cowen and company 5th annual ultimate energy...

TRANSCRIPT

Jenniffer Deckard, President and Chief Executive Officer

Mark Barrus, Interim Chief Financial Officer

Sharon VanZeeland, Vice President, Investor Relations & Business Development

Cowen and Company

5th Annual Ultimate Energy Conference

December 2, 2015

Forward-Looking Statements and Non-GAAP Financial Measures

This presentation contains forward-looking statements. These statements can be identified by the use of forward-looking terminology including “will,”

“may,” “believe,” “expect,” “anticipate,” “estimate,” “continue,” or other similar words. These statements discuss future expectations including company

growth expectations, demand for our products, capacity expansion plans, market trends, commercial product launches and research and development

plans and may contain projections of financial condition or of results of operations, or state other “forward-looking” information. These forward-looking

statements involve risks and uncertainties. Many of these risks are beyond management’s control. When considering these forward-looking

statements, you should keep in mind the risk factors, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and

other cautionary statements in the company’s SEC filings. Forward-looking statements are not guarantees of future performance or an assurance that

our current assumptions or projections are valid. Our actual results and plans could differ materially from those expressed in any forward-looking

statements. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information or future events,

except as required by law.

This presentation includes certain non-GAAP financial measures, including EBITDA, Adjusted EBITDA and Adjusted EPS, and Adjusted Diluted EPS.

These non-GAAP financial measures are used as supplemental financial measures by our management to evaluate our operating performance and

compare the results of our operations from period to period without regard to the impact of our financing methods, capital structure or non-operating

income and expenses. Adjusted EBITDA is also used by our lenders to evaluate our compliance with covenants. We believe that these measures are

meaningful to our investors to enhance their understanding of our financial performance. These measures should be considered supplemental to and

not a substitute for financial information prepared in accordance with GAAP and may differ from similarly titled measures used by other companies. For

a reconciliation of such measures to the most directly comparable GAAP term, please see the slides 21-23 of this presentation.

2

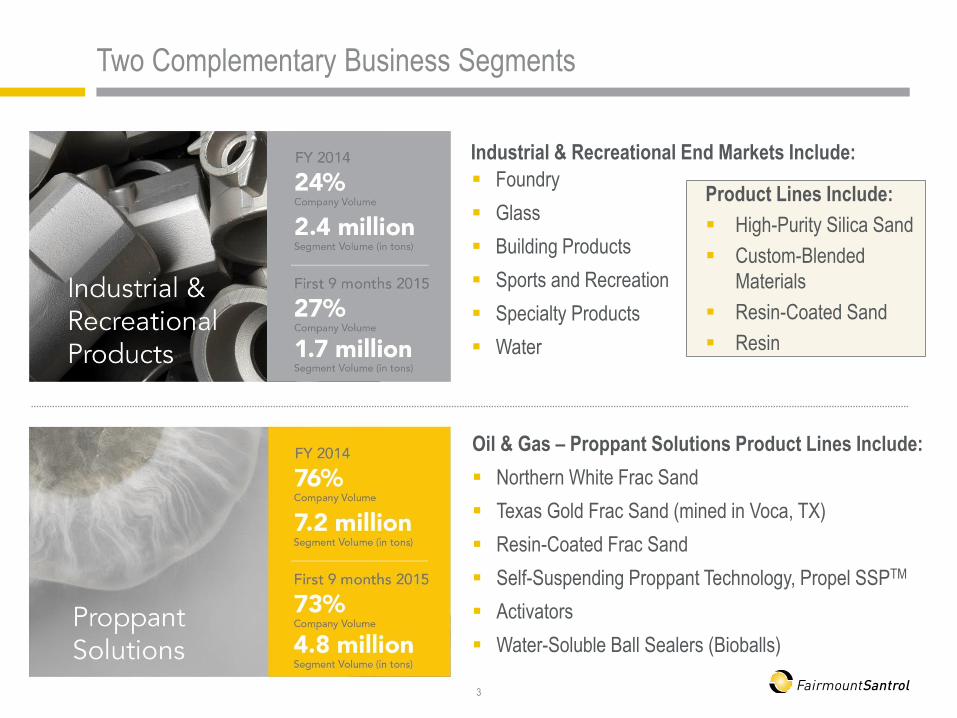

Two Complementary Business Segments

Oil & Gas – Proppant Solutions Product Lines Include:

Northern White Frac Sand

Texas Gold Frac Sand (mined in Voca, TX)

Resin-Coated Frac Sand

Self-Suspending Proppant Technology, Propel SSPTM

Activators

Water-Soluble Ball Sealers (Bioballs)

Industrial & Recreational End Markets Include:

Foundry

Glass

Building Products

Sports and Recreation

Specialty Products

Water

Product Lines Include:

