curr futures

TRANSCRIPT

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 1/68

CURRENCY AND INTEREST RATEFUTURES

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 2/68

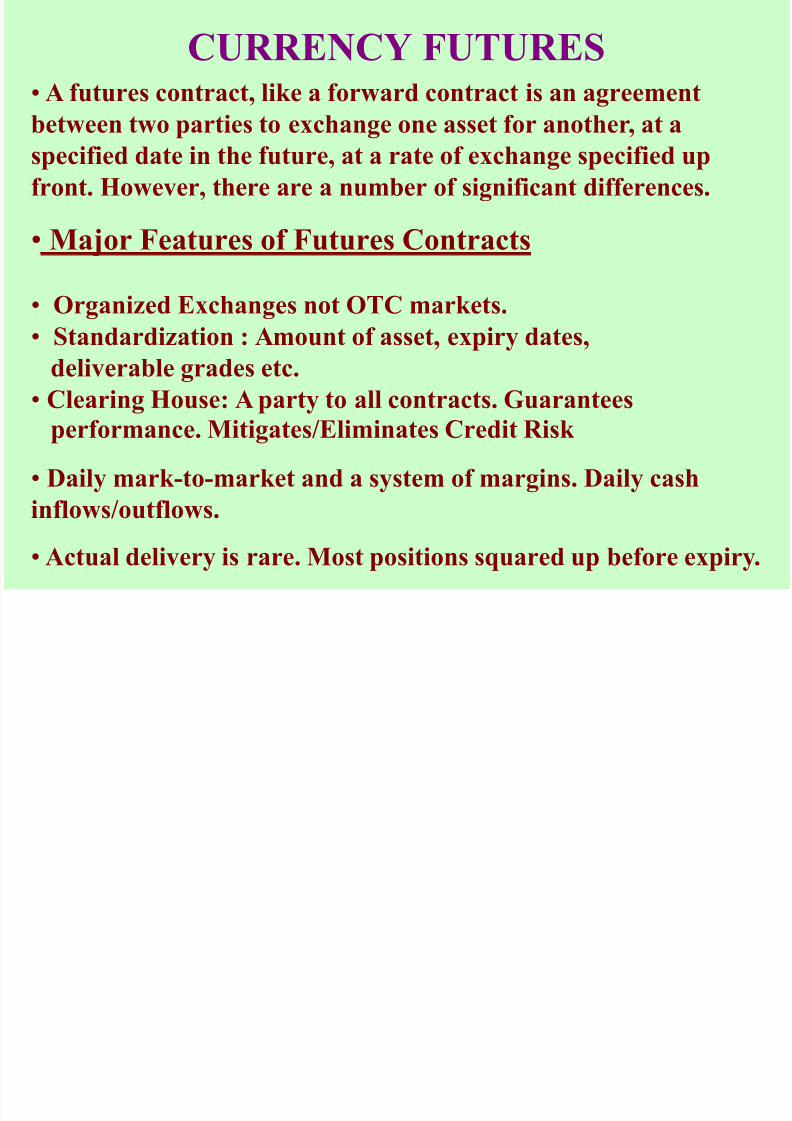

CURRENCY FUTURES• A futures contract, like a forward contract is an agreement

between two parties to exchange one asset for another, at aspecified date in the future, at a rate of exchange specified up

front. However, there are a number of significant differences.

• Major Features of Futures Contracts

• Organized Exchanges not OTC markets.

• Standardization : Amount of asset, expiry dates,

deliverable grades etc.

• Clearing House: A party to all contracts. Guarantees

performance. Mitigates/Eliminates Credit Risk • Daily mark-to-market and a system of margins. Daily cash

inflows/outflows.

• Actual delivery is rare. Most positions squared up before expiry.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 3/68

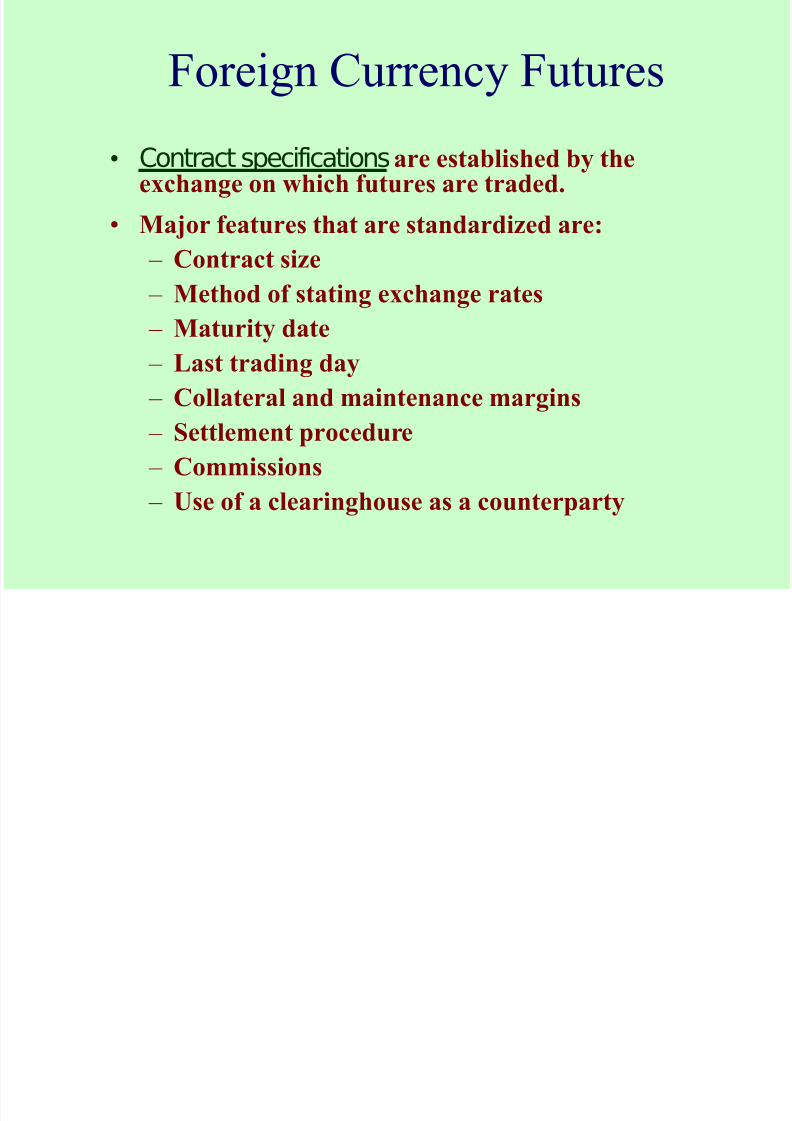

Foreign Currency Futures

• Contract specificationsare established by theexchange on which futures are traded.

• Major features that are standardized are:

– Contract size

– Method of stating exchange rates

– Maturity date

– Last trading day

– Collateral and maintenance margins

– Settlement procedure

– Commissions

– Use of a clearinghouse as a counterparty

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 4/68

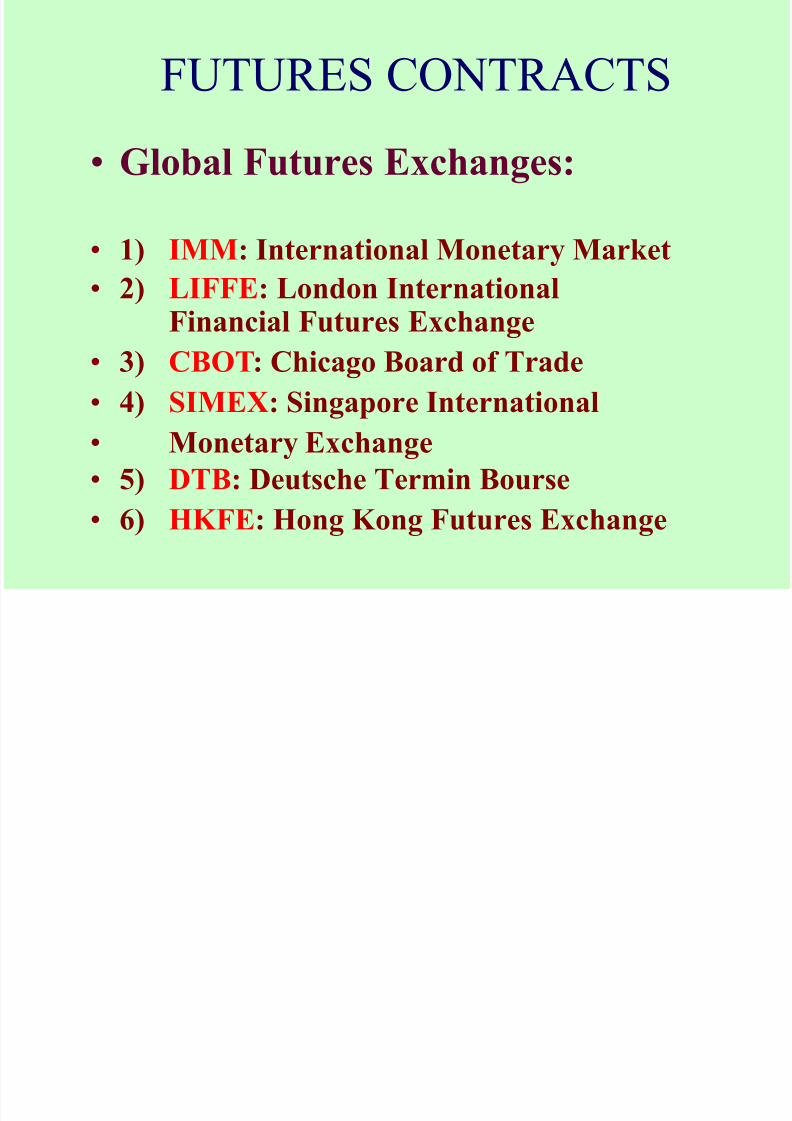

FUTURES CONTRACTS

• Global Futures Exchanges:

• 1) IMM: International Monetary Market

• 2) LIFFE: London InternationalFinancial Futures Exchange

• 3) CBOT: Chicago Board of Trade

•

4) SIMEX: Singapore International• Monetary Exchange

• 5) DTB: Deutsche Termin Bourse

• 6) HKFE: Hong Kong Futures Exchange

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 5/68

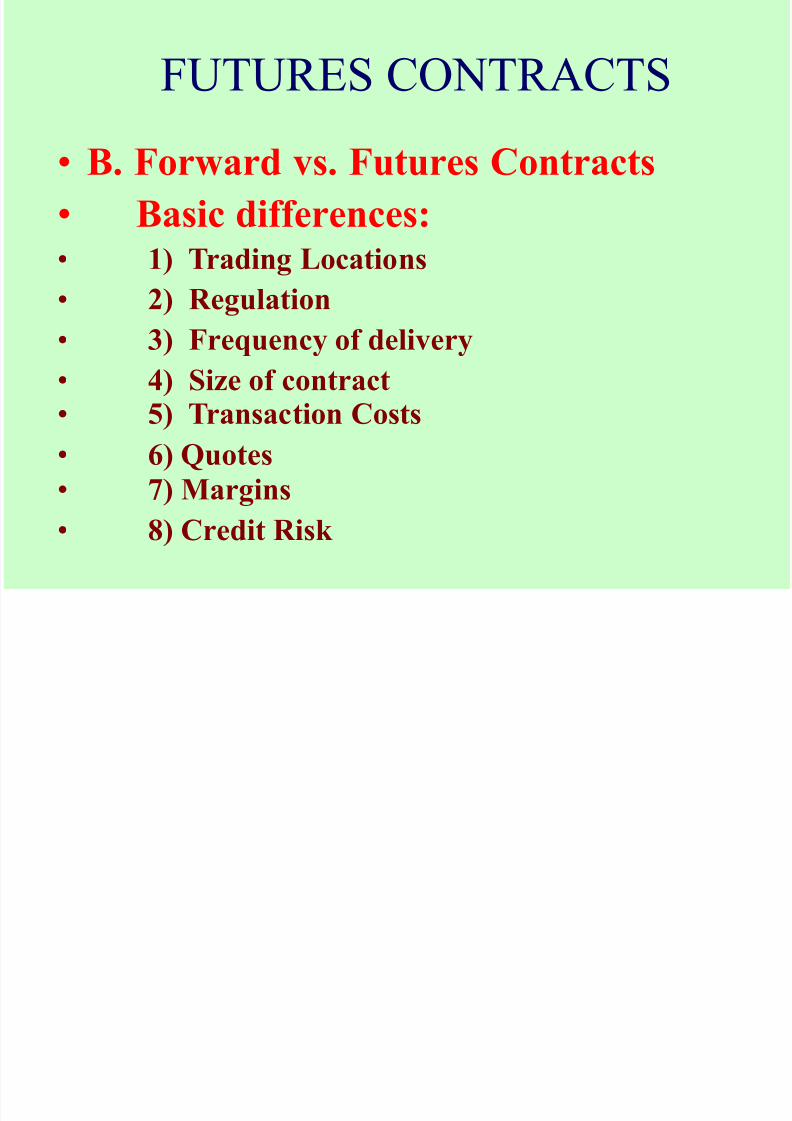

FUTURES CONTRACTS

• B. Forward vs. Futures Contracts

• Basic differences:• 1) Trading Locations

• 2) Regulation

• 3) Frequency of delivery

• 4) Size of contract

• 5) Transaction Costs• 6) Quotes • 7) Margins

• 8) Credit Risk

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 6/68

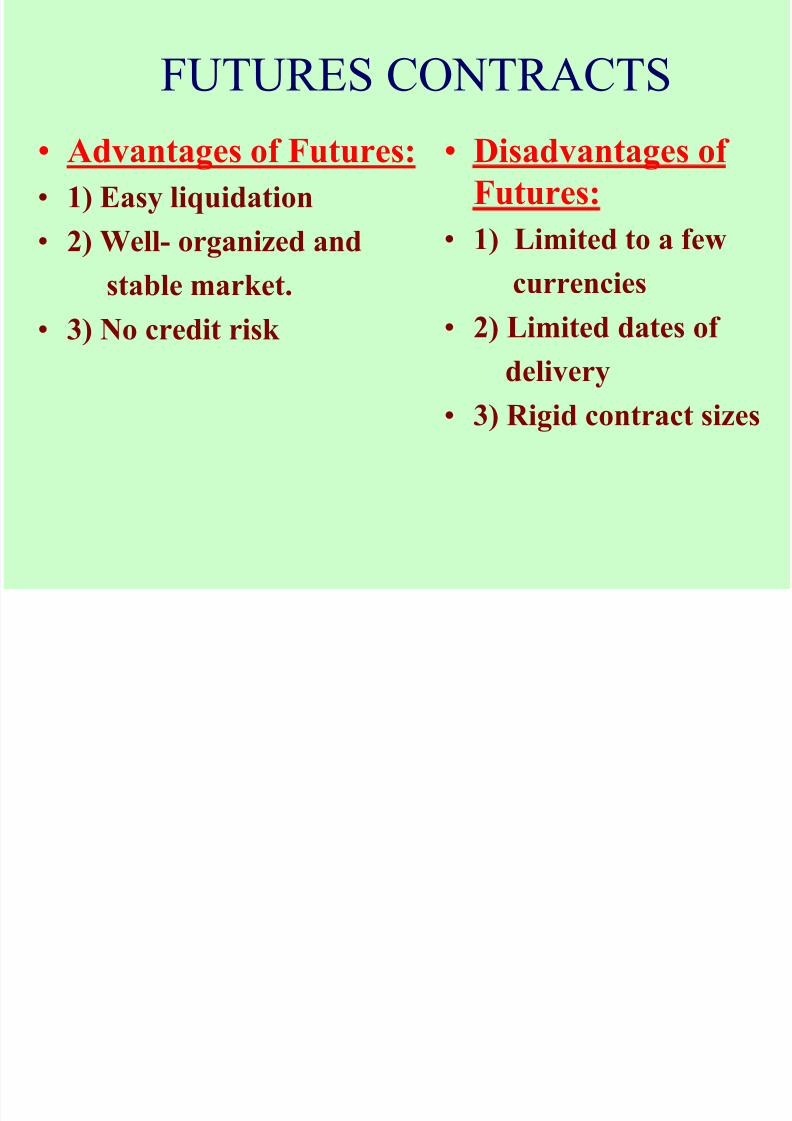

FUTURES CONTRACTS

• Advantages of Futures:

• 1) Easy liquidation

• 2) Well- organized and

stable market.

• 3) No credit risk

• Disadvantages of

Futures:

• 1) Limited to a few

currencies

• 2) Limited dates of

delivery

• 3) Rigid contract sizes

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 7/68

FUTURES CONTRACTS ON IMM

• Available Futures Currencies/Contract Size:

• 1) British pound / 62500

•

2) Canadian dollar /100000• 3) Euro / 125000

• 4) Swiss franc / 125000

•

5) Japanese yen / 12.5 million• 6) Mexican peso / 500000

• 7) Australian dollar / 100000

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 8/68

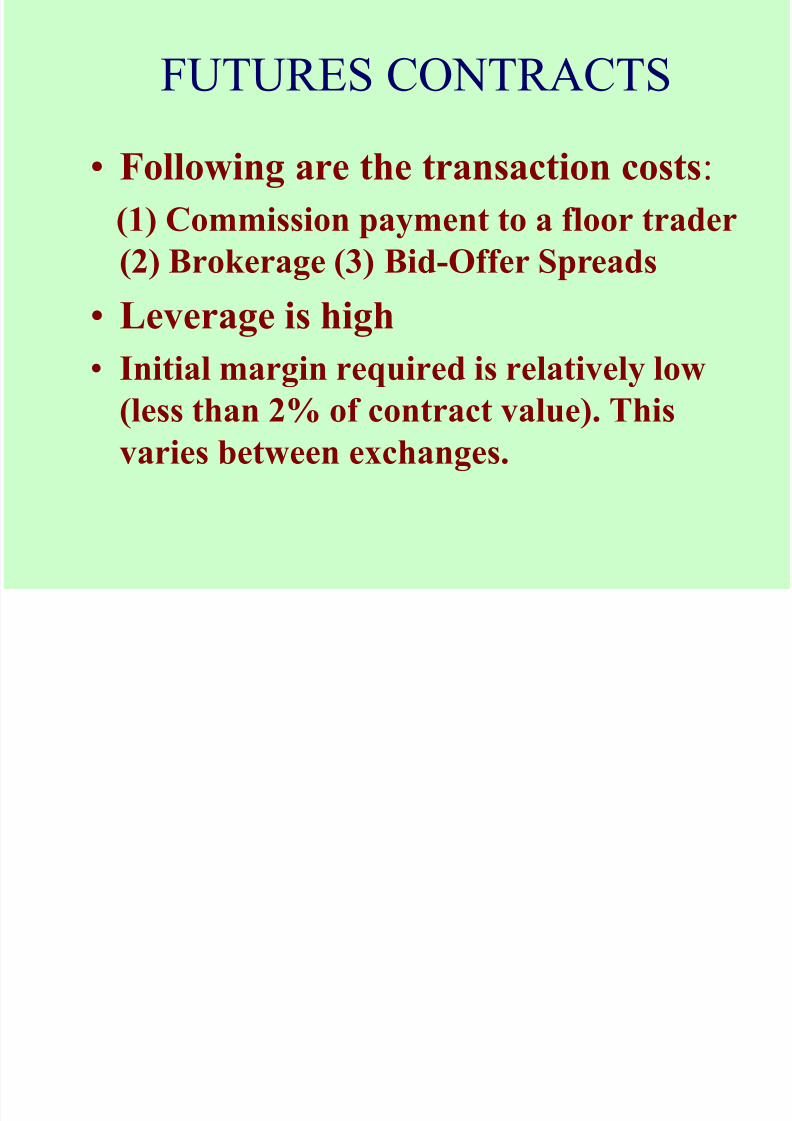

FUTURES CONTRACTS

• Following are the transaction costs:

(1) Commission payment to a floor trader

(2) Brokerage (3) Bid-Offer Spreads• Leverage is high

• Initial margin required is relatively low

(less than 2% of contract value). Thisvaries between exchanges.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 9/68

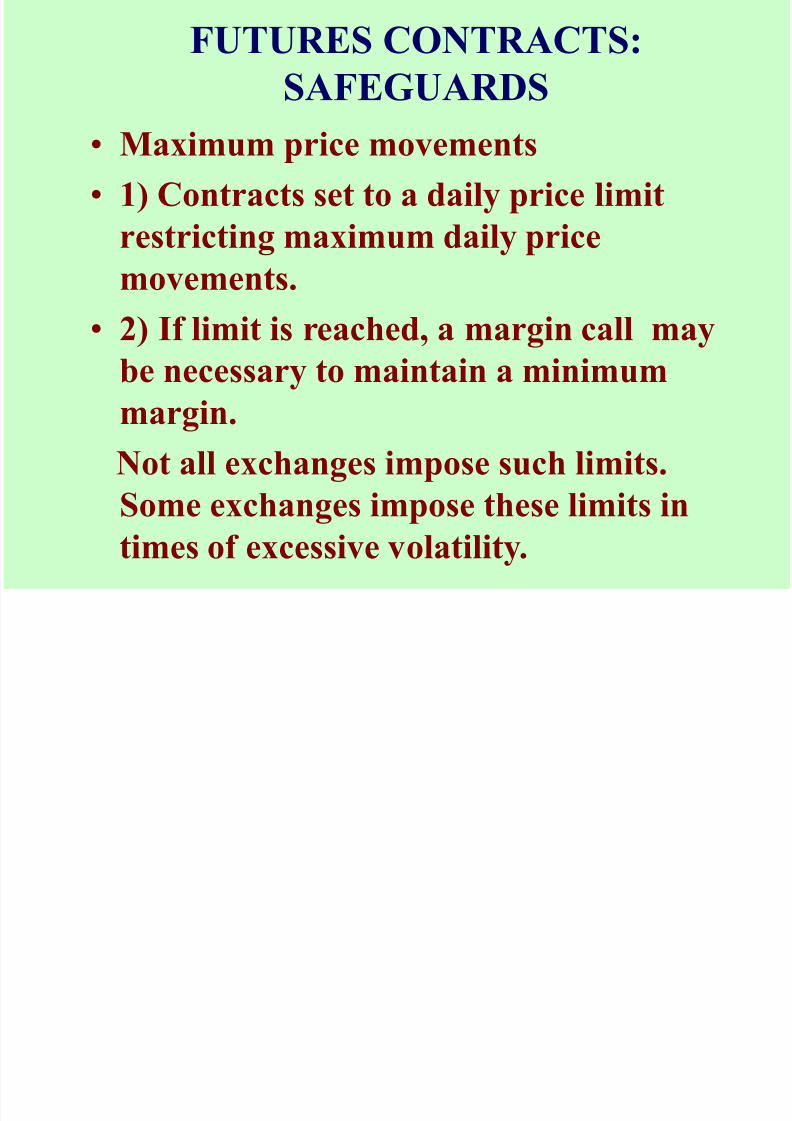

FUTURES CONTRACTS:

SAFEGUARDS

• Maximum price movements

• 1) Contracts set to a daily price limit

restricting maximum daily price

movements.

• 2) If limit is reached, a margin call may

be necessary to maintain a minimum

margin.Not all exchanges impose such limits.

