cultural biases in economic exchange? *

TRANSCRIPT

CULTURAL BIASES IN ECONOMIC EXCHANGE?∗

LUIGI GUISO

PAOLA SAPIENZA

LUIGI ZINGALES

How much do cultural biases affect economic exchange? We answer this ques-tion by using data on bilateral trust between European countries. We documentthat this trust is affected not only by the characteristics of the country beingtrusted, but also by cultural aspects of the match between trusting country andtrusted country, such as their history of conflicts and their religious, genetic, andsomatic similarities. We then find that lower bilateral trust leads to less trade be-tween two countries, less portfolio investment, and less direct investment, even af-ter controlling for the characteristics of the two countries. This effect is stronger forgoods that are more trust intensive. Our results suggest that perceptions rooted inculture are important (and generally omitted) determinants of economic exchange.

We always have been, we are, and I hope that we alwaysshall be detested in France.

Duke of Wellington

I. INTRODUCTION

There are remarkable differences in the level of trust amongEuropean managers. When asked to score fellow managers of dif-ferent countries on the basis of their trustworthiness their re-sponses implied the following ranking (where 1 is the best and 5the worst):1

∗We thank Giuseppe Nicoletti for providing the Organisation for EconomicCo-operation and Development data set, Michele Gambera for providing the Morn-ingstar portfolio data, and Roc Armenter for his excellent job as a research assis-tant. We also thank Franklin Allen, Marianne Baxter, Patricia Ledesma, MitchellPetersen, Andrei Shleifer, Rene Stulz, and Samuel Thompson for their very help-ful comments. We thank Jim Fearon and Romain Wacziarg for their help with themeasure of linguistic common roots. We benefited from the comments of partici-pants to seminars at the European University Institute, Wharton, NorthwesternUniversity, University of Chicago, University of Wisconsin, NBER Corporate Fi-nance, International Trade, and Behavioral Meetings and Peggy Eppink for edito-rial help. Luigi Guiso acknowledges financial support from MURST and the EEC.Paola Sapienza acknowledges financial support from the Center for InternationalEconomics and Development at Northwestern University. Luigi Zingales acknowl-edges financial support from the Center for Research on Security Prices and theStigler Center at the University of Chicago.

1. The survey was carried out by the 3i/Cranfield European Enterprise Centeron a total of 1,016 managers (managing companies under 500 employees) fromfive major European Community countries: Great Britain (433 responses), France(127), Germany (135), Italy (185), and Spain (136). See Burns, Myers, and Bailey(1993).C© 2009 by the President and Fellows of Harvard College and the Massachusetts Institute ofTechnology.The Quarterly Journal of Economics, August 2009

1095

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1096 QUARTERLY JOURNAL OF ECONOMICS

View Great Britain France Germany Italy Spain

British 1 4 2 5 3French 4 2 1 5 3German 2 3 1 5 4Italian 3 2 1 4 5Spanish 2 4 1 5 3

Among these managers there seem to be some common views:everyone ranks German managers relatively high and Italianones relatively low. There is also a “home-country bias”: man-agers trust their fellow countrymen more than what managersfrom other countries rank them. For instance, Italian managersrank themselves fourth in trustworthiness, while they are rankedfifth (last) by every other group. More surprising, there are somematch-specific attitudes. French managers rate British managersmuch lower than any other ones except the Italians, which seemsat odds with the ranking chosen by every other group. However,the British managers reciprocate this attitude (as the Duke ofWellington’s opening quote seems to suggest).

These facts are not peculiar to this data set. As we show,they are exactly replicated in an independent and broader survey(Eurobarometer). In this paper, we use this larger data set toexplain why the perception of trustworthiness differs so greatlyacross Europe. We also use it to explore the economic consequencesof these different perceptions.

To disentangle the country-specific components of trust fromthe match-specific ones we regress bilateral trust on fixed effectsfor the country receiving trust (country-of-destination fixed ef-fects) and fixed effects for the country trusting (country-of-originfixed effects). The country-of-destination fixed effects capture thecommon view about the trustworthiness of a country, which derivefrom the quality of the law and its enforcement. The country-of-origin fixed effects capture possible systematic differences in theway different populations answer the survey.

We then try to explain bilateral trust, after controlling for theabove fixed effects, with differences in information and culture.We find that geographical distance between two countries, theirproximity, and the commonality between the two languages havea significant effect on bilateral trust. By contrast, bilateral trustis negatively correlated with a country’s exposure in the domesticnewspapers of another country. Sharing the same legal origin (avariable that could proxy for both information and culture) has

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1097

a positive and significant effect on the level of trust, as long aswe do not control for the common linguistic root. Once we controlfor linguistic root, the commonality-of-law effect halves and be-comes insignificant, suggesting that most of the effect comes fromcultural commonalities.

As a first pure measure for a country’s cultural tradition, weuse commonality of religion. Religion had (and still has) a greatimpact on what is taught in school and how it is taught. Hence,we expect that two countries with the same religion tend to havesimilar cultures and therefore will trust each other more. Indeed,we find this to be the case. A pair of countries where 90% ofcitizens share the same religion (e.g., Italy and Spain) has a levelof bilateral trust one-quarter of a standard deviation higher.

To further measure cultural similarity between two popula-tions, we introduce two new variables. First is the genetic distancebetween two populations that—as Ammerman and Cavalli-Sforza(1985) claim—reflects the history of invasions during the Neo-lithic Age and thus their common linguistic and cultural roots. AsDeBruine (2002) has shown in an experiment, people trust peoplewho look like them more than those who do not. We find this to betrue also in our sample. A one-standard-deviation increase in ge-netic distance reduces the level of bilateral trust by 1.8 standarddeviations.

Second, we derive from Biasutti (1954) an indicator of so-matic distance, based on the average frequency of specific traits(hair color, height, etc.) present in the indigenous population.People trust other people who look like them more. A one-standard-deviation increase in somatic distance decreases trustby one-quarter of a standard deviation. When we use both theaforementioned variables, only the latter remains significant.

Finally, to capture the effect of more recent aspects of the cul-tural tradition, we use a country’s history of wars. People’s priorscan be affected by their education and in particular by the historythey study in school. For instance, Italian education emphasizesthe struggles that led to the reunification of the country in thenineteenth century. Because the major battles during this periodwere fought against Austria, Italian students may develop, as ourdata show, a negative image of Austrians. We find that countrieswith a long history of wars tend to trust each other less. Franceand England, which have a record 198 years of war (more thanten times the average of nineteen) should exhibit a bilateral trustthat is 0.7 of a standard deviation lower than average, which fully

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1098 QUARTERLY JOURNAL OF ECONOMICS

accounts for the lower bilateral trust we observe between the twocountries.

Once we establish the cultural roots of trust, we move tostudy the effect of trust on international trade and investments.Unlike Anderson and Marcouiller (2002), De Groot et al. (2004),Berkowitz, Moenius, and Pistor (2006), and Nunn (2007), wholook at the effect of country-level institutional variables (for eitherthe importing or the exporting country) on trade, we look at theeffect of a match-specific variable (bilateral trust) on trade andinvestments.

We find that a higher level of bilateral trust can explaincross-country trade beyond what extended gravity models can ac-count for, even after controlling for the better estimates of trans-portation costs suggested by Giuliano, Spilimbergo, and Tonon(2006). At sample means, a one-standard-deviation increase inthe importer’s trust toward the exporter raises exports by 10%.Consistent with a trust-based explanation, we find that trustmatters more for trade in goods that Rauch (1999) classifies asdifferentiated goods, which can vary greatly in quality.

We then instrument trust with its long-term cultural compo-nents (the commonality in religion and in ethnic origin) and obtainmuch larger coefficients. Despite the fact that we pass the test ofoveridentifying restrictions, this difference suggests that cultureis likely to affect trade through other channels besides trust.

We find similar results when we analyze the pattern of foreigndirect investments (FDI) and portfolio investments. A country ismore willing to invest in another (either directly or via the equitymarket) when it trusts the other country’s citizens more. Not onlydo the latter results confirm our trade ones, but they also suggestthat cultural effects are not limited to unsophisticated consumers,but are also present among sophisticated professionals such asmutual fund managers.

