chemicals & plastics outlook - · pdf filechemicals & plastics outlook . ... global...

TRANSCRIPT

Howard Rappaport

Senior Director, Chemicals

IHS Global Insight – Pricing & Purchasing

September 27, 2012

Chemicals & Plastics Outlook

Copyright © 2012 IHS Inc. All Rights Reserved.

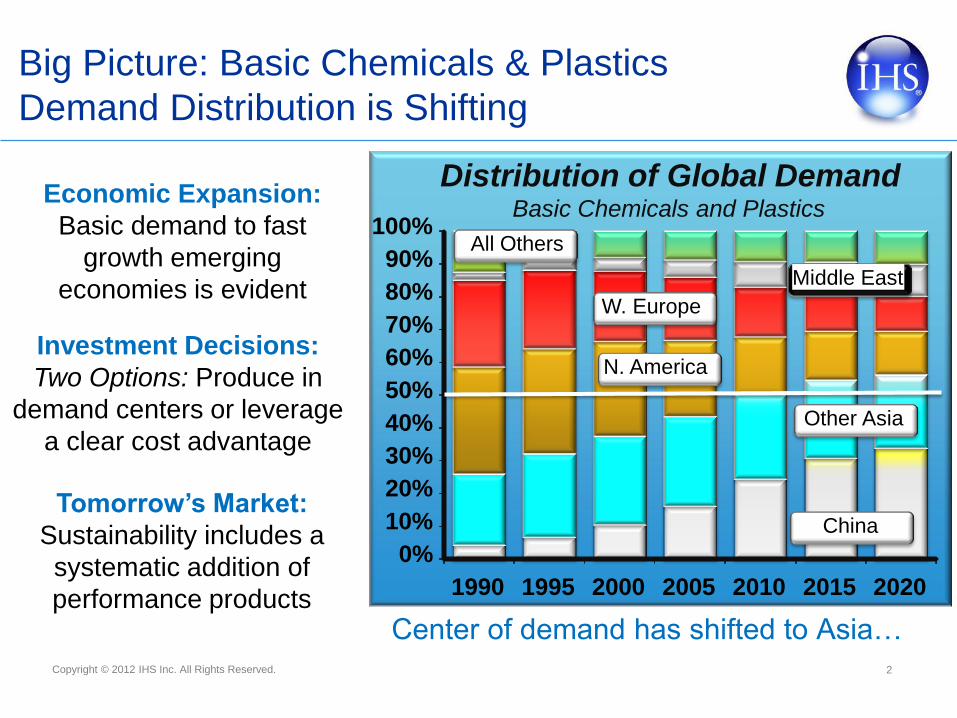

Center of demand has shifted to Asia…

Economic Expansion:

Basic demand to fast

growth emerging

economies is evident

Investment Decisions:

Two Options: Produce in

demand centers or leverage

a clear cost advantage

Tomorrow’s Market:

Sustainability includes a

systematic addition of

performance products

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990 1995 2000 2005 2010 2015 2020

W. Europe

Middle East

All Others

Other Asia

China

N. America

Basic Chemicals and Plastics

Distribution of Global Demand

Big Picture: Basic Chemicals & Plastics

Demand Distribution is Shifting

2

Copyright © 2012 IHS Inc. All Rights Reserved.

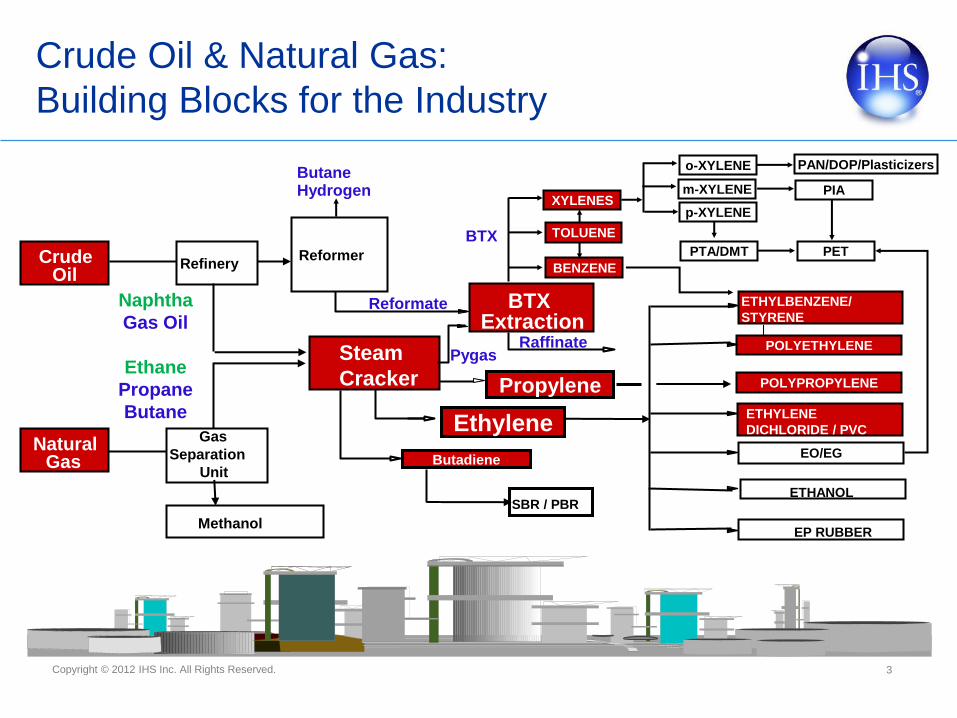

Natural Gas

Gas

Separation

Unit

Refinery Crude Oil

Reformer

Reformate BTX Extraction

Steam

Cracker

Butane Hydrogen

Propylene

Pygas

BTX

Raffinate

Ethylene EO/EG

POLYETHYLENE

ETHYLENE

DICHLORIDE / PVC

EP RUBBER

ETHANOL

Naphtha

Gas Oil

Ethane

Propane

Butane

TOLUENE

m-XYLENE

p-XYLENE

BENZENE

o-XYLENE

XYLENES

PTA/DMT PET

PIA

PAN/DOP/Plasticizers

POLYPROPYLENE

Butadiene

Methanol

SBR / PBR

ETHYLBENZENE/

STYRENE

Crude Oil & Natural Gas:

Building Blocks for the Industry

3

Copyright © 2012 IHS Inc. All Rights Reserved.

