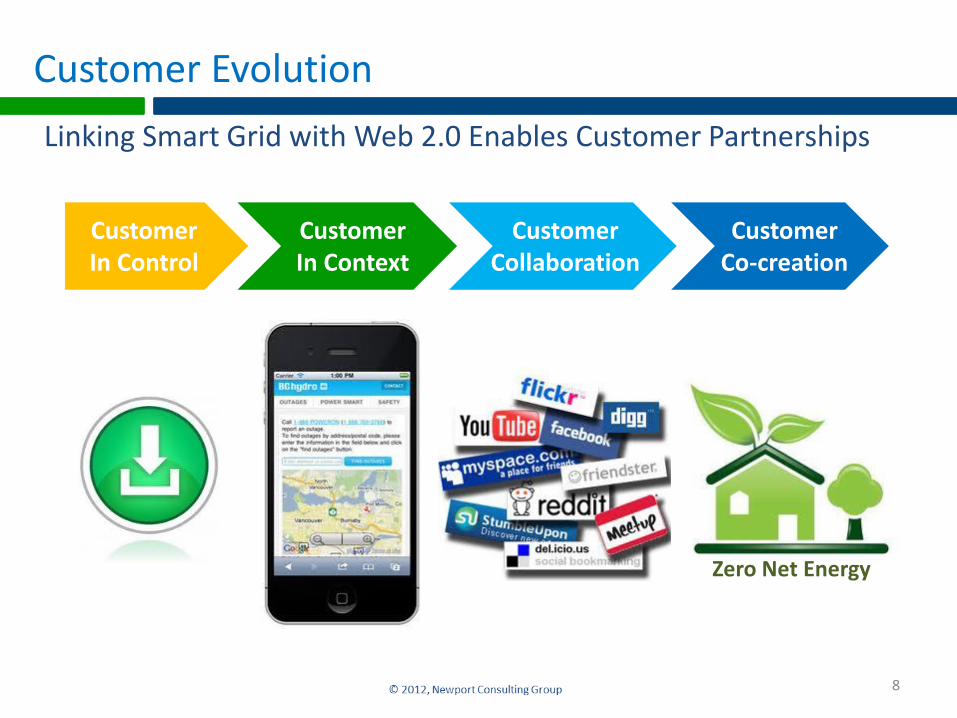

Customer Evolution

Linking Smart Grid with Web 2.0 Enables Customer Partnerships

8

CustomerIn Control

CustomerIn Context

CustomerCollaboration

CustomerCo-creation

Zero Net Energy

Transactive Energy

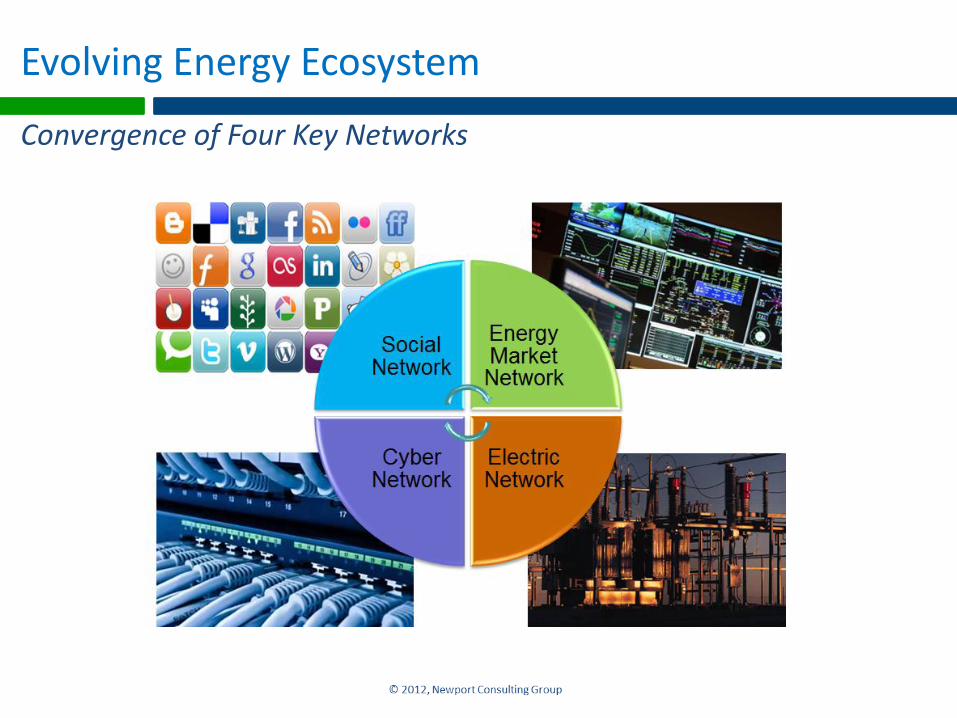

Evolving Energy Ecosystem

Convergence of Four Key Networks

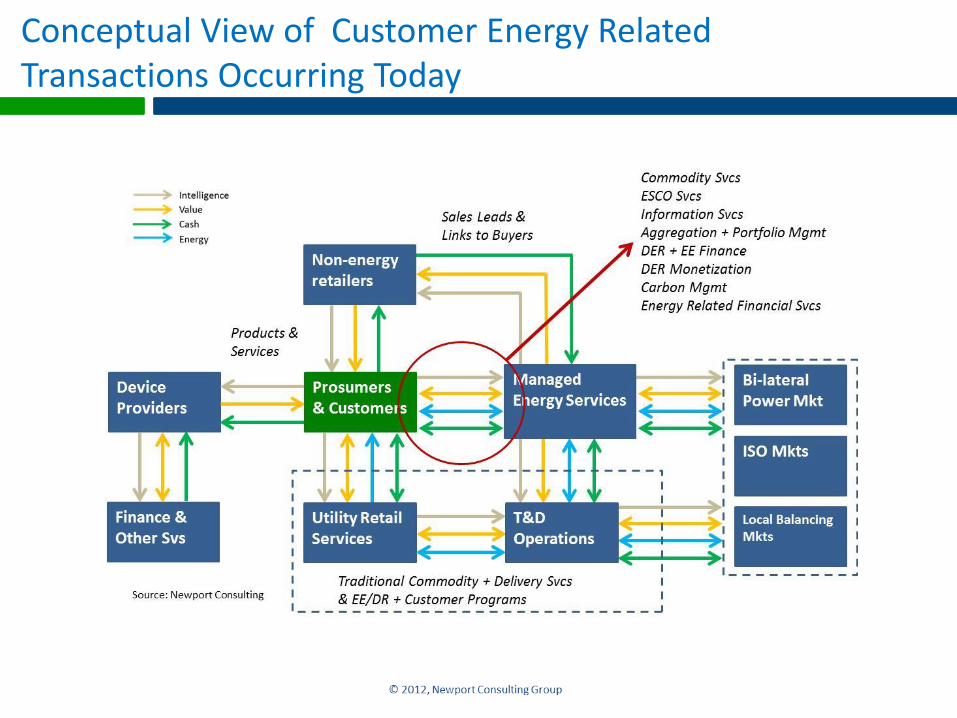

Conceptual View of Customer Energy Related Transactions Occurring Today

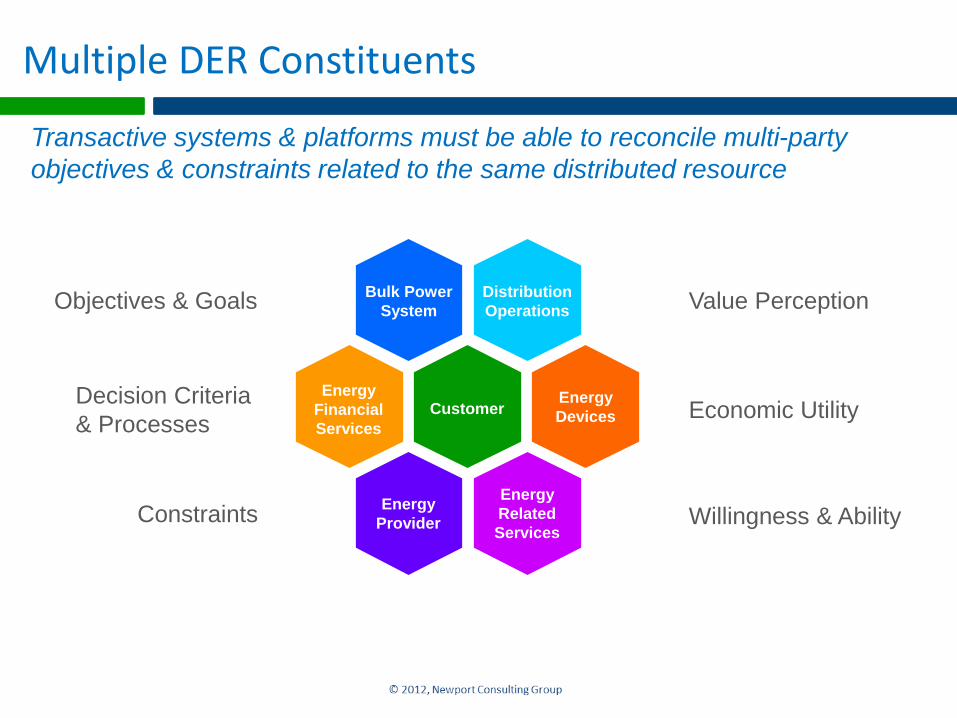

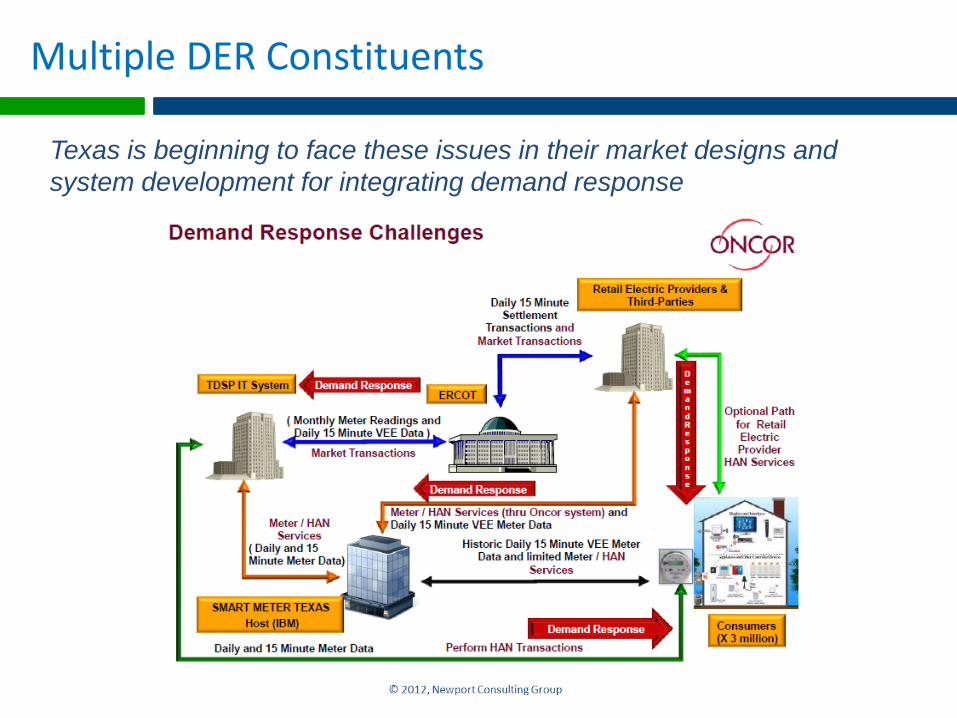

Multiple DER Constituents

Transactive systems & platforms must be able to reconcile multi-party

objectives & constraints related to the same distributed resource

Bulk Power

System

Distribution

Operations

Customer

Energy

Provider

Energy

Related

Services

Energy

Devices

Energy

Financial

Services

Objectives & Goals

Decision Criteria

& Processes

Constraints

Value Perception

Economic Utility

