charlotte, nc market activity for september 2011

DESCRIPTION

Market Activity and Trends for Charlotte, NC and the surrounding areas for the month of August 2011.TRANSCRIPT

ON MOve Market Activity and Trends for Charlotte & Surrounding Counties

S E P T E M B E R 2 0 1 1

There were 2289 total closings in Aug. 2011, up 25.6% compared to Aug. 2010. 70% of all home sales in Aug. 2011 were in the $200,000 and under category. The average closing price for the

Charlotte metro area in Aug. 2011 was $205,915, down 9.2% from Aug. 2010. In Aug. 2011, new listings decreased by 18.4%, pending sales increased by 24.6%, total active listings decreased by 22.5%.

Residential Closings - Entire MLS August 2010 - August 2011

August 2011 Sales by Price Range

www.helenadamsrealty.com

the

Current Active Listings by Price Range

Under $100,000

$100,001 - $150K

$150,001 - $200K

$200,001 - $300K

$300,001 - $450K

Total Active Listings = 20,924

20%

20%

18%

11%

3%

ASP = Average Sold Price Data Courtesy Carolina MLS.

Total Sold August, 2011 = 2289 Data Courtesy Carolina MLS.

$450,001 - $600K

$600,001 - $800K

17%

5%

$800,001 - $1M

Over $1 Million

2% 1% Under $100,000

$100,001 - $150K

$150,001 - $200K

$200,001 - $300K

$300,001 - $450K 35%

19%

18%

12%

5%

$450,001 - $600K

$600,001 - $800K 16%

$800,001 - $1M

Over $1 Million

1% 1% 3%

Change in Closed Sales

Change in New Listings

Average Sales Price

Total Active Listings

Months Supply of Homes for Sale

Average Days on Market

Pending Sales

+25.6 +24.6 -18.4% -9.2% -22.5% 146 11.4

Brought to You by Evelyn McCorkle

Evelyn McCorkle — 704. 957. 3558 — [email protected] — www.evelynmccorkle.com

Page 2 On the Move - He len Adams Realty Volume 4, Issue 9

Closed Units by Area August 2011 - By MLS Areas

Residential Single Family, Townhomes & Condos

MLS Area Units Closed

1 Year Change

Average Sales Price

Charlotte - Gastonia - Rock Hill 1772 +23.1 $211,400

All of Mecklenburg County 1066 +23.7 $219,763

01 - Mecklenburg County (N) 182 +14.5 $ 178,481

02 - Mecklenburg County (E) 139 +46.3 $ 98,450

03 - Mecklenburg County (SE) 57 +3.76 $ 151,443

04 - Mecklenburg County (SSE) 104 +14.3 $ 329,703

05 - Mecklenburg County (S) 197 +10.1 $ 360,370

06 - Mecklenburg County (SSW) 72 +50.0 $ 188,826

07 - Mecklenburg County (SW) 81 +97.6 $ 123,018

08 - Mecklenburg County (W) 62 +24.0 $ 74,107

10 - Union County 189 +7.4 $ 261,095

11 - Cabarrus County 186 +27.4 $ 190,989

12 - Iredell County 174 +42.6 $ 239,822

13 - Lake Norman 122 +27.1 $ 403,584

14 - Lincoln County 52 +15.6 $ 173,285

15 - Lake Wylie 39 +25.8 $306,662

16 - Gaston County 149 +3.5 $ 127,225

17 - York County, SC 178 +8.5 $233,365

42 - Mtn. Island Lake 17 +35.3 $179,607

99 - Uptown Charlotte 11 -15.4 $285,933

TOTAL (for All CMLS Area) 2289 +25.6 $205,915

09 - Mecklenburg County (NW) 97 +24.4 $160,942

August Home Sales Snapshot

Data Courtesy Carolina MLS & 10K Research and Marketing.

+9.7% -0.1% -4.5%Price Range with Strongest Sales:

Under $100,000

# Bedrooms Strongest Sales: 4+ bedrooms

Property Type Strongest Sales: Single Family

Page 3 On the Move - He len Adams Realty Volume 4, Issue 9

Pending Contracts

Average Residential Sales Price

New Listings

30 Year Fixed Mortgage Rates

Source: Freddie Mac, NAR, August, 2011

Data Courtesy Carolina MLS.