The Energy Outlook

4

1

3

5

7

9

11

13

10

30

50

70

90

110

130

2004 2006 2008 2010 2012 2014

Oil, US Refinery Acqusition Price, $/barrel (left)

Natural Gas, Henry Hub Spot, $/mmbtu (right)

Copyright © 2012 IHS Inc. All Rights Reserved.

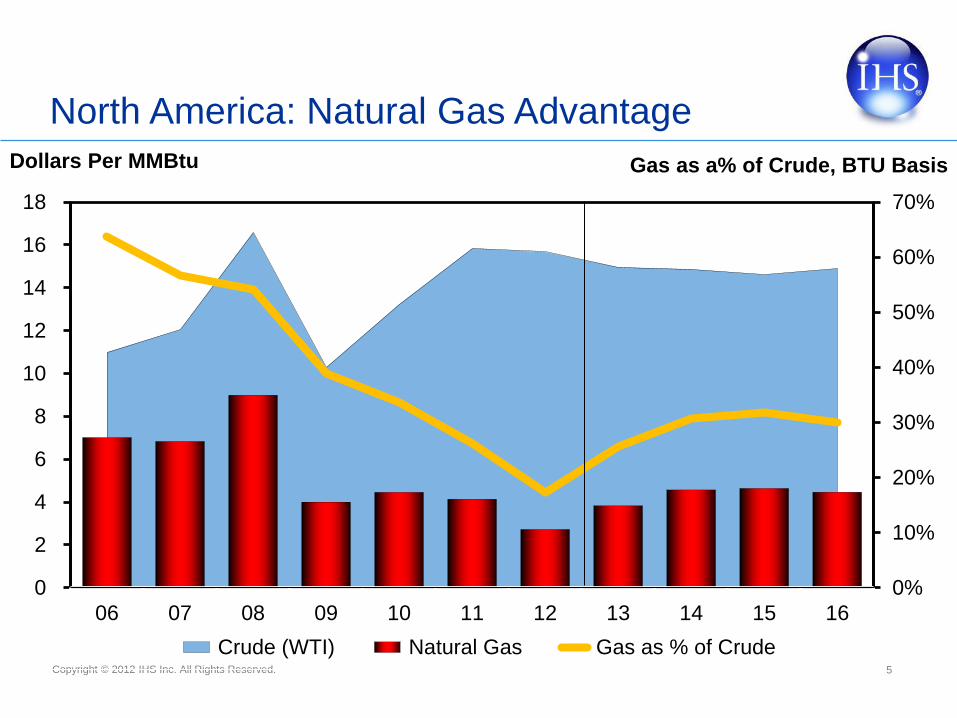

0%

10%

20%

30%

40%

50%

60%

70%

0

2

4

6

8

10

12

14

16

18

06 07 08 09 10 11 12 13 14 15 16

Crude (WTI) Natural Gas Gas as % of Crude

Dollars Per MMBtu Gas as a% of Crude, BTU Basis

5

North America: Natural Gas Advantage

Copyright © 2012 IHS Inc. All Rights Reserved.

North American Feedslate Becoming Lighter

• Given its high selectivity

to ethylene & relative cost

position to other feeds,

ethane is consistently the

most favored feed

• Once oil & gas began to

diverge, producers have

been shifting feedslates

lighter to capitalize on the

advantage

6

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Monthly Ethylene Production By Feedstock

Ethane Propane Butane Naphtha Gas Oil

Wt% Produced

From Feedstock

Ethylene & Polyethylene

Copyright © 2012 IHS Inc. All Rights Reserved.

SE Asia Avg.

NE Asia Avg.

West Europe Avg.

Middle East Avg.

U.S. Avg.

U.S. Ethane

50

250

450

650

850

1050

1250

1450

1650

0 20 40 60 80 100 120 140 160

Dollars per Ton

CUMULATIVE ETHYLENE CAPACITY (million tons)

WTI Crude $95/Barrel

Nat Gas $4.14/MMBtu

Ethane 76.7 cpg

North America Second Lowest Cost Region 2011 Global Ethylene Cash Costs

Alberta Ethane

Middle East Ethane

8

Copyright © 2012 IHS Inc. All Rights Reserved.

2012 U.S. Ethylene Production Losses

Higher Than Expected

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

200

400

600

800

1,000

1,200

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Planned* Unplanned**

'11 Cumulative Production Loss Forecast '13 Cumulative Production Loss

Series4

* Includes both confirmed and unconfirmed outages

Million Pounds, Monthly Million Pounds, Cumulative

9

Copyright © 2012 IHS Inc. All Rights Reserved.

300

500

700

900

1,100

1,300

1,500

1,700

1,900

2,100

10 A J O 11 A J O 12 A J O 13 A J O

U.S. Large Buyer Contract Price WEP Contract Price SEA CFR Spot Price

Dollars Per Metric Ton

Forecast

Global Monthly Ethylene Prices

10

Copyright © 2012 IHS Inc. All Rights Reserved.

