consolidated financial statements years ended december …€¦ · the accompanying consolidated...

TRANSCRIPT

APPALACHIAN MOUNTAIN CLUB

CONSOLIDATED FINANCIAL STATEMENTS YEARS ENDED DECEMBER 31,2011 AND 2010

tonneson + CO Certified Public Accountants & Consultants

APPALACHIAN MOUNTAIN CLUB

TABLE OF CONTENTS

INDEPENDENT AUDITORS' REPORT

FINANCIAL STATEMENTS

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

CONSOLIDA TED STATEMENTS OF ACTNITIES

CONSOLIDA TED STATEMENTS OF CASH FLOWS

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

PRINTED ON RECYCLED PAPER

2

3

4

5 - 13

INDEPENDENT AUDITORS' REPORT

Board of Directors Appalachian Mountain Club Boston, Massachusetts

We have audited the accompanying consolidated statements offmancial position of the Appalachian Mountain Club and affiliates as of December 31, 2011 and 2010, and the related consolidated statements of activities and cash flows for the years then ended. These fmancial statements are the responsibility of Appalachian Mountain Club's management. Our responsibility is to express an opinion on these fmancial statements based on our audits.

We conducted our audits in accordance with U.S. generally accepted auditing standards. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the fmancial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated fmancial statements referred to above present fairly, in all material respects, the consolidated financial position of the Appalachian Mountain Club and affiliates as of December 31,2011 and 2010, and the changes in their net assets and cash flows for the years then ended in conformity with U.S. generally accepted accounting principles.

Tonneson + Co

May 17,2012

tonneson co Certified Public Accountants & Consultants

401 Edgewater Place, Suite 300, Wakefield, MA 01880-6208 t. 781.245.9999 f . 781.245.8731 www.tonneson.com

- 1 -

APPALACHIAN MOUNTAIN CLUB

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

DECEMBER 31,2011 AND 2010

2011 2010 Assets:

Cash and Cash Equivalents $ 5,249,275 $ 3,655,624 Accounts Receivable, less allowance for doubtful accounts

of$23,730 in 2011 and $24,000 in 2010 516,384 431,364 Pledges Receivable 907,349 4,155,136 Prepaid Expenses 300,291 441 ,963 Inventories 656,485 576,200 Notes Receivable 11,065,000 23 ,065,000 Propelty and Equipment, net 40,282,103 41,035,142 Investments, at market 53 ,852,213 53 ,488,309

Total Assets $ 112,829,100 $ 126,848,738

Liabilities: Accounts Payable $ 546,180 $ 469,719 Accrued Expenses and Other Liabilities 850,082 1,993,073 Annuity Payments Liability 576,131 614,144 Deferred Revenue 844,614 708,626 Loans Payable 14,550,000 31,050,000

Total Liabilities 17,367,007 34,835,562

Net Assets: Unrestricted 80,099,267 71,559,034 Temporarily Restricted 12,131,167 17,289,502 Permanently Restricted 3,231,659 3,164,640

Total Net Assets 95,462,093 92,013 ,176

Total Liabilities and Net Assets $ 112,829,100 $ 126,848,738

See Notes to Conso lidated Financial Statements. - 2 -

APPALACHIAN MOUNTAIN CLUB

CONSOLIDATED STATEMENTS OF ACTIVITIES

YEARS ENDED DECEMBER 31, 2011 AND 2010

2011 2010

Unrestricted Temporarily Permanently Unrestricted Tempo,-arily Permanently

O~erating Other Restricted Restricted Total O~erating Other Restricted Restricted Total

Reve nues:

Contributions and Gifts $ 2,710, 109 $ 5, 127,652 $ 894,869 $ 110,984 $ 8,843 ,614 $ 2,536,399 $ 701 ,585 $ 2,056,883 $ 257,585 $ 5,552,452

