corporate governance practices of u.s. s initial public ... · board size at ipo ... corporate...

TRANSCRIPT

Corporate GovernancePractices of U.S. Initial Public Offerings(Controlled Companies Only)

October 2011

Davis Polk & Wardwell llP

IPO

Go

vern

ance

Sur

vey

Table of Contents

Overview ..........................................................................................................................................1

The Companies ...............................................................................................................................1

Significant Findings..........................................................................................................................2

Primary Listing Exchange ................................................................................................................3

Classes of Outstanding Common Stock at IPO ..............................................................................4

Board Size at IPO............................................................................................................................4

Level of Board Independence at IPO ..............................................................................................5

Classified Board at IPO ...................................................................................................................5

Separation of Chairman and CEO...................................................................................................6

Lead Director ...................................................................................................................................6

Audit Committee Financial Experts at IPO ......................................................................................7

Audit Committee Independence at IPO...........................................................................................8

Voting in Uncontested Board Elections ...........................................................................................9

Supermajority Vote for Amending the Charter and Bylaws ...........................................................10

Poison Pills and Blank Check Preferred Stock..............................................................................11

Exclusive Forum Provisions...........................................................................................................12

Compensation Consultants............................................................................................................13

Shareholder Action by Written Consent.........................................................................................14

OverviewAs an advisor to underwriters and issuers in initial public offerings, we surveyed the corporate

governance practices of recent U.S. IPOs to identify current market trends. We focused on the top 50

IPOs of U.S. companies from January 1, 2009 through August 31, 2011 in terms of deal size of the IPO.*

Of those top 50 IPOs, 28 were “controlled companies,” as defined under the NYSE and NASDAQ listing

standards. Because controlled companies are exempt from certain NYSE and NASDAQ board and

committee independence requirements, we examined the corporate governance provisions at these

companies separately from those of noncontrolled companies. The deal size of the examined IPOs of

controlled companies ranged from $239.95 million to $4.35 billion.

The CompaniesWe examined the following 28 controlled companies, spanning 20 industries:

1

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Aeroflex Holding Corp.

Apollo Global Management LLC

Bankrate Inc.

Booz Allen Hamilton Hldg. Corp.

Cobalt Intl Energy, Inc.**

Dole Food Co. Inc.

Dollar General Corp.

Dunkin’ Brands Group, Inc.

Education Management Corp.

Emdeon Inc.**

Express Inc.

The Fresh Market Inc.

FXCM Inc.

Generac Holdings Inc.

GNC Holdings Inc.

HCA Holdings, Inc.

Hyatt Hotels Corp.

KAR Auction Services, Inc.

Kinder Morgan Inc.

LPL Investment Holdings Inc.

Mead Johnson Nutrition Co.**

Metals USA Holdings Corp.

Oasis Petroleum Inc.

RailAmerica, Inc.

Select Medical Holdings Corp.**

Talecris Biotherapeutics Holdings

Vanguard Health Systems, Inc.

Wesco Aircraft Holdings, Inc.**

* Excludes limited partnerships, REITs, trusts and blank check companies.

**Davis Polk & Wardwell participated in the IPO.

Significant FindingsIn comparing the corporate governance provisions at “controlled companies” versus those we surveyed

at noncontrolled companies, we noted some key differences, including:

■ 82% of controlled companies were listed on the NYSE versus 52% of noncontrolled companies.

■ 64% of controlled companies had a classified board as compared to 78% of noncontrolled

companies.

■ The average level of director independence at controlled companies was 39% versus 74% at

noncontrolled companies.

■ 4% of controlled companies had a lead director as compared to 26% of noncontrolled

companies.

■ 50% of controlled companies had fully independent audit committees at the time of their IPO

versus 78% of noncontrolled companies.

■ 26% of controlled companies had an exclusive forum provision as compared to 14% of

noncontrolled companies.

■ 54% of controlled companies permitted shareholder action by written consent versus 10% of

noncontrolled companies.

