creating and releasing shareholder value - osborne · pdf filecreating and releasing...

TRANSCRIPT

Creating and Releasing Shareholder ValueTim Morris, Michael Bell & Jonathan King 20 May 2010

osborneclarke.com

1

Introduction

• Welcome

• Market trends

• Methods of unlocking shareholder value

• Carphone Warehouse demerger – a company perspective

• Carphone Warehouse demerger – the lawyers' perspective

• OC survey – the results

osborneclarke.com

2

Market Trends

• Paradigm shift in deal cycle – dearth of corporate buyers, subdued private equity and availability of debt finance have all contributed

• Focus now on delivering shareholder value through alternative means to M&A

• Recent demergers of Carphone Warehouse, Cable & Wireless and Liberty International - just the beginning?

Methods of unlocking shareholder value

osborneclarke.com

4

Methods of unlocking shareholder value

1. Common methods

– Special dividend

– Share buy back

– B share scheme

– Demerger

2. Drivers

– Anatomy of share register

– Reserves/free cash

– Tax

osborneclarke.com

5

Methods of unlocking shareholder value

Special Dividends

1. Suited for companies with institutional shareholders

2. UK corporate shareholders will generally receive dividends tax free

3. Individual shareholders

osborneclarke.com

6

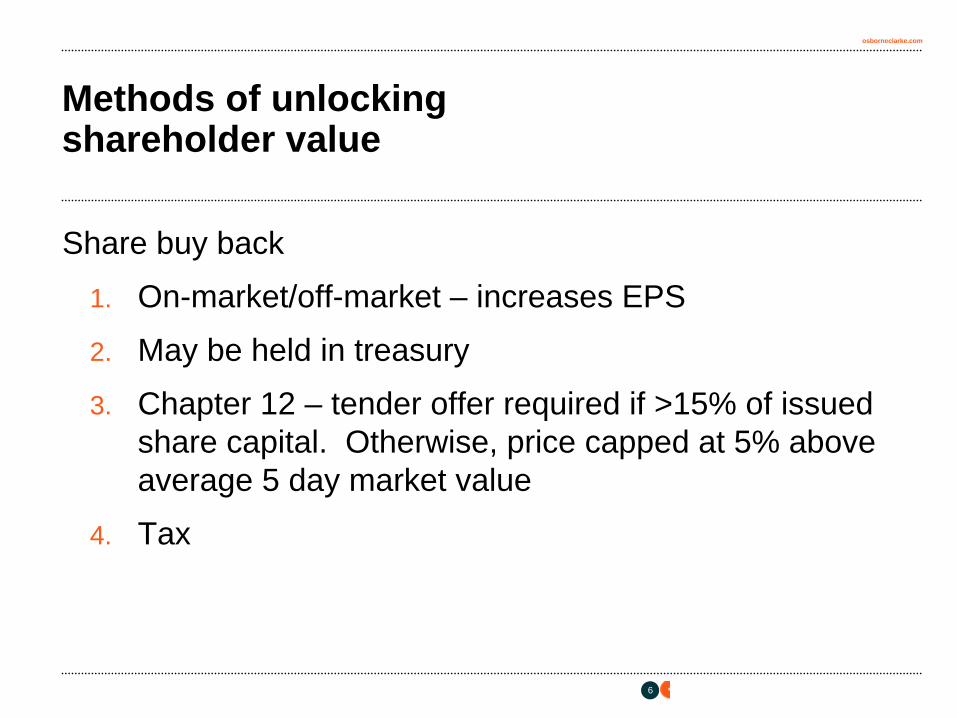

Methods of unlocking shareholder value

Share buy back

1. On-market/off-market – increases EPS

2. May be held in treasury

3. Chapter 12 – tender offer required if >15% of issued share capital. Otherwise, price capped at 5% above average 5 day market value