Debt Forgiveness 4,072,962 4,072,962

Membership 2,965, 136 2,965, 136 2,879,314 2,879,314

Outdoor Program Centers 9,241 ,654 14,442 9,256,096 9,154,800 912 9,155,712

Programs 2,572,219 326,884 2,899,103 2,561 ,230 351 ,634 8, 188 2,921 ,052

Publications 710,969 710,969 722,267 722,267

Income from Investments 1,092,674 178,365 1,271 ,039 1,095,918 161 ,250 1,257, 168

Gains (Losses) from Investments, net (714,925) (359,209) (43,965) (1 ,118,099) 3,634,023 1, 187,087 37,689 4,858,799

Endowment Spending Allocation 1,861 ,551 (1 ,861 ,551) 1,809,044 (1 ,809,044)

Special Project Funding 1,889,288 (1 ,889,288) 938,222 (938,222)

Total Revenues 21 ,950,926 6,168,850 714,025 67,019 28,900,820 20,601 ,276 3,036,806 3,4 13,408 295,274 27,346,764

Expenses:

Member Services 2,742,287 2,742,287 2,469,946 8,343 2,478,289

Outdoor Program Centers 9,654,398 172,935 9,827,333 9,325,741 143,944 9,469,685

Programs 5,782,176 7, 105 5,789,281 5,217,749 5,121 5,222,870

Publications 643,454 4,968 648,422 613 ,555 6,235 6 19,790

Administrative 1,950,045 88,028 2,038,073 1,786,454 59,330 1,845,784

Fundraising 1,073,159 158,097 1,231 ,256 1,066,260 178,954 1,245,214

Interest Expense 675,251 675,251 706,501 706,501

Reduction in Land Carrying Value 2,500,000 2,500,000

Total Expenses 21 ,845,519 3,606,384 25,451 ,903 20,479,705 1,108,428 21 ,588,133

Cha nge in Net Assets Before Transfers and Releases 105,407 2,562,466 714,025 67,019 3,448,917 121 ,571 1,928,378 3 ,413 ,408 295,274 5,758,631

Transfers and Releases:

Transfer of Operating Surplus (105,407) 105,407 (121 ,571) 121 ,571

Releases of Restricted Net Assets 5,872,360 (5 ,872,360) 2,482,640 (2,482,640)

Total C hange in Net Assets 8,540,233 (5, 158,335) 67,019 3,448,917 4,532,589 930,768 295 ,274 5,758,63 1

Net Assets, Beginning of Year 71 ,559,034 17,289,502 3,164,640 92,013,176 67,026,445 16,358,734 2,869,366 86,254,545

Net Assets, End of Yea r $ $ 80,099,267 $ 12,131 ,167 $ 3,231 ,659 $ 95,462,093 $ $ 71 ,559,034 $ 17,289,502 $ 3,164,640 $ 92,013,176