2

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

3

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

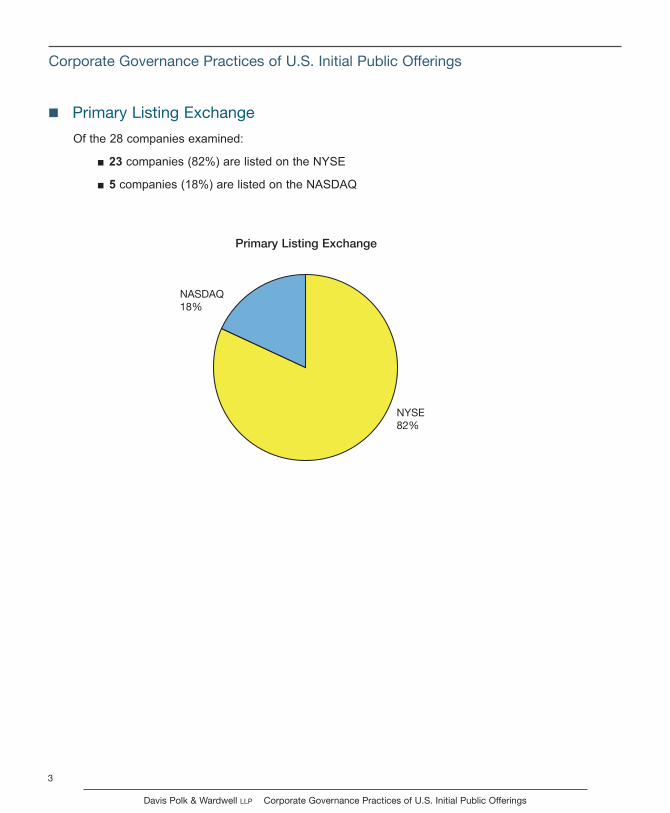

Primary listing Exchange

Of the 28 companies examined:

■ 23 companies (82%) are listed on the NYSE

■ 5 companies (18%) are listed on the NASDAQ

NASDAQ18%

NYSE82%

Primary Listing Exchange

Classes of Outstanding Common Stock at IPO

Of the 28 companies examined:

■ 20 companies (72%) had one class of outstanding common stock

■ 6 companies (21%) had two classes of outstanding common stock

■ 2 companies (7%) had four classes of outstanding common stock

Board Size at IPO

Of the 28 companies examined:

■ The average board size was 9

■ The median board size was 9

■ The board sizes ranged from 5 to 15 members

■ There is no distinct correlation between deal size and board size

6

2

20

0

5

10

15

20

25

One Class Two Classes Four Classes

4

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

0 1,000 2,000 3,000 4,000 5,00002468101214161820

Deal Size vs. Board Size

Bo

ard

Siz

e

Classes of Outstanding Common Stock

Deal Size($ millions)

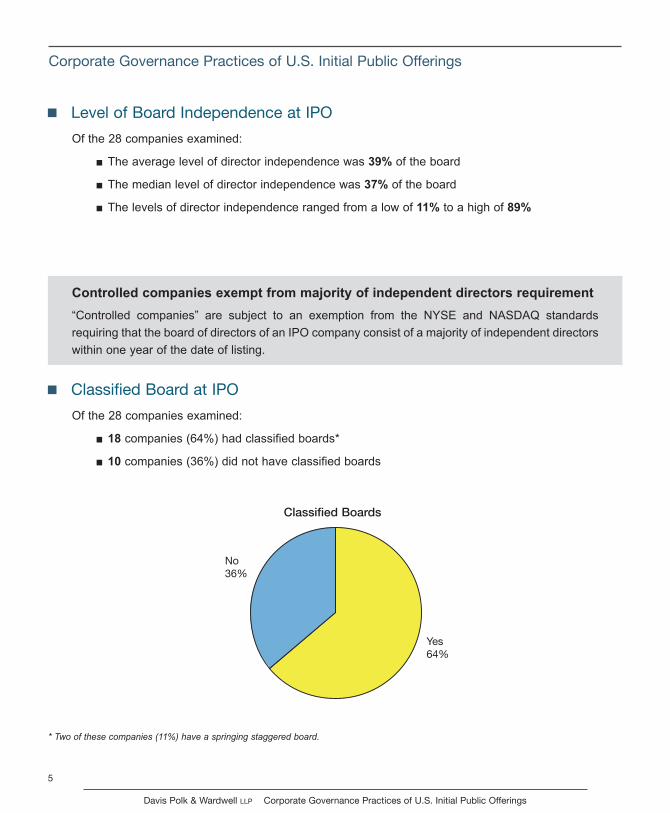

level of Board Independence at IPO

Of the 28 companies examined:

■ The average level of director independence was 39% of the board

■ The median level of director independence was 37% of the board

■ The levels of director independence ranged from a low of 11% to a high of 89%

Controlled�companies�exempt�from�majority�of�independent�directors�requirement

“Controlled companies” are subject to an exemption from the NYSE and NASDAQ standards

requiring that the board of directors of an IPO company consist of a majority of independent directors

within one year of the date of listing.

Classified Board at IPO

Of the 28 companies examined:

■ 18 companies (64%) had classified boards*

■ 10 companies (36%) did not have classified boards

*�Two�of�these�companies�(11%)�have�a�springing�staggered�board.

5

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Classified Boards

No36%

Yes64%

6

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

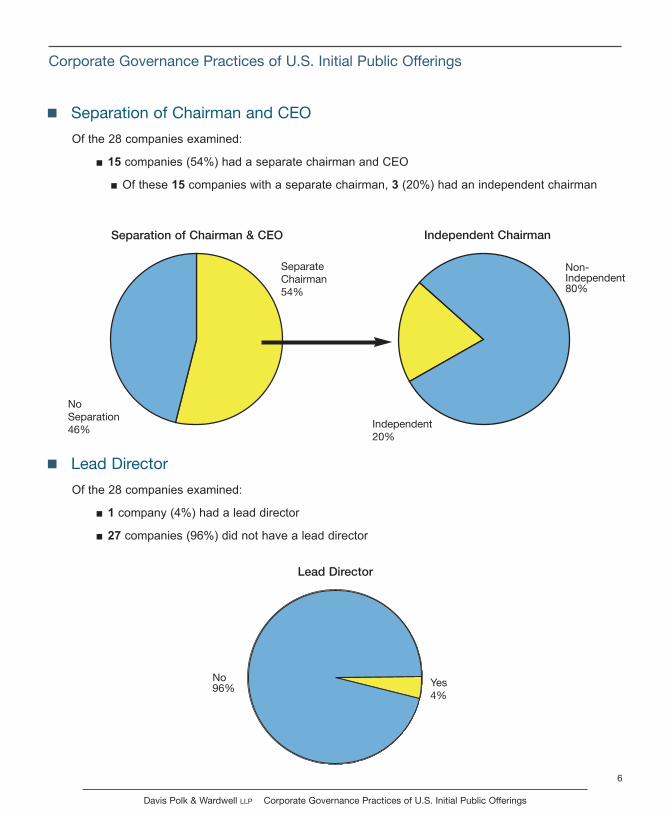

Separation of Chairman and CEO

Of the 28 companies examined:

■ 15 companies (54%) had a separate chairman and CEO

■ Of these 15 companies with a separate chairman, 3�(20%) had an independent chairman

lead Director

Of the 28 companies examined:

■ 1�company (4%) had a lead director

■ 27�companies (96%) did not have a lead director

Separation of Chairman & CEO Independent Chairman

Independent20%

Non-Independent80%

SeparateChairman54%

NoSeparation46%

Lead Director

Yes4%

No96%

Audit Committee Financial Experts at IPO

Of the 28 companies examined:

■ 21 companies (75%) had one financial expert

■ 4 companies (14%) had three financial experts

■ 3 companies (11%) had no financial experts

Disclosure�of�an�Audit�Committee�Financial�Expert�at�IPO

The SEC requires a listed company to disclose in its annual report whether the board of directors

has determined that the company has at least one audit committee financial expert serving on its

audit committee, or why it does not have one.

