[email protected] why microinsurance? véronique faber, microinsurance network

TRANSCRIPT

[email protected] www.e-mfp.eu

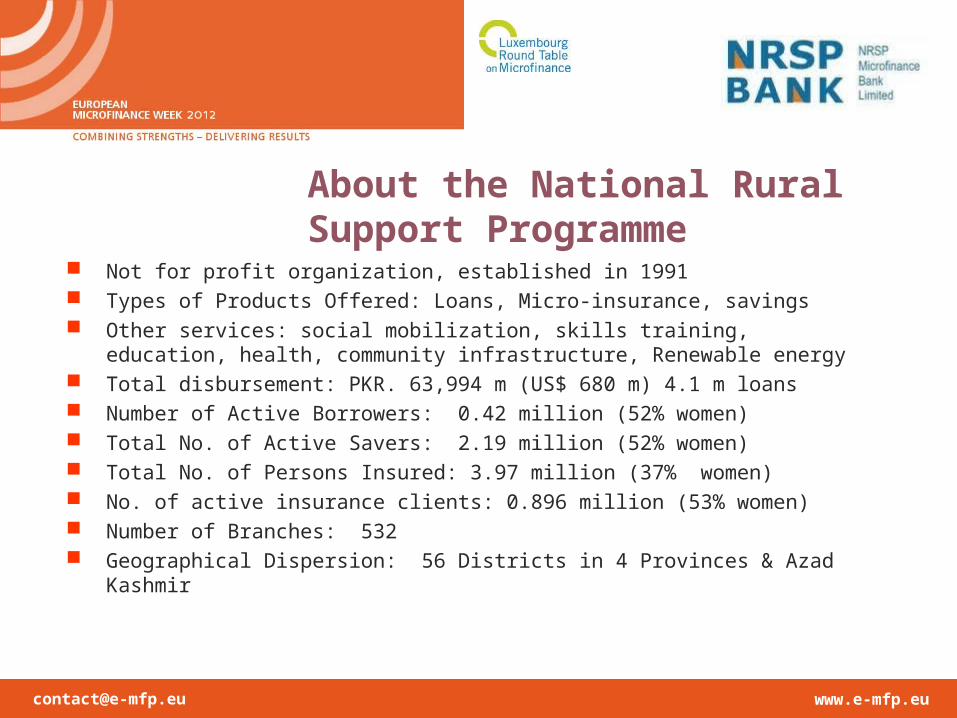

About the National Rural Support Programme

Not for profit organization, established in 1991 Types of Products Offered: Loans, Micro-insurance, savings Other services: social mobilization, skills training, education, health,

community infrastructure, Renewable energy Total disbursement: PKR. 63,994 m (US$ 680 m) 4.1 m loans Number of Active Borrowers: 0.42 million (52% women) Total No. of Active Savers: 2.19 million (52% women) Total No. of Persons Insured: 3.97 million (37% women) No. of active insurance clients: 0.896 million (53% women) Number of Branches: 532 Geographical Dispersion: 56 Districts in 4 Provinces & Azad Kashmir

[email protected] www.e-mfp.eu

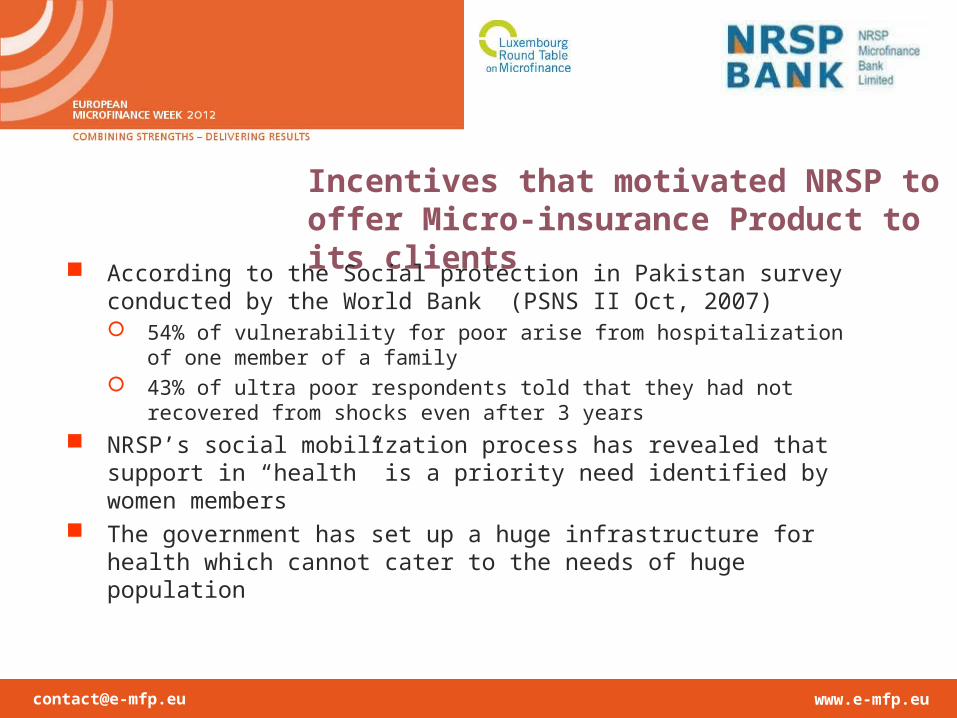

Incentives that motivated NRSP to offer Micro-insurance Product to its clients

According to the Social protection in Pakistan survey conducted by the World Bank (PSNS II Oct, 2007) 54% of vulnerability for poor arise from hospitalization of one

member of a family 43% of ultra poor respondents told that they had not recovered

from shocks even after 3 years

NRSP’s social mobilization process has revealed that support in “health” is a priority need identified by women members

The government has set up a huge infrastructure for health which cannot cater to the needs of huge population

