consumer finance seminar 2013 - presentation slides

TRANSCRIPT

The changing face

of consumer finance

An update on the

latest developments

Consumer Finance Seminar

Interim Permission

Joanne Owens, Principal Associate, Eversheds LLP

October 2013

Interim Permission

•What is Interim Permission?

•How do you get Interim Permission?

•Categories of regulated activity and exemptions

•Challenging Areas

•Implications of registering for Interim Permission

•What do I need to do post 1 April 2014?

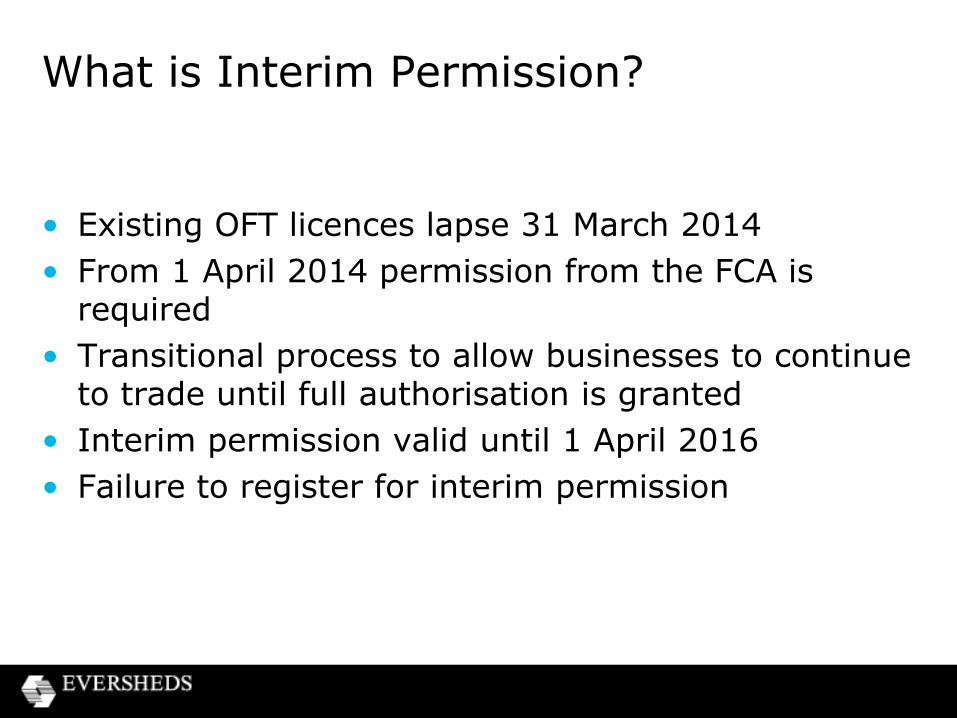

What is Interim Permission?

• Existing OFT licences lapse 31 March 2014

• From 1 April 2014 permission from the FCA is required

• Transitional process to allow businesses to continue to trade until full authorisation is granted

• Interim permission valid until 1 April 2016

• Failure to register for interim permission

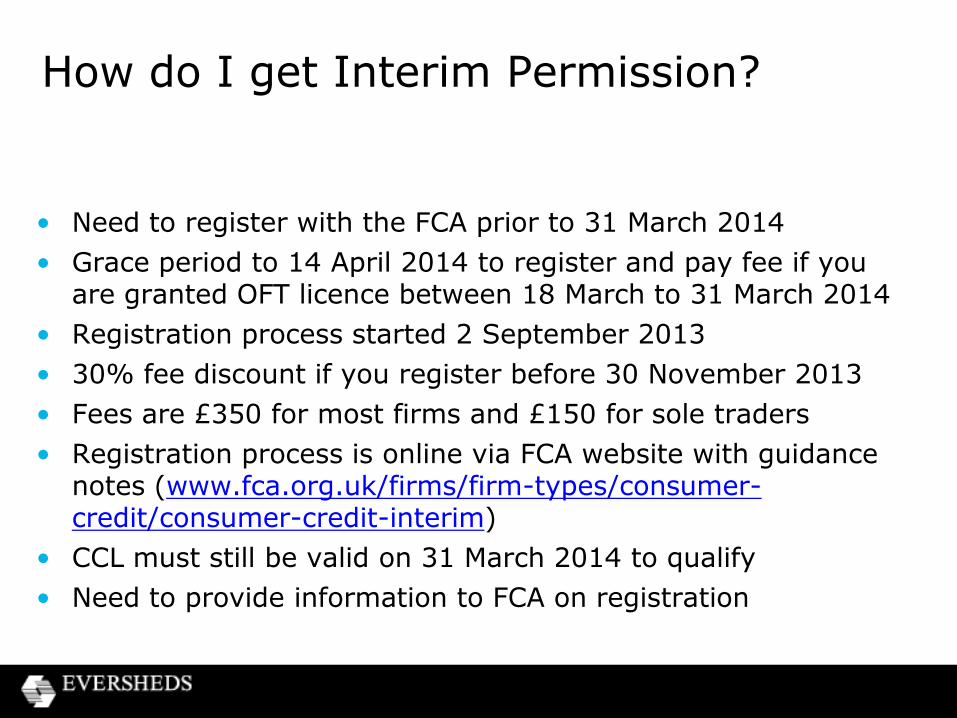

How do I get Interim Permission?

• Need to register with the FCA prior to 31 March 2014

• Grace period to 14 April 2014 to register and pay fee if you are granted OFT licence between 18 March to 31 March 2014

• Registration process started 2 September 2013

• 30% fee discount if you register before 30 November 2013

• Fees are £350 for most firms and £150 for sole traders

• Registration process is online via FCA website with guidance notes (www.fca.org.uk/firms/firm-types/consumer-credit/consumer-credit-interim)

• CCL must still be valid on 31 March 2014 to qualify

• Need to provide information to FCA on registration

Categories of Regulated Activity

• Financial Services and Markets Act 2000 (Regulated Activities) (Amendment) (No 2) Order 2013

• Interim permission is based on current categories on your existing OFT licence

• 10 categories:

– consumer credit (category A)

– consumer hire (category B)

– credit brokerage (category C)

– Debt Collection (category F)

– Debt adjusting, debt counselling, debt administration (categories D, E and G)

– credit information services (category H)

– Canvassing off trade premises

– credit reference agency (category I)

Categories of Regulated Activity

• Exemptions:

– Insolvency Practitioners

– 3rd party tracing agents

– not-for-profit debt advice

– canvassing off trade premises

Challenging Areas

• Professional firms

• Credit brokerage

• Peer to peer lending/operating an electronic system in relation to lending (debt administration)

• Debt adjusting and debt counselling

• Appointed representatives during interim permission regime

Implications of Interim Permission

• Authorised by the FCA to trade in the activities covered by the interim permission only

• Compliance with CONC and FCA Handbook generally (PRIN, GEN, SYSC, DISP)

• Supervision by FCA – thematic reviews/events driven approach

• AML requirements

• Disclosure – no need to specifically refer to interim permission

• Reporting

• Notification of Changes post registration

Post 1 April 2014

• Can apply for full authorisation from 1 April 2014

• New rules specifically for high cost short term loans and P2P lending

• TCF culture within your organisation

• Prudential standards for debt management firms or not for profit debt advisors

• 6 month transitional period to be compliant with rules

• Ensure standard disclosure of the FCA as regulator is given

• New financial promotions regime applies (clear, fair and not misleading)

Post 1 April 2014

• Working towards full authorisation:

– Identification and training of approved persons

– Meeting the threshold conditions including the business model threshold condition (mind and management in the UK)

– Identify areas of compliance risk and address

– Training and competence

– Organisation and control

– Product development and marketing

Bethan Evans, Senior Associate, Eversheds LLP

Geraint Thomas, Partner, Eversheds LLP

October 2013

Consumer Finance Seminar

The Draft Financial Promotions Rules

Chapter 3 (Conc 3)

Overview

• Detailed rules and guidance

• Combination of existing 2004 and 2010 regulations and elements of existing OFT guidance:

– ILG (2010/2011)

– CBG (2011)

– DMG (2012)

• Proposal:

– clear, fair and not misleading;

– broadly equivalent to current CCA (and CCD) regulations; and

– carry across relevant OFT guidance

Overview (continued)

• New provisions dealing with:

– high-cost short-term credit

– cold calling

– debt management

• Timing:

– to be in force on 1 April 2014

– six-month transitional period from 1 April 2014

Application

• 3.1.3:

– to communications in relation to credit agreements

– to communications in relation to credit-broking

– to communications with borrowers (or prospective borrowers) in relation to operating an electronic system in relation to lending

Application (continued)

• 3.1.6: – contains certain exemptions where for customer’s business – excludes “qualifying credit” (first charge residential lending)

• 3.1.7(i) – where only:

name of firm logo contact details brief practical description of type of credit provided

– limited obligations

• Set out in 3.1.7(2)

• Application of 3.1.8

Clear fair and not misleading and general requirements

• 3.3.1 – communications and financial promotions to be clear, fair and not

misleading

• 3.3.2 – use plain and intelligible language – be easily legible (or clearly audible) – specify the name of the person – in case of credit broking, specify name of lender (where known)

• 3.3.3 – rule against stating/implying that credit is available regardless of

customer’s financial status – this may be implied by the name of a firm or its logo or internet

address

• Also apply to consumer hire and to provision of credit information services

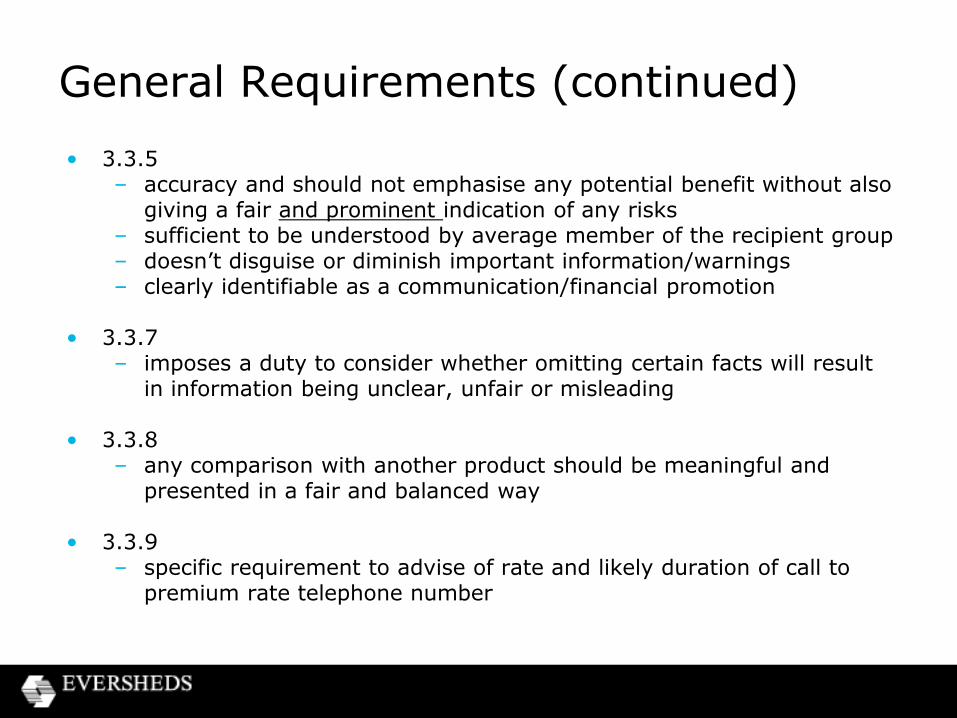

General Requirements (continued)

• 3.3.5 – accuracy and should not emphasise any potential benefit without also

giving a fair and prominent indication of any risks – sufficient to be understood by average member of the recipient group – doesn’t disguise or diminish important information/warnings – clearly identifiable as a communication/financial promotion

• 3.3.7 – imposes a duty to consider whether omitting certain facts will result

in information being unclear, unfair or misleading

• 3.3.8 – any comparison with another product should be meaningful and

presented in a fair and balanced way

• 3.3.9 – specific requirement to advise of rate and likely duration of call to

premium rate telephone number

General Requirements (continued)

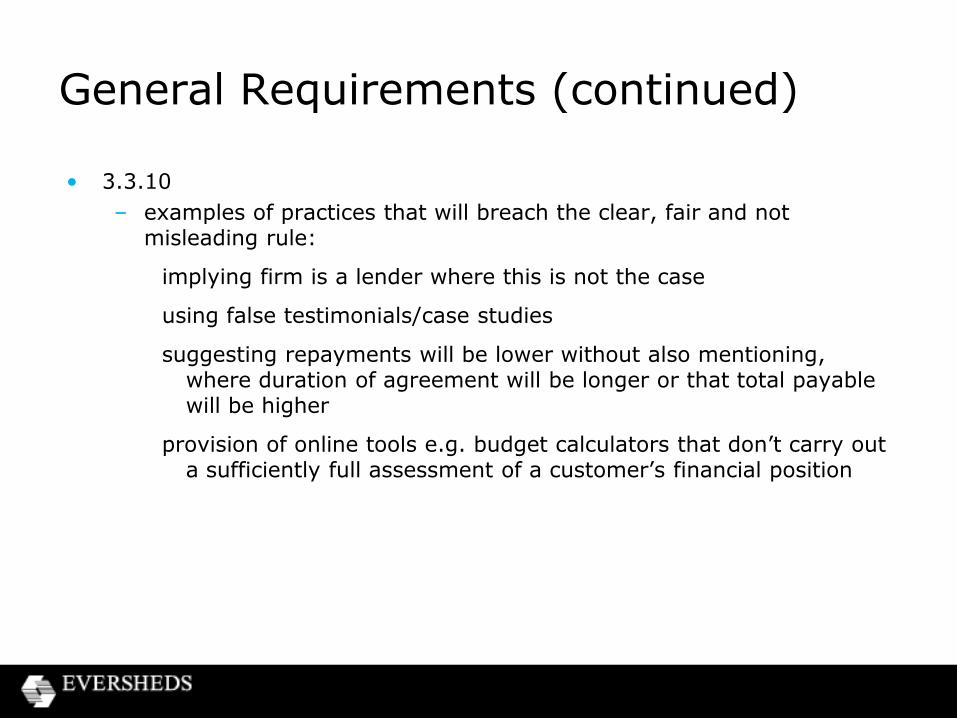

• 3.3.10

– examples of practices that will breach the clear, fair and not misleading rule:

implying firm is a lender where this is not the case

using false testimonials/case studies

suggesting repayments will be lower without also mentioning, where duration of agreement will be longer or that total payable will be higher

provision of online tools e.g. budget calculators that don’t carry out a sufficiently full assessment of a customer’s financial position

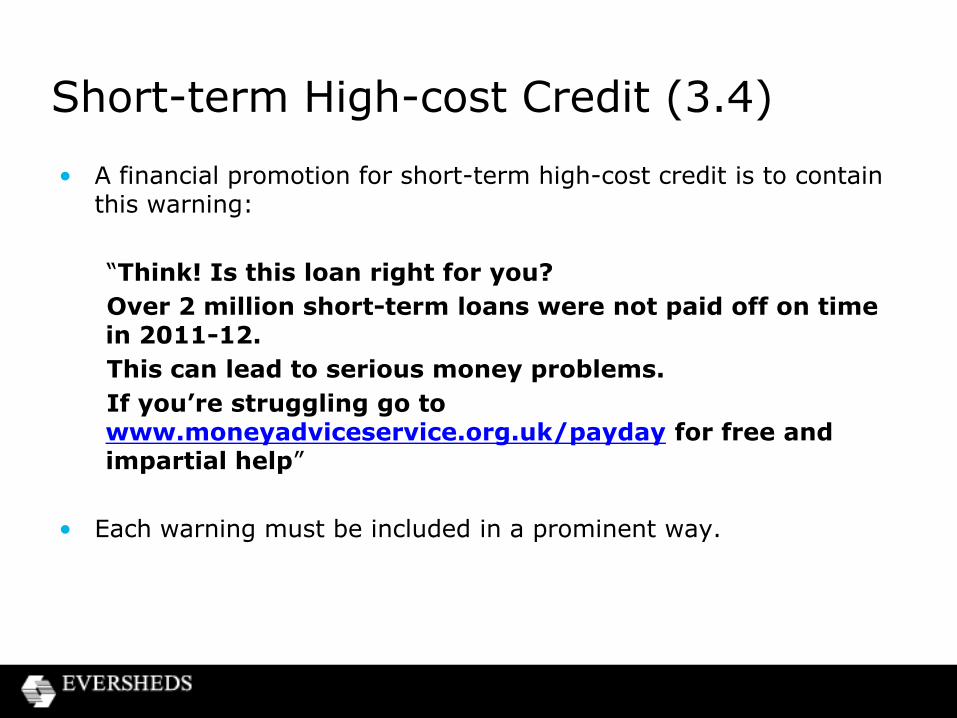

Short-term High-cost Credit (3.4)

• A financial promotion for short-term high-cost credit is to contain this warning:

“Think! Is this loan right for you?