An audit committee financial expert is a person who has the following attributes: (1) an

understanding of generally accepted accounting principles and financial statements; (2) the ability to

assess the general application of such principles in connection with the accounting for estimates,

accruals and reserves; (3) experience preparing, auditing, analyzing or evaluating financial

statements that present a breadth and level of complexity of accounting issues that are generally

comparable to the breadth and complexity of issues that can reasonably be expected to be raised

by the company’s financial statements, or experience actively supervising one or more persons

engaged in such activities; (4) an understanding of internal control over financial reporting; and (5)

an understanding of audit committee functions.

7

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Audit Committee Financial Experts at IPO

Three14%

Zero11%

One75%

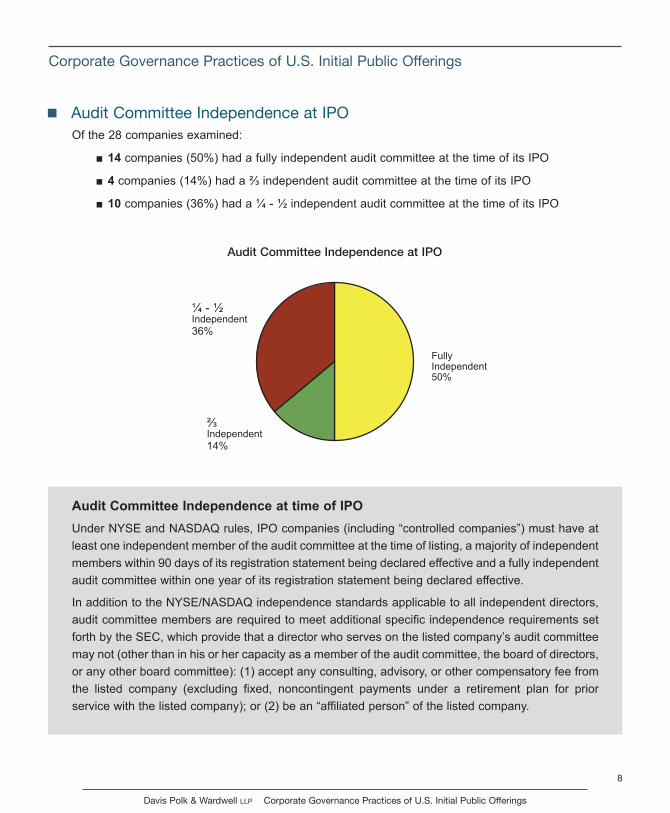

Audit Committee Independence at IPOOf the 28 companies examined:

■ 14 companies (50%) had a fully independent audit committee at the time of its IPO

■ 4 companies (14%) had a ⅔ independent audit committee at the time of its IPO

■ 10 companies (36%) had a ¼ - ½ independent audit committee at the time of its IPO

Audit�Committee�Independence�at�time�of�IPO

Under NYSE and NASDAQ rules, IPO companies (including “controlled companies”) must have at

least one independent member of the audit committee at the time of listing, a majority of independent

members within 90 days of its registration statement being declared effective and a fully independent

audit committee within one year of its registration statement being declared effective.

In addition to the NYSE/NASDAQ independence standards applicable to all independent directors,

audit committee members are required to meet additional specific independence requirements set

forth by the SEC, which provide that a director who serves on the listed company’s audit committee

may not (other than in his or her capacity as a member of the audit committee, the board of directors,

or any other board committee): (1) accept any consulting, advisory, or other compensatory fee from

the listed company (excluding fixed, noncontingent payments under a retirement plan for prior

service with the listed company); or (2) be an “affiliated person” of the listed company.

8

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

FullyIndependent50%

Audit Committee Independence at IPO

⅔Independent

14%

¼ - ½Independent

36%

9

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Voting in Uncontested Board Elections

Of the 28 companies examined:

■ 25 companies (89%) required a plurality standard for board elections

■ 3 companies (11%) required a majority standard for board elections

Voting�standard�for�director�elections�under�Delaware�Law

Under Delaware Law, in the absence of a different specification in the certificate of incorporation or

bylaws of the company, directors are elected by a plurality voting system. Under the plurality voting

system, the nominees for directorships are elected based on who receives the highest number of

affirmative votes cast. Under a majority voting system, a nominee for directorship is elected if he or

she receives the affirmative vote of a majority of the total votes cast for and against such nominee.

