current trends in ethanol, bioplastics, cogeneration and ... · current trends in ethanol,...

TRANSCRIPT

International Sugar Organization

11 September 2014

Kingsman Miami Sugar Conference

Current Trends in Ethanol, Bioplastics, Cogeneration and Sustainability

Jose Orive Executive Director

International Sugar Organization

1

2 International Sugar Organization

Structure of Presentation

Quick Round-up on World Sugar in 2014/15

The World Ethanol Market in 2014 and Beyond

The World Ethanol Market in 2013 and 2014

The main markets: USA, Brazil, EU

Long-Term Outlook by Region to 2020

Bioplastics and Cogeneration

Conclusions and Implications for Key Stakeholders

2

International Sugar Organization

5- Year World Surplus Weighing on Sugar Prices • The accumulated world sugar

surplus over 4 seasons

means the global stocks to

consumption ratio will

remain above 40% for at

least another year.

036912151821242730

135

145

155

165

175

185

US

cen

ts/lb

mln

mtrv

Production Consumption ISA price

3

International Sugar Organization

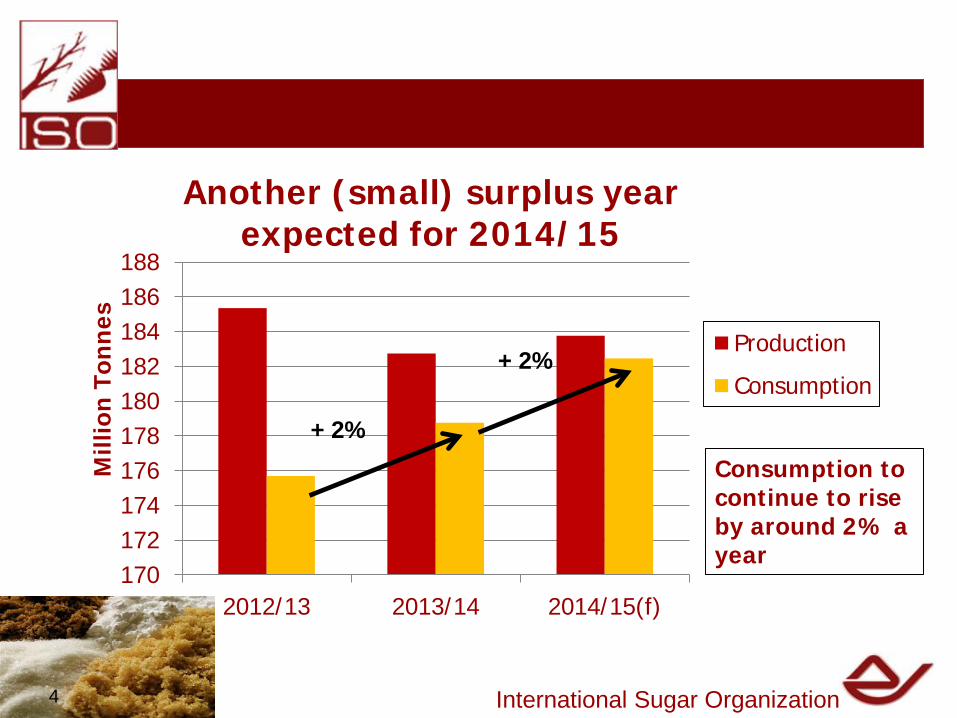

170172174176178180182184186188

2012/13 2013/14 2014/15(f)