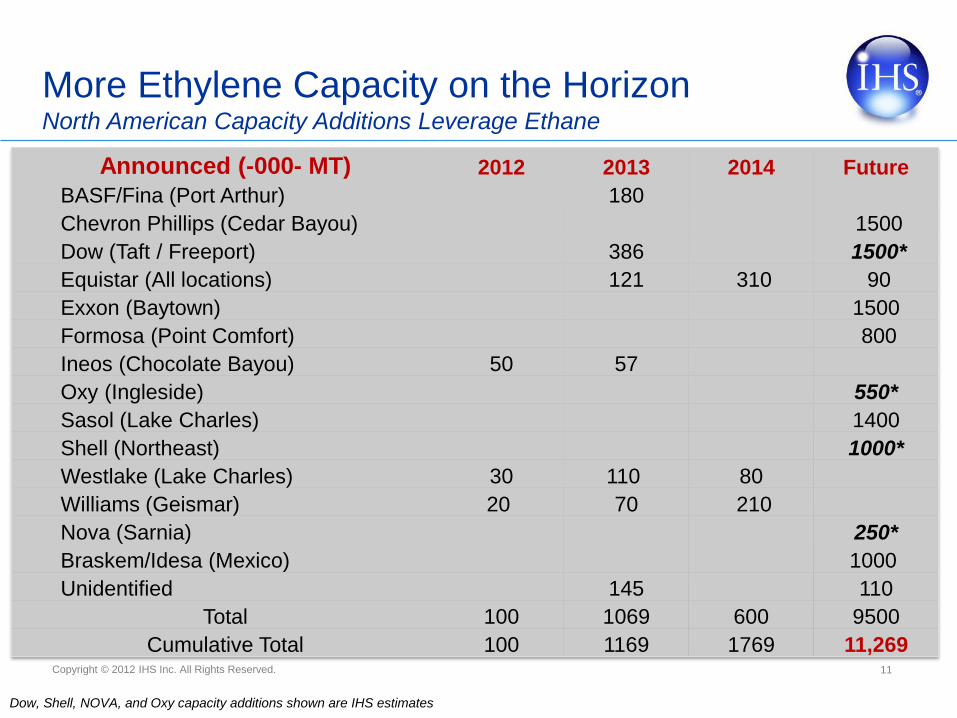

Dow, Shell, NOVA, and Oxy capacity additions shown are IHS estimates

Announced (-000- MT) 2012 2013 2014 Future

BASF/Fina (Port Arthur) 180

Chevron Phillips (Cedar Bayou) 1500

Dow (Taft / Freeport) 386 1500*

Equistar (All locations) 121 310 90

Exxon (Baytown) 1500

Formosa (Point Comfort) 800

Ineos (Chocolate Bayou) 50 57

Oxy (Ingleside) 550*

Sasol (Lake Charles) 1400

Shell (Northeast) 1000*

Westlake (Lake Charles) 30 110 80

Williams (Geismar) 20 70 210

Nova (Sarnia) 250*

Braskem/Idesa (Mexico) 1000

Unidentified 145 110

Total 100 1069 600 9500

Cumulative Total 100 1169 1769 11,269

More Ethylene Capacity on the Horizon North American Capacity Additions Leverage Ethane

11

Copyright © 2012 IHS Inc. All Rights Reserved.

• Shale development has enabled the North American producer to become

one of the lowest cost producers in the world

• Combined with the Middle East, over 40% of the global ethylene capacity

is now cost advantaged

• Other cracking capacity likely to trend towards increased LPG

consumption in order to try and remain competitive

• Higher cost countries may respond with protectionist measures

Ethylene Market View Development of Two Low-Cost Production Regions

*

* 12

Copyright © 2012 IHS Inc. All Rights Reserved.

• Short Term: Global demand growth for PE may be slowing as China

demand weakens and Europe contends with recession

• Longer Term: Two “low cost” regions (North America and the Middle East)

are set to compete for much of the global demand growth. The industry

has never before included two major “cost advantaged” regions • Numerous capacity additions expected in North America as producers in the

region seek to leverage cost advantage driven by “shale gas”

• Continued demand strength anticipated for specialty polyethylene products

such as metalocenes and bio-based resins

• While annual integrated margins are generally expected to trend higher,

most of the margin is forecast to remain upstream with the ethylene

molecule

Key Issues: Polyethylene

13

Copyright © 2012 IHS Inc. All Rights Reserved.

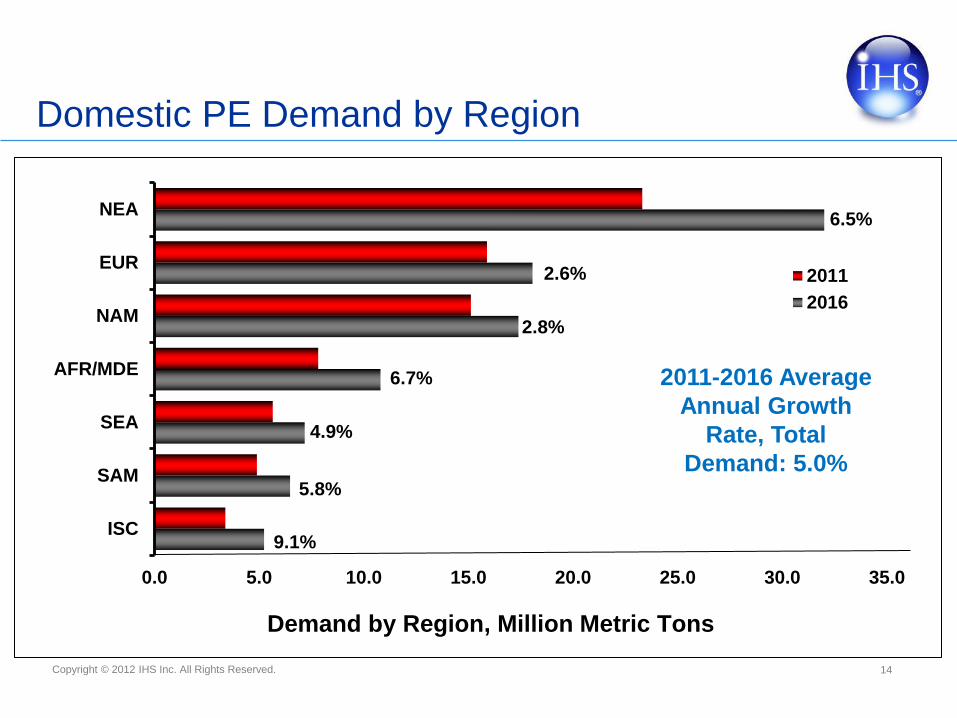

%: 11-16 Average Annual Growth Rate

Domestic PE Demand by Region

0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0

ISC

SAM

SEA

AFR/MDE

NAM

EUR

NEA

2011

2016

Demand by Region, Million Metric Tons

2.8%

9.1%

5.8%

4.9%

6.5%

2.6%

6.7% 2011-2016 Average

Annual Growth

Rate, Total

Demand: 5.0%

14

Copyright © 2012 IHS Inc. All Rights Reserved.