See Notes to Consolidated Financial Statements_ - 3 -

APPALACHIAN MOUNTAIN CLUB

CONSOLIDATED STATEMENTS OF CASH FLOWS

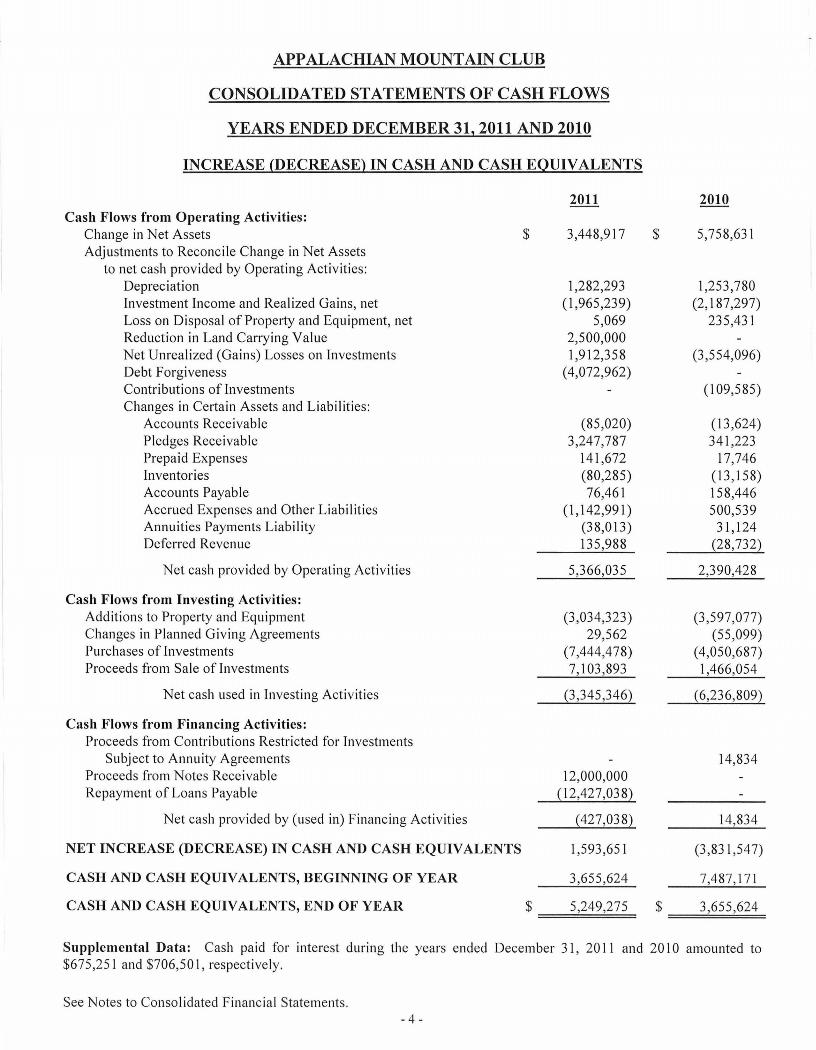

YEARS ENDED DECEMBER 31,2011 AND 2010

INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS

Cash Flows from Operating Activities: Change in Net Assets Adjustments to Reconci le Change in Net Assets

to net cash provided by Operating Activities: Depreciation Investment Income and Realized Gains, net Loss on Disposal of Property and Equipment, net Reduction in Land Carrying Value Net Unrealized (Gains) Losses on Investments Debt Forgiveness Contributions of Investments Changes in Certain Assets and Liabilities:

Accounts Receivable Pledges Receivable Prepaid Expenses Inventories Accounts Payable Accrued Expenses and Other Liabilities Annuities Payments Liability Deferred Revenue

Net cash provided by Operating Activities

Cash Flows from Investing Activities: Additions to Property and Equipment Changes in Planned Giving Agreements Purchases of Investments Proceeds from Sale of Investments

Net cash used in Investing Activities

Cash Flows from Financing Activities: Proceeds from Contributions Restricted for Investments

Subject to Annuity Agreements Proceeds from Notes Receivable Repayment of Loans Payable

Net cash provided by (used in) Financing Activities

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS

CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR

CASH AND CASH EQUIVALENTS, END OF YEAR

2011

$ 3,448,9 17

1,282,293 (1 ,965 ,239)

5,069 2,500,000 1,912,358

( 4,072,962)

(85 ,020) 3,247,787

141,672 (80,285) 76,461

(1,142,991) (38,013) 135,988

5,366,035

(3,034,323) 29,562

(7,444,478) 7,103 ,893

{3 ,345,346}

12,000,000 {12,427,038}

{427,038}

1,593 ,651

3,655 ,624

$ 5,249,275

2010

$ 5,758,631

1,253,780 (2,187,297)

235,431

(3,554,096)

(109,585)

(13,624) 341,223

17,746 (13,158) 158,446 500,539

31,124 {28,732}

2,390,428

(3,597,077) (55 ,099)

(4,050,687) 1,466,054

{6,236,809}

14,834

14,834

(3,831,547)

7,487,171

$ 3,655,624

Supplemental Data: Cash paid for interest during the years ended December 31, 2011 and 2010 amounted to $675,251 and $706,501, respective ly.