Mill

ion

Tonn

es

Another (small) surplus year expected for 2014/15

Production

Consumption+ 2%

+ 2% Consumption to continue to rise by around 2% a year

4

International Sugar Organization

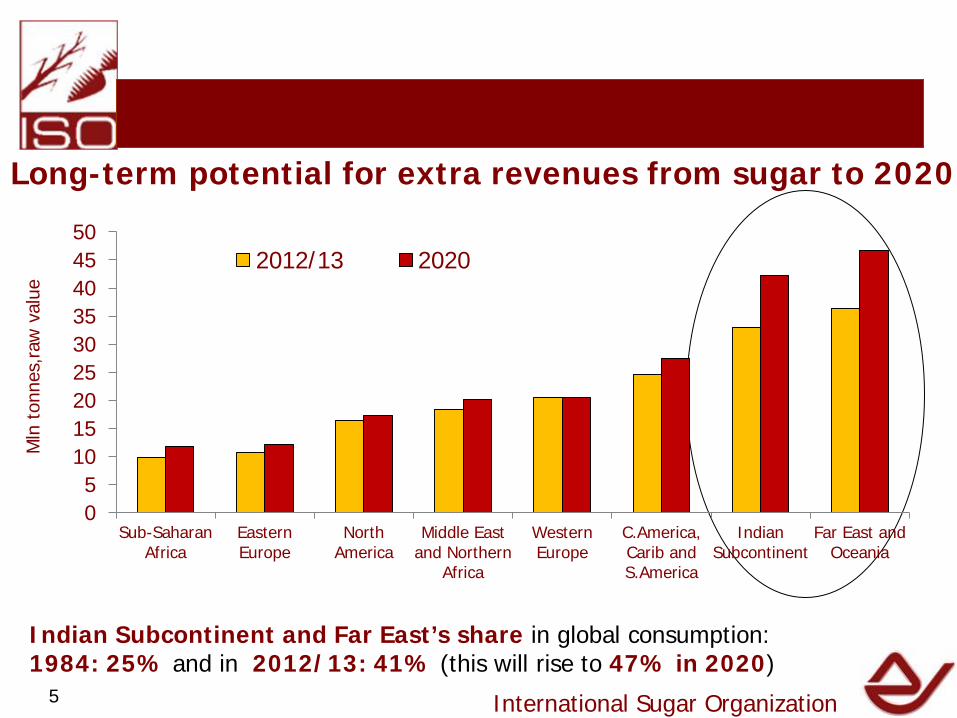

Long-term potential for extra revenues from sugar to 2020

Indian Subcontinent and Far East’s share in global consumption: 1984: 25% and in 2012/13: 41% (this will rise to 47% in 2020)

05

101520253035404550

Sub-SaharanAfrica

EasternEurope

NorthAmerica

Middle Eastand Northern

Africa

WesternEurope

C.America,Carib andS.America

IndianSubcontinent

Far East andOceania

Mln

ton

nes,

raw

val

ue 2012/13 2020

5

6 6

Brazil: Sugar and Ethanol to 2015/16 (Sugar in mln tonnes, tel quel; ethanol in bln litres)

April/ March

International Sugar Organization

Year Sugar Production

Sugar Exports

Ethanol Production

2010/2011 38.0 27.5 27.5

2011/2012 35.9 24.9 22.6

2012/2013 38.2 26.8 23.6

2013/2014 37.5 26.6 27.6

2014/2015 (f)

37.6 25.5 27.1

2015/2016 (f)

