credit rating agencies , greek crisis, financial crisis 2008

DESCRIPTION

PPT on CRA , Greek Crisis and Financial Crisis 2008TRANSCRIPT

KA N I S H KA M E H R O T RA A N D P RA B H AT B A H L

CREDIT RATING AGENCIESSUBPRIME MORTGAGE CRISIS

GREEK CRISIS

WHAT IS CREDIT RATING AGENCY ?

• An independent company that evaluates the financial condition of issuers of debt instruments and then assigns a rating that reflects its assessment of the issuer's ability to make the debt payments.

• Potential investors, customers, employees and business partners rely upon the data and objective analysis of credit rating agencies in determining the overall strength and stability of a company.

• Examples : Moody’s, Fitch Group, Standard & Poor’s etc…..

WHAT DOES CREDIT RATING CONVEY?

• A credit rating is an opinion‘ on the creditworthiness or the relative degree of risk of timely payment of interest and principal on a debt instrument.

• Most rating agencies adopt some variation of this definition for their credit ratings.

• The ratings are a comment on the relative likelihood of default in comparison to other rated instruments.

• In other words, a rating indicates the probability of default of the rated instrument and therefore provides a benchmark for measuring and pricing credit risk.

RATING RELATED PRODUCTS

CRAs rate a large number of financial products: 1. Bonds/ debentures- [the main product] 2. Commercial paper 3. Structured finance products4. Bank loans 5. Fixed deposits and bank certificate of deposits6. Mutual fund debt schemes 7. Initial Public Offers (IPOs) and many more……

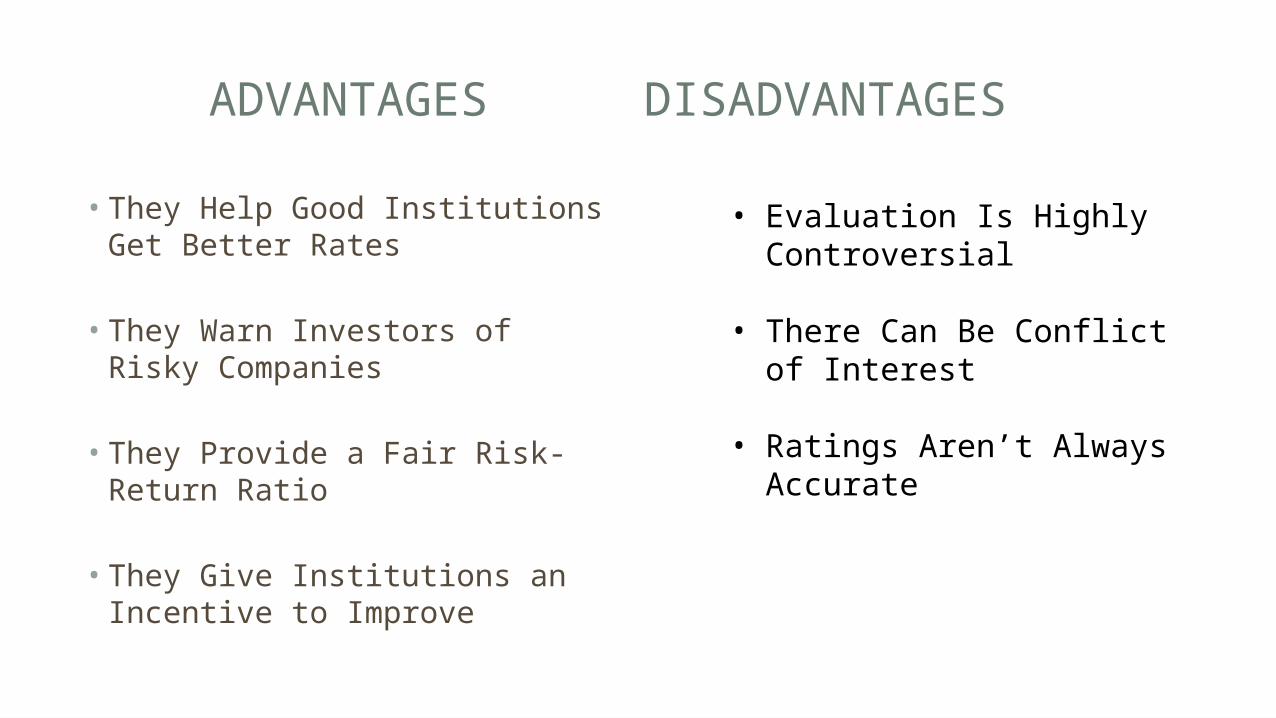

ADVANTAGESDISADVANTAGES

• They Help Good Institutions Get Better Rates

• They Warn Investors of Risky Companies

• They Provide a Fair Risk-Return Ratio

• They Give Institutions an Incentive to Improve

• Evaluation Is Highly Controversial

• There Can Be Conflict of Interest

• Ratings Aren’t Always Accurate

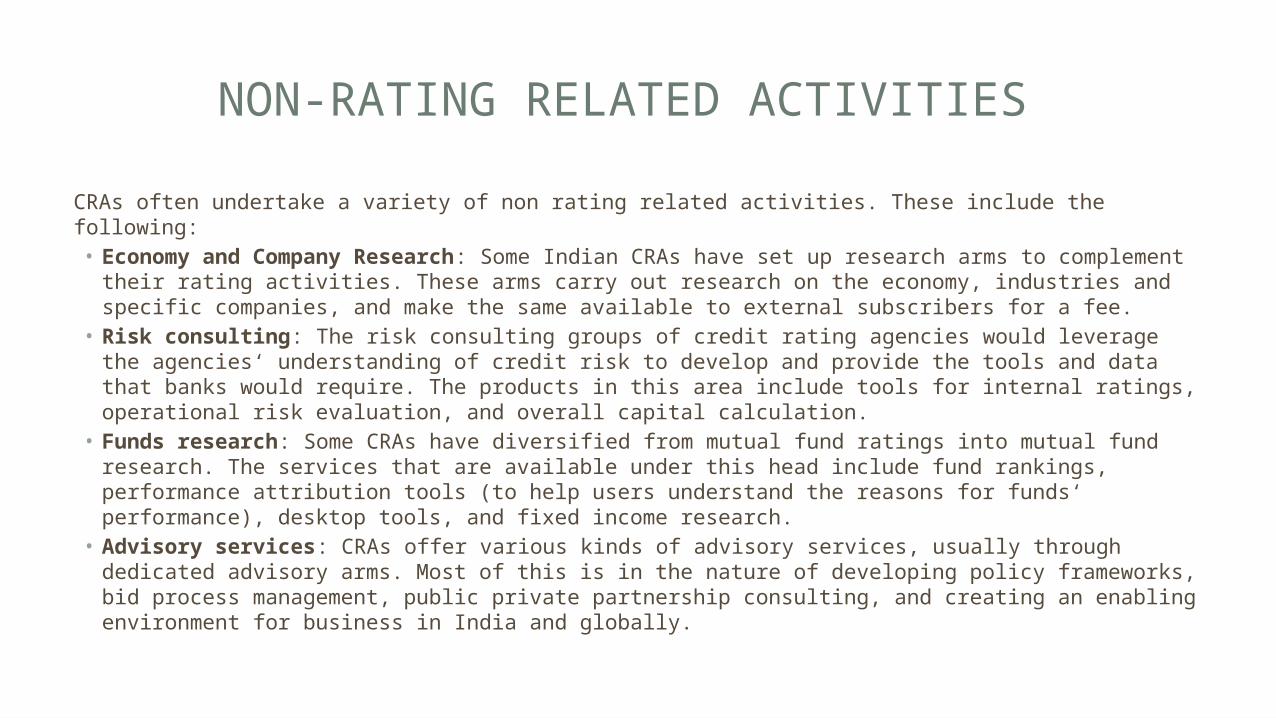

NON-RATING RELATED ACTIVITIES

CRAs often undertake a variety of non rating related activities. These include the following:• Economy and Company Research: Some Indian CRAs have set up research arms to

complement their rating activities. These arms carry out research on the economy, industries and specific companies, and make the same available to external subscribers for a fee.

• Risk consulting: The risk consulting groups of credit rating agencies would leverage the agencies‘ understanding of credit risk to develop and provide the tools and data that banks would require. The products in this area include tools for internal ratings, operational risk evaluation, and overall capital calculation.