High-Purity Silica Sand

Custom-Blended

Materials

Resin-Coated Sand

Resin

3

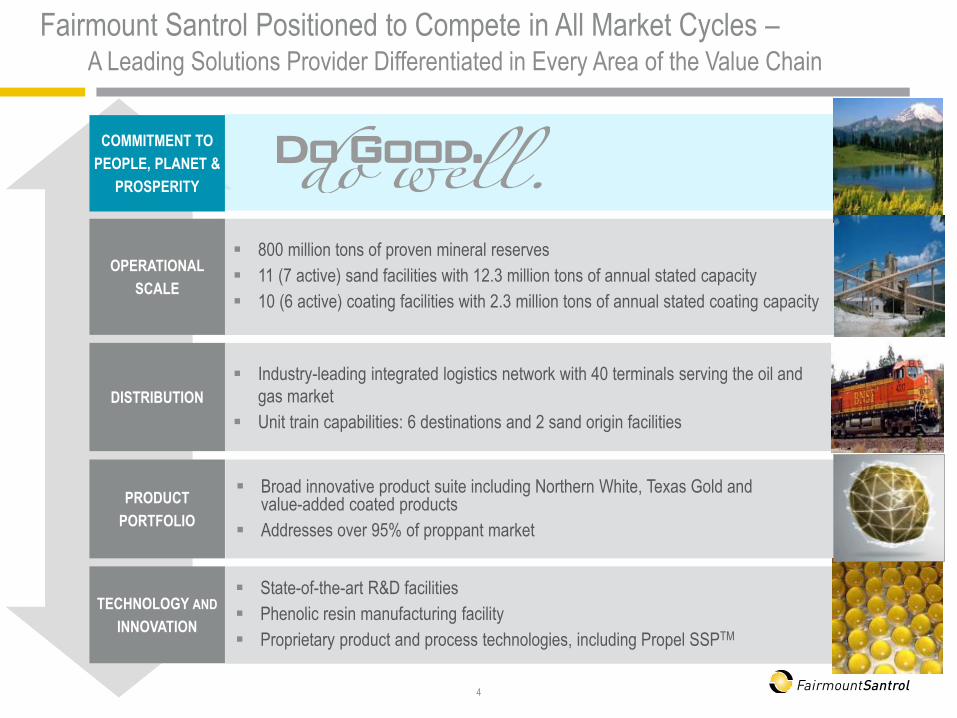

Industry-leading integrated logistics network with 40 terminals serving the oil and

gas market

Unit train capabilities: 6 destinations and 2 sand origin facilities

State-of-the-art R&D facilities

Phenolic resin manufacturing facility

Proprietary product and process technologies, including Propel SSPTM

800 million tons of proven mineral reserves

11 (7 active) sand facilities with 12.3 million tons of annual stated capacity

10 (6 active) coating facilities with 2.3 million tons of annual stated coating capacity

Broad innovative product suite including Northern White, Texas Gold and value-added coated products

Addresses over 95% of proppant market

Fairmount Santrol Positioned to Compete in All Market Cycles – A Leading Solutions Provider Differentiated in Every Area of the Value Chain

OPERATIONAL

SCALE

PRODUCT

PORTFOLIO

TECHNOLOGY AND

INNOVATION

COMMITMENT TO

PEOPLE, PLANET &

PROSPERITY

DISTRIBUTION

4

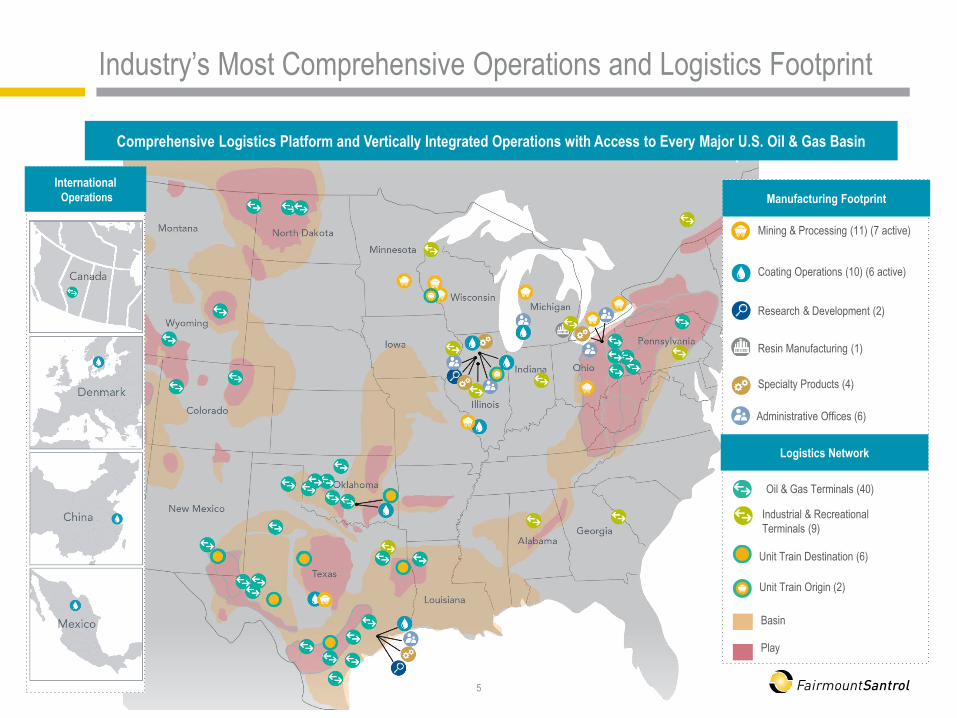

Industry’s Most Comprehensive Operations and Logistics Footprint

5

Comprehensive Logistics Platform and Vertically Integrated Operations with Access to Every Major U.S. Oil & Gas Basin

Coating Operations (10) (6 active)

Mining & Processing (11) (7 active)

Research & Development (2)

Resin Manufacturing (1)

Specialty Products (4)

Basin

Play

Oil & Gas Terminals (40)

Unit Train Destination (6)

Manufacturing Footprint

Logistics Network

Industrial & Recreational

Terminals (9)

Unit Train Origin (2)

Administrative Offices (6)

International Operations

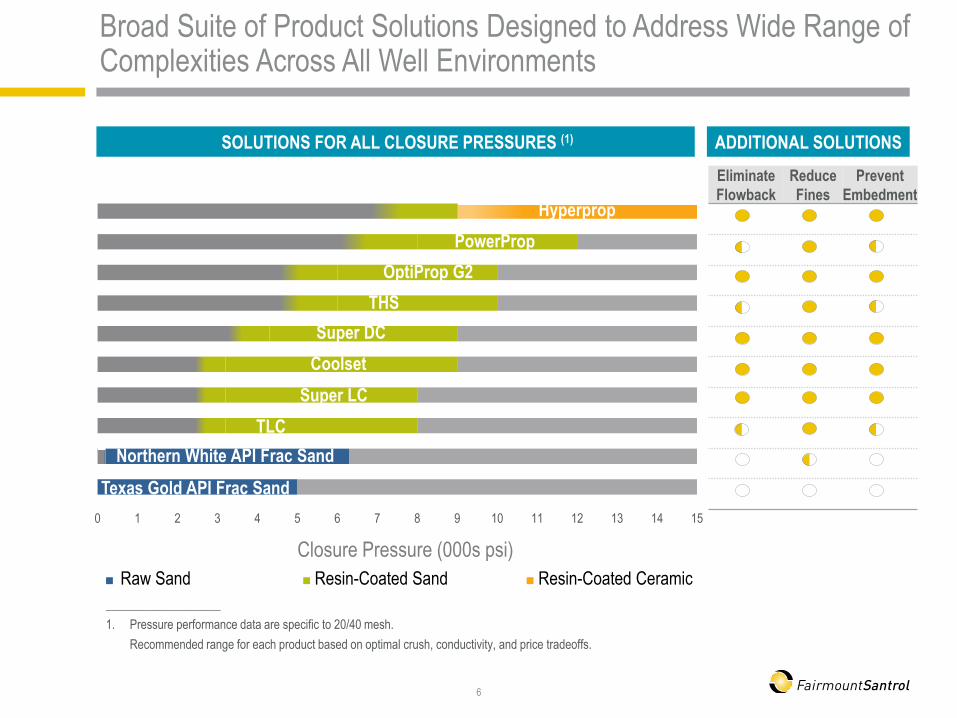

Super LC

Coolset

OptiProp G2

PowerProp

Hyperprop

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Closure Pressure (000s psi)