Willingness & Ability

Transactive Energy

Refers to techniques for managing the generation, consumption or flow of electric power within an electric power system through the use of economic or market based constructs while considering grid reliability constraints.

The term “transactive” comes from considering that decisions are made based on a value. These decisions may be analogous to or literally economic transactions.

Transactive Energy Workshop Proceedings 2012, prepared by the GridWise® Architecture Council,

March 2012, PNNL-SA-90082 (http://www.gridwiseac.org/historical/tew2012/tew2012.aspx)

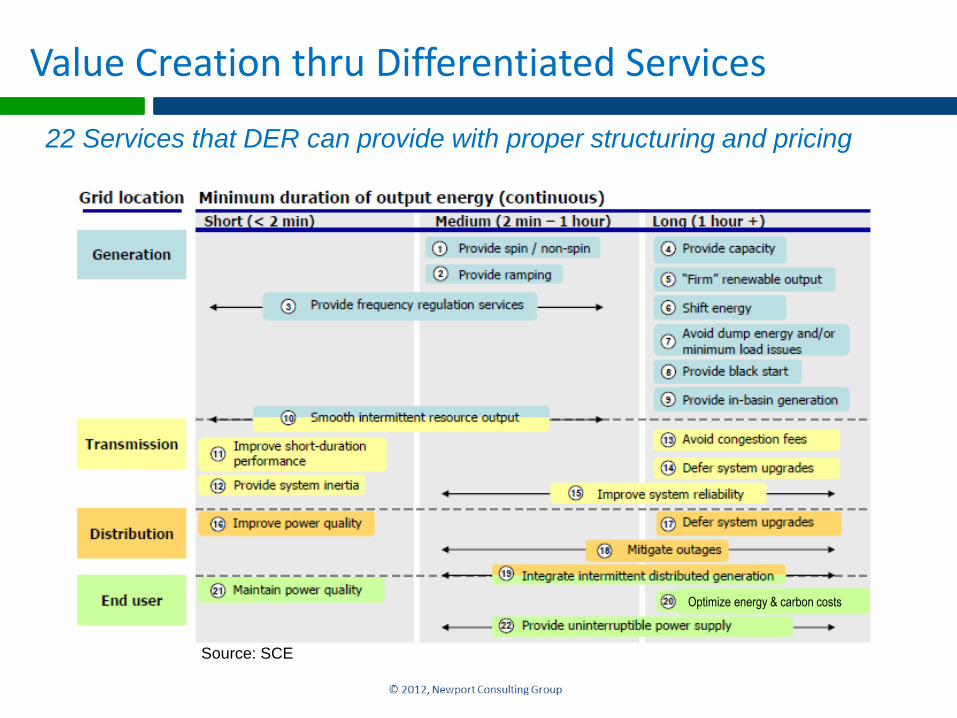

Value Creation thru Differentiated Services

22 Services that DER can provide with proper structuring and pricing

Source: SCE

Optimize energy & carbon costs

Unlocking Latent DER – Pricing Structure Matters

Traditional “best efforts” programs are not effective for most grid operations – need new approach