-4

-2

0

2

4

6

8

10

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Asia/Pacific Africa/ Middle East North America

South America Central Europe/ CIS West Europe

Capacity, Million Metric Tons

Global Polyethylene Capacity Additions

15

Copyright © 2012 IHS Inc. All Rights Reserved.

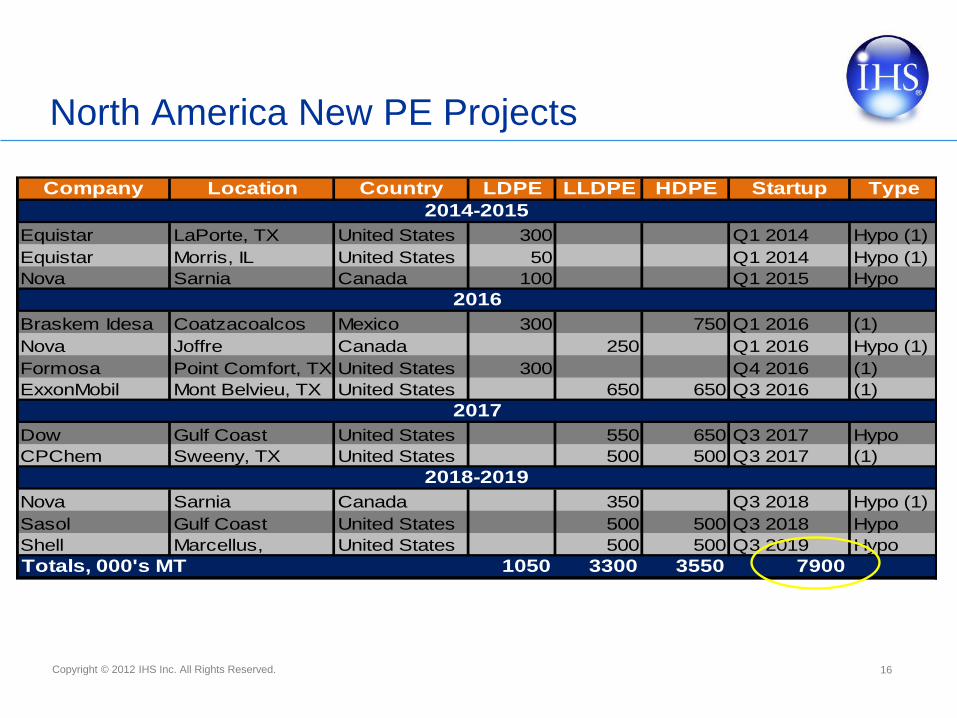

North America New PE Projects

Company Location Country LDPE LLDPE HDPE Startup Type

2014-2015

Equistar LaPorte, TX United States 300 Q1 2014 Hypo (1)

Equistar Morris, IL United States 50 Q1 2014 Hypo (1)

Nova Sarnia Canada 100 Q1 2015 Hypo

2016

Braskem Idesa Coatzacoalcos Mexico 300 750 Q1 2016 (1)

Nova Joffre Canada 250 Q1 2016 Hypo (1)

Formosa Point Comfort, TX United States 300 Q4 2016 (1)

ExxonMobil Mont Belvieu, TX United States 650 650 Q3 2016 (1)

2017

Dow Gulf Coast United States 550 650 Q3 2017 Hypo

CPChem Sweeny, TX United States 500 500 Q3 2017 (1)

2018-2019

Nova Sarnia Canada 350 Q3 2018 Hypo (1)

Sasol Gulf Coast United States 500 500 Q3 2018 Hypo

Shell Marcellus, United States 500 500 Q3 2019 Hypo

Totals, 000's MT 1050 3300 3550 7900

Notes: (1): Announced projects included in our capacity database; (2): Announced expansions with IHS

estimate of product and size, also not included in database; Hypo (1): reported projects not fully verified

or approved and not included in the database; Hypo: IHS estimates of product and size for announced

ethylene crackers - PE not in database.

16

Copyright © 2012 IHS Inc. All Rights Reserved.

0

10

20

30

40

50

60

70

80

90

100

Jan-07 Sep-07 May-08 Jan-09 Sep-09 May-10 Jan-11 Sep-11 May-12 Jan-13 Sep-13

NAM Cash Cost, Integrated NAM LLDPE WEP LLDPE CHINA LLDPE (Spot)

Cents Per Pound

17

Regional LLDPE Butene Prices

Copyright © 2012 IHS Inc. All Rights Reserved.

Polyethylene Chain Margins

-220

0

220

440

660

880

-10

0

10

20

30

40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

PE Margin - Contract HDPE Blow Molding Non-Int. Including Discounts

Ethylene Margin - Average Acquisition Ethylene Price Minus Ethane Cracking Costs

Cents Per Pound Polyethylene Dollars Per Metric Ton

18

Copyright © 2012 IHS Inc. All Rights Reserved.