37.0 25.0 28.7

6

International Sugar Organization 7

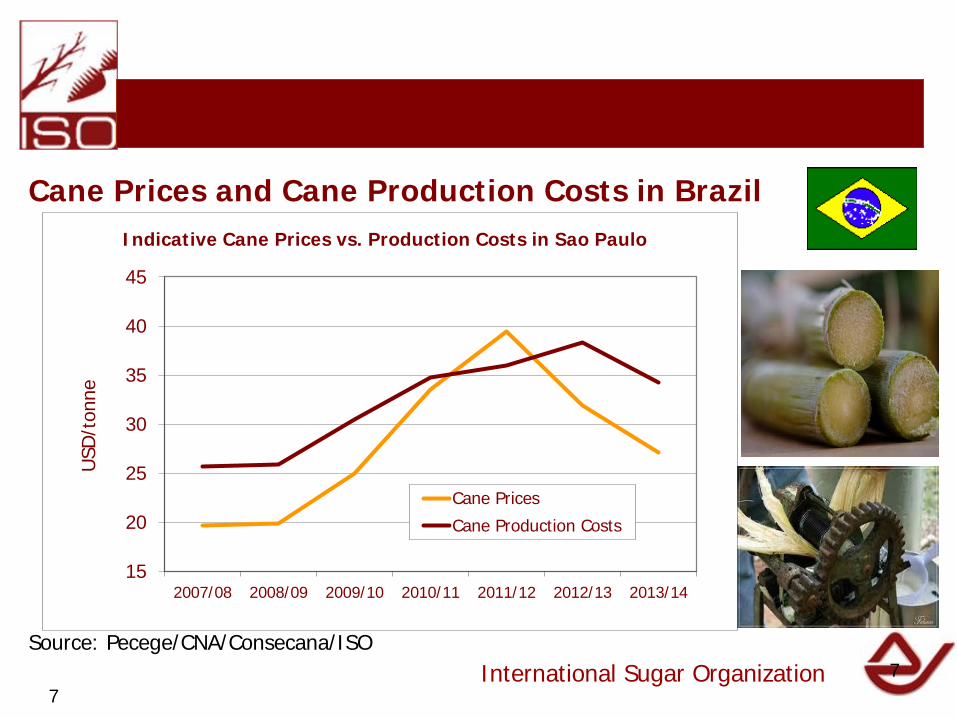

Cane Prices and Cane Production Costs in Brazil

Source: Pecege/CNA/Consecana/ISO

15

20

25

30

35

40

45

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

USD

/ton

ne

Indicative Cane Prices vs. Production Costs in Sao Paulo

Cane Prices

Cane Production Costs

7

International Sugar Organization 8

Revenues from sugar are 40% lower than in 2011 – Ethanol revenues down only 15%

Source: ISO

05

1015202530354045

2007 2008 2009 2010 2011 2012 2013

Estimated Total Revenues from Sugar/Ethanol in Brazil, in Bln USD

Sugar

Ethanol

Total

8

International Sugar Organization

The Ethanol Market in 2014 and Beyond

9

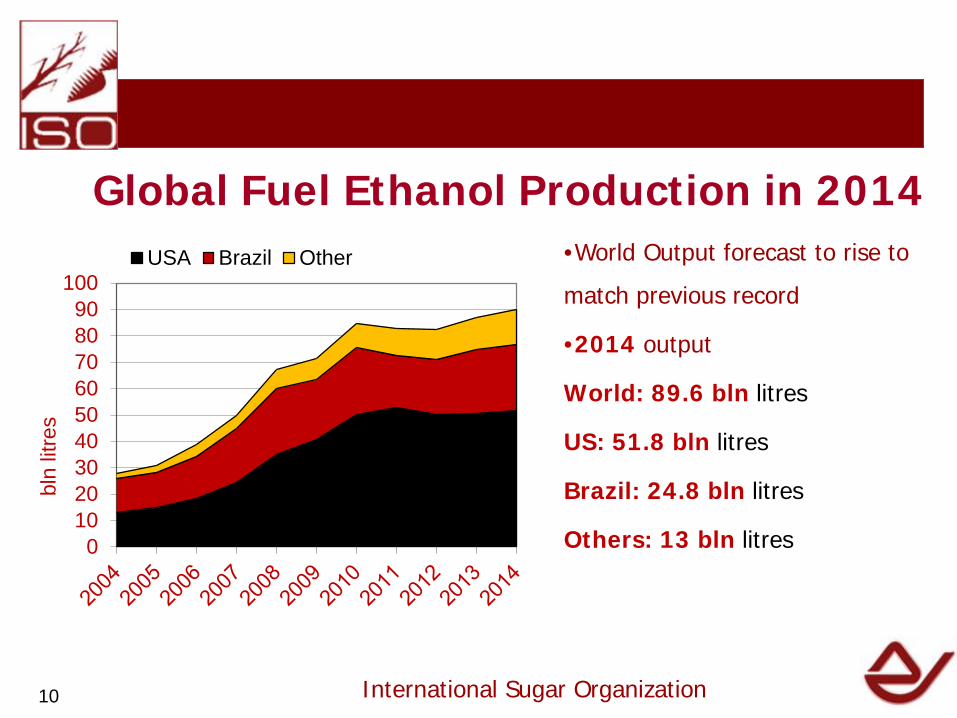

Global Fuel Ethanol Production in 2014

International Sugar Organization

•World Output forecast to rise to

match previous record

•2014 output

World: 89.6 bln litres

US: 51.8 bln litres

Brazil: 24.8 bln litres

Others: 13 bln litres 0102030405060708090

100

bln

litre

s

USA Brazil Other

10

Fuel Ethanol Production, outside USA and Brazil

International Sugar Organization

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

EU China Canada Thailand India Australia Argentina Colombia

mln

litr

es 2010 2011 2012 2013e 2014f

Among other producers, EU already had record output in 2013; strong

growth for Thailand and Argentina in both 2013 and 2014.

11