4. Tax

osborneclarke.com

7

Methods of unlocking shareholder value

B Share Scheme

1. Issue of shares out of capital

2. Use of share premium account or other share capital for the issue of shares

3. Combined with a special dividend?

4. Tax treatment and HMRC treatment

osborneclarke.com

8

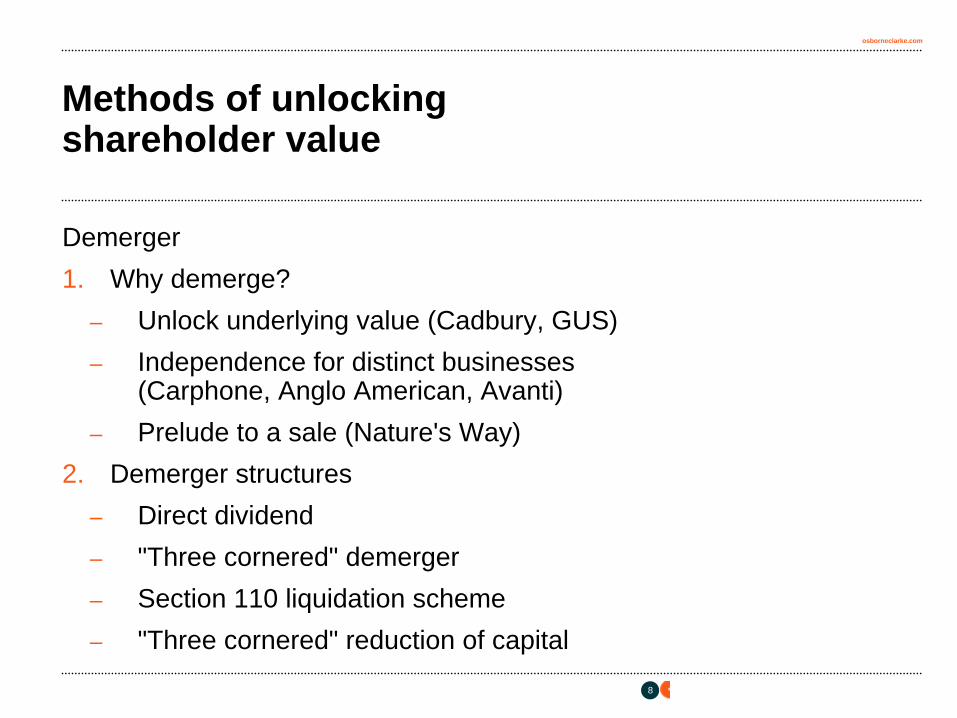

Methods of unlocking shareholder value

Demerger1. Why demerge?

– Unlock underlying value (Cadbury, GUS)– Independence for distinct businesses

(Carphone, Anglo American, Avanti)– Prelude to a sale (Nature's Way)

2. Demerger structures– Direct dividend– "Three cornered" demerger– Section 110 liquidation scheme– "Three cornered" reduction of capital