Some exchanges impose these limits in

times of excessive volatility.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 10/68

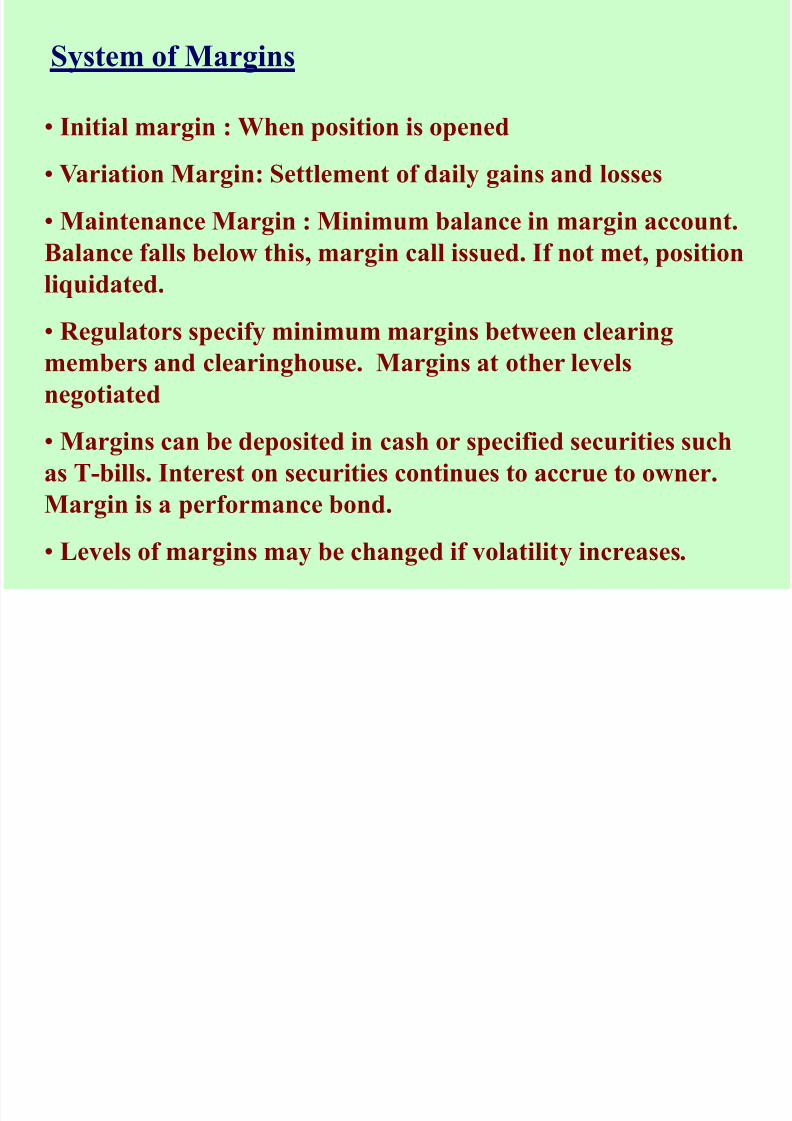

System of Margins

•

Initial margin : When position is opened• Variation Margin: Settlement of daily gains and losses

• Maintenance Margin : Minimum balance in margin account.

Balance falls below this, margin call issued. If not met, position

liquidated.

• Regulators specify minimum margins between clearing

members and clearinghouse. Margins at other levels

negotiated

• Margins can be deposited in cash or specified securities such

as T-bills. Interest on securities continues to accrue to owner.

Margin is a performance bond.

• Levels of margins may be changed if volatility increases.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 11/68

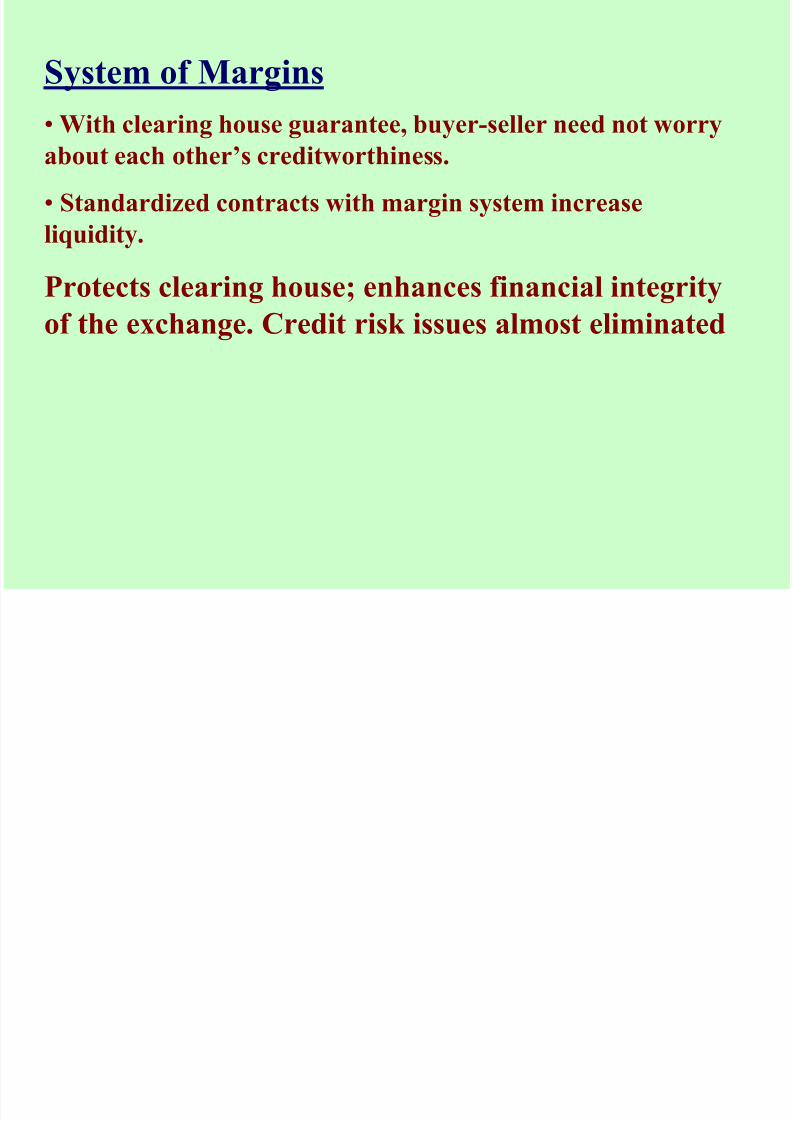

System of Margins

• With clearing house guarantee, buyer-seller need not worry

about each other’s creditworthiness.

• Standardized contracts with margin system increase

liquidity.

Protects clearing house; enhances financial integrity

of the exchange. Credit risk issues almost eliminated

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 12/68

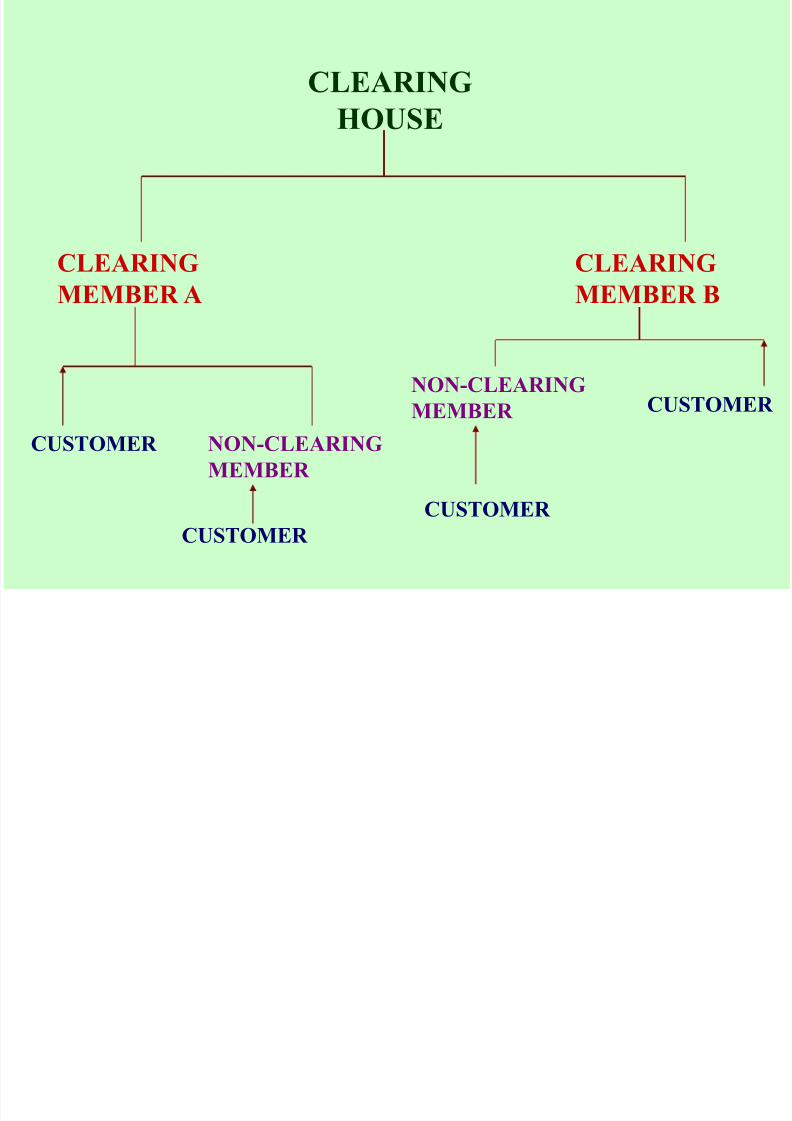

CLEARING

HOUSE

CLEARING

MEMBER A

CLEARING

MEMBER B

NON-CLEARING

MEMBER

CUSTOMER

CUSTOMER

NON-CLEARING

MEMBER CUSTOMER

CUSTOMER

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 13/68

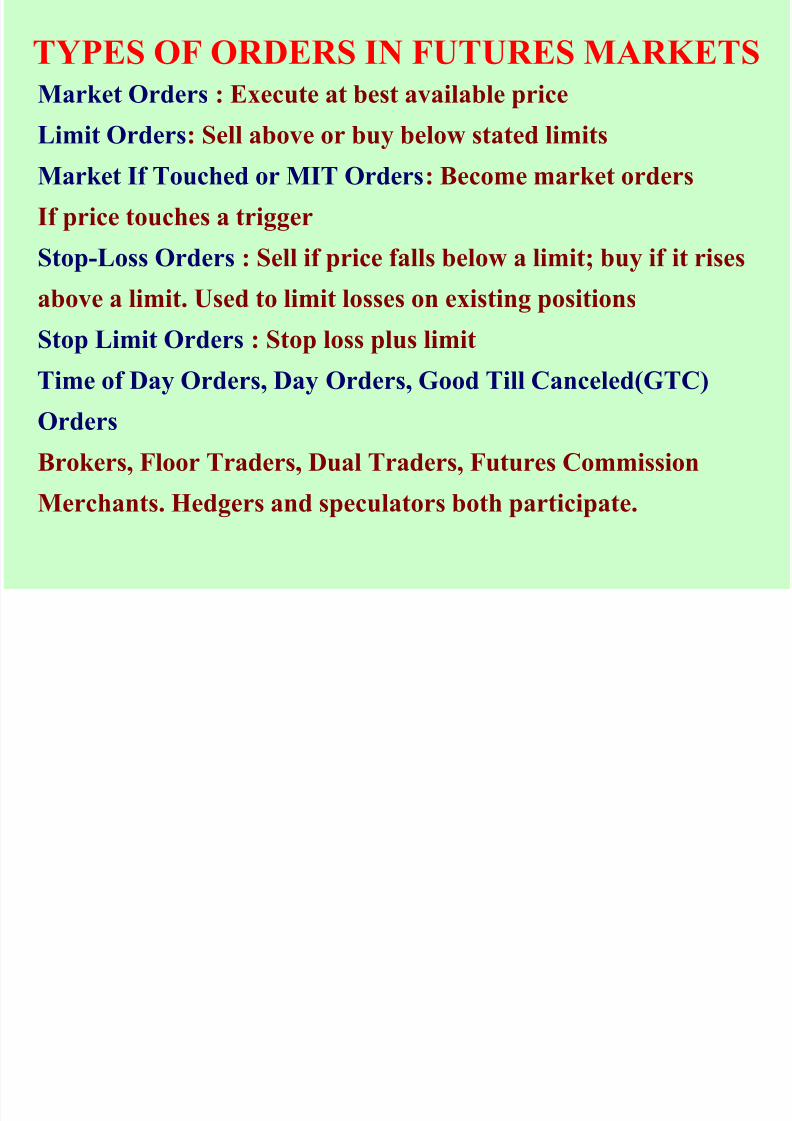

TYPES OF ORDERS IN FUTURES MARKETSMarket Orders : Execute at best available price

Limit Orders: Sell above or buy below stated limitsMarket If Touched or MIT Orders: Become market orders

If price touches a trigger

Stop-Loss Orders : Sell if price falls below a limit; buy if it rises

above a limit. Used to limit losses on existing positions

Stop Limit Orders : Stop loss plus limit

Time of Day Orders, Day Orders, Good Till Canceled(GTC)

Orders

Brokers, Floor Traders, Dual Traders, Futures Commission

Merchants. Hedgers and speculators both participate.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 14/68

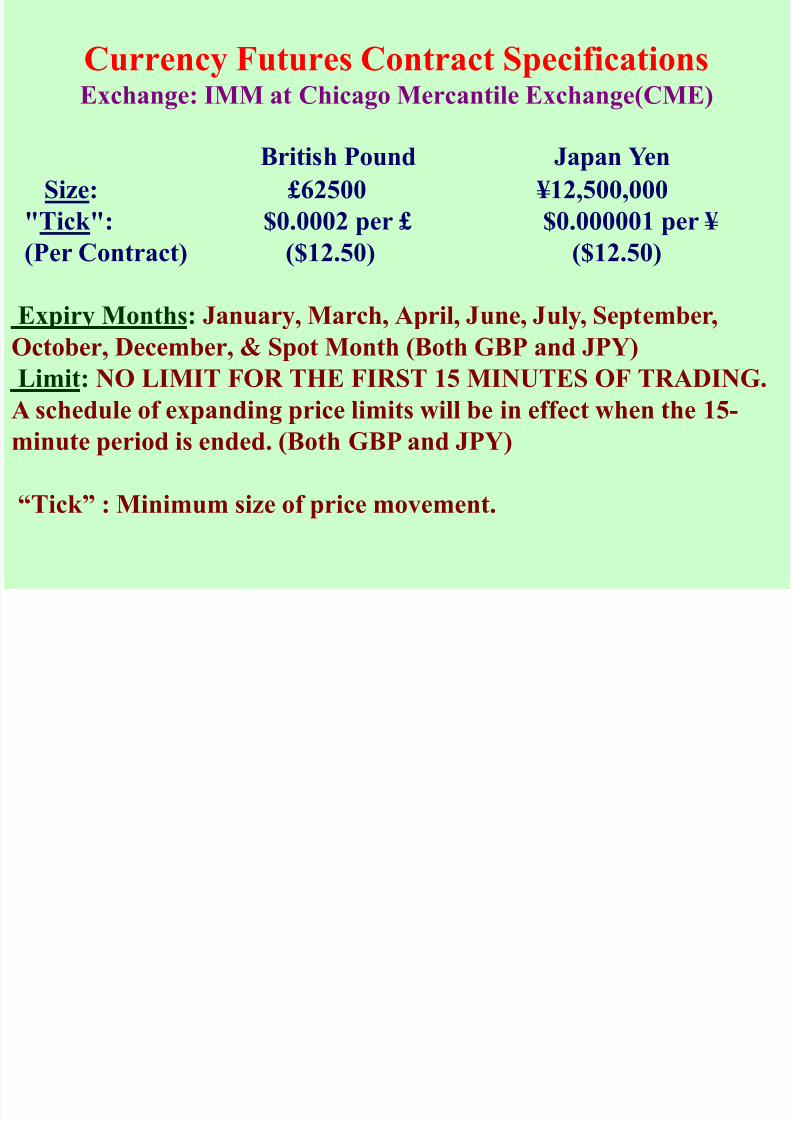

Currency Futures Contract Specifications Exchange: IMM at Chicago Mercantile Exchange(CME)

British Pound Japan Yen Size: £62500 ¥12,500,000

"Tick": $0.0002 per £ $0.000001 per ¥

(Per Contract) ($12.50) ($12.50)

Expiry Months: January, March, April, June, July, September,

October, December, & Spot Month (Both GBP and JPY)

Limit: NO LIMIT FOR THE FIRST 15 MINUTES OF TRADING.

A schedule of expanding price limits will be in effect when the 15-minute period is ended. (Both GBP and JPY)

“Tick” : Minimum size of price movement.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 15/68

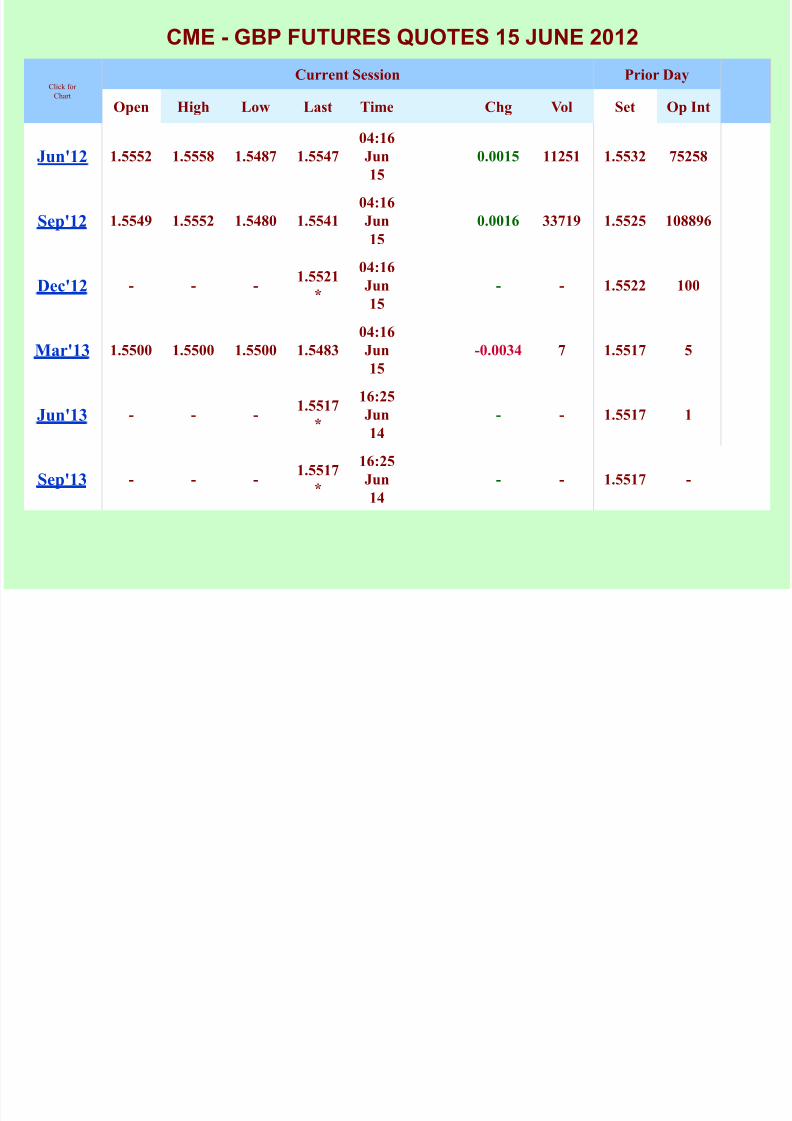

Click for

Chart

Current Session Prior Day

Open High Low Last Time Chg Vol Set Op Int

Jun'12 1.5552 1.5558 1.5487 1.554704:16Jun

15 0.0015 11251 1.5532 75258

Sep'12 1.5549 1.5552 1.5480 1.5541

04:16

Jun

15 0.0016 33719 1.5525 108896

Dec'12 - - - 1.5521*

04:16

Jun

15 - - 1.5522 100

Mar'13 1.5500 1.5500 1.5500 1.5483

04:16

Jun

15 -0.0034 7 1.5517 5

Jun'13 - - - 1.5517

*

16:25

Jun14

- - 1.5517 1

Sep'13 - - - 1.5517

*

16:25

Jun

14 - - 1.5517 -

CME - GBP FUTURES QUOTES 15 JUNE 2012

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 16/68

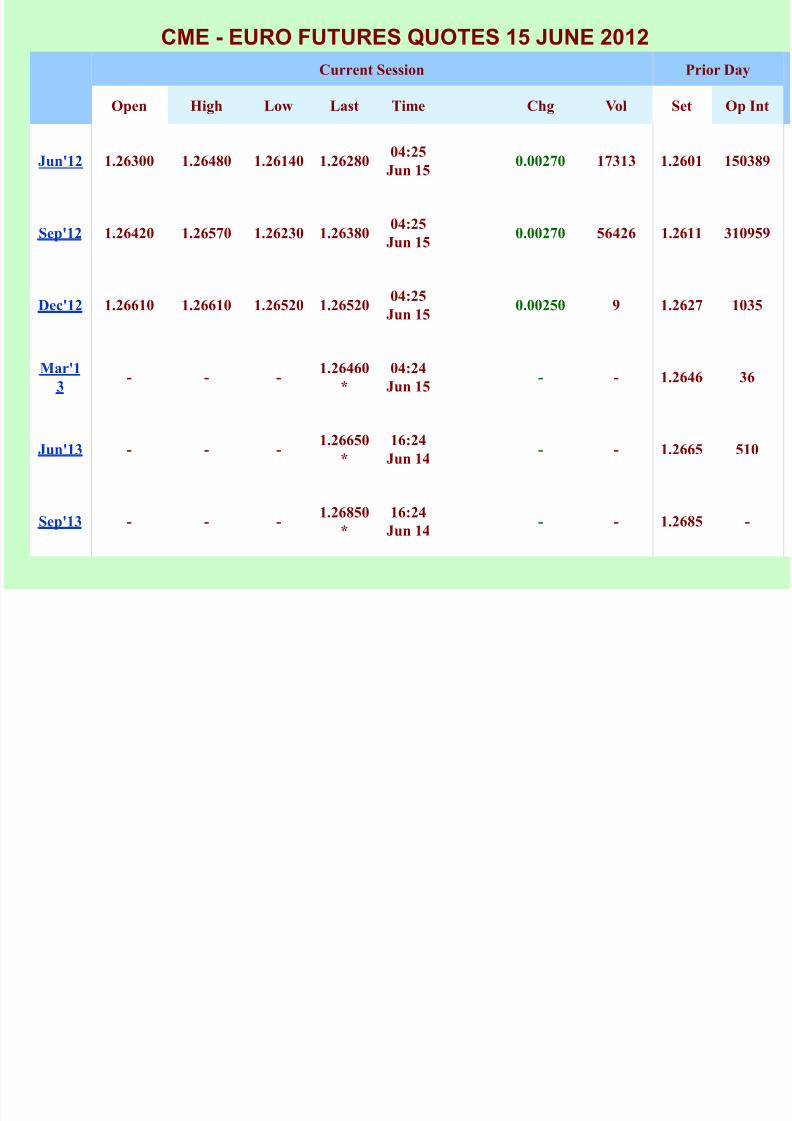

Current Session Prior Day

Open High Low Last Time Chg Vol Set Op Int

Jun'12 1.26300 1.26480 1.26140 1.2628004:25

Jun 15 0.00270 17313 1.2601 150389

Sep'12 1.26420 1.26570 1.26230 1.2638004:25

Jun 15 0.00270 56426 1.2611 310959

Dec'12 1.26610 1.26610 1.26520 1.2652004:25

Jun 15 0.00250 9 1.2627 1035

Mar'1

3 - - -

1.26460

* 04:24

Jun 15 - - 1.2646 36

Jun'13 - - - 1.26650

* 16:24

Jun 14 - - 1.2665 510

Sep'13 - - - 1.26850

* 16:24

Jun 14 - - 1.2685 -

CME - EURO FUTURES QUOTES 15 JUNE 2012

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 17/68

Click for

Chart

Current Session Prior Day

Open High Low Last Time Set Chg Vol Set Op Int

Jun'12 1.05120 1.05310 1.05050 1.0516004:33

Jun 15 - 0.00250 2741 1.04910 43533

Sep'12 1.05410 1.05540 1.05270 1.0540004:33

Jun 15 - 0.00250 9802 1.05150 54758

Dec'12 - - - 1.05480

* 04:32

Jun 15 - - - 1.05480 6

Mar'13 - - - 1.05780

* 04:33

Jun 15 - - - 1.05780 3

Jun'13 - - - 1.06190

* 16:27

Jun 14 - - - 1.06190 -

Sep'13 - - - 1.06500

* 16:27

Jun 14 - - - 1.06500 -

CME - CHF FUTURES QUOTES 15 JUNE 2012

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 18/68

CURRENCY FUTURES IN INDIA

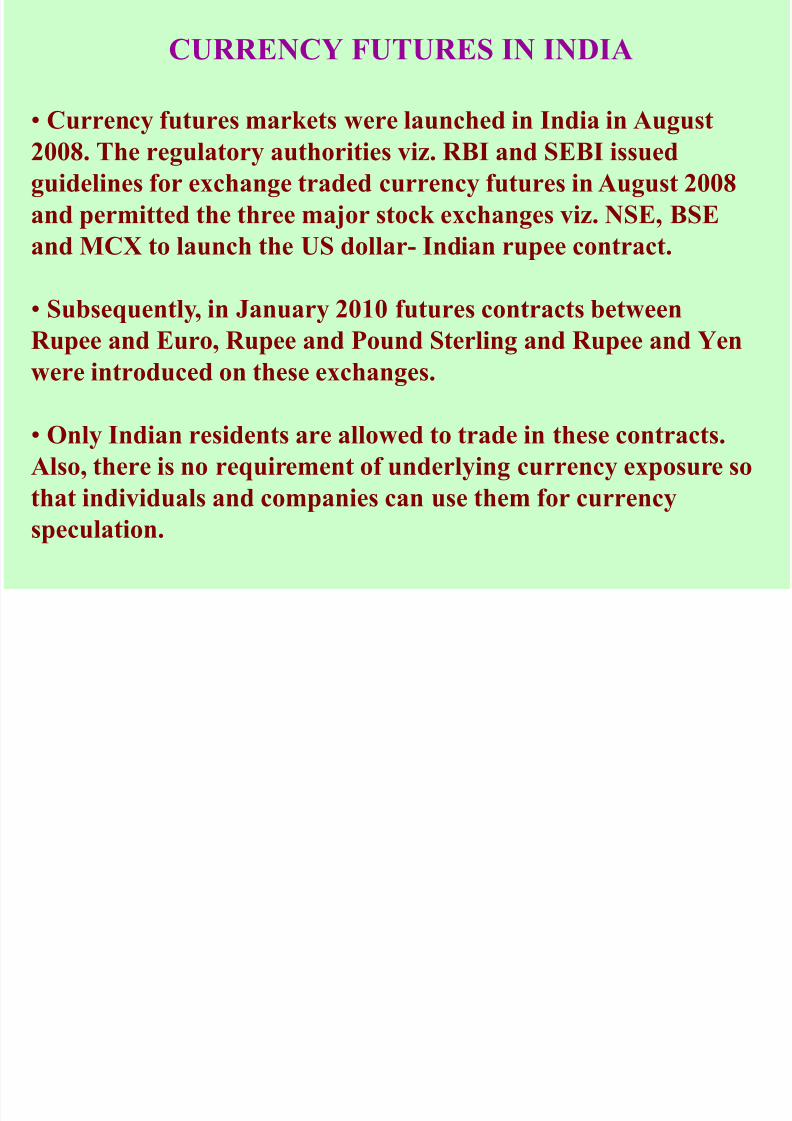

• Currency futures markets were launched in India in August

2008. The regulatory authorities viz. RBI and SEBI issued

guidelines for exchange traded currency futures in August 2008

and permitted the three major stock exchanges viz. NSE, BSE

and MCX to launch the US dollar- Indian rupee contract.