[email protected] www.e-mfp.eu

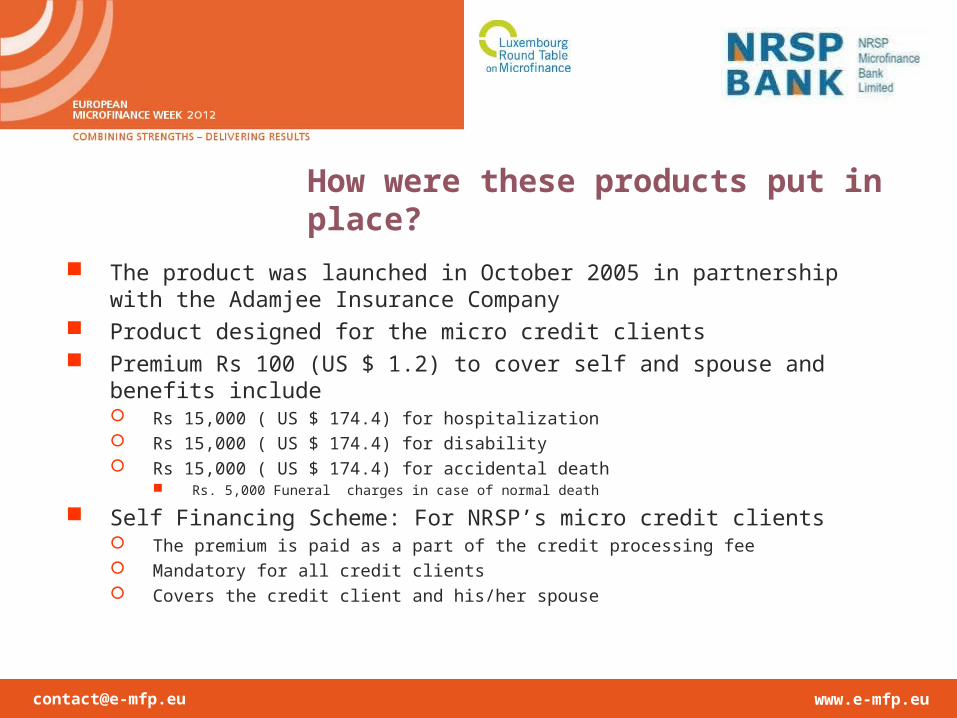

How were these products put in place?

The product was launched in October 2005 in partnership with the Adamjee Insurance Company

Product designed for the micro credit clients Premium Rs 100 (US $ 1.2) to cover self and spouse and benefits

include Rs 15,000 ( US $ 174.4) for hospitalization Rs 15,000 ( US $ 174.4) for disability Rs 15,000 ( US $ 174.4) for accidental death

Rs. 5,000 Funeral charges in case of normal death

Self Financing Scheme: For NRSP’s micro credit clients The premium is paid as a part of the credit processing fee Mandatory for all credit clients Covers the credit client and his/her spouse