osborneclarke.com

9

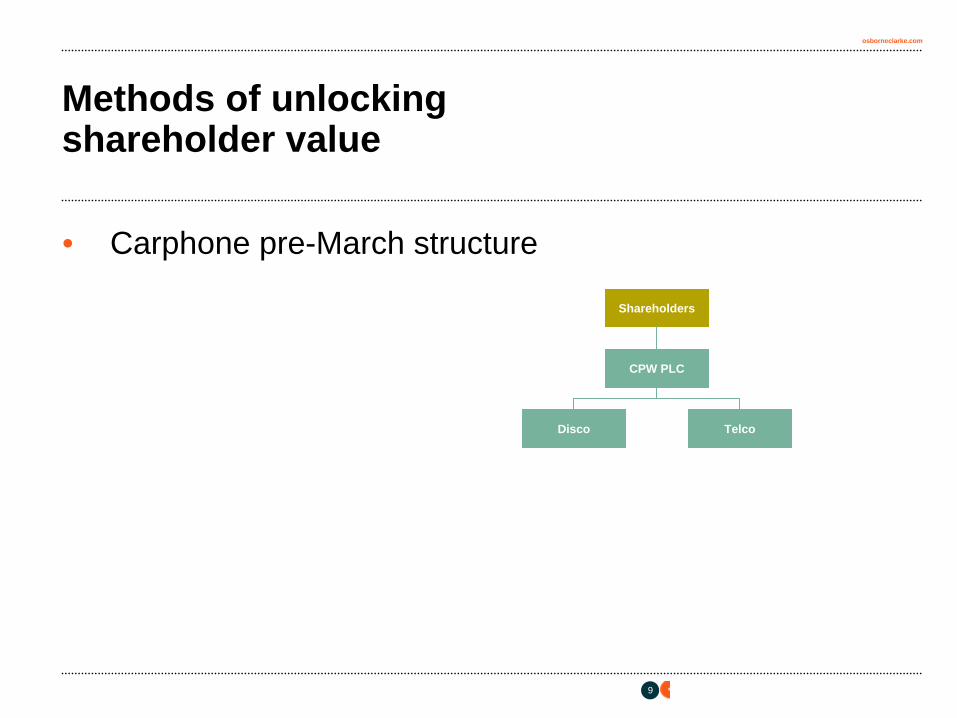

Methods of unlocking shareholder value

• Carphone pre-March structure

Shareholders

CPW PLC

TelcoDisco

Carphone Warehouse Demerger A company perspective

osborneclarke.com

11

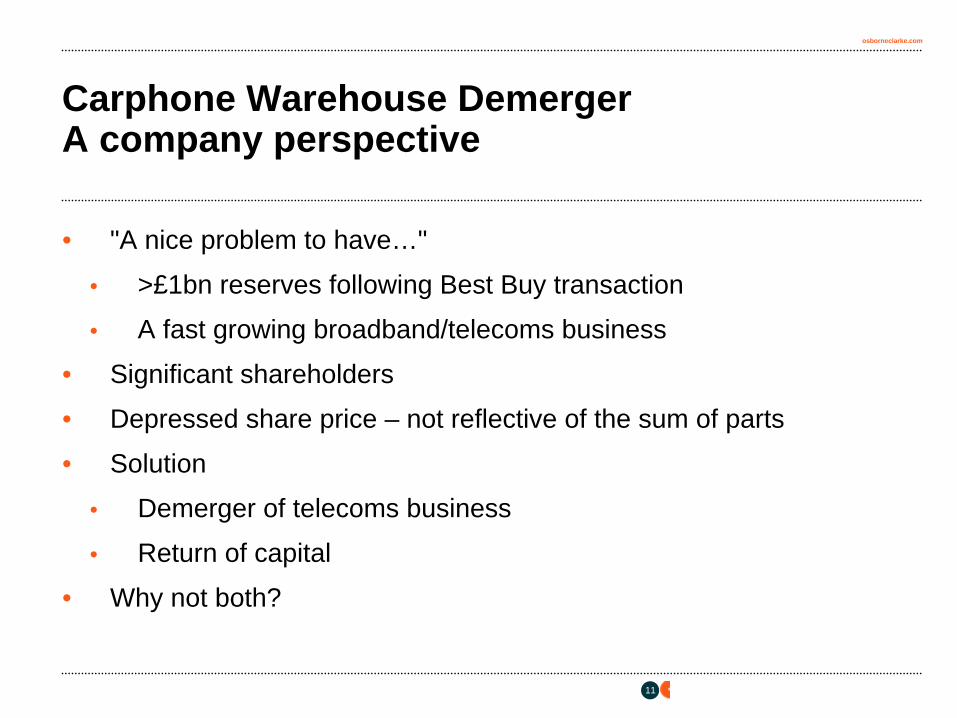

Carphone Warehouse Demerger A company perspective

• "A nice problem to have…"

• >£1bn reserves following Best Buy transaction

• A fast growing broadband/telecoms business

• Significant shareholders

• Depressed share price – not reflective of the sum of parts

• Solution

• Demerger of telecoms business

• Return of capital

• Why not both?

osborneclarke.com

12

Carphone Warehouse Demerger A company perspective

• Early restructuring

• Change of control

• Software providers/other suppliers – think ahead

• UKLA issues

• Financial reporting

• Senior management

• Share schemes

Methods of unlocking shareholder value

osborneclarke.com

14

Methods of unlocking shareholder value

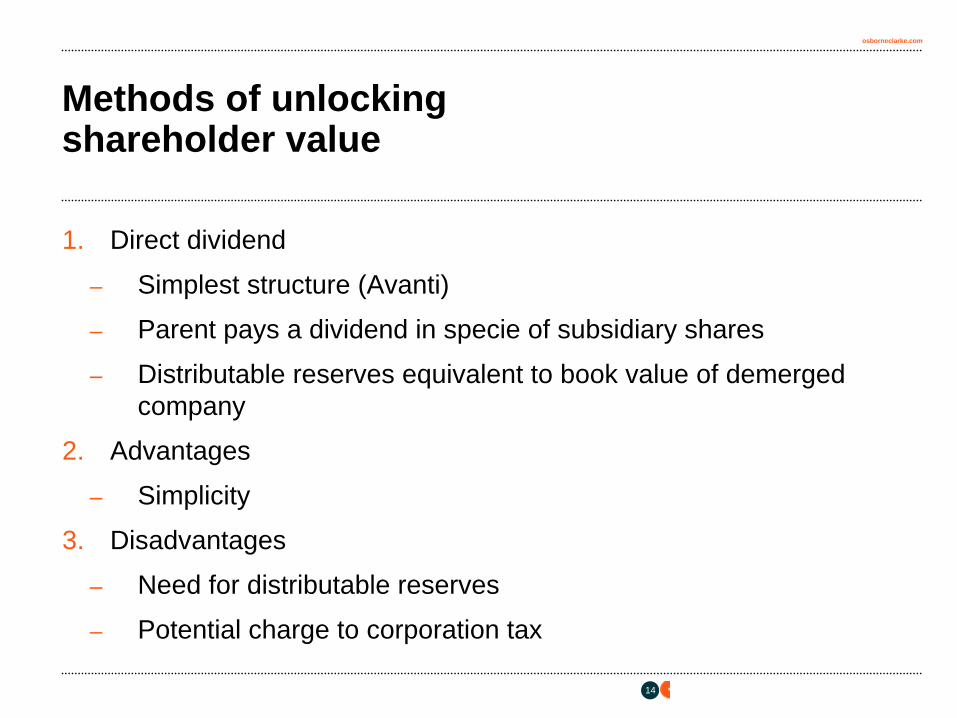

1. Direct dividend

– Simplest structure (Avanti)