Over 2 million short-term loans were not paid off on time in 2011-12.

This can lead to serious money problems.

If you’re struggling go to www.moneyadviceservice.org.uk/payday for free and impartial help”

• Each warning must be included in a prominent way.

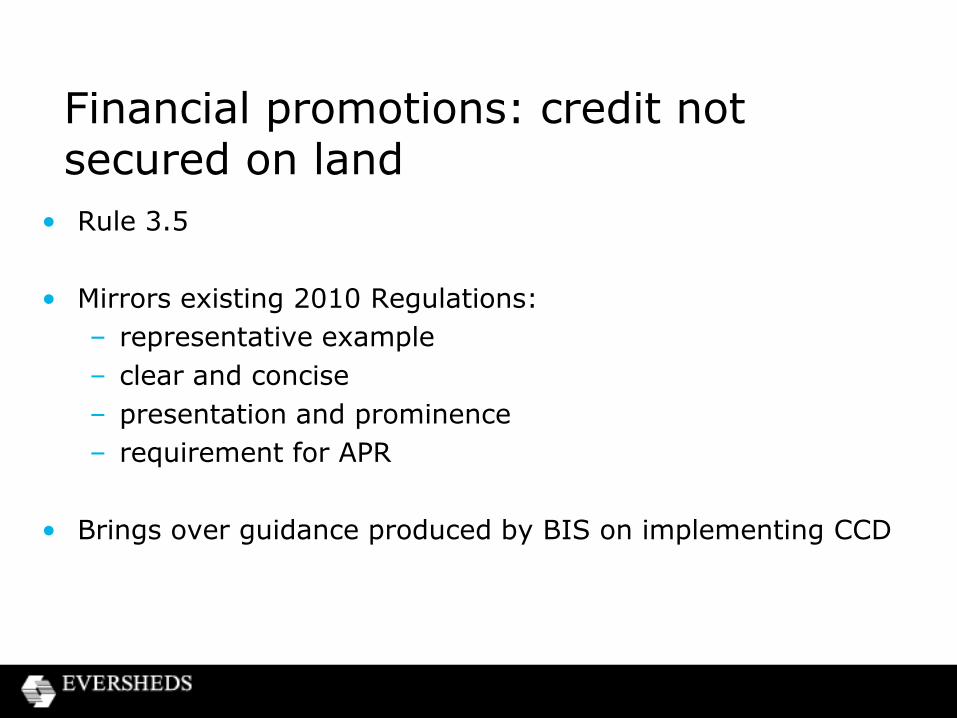

Financial promotions: credit not secured on land

• Rule 3.5

• Mirrors existing 2010 Regulations:

– representative example

– clear and concise

– presentation and prominence

– requirement for APR

• Brings over guidance produced by BIS on implementing CCD

Financial promotions : credit secured on land

• Rule 3.6

• Carries over 2004 Regulations

– existing warnings

“your home may be repossessed....”

“think carefully.....”

“check that this mortgage will meet your needs.....”

– prominence

– APR

– Schedule 2 information

Credit broking (3.7)

• Indicate the extent of its powers and in particular whether it works exclusively with one or more lenders or works independently

• Make clear: – nature of service it provides – indicate ‘in a prominent way’ any arrangements that

may impact impartiality in promoting credit products – independent – only if able to provide access to a

representative range of credit products on competitive terms and not constrained by arrangements with lenders

• Much of this carried over from CBG

Other obligations on lenders (3.8)

• Must not:

– provide application with pre-completed credit amount without having assessed creditworthiness;

– state or imply that provision of credit depends solely on value of equity in any security property; or

– promote unsuitable credit (either knowingly or where reason to believe)

• Examples (from ILG):

– replacing unsecured with secured credit when not in interests of customer

– promote high-cost short-term credit as being suitable for long term borrowing

Debt Counselling and Debt Adjusting (3.9)

• Complexity of debt counselling – restricted space media unlikely to be suitable for promoting debt solutions

• Sets out guidance from DMG on marketing debt management services

• Particular focus on:

– not claiming advice is provided on a free/impartial basis where the firm has a profit seeking motive

– not claiming firm is charitable/not-for-profit

• Application of clear, fair and not misleading rule and general requirements (3.3) to debt counselling and debt adjusting

3.10/3.11

• Promotions that are not in writing and made to a customer outside firm’s premises:

– to be made at an appropriate time of day

– firm to be identified at outset, making clear the purpose of the communication

• Not approving – a firm must not approve a financial promotion to be made in the course of a personal visit, telephone conversation or other interactive dialogue

Consumer Finance Seminar

The Draft Conduct of Business Rules

Geraint Thomas, Partner, Eversheds LLP

October 2013

CONC

• Structure

– Rules

– Guidance

• Approach

– CCA provisions

– Guidance

– Codes

• Transition

• Waivers

CONC 1 & 2

• Application

• Responsibility

– See also CONC 14

• Principles

• General Standards

• E-commerce

• Financial difficulties

• Mental capacity

CONC 4 – Pre-Contract Matters

• Disclosure

• Adequate explanations

• Commission/fees

• CPAs

• Other cases:

– current accounts

– P2P

• Pressure sales

CONC 5 – Responsible Lending

• Creditworthiness

• Brokers

• P2P

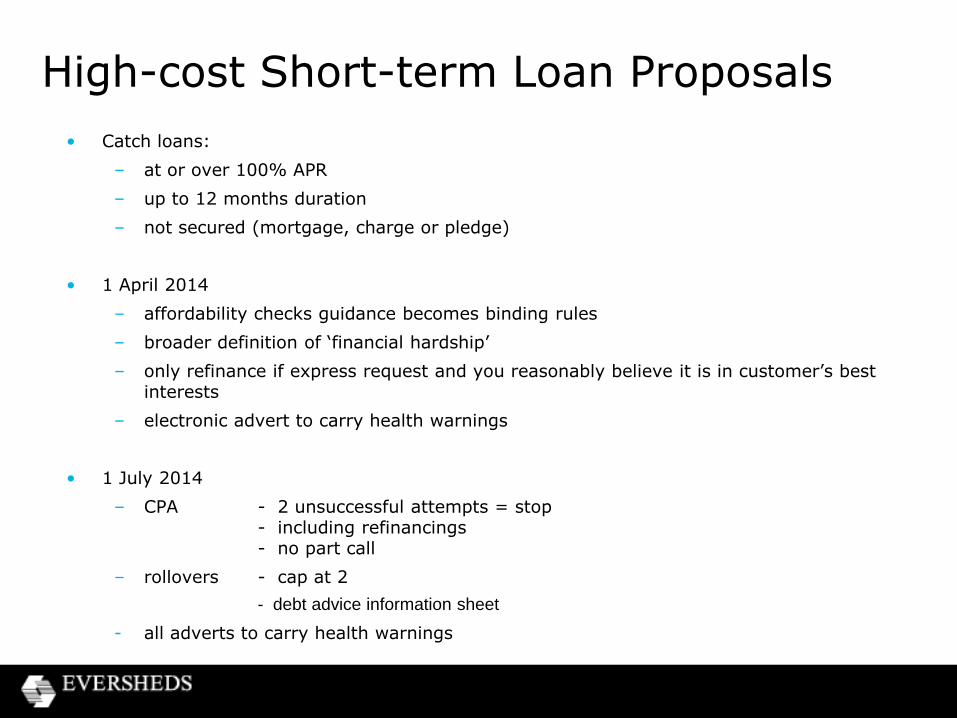

High-cost Short-term Loan Proposals

• Catch loans:

– at or over 100% APR

– up to 12 months duration

– not secured (mortgage, charge or pledge)

• 1 April 2014

– affordability checks guidance becomes binding rules

– broader definition of ‘financial hardship’

– only refinance if express request and you reasonably believe it is in customer’s best interests

– electronic advert to carry health warnings

• 1 July 2014

– CPA - 2 unsuccessful attempts = stop - including refinancings - no part call

– rollovers - cap at 2

- debt advice information sheet

- all adverts to carry health warnings

CONC 6 – Post Contract

• Creditworthiness

• Assignment

• Credit/Store cards

• Brokers

• Special cases:

– current accounts

– pawnbroking

• Conc 11

• Conc 13

Conc 7 – Arrears etc

• Policies

• Treatment – forbearance and consideration

• Information

• CPAs

• Interest/charges

• Customer contact

• Lender responsibilities

• Accuracy

• P2Ps

Special Cases

• Advice

• Debt Management

• CRAs

• P2P

• Secured lenders:

– OFT Guidance

– The future (?)