Adapt Quality of Service Concept:

Availability (On/Off or Will be)

Guarantees (Firmness)

Auditability (Measurement & Verification)

Use of forward pricing structures to balance customer needs for comfort and convenience while providing firm resources for grid operations

Differentiated services may be bundled to keep pricing simple – “good enough” is fine

Forward pricing structures also enable customer side investments in enabling technology

Value Realization Requires Satisfying Multi-Party Requirements

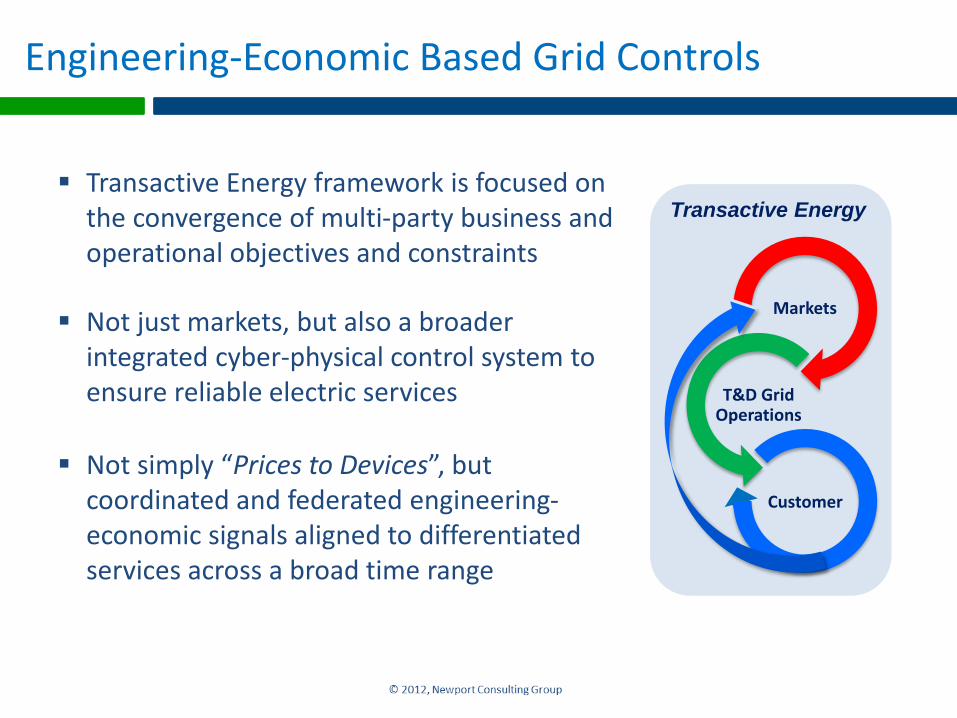

Engineering-Economic Based Grid Controls

Transactive Energy framework is focused on the convergence of multi-party business and operational objectives and constraints

Not just markets, but also a broader integrated cyber-physical control system to ensure reliable electric services

Not simply “Prices to Devices”, but coordinated and federated engineering-economic signals aligned to differentiated services across a broad time range