• Subsequently, in January 2010 futures contracts between

Rupee and Euro, Rupee and Pound Sterling and Rupee and Yen

were introduced on these exchanges.

• Only Indian residents are allowed to trade in these contracts.

Also, there is no requirement of underlying currency exposure so

that individuals and companies can use them for currency

speculation.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 19/68

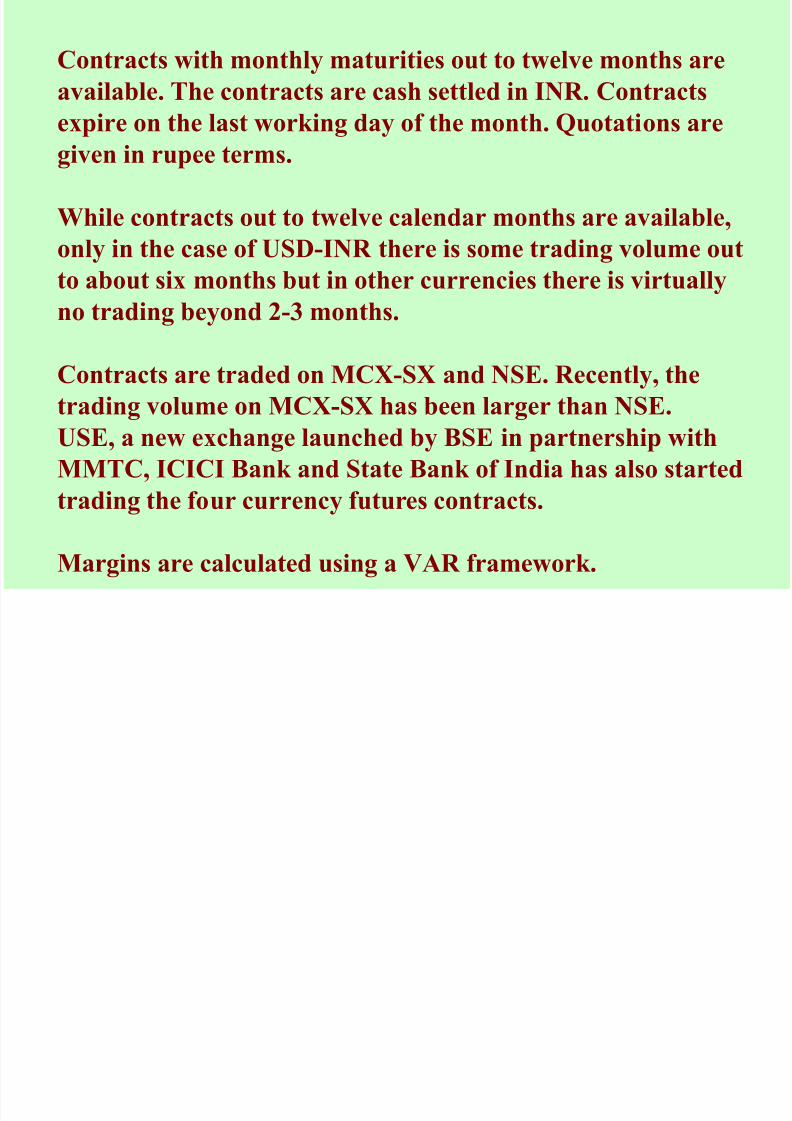

Contracts with monthly maturities out to twelve months are

available. The contracts are cash settled in INR. Contracts

expire on the last working day of the month. Quotations are

given in rupee terms.

While contracts out to twelve calendar months are available,

only in the case of USD-INR there is some trading volume out

to about six months but in other currencies there is virtuallyno trading beyond 2-3 months.

Contracts are traded on MCX-SX and NSE. Recently, the

trading volume on MCX-SX has been larger than NSE.USE, a new exchange launched by BSE in partnership with

MMTC, ICICI Bank and State Bank of India has also started

trading the four currency futures contracts.

Margins are calculated using a VAR framework.

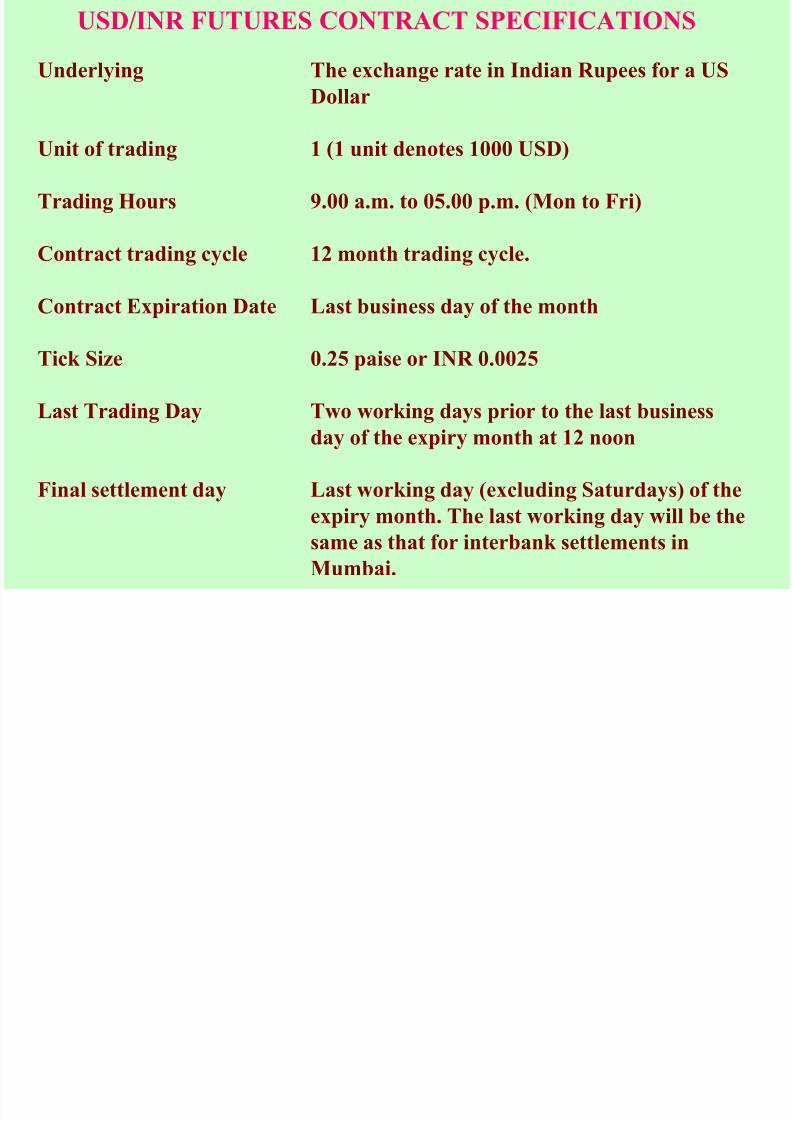

USD/INR FUTURES CONTRACT SPECIFICATIONS

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 20/68

Underlying

Unit of trading

Trading Hours

Contract trading cycle

Contract Expiration Date

Tick Size

Last Trading Day

Final settlement day

The exchange rate in Indian Rupees for a US

Dollar

1 (1 unit denotes 1000 USD)

9.00 a.m. to 05.00 p.m. (Mon to Fri)

12 month trading cycle.

Last business day of the month

0.25 paise or INR 0.0025

Two working days prior to the last businessday of the expiry month at 12 noon

Last working day (excluding Saturdays) of the

expiry month. The last working day will be the

same as that for interbank settlements in

Mumbai.

USD/INR FUTURES CONTRACT SPECIFICATIONS

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 21/68

USD/INR FUTURES CONTRACT SPECIFICATIONS

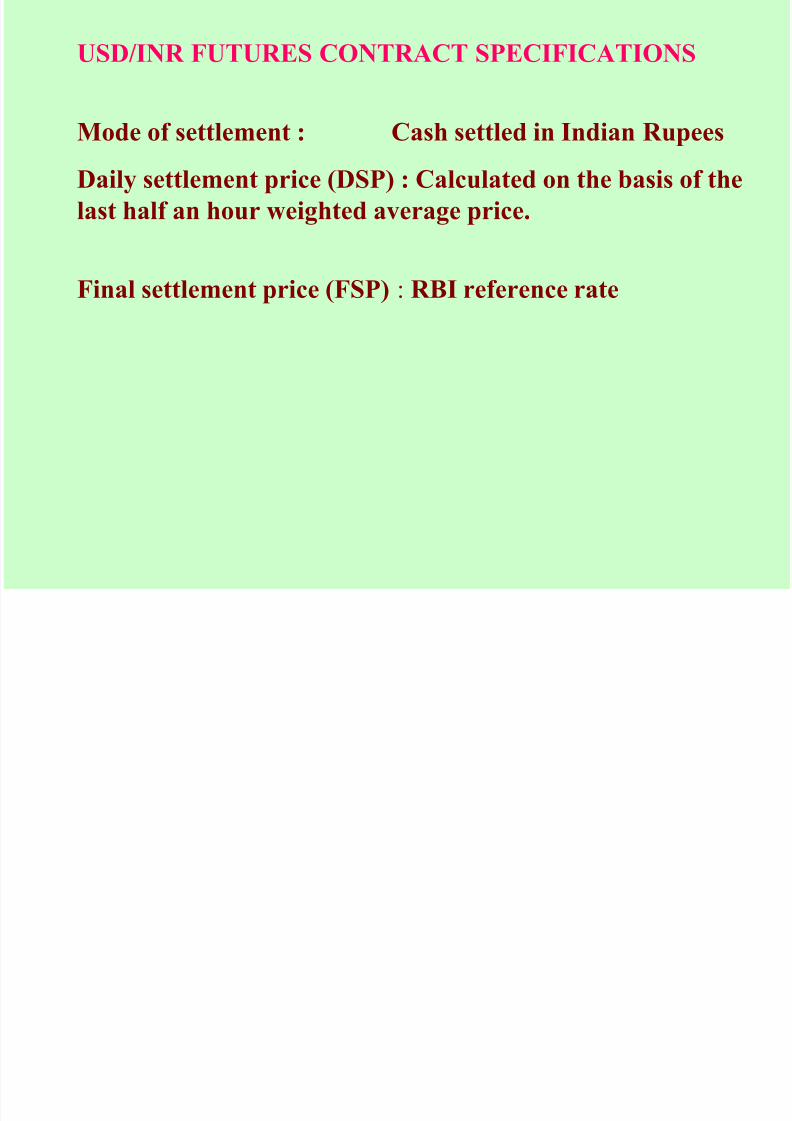

Mode of settlement : Cash settled in Indian Rupees Daily settlement price (DSP) : Calculated on the basis of the

last half an hour weighted average price.

Final settlement price (FSP) : RBI reference rate

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 22/68

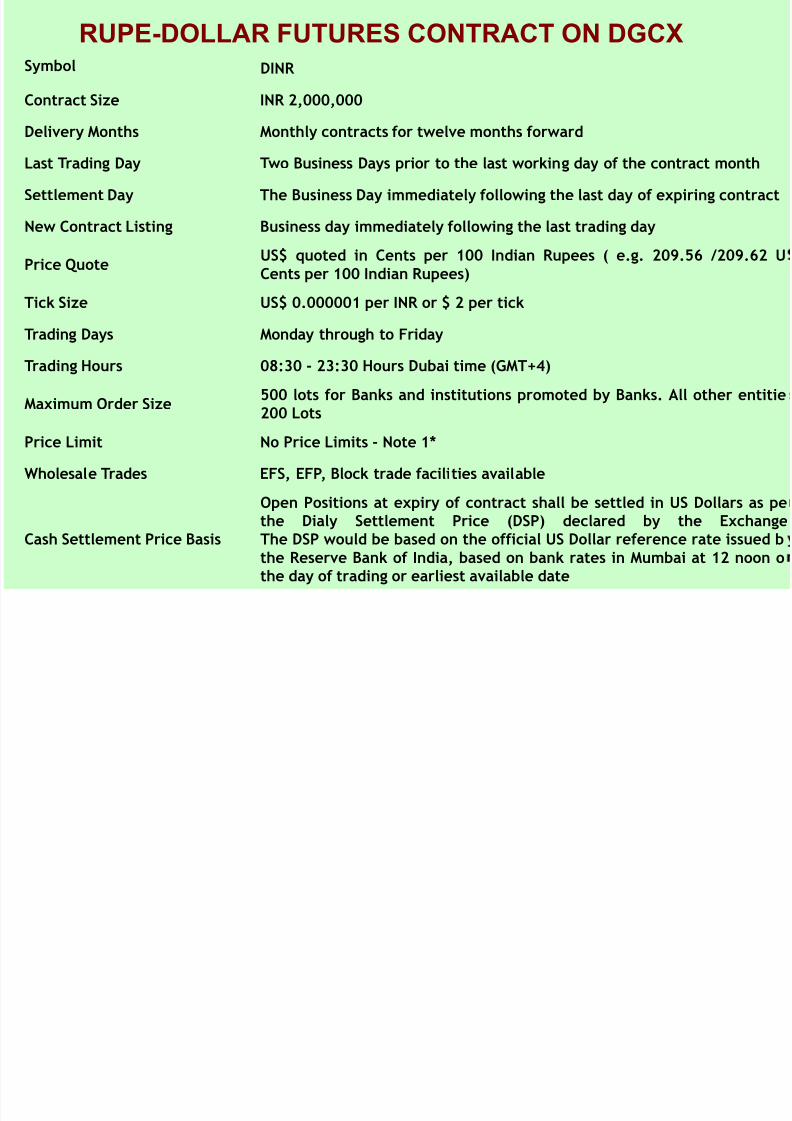

Symbol DINR

Contract Size INR 2,000,000

Delivery Months Monthly contracts for twelve months forward

Last Trading Day Two Business Days prior to the last working day of the contract month

Settlement Day The Business Day immediately following the last day of expiring contract

New Contract Listing Business day immediately following the last trading day

Price QuoteUS$ quoted in Cents per 100 Indian Rupees ( e.g. 209.56 /209.62 U

Cents per 100 Indian Rupees)Tick Size US$ 0.000001 per INR or $ 2 per tick

Trading Days Monday through to Friday

Trading Hours 08:30 - 23:30 Hours Dubai time (GMT+4)

Maximum Order Size500 lots for Banks and institutions promoted by Banks. All other entitie

200 LotsPrice Limit No Price Limits - Note 1*

Wholesale Trades EFS, EFP, Block trade facilities available

Cash Settlement Price Basis

Open Positions at expiry of contract shall be settled in US Dollars as pethe Dialy Settlement Price (DSP) declared by the ExchangeThe DSP would be based on the official US Dollar reference rate issued b

the Reserve Bank of India, based on bank rates in Mumbai at 12 noon othe day of trading or earliest available date

RUPE-DOLLAR FUTURES CONTRACT ON DGCX

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 23/68

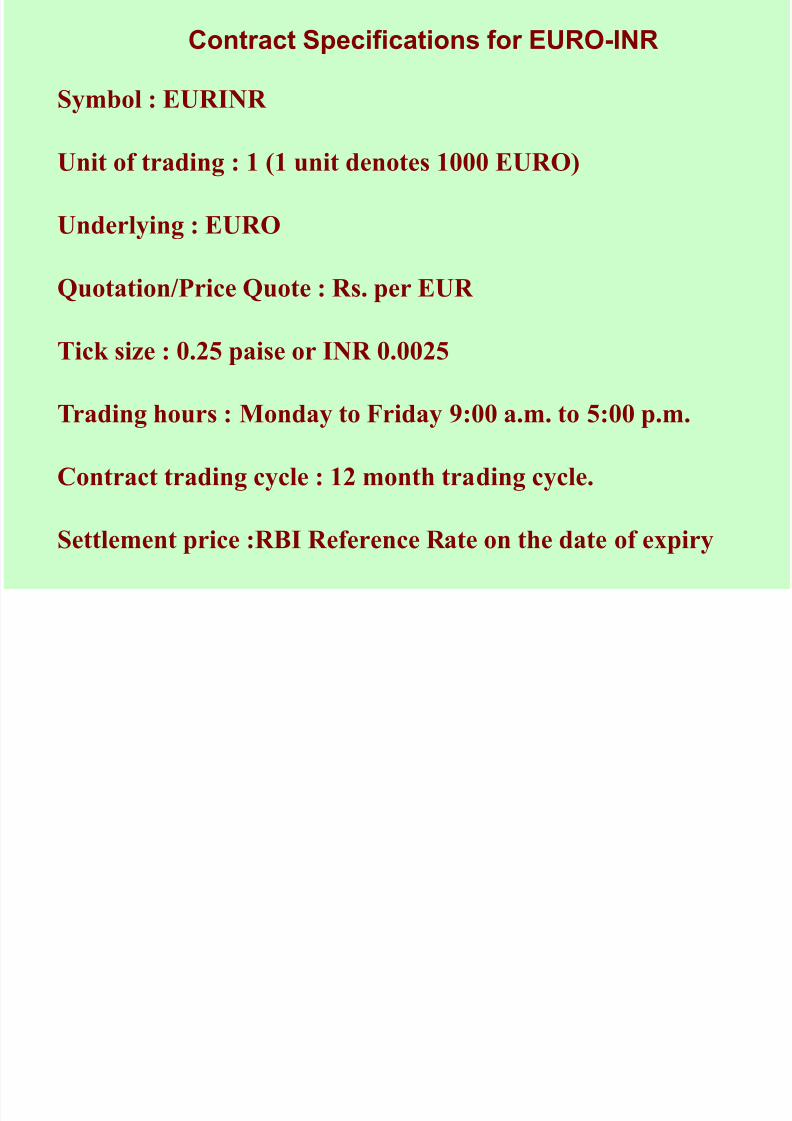

Contract Specifications for EURO-INR

Symbol : EURINR

Unit of trading : 1 (1 unit denotes 1000 EURO)

Underlying : EURO

Quotation/Price Quote : Rs. per EUR

Tick size : 0.25 paise or INR 0.0025

Trading hours : Monday to Friday 9:00 a.m. to 5:00 p.m.

Contract trading cycle : 12 month trading cycle.

Settlement price :RBI Reference Rate on the date of expiry

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 24/68

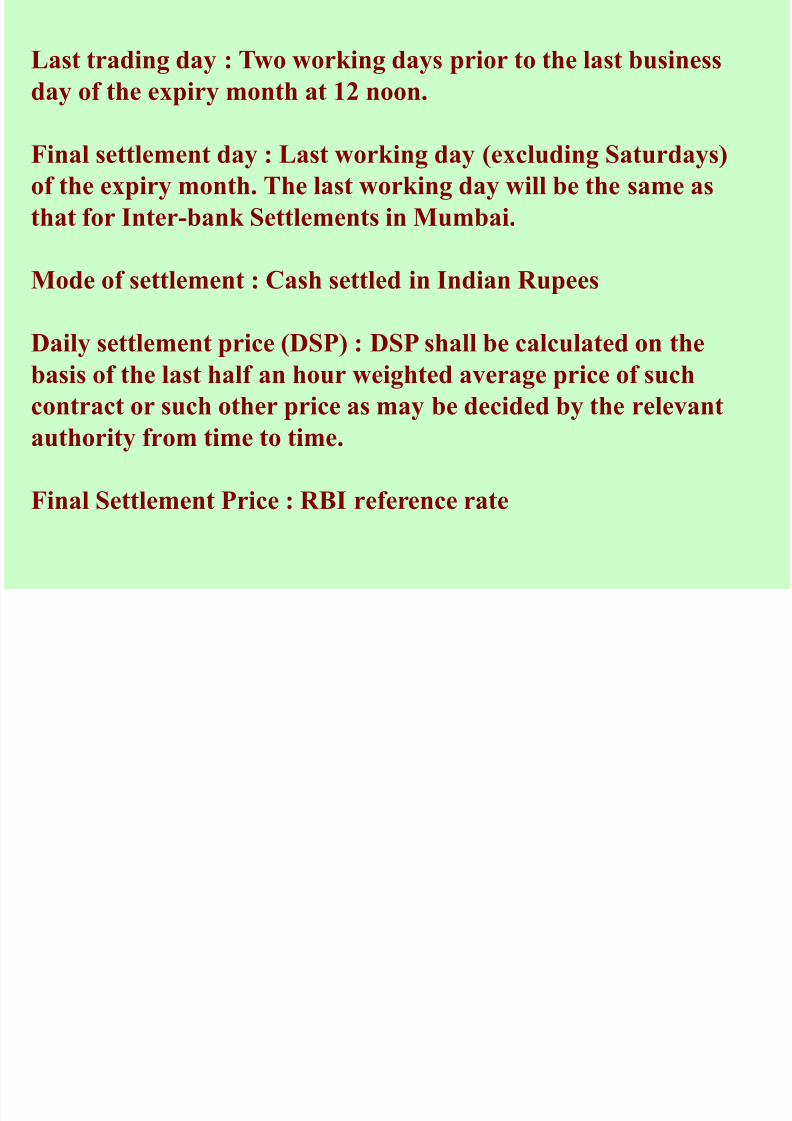

Last trading day : Two working days prior to the last business

day of the expiry month at 12 noon.

Final settlement day : Last working day (excluding Saturdays)

of the expiry month. The last working day will be the same as

that for Inter-bank Settlements in Mumbai.

Mode of settlement : Cash settled in Indian Rupees

Daily settlement price (DSP) : DSP shall be calculated on the

basis of the last half an hour weighted average price of such

contract or such other price as may be decided by the relevantauthority from time to time.