• Funds research: Some CRAs have diversified from mutual fund ratings into mutual fund research. The services that are available under this head include fund rankings, performance attribution tools (to help users understand the reasons for funds‘ performance), desktop tools, and fixed income research.

• Advisory services: CRAs offer various kinds of advisory services, usually through dedicated advisory arms. Most of this is in the nature of developing policy frameworks, bid process management, public private partnership consulting, and creating an enabling environment for business in India and globally.

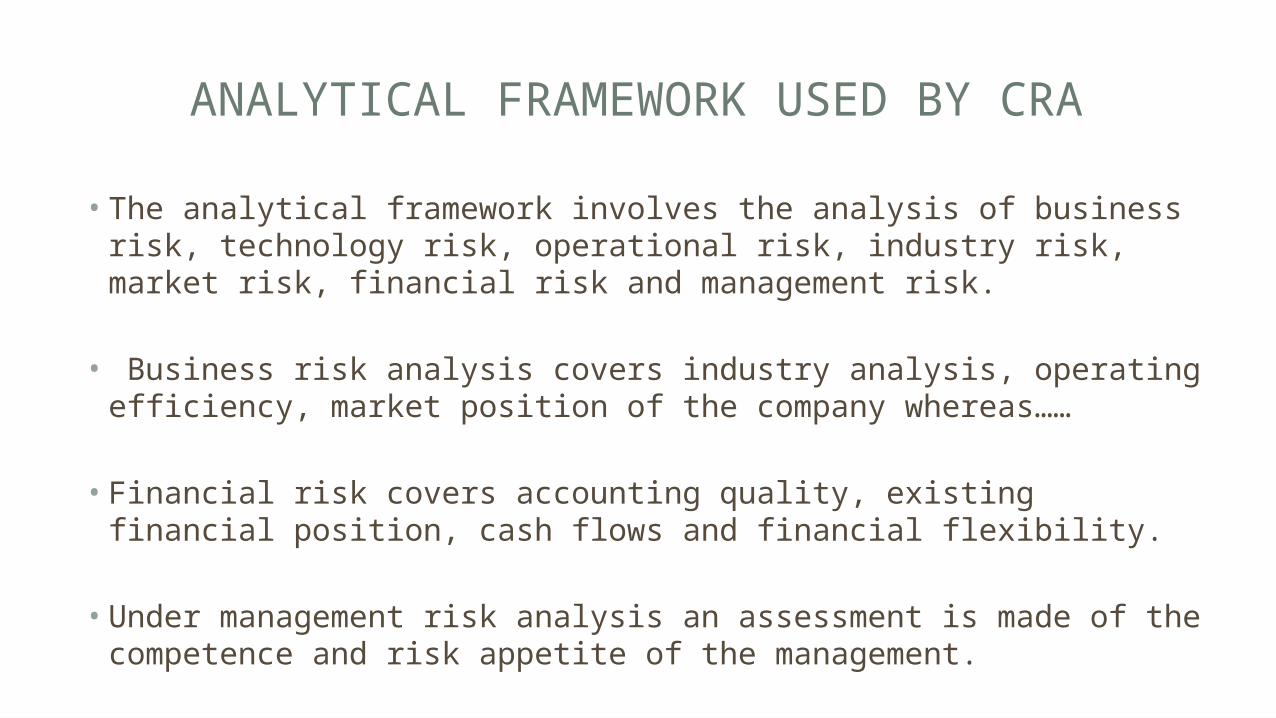

ANALYTICAL FRAMEWORK USED BY CRA

• The analytical framework involves the analysis of business risk, technology risk, operational risk, industry risk, market risk, financial risk and management risk.

• Business risk analysis covers industry analysis, operating efficiency, market position of the company whereas……

• Financial risk covers accounting quality, existing financial position, cash flows and financial flexibility.

• Under management risk analysis an assessment is made of the competence and risk appetite of the management.

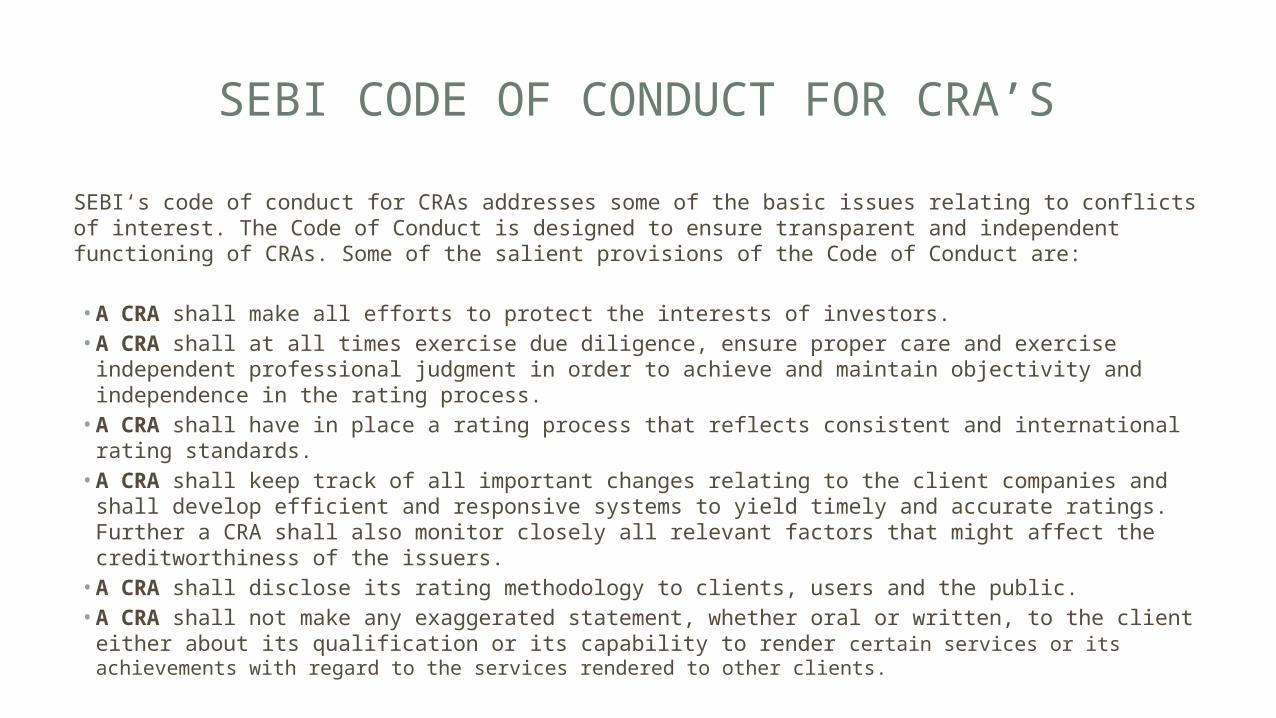

SEBI CODE OF CONDUCT FOR CRA’S

SEBI‘s code of conduct for CRAs addresses some of the basic issues relating to conflicts of interest. The Code of Conduct is designed to ensure transparent and independent functioning of CRAs. Some of the salient provisions of the Code of Conduct are:

• A CRA shall make all efforts to protect the interests of investors. • A CRA shall at all times exercise due diligence, ensure proper care and exercise independent

professional judgment in order to achieve and maintain objectivity and independence in the rating process.

• A CRA shall have in place a rating process that reflects consistent and international rating standards.

• A CRA shall keep track of all important changes relating to the client companies and shall develop efficient and responsive systems to yield timely and accurate ratings. Further a CRA shall also monitor closely all relevant factors that might affect the creditworthiness of the issuers.

• A CRA shall disclose its rating methodology to clients, users and the public. • A CRA shall not make any exaggerated statement, whether oral or written, to the client either

about its qualification or its capability to render certain services or its achievements with regard to the services rendered to other clients.