Transactive Energy

Markets

T&D Grid Operations

Customer

Distributed Energy Resources Platform

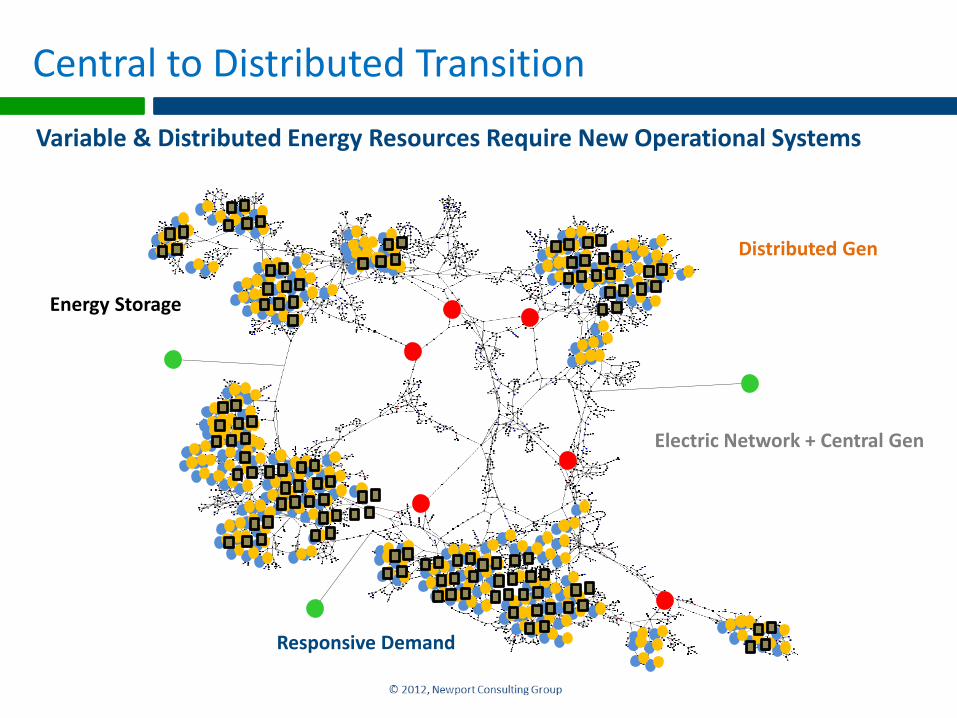

Responsive Demand

Central to Distributed Transition

Variable & Distributed Energy Resources Require New Operational Systems

Distributed Gen

Electric Network + Central Gen

Energy Storage

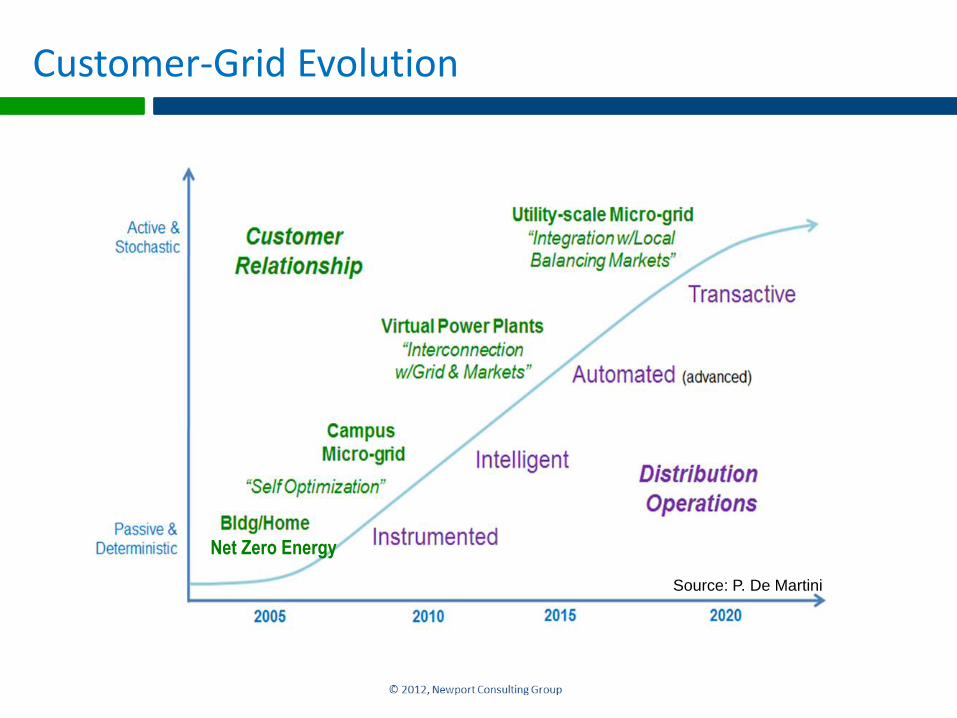

Net Zero Energy

Source: P. De Martini

Customer-Grid Evolution

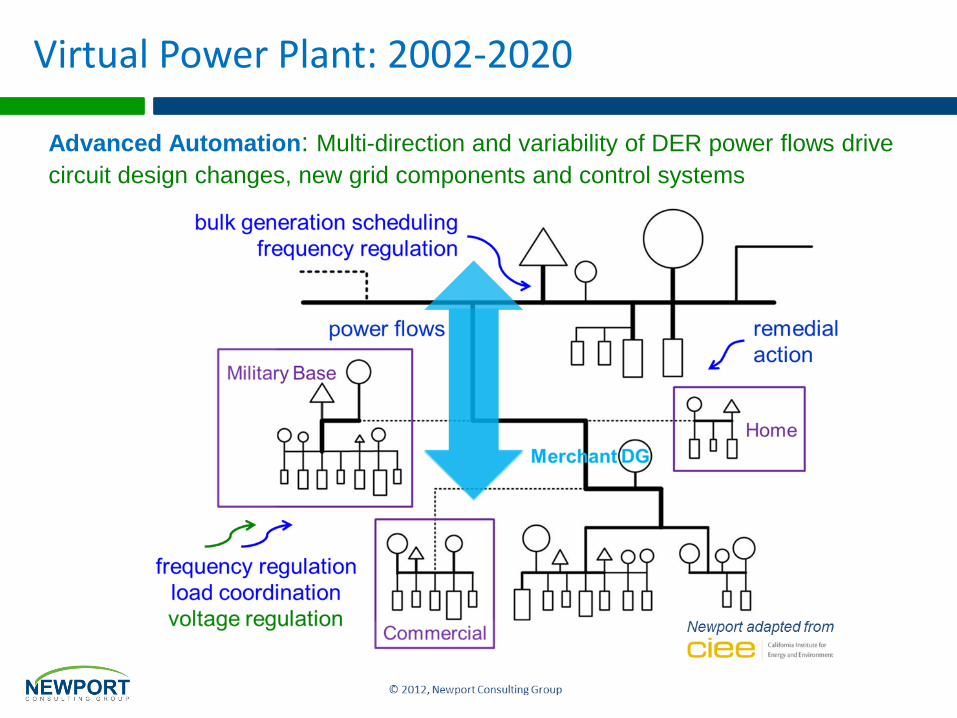

Virtual Power Plant: 2002-2020

Advanced Automation: Multi-direction and variability of DER power flows drive

circuit design changes, new grid components and control systems

