critical illness insurance: an introduction to pricing -...

TRANSCRIPT

To change photo:

1. Delete the current

image. This will leave

a blank placeholder

with a picture icon.

2. Click the icon to add a

new image. The photo

will be automatically

be cropped to fit the

placeholder.

NOTE: If you use the

“Change Picture”

function,

the image will be

imported in its original

proportions and won’t fill

the placeholder

completely and will need

to be cropped. Critical Illness Insurance: An Introduction to Pricing

Chris Jewson

22 October 2015

Head of Protection Pricing, UK & Ireland

2

See Appendix for

instructions on how to

change sidebar photo

Agenda

The Evolution of Critical Illness Pricing

Setting The Long-Term Trend Assumption

Product Innovation

• Adding New CI Conditions

• Severity-based Payments

• Multi-pay Critical Illness

Lessons Learned

Recent Research

Risk Management Controls

3

To change photo:

1. Delete the current

image. This will leave

a blank placeholder

with a picture icon.

2. Click the icon to add a

new image. The photo

will be automatically

be cropped to fit the

placeholder.

NOTE: If you use the

“Change Picture”

function,

the image will be

imported in its original

proportions and won’t fill

the placeholder

completely and will need

to be cropped. The Evolution of Critical Illness Pricing

4

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Variety of product designs, influenced by pricing uncertainty and with support of reinsurers

Accelerated term assurance

• Typically 6 or 7 CI conditions

Flexible Whole of Life (Universal Life)

• Unit-linked with investment underpin

Mortgage endowment assurance

• Pays full sum assured on expiry, if not already claimed

• With-profits allows for retrospective pricing via bonuses

1980’s: The Early Pioneers

5

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Research paper presented in January 1990, more commonly known as “Dash & Grimshaw” after its authors

Recognised the lack of reliable data on post-CI mortality from non-CI causes, which is needed to price an accelerated term assurance

Proposed the “heroic assumption” that post-CI mortality from non-CI causes is the same as the mortality of healthy lives

Accelerated incidence rate = ix + (1 - kx) qx

• ix = critical illness incidence rate

• qx = mortality rate

• kx = proportion of deaths that are due to a critical illness

1990: “Dread Disease Cover, An Actuarial Perspective”

6

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Actuarial research paper presented in March 2000

Developed the first UK Critical Illness Base Table (CIBT93) from population data

Also presented an analysis of insured lives experience for the period 1991-97

2000: “A Critical Review”

7

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Reinsurers started to worry about future trend and reduced or withdrew capacity at guaranteed rates

Guaranteed capacity reserved for key clients & distribution channels

Reviewable rates for everyone else

GE continued to offer guaranteed CI in volume

• Prudent margins: priced for >3% p.a. deterioration in experience

• Guaranteed rates ~40% higher than reviewable

• Significant profits

2003: Reinsurers get Cold Feet

8

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Actuarial research paper presented in December 2006

A major report (over 200 pages) with substantial commentary on individual conditions, trends etc.

Developed the second UK Critical Illness Base Table (CIBT02) from population data

Presented as a work-in-progress and never fully completed

2006: “Exploring the Critical Path”

9

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

The first full UK industry tables using insured lives data

Graduated from the industry experience submitted by CMI members

Covers experience during 2003-2006

More stable mix of contributing offices than previous industry data

Still immature by age and duration

2011: AC04 Standard Tables

10

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Consistent reporting of claim dates

• Date of Diagnosis / Reporting / Claim / Settlement

Consistent reporting of claim amounts

• Mortgage business

• Child CI, other part payments, proportionate settlements

Cause of claim

• Lack of consistency, free-form entries

• Recording of deaths caused by CI

Incurred But Not Settled (IBNS)