Consumer Finance Seminar Full Authorisation Process

Kate Mowbray, Associate, Eversheds LLP October 2013

The Authorisation Process

•Firms can apply for full authorisation from 1 April 2014 (previously October 2014).

•Firms will be called forwards for authorisation but you do not have to wait to be called to apply.

•There will be an announcement early in 2014 of dates (starting in autumn 2014) by when specific types of firms with interim permissions must apply for full authorisation.

•Applications will be available online with draft authorisation packs being produced and published by the FCA shortly prior to 1 April 2014.

•Applications contain a number of forms and documents and must be completed in full.

•If the FCA think the application is incomplete they can request clarification/further documents.

•The size of firm will play a part in how intrusive the FCA are in assessing its application.

•Applications must include the required fee and will not be processed until it is received. There is still no detail on what the fees will be.

•October 2013 - consultation paper on fees, including authorisation fees for consumer credit firms and how the FCA propose to calculate periodic fees.

•March 2014 –proposals for periodic fee rates for 2014/15.

•The FCA must make a determination within 6 months of receiving the completed application and all received applications must be determined within 12 months.

Documentation required

• Business plan

• Competitor analysis

• Organisation, board and compliance structures

• An assessment of the board

• Membership - board and executive committee and terms of reference

• Procedures/monitoring of compliance and relevant compliance documentation e.g. policies regarding lending, arrears, treating customers fairly and financial crime

• Business continuity plan

• IT systems

• Training and competence rules

• Outsourcing to third parties (SYSC 8.1 and tracing agents)

• Many of the new requirements for firms under the FCA regime will not apply until a firm receives full authorisation. These include:

– approved persons requirements;

– prudential standards and client assets for debt management firms;

– requirements relating to controllers;

– periodic reporting; and

– complaints reporting and publication rules (note that firms will be required to record complaints from 1 April 2014).

•Firms will be categorised by the FCA once they become fully authorised.

•The distinction between higher-risk and lower-risk activities remains. A key difference is that firms carrying out lower-risk activities can only apply for a limited permission.

Requirements on full authorisation

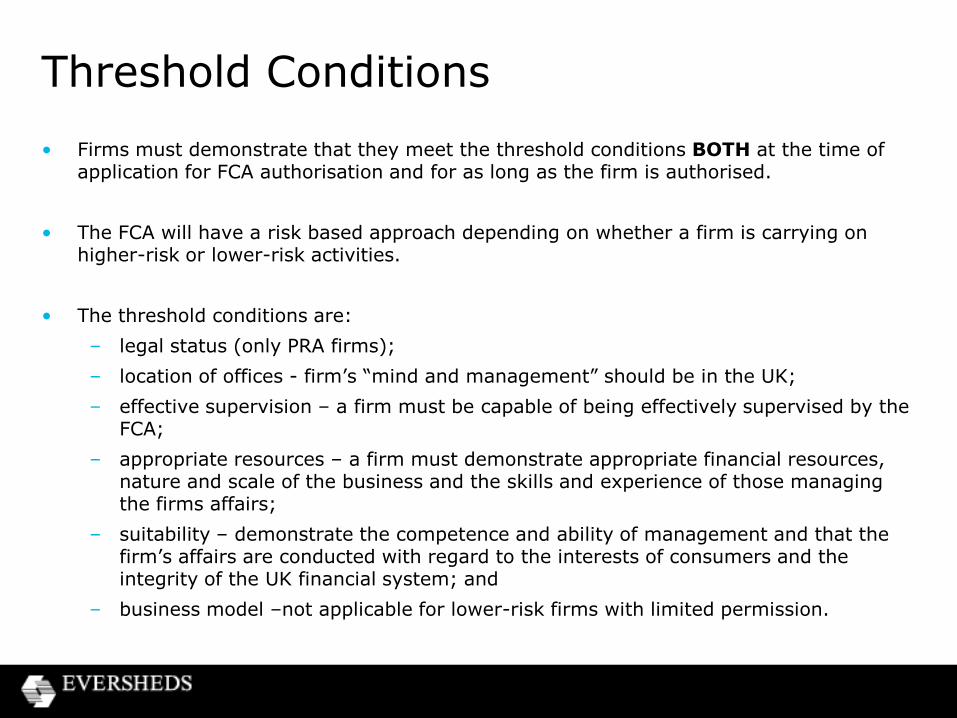

Threshold Conditions

• Firms must demonstrate that they meet the threshold conditions BOTH at the time of application for FCA authorisation and for as long as the firm is authorised.

• The FCA will have a risk based approach depending on whether a firm is carrying on higher-risk or lower-risk activities.

• The threshold conditions are:

– legal status (only PRA firms);

– location of offices - firm’s “mind and management” should be in the UK;

– effective supervision – a firm must be capable of being effectively supervised by the FCA;

– appropriate resources – a firm must demonstrate appropriate financial resources, nature and scale of the business and the skills and experience of those managing the firms affairs;

– suitability – demonstrate the competence and ability of management and that the firm’s affairs are conducted with regard to the interests of consumers and the integrity of the UK financial system; and

– business model –not applicable for lower-risk firms with limited permission.

Business Model

• All higher-risk firms will be required to have a detailed business model.

• COND 2.7.8G

– the assumptions underlying the firm's business model and justification for it;

– the rationale for the business the firm proposes to do or continues to do, its competitive advantage, viability and the longer-term profitability of the business;

– the needs of and risks to consumers;

– the expectations of stakeholders, for example, shareholders and regulators;

– the products and services being offered and product strategy;

– the governance and controls of the firm and of any member of its group (if appropriate);

– the growth strategy and any risks arising from it;

– any diversification strategies; and

– the impact of the external macroeconomic and business environment.

Alternatives to authorisation

• These include:

– being an appointed representative of an authorised firm;

– being a self-employed agent; and

– being an exempt profession firm.

Appointed representatives

• An option for most consumer credit firms apart from lenders (other than lenders providing interest-free credit without any other charges), credit reference agencies and P2P lending platforms carrying on new regulated activity of “operating an electronic system in relation to lending”.

• Multi-principal arrangements to also be an option for appointed representative debt collectors.

• A firm cannot have appointed representatives until it is fully authorised. However, the FCA plans to call firms that wish to act as principals forward to apply early in the authorisation period.

• A principal must have a written agreement in place with its authorised representatives and, where a an appointed representative acts as an appointed representative for other principals, the principals must also enter into a written agreement.

• A firm will always be responsible for the acts and omissions of its appointed representatives in carrying on business for which the firm has accepted responsibility.

• SUP 12 sets out requirements which apply to firms using appointed representatives.

• SUP 12.4.2R - before a firm appoints a person as an appointed representative AND on a continuing basis, it must establish on reasonable grounds that:

– the appointment does not prevent the firm from satisfying and continuing to satisfy the threshold conditions;

– the person:

(a) is solvent;

(b) is otherwise suitable to act for the firm in that capacity; and

(c) has no close links which would be likely to prevent the effective supervision of the person by the firm;

– the firm has adequate:

(a) controls over the person’s regulated activities for which the firm has responsibility; and

(b) resources to monitor and enforce compliance by the person with the relevant requirements applying to the regulated activities for which the firm is responsible and with which the person is required to comply under its contract with the firm; and

– the firm is ready and organised to comply with the other applicable requirements contained or referred to in this chapter.

• SUP 12 also sets out other provisions applicable to firms with appointed representatives including: continuing obligations; training and competence requirements and notification requirement.

Self-employed agents

• Principal firms will be held fully responsible for the conduct of their agents contracted to carry on business on their behalf and enforcement action could be taken against the principal in the case of misconduct by an agent.