Board Elections

Plurality89%

Majority11%

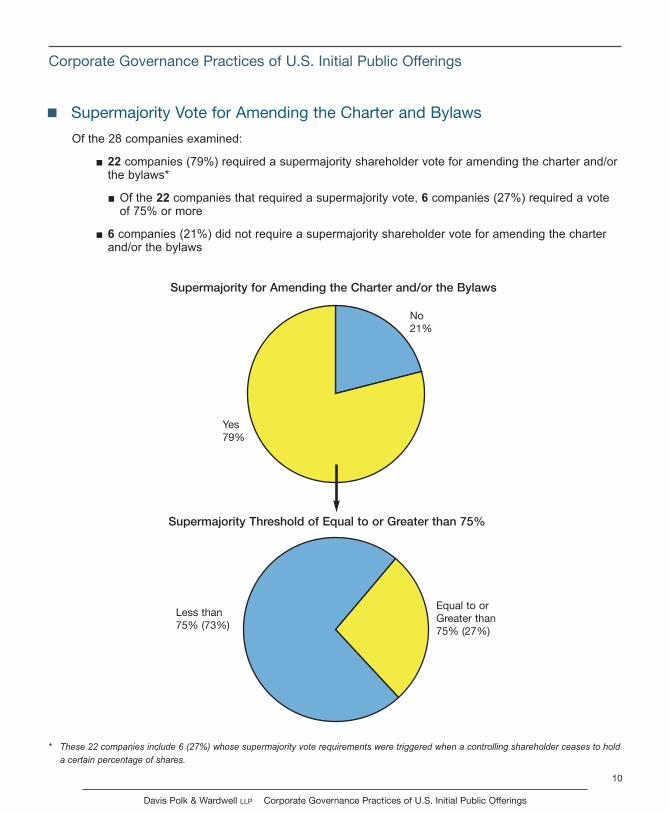

Supermajority Vote for Amending the Charter and Bylaws

Of the 28 companies examined:

■ 22 companies (79%) required a supermajority shareholder vote for amending the charter and/orthe bylaws*

■ Of the 22 companies that required a supermajority vote, 6 companies (27%) required a voteof 75% or more

■ 6 companies (21%) did not require a supermajority shareholder vote for amending the charter and/or the bylaws

* These�22�companies�include�6�(27%)�whose�supermajority�vote�requirements�were�triggered�when�a�controlling�shareholder�ceases�to�hold

a�certain�percentage�of�shares.

10

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Supermajority for Amending the Charter and/or the Bylaws

Supermajority Threshold of Equal to or Greater than 75%

No21%

Yes79%

less than 75% (73%)

Equal to orGreater than 75% (27%)

11

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

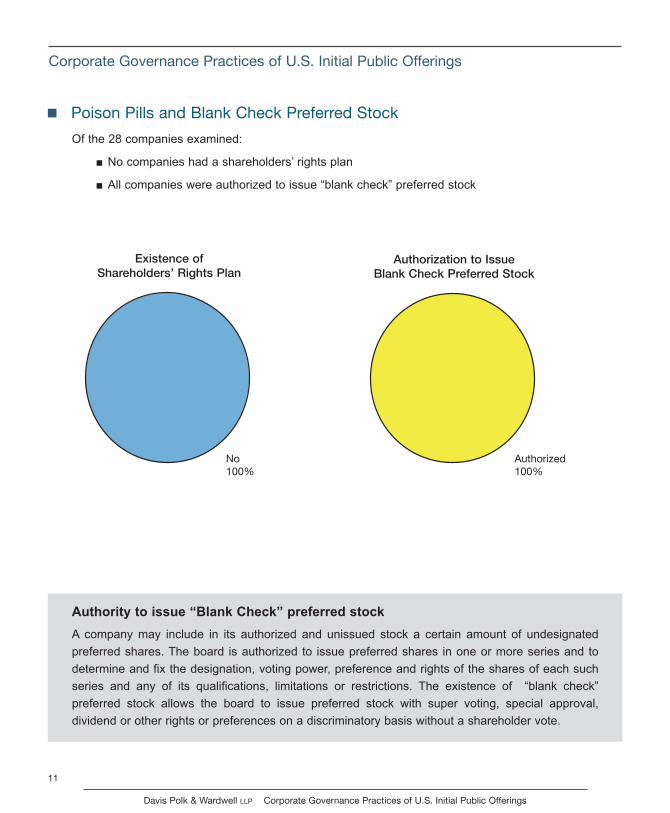

Poison Pills and Blank Check Preferred Stock

Of the 28 companies examined:

■ No companies had a shareholders’ rights plan

■ All companies were authorized to issue “blank check” preferred stock

Authority�to�issue�“Blank�Check”�preferred�stock

A company may include in its authorized and unissued stock a certain amount of undesignated

preferred shares. The board is authorized to issue preferred shares in one or more series and to

determine and fix the designation, voting power, preference and rights of the shares of each such

series and any of its qualifications, limitations or restrictions. The existence of “blank check”

preferred stock allows the board to issue preferred stock with super voting, special approval,

dividend or other rights or preferences on a discriminatory basis without a shareholder vote.

No100%

Authorized100%

Existence of Shareholders’ Rights Plan

Authorization to Issue Blank Check Preferred Stock

12

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Exclusive Forum Provisions

Of the 28 companies examined:

■ 7 companies (25%) had exclusive forum provisions, all of which specified Delaware as the

exclusive forum

■ Of these 7 companies with exclusive forum provisions, all adopted them in the company’scharter

■ 21 companies (75%) did not have exclusive forum provisions

■ All companies with exclusive forum provisions were from 2010 or 2011 IPOs

Exclusive Forum Provisions

Charter100%

No75%

Yes25%

Compensation Consultants

Of the 28 companies examined:

■ 13 companies (46%) disclosed the use of compensation consultants

■ Of these 13 companies that disclosed using consultants, all specified the consultant used

■ The specified consultants included:

Compensation�Consultants

The SEC requires a listed company to disclose in its Form S-1 and its proxy statement any role of

compensation consultants in determining or recommending the amount or form of executive and

director compensation, identifying such consultants, stating whether such consultants are engaged

directly by the compensation committee (or persons performing the equivalent functions) or any

other person, describing the nature and scope of their assignment, and the material elements of the

instructions or directions given to the consultants with respect to the performance of their duties

under the engagement.

13

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Frederic W. Cook & Co.

Hewitt Associates

Longnecker & Associates

Mercer, LLC

Semler Brossy Consulting Group LLC

Compensation Consultants Disclosure

Yes46%

No54%

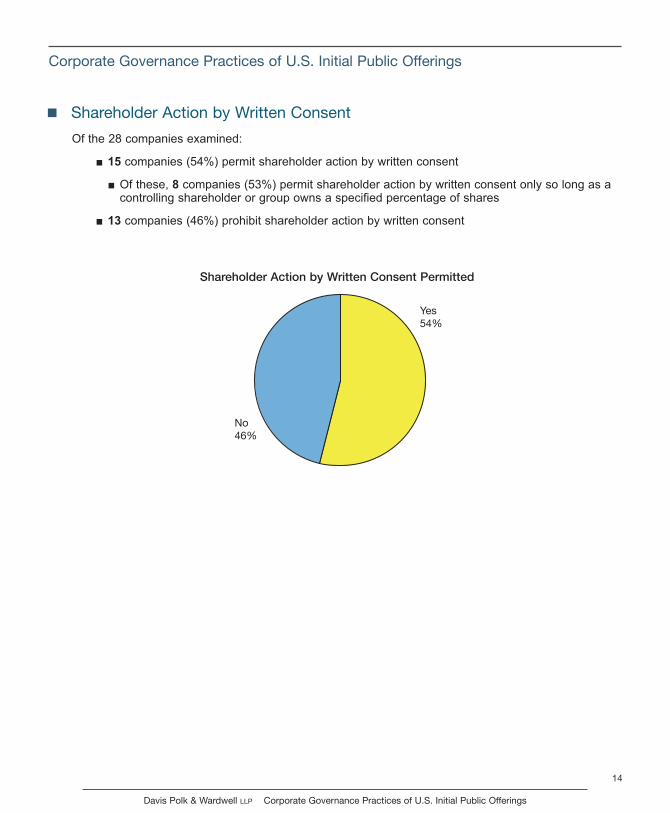

Shareholder Action by Written Consent

Of the 28 companies examined:

■ 15 companies (54%) permit shareholder action by written consent

■ Of these, 8 companies (53%) permit shareholder action by written consent only so long as acontrolling shareholder or group owns a specified percentage of shares

■ 13 companies (46%) prohibit shareholder action by written consent

14

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Shareholder Action by Written Consent Permitted

Yes54%

No46%

15

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Davis Polk’s Capital Markets PracticeDavis Polk & Wardwell LLP has one of the world’s premier capital markets practices. We provide a full

range of services for issuers and underwriters in initial public offerings, follow-on offerings, investment-

grade and high-yield debt issuances, and in the design and execution of sophisticated equity derivative

products. As counsel of choice for many of the world’s leading investment banks and for a broad

spectrum of U.S. and non-U.S. issuers, Davis Polk consistently ranks among the top handful of law firms

engaged globally in capital markets work.

Davis Polk is the premier international IPO advisor. We have extensive experience acting as

counsel to companies, selling shareholders and underwriters in connection with these transactions.

Some recent IPO practice highlights include:

• advising on the five largest IPOs in history, three of which were completed in 2010;

• advising on the largest�IPO�globally,�and�the�largest�in�the�U.S.,�Asia�and�Latin�America;

• ranking as the #1� IPO� advisor� in� the� U.S.� in� 2010,� 2009� and� 2008, having advised on

approximately 30%, approximately 40% and more than 70% of IPOs by volume in 2010, 2009 and

2008, respectively;

• advising the lead managers on the $23.1 billion SEC-registered IPO of common stock and

convertible junior preferred stock of General Motors ― this�is�the�largest�IPO�in�history;

• advising the Agricultural Bank of China on its $22 billion Rule 144A/Regulation S global IPO and

dual listing of H shares and A shares ― this�is�the�second-largest�IPO�in�history�and�the�largest-

ever�by�an�Asian�issuer;

• advising the Federal Reserve Bank of New York (FRBNY) on the $20.5 billion Rule

144A/Regulation S global IPO of common shares of AIA Group. The shares were sold by American

International Group (AIG) and represented the sale of 67.1% of AIG’s formerly 100% stake in AIA

― this�is�the�largest-ever�IPO�on�the�Hong�Kong�Stock�Exchange;

• advising Bankia on its €3.1 billion ($4.4 billion) Rule 144A/Regulation S IPO of ordinary shares ―

this�is�the�first�IPO�to�be�conducted�by�former�Spanish�savings�banks�and�is�the�largest�IPO

in�Spain�since�December�2007;

• advising Prada on its $2.15 billion Rule 144A/Regulation S IPO and Hong Kong Stock Exchange

listing of ordinary shares ― this�is�the�largest�Hong�Kong�IPO�to�date�in�2011;

• advising PANDORA on its $2 billion Rule 144A/Regulation S IPO of common stock ― this�is�the

largest�Danish�IPO�since�1994�and�the�second-largest�IPO�in�Western�Europe�in�2010;

• advising the joint global coordinators on the €1.3 billion ($1.7 billion) Rule 144A/Regulation S IPO

of common stock of Amadeus IT Holding ― this� was� Spain’s� first� public� offering� on� the

Continuous�Market�of�the�Spanish�Stock�Exchanges�since�2007;

• advising Arcos Dorados Holdings on its $1.4 billion SEC-registered IPO of Class A shares ― this

is�the�largest�IPO�by�a�Latin�American�issuer�to�date�in�2011;

• advising the underwriters on the $1.4 billion SEC-registered IPO of Class A shares by Yandex ―

the�offering�is�the�biggest�technology�IPO�worldwide�in�2011�to�date�and�the�largest�IPO�of

an�Internet�company�since�Google’s�IPO�in�2004;

• advising the lead managers on the $923 million SEC-registered IPO of Class A common stock of Air

Lease Corporation ― this�transaction�is�the�jet-leasing�industry’s�largest-ever�IPO;