THS

Super DC

SOLUTIONS FOR ALL CLOSURE PRESSURES (1)

_____________________

1. Pressure performance data are specific to 20/40 mesh.

Recommended range for each product based on optimal crush, conductivity, and price tradeoffs.

Northern White API Frac Sand

Texas Gold API Frac Sand

Raw Sand Resin-Coated Sand Resin-Coated Ceramic

ADDITIONAL SOLUTIONS

Eliminate

Flowback

Reduce

Fines

Prevent

Embedment

Broad Suite of Product Solutions Designed to Address Wide Range of Complexities Across All Well Environments

6

TLC

2015-2016: Proppant Intensity Continues to Increase

7

___________________________

Sources Include public E&P presentations, internal estimates and order flow analysis

PacWest Consulting Partners The Freedonia Group

Stages Per Foot ~+10%

Proppant Per Stage ~+10%

Lateral Length

Wells per Rig

Proppant

Intensity

+20-25%

Rig Efficiencies Drilling Hours/Rig

Proppant Driver Expectations:

Lower rig counts

Greater rig efficiencies offset by

fewer hours per rig

= Flat wells per rig… but when market

rebounds, expect increasing well

count and proppant per rig as rig

utilization increases

Flat lateral length

Increased stages/foot (up ~10%)

Increased proppant/stage (up ~10%)