Final Settlement Price : RBI reference rate

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 25/68

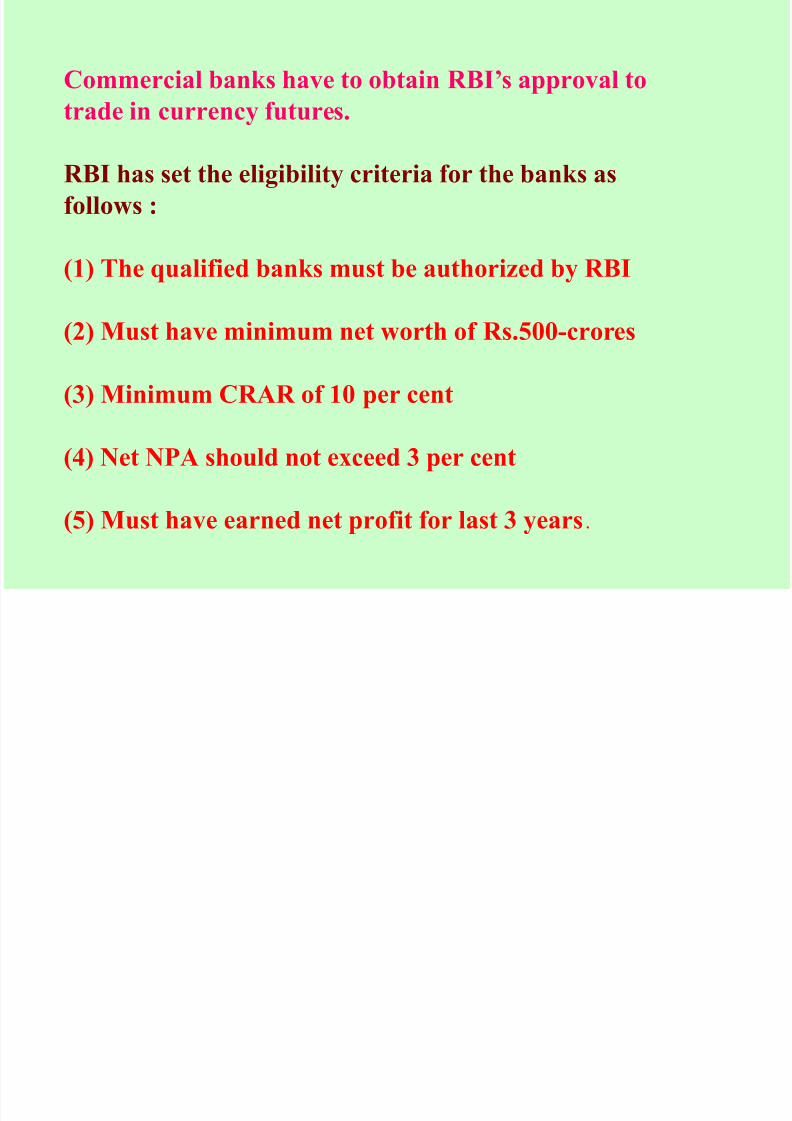

Commercial banks have to obtain RBI’s approval to

trade in currency futures.

RBI has set the eligibility criteria for the banks as

follows :

(1) The qualified banks must be authorized by RBI

(2) Must have minimum net worth of Rs.500-crores

(3) Minimum CRAR of 10 per cent

(4) Net NPA should not exceed 3 per cent

(5) Must have earned net profit for last 3 years.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 26/68

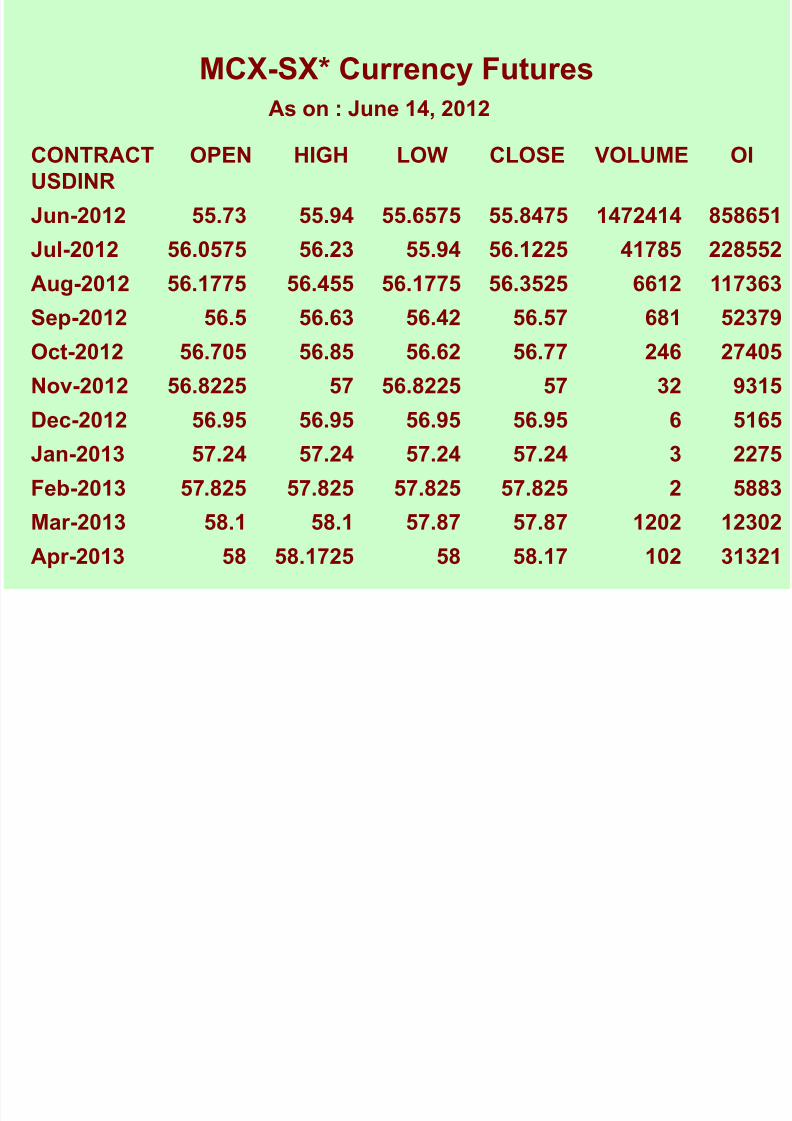

CONTRACT OPEN HIGH LOW CLOSE VOLUME OIUSDINR

Jun-2012 55.73 55.94 55.6575 55.8475 1472414 858651

Jul-2012 56.0575 56.23 55.94 56.1225 41785 228552

Aug-2012 56.1775 56.455 56.1775 56.3525 6612 117363

Sep-2012 56.5 56.63 56.42 56.57 681 52379

Oct-2012 56.705 56.85 56.62 56.77 246 27405

Nov-2012 56.8225 57 56.8225 57 32 9315

Dec-2012 56.95 56.95 56.95 56.95 6 5165Jan-2013 57.24 57.24 57.24 57.24 3 2275

Feb-2013 57.825 57.825 57.825 57.825 2 5883

Mar-2013 58.1 58.1 57.87 57.87 1202 12302

Apr-2013 58 58.1725 58 58.17 102 31321

MCX-SX* Currency FuturesAs on : June 14, 2012

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 27/68

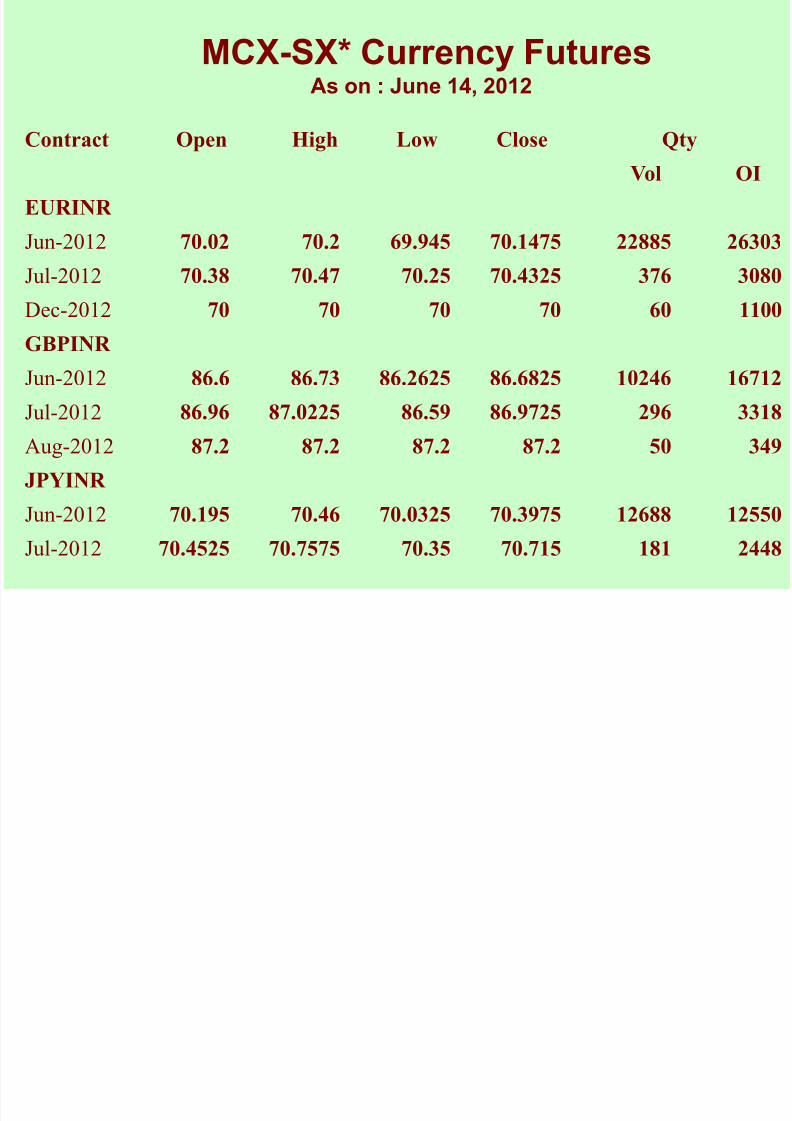

Contract Open High Low Close Qty Vol OI

EURINR

Jun-2012 70.02 70.2 69.945 70.1475 22885 26303

Jul-2012 70.38 70.47 70.25 70.4325 376 3080 Dec-2012 70 70 70 70 60 1100

GBPINR

Jun-2012 86.6 86.73 86.2625 86.6825 10246 16712

Jul-2012 86.96 87.0225 86.59 86.9725 296 3318 Aug-2012 87.2 87.2 87.2 87.2 50 349

JPYINR

Jun-2012 70.195 70.46 70.0325 70.3975 12688 12550

Jul-2012 70.4525 70.7575 70.35 70.715 181 2448

MCX-SX* Currency FuturesAs on : June 14, 2012

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 28/68

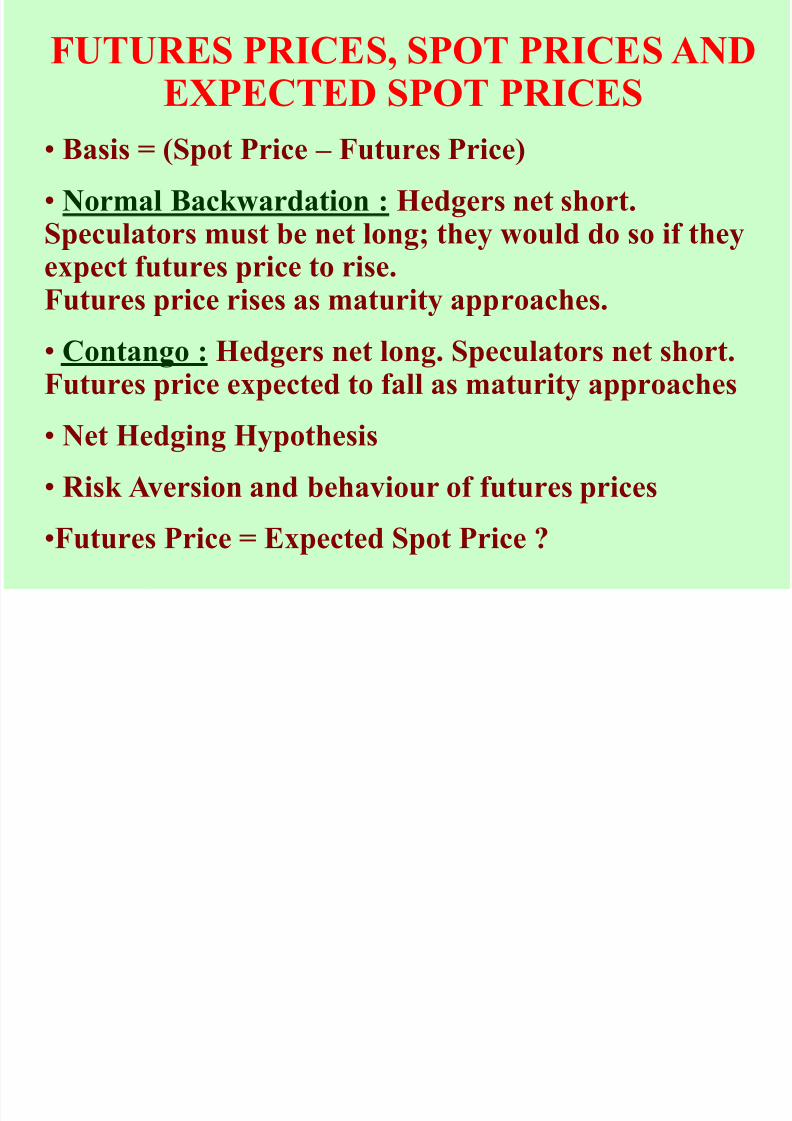

FUTURES PRICES, SPOT PRICES ANDEXPECTED SPOT PRICES

• Basis = (Spot Price – Futures Price)

• Normal Backwardation : Hedgers net short.Speculators must be net long; they would do so if they

expect futures price to rise.Futures price rises as maturity approaches.

• Contango : Hedgers net long. Speculators net short.Futures price expected to fall as maturity approaches

• Net Hedging Hypothesis

• Risk Aversion and behaviour of futures prices

•Futures Price = Expected Spot Price ?

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 29/68

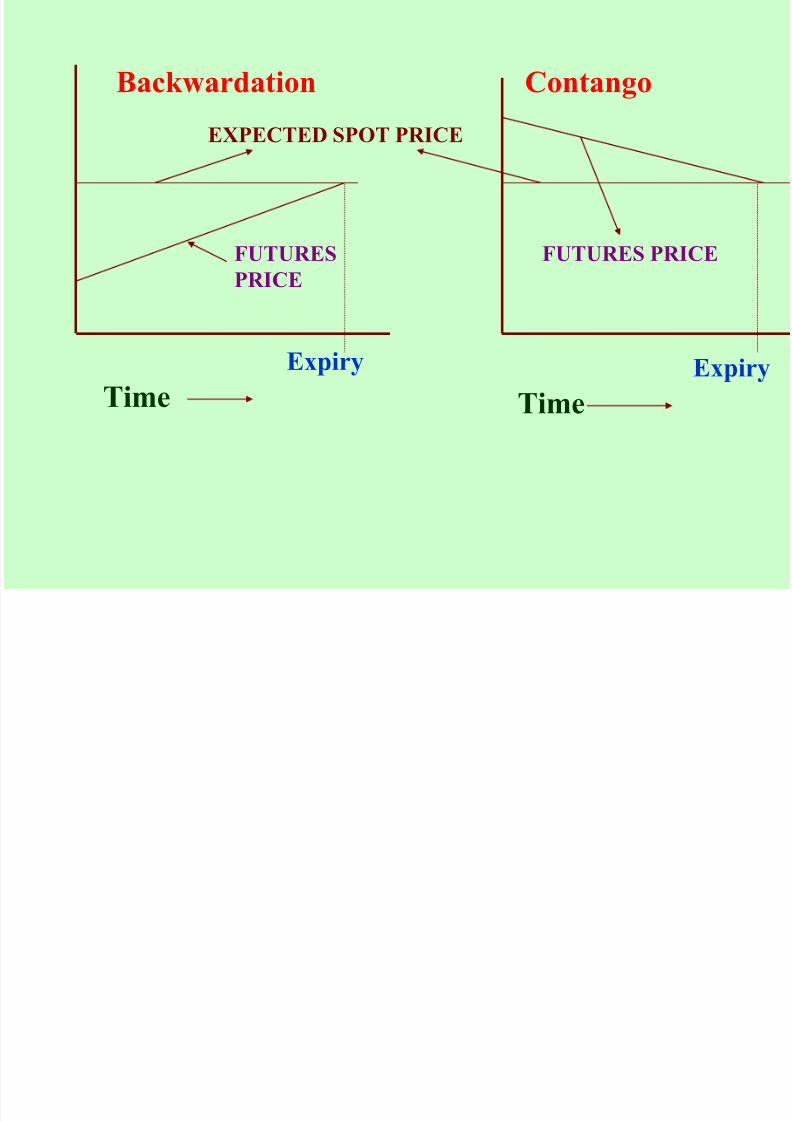

Backwardation Contango

FUTURES

PRICE

EXPECTED SPOT PRICE

FUTURES PRICE

Time

Expiry Expiry

Time

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 30/68

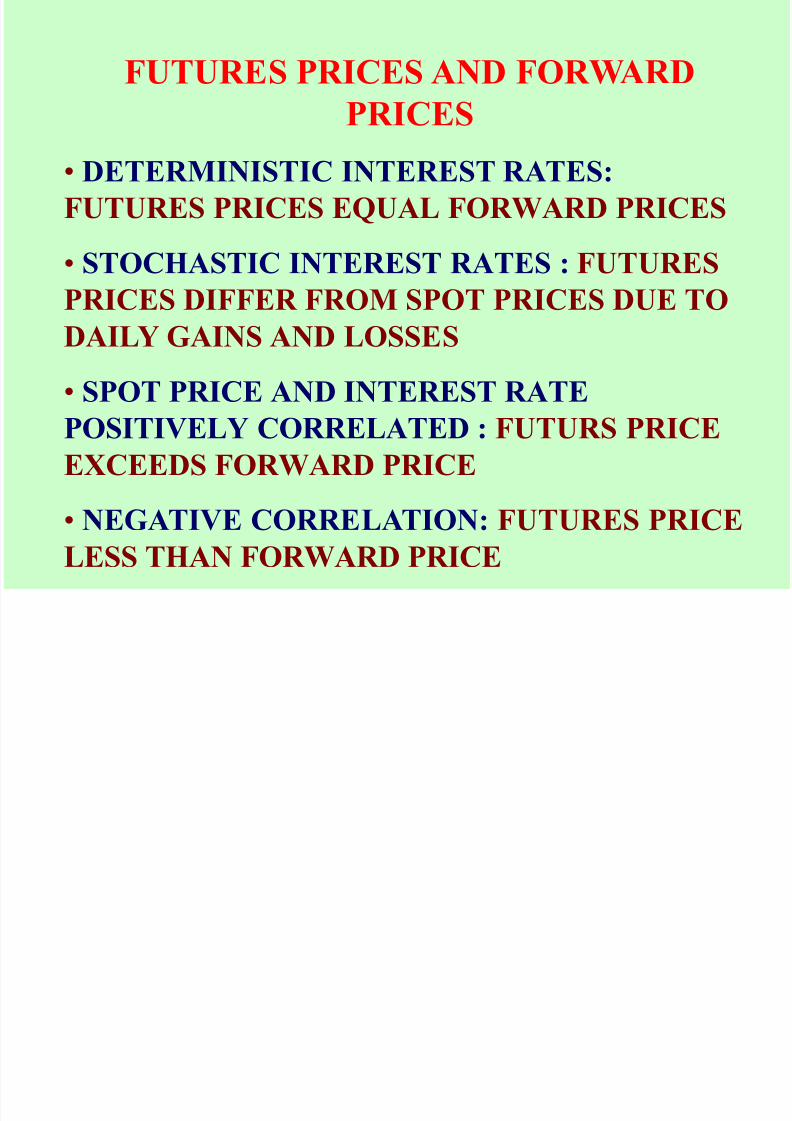

FUTURES PRICES AND FORWARD

PRICES

• DETERMINISTIC INTEREST RATES:

FUTURES PRICES EQUAL FORWARD PRICES

• STOCHASTIC INTEREST RATES : FUTURES

PRICES DIFFER FROM SPOT PRICES DUE TO

DAILY GAINS AND LOSSES

• SPOT PRICE AND INTEREST RATE

POSITIVELY CORRELATED : FUTURS PRICE

EXCEEDS FORWARD PRICE

• NEGATIVE CORRELATION: FUTURES PRICE

LESS THAN FORWARD PRICE

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 31/68

FUTURES PRICE AND SPOT PRICE

CASH-AND -CARRY ARBITRAGE

• Spot Price of a dollar : Rs.52.00

• 3-month Futures Price : Rs.53.80

• Rupee interest rate : 6% p.a.

• Dollar interest rate : 4% p.a.

• Borrow rupees, buy dollars and deposit, sell futures.

• 3 months later, deliver, get rupees, repay loan.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 32/68

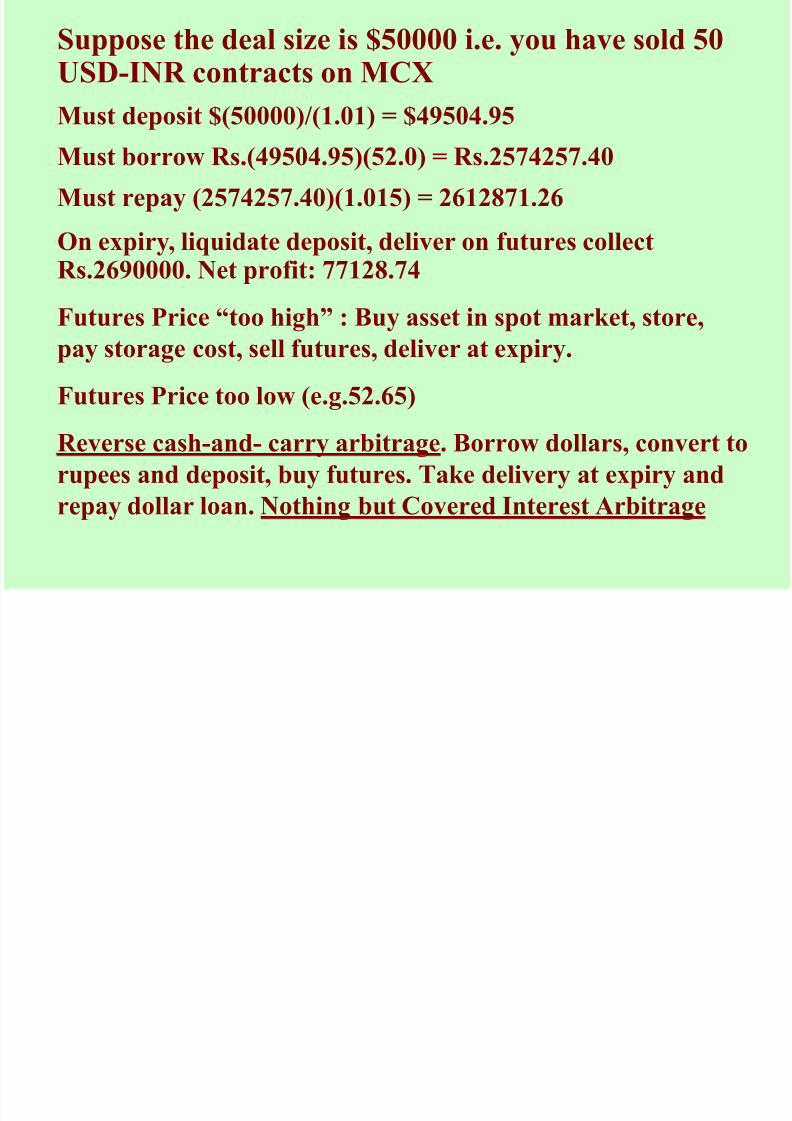

Suppose the deal size is $50000 i.e. you have sold 50USD-INR contracts on MCX

Must deposit $(50000)/(1.01) = $49504.95

Must borrow Rs.(49504.95)(52.0) = Rs.2574257.40

Must repay (2574257.40)(1.015) = 2612871.26

On expiry, liquidate deposit, deliver on futures collect

Rs.2690000. Net profit: 77128.74Futures Price “too high” : Buy asset in spot market, store,

pay storage cost, sell futures, deliver at expiry.