[email protected] www.e-mfp.eu

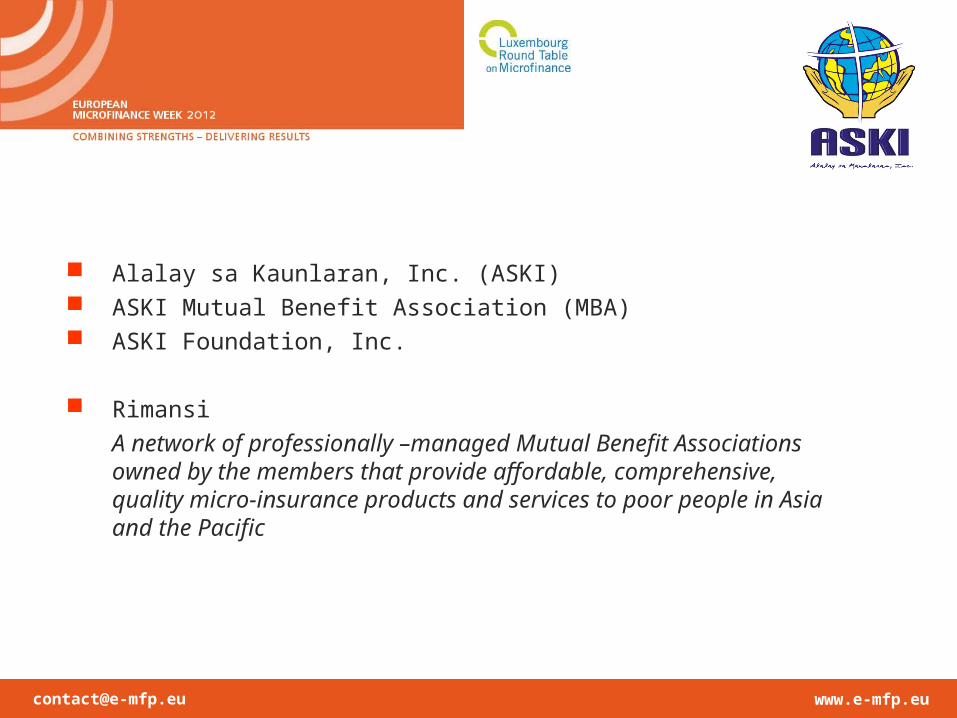

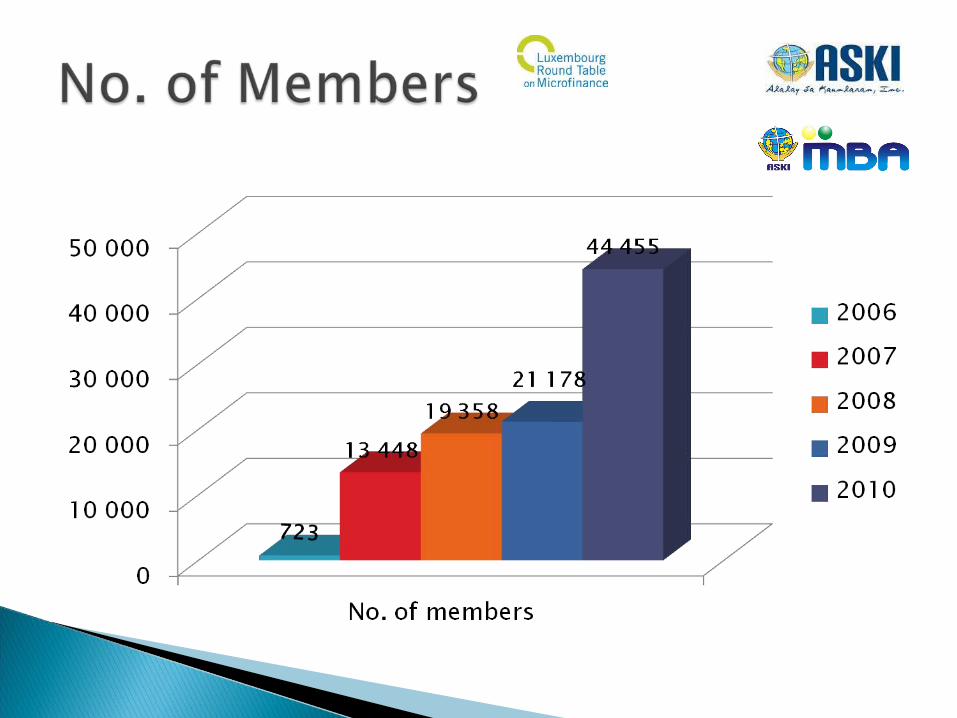

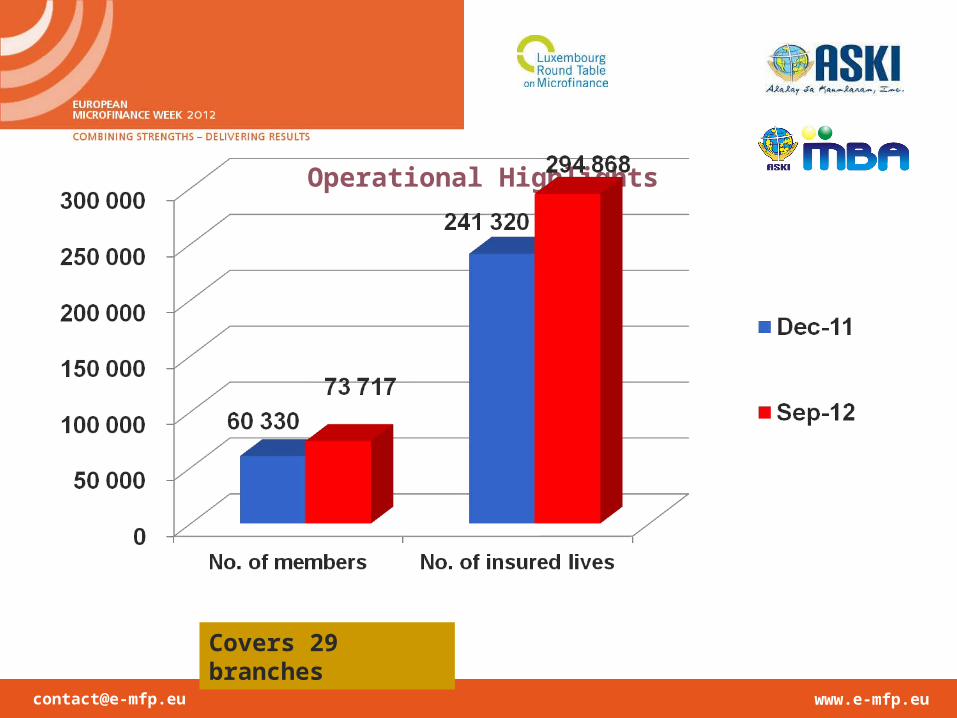

Alalay sa Kaunlaran, Inc. (ASKI) ASKI Mutual Benefit Association (MBA) ASKI Foundation, Inc.

Rimansi

A network of professionally –managed Mutual Benefit Associations owned by the members that provide affordable, comprehensive, quality micro-insurance products and services to poor people in Asia and the Pacific

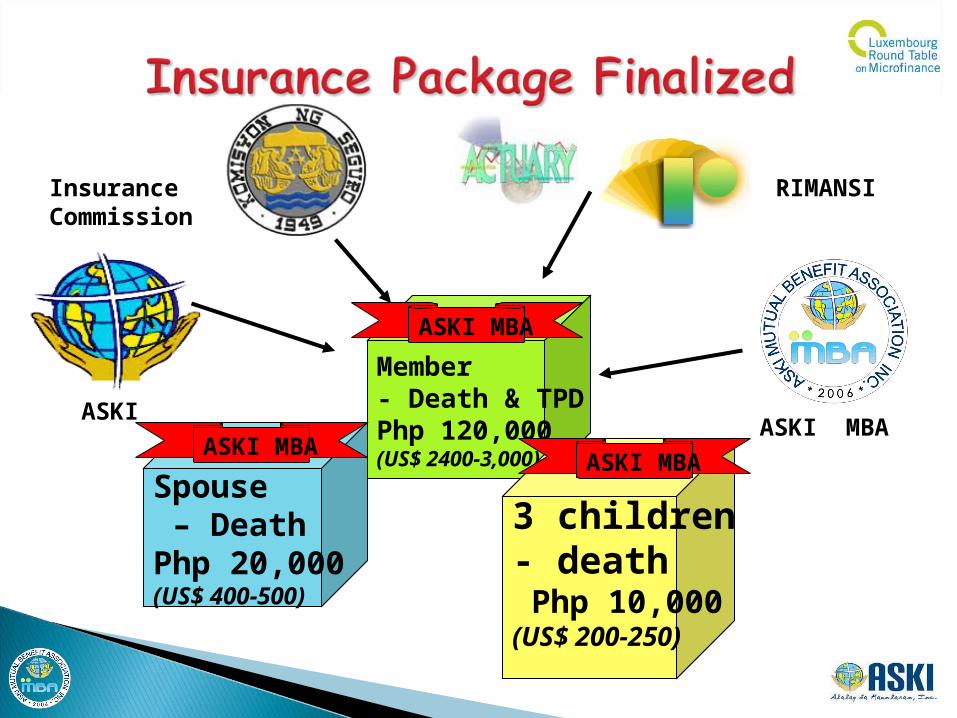

ASKI

Insurance Commission

Member- Death & TPDPhp 120,000(US$ 2400-3,000)

ASKI MBA

RIMANSI

ASKI MBA

3 children - death Php 10,000(US$ 200-250)

Spouse – DeathPhp 20,000(US$ 400-500)