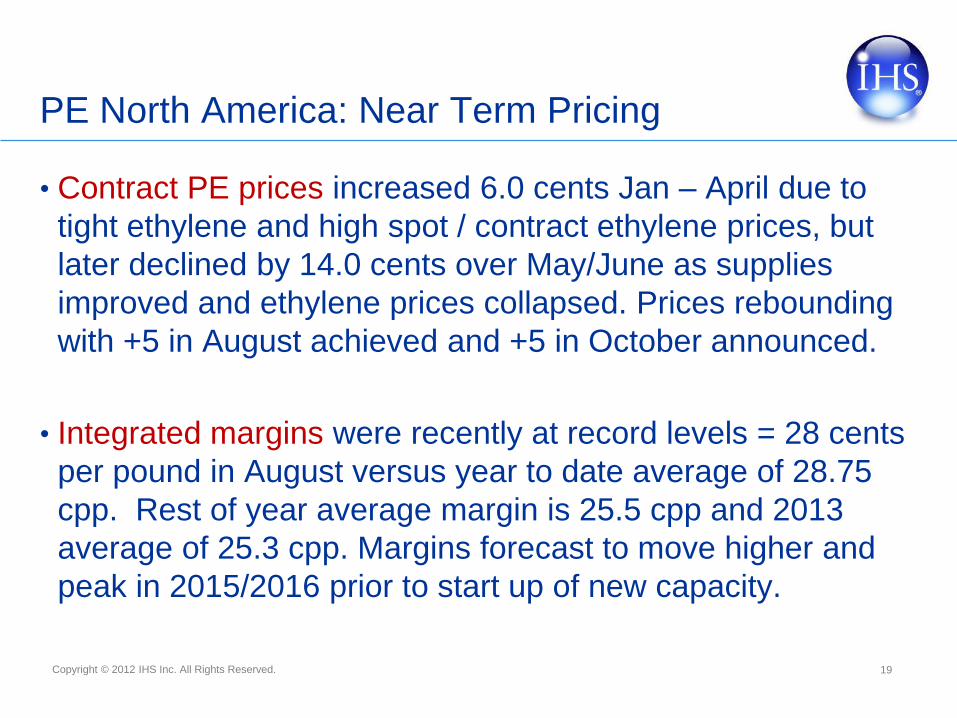

PE North America: Near Term Pricing

• Contract PE prices increased 6.0 cents Jan – April due to

tight ethylene and high spot / contract ethylene prices, but

later declined by 14.0 cents over May/June as supplies

improved and ethylene prices collapsed. Prices rebounding

with +5 in August achieved and +5 in October announced.

• Integrated margins were recently at record levels = 28 cents

per pound in August versus year to date average of 28.75

cpp. Rest of year average margin is 25.5 cpp and 2013

average of 25.3 cpp. Margins forecast to move higher and

peak in 2015/2016 prior to start up of new capacity.

19

Copyright © 2012 IHS Inc. All Rights Reserved.

• Nearly 6.7 MMT of “cost advantaged” new production capacity is

anticipated to be added within the region during the next five years*

• Nearly 5.4 MMT of the referenced capacity is expected in the US

• An additional 6.5 MMT tons of new production capacity is expected to

come on line in the 2017 – 2022 timeframe

• While most of the new production capacity will be targeted into the export

market, the domestic price premium that has existed within the region is

expected to erode as competition for the domestic demand increases

• The first new major complex to start up in the region (Braskem / Idesa) will

impact trade flows from the US to Mexico when production begins

• US producers are likely to look further south in an effort to move any

displaced sales volume

Implications for Buyers: Polyethylene

20

Propylene & Polypropylene

Copyright © 2012 IHS Inc. All Rights Reserved.

Propylene Supply Profile

Other

Technologies

Steam Cracker or

Olefin Plant Ethane

Propane Other propylene consumers:

acrylonitrile, propylene oxide, acrylic

acid, oxo-alcohols

PG & CG

Propylene

Markets

Propane to LPG

Cumene, Oligomers

Isopropanol

FCC

Unit

Alkylation

Unit Isobutane High Octane Alkylate

Gasoline

Other Fuel Uses

Purification

Splitter Unit

Refining Industry

Chemical Industry

Gas

Oil

RG

Propylene

Market

Crude

Unit Crude

Oil

Motor

Gasoline

Motor

Gasoline

Naphtha

Ethylene

& Olefins

Polypropylene

Unit

Injection

Molding,

Fibers,

Films

PDH

Metathesis

MTO and MTP

HSFCC

Olefin Cracking

Others 22

Copyright © 2012 IHS Inc. All Rights Reserved.

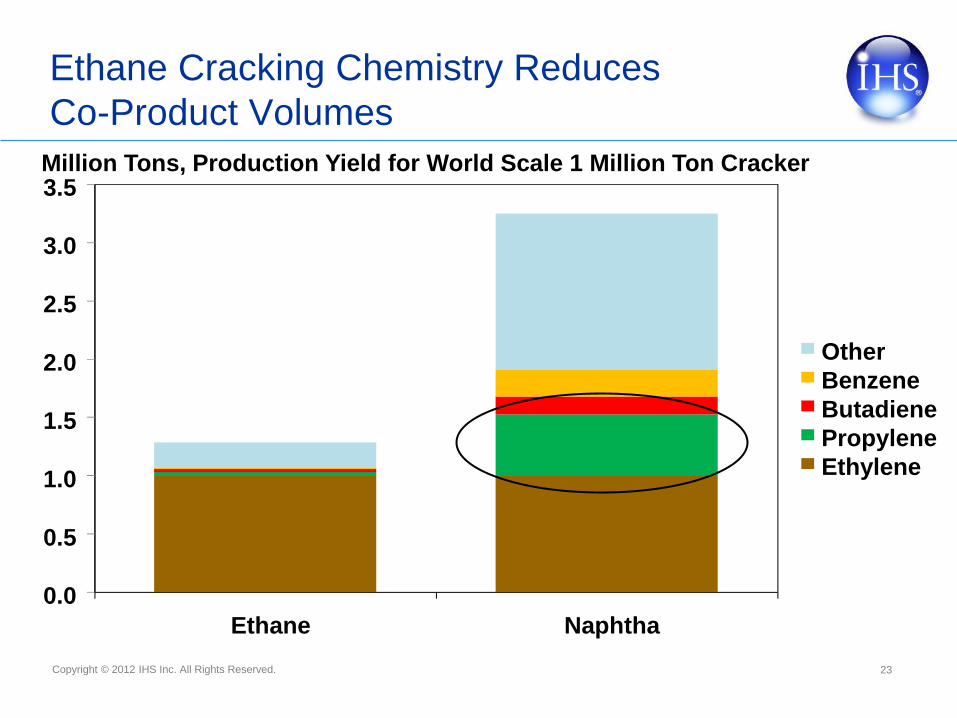

Ethane Cracking Chemistry Reduces

Co-Product Volumes

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Ethane Naphtha

Million Tons, Production Yield for World Scale 1 Million Ton Cracker

Other

Benzene

Butadiene

Propylene

Ethylene

23

Copyright © 2012 IHS Inc. All Rights Reserved.