Futures Price too low (e.g.52.65)

Reverse cash-and- carry arbitrage. Borrow dollars, convert to

rupees and deposit, buy futures. Take delivery at expiry and

repay dollar loan. Nothing but Covered Interest Arbitrage

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 33/68

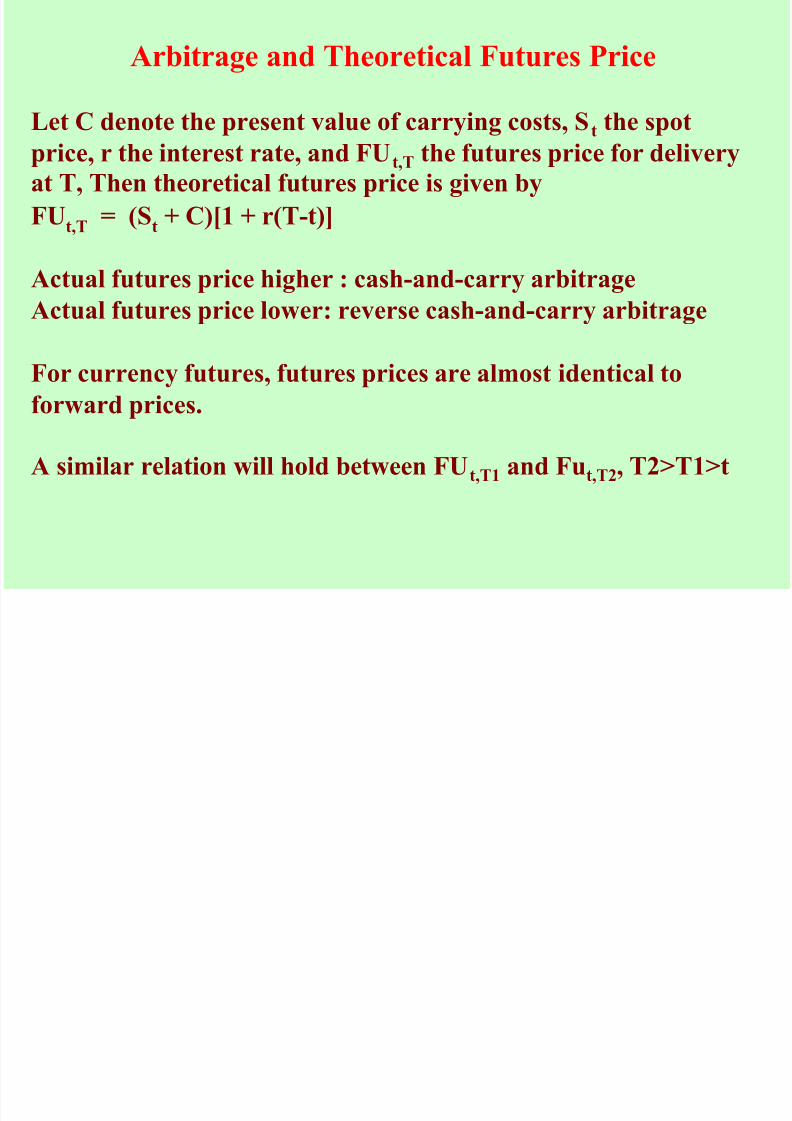

Arbitrage and Theoretical Futures Price

Let C denote the present value of carrying costs, St the spot

price, r the interest rate, and FUt,T the futures price for delivery

at T, Then theoretical futures price is given by FU

t,T= (S

t+ C)[1 + r(T-t)]

Actual futures price higher : cash-and-carry arbitrageActual futures price lower: reverse cash-and-carry arbitrage

For currency futures, futures prices are almost identical to

forward prices.

A similar relation will hold between FUt,T1 and Fut,T2, T2>T1>t

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 34/68

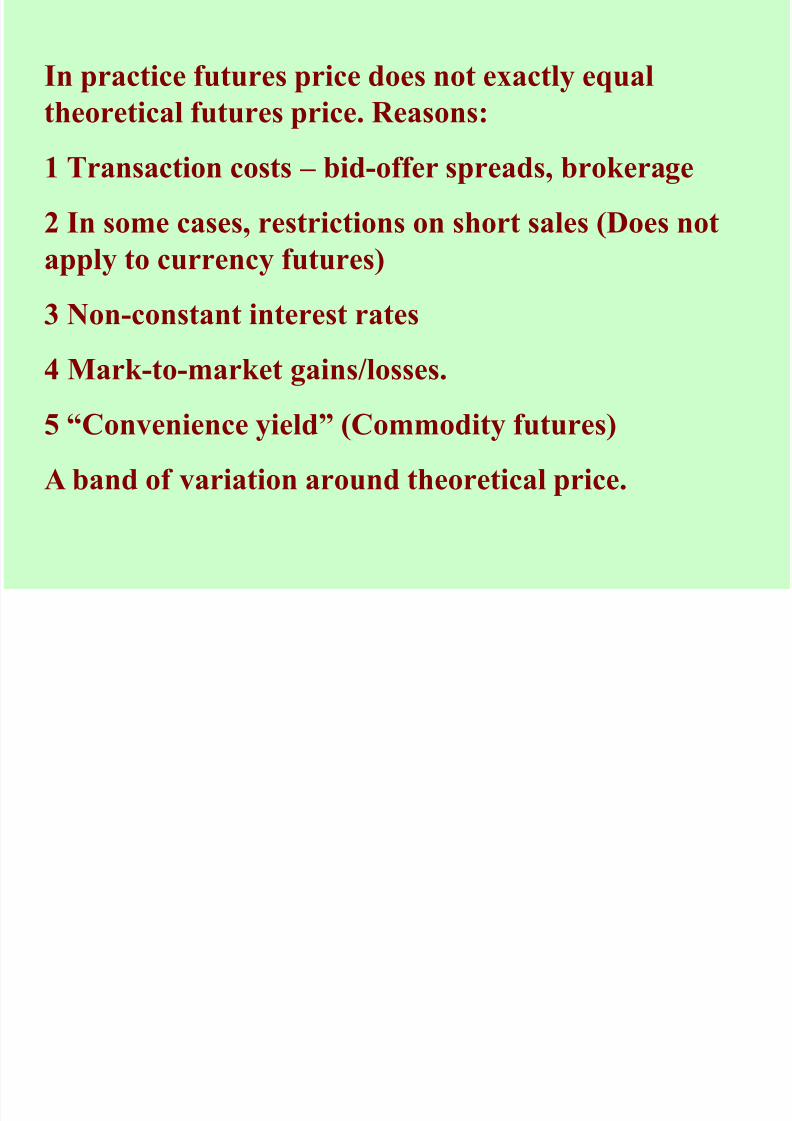

In practice futures price does not exactly equal

theoretical futures price. Reasons:

1 Transaction costs – bid-offer spreads, brokerage

2 In some cases, restrictions on short sales (Does not

apply to currency futures)

3 Non-constant interest rates

4 Mark-to-market gains/losses.

5 “Convenience yield” (Commodity futures)

A band of variation around theoretical price.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 35/68

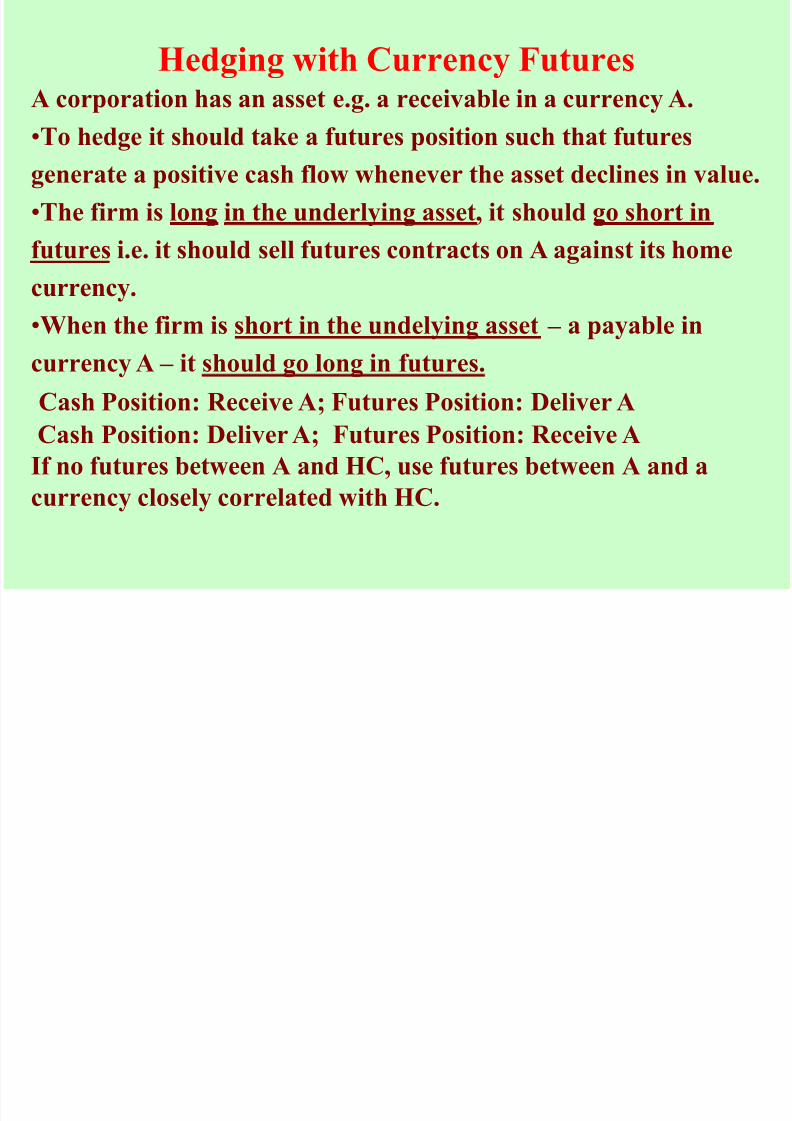

Hedging with Currency Futures A corporation has an asset e.g. a receivable in a currency A.

•

To hedge it should take a futures position such that futuresgenerate a positive cash flow whenever the asset declines in value.

•The firm is long in the underlying asset, it should go short in

futures i.e. it should sell futures contracts on A against its home

currency.

•When the firm is short in the undelying asset – a payable in

currency A – it should go long in futures.

Cash Position: Receive A; Futures Position: Deliver A

Cash Position: Deliver A; Futures Position: Receive A

If no futures between A and HC, use futures between A and a

currency closely correlated with HC.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 36/68

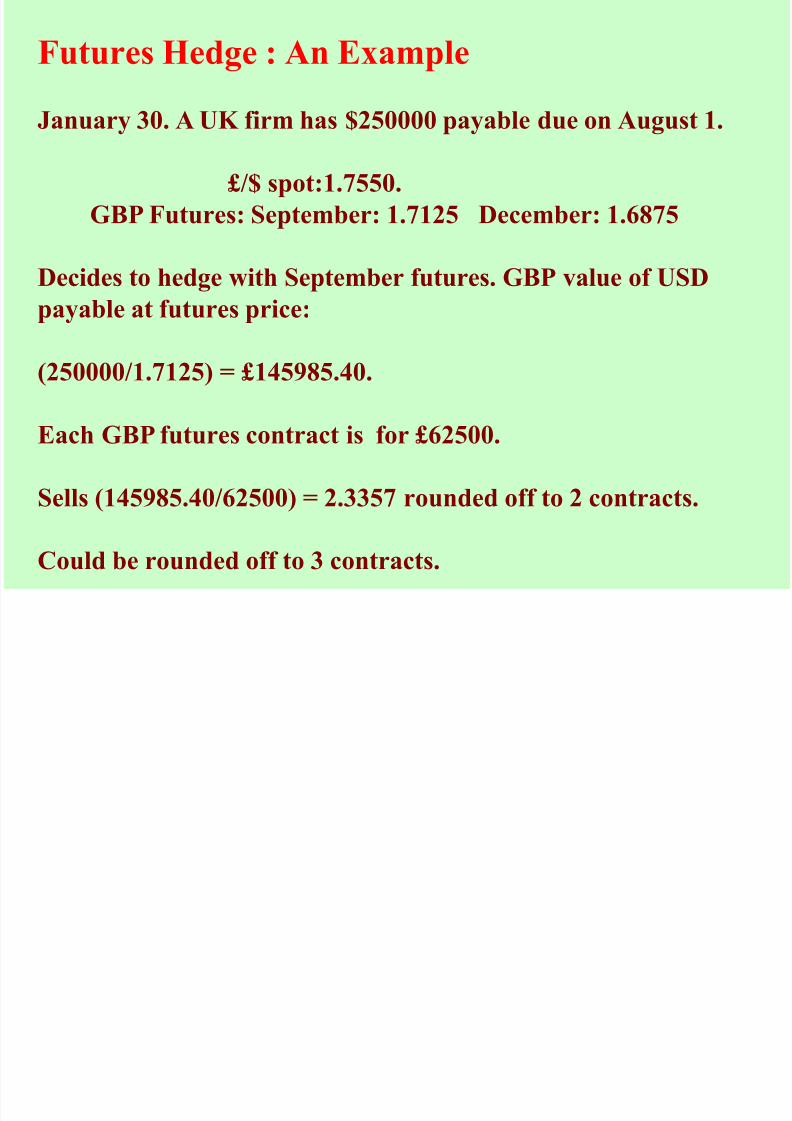

Futures Hedge : An Example

January 30. A UK firm has $250000 payable due on August 1.

£/$ spot:1.7550.

GBP Futures: September: 1.7125 December: 1.6875

Decides to hedge with September futures. GBP value of USDpayable at futures price:

(250000/1.7125) = £145985.40.

Each GBP futures contract is for £62500.

Sells (145985.40/62500) = 2.3357 rounded off to 2 contracts.

Could be rounded off to 3 contracts.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 37/68

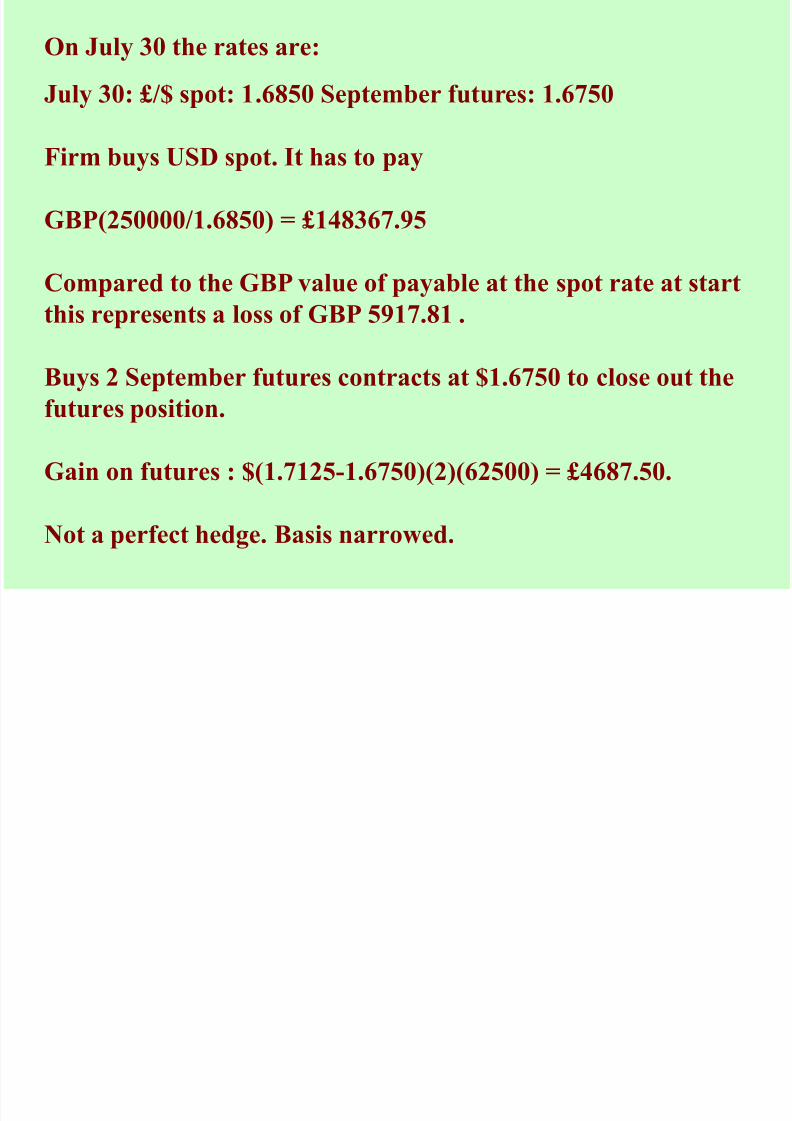

On July 30 the rates are:

July 30: £/$ spot: 1.6850 September futures: 1.6750

Firm buys USD spot. It has to pay

GBP(250000/1.6850) = £148367.95

Compared to the GBP value of payable at the spot rate at startthis represents a loss of GBP 5917.81 .

Buys 2 September futures contracts at $1.6750 to close out the

futures position.

Gain on futures : $(1.7125-1.6750)(2)(62500) = £4687.50.

Not a perfect hedge. Basis narrowed.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 38/68

Futures Hedge : Example (contd)

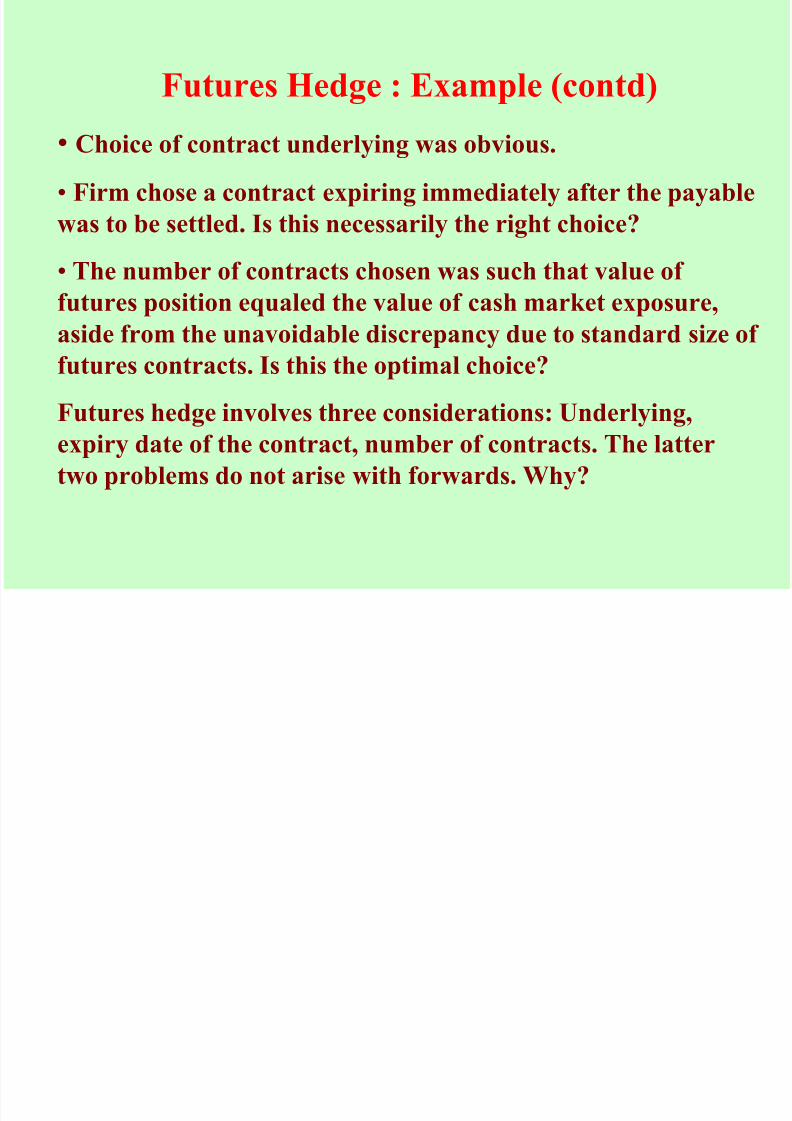

• Choice of contract underlying was obvious.

• Firm chose a contract expiring immediately after the payable

was to be settled. Is this necessarily the right choice?

•

The number of contracts chosen was such that value of futures position equaled the value of cash market exposure,

aside from the unavoidable discrepancy due to standard size of

futures contracts. Is this the optimal choice?

Futures hedge involves three considerations: Underlying,expiry date of the contract, number of contracts. The latter

two problems do not arise with forwards. Why?

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 39/68

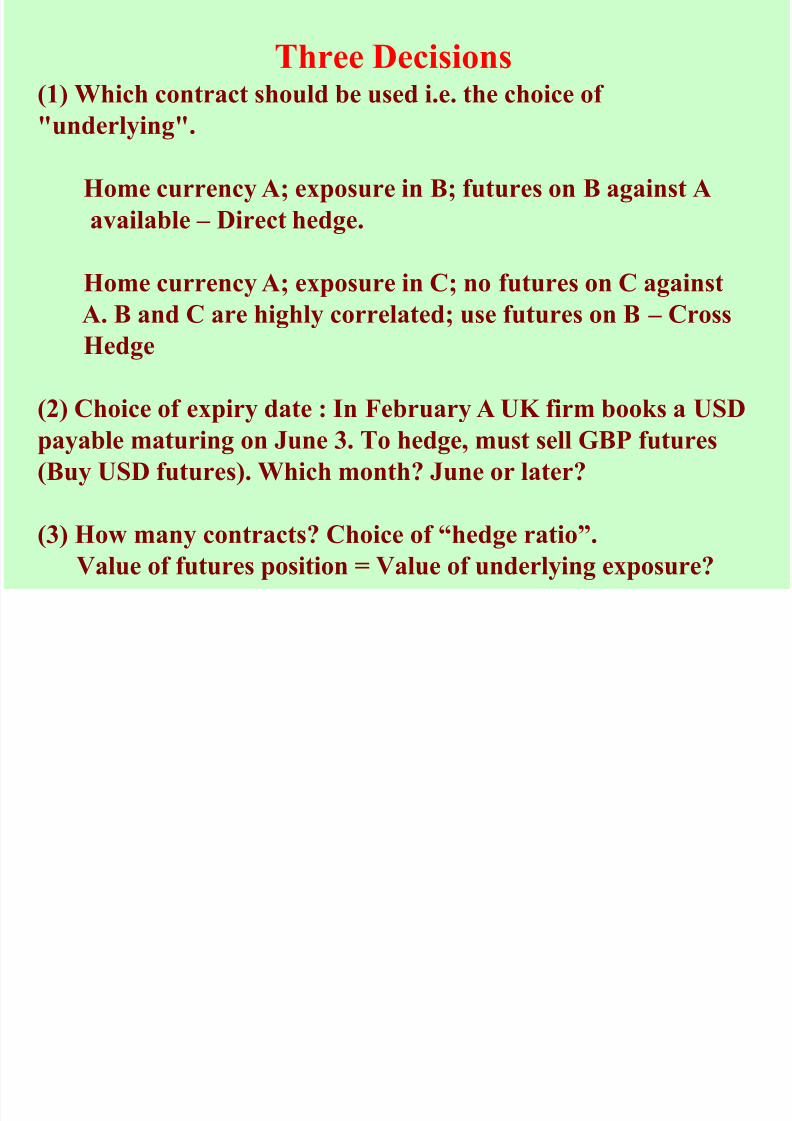

Three Decisions (1) Which contract should be used i.e. the choice of

"underlying".

Home currency A; exposure in B; futures on B against A

available – Direct hedge.

Home currency A; exposure in C; no futures on C againstA. B and C are highly correlated; use futures on B – Cross

Hedge

(2) Choice of expiry date : In February A UK firm books a USDpayable maturing on June 3. To hedge, must sell GBP futures

(Buy USD futures). Which month? June or later?

(3) How many contracts? Choice of “hedge ratio”.

Value of futures position = Value of underlying exposure?

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 40/68

Choice of expiry date: As expiry date approaches, basis narrows.

On expiry date futures price equals spot price. This is known as

“Convergence”.

Does convergence help you or hurt you?