ASKI MBAASKI MBA

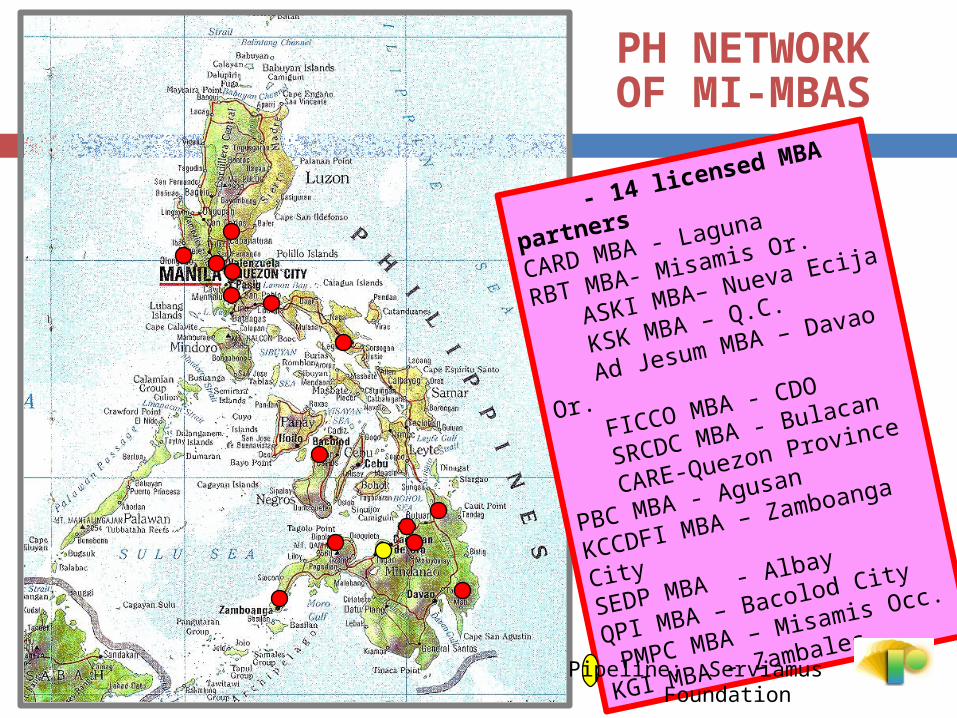

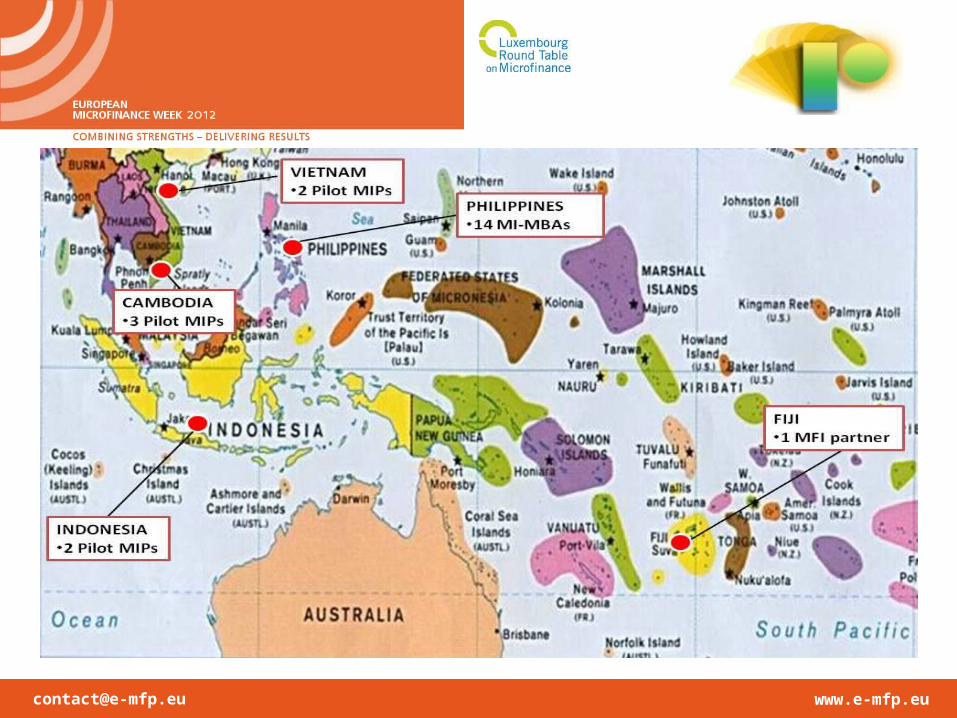

PH NETWORK OF MI-MBAS

- 14 licensed MBA partners

CARD MBA - Laguna

RBT MBA- Misamis Or.

ASKI MBA– Nueva Ecija

KSK MBA – Q.C.

Ad Jesum MBA – Davao Or.

FICCO MBA - CDO

SRCDC MBA - Bulacan

CARE-Quezon Province

PBC MBA - Agusan

KCCDFI MBA – Zamboanga City

SEDP MBA - Albay

QPI MBA – Bacolod City

PMPC MBA – Misamis Occ.

KGI MBA - Zambales

Pipeline: Serviamus Foundation

[email protected] www.e-mfp.eu

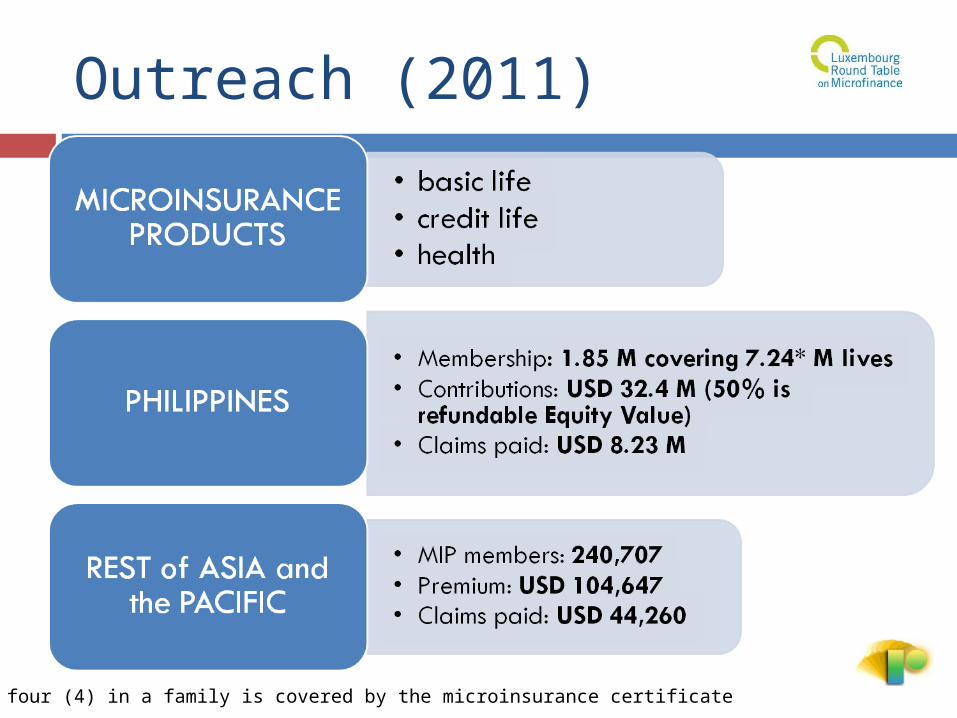

Outreach (2011)