• Principals and agents must meet the FCA’s criteria for an agent to be considered to be carrying on the business of the principal or agents will need to be authorised or an authorised representative of the principal.

• The exemption for mail order agents has been amended to allow for financing of the credit agreement to be done by a finance arm in the same group as the mail order firm.

• CONC 14.1.2R sets out the requirements relating to agents.

• The conditions that must be met at the date of the individual’s appointment and while the individual continues to act as the firm’s agent are that:

– the firm appoints the individual as the firm’s agent;

– the individual works as agent only for the firm and not as agent for any other principal;

– the firm has a written agreement with the individual which:

(a) sets out effective measures for the firm to control the individual’s activities when acting on its behalf in the course of business;

(b) require the individual to make clear to customers that the individual is representing the firm as the individual’s principal and the name of the firm;

– (in the case of collecting debts) receipt of payments by the individual is treated as receipt by the firm; and

– the firm accepts full responsibility for the conduct of the individual when the individual is acting on the firm’s behalf in the course of the firm’s business.

Jonathan Guest, Partner, Eversheds LLP

October 2013

Consumer Finance Seminar Approved Persons and Reporting

Approved Persons

• Why?

• Who?

• How?

Reporting

• Financial

• Product sales

• Complaints

• Control

Approved Persons

Why?

• Compliance culture can only be established from the top

• Walking the walk, not just talking the talk

• Personal accountability – the only way to secure focus

• Personal liability

• “Fining firms is not enough… In order to achieve credible deterrence, senior managers must be held to account.”

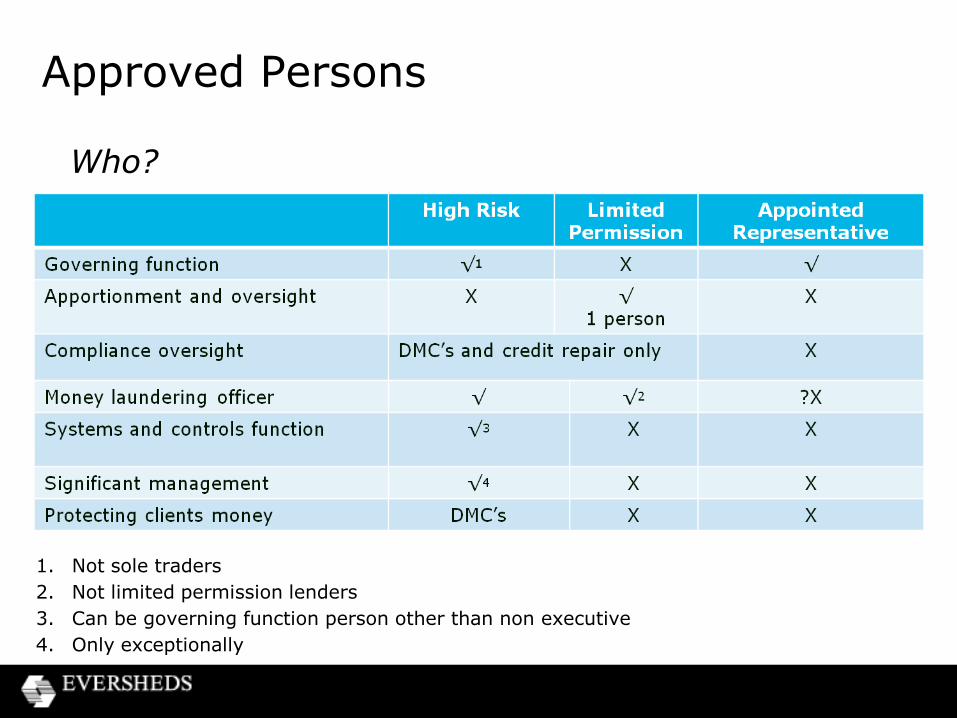

Approved Persons

Who?

1. Not sole traders

2. Not limited permission lenders

3. Can be governing function person other than non executive

4. Only exceptionally

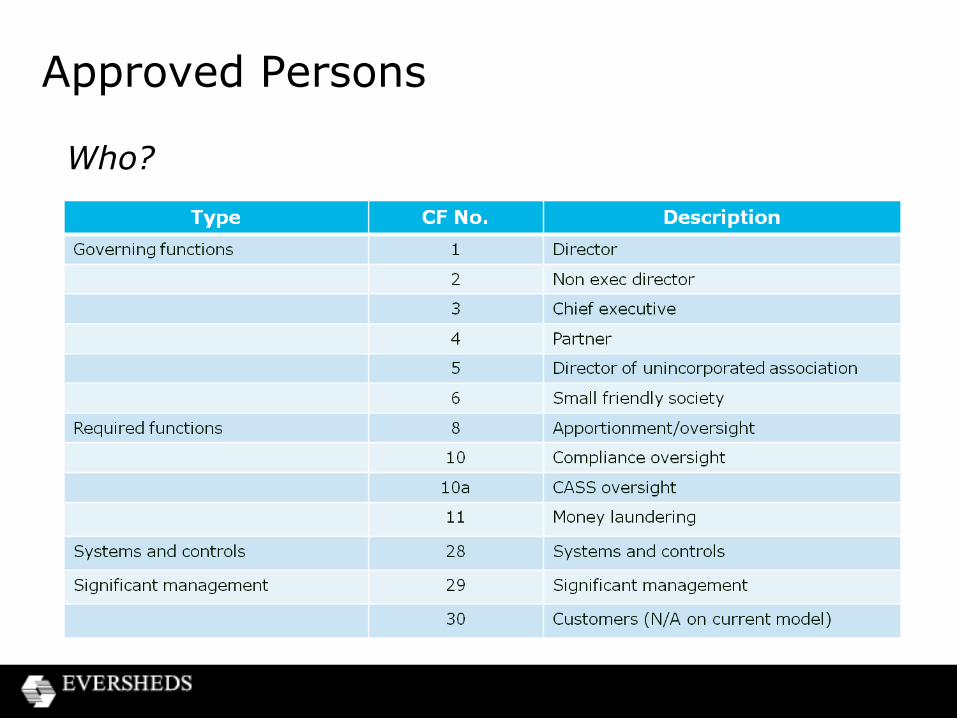

Approved Persons

Who?

Approved Persons

How?

• Pre-approval

• Process for consumer credit not yet announced (40,000 people?)

• FCA’s Fit and Proper Test (FIT)

• Statements of principle and Code of Practice (APER)

• Process currently

– apply via firm completing – Long Form A

– submit application to FCA via ‘ONA’

(online notifications and applications)

– statutory duty to decide within 90 days

– interview on request – 60/90 minutes with 4 to 5 FCA employees

– 85% within 10 days = current self imposed service level

Approved Persons

How?

Data to be submitted can include:

• CV

• Role specification

• Organisation chart

• Recruitment process

• Board and Committee minutes

• Interview notes

• Skills cap analysis

• Skills mapping document

• Learning and development plan

• Biographies/team mix

Approved Persons

How?

Candidates expected to be able to cover:

• Specific areas for function – compliance, risk and audit functions and challenge business

• Market knowledge

• Business strategy and model

• Risk management and control

• Financial analysis and controls

• Governance, oversight and controls

• Regulatory framework and requirements

Approved Persons

How?