Cracker Feedstocks Also Influence

Pygas \ Benzene Yields

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Ethane Propane Butane LightNaphtha

HeavyNaphtha

Gasoil

Cracker Feedstocks

Benzene Produced Per Ton of Ethylene

Heavier Feeds

24

Copyright © 2012 IHS Inc. All Rights Reserved.

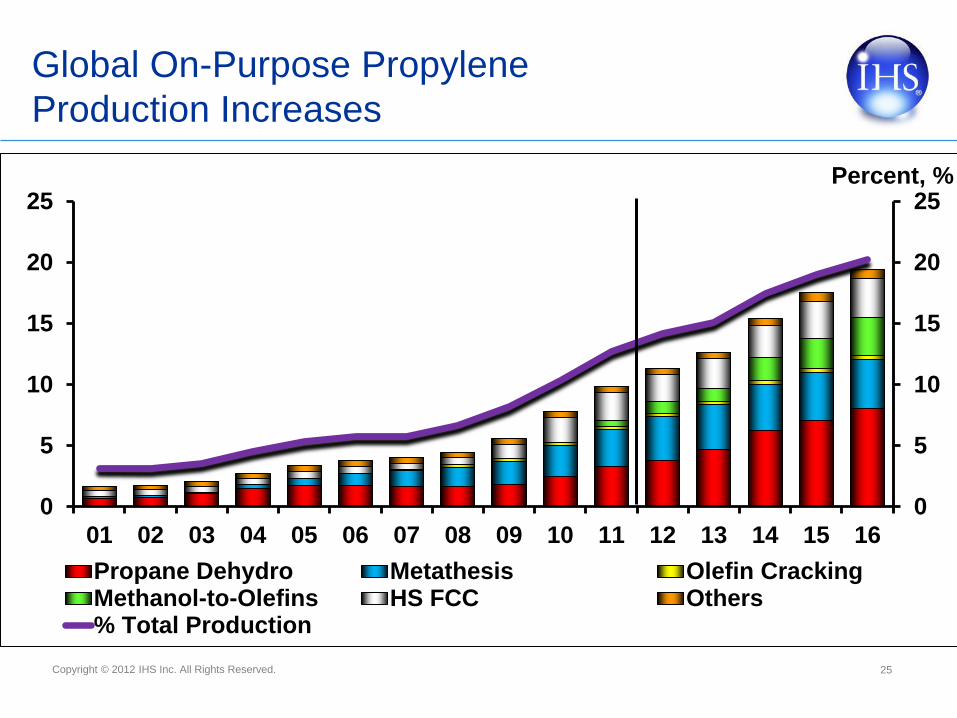

0

5

10

15

20

25

0

5

10

15

20

25

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Percent, %

Propane Dehydro Metathesis Olefin CrackingMethanol-to-Olefins HS FCC Others% Total Production

Million Metric Tons

Global On-Purpose Propylene

Production Increases

25

Copyright © 2012 IHS Inc. All Rights Reserved.

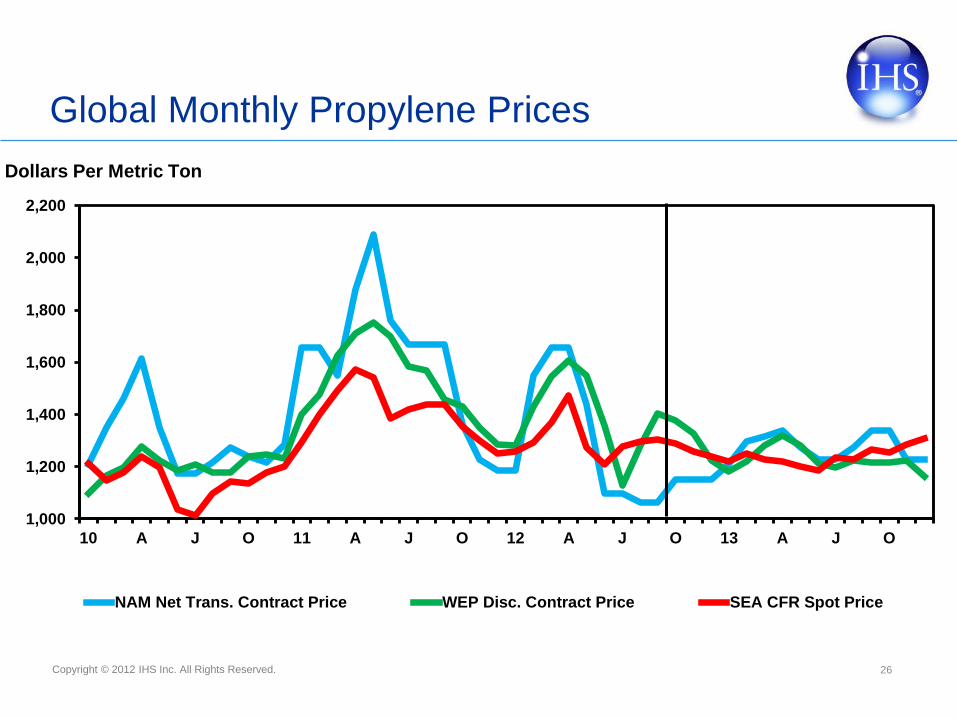

Global Monthly Propylene Prices

26

1,000

1,200

1,400

1,600

1,800

2,000

2,200

10 A J O 11 A J O 12 A J O 13 A J O

NAM Net Trans. Contract Price WEP Disc. Contract Price SEA CFR Spot Price

Dollars Per Metric Ton

Forecast

Copyright © 2012 IHS Inc. All Rights Reserved.