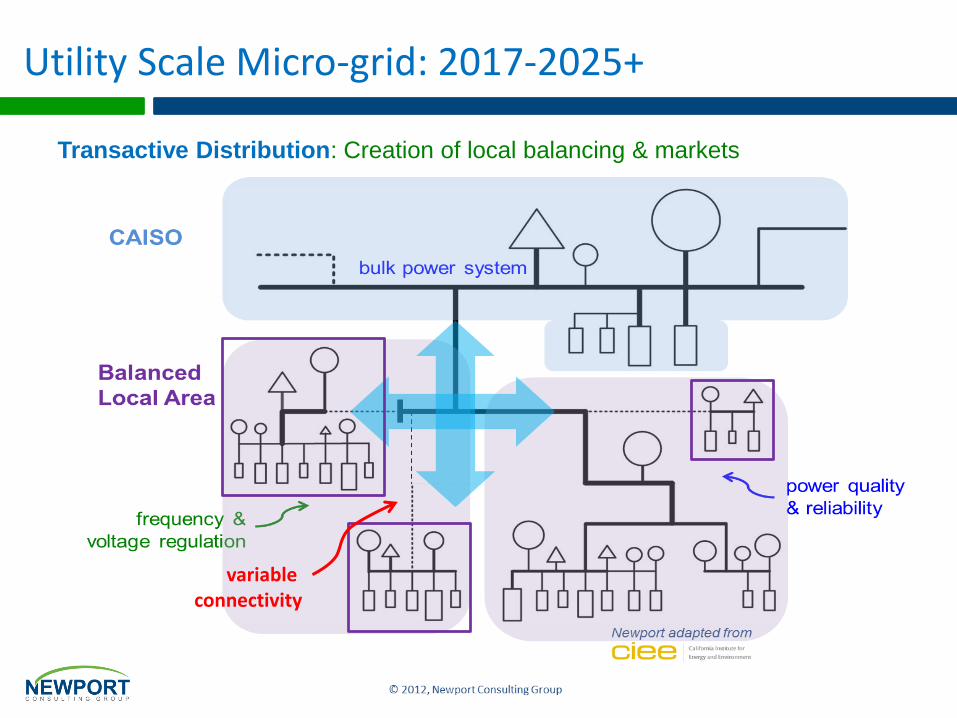

Operational Evolution: 1978-2001Utility Scale Micro-grid: 2017-2025+

Transactive Distribution: Creation of local balancing & markets

variable connectivity

Multiple DER Constituents

Transactive schemes must be able to reconcile multi-party

objectives & constraints related to the same distributed resourceTexas is beginning to face these issues in their market designs and

system development for integrating demand response

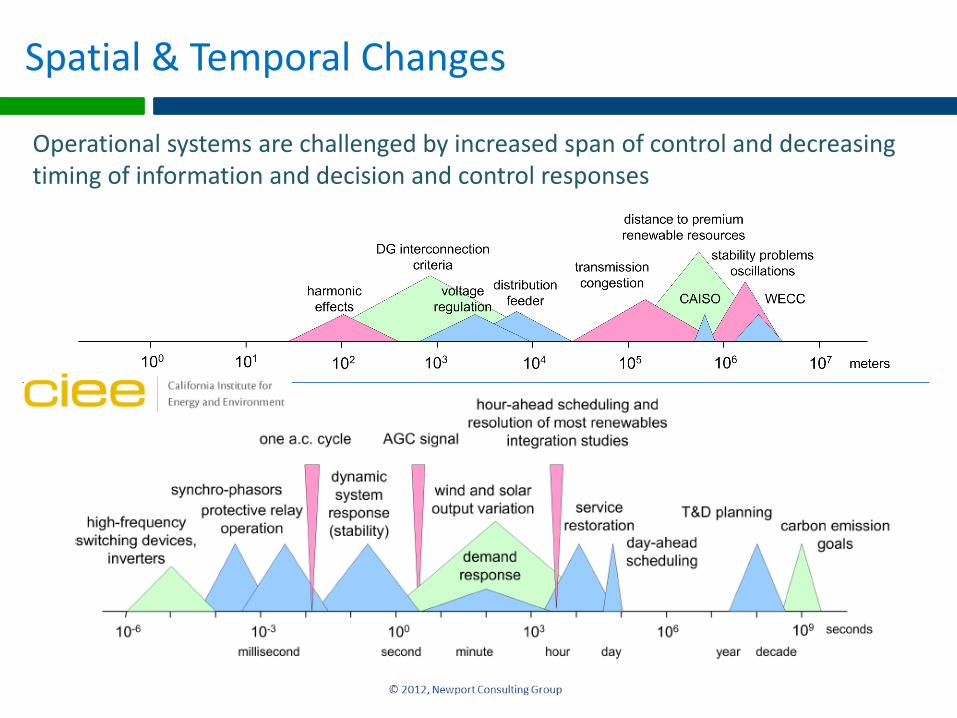

Spatial & Temporal Changes

Operational systems are challenged by increased span of control and decreasing timing of information and decision and control responses