Our combined results suggest that cultural relationships af-fect trust and are an important omitted factor in internationaltrade and investments. In this respect, our paper is part ofa new strand of literature that looks at the effect of cultureon economic and political outcomes (Barro and McCleary 2003;Guiso, Sapienza, and Zingales 2003, 2004b, 2006, 2008a, 2008b;Fernandez and Fogli 2007; Giuliano 2007; and Tabellini 2007,2008).

Because genetically similar countries trust each other moreand thus can transfer technology faster and more effectively, our

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1099

results explain the correlation between level of development andgenetic distance found by Spolaore and Wacziarg (2009). Finally,our results are validated in a micro setting by Bottazzi, Da Rin,and Hellmann (2007), who find that that venture capitalists aremore likely to invest in start-ups of countries they trust more.

In our attempt to explain several international exchange puz-zles, our paper is similar to that of Portes and Rey (2005). How-ever, they do not consider trust as a key determinant, but insteadfocus on differences in information, measured as telephone traf-fic between two countries and the number of local foreign bankbranches.2

II. BILATERAL TRUST

We obtain our measures of trust from a set of surveys con-ducted by Eurobarometer and sponsored by the European Com-mission. The surveys were designed to measure public awarenessof, and attitudes toward, the Common Market and other Euro-pean Community institutions (see the Online Data Appendix fordetails). They were conducted on a representative sample of thetotal population of age sixteen (or fifteen depending on the wave)and older: about 1,000 individuals per country. The set of countriessampled varies over time with the enlargement of the EuropeanUnion: there were five in 1970 (France, Belgium, The Netherlands,Germany, and Italy), when the first survey was conducted, and ithad grown to seventeen in 1995, the last survey to which we haveaccess (besides the five countries above, Luxembourg, Denmark,Ireland, Great Britain, Northern Ireland, Greece, Spain, Portugal,Norway, Sweden, Finland, and Austria are also included).

One distinct feature of these surveys is that respondents wereasked to report how much they trust their fellow citizens andhow much they trust the citizens of each of the countries in theEuropean Union. More specifically, they were asked the following:

2. Our paper is also related to those of Vlachos (2004), Morse and Shive (2006),and Cohen (2009). Morse and Shive (2006) relate portfolio choices to the degree ofpatriotism of a country. Cohen (2009) shows that employees’ bias toward investingin their own company is not due to information, but to some form of loyalty towardtheir company, which can easily be interpreted as trust. Both of these papersthus illustrate one specific dimension in which cultural biases can affect economicchoices. Our paper can be seen as a generalization of Rauch and Trindade (2002).They find that the percentage of ethnic Chinese in a country helps predict the levelof trade beyond the standard specification. We show that this result is not specificto ethnic networks. Any cultural barrier (or lack thereof) significantly impactstrade and investments.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1100 QUARTERLY JOURNAL OF ECONOMICS

“I would like to ask you a question about how much trust you havein people from various countries. For each, please tell me whetheryou have a lot of trust, some trust, not very much trust, or no trustat all.”

In some of the surveys, this same question was also asked withreference to citizens of a number of non–European Union coun-tries, including the United States, Russia, Switzerland, China,Japan, Turkey, and some Eastern and Central European countries(Bulgaria, Slovakia, Romania, Hungary, Poland, Slovenia, and theCzech Republic). To ensure a relative degree of homogeneity intrading-rule and living standards, we restrict our analysis to thecountries belonging to the European Economic Area (EEA): Euro-pean Union members plus Norway. These are also the countriesfor which we have both the trust from and to, thereby making thematrix quadratic.3

As in every survey, there may be some doubts about the waypeople interpret the trust question. First, there is some ambiguityon how to interpret it. In a trust game, the level of trust maps intothe amount of money you are willing to risk. Here, this mappingis missing. Second, we are concerned whether a high level of trustreflects a high trust in a generic citizen of a different country ora better ability to identify the trustworthy people in a differentcountry, which translates into a higher willingness to trust them.

To address these doubts, in a separate survey we asked asample of 1,990 individuals both the question above and the twofollowing ones: (i) “Suppose that a random person you do not knowpersonally receives by mistake a sum of 1,000 euros that belongto you. He or she is aware that the money belongs to you andknows your name and address. He or she can keep the moneywithout incurring in any punishment. According to you what isthe probability (a number between zero and 100) that he or shereturns the money?” and (ii) “How good are you (very good, good,not very good, not good at all) in detecting people who are trust-worthy?” (Guiso, Sapienza, and Zingales, 2008c). We find that thefirst question is highly statistically correlated with the measureof trust used in this paper, but the second one is not (the sign isactually negative, albeit not statistically significant). Hence, thesedata provide evidence that the reported level of trust reflects thesubjective probability that a random person is trustworthy.

3. In the NBER working paper version we also considered the full rectangularmatrix of trust.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1101

There can also be doubts on the external validity of this ques-tion. Glaeser et al. (2000), for instance, raise doubts on the va-lidity of the World Values Survey (WVS) trust question (whichis similar to the one we use), by showing that it is not corre-lated with the sender behavior in the standard trust game (Berg,Dickhaut, and McCabe 1995). However, Sapienza, Toldra, andZingales (2007) argue that the sender’s behavior in the trustgame is not a good measure of trust, because it is affected byother regarding preferences. From the trust game we can de-rive a better indicator of trust: the sender’s expectation aboutthe receiver’s behavior. Sapienza, Toldra, and Zingales (2007)show that the WVS trust question as well as other similar trustquestions are strongly correlated with these expectations. Fur-thermore, in a sample of Dutch households, Guiso, Sapienza,and Zingales (2008c) find a correlation between the answer tothe WVS question on trust and the decision to invest in eq-uity. Thus, this survey-based measure does have some externalvalidity.

This WVS-type of question measures generalized trust, thetrust people have toward a random member of an identifiablegroup (e.g., Guiso, Sapienza, and Zingales [2004b]; McEvily et al.[2006]). This is different from personalized trust, the mutual trustpeople develop through repeated interactions (Greif 1993), whichis more important in relational contracts.

For our purposes, we first recoded the answers to the trustquestion, setting them to 1 (no trust at all), 2 (not very muchtrust), 3 (some trust), and 4 (a lot of trust). We then aggregatedresponses by country and year, computing the mean value of theresponses to each survey.

Table I shows the average level of trust that citizens from eachcountry have toward citizens of other countries. There is consid-erable variation in the level of trust exhibited from one country toanother. The average level of trust ranges from a minimum trustof 2.13 (the trust of Portuguese toward Austrians) to a maximumof 3.69 (the trust of Finns toward Finns).

Besides this variability, in Table I we find the same three reg-ularities found in the small survey presented in the Introduction.First, there are systematic differences in how much a given coun-try trusts and how much it is trusted by others (see the last rowand last column of Table I). For instance, Panel B shows that thePortuguese and the Greeks are those who trust the least and theSwedes those who trust the most.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1102 QUARTERLY JOURNAL OF ECONOMICST

AB

LE

IT

HE

TR

US

TM

AT

RIX

Cou

ntr

ies

ofde

stin

atio

n

Cou

ntr

ies

ofor

igin

Au

sB

elU

KD

enN

LF

inF

raG

erG

reIr

eIt

aN

orP

orS

paS

we

Ave

rage

Au

stri

a3.

562.

952.

612.

952.

952.

942.

623.

092.

522.

552.

433.

002.

502.

583.

052.

82B

elgi

um

2.83

3.28

2.84

3.01

2.90

2.92

2.92

2.75

2.45

2.75

2.40

2.91

2.53

2.59

2.99

2.80

Un

ited

Kin

gdom

2.89

2.91

3.29

3.13

3.16

2.98

2.32

2.62

2.54

2.61

2.51

3.06

2.74

2.47

3.03

2.82

Den

mar

k3.

223.

183.

223.

393.

333.

202.

863.

122.

613.

022.

533.

502.

672.

663.

413.

06N

eth

erla

nds

2.90

3.18

3.00

3.29

3.28

3.25

2.72

2.84

2.59

2.80

2.35

3.30

2.74

2.64

3.34

2.95

Fin

lan

d3.

293.

073.

183.

303.

143.

692.

922.

892.

682.

922.

513.

482.

672.

613.

353.

05F

ran

ce2.

703.

072.

552.

962.

942.

913.

182.

742.

532.

722.

432.

972.

592.

682.

992.

