criteria review seminar 2015 stochastic-based bcar (best’s capital adequacy ratio)

TRANSCRIPT

Criteria Review Seminar

etc.venues St.Paul’s, London

04 November 2015

Disclaimer

Criteria Review Seminar 4 November 2015 4

© AM Best Company (AMB) and/or its licensors and affiliates. All rights reserved. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY

COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER

TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH

PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT AMB’s PRIOR

WRITTEN CONSENT. All information contained herein is obtained by AMB from sources believed by it to be accurate and reliable. Because of the

possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any

kind. Under no circumstances shall AMB have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from,

or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of AMB or any of its directors, officers,

employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any

such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost

profits), even if AMB is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The credit

ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be

construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities, insurance policies,

contracts or any other financial obligations, nor does it address the suitability of any particular financial obligation for a specific purpose or purchaser.

Credit risk is the risk that an entity may not meet its contractual, financial obligations as they come due. Credit ratings do not address any other risk,

including but not limited to, liquidity risk, market value risk or price volatility of rated securities. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE

ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR

OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY AMB IN ANY FORM OR MANNER WHATSOEVER. Each credit rating or other opinion

must be weighed solely as one factor in any investment or purchasing decision made by or on behalf of any user of the information contained herein, and

each such user must accordingly make its own study and evaluation of each security or other financial obligation and of each issuer and guarantor of, and

each provider of credit support for, each security or other financial obligation that it may consider purchasing, holding or selling.

Disclaimer

Criteria Review Seminar 4 November 2015 5

US Securities Laws explicitly prohibit the issuance or maintenance of a credit rating where a person involved in the

sales or marketing of a product or service of the CRA also participates in determining or monitoring the credit rating, or

developing or approving procedures or methodologies used for determining the credit rating.

No part of this presentation amounts to sales / marketing activity and A.M. Best’s Rating Division employees

are prohibited from participating in commercial discussions.

Any queries of a commercial nature should be directed to A.M. Best’s Market Development function.

Criteria Review Seminar

Criteria Review Seminar

4 November 2015 36

Stochastic-based BCAR(Best’s Capital Adequacy Ratio)

Mathilde Jakobsen

Associate Director, Analytics, A.M. Best

Criteria Review Seminar

Agenda

• The role of BCAR in the rating process

• Current BCAR approach

• Proposed BCAR approach

• Overview of planned changes (US P&C BCAR)

• Application of new BCAR in the rating process

• Updated timeline

4 November 2015 37

Criteria Review Seminar

The Role of BCAR in the Rating

Process

4 November 2015

• Best’s Capital Adequacy Ratio (BCAR) provides an overall view of risk-based capitalisation

• Separate BCAR models for different areas – including the US P&C, US Life and the Universal BCAR model

• BCAR is used as a global benchmarking tool

38

Criteria Review Seminar

The Role of BCAR in the Rating

Process

4 November 2015

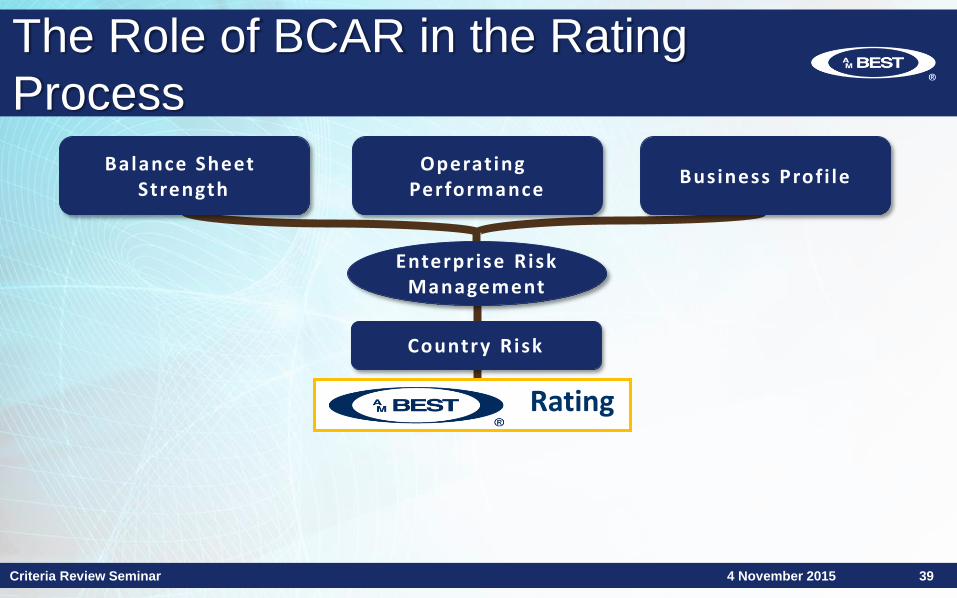

Balance Sheet Strength

Operating Performance

Business Prof i le

Country Risk

Enterprise RiskManagement

Rating

39

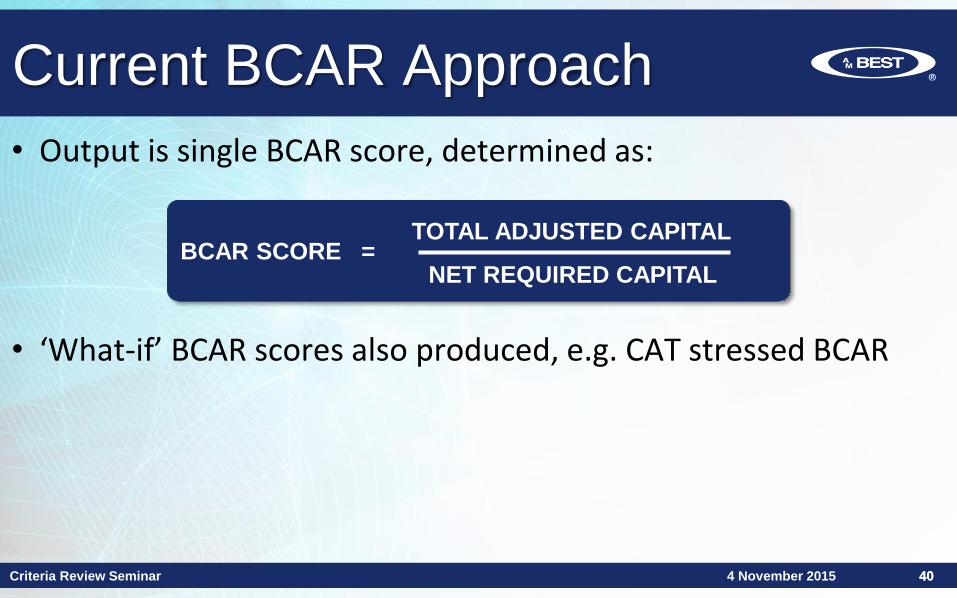

Current BCAR Approach

• Output is single BCAR score, determined as:

• ‘What-if’ BCAR scores also produced, e.g. CAT stressed BCAR

4 November 2015Criteria Review Seminar 404 November 2015 40

BCAR SCORE =TOTAL ADJUSTED CAPITAL

NET REQUIRED CAPITAL

NET REQUIRED CAPITAL*

+ (B1) Fixed-Income Securities

+ (B2) Equity Securities

+ (B3) Interest Rate

+ (B4) Credit

+ (B5) Loss Reserves

+ (B6) Net Written Premium

+ (B7) Off Balance Sheet Risks

- COVARIANCE

Criteria Review Seminar

Current BCAR Approach

4 November 2015

TOTAL ADJUSTED CAPITAL

+ Shareholders’ funds

+ Adjustments made to ensure a more economic and comparable basis for capital adequacy

+ Deduction of one net tax adjusted probable maximum loss

BCAR SCORE = TOTAL ADJUSTED CAPITAL / NET REQUIRED CAPITAL

*Net required capital = SQRT [(B1)²+(B2)²+(B3)²+(0.5*B4)² +[(0.5*B4)+B5)]²+(B6)² ] + B7

41

Criteria Review Seminar

New BCAR - Caveat

4 November 2015

• US P&C is the first model developed

• The application of changes to the Universal BCAR model is a work in progress

• A.M. Best’s view of risk will be the same in all models

42

2015 Insurance Market Briefing - Europe

New BCAR Approach

• Look and feel of the model will be similar – structure maintained where possible

• The risk factors will be generated using stochastic simulations from probability curves – with company specific adjustments

• BCAR scores will be shown at five confidence levels

• Underlying calculations are different

• Ratio calculation has changed

• Application does change

4 November 2015Criteria Review Seminar 434 November 2015 43

2015 Insurance Market Briefing - Europe

New BCAR Approach

• Utilising VaR risk metrics

– Ensures a consistent risk metric across different model components

– Reasonable tail issues still covered

• Consistent confidence intervals across risks

– 98% 99% 99.5% 99.8% 99.9%

• BCAR scores will be shown at these confidence levels

4 November 2015Criteria Review Seminar 444 November 2015 44

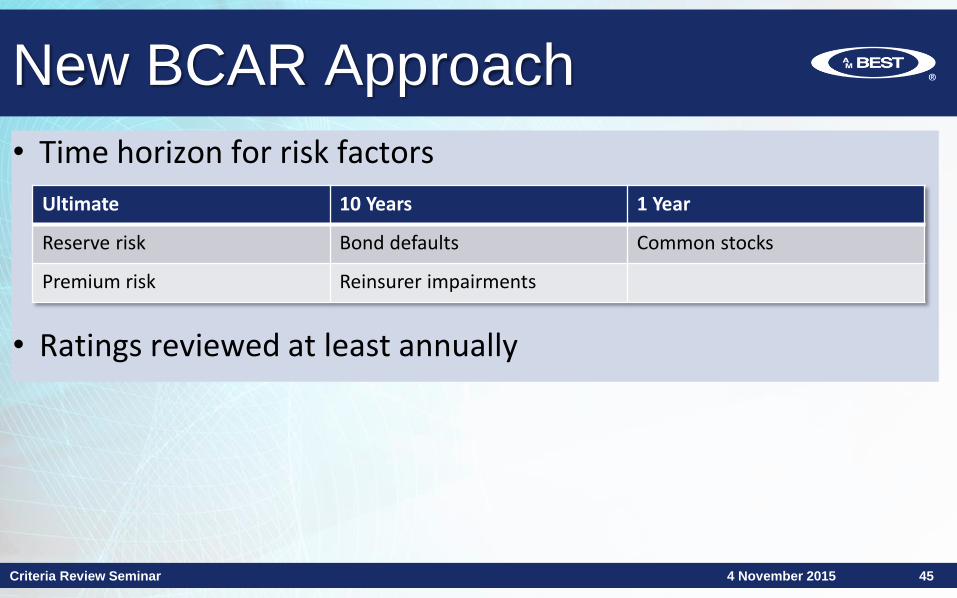

Criteria Review Seminar

New BCAR Approach

4 November 2015

• Time horizon for risk factors

• Ratings reviewed at least annually

Ultimate 10 Years 1 Year

Reserve risk Bond defaults Common stocks

Premium risk Reinsurer impairments

45

NET REQUIRED CAPITAL*

+ (B1) Fixed-Income Securities

+ (B2) Equity Securities

+ (B3) Interest Rate

+ (B4) Credit

+ (B5) Loss Reserves

+ (B6) Net Written Premium

+ (B7) Off Balance Sheet Risks

+ (B8) Catastrophe Exposure

- COVARIANCE

Criteria Review Seminar

New BCAR Approach

4 November 2015

AVAILABLE CAPITAL

+ Shareholders’ funds

+ Adjustments made to ensure a more economic and comparable basis for capital adequacy

BCAR SCORE = (AVAILABLE CAPITAL – NET REQUIRED CAPITAL)

/ AVAILABLE CAPITAL

*Net required capital = SQRT [(B1)²+(B2)²+(B3)²+(0.5*B4)² +[(0.5*B4)+B5)]²+(B6)² ] + B7 + B8

46

Criteria Review Seminar

New BCAR Approach

4 November 2015 47

• Current BCAR Calculation(ratio to NRC)

Potential Scores:Low of 0.0 to Max of 999.9Want BCAR > 100.0

• Planned BCAR Calculation (ratio to Available Capital)

Potential Scores:Low of -999.9 to Max of 100.0Want BCAR > 0.0

2015 Insurance Market Briefing - Europe

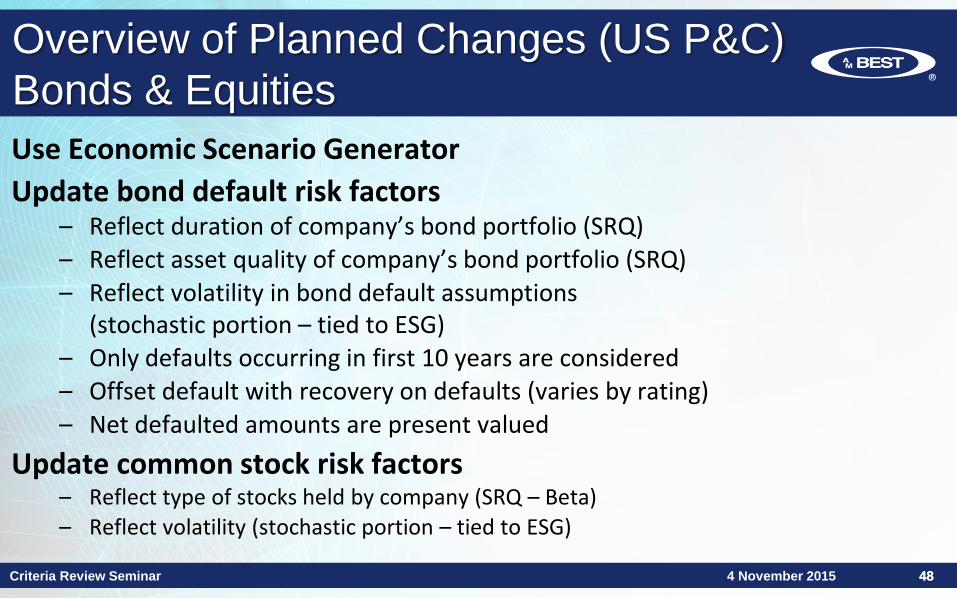

Overview of Planned Changes (US P&C)

Bonds & Equities

Use Economic Scenario Generator

Update bond default risk factors – Reflect duration of company’s bond portfolio (SRQ)– Reflect asset quality of company’s bond portfolio (SRQ)

– Reflect volatility in bond default assumptions (stochastic portion – tied to ESG)

– Only defaults occurring in first 10 years are considered– Offset default with recovery on defaults (varies by rating)

– Net defaulted amounts are present valued

Update common stock risk factors– Reflect type of stocks held by company (SRQ – Beta)

– Reflect volatility (stochastic portion – tied to ESG)

4 November 2015Criteria Review Seminar 484 November 2015 48

2015 Insurance Market Briefing - Europe

Overview of Planned Changes (US P&C)

Interest Rate Risk

Use Economic Scenario Generator

Update risk charges for interest rate risk – Simulated 10,000 potential one-year changes in interest rates

– Measured at various VaR levels

– Range from 210 to 310 basis points

– Reflect duration of company’s fixed income portfolio (SRQ)

– Reflect liquidity need using greater of gross PML or 10% of assets

4 November 2015Criteria Review Seminar 494 November 2015 49

2015 Insurance Market Briefing - Europe

Overview of Planned Changes (US P&C)

Reinsurance

Update reinsurance credit risk factors– Reflect type of recoverable (paid, unpaid, upr)– Reflect rating of each reinsurer (Schedule F/S and ratings data)

– Reflects concentration risk (how many reinsurers)– Reflect duration of recoverables (can go out 30 years)– Reflects partial recovery when reinsurer impaired

– Simulates 10,000 impairment scenarios for each reinsurer• Only uses impairments occurring in first 10 years

• Uncollected amounts are present valued

4 November 2015Criteria Review Seminar 504 November 2015 50

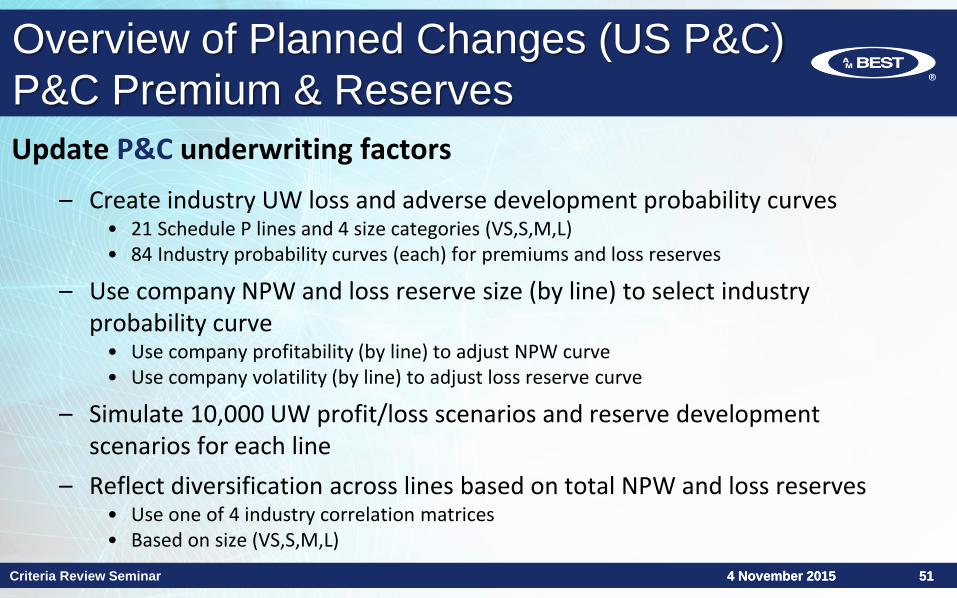

Criteria Review SeminarCriteria Review Seminar

Update P&C underwriting factors

– Create industry UW loss and adverse development probability curves• 21 Schedule P lines and 4 size categories (VS,S,M,L)• 84 Industry probability curves (each) for premiums and loss reserves

– Use company NPW and loss reserve size (by line) to select industry probability curve

• Use company profitability (by line) to adjust NPW curve• Use company volatility (by line) to adjust loss reserve curve

– Simulate 10,000 UW profit/loss scenarios and reserve development scenarios for each line

– Reflect diversification across lines based on total NPW and loss reserves• Use one of 4 industry correlation matrices• Based on size (VS,S,M,L)

Overview of Planned Changes (US P&C)

P&C Premium & Reserves

4 November 20154 November 2015 5151

Criteria Review Seminar

Update natural catastrophe approach

– Per occurrence

– Total all perils

– Measured at various VaR levels

– Risk added to Net Required Capital

– Will continue stress test approach

– Will stress higher VaR levels if concerned with tail risk

– Reinstatement premium and tax adjustments remain

– Terrorism and other stress tests remain

Overview of Planned Changes (US P&C)

Natural Catastrophe

4 November 20154 November 2015 5252

Criteria Review Seminar

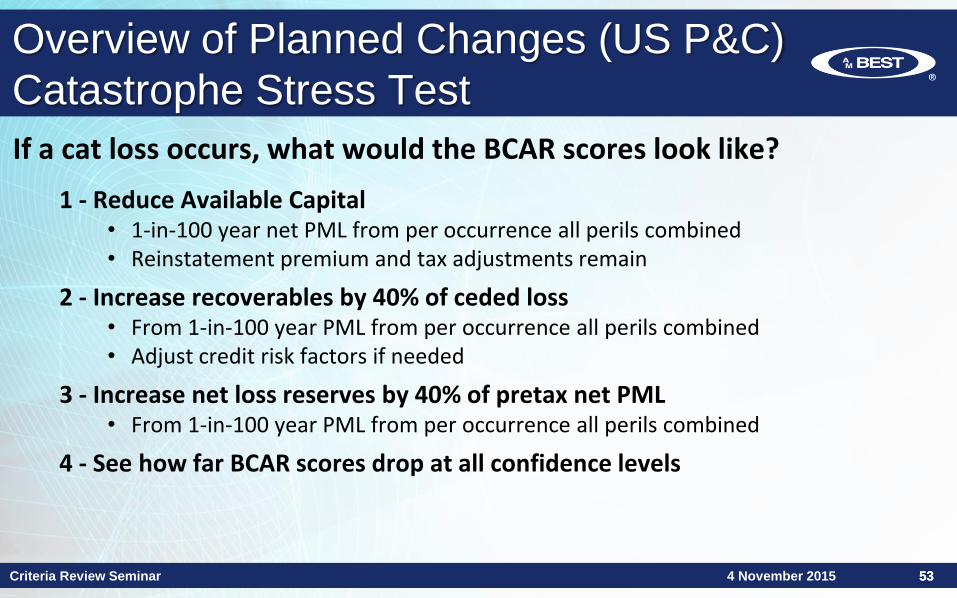

Overview of Planned Changes (US P&C)

Catastrophe Stress Test

If a cat loss occurs, what would the BCAR scores look like?

1 - Reduce Available Capital• 1-in-100 year net PML from per occurrence all perils combined• Reinstatement premium and tax adjustments remain

2 - Increase recoverables by 40% of ceded loss• From 1-in-100 year PML from per occurrence all perils combined• Adjust credit risk factors if needed

3 - Increase net loss reserves by 40% of pretax net PML• From 1-in-100 year PML from per occurrence all perils combined

4 - See how far BCAR scores drop at all confidence levels

4 November 2015 5353

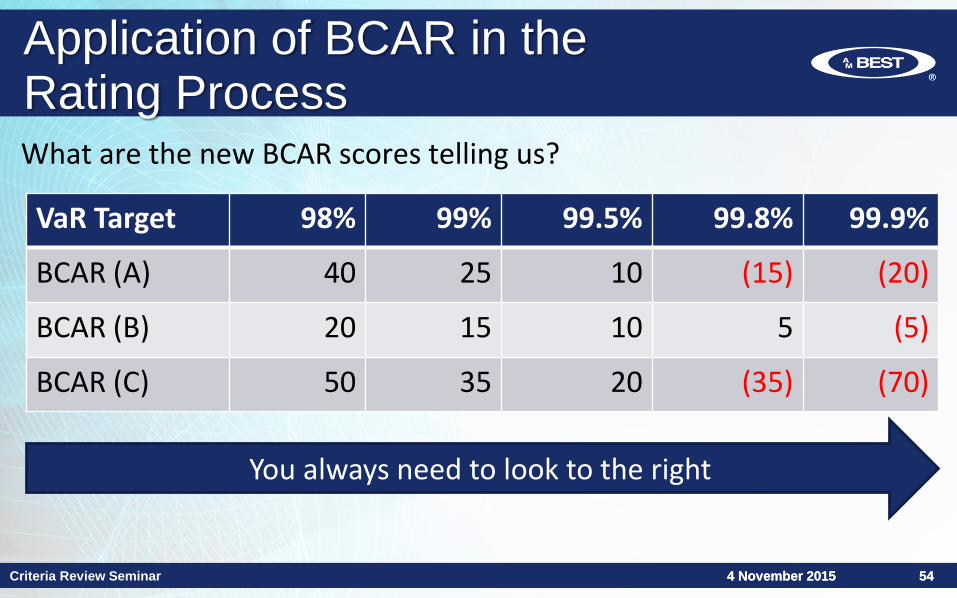

Criteria Review Seminar

Application of BCAR in the Rating ProcessWhat are the new BCAR scores telling us?

You always need to look to the right

4 November 20154 November 2015 5454

VaR Target 98% 99% 99.5% 99.8% 99.9%

BCAR (A) 40 25 10 (15) (20)

BCAR (B) 20 15 10 5 (5)

BCAR (C) 50 35 20 (35) (70)

Criteria Review Seminar

Application of BCAR in the

Rating Process• Changes in BCAR approach affects the broader credit methodology,

Best’s Credit Rating Methodology (BCRM)

– New BCAR score calculation

– View of capital adequacy at different VaR confidence levels rather than a single score

• BCRM update will provide clarity on how the new BCAR output (with scores displayed at five VaR confidence levels) will be considered in the rating evaluation

4 November 20154 November 2015 5555

Updated Timeline

• Q1 2016 – likely release for public comment of US P&C BCAR draft Criteria and draft BCRM update

– Company BCAR output will be shared with rated entities

• Later 2016 – likely release for public comment of US Life/Health and Universal draft BCAR criteria and models

– Company BCAR output will be shared with rated entities

• Comment period will include updates

• Comment period will be extended to cover the release of all BCAR models to ensure consistent application of the new BCAR approach across all ratings

564 November 2015Criteria Review Seminar 4 November 20154 November 2015 5656

4 November 2015Criteria Review Seminar

Updated Timeline – Next Steps

• What must happen before US P&C BCAR criteria procedure is released for public comment?

– Complete the update of BCRM

– Complete the initial review of the Life and Non-US BCARs

– Complete all internal training on the US P&C model and the application of BCAR

– A.M. Best will need to be comfortable that the change in application and the implications of the new BCAR on all industries is understood (Life/Health and Non-Life; US andNon-US)

4 November 20154 November 2015 5757

Further Information

A.M. Best webinars on the new BCAR (from April, May and October 2015) provide further information and can be found here:

www.ambest.com/conferences/webinars.asp

Criteria Review Seminar 584 November 2015

Criteria Review Seminar

Q & A

4 November 2015 59

Stochastic-based BCAR(Best’s Capital Adequacy Ratio)

Mathilde Jakobsen

Associate Director, Analytics, A.M. Best