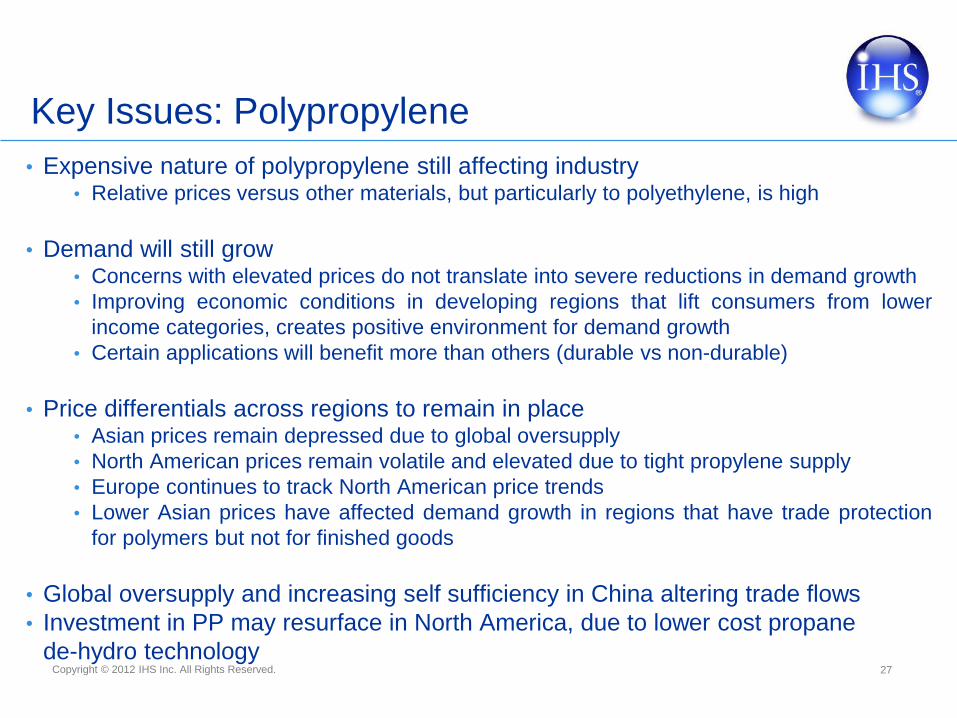

• Expensive nature of polypropylene still affecting industry • Relative prices versus other materials, but particularly to polyethylene, is high

• Demand will still grow • Concerns with elevated prices do not translate into severe reductions in demand growth

• Improving economic conditions in developing regions that lift consumers from lower

income categories, creates positive environment for demand growth

• Certain applications will benefit more than others (durable vs non-durable)

• Price differentials across regions to remain in place • Asian prices remain depressed due to global oversupply

• North American prices remain volatile and elevated due to tight propylene supply

• Europe continues to track North American price trends

• Lower Asian prices have affected demand growth in regions that have trade protection

for polymers but not for finished goods

• Global oversupply and increasing self sufficiency in China altering trade flows

• Investment in PP may resurface in North America, due to lower cost propane

de-hydro technology

Key Issues: Polypropylene

27

Copyright © 2012 IHS Inc. All Rights Reserved.

%: 11-16 Average Annual Growth Rate

Domestic PP Demand by Region

0.0 5.0 10.0 15.0 20.0 25.0 30.0

SAM

ISC

SEA

AFR/MDE

NAM

EUR

NEA

2011

2016

Demand by Region, Million Metric Tons

1.0%

5.4%

9.0%

6.0%

5.3%

2.8%

6.5% 2011-2016 Average

Annual Growth

Rate, Total

Demand: 5.1%

28

Copyright © 2012 IHS Inc. All Rights Reserved.

In Recent Years,

PP Cost Position Has Changed

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

PP/HDPE North America PP/HDPE West Europe PP/HDPE China

Price Ratio

29

Copyright © 2012 IHS Inc. All Rights Reserved.

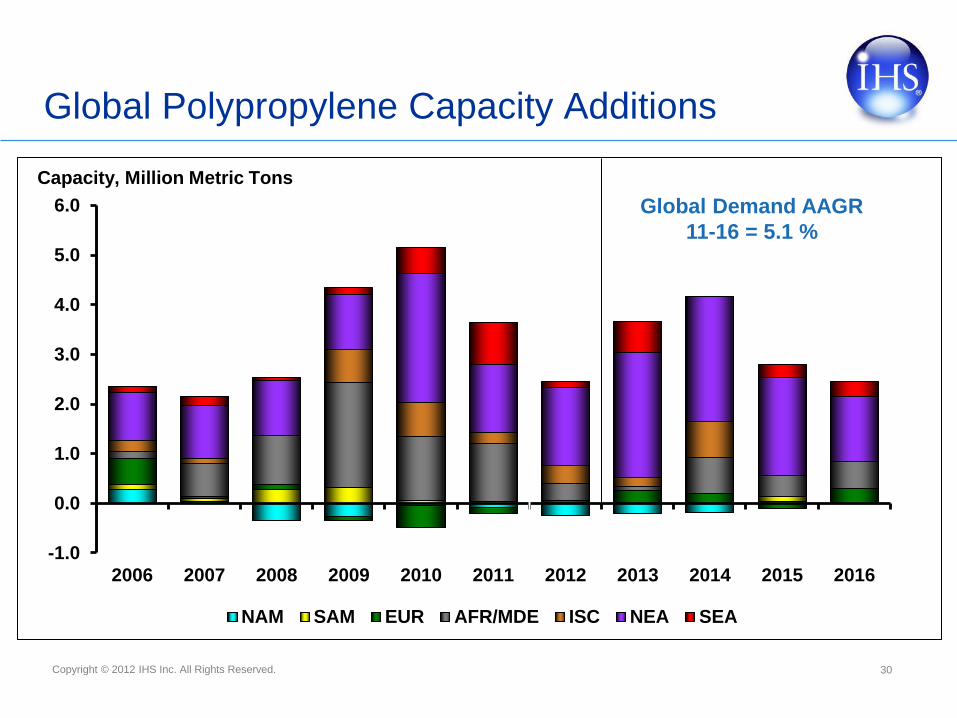

Global Polypropylene Capacity Additions

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

NAM SAM EUR AFR/MDE ISC NEA SEA

Capacity, Million Metric Tons

Global Demand AAGR

11-16 = 5.1 %

30

Copyright © 2012 IHS Inc. All Rights Reserved.