• advising the underwriters on the $900 million SEC-registered IPO of common stock of BankUnited

― this�is�the�largest�U.S.�bank�IPO�in�history;

• advising the joint bookrunners on the $681 million Rule 144A/Regulation S IPO of common stock of

Grupo Qualicorp;

• advising Kosmos Energy on its $621 million SEC-registered IPO of common stock;

• advising the lead managers on the $476 million SEC-registered IPO of common stock of NXP

Semiconductors;

• advising the lead managers on the $408 million IPO of common stock of Molycorp;

• advising Pandora Media on its $235 million SEC-registered IPO of common stock; and

• advising the underwriters on the $224 million SEC-registered IPO of ADSs by 21Vianet.

16

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Our lawyers

Our global capital markets practice has approximately 235 lawyers, including 46 partners in our offices

around the world.

For more information, please contact:

Phone Email

New�York

Sarah E. Beshar 212 450 4131 [email protected]

Maurice Blanco 212 450 4086 [email protected]

Ning Chiu 212 450 4908 [email protected]

John G. Crowley 212 450 4550 [email protected]

Alan Dean 212 450 4126 [email protected]

Richard A. Drucker 212 450 4745 [email protected]

Manuel Garciadiaz 212 450 6095 [email protected]

Joseph A. Hall 212 450 4565 [email protected]

Michael Kaplan 212 450 4111 [email protected]

Deanna L. Kirkpatrick 212 450 4135 [email protected]

Nicholas A. Kronfeld 212 450 4950 [email protected]

Richard J. Sandler 212 450 4224 [email protected]

Richard D. Truesdell, Jr. 212 450 4674 [email protected]

Elizabeth Weinstein 212 450 4803 [email protected]

17

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

Our lawyers (cont.)

Phone Email

Menlo�Park���������������������������

Julia K. Cowles 650 752 2007 [email protected]

Francis S. Currie 650 752 2002 [email protected]

Bruce K. Dallas 650 752 2022 [email protected]

Alan F. Denenberg 650 752 2004 [email protected]

Daniel G. Kelly, Jr. 650 752 2001 [email protected]

William M. Kelly 650 752 2003 [email protected]

Sarah K. Solum 650 752 2011 [email protected]

Mischa Travers 650 752 2014 [email protected]

Martin A. Wellington 650 752 2018 [email protected]

18

Davis Polk & Wardwell llP Corporate Governance Practices of U.S. Initial Public Offerings

Corporate Governance Practices of U.S. Initial Public Offerings

NEW YORK450 lexington Avenue New York, NY 10017212 450 4000 tel 212 450 3800 fax

MENlO PARK 1600 El Camino Real Menlo Park, CA 94025 650 752 2000 tel 650 752 2111 fax

WASHINGTON DC1300 I Street, N.W.Suite 1000 Washington, D.C. 20005 202 962 7000 tel 202 962 7111 fax

SÃO PAUlOAv. Brig. Faria lima, 390011° andar – cj 1102São Paulo – SP 04538-13255 11 4871 8400 tel55 11 4871 8500 fax

lONDON 99 Gresham Street london EC2V 7NG 44 20 7418 1300 tel 44 20 7418 1400 fax

PARIS 121, avenue des Champs-Elysées 75008 Paris 33 1 56 59 36 00 tel 33 1 56 59 37 00 fax

MADRID Paseo de la Castellana, 41 28046 Madrid 34 91 768 9600 tel 34 91 768 9700 fax

TOKYO Izumi Garden Tower 33F 1-6-1 Roppongi Minato-ku, Tokyo 106-6033 81 3 5561 4421 tel 81 3 5561 4425 fax

BEIJING 2201 China World Office 21 Jian Guo Men Wai AvenueChao Yang District Beijing 10000486 10 8567 5000 tel86 10 8567 5123 fax

HONG KONG The Hong Kong Club Building 3A Chater Road Hong Kong 852 2533 3300 tel 852 2533 3388 fax

FOR MORE INFORMATION, CONTACT:

Kevin Cavanaugh

Director of Business Development

212 450 6811

davispolk.com