cocoaland holdings bhd rr 3q fy2015 factset

DESCRIPTION

Quarterly Results Report for Cocoaland Holdings Bhd - 3Q FY 2015TRANSCRIPT

WILSON & YORK 25/11/2015

Copyright 2015, Wilson & York Global Advisers Sdn Bhd | See important disclosures at end of this report

RESULTS REPORT

INVESTMENT RISKS

RECOMMENDATION

ANNUAL RESULTS AND METRICS (MYR mn)

Page 1 of 3

YTD 3Q FY15 total revenue increased 0.1% vs YTD 3Q FY14; exports

are slowing down, but local sales are increasing. YTD 3Q FY15 net

profits increased 83.3% vs YTD 3Q FY14. YTD 3Q FY15 operating

margins came in at 16.1% vs 9.3% in YTD 3Q 2014. We expect operating

margins of 14-17% to prevail over the next several quarters. Cocoaland

continues to open new markets and is making good progress under

challenging trading conditions. Exports account for about 57% of

Cocoaland sales currently, and are expected to rise to about 60% of

sales in FY 2016. Low commodity prices and the lower value of the

MYR has been a beneficial factor for margins.

Risks to our recommendation and target price include: i) rising trends in

material costs, ii) an increase in the general level of interest rates, and iii)

a sharp slowdown in the general level of economic activity in Malaysia

or in the economies of the company’s major ‘own brand’ export markets

- China/HK and the Middle East.

We maintain our BUY recommendation on Cocoaland Holdings Bhd, and

raise our fair value estimate to MYR 2.40. It is possible that the share

price will surprise on the upside; sales growth and capacity utilisation

may accelerate more quickly than we expect. Cocoaland has very little

debt on the balance sheet as well as plenty of cash.

Cocoaland has a clean balance sheet and a proven record of growing

export sales. Exports are likely to account for 60% or more of total

revenue by year end 2016. In terms of ‘own brand’ China/HK remains in

the top spot as the company’s largest export market, followed by Saudi

Arabia in importance. Management has been very diligent in developing

new markets that more than compensate for OEM beverage business

lost in the Thai market in 2014.

Cocoaland Holdings Bhd is ranked approximately in the middle of the

thirty listed companies in the Malaysian snack food industry. The com-

pany is one of the few home grown Malaysian consumer firms that have

successfully penetrated regional markets. Cocoaland Holding’s pred-

ecessor company, MFESB, was formed in 1980. This company and

others were consolidated and converted to a public limited company in

2000 under the name Cocoaland Holdings Bhd, prior to listing in 2005.