See Notes to Consolidated Financial Statements. - 4 -

APPALACHIAN MOUNTAIN CLUB

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31, 2011 AND 2010

A. Organization:

The Appalachian Mountain Club, together with its consolidated affiliates (collectively, the "AMC"), is a not-forprofit environmental conservation and recreation corporation with the mission of promoting the protection, enjoyment and understanding of the mountains, forest, waters, and trails of the Appalachian Region. In pursuit of this aim it provides educational and experiential opportunities to its membership and the general public in the belief that successful conservation depends on this experience. Backcountry shelter and lodging facilities, trail maintenance programs, land stewardship, scientific research, environmental conservation, and local chapter activities together with the publication of guidebooks, maps, and a variety of other publications further this mission .

B. Summary of Significant Accounting and Reporting Policies:

The significant accounting policies followed by the AMC are as follows:

Basis of Presentation

The accompanying consolidated financial statements include the accounts of the AMC, its affiliates, and its volunteer-managed facilities and chapters. All significant intercompany accounts and transactions are eliminated in the consolidated financial statements.

Estimates

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities . Significant estimates for the AMC include the present value of future cash flows from pledges receivable, the allowance for doubtful accounts in connection with pledges receivable, allowances for inventory obsolescence and accrued liabilities, and the fair value of investments. Actual results could differ from those estimates.

Basis of Accounting

The accompanying consol idated financial statements of the AMC for the years ended December 31, 2011 and 2010 are prepared on the accrual basis of accounting in accordance with U.S . generally accepted accounting principles. Contributions received, including unconditional promises to give, are recognized as revenues in the period received at their fair values. Restricted contributions that are received and expensed in the current year for the restricted purpose are recorded as unrestricted contributions.

Net assets are reported by classification based on the existence or absence of donor imposed restrictions :

Unrestricted net assets include all resources which are not subject to donor-imposed restrictions. Activity in unrestricted net assets is shown in the Consolidated Statements of Activities classified as Operating and Other. Unrestricted-Operating revenues consist of revenues, endowment spending allocations, and special project funding which supp0l1 annual operating and program expenses of the organization. Unrestricted-Operating expenses consist of annual operating expenses of the organization related to member services, outdoor program centers, other programs, publications, administrative, and annual fundraising. Unrestricted-Other revenues and expenses include unrestricted revenues and expenses from capital fundraising campaigns, income and gains (losses) from investments, interest expense and other financing costs, allocation of a portion of depreciation expense reflecting asset acquisitions that are funded through donor contributions, and the reduction in land carrying value in 2011 (see note G).

- 5 -

APP ALACHIAN MOUNTAIN CLUB

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31,2011 AND 2010

Summary of Significant Accounting and RepOiting Policies, Continued

Basis of Accounting, Continued

Temporarily restricted net assets carry specific, donor-imposed restrictions on the expenditure or other use of contributed funds . Temporary restrictions may expire either because of the passage of time or because certain actions are taken by the AMC which fulfill the restrictions. When a donor restriction expires, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the Consolidated Statements of Activities as use of restricted funds.

Temporarily restricted net assets consist of the following at December 31 ,20 II and 20 I 0:

Accumulated appreciation on permanently restricted net assets Funds for future operations and programs Donor pledges receivable

$

$

2011

3,659,234 7,564,584

907,349

12,131 ,167

$

$

2010

3,920,457 9,213,909 4,155,136

17,289,502

Permanently restricted net assets are those that are subject to donor-imposed restrictions which will never lapse, thus requiring that the funds be retained permanently. Permanently restricted net assets consist of the original gift value of investments to be held indefinitely as endowment, the income of which is available to support celtain operations of the Appalachian Mountain Club.

Investments

Investments are carried at fair value based upon quoted market prices, when available, or estimates of fair value in the Consolidated Statements of Financial Position. Dividends, interest and net gainsllosses on investments are reflected in the Consolidated Statements of Activities. Investment income from restricted assets that is earned and used in the current year for the restricted purpose is recorded as unrestricted investment income.