80G

erm

any

2.98

2.84

2.69

2.97

2.90

2.85

2.85

3.50

2.51

2.59

2.36

2.92

2.48

2.66

2.99

2.81

Gre

ece

2.32

2.60

2.34

2.56

2.55

2.42

2.78

2.31

3.21

2.55

2.33

2.40

2.60

2.71

2.51

2.55

Irel

and

2.93

2.93

2.81

2.99

3.00

2.92

2.81

2.78

2.50

3.33

2.65

2.93

2.65

2.64

2.92

2.85

Ital

y2.

662.

642.

512.

702.

772.

782.

662.

632.

402.

372.

802.

782.

322.

642.

892.

64N

orw

ay—

3.18

3.27

3.53

3.26

—2.

932.

992.

523.

012.

65—

2.60

2.56

—2.

95P

ortu

gal

2.13

2.66

2.66

2.66

2.70

2.18

2.91

2.54

2.41

2.51

2.55

2.22

3.29

2.59

2.24

2.55

Spa

in2.

652.

732.

312.

732.

852.

712.

372.

662.

472.

572.

612.

792.

513.

322.

842.

67S

wed

en3.

533.

233.

433.

573.

333.

493.

043.

132.

883.

262.

813.

652.

972.

863.

593.

25

Ave

rage

2.90

2.96

2.85

3.05

3.00

2.95

2.79

2.84

2.59

2.77

2.53

2.99

2.66

2.68

3.01

Not

e.T

his

tabl

edi

spla

ysth

eav

erag

ele

velo

ftru

stfr

omci

tize

ns

ofco

un

try

ofor

igin

(row

s)to

citi

zen

sof

cou

ntr

yof

dest

inat

ion

(col

um

ns)

.Tru

stis

calc

ula

ted

byta

kin

gth

eav

erag

ere

spon

seto

the

foll

owin

gqu

esti

on:“

Iw

ould

like

toas

kyo

ua

ques

tion

abou

th

owm

uch

tru

styo

uh

ave

inpe

ople

from

vari

ous

cou

ntr

ies.

For

each

,ple

ase

tell

me

wh

eth

eryo

uh

ave

alo

tof

tru

st,s

ome

tru

st,n

otve

rym

uch

tru

st,o

rn

otr

ust

atal

l.”T

he

answ

ers

are

code

din

the

foll

owin

gw

ay:1

(no

tru

stat

all)

,2(n

otve

rym

uch

tru

st),

3(s

ome

tru

st),

4(a

lot

oftr

ust

).

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1103

To isolate these country-specific factors we run the followingregression:

(1) ¯Trusti jt = κi + λ j +n∑

t=1

γtYeart + εi jt,

where ¯Trusti jt is the trust of country i for country j in the surveydone at time t, κi a country-of-origin fixed effect, λ j a country-of-destination fixed effect, and Yeart calendar-year dummies. Be-cause we are interested in trust across different populations, wedrop all the observations when i = j.

In Figure I, we report the fixed effects of the country of ori-gin and the country of destination relative to Ireland (the actualestimates are reported in the Online Appendix). A Swedish cit-izen trusts others 17% more on average than an Irish citizenand 27% more than a Greek citizen. The least trusted popula-tion is the Italians (like in the introductory example), whereasthe most trusted ones are the Swedes. Interestingly, there is acorrelation between trusting and being trusted. Nordic countriesare at the top of the level of trustworthiness and tend to trustothers the most. Although not definitive proof, this fact suggeststhat people excessively apply the level of trustworthiness of theirown countrymen to people from other countries. This result is alsoconsistent with experimental evidence in Glaeser et al. (2000) andSapienza, Toldra, and Zingales (2007).

If all (or almost all) the variation in the data was explainedby the attitude that citizens of a country have toward trust (beingtrusted), there would be little hope for relative trust to be able toaffect the patterns of bilateral trade. However, country-of-originfixed effects and country-of-destination fixed effects explain only64% of the variability in trust. There remains a considerable por-tion to be explained with match-specific variables. The British,for instance, tend to trust the French even less than they trustthe Italians and the Spanish and much less than they trust theBelgians and the Dutch. The French reciprocate by trusting theBritish as much as they trust (little) the Greeks.

III. WHAT EXPLAINS BILATERAL DIFFERENCES IN TRUST?

In this section we try to explain bilateral trust with match-specific variables, after controlling for country fixed effects.To avoid understating the standard errors due to repeated

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1104 QUARTERLY JOURNAL OF ECONOMICS

FIGURE IFixed Effects of Country of Origin and Destination Relative to Ireland

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1105

observations, we follow Bertrand, Duflo, and Mullainathan (2004)and collapse the data by averaging over time the residuals of re-gressing trust on calendar-year dummies. Hence, our regressionwill be

(2) ¯Trusti j = κi + λ j + βXij + εi j,

where ¯Trusti j are the residuals of regressing trust on calendar-year dummies averaged over time and Xij are match-specific vari-ables that we describe soon.

III.A. Determinants of Bilateral Trust

Why should countries differ in their trust toward the samepopulation? One possibility is that these variations are just noiseand, as such, it should not be correlated with any possible deter-minants. Another possibility is that these variations arise fromdifferences in the information sets: more informed countries willhave a better estimate, whereas poorly informed ones will have aworse estimate. The alternative is that there might be some sortof bias, in either the perception or the behavior. The British mighthave a distorted view of French reliability or the French mightderive a special pleasure from breaching the trust of a Britishperson. For the moment, we are going to collapse both of these lat-ter explanations, which are difficult to separate, under the termof “cultural determinants,” but we will return to this later.

Proxies for Information. As measures of information, we usethe geographical distance between the two countries, their prox-imity, and the commonality between the two languages. The geo-graphical distance between two countries is the log of distance inkilometers between the major cities (usually the capital) of therespective countries.4 We also add a dummy variable to indicatewhen two countries share a common land border (Frankel, Stein,and Wei 1995). As a measure of language commonality, we usean indicator variable equal to 1 if two countries share the sameofficial language.5 We use the transportation cost estimates intro-duced by Giuliano, Spilimbergo, and Tonon (2006) as an additional

4. This measure is from Frankel, Stein, and Wei (1995). We also tried ourregressions with alternative measures of distance between two countries and theresults did not change substantially. Specifically, we used distance in radians ofthe unit circle between country centroids (Boisso and Ferrantino 1997) and thegreat circle between the largest cities (Fitzpatrick and Modlin 1986).

5. This variable is from Jon Haveman’s website: http://www.macalester.edu/research/economics/PAGE/HAVEMAN/Trade.Resources/TradeData.html.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1106 QUARTERLY JOURNAL OF ECONOMICS

measure of distance. These transportation costs are measured us-ing shipping companies’ quotes collected from Import Export Wiz-ard (a shipping company providing transportation quotes aroundthe world).6

To measure the level of information the citizens of one countryhave about citizens of another, we follow Portes and Rey (2005)and collect the number of times the country toward which trustis expressed appears in the headlines of a major newspaper inthe country that expresses the trust. In Factiva, we searched thenewspaper with the highest circulation for each country. For eachpair of countries i and j, we recorded the number of articles in thenewspaper of country i that mentioned country j or its citizens inthe headline. We divided this number by the number of total newsstories on foreign countries.7

In addition to these measures, we use the La Porta et al.(1998) classification of legal origin and construct a dummy vari-able equal to 1 when the legal system of two countries is derivedfrom the same legal family (i.e., French, German, Scandinavian,English). Commonality in legal origin may in principle reflect thefact that citizens of countries having similar legal systems trusteach other more because there is less fear of the unknown. Thelegal tradition is likely to be very highly correlated with a commonheritage and other cultural variables. Thus, controlling for com-mon legal origin, we underestimate the potential effect of culturein biasing the perception of trustworthiness.

Proxies for Culture. The first proxy for culture is an indicatorof religious similarity equal to the empirical probability that tworandomly chosen individuals in two countries will share the samereligion. We obtain this measure by taking the product of the frac-tion of individuals in country j and in country i who have religionk and then we sum across all religions k (k = Catholic, Protestant,Jewish, Muslim, Hindu, Buddhist, Orthodox, no religion, otheraffiliation). To calculate this variable we use the percentage ofpeople belonging to each religious denomination from the WVS(see Guiso, Sapienza, and Zingales [2003]).