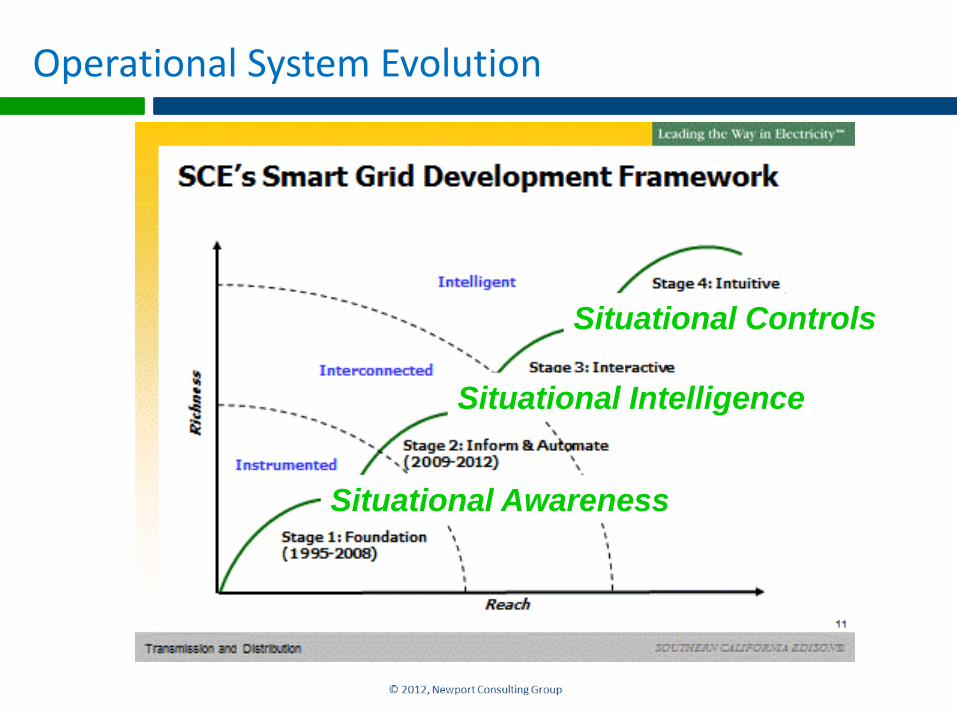

Operational System Evolution

Situational Awareness

Situational Intelligence

Situational Controls

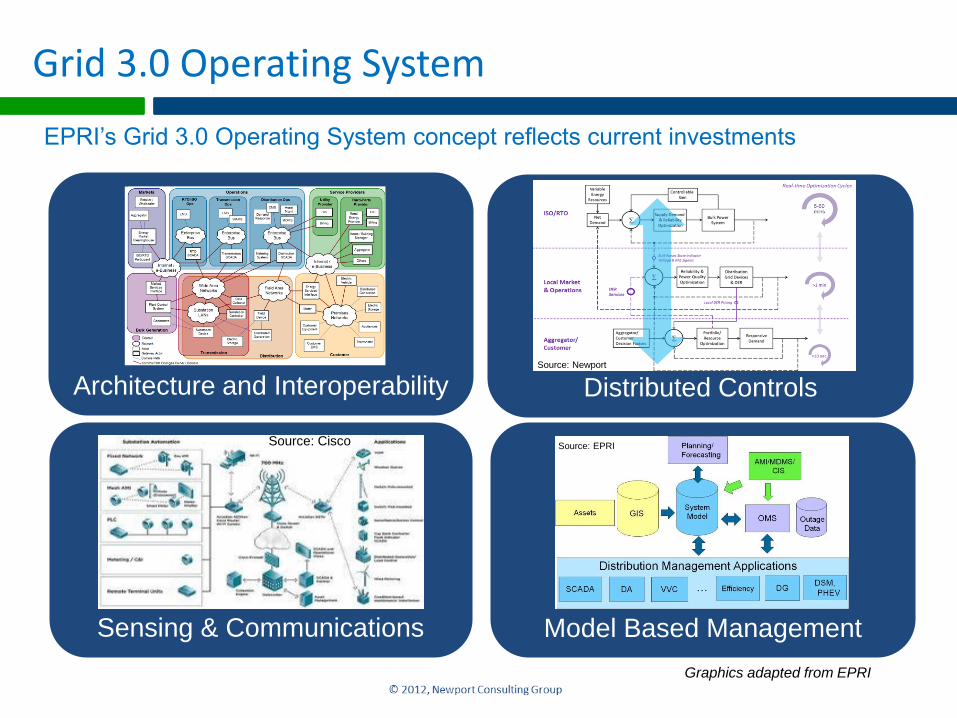

Grid 3.0 Operating System

Sensing & Communications

Distributed Controls

Model Based Management

Architecture and InteroperabilitySource: Newport

Source: EPRI

EPRI’s Grid 3.0 Operating System concept reflects current investments

Graphics adapted from EPRI

Source: Cisco

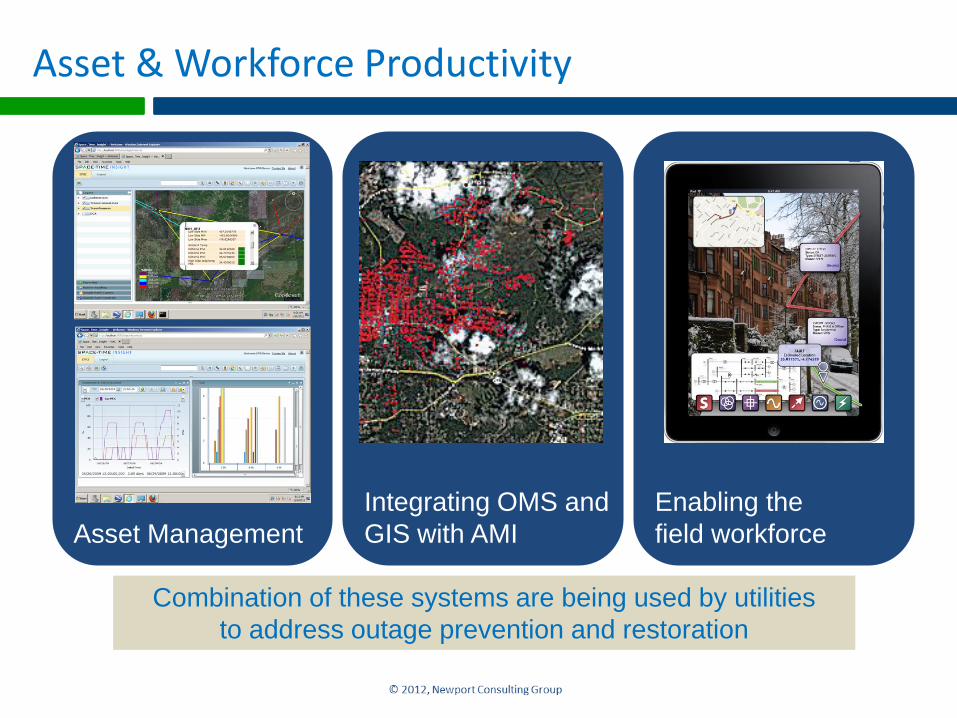

Asset & Workforce Productivity

Asset Management

Enabling the

field workforce

Integrating OMS and

GIS with AMI

Combination of these systems are being used by utilities

to address outage prevention and restoration

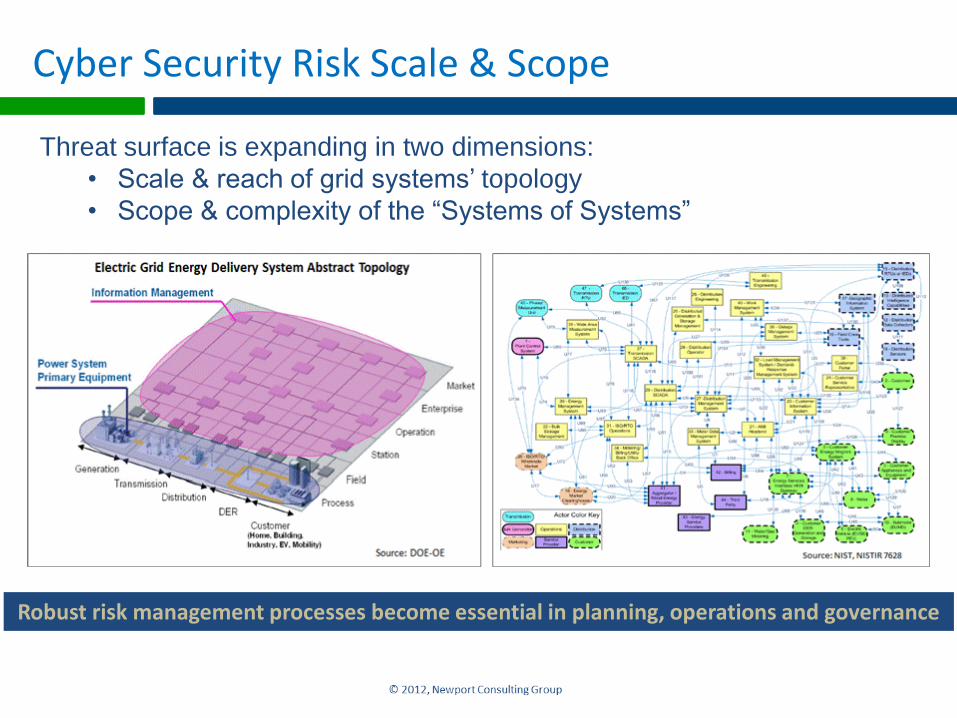

Cyber Security Risk Scale & Scope

Threat surface is expanding in two dimensions:

• Scale & reach of grid systems’ topology

• Scope & complexity of the “Systems of Systems”

Robust risk management processes become essential in planning, operations and governance