= Proppant intensity up 20 to 25%

2,300

2,700

3,400

4,300

Average Proppant Tons/ US Horizontal Well

1Q 2014 4Q 2014

4Q 2015 4Q 2016

+26% additional

anticipated increase

7

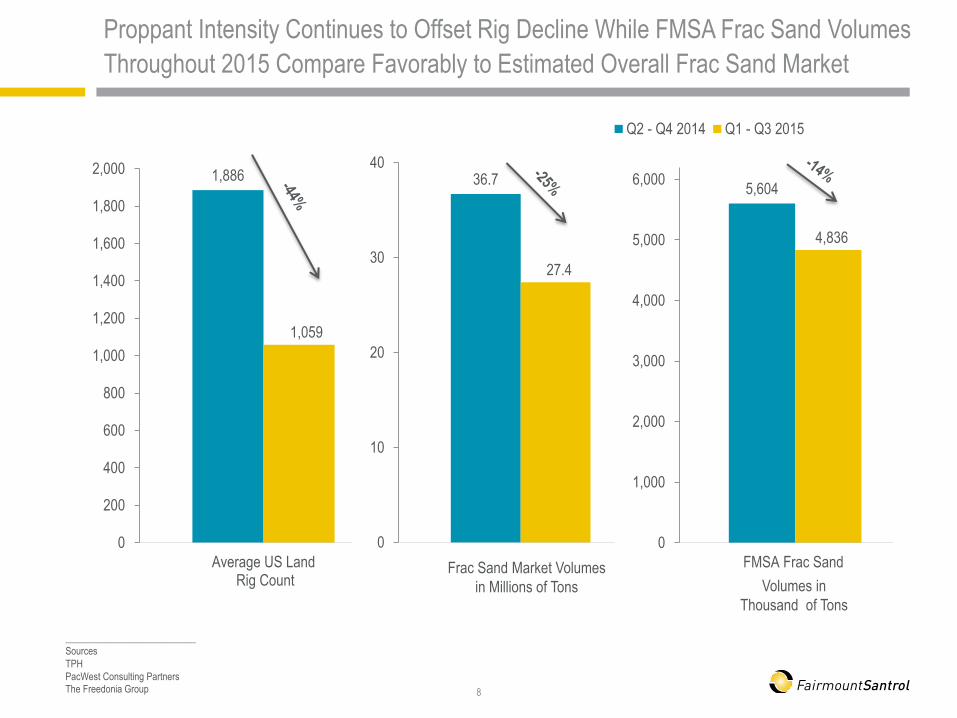

1,886

1,059

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Average US Land Rig Count

Q2 - Q4 2014 Q1 - Q3 2015

36.7

27.4

0

10

20

30

40

5,604

4,836

0

1,000

2,000

3,000

4,000

5,000

6,000

FMSA Frac Sand

Proppant Intensity Continues to Offset Rig Decline While FMSA Frac Sand Volumes

Throughout 2015 Compare Favorably to Estimated Overall Frac Sand Market

Frac Sand Market Volumes

in Millions of Tons

___________________________

Sources

TPH

PacWest Consulting Partners

The Freedonia Group 8

Volumes in

Thousand of Tons

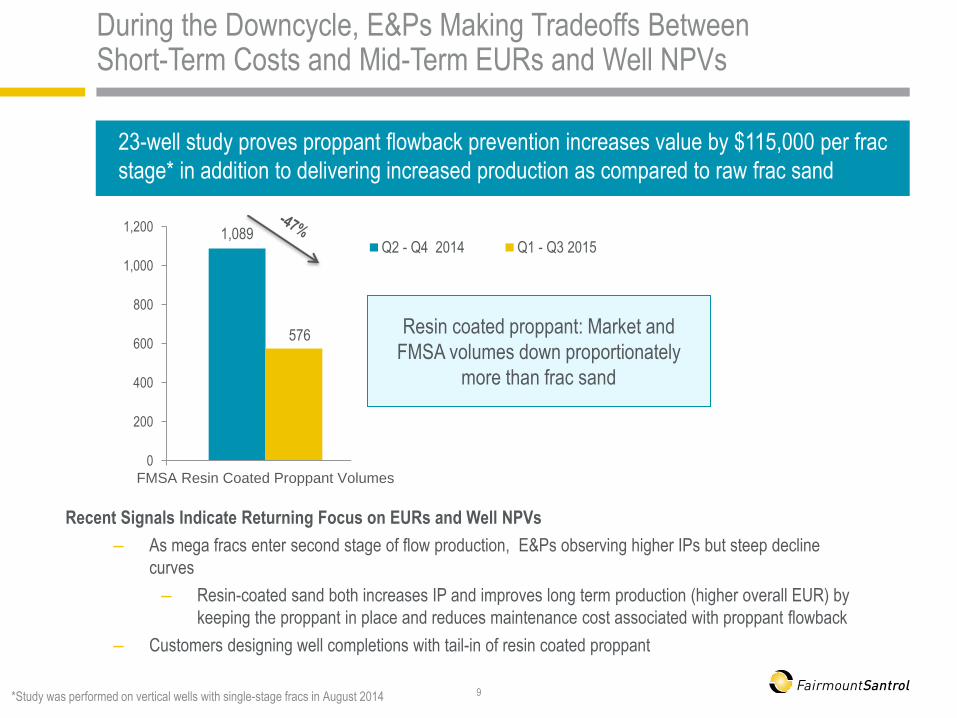

*Study was performed on vertical wells with single-stage fracs in August 2014

Resin coated proppant: Market and

FMSA volumes down proportionately

more than frac sand

During the Downcycle, E&Ps Making Tradeoffs Between Short-Term Costs and Mid-Term EURs and Well NPVs

Recent Signals Indicate Returning Focus on EURs and Well NPVs

– As mega fracs enter second stage of flow production, E&Ps observing higher IPs but steep decline

curves

– Resin-coated sand both increases IP and improves long term production (higher overall EUR) by

keeping the proppant in place and reduces maintenance cost associated with proppant flowback

– Customers designing well completions with tail-in of resin coated proppant

1,089

576

0

200

400

600

800

1,000

1,200

FMSA Resin Coated Proppant Volumes

Q2 - Q4 2014 Q1 - Q3 2015

23-well study proves proppant flowback prevention increases value by $115,000 per frac

stage* in addition to delivering increased production as compared to raw frac sand

9

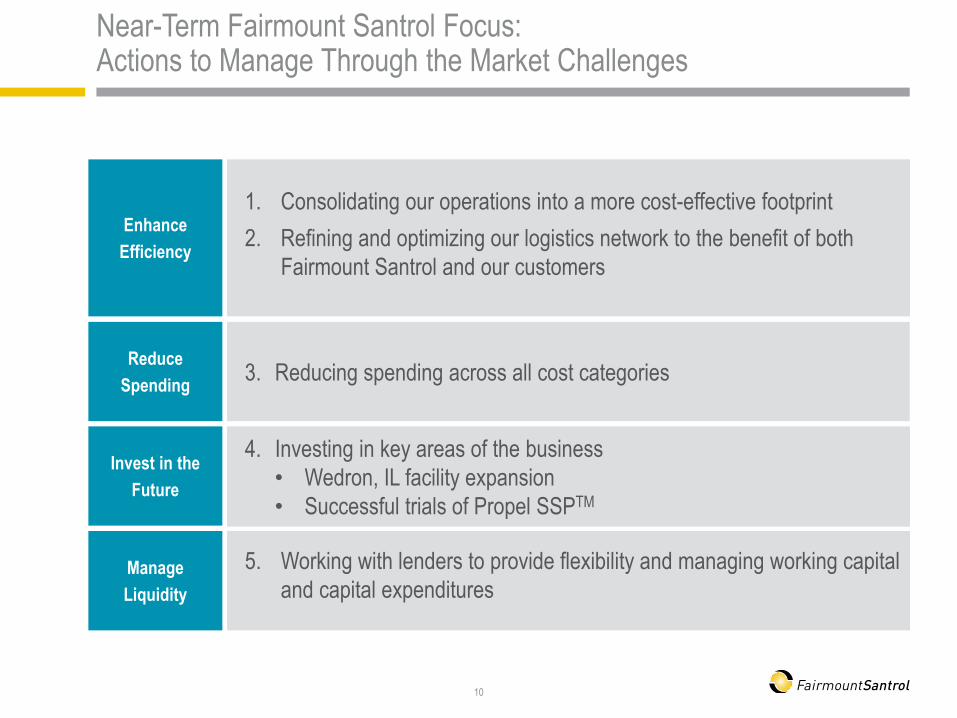

Near-Term Fairmount Santrol Focus: Actions to Manage Through the Market Challenges