In other countries: FDI and blend mandates should encourage ethanol output growth

Country Blend % Time

Argentina E5 2010

Peru, Uruguay E8 2011

Bolivia E10 2010

Canada E-5 2008

China E-5 2008

Colombia E-10 2008

Dominican Rep. E-7.5 authorised

Ethiopia E-5 2009

India E-10 In 17 of 25 states

Indonesia E-10 2009

Jamaica E-10 2009

Kenya E-10 Future date

Malaysia E-5 2010

Mexico E-5 2012

Paraguay E-25 2010

Philippines E-5 2009

Vietnam E-5 2009

International Sugar Organization 12

13 13

International Sugar Organization

Global Fuel Ethanol Demand to 2020

Top consumers of Fuel Ethanol United States – 75 bln litres (RFS2) Brazil 35 bln litres EU (28) 11 bln litres China - 8 bln litres Others 28 bln litres World Total – 157 bln litres – Up 80% from today’s level, in part counting on success of second generation ethanol demand in the US. 13

Brazil contraction affecting world trade in 2014 – more countries needed

(Mln Litres)

EU,100 US, 900

EU, 500

Canada, 1,000

Brazil, 300

Caribbean, 100

Thailand to Philippines, 100

Asia, 400

International Sugar Organization 14

International Sugar Organization

Bioplastics and Cogeneration

15

• Annual production capacity expected to rise from 1.4 mln tonnes in 2012 to 6.2 million tonnes by 2017.

• Production in the EU may require 1.2 mln tonnes of sugar by 2020.

• Some are less optimistic for demand growth, but here sustainability is key if marketed correctly by the industry.