*at least four (4) in a family is covered by the microinsurance certificate

[email protected] www.e-mfp.eu

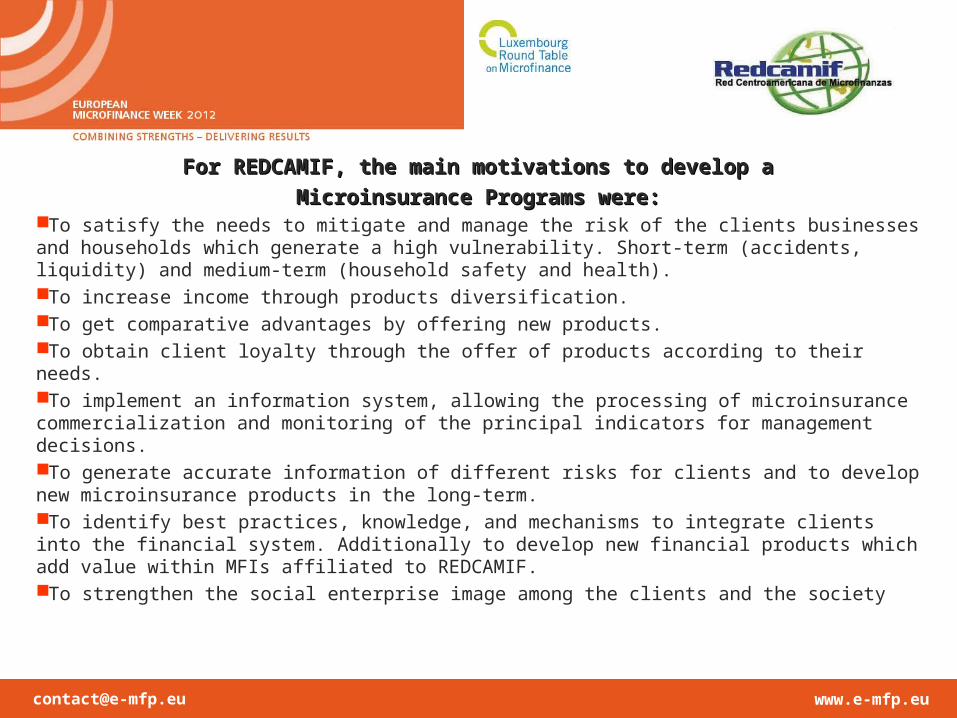

For REDCAMIF, the main motivations to develop aFor REDCAMIF, the main motivations to develop a

Microinsurance Programs were:Microinsurance Programs were:To satisfy the needs to mitigate and manage the risk of the clients businesses and households which generate a high vulnerability. Short-term (accidents, liquidity) and medium-term (household safety and health). To increase income through products diversification. To get comparative advantages by offering new products.To obtain client loyalty through the offer of products according to their needs. To implement an information system, allowing the processing of microinsurance commercialization and monitoring of the principal indicators for management decisions. To generate accurate information of different risks for clients and to develop new microinsurance products in the long-term.To identify best practices, knowledge, and mechanisms to integrate clients into the financial system. Additionally to develop new financial products which add value within MFIs affiliated to REDCAMIF. To strengthen the social enterprise image among the clients and the society

[email protected] www.e-mfp.eu

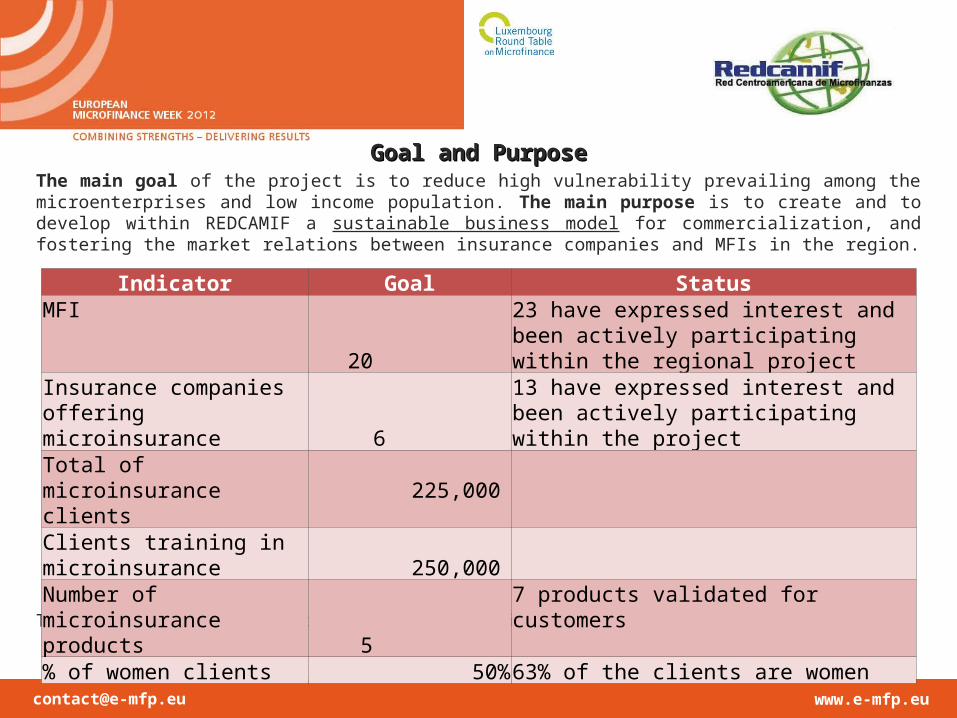

Goal and PurposeGoal and PurposeThe main goal of the project is to reduce high vulnerability prevailing among the microenterprises and low income population. The main purpose is to create and to develop within REDCAMIF a sustainable business model for commercialization, and fostering the market relations between insurance companies and MFIs in the region.

The microinsurance products were designed using the Regional Market Research.

Indicator Goal StatusMFI 20 23 have expressed interest and been actively

participating within the regional project

Insurance companies offering microinsurance

6 13 have expressed interest and been actively participating within the project

Total of microinsurance clients

225,000

Clients training in microinsurance

250,000

Number of microinsurance products

5 7 products validated for customers

% of women clients 50%63% of the clients are women

[email protected] www.e-mfp.eu

PRODUCTSPRODUCTS

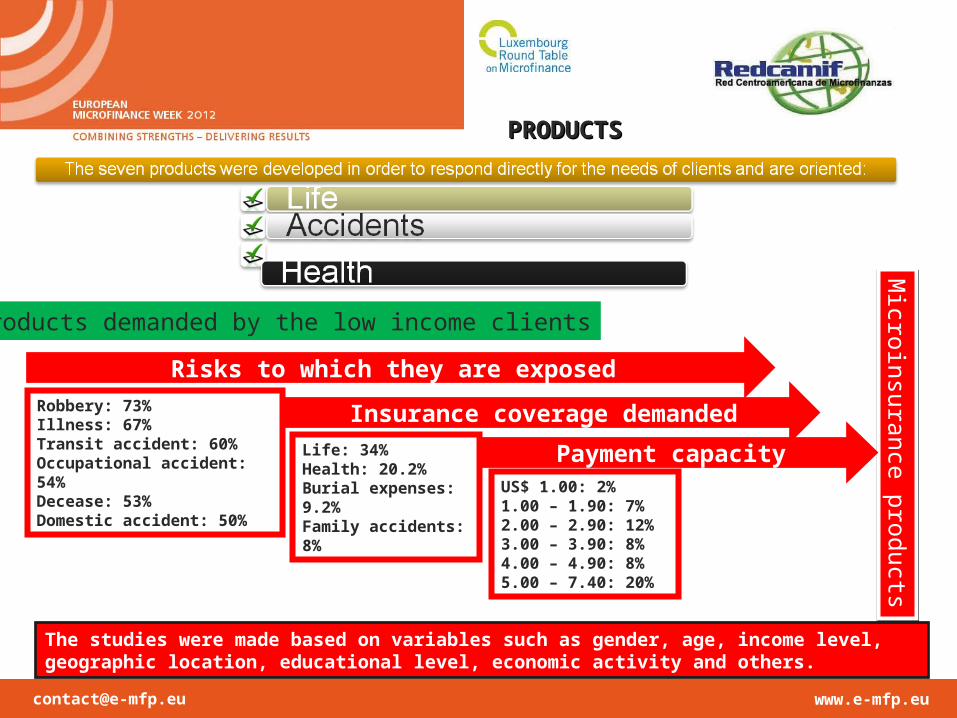

Products demanded by the low income clients

Microinsurance products

Microinsurance products

Robbery: 73%Illness: 67%Transit accident: 60%Occupational accident: 54%Decease: 53%Domestic accident: 50%

Risks to which they are exposed

Insurance coverage demanded

Payment capacityLife: 34%Health: 20.2%Burial expenses: 9.2%Family accidents: 8%

US$ 1.00: 2%1.00 – 1.90: 7%2.00 – 2.90: 12%3.00 – 3.90: 8%4.00 – 4.90: 8%5.00 – 7.40: 20%

The studies were made based on variables such as gender, age, income level, geographic location, educational level, economic activity and others.