Although religious differences are rooted in past history, thishistory is relatively recent (300–400 years) and could reflect some

6. http://www.importexportwizard.com. Specifically, we use the cost in U.S.dollars of transporting 1,000 kg of unspecified freight type load (including machin-ery, chemicals, etc.) with no special handling required, using the optimal combi-nation of going through land and water to transport the goods.

7. In Factiva, we were unable to locate any newspaper from Greece andFinland. Hence, when we use press coverage the size of sample drops.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1107

comparative advantage in trading. For this reason, we resort toethnic differences to capture deeper cultural roots. Much of theethnic variation in Europe reflects Neolithic invasions: two-thirdsof Europeans descend from Asian invaders and one-third fromAfrican invaders (Cavalli-Sforza 2000).8

To measure these ethnic differences, we use the genetic dis-tance between indigenous populations as developed by Cavalli-Sforza, Menozzi, and Piazza (1996).9 This measure is based onthe existence of genetic or DNA polymorphism (a situation inwhich a gene or a DNA sequence exists in at least two differentforms [alleles]). A simple example of polymorphism is the ABOblood group classification. Although ABO alleles are present inall populations, the frequency of each allele varies substantiallyacross populations. For example, the O allele is frequent in 61%of African populations and 98% of Native American populations.These frequency differences in alleles hold true for other genes orDNA sequences as well. As a first approximation, Cavalli-Sforza,Menozzi, and Piazza (1996) derive a measure of the differences inthe genetic composition between two populations by summing thedifferences in frequencies of these polymorphisms.10

As an alternative measure of distance between two popula-tions, we derive an indicator of somatic distance, based on theaverage frequency of specific traits in the indigenous populationreported by Biasutti (1954). For height, hair color (pigmentation),and cephalic index (the ratio of the length and width of the skull),Biasutti (1954) draws a map of the prevailing traits in each coun-try in Europe. For each trait, European Union countries fall intothree different categories. For hair color we have “Blond prevails,”“Mix of blond and dark,” and “Dark prevails.” We arbitrarily assignthe score of 1 to the first, 2 to the second, and 3 to the third. Whenone’s country somatic characteristics belong to more than one cat-egory, we take the country’s most prevalent category. We thencompute the somatic distance between two countries as the sumof the absolute value of the difference in each of these traits (seeOnline Appendix for more details). Somatic and genetic distances

8. Giuliano, Spilimbergo, and Tonon (2006) claim that genetic distance issimply a proxy for transportation costs, at least in the Neolithic Age. Historicaltransportation costs, however, are not identical to current ones. Before the creationof several tunnels, the Alps represented a formidable barrier to communicationbetween Italy and the neighboring countries. Hence, when we control for today’stransportation costs in the regressions, genetic (or somatic) distance captures thehistorical transportation costs, which led to different cultural enclaves.

9. See also Menozzi, Piazza, and Cavalli-Sforza (1978).10. For a more detailed description of this measure see the Online Appendix.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1108 QUARTERLY JOURNAL OF ECONOMICS

are highly correlated (.53). Hence, we will be able to use only oneat a time.

Besides proxies for cultural distance, both somatic and ge-netic distances can be interpreted as measures of genetic dissim-ilarities. As DeBruine (2002) has shown in an experiment, peopletrust people who look like them more than those who do not.Hence, these two variables might proxy for a genetic element intrust, rather than for a cultural one. Either way, however, they area source of a potential bias that distorts an objective assessmentof the trustworthiness of a foreign population.

To capture these long-term elements of culture, we also usea measure of linguistic common roots created by Fearon andLaitin (2003). It is based on a count of the number of commonbranches two languages share in the language trees as reportedby Ethnologue.11

As a last measure of culture, we compute the number of yearsa country pair has been engaged in a war between year 1000 and1970. Because “history is very much a mythical construction, inthe sense that it is a representation of the past linked to the estab-lishment of an identity in the present” (Friedman 1992, pg. 195),we reconstruct wars using today’s borders. Cultural formation atschool is a vehicle for prolonging the memory of facts that tookplace many years ago (this is why we count wars over almost amillennium). Presumably, countries that have a long history ofwars and conflict will mistrust each other. As Table I shows, theclear tendency of the French to trust the British less than anyother country may reflect the 198 years that these two countrieshave waged war against each other since year 1000.

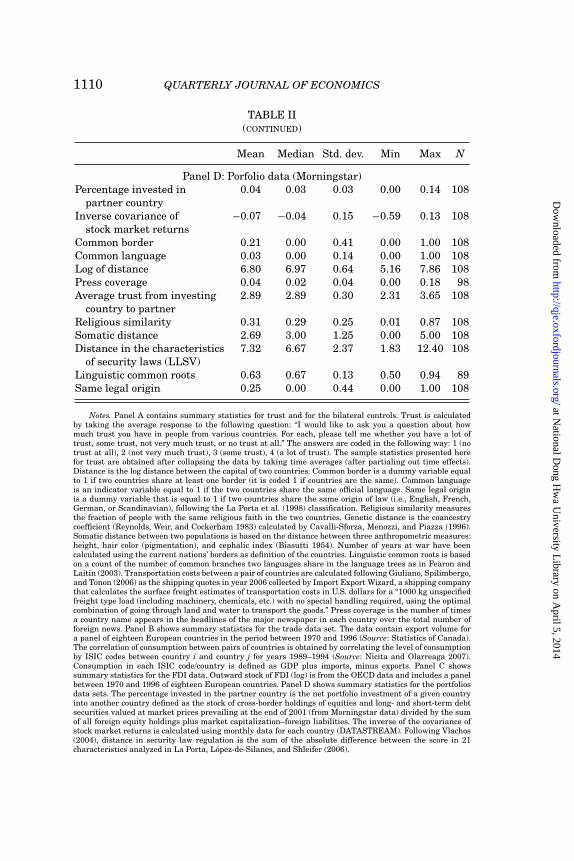

The summary statistics of these variables are reported inTable II (Panels A, C, D, and E), computed for the different samplesused in the paper.

III.B. Empirical Results

In Table III, we report the results of our estimates on thedeterminants of trust according to (2). Our dependent variable

11. http://www.ethnologue.com. Two languages that come from completelydifferent families have zero branches in common, whereas (say) English andFrench have one branch in common because they are both Indo-European, butEnglish is Germanic and French is Romance. Fearon and Laitin (2003) argue thatfor a measure of cultural distance, the move from zero to one common node ismore meaningful than a move from, say, five to six, so that a transformation with“diminishing returns” is better than simply counting common nodes. So, we uselinguistic common roots = # common nodes/(1 + # common nodes), though we alsotried other specifications with similar results.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1109

TABLE IISUMMARY STATISTICS

Mean Median Std. dev. Min Max N

A. Trust and control variablesAverage trust 0.06 0.04 0.30 −0.62 0.90 207Log of distance 7.08 7.18 0.64 5.16 8.12 207Common border 0.14 0.00 0.35 0.00 1.00 207Common language 0.04 0.00 0.19 0.00 1.00 207Same legal origin 0.27 0.00 0.45 0.00 1.00 207Religious similarity 0.29 0.23 0.26 0.00 0.87 207Genetic distance 73.66 63.00 54.80 9.00 289.00 207

(FST values ×10,000)Somatic distance 2.56 3.00 1.26 0.00 5.00 207Fraction of years at war 0.02 0.00 0.03 0.00 0.20 207

(1000–1970)Linguistic common roots 0.51 0.50 0.24 0.00 0.94 180Transportation costs 186.13 185.00 17.09 160.00 249.00 207Press coverage 0.03 0.01 0.04 0.00 0.31 179