FTSE-BURSA INDEX MEMBERSHIP

REPORT INDEX

COMPANY PROFILE

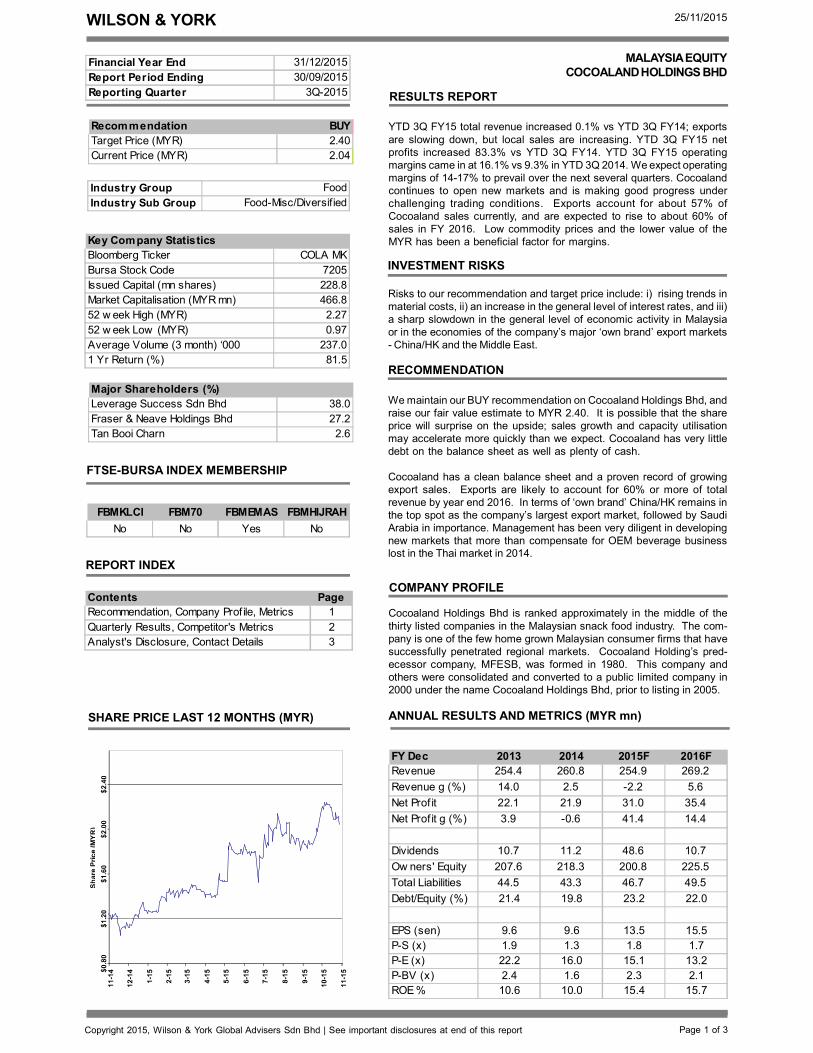

SHARE PRICE LAST 12 MONTHS (MYR)

MALAYSIA EQUITY

COCOALAND HOLDINGS BHD

Industry Group Food

Industry Sub Group Food-Misc/Diversified

FBMKLCI FBM70 FBMEMAS FBMHIJRAH

No No Yes No

Recommendation BUY

Target Price (MYR) 2.40

Current Price (MYR) 2.04

Key Company Statistics

Bloomberg Ticker COLA MK

Bursa Stock Code 7205

Issued Capital (mn shares) 228.8

Market Capitalisation (MYR mn) 466.8

52 w eek High (MYR) 2.27

52 w eek Low (MYR) 0.97

Average Volume (3 month) ‘000 237.0

1 Yr Return (%) 81.5

Major Shareholders (%)

Leverage Success Sdn Bhd 38.0

Fraser & Neave Holdings Bhd 27.2

Tan Booi Charn 2.6

FY Dec 2013 2014 2015F 2016F

Revenue 254.4 260.8 254.9 269.2

Revenue g (%) 14.0 2.5 -2.2 5.6

Net Prof it 22.1 21.9 31.0 35.4

Net Prof it g (%) 3.9 -0.6 41.4 14.4

Dividends 10.7 11.2 48.6 10.7

Ow ners' Equity 207.6 218.3 200.8 225.5

Total Liabilities 44.5 43.3 46.7 49.5

Debt/Equity (%) 21.4 19.8 23.2 22.0

EPS (sen) 9.6 9.6 13.5 15.5

P-S (x) 1.9 1.3 1.8 1.7

P-E (x) 22.2 16.0 15.1 13.2

P-BV (x) 2.4 1.6 2.3 2.1

ROE % 10.6 10.0 15.4 15.7

Financial Year End 31/12/2015

Report Period Ending 30/09/2015

Reporting Quarter 3Q-2015

Contents Page

Recommendation, Company Prof ile, Metrics 1

Quarterly Results, Competitor's Metrics 2

Analyst's Disclosure, Contact Details 3

WILSON & YORK 25/11/2015

Copyright 2015, Wilson & York Global Advisers Sdn Bhd | See important disclosures at end of this report

QUARTERLY RESULTS TABLE (All figures in MYR mn unless otherwise indicated)