– Parent pays a dividend in specie of subsidiary shares

– Distributable reserves equivalent to book value of demerged company

2. Advantages

– Simplicity

3. Disadvantages

– Need for distributable reserves

– Potential charge to corporation tax

osborneclarke.com

15

Methods of unlocking shareholder value

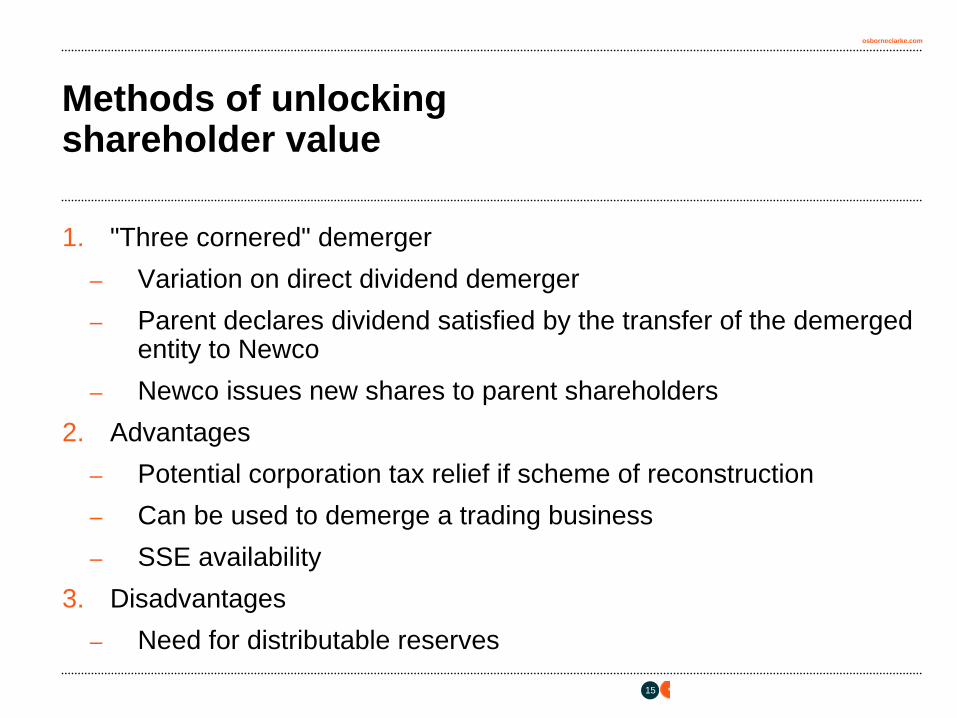

1. "Three cornered" demerger– Variation on direct dividend demerger– Parent declares dividend satisfied by the transfer of the demerged

entity to Newco– Newco issues new shares to parent shareholders

2. Advantages– Potential corporation tax relief if scheme of reconstruction– Can be used to demerge a trading business– SSE availability

3. Disadvantages– Need for distributable reserves

osborneclarke.com

16

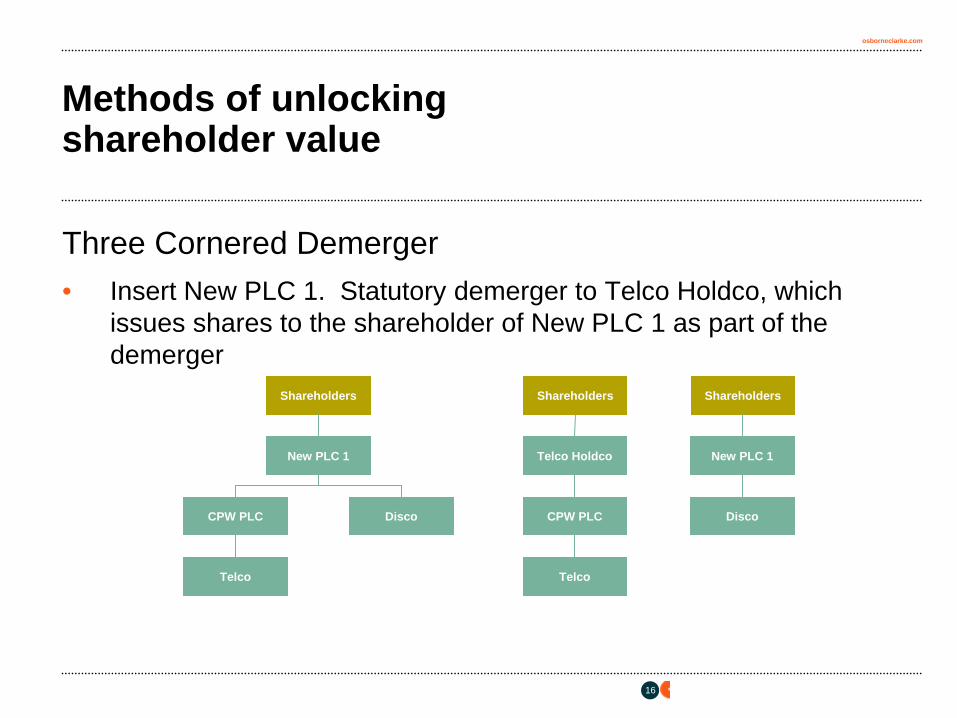

Methods of unlocking shareholder value

Three Cornered Demerger• Insert New PLC 1. Statutory demerger to Telco Holdco, which