B. Statistics of CanadaLog of export to 14.78 14.79 1.58 9.94 17.83 595

partner countryAverage trust from 2.74 2.74 0.28 1.99 3.57 595

importer to exporterPress coverage 0.04 0.02 0.05 0.00 0.31 595Log of distance 6.86 7.01 0.69 5.16 8.12 595Common border 0.21 0.00 0.41 0.00 1.00 595Common language 0.06 0.00 0.24 0.00 1.00 595Religious similarity 0.33 0.32 0.26 0.00 0.87 595Somatic distance 2.49 3.00 1.21 0.00 5.00 595Same origin of the law 0.30 0.00 0.46 0.00 1.00 595Transportation costs 5.19 5.18 0.08 5.08 5.52 595Linguistic common roots 0.56 0.50 0.17 0.00 0.94 573Correlation of consumption 0.89 0.90 0.06 0.72 0.99 474

by industry

C. OECD foreign direct investmentOutward stock of FDI (log) 21.10 21.40 2.14 12.42 24.18 439Average trust from country 2.77 2.77 0.27 2.10 3.53 439

to each partnerPress coverage 0.05 0.04 0.06 0.00 0.31 439Log of distance 6.78 6.96 0.72 5.16 8.12 439Common border 0.24 0.00 0.43 0.00 1.00 439Common language 0.09 0.00 0.28 0.00 1.00 439Same legal origin 0.32 0.00 0.47 0.00 1.00 439Religious similarity 0.37 0.34 0.23 0.01 0.87 439Somatic distance 2.67 3.00 1.27 0.00 5.00 439Linguistic common roots 0.56 0.50 0.21 0.00 0.94 413Transportation costs 5.18 5.15 0.09 5.08 5.52 439

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1110 QUARTERLY JOURNAL OF ECONOMICS

TABLE II(CONTINUED)

Mean Median Std. dev. Min Max N

Panel D: Porfolio data (Morningstar)Percentage invested in 0.04 0.03 0.03 0.00 0.14 108

partner countryInverse covariance of −0.07 −0.04 0.15 −0.59 0.13 108

stock market returnsCommon border 0.21 0.00 0.41 0.00 1.00 108Common language 0.03 0.00 0.14 0.00 1.00 108Log of distance 6.80 6.97 0.64 5.16 7.86 108Press coverage 0.04 0.02 0.04 0.00 0.18 98Average trust from investing 2.89 2.89 0.30 2.31 3.65 108

country to partnerReligious similarity 0.31 0.29 0.25 0.01 0.87 108Somatic distance 2.69 3.00 1.25 0.00 5.00 108Distance in the characteristics 7.32 6.67 2.37 1.83 12.40 108

of security laws (LLSV)Linguistic common roots 0.63 0.67 0.13 0.50 0.94 89Same legal origin 0.25 0.00 0.44 0.00 1.00 108

Notes. Panel A contains summary statistics for trust and for the bilateral controls. Trust is calculatedby taking the average response to the following question: “I would like to ask you a question about howmuch trust you have in people from various countries. For each, please tell me whether you have a lot oftrust, some trust, not very much trust, or no trust at all.” The answers are coded in the following way: 1 (notrust at all), 2 (not very much trust), 3 (some trust), 4 (a lot of trust). The sample statistics presented herefor trust are obtained after collapsing the data by taking time averages (after partialing out time effects).Distance is the log distance between the capital of two countries. Common border is a dummy variable equalto 1 if two countries share at least one border (it is coded 1 if countries are the same). Common languageis an indicator variable equal to 1 if the two countries share the same official language. Same legal originis a dummy variable that is equal to 1 if two countries share the same origin of law (i.e., English, French,German, or Scandinavian), following the La Porta et al. (1998) classification. Religious similarity measuresthe fraction of people with the same religious faith in the two countries. Genetic distance is the coancestrycoefficient (Reynolds, Weir, and Cockerham 1983) calculated by Cavalli-Sforza, Menozzi, and Piazza (1996).Somatic distance between two populations is based on the distance between three anthropometric measures:height, hair color (pigmentation), and cephalic index (Biasutti 1954). Number of years at war have beencalculated using the current nations’ borders as definition of the countries. Linguistic common roots is basedon a count of the number of common branches two languages share in the language trees as in Fearon andLaitin (2003). Transportation costs between a pair of countries are calculated following Giuliano, Spilimbergo,and Tonon (2006) as the shipping quotes in year 2006 collected by Import Export Wizard, a shipping companythat calculates the surface freight estimates of transportation costs in U.S. dollars for a “1000 kg unspecifiedfreight type load (including machinery, chemicals, etc.) with no special handling required, using the optimalcombination of going through land and water to transport the goods.” Press coverage is the number of timesa country name appears in the headlines of the major newspaper in each country over the total number offoreign news. Panel B shows summary statistics for the trade data set. The data contain export volume fora panel of eighteen European countries in the period between 1970 and 1996 (Source: Statistics of Canada).The correlation of consumption between pairs of countries is obtained by correlating the level of consumptionby ISIC codes between country i and country j for years 1989–1994 (Source: Nicita and Olarreaga 2007).Consumption in each ISIC code/country is defined as GDP plus imports, minus exports. Panel C showssummary statistics for the FDI data. Outward stock of FDI (log) is from the OECD data and includes a panelbetween 1970 and 1996 of eighteen European countries. Panel D shows summary statistics for the portfoliosdata sets. The percentage invested in the partner country is the net portfolio investment of a given countryinto another country defined as the stock of cross-border holdings of equities and long- and short-term debtsecurities valued at market prices prevailing at the end of 2001 (from Morningstar data) divided by the sumof all foreign equity holdings plus market capitalization–foreign liabilities. The inverse of the covariance ofstock market returns is calculated using monthly data for each country (DATASTREAM). Following Vlachos(2004), distance in security law regulation is the sum of the absolute difference between the score in 21characteristics analyzed in La Porta, Lopez-de-Silanes, and Shleifer (2006).

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1111T

AB

LE

III

DE

TE

RM

INA

NT

OF

TR

US

T

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

Com

mon

lan

guag

e0.

050.

09∗

0.11

∗0.

09∗

0.08

0.02

0.04

0.05

0.08

(0.0

7)(0

.05)

(0.0

6)(0

.05)

(0.0

5)(0

.06)

(0.0

6)(0

.06)

(0.0

6)L

og(d

ista

nce

)−0

.11∗

∗∗−0

.04∗

−0.0

5∗−0

.04

−0.0

1−0

.01

0.00

0.01

−0.0

1(0

.03)

(0.0

2)(0

.03)

(0.0

3)(0

.02)

(0.0

2)(0

.03)

(0.0

3)(0

.03)

Com

mon

bord

er−0

.01

−0.0

5−0

.01

−0.0

5−0

.04

−0.0

4−0

.05

−0.0

5−0

.03

(0.0

5)(0

.04)

(0.0

4)(0

.04)

(0.0

3)(0

.03)

(0.0

4)(0

.04)

(0.0

4)F

ract

ion

ofye

ars

atw

ar−1

.16∗

∗∗−1

.07∗

∗∗−1

.16∗

∗∗−1

.07∗

∗∗−1

.16∗

∗∗−1

.26∗

∗∗−1

.26∗

∗∗−1

.07∗

∗∗

(100

0–19

70)

(0.2

9)(0

.39)

(0.2

9)(0

.29)

(0.2

9)(0

.39)

(0.3

9)(0

.39)

Rel

igio

us

sim

ilar

ity

0.15

∗∗∗

0.24

∗∗∗

0.15

∗∗∗

0.15

∗∗∗

0.11

∗∗0.

13∗∗

∗0.

13∗∗

∗0.

15∗∗

∗

(0.0

4)(0

.05)

(0.0

4)(0

.04)

(0.0

4)(0

.05)

(0.0

5)(0

.05)

Som

atic

dist

ance

−0.0

6∗∗∗

−0.0

6∗∗∗

−0.0

5∗∗∗

−0.0

4∗∗∗

−0.0

4∗∗∗

−0.0

4∗∗∗

−0.0

3∗∗∗

(0.0

1)(0

.01)

(0.0

1)(0

.01)

(0.0

1)(0

.01)

(0.0

1)G

enet

icdi

stan

ce−1

0.00

∗0.

06(5

.94)

(5.0

7)D

iffe

ren

ces

inG

DP

per

−0.1

4∗∗∗

−0.1

4∗∗∗

−0.1

3∗∗∗

−0.1

3∗∗∗

−0.0

9∗∗

capi

ta(p

erce

nta

ge)

(0.0

4)(0

.03)

(0.0

3)(0

.03)

(0.0

3)S

ame

lega

lori

gin

0.07

∗∗0.

050.

050.

05(0

.03)

(0.0

3)(0

.03)

(0.0

4)L

ingu

isti

cco

mm

onro

ots

0.20

∗0.