If convergence helps, choose near contract

If convergence hurts, choose far contract.

However, liquidity less in far contracts; bid-offer spreads are

higher; basis volatility more.

Thumb rule followed by practitioners: Choose expiry date

immediately after underlying exposure is to be settled.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 41/68

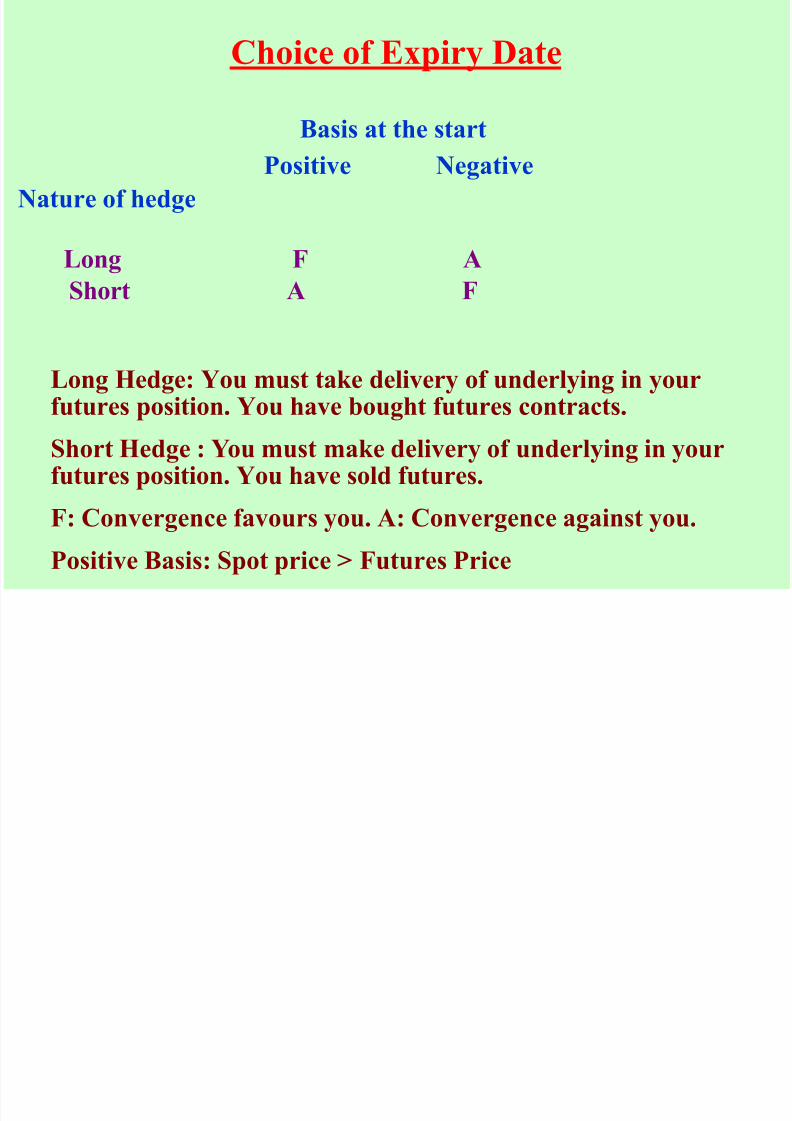

Choice of Expiry Date

Basis at the start Positive Negative

Nature of hedge

Long F A

Short A F

Long Hedge: You must take delivery of underlying in yourfutures position. You have bought futures contracts.

Short Hedge : You must make delivery of underlying in yourfutures position. You have sold futures.

F: Convergence favours you. A: Convergence against you.

Positive Basis: Spot price > Futures Price

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 42/68

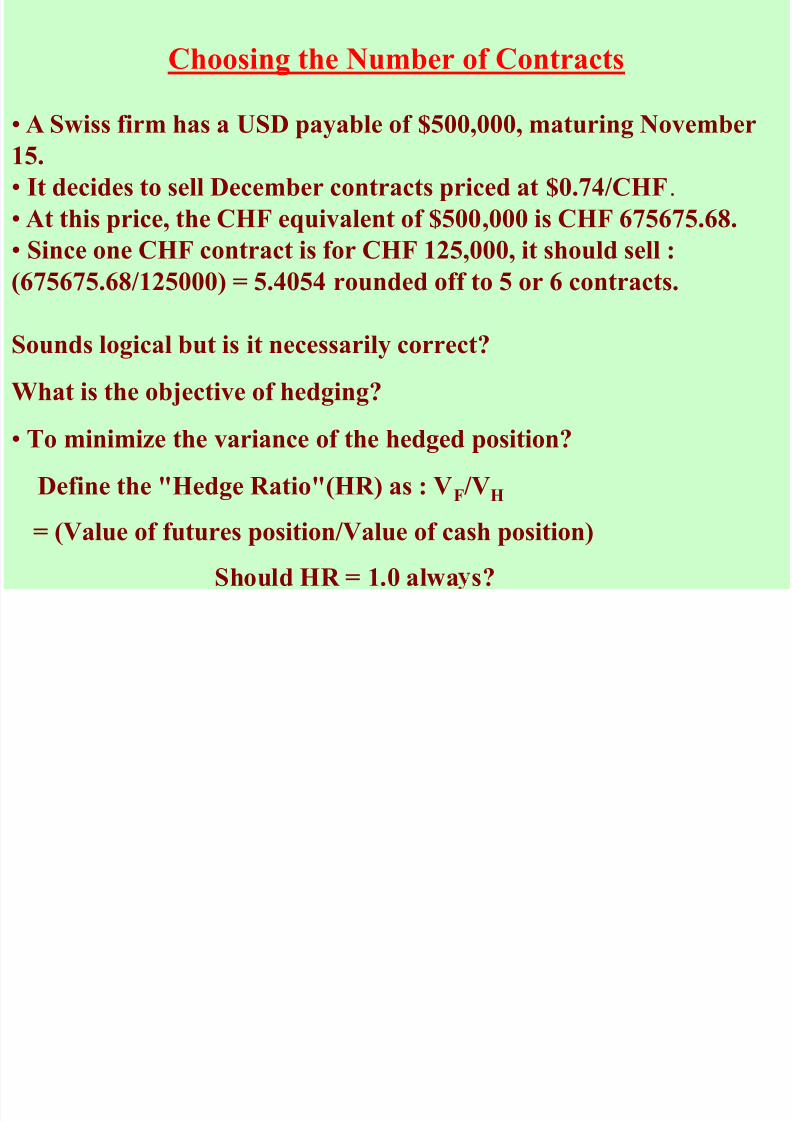

Choosing the Number of Contracts

• A Swiss firm has a USD payable of $500,000, maturing November

15.

• It decides to sell December contracts priced at $0.74/CHF.

• At this price, the CHF equivalent of $500,000 is CHF 675675.68.

• Since one CHF contract is for CHF 125,000, it should sell :

(675675.68/125000) = 5.4054 rounded off to 5 or 6 contracts.

Sounds logical but is it necessarily correct?

What is the objective of hedging?

• To minimize the variance of the hedged position?

Define the "Hedge Ratio"(HR) as : VF/VH

= (Value of futures position/Value of cash position) Should HR = 1.0 alwa s?

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 43/68

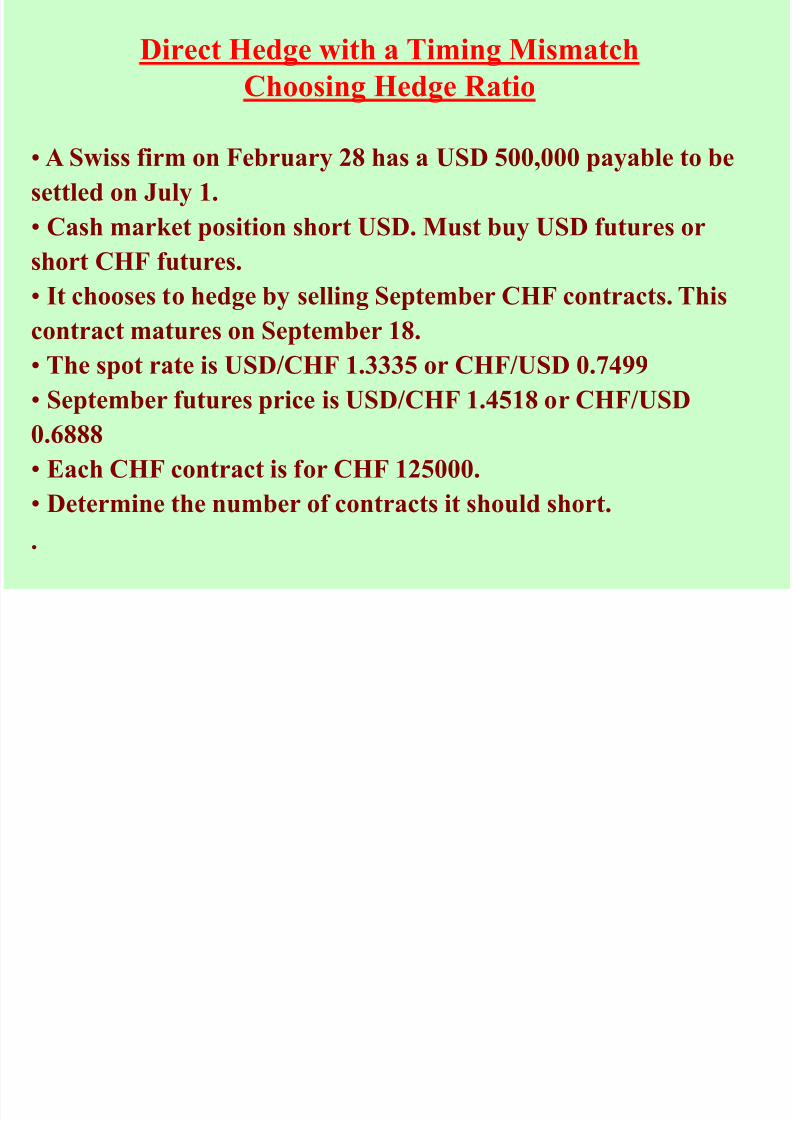

Direct Hedge with a Timing Mismatch

Choosing Hedge Ratio

• A Swiss firm on February 28 has a USD 500,000 payable to be

settled on July 1.

• Cash market position short USD. Must buy USD futures or

short CHF futures.

• It chooses to hedge by selling September CHF contracts. This

contract matures on September 18.

• The spot rate is USD/CHF 1.3335 or CHF/USD 0.7499

• September futures price is USD/CHF 1.4518 or CHF/USD

0.6888

• Each CHF contract is for CHF 125000.

• Determine the number of contracts it should short.

.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 44/68

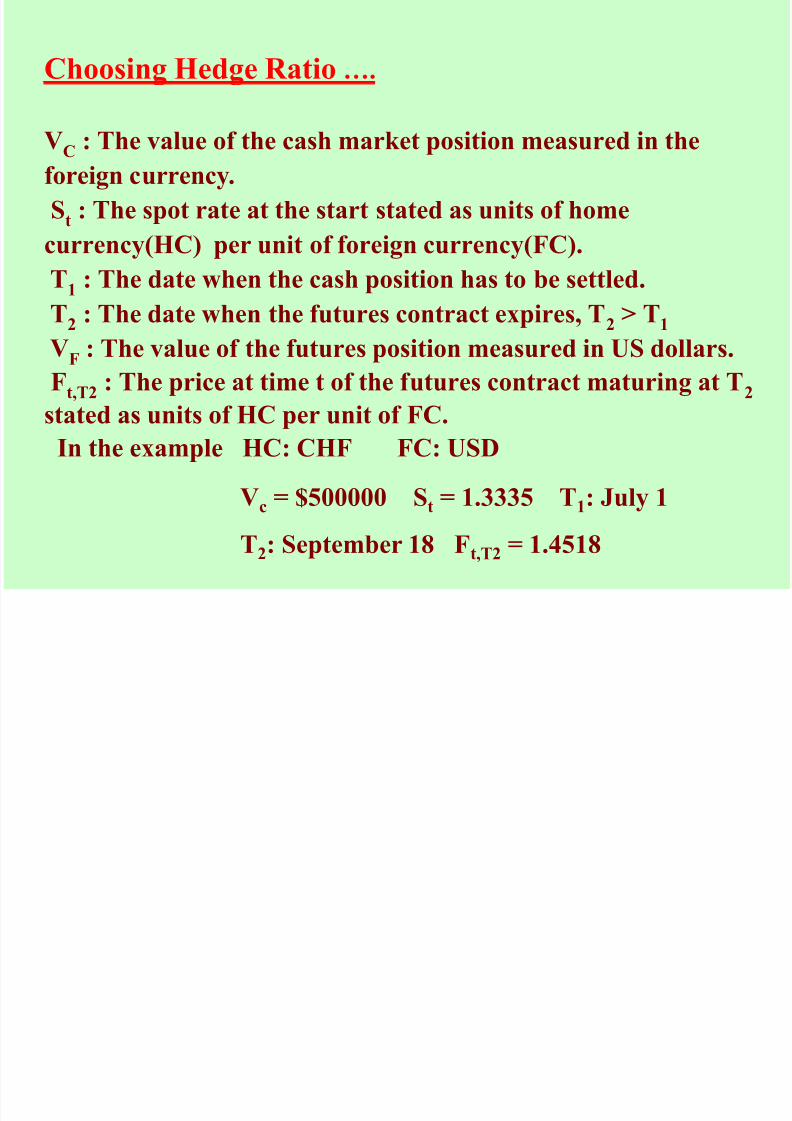

Choosing Hedge Ratio ….

VC : The value of the cash market position measured in theforeign currency.

St: The spot rate at the start stated as units of home

currency(HC) per unit of foreign currency(FC).

T1 : The date when the cash position has to be settled.T2 : The date when the futures contract expires, T2 > T1 V

F: The value of the futures position measured in US dollars.

Ft,T2

: The price at time t of the futures contract maturing at T2

stated as units of HC per unit of FC. In the example HC: CHF FC: USD

Vc = $500000 St = 1.3335 T1: July 1

T2: September 18 F

t,T2= 1.4518

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 45/68

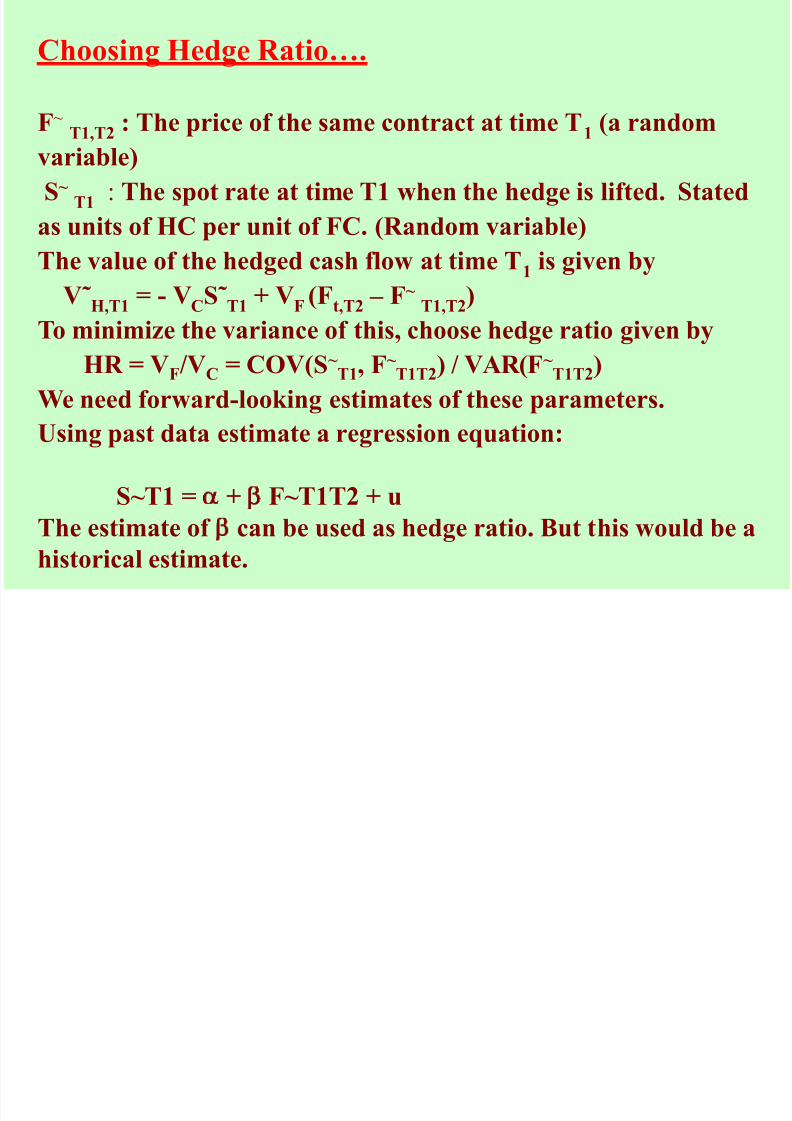

Choosing Hedge Ratio….

F~ T1,T2

: The price of the same contract at time T1

(a random

variable) S~

T1 : The spot rate at time T1 when the hedge is lifted. Stated

as units of HC per unit of FC. (Random variable)

The value of the hedged cash flow at time T1

is given by V˜H,T1

= - VCS˜T1

+ VF

(Ft,T2

– F~ T1,T2

)

To minimize the variance of this, choose hedge ratio given by

HR = VF/VC = COV(S~ T1, F

~ T1T2) / VAR(F~

T1T2)

We need forward-looking estimates of these parameters.

Using past data estimate a regression equation:

S~T1 = + F~T1T2 + u

The estimate of can be used as hedge ratio. But this would be a

historical estimate.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 46/68

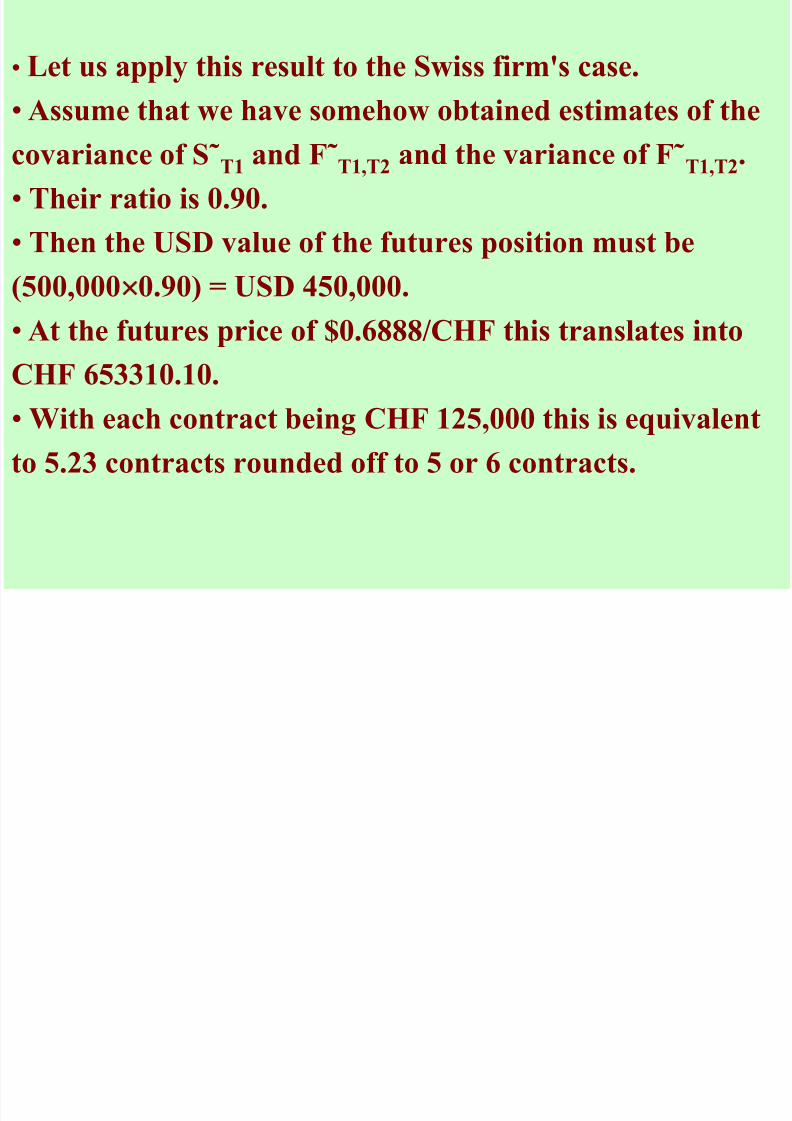

• Let us apply this result to the Swiss firm's case.

• Assume that we have somehow obtained estimates of the

covariance of S˜T1 and F˜T1,T2 and the variance of F˜T1,T2.

• Their ratio is 0.90.

• Then the USD value of the futures position must be

(500,0000.90) = USD 450,000.

• At the futures price of $0.6888/CHF this translates into

CHF 653310.10.

• With each contract being CHF 125,000 this is equivalentto 5.23 contracts rounded off to 5 or 6 contracts.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 47/68

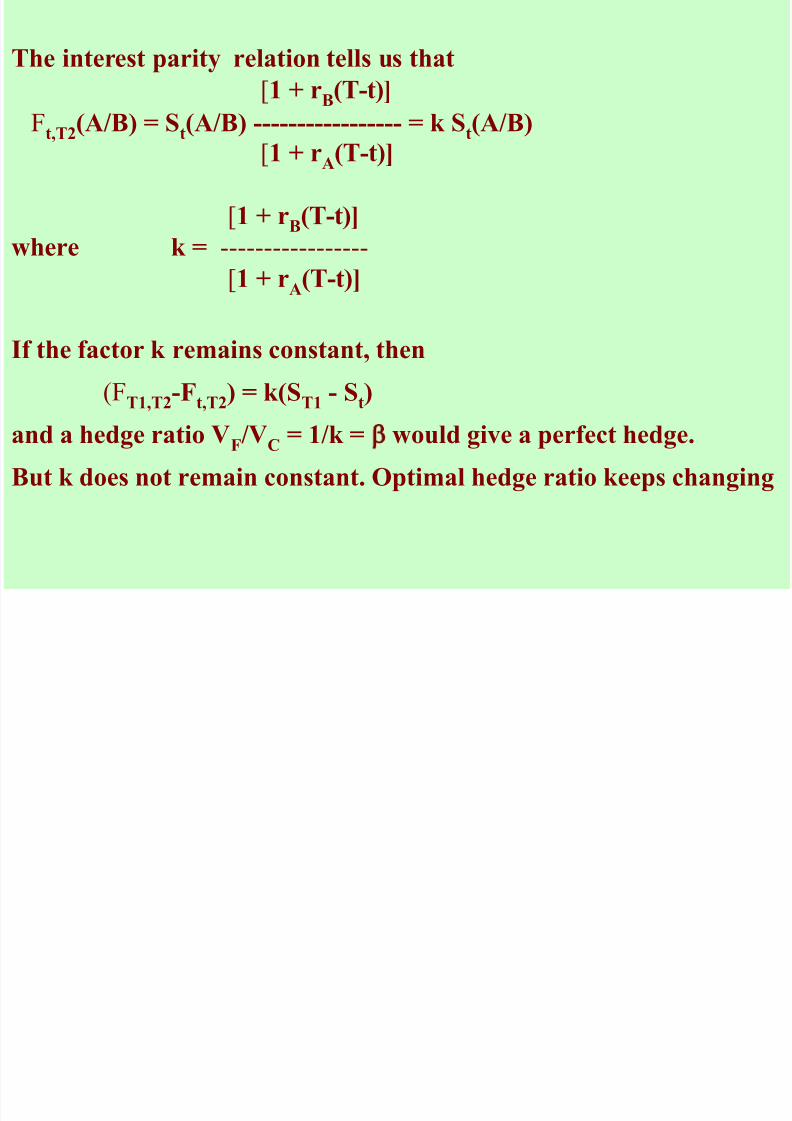

The interest parity relation tells us that [1 + rB(T-t)]

Ft,T2

(A/B) = St(A/B) ----------------- = k S

t(A/B)

[1 + rA(T-t)] [1 + rB(T-t)]

where k = ----------------- [1 + rA(T-t)]

If the factor k remains constant, then

(FT1,T2-Ft,T2) = k(ST1 - St)

and a hedge ratio VF/V

C= 1/k = would give a perfect hedge.