FY Dec 3Q-15 3Q-14 Q-o-Q YTD YTD Y-o-Y

%chg FY15 FY14 %chg

Revenue 58.9 63.8 -7.6 188.3 188.1 0.1

Operating Profit 9.2 6.7 37.6 30.3 17.6 72.1

Other Income 3.1 0.0 >100 5.1 1.3 >100

Share of Associates 0.0 0.0 na 0.0 0.0 na

Depreciation/Amort'n -2.7 -2.7 -1.3 -7.9 -8.0 -1.7

Finance Costs 0.0 0.0 na 0.0 0.0 na

Pre Tax Profit 9.2 6.7 37.6 30.3 17.6 72.1

Tax -2.7 -2.5 na -8.1 -5.5 na

Minority Interest 0.0 0.0 na 0.0 0.0 na

Net Prof it to S'holders 6.6 4.2 55.7 22.1 12.1 83.3

Dividends 0.0 0.0 na 4.3 2.6 66.7

EPS (sen) 2.9 1.8 55.7 9.7 5.3 83.3

DPS (sen) 0.0 0.0 na 1.9 1.1 66.7

Operating Margin (%) 15.7 10.5 49.0 16.1 9.3 71.9

Net Margin (%) 11.2 6.6 68.5 11.8 6.4 83.1

Tax Rates (%) 28.8 37.1 -22.3 26.9 31.3 -14.2

NTA/share (RM) 1.03 0.95 8.9

COMPETITOR’S METRICS (All figures in MYR mn unless otherwise indicated)

Page 2 of 3

Comments

Revenue increased 0.1% YTD 3Q FY15 vs.

YTD 3Q FY14. Export grow th is slow ing

dow n, but local sales are rising nicely.

Net Profit increased 83.3% YTD

3Q FY15 vs. YTD 3Q FY 14. The company

continues to broaden its export markets

despite challenging trading conditions.

Operating margins continue to improve and

are likely to stay above 10% next 2 qtrs.

Tax rates still above statutory rates, but not

by much.

MALAYSIA EQUITY

COCOALAND HOLDINGS BHD

Current Year

Cocoaland

Holdings

Bhd

Apollo Food

Holdings

Bhd

London

Biscuits

Bhd

Ending* Dec-15 Apr-16 Jun-16

Revenue 254.9 199.7 355.3

Net Prof it 31.0 44.7 17.1

Ow ners' Equity 200.8 273.1 500.1

Dividends 48.6 20.0 1.4

Market Cap 466.8 424.0 112.2

P-S (x) 1.8 2.1 0.3

P-E (x) 15.1 9.5 6.6

P-BV (x) 2.3 1.6 0.2

Div Yield (%) 10.4 4.7 1.2

Net Margins (%) 12.2 22.4 4.8

ROE (%) 15.4 16.4 3.4

Payout Ratio (%) 156.9 44.7 8.2

Sales Grow th (%) -2.2 -6.1 -11.7

Total Debt/Equity (%) 13.5 9.3 63.6

WILSON & YORK 25/11/2015

Copyright 2015, Wilson & York Global Advisers Sdn Bhd | See important disclosures on this page. Page 3 of 3

ANALYST’S DISCLOSURE

MALAYSIA EQUITY

COCOALAND HOLDINGS BHD

BUY: Share price may exceed 10% over the next 12 months

TRADING BUY: Share price may exceed 15% over the next 3 months, however longer-term outlook remains uncertain

HOLD: Share price may fall within the range of +/- 10% over the next 12 months

TAKE PROFIT: Target price has been attained. Look to accumulate at lower levels

SELL: Share price may fall by more than 10% over the next 12 months

NOT RATED (NR): Stock is not within regular research coverage

All research is based on materials compiled from data considered to be reliable at the time of writing. However, information and opinions

expressed are subject to change at short notice, and no part of this report is to be construed as an offer or solicitation of an offer to transact

any securities or financial instruments whether referred to herein or otherwise.

We do not accept any liability directly or indirectly that may arise from investment decision-making based on this report. The company, its

directors, officers, employees and/or connected persons may periodically hold an interest and/or underwriting commitments in the secu-

rities mentioned.

All Rights Reserved. No part of this publication may be used or re-produced without expressed permission from Wilson & York Global

Advisers Sdn Bhd.

J Charles Wilson

Head of Research

QUESTIONS?

CONTACT THE INVESTMENT ADVISER:

Wilson & York Global Advisers Sdn Bhd

Suite B-11-3A, Level 11, Block B, Plaza Mont’ Kiara

2, Jalan Kiara, Mont’ Kiara

50480 Kuala Lumpur

Malaysia

Tel: +603 6203 2280

Fax: +603 6203 2281

E-mail [email protected]

Website: www.wygainvestments.com