20∗

0.21

∗

(0.1

1)(0

.11)

(0.1

1)T

ran

spor

tati

onco

sts∗

1,00

0−0

.58

−1.0

5(1

.00)

(0.9

6)P

ress

cove

rage

−0.7

3∗∗

(0.3

4)O

bser

vati

ons

207

207

207

207

207

207

180

180

154

R2

.772

.840

.806

.840

.854

.858

.832

.832

.837

Not

es.

Th

ede

pen

den

tva

riab

leis

the

aver

age

tru

stac

ross

indi

vidu

als

ofa

give

nco

un

try

tow

ard

citi

zen

sof

oth

erco

un

trie

s.T

oap

prop

riat

ely

esti

mat

eth

est

anda

rder

rors

,w

efi

rst

regr

esse

dth

eob

serv

atio

ns

onye

arfi

xed

effe

cts,

and

then

we

took

the

resi

dual

and

coll

apse

dth

eob

serv

atio

ns

byye

ar.T

rust

isca

lcu

late

dby

taki

ng

the

aver

age

resp

onse

toth

efo

llow

ing

ques

tion

:“I

wou

ldli

keto

ask

you

aqu

esti

onab

out

how

mu

chtr

ust

you

hav

ein

peop

lefr

omva

riou

sco

un

trie

s.F

orea

ch,

plea

sete

llm

ew

het

her

you

hav

ea

lot

oftr

ust

,so

me

tru

st,n

otve

rym

uch

tru

st,o

rn

otr

ust

atal

l.”T

he

answ

ers

are

code

din

the

foll

owin

gw

ay:1

(no

tru

stat

all)

,2(n

otve

rym

uch

tru

st),

3(s

ome

tru

st),

4(a

lot

oftr

ust

).A

llot

her

vari

able

sar

ere

port

edin

the

not

esto

Tab

leII

.Th

ere

gres

sion

sin

clu

deco

un

try-

of-o

rigi

nan

dco

un

try-

of-d

esti

nat

ion

fixe

def

fect

s.S

pati

alco

rrec

ted

stan

dard

erro

r(s

eeC

onle

y[1

999]

)ar

ere

port

edin

pare

nth

eses

.C

oeffi

cien

tis

stat

isti

call

ydi

ffer

ent

from

zero

atth

e∗∗

∗ 1%

,∗∗ 5

%,a

nd

∗ 10%

leve

l.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1112 QUARTERLY JOURNAL OF ECONOMICS

is average residual trust.12 Because in regression (1) we removedthe effect of a country-of-origin factor and a country-of-destinationfactor, this specification tries to capture the match-specific factorthat drives trust. To correct for potential geographical clusteringof our standard errors, all our OLS regressions report spatial cor-rected standard error (Conley 1999).13

We start by regressing the average residual trust of country i’scitizens toward citizens of country j on our proxies for differencesin the information sets (column (1)). If familiarity breeds trust,we should expect that distance and common language have a pos-itive effect on trust. More information, however, allows us to makemore precise inferences about other populations’ trustworthiness,which does not necessarily imply more or less trust on average.

Common language has a positive effect on trust, but in thebasic specification this effect is not statistically significant. Bycontrast, a greater distance between two countries reduces thelevel of trust between them. A one-standard-deviation increase inlog distance decreases trust by one-fourth of a standard deviation.The common-border dummy has a negative sign, but it is notstatistically significant.

In column (2), we introduce our cultural variables. The re-sults show that cultural factors are important overall. The threecultural proxies are jointly statistically significant with an F-testof 21.6. Countries with a long history of wars tend to trust eachother less. France and England, for example, which have a recordof 198 years of war (more than ten times the average of nineteen)should exhibit a bilateral trust that is 0.7 of a standard deviationlower than average, which accounts for the lower bilateral trustthat we observe between them. Religious similarity has a positiveimpact on trust: compared to a case where no common religion isshared, a match where 90% of the citizens share the same reli-gion (e.g., Italy and Spain) raises trust by 15 percentage points(corresponding to 40% of its standard deviation).

The coefficient of somatic distance shows that citizens of onecountry tend to be more trusting toward citizens of other countriesthat are somatically closer. A one-standard-deviation increase in

12. We obtained similar results (not reported) when we use as dependentvariable median trust or the percentage of individuals trusting a lot.

13. Because we have both the trust from France to Great Britain and fromGreat Britain to France, and all of the bilateral regressors for this pair of countriesare unchanged, we need to assume that their residuals are not independent. Forthis reason, in a previous version we clustered the standard errors at the pair-of-countries level, with very similar results.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1113

somatic distance lowers bilateral trust by one-quarter of a stan-dard deviation. If we modify our measure of somatic distance to in-clude only differences in the more visible traits (hair and height),the effect is even stronger (not reported).

In column (3), we substitute for somatic distance with ge-netic distance. The effect is similar but stronger. A one-standard-deviation increase in genetic distance lowers bilateral trust by 1.8standard deviations. When we introduce both in the regression(column (4)), the genetic-distance coefficient drops dramaticallyand loses statistical significance. This is not surprising given thehigh correlation between these two variables. Because both aretrying to capture the same dimension, we will drop the least sig-nificant of the two (i.e., genetic distance) from the following re-gressions.

Alesina and La Ferrara (2002) document that, in the UnitedStates, differences in income are important factors in explainingtrust within a community. In column (5), we try to see whetherthese ideas also apply to trust across communities (or countries)by inserting the relative difference in gross domestic productper capita as an additional regressor. Confirming Alesina andLa Ferrara (2002), this variable has a negative and statisticallysignificant effect on trust, but its insertion does not change themagnitude of the coefficients of the other variables substantially.

Another possibility is that our cultural variables are a proxyfor differences in the legal origin. If countries with a similar legalsystem understand each other more and trust more, it is am-biguous whether this is an information effect or a cultural effect.For this reason, in column (6), we introduce an indicator variableequal to 1 if two countries have the same legal origin. Not sur-prisingly, this variable has a positive and statistically significanteffect. Countries with a common legal origin have one-fourth of astandard deviation higher trust. This effect reduces the impact oftwo of the other three cultural variables (religion similarity andsomatic distance), but they remain statistically significant.

Another variable that may proxy for culture, but may alsoproxy for ease in (verbal) communication is the commonality inlinguistic roots. When we insert it in column (7), we find thatit has a positive but not statistically significant effect. Interest-ingly, commonality of linguistic roots reduces the effect of com-mon legal origin (which becomes insignificant) but does not affectthe other cultural proxies, which remain statistically significant.Thus, even when we control for variables that, at least in part,

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1114 QUARTERLY JOURNAL OF ECONOMICS

proxy for culture, our cultural variables retain an economicallyand statistically significant effect.

Giuliano, Spilimbergo, and Tonon (2006) claim that geneticdistance is just a proxy for transportation costs, which are mis-measured by the log distance between two countries. If this werethe case, trust might simply be the result of trade, with little orno cultural effect. To address this concern, we add transportationcosts to the regression (column (8)). Transportation costs have anegative effect on trust, but this effect is not statistically signifi-cant. More important, the coefficients of all the other variables (inparticular, somatic distance) are unaffected. This result is not spe-cific to somatic distance; with genetic distance, we reach similarconclusions.

Finally, in column (9) we introduce a direct measure of theknowledge that citizens of country i have regarding the citizens ofcountry j, as measured by press coverage. The coefficient is neg-ative and statistically significant. The most likely interpretationof this result is that newspapers tend to report bad news and thiscreates a negative bias, which is stronger when more news abouta country is reported. All the other results remain the same.

IV. THE EFFECT OF TRUST ON TRADE

Now that we have a better sense of the determinants of bilat-eral trust we can explore its effects. Is it true that trust (or lackthereof) has first-order economic effects, as suggested by Arrow(1972)?14 More important, can we establish that some culturalfactors impact economic exchange? To do so, we try to see whatthe effect of trust is when inserted in traditional models of eco-nomic exchange across countries. We start with trade of goods andservices.

IV.A. Data

The first variables we use are data on trade of goods andservices assembled by Statistics of Canada. The World TradeDatabase is derived from UN COMTRADE data; its advantageover other data sets is that it provides bilateral trade statis-tics at the four-digit Standard International Trade Classification(SITC) level.15 This database provides a time series of trade value,

14. For a simple model of how small differences in trust can have first-order ef-fects on economic decisions, see Section I of Guiso, Sapienza, and Zingales (2004a).