Evelyn McCorkle — 704. 957. 3558 — [email protected] — www.evelynmccorkle.com

Page 4 On the Move - He len Adams Realty Volume 4, Issue 9

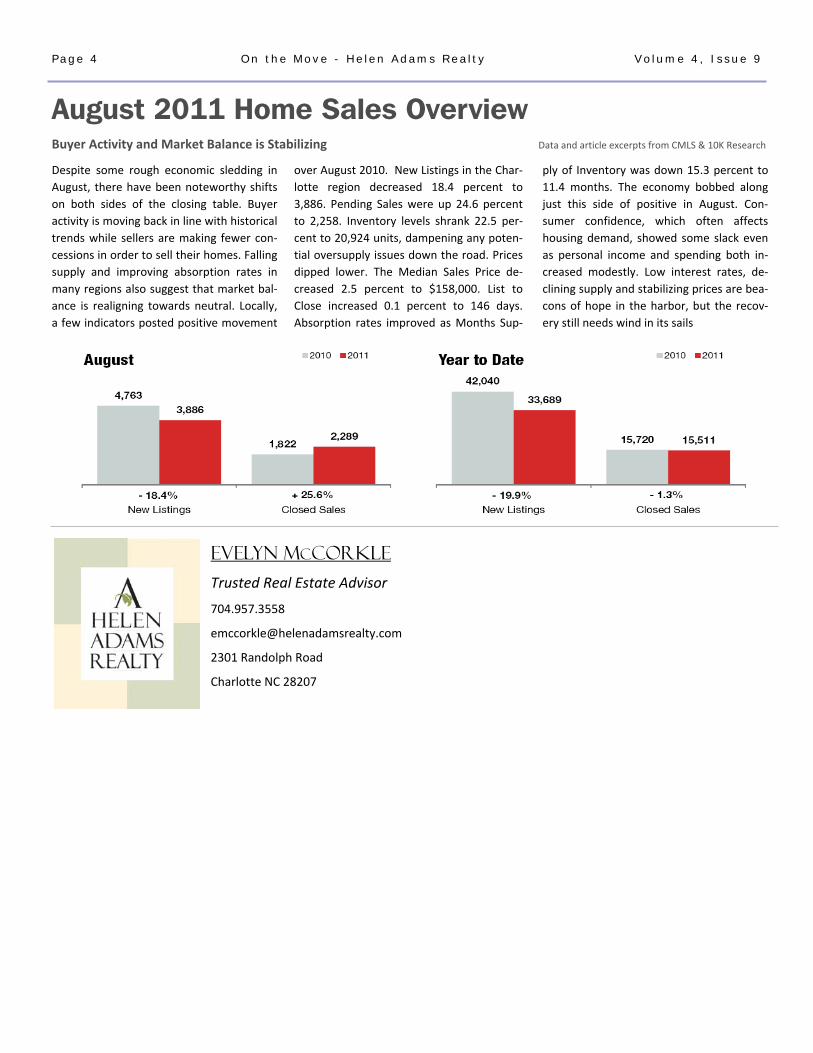

August 2011 Home Sales Overview

Despite some rough economic sledding in August, there have been noteworthy shifts on both sides of the closing table. Buyer activity is moving back in line with historical trends while sellers are making fewer con-cessions in order to sell their homes. Falling supply and improving absorption rates in many regions also suggest that market bal-ance is realigning towards neutral. Locally, a few indicators posted positive movement

Buyer Activity and Market Balance is Stabilizing Data and article excerpts from CMLS & 10K Research

over August 2010. New Listings in the Char-lotte region decreased 18.4 percent to 3,886. Pending Sales were up 24.6 percent to 2,258. Inventory levels shrank 22.5 per-cent to 20,924 units, dampening any poten-tial oversupply issues down the road. Prices dipped lower. The Median Sales Price de-creased 2.5 percent to $158,000. List to Close increased 0.1 percent to 146 days. Absorption rates improved as Months Sup-

ply of Inventory was down 15.3 percent to 11.4 months. The economy bobbed along just this side of positive in August. Con-sumer confidence, which often affects housing demand, showed some slack even as personal income and spending both in-creased modestly. Low interest rates, de-clining supply and stabilizing prices are bea-cons of hope in the harbor, but the recov-ery still needs wind in its sails

Evelyn MCCorkle

Trusted Real Estate Advisor 704.957.3558

2301 Randolph Road

Charlotte NC 28207