issues shares to the shareholder of New PLC 1 as part of the demerger

Shareholders

Telco Holdco

CPW PLC

Telco

Shareholders

New PLC 1

Disco

Shareholders

New PLC 1

DiscoCPW PLC

Telco

osborneclarke.com

17

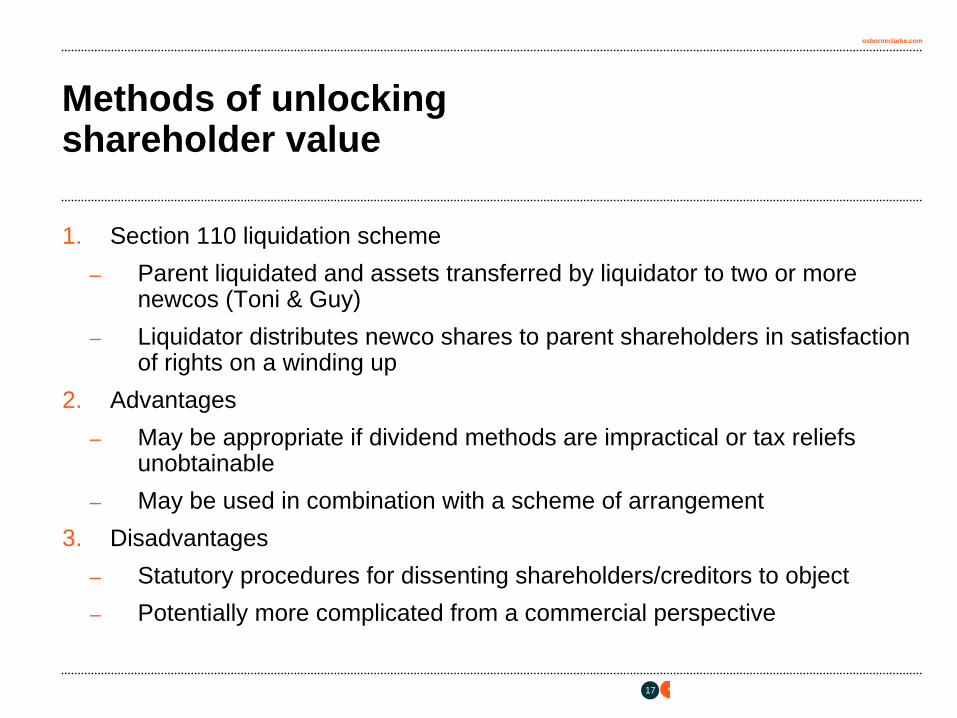

Methods of unlocking shareholder value

1. Section 110 liquidation scheme– Parent liquidated and assets transferred by liquidator to two or more

newcos (Toni & Guy)– Liquidator distributes newco shares to parent shareholders in satisfaction

of rights on a winding up2. Advantages

– May be appropriate if dividend methods are impractical or tax reliefs unobtainable

– May be used in combination with a scheme of arrangement3. Disadvantages

– Statutory procedures for dissenting shareholders/creditors to object– Potentially more complicated from a commercial perspective