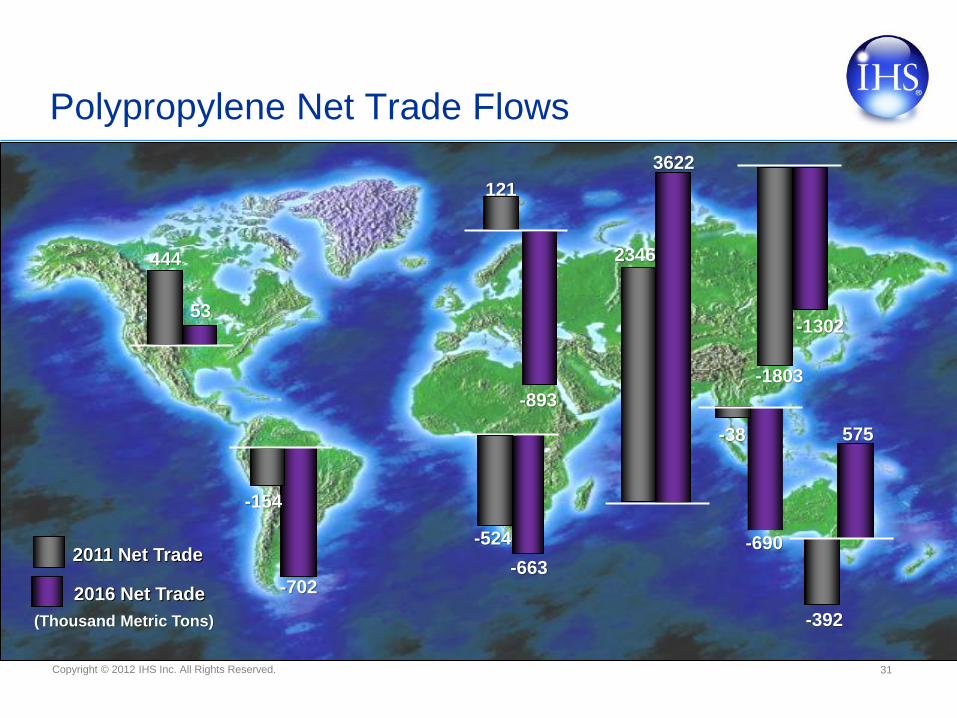

Polypropylene Net Trade Flows

-702 -663

3622

-690

-1302

575

53

-893

-154

-524

2346

-1803

-38

-392

444

121

2011 Net Trade

2016 Net Trade

(Thousand Metric Tons)

31

Copyright © 2012 IHS Inc. All Rights Reserved.

Asia PP Prices: Lowest Price Region

661

882

1,102

1,323

1,543

1,764

1,984

2,205

2,425

30

40

50

60

70

80

90

100

110

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

North America Discounted West Europe DiscountedNorth America Spot Export China Spot

Price, Dollars Per Metric Ton Price, Cents Per Pound

32

Copyright © 2012 IHS Inc. All Rights Reserved.

North America Price Volatility:

Propylene Supply Affecting PP Price

60

65

70

75

80

85

90

95

100

105

110

-300

-200

-100

0

100

200

300

400

Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12

Monthly Growth PP Homopolymer Discounted Price

Million Pounds Cents Per Pound

33

Copyright © 2012 IHS Inc. All Rights Reserved.

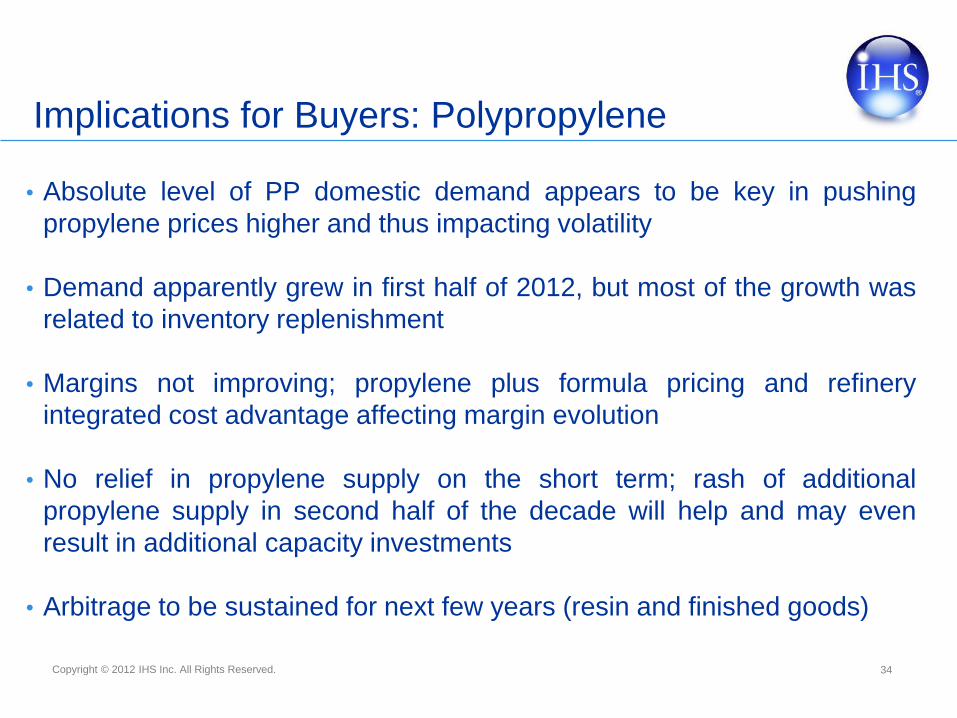

• Absolute level of PP domestic demand appears to be key in pushing

propylene prices higher and thus impacting volatility

• Demand apparently grew in first half of 2012, but most of the growth was

related to inventory replenishment

• Margins not improving; propylene plus formula pricing and refinery

integrated cost advantage affecting margin evolution

• No relief in propylene supply on the short term; rash of additional

propylene supply in second half of the decade will help and may even

result in additional capacity investments

• Arbitrage to be sustained for next few years (resin and finished goods)

Implications for Buyers: Polypropylene

34