Bioplastics

International Sugar Organization 16

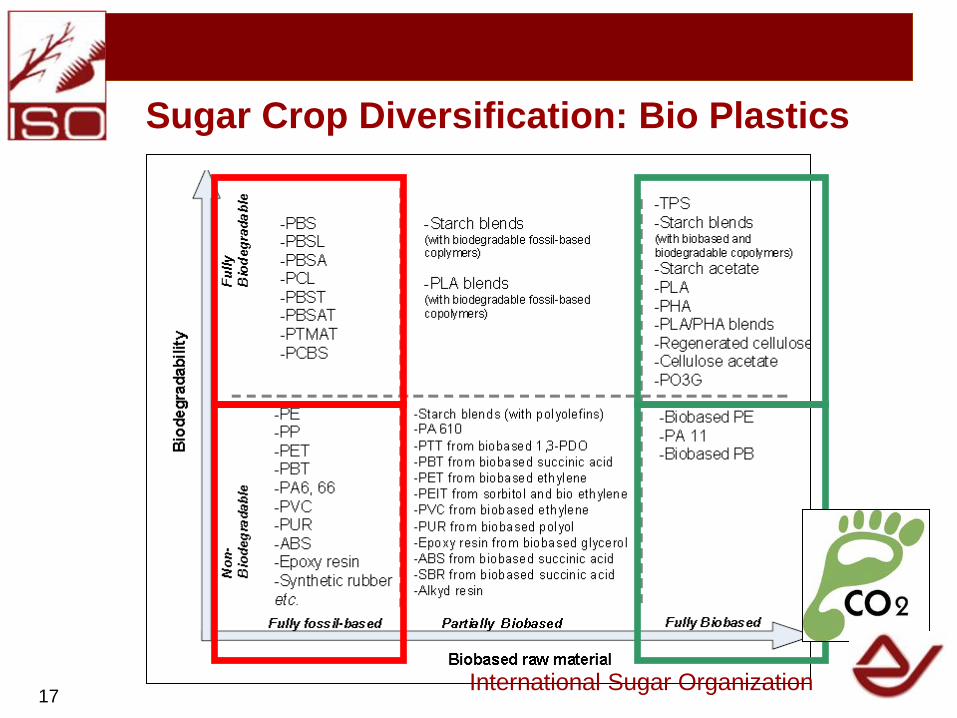

Sugar Crop Diversification: Bio Plastics

International Sugar Organization 17

18

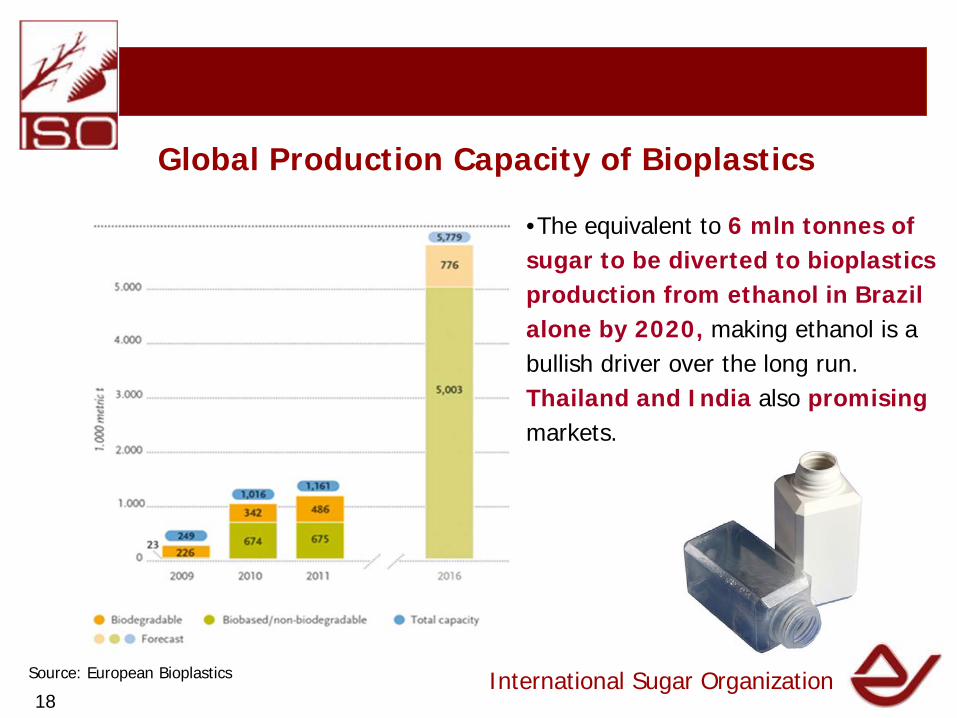

Global Production Capacity of Bioplastics

Source: European Bioplastics International Sugar Organization

•The equivalent to 6 mln tonnes of sugar to be diverted to bioplastics production from ethanol in Brazil alone by 2020, making ethanol is a bullish driver over the long run. Thailand and India also promising markets.