osborneclarke.com

18

Methods of unlocking shareholder value

Liquidation Scheme

Shareholders

Liquidation Newco

Disco

Disco Holdco Telco Holdco

CPW PLC

Telco

Issues: A Shares

Issues: Ord shares

B shares

Transfer Disco shares

Transfer CPW PLC shares

osborneclarke.com

19

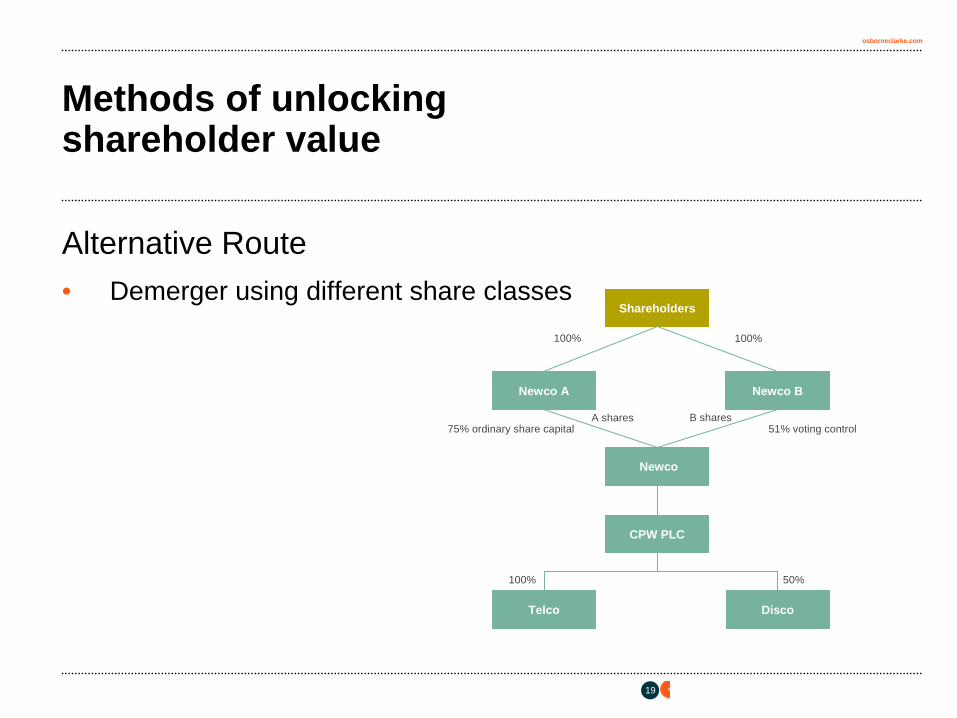

Methods of unlocking shareholder value

Alternative Route • Demerger using different share classes

Shareholders

Newco A

Newco

CPW PLC

Telco

Newco B

Disco

100%100%

B sharesA shares75% ordinary share capital 51% voting control

100% 50%

osborneclarke.com

20

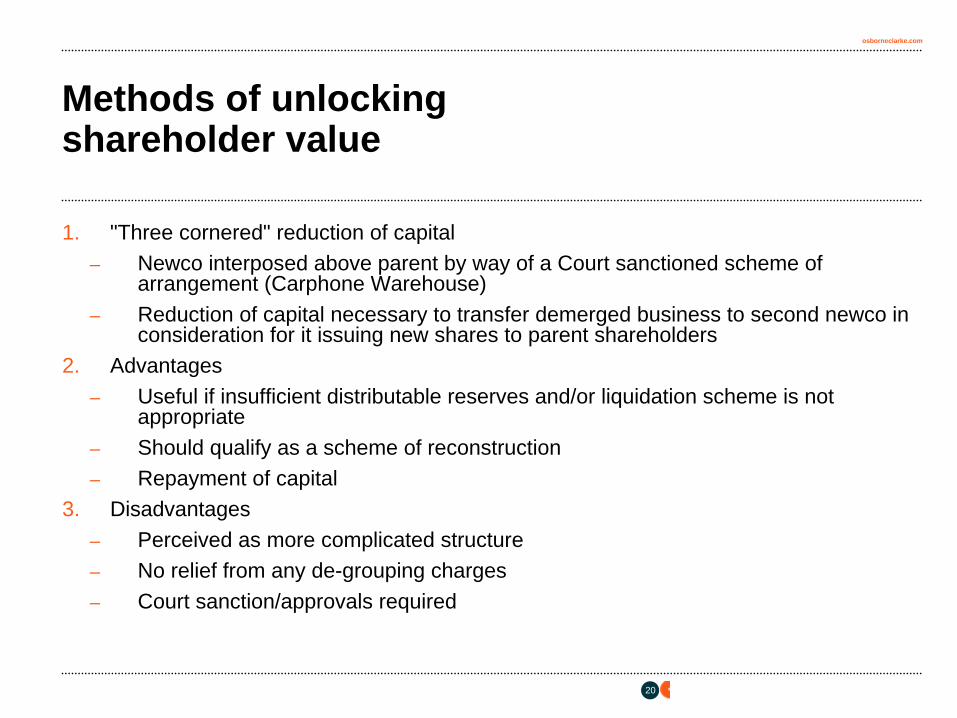

Methods of unlocking shareholder value

1. "Three cornered" reduction of capital– Newco interposed above parent by way of a Court sanctioned scheme of

arrangement (Carphone Warehouse)– Reduction of capital necessary to transfer demerged business to second newco in

consideration for it issuing new shares to parent shareholders2. Advantages

– Useful if insufficient distributable reserves and/or liquidation scheme is not appropriate

– Should qualify as a scheme of reconstruction– Repayment of capital

3. Disadvantages– Perceived as more complicated structure– No relief from any de-grouping charges– Court sanction/approvals required