Planned Giving Agreements

The AMC has planned giving agreements with donors consisting primarily of charitable gift annuities and pooled life income funds. Assets are invested and payments are made to donors and/or other beneficiaries in accordance with the agreements.

Contribution revenue is recorded as restricted income when the agreements are executed, measured by the fair value of assets received net of the liabilities for future payments to donors . Investments are adjusted to fair value, and the liabilities for future payments are adjusted based on donor life expectancies and on prevailing interest rates.

Cash Equivalents

Cash equivalents are comprised of highly liquid investments, with a maturity of less than three months at the time of investment. This may include money market deposits or other similar investments.

- 6 -

APP ALACHIAN MOUNTAIN CLUB

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31,2011 AND 2010

Summary of Significant Accounting and Reporting Policies, Continued

Accounts Receivable

Accounts receivable are stated at the amount management expects to collect from outstanding balances. The allowance for doubtful accounts is determined by applying a percentage against total receivables, based on management's judgment concerning the future collectability of the receivables. Amounts considered to be past due are charged against the allowance when the account is referred to a collection agency, or otherwise deemed uncollectible.

Inventories

Inventories, principally retail merchandise and books, are stated at the lower of cost (on an average cost method) or market.

Propelty and Equipment

Property and equipment are recorded at historical cost or fair value at date of gift or bequest. Major renewals and improvements are capitalized, while maintenance and repairs are expensed when incurred. Depreciation is determined using the straight-line method over the estimated useful lives . Estimated lives for building and improvements, land improvements, furniture, fixtures, and equipment range from 3 to 40 years.

Donated Services

The financial statements do not include amounts for donated services since an objective basis for measurement of the value of such services is not available, and these services are not specialized as defined by U.S . generally accepted accounting principles; however, substantial numbers of volunteers have donated significant amounts of their time and energy to the AMC.

Concentration of Credit Risk

Financial instruments which potentially subject the AMC to concentrations of credit risk consist principally of cash and cash equivalents and short term investments. The Organization is not aware of any concentrations of credit risks as of December 31, 20 II and 20 I O.

Tax Status

The AMC has been granted a tax exemption under Section 501(c)(3) of the Internal Revenue Code. In determining the recognition of uncertain tax positions, the AMC recognizes the financial statement impact of a tax position when it is more likely than not that the position will be sustained upon examination by a taxing authority. As of December 31, 20 II, the AMC has no uncertain tax positions that qualify for either recognition or disclosure in the consolidated financial statements.

Subsequent Events

The date to whieh events occurring after December 31, 20 II have been evaluated for possible adjustment to the consolidated financial statements or disclosure is the date of the Independent Auditors' Report which is the date the consolidated financial statements were available to be issued.

- 7 -

C.

APPALACHIAN MOUNTAIN CLUB

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31,2011 AND 2010

Investments:

The following table summarizes the AMC's financia l assets measured at fair value as of December 31, 2011 and December 31,2010:

2011 2010

Quoted Prices Quoted Prices in Active in Active

Markets for Markets for Identical Unobservable Identical Unobservab le

Assets Inj2uts Assets Inj2uts

Uninvested Cash and Cash Equivalents Pending Investment $ 855 ,853 $ $ 4,446,737 $

Mutual Funds: U.S. Equity 14,761,814 13,391,024 Non-U.S. Equity 9,375,207 9,571 ,4 14 U.S . Fixed Income 15 ,401,142 12,659,368 Non-U.S . Fixed Income 2,733,574 2,743 ,2 15 Blended 841 ,245 771,981

Alternative Investments: Marketable A lternatives 5,870,540 6,127,834 Private EquityiVenture Capital 3,110,913 2,736,772

Split Interest Agreements: Gift Annuity Fund 572,335 621,524 Pooled Life Income Fund 329,590 418,440

$ 44,870,760 $ 8,981 ,453 $ 44,623 ,703 $ 8,864,606

The fair value of publicly traded mutual funds is based upon quoted market prices and net asset values. Amounts held as alternative investments represent hedge funds and private equity paltnerships for which quoted market prices or va luations are not readily available and are carried at estimated fair values provided by investment managers. The following are the changes in alternative investments measured at fair value for the years ended December 31, 2011 and December 31 , 2010:

Beginning ba lance Total gains (realized/unrealized) Total investment income (loss) , net Purchases and capital cal ls Sales and distributions

Ending balance

$

$

- 8 -

Fair Value Measurements Using Significant Unobservable Inputs

2011 2010

8,864,606 $ 9,734,504 7,393 1,219,308

(14,335) 1,976 503,405 873 ,65 1

(379,616) (2,964,833)

8,981 ,453 $ ==8=,8::::::64=,=60=6=

D.

APPALACHIAN MOUNTAIN CLUB

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31,2011 AND 2010

Investments, Continued

The components of gains (losses) from investments for the years ended December 31, 2011 and 2010 are as follows:

2011 2010

Realized gains, net $ 924,520 $ 1,252,252 Unrealized gains (losses), net (1,941,920) 3,554,096 Change in value of planned giving

agreements {I 00,699~ 52,451

Total gains (losses), net $ (1,118,099) $ 4,858,799

Pledges Receivable:

Pledges receivab le of $907,349 and $4,155,136 are recorded in the consolidated financial statements as of December 31, 2011 and December 31,20 10, respectively. Pledges are recorded at the present value of estimated future cash flows. The present va lue of est imated future cash flows has been measured uti lizing a risk free-rate of return (1.6% at December 31,20 II and 3.2% at December 31,2010). The resulting discount amounted to $30,481 at December 31 , 2011 and $81,028 at December 31, 2010. An allowance of $100,817 has been made for potentially unfu lfilled pledges at December 31 , 20 11 and $461,682 at December 31,2010.

Pledges, net of discounts and allowances, are expected to be collected as fo llows:

In one year or less Between one and five years Greater than five years

Total Pledges Receivable

$

$

352,5 62 $ 529,831

24,956

907,349 $

3,388,028 745,103

22,005

4,155,136

E. Endowment:

The AMC's endowment consists of approximately 90 individual funds estab lished for a variety of purposes. It includes both donor-restricted endowment funds and funds designated by the Board of Directors to function as endowments. As required by U.S. general ly accepted accounting principles, net assets associated with endowment funds , inc luding funds designated by the Board of Di rectors to function as endowments, are classified and reported based on the existence or absence of donor-imposed restrictions.

The AMC interprets the Uniform Prudent Management of Institutional Funds Act (UPMlFA) as requiring the preservation of the fair value of the original gift as of the gift date of the donor-restricted endowment funds absent explicit donor stipulations to the contrary. As a result, the AMC classifies as permanently restricted net assets (a) the origina l va lue of gifts donated to the permanent endowment, (b) the origina l value of subsequent gifts to the permanent endowment, and (c) accumu lations to the permanent endowment made in accordance with the direction of the applicable donor gift instrument at the time the accumulation is added to the fund. The remaining pOltion of the donor-restricted net assets is classified as temporarily restricted net assets until those amounts are appropriated for expenditure by the AMC.

- 9 -

APPALACHIAN MOUNTAIN CLUB

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31,2011 AND 2010

Endowment, Continued

In accordance with UPMIFA, when making a determination to appropriate or accumu late donor-restricted endowment funds , the AMC cons iders factors which include: the duration and preservation of the fund; the purposes of the AMC and the donor-restricted endowment fund; general economic conditions; the possible effect of inflation and deflation; the expected tota l return from income and the appreciation of investments; other resources of the AMC; and the investment policies of the AMC.