18

Cogeneration in Brazil

International Sugar Organization

0200400600800

1,0001,2001,4001,6001,8002,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Electricity Exported to the Grid, Brazil, in average MW

10

60

110

160

210

260

310

360

2005 2006 2007 2008 2009 2010 2011 2012 2013

Spot Electricity Prices in Brazil as of end-May, in BRL/MWh

19

20

Brazil

India

Thailand

Cost Rica Guatemala

Mauritius

Réunion

El Salvador

Pakistan

Australia

Uganda Kenya Philippines

South Africa

Colombia

Swaziland

Mexico Vietnam

Honduras

Nicaragua

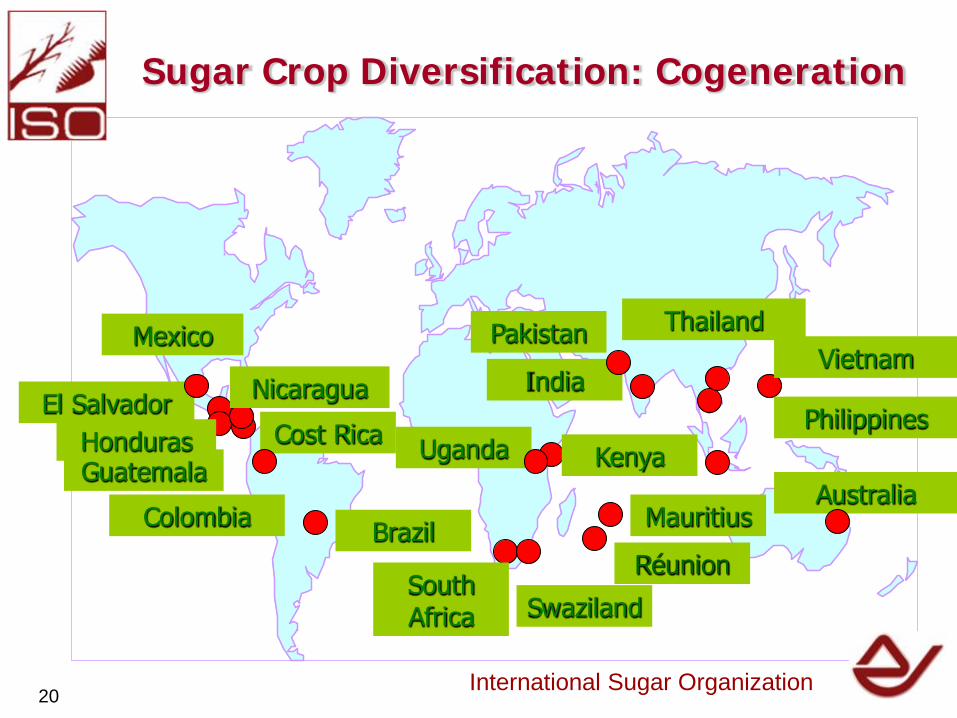

Sugar Crop Diversification: Cogeneration

International Sugar Organization 20

0 500 1000 1500 20001998-99

2000-01

2002-03

2004-05

2006-07

2008-09

2010-11

2012-13

Evolution of Sugar Mill Cogeneration with Bagasse

GWh

International Sugar Organization

Cogeneration in Guatemala

21

International Sugar Organization

Conclusions – Diversifying away from Sugar?

Small sugar surplus projected for 2014/15: 1) Higher output projected for India, EU, Russia and Ukraine; 2) But key producer Brazil facing shrinking revenues from sugar ; 3) Rapid consumption growth in Asia provides bullish outlook over the

longer-term.

In the meantime, countries should be focusing on alternative sources of revenue, like fuel ethanol, bioplastics and cane-bagasse cogeneration.

22

23

Conclusions – Ethanol, Bioplastics and Cogeneration

• World record output for fuel ethanol in 2014.

• The equivalent of 6 mln tonnes of sugar to be diverted to bioplastics production from ethanol in Brazil alone by 2020. Bullish for the Longer Term.

• World fuel ethanol demand/supply to grow by 80% to 157 bln litres by 2020.

• Record spot market electricity prices in Brazil providing an unmissable opportunity to cane bagasse cogeneration.

International Sugar Organization 23

Tuesday 25 - Wednesday 26 November 2014

23rd ISO Seminar

“Sugar and Ethanol: Fresh Options“

Canary Wharf, London.

www.isosugar.org

International Sugar Organization

Thank you!