Training will be required

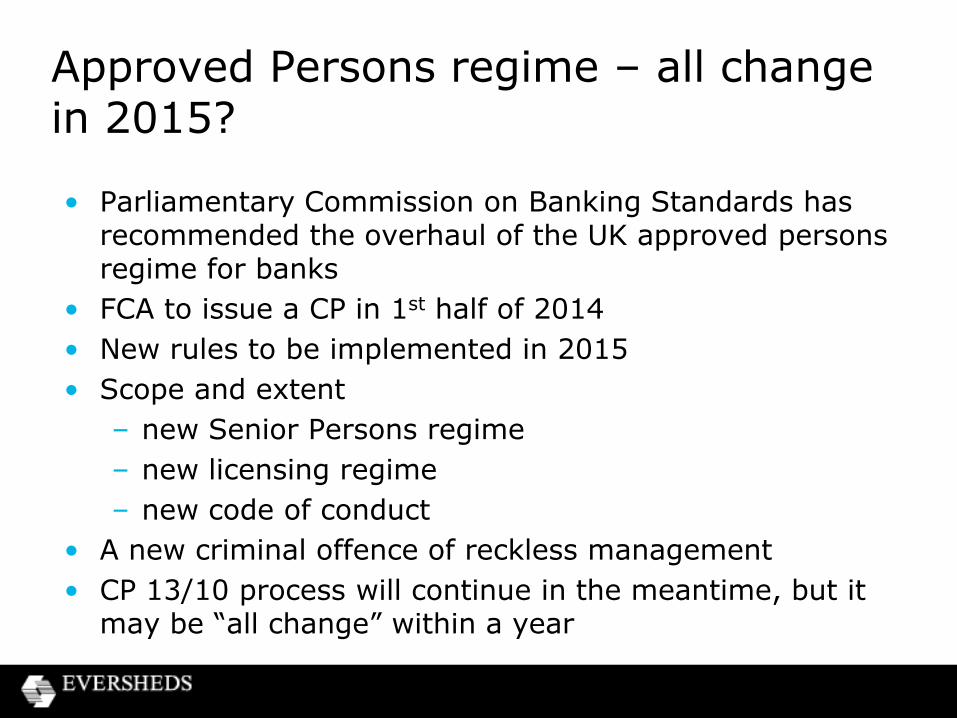

Approved Persons regime – all change in 2015? • Parliamentary Commission on Banking Standards has

recommended the overhaul of the UK approved persons regime for banks

• FCA to issue a CP in 1st half of 2014

• New rules to be implemented in 2015

• Scope and extent

– new Senior Persons regime

– new licensing regime

– new code of conduct

• A new criminal offence of reckless management

• CP 13/10 process will continue in the meantime, but it may be “all change” within a year

Reporting

Types of reporting:

• Financial data

• Product sales data

• Complaints data

• Control data/approval

From later of 1 October 2014 and full authorisation/limited

permission status.

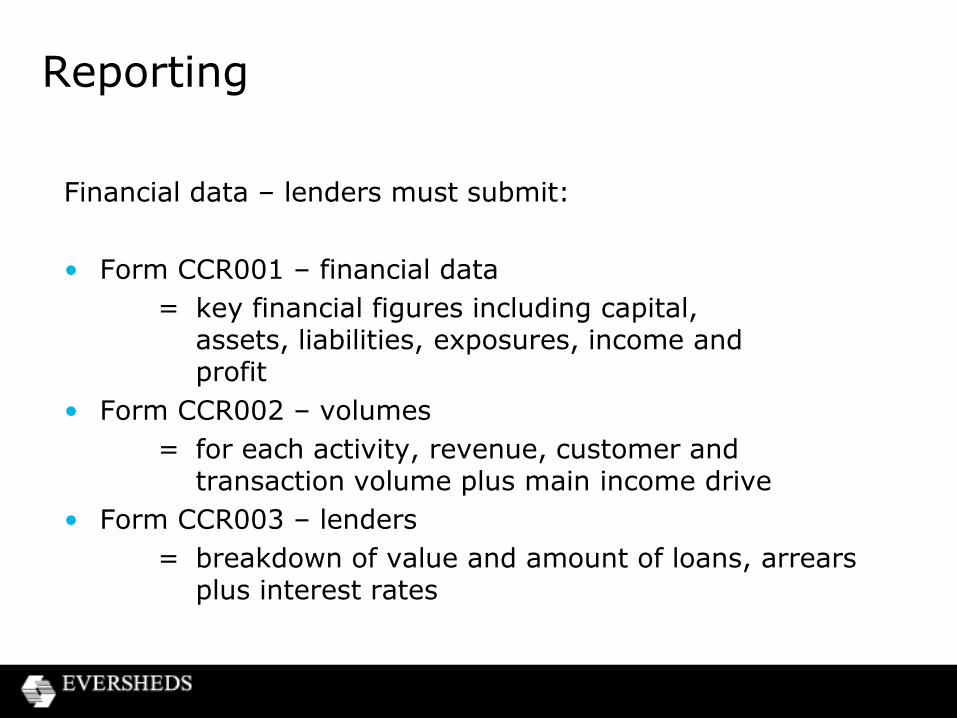

Reporting

Financial data – lenders must submit:

• Form CCR001 – financial data

= key financial figures including capital, assets, liabilities, exposures, income and profit

• Form CCR002 – volumes

= for each activity, revenue, customer and transaction volume plus main income drive

• Form CCR003 – lenders

= breakdown of value and amount of loans, arrears plus interest rates

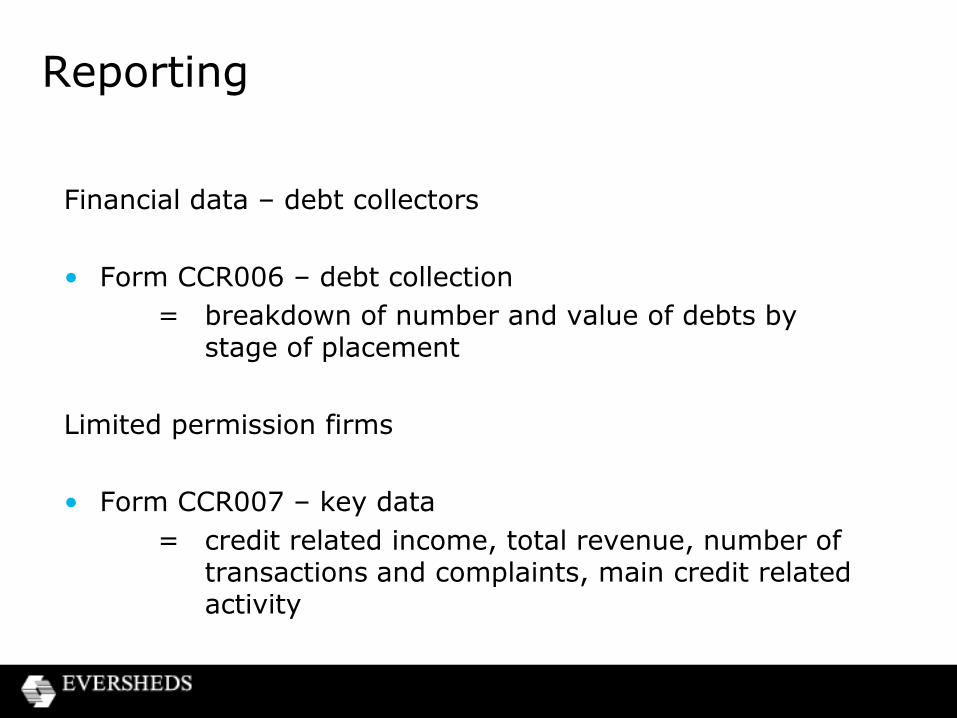

Reporting

Financial data – debt collectors

• Form CCR006 – debt collection

= breakdown of number and value of debts by stage of placement

Limited permission firms

• Form CCR007 – key data

= credit related income, total revenue, number of transactions and complaints, main credit related activity

Reporting

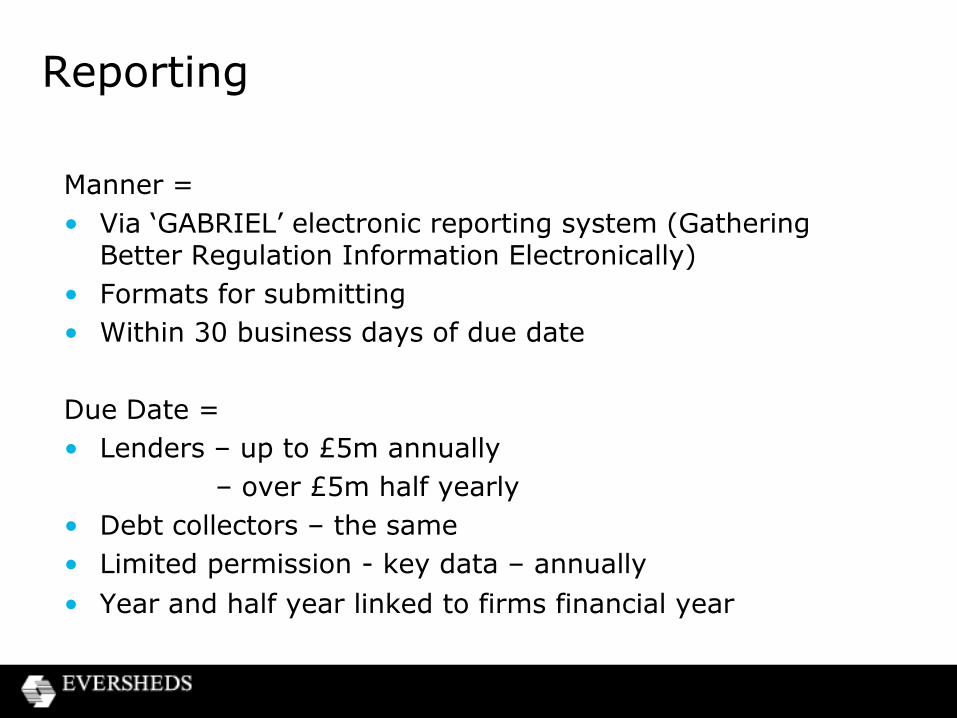

Manner =

• Via ‘GABRIEL’ electronic reporting system (Gathering Better Regulation Information Electronically)