[email protected] www.e-mfp.eu

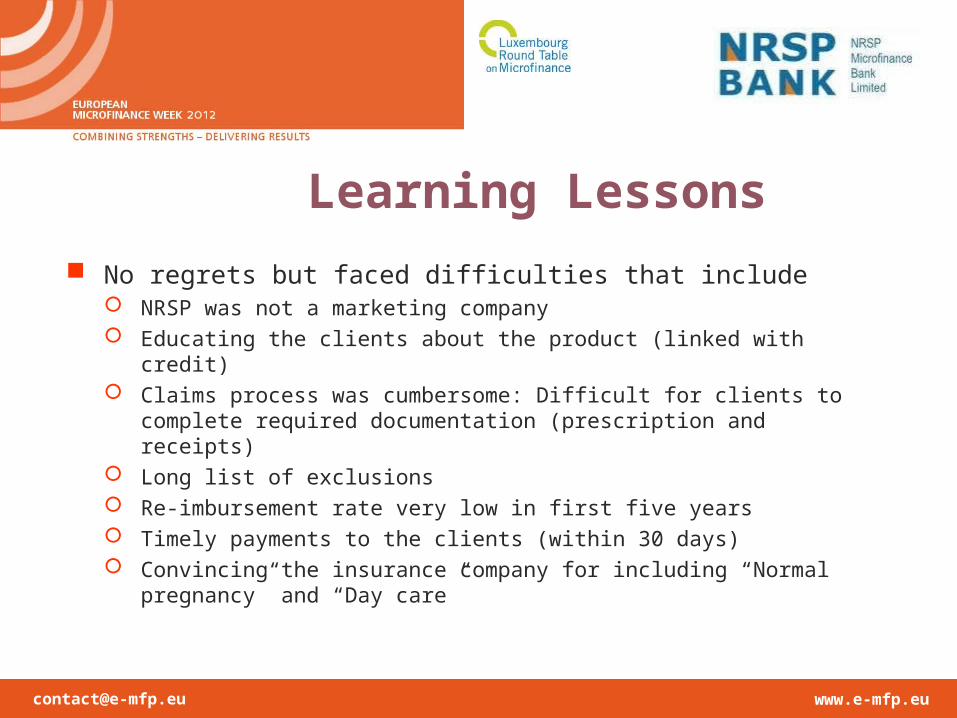

Learning Lessons

No regrets but faced difficulties that include NRSP was not a marketing company Educating the clients about the product (linked with credit) Claims process was cumbersome: Difficult for clients to

complete required documentation (prescription and receipts) Long list of exclusions Re-imbursement rate very low in first five years Timely payments to the clients (within 30 days) Convincing the insurance company for including “Normal

pregnancy” and “Day care”

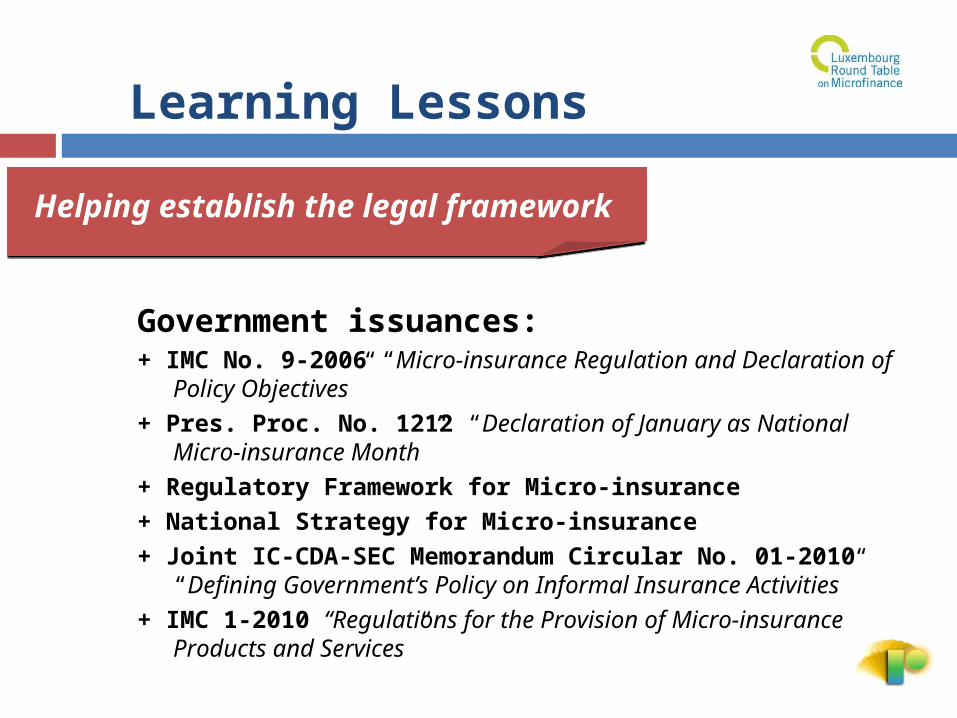

Government issuances:+ IMC No. 9-2006 “Micro-insurance Regulation and Declaration of Policy

Objectives”+ Pres. Proc. No. 1212 “Declaration of January as National Micro-insurance

Month”+ Regulatory Framework for Micro-insurance+ National Strategy for Micro-insurance+ Joint IC-CDA-SEC Memorandum Circular No. 01-2010 “Defining

Government’s Policy on Informal Insurance Activities”+ IMC 1-2010 “Regulations for the Provision of Micro-insurance Products and

Services”