osborneclarke.com

21

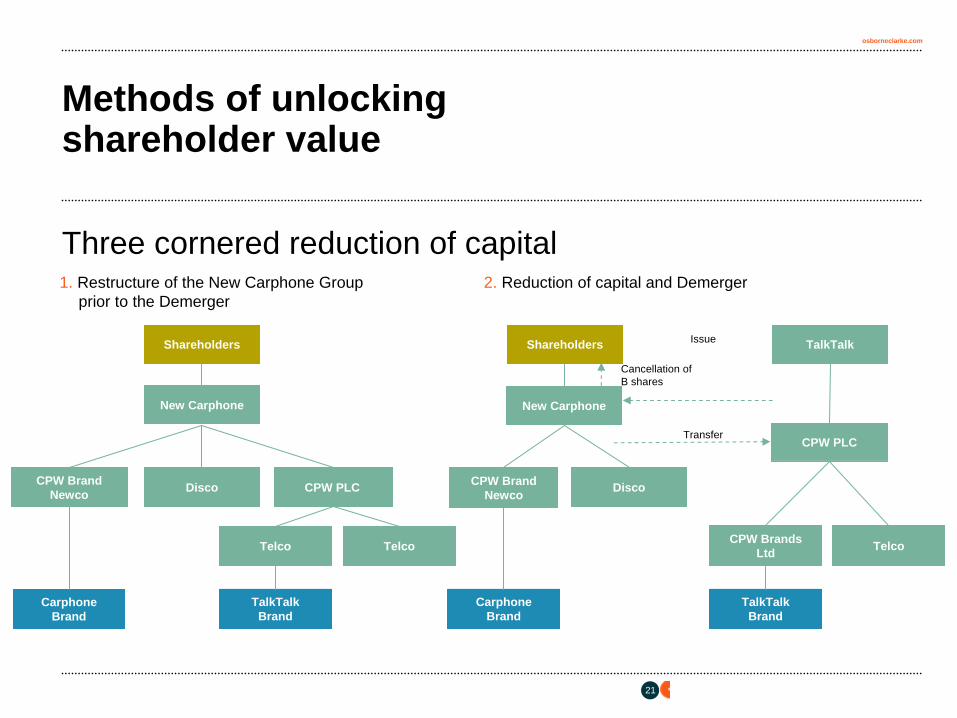

Methods of unlocking shareholder value

1. Restructure of the New Carphone Group prior to the Demerger

2. Reduction of capital and Demerger

Disco

CPW PLC

Issue

Transfer

Cancellation of B shares

CPW Brand NewcoDisco CPW PLC CPW Brand

Newco

CPW Brands Ltd

New Carphone

Shareholders

New Carphone

Shareholders TalkTalk

TelcoTelco Telco

TalkTalk Brand

Carphone Brand

TalkTalk Brand

Carphone Brand

Three cornered reduction of capital

osborneclarke.com

22

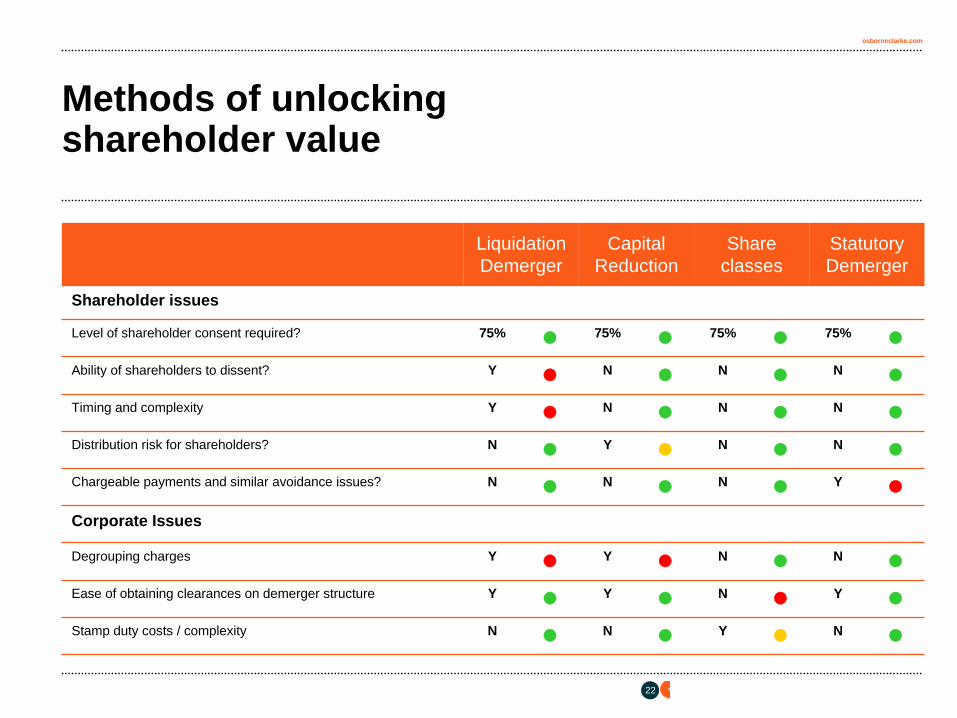

Methods of unlocking shareholder value

Liquidation Demerger

Capital Reduction

Share classes

Statutory Demerger

Shareholder issues

Level of shareholder consent required? 75% 75% 75% 75% Ability of shareholders to dissent? Y N N N Timing and complexity Y N N N Distribution risk for shareholders? N Y N N Chargeable payments and similar avoidance issues? N N N Y