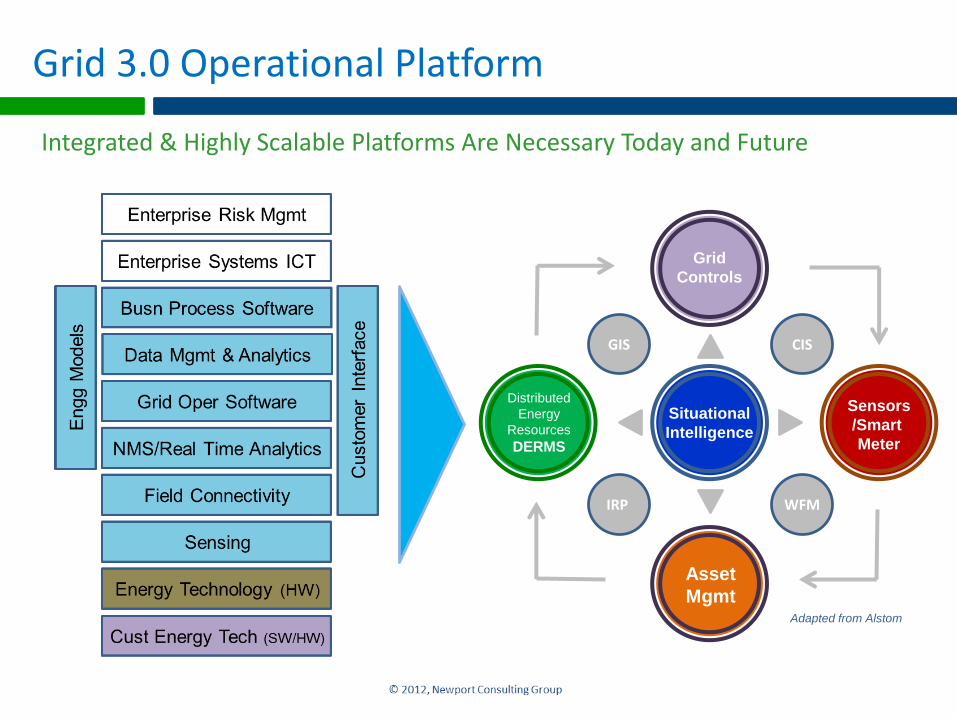

Grid 3.0 Operational Platform

Adapted from Alstom

Integrated & Highly Scalable Platforms Are Necessary Today and Future

GIS CIS

WFMIRP

Distributed

Energy

Resources

DERMS

Grid

Controls

Asset

Mgmt

Sensors

/Smart

Meter

Situational

Intelligence

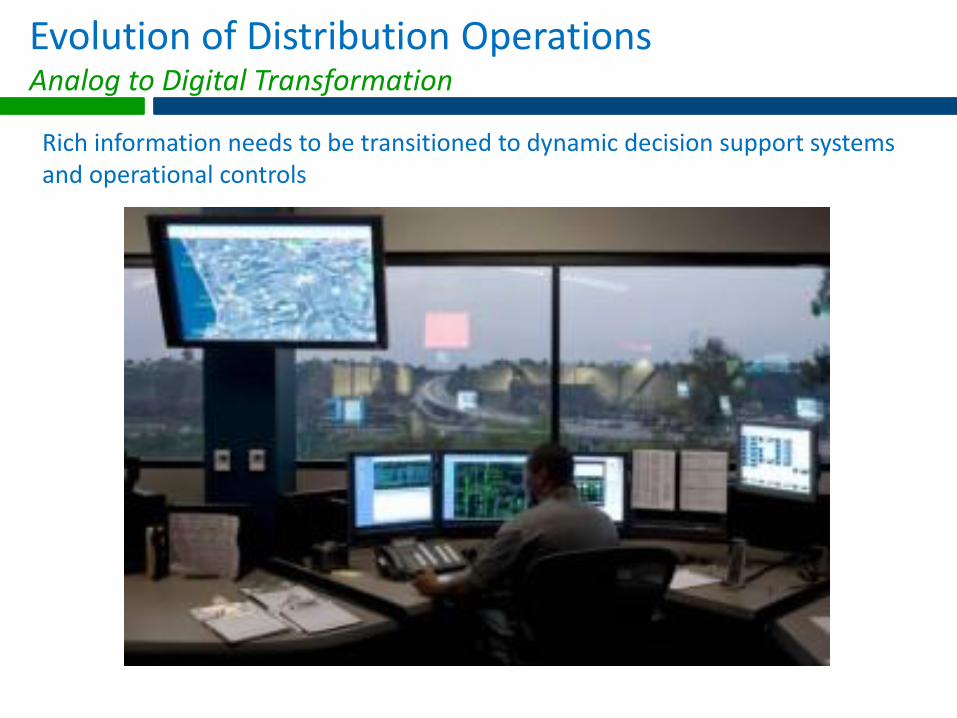

Evolution of Distribution OperationsAnalog to Digital Transformation

29

Images: A. von Meier

Rich information needs to be transitioned to dynamic decision support systems and operational controls

Investment Challenges & Strategies

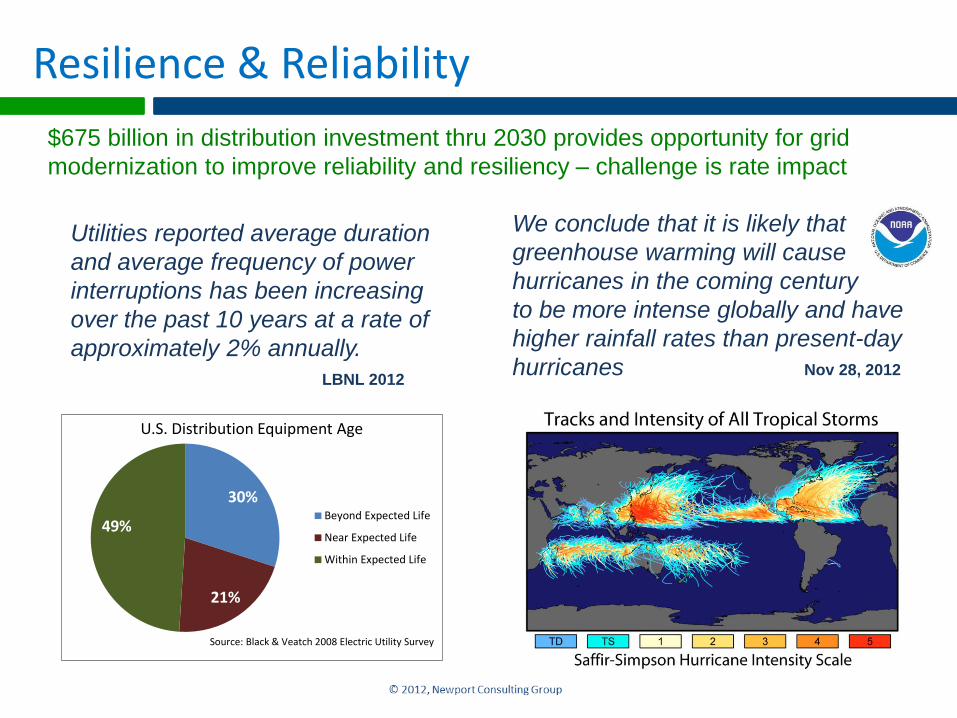

Resilience & Reliability

We conclude that it is likely that

greenhouse warming will cause

hurricanes in the coming century

to be more intense globally and have

higher rainfall rates than present-day

hurricanes Nov 28, 2012

30%

21%

49%

U.S. Distribution Equipment Age

Beyond Expected Life

Near Expected Life

Within Expected Life

Source: Black & Veatch 2008 Electric Utility Survey

Utilities reported average duration

and average frequency of power

interruptions has been increasing

over the past 10 years at a rate of

approximately 2% annually.

LBNL 2012

$675 billion in distribution investment thru 2030 provides opportunity for grid

modernization to improve reliability and resiliency – challenge is rate impact

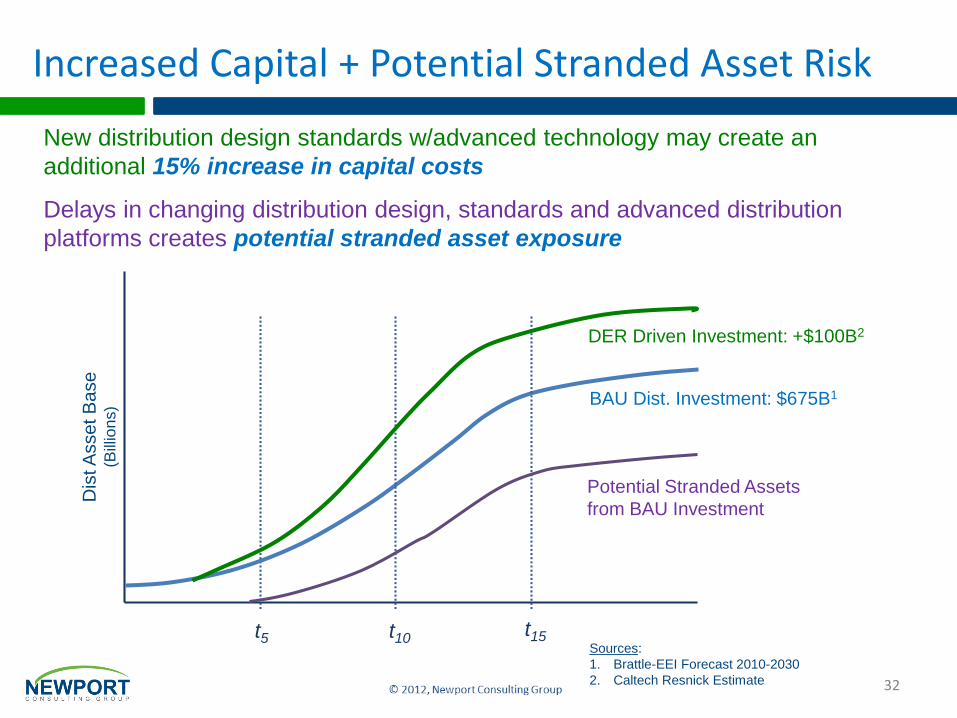

Increased Capital + Potential Stranded Asset RiskD

istA

sse

t B

ase

(Bill

ion

s)

t5 t10t15

Potential Stranded Assets

from BAU Investment

BAU Dist. Investment: $675B1

32

Sources:

1. Brattle-EEI Forecast 2010-2030

2. Caltech Resnick Estimate

DER Driven Investment: +$100B2

$775B +15%

New distribution design standards w/advanced technology may create an

additional 15% increase in capital costs

Delays in changing distribution design, standards and advanced distribution

platforms creates potential stranded asset exposure

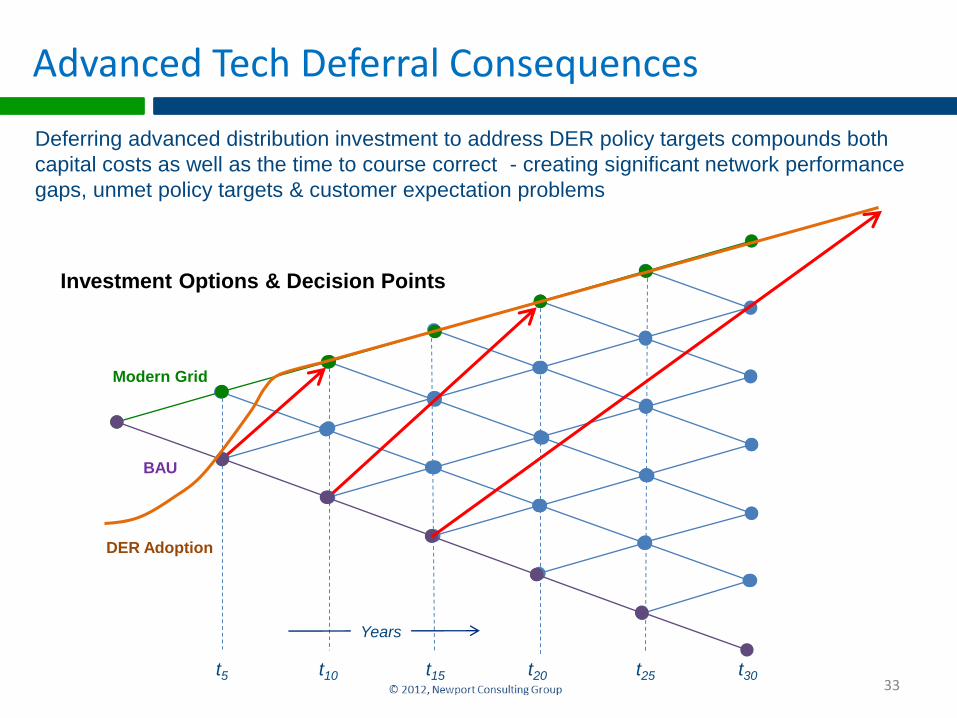

Advanced Tech Deferral Consequences

Modern Grid

BAU

t5 t10 t15 t20 t25 t30

Deferring advanced distribution investment to address DER policy targets compounds both

capital costs as well as the time to course correct - creating significant network performance

gaps, unmet policy targets & customer expectation problems

DER Adoption

33

Investment Options & Decision Points

Years

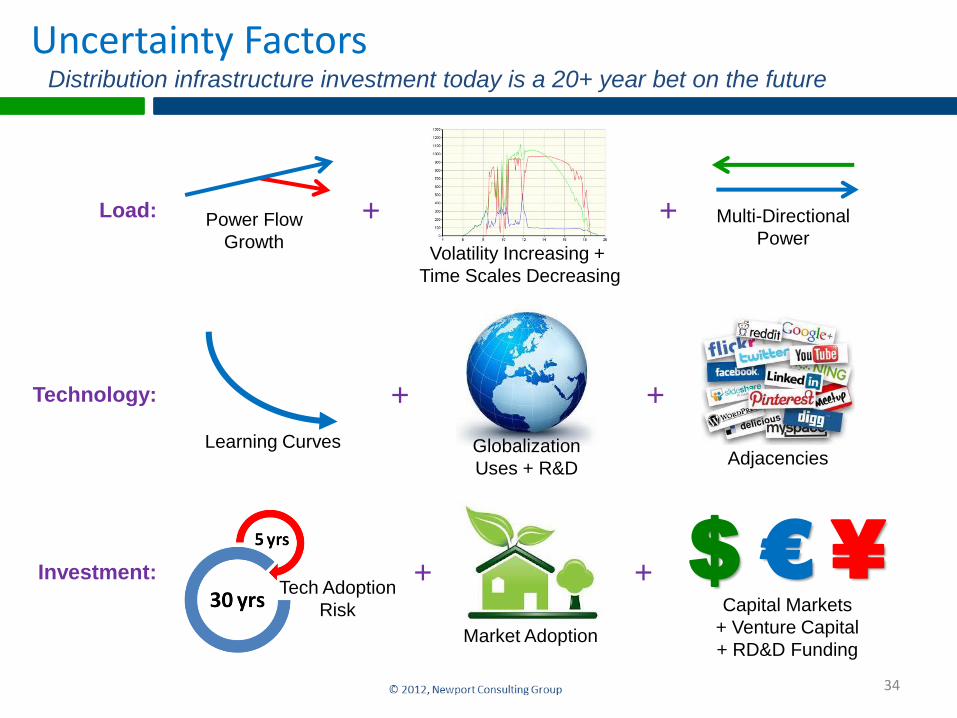

Uncertainty Factors

34

Load: Power Flow

Growth

+ + Multi-Directional

PowerVolatility Increasing +

Time Scales Decreasing

Technology: + +

AdjacenciesLearning Curves Globalization

Uses + R&D

Investment:

Market Adoption

+ + $ € ¥Capital Markets

+ Venture Capital

+ RD&D Funding

Tech Adoption

Risk

Distribution infrastructure investment today is a 20+ year bet on the future

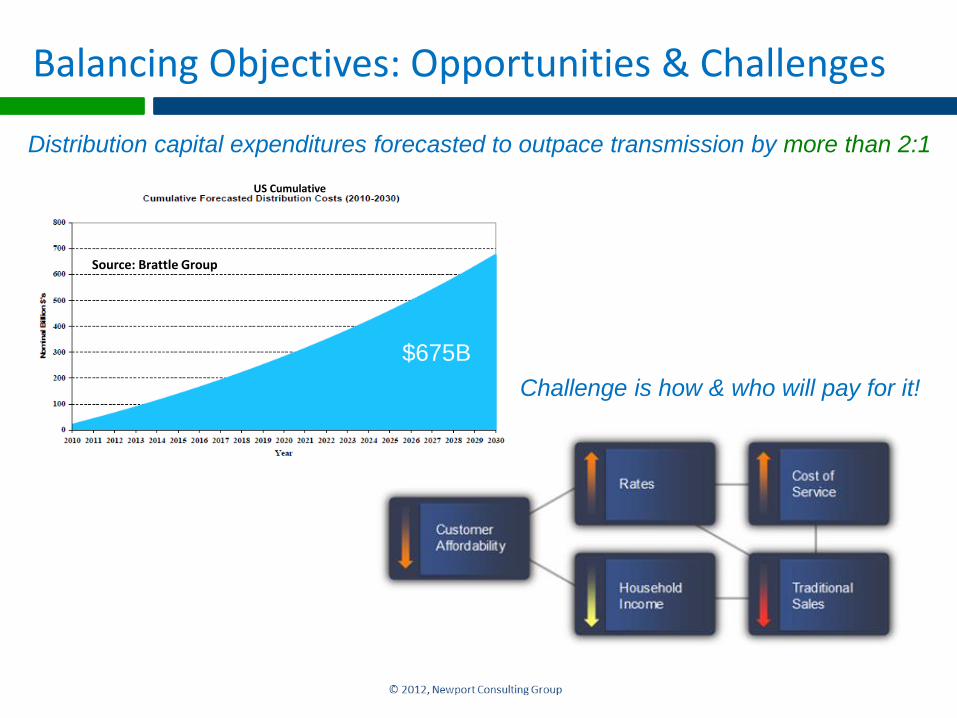

Balancing Objectives: Opportunities & Challenges

Distribution capital expenditures forecasted to outpace transmission by more than 2:1

Challenge is how & who will pay for it!

US Cumulative

Source: Brattle Group

$675B

www.newportcg.com