10

1. Consolidating our operations into a more cost-effective footprint

2. Refining and optimizing our logistics network to the benefit of both

Fairmount Santrol and our customers

3. Reducing spending across all cost categories

4. Investing in key areas of the business

• Wedron, IL facility expansion

• Successful trials of Propel SSPTM

5. Working with lenders to provide flexibility and managing working capital

and capital expenditures

Enhance

Efficiency

Reduce

Spending

Invest in the

Future

Manage

Liquidity

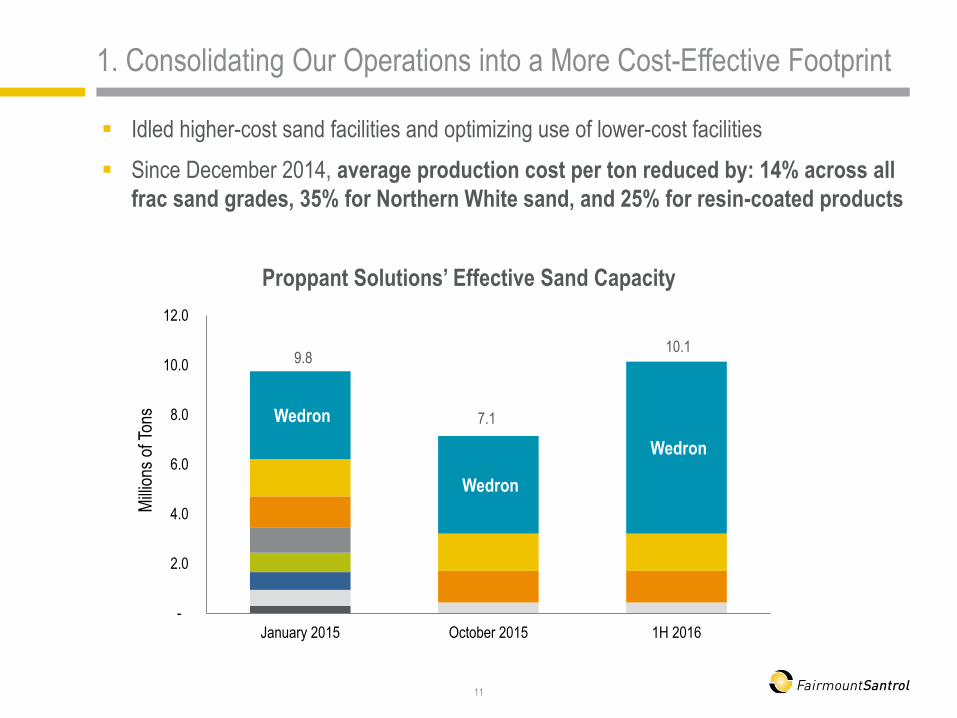

1. Consolidating Our Operations into a More Cost-Effective Footprint

Idled higher-cost sand facilities and optimizing use of lower-cost facilities

Since December 2014, average production cost per ton reduced by: 14% across all

frac sand grades, 35% for Northern White sand, and 25% for resin-coated products

11

Wedron

Wedron

Wedron

-

2.0

4.0

6.0

8.0

10.0

12.0

January 2015 October 2015 1H 2016

Mill

ions

of T

ons

9.8

7.1

10.1

Proppant Solutions’ Effective Sand Capacity

FMSA Terminal

FMSA Active Proppant

Solutions Mining & Processing

Unit Train Destination

Unit Train Origin

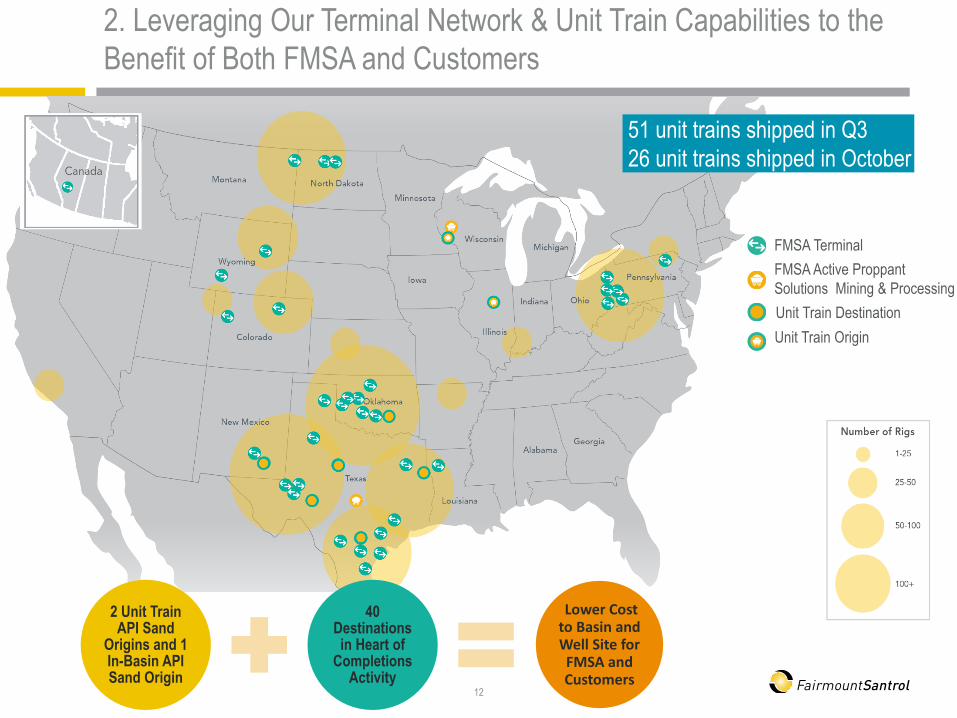

2 Unit Train API Sand

Origins and 1 In-Basin API Sand Origin

40 Destinations in Heart of

Completions Activity

Lower Cost to Basin and Well Site for FMSA and Customers

2. Leveraging Our Terminal Network & Unit Train Capabilities to the

Benefit of Both FMSA and Customers

12

51 unit trains shipped in Q3

26 unit trains shipped in October

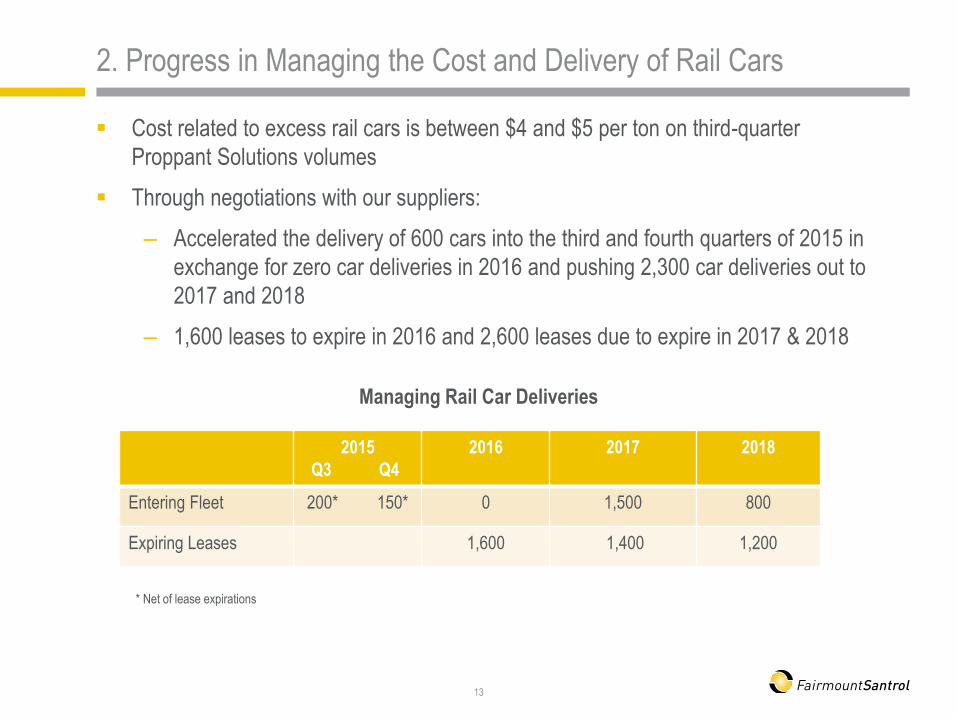

2. Progress in Managing the Cost and Delivery of Rail Cars

Cost related to excess rail cars is between $4 and $5 per ton on third-quarter

Proppant Solutions volumes

Through negotiations with our suppliers:

– Accelerated the delivery of 600 cars into the third and fourth quarters of 2015 in

exchange for zero car deliveries in 2016 and pushing 2,300 car deliveries out to

2017 and 2018

– 1,600 leases to expire in 2016 and 2,600 leases due to expire in 2017 & 2018

13

Managing Rail Car Deliveries

2015

Q3 Q4

2016 2017 2018

Entering Fleet 200* 150* 0 1,500 800

Expiring Leases 1,600 1,400 1,200

* Net of lease expirations

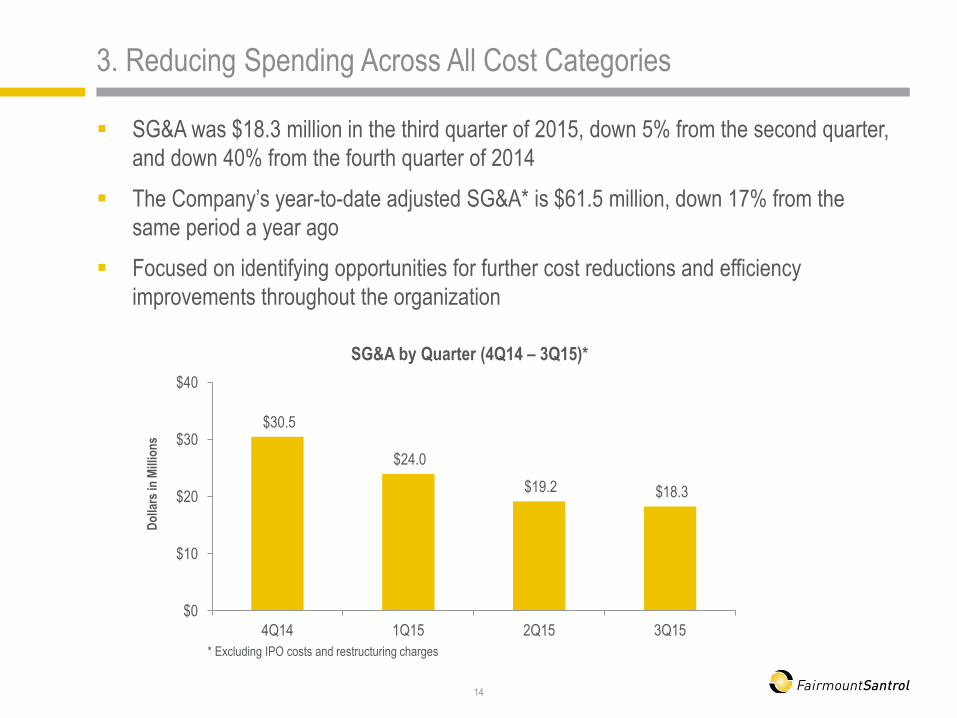

3. Reducing Spending Across All Cost Categories

SG&A was $18.3 million in the third quarter of 2015, down 5% from the second quarter,

and down 40% from the fourth quarter of 2014

The Company’s year-to-date adjusted SG&A* is $61.5 million, down 17% from the

same period a year ago

Focused on identifying opportunities for further cost reductions and efficiency

improvements throughout the organization

14

$30.5

$24.0

$19.2 $18.3

$0

$10

$20

$30

$40

4Q14 1Q15 2Q15 3Q15

SG&A by Quarter (4Q14 – 3Q15)*

Do

llars

in M

illio

ns

* Excluding IPO costs and restructuring charges

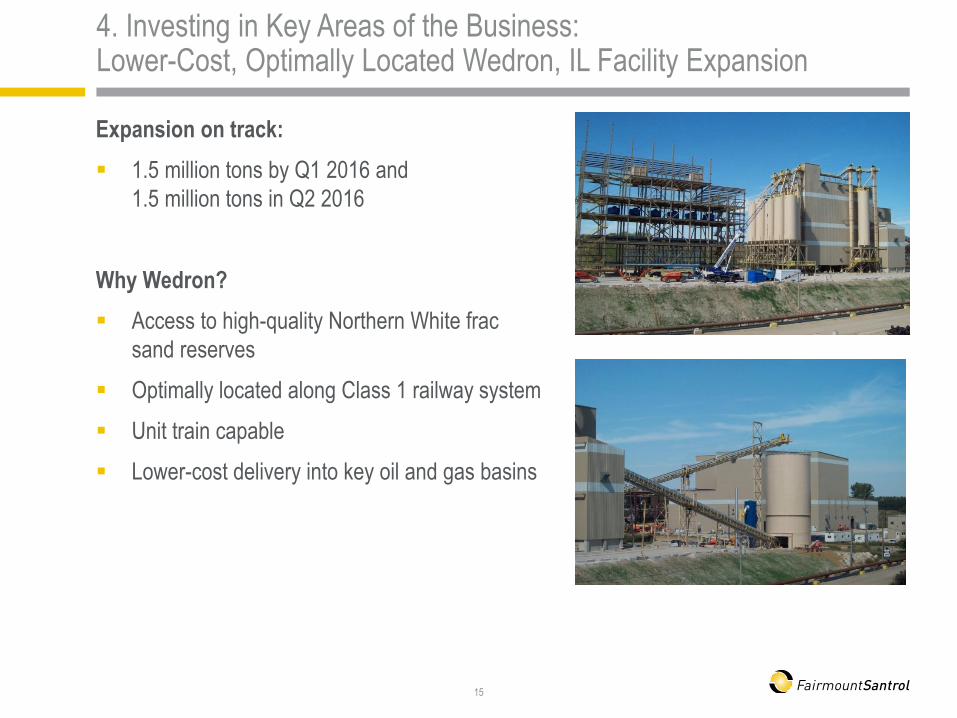

4. Investing in Key Areas of the Business: Lower-Cost, Optimally Located Wedron, IL Facility Expansion

Expansion on track:

1.5 million tons by Q1 2016 and

1.5 million tons in Q2 2016

Why Wedron?