But k does not remain constant. Optimal hedge ratio keeps changing

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 48/68

• Dynamic hedging: As interest rates and spot rate

keep changing, recalculate the optimal hedge ratio

and rebalance the hedge by selling more futures orbuying futures. How frequently?

• Transaction costs must be considered. Any gain

from frequent rebalancing must be weighed against

increased transaction costs.

• Large position, long duration of hedge, more

frequent rebalancing warranted.

• Standard-size problem cannot be circumvented.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 49/68

SPECULATION WITH CURRENCY FUTURES

• Open Position Trading

In April Spot EUR/USD: 1.5750

June Futures : 1.5925

September Futures: 1.6225

You do not think EUR will rise. It will fall.

You do not think EUR will rise so much.

How to profit from this view? Sell September.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 50/68

SPECULATION WITH CURRENCY

FUTURES

On September 10 the rates are :

Spot EUR/USD: 1.5940 September futures: 1.5950

Close out by buying a September contract.Profit USD(1.6225-1.5950) per EUR on 125000 EUR

= USD 3437.50 minus brokerage etc.

First view was wrong; EUR did appreciate but not as

much as implied by futures price.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 51/68

SPREAD TRADING

• Intercommodity Spread

In April : Spot EUR/USD : 1.5500 GBP/USD: 1.9000

September Futures: EUR: 1.5800 GBP: 1.8580

Your view: GBP is going to rise against EUR.

What should you do?

• Intracommodity Spread (Calender Spreads)

June EUR: 1.5800 September EUR : 1.7500Your view: Between June and September EUR will notrise so much. What should you do?

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 52/68

INTEREST RATE FUTURES

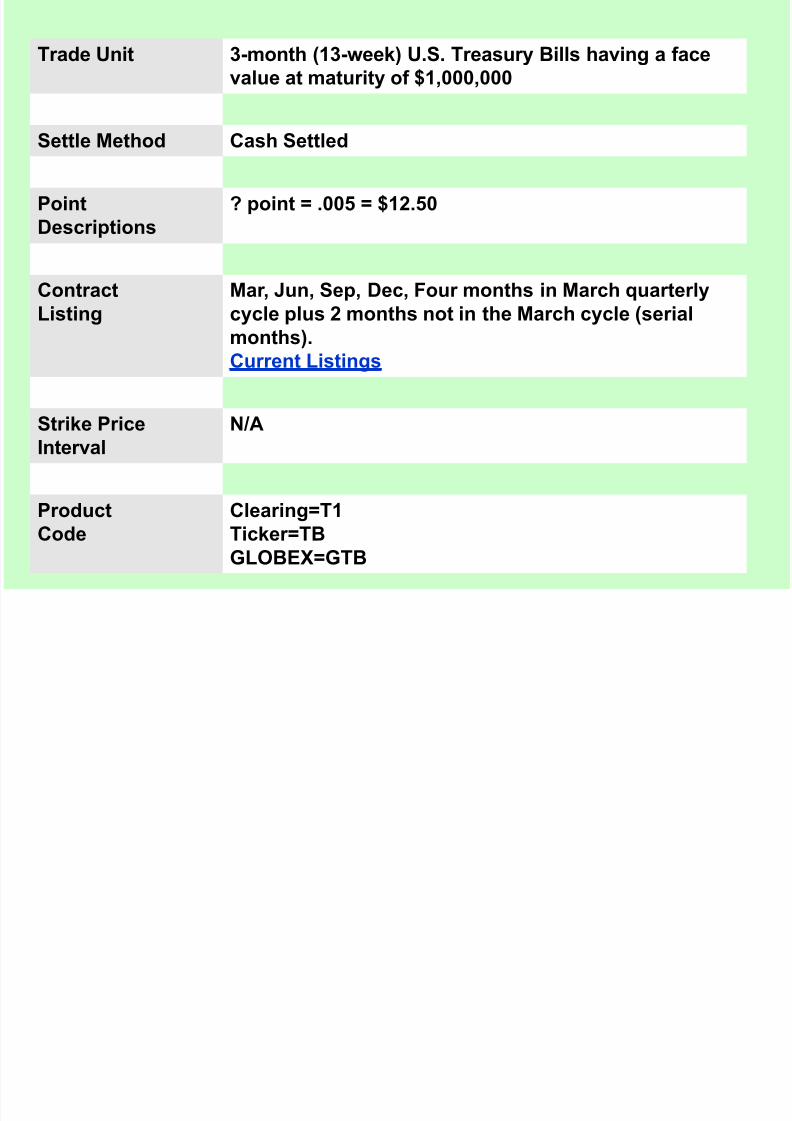

Treasury Bill Futures A futures contract on US treasury bills is traded on

the CME. Its specifications are as follows: Product and Trading unit: 13 WEEK TREASURYBILL FUTURES 3-month (13-week) U.S. Treasury Bills having a face

value at maturity of $1,000,000 Point Description: ½ point = .005 = $12.50. A point

here is one basis point or (1/100)th of 1 percent.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 53/68

Trade Unit 3-month (13-week) U.S. Treasury Bills having a facevalue at maturity of $1,000,000

Settle Method Cash Settled

PointDescriptions

? point = .005 = $12.50

ContractListing

Mar, Jun, Sep, Dec, Four months in March quarterlycycle plus 2 months not in the March cycle (serialmonths).Current Listings

Strike PriceInterval

N/A

ProductCode

Clearing=T1Ticker=TB

GLOBEX=GTB

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 54/68

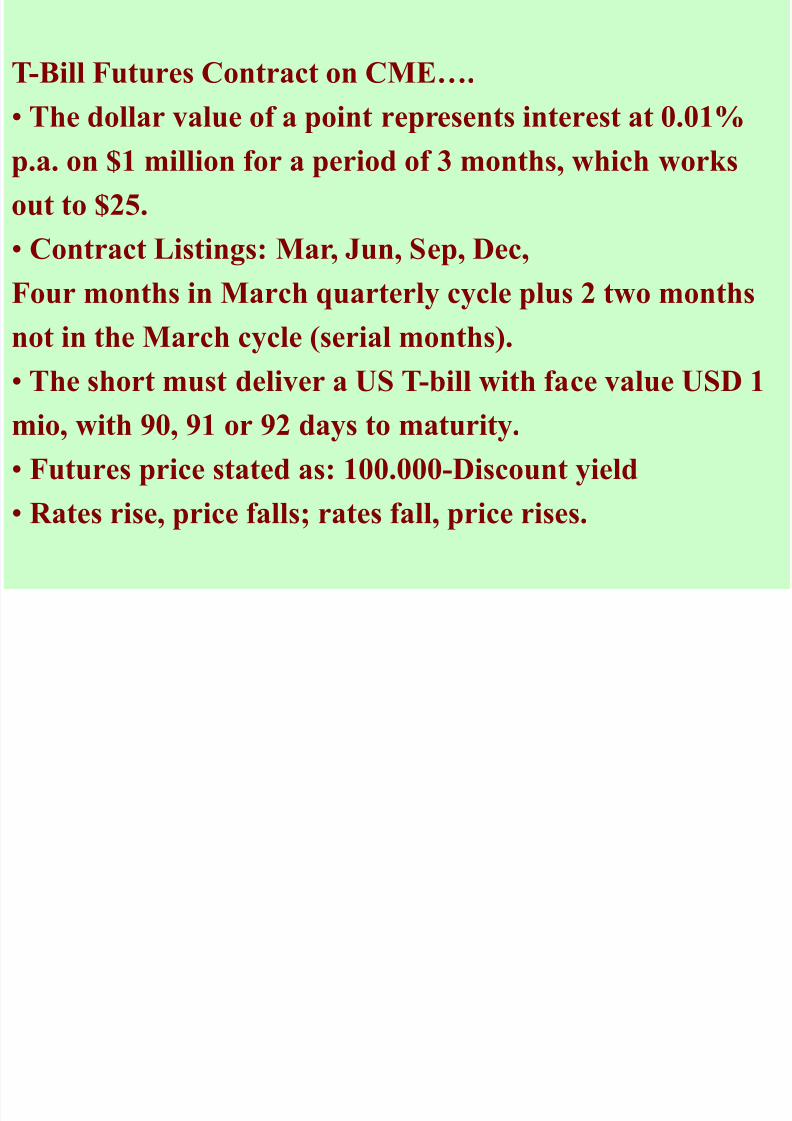

T-Bill Futures Contract on CME….

• The dollar value of a point represents interest at 0.01%

p.a. on $1 million for a period of 3 months, which works

out to $25. • Contract Listings: Mar, Jun, Sep, Dec, Four months in March quarterly cycle plus 2 two months

not in the March cycle (serial months).

• The short must deliver a US T-bill with face value USD 1

mio, with 90, 91 or 92 days to maturity.

• Futures price stated as: 100.000-Discount yield • Rates rise, price falls; rates fall, price rises.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 55/68

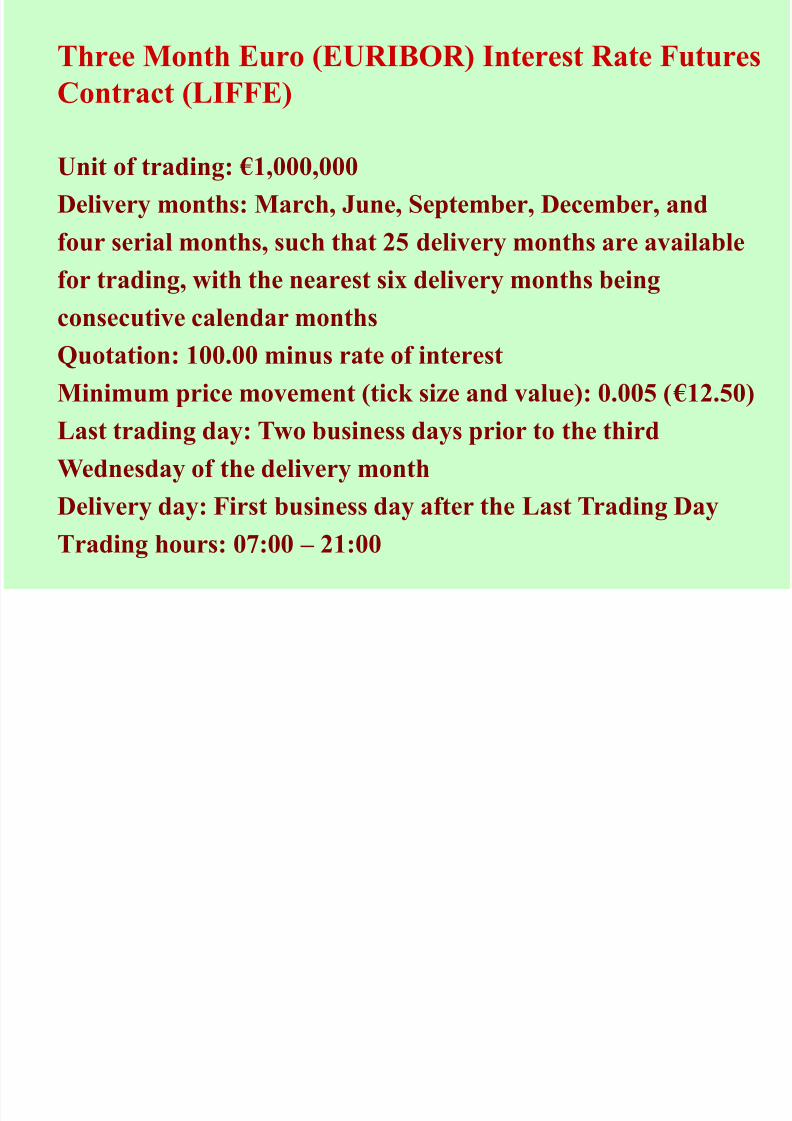

Three Month Euro (EURIBOR) Interest Rate Futures

Contract (LIFFE)

Unit of trading: €1,000,000

Delivery months: March, June, September, December, and

four serial months, such that 25 delivery months are available

for trading, with the nearest six delivery months beingconsecutive calendar months

Quotation: 100.00 minus rate of interest

Minimum price movement (tick size and value): 0.005 ( €12.50)

Last trading day: Two business days prior to the third

Wednesday of the delivery month

Delivery day: First business day after the Last Trading Day

Trading hours: 07:00 – 21:00

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 56/68

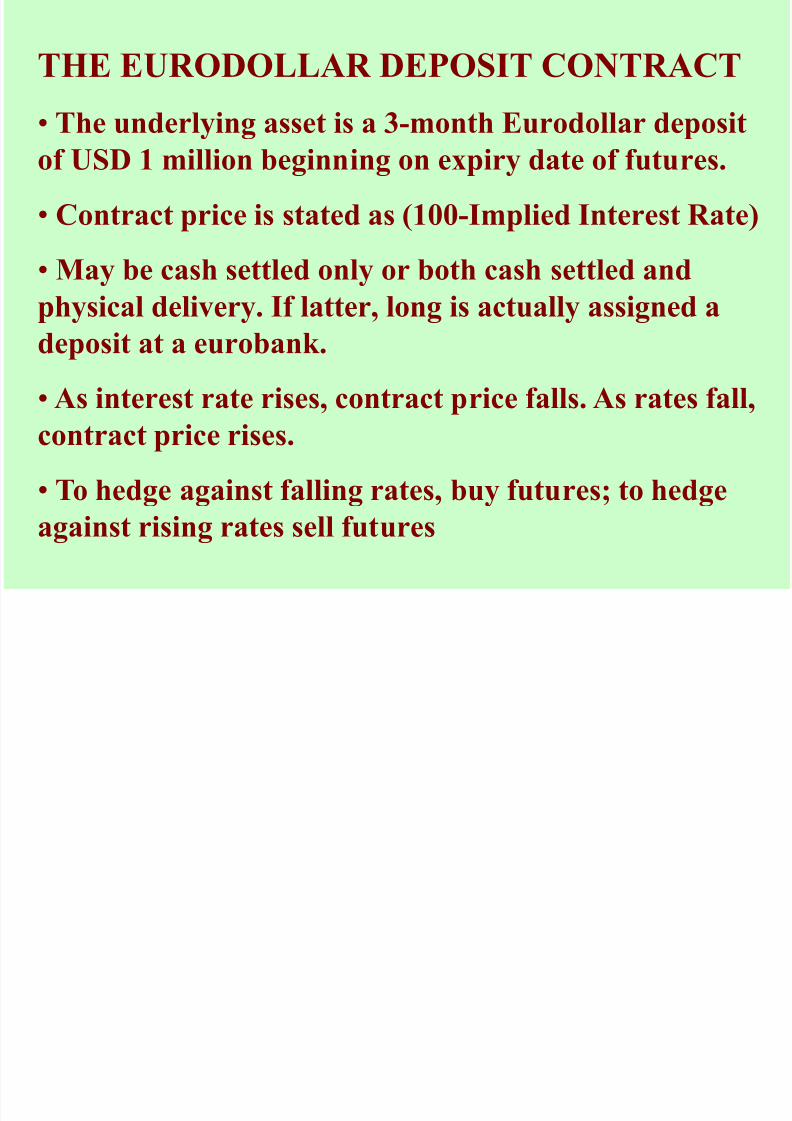

THE EURODOLLAR DEPOSIT CONTRACT

• The underlying asset is a 3-month Eurodollar deposit

of USD 1 million beginning on expiry date of futures.

• Contract price is stated as (100-Implied Interest Rate)

•

May be cash settled only or both cash settled andphysical delivery. If latter, long is actually assigned a

deposit at a eurobank.

• As interest rate rises, contract price falls. As rates fall,

contract price rises.

• To hedge against falling rates, buy futures; to hedge

against rising rates sell futures

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 57/68

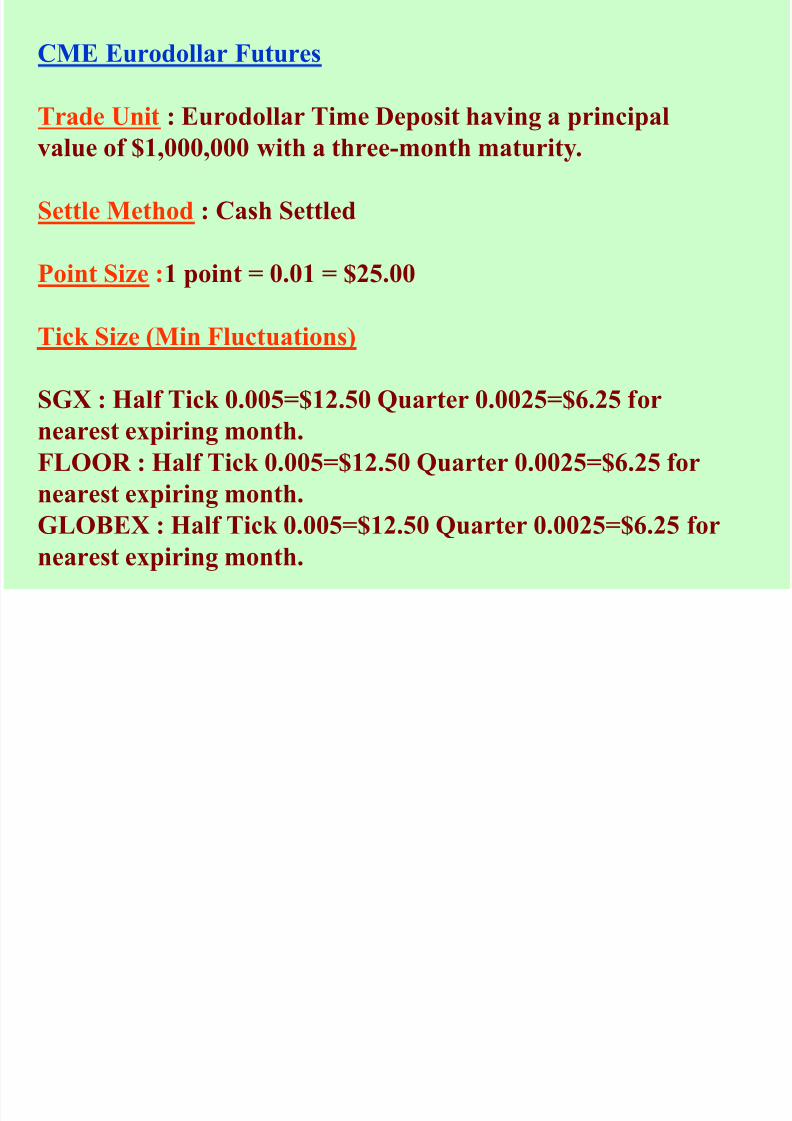

CME Eurodollar Futures

Trade Unit : Eurodollar Time Deposit having a principal

value of $1,000,000 with a three-month maturity.

Settle Method : Cash Settled

Point Size :1 point = 0.01 = $25.00

Tick Size (Min Fluctuations)

SGX : Half Tick 0.005=$12.50 Quarter 0.0025=$6.25 for

nearest expiring month.

FLOOR : Half Tick 0.005=$12.50 Quarter 0.0025=$6.25 for

nearest expiring month.

GLOBEX : Half Tick 0.005=$12.50 Quarter 0.0025=$6.25 for

nearest expiring month.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 58/68