The endowment net assets composition by type of fund as of December 31, 2011 and 2010 is as follows:

2011 Temporarily Permanently

Unrestricted Restricted Restricted Total

Donor restricted endowment funds $ $ 8,530,485 $ 3,23 1,659 $ 11,762,144 Board designated endowment funds 38,726,590 38,726,590

Endowment Net Assets, End of Year $ 38,726,590 $ 8,530,485 $ 3,231,659 $ 50,488,734

2010 Temporarily Permanently

Unrestricted Restricted Restricted Tota l

Donor restricted endowment funds $ $ 9,384,622 $ 3,164,640 $ 12,549,262 Board designated endowment funds 38,006,245 38,006,245

Endowment Net Assets, End of Year $ 38,006,245 $ 9,384,622 $ 3,164,640 $ 50,555,507

The changes in endowment net assets for the years ended December 31,2011 and 2010 are as follows:

2011 Temporarily Permanently

Unrestricted Restricted Restricted Total

Endowment Net Assets, Beginning of Year $ 38,006,245 $ 9,384,622 $ 3,164,640 $ 50,555,507 Net assets released from restriction 376,446 (376,446) Investment income and gains (losses), net 107,910 (80,105) (43,965) (16,160) Contributions and transfers 2,097,140 (397,586) 110,984 1,810,538 Appropriations of cumulative ga ins ~1,861,15 1 2 ~1,861, 1 512

Endowment Net Assets, End of Year $ 38,726,590 $ 8,530,485 $ 3,231,659 $ 50,488,734

2010 Temporarily Permanently

Unrestricted Restricted Restricted Total

Endowment Net Assets, Beginning of Year $ 32,030,489 $ 8,506,265 $ 2,869,366 $ 43,406,120 Net assets released from restriction 410,651 (410,65 1) Investment income and gains, net 4,195,205 1,286,036 37,689 5,5 18,93 0 Contr i butions 3,178,944 2,972 257,585 3,439,501 Appropriations of cumulative gains ~1 ,809,0442 ~1,809,0442

Endowment Net Assets, End of Year $ 38,006,245 $ 9,384,622 $ 3,164,640 $ 50,555,507

- 10 -

APPALACHIAN MOUNTAIN CLUB

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31,2011 AND 2010

Endowment, Continued

From time to time, the fair value of assets associated with individual donor-restricted endowments may fa ll below the level that the donor or the UPMIF A requires the AMC to retain as a fund for perpetual duration. In accordance with U.S. generally accepted accounting principles, deficiencies of this nature that were repOJied in unrestricted net assets as of December 31, 2011 are $603. There were no deficiencies reported in unrestricted net assets as of December 31,2010 .

The AMC's investment goal for the Endowment Fund is to provide a current spendable return consistent with the long-term preservation of assets in real terms. Endowment fund investments are exposed to various risks such as interest rate, credit, and overall market volatility. Accordingly, the AMC has established an asset allocation policy, investment guidelines and performance standards for the investment of the Fund's assets, in order to control risks and monitor investment performance. However, experience has shown that market performance wi ll vary and that the pOJifolio 's investment objectives may not be achievable during shOJi-term periods. The annual endowment spending made available for the operations of the AMC is an amount equal to a weighted average calculation of the prior year's spending amount, adjusted for inflation, and 4.5% of the previous year's invested endowment balance.

F. Notes Receivab le:

Notes receivable consists of the following at December 31, 2011 and 2010:

2011 2010

Note Receivable due 2011; Interest receivable at LIBOR +.75%; to be received concurrent with the sett lement of AMC's loan payable due 2011 $ $ 12,000,000

Note Receivable due 2034; Interest receivab le at 1 %; to be received on the earlier of 2034 or the settlement of AMC's loan payab le due 2039 11,065,000 11 ,065 ,000

Total Notes Receivable $ 11 ,065,000 $ 23,065,000

The above referenced notes are pa!i of financings structured under the New Markets Tax Credit ("NMTC") program of the U.S. Treasury Department (see also Loans Payable and Commitments). On December 23,2011, the Note Receivable then outstanding in the amount of $12,000,000 was paid concurrent with the settlement of the corresponding loan described under Loans Payable. The remaining Note Receivable of $11,065,000 wi ll be paid concurrent with the settlement of the corresponding Loan Payab le.