15. We also used an aggregate OECD data set, based on custom data, andfound very similar results.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1115

disaggregated according to trading partner and four-digit SITClevel for the period 1970–1996. Of this long panel we use onlydata for the years for which trust survey data are available (1970,1976, 1980, 1986, 1990, 1993, 1994, and 1996). The sample statis-tics for the data are reported in Panel C of Table III.16

IV.B. Empirical Results

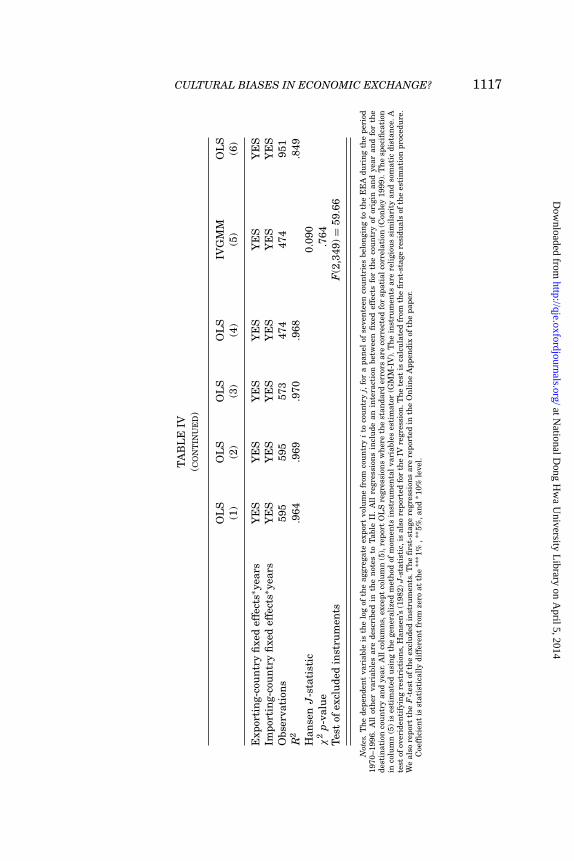

Table IV estimates the effect of trust on the amount of tradebetween two countries according to the following model:

LogExport jit = κi ∗ Yeart + λ j ∗ Yeart + βTrusti jt + δXij + εi jt,

(3)

where Export jit is the export of country j in country i in year taggregated over four-digit SITC industries. Trusti jt is the trustof citizens of country i for citizens of country j in the survey inyear t, and Xij are bilateral-specific variables, which do not varyover time, such as distance; κi a country-of-origin fixed effect,λ j a country-of-destination fixed effect, and Yeart calendar-yeardummies.

De facto, regression (3) is a standard gravity regression (e.g.,Anderson and van Wincoop [2003]), with the addition of our mea-sure of trust of the importing country toward the exporting one,the Giuliano, Spilimbergo, and Tonon (2006) measure of trans-portation costs, country fixed effects for both the importing andthe exporting countries, and calendar-year dummies. FollowingAnderson and van Wincoop (2003), we insert fixed exporter-by-year and importer-by-year fixed effects to account for time-variantfrictions.17 Because we are looking at European countries and ag-gregate the statistics at the country level, we do not have anyzero-flow observations, which could bias the estimates (Lindersand de Groot 2006).18 The standard errors reported in bracketsare corrected for spatial correlation (Conley 1999).

16. In a robustness test, as a dependent variable we used the log of the averagelevel of export in the years following each survey: 1970–1974 with the 1970 survey,1975–1979 with the 1976 survey, 1980–1984 with the 1980 survey, 1985–1988 withthe 1986 survey, 1989–1991 with the 1990 survey, 1992 with the 1992 survey, 1993with the 1993 survey data, 1994 with the 1994 survey data, and 1995–1996 withthe 1996. The results (available from the authors) are unchanged.

17. Our results are even stronger if instead of the interaction terms we in-clude exporter fixed effect, importer fixed effect, and year fixed effect (see Guiso,Sapienza, and Zingales [2004a]). Anderson and van Wincoop (2003) argue againstthe insertion of “remoteness” into the gravity equation. Our results are unchangedif we add a measure of remoteness.

18. For a theoretical justification of the use of the gravity equation, seeHelpman and Krugman (1985).

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1116 QUARTERLY JOURNAL OF ECONOMICST

AB

LE

IVE

FF

EC

TO

FT

RU

ST

ON

TR

AD

E

OL

SO

LS

OL

SO

LS

IVG

MM

OL

S(1

)(2

)(3

)(4

)(5

)(6

)

Mea

ntr

ust

ofpe

ople

inim

port

ing

0.36

∗∗0.

29∗

0.25

0.34

∗∗1.

20∗∗

∗0.

19co

un

try

tope

ople

inex

port

ing

cou

ntr

y(0

.17)

(0.1

7)(0

.19)

(0.1

6)(0

.20)

(0.2

2)In

tera

ctio

nbe

twee

ntr

ust

and

0.83

∗∗∗

dive

rsifi

edgo

od(0

.05)

Com

mon

lan

guag

e0.

58∗∗

∗0.

32∗∗

0.37

∗∗0.

82∗∗

∗0.

94∗∗

∗1.

04∗∗

∗(0

.22)

(0.1

6)(0

.16)

(0.2

1)(0

.14)

(0.2

7)L

og(d

ista

nce

)−0

.31∗

∗∗−0

.43∗

∗∗−0

.43∗

∗∗−0

.57∗

∗∗−0

.61∗

∗∗−0

.73∗

∗∗(0

.09)

(0.0

9)(0

.09)

(0.1

0)(0

.07)

(0.1

2)C

omm

onbo

rder

0.49

∗∗∗

0.43

∗∗∗

0.41

∗∗∗

0.41

∗∗∗

0.36

∗∗∗

0.35

∗∗∗

(0.1

1)(0

.10)

(0.1

1)(0

.10)

(0.0

6)(0

.13)

Pre

ssco

vera

ge0.

45−0

.03

−0.0

9−1

.34

−0.8

9−2

.83∗

∗(1

.05)

(0.9

3)(0

.94)

(1.0

)(0

.60)

(1.1

2)T

ran

spor

tati

onco

sts

−1.8

1∗∗

−0.3

3−0

.28

0.10

0.63

−1.8

3(0

.79)

(0.7

4)(0

.76)

(0.7

3)(0

.52)

(1.1

7)S

ame

lega

lori

gin

0.45

∗∗∗

0.43

∗∗∗

0.36

∗∗∗

0.24

∗∗∗

0.57

∗∗∗

(0.1

0)(0

.10)

(0.1

1)(0

.07)

(0.1

5)L

ingu

isti

cco

mm

onro

ots

0.09

(0.2

8)C

orre

lati

onof

con

sum

ptio

n−0

.95

−1.0

5∗∗∗

−1.8

2∗∗

betw

een

the

two

cou

ntr

ies

(0.6

8)(0

.37)

(0.8

9)

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1117

TA

BL

EIV

(CO

NT

INU

ED

)

OL

SO

LS

OL

SO

LS

IVG

MM

OL

S(1

)(2

)(3

)(4

)(5

)(6

)

Exp

orti

ng-

cou

ntr

yfi

xed

effe

cts∗

year

sY

ES

YE

SY

ES

YE

SY

ES

YE

SIm

port

ing-

cou

ntr

yfi

xed

effe

cts∗

year

sY

ES

YE

SY

ES

YE

SY

ES

YE

SO

bser

vati

ons

595

595

573

474

474

951

R2

.964

.969

.970

.968

.849

Han

sen

J-s

tati

stic

0.09

0χ

2p-

valu

e.7

64T

est

ofex

clu

ded

inst

rum

ents

F(2

,349

)=

59.6

6

Not

es.

Th

ede

pen

den

tva

riab

leis

the

log

ofth

eag

greg

ate

expo

rtvo

lum

efr

omco

un

try

ito

cou

ntr

yj,

for

apa

nel

ofse

ven

teen

cou

ntr

ies

belo

ngi

ng

toth

eE

EA

duri

ng

the

peri

od19

70–1

996.