INTEREST RATE FUTURES QUOTATIONS 29 JUNE, 2010

____________________________________________

Expiry Open Sett Change High Low Open

Month Interest

Euribor MAR11 98.92 98.94 +0.03 98.96 98.92 503091

Euribor JUN11 98.87 98.88 +0.03 98.90 98.87 353521

Sterling DEC10 99.04 99.04 +0.01 99.07 99.03 363713

Sterling MAR11 98.96 98.97 +0.02 99.01 98.96 326657

Sterling JUN11 98.84 98.84 +0.03 98.88 98.81 302845

Euro$ AUG10 99.370 99.39 -0.005 99.395 99.370 11901

Euro$ NOV10 99.245 99.24 --- 99.245 99.235 545

Euro$ MAR11 99.150 99.16 +0.010 99.165 99.130 823929

Euro$ JUN11 99.050 99.07 +0.020 99.075 99.040 864090

Euro¥ DEC10 99.635 99.645 +0.005 99.645 99.635 222300

Euro¥ MAR11 99.640 99.650 +0.010 99.650 99.635 155336

Euro¥ JUN11 99.640 99.650 +0.010 99.655 99.635 132474

____________________________________________

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 59/68

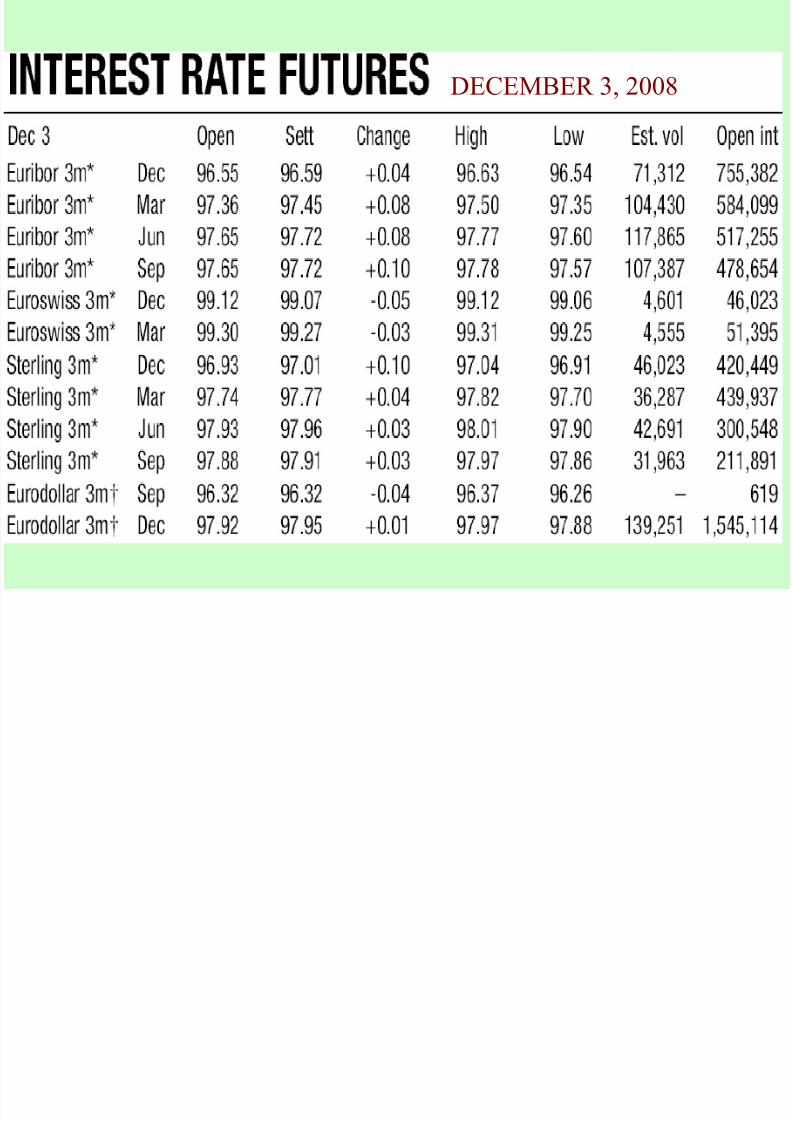

DECEMBER 3, 2008

INTEREST RATE FUTURES DECEMBER 3 2008

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 60/68

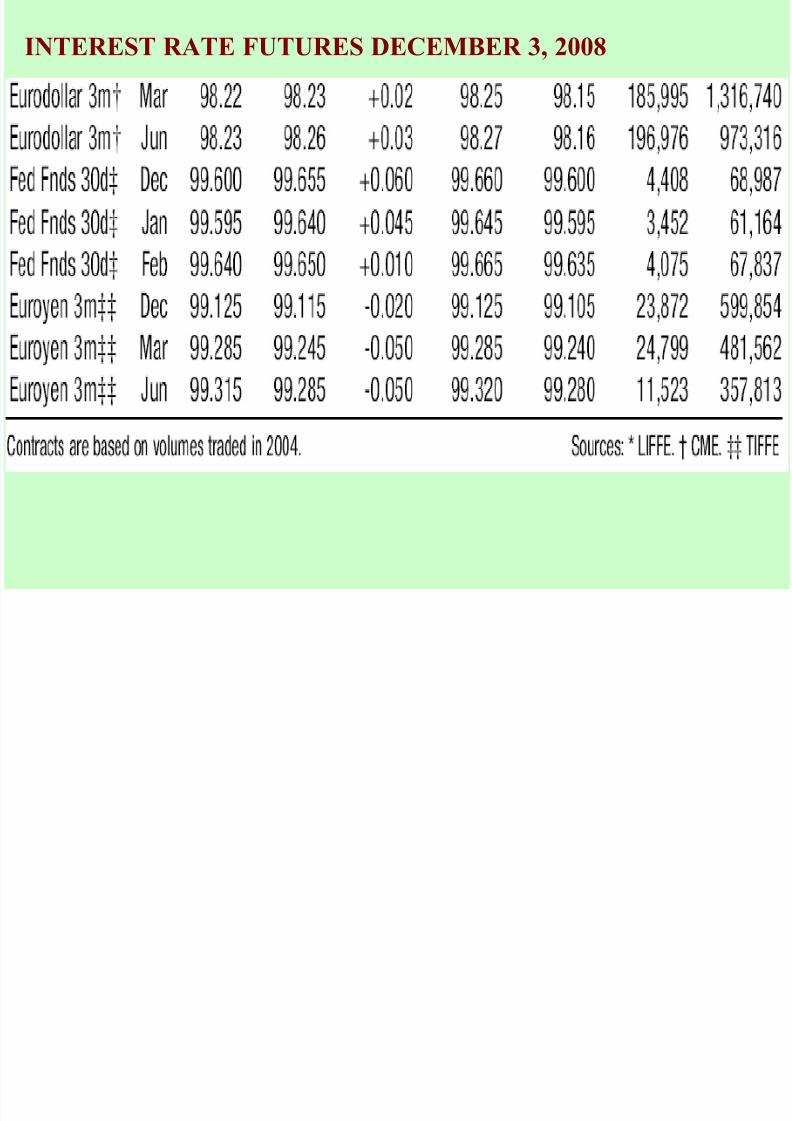

INTEREST RATE FUTURES DECEMBER 3, 2008

LONG TERM INTEREST RATE FUTURES

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 61/68

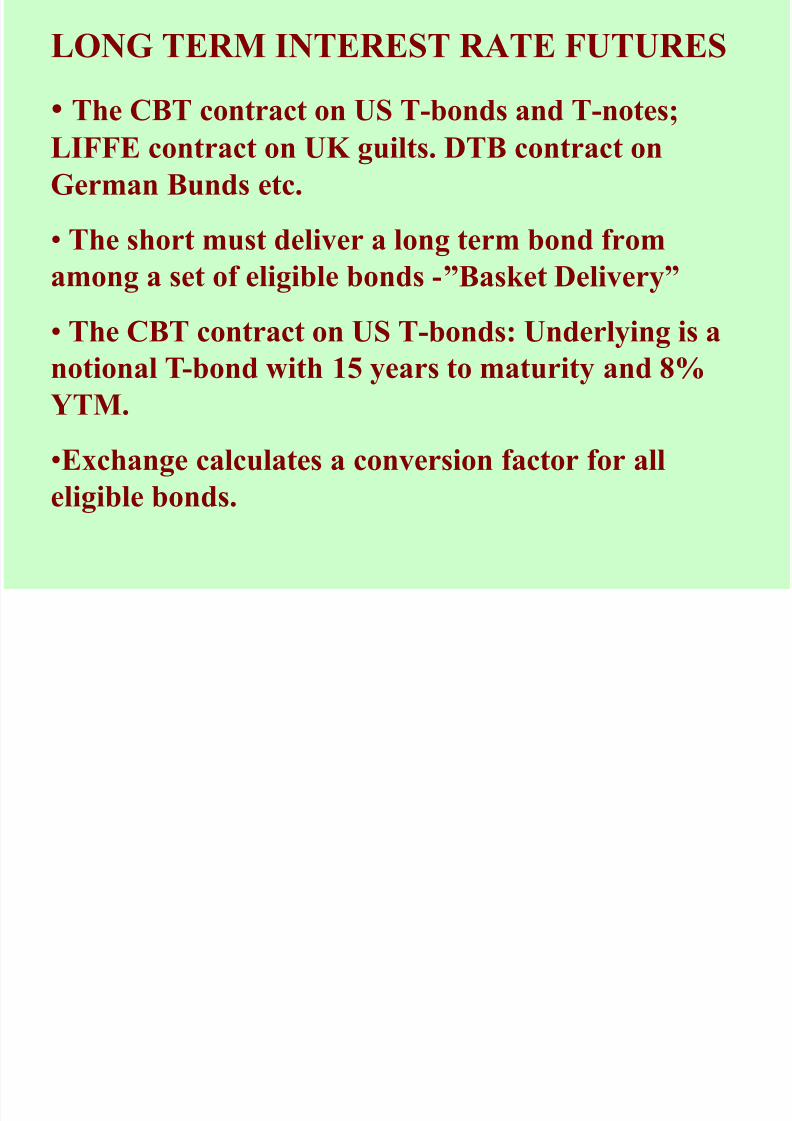

LONG TERM INTEREST RATE FUTURES

• The CBT contract on US T-bonds and T-notes;

LIFFE contract on UK guilts. DTB contract onGerman Bunds etc.

• The short must deliver a long term bond from

among a set of eligible bonds -”Basket Delivery”

• The CBT contract on US T-bonds: Underlying is a

notional T-bond with 15 years to maturity and 8%

YTM.

•Exchange calculates a conversion factor for all

eligible bonds.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 62/68

LONG TERM INTEREST RATE FUTURES

For US T-bond futures, price stated as % of face value with

minimum 1/32% e.g.

Price : 103-18 means 103 and (18/32) percent of $100000

Long pays: Settlement Price × Conversion factor

+ Accrued Interest

Conversion Factor necessary because different bonds have

different coupons and maturities.

An eligible bond has CF of 1.5 - Each of these bonds equals 1.5

of notional bonds.

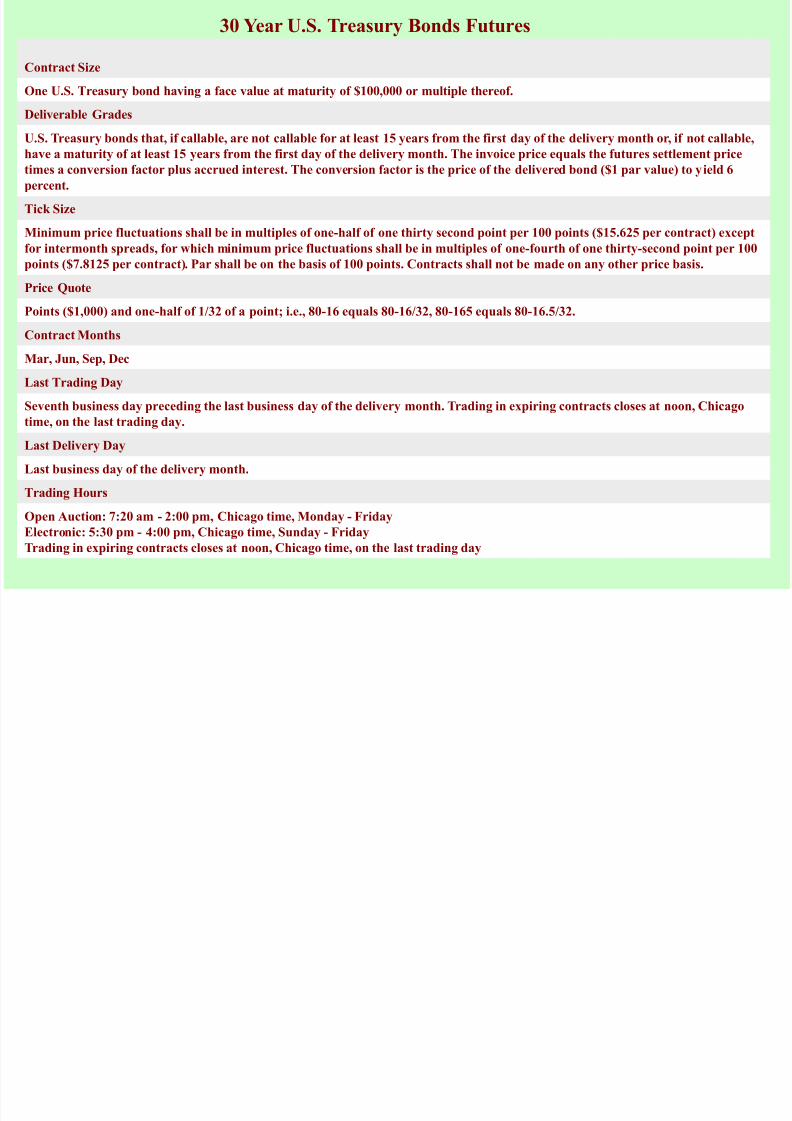

30 Year U.S. Treasury Bonds Futures

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 63/68

Contract Size

One U.S. Treasury bond having a face value at maturity of $100,000 or multiple thereof.

Deliverable Grades

U.S. Treasury bonds that, if callable, are not callable for at least 15 years from the first day of the delivery month or, if not callable,

have a maturity of at least 15 years from the first day of the delivery month. The invoice price equals the futures settlement price

times a conversion factor plus accrued interest. The conversion factor is the price of the delivered bond ($1 par value) to yield 6

percent.

Tick Size

Minimum price fluctuations shall be in multiples of one-half of one thirty second point per 100 points ($15.625 per contract) except

for intermonth spreads, for which minimum price fluctuations shall be in multiples of one-fourth of one thirty-second point per 100

points ($7.8125 per contract). Par shall be on the basis of 100 points. Contracts shall not be made on any other price basis.

Price Quote

Points ($1,000) and one-half of 1/32 of a point; i.e., 80-16 equals 80-16/32, 80-165 equals 80-16.5/32.

Contract Months

Mar, Jun, Sep, Dec

Last Trading Day

Seventh business day preceding the last business day of the delivery month. Trading in expiring contracts closes at noon, Chicago

time, on the last trading day.

Last Delivery Day

Last business day of the delivery month.

Trading Hours

Open Auction: 7:20 am - 2:00 pm, Chicago time, Monday - Friday

Electronic: 5:30 pm - 4:00 pm, Chicago time, Sunday - Friday

Trading in expiring contracts closes at noon, Chicago time, on the last trading day

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 64/68

30-YEAR T-BOND FUTURES QUOTES

Thursday, 4 December

Contract Last Change Open High Low Prev.Stl.

Dec '08 132-310 +0-245 132-090 132-310 132-010 132-065

Mar '09 131-305 +0-230 130-315 131-315 130-150 131-075

Jun '09) 130-250 +0-230 0-000 130-250 130-020 130-020

Sep '09 129-135 +0-230 0-000 129-135 128-225 128-225

Dec '09 128-015 +0-230 0-000 128-015 127-105 127-105

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 65/68

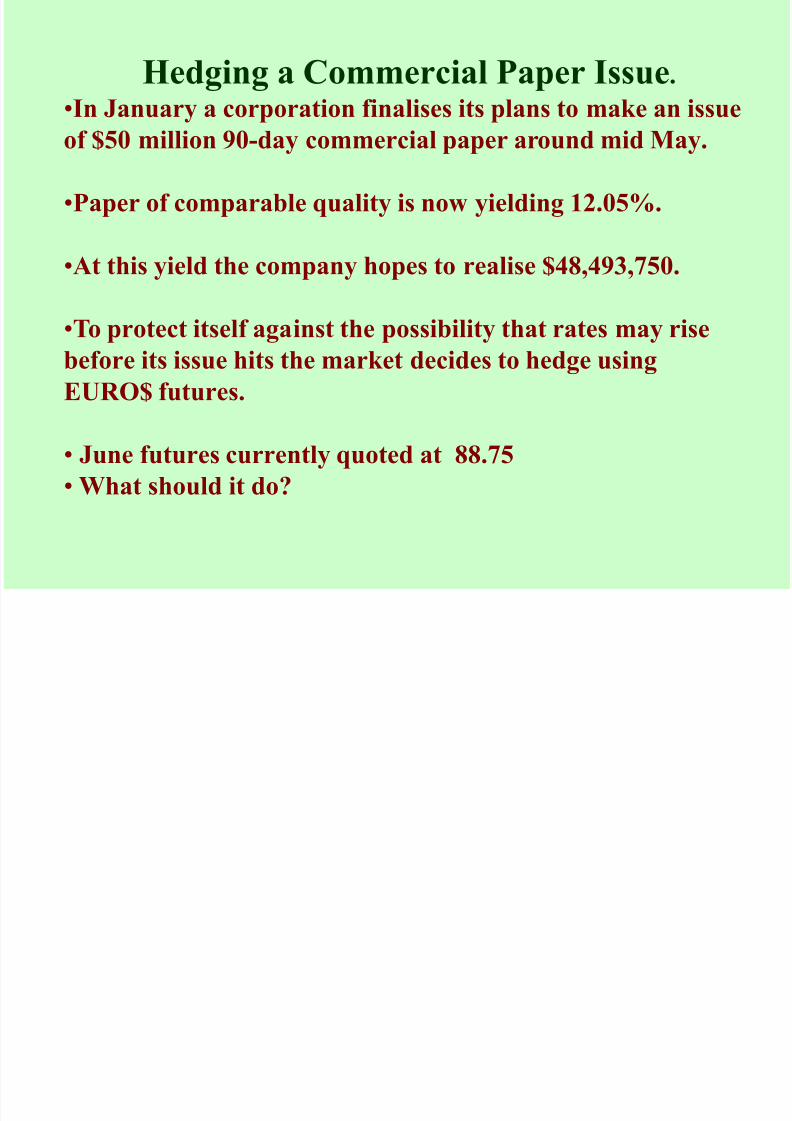

Hedging a Commercial Paper Issue.

•In January a corporation finalises its plans to make an issue

of $50 million 90-day commercial paper around mid May.

•Paper of comparable quality is now yielding 12.05%.

•At this yield the company hopes to realise $48,493,750.

•To protect itself against the possibility that rates may rise

before its issue hits the market decides to hedge using

EURO$ futures.

• June futures currently quoted at 88.75

• What should it do?

S C A O S A

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 66/68

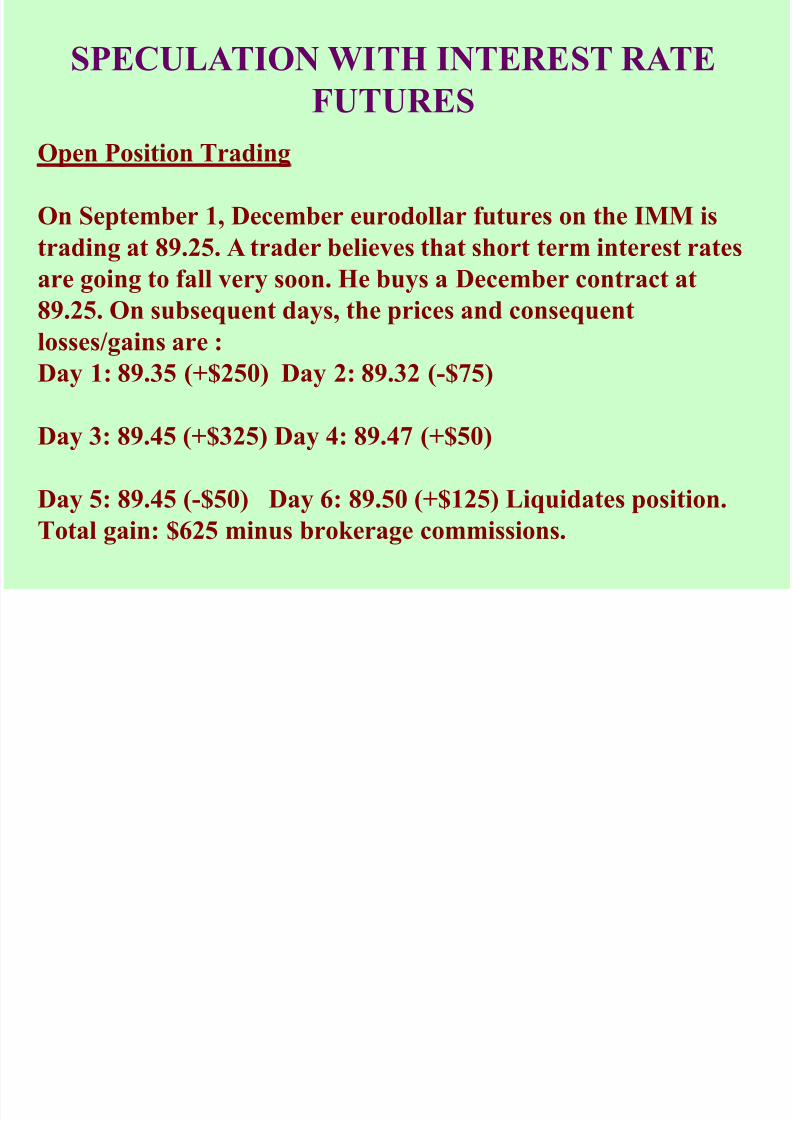

SPECULATION WITH INTEREST RATE

FUTURES

Open Position Trading

On September 1, December eurodollar futures on the IMM is

trading at 89.25. A trader believes that short term interest rates

are going to fall very soon. He buys a December contract at89.25. On subsequent days, the prices and consequent

losses/gains are :

Day 1: 89.35 (+$250) Day 2: 89.32 (-$75)

Day 3: 89.45 (+$325) Day 4: 89.47 (+$50)

Day 5: 89.45 (-$50) Day 6: 89.50 (+$125) Liquidates position.

Total gain: $625 minus brokerage commissions.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 67/68

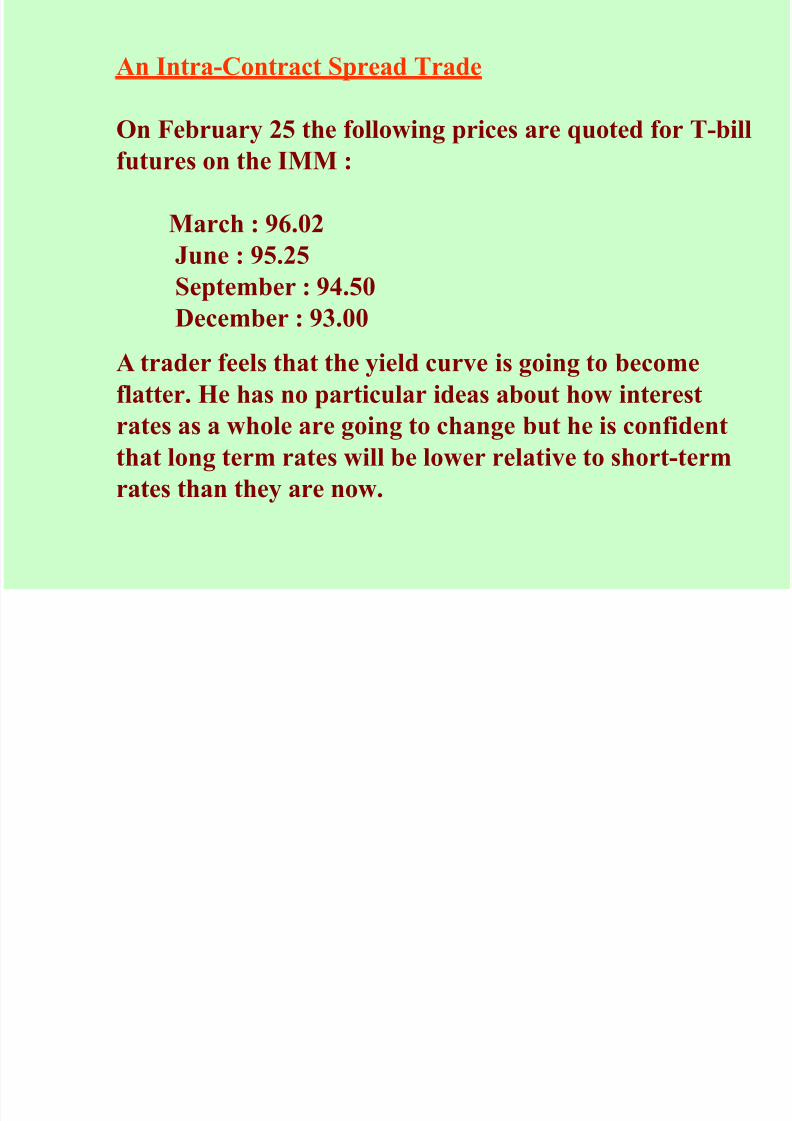

An Intra-Contract Spread Trade

On February 25 the following prices are quoted for T-bill

futures on the IMM :

March : 96.02

June : 95.25

September : 94.50December : 93.00

A trader feels that the yield curve is going to become

flatter. He has no particular ideas about how interest

rates as a whole are going to change but he is confidentthat long term rates will be lower relative to short-term

rates than they are now.

7/29/2019 Curr Futures

http://slidepdf.com/reader/full/curr-futures 68/68

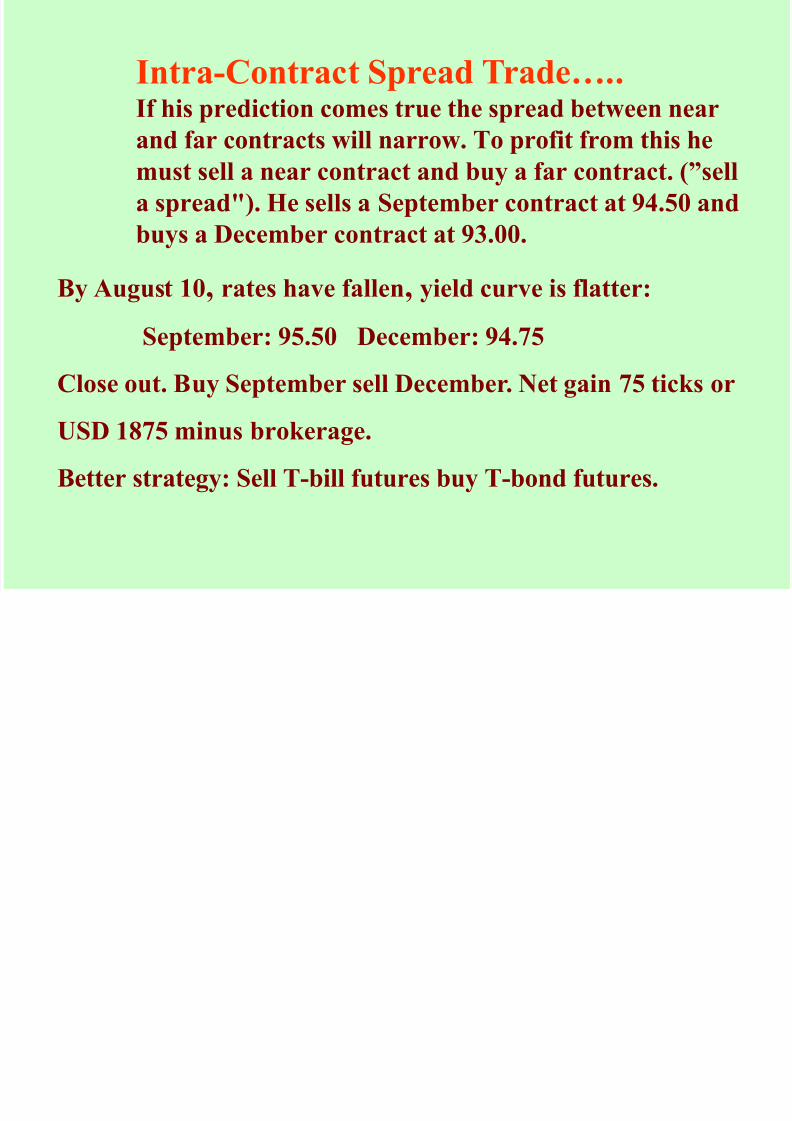

Intra-Contract Spread Trade….. If his prediction comes true the spread between near

and far contracts will narrow. To profit from this hemust sell a near contract and buy a far contract. (”sell

a spread"). He sells a September contract at 94.50 and

buys a December contract at 93.00.

By August 10, rates have fallen, yield curve is flatter:

September: 95.50 December: 94.75

Close out. Buy September sell December. Net gain 75 ticks or

USD 1875 minus brokerage.

Better strategy: Sell T-bill futures buy T-bond futures.