- 1 1 -

APPALACHIAN MOUNTAIN CLUB

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31,2011 AND 2010

G. Propelty and Equipment:

Property and equipment consists of the following as of December 31, 2011 and 2010:

2011

Land Bui ldings and improvements Furniture, fixtures and equipment Construction in progress

Accumulated depreciation

Property and equipment, net

$ 19,202,568 30,633,299

9,536,672 1,203 ,226

60,575,765 (20,293,662)

$ 40,282,103

2010

$ 21,549,953 26,508,436

9,007,585 2,980,534

60,046,508 (19,011,366)

$ 41 ,035,142

Depreciation expense for 2011 tota led $1,282,293 and $1,253,780 for 2010. The AMC has a perm it with the U.S.D.A Forest Service to operate and maintain huts within the boundaries of the White Mountain National Forest that expires on May 14, 2029. In 2009, the AMC received a commitment for a $2,500,000 grant related to the purchase of land in Maine. In 20 II, the AMC fulfilled conditions of the grant related to preservation of the land, primarily through conservation easements, and recorded $2,500,000 as contribution revenues . In addition, $2,500,000 has been recorded as a reduction in the carrying value of the land and a corresponding amount of expense on the Consolidated Statements of Act ivities.

H. Loans Payable:

Loans payable consists of the following at December 31, 2011 and 2010:

2011 2010

Secured borrowing due 20 I I; interest payable at 3% $ $ 16,500,000

Secured borrowing due 2039 (subject to put & ca ll agreement); interest payable at 1.4337% 14,550,000 14,550,000

Total Loans Payable $ 14,550,000 $ 31,050,000

Both of the above referenced loans are part of financings structured under the NMTC program of the U.S. Treasury Department (see a lso Notes Receivable and Commitments). Loan proceeds from both loans were used for the AMC ' s Maine Woods Initiative project. Interest expense was $675,251 for 2011 and $706,501 for 2010 . On December 23, 20 I I, the Loan Payable then outstanding in the amount of $16,500,000 matured and was fully satisfied. In conjunction with the satisfaction of this loan and the correspond ing Note Receivable, and after payment of celtain costs of satisfaction, the AMC recorded debt forgiveness of $4,072,962 as revenue.

For the Loan Payable at December 31, 2011 of $14,550,000, the loan agreement specifies celtain debt forgiveness provisions at maturity, and requires the AMC to comply with celtain covenants. The AMC was in compliance with these covenants at December 31, 2011. In conjunction with the Loan Payable due 2039, a single purpose lending entity was estab lished by a commercial bank whose so le activity is the loan to the AMC. The AMC has entered into a put and call agreement with the bank whereby the AMC may acquire the lending entity from the bank in 2014 or thereafter. It is expected that the AMC will acqu ire the entity in 2014 and will repay all amounts outstanding, less debt forgiveness amounts, at that time.

- 12 -

APPALACHIAN MOUNTAIN CLUB

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31, 2011 AND 2010

1. Commitments:

The AMC has a secured line of credit agreement with a commercial bank which expires in 2012. The maximum borrowings available under the agreement are $5 ,000,000. The agreement provides that any borrowings are due on or before the expiration date of the agreement and bear interest at LIBOR plus I %. There were no outstanding borrowings under the agreement at December 31, 2011 and 2010, respectively.

J. Retirement Plans:

The AMC has a defined contribution plan which covers substantially all of its full-time employees. Contributions are determined as a percent of each covered employee ' s gross salary. The percentage rate is based on an employee's years of completed service. Employees are immediately vested. The expense related to the plan was $377,494 for 2011 and $357,730 for 2010. The AMC also sponsors a deferred compensation plan in which all eligible employees may participate. The AMC makes no contribution to this plan.

Although it has not expressed any intent to do so, the AMC has the right under the plan to discontinue its contributions at any time and to terminate the plan subject to the provisions of the Employee Retirement Income Security Act of 1974. However, no such action may deprive any palticipant or beneficiary under the plan of any vested right. In the event of plan termination, pmticipants remain 100% vested in their accounts.

- 13 -