Access to high-quality Northern White frac

sand reserves

Optimally located along Class 1 railway system

Unit train capable

Lower-cost delivery into key oil and gas basins

15

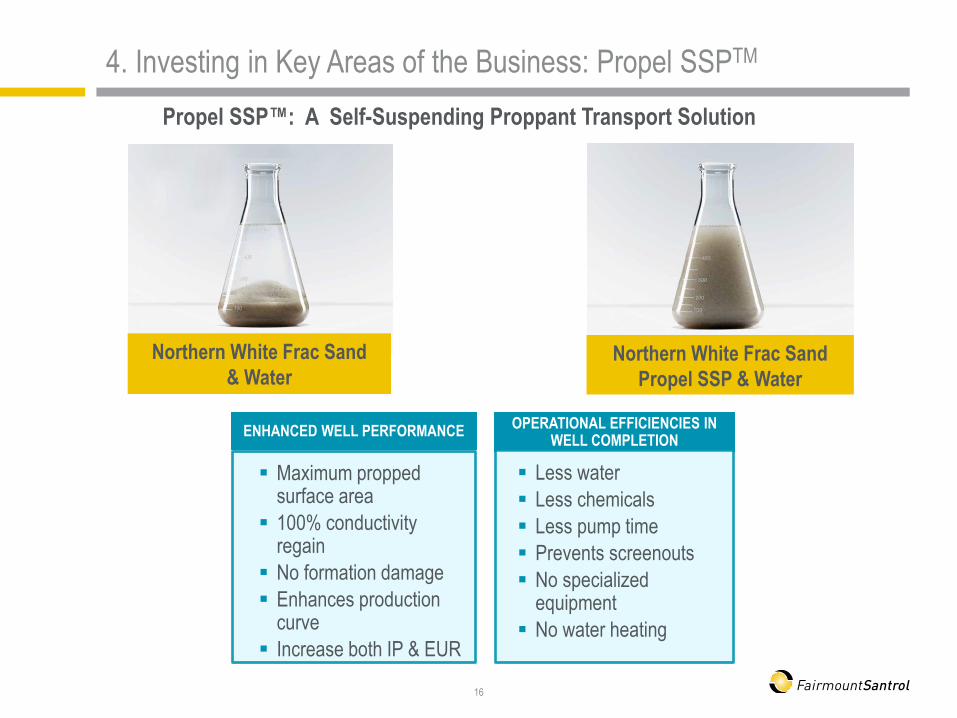

ENHANCED WELL PERFORMANCE

Maximum propped surface area

100% conductivity regain

No formation damage

Enhances production curve

Increase both IP & EUR

OPERATIONAL EFFICIENCIES IN WELL COMPLETION

Less water

Less chemicals

Less pump time

Prevents screenouts

No specialized equipment

No water heating

4. Investing in Key Areas of the Business: Propel SSPTM

16

Propel SSP™: A Self-Suspending Proppant Transport Solution

Northern White Frac Sand

& Water Northern White Frac Sand

Propel SSP & Water

Customer Adoption

Multiple customers plan to continue use of Propel SSP™ through 2016

Backed by Results of Recent Six-Well Field Trial in North Dakota’s Williston Basin

Increased 90-day cumulative oil production 39% compared with the geologic

offset wells

Specifically, in areas with lower porosity and permeability, production improved

more than 80%

Improved efficiency by not requiring fluid heating at 35° F and above

4. Increased Production and Operational Efficiency Drive Customer Adoption of Propel SSP™

17

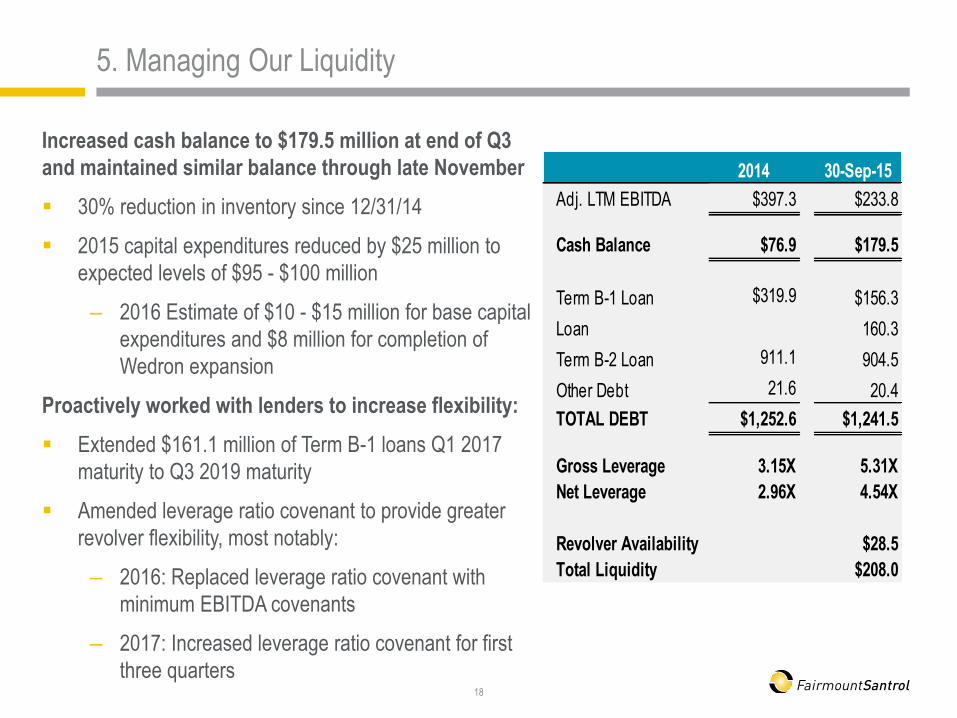

5. Managing Our Liquidity

Increased cash balance to $179.5 million at end of Q3

and maintained similar balance through late November

30% reduction in inventory since 12/31/14

2015 capital expenditures reduced by $25 million to

expected levels of $95 - $100 million

– 2016 Estimate of $10 - $15 million for base capital

expenditures and $8 million for completion of

Wedron expansion

Proactively worked with lenders to increase flexibility:

Extended $161.1 million of Term B-1 loans Q1 2017

maturity to Q3 2019 maturity

Amended leverage ratio covenant to provide greater

revolver flexibility, most notably:

– 2016: Replaced leverage ratio covenant with

minimum EBITDA covenants

– 2017: Increased leverage ratio covenant for first

three quarters

18

2014 30-Sep-15

Adj. LTM EBITDA $397.3 $233.8

Cash Balance $76.9 $179.5

Term B-1 Loan $319.9 $156.3 Extended Term B-1

Loan 160.3

Term B-2 Loan 911.1 904.5

Other Debt 21.6 20.4

TOTAL DEBT $1,252.6 $1,241.5

Gross Leverage 3.15X 5.31X

Net Leverage 2.96X 4.54X

Revolver Availability $28.5

Total Liquidity $208.0

Scalability and flexibility of

sand and valued added

coated product offerings to

match market needs

Advantaged distribution

network with key unit train

origins and destinations

Fairmount Santrol Positioned to Compete in All Market Cycles – A Leading Solutions Provider Differentiated in Every Area of the Value Chain

19

OPERATIONAL

SCALE

PRODUCT

PORTFOLIO

TECHNOLOGY AND

INNOVATION

COMMITMENT TO

PEOPLE, PLANET &

PROSPERITY

DISTRIBUTION

Tightly managing costs

and efficiencies in the

near-term

Selectively investing in

key areas that will best

position us today and for

the eventual recovery

Proactively managing

our liquidity and debt

structure

Enhance

Efficiency

Reduce

Spending

Invest in the

Future

Manage

Liquidity

Short to Mid-term Focus in Downcycle Customers Value our

Differentiated Business Model

Thank You & Questions

www.FairmountSantrol.com

20

Appendix: Reconciliation of Non-GAAP Financial Measures

21

Appendix: Reconciliation of Non-GAAP Financial Measures

22

Appendix: Reconciliation of Non-GAAP Financial Measures

23

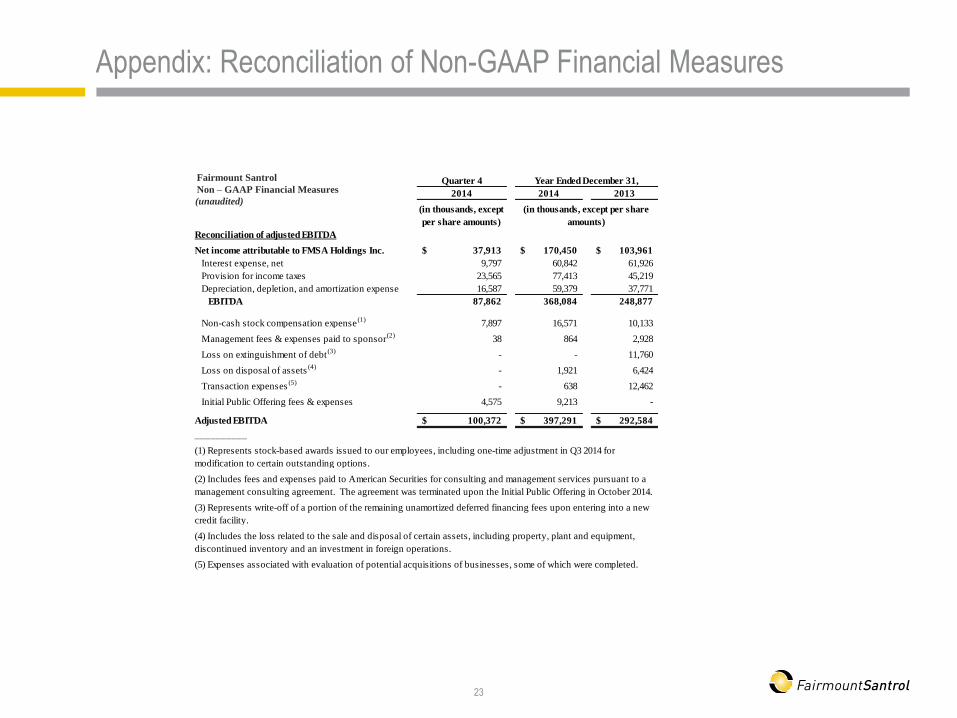

Quarter 4

2014 2014 2013

Reconciliation of adjusted EBITDA

Net income attributable to FMSA Holdings Inc. 37,913$ 170,450$ 103,961$

Interest expense, net 9,797 60,842 61,926

Provision for income taxes 23,565 77,413 45,219

Depreciation, depletion, and amortization expense 16,587 59,379 37,771

EBITDA 87,862 368,084 248,877

Non-cash stock compensation expense(1)

7,897 16,571 10,133

Management fees & expenses paid to sponsor(2)

38 864 2,928

Loss on extinguishment of debt(3)

- - 11,760

Loss on disposal of assets(4)

- 1,921 6,424

Transaction expenses(5)

- 638 12,462

Initial Public Offering fees & expenses 4,575 9,213 -

Adjusted EBITDA 100,372$ 397,291$ 292,584$

__________

(5) Expenses associated with evaluation of potential acquisitions of businesses, some of which were completed.

(4) Includes the loss related to the sale and disposal of certain assets, including property, plant and equipment,

discontinued inventory and an investment in foreign operations.

(in thousands, except

per share amounts)

(in thousands, except per share

amounts)

Year Ended December 31,

(3) Represents write-off of a portion of the remaining unamortized deferred financing fees upon entering into a new

credit facility.

(1) Represents stock-based awards issued to our employees, including one-time adjustment in Q3 2014 for

modification to certain outstanding options.

(2) Includes fees and expenses paid to American Securities for consulting and management services pursuant to a

management consulting agreement. The agreement was terminated upon the Initial Public Offering in October 2014.

(unaudited)

Fairmount Santrol

Non – GAAP Financial Measures