Learning Lessons

Helping establish the legal framework Helping establish the legal framework

[email protected] www.e-mfp.eu

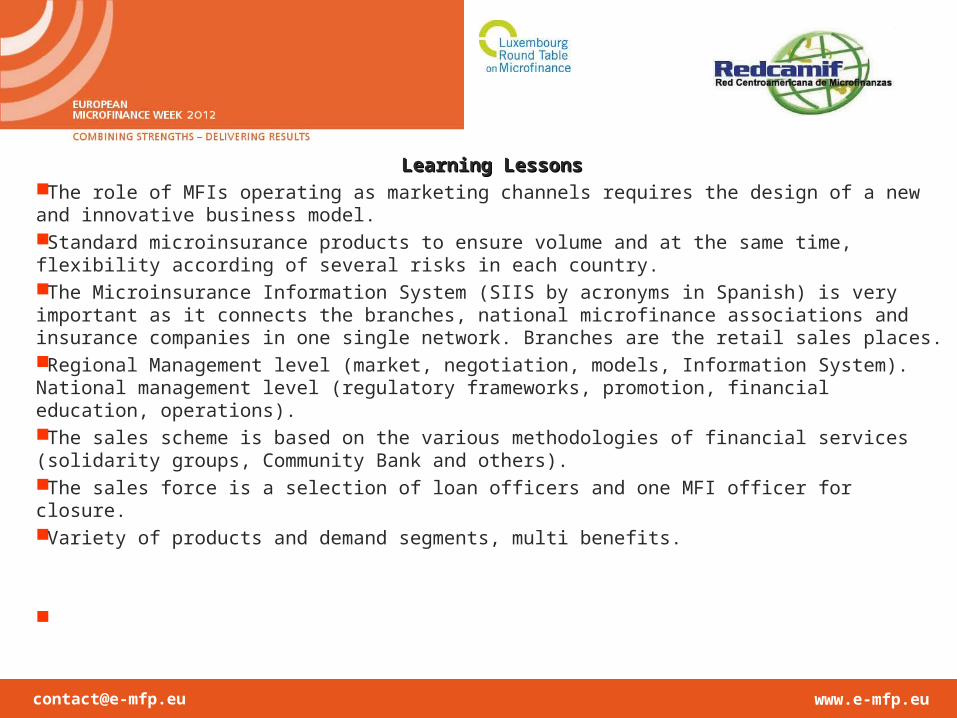

Learning LessonsLearning LessonsThe role of MFIs operating as marketing channels requires the design of a new and innovative business model.Standard microinsurance products to ensure volume and at the same time, flexibility according of several risks in each country.The Microinsurance Information System (SIIS by acronyms in Spanish) is very important as it connects the branches, national microfinance associations and insurance companies in one single network. Branches are the retail sales places.Regional Management level (market, negotiation, models, Information System). National management level (regulatory frameworks, promotion, financial education, operations).The sales scheme is based on the various methodologies of financial services (solidarity groups, Community Bank and others).The sales force is a selection of loan officers and one MFI officer for closure.Variety of products and demand segments, multi benefits.

[email protected] www.e-mfp.eu

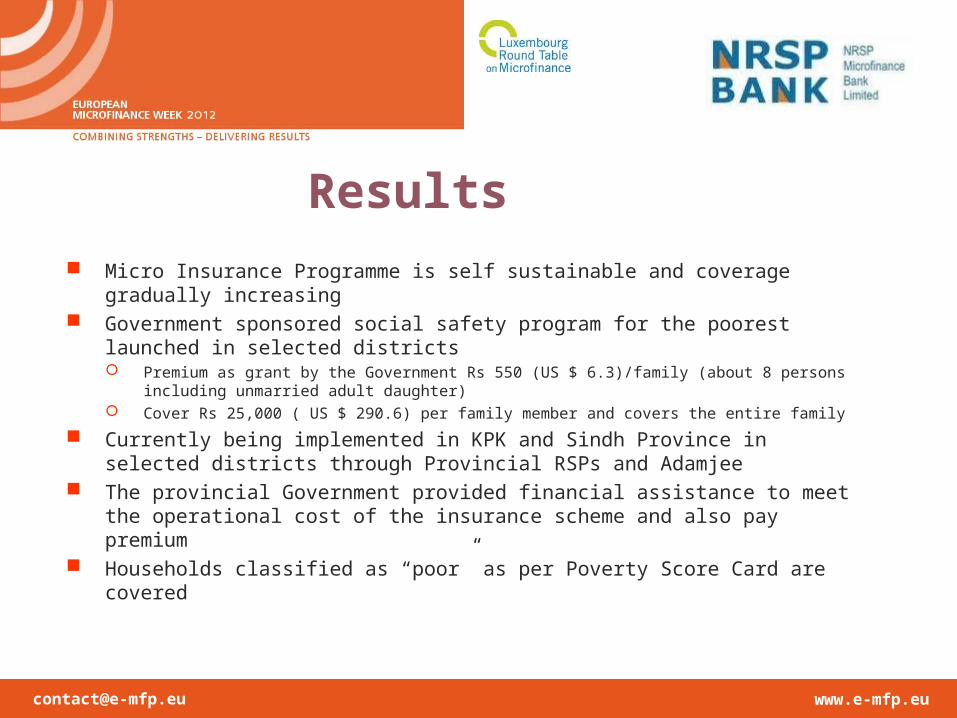

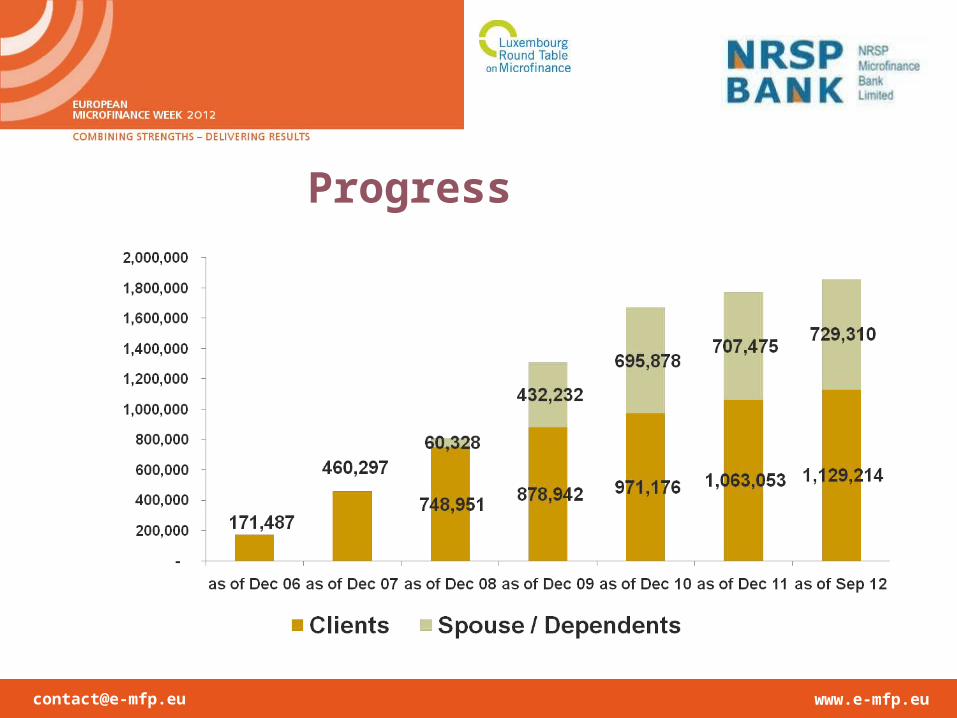

Results

Micro Insurance Programme is self sustainable and coverage gradually increasing

Government sponsored social safety program for the poorest launched in selected districts Premium as grant by the Government Rs 550 (US $ 6.3)/family (about 8 persons

including unmarried adult daughter) Cover Rs 25,000 ( US $ 290.6) per family member and covers the entire family