All

oth

erva

riab

les

are

desc

ribe

din

the

not

esto

Tab

leII

.A

llre

gres

sion

sin

clu

dean

inte

ract

ion

betw

een

fixe

def

fect

sfo

rth

eco

un

try

ofor

igin

and

year

and

for

the

dest

inat

ion

cou

ntr

yan

dye

ar.A

llco

lum

ns,

exce

ptco

lum

n(5

),re

port

OL

Sre

gres

sion

sw

her

eth

est

anda

rder

rors

are

corr

ecte

dfo

rsp

atia

lco

rrel

atio

n(C

onle

y19

99).

Th

esp

ecifi

cati

onin

colu

mn

(5)

ises

tim

ated

usi

ng

the

gen

eral

ized

met

hod

ofm

omen

tsin

stru

men

tal

vari

able

ses

tim

ator

(GM

M-I

V).

Th

ein

stru

men

tsar

ere

ligi

ous

sim

ilar

ity

and

som

atic

dist

ance

.Ate

stof

over

iden

tify

ing

rest

rict

ion

s,H

anse

n’s

(198

2)J

-sta

tist

ic,i

sal

sore

port

edfo

rth

eIV

regr

essi

on.T

he

test

isca

lcu

late

dfr

omth

efi

rst-

stag

ere

sidu

als

ofth

ees

tim

atio

npr

oced

ure

.W

eal

sore

port

the

F-t

est

ofth

eex

clu

ded

inst

rum

ents

.Th

efi

rst-

stag

ere

gres

sion

sar

ere

port

edin

the

On

lin

eA

ppen

dix

ofth

epa

per.

Coe

ffici

ent

isst

atis

tica

lly

diff

eren

tfr

omze

roat

the

∗∗∗ 1

%,∗

∗ 5%

,an

d∗ 1

0%le

vel.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1118 QUARTERLY JOURNAL OF ECONOMICS

As in the standard gravity equation, a greater distancebetween two countries negatively affects the level of exports,whereas the presence of a common border and of a common lan-guage positively affects it. All these effects are highly statisticallysignificant. As in Giuliano, Spilimbergo, and Tonon (2006), thetransportation costs measure has a negative effect on trade, whichis statistically significant at the 5% level.19

After controlling for all these variables, our measure of trusthas a positive and statistically significant effect on trade. Theeffect is also economically very large. A one-standard-deviationincrease in trust increases exports to a country by ten percentagepoints, equal to 1.6 standard deviations.

In column (2), we test the robustness of this result to theinsertion of an indicator variable for commonality of legal origin.This variable can capture the fact that similar institutions fostermore trade because they provide more guarantee to the partiesinvolved (De Groot et al. 2004; Vlachos 2004). Alternatively, itcan capture part of the cultural effect. This indicator variable hasa positive and statistically significant effect on trade. Countrieswith the same legal tradition trade among themselves 1.5 timesmore. We find a similar effect when we introduce the commonalityof linguistic roots, which does not have a statistically significantimpact on trade (column (3)).

Another possible objection is that trust might pick up someother cultural similarities such as commonalities in taste. If twocountries share the same taste for consumption (e.g., for cheese),they might trade more. To address this problem we construct anindex of similarity in consumption patterns across countries. Thisindex is calculated by computing domestic consumption as thesum of gross domestic production in each ISIC code plus importsand minus exports between 1989 and 1994. For each pair of coun-tries, then, we compute the correlation in consumption across ISICsectors.20

When we insert this variable in the OLS specification ofour trade regression (column (4)), the sign is negative, but not

19. In an unreported regression, we also controlled for the geographical bar-riers used by Giuliano, Spilimbergo, and Tonon (2006): the presence of a commonsea and the presence of a mountain chain between two countries. These variablesare not significant and do not affect the other results.

20. Data on consumptions are calculated by extracting data from thefollowing data set: http://econ.worldbank.org/WBSITE/EXTERNAL/EXTDEC/EXTRESEARCH/0,,contentMDK:21085384∼pagePK:64214825 ∼piPK:64214943∼theSitePK:469382,00.html.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

CULTURAL BIASES IN ECONOMIC EXCHANGE? 1119

statistically significant. The size and the statistical significanceof the coefficient of trust are unaffected. A similar concern is thatcountries with a more similar structure of production trade morewith each other. To address it, we create an index of productionsimilarity by correlating the GDP data across sectors in the sameway as described above. The results (not reported) are unchanged.

There are at least three reasons to worry about these OLSresults. First, although it is possible that trust fosters trade, itis equally possible that trade breeds trust. The second problemis that bilateral trust can capture the effect of other omittedvariables (e.g., the existence of established trading outposts, assuggested by Rauch and Trindade [2002]). Finally, measurementerrors in the trust variable may affect our results.

To address these concerns we instrument our trust variableby using the generalized method of moments estimator (GMM-IV),which allows for heteroscedasticity of unknown form. As instru-ments we use the cultural determinants of trust (commonality ofreligion and somatic distance). Note that these instruments aretime invariant, yet the average level of trust varies over time.These two instruments pass the Hansen J-test for overidentify-ing restrictions, but were we to add also the history of wars, thetest would fail.

The IV estimates are presented in column (5). Not only doestrust retain its effect on trade, but the size of the coefficient in-creases fourfold. A possible explanation is that our instrumentsmay be only weakly correlated with trust. If this is the case, thenthe two-stage least-squares regressions will be biased and thestandard errors misleading. To address this concern, we computethe F-statistics for the joint hypothesis that the instruments’ co-efficients are zero in the first-stage regression and report it atthe bottom of the table. In this specification, the F-test is 59.66,comfortably above the threshold recommended by Stock and Yogo(2002).

An alternative explanation for the difference in the coefficientis that our trust measure is a noisy measure of the true trustbetween two countries, and the increase in the coefficient would bethe result of a reduction in the standard attenuation bias presentwhen variables are measured with error. If this is the case, thetrue economic effect is closer to the GMM-IV estimates, whichsuggests a much larger result. A one-standard-deviation increasein trust increases exports to a country by 63 percentage points.The magnitude of this effect is not very different from the one

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from

1120 QUARTERLY JOURNAL OF ECONOMICS

found by Rauch and Trindade (2002). They find that the presenceof ethnic Chinese networks increases the amount of bilateral tradein differentiated goods by 60%.

Alternatively, it is possible that—test of overidentifying re-strictions notwithstanding—our instruments are not orthogonalto trade, but pick up a set of cultural, institutional, and legal con-nections that facilitate trade flows. These cultural effects mustbe match specific because the institutional factors are controlledfor in the country-of-origin or in the country-of-destination fixedeffects. If this is the case, our results suggest the importance ofculture-specific factors in trade relationships. These factors canhelp explain the famous Rose (2000) result (confirmed by Rose andStanley [2005]) that currency unions are associated with a verylarge increase in trade. Because most of the countries belongingto currency unions in the Rose (2000) sample were countries veryculturally connected, where trust is higher, trade will be naturallyhigher once the obstacle to trade imposed by national currenciesis removed.

In the last column of Table IV, we test whether the impact oftrust on trade varies according to what theory would suggest. Ourhypothesis predicts that trust should matter more for goods whosequality can differ more. For these goods, contracts are more diffi-cult to write and hence they are more likely to leave gaps, wheretrust plays a very important role. Rauch (1999) distinguishes be-tween goods traded in an organized exchange, goods with a refer-ence price, and differentiated goods. Clearly, goods can be tradedin an organized exchange only if they are very homogeneous inquality. Similarly, they can have a reference price only if theyare not too dissimilar in their intrinsic quality. Hence, Rauch’s(1999) classification can also be interpreted as a classification ofthe degree of trust intensiveness of the different goods.21

For this reason, in the last column of Table IV, we aggregateexports for two subsamples of industries (organized exchange anddifferentiated goods); then, we run the regression by using theinteraction between trust and whether the good is classified asa differentiated good. The effect of trust appears to be economi-cally and statistically indistinguishable from zero for the sampleof homogeneous goods, which are traded in organized exchanges.

21. Rauch (1999) made a “conservative” and a “liberal” classification of in-dustries. To minimize ambiguity we excluded industries that were classified indifferent ways under the two classifications and ran our regressions only for orga-nized exchange goods and differentiated goods.

at National D

ong Hw

a University L

ibrary on April 5, 2014

http://qje.oxfordjournals.org/D

ownloaded from