• Formats for submitting

• Within 30 business days of due date

Due Date =

• Lenders – up to £5m annually

– over £5m half yearly

• Debt collectors – the same

• Limited permission - key data – annually

• Year and half year linked to firms financial year

Reporting

Product sales data

• High cost short-term credit and home collected credit only

= Loan amount, term, interest rate and fee, rollover information, reason for loan (if known), date of birth and postcode of borrower, borrower and household income, borrower status e.g. marital, residential, employment, car

Reporting

Complaints

• All firms record complaints data from 1 April 2014

• No change during interim permission period

• From full authorisation/limited permission stage:

– reporting – as per previous slides and forms

– publishing

larger firms = if 500 or + complaints in 6 month period (broken down by category)

smaller firms/interim permission = if 1,000 or + complaints in 12 month period (no breakdown)

Reporting

Control notifications

Full authorisation

• Non –directive firm (i.e. not banks, insurance companies and MiFID investment firms)

– person decides to acquire 20% or more of shares or voting power or shares/votes giving significant influence over management (firm or its parent undertaking)

– existing controller decides to act so will fall outside these criteria

• Think laterally e.g. insisting an intermediate holding company requires approval

Reporting

Control notifications

Limited permission 33% trigger rather than 20% on same basis

Reporting

Control notifications

• Section 178 notification required to FCA

• FCA 60 days to agree

• If approved – advise FCA once happened

Greg Brandman, Partner, Eversheds LLP

Adam Berry, Associate, Eversheds LLP

October 2013

Consumer Finance Seminar

Governance, Culture and Enforcement

OFT to FCA – Implications of changing regulator

• A new approach to supervision

• Principles-based, outcomes-focused regulation

• A lower conduct risk appetite

– more intervention, earlier

– implications for product governance

• A new, more sophisticated regulatory tool kit

• A better-resourced enforcement division

– rules will be enforced by the FCA

– patchy compliance is no longer an option

– individuals, not just the firm, are exposed

Governance - FCA focus

• Stated aim:

“to see how effectively a firm identifies, manages and reduces conduct risk.”

Governance and Culture

• FCA’s approach informed by lessons learned from the financial crisis

• Governance is key to prudential risk

• Culture is seen as key to governance and conduct risk

• Paragraph 4.27 of CP 13/10

For consumer credit firms “...the assessment of governance and

culture will be crucial, as these are key factors that drive whether a firm treats its customer fairly.”

Good governance: The FCA’s vision of an effective board

• Asks the “what if” questions

– understands the business model

– understands and focuses on material risks

– effectively challenges executive on execution of the strategic plan

– quality MI essential for this

• Sets the right tone re culture and ethics

– communicates this to the business

– incentivises the right behaviours

– deals effectively with transgressors

Governance: Role of the NEDs

• “An important and unique role to influence firm behaviour”

• A key role in providing challenge to the executive

– being willing to ask the difficult questions (and demand satisfactory answers)

• NEDs have a “pivotal” role in delivering fair treatment for customers of retail firms

FCA’s expectations of NEDs at retail firms

• Risk identification is about identifying risks to the firm and its shareholders and also to customers:

– does the firm have a customer strategy?

– is the business model geared towards delivering good outcomes for customers?

– who are your customers /their needs; are the products you are selling to them appropriate?

– sales incentives driving the right behaviours?

– is potential impact on customers duly considered when making strategic decisions?

FCA focus on Culture

• A firm’s culture shapes judgements, ethics and behaviours displayed at key moments

• A firm’s cultural characteristics are a key driver of potentially poor behaviour

• Clive Adamson, FCA Director of Supervision

“ In many cases where things have gone wrong, whether it is mis-selling of PPI or in attempting to manipulate LIBOR, a cultural issue is at the heart of the problem”

FCA messaging on culture

• Culture can only be established /changed by the CEO and senior management

• Key cultural levers

– supporting the right behaviours

– embedding them in business practices through performance management, training and reward programmes

How will the FCA assess culture ?

• Conclusions to be drawn from empirical observation

• Key cultural indicators include:

– customer sales experience

– how customer complaints are dealt with

– how the firm deals with regulatory issues

– the firm’s product governance process

– remuneration structures, sales incentives and performance management in practice

FCA approach to supervision

• Roll-out of supervision for CC firms “will be aligned with the FCA supervision model” (CP13/10)

• New categories of firms:

– C1 to C4 (size and impact)

– For C1 firms, the FCA will carry out firm-by-firm business model and strategy analysis

– Event-driven approach to firms with interim permission

– Thematic supervision of specific issues

• Firm Systematic Framework replaces ARROW

– To allow FCA to assess firms’ conduct risks and asks:

– “Are the interests of customers and market integrity at the heart of how the firm is run ?”

Firm Systematic Framework

“The FSF assessment process will help us come to a view about the extent to which a firm embeds fair treatment of customers and market integrity in the way it is run. This, at the most intensive end of assessment, covers the product/service lifespan from design through to sales/service delivery and after sales/service handling. The assessment of governance and culture will be crucial, as these are key factors that drive whether a firm treats its customer fairly.” (CP13/10, para 4.27)

Supervisory focus on the business model

• Supervisors to understand where the money is made

• Does the BM achieve a fair deal for consumers?

• New BM threshold condition?

• Firms will be expected to base their business models, their culture and how they run their business on a foundation of TCF

• Presumption that supervisors will intervene if they believe that a firm’s judgment is at variance with the regulator’s objectives

Behavioural economics – implications for consumer credit lending ?

• Product design, marketing and sales processes can accentuate the effects of human biases

• Caveat emptor principle difficult to justify in relation to complex financial products with a long time horizon and significant information asymmetries between buyer and seller

• “Huge scope to use BE to understand consumer decisions and to improve regulation”

• This area will be a “hugely important feature of the new regulatory system” Martin Wheatley, CEO FCA 2013

• “Firms who want their customers to make the right decisions” will cooperate

OFT to FCA: implications for enforcement

• FCA will apply the same general enforcement approach to consumer credit activities as to other regulated activities – no need to amend Handbook

• FCA penalties policy will apply to disciplinary action in respect of retained elements of the CCA

• FCA will enforce MLRs from 1 April 2014

– other AML implications

• All CC firms must establish and maintain appropriate financial crime systems and controls

• Getting to grips with the FCA’s Financial Crime Guide

The sharp end of enforcement

• Transition has serious implications for firms and individuals

– FCA’s penalty regime

– Approved persons also within disciplinary jurisdiction of the FCA

• The FCA’s focus is increasingly on senior management accountability

• “Fining firms is not enough ... In order to achieve credible deterrence, senior managers must be held to account” Tracey McDermott (June 2013)

• FCA will consider investigating SIFs when investigating every serious systemic failure

• More actions now against individuals than firms

Consumer Finance Seminar Compliance

Graham Richardson, Practice Group Head, Eversheds LLP Lee O’Connell, Head of Legal and Compliance Consulting, Eversheds LLP October 2013

FCA Compliance Implementation

The following questions need to be answered when considering FCA Compliance:

Questions:

Are the interests of the customers and market integrity at the heart of the how your firm

is run?

Are you able to demonstrate through evidence that your services are

compliant, well run, fit and proper and has a suitable sustainable

business model (higher-risk firms)?

Can you demonstrate through evidence the robustness of your

compliance arrangements in protecting your customers, your

stakeholders, your staff and satisfying the regulator?