Corporate Issues

Degrouping charges Y Y N N Ease of obtaining clearances on demerger structure Y Y N Y Stamp duty costs / complexity N N Y N

Carphone Warehouse The lawyers' perspective

osborneclarke.com

24

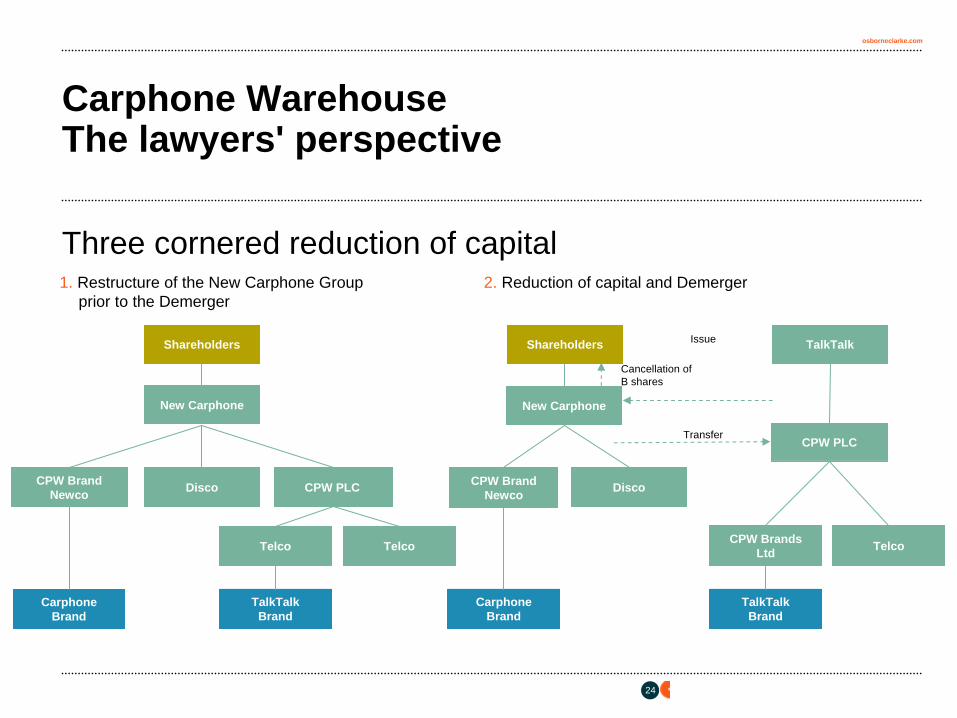

Carphone Warehouse The lawyers' perspective

1. Restructure of the New Carphone Group prior to the Demerger

2. Reduction of capital and Demerger

Disco

CPW PLC

Issue

Transfer

Cancellation of B shares

CPW Brand NewcoDisco CPW PLC CPW Brand

Newco

CPW Brands Ltd

New Carphone

Shareholders

New Carphone

Shareholders TalkTalk

TelcoTelco Telco

TalkTalk Brand

Carphone Brand

TalkTalk Brand

Carphone Brand

Three cornered reduction of capital

osborneclarke.com

25

Carphone Warehouse The lawyers' perspective

1. Structure – Three cornered reduction of capital– "New Carphone" established as holding company of Carphone by way of

a scheme of arrangement under Part 26 of the Companies Act 2006– New Carphone incorporated with two classes of ordinary share capital,

each representing the value of the retail/distribution business and the TalkTalk business respectively following the scheme

– Pre-demerger reorganisation following the scheme becoming effective– Reduction of capital accompanied by transfer of TalkTalk business to

TalkTalk Telecom plc– Capitalisation of merger reserve and further reductions of share premium

account to create distributable reserves in both listed companies2. Invest time upfront in structuring

osborneclarke.com

26

Carphone Warehouse The lawyers' perspective

• Listing issues– Eligibility – structure of "New Carphone" necessitated a Standard Listing– Voluntary adoption of Premium Listing principles but no FTSE inclusion– Documentation

• Scheme document/class 1 circular and two prospectuses – 300 others!• Financial information• Risk factors – impact on working capital statements (see List! 24)

– Project management/logistical challenges• Choose your advisers carefully….

OC Survey The results

Questions

osborneclarke.com

29

Contacts

Jonathan KingPartnerBusiness TransactionsT +44 (0) 20 7015 7046M +44 (0) 7730 731 [email protected]

Michael BellPartnerTaxT +44 (0) 117 917 4312M +44 (0) 7730 731 [email protected]

Adrian BottPartnerBusiness TransactionsT +44 (0) 20 7105 7458M +44 (0) [email protected]

[insert photo here]Height = 5.39cmWidth = 5.81cm

Thank you

Creating and Releasing Shareholder ValueTim Morris, Michael Bell & Jonathan King 20 May 2010