• Can be lengthy delay from claim to settlement

Data Challenges

11

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Mix of products has changed

• Old: Endowments, light underwriting

• New: Pure protection (term assurances), stringent underwriting

Mix of contributing offices has changed

• Different underwriting standards

• Different distribution models

• Inconsistent from one industry study to the next

Industry Study Challenges

12

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Industry Study Challenges

13

See Appendix for

instructions on how to

change sidebar photo

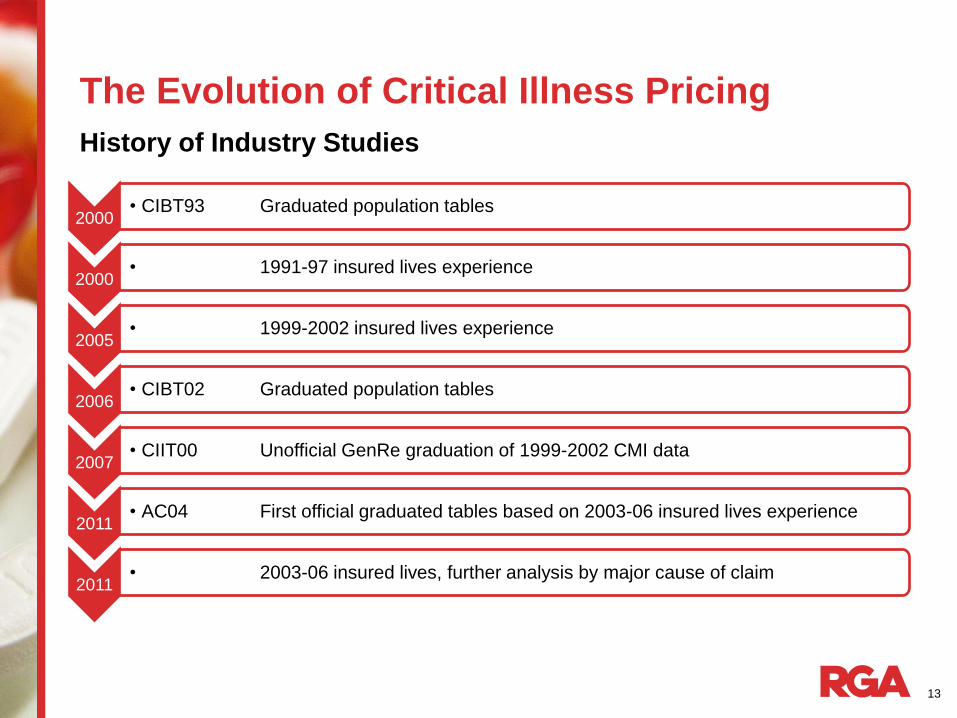

The Evolution of Critical Illness Pricing

History of Industry Studies

2000 • CIBT93 Graduated population tables

2000 • 1991-97 insured lives experience

2005 • 1999-2002 insured lives experience

2006 • CIBT02 Graduated population tables

2007 • CIIT00 Unofficial GenRe graduation of 1999-2002 CMI data

2011 • AC04 First official graduated tables based on 2003-06 insured lives experience

2011 • 2003-06 insured lives, further analysis by major cause of claim

14

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

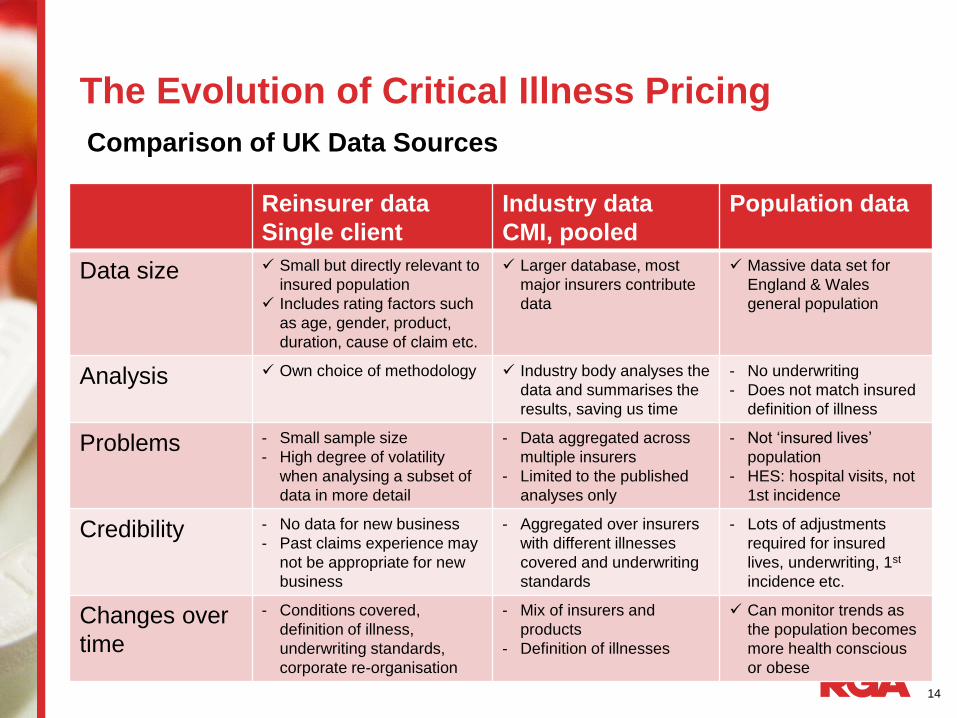

Comparison of UK Data Sources

Reinsurer data

Single client

Industry data

CMI, pooled

Population data

Data size Small but directly relevant to

insured population

Includes rating factors such

as age, gender, product,

duration, cause of claim etc.