Categorisation and supervision in practice Categorisation in practice:

C1 and C2 firms

– “fixed portfolio” – dedicated supervisor

C3 and C4 firms

– “flexible portfolio” – no dedicated supervisor, supervised by a team sector

specialists

Supervisory Framework – the impact:

C1 – firm by firm business model and strategy analysis

C2 - group of similar firms identifying common risks

C3 – sample of firms business model across sector

C4 – less intensive assessment

Focus areas to be addressed - 1 • Business model, strategy and culture

- risk-based business model, compliance risk early warning system, ethical compliance training, suitable management and appropriately trained resources

• Product design and governance (CONC 3/4)

- lessons learnt from similar products, someone as the “voice of the customer”,

“root-cause” analysis, customer experience, TCF, unfair terms and meeting needs

• Sales (CONC 5)

- affordability assessments, responsible lending, CPA’s, incentives

and remuneration structures, fit for purpose sales oversight

• Fair treatment of customers and market integrity (CONC 4/5)

- suitability, no “hard sell” - monitoring outcomes, clear, fair and not

misleading information, transparency

Focus areas to be addressed - 2

• Post sales process (CONC 4/6/7)

- Embedded TCF, call monitoring, feedback, arrears strategy, supervision, monitoring, retraining, quality auditing and control, non-compliant procedures

• Complaints

- handling, root cause analysis, feedback loops, retraining and regulatory reporting

• Risk frameworks

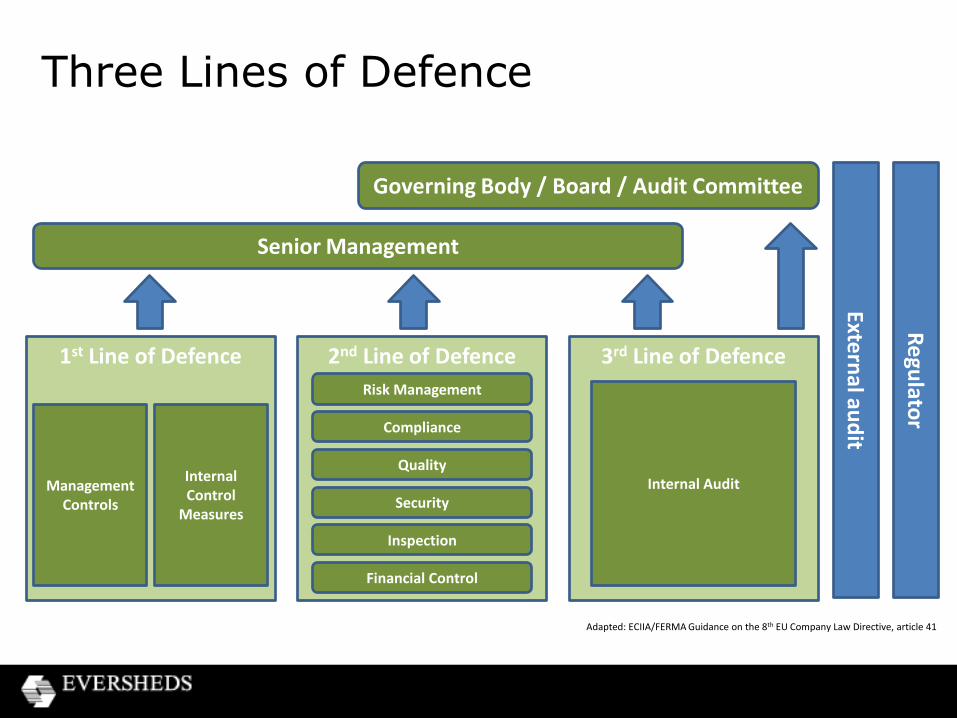

- three lines of defence model

• Policies, procedures, reporting & record keeping

- documented, accessible, trained and data management

Focus areas to be addressed - 3

• FCA Relationship

- regular interaction, compliance reporting, dealing with requests and reporting issues

• BCP

- business survival plan including customer impact and control process

Compliance Reporting Regimes Summary

Effective: 1 October 2014

Application: fully authorised firms only

Frequency: depending on size of firm, annual or 6 monthly (aligned to firms year end)

Process: e-reporting system “GABRIEL”

Timing: 30 business days

Two key components:

• Regulatory reporting; and

• Product sales data reporting (PSD) – to include lenders of

high cost short term credit and home collected credit

Already authorised will not to need to resend data already submitted

eg Financial Information

Three Lines of Defence

Governing Body / Board / Audit Committee

Senior Management

1st Line of Defence

2nd Line of Defence 3rd Line of Defence

Internal Control

Measures

Risk Management

Compliance

Quality

Security

Inspection

Financial Control

Internal Audit Management Controls

Extern

al aud

it

Re

gulato

r

Adapted: ECIIA/FERMA Guidance on the 8th EU Company Law Directive, article 41

Seven Elements of Compliance

The seven elements considered fundamental to an effective compliance programme are:

1. Written polices and procedures

2. Defined responsibility and oversight

3. Effective training and awareness

4. Effective lines of communication

5. Internal monitoring and auditing

6. Reporting and responding

7. Promotion and enforcement

Adapted:

US Federal Sentencing Guidelines for Organisations'

OECD Good Practice Guidance for Internal Controls, Ethics and

Compliance

Consumer Finance Seminar A few recent developments - OFT, FOS, the

courts and CMCs

Chris Busby, Partner, Eversheds LLP October 2013

Overview

• OFT news

– power to suspend credit licence used

– requirements in relation to charging orders

• Financial Ombudsman Service

– claims trends

– publication of decisions

• The courts

– the Binns case

– section 75 claims

• Claims farmers

– new regulatory powers

OFT uses suspension powers for the first time

• New power granted under Financial Services Act 2012

• Guidance issued in February 2013

• OFT can now suspend consumer credit licences with immediate effect

• 3 requirements to be met:

– urgent need to protect customers

– potential for harm

– it must be necessary to suspend

• Power exercised for the first time on 17 June

2013 against Donegal Finance Limited

Charging order requirements imposed NatWest and RBS affected

• Requirements issued to address concerns about how some

customer debts are enforced via charging orders

• Concerns stemmed from:

– failure to consider customers’ financial circumstances; and

– proportionality of the approach

• Requirements imposed which required the

banks to act in a fairer manner

• Potential financial sanctions if not followed

FOS news

• Latest statistics (April – June 2013)

– Top 5 products – PPI, current accounts, mortgages, credit cards, car insurance

– 70% in favour of consumer

– 2,000 PPI complaints per day, second wave trend

• Trends – packaged accounts, insurance add-ons

• Publication of decisions commenced

– all ombudsman decisions post 1 April 2013

– useful search engine

– any negative repercussions?

The courts – July 2013 decision Binns v Firstplus Financial Group plc

• Binns complained re. mis-selling of PPI

• Firstplus offered full compensation, but not legal costs

• Claimant issued proceedings to recover legal costs

• Firstplus argued abuse of process

• On appeal, High Court agreed with Firstplus – it was

not reasonable to bring a claim which has already

received full redress via ADR

• ‘Full redress’ relates to matters intrinsic to the

case, not costs adjunctive to it

• Very useful decision where proceedings are a

vehicle for building and recovering costs

The courts – section 75 CCA Lessons from PIP implant claims so far

• A few claimant firms bringing most claims

• Typically pre-April CFA and sometimes ATE insurance

• GLO for clinics established – should s75 defendants be joined?

• Consider tactics in such claims

– s75 issues

– liability for underlying claim

– legal costs

– co-ordination between Defendants

• Co-ordination between legal and complaint

handling teams

• Likely future post Jackson reforms?

Claims management companies Recent news

• Conduct of Authorised Persons Rules – changes effective from 8 July 2013

– no reference to MoJ

– standard terms must be on website

– written signature on terms required before taking payment

– must inform customers of variation or suspension

of authorisation

• Trends

– 180 more CMCs operate in financial

products claims this year – total 1155

– 94% of consumer complaints to MoJ in this area

– Consumers increasingly bring own claims

Complaints round table discussion Friday 6 December 2013 (10am – 12 noon)

• Join Eversheds, Kevin Rousell, the MoJ’s Head of Claims Management Regulation and Caroline Wayman, Legal Director & Principal Ombudsman at FOS

• Topics will include:

– developments around the MoJ’s regulation of CMCs

– recent trends in FOS claims

– review of impact of publication of FOS decisions

– new claims areas and likely developments

• Opportunity to put questions in advance

• Contact Chris Busby or Rebecca Nicholas