Currently being implemented in KPK and Sindh Province in selected districts through Provincial RSPs and Adamjee

The provincial Government provided financial assistance to meet the operational cost of the insurance scheme and also pay premium

Households classified as “poor” as per Poverty Score Card are covered

[email protected] www.e-mfp.eu

Why Micro-insurance? Incentives and first results

Fatima receiving treatment in flood affect areas of Punjab

Zareena before treatment in a shrine (MI client in Sindh)

Zarina during treatment in Private hospital (MI client in Sindh)

CBO meeting in Bahawalpur

Children receiving treatment in Sindh

Micro Insurance clients of NRSP

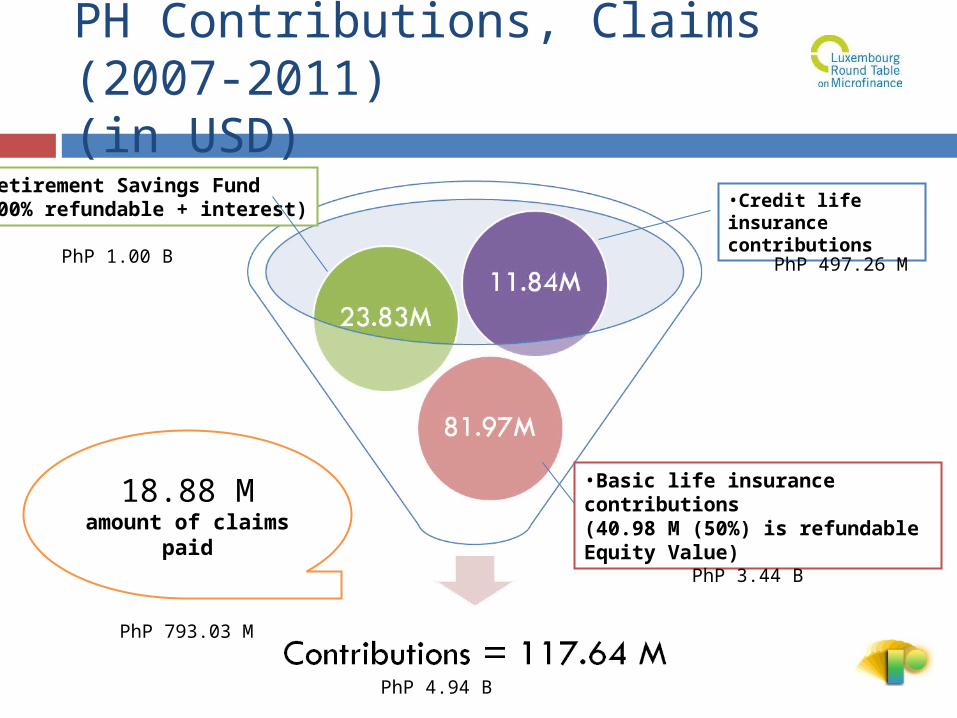

PH Contributions, Claims (2007-2011)(in USD)

•Basic life insurance contributions(40.98 M (50%) is refundable Equity Value)

•Retirement Savings Fund(100% refundable + interest) •Credit life

insurance contributions

18.88 Mamount of claims

paid

PhP 1.00 B PhP 497.26 M

PhP 3.44 B

PhP 4.94 B

PhP 793.03 M

[email protected] www.e-mfp.eu

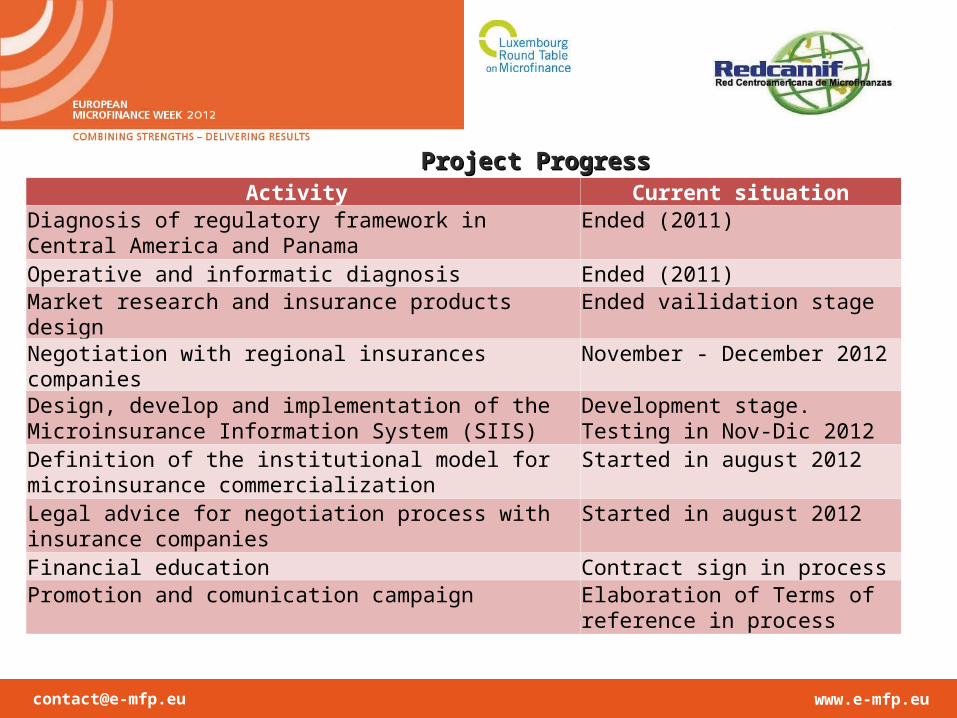

Project ProgressProject Progress

Projection: The program will start in the first semester of 2013.

Activity Current situationDiagnosis of regulatory framework in Central America and Panama

Ended (2011)

Operative and informatic diagnosis Ended (2011)Market research and insurance products design Ended vailidation stageNegotiation with regional insurances companies November - December 2012Design, develop and implementation of the Microinsurance Information System (SIIS)

Development stage. Testing in Nov-Dic 2012

Definition of the institutional model for microinsurance commercialization

Started in august 2012

Legal advice for negotiation process with insurance companies Started in august 2012

Financial education Contract sign in processPromotion and comunication campaign Elaboration of Terms of reference in

process