Larger database, most

major insurers contribute

data

Massive data set for

England & Wales

general population

Analysis Own choice of methodology Industry body analyses the

data and summarises the

results, saving us time

- No underwriting

- Does not match insured

definition of illness

Problems - Small sample size

- High degree of volatility

when analysing a subset of

data in more detail

- Data aggregated across

multiple insurers

- Limited to the published

analyses only

- Not ‘insured lives’

population

- HES: hospital visits, not

1st incidence

Credibility - No data for new business

- Past claims experience may

not be appropriate for new

business

- Aggregated over insurers

with different illnesses

covered and underwriting

standards

- Lots of adjustments

required for insured

lives, underwriting, 1st

incidence etc.

Changes over

time

- Conditions covered,

definition of illness,

underwriting standards,

corporate re-organisation

- Mix of insurers and

products

- Definition of illnesses

Can monitor trends as

the population becomes

more health conscious

or obese

15

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Source: Continuous Mortality Investigation (CMI)

UK Selection Pattern by Duration and Risk Class

16

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Source: Continuous Mortality Investigation (CMI)

Cause of Claim, UK: Males

17

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

Source: Continuous Mortality Investigation (CMI)

Cause of Claim, UK: Females

18

See Appendix for

instructions on how to

change sidebar photo

The Evolution of Critical Illness Pricing

History of RGA Pricing

2000 • Derived from population data with adjustments to estimate

an insured population

2004 • Insured lives experience starting to emerge at early

durations

2008 • Basket of major conditions calibrated to CMI industry data

and own experience

2012 • GLM analysis of insured data for established CI conditions

with traditional methods for more recent conditions

19

To change photo:

1. Delete the current

image. This will leave

a blank placeholder

with a picture icon.

2. Click the icon to add a

new image. The photo

will be automatically

be cropped to fit the

placeholder.

NOTE: If you use the

“Change Picture”

function,

the image will be

imported in its original

proportions and won’t fill

the placeholder

completely and will need

to be cropped. The Long-Term Trend Assumption

20

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

Influences on Trends

• Real changes in population morbidity

• Earlier detection of disease

• Medical definition drift Population

• Real changes in assured population morbidity

• Weakness in insured definition

• Insured definition drift

• Anti-selective lapsation

Insured Lives

21

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

To estimate future incidence-rate trends for a standard acceleration critical illness product

Particular emphasis on adverse scenarios appropriate to pricing of guaranteed business

Not a ‘tail scenario’ investigation

Objective

22

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

Heart Attack

Stroke

MS

CABG

Angioplasty

Colorectal Cancer

Pancreatic Cancer

Stomach Cancer

Prostate Cancer

Bladder Cancer

Lung Cancer

Breast Cancer

Ovarian Cancer

Uterus Cancer

Melanoma

Non-CI deaths

Conditions Covered

23

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

Who should we call for the ‘crystal ball’ gazing?

Options Pros Cons

Academics Ahead of the

game

Narrow, unworldly

Consultants,

Practitioners

Broader view Stuck in the

present, don’t

understand

insurance

CMO’s Understand

insurance

Stuck in the present

Underwriters Understand

insurance

Not enough

expertise

Dr. Google Available 24/7 None

24

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

CMO’s with relevant specialism

Briefing packs provided

• Insured definition

• Chart of past trends (from HES, Cancer Registration Statistics)

• Suggested rationale for past trends

Telephone discussions, strictly moderated, 1 hour per condition

Discussions must reach consensus on future trends, which is documented as the ‘Expert Opinion Statement’

Expert Sessions

25

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

Level and direction of recent population trends, with rationale

Projected trend for next 10yrs and subsequent 10yrs, with rationale:

• No change

• Slightly up/down

• Sharply up/down

Potential ‘shocks’ in next 10yrs and subsequent 10yrs, with rationale

Expert Opinion Statement

26

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

A ‘shock’ is an event which the experts expect to occur in the future with some level of likelihood

A ‘shock’ gives rise to a one-off increase in incidence rates above the current trend, to a sustained higher level

A ‘shock’ is described by three parameters:

• The assumed date of occurrence

• The assumed likelihood of occurrence

• The assumed impact on incidence rates

A ‘shock’ is NOT an unpredicted or random event!

Expert Opinion: ‘Shocks’

27

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

Actuaries interpreted the choices into numbers, by age band, starting with the trend over most recent 5 year period

Expert opinion statements ‘slightly up’ etc. converted into numeric trend assumptions for 20 years, in blocks of 5 years

Further adjustment for expected differences between general population and insured population, using insured v. population incidence trends as a clue

For non-CI deaths, used trends in available ‘death by cause’ data

Converting Expert Opinion Statements into Numbers

28

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

Converting ‘Shocks’ into Numbers

Starting point is Expert Opinion for time, likelihood and impact

Adjust for deemed differences between population and insured lives

• Socio-economic

• Effect of underwriting

Grade impact variation in 10-year age groups

Further discussion and refinements following discussions with claims team

29

See Appendix for

instructions on how to

change sidebar photo

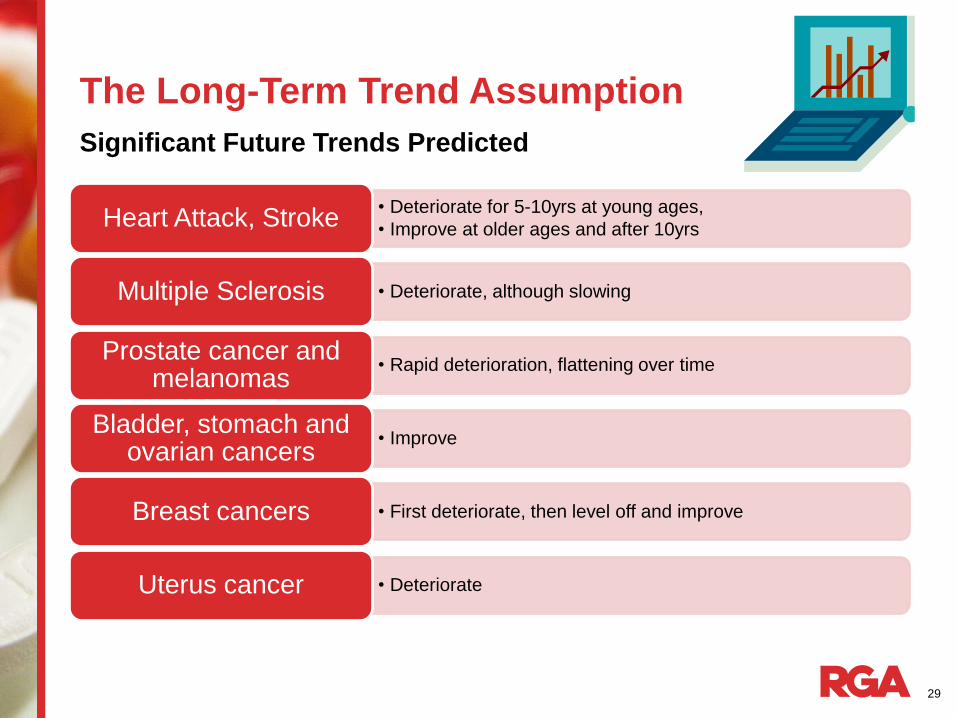

The Long-Term Trend Assumption

Significant Future Trends Predicted

• Deteriorate for 5-10yrs at young ages,

• Improve at older ages and after 10yrs Heart Attack, Stroke

• Deteriorate, although slowing Multiple Sclerosis

• Rapid deterioration, flattening over time Prostate cancer and

melanomas

• Improve Bladder, stomach and

ovarian cancers

• First deteriorate, then level off and improve Breast cancers

• Deteriorate Uterus cancer

30

See Appendix for

instructions on how to

change sidebar photo

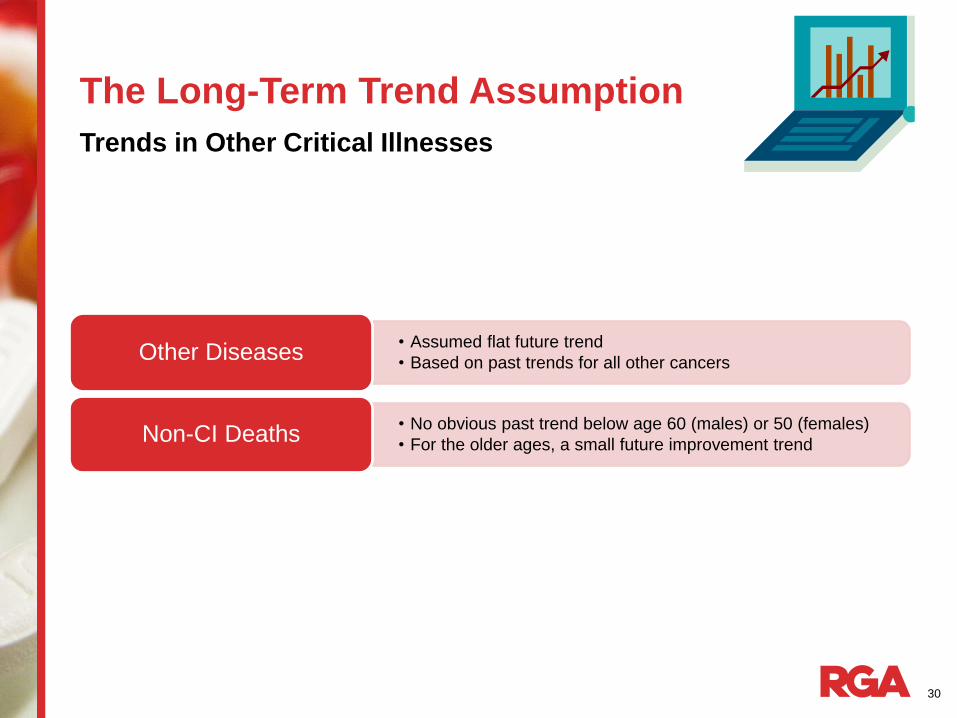

The Long-Term Trend Assumption

Trends in Other Critical Illnesses

• Assumed flat future trend

• Based on past trends for all other cancers Other Diseases

• No obvious past trend below age 60 (males) or 50 (females)

• For the older ages, a small future improvement trend Non-CI Deaths

31

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

Significant Future ‘Shocks’ Predicted

• Exploitation of weak insured definition for symptoms (and for MS)

• Inclusion of some transient ischaemic attacks (TIAs)

• 20% likelihood, up to 20% impact at youngest ages for weak definition

• 10% likelihood, up to 20% impact at youngest ages for TIAs

Stroke

• Risk of having to accept lower clinical Troponin threshold 0.1 instead of 1.0 in the insured definition Heart Attack

• Earlier detection of malignancies; but earlier detection of pre-malignant cancers would be beneficial and work in our favour Various Cancers

32

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

Best Estimate (Reviewable Premium Business)

• Include <100% of the ‘shock’ impacts

• Allow for improvements where expected for some conditions

Trend Scenarios: Principles for Best Estimate

33

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

Guaranteed Premium Business

• Aim to be P% (?) certain of claims costs within pricing

• Various scenarios from optimistic to pessimistic

• Cautious interpretation of past trends

• Reduced allowance for long-term improvements in some for conditions

• Include >100% of the ‘shock’ impacts

• Keep a sense of balance: there are beneficial environmental and technological drivers, as well as adverse ones

• ‘Shocks’ limited to small set of predicted causes, not a 1 in 200 event or ‘wildcard’ unknown

Trend Scenarios: Principles for Guaranteed Business

34

See Appendix for

instructions on how to

change sidebar photo

The Long-Term Trend Assumption

Trends and ‘Shocks’ weighted appropriately to produce a two-way table by age and duration for each risk class

Further variations by age, smoker status, policy term

Combining Trends and ‘Shocks’ for All Conditions

35

To change photo:

1. Delete the current

image. This will leave

a blank placeholder

with a picture icon.

2. Click the icon to add a

new image. The photo

will be automatically

be cropped to fit the

placeholder.

NOTE: If you use the

“Change Picture”

function,

the image will be

imported in its original

proportions and won’t fill

the placeholder

completely and will need

to be cropped. Product Innovation

36

See Appendix for

instructions on how to

change sidebar photo

Product Innovation

Process and Stakeholders

Insurer’s proposed definition

Definition Review

Pricing

Refine Definition

Refine Price

Refine definition and

price

Insurer

challenge

CM

O

Mark

eti

ng

Insurer

37

See Appendix for

instructions on how to

change sidebar photo

Product Innovation

Identify what data sources are available

• Often no insured data

• Population data (eg. HES) – use CMO’s, Dr. Google etc.

• Identify the most relevant ICD codes

Subjective adjustments

• Under-reporting or multiple treatments for the same patient

• Severity of insurance definition v. medical definition

• Insured population v. general population

• Overlaps with existing cover

Pricing New Conditions

38

See Appendix for

instructions on how to

change sidebar photo

Product Innovation

Began selling CI in 1985

Sophisticated market

Complex CI products and little standardisation

Highly competitive between providers

• Driven by definitions – numbers of conditions covered, and the scope of each definition

• Insurers are pushing the boundaries to differentiate

Sold by broker as a rider to death or standalone cover

CI in South Africa

39

See Appendix for

instructions on how to

change sidebar photo

Product Innovation

CI in South Africa: Plain Vanilla to ‘The Works’…

CI in 1985 CI in 2015

40

See Appendix for

instructions on how to

change sidebar photo

Product Innovation

CI in South Africa

1985

Heart Attack, Stroke, CABG, Cancer

Accelerated (part of Life policy)

2015

> 50 impairments covered

Stand Alone and Accelerated

Scaled – severity levels, paying

out more for more severe

disease

41

See Appendix for

instructions on how to

change sidebar photo

Product Innovation: Severity-based Payments

Key Features of CI Products

South Africa Australia Singapore

Accelerated rider or Standalone

Limited Premium

guarantees (10years)

Fully reviewable rates Premium guarantees

50+ conditions 50+ conditions 37 conditions

Reinstatement / buy-

back

Reinstatement / buy-

back

Reinstatement / buy-

back

Staged / multi-pay Staged /multi-pay

(developing)

Staged / multi-pay

Early Stage Early Stage

Whole of Life No WOL No WOL

42

See Appendix for

instructions on how to

change sidebar photo

Product Innovation: Severity-based Payments

Better meets client needs

Matches payment to disease severity

Improved public image….

• fewer ‘declined’ claims

More resilient to medical advances

• as long as definitions well controlled

Insurable interest

Affordable insurance

Multiple events

Arguments for Scaled CI

Windfall payments on

non-Scaled products:

Is it fair to pay someone who

has had a mild heart attack and

back at work next week the

same as a paraplegic?

43

See Appendix for

instructions on how to

change sidebar photo

Product Innovation: Severity-based Payments

Product complexity

Consumer understanding

Agent sells the “100% level”

Marketed as being not as comprehensive

Pricing statistics

• Country variations in stage distribution?

• Stage progression?

• Multiple claims?

• Impact of future screening?

• Lacking credible experience or population data

Challenges with Scaled CI

44

See Appendix for

instructions on how to

change sidebar photo

Product Innovation: Severity-based Payments

Example: Cancer Definition

“Cancer” is a malignant tumour positively diagnosed with histological confirmation and characterised by the

uncontrolled growth of malignant cells and invasion of tissue. The term malignant tumour includes leukaemia,

lymphoma and sarcoma.

The following conditions are excluded from this definition:

-All cancers in situ and all pre-malignant conditions

-All tumours of the prostate unless histologically classified as having a Gleason score greater than 6 or having

progressed to at least clinical TNM classification T2N0M0

-All skin cancers, other than, malignant melanoma that has been histologically classified as having caused invasion

beyond the epidermis (outer layer of skin)

Non-Tiered Tiered (except Prostate, leukemia and lymphoma)

100% The cancer must require

treatment by surgery,

radiotherapy, or chemotherapy.

25% TNM Stage I malignant tumour

50% TNM Stage II malignant tumour

75% TNM Stage III malignant tumour

100% TNM Stage IV malignant tumour

45

See Appendix for

instructions on how to

change sidebar photo

Product Innovation: Severity-based Payments

Scaled Cancer Pricing

Progression

Cancer

Stage IV

Stage III

Stage II

Stage I

46

See Appendix for

instructions on how to

change sidebar photo

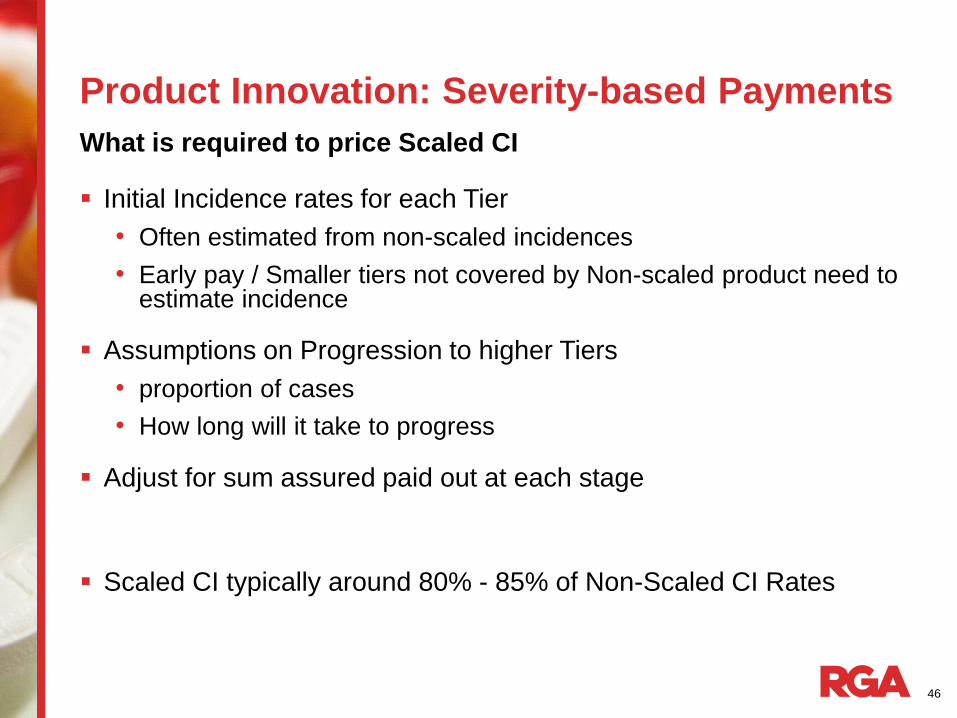

Product Innovation: Severity-based Payments

Initial Incidence rates for each Tier

• Often estimated from non-scaled incidences

• Early pay / Smaller tiers not covered by Non-scaled product need to estimate incidence

Assumptions on Progression to higher Tiers

• proportion of cases

• How long will it take to progress

Adjust for sum assured paid out at each stage

Scaled CI typically around 80% - 85% of Non-Scaled CI Rates

What is required to price Scaled CI

47

See Appendix for

instructions on how to

change sidebar photo

Product Innovation: Multi-pay Critical Illness

On standalone CI can claim more than once for unrelated conditions

Product paying up to 5 times the sum assured or more on multiple CI events

Usually CI events are grouped by related conditions and only 1 payment per group is allowed

Require waiting period between claims to be considered unrelated

48

See Appendix for

instructions on how to

change sidebar photo

Product Innovation: Multi-pay Critical Illness

Incidence Rates

• Base single event incident rates by condition, age , gender, smoking habit

• Discount rates

• Lapses (pre and post first claim)

• Issue Age and Policy Term

Risk Relativities

• Probability of Second/Subsequent Event given First Event has occurred

• Product Groupings to allow for implicit price adjustment

Survival Probabilities

• Initial Extra Mortality over one year waiting period following the first event

• Extra mortality by duration for further four years following the first event

Expenses, capital, profits etc.

What is required to price Multi-pay CI

49

To change photo:

1. Delete the current

image. This will leave

a blank placeholder

with a picture icon.

2. Click the icon to add a

new image. The photo

will be automatically

be cropped to fit the

placeholder.

NOTE: If you use the

“Change Picture”

function,

the image will be

imported in its original

proportions and won’t fill

the placeholder

completely and will need

to be cropped. Lessons Learned

50

See Appendix for

instructions on how to

change sidebar photo

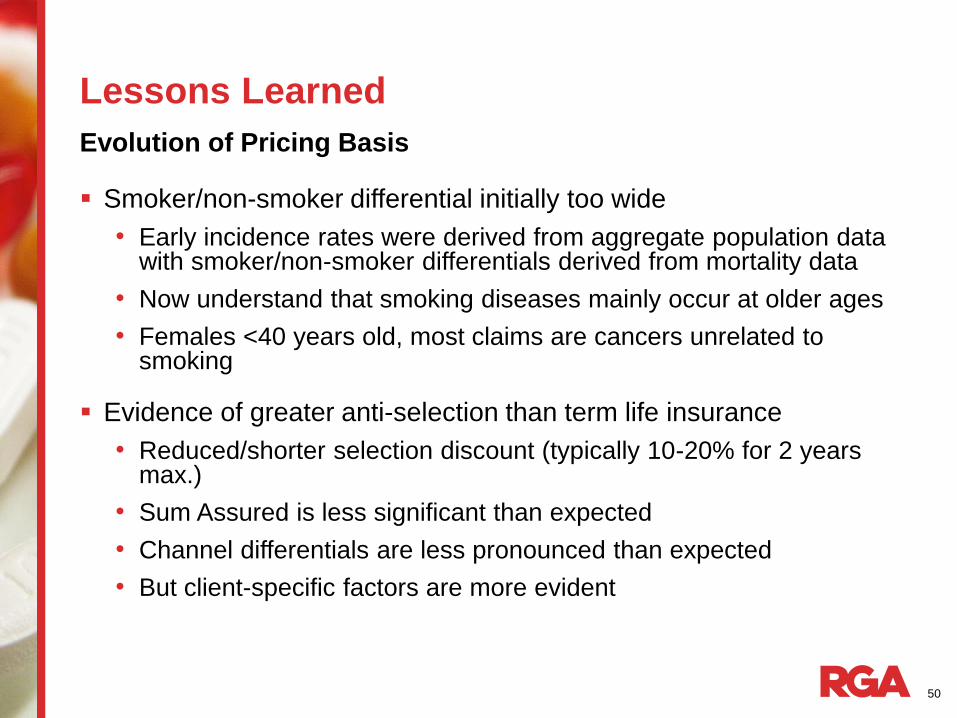

Lessons Learned

Smoker/non-smoker differential initially too wide

• Early incidence rates were derived from aggregate population data with smoker/non-smoker differentials derived from mortality data

• Now understand that smoking diseases mainly occur at older ages

• Females <40 years old, most claims are cancers unrelated to smoking

Evidence of greater anti-selection than term life insurance

• Reduced/shorter selection discount (typically 10-20% for 2 years max.)

• Sum Assured is less significant than expected

• Channel differentials are less pronounced than expected

• But client-specific factors are more evident

Evolution of Pricing Basis

51

See Appendix for

instructions on how to

change sidebar photo

Lessons Learned

Variation in Duration 0 Selection Discount by Insurer

52

See Appendix for

instructions on how to

change sidebar photo

Lessons Learned

Population Trend (Male aged 40-60, 1980-2000, England & Wales)

53

See Appendix for

instructions on how to

change sidebar photo

Lessons Learned

Insurer and reinsurer agree timelines at outset

Requires careful management of all stakeholders

• Marketing

• Underwriting

• Claims

• Pricing

May require multiple iterations before settling on the final product specification

‘Package price’ easier to determine than individual conditions

Product Developments and New Conditions

54

To change photo:

1. Delete the current

image. This will leave

a blank placeholder

with a picture icon.

2. Click the icon to add a

new image. The photo

will be automatically

be cropped to fit the

placeholder.

NOTE: If you use the

“Change Picture”

function,

the image will be

imported in its original

proportions and won’t fill

the placeholder

completely and will need

to be cropped. Recent Research

55

See Appendix for

instructions on how to

change sidebar photo

Recent Research

The full HES dataset covers 1989/90 to 2009/10

Unique patient identifier from 1997/98 to 2009/10 and ICD10 codes

Potential uses include:

• Pricing new CI conditions where insured data is not available

• More accurate adjustments for repeat visits

• Understanding correlations and overlaps between conditions

• Socio-economic studies to assist in predictive modelling?

No longer available due to privacy concerns

The Hospital Episodes Statistics (HES) Dataset

56

See Appendix for

instructions on how to

change sidebar photo

Recent Research

The Hospital Episodes Statistics (HES) Dataset

• 47m unique patient identifiers Patient Identifier

• Age, gender Basic Patient Information

• Date started, date finished, admission method, current status etc.

Basic Episode Information

• Up to 20 different diagnoses per patient Diagnosis Information

• Up to 20 different operations, with date of operation Procedure Information

• Postal district, local super output area, deprivation index ranking Geographic Information

57

To change photo:

1. Delete the current

image. This will leave

a blank placeholder

with a picture icon.

2. Click the icon to add a

new image. The photo

will be automatically

be cropped to fit the

placeholder.

NOTE: If you use the

“Change Picture”

function,

the image will be

imported in its original

proportions and won’t fill

the placeholder

completely and will need

to be cropped. Risk Management Controls

58

See Appendix for

instructions on how to

change sidebar photo

Risk Management Controls

Product Design

• Limit volumes of single-condition cover

• Maximum term (for guaranteed rates)

Alignment of Interest

• Insurer retention, if using reinsurance

Pricing Mis-estimation

• Increased availability of insured data

• Regular experience studies eg. when quoting for new business

Trend risk

• Future-proof definitions, regular review

• CMO approval

‘We are all risk managers’

59

To change photo:

1. Delete the current

image. This will leave

a blank placeholder

with a picture icon.

2. Click the icon to add a

new image. The photo

will be automatically

be cropped to fit the

placeholder.

NOTE: If you use the

“Change Picture”

function,

the image will be

imported in its original

proportions and won’t fill

the placeholder

completely and will need

to be cropped. Thank You

Any Questions?

©2015 RGA. All rights reserved.

No part of this publication may be reproduced in any form without the prior permission of RGA.

The information in this publication is for the exclusive, internal use of the recipient and may not be relied upon by any other party

other than the recipient and its affiliates, or published, quoted or disseminated to any party other than the recipient without the prior

written consent of RGA.