TOP CRA’S – GLOBAL AND INDIA

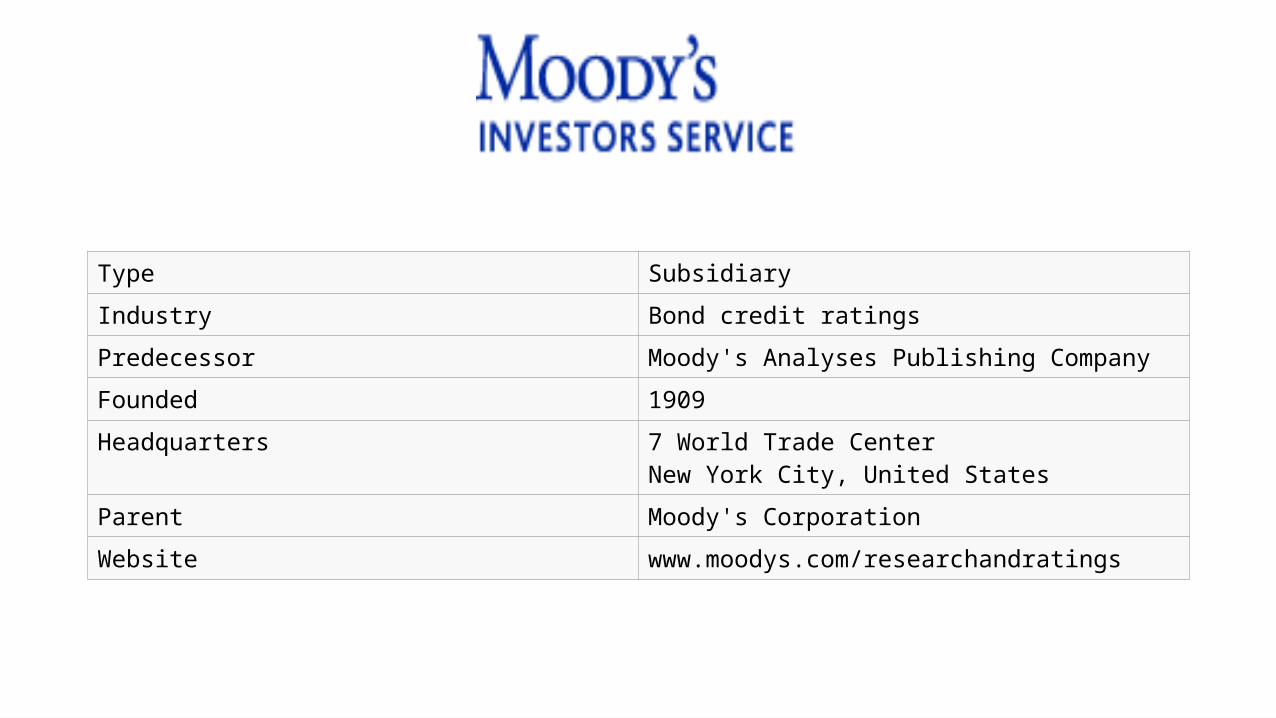

Type Subsidiary

Industry Bond credit ratings

Predecessor Moody's Analyses Publishing Company

Founded 1909

Headquarters 7 World Trade CenterNew York City, United States

Parent Moody's Corporation

Website www.moodys.com/researchandratings

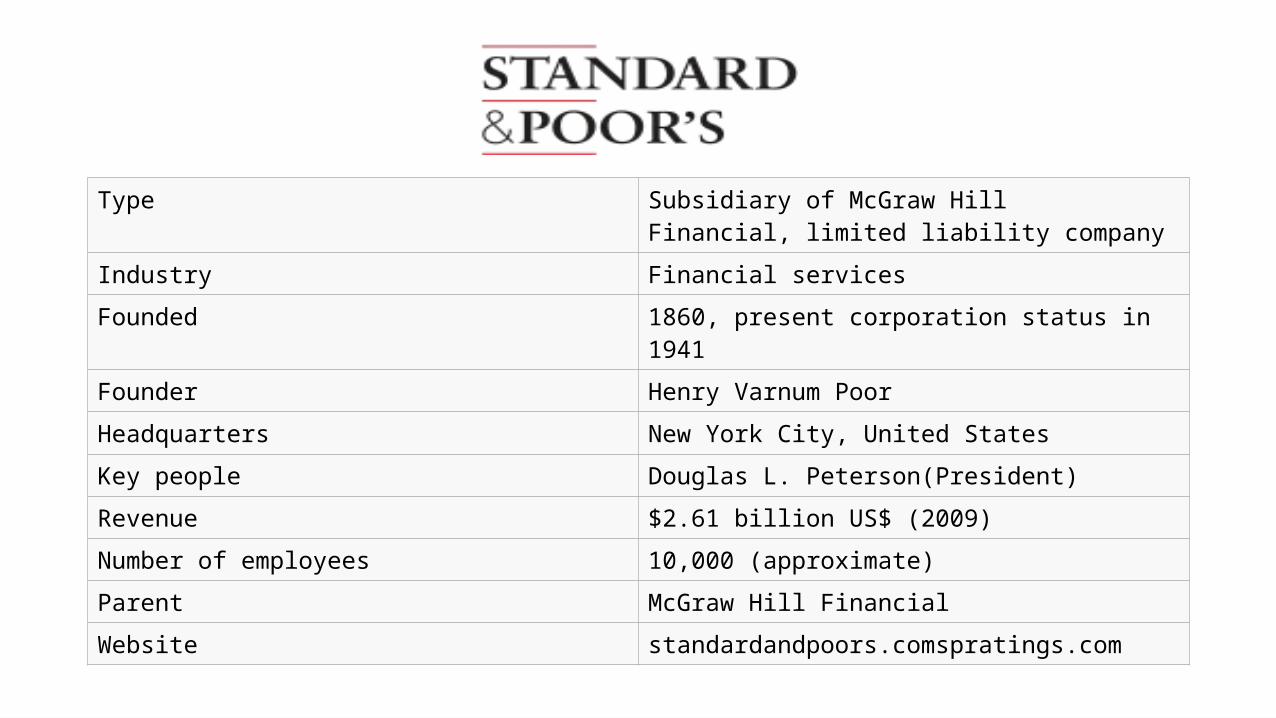

Type Subsidiary of McGraw Hill Financial, limited liability company

Industry Financial services

Founded 1860, present corporation status in 1941

Founder Henry Varnum Poor

Headquarters New York City, United States

Key people Douglas L. Peterson(President)

Revenue $2.61 billion US$ (2009)

Number of employees 10,000 (approximate)

Parent McGraw Hill Financial

Website standardandpoors.comspratings.com

Type Subsidiary

Industry Financial services

Founded 1914

Founder John Knowles Fitch

Headquarters New York City, United States, and London, United Kingdom

Key people Paul TaylorPresident & CEO

Revenue $732.5 Million (2011)

Owner Hearst Corporation and FIMALAC SA

Number of employees 2,000 (approximate)

Website www.fitchratings.com

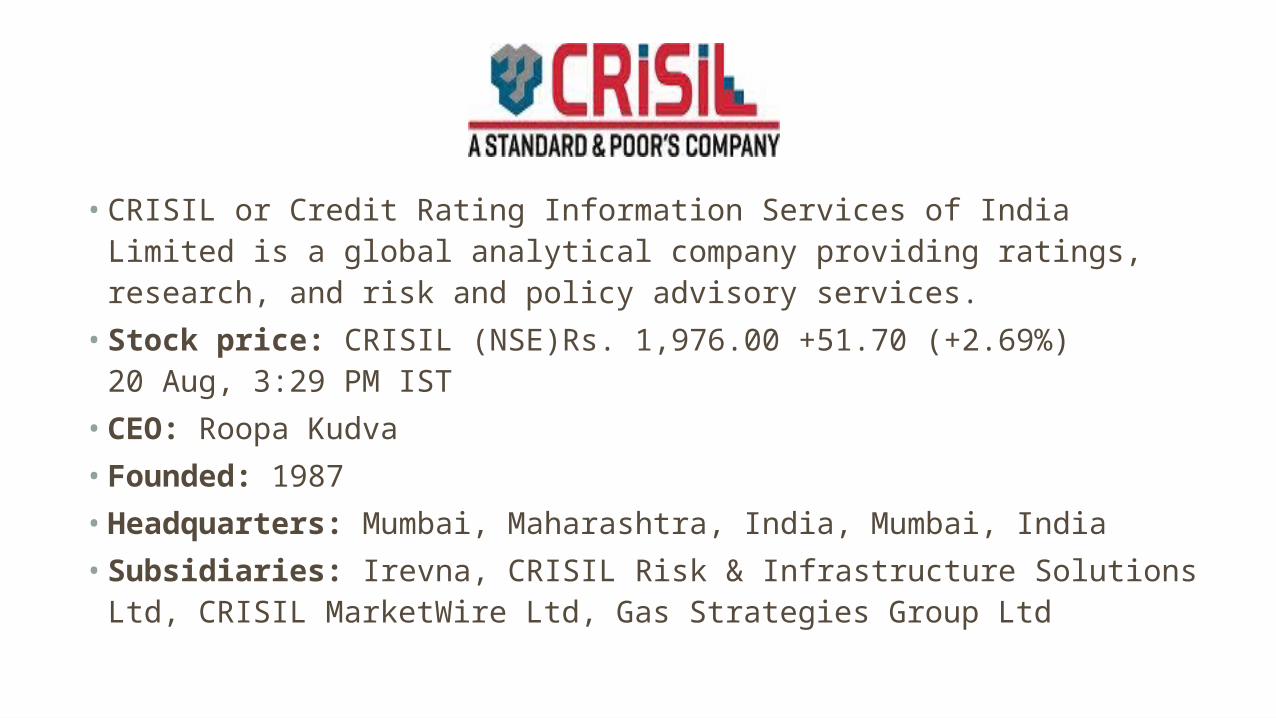

• CRISIL or Credit Rating Information Services of India Limited is a global analytical company providing ratings, research, and risk and policy advisory services.

• Stock price: CRISIL (NSE)Rs. 1,976.00 +51.70 (+2.69%)20 Aug, 3:29 PM IST

• CEO: Roopa Kudva• Founded: 1987• Headquarters: Mumbai, Maharashtra, India, Mumbai, India• Subsidiaries: Irevna, CRISIL Risk & Infrastructure Solutions

Ltd, CRISIL MarketWire Ltd, Gas Strategies Group Ltd

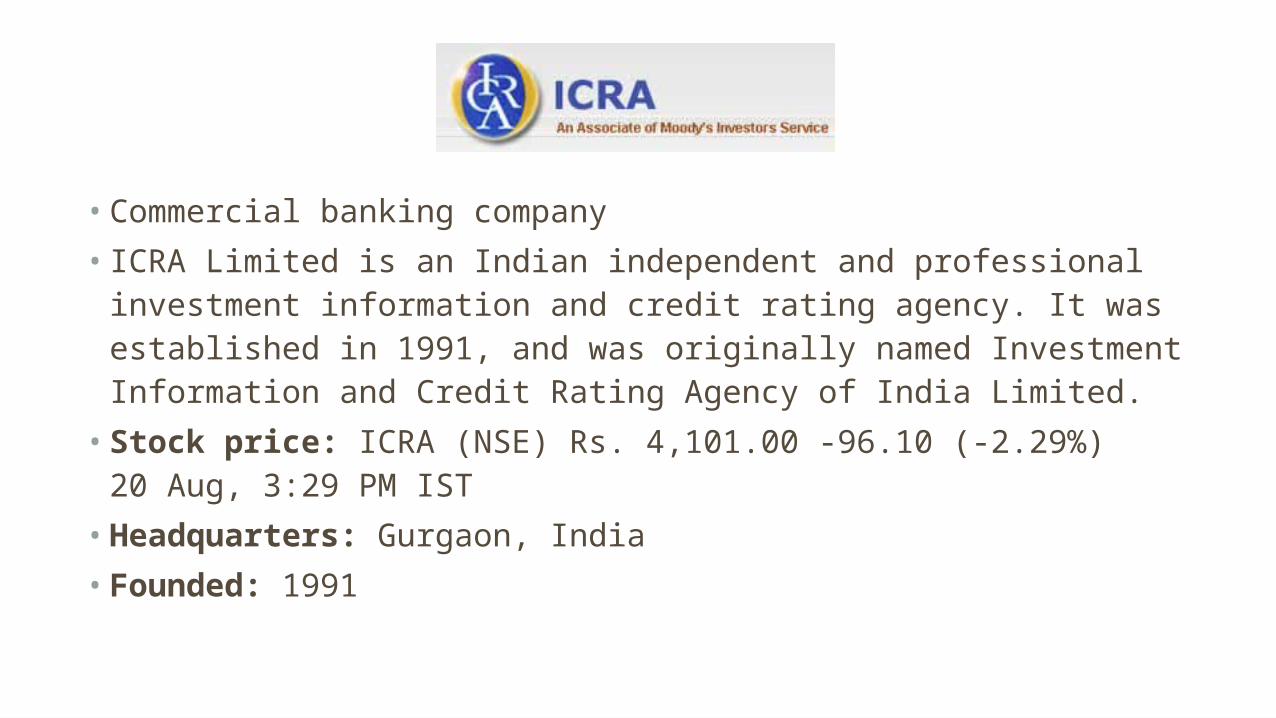

• Commercial banking company• ICRA Limited is an Indian independent and professional investment

information and credit rating agency. It was established in 1991, and was originally named Investment Information and Credit Rating Agency of India Limited.

• Stock price: ICRA (NSE) Rs. 4,101.00 -96.10 (-2.29%)20 Aug, 3:29 PM IST

• Headquarters: Gurgaon, India• Founded: 1991

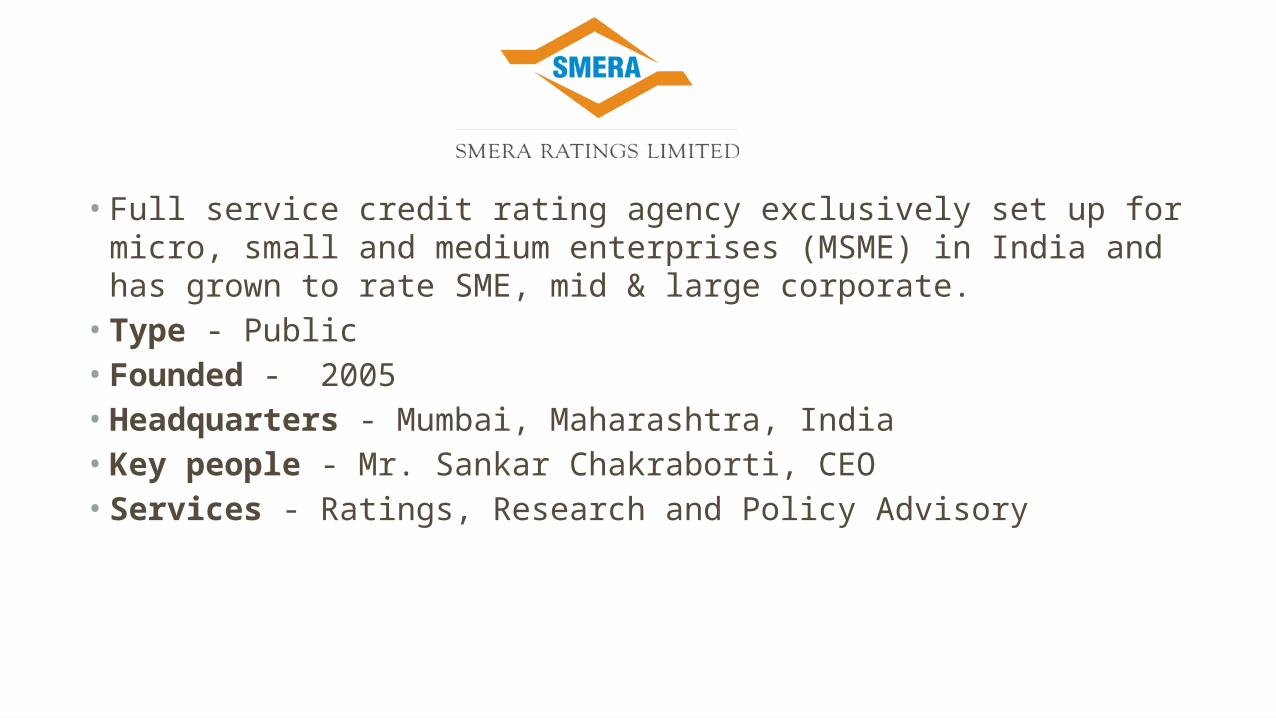

• Full service credit rating agency exclusively set up for micro, small and medium enterprises (MSME) in India and has grown to rate SME, mid & large corporate.

• Type - Public• Founded - 2005 • Headquarters - Mumbai, Maharashtra, India• Key people - Mr. Sankar Chakraborti, CEO• Services - Ratings, Research and Policy Advisory

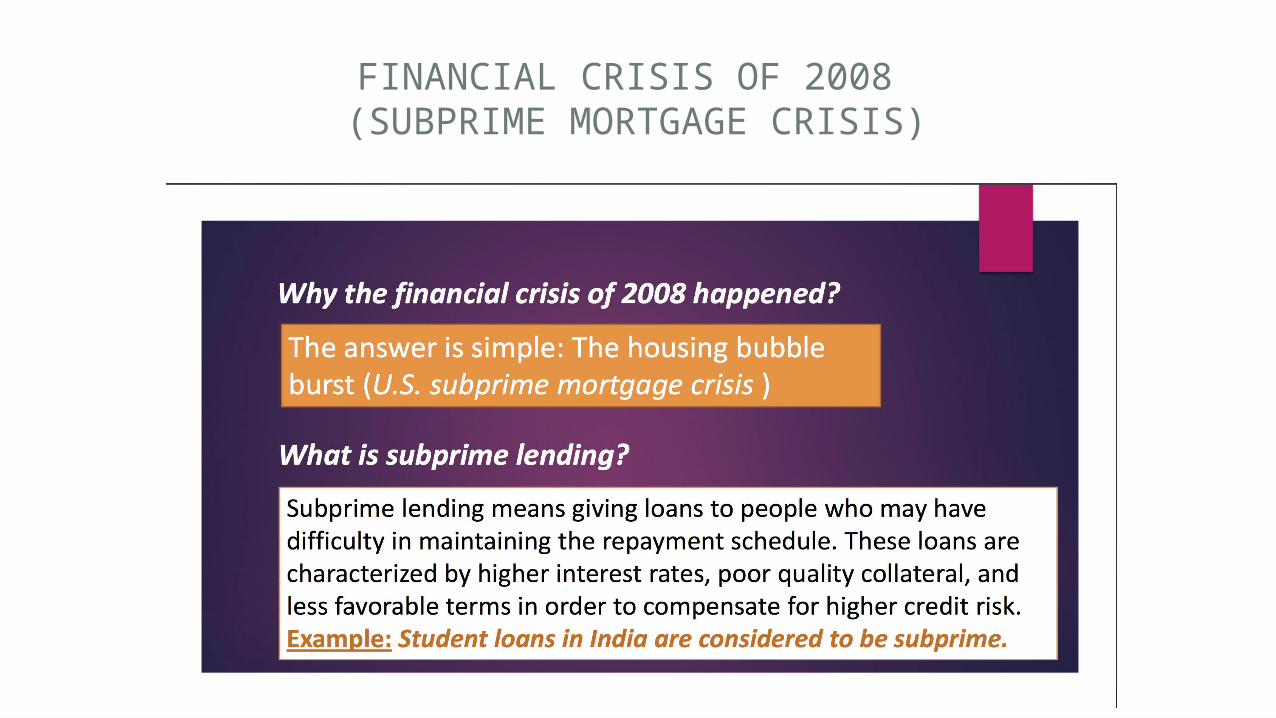

FINANCIAL CRISIS OF 2008 (SUBPRIME MORTGAGE CRISIS)

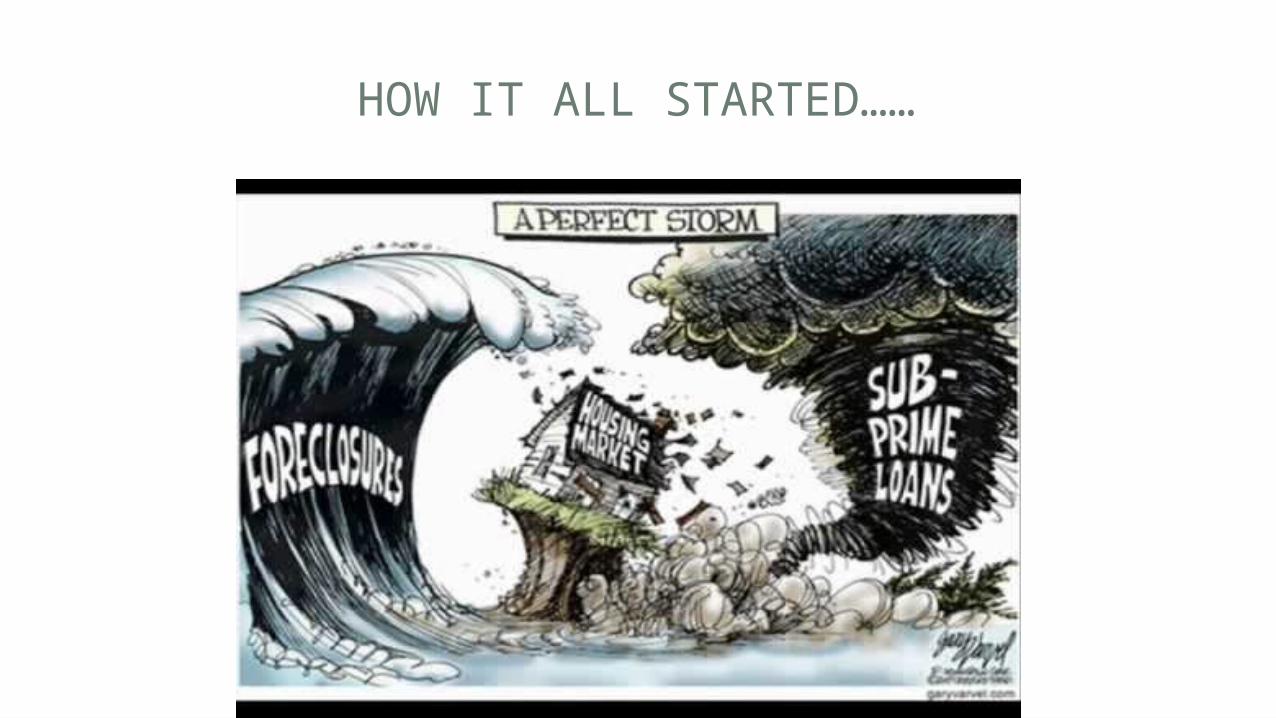

HOW IT ALL STARTED……

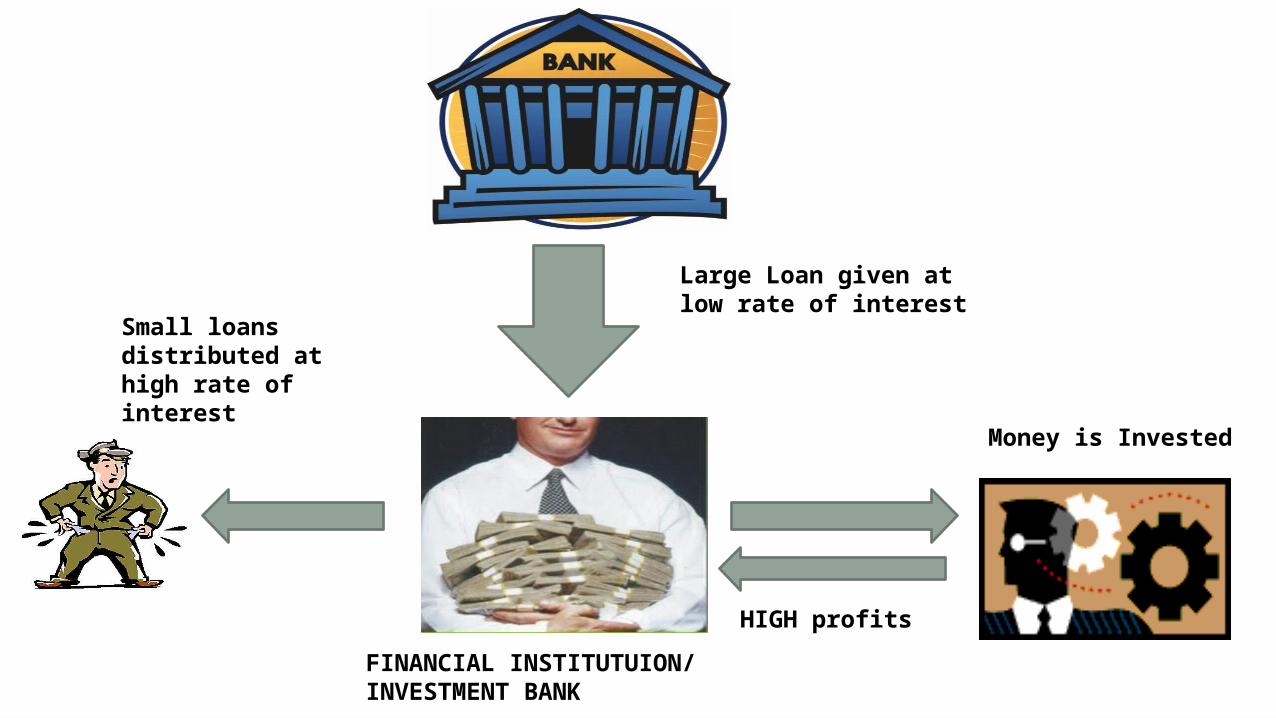

Large Loan given at low rate of interest

FINANCIAL INSTITUTUION/INVESTMENT BANK

Small loans distributed at high rate of interest

Money is Invested

HIGH profits

ABOUT THE CRISIS

Post 2001, the US government had encouraged US banks to lend money to people, to encourage spending & investing mainly for the purpose of buying houses

These banks granted loans to large number of borrowers despite having lower income levels, unsure employment status, unscrupulous credit history, etc.

Huge number of borrowers availed of bank credit without evaluating their repayment capacities. The economy was flush with liquidity & stock markets were booming

CONTINUED…..

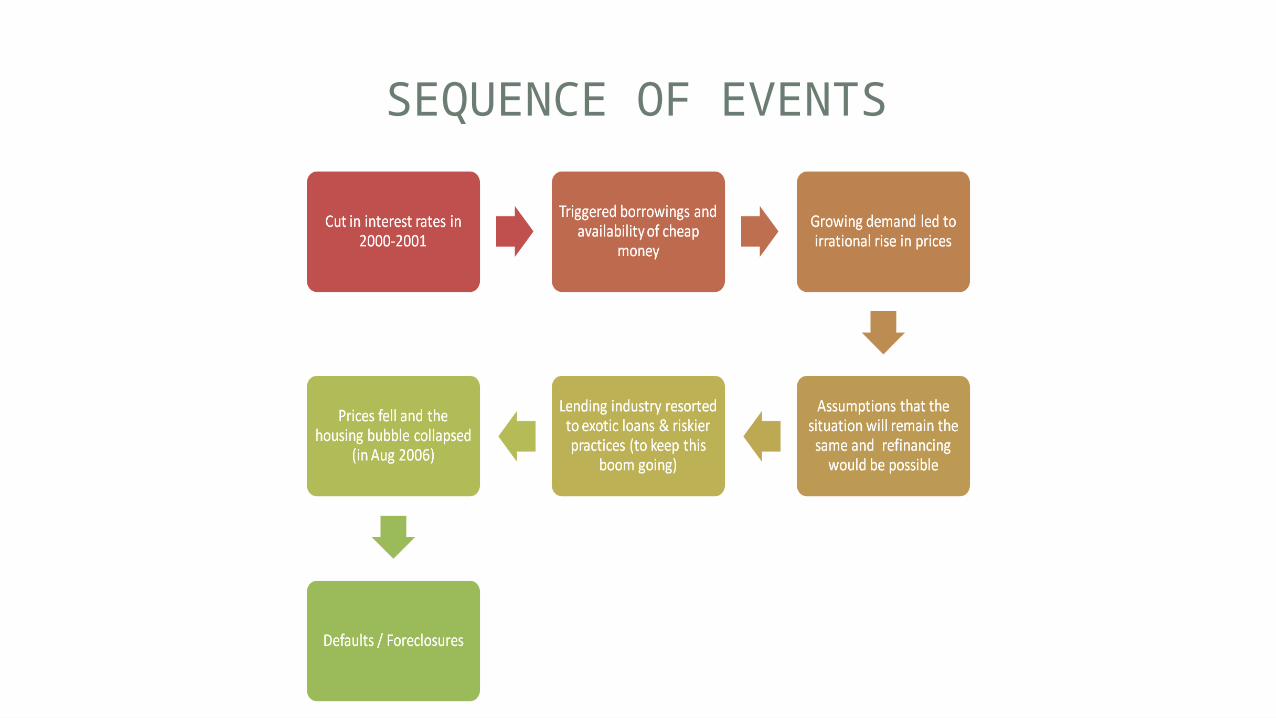

• A silent storm brewed in international financial markets with origins in the US housing market, which witnessed an unprecedented boom since 2001

• The boom was led by rising housing prices, low interest rates.

• Housing prices in USA began to drop in 2006. Rising interest rates & falling housing prices led to rise in sub prime mortgage delinquencies & resultant foreclosure

• Result: The housing bubble burst in Aug 2006

SEQUENCE OF EVENTS

CONTINUED….. (HOUSING BUBBLE)

• Up until 2006, the housing market in the United States was flourishing due to the fact that it was so easy to get a home loan.

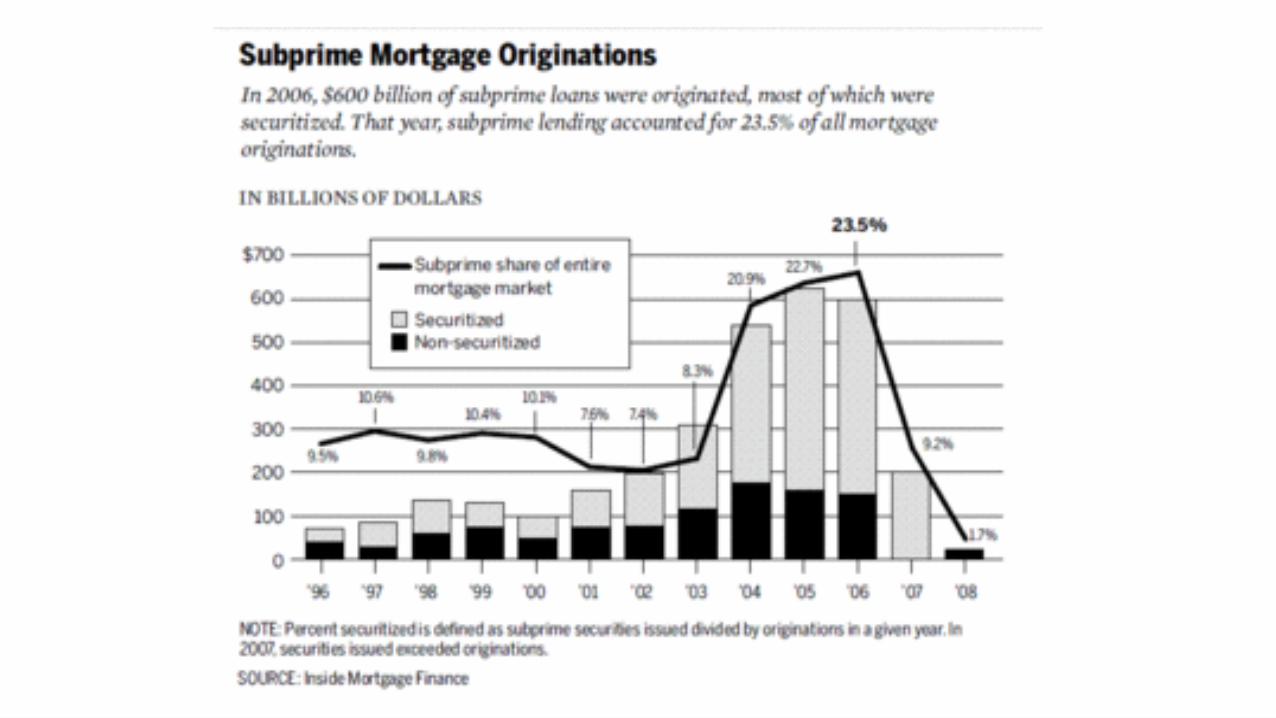

• Individuals were taking on subprime mortgages, with the expectations that the price of their home would continue to rise and that they would be able to refinance their home before the higher interest rates were to go into effect. 2005 was the peak of the subprime boom. At this time, 1 in 5 mortgages was subprime.

• However, the housing bubble burst and housing prices had reached their peak. They were now on a decline.

BUBBLE BURST

CONTINUED….

• Home prices reached their peak in the second quarter of 2006. They did not fall drastically at first.

• Home prices fell by less than 2 percent from the 2nd quarter of 2006 to the 4th quarter of 2006.

• The foreclosure start rates increased by 43 percent over these two quarters, and increased by 75 percent in 2007 compared to 2006.

• This implies that mortgage default rates began to rise as soon as home prices began to fall.

CONTINUED….

• The increase in foreclosures added to the inventory of homes available for sale.

• This further decreased home prices, putting more homeowners into a negative equity position and leading to more foreclosures.

• The increase in foreclosures also decreased the value of mortgage-backed securities.

• This made it difficult for investment banks to issue new mortgage-backed securities, eliminating a major source of financing for new mortgage loans and contributing to the continuing decline in home prices.

IMPACTS ON FINANCIAL SYSTEM

Large losses were incurred by the following groups:I. Mortgage lenders: One thirds of top 30 mortgage lenders have

either been acquired or have filed for bankruptcy or have been liquidated.

II. Investment banks: Since the housing bubble burst, the five largest U.S. investment banks have either filed for bankruptcy (Lehman Brothers), been acquired by other Firms or become commercial banks subject to greater Regulation.

III. Foreign investors (mainly banks and governments) who had invested in mortgage backed securities.

IV. Insurance companies: (e.g., AIG) who had sold credit default swaps. Credit default swaps are a type of contract that insures against the mortgage-backed securities.

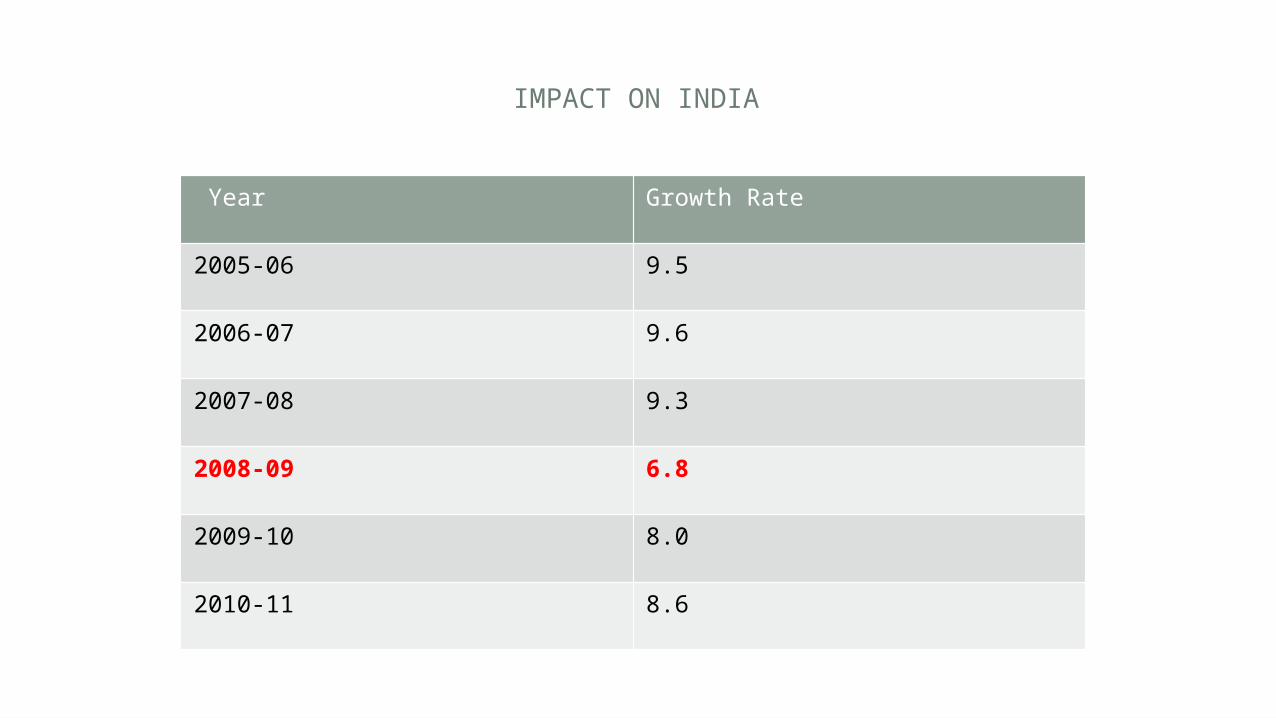

IMPACT ON INDIA

Year Growth Rate

2005-06 9.5

2006-07 9.6

2007-08 9.3

2008-09 6.8

2009-10 8.0

2010-11 8.6

BSE ‘SENSEX’ PERFORMANCE IN 2008

Month Open High Low Close

January 20325.27 21,206.77 15,332.42 17468.71

February 17820.67 18,895.34 16,457.74 17578.72

March 17227.56 17,227.56 14,677.24 15644.44

April 15771.72 17,480.74 15,297.96 17287.31

May 17560.15 17,735.70 16,196.02 16415.57

June 16591.46 16,632.72 13,405.54 13461.60

July 13480.02 15,130.09 12,514.02 14355.75

August 14064.26 15,579.78 14,002.43 14564.53

September 14412.99 15,107.01 12,153.55 12860.43

October 13006.72 13,203.86 7,697.39 9788.06

November 10209.37 10,945.41 8,316.39 9092.72

December 9162.94 10,188.54 8,467.43 9647.31

FALL OF INR

Dec 30th 08 : 1USD =48INRJan 1st 08 : 1USD =39INR

Dec 1st 08 : 1USD=50INR

GREEK CRISIS

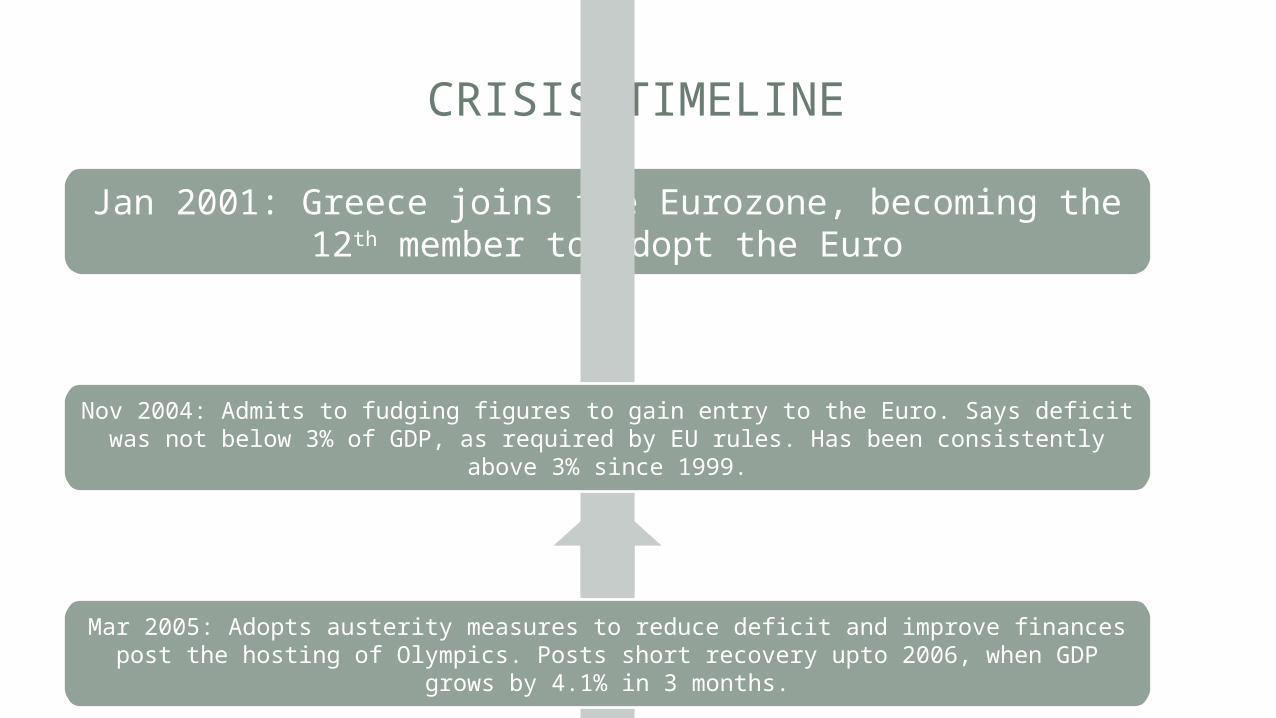

CRISIS TIMELINE

Jan 2001: Greece joins the Eurozone, becoming the 12th member to adopt the Euro

Nov 2004: Admits to fudging figures to gain entry to the Euro. Says deficit was not below 3% of GDP, as required by EU rules. Has been consistently above 3% since

1999.

Mar 2005: Adopts austerity measures to reduce deficit and improve finances post the hosting of Olympics. Posts short recovery upto 2006, when GDP grows by 4.1% in 3

months.

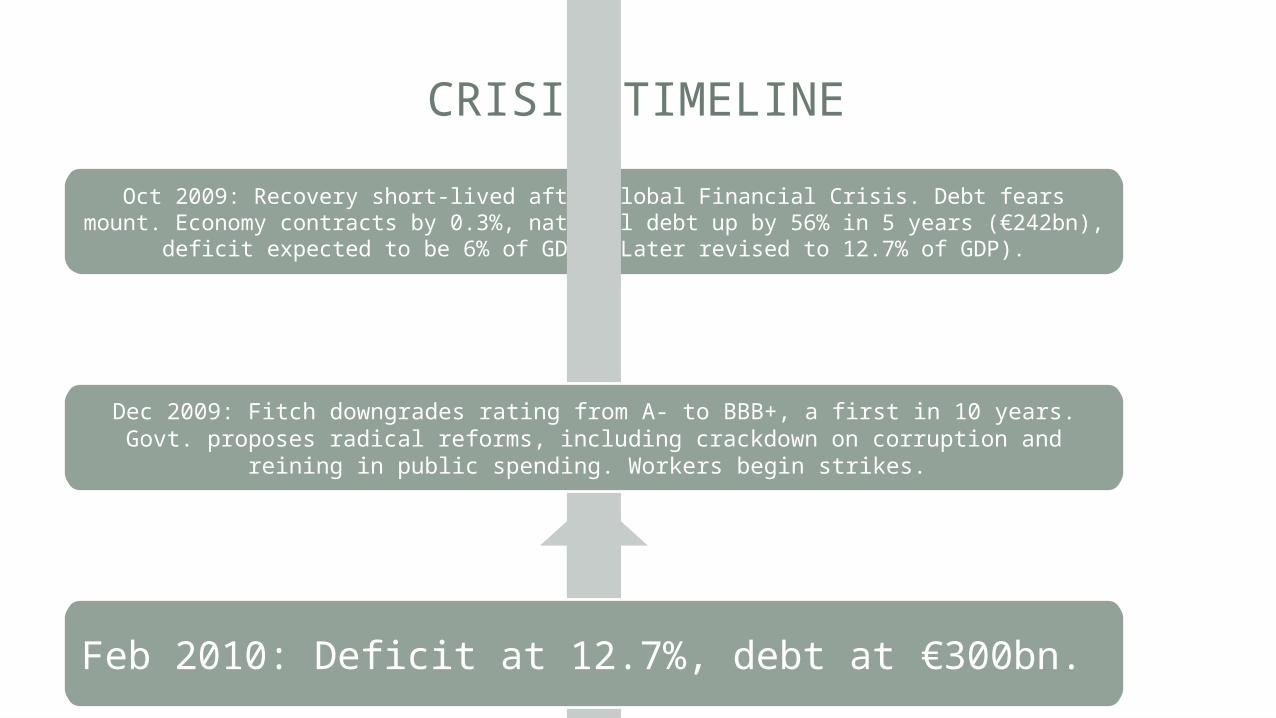

CRISIS TIMELINE

Oct 2009: Recovery short-lived after Global Financial Crisis. Debt fears mount. Economy contracts by 0.3%, national debt up by 56% in 5 years (€242bn), deficit

expected to be 6% of GDP. (Later revised to 12.7% of GDP).

Dec 2009: Fitch downgrades rating from A- to BBB+, a first in 10 years. Govt. proposes radical reforms, including crackdown on corruption and reining in public

spending. Workers begin strikes.

Feb 2010: Deficit at 12.7%, debt at €300bn.

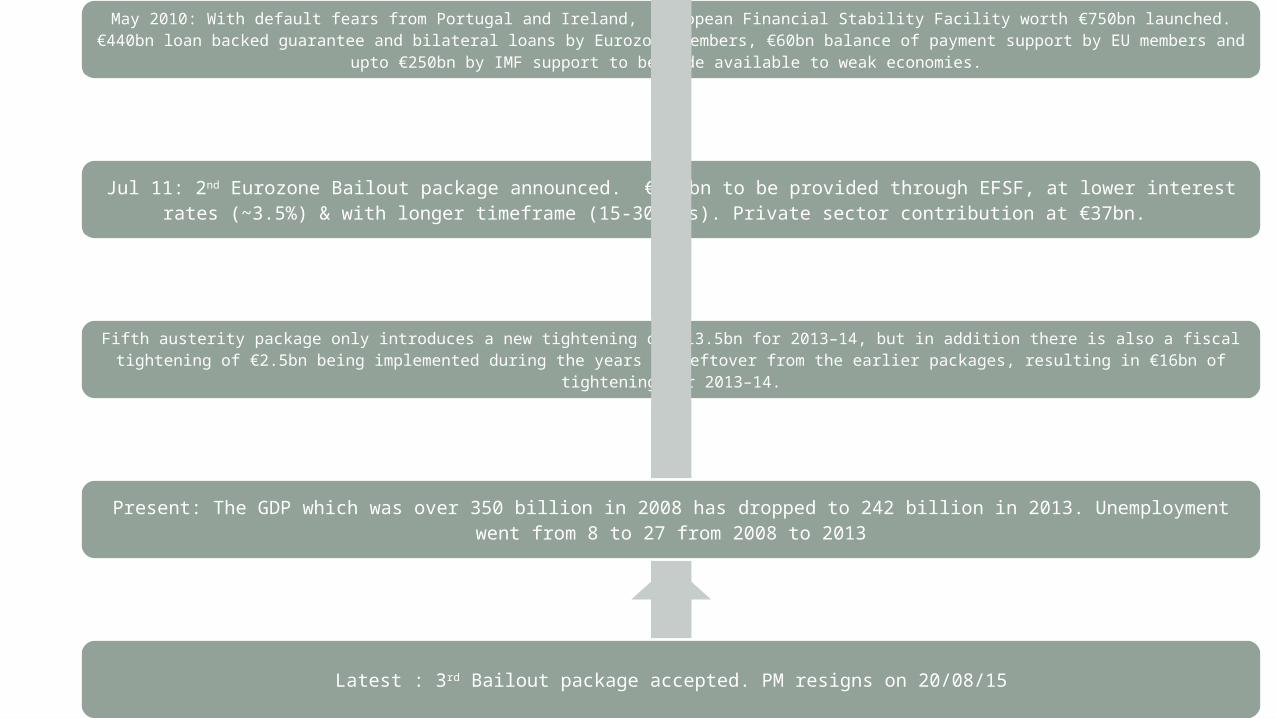

May 2010: With default fears from Portugal and Ireland, European Financial Stability Facility worth €750bn launched. €440bn loan backed guarantee and bilateral loans by Eurozone members, €60bn balance of payment support by EU members and upto €250bn by IMF support to be made available to weak economies.

Jul 11: 2nd Eurozone Bailout package announced. €109bn to be provided through EFSF, at lower interest rates (~3.5%) & with longer timeframe (15-30 yrs). Private sector contribution at €37bn.

Fifth austerity package only introduces a new tightening of €13.5bn for 2013–14, but in addition there is also a fiscal tightening of €2.5bn being implemented during the years as leftover from the earlier packages, resulting in €16bn of tightening for 2013–14.

Present: The GDP which was over 350 billion in 2008 has dropped to 242 billion in 2013. Unemployment went from 8 to 27 from 2008 to 2013

Latest : 3rd Bailout package accepted. PM resigns